emir 2013 presentation

TRANSCRIPT

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 1/69

Delivering aprofitable waterpure-play

Kemira Capital Markets Day 2013, September 10

Wolfgang Büchele, President and CEO

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 2/69

Structural changes starting to deliver results

Food and pharmaceuticals

business divestment

Sachtleben

divestment

Stringent

capital allocation

L

m

3F acquisitio

New organizationstructure

Fit for Growth

Segment roles:

growth and/or cash focus

Netdebt

Equity

value

Kemira Capital Markets Day 2013

Performance

management

system

Compensation

structure

Pa

Lean

operation

Q2 2012

Result

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 3/69

Managing businesses from their growth regions

Oil & Mining

management based

in Atlanta, US

Municipal & Industrial

management relocatingfrom Helsinki to Frankfurt

Paper m

relocatin

to Hong

EMEA Paper management

relocating from Helsinki to

Frankfurt

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 4/69

2012 Q4 2012 Q1 2013

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan 2012 Jun 2012 Dec 2012 Mar 2013 Jun 2013

Differentiated products together with balanced weshale portfolio driving revenue recovery in Oil & M15% reduction in total number of US oil (+17%) and gas

(-56%) rigs in 2013 compared to January 2012

Oil & Mining revenue increasing sequen

despite decreased oil and gas drilling ac

Differentiated products share of revenue

increasing to 82%

+6%

# of Oil rigs

in the US*

# of Gas rigsin the US*

*) Source: Baker Hughes International

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 5/69

Restructuring initiatives improving profitabilityin Municipal & Industrial

0

100

200

300

400

500

600

700

800

2010 2011 2012 1-6 2013

7.1%

5.7%

7.1%

9.2%

644665

687

343

Revenue,

EUR million

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 6/69

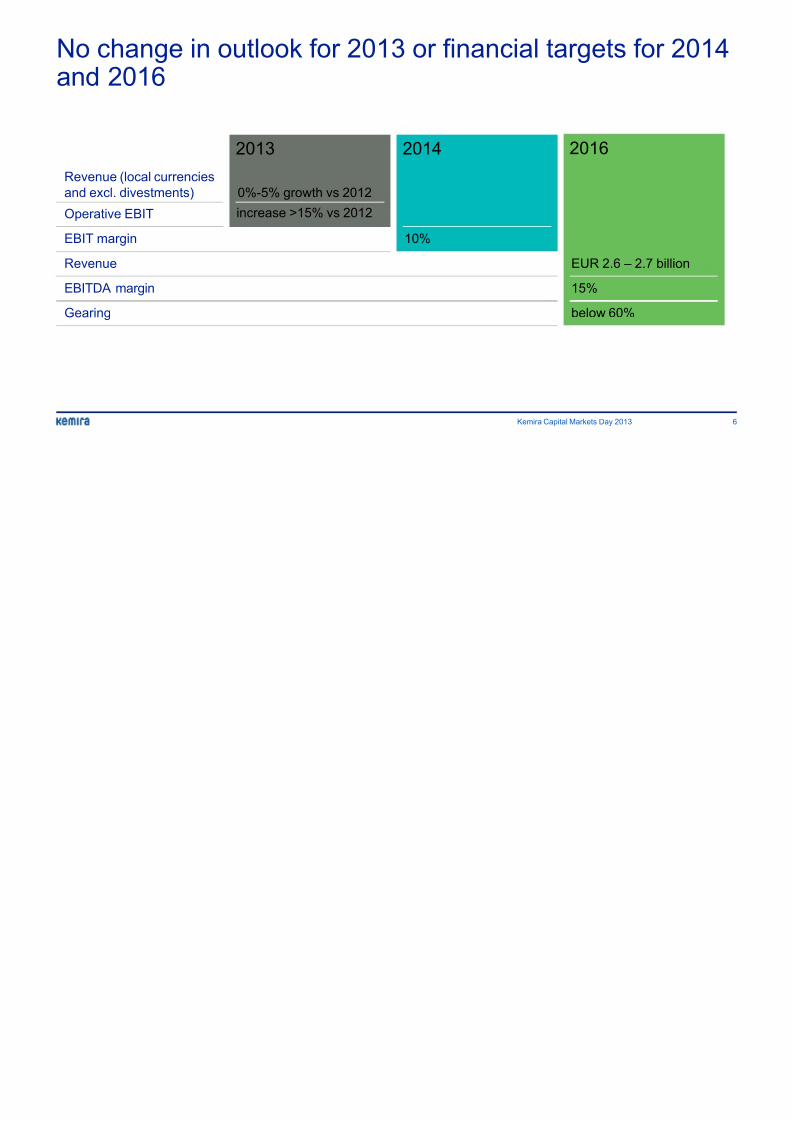

2013

Revenue (local currencies

and excl. divestments)

2014 2016

Operative EBIT

0%-5% growth vs 2012

EBIT margin 10%

Revenue

EBITDA margin

Gearing

EUR 2.6 –

15%

below 60%

increase >15% vs 2012

No change in outlook for 2013 or financial targets and 2016

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 7/69

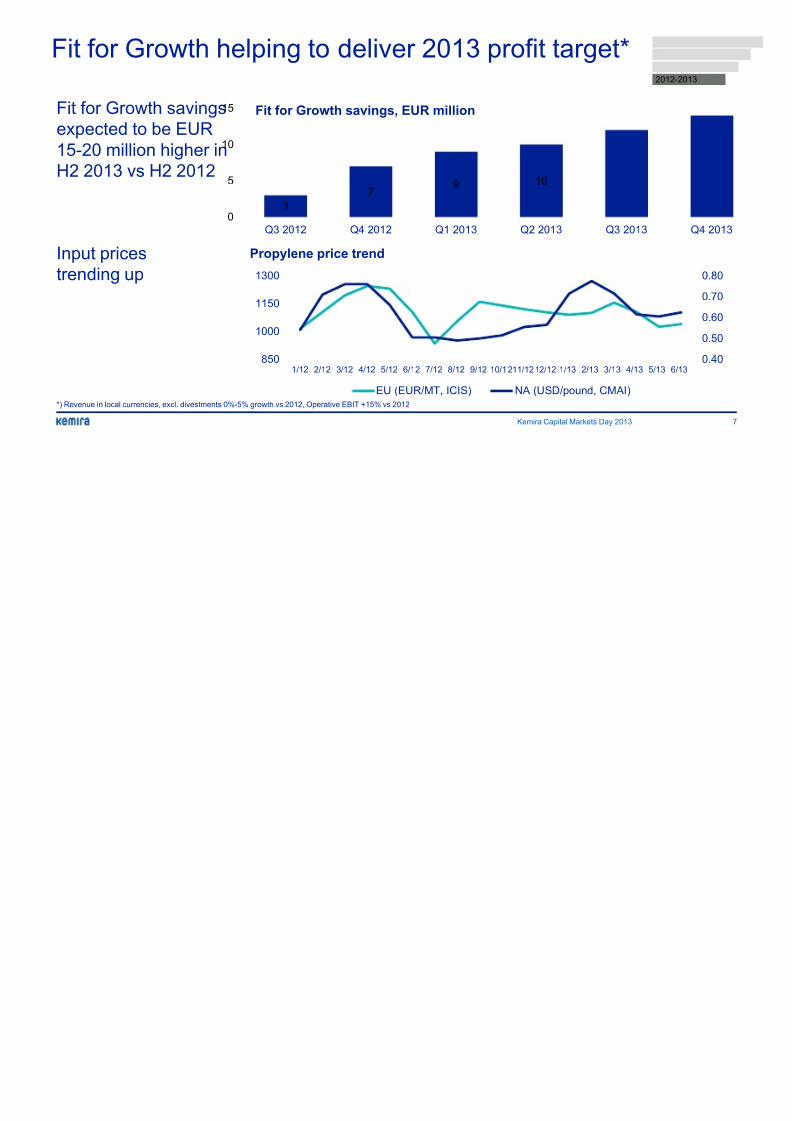

Fit for Growth helping to deliver 2013 profit target*

Fit for Growth savings

expected to be EUR

15-20 million higher in

H2 2013 vs H2 2012

Input prices

trending up

*) Revenue in local currencies, excl. divestments 0%-5% growth vs 2012, Operative EBIT +15% vs 2012

Propylene price trend

Kemira Capital Markets Day 2013

850

1000

1150

1300

1/12 2/12 3/12 4/12 5/12 6/12 7/12 8/12 9/12 10/1211/1212/12 1/13 2/13 3/13 4

EU (EUR/MT, ICIS) NA (USD/pound, CMAI)

3

79 10

0

5

10

15

Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2

Fit for Growth savings, EUR million

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 8/69

External indicators show stable economic develoEMEA and NAFTA, uncertainty in emerging markKemira early warning dashboard

Kemira Capital Markets Day 2013

1. Lead time is the estimated time (months) between movement of indicator vs. resultant 2. Average new order value (3 months rolling)

Indicators Status Trend Ch

Overall WTI crude oil futures (9/13)

OECD + Emerging market bus. confidence index (6/13)

FOEX China BHKP pulp (9/13)

Chicago fed nat. activity (7/13)

EMEA IFO manufacturing business expectations (8/13)

Eurozone PMI survey (8/13)

NA S&P 500 index (9/13)

ISM business supplier deliveries (8/13)

SA Brazil industry production % growth (6/13)

Brazil company leading indicator (6/13)

APAC Major 5 Asia companies leading indicator (6/13)

China containerized freight index (8/13)

Contracting: indicator has decreased for at least 3 consecutive months

Expanding: indicator has increased for at least 3 consecutive months

Normal: indicator moves within standard deviation corridor

Above: indicator moves above standard deviation corridor

Below: indicator moves below standard deviation corridor

Trend

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 9/69

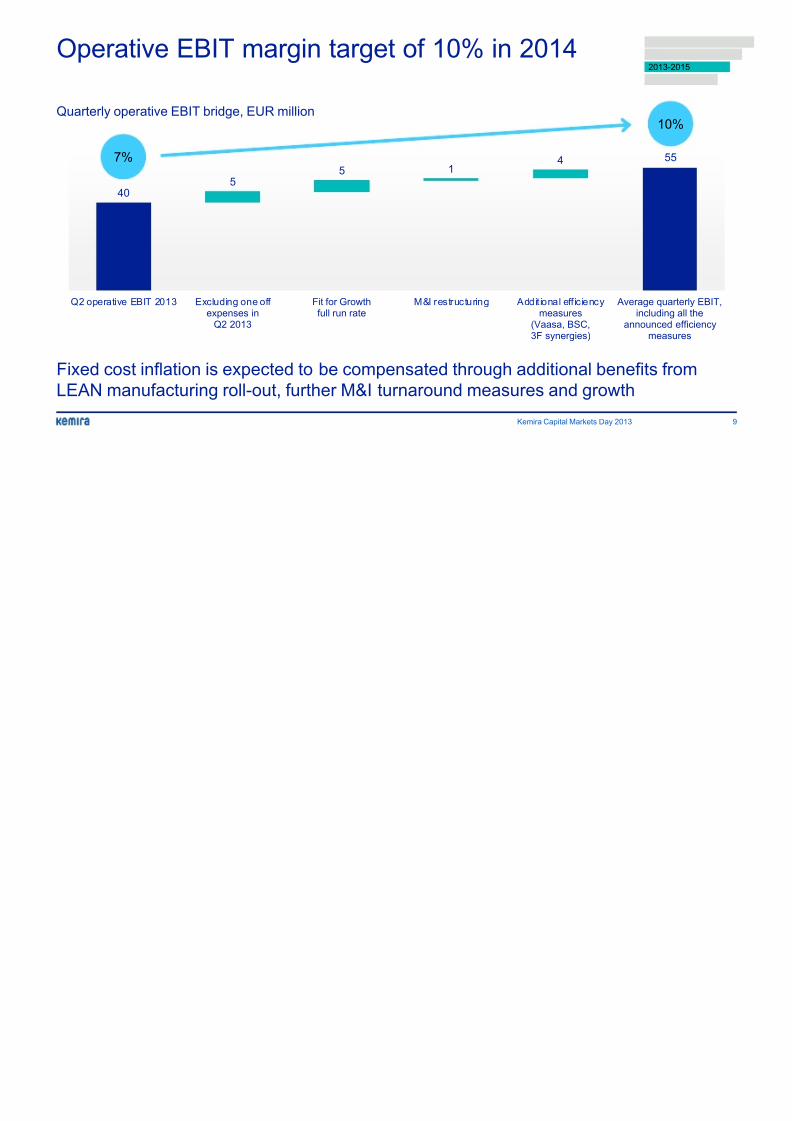

Operative EBIT margin target of 10% in 2014

Fixed cost inflation is expected to be compensated through additional bene

LEAN manufacturing roll-out, further M&I turnaround measures and growth

Q2 operative EBIT 2013 Excluding one off expenses in

Q2 2013

Fit for Growthfull run rate

M&I restructuring Addit ional eff iciencymeasures

(Vaasa, BSC,3F synergies)

Ave

a

40

415

5

Kemira Capital Markets Day 2013

Quarterly operative EBIT bridge, EUR million

7%

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 10/69

Capital allocation focusing on growth marketsand product lines

Targeted payback time for new greenfield investments is max. 7 years and

for capacity additions on existing productsFocus on Paper in China, strengthening Oil & Mining in mature markets,

South America, Middle East and Africa

65%35%

6.0%

2012

Capex split average

2010-2012

Targeted capex split

2016

Capex-to-sales ra

30% 70%

Kemira Capital Markets Day 2013

Differentiated products

Commodity products

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 11/69

• Current 36% gearing means EUR 280 million

headroom against the targeted <60% gearing• Strict M&A criteria for focused growth

– Must strengthen our market position and/or our

technologies/competencies

– EBIT accretive in second full year after closing

• 3F acquisition demonstrates Kemira’s M&A strategy

– Accessing technologies lacking in the portfolio (e.g. monomers) – Accelerating geographical expansion in order to shorten

the strategic path (e.g. dry polyacrylamides in the US)

Acquisitions expected to contribute to growth targe

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 12/69

Positioning based on 2 years performance

Portfolio focus shifting from commodity to differentiated business

Kemira Capital Markets Day 2013

Revenue growth

Profitability

O&M SAO&M

APAC

M&I SA

M&I

APAC

M&I

NAFTA

O&M

EMEA

Paper

SA

O&M

NAFTA

Paper

NAFTA

Paper

EMEA Paper

APACCSEvaluating exit

options

M&I

EMEA

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 13/69

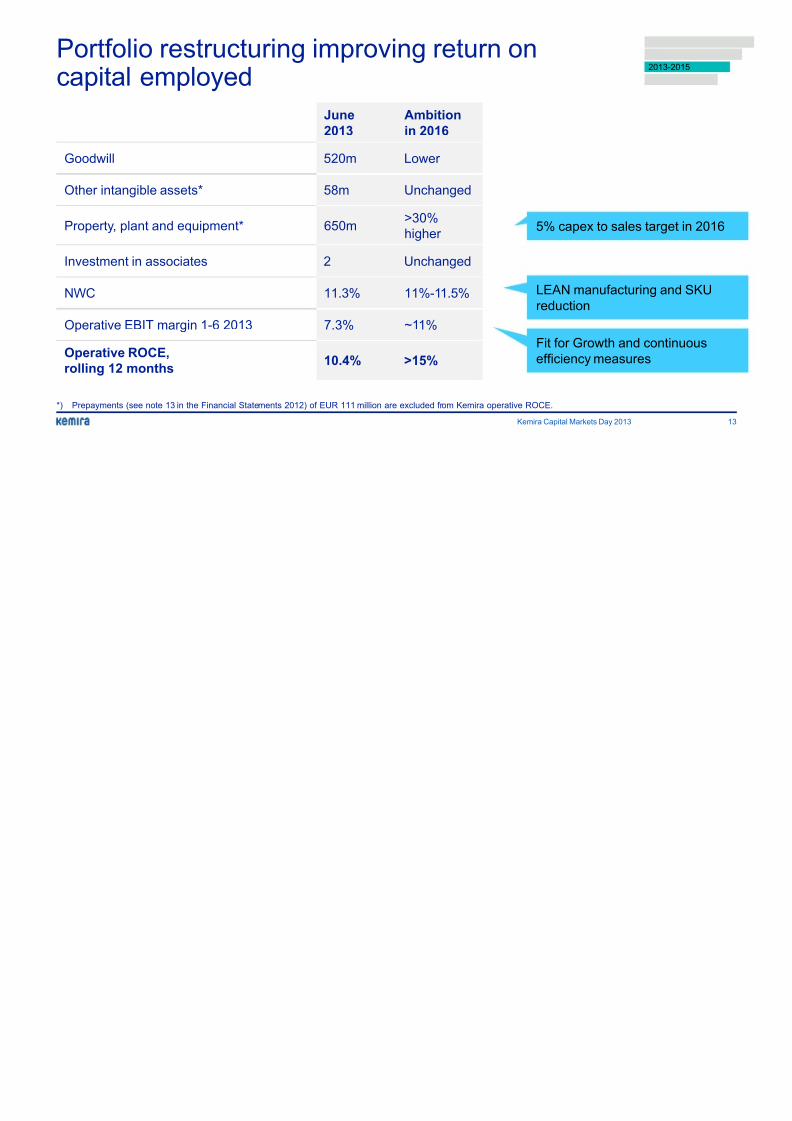

Portfolio restructuring improving return oncapital employed

June

2013

Ambition

in 2016

Goodwill 520m Lower

Other intangible assets* 58m Unchanged

Property, plant and equipment* 650m>30%

higher

Investment in associates 2 Unchanged

NWC 11.3% 11%-11.5%

Operative EBIT margin 1-6 2013 7.3% ~11%

Operative ROCE,

rolling 12 months10.4% >15%

5% capex to sale

LEAN manufactu

reduction

Fit for Growth an

efficiency measu

*) Prepayments (see note 13 in the Financial Statements 2012) of EUR 111 million are excluded from Kemira operative ROCE.

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 14/69

Innovation focusing on Paper and Oil & Mining

Technology Management

Board targeting 50%reduction in development

times for ”R” and ”D”

projects

Dedicated global team

and structured process

to drive ideation

R&D projects per New

Product Development stageDevelopment Scale-up

Kemira Capital Markets Day 2013

Paper

Oil &

Mining

Municipal

& Industrial

ChemSolutions

Oil &

Mining

Municipal

& Industrial

ChemSolutions

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 15/69

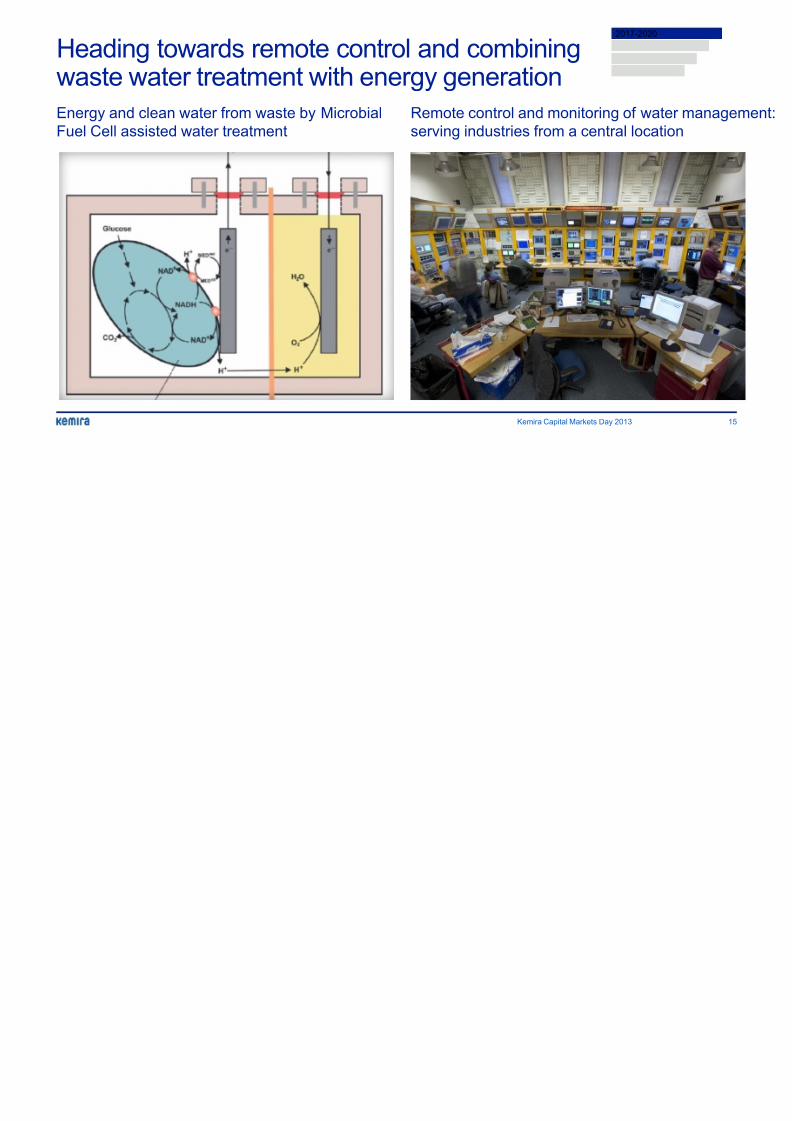

Heading towards remote control and combiningwaste water treatment with energy generation

Remote control and monitoring o

serving industries from a central

Kemira Capital Markets Day 2013

Energy and clean water from waste by Microbial

Fuel Cell assisted water treatment

201

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 16/69

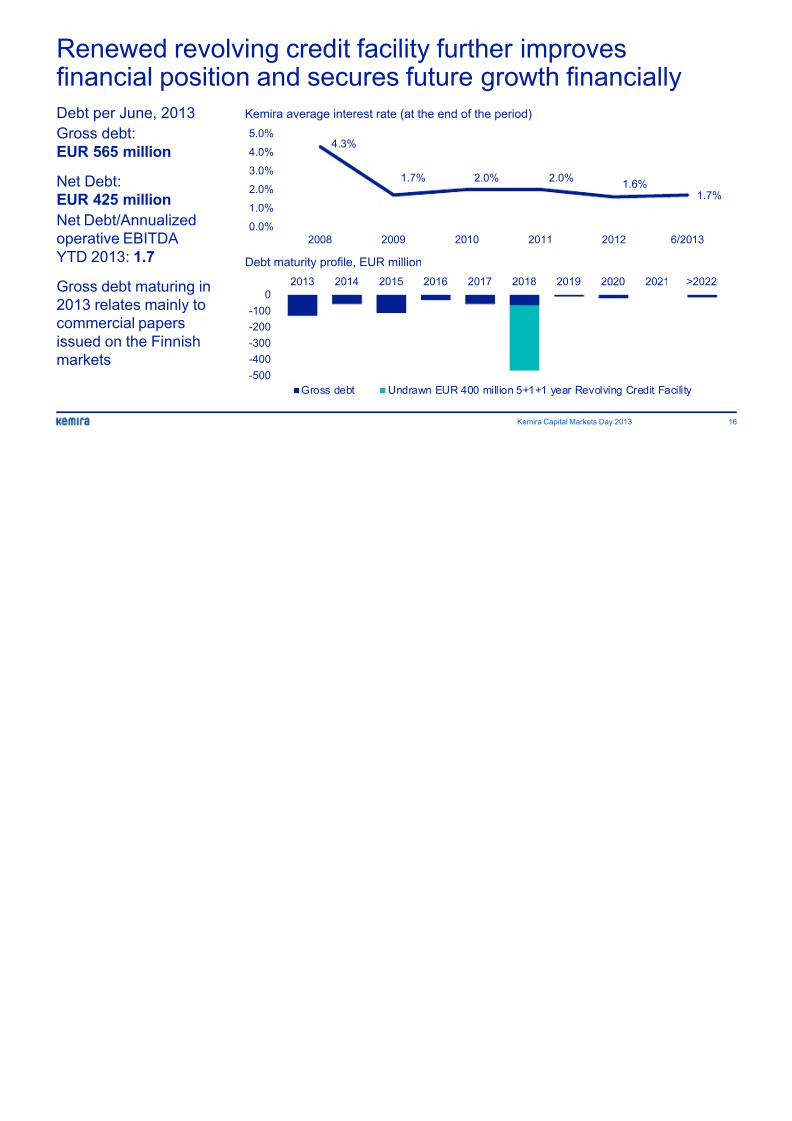

Renewed revolving credit facility further improvesfinancial position and secures future growth financ

Debt per June, 2013

Gross debt:

EUR 565 million

Net Debt:

EUR 425 million

Net Debt/Annualized

operative EBITDA

YTD 2013: 1.7

Gross debt maturing in

2013 relates mainly to

commercial papers

issued on the Finnish

markets

4.3%

1.7% 2.0% 2.0%1

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2008 2009 2010 2011 2012

-500

-400

-300

-200

-100

02013 2014 2015 2016 2017 2018 2019 2020

Gross debt Undrawn EUR 400 million 5+1+1 year Revolving C

Debt maturity profile, EUR million

Kemira average interest rate (at the end of the period)

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 17/69

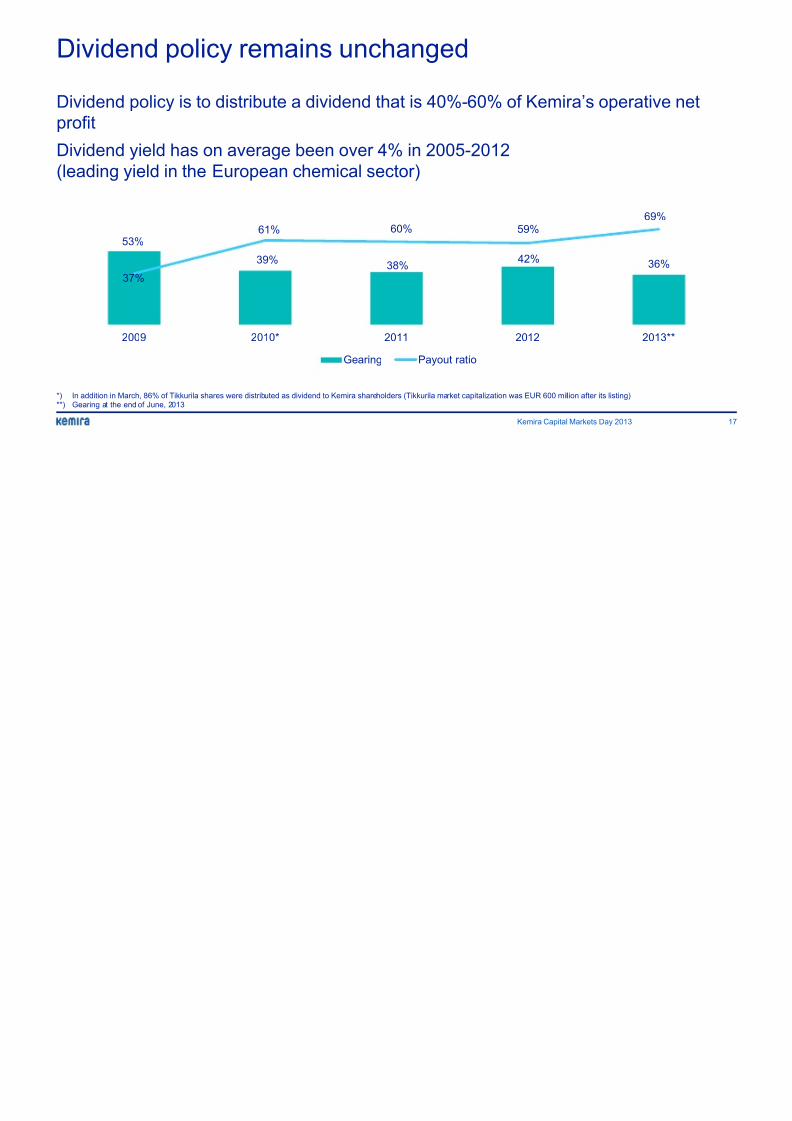

Dividend policy remains unchanged

Dividend policy is to distribute a dividend that is 40%-60% of Kemira’s oper

profit

Dividend yield has on average been over 4% in 2005-2012

(leading yield in the European chemical sector)

Kemira Capital Markets Day 2013

*) In addition in March, 86% of Tikkurila shares were distributed as dividend to Kemira shareholders (Tikkurila market capitalization was EUR 600 million after its listing)**) Gearing at the end of June, 2013

53%

39%38%

42%

37%

61% 60% 59%

2009 2010* 2011 2012

Gearing Payout ratio

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 18/69

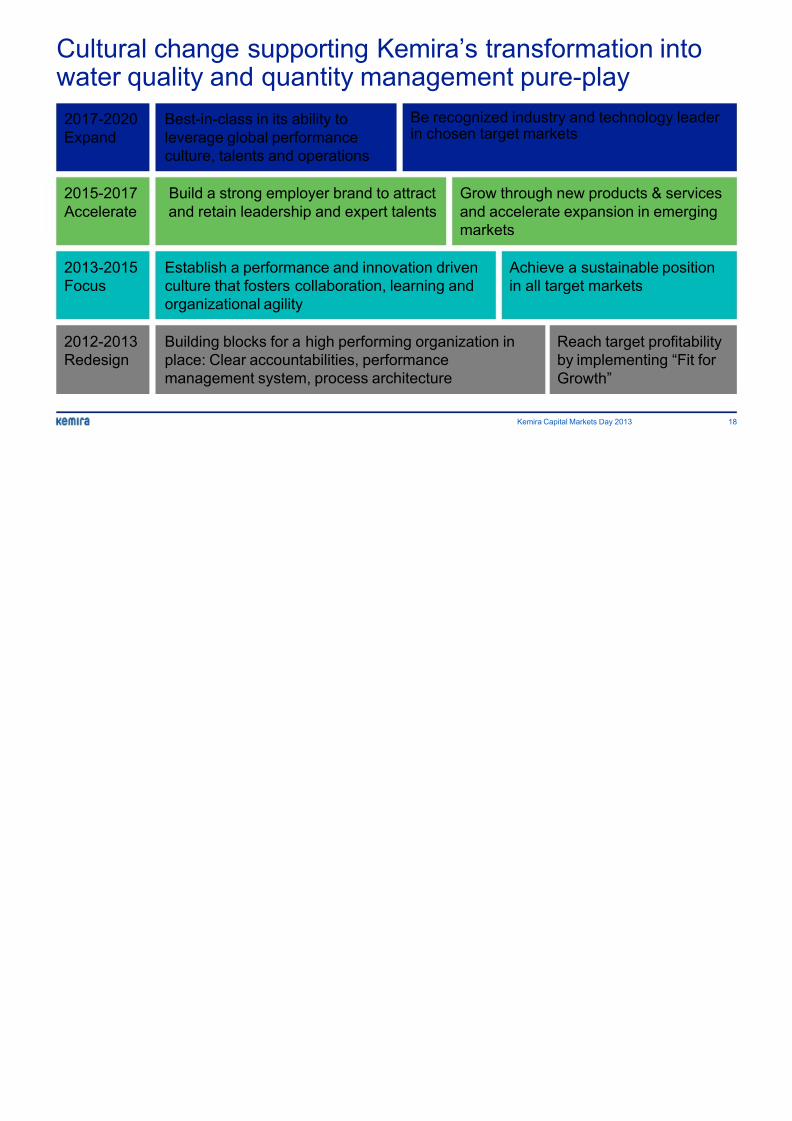

Cultural change supporting Kemira’s transformatiowater quality and quantity management pure-play

2013-2015

Focus

2017-2020

Expand

Be recognized industry and technin chosen target markets

2015-2017

Accelerate

Grow through new produc

and accelerate expansion

markets

Achieve a sustain

in all target marke

2012-2013

Redesign

Reach targ

by impleme

Growth”

Best-in-class in its ability to

leverage global performanceculture, talents and operations

Build a strong employer brand to attract

and retain leadership and expert talents

Establish a performance and innovation driven

culture that fosters collaboration, learning andorganizational agility

Building blocks for a high performing organization in

place: Clear accountabilities, performance

management system, process architecture

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 19/69

Increased focuson efficiency andsavings

Kemira Capital Markets Day 2013, September 10

Michael Löffelmann, SVP restructuring

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 20/69

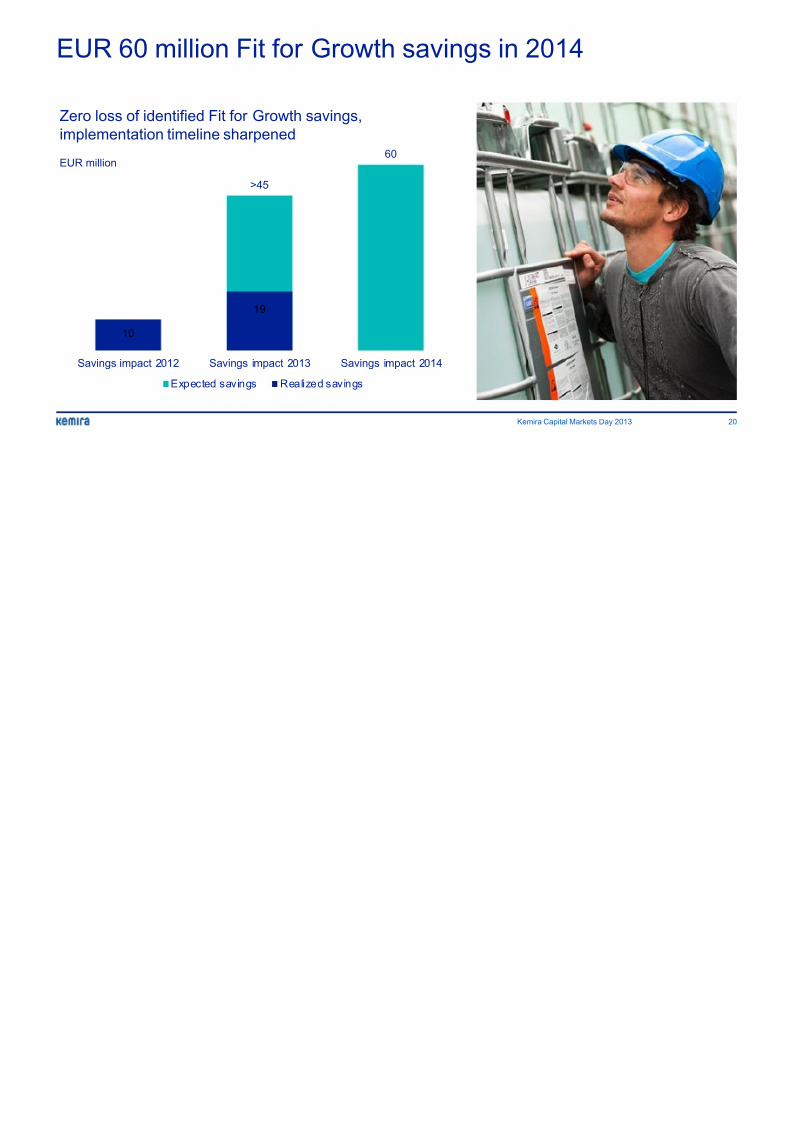

EUR 60 million Fit for Growth savings in 2014

>45

60

10

19

Savings impact 2012 Savings impact 2013 Savings impact 2014

Expected savings Realized savings

Zero loss of identified Fit for Growth savings,

implementation timeline sharpened

EUR million

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 21/69

Offsetting

Kemira’s fixedcost inflation

through ongoing

cost savings driven

by continuous

improvement

process

Implementing LEAN to continue focus on cost efficWhy is LEAN important for Kemira?

Reduce complexity

Reduce costs

Increase competitiveness

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 22/69

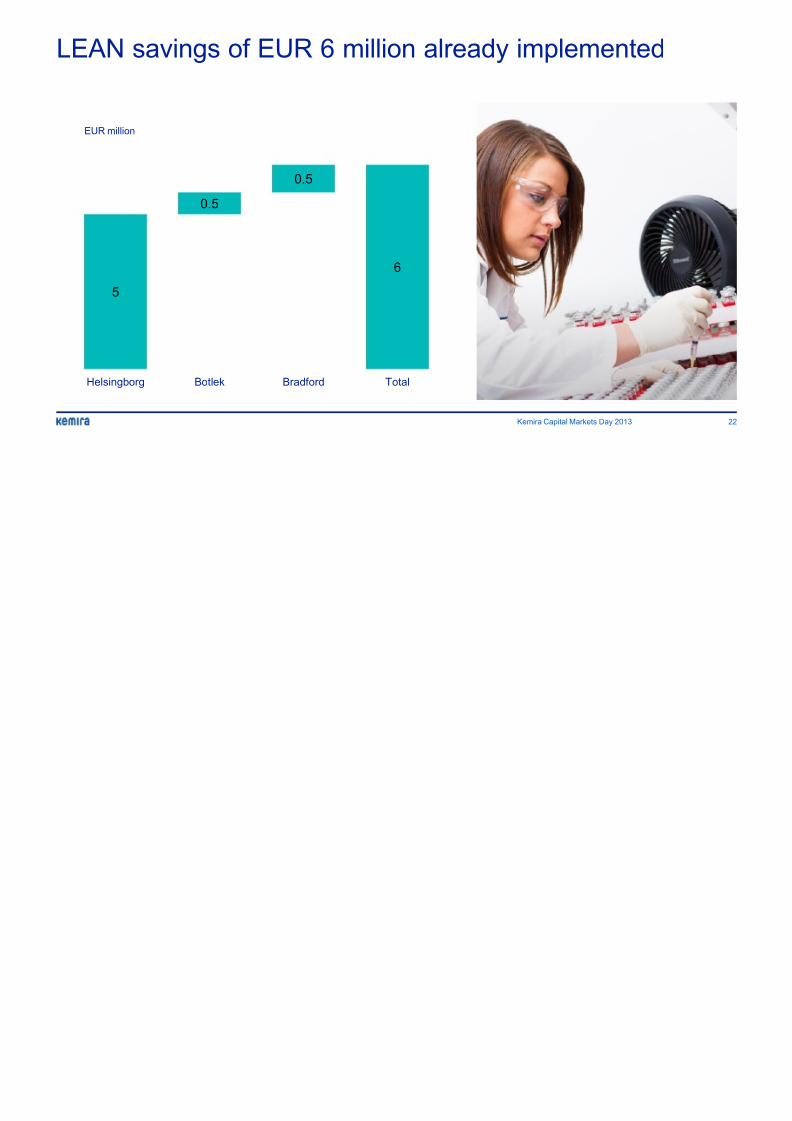

LEAN savings of EUR 6 million already implemen

Kemira Capital Markets Day 2013

5

0.5

0.5

6

Helsingborg Botlek Bradford Total

EUR million

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 23/69

4.

Self-loadin

3.

LEAN lab &

in-process

analysis

Global roll-out of standardized LEAN savings mod

Kemira Capital Markets Day 2013

2.

Material handling

benchmark

1.

Weighing

& filling

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 24/69

Strong focus on implementation discipline

Kemira Capital Markets Day 2013

Enhanced implementation• Higher and constant drive to achieve results

• Continuous identification of savings

• Greater sense of urgency

Resources

• Closer interaction and follow-up

• Full time LEAN resources

• Dedicated manufacturing

optimization resources

Tools

• Action based with financial tracking

• Standardized LEAN tools

• Additional training for sites

Delivering high performance driven culture

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 25/69

Acceleratingthe turnaround

in Municipal &Industrial

Kemira Capital Markets Day 2013, September 10

Frank Wegener, President, Municipal & Industrial

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 26/69

Fit for Growth has started to improve profitability

RevenueEUR million

Operative EBIT %

Municipal & Industrial targets cross-the-cycle operative EBIT margin of 10% in 2014

1) Targeted Fit for Growth savings above EUR 20 million

2) New organization and customer segmentation leading to more than EUR 5 millionadditional savings

3) Further benefits from manufacturing network optimization, SKU reduction and R&D

improvements

161

165

174

178

150

155

160

165

170175

180

Q1 2012 Q1 2013 Q2 2012 Q2 2013

3.5%

5.2%

6.9%

0%

2%

4%

6%

8%

10%

Q1 2012 Q1 2013 Q2 201

+2%

+2%

+49%

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 27/69

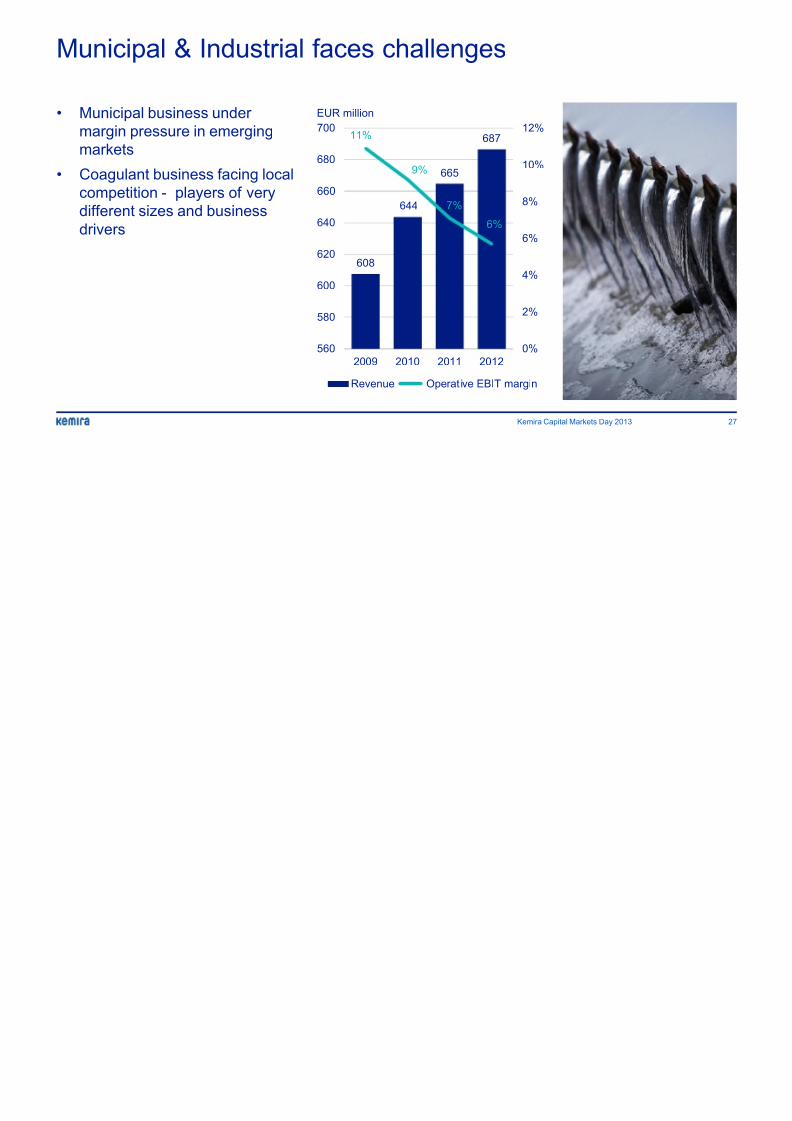

Municipal & Industrial faces challenges

• Municipal business under

margin pressure in emerging

markets

• Coagulant business facing local

competition - players of very

different sizes and business

drivers

608

644

665

68711%

9%

7%

6%

0%

2%

4%

6%

8%

10%

12%

560

580

600

620

640

660

680

700

2009 2010 2011 2012

Revenue Operative EBIT margin

EUR million

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 28/69

Historic business model New business model

New business model and organization to address challenging business environment

Kemira Capital Markets Day 2013

• Sales model with simplified organiz

and channel strategy

• Headcount reduction of ~50 emplo

• R&D focus in line with strategy, po

by 40%

• Uniform service approach with limited

customer segmentation

• Sales force weighted more towards

direct sales vs. distribution sales

• Global geographical focus with scattered

manufacturing footprint

• Limited focus on production technology

• World class coagulant footprint foc

mature markets

• Over 1,000 SKU’s • Number of SKU’s reduced by 50%

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 29/69

Segmented customer business model increasingprofitability

Historic model –

unsegmented

New model with two custo

segments

Kemira Capital Markets Day 2013

Kemira offering:• Reliable delivery and effective treatment

• Tailor made solutions

• Fast time to resolution

• Technical support

Paying for:

Reliable delivery and effective treatment

Value and

performance

Price>9,000 municipal and industrial

customers buying coagulants and polymers >9000

customers

>4500

customers

>4500

customers

Paying fo

Effective t

Paying foFaster res

Some tech

and

Tailored s

immediate

tech suppo

offering

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 30/69

Securing competitive position through manufacturnetwork consolidation

Fit for Growth measures will be fully implemented by the end of Q2 2014• 6 sites closed, closure of 2 sites and 2 production plants under implementation

• 2 sites to be closed only after new Tarragona coagulant site is on stream (delayed to Q1 2014)Further manufacturing optimization through economies of scale and the use of industr

Additional rationalization expected in NAFTA

*) Europoort and Krems (production plants), Lauterburg, Sevilla, Flix, Tarragona old, St. Petersburg, Houston, Savannah, Xoxla, Camacari, Romania

Coagula

New pro

Sites an

closed o

closed

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 31/69

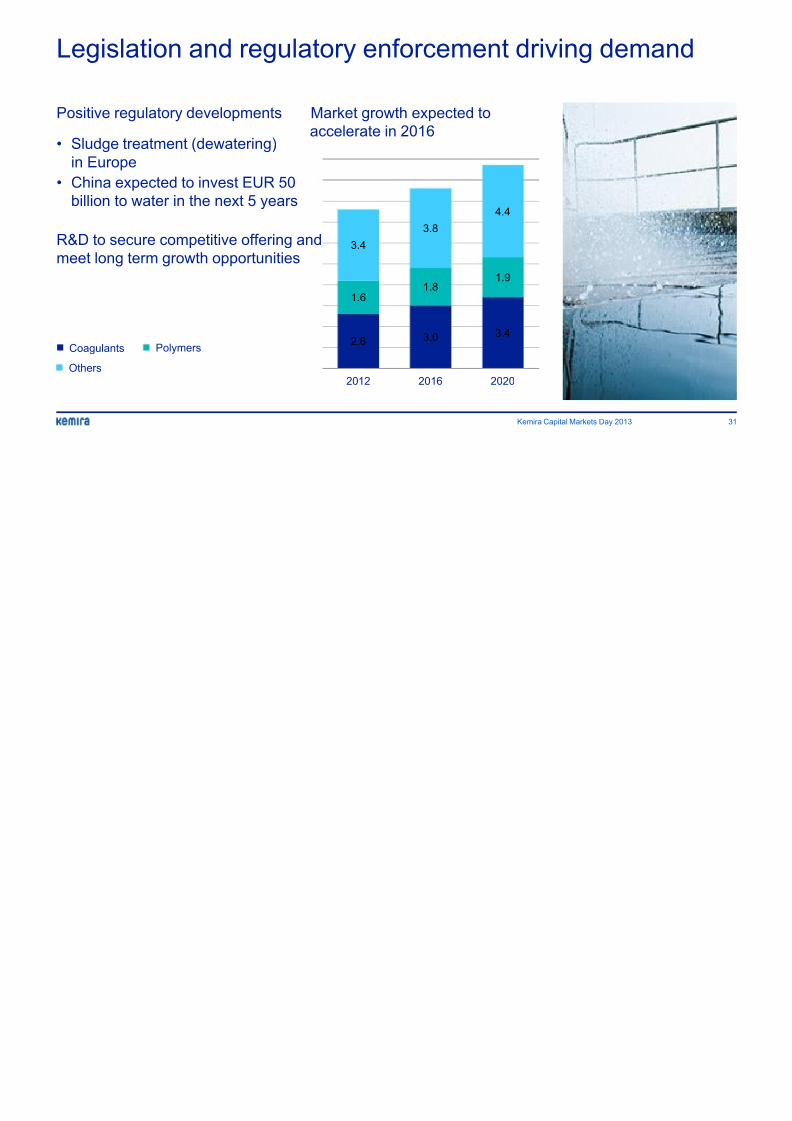

Legislation and regulatory enforcement driving de

• Sludge treatment (dewatering)in Europe

• China expected to invest EUR 50

billion to water in the next 5 years

R&D to secure competitive offering and

meet long term growth opportunities

Positive regulatory developments Market growth expected to

accelerate in 2016

2.6 3.0 3.4

1.61.8

1.9

3.4

3.8

4.4

2012 2016 2020

Coagulants

Others

Polymers

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 32/69

Accelerating the turnaround in Municipal & Industr

Streamlined businessmodel focused on

maximizing cash flow

generation

Focus on mature

markets, captureselected growth

opportunities in APAC

Structural profitimprovement th

reduction of com

customer segm

organizational o

Selective applic

production procdevelopment as

new products p

way to a sustain

43

21BUSINESS

INNOVATIONGEOGRAPHY

EFFICIENCY

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 33/69

Innovating for growth

Kemira Capital Markets Day 2013, September 10

Dr. Heidi Fagerholm, CTO

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 34/69

Research Center network focusing on competencedevelopment and regional business support

Shanghai,

China

• Paperapplication

• Tissue• TCS

Espoo, Finl• Fundamenta

• Paper resea

• M&I• TCS

Sao Paolo, Brazil• Minerals & Metals

• TCS

Atlanta, GA, USA• Oil & Gas

• Minerals & Metals• Paper

• TCS

TCS = Technical Customer Service & Production Support

Kemira Capital Markets Day 2013

Total personnel 250

Patent families ~350

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 35/69

• Increase in total portfolio value by

50% from 2013 to 2020

• Increase in cross-regional

participation across R&D projects

• Every second project has an external research

partner

• FTE per project growing more than 50% due to

increased focus

R&D portfolio aligned with strategy

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 36/69

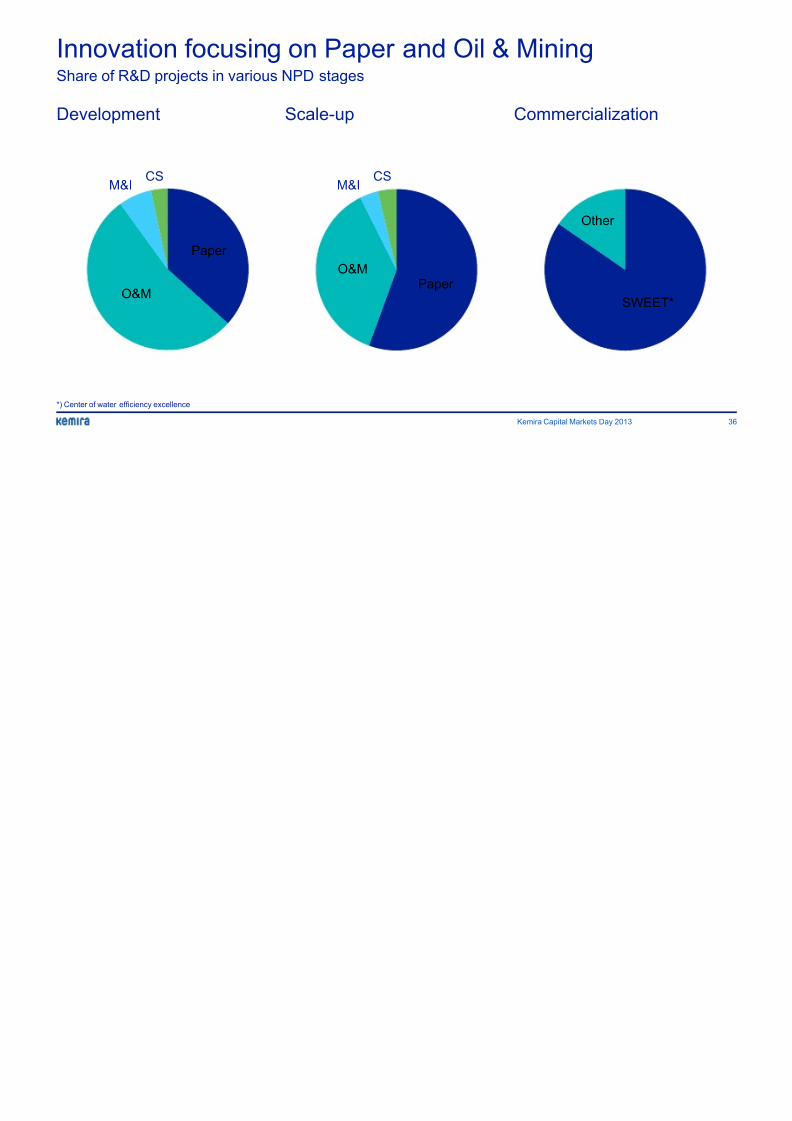

Innovation focusing on Paper and Oil & Mining

Development Scale-up

Share of R&D projects in various NPD stages

Commercializa

Paper

O&M

M&ICS

M&ICS

Paper

O&M

S

Other

*) Center of water efficiency excellence

Kemira Capital Markets Day 2013

I i l EUR 250 illi i 2016

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 37/69

40

106

140

0

20

40

60

80

100

120

140

160

2011 2012 2013**

Innovation sales target EUR 250 million in 2016

Kemira innovation sales*, EUR million

*) Sales from new products or existing products for new applications launched within the previous 5 years

**) Annualized Jan-Jun 2013 innovation sales

Fennobond

strength

Fennobind

bindersKemflite,

control & monitoring

KemFlow

friction

reducer

KemFlow

biocide

Kemira Capital Markets Day 2013

O&M

Paper

M&I

Tagged antiscalant

Guar replacement

Green friction

reducer

Rheology modifiers

Performic acid

Next Fennobind

generation

New innovation are

Targeting to double innovation driven sales from 5% in 2012 to ~10% of total sales in 2

P l t f 50%

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 38/69

Polymers account for 50%of Kemira’s differentiatedproduct revenue

• Case study: Polymers in flocculation

and sludge dewatering

• Technical benefits for customer include

improved reject water quality and

increased solid content of sludge

• Global polymer market growing from

EUR 7 billion to EUR 10 billion in 2020

• Kemira targeting faster than market

growth

Kemira Capital Markets Day 2013

Case Fennobind For better printability in Paper &

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 39/69

Benefits for customer:

• Significant cost savings via decreased binder

demand on coating application

• Increased sustainability through reduced

dependency on oil-based chemistry

Kemira:

• Creating innovative high performance binder

concept based on future chemistry and

application requirementsThe global binder market for paper

and board is EUR 2.5 billion

Case Fennobind – For better printability in Paper &Innovative binder concept

Kemira Capital Markets Day 2013

Fennobind

Particle diameter 46

Sh l G & Oil

8/13/2019 Emir 2013 Presentation

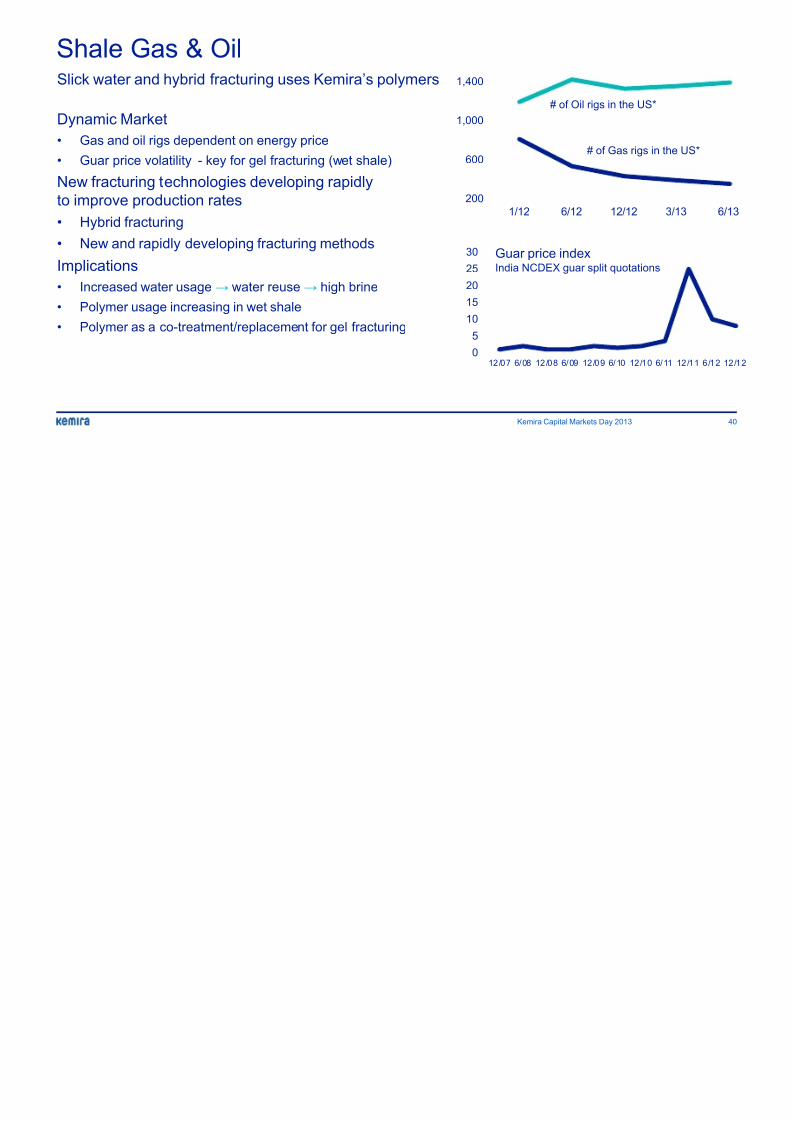

http://slidepdf.com/reader/full/emir-2013-presentation 40/69

Shale Gas & OilSlick water and hybrid fracturing uses Kemira’s polymers

Kemira Capital Markets Day 2013

Dynamic Market

• Gas and oil rigs dependent on energy price

• Guar price volatility - key for gel fracturing (wet shale)

New fracturing technologies developing rapidly

to improve production rates

• Hybrid fracturing

• New and rapidly developing fracturing methods

Implications

• Increased water usage → water reuse → high brine• Polymer usage increasing in wet shale

• Polymer as a co-treatment/replacement for gel fracturing

200

600

1,000

1,400

1/12 6/12 12/1

# of Oil rigs in the

# of Gas

0

5

10

1520

25

30

12/07 6/08 12/08 6/09 12/09 6/10

Guar price indexIndia NCDEX guar split quot

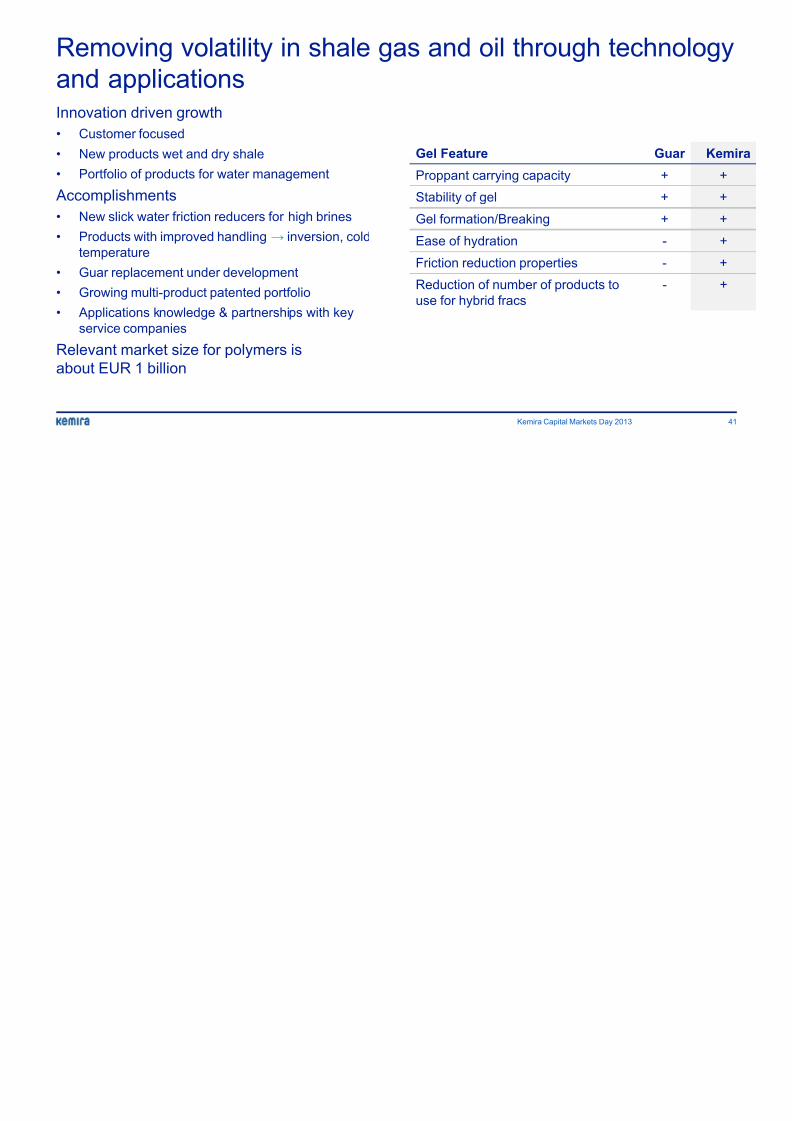

Removing volatility in shale gas and oil through te

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 41/69

Removing volatility in shale gas and oil through te

and applications

Kemira Capital Markets Day 2013

Innovation driven growth

• Customer focused

• New products wet and dry shale

• Portfolio of products for water management

Accomplishments

• New slick water friction reducers for high brines

• Products with improved handling → inversion, cold

temperature

• Guar replacement under development

• Growing multi-product patented portfolio

• Applications knowledge & partnerships with key

service companies

Relevant market size for polymers is

about EUR 1 billion

Gel Feature

Proppant carrying capacity

Stability of gel

Gel formation/Breaking

Ease of hydration

Friction reduction properties

Reduction of number of products touse for hybrid fracs

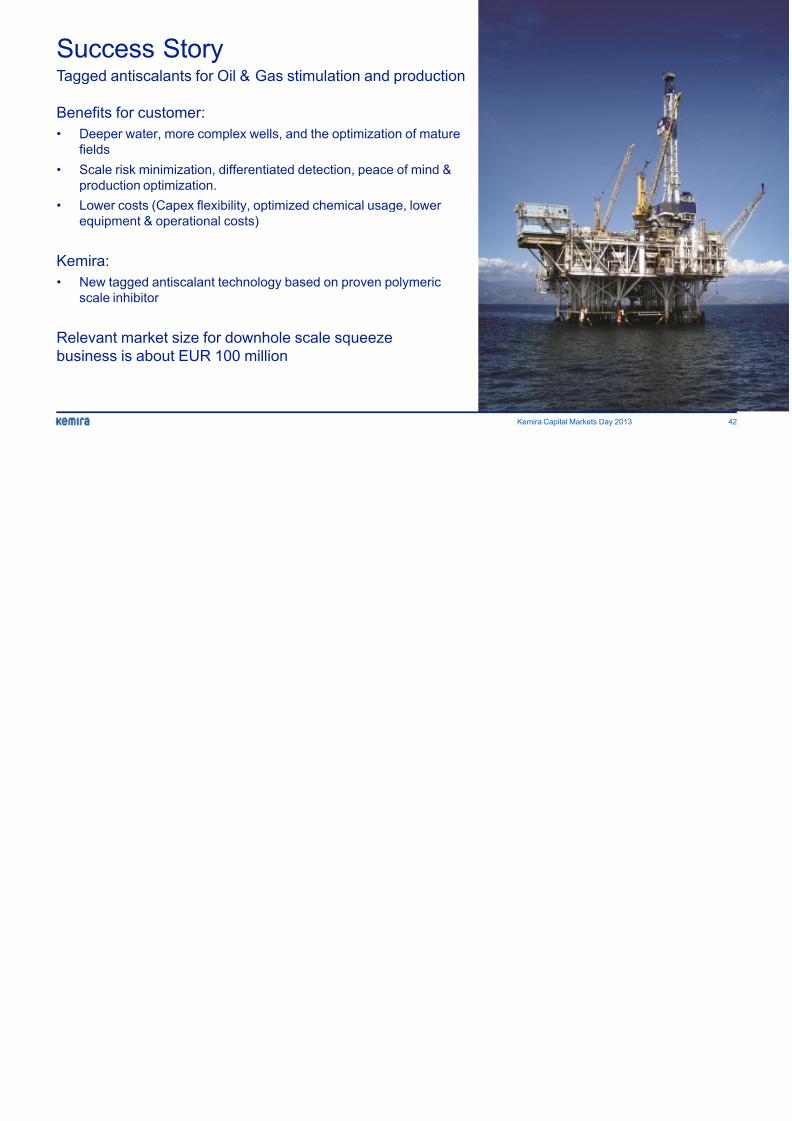

Success Story

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 42/69

Benefits for customer:

• Deeper water, more complex wells, and the optimization of mature

fields• Scale risk minimization, differentiated detection, peace of mind &

production optimization.

• Lower costs (Capex flexibility, optimized chemical usage, lower

equipment & operational costs)

Kemira:

• New tagged antiscalant technology based on proven polymeric

scale inhibitor

Relevant market size for downhole scale squeeze

business is about EUR 100 million

Success StoryTagged antiscalants for Oil & Gas stimulation and production

Kemira Capital Markets Day 2013

Building a culture of

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 43/69

Building a culture ofinnovation throughout theorganization

Innovation Community to inspire people,

to stimulate creativity and to create

enablers for an innovation culture

Training to enhance innovation

capabilities

Create measurable success criteriafor innovation work

”Innovate today for

a prosperous tomorrow”

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 44/69

Appendix

Kemira Capital Markets Day 2013, September 10

Kemira Capital Markets Day 2013

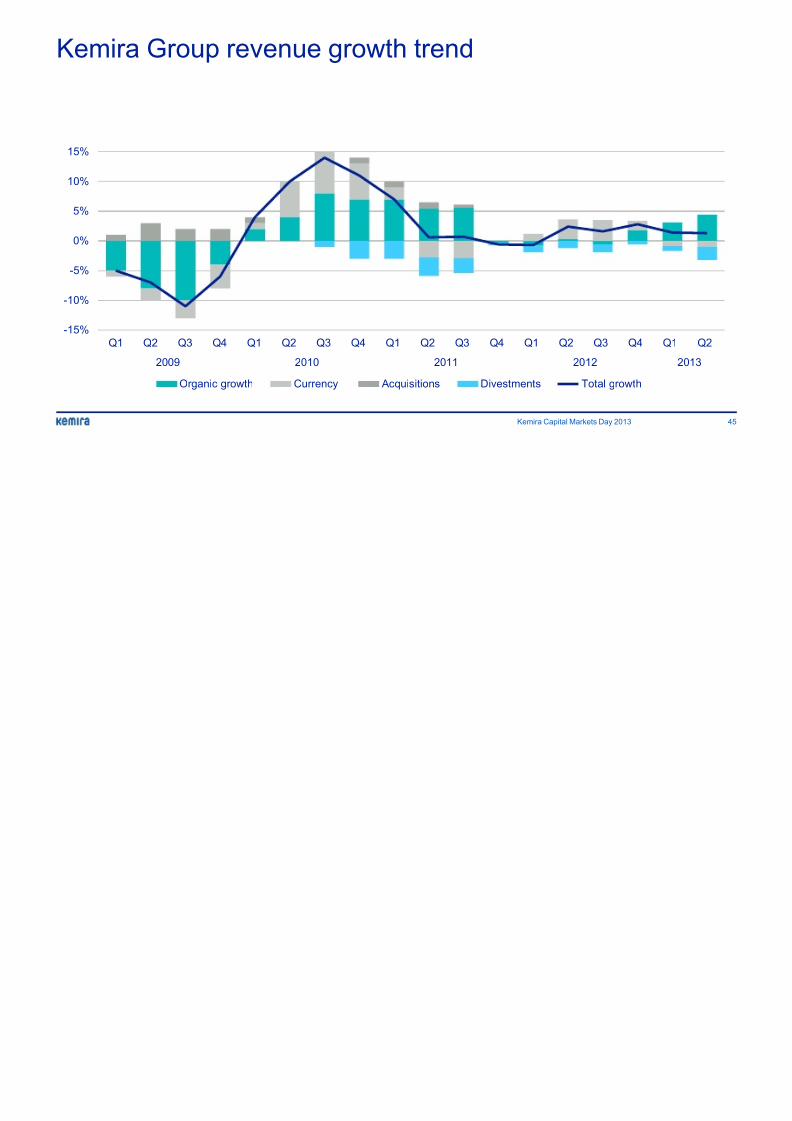

Kemira Group revenue growth trend

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 45/69

Kemira Group revenue growth trend

-15%

-10%

-5%

0%

5%

10%

15%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2009 2010 2011 2012

Organic growth Currency Acquisitions Divestments Total grow

Kemira Capital Markets Day 2013

Differentiated products expected to grow substantially

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 46/69

Differentiated products expected to grow substantiallymarket, commodity products focusing on efficiency im

Differentiated products

• Growth target substantially above the market

• Driven by innovation and expertise

• Higher margins due to higher value to the

customer

• Flexible manufacturing capabilities with

sufficient scale

• Higher barriers to entry (technology)

781843 879

0

200

400

600

800

1000

2010 2011 2012

Commodity products• Targeting growth, but slightly lower than

the market

• Maximizing profitability and cash flow by

leveraging existing capacity

Differentiated products revenue, EUR m

1380 1365 1362

0

500

1000

1500

2010 2011 2012

Commodity products revenue, EUR mil

Kemira revenue split into differentiated and comm

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 47/69

Kemira revenue split into differentiated and commproducts

Differentiated product lines Commodity product lines

%-of total

revenue in

1-6 2013

Polymers Sizing and

strength

Defoamers,

dispersants,

biocides and

other process

chemicals

Coagulants Bleaching

chemicals

Formic acid

and derivativ

Paper 10% 20% 15% 5% 25% -

M&I 20% - 5% 65% - -

O&M 55% - 25% 5% - - Chem-

Solutions

- - - - - 80%

Kemira 20% 10% 10% 25% 15% 5%

*) Mainly sodium percarbonate, colorants, acrylamide, inorganic salts and acids as well as caustic soda

Kemira Capital Markets Day 2013

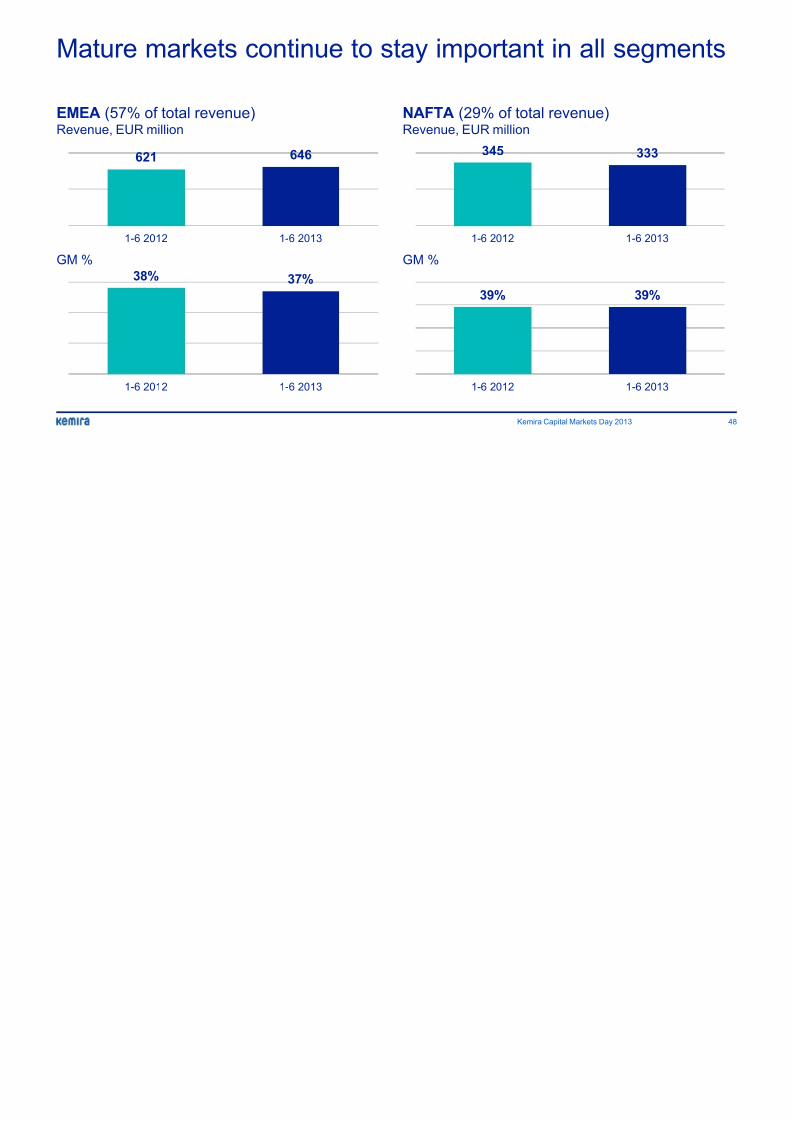

Mature markets continue to stay important in all se

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 48/69

Mature markets continue to stay important in all se

621 646

1-6 2012 1-6 2013

EMEA (57% of total revenue)Revenue, EUR million

345

1-6 2012 1

NAFTA (29% of total revenue)Revenue, EUR million

38% 37%

1-6 2012 1-6 2013

GM %

39%

1-6 2012 1

GM %

Kemira Capital Markets Day 2013

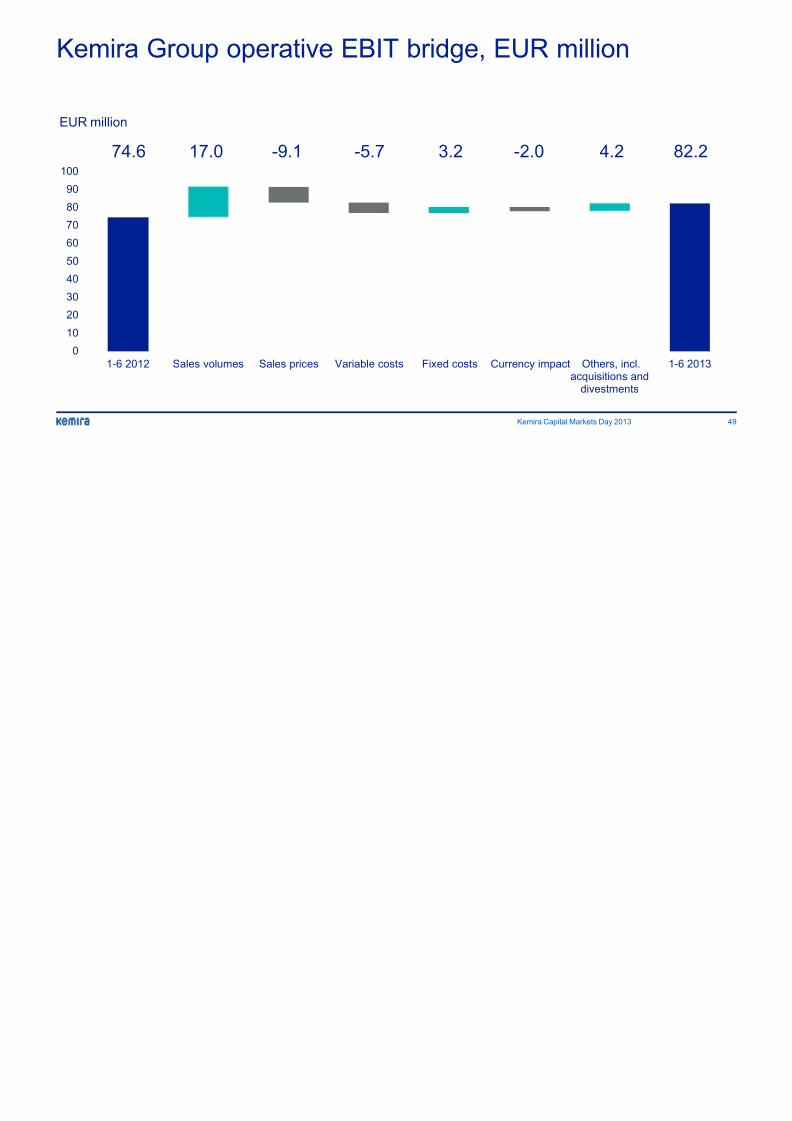

Kemira Group operative EBIT bridge EUR million

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 49/69

Kemira Group operative EBIT bridge, EUR million

0

10

20

30

40

50

60

70

80

90

100

1-6 2012 Sales volumes Sales prices Variable costs Fixed costs Currency impact Others, incacquisitions

divestmen

74.6 17.0 4.23.2-9.1 -5.7 -2.0

EUR million

Kemira Capital Markets Day 2013

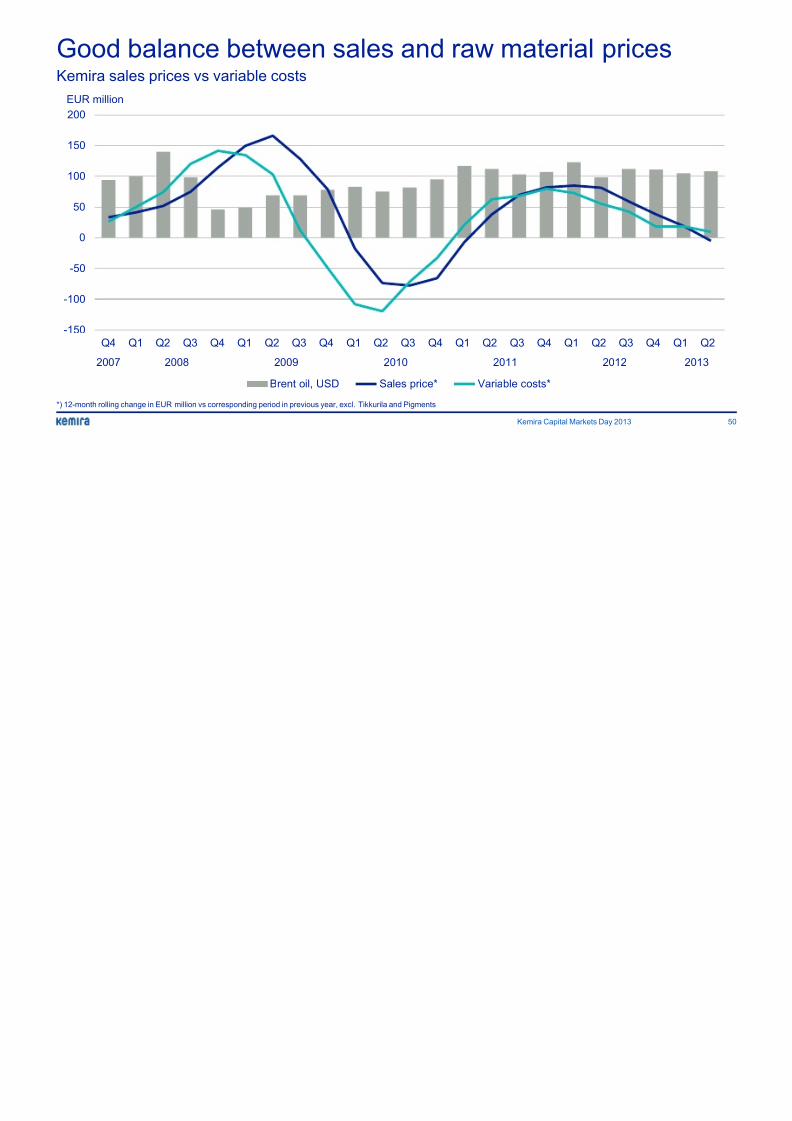

Good balance between sales and raw material pri

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 50/69

Good balance between sales and raw material priKemira sales prices vs variable costs

*) 12-month rolling change in EUR million vs corresponding period in previous year, excl. Tikkurila and Pigments

-150

-100

-50

0

50

100

150

200

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q

2007 2008 2009 2010 2011 2012

Brent oil, USD Sales price* Variable costs*

EUR million

Kemira Capital Markets Day 2013

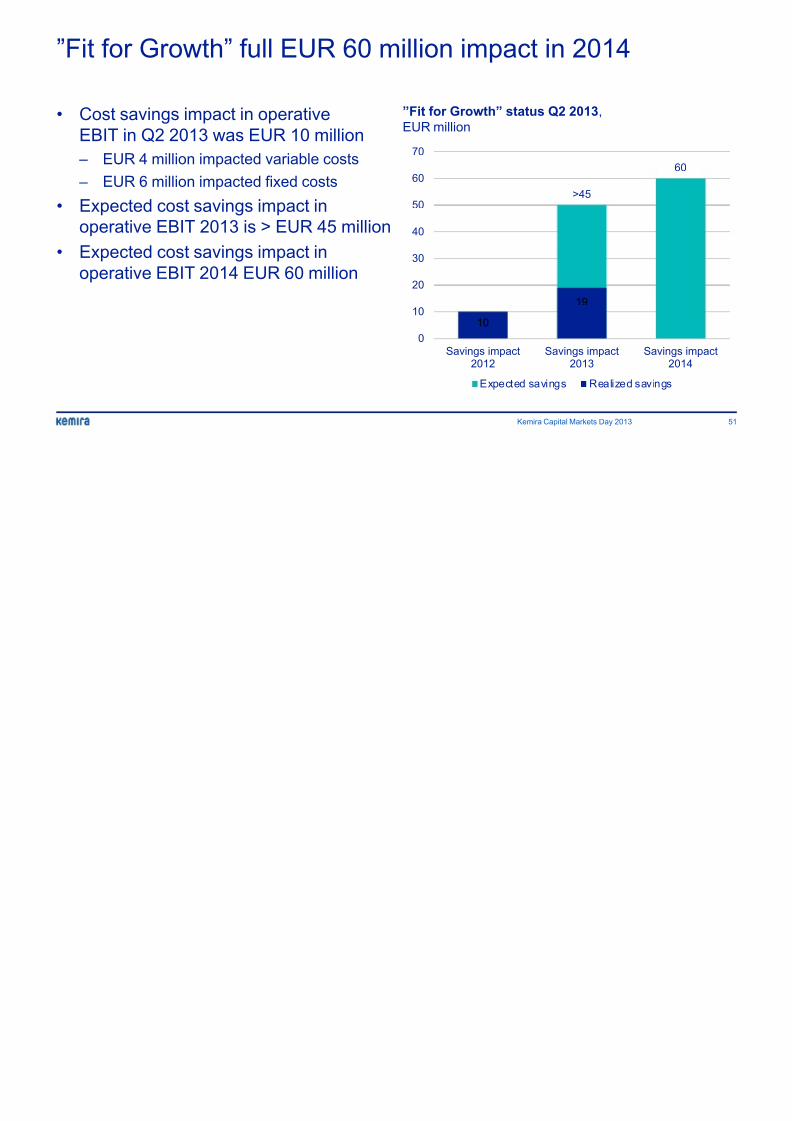

”Fit for Growth” full EUR 60 million impact in 2014

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 51/69

Fit for Growth full EUR 60 million impact in 2014

• Cost savings impact in operative

EBIT in Q2 2013 was EUR 10 million

– EUR 4 million impacted variable costs

– EUR 6 million impacted fixed costs

• Expected cost savings impact in

operative EBIT 2013 is > EUR 45 million

• Expected cost savings impact in

operative EBIT 2014 EUR 60 million

”Fit for Growth” status Q2 2013,

EUR million

>45

10

19

0

10

20

30

40

50

60

70

Savings impact2012

Savings impact2013

Expected savings Realized

Kemira Capital Markets Day 2013

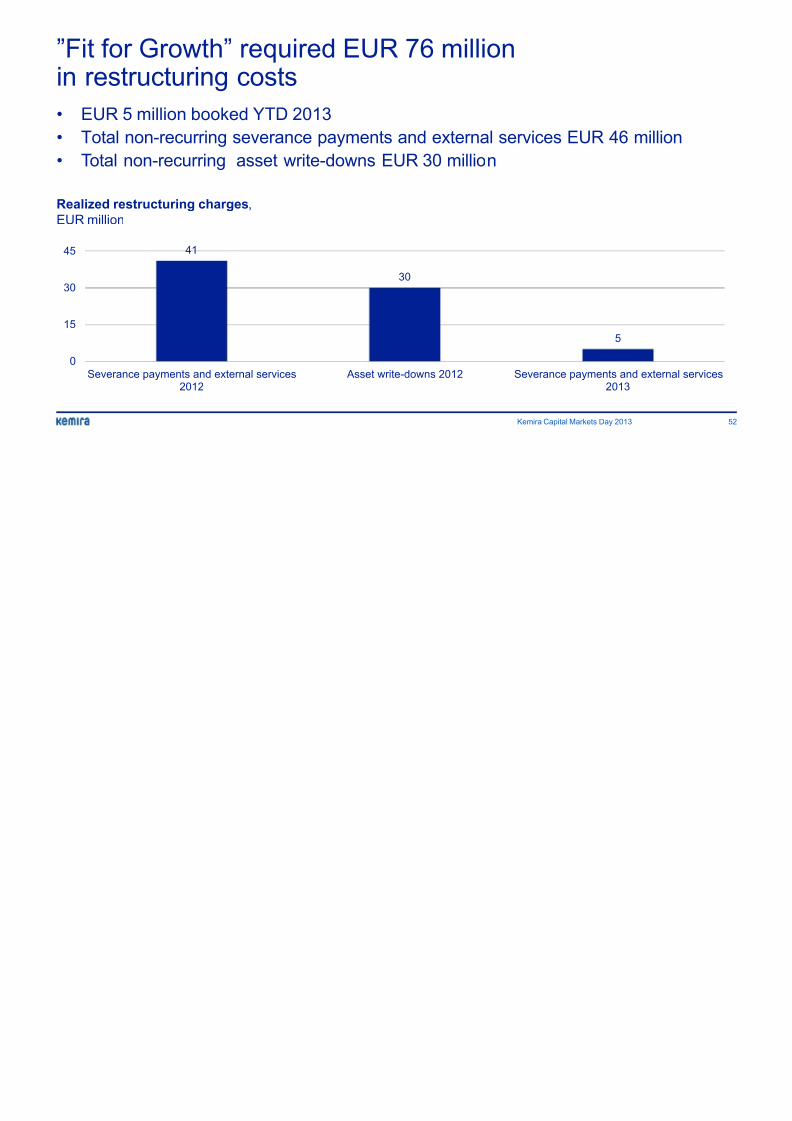

”Fit for Growth” required EUR 76 million

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 52/69

Fit for Growth required EUR 76 millionin restructuring costs

• EUR 5 million booked YTD 2013

• Total non-recurring severance payments and external services EUR 46

• Total non-recurring asset write-downs EUR 30 million

41

30

5

0

15

30

45

Severance payments and external services2012

Asset write-downs 2012 Severance payments an2013

Realized restructuring charges,

EUR million

Kemira Capital Markets Day 2013

Key figures and ratios

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 53/69

Key figures and ratios

EUR million (except ratios) 4-6/2013 4-6/2012 % 1-6/2013 1-6/2012

Revenue 569.3 562.3 1 1,130.2 1,115.2

Operative EBITDA 61.5 58.2 6 125.0 121.0

of which margin 10.8 10.3 - 11.1 10.8 Operative EBIT 40.0 36.0 11 82.2 74.6

of which margin 7.0 6.4 - 7.3 6.7

Share of profit or loss

of associates

0.1 5.8 - -1.1 16.6

Financing income and expenses -4.2 1.4 - -28.9 -8.9

Operative EPS, EUR 0.14 0.21 -33 0.31 0.41

Operative ROCE* 10.4 10.5 - 10.4 10.5

Capital expenditure 30.9 51.0 -39 59.9 70.4

Casf flow after investingactivities**

10.5 24.2 -57 200.4 16.1

Gearing, % at period-end 36 44 - 36 44

Personnel at period-end 4,664 5,181 -10 4,664 5,181

*12-month rolling average

**2012 numbers include EUR 5.3 million dividends and EUR 27.3 million paid-in-capital from JV Sachtleben. 1-6/2013 numbers include EUR 97.5 m

divestment of the JV Sachtleben shares and EUR 80.6 million from the divestment of the food and pharmaceuticals businesses.

Kemira Capital Markets Day 2013

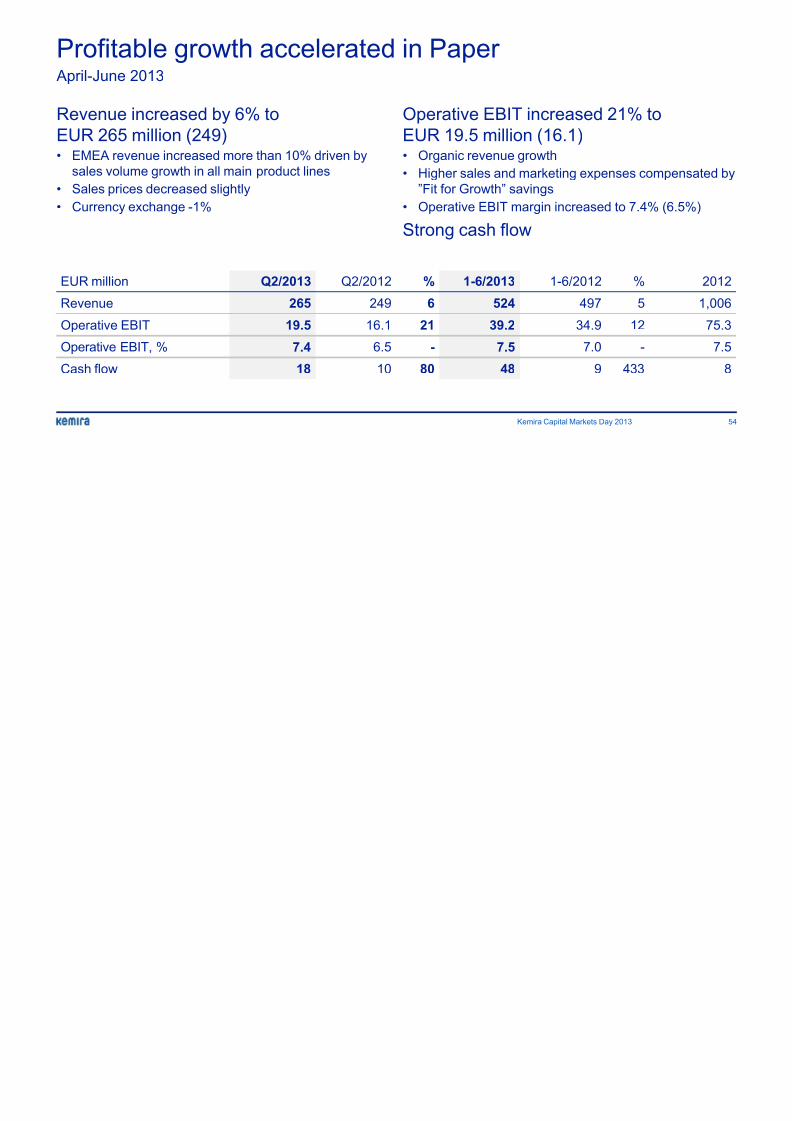

Profitable growth accelerated in Paper

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 54/69

g p April-June 2013

Revenue increased by 6% to

EUR 265 million (249)

• EMEA revenue increased more than 10% driven bysales volume growth in all main product lines

• Sales prices decreased slightly

• Currency exchange -1%

EUR million Q2/2013 Q2/2012 % 1-6/2013 1-6/2012

Revenue 265 249 6 524 497

Operative EBIT 19.5 16.1 21 39.2 34.9

Operative EBIT, % 7.4 6.5 - 7.5 7.0

Cash flow 18 10 80 48 9 4

Operative EBIT increased 21%

EUR 19.5 million (16.1)

• Organic revenue growth• Higher sales and marketing expense

”Fit for Growth” savings

• Operative EBIT margin increased to

Strong cash flow

Kemira Capital Markets Day 2013

Profitable growth in Municipal & Industrial

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 55/69

g p April-June 2013

Revenue increased 2% to

EUR 178 million (174)

• Revenues increased in all regions, except APAC• Currency exchange -1%

EUR million Q2/2013 Q2/2012 % 1-6/2013 1-6/2012

Revenue 178 174 2 343 335

Operative EBIT 15.9 12.0 33 24.5 17.7

Operative EBIT, % 8.9 6.9 - 7.1 5.3

Cash flow 5 -3 - 5 4

Operative EBIT increased 33%

EUR 15.9 million (12.0)

• Increased sales prices and sales volulower fixed costs

• Higher variable costs due to increase

based raw material prices during Q1

• Operative EBIT margin increased to

Kemira Capital Markets Day 2013

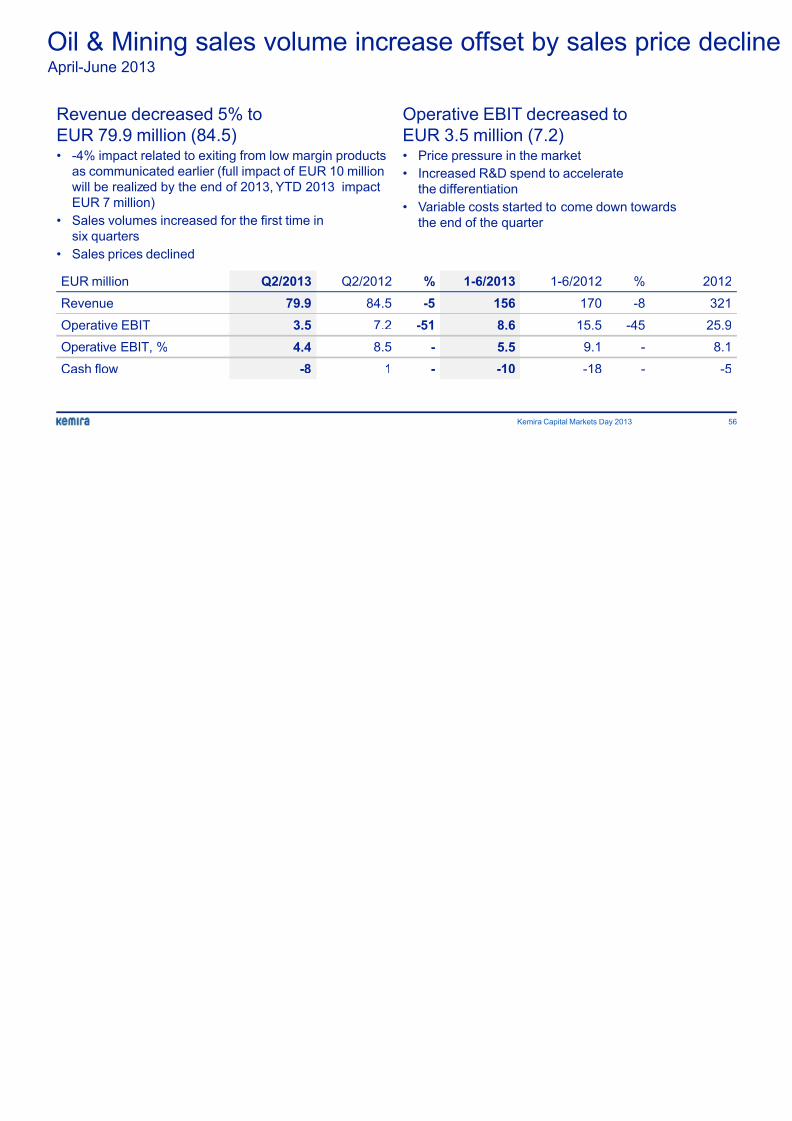

Oil & Mining sales volume increase offset by sales

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 56/69

April-June 2013

Revenue decreased 5% to

EUR 79.9 million (84.5)

• -4% impact related to exiting from low margin productsas communicated earlier (full impact of EUR 10 million

will be realized by the end of 2013, YTD 2013 impact

EUR 7 million)

• Sales volumes increased for the first time in

six quarters

• Sales prices declined

EUR million Q2/2013 Q2/2012 % 1-6/2013 1-6/2012

Revenue 79.9 84.5 -5 156 170

Operative EBIT 3.5 7.2 -51 8.6 15.5 -

Operative EBIT, % 4.4 8.5 - 5.5 9.1

Cash flow -8 1 - -10 -18

Operative EBIT decreased to

EUR 3.5 million (7.2)

• Price pressure in the market• Increased R&D spend to accelerate

the differentiation

• Variable costs started to come down

the end of the quarter

Kemira Capital Markets Day 2013

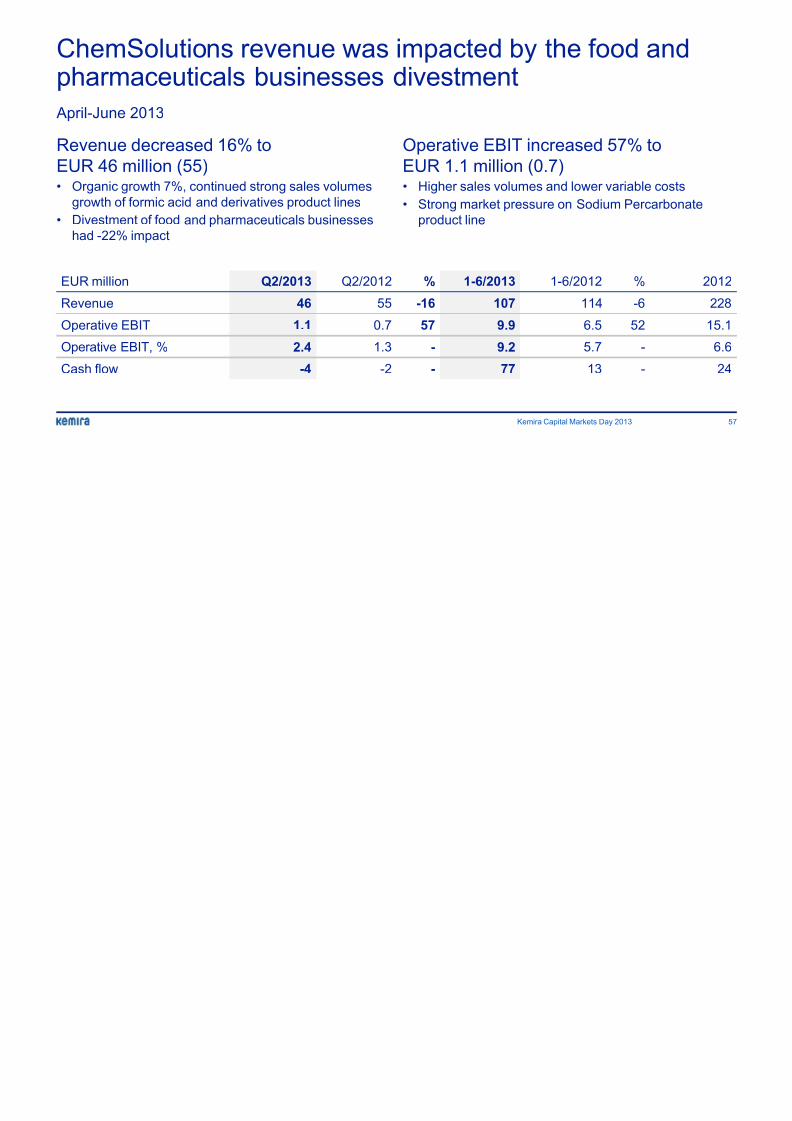

ChemSolutions revenue was impacted by the food

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 57/69

p ypharmaceuticals businesses divestment

April-June 2013

Revenue decreased 16% to

EUR 46 million (55)• Organic growth 7%, continued strong sales volumes

growth of formic acid and derivatives product lines

• Divestment of food and pharmaceuticals businesses

had -22% impact

EUR million Q2/2013 Q2/2012 % 1-6/2013 1-6/2012

Revenue 46 55 -16 107 114

Operative EBIT 1.1 0.7 57 9.9 6.5

Operative EBIT, % 2.4 1.3 - 9.2 5.7

Cash flow -4 -2 - 77 13

Operative EBIT increased 57%

EUR 1.1 million (0.7)• Higher sales volumes and lower varia

• Strong market pressure on Sodium P

product line

Kemira Capital Markets Day 2013

Kemira capital expenditure

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 58/69

p p

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 1-6 2013

EUR million

134

56

98

7669

109

Kemira Capital Markets Day 2013

Net working capital ratio

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 59/69

Kemira ambition is to keep net working capital ratio* between 11%-11.5%

14.1%

13.3%

11.3%

13.4%

12.8%

9%

11%

13%

15%

2008 2009 2010 2011 2012

*) Rolling 12-month average

Kemira Capital Markets Day 2013

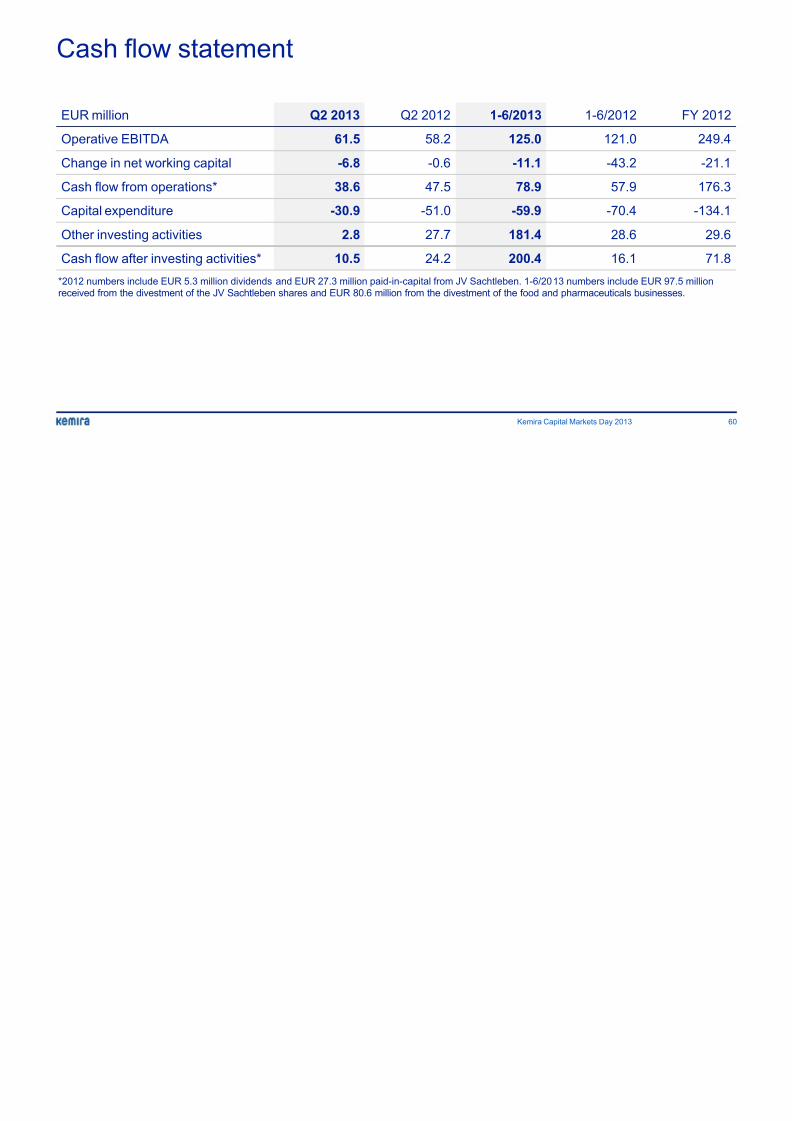

Cash flow statement

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 60/69

EUR million Q2 2013 Q2 2012 1-6/2013 1-6/201

Operative EBITDA 61.5 58.2 125.0 121.

Change in net working capital -6.8 -0.6 -11.1 -43.

Cash flow from operations* 38.6 47.5 78.9 57.

Capital expenditure -30.9 -51.0 -59.9 -70.4

Other investing activities 2.8 27.7 181.4 28.

Cash flow after investing activities* 10.5 24.2 200.4 16.

Kemira Capital Markets Day 2013

*2012 numbers include EUR 5.3 million dividends and EUR 27.3 million paid-in-capital from JV Sachtleben. 1-6/2013 numbers includ

received from the divestment of the JV Sachtleben shares and EUR 80.6 million from the divestment of the food and pharmaceuticals

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 61/69

Market andproduct

specifications

Kemira Capital Markets Day 2013, September 10

Kemira Capital Markets Day 2013

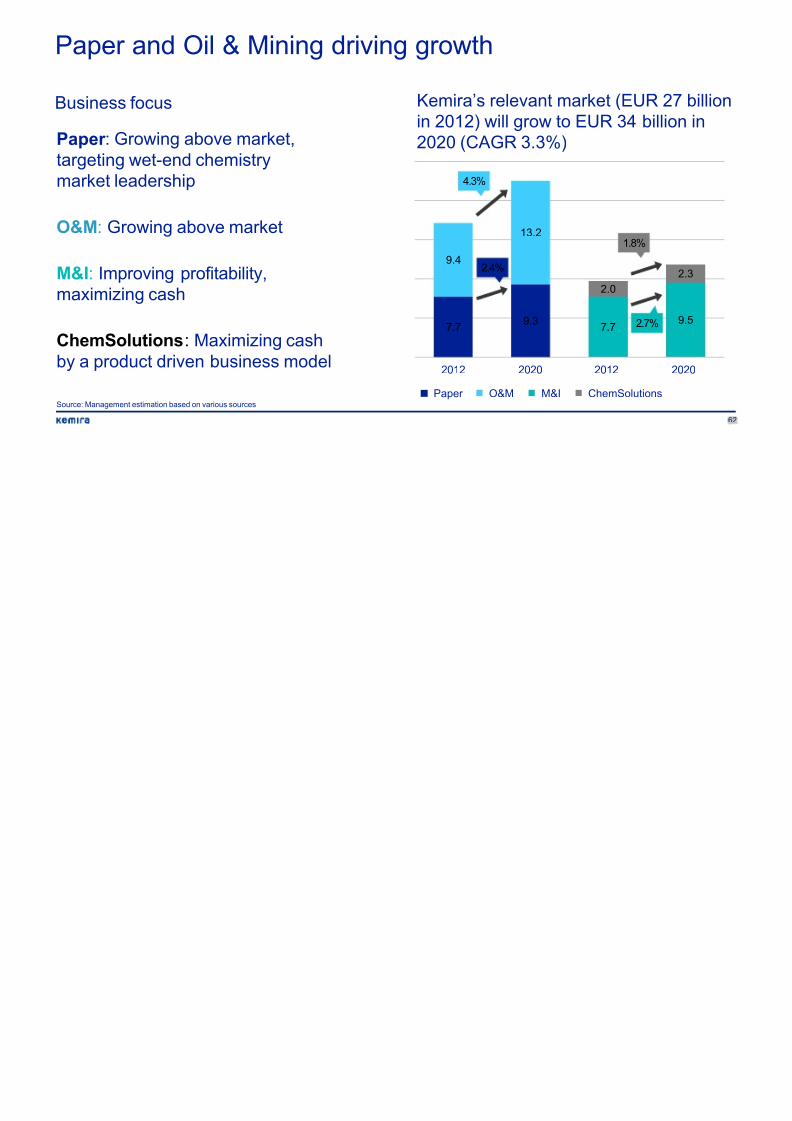

Paper and Oil & Mining driving growth

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 62/69

Kemira’s relevant market (E

in 2012) will grow to EUR 34

2020 (CAGR 3.3%)Paper : Growing above market,

targeting wet-end chemistrymarket leadership

O&M: Growing above market

M&I: Improving profitability,

maximizing cash

ChemSolutions: Maximizing cash

by a product driven business model

Source: Management estimation based on various sources

7.79.3

7.7

9.4

13.2

2.0

2012 2020 2012'

O&MPaper

2.4%

ChemSoM&I

4.3%

1.

Business focus

Paper segment - Demand for sizing and strengthh i l i i f t t l b ll

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 63/69

1.5 1.7 1.9 2.0 2.1 2

0.91.0

1.1

1.82.0

21.5

1.61.8

2012 2016 2020 2012 2016 20

Defoamers, biocides and other wet-end pr

chemicals is growing fastest globally

Pulp and paper industry trends increasing

chemical demand:

• Increased use of recycled fibres• Hardwood replacing softwood in virgin

pulp

• Lightweighting of packaging and board

grades

• Higher filler loads in graphic papers

• New digital printing methods

• Lower water / energy consumption

Market size,

EUR billion (CAGR: 2.4%)

Sizing and strength

Miscellaneous co

Bleaching chemi

Polymers

Kemira Capital Markets Day 2013

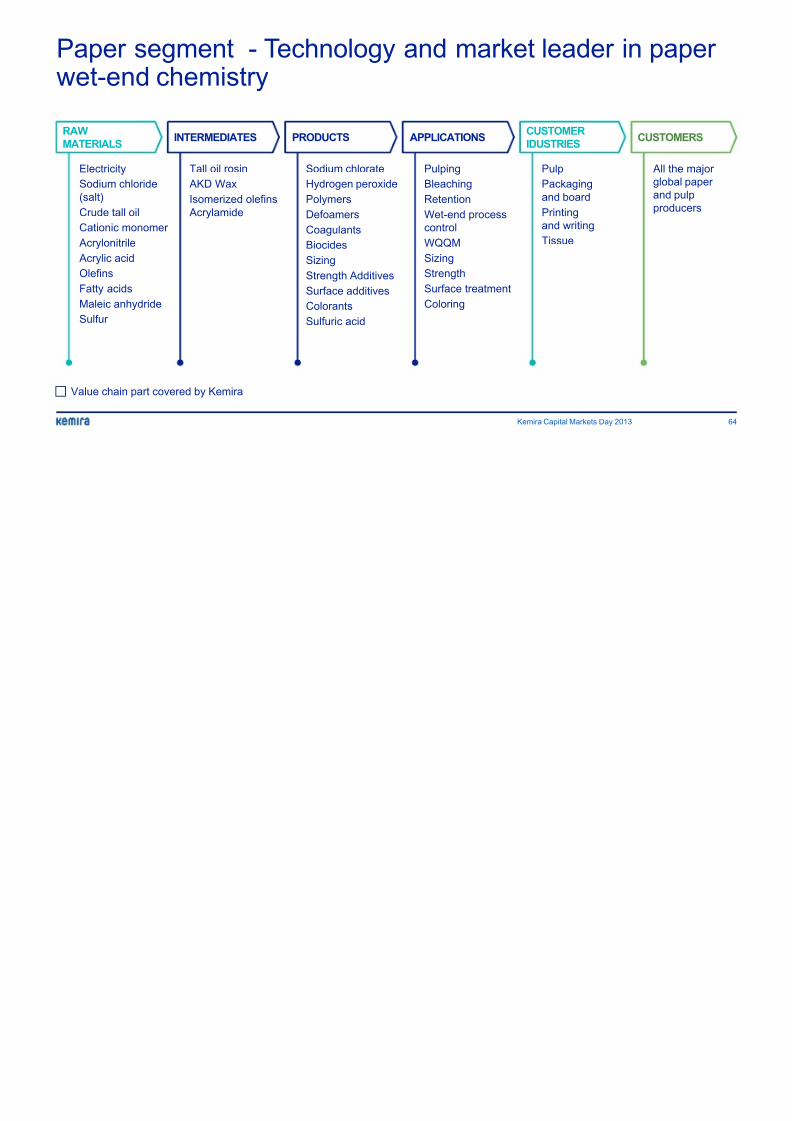

Paper segment - Technology and market leader it d h i t

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 64/69

wet-end chemistry

Value chain part covered by Kemira

RAW

MATERIALSINTERMEDIATES PRODUCTS APPLICATIONS

CUSTOMER

IDUSTRIES

Electricity

Sodium chloride

(salt)

Crude tall oil

Cationic monomer

Acrylonitrile

Acrylic acid

Olefins

Fatty acids

Maleic anhydride

Sulfur

Tall oil rosin

AKD Wax

Isomerized olefins

Acrylamide

Sodium chlorate

Hydrogen peroxide

Polymers

Defoamers

Coagulants

Biocides

Sizing

Strength Additives

Surface additives

Colorants

Sulfuric acid

Pulping

Bleaching

Retention

Wet-end process

control

WQQM

Sizing

Strength

Surface treatment

Coloring

Pulp

Packaging

and board

Printing

and writing

Tissue

Kemira Capital Markets Day 2013

Oil & Mining segment - Strong market growth acrod t li

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 65/69

product lines

• High oil price spurs demand for

identifying new sources

• Global growth of shale gas and wetshale

• Declining ore assays require improved

processing

• Increasing environmental pressure

which increases demand for waste

water treatment

Market size,

EUR billion (CAGR: 4.7%)

3.1 3.6 4.3

2.0

4.3

5.1

6.1

2012 2016 2020 2012

Polymers Defoamers, biocides

and other process

chemicals

Kemira Capital Markets Day 2013

Oil & Mining segment - Winning market share withtiti bi ti f i ti h i l

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 66/69

competitive combination of innovation chemicals aapplication knowledge

Value chain part covered by Kemira

RAW

MATERIALS

INTERMEDIATES PRODUCTS APPLICATIONS CUST

Acrylonitrile

Acrylic acid

Various monomers

Miscellaneous

specialty chemicalsand commodities

Acrylamide Polymers

Dispersants &

Antiscalants

Biocides

Emulsifiers

Defoamers

Coagulants

Formulations

Friction Reduction

Formation & Well Scale

Control

Asset integrity Microbial

Induced Corrosion

Enhanced Oil Recovery

Drilling muds

Concentrate thickening

Mineral slurrypreservation

Mining processes

Scale Control

P

O

op

S

co

M

Kemira Capital Markets Day 2013

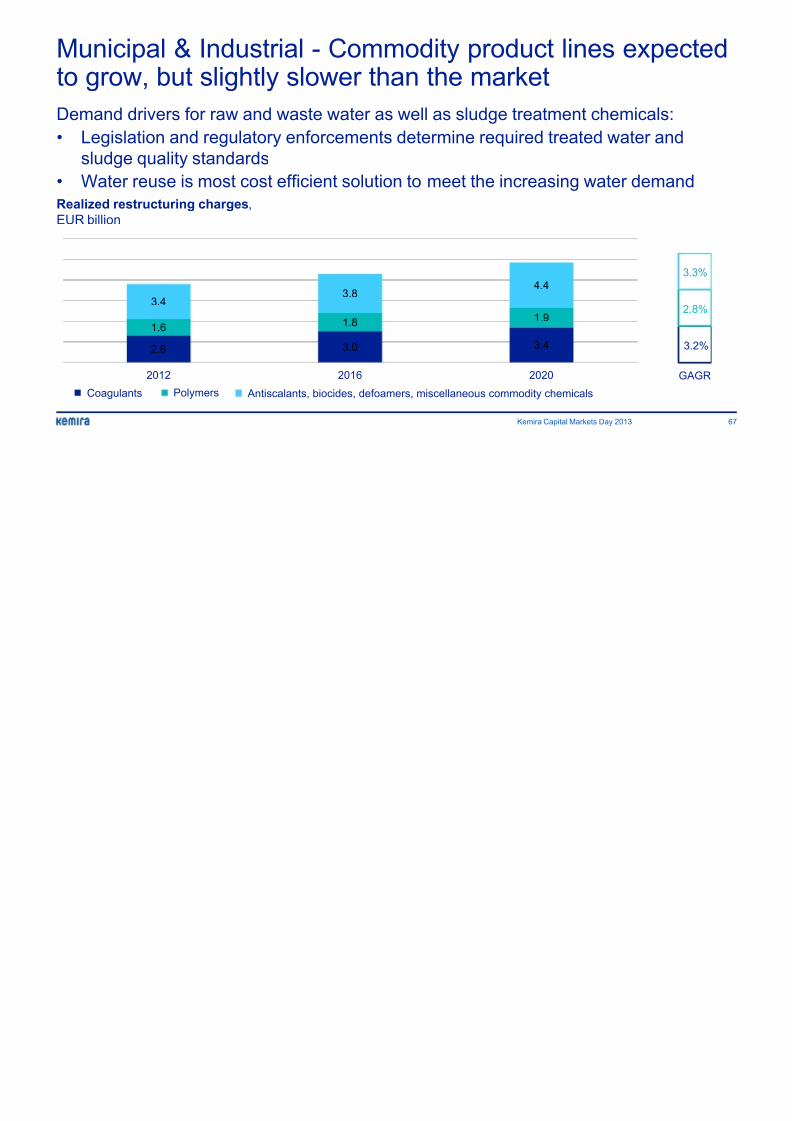

Municipal & Industrial - Commodity product lines eto grow but slightly slower than the market

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 67/69

to grow, but slightly slower than the market

Demand drivers for raw and waste water as well as sludge treatment chem

• Legislation and regulatory enforcements determine required treated wat

sludge quality standards• Water reuse is most cost efficient solution to meet the increasing water

2.6 3.0 3.4

1.6 1.8 1.9

3.4 3.8

4.4

2012 2016 2020

Coagulants Antiscalants, biocides, defoamers, miscellaneous commodity chemicalsPolymers

Realized restructuring charges,

EUR billion

Kemira Capital Markets Day 2013

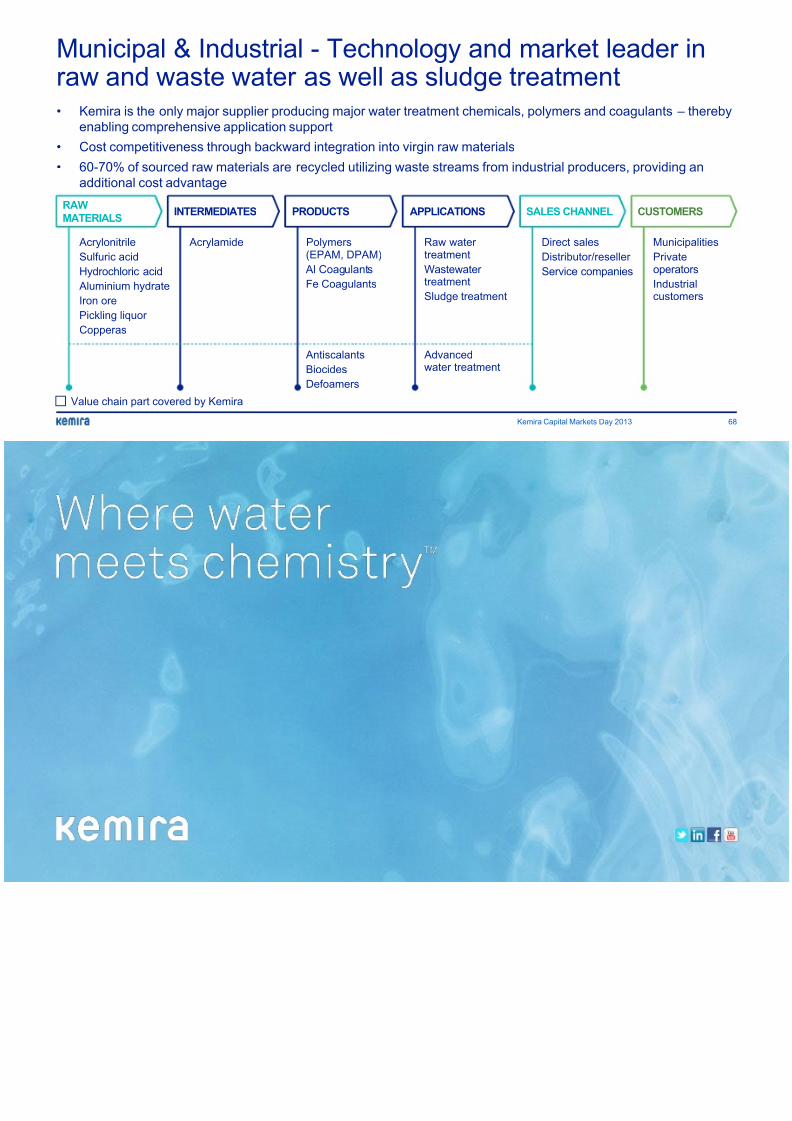

Municipal & Industrial - Technology and market learaw and waste water as well as sludge treatment

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 68/69

raw and waste water as well as sludge treatment• Kemira is the only major supplier producing major water treatment chemicals, polymers and coa

enabling comprehensive application support

• Cost competitiveness through backward integration into virgin raw materials

• 60-70% of sourced raw materials are recycled utilizing waste streams from industrial producers,

additional cost advantage

RAW

MATERIALSINTERMEDIATES PRODUCTS APPLICATIONS SALES CHANNEL

Acrylonitrile

Sulfuric acid

Hydrochloric acid

Aluminium hydrate

Iron orePickling liquor

Copperas

Acrylamide Polymers(EPAM, DPAM)

Al Coagulants

Fe Coagulants

Antiscalants

Biocides

Defoamers

Raw watertreatment

Wastewatertreatment

Sludge treatment

Advancedwater treatment

Direct sales

Distributor/reseller

Service companies

Value chain part covered by Kemira

Kemira Capital Markets Day 2013

8/13/2019 Emir 2013 Presentation

http://slidepdf.com/reader/full/emir-2013-presentation 69/69