employee benefits for smes section 28, ifrs for sme vs. ias 19

TRANSCRIPT

Employee Benefits for SMEs

Section 28, IFRS for SME vs. IAS 19

Basically the same treatment for Short-term benefits Termination benefits

Similarities

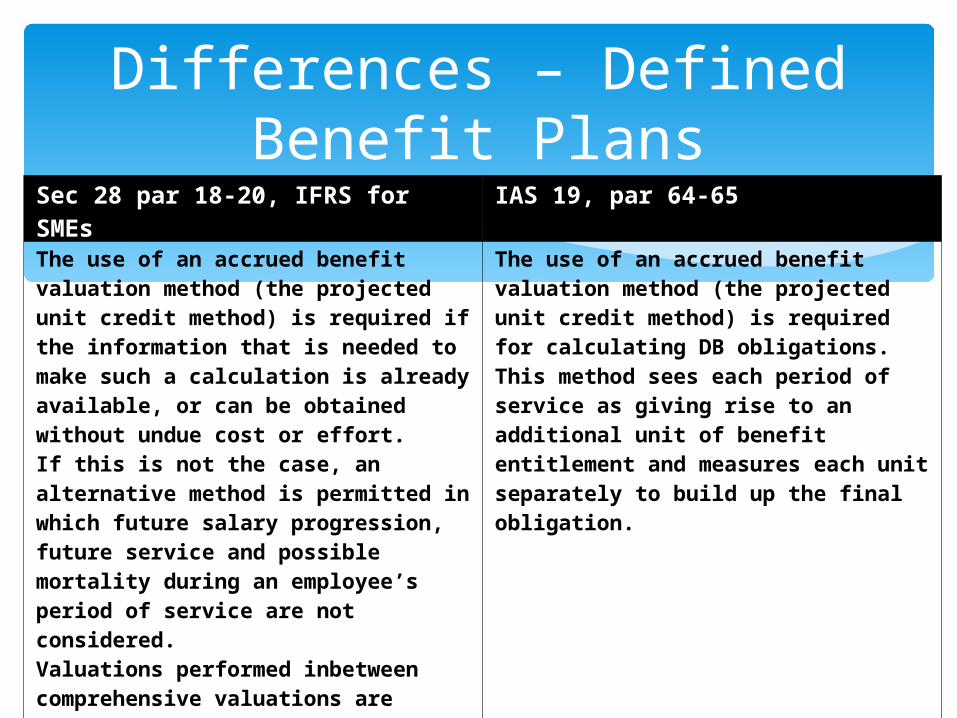

Differences – Defined Benefit Plans

Sec 28 par 14, IFRS for SMEs IAS 19, par 54, 61, 92-93B, 96"An entity recognises a liability for its obligation under DB plans net of plan assets; it recognises the net change in that liability during the period as the cost of its DB plans during the period."

Similar to IFRS for SMEs, except for the following:• Actuarial gains or losses can be recognised immediately either in profit or loss or in other comprehensive income) or deferred using the ‘corridor’ method (whereby gains and losses are amortised into profit or loss over the expected remaining lives of participating employees).• Past-service costs are recognized in profit or loss on a straight-line basis over the average period until the plan amendments vest.

Differences – Defined Benefit Plans

Sec 28 par 15, IFRS for SMEs IAS 19, par 54The DB liability is the net total of:• The present value of the DB obligation at the end of the reporting period;• Less the fair value at the reporting date of plan assets (if any) out of which the obligations are to be settled directly.

The DB liability is the net total of:• The present value of the DB obligation at the end of the reporting period;• Plus any actuarial gains (less any actuarial losses) not recognised due to the corridor method;• Minus any unrecognised past service costs;• Minus the fair value at the reporting date of plan assets (if any) out of which the obligations are to be settled directly.

Differences – Defined Benefit Plans

Sec 28 par 18-20, IFRS for SMEs IAS 19, par 64-65The use of an accrued benefit valuation method (the projected unit credit method) is required if the information that is needed to make such a calculation is already available, or can be obtained without undue cost or effort.If this is not the case, an alternative method is permitted in which future salary progression, future service and possible mortality during an employee’s period of service are not considered.Valuations performed inbetween comprehensive valuations are adjusted for the changes in number of employees and salaries if the principal actuarial assumptions have not changed significantly.

The use of an accrued benefit valuation method (the projected unit credit method) is required for calculating DB obligations. This method sees each period of service as giving rise to an additional unit of benefit entitlement and measures each unit separately to build up the final obligation.

Differences – Defined Benefit Plans

Sec 28 par 25(c), IFRS for SMEs IAS 19, par 105-106No distinction between expected and actual return on plan assets. All changes in the fair value of plan assets are recorded in profit or loss.

The expected return on plan assets is based on market expectations at the beginning of the period for returns over the entire life of the related obligation. It reflects changes in the fair value of plan assets as a result of actual contributions and benefits paid. The difference between actual and expected returns on plan assets is an actuarial gain or loss.

Differences – Defined Benefit Plans

Sec 28 par 25(c), IFRS for SMEs IAS 19, par 58If the present value of the defined benefit obligation at the reporting date is less than the fair value of plan assets at that date, the plan has a surplus. An entity shall recognise a plan surplus as a defined benefit plan asset only to the extent that it is able to recover the surplus either through reduced contributions in the future or through refunds from the plan.

Different wording for the asset ceiling test (the total of any cumulative unrecognised net actuarial losses and past service cost and the present value of any economic benefits available in the form of refunds from the plan or reductions in future contributions to the plan) due to different treatment of PSC and AGL, but since all recognized and unrecognized PSC & AGL are either in PVBO or FVPA in sec28, the upper limit for recognition of asset is basically the same.

Defined Contribution Plans discounting is not required if the contributions do not fall due wholly within 12 months after the end of the period

Other Long-term benefits PUCM is not required to be used for SMEs

Other Differences

The following information is given about a funded defined benefit plan. To keep interest computations simple, all transactions are assumed to be made at the year-end. The present value of the obligation and the fair value of the plan assets were both Php1,000 at 1 January 20X1.

In 20X2, the plan was amended to provide additional benefits with effect from 1 January 20X2. The present value as at 1 January 20X2 of additional benefits for employee service before 1 January 20X2 was Php50 for vested benefits and Php30 for non-vested benefits.

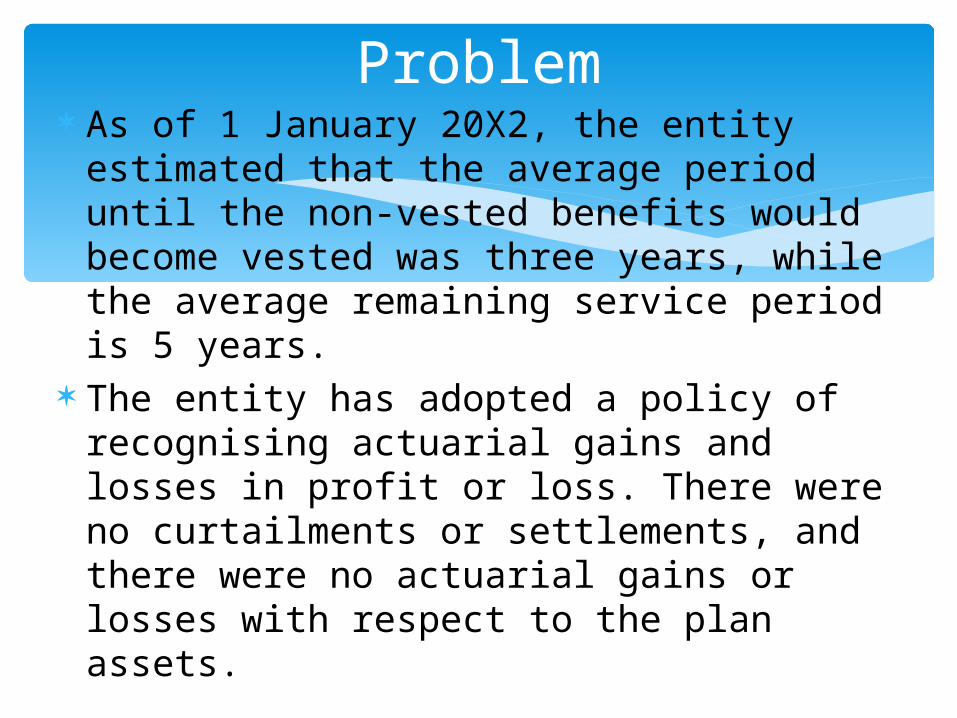

Problem

As of 1 January 20X2, the entity estimated that the average period until the non-vested benefits would become vested was three years, while the average remaining service period is 5 years.

The entity has adopted a policy of recognising actuarial gains and losses in profit or loss. There were no curtailments or settlements, and there were no actuarial gains or losses with respect to the plan assets.

Problem

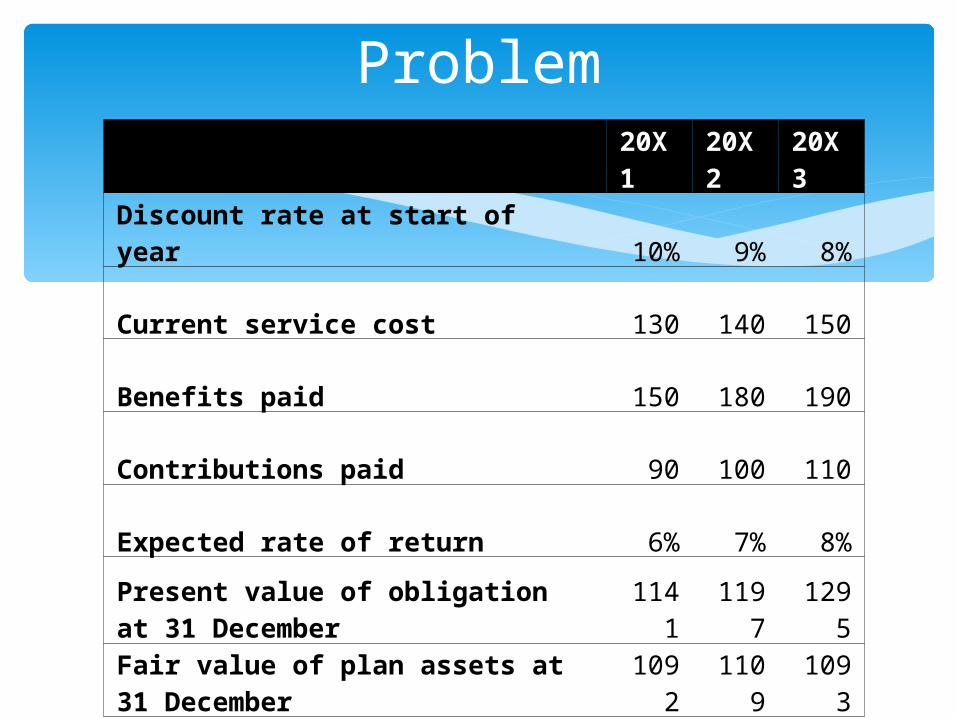

20X1

20X2

20X3

Discount rate at start of year 10% 9% 8%

Current service cost 130 140 150

Benefits paid 150 180 190

Contributions paid 90 100 110

Expected rate of return 6% 7% 8%

Present value of obligation at 31 December

1141

1197

1295

Fair value of plan assets at 31 December

1092

1109

1093

Problem

Solution – IAS 19

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

1/1/2001 - (1,000.00) 1,000.00 - CSC 130.00 (130.00) (130.00) Cont (90.00) 90.00 90.00 Ben Paid - 150.00 (150.00) Return (sq) (60.00) 60.00 152.00 (92.00) Int 100.00 (100.00) (100.00) Actuarial change - AGL (sq) - - (61.00) 61.00 Amort AGL /PSC - - - - Total (90.00) 170.00 (80.00) (1,141.00) 1,092.00 - (31.00)

Solution – IAS 19

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

1/1/2002 (80.00) (1,141.00) 1,092.00 (31.00) CSC 140.00 (140.00) (140.00) Cont (100.00) 100.00 100.00 Ben Paid - 180.00 (180.00) Return (76.44) 76.44 97.00 (20.56) Int 102.69 (102.69) (102.69) Actuarial change - (80.00) 80.00 AGL (sq) - - 76.69 (76.69) Amort AGL /PSC - - 10.00 (10.00) - Total (100.00) 166.25 (146.25) (1,197.00) 1,109.00 70.00 (128.25)

Solution – IAS 19

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

1/1/2003 (146.25) (1,197.00) 1,109.00 70.00 (128.25) CSC 150.00 (150.00) (150.00) Cont (110.00) 110.00 110.00 Ben Paid - 190.00 (190.00) Return (88.72) 88.72 64.00 24.72 Int 95.76 (95.76) (95.76) Actuarial change - - - AGL (sq) - - (50.53) 50.53 Amort AGL /PSC - - 8.29 (10.00) 1.71 Total (110.00) 157.04 (193.29) (1,295.00) 1,093.00 60.00 (51.29)

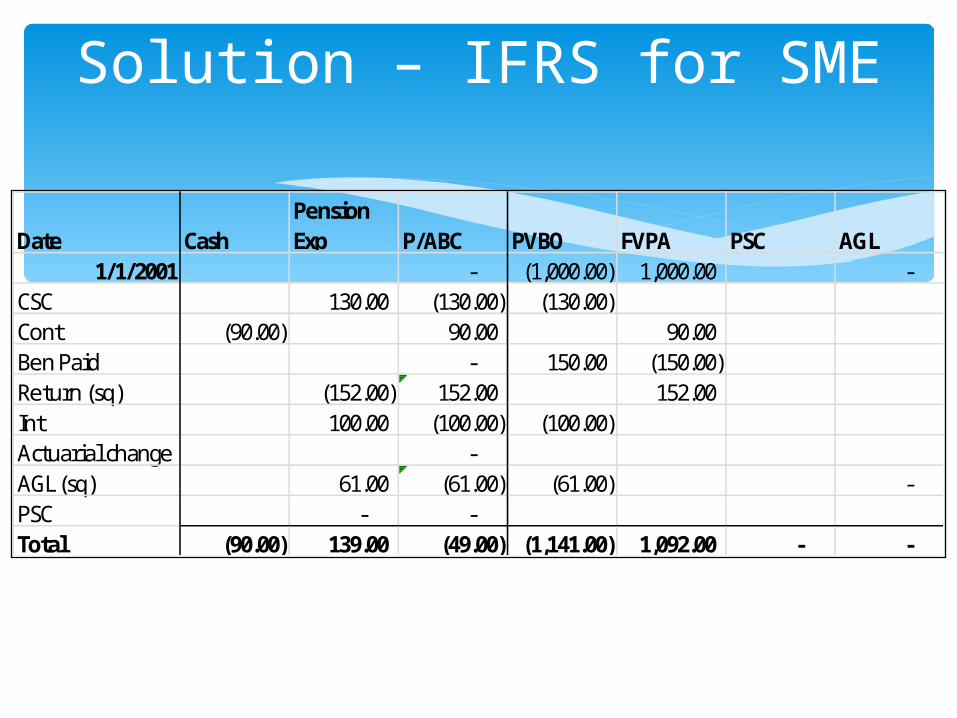

Solution – IFRS for SME

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

1/1/2001 - (1,000.00) 1,000.00 - CSC 130.00 (130.00) (130.00) Cont (90.00) 90.00 90.00 Ben Paid - 150.00 (150.00) Return (sq) (152.00) 152.00 152.00 Int 100.00 (100.00) (100.00) Actuarial change - AGL (sq) 61.00 (61.00) (61.00) - PSC - - Total (90.00) 139.00 (49.00) (1,141.00) 1,092.00 - -

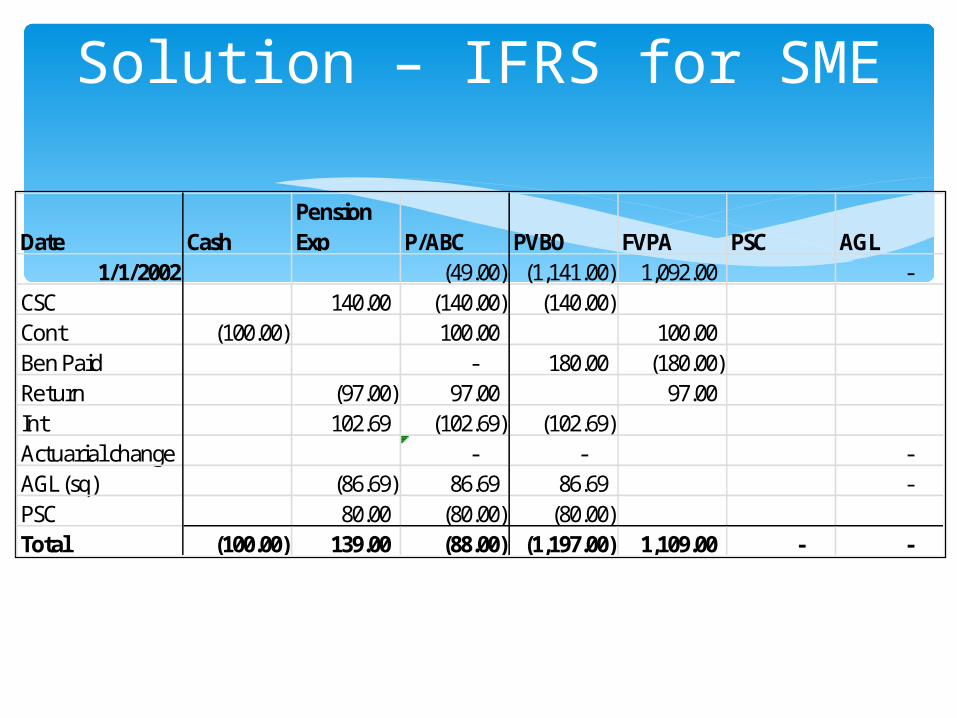

Solution – IFRS for SME

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

1/1/2002 (49.00) (1,141.00) 1,092.00 - CSC 140.00 (140.00) (140.00) Cont (100.00) 100.00 100.00 Ben Paid - 180.00 (180.00) Return (97.00) 97.00 97.00 Int 102.69 (102.69) (102.69) Actuarial change - - - AGL (sq) (86.69) 86.69 86.69 - PSC 80.00 (80.00) (80.00) Total (100.00) 139.00 (88.00) (1,197.00) 1,109.00 - -

Solution – IFRS for SME

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

1/1/2003 (88.00) (1,197.00) 1,109.00 - - CSC 150.00 (150.00) (150.00) Cont (110.00) 110.00 110.00 Ben Paid - 190.00 (190.00) Return (64.00) 64.00 64.00 Int 95.76 (95.76) (95.76) Actuarial change - - - AGL (sq) 42.24 (42.24) (42.24) - PSC - - Total (110.00) 224.00 (202.00) (1,295.00) 1,093.00 - -

Summary figures –Sec28 vs IAS 19

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

12/31/2001 (90.00) 139.00 (49.00) (1,141.00) 1,092.00 - - 12/31/2002 (100.00) 139.00 (88.00) (1,197.00) 1,109.00 - - 12/31/2003 (110.00) 224.00 (202.00) (1,295.00) 1,093.00 - -

Date CashPension Exp P/ABC PVBO FVPA PSC AGL

12/31/2001 (90.00) 170.00 (80.00) (1,141.00) 1,092.00 - (31.00) 12/31/2002 (100.00) 166.25 (146.25) (1,197.00) 1,109.00 70.00 (128.25) 12/31/2003 (110.00) 157.04 (193.29) (1,295.00) 1,093.00 60.00 (51.29)

IFRS for SMEs

IAS 19