intelligent cost reduction

TRANSCRIPT

Intelligent Project Prioritisation

‘This year the UK will waste £10billion or more on IT projects that go over time, over budget and just plain wrong.’

This quote is from a recent article in the business pages of The Observer. You may or may not accept the nice, round, £10billion figure but if you have had any long term practical exposure to the field of project management you will not be surprised that it is somewhere in this ballpark. So how do we end up running so many ‘bad’ projects? How come they were prioritised and funded in the first place? I mean, project prioritisation is simple: all you do is compare the costs, benefits and risks of all candidate projects and then select the subset of the projects that on balance offer the highest benefit, lowest cost, lowest risk portfolio of projects within the available cost/resource budget. What’s so hard about that? Well, quite a lot in practice.

What’s the problem?

The typical organisation faces many project prioritisation problems• Too many proposed projects with too little money/time/resources• Projects can ‘appear from nowhere’ and are expected to be

‘absorbed’ • Project approval/priority set in departmental ‘silos’ based typically

on ‘can we afford it’ and/or ‘can we resource it’ rather than a compelling, credible, objective Business Case

• The ‘project lottery’ of having no consistent/objective process for approving and prioritising competing proposed projects

• The inability to identify and stop rogue projects already approved and funded

What’s the solution?

Fundamental to consistently, objectively assessing the relative commercial merits of projects competing for investment is that they actually have consistent, objectively defined Business Cases in the first place. But how often does that actually happen?

Page | 1 ©Bestoutcome Limited 2011

The fact of the matter is that many (most?) project Business Cases are developed in a spirit of ‘collusion and illusion’; in fact this is almost the norm for big, complex, grandiose projects (much loved by Board Directors and Government Ministers). The Director/Minister obviously wants the project to happen because he or she wants the benefits promised and the project developer obviously wants to get the project contract. So in the happy spirit of joint wish-fulfilment it suits both parties very well to tacitly collude and enter an illusory (if temporarily comforting) world in which completely unrealistic assumptions about the costs, benefits and risks are made in order to justify the project. And once the project is started and real world difficulties rear their ugly heads, well, then it’s just too embarrassing for the customer to admit that the project he or she sanctioned was ‘plain wrong’ before it even started. And, of course, once you’ve run up some big bills, the customer doesn’t want all that wasted money publicised any more than the supplier does. So, just plough on and hope for the best (even though that didn’t work out last time; or the time before; or, come to think of it, ever).

How do you produce the ‘right answer’ (i.e. the answer that will get your project approved and funded)? There are many techniques, including · ‘reverse estimation’ (‘How do I have to estimate the costs and

benefits of this project in order to beat the bean counters’ hurdle rate and win the funding?)

· assuming that with greater knowledge of the problem and solution once the project starts the costs will not rise (which they always do) and the benefits will not fall (which they always do)

· omitting support, infrastructure, consultancy, etc. costs from your numbers

· pretending that the benefits will all be fully realised from day 1 (which they never are). And the realisation of the benefits promised isn’t the Project Manager’s problem, is it? That’s the customer’s problem

· performing little or no rigorous risk assessment

In short, we know that many (if not most) project justifications would not fly (or even make it to the end of the runway) if we were realistic in

Page | 2 ©Bestoutcome Limited 2011

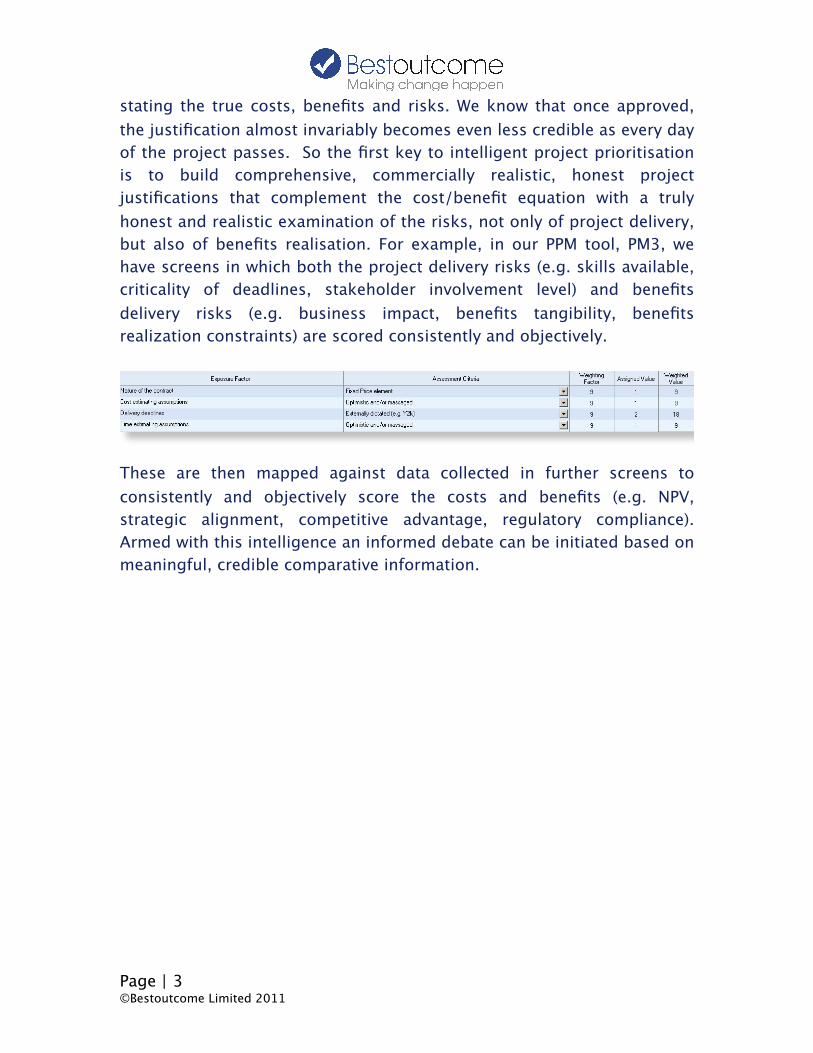

stating the true costs, benefits and risks. We know that once approved, the justification almost invariably becomes even less credible as every day of the project passes. So the first key to intelligent project prioritisation is to build comprehensive, commercially realistic, honest project justifications that complement the cost/benefit equation with a truly honest and realistic examination of the risks, not only of project delivery, but also of benefits realisation. For example, in our PPM tool, PM3, we have screens in which both the project delivery risks (e.g. skills available, criticality of deadlines, stakeholder involvement level) and benefits delivery risks (e.g. business impact, benefits tangibility, benefits realization constraints) are scored consistently and objectively.

These are then mapped against data collected in further screens to consistently and objectively score the costs and benefits (e.g. NPV, strategic alignment, competitive advantage, regulatory compliance). Armed with this intelligence an informed debate can be initiated based on meaningful, credible comparative information.

Page | 3 ©Bestoutcome Limited 2011

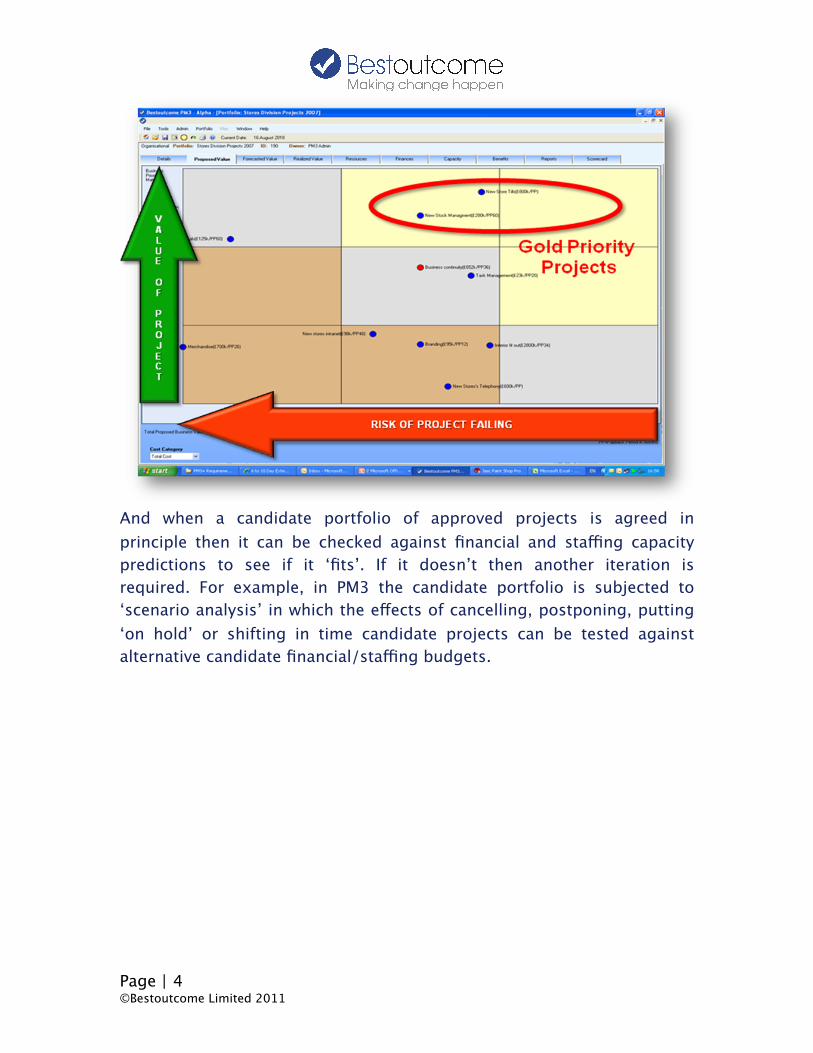

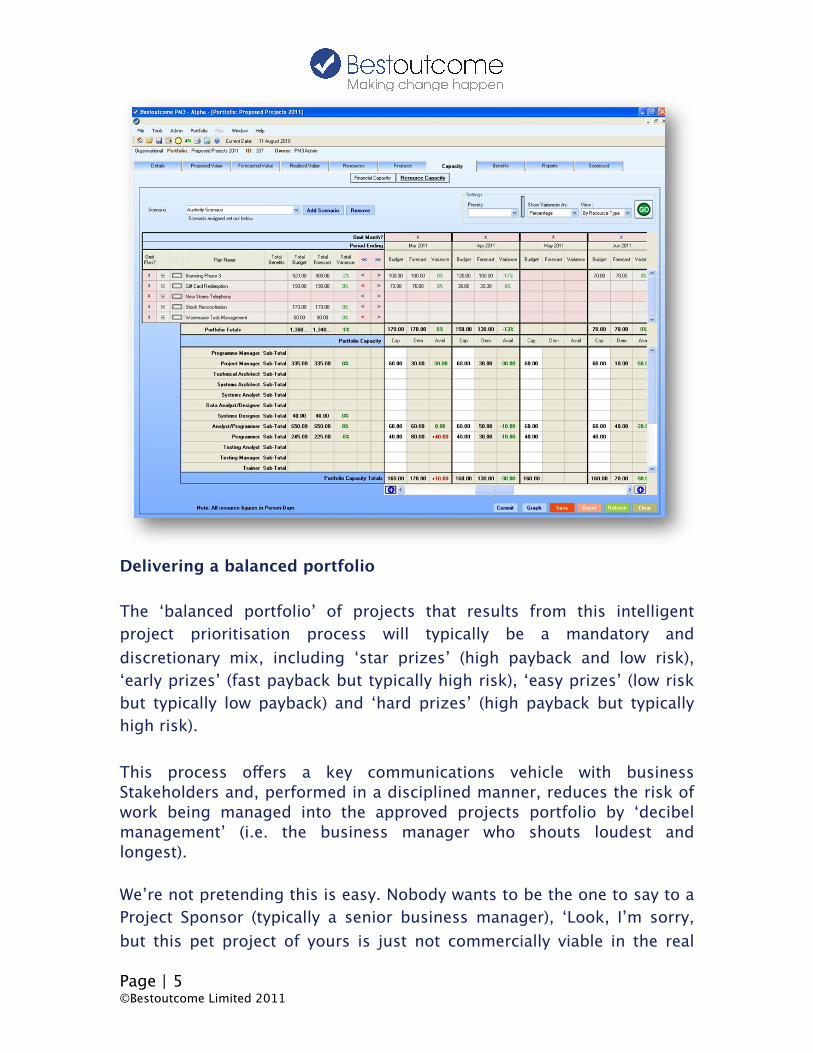

And when a candidate portfolio of approved projects is agreed in principle then it can be checked against financial and staffing capacity predictions to see if it ‘fits’. If it doesn’t then another iteration is required. For example, in PM3 the candidate portfolio is subjected to ‘scenario analysis’ in which the effects of cancelling, postponing, putting ‘on hold’ or shifting in time candidate projects can be tested against alternative candidate financial/staffing budgets.

Page | 4 ©Bestoutcome Limited 2011

Delivering a balanced portfolio

The ‘balanced portfolio’ of projects that results from this intelligent project prioritisation process will typically be a mandatory and discretionary mix, including ‘star prizes’ (high payback and low risk), ‘early prizes’ (fast payback but typically high risk), ‘easy prizes’ (low risk but typically low payback) and ‘hard prizes’ (high payback but typically high risk).

This process offers a key communications vehicle with business Stakeholders and, performed in a disciplined manner, reduces the risk of work being managed into the approved projects portfolio by ‘decibel management’ (i.e. the business manager who shouts loudest and longest).

We’re not pretending this is easy. Nobody wants to be the one to say to a Project Sponsor (typically a senior business manager), ‘Look, I’m sorry, but this pet project of yours is just not commercially viable in the real

Page | 5 ©Bestoutcome Limited 2011

world, so let’s not even start it.’ Nobody wants to be the one to say, ‘Look, I’m sorry, I know we have spent a small fortune on this project already, but the costs have risen and it just isn’t going to realise its promised benefits, at least not in its current state today, so lets kill it now.’ Nobody even wants to say, ‘Look, I’m sorry, although this project is commercially viable, the level of benefits you are pinning your hopes on are simply not remotely achievable in the real world and, anyway, we can probably get a bigger bang for our buck investing elsewhere.’ But if you don’t have the courage to take this ‘reality check’ on your project portfolio the financial consequences will almost inevitably be dire.

“IT Portfolio Management, with its continuing focus on value, risk and cost, has helped businesses reduce costs by up to 30% with a 2x-3x

increase in value” (Meta Group – ‘The Business of IT Portfolio Management: Balancing Risk, Innovation and ROI’)

Page | 6 ©Bestoutcome Limited 2011