huntsman - jp morgan hy & lev. fin. conf. - feb...

TRANSCRIPT

Huntsman CorporationJP Morgan Global High Yield and Leveraged Finance Conference

February 3, 2009

2

Forward Looking Statements

This presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements include statements concerning our plans, objectives, goals, strategies, future events, future revenue or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions, business trends and other information that is not historical information. When used in this presentation, the words “estimates,” “expects,” “anticipates,”“projects,” “plans,” “intends,” “believes,” “forecasts,” or future or conditional verbs, such as “will,” “should,” “could” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. All forward-looking statements, including, without limitation, management’s examination of historical operating trends and data, are based upon our current expectations and various assumptions. Our expectations, beliefs and projections are expressed in good faith, and we believe there is a reasonable basis for them. However, there can be no assurance that management’s expectations, beliefs and projections will be achieved.

There are a number of risks and uncertainties that could cause our actual results to differ materially from the forward-looking statements contained in this presentation. Such risks, uncertainties and other important factors include, among others: future global economic conditions, changes in raw material and energy prices, access to capital markets, industry production capacity and operating rates, the supply demand balance for our products and that of competing products, pricing pressures, technological developments, changes in government regulations, geopolitical events and other risk factors as discussed in our most recently filed Form 10-K and Forms 10-Q.

All forward-looking statements attributable to us or persons acting on our behalf apply only as of the date made and are expressly qualified in their entirety by the cautionary statements included in this presentation. We undertake no obligation to update or revise forward-looking statements which may be made to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events.This presentation contains financial measures that are not in accordance with generally accepted accounting principles in the U.S. ("GAAP"), including EBITDA, adjusted EBITDA from continuing operations, adjusted EBITDA from discontinued operations, normalized EBITDA and net debt. The Company has provided reconciliations of non-GAAP financial measures to the most directly comparable GAAP financial measures in the Appendix to this presentation.

3

$0

$2

$4

$6

$8

$10

$12

$14

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Huntsman Growth

MonsantoMAn/LAB

Rexene

Packaging Spinoff

Nova Styrenics Sale

Shell PP

American Hoechst Texaco

Chemical

TexacoPO/MTBE

Vantico

ICI

Ciba TEButadiene/MTBE SaleEuropean Base Sale

Total revenues Differentiated and Inorganic revenues

Dow Ethyleneamines and Rhodia Surfactants

Recent Events of Significance

Rev

en

ue (

$ in

Billio

ns)

Polymers SaleU.S. Base Sale

Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08

12/06 - Sold European

Petrochemicals

business to Sabic 06/07 - Basell to acquire

HUN for $25.25/share

07/07 - Hexion/Apollo to

acquire HUN for $28/share11/07 - Sold U.S. Base

Chemicals business to Koch

08/07 - Sold U.S. Polymer

business to Koch

09/08 - Decisive HUN legal

victory in Delaware against

Hexion/Aopllo

01/09 - $150 mm cost cutting,

significant capex reduction

12/08 - Settlement with

Hexion/Apollo for $1 billion

10/08 - Credit Suisse &

Deutsche Bank unwilling to

fund the Merger

06/08 - Hexion/Apollo attempt

to backout of Merger

4

Geographically DiverseQ3 2008 LTM Differentiated and Inorganic Revenue Distribution

New plant construction

Differentiated and inorganic revenues include Polyurethanes, Materials & Effects, Performance Products and Pigments

U.S. & Canada32 %

Europe 33 % Asia Pacific

21%

Rest of World14%

5

Growth ProfileRevenue Growth Targets

Target: ~GDPPerf. Spec., MAn ~3x GDPPerf. Int. ~GDP

Adv. Mtls. ~1.5x GDPTextile Effects ~GDP

~3x GDP

Polyurethanes

MDI

Polyols

PO/MTBE

TPU

Systems

Materials and Effects

Design & Composites Engineering

Power & Electronics

Coatings, Construction & Adhesives

Pigments

Titanium Dioxide

Performance Products

Performance Specialties

Performance Intermediates

Maleic Anhydride & Licensing

Textile Effects

Differentiated Pigments

6

Paints & Coatings

17%

Construction Materials

13%

Insulation

12%

Chemicals

11%

Energy

11%Aerospace

2%

Leisure Products 2%

Personal Care 3%

Household Products 4%

Home Furnishings 4%

Apparel 8%

Footwear 1%

Household Appliance 4%

Automotive 8%

Differentiated and Inorganic End Markets

Source: management estimates

Differentiated and inorganic revenues include: Polyurethanes, Materials & Effects, Performance Products and Pigments

Consumer durables & non-durables

7

Portfolio Composition – New Huntsman

(1) Adjusted EBITDA excludes restructuring and plant closing costs, loss on the sale of accounts receivables and other unusual

items; segment allocation is before corporate and other unallocated items.

Polyurethanes

53%

Performance

Products

24%

Materials &

Effects

19%

Pigments

4%

Materials &

Effects

24%

Performance

Products

25%

Pigments

11%Polyurethanes

40%

Q3 2008 LTM Revenue: $10.7 billion Q3 2008 LTM Adjusted EBITDA(1): $786 million

Inorganic

Differentiated

8

PolyurethanesBusiness Dimensions

Markets include:

� Adhesives, Coatings and Elastomers

� Appliances

� Automotive

� Construction

� Composite Wood Products

� Footwear

� Furniture and Bedding

� Q3 2008 LTM: Revenue $4.2 billion, Adjusted EBITDA $511 million

� Global reach: 2,000+ customers and sales in 90+ countries

� Commitment and focus on MDI-based applications, over 2,000 distinct MDI-based products

Adjusted EBITDA

$357

$264

$409

$734

$573 $593$511

$-

$250

$500

$750

2002 2003 2004 2005 2006 2007 Q308

LTM$ m

illio

ns

9

Materials & EffectsBusiness Dimensions

Markets include:

� Adhesives ���� Marine

� Aerospace ���� Power

� Apparel ���� Coatings

� Automotive

� Construction

� Electronics

� Sports and Leisure

� Textiles - Home and Technical

� Wind Energy

� Q3 2008 LTM: Revenue $2.5 billion, Adjusted EBITDA $185 million

� Sales in more than 90 countries

� Over 6,000 products to more than 5,000 customers

Adjusted EBITDA

$177$162

$226$242

$202$224

$185

-

100

200

300

2002 2003 2004 2005 2006 2007 Q308

LTM$ m

illio

ns

10

Performance ProductsBusiness Dimensions

Markets include:

� Agriculture ���� Paper

� Construction ���� Fuels

� Personal Care ���� Mining

� Gas Treatment

� Paints and Coatings

� Soaps and Detergents

� Ceramics

� Electronics

� Composites

� Metalworking

� Water Treatment

� Polyurethanes

Adjusted EBITDA

$196

$150

$186 $176

$209 $209$233

-

100

200

300

2002 2003 2004 2005 2006 2007 Q308

LTM$ m

illio

ns

� Q3 2008 LTM: Revenue $2.7 billion, Adjusted EBITDA $233 million

� Over 2,000 products sold to more than 4,000 customers

� Maleic Anhydride Expansion – 100mm lbs Geismar 2009,

100 mm lbs German JV 2011

� Ethyleneamines – 30kt Saudi JV 2009

11

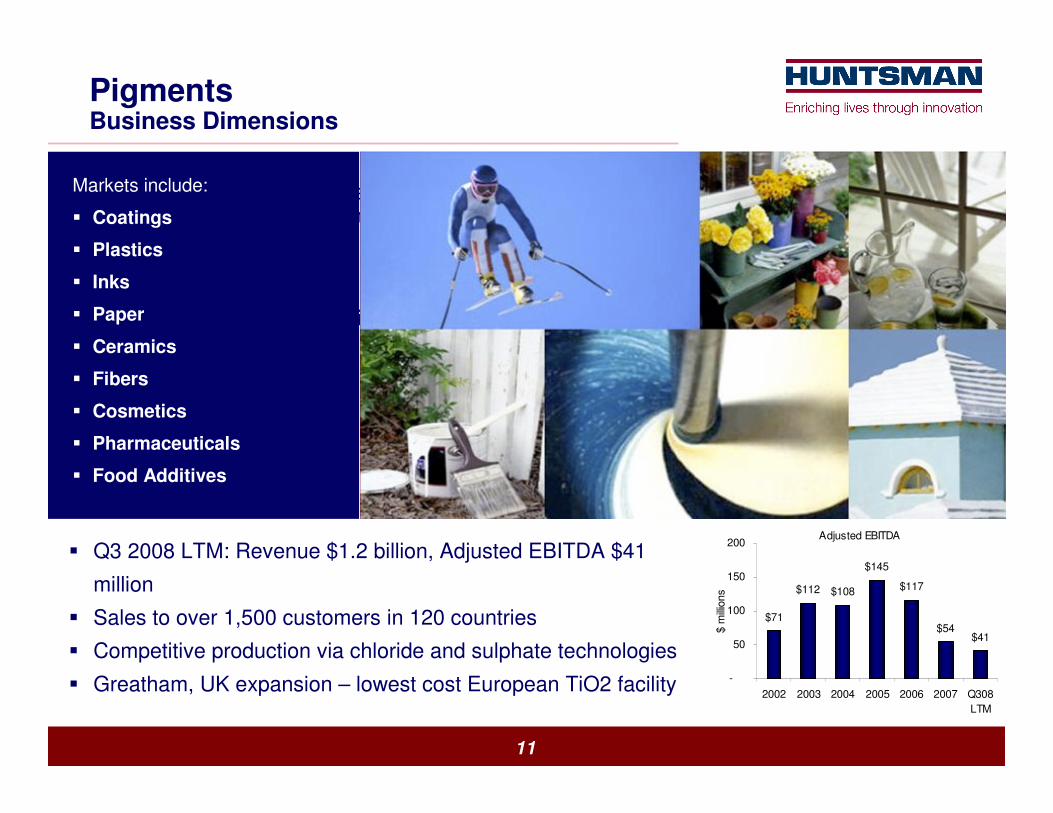

PigmentsBusiness Dimensions

� Q3 2008 LTM: Revenue $1.2 billion, Adjusted EBITDA $41 million

� Sales to over 1,500 customers in 120 countries

� Competitive production via chloride and sulphate technologies

Markets include:

� Coatings

� Plastics

� Inks

� Paper

� Ceramics

� Fibers

� Cosmetics

� Pharmaceuticals

� Food Additives

Adjusted EBITDA

$71

$112 $108

$145

$117

$54$41

-

50

100

150

200

2002 2003 2004 2005 2006 2007 Q308

LTM$ m

illio

ns

� Q3 2008 LTM: Revenue $1.2 billion, Adjusted EBITDA $41

million

� Sales to over 1,500 customers in 120 countries

� Competitive production via chloride and sulphate technologies

� Greatham, UK expansion – lowest cost European TiO2 facility

12

$ 759$ 661

$ 875

$ 1,166

$ 958 $ 925$ 786

-$200

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2002 2003 2004 2005 2006 2007 2008 LTM

Annual Adjusted EBITDA

Financial Performance

$2 6 2

$3 0 1

$2 2 1

$175

$2 4 4 $2 4 7 $2 4 0

$19 4 $18 8$2 10

$19 4

$ 0

$ 100

$ 200

$ 300

$ 400

Q1 06 Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q308

Quarterly Adjusted EBITDA

Polyurethanes

Performance Products

Materials & Effects

Corp/Other

Pigments$ in m

illio

ns

$ in m

illio

ns

Includes $49 million of hurricane impact

13

Cost Structure

0%

5%

10%

15%

20%

25%

30%

2002 2003 2004 2005 2006 2007 2008

% o

f N

et

Sale

s

Total Fixed Costs Plant Indirects SG&A

Fixed Costs(~25% of 2008 total costs)

Raw Material Costs(~65% of 2008 total costs)

50%

55%

60%

65%

2002 2003 2004 2005 2006 2007 2008

% o

f N

et

Sale

s

Raw Materials

Raw material costs increased over $800 million

2008 vs 2007

Note: proforma to include the results of Textile Effects prior to acquisition in June 2006

14

Cost CuttingAnnual Operating Cost Savings of $150 million

� Restructuring- 9% reduction in headcount: 1,175 positions to be eliminated by

year-end 2009

- Full-time contractor reduction of 490 positions

- Pigments Grimbsy, UK plant closure

- 40,000 tonne capacity to cease Q1 2009

- Annual operating cost savings of $28 million

- Estimated Q1 2009 charge of $60 million

- Total cash cost approximately $125 million

� Capital Expenditures

- 2009 capital expenditures expected to be approximately $230 million

15

Capitalization as of September 30, 2008(Excludes $1 billion received in December)

$ in millions Amount Maturity Moody's S&P

Secured Debt

Revolver ($650 million borrow ing capacity) 354 .5 x Aug-10 LIBOR + 1.75% Ba1 BB+

HI Term Loan B 1,540 2.4 x Aug-14 LIBOR + 1.75% Ba1 BB+

11.625% Senior Secured Notes due 2010 295 2.8 x Oct-10 Oct-07 11.63% Ba1 BB+

Senior Unsecured

11.5% Senior Fixed rate Notes due 2012 198 3.0 x Jul-12 Jul-08 11.50% Ba3 B+

Senior Subordinated Debt

6.875% Senior Subordinated Notes due 2013 584 3.8 x Nov-13 Nov-09 6.88% B2 B

7.875% Senior Subordinated Notes due 2014 352 4.2 x Nov-14 Nov-10 7.88% B2 B7.375% Senior Subordinated Notes due 2015 175 4.5 x Jan-15 Jan-10 7.38% B2 B

7.5% Senior Subordinated Notes due 2015 197 4.7 x Jan-15 Jan-10 7.50% B2 B

Other Debt

Huntsman Corporation Australia Credit facility 35 4.7 x May-10 10.15%

Huntsman Chemical Company Australia Credit Facility 19 4.8 x May-10 10.15%

PU Shanghai 127 4.9 x Dec-14 LIBOR + 0.48%

Other Debt 82 5.0 x N/A

Total GAAP Debt 3,958 5.0 x

Wtd. Avg. Interest Rate 6.80%

Cash (113) Wtd. Avg. Interest Rate on Variable Borrowings 5.48%

Total GAAP Net Debt 3,845 4.9 x

AR Securitization 422

Total HC Net Debt 4,267 5.4 x

Pro forma HC Net Debt ($750 settlement proceeds) 3,517 4.5 x

Adjusted LTM EBITDA 786

Multiple of

09/30/08 LTM

EBITDA

First Call

Date Interest Rate

Rating

16

1) Debt maturity does not include off balance sheet Accounts Receivable securitization program ($422 mm as of 09/30/08)2) As represented by first date at which debt becomes callable by its terms3) Huntsman Revolver has a stated maturity of 2010, however for US GAAP purposes it is classified as current debt

752

4468

51

2,816

227

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2008 2009 2010 2011 2012 Thereafter

957

352198

2,451

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Current 2008 2009 2010

Debt Maturities (1) (3) Callable Debt(1)(2)

($ in millions)($ in millions)

Debt Maturities & Callable Debtas of September 30, 2008

17

Summary

� Strong balance sheet- Ample liquidity ($1 billion received in December)

- Attractive debt maturity profile

- Low borrowing costs

� Insurance claim outstanding for $235 million in arbitration / mediation- $365 million received separately thus far

� Multi-billion dollar tortious interference claim against Credit Suisse and Deutsche Bank

- Texas trial set for May 11, 2009

� Attractive product offering- Most products grow at positive GDP multiples (substitution effect)

� End market usage well diversified

� Strong global position

� Low cost manufacturer

� Proven management team

Appendix

19

Adjusted EBITDA Reconciliation

$ in millions

Q1 '06 Q2 '06 Q3 '06 Q4 '06 Q1 '07 Q2 '07 Q3 '07 Q4 '07 Q1 '08 Q2 '08 Q3 '08

Net (loss) / income 69$ 263$ (182)$ 80$ 47$ (71)$ (150)$ 2$ 7$ 24$ (20)$

Interest expense - net 87 95 83 86 74 70 72 70 65 66 68

Income tax expense / (benefit) 15 18 (18) (65) 12 (8) (13) (3) 3 21 18

Depreciation and amortization 88 88 89 98 95 94 93 99 94 98 99

Income taxes, depreciation and amortization in discont. ops. 23 36 41 38 14 (62) 7 (65) 0 2 1

EBITDA 281 499 14 237 242 23 8 102 170 210 165

Loss on sale of accounts receivable 2 3 3 4 4 5 7 4 5 5 6

Unallocated foreign currency loss 1 (2) (12) 4 3 4 4 2 5 6 (4)

Legal and contract settlement expense, net - (9) - - - 6 - - - - -

Loss on early extinguishment of debt - - 15 13 1 0 - 0 - - -

Other restructuring, impairment and plant closing costs 8 1 4 3 - 13 9 8 - 1 4

Merger associated expenses - - - - 11 - 205 5 4 4 26

Gain (loss) on disposition of assets - (92) (1) 1 (4) - - (69) 5 - -

(Income) loss from discontinued operations net of tax (53) (71) 206 (88) (11) 187 7 141 1 (7) (1)

Extraordinary gain on the acquisition of a business, net of tax - (51) (7) 2 (2) 9 - - (0) (8) (2)

Cumulative effect of changes in accounting principle - - - - - - - - - - -

Adjusted EBITDA from continuing operations 239 279 221 175 244 247 240 194 188 210 194

Acquisition - Textile Effects 22 22 - - - - - - - - - Pro Forma Adjusted EBITDA from continuing operations 262$ 301$ 221$ 175$ 244 247 240$ 194$ 188$ 210$ 194$

2002 2003 2004 2005 2006 2007 Q308 LTM

Net (loss) / income (167)$ (426)$ (228)$ (35)$ 230$ (172)$ 13$

Interest expense - net 544 578 613 427 351 286 269

Income tax (benefit) / expense(1)

(10) 32 (29) 21 (50) (12) 39

Depreciation and amortization(1)

488 480 537 501 363 380 389

Income taxes, depreciation and amortization in discont. ops. n/a n/a n/a n/a 138 (107) (62)

EBITDA 854 664 893 913 1,031 375 647

Loss on sale of accounts receivable 6 32 13 9 13 20 20

Unallocated foreign currency loss (48) (109) (109) 33 (10) 12 8

Legal and contract settlement expense, net (9) 8 7 - (9) 6 -

Loss on early extinguishment of debt 7 - 26 323 27 2 0

Other restructuring, impairment and plant closing costs 109 90 274 107 15 31 13

Merger associated expenses - - - - - 221 38

Gain (loss) on disposition of assets - - - - (92) (73) (64)

(Income) loss from discontinued operations net of tax (109) (117) (301) (337) (6) 324 133

Extraordinary gain on the acquisition of a business, net of tax - - - - (56) 7 (10)

Cumulative effect of changes in accounting principle (167) - - 31 - - -

Adjusted EBITDA from continuing operations 643 567 803 1,078 914 925 786

Acquisition - Textile Effects 116 94 72 88 45 - - Pro Forma Adjusted EBITDA from continuing operations 759$ 661$ 875$ 1,166$ 958$ 925$ 786$

(1) Includes discontinued operations for periods 2002 - 2005

20

Segment Adjusted EBITDA

$ in millions

Q1 '06(2)

Q2 '06(2)

Q3 '06 Q4 '06 Q1 '07 Q2 '07 Q3 '07 Q4 '07 Q1 '08 Q2 '08 Q3 '08

Adjusted EBITDA

Polyurethanes 158$ 172$ 136$ 108$ 119$ 159$ 173$ 142$ 132 148 89 Materials & Effects 60 56 47 40 63 61 53 47 40 51 48

Performance Products 52 77 38 42 72 40 48 49 53 51 81 Pigments 36 32 26 23 23 21 4 7 12 7 16

Corporate and other (43) (35) (26) (37) (32) (35) (37) (50) (48) (46) (40)

Segment Adjusted EBITDA from cont. ops.(1)

262$ 301$ 221$ 175$ 244$ 247$ 240$ 194$ 188$ 210$ 194$

Pro Forma(2,3)

Pro Forma(2,3)

Pro Forma(2)

Pro Forma(2)

Pro Forma(2)

2002 2003 2004 2005 2006 2007 Q308 LTM

Adjusted EBITDA

Polyurethanes 357$ 264$ 409$ 734$ 573$ 593$ 511$

Materials & Effects 177 162 226 242 202 224 185 Performance Products 196 150 186 176 209 209 233

Pigments 71 112 108 145 117 54 41 Corporate and other (42) (28) (54) (131) (142) (154) (184)

Segment Adjusted EBITDA from cont. ops.(1)

759$ 661$ 875$ 1,166$ 958$ 925$ 786$

(1) For a reconcilation of Segment Adjusted EBITDA to Net Income see previous page.

(2) Pro forma as if Huntsman had acquired its interest in Textile Effects as of January 1, 2002.

(3) Pro forma as if Huntsman had acquired the remaining interest in HIH as of January 1, 2002 and its interest in Advanced Materials as of January 1, 2002.