evaluation of poverty alleviation...

TRANSCRIPT

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 191

CHAPTER 6

EVALUATION OF POVERTY ALLEVIATION PROGRAMMES

Evaluation not only helps in counting the milestones but also setting the target in

future. It can be done during the implementation of the programme or after the completion of

the programme. In our study, evaluation is specifically related to socio-economic impact of

these poverty alleviation programmes. In this chapter an attempt has been made to evaluate

various poverty alleviation programmes adopted to check poverty. This chapter has been

divided into three sections. The first section delineates various poverty alleviation

programmes that are in vogue, in India. Section II deals with effectiveness of various poverty

alleviation programmes implemented in Punjab. Section III gives an overview of evaluation

of poverty alleviation programmes on the basis of feed back of 100 beneficiaries from Punjab

(Doaba region).

SECTION I

6.1 Various Poverty Alleviation Programmes Working in India

Poverty is a most threatening single challenge that needs a multidimensional

approach. A broad spectrum solution is required to curb and control it. It has been apparent

from various empirical studies. Sundaram (2004), and Verma and Gogna (2009) observed

that education is a necessary condition for improving the lot of poor. Mishra and Rao (2003)

found that trade liberalization accelerates growth and thereby reduces poverty. Rajan (2002)

provided the empirical authentication that various countries managed to reduce poverty with

trade liberalization policies. Ray and Lancaster (2005) established the evidence that public

distribution system is useful for backward classes as anti-poverty programme. Dev (2000)

observed that expenditure on rural infrastructure and technical support to agriculture had a

better impact than government spending on poverty alleviation programmes. Various studies

such as Ahluwalia (1978), Shrinivasan (1985), and Dev (1988) show that agricultural

development reduces poverty.

The government has taken various steps to alleviate poverty in the country. Explicitly,

the emphasis has been on removing poverty through two approaches i.e. training for rural

self-employment and provision of wage employment.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 192

6.1.1 Rural Poverty Alleviation Programmes

Drive against poverty has been undertaken from Fourth Five Year Plan onwards in

the country. During Fourth Five Year Plan, following programmes were launched: Small

Farmer Development Programmes (SFDP) and Drought-Prone Area Programme. Poverty

alleviation programmes started in Fifth Plan were: Food for Work Programme and Minimum

Needs Programme. Particular programmes for employment were started in Sixth Plan (1980-

85), viz Integrated Rural Development Program (IRDP), National Rural Employment

Program (NREP), Training Rural Youth for Self-Employment (TRYSEM) and Rural

Landless Employment Guarantee Programme (RLEGP). In Seventh Plan (1985-90)

government started the Jawaharlal Rozgar Yojana in 1989, and later on NREP and RLEGP

were merged with it. Employment Assurance Scheme (EAS) was implemented on October 2,

1993 during the Eighth Plan. The process of rural employment continued during Ninth Plan

and the following three schemes were started:

i) Pradhan Mantri Gramodaya Yojana (PMGY, 2000-01) the focus of PMGY is on

health, primary education, drinking water, housing and rural roads. It covers

following programmes:

• Pradhan Mantri Gram Sadak Yojana (PMGSY), launched on 25th December 2000

for constructing roads in rural areas. It is a 100 per cent centrally funded scheme.

• Pradhan Mantri Gramodaya Yojana (Rural Drinking Water Project)

• Pradhan Mantri Gramodaya Yojana (Gramin Awas) fulfills housing needs of

poor.

ii) Swarnjayanti Gram Swarojgar Yojana (SGSY) is an integrated rural development

scheme. Various other programmes (TRYSEM, DWCRA, MWS, SITRA and GKY)

were merged into Swarnjayanti Gram Swarojgar Yojana (SGSY) from April 1, 1999.

It assisted 83 lac people in 2002-03 and 90 lac people in 2003-04.

iii) Sampoorana Grameen Rozgar Yojana (SGRY) is a wage employment scheme.

The Employment Assurance Scheme (EAS) and Jawahar Gram Samridhi Yojana

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 193

(JGSY) were merged into Sampoorana Gramin Rojgar Yojana. (SGRY) on

September 25, 2001. It is implemented through Panchayati Raj institutions (PRIs).

Rural Employment Guarantee Scheme was launched by Prime Minister Manmohan

Singh on February 2, 2006. This programme guarantees 100 days of wage employment to

every rural household in the country.

6.1.2 Urban Employment Guarantee Programmes

The proportion of urban poor in India was estimated at 23.62 per cent of total urban

population in 1999 and 15.01 per cent in 2007 (Planning Commission). In order to improve

the conditions of the urban poor, two employment schemes namely Prime Minister’s Swarna

Jayanti Shahari Rozgar Yojana (SJSRY) and Prime Minister Rozgar Yojana (PMRY) were

launched. Salient features of the schemes are given below:-

i) Swarna Jayanti Shahari Rozgar Yojana was launched on December 1, 1997. The

three urban employment generation programmes already in operation were subsumed

in SJSRY. These were: Nehru Rozgar Yojana (NRY), Urban Basic Service for Poor

(UBSP), Prime Minister’s Integrated Urban Poverty Eradication Programme

(PMIUPEP)1. This scheme is funded by centre and state, with the objective of

providing self-employment and urban wage employment. This scheme is being

monitored by State Urban Development Authority (SUDA). The SUDA implements

the programme through District Development Agency. Overall responsibility for

execution of these schemes lies with the Ministry of Urban Development and Poverty

Alleviation. The expenditure incurred on this scheme during 2004-05 was Rs.103

crore.

ii) Prime Minister Rozgar Yojana (PMRY) is a 100 per cent centrally funded scheme.

It provides self-employment to urban educated unemployed youth. At district level, it

is implemented by District Industries Centre (DIC). In metropolitan cities, it is

operated by Small Industries Services Institute (SISI).

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 194

6.1.3 Micro Credit and Poverty Alleviation

Dr. Mohammad Yunus, founder of Grameen Bank, “If we are looking for one single

action which will enable the poor to overcome their poverty, I will focus on credit”

Micro finance in its simplest form is termed as “banking for the poor.” It creates

employment opportunities, empowers the rural women, improves the living standard of the

rural people and alleviates poverty. Micro finance programmes provide loan to poor people

for self-employment projects and helps in generating income, allowing them to care for their

families. Khandelwal (2007) pointed out that micro credit programmes are potentially a very

significant contributor to pro-poor development. Swaminathan (2007), a noted agricultural

scientist, observed that by providing micro credit to the “poorest of the poor” the gap in the

formal rural credit sector can be filled. Fernandez (2007) opined that the non-government

organizations (NGOs) and microfinance institutions (MFIs) together can maintain balance

between the environments for poverty eradication and a loan portfolio.Vasimalai and

Narinder (2007) expressed the view that micro-financing has shown substantial change in the

income in urban context (77 per cent) as compared to rural area (65 per cent). Significantly

the change in income in both the areas has been substantial. In short, micro-credit has been

viewed as the most effective method of providing finance to the less privileged.

Indian money market system there is organized as well as unorganized sector.

Organised money market (Commercial Banks, Regional Rural Banks and Co-operative

Banks) lend money against personal credit of borrowers. It insists on security, which small

landless farmers or poor people can not offer. About 70 crore people live in rural areas. This

section of the population does not have large sum of money and is in dire need of money.

Unfortunately total demand for credit from Indian society cannot be met by Indian banking

alone. Moreover there are a number of people who do not qualify for bank loans. Here comes

the role of micro-credit. Microfinance institutions exist in the form of credit unions,

commercial banks and NGOs and SHGs. The present framework of micro credit in India is as

given below.

i) National Bank of Agriculture and Rural Development (NABARD): - It provides

financial support to Bankers, SHGs and NGOs for promotions of micro-finance. It

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 195

provides 100 per cent refinance backing to banks for financing SHGs. NABARD has

formulated a scheme for giving assistance to District Co-operative Central Banks

(DCCBs) and Primary Agricultural Co-operatives Credit Societies (PACs) to cherish

self-help groups. The scheme is implemented in various states of the country through

Regional Rural Banks (RRBs). NABARD conducted various training programmes.

Training of staff of banks, NGOs, Government agencies and SHGs leads to booming

operation2.

ii) State Bank of India (SBI):- It has enthusiastically participated in SHG-Bank Credit

Linkage programme project of NABARD. SBI has made a continuous progress in

financing SHGs. Majority of these are women SHGs. SBI is maintaining its position

as a leader among commercial banks in financing of SHGs. As at the end of March

2006, out of total SHGs financed by commercial banks, SBI’s share has been

approximately 47 per cent. SBI had credit linking with 1 million SHGs by March

20083.

iii) Small Industries Development Bank of India (SIDBI):- SIDBI identifies, takes

care of and develops micro financing institutions and provides credit support. SIDBI

Foundation for Micro Credit (SFMC) was launched by the Bank in January 1999 for

providing funds to the poor. SFMC’s mission is to create a national network of strong,

workable and sustainable microfinance institutions (MFIs)4.

iv) Self-help Groups (SHGs):- Micro-credit has proven an effective measure in on

going struggle against poverty. The programme of linking SHGs of rural poor with

banking was launched in 1992 to strengthen credit delivery in rural areas. Its focus is

on the rural poor. There are three forms of SHGs with banks viz.; i) SHGs formed

and financed by banks; ii) SHGs formed by agencies and financed by banks; iii)

SHGs financed by banks using NGOs as financial intermediates5.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 196

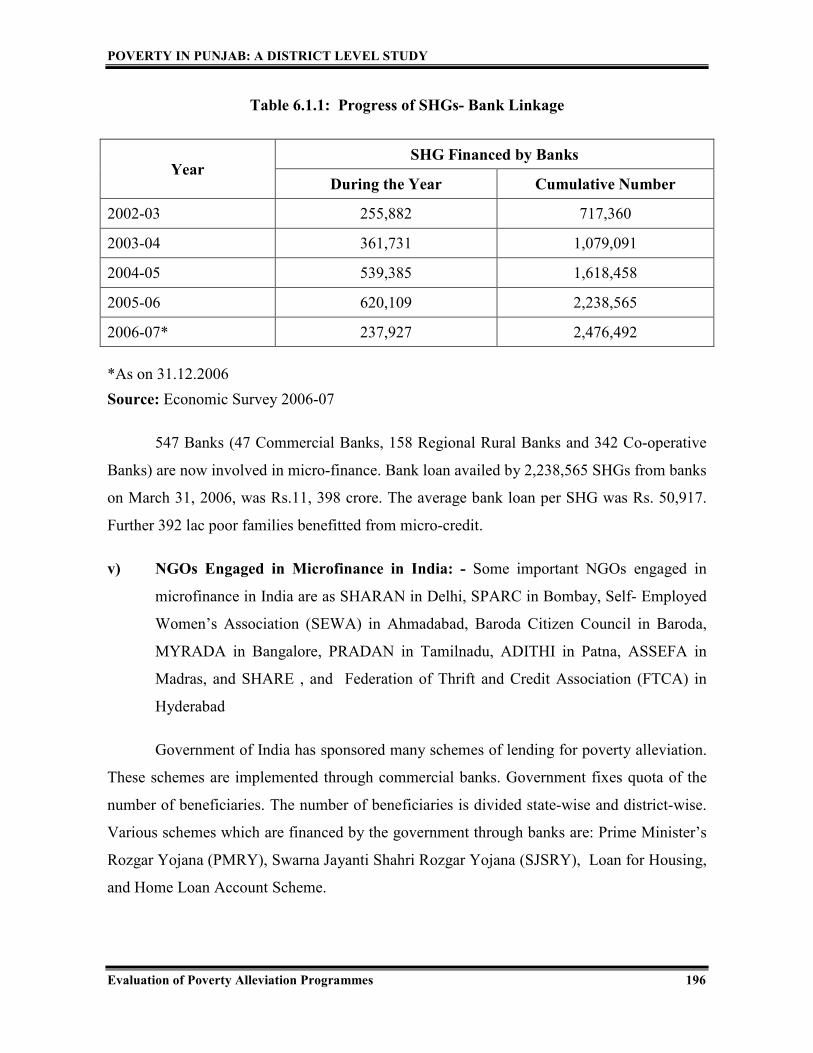

Table 6.1.1: Progress of SHGs- Bank Linkage

Year SHG Financed by Banks

During the Year Cumulative Number

2002-03 255,882 717,360

2003-04 361,731 1,079,091

2004-05 539,385 1,618,458

2005-06 620,109 2,238,565

2006-07* 237,927 2,476,492

*As on 31.12.2006

Source: Economic Survey 2006-07

547 Banks (47 Commercial Banks, 158 Regional Rural Banks and 342 Co-operative

Banks) are now involved in micro-finance. Bank loan availed by 2,238,565 SHGs from banks

on March 31, 2006, was Rs.11, 398 crore. The average bank loan per SHG was Rs. 50,917.

Further 392 lac poor families benefitted from micro-credit.

v) NGOs Engaged in Microfinance in India: - Some important NGOs engaged in

microfinance in India are as SHARAN in Delhi, SPARC in Bombay, Self- Employed

Women’s Association (SEWA) in Ahmadabad, Baroda Citizen Council in Baroda,

MYRADA in Bangalore, PRADAN in Tamilnadu, ADITHI in Patna, ASSEFA in

Madras, and SHARE , and Federation of Thrift and Credit Association (FTCA) in

Hyderabad

Government of India has sponsored many schemes of lending for poverty alleviation.

These schemes are implemented through commercial banks. Government fixes quota of the

number of beneficiaries. The number of beneficiaries is divided state-wise and district-wise.

Various schemes which are financed by the government through banks are: Prime Minister’s

Rozgar Yojana (PMRY), Swarna Jayanti Shahri Rozgar Yojana (SJSRY), Loan for Housing,

and Home Loan Account Scheme.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 197

Verma and Gogna (2007) expressed the view that there should be proper

identification of target group for micro-financing. Along with credit, training should be given

for proper utilization of resources. There is a need for continuous improvement in programme

design also. Finance should be used for productive purpose and not for consumption purpose,

and there should be coordination among all the micro-credit institutions.

An attempt has been made to catalogue a brief design of poverty alleviation

programmes in rural and urban areas. Now the question is how these programmes work at

grass root level. The other area that need enquiry is the effectiveness of such programmes for

the poor. The question that haunts is if, the programmes meant for the poor reach them or not.

SECTION II

6.2 Poverty Alleviation Programmes in Punjab

6.2.1 Poverty Alleviation Programmes in Operation in Punjab

This section deals with various poverty alleviation programmes under operation in

Punjab with special reference to district Kapurthala and their effectiveness. At present the

government of Punjab is implementing following poverty alleviation programmes:

Swarnjayanti Gram Swarojgar Yojana (SGSY), National Rural Employment Guarantee

Scheme (NREGS), Indira Awas Yojana (IAY), and Atta Dal Scheme.

6.2.1.1 Swarnjayanti Gram Swarojgar Yojana (SGSY)

The SGSY is a programme for rural poor entrepreneurs. This scheme is meant for

rural BPL families as well as vulnerable groups like SC/STs, women and disabled persons. It

helps the swarozgaries through bank credit and government subsidy. It provides funds to

individuals as well as self-help groups. The objective of SGSY is to bring swarozgaries

above poverty line within three years. Persons covered under this programme are known as

swarozgaries6. There are two types of swarozgaries: Individual Swarozgaries and Self-help

Groups. The financial and physical performance of SGSY has been evaluated for all blocks

of Kapurthala district on the basis of use of funds.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 198

Table 6.2.1: Funds Available under SGSY Programme for Kapurthala District

(Rs.in Lac)

Year Opening

Balance

Release of

Fund from

Centre

Release of

Fund from

State

Miscellaneous

Total

Available

Fund

2005-06 0.06 8.90 9.39 4.19 22.54

2006-07 0.31 30.36 6.68 1.01 38.36

2007-08 1.88 21.13 10.03 0.86 33.90

2008-09 2.98 37.18 6.65 0.85 47.67

2009-10 12.43 38.37 12.55 2.38 65.73

Source: District Rural Development Agency, Kapurthala.

The year-wise details of funds released by the center as well as the state government

for SGSY program (Self-help Groups and Swarozgaris) is depicted in Table 6.2.1. During the

year 2006-07, the total funds available was Rs. 38.36 lacs, which decreased to Rs. 33.90 lacs

in 2007-08 but after that it increased to Rs. 47.67 lacs in 2008-09 and to Rs. 65.73 lacs in

2009-10. Thus the release of funds increased excepting the year 2007-08.

Table 6.2.2: Expenditure under SGSY Program for Kapurthala District (Rs. in Lac)

Year Expenditure on

Individual Case

Expenditure

Self-Help group

as Subsidy

Revolving

Fund

Total

Expenditure

2005-06 9.60

(43.18)

11.70

(52.63)

0.93

(4.18)

22.23

(100)

2006-07 15.78

(43.25)

18.00

(49.34)

2.70

(7.40)

36.48

(100)

2007-08 11.12

(35.96)

18.23

(58.95)

1.57

(5.09)

30.92

(100)

2008-09 15.07

(42.76)

16.95

(48.09)

3.22

(9.15)

35.24

(100)

2009-10 26.34

(68.25)

9.60

(24.88)

2.63

(6.87)

38.57

(100)

Note: Figures in parenthesis represent percentages.

Source: District Rural Development Agency, Kapurthala

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 199

In Kapurthala district, the funds of SGSY programme were spent on individual cases,

self-help groups and in the form of revolving fund. The major portion of the fund till 2008-09

was spent on subsidy to self-help groups. In 2009-10, ratio of expenditure on individual cases

is more in comparison to self-help groups. But amount of expenditure on self-help groups

shows increased tendency till 2007-08, after which it declined.

The financial assistance to individual swarozgaries was 43.18 per cent in 2005-06. It

declined to 35.96 per cent in 2007-08. It shows that during this period comparatively more

attention was given to self-help groups than individual swarozgaries for performing various

activities (dairy, steel furniture, welding, shuttering, timber merchant, embroidery, vegetable

vendors, grocery, electricity, stitching, cycle repair, radio, television repair etc). But after

2007-08, more attention in terms of distribution of funds under SGSY program was given to

individual cases and by 2009-10 more than two-third of expenditure under this scheme was

incurred on individual cases. The expenditure incurred on subsidies to SHGs has been merely

a little less than 25 per cent. However, about 7 per cent of the funds under this scheme were

kept as revolving fund in 2009-10.

Table 6.2.3: Budget of Financial Assistance under SGSY for Kapurthala District

(Rs. in Lac)

Year Total Available Fund Expenditure Balance

2005-06 22.54 22.23

(98.6)

0.31

(1.4)

2006-07 38.36 36.48

(95.09)

1.88

(4.91)

2007-08 33.90 30.92

(91.21)

2.98

(8.79)

2008-09 47.67 35.24

(73.92)

12.47

(26.08)

2009-10 65.73 38.57

(58.67)

27.16

(41.33)

Note: Figures in parenthesis represent percentages.

Source: District Rural Development Agency, Kapurthala

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 200

Table 6.2.3 shows that in 2005-06 the percentage of utilisation of funds under SGSY

was 98.6 per cent which declined steadily to 95.09 per cent in 2006-07, 91.21 per cent in

2007-08, 73.92 per cent in 2008-09 and finally to 58.67 per cent in 2009-10. Thus, under

utilization of funds under this scheme accelerated over the years. It is clear from the Table

that even the available funds were not fully utilized. From this point of view, it can be

concluded that SGSY is not performing well.

Table 6.2.4: Block-wise Number of Beneficiaries under Self-help Groups

Year Dhilwan Kapurthala Nadala Phagwara Sultanpur

2005-06 23 24 35 20 23

2006-07 29 30 35 22 24

2007-08 32 35 35 28 27

2008-09 38 37 35 30 28

2009-10 40 40 36 32 31

Source: District Rural Development Agency, Kapurthala

So far as progress in terms of member of self-help groups is concerned, it has been

increasing in all the blocks of Kapurthala district. Highest progress is observed in Dhilwan

block and lowest in Nadala. The number of self -help groups increased from 23 to 40 (75.9

per cent increase) in Dhilwan, from 24 to 40 (66.6 per cent increase) in Kapurthala, from 35

to 36 (2.08 per cent increase) in Nadala, from 20 to 32 (60.0 per cent increase) in Phagwara,

from 23 to 31 (75.9 per cent increase) in Sultanpur. Thus it can be concluded that the

progress of SGSY is uneven. It is clear from the Table that even the available funds in any

year were not fully utilised. There should be more involvement of BDOs in the formation of

self-help groups so that more and more funds are utilized and poor people get the benefit of

this scheme.

6.2.1.2 National Rural Employment Guarantee Scheme (NREGS)

The National Rural Employment Guarantee Act was passed in September 2005 and

NREGA was launched in 2006-07 in 200 districts. It covered 130 more districts in 2007-08

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 201

under further expansion. From April 1, 2008 it has been applied to whole country. On

October 2, 2009 it was renamed as MNREGA. Under this scheme, 3.67 crore rural

households were provided employment during 20107.

Appendix 6.1 shows that employment generated under NREGA scheme varied from

state to state. Appendix 6.2 shows district-wise employment generated in Punjab during the

year 2009-10. Families that completed 100 working days under this scheme varied from

district to district.

Table 6.2.5: Year- wise Details of Employment Generated under NREGA in

Kapurthala District

Year

No of

Registered

Households

Job

Cards

Issued

Employment No. of

Families

Completed

100 days Demanded Offered Provided

2007-08 00526 00000 0000 0000 0000 000

2008-09 11443 10933 0000 0000 0000 000

2009-10 12557 12547 4397 4397 4392 063

Source: http://nrega.nic.in/netnrega

Official data of Kapurthala district shows impressive figure of households registered

and job cards issued. It is found that the number of households registered (12557) is very

close to job cards issued (12547) in 2009-10. Almost all the persons who demanded

employment were offered job under this scheme. The share of SCs in NREGA employment

is 83.86 per cent in Kapurthala district whereas the corresponding figure in Punjab is 78.92

per cent in 2010-20118.

As per the rules and regulation of NREGA scheme, one third of the persons offered

employment should be women9. It is noticed that the share of women in NREGA workforce

has been 33.9 per cent in Kapurthala District, whereas in the Punjab it is 26.28 per cent10

.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 202

Table 6.2.6: Block-wise Employment Generated in Kapurthala District under NREGA

up to the Year 2009-10

Year Registered

HHs

Job

Cards

Issued

Employment Families

Completed

100 days Demanded Offered Provided

Dhilwan

Up to

2008 0010 0000 0000 0000 0000 00

Up to

2009 1964 1950 0000 0000 0000 00

Up to

2010 2072 2072 0745 0745 0745 12

Kapurthala

Up to

2008 0053 0000 0000 0000 0000 00

Up to

2009 2425 2186 0000 0000 0000 00

Up to

2010 2740 2734 1074 1074 1074 29

Nadala

Up to

2008 0174 0000 0000 0000 0000 00

Up to

2009 2149 2149 0000 0000 0000 00

Up to

2010 2307 2307 0941 0941 0941 00

Phagwara

Up to

2008 0058 0000 0000 0000 0000 00

Up to

2009 2203 2156 0000 0000 0000 00

Up to

2010 2447 2447 0764 0764 0764 03

Sultanpur

Up to

2008 0231 0000 0000 0000 0000 00

Up to

2009 2702 2492 0000 0000 0000 00

Up to

2010 2991 2987 0873 0873 0868 19

Source: District Rural Development Agency, Kapurthala

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 203

A continuous increase in wage rate under this scheme has been observed. The wage

rate was increased from Rs. 60 to Rs. 75 per day in 2007-08 i.e. a hike of 15 per cent. It was

again raised to Rs. 100 in 2008-09.The new wage rate Rs.100 per day was made effective

from 1st April 2009

11. It is mentioned in National Rural Employment Guarantee Act

“Different wage rate may be given for different areas but not less than Rs.100”12

.But state

government was given a free hand to add to this centrally fixed wage rate. Just seven states

Haryana, Himachal Pradesh, Kerala, Punjab, Sikkim and Tripura pay Rs.100 or more13

. The

various works undertaken under NREGA are water conservation, irrigation and flood

protection etc14

.The purpose of the scheme is double fold to provide employment and

amenities.

Table 6.2.6 depicts that the progress of number of households registered, job cards

issued, employment demanded, employment offered and employment provided is observed in

all the blocks of the district. But the number of families that completed 100 days of

employment in a year is very less.

6.2.1.3 Indira Awas Yojana (IAY)

This scheme is launched for scheduled caste and non-scheduled caste BPL rural poor.

IAY was started in 1985-86 as a sub-scheme of Rural Landless Employment Guarantee

Program (RLEGP). Since January 1, 1996, it has been working as an independent scheme.

IAY is a centrally sponsored scheme. However the contributory share between centre and

state is 80:20. But in case of union territories, it is funded by Government of India. During a

financial year, 60 per cent of IAY assistance is marked for scheduled castes/ schedule tribes

and remaining 40 per cent is meant for others. It also caters to the need of freed bonded

labour, victim of atrocities and natural calamities, and the families headed by widows and

unmarried women15

.

Under IAY, Rs.25,000 is given to the BPL families for the construction of houses,

sanitary latrines and smokeless chulhas. The beneficiaries are selected from the list of eligible

households by the Gram Sabha.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 204

Table 6.2.7: Budget of Financial Assistance under IAY for Kapurthala District

(Rs. in Lac)

Year Receipts Expenditure Balance

2007-08 94.37 74.00

(78.41) 20.37

2008-09 135.56 95.52

(70.46) 40.04

2009-10 261.62 52.97

(20.25) 208.65

Note: Figures in parenthesis represent percentages.

Source: District Rural Development Agency, Kapurthala.

The year -wise release of funds shows that total receipts increased from Rs.94.37 lac

in 2007-08 to Rs. 135.56 lac in 2008-09 and to Rs. 261.62 in 2009-10. Allocation and

receipts under this scheme were observed increasing. These funds were spent for renovation

of old houses. However on the other hand, the ratio of utilization of funds under this scheme

has been decreasing, being 78.41 per cent in 2007-08, 70.46 per cent in 2008-09 and 20.25

per cent in 2009-10. Hence, it shows lack of involvement and awareness among people

regarding IAY (Table 6.2.7).

The release of funds increased over the period under consideration in Dhilwan,

Kapurthala, Phagwara and Sultanpur block, but the same pattern was not observed in case of

Nadala block. Table 6.2.8 shows that in 2007-08 the balance of unutilisated fund under IAY

was only in Nadala and Phagwara, but in 2008-09 it was found in Dhilwan, and in 2009-

10 it is observed in all districts. Further, under utilization of funds under this scheme

accelerated over the years.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 205

Table 6.2.8: Block-wise details of Funds Released for Kapurthala District under Indira

Awas Yojana (Rs. in Lac)

District Year Receipts Expenditure Balance

Dhilwan

2007-08 16.88 16.88 00.00

2008-09 18.95 06.20 12.75

2009-10 31.216 - 31.216

Total 67.046 23.08 43.966

Nadala

2007-08 23.12 09.62 13.50

2008-09 17.10 09.92 07.18

2009-10 37.16 06.62 30.54

Total 77.38 26.16 51.22

Kapurthala

2007-08 17.50 17.50 00.00

2008-09 32.68 32.68 00.00

2009-10 92.186 16.10 76.086

Total 142.366 66.28 76.086

Phagwara

2007-08 19.62 12.75 06.87

2008-09 22.21 02.10 20.11

2009-10 34.75 02.65 32.10

Total 76.58 17.50 59.08

Sultanpur

2007-08 17.25 17.25 00.00

2008-09 44.62 44.62 00.00

2009-10 66.31 27.60 38.71

Total 128.18 89.47 38.71

Source: District Rural Development Agency, Kapurthala.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 206

6.2.1.4 Atta Dal Scheme

Table 6.2.9 shows that district Faridkot, Muktsar, Nawan Shehar, Ferozepur,

Bathinda, Gurdaspur, Mansa, Barnala, Patiala, Sangrur and Taran Taran have poverty ratio

above average. Ropar, Hoshiarpur, Fatehgarh, Kapurthala, Jalandhar, Mohali, Amritsar,

Ludhiana, Moga on the other hand, have poverty ratio below the state average. As per the

survey conducted for Atta Dal Scheme a total number of families in 2007 in Kapurthala were

1,43,116. Out of these total 1,43,116 families 5,765 were declared BPL as per Planning

Commission report i.e. 4.22 per cent families were below poverty line. But the BPL families

identifies in Atta Dal Survey were 39,956 i.e. 27.92 per cent i.e. difference of 24.70

percentage points.

Big difference in the percentage of BPL families identified through census survey by

Planning Commission and those identified under Atta Dal scheme by Punjab Government has

been observed. In some cases the difference in percentage distribution is inexplicably large.

For instance, in case of district Faridkot the percentage of BPL families identified by the

Planning Commission is 8.23 per cent. This figure is 43.29 per cent under Atta Dal Scheme

of the Punjab Government, a difference between these two estimates being as large as 35.06

percentage points. Like wise, for Nawan Shehar, the difference in the proportion of BPL

families identified by the Punjab Government against these identified by Planning

Commission is 30.26 percentage points. The story is almost similar in case of other districts

too. For all the districts together, Planning Commission surveyed 11.59 per cent of families

as living below poverty line. This figure is as high as 28.31 per cent (a difference of 16.72

percentage points) for the state as a whole. It also gives an indication that even officially the

state Government acknowledges that poverty ratio in the state is much higher than what has

been specified by the Planning Commission.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 207

Table 6.2.9: District-wise Number of BPL Families Introduced by Planning Commission

and the BPL Families Identified Under Atta Dal Scheme by Punjab Government

S.

No Districts

Families

Surveyed

BPL Families

Identified by Census

Survey

(Planning

Commission)

BPL Families

Identified under

Atta Dal Scheme by

Punjab Government Difference

Percentage

BPL

Families Percentage

BPL

Families Percentage

1 2 3 4 5 6 7 8 (7-5)

1 Amritsar 410483 40325 10.51 97239 23.69 13.18

2 Bathinda 234627 23884 11.43 74452 31.73 20.30

3 Fatehgarh 96527 14598 15.63 27673 28.67 13.04

4 Faridkot 115684 8044 08.23 50077 43.29 35.06

5 Ferozepur 364568 53407 17.74 109908 30.15 12.41

6 Gurdaspur 429288 34341 09.38 128854 30.02 20.64

7 Hoshiarpur 295799 23082 08.25 83582 28.26 20.01

8 Jalandhar 360011 71870 19.74 99343 27.59 07.85

9 Kapurthala 143116 5765 04.22 39956 27.92 23.70

10 Ludhiana 545594 31351 05.61 131613 24.12 18.51

11 Mansa 141620 15715 12.98 40389 28.52 15.54

12 Moga 174778 18860 12.27 31879 18.24 05.97

13 Muktsar 184085 16848 12.44 65451 35.55 23.11

14 Nawanshehar 119446 5993 05.56 42782 35.82 30.26

15 Patiala 325053 38293 13.20 93789 28.85 15.65

16 Ropar 129542 8543 07.64 33592 25.93 18.29

17 Sangrur 291819 43591 16.97 82665 28.33 11.36

18 Mohali 140244 9044 06.86 35159 25.07 18.21

19 Barnala 92401 25809 28.05 29987 32.45 04.40

20 Taran Taran 164298 14474 09.18 48972 29.81 20.63

Total 4758983 503837 11.59 1347362 28.31 16.72

Source : Atta Dal Scheme 31/05/2007.x

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 208

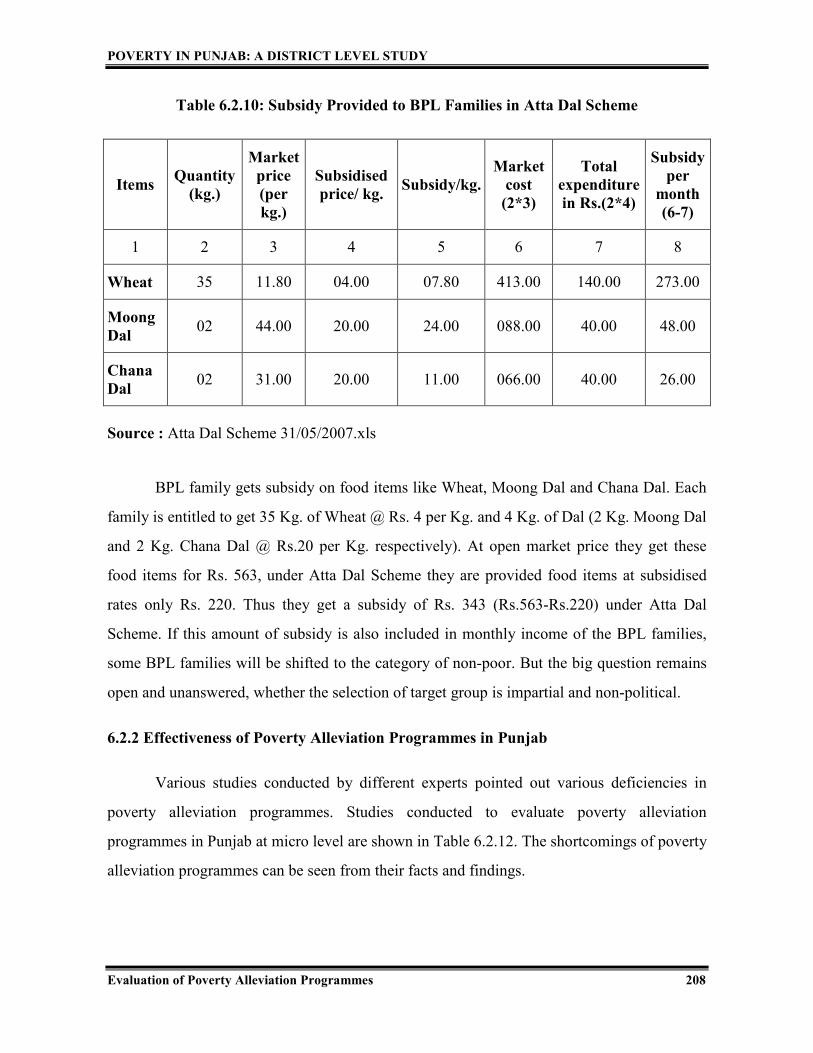

Table 6.2.10: Subsidy Provided to BPL Families in Atta Dal Scheme

Items Quantity

(kg.)

Market

price

(per

kg.)

Subsidised

price/ kg. Subsidy/kg.

Market

cost

(2*3)

Total

expenditure

in Rs.(2*4)

Subsidy

per

month

(6-7)

1 2 3 4 5 6 7 8

Wheat 35 11.80 04.00 07.80 413.00 140.00 273.00

Moong

Dal 02 44.00 20.00 24.00 088.00 40.00 48.00

Chana

Dal 02 31.00 20.00 11.00 066.00 40.00 26.00

Source : Atta Dal Scheme 31/05/2007.xls

BPL family gets subsidy on food items like Wheat, Moong Dal and Chana Dal. Each

family is entitled to get 35 Kg. of Wheat @ Rs. 4 per Kg. and 4 Kg. of Dal (2 Kg. Moong Dal

and 2 Kg. Chana Dal @ Rs.20 per Kg. respectively). At open market price they get these

food items for Rs. 563, under Atta Dal Scheme they are provided food items at subsidised

rates only Rs. 220. Thus they get a subsidy of Rs. 343 (Rs.563-Rs.220) under Atta Dal

Scheme. If this amount of subsidy is also included in monthly income of the BPL families,

some BPL families will be shifted to the category of non-poor. But the big question remains

open and unanswered, whether the selection of target group is impartial and non-political.

6.2.2 Effectiveness of Poverty Alleviation Programmes in Punjab

Various studies conducted by different experts pointed out various deficiencies in

poverty alleviation programmes. Studies conducted to evaluate poverty alleviation

programmes in Punjab at micro level are shown in Table 6.2.12. The shortcomings of poverty

alleviation programmes can be seen from their facts and findings.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 209

Table 6.2.11: Evaluation of Poverty Alleviation Programs in Punjab

Investigator Period District Programme Results

Navreet

Singh

1980-85 Bathinda He observed lack of political interest in the schemes.

He also noted that most of bank officials ask for

“cuts” before they sanction the loan. He also found

that many undeserving people had been issued yellow

cards simply because of corruption.

Chander 1984-87 Bathinda He was satisfied that some real poor have been

assisted but he suggested proper publicity of these

programmes.

Karan 1985-86 Sangrur He noticed that 90 per cent of the loans were

sanctioned for dairy purpose and there was misuse of

loans.

Sandhu 1985-86 Ropar He observed that the well-off persons had been issued

yellow cards. He concluded that the whole process is

fraud with misutilization, leakages, undue influences

etc.

Kalsi 1985-86 Ludhiana 55,117 families were identified as below poverty line

by the end of 1982-83 and out of them 22,489 families

benefitted from poverty alleviation programmes.

Sidhu 1985-86 Patiala He focused on defects of yellow cards and reported

the inclusion of many undeserving cases and

exclusion of deserving cases.

Khanna 1988-89 Patiala He found that there were 29 beneficiaries in district

Patiala, village Bhunerheri during 1988-89. “The

BDO’s office has also taken up construction of drains

and streets, latrines and planting of trees in the village,

it also helped out in the creation of other assets.”

Sarangal 1986-87 Amritsar He concluded that “people are not getting proper

benefits from the special programmes”. He found that

undeserving people get the benefit by influencing the

local Sarpanchs, whereas genuine people were

deprived of the benefit.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 210

Investigator Period District Programme Results

Mittal 1986-87 Ludhiana “A close study of the programme in district Ludhiana

reveals that its impact on the rural poor has not been

as good as was expected by planners”.

Reddy 1986-87 Hoshiarpur He found that identification of viable schemes has not

been done by administration. He strongly

recommended use of administrative efficiency and

more staff.

Chhatwal 1987-88 Ludhiana His finding has been that none of the beneficiaries

belonged to the poorest of the poor category. Most of

them were no doubt poor but many poorer than those

were left out.

Gupta 1989-90 Many yellow card holders are still waiting for IRDP

loans.

Shankar 1990-91 Amritsar He observed that all surveyed families had mis-

utilized loan amount taken under IRDP. He found

JRY is better as Panchayats use it for making drainage

system and street etc.

Tewari 1991-92 Sangrur JRY was not very helpful as it gives only seasonal

employment.

Vikram 1992-93 Poorest sections of the village i.e. the Harijan Basti

have remained untouched. These parts of the village

have neither proper streets nor drains and they

invariably get water logged and slushy during each

monsoon.

Source: Vora,R. (2000),”Government Programmes in Socio Economic Profile of Rural

India”, Concept Publishing Company, New Delhi.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 211

SECTION III

6.3 Empirical Analysis of Poverty Alleviation Programs

This section deals with empirical analysis of poverty alleviation programmes. Poverty

ratio is maximum in Kapurthala district of Doaba region. So, Kapurthala district was selected

for the purpose of survey. Kapurthala district has five blocks –Dhilwan, Kapurthala, Nadala,

Phagwara and Sultanpur and on the basis of highest number of BPL families, Phagwara block

has been selected. The selection of three villages was finalized after consultations with the

concerned Block Development Officer (BDO). Finally, 100 households from rural area were

surveyed. A structured schedule has been used for survey of beneficiaries of different

schemes. The samples were drawn from the beneficiaries’ list provided by the BDO and 100

households from Kapurthala district were surveyed for evaluation of poverty alleviation

programme. Both primary and secondary data were used to evaluate the performance of

poverty alleviation programmes. Secondary data was compiled from the Annual Progress

Reports maintained by the Department of Rural Development, Government of Punjab. For

primary data, out of the sampled 100 BPL households, we took 40 Swarozgaris of Self-help

groups (SGSY) from village Bhularai, 20 MNREGA workers and 10 beneficiaries of Indira

Awas Yojana (IAY) from village Mauli and 30 beneficiaries of Atta Dal Scheme from our

sample survey for poverty estimation.

6.3.1 Socio -Economic Condition of the Beneficiaries

Evaluation of poverty alleviation programmes is based on the feed back of 100

beneficiaries’ households. Out of them ninety per cent households were of scheduled caste

and 10 per cent were of non-scheduled castes. These 100 beneficiaries’ households surveyed

had 544 family members. Out of them, 290 were males and 254 were females. Further, as

regards the education level, it can be seen that out of 502 beneficiaries of +7 years age, 355

beneficiaries were literate and 147 were illiterate. Out of 355 literate people, 134 members

had educational background of primary, 108 members of middle, 69 members of matriculate,

and 42 members of senior secondary, and only 02 members of graduate and above level. In

short, 48.20 per cent had under matriculate qualification. It has been found that 45 per cent

beneficiaries had a family size of 1-5 members, 51 per cent had 6-10 members and 04 per

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 212

cent had family size of 11 or more members. The family size affects the per capita income

negatively and dependency ratio positively. Table 6.3.1 also depicts the occupation structure

of these respondent beneficiaries. Five per cent beneficiaries were self-employed in non-

agriculture, 4 per cent self-employed in agriculture, 8 per cent were regular labour, 80 per

cent were casual labour and remaining 3 per cent were engaged in private jobs.

Table 6.3.1: Social Characteristics of Households Possessing BPL Card

S.No. Characteristics Number Percentage

1 Gender-wise Household Members

Male 290 53

Female 254 46

2 Caste of Household Head

Scheduled Caste (SC) 91 91

Non-Scheduled Caste (Non - SC) 09 09

3 Size of family

1-5 Members 244 45

6-10 Members 276 51

11 and above members 24 04

4 Literacy of Household Members

Literate 355 65

Illiterate 147 35

5 Literacy Level of Household Members

Primary 134 38.00

Middle 108 30.00

Matriculate 69 19.44

Senior Secondary 42 12.00

Graduate and Above 02 0.56

6 Occupation of Households

Self- employed in non agriculture 05 05

Self -employed in agriculture 04 04

Regular labour 08 08

Casual labour 80 80

Private jobs 03 03

Source: Author’s Calculations

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 213

Table 6.3.2: Economic Characteristics of Household Possessing a BPL Card

S.No. Characteristics Number

1 Income

i) Below poverty line

Up to 300 04

300-500 23

ii) Above poverty line

500-750 35

750 and above 38

2 Type of house

Kutcha house 27

Semi-pucca house 30

Pucca house 43

3 No. of rooms

One room 27

Two room 54

Three room 15

Four room and more 04

4 Kitchen

Availability of separate kitchen 48

Non-availability of separate kitchen 52

5 Electricity and toilet

Availability of electricity and toilet 53

Non-availability of electricity and toilet 47

6 Tenure status

Own house 93

Rented house 07

7 Use of LPG 46

8 Household durables

Fan 91

Heater 01

Cooler 01

Television 78

Refrigerator 51

Microwave 00

Cycle 78

Scooter/Bike 06

Car 00

Sewing machine 59

Washing machine 02

Telephone 32

Source: Author’s Calculations

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 214

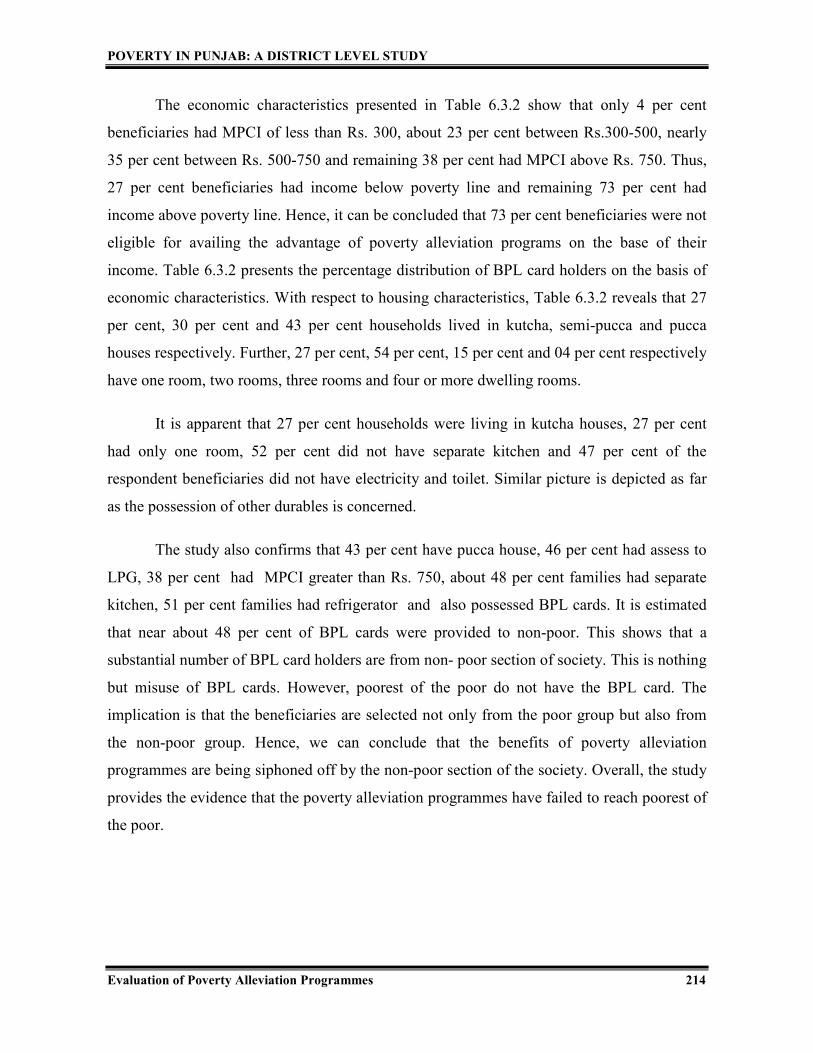

The economic characteristics presented in Table 6.3.2 show that only 4 per cent

beneficiaries had MPCI of less than Rs. 300, about 23 per cent between Rs.300-500, nearly

35 per cent between Rs. 500-750 and remaining 38 per cent had MPCI above Rs. 750. Thus,

27 per cent beneficiaries had income below poverty line and remaining 73 per cent had

income above poverty line. Hence, it can be concluded that 73 per cent beneficiaries were not

eligible for availing the advantage of poverty alleviation programs on the base of their

income. Table 6.3.2 presents the percentage distribution of BPL card holders on the basis of

economic characteristics. With respect to housing characteristics, Table 6.3.2 reveals that 27

per cent, 30 per cent and 43 per cent households lived in kutcha, semi-pucca and pucca

houses respectively. Further, 27 per cent, 54 per cent, 15 per cent and 04 per cent respectively

have one room, two rooms, three rooms and four or more dwelling rooms.

It is apparent that 27 per cent households were living in kutcha houses, 27 per cent

had only one room, 52 per cent did not have separate kitchen and 47 per cent of the

respondent beneficiaries did not have electricity and toilet. Similar picture is depicted as far

as the possession of other durables is concerned.

The study also confirms that 43 per cent have pucca house, 46 per cent had assess to

LPG, 38 per cent had MPCI greater than Rs. 750, about 48 per cent families had separate

kitchen, 51 per cent families had refrigerator and also possessed BPL cards. It is estimated

that near about 48 per cent of BPL cards were provided to non-poor. This shows that a

substantial number of BPL card holders are from non- poor section of society. This is nothing

but misuse of BPL cards. However, poorest of the poor do not have the BPL card. The

implication is that the beneficiaries are selected not only from the poor group but also from

the non-poor group. Hence, we can conclude that the benefits of poverty alleviation

programmes are being siphoned off by the non-poor section of the society. Overall, the study

provides the evidence that the poverty alleviation programmes have failed to reach poorest of

the poor.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 215

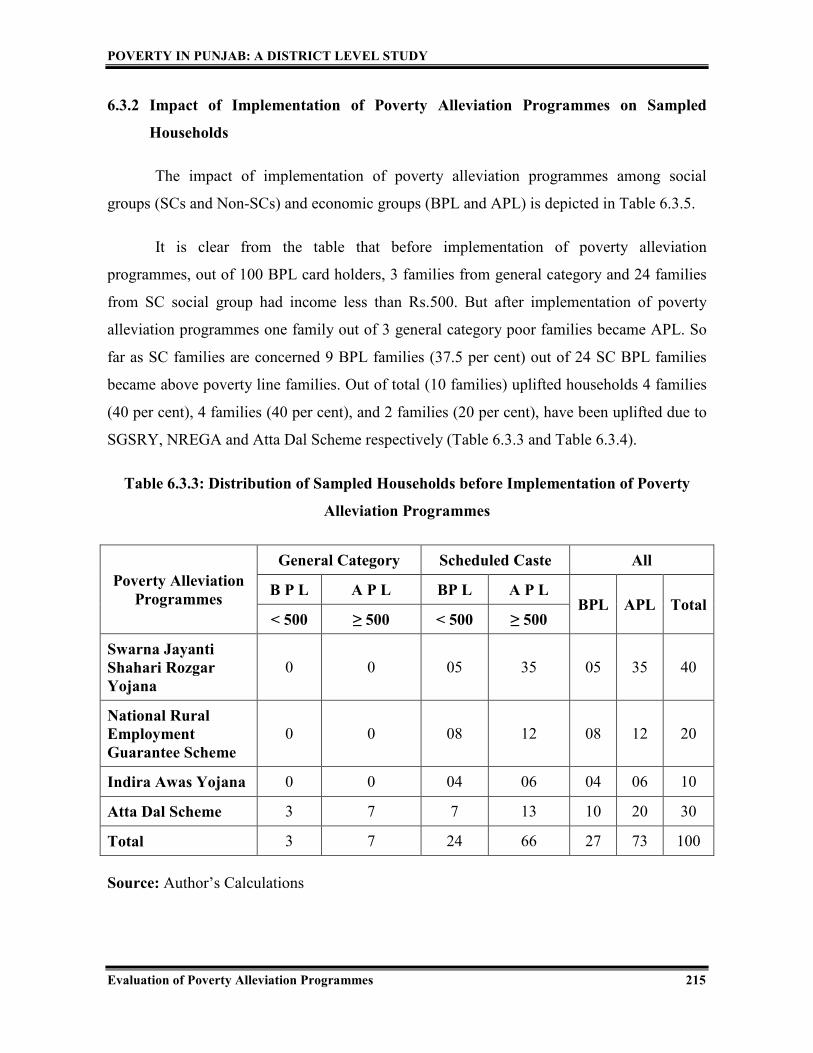

6.3.2 Impact of Implementation of Poverty Alleviation Programmes on Sampled

Households

The impact of implementation of poverty alleviation programmes among social

groups (SCs and Non-SCs) and economic groups (BPL and APL) is depicted in Table 6.3.5.

It is clear from the table that before implementation of poverty alleviation

programmes, out of 100 BPL card holders, 3 families from general category and 24 families

from SC social group had income less than Rs.500. But after implementation of poverty

alleviation programmes one family out of 3 general category poor families became APL. So

far as SC families are concerned 9 BPL families (37.5 per cent) out of 24 SC BPL families

became above poverty line families. Out of total (10 families) uplifted households 4 families

(40 per cent), 4 families (40 per cent), and 2 families (20 per cent), have been uplifted due to

SGSRY, NREGA and Atta Dal Scheme respectively (Table 6.3.3 and Table 6.3.4).

Table 6.3.3: Distribution of Sampled Households before Implementation of Poverty

Alleviation Programmes

Poverty Alleviation

Programmes

General Category Scheduled Caste All

B P L A P L BP L A P L BPL APL Total

< 500 ≥ 500 < 500 ≥ 500

Swarna Jayanti

Shahari Rozgar

Yojana

0 0 05 35 05 35 40

National Rural

Employment

Guarantee Scheme

0 0 08 12 08 12 20

Indira Awas Yojana 0 0 04 06 04 06 10

Atta Dal Scheme 3 7 7 13 10 20 30

Total 3 7 24 66 27 73 100

Source: Author’s Calculations

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 216

Table 6.3.4: Distribution of Households after Implementation of Poverty Alleviation

Programmes

Poverty

Alleviation

Programs

General Category Scheduled Caste All

B P L A P L BP L A P L BPL APL Total

< 500 ≥ 500 < 500 ≥ 500

Swarna Jayanti

Shahari Rozgar

Yojana

0 0 01 39 01 39 40

National Rural

Employment

Guarantee

Scheme

0 0 04 16 04 16 20

Indira Awas

Yojana 0 0 04 06 04 06 10

Atta Dal Scheme 2 8 06 14 08 22 30

Total 2 8 15 75 17 83 100

Source: Author’s Calculations

Table 6.3.5: Percentage of Poor Before and After Implementation of Poverty Alleviation

Programmes

Particulars

General Category Scheduled Caste All

B P L A P L BP L A P L BPL APL

< 500 ≥ 500 < 500 ≥ 500

Household before

Implementation of

PAP Programs

3 7 24 66 27 73

Household after

Implementation of

PAP programs

2 8 15 75 17 83

Change -1 +1 -9 +9 -10 +10

Source: Author’s Calculations

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 217

We find that the Atta Dal Scheme pushed 20 per cent below poverty line households

to above poverty line. In case this benefit is withdrawn, people will slip down again to their

previous status i.e. BPL. So, not only food subsidy but also some supplementary requirement

should be met in such a manner that they are able to raise their income by involving

themselves in self-help groups or working as individual swarozgaries. Micro-financing and

wage employment programmes like MNREGA make them self-dependent. How long one can

continue to depend entirely on poverty alleviation programmes? The poverty alleviation

programmes should act only as a pull factor. After providing help to some poor people the

support system of government should cover other poor groups i.e. once a poor should not

remain poor for always. Rather the uplifted people should act as a role model for the other

needy people. Once this system starts working the process of upliftment will go on and the

condition of poor will go on improving. This is the crux of study.

Table 6.3.6: Opinion of Respondents on Implementation of Poverty Alleviation

Programmes

Particulars

General Category Scheduled Caste

All BPL APL BPL APL

< 300 300-

500

500-

750 ≥750 < 300

300-

500

500-

750 ≥750

Beneficiary

households satisfied

with distribution of

benefits under PAP

- - - 4 - - - 34 38

Beneficiary

households satisfied

to some extent

- - 3 - - - 32 - 35

Beneficiary

households not

satisfied

0 3 - - 4 20 - - 27

Total households

holding BPL cards 0 3 3 4 4 20 32 34 100

Source: Author’s Calculations

Table 6.3.6 depicts the opinion of respondents on implementation of poverty

alleviation programmes. Out of 10 beneficiaries (BPL card holders) under general category

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 218

only 3 families are from below poverty line income group and 7 are from APL income group

(3 household in income group Rs.500-750 and 4 households from ≥Rs.750). However,

among SC households, out of 90 beneficiary families (BPL card holders) 24 families are

below poverty line (4 household in income group < Rs.300 and 20 households from Rs.300-

500) and 66 families are from APL income group (32 household in income group Rs.500-750

and 34 households from ≥ Rs.750). On the basis of income group, we find that the

beneficiaries having less than Rs. 500 income are not satisfied with the benefits under various

poverty alleviation programs. Beneficiaries in the income group Rs.500-750 are satisfied to

some extent. Households with income ≥ Rs. 750 are satisfied with poverty alleviation

programmes. This is found applicable both for SC and non-SC category.

Table 6.3.7: Distribution of Households Regarding their Satisfaction Level for

Various Poverty Alleviation Programmes

Poverty Alleviation

Programs Satisfaction Level

Number Percentage

Swarna Jayanti Shahari

Rozgar Yojana

Satisfied 17 42.50

Satisfied to some extent 17 42.50

Not satisfied 6 15.00

Total 40 100

National Rural

Employment Guarantee

Programme

Satisfied 6 30.00

Satisfied to some extent 6 30.00

Not satisfied 8 40.00

Total 20 100

Indira Awas Yojana

Satisfied 5 50.00

Satisfied to some extent 2 20.00

Not satisfied 3 10.00

Total 10 100

Atta Dal Scheme

Satisfied 10 33.33

Satisfied to some extent 10 33.33

Not satisfied 10 33.33

Total 30 100 ,

Source: Author’s Calculations

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 219

The results of our study indicates that of the 40 beneficiaries, 17 (42.50 per cent) of

Swarna Jayanti Shahari Rozgar Yojana were satisfied, 17 (42.50 per cent) satisfied to some

extent and 06 (15.00 per cent) were not satisfied with this programme, with regard to training

programme, amount of loans, repayment of installments and income generation.

Out of 20 beneficiaries of National Rural Employment Guarantee Scheme, only 06

(30.00 per cent) beneficiaries reported that they were satisfied with availability of input. They

also reported that their condition has improved. But 06 (30.00 per cent) beneficiaries reported

that they were satisfied to some extent. Remaining 08 (40.00 per cent) beneficiaries reported

that they were not at all satisfied due to inadequacy of input. They further reported that they

were not getting 100 days’ employment under this scheme. They alleged that employment

was provided to kith and kin of the authorities. Moreover, they were not satisfied with the

wage rate also. They suggested improvement in infrastructure for the success of scheme. It is

noteworthy that not even a single beneficiary reported that he/she was selected by giving

bribe.

Out of 10 beneficiaries of Indira Awas Yojana, 05 (50 per cent) responded that they

were satisfied; 02 (20 per cent) were satisfied to some extent; and the remaining only 03

(30.00 per cent) beneficiaries reported that they were not satisfied with the amount available.

Most of them were however thankful to Government for implementing such schemes.

However, out of 30 beneficiaries of Atta Dal schemes the percentage of satisfied,

satisfied to some extent and not satisfied is equal (33.33 per cent). The beneficiaries of Atta

dal scheme have suggested that there should be distribution of Atta and dal of better quality.

Besides, some beneficiaries of Atta dal scheme reported that delivery of Atta dal was not at

proper time. But 100 per cent beneficiaries agreed that the program had significantly

improved their income. They also remarked that Atta dal scheme had fulfilled their

nutritional need.

Under Swarna Jayanti Shahari Rozgar Yojana, formation of SHGs should not be

slow. It can be concluded that though adequate level of employment could not be provided to

them under MNREGA scheme yet it provided employment to a few and improved their

standard of living. It can be suggested that such employment oriented schemes for physical

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 220

and mental work should be undertaken by the government, communities, clubs and NGOs on

a large scale. The fact is that it should cover more and more people.

We can clearly say that IAY, NREGA, SGSY and Atta Dal Scheme though have not

been working up to mark, yet the role of poverty alleviation programmes have been very

positive. Such programmes like micro financing, self-help groups and MNREGA not only

break vicious circle of poverty but also start the circle of prosperity and bring economic

transformation in rural area.

The problem of poverty can not be eradicated unless it is backed by fundamental

transformation. On the basis of the study, following measures are suggested to reduce

poverty. There should be transformation of education system so that there may be awareness

among people. There should be effective check on Panchayati Raj System also.

Transparency, accountability and honesty need to be applied in implementation of the

programmes. Besides, the implementation of programme should be time bound. At the same

time, there should be public awareness about various poverty alleviation programmes of the

Government. Authentic and reliable information about the poverty alleviation programmes

should be provided to the public.

POVERTY IN PUNJAB: A DISTRICT LEVEL STUDY

Evaluation of Poverty Alleviation Programmes 221

ENDNOTES

1 http://www.nagarnigamdehradun.com/acts/FINAL%5B1%5D-SJSRY-Web.pdf

2 http://www.nabard.org/microfinance/nabardsupport.asp

3 http://www.sbi.co.in/viewsection.jsp

4 http://www.sidbi.com/micro/aboutus.htm

5 http://megselfhelp.gov.in/workshop/02122006/Micro%20Finance%20 and % 20 Micro

6 http://hpkinnaur.nic.in/DRDA/drdaschemes.htm

7 http://nrega.nic.in/netnrega

8 http://nrega.nic.in/homestciti.asp

9 http://nrega.nic.in/homestciti.asp

10 http://nrega.nic.in/homestciti.asp

11 http://nrega.nic.in/WageRateRevision.pdf

12 http://www.business.standard.com

13 http://www.livemint.com2010/03/21205847

14 http://nrega.nic.in/NREGArpt_eng.pdf

15 http://bergarh.nic.in/prfl_drda_IAY.http