for what it’s worth: how an appraiser values your business presented by sherry c. smith to the...

TRANSCRIPT

FOR WHAT IT’S WORTH:HOW AN APPRAISER VALUES YOUR BUSINESS

Presented by Sherry C. Smith

To The Rotary Club of Pawleys Island

May 3, 2007

Events That May Trigger the Need for a Business Valuation

• Estate Planning, Gifting – minority interests• Death – step up the basis • Sale of Business• Recapitalization – new equity• Buyout of a Partner – buy/sell provisions• Minority Shareholder Dispute• Employee Stock Ownership Plan (ESOP)• Divorce, Litigation

Drivers of Value

• In investment theory, the two drivers of value are risk and return

• Higher value = lower risk and/or higher return

• Discount rate = the return required by an investor to make a particular investment

• Return = true cash return, not income that has been manipulated by tax planning

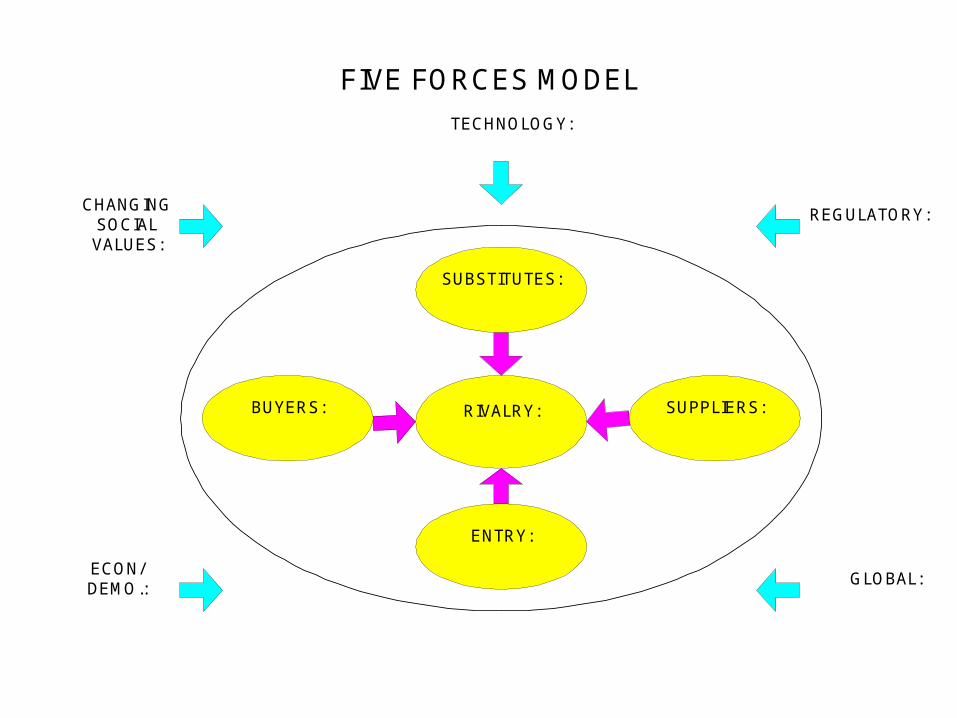

Context: Look at the Economy, Industry, and Subject Company

• What are the prospects for growth?

• How risky is it?

• How well has the company performed historically?

• What are the implications of trends in the economy, industry, and company on:– Revenue Growth?

– Operating Profit Margins?

– Interest Costs?

– Business Risk?

– Financial Risk?

RIVALRY:

SUBSTITUTES:

BUYERS:

ENTRY:

SUPPLIERS:

TECHNOLOGY:

CHANGINGSOCIALVALUES:

ECON/DEMO.:

GLOBAL:

REGULATORY:

FIVE FORCES MODEL

SWOT ANALYSIS

Strengths

Weaknesses

Opportunities

Threats

Valuation Approach #1: Income Approach

• Favorite method of appraisers (when possible) because treats the business as an investment

• Best measure for income approach: project future cash flows to invested capital (debt and equity)

• Estimate a rate of return appropriate for the business that takes into account the level of risk

• Two methods within this approach: Single Period Capitalization Method and Multiple Period Discounting Method

Build-up Method of Determining a Discount Rate and Capitalization Rate

Symbol Component Increment Rate

Long-term Treasury Bond Yield1 5.70 + Equity Risk Premium, 7.40 = Average Market Return 13.10

Specific Risk Adjustment

+ Risk Premium for Size, microcap stocks2 9.15

+ Industry Risk2 0.94

+ Management Depth3 1.00

+ Diversification - Customer and Geographic3 1.00

+ Financial Risk3 (2.00) = Net Cash Flow Discount Rate - Next Year's 23.19 - Long-term Sustainable Growth Rate (5.00) = NET CASH FLOW CAPITALIZATION RATE - ROUNDED 18.00

Valuation Approach #2: Market Approach

• Guideline Public Company Method – look for close comparables

• Merger & Acquisition Method – look for transactions in the marketplace

• Direct Market Data Method – statistical, large database, not close comps

Goal is to find appropriate multiples of revenues, or some other measure (cash flow, earnings, etc.)

Direct Market Data Method

Scatterplot of Price to Revenues Ratios

0

500

1000

1500

2000

2500

3000

0 200 400 600 800 1000 1200 1400

Annual Revenues in thousands

Sel

ling

Pri

ce in

th

ou

san

ds

+10

+25

Median-25

-10

Valuation Approach #3: Asset

• Usually last choice

• The value of the whole business should be greater than the sum of its parts

• If not: liquidation

• The asset-based approach marks every entry on the balance sheet to market

• The Excess Earnings Method (an asset-based method) gives a value for goodwill

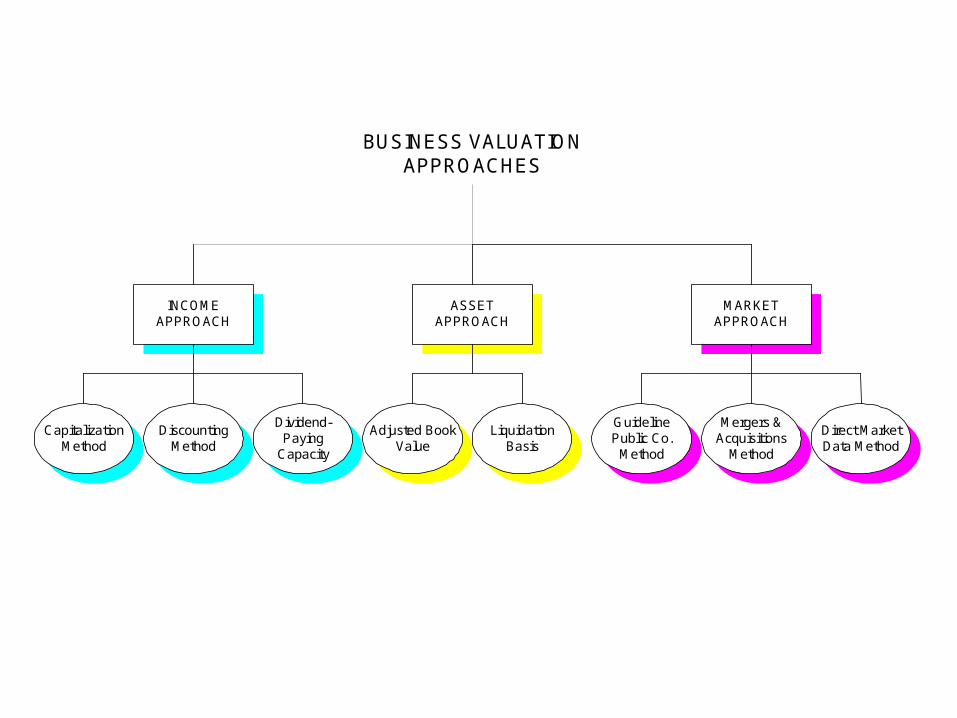

BUSINESS VALUATIONAPPROACHES

ASSETAPPROACH

INCOMEAPPROACH

MARKETAPPROACH

CapitalizationMethod

DiscountingMethod

Dividend-Paying

Capacity

Adjusted BookValue

LiquidationBasis

Mergers &Acquisitions

Method

GuidelinePublic Co.

Method

Direct MarketData Method

LEVELS OF VALUE APPRAISAL METHODS

CONTROL MARKETABLE VALUEControl value as if freely traded

CONTROL MARKETABLE VALUEControl value as if freely traded

CONTROL NON-MARKETABLE VALUEControl value not freely traded

MARKETABLE NON-CONTROL VALUEMinority interest as if freely traded

NON-MARKETABLE NON-CONTROL VALUEMinority interest not freely traded

Ÿ Single Period Capitalization Method (controlstream)

Ÿ Multiple Period Discounting Method (controlstream)

Ÿ Merger & Acquisition Transaction Method

Ÿ Adjusted Book Value MethodŸ Excess Earnings MethodŸ Direct Market Data Method

Ÿ Guideline Public Company MethodŸ Single Period Capitalization Method (non-control stream)

Ÿ Multiple Period Discounting Method (non-control stream)

No direct appraisal method available for thisvalue level

Above methods must be used and discountsapplied

Control premium

Discount for lack ofmarketability (control

interest)

Discount for lack of control

Discount for lack of marketability(non-control interest)

SOURCE: Adapted from a chart presented by Paul R. Hyde in the Summer 2000 issue of Business Appraisal Practice

NOTE: The Single Period Capitalization Method and the Multiple Period Discounting Method (Income Approaches) mayyield either a control or non-control value based on the income stream used.

So, How to Increase Value• Most importantly, keep good financial records

• Increase returns by:– Going after new, growing markets

– Seeking advantages over competitors (strong brand recognition, dominant market share, excellent distribution channels, patents)

– Lowering expenses

• Reduce risk by:– Building management strength

– Stabilizing balance sheet

– Locking in customer contracts

– Diversifying in terms of customers, geography, suppliers

4420 Oleander Drive, Suite 203

Myrtle Beach, SC 29577

843-839-3763

Sherry C. Smith