emerging chinese market & consumer insights€¦ · emerging chinese market & consumer...

TRANSCRIPT

Emerging Chinese Market & Consumer Insights

Vinay DixitSenior Director – Asia Consumer CentersMcKinsey & Company

15 October 2010

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company 1|

Presentation Outline

Role of Internet in lifestyle & consumption

Increasing consumer sophistication

▪ Continued shift towards discretionary spend categories

▪ City-tiers no longer the best business opportunity framework in China; city-clusters more effective & efficient

▪ Brands remain important, but loyalty is falling; moreover loyalty is largely to a suite of brands rather than a single brand

▪ While some consumers are upgrading, a majority are “trading-off”to manage their share of wallet

Chinese market & consumers

Continued macroeconomic resilience

▪ Macroeconomic fundamentals remain strong

▪ Continued drive towards urbanization results in majority of economic activity to be concentrated in urban centers

▪ The explosive growth of internet is causing significant shifts in lifestyles, research process and purchase channels in China & India

▪ Consumers are turning into “smart-shoppers” at accelerated pace

McKinsey & Company 2|

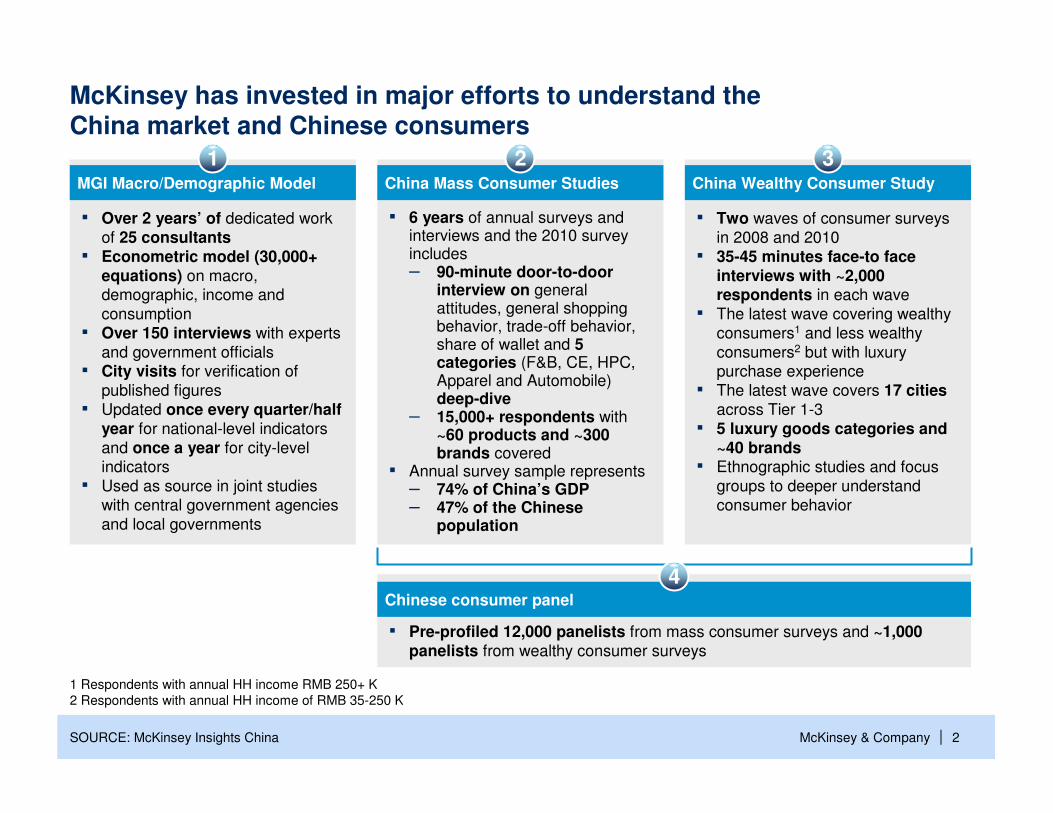

McKinsey has invested in major efforts to understand the China market and Chinese consumers

SOURCE: McKinsey Insights China

1 Respondents with annual HH income RMB 250+ K

2 Respondents with annual HH income of RMB 35-250 K

▪ Over 2 years’ of dedicated work

of 25 consultants▪ Econometric model (30,000+

equations) on macro, demographic, income and

consumption

▪ Over 150 interviews with experts

and government officials▪ City visits for verification of

published figures

▪ Updated once every quarter/half year for national-level indicators

and once a year for city-level indicators

▪ Used as source in joint studies

with central government agencies

and local governments

▪ Two waves of consumer surveys

in 2008 and 2010

▪ 35-45 minutes face-to face interviews with ~2,000 respondents in each wave

▪ The latest wave covering wealthy

consumers1 and less wealthy

consumers2 but with luxury purchase experience

▪ The latest wave covers 17 citiesacross Tier 1-3

▪ 5 luxury goods categories and ~40 brands

▪ Ethnographic studies and focus

groups to deeper understand

consumer behavior

▪ 6 years of annual surveys and interviews and the 2010 survey includes– 90-minute door-to-door

interview on general attitudes, general shopping behavior, trade-off behavior, share of wallet and 5categories (F&B, CE, HPC, Apparel and Automobile)deep-dive

– 15,000+ respondents with ~60 products and ~300 brands covered

▪ Annual survey sample represents– 74% of China’s GDP– 47% of the Chinese

population

MGI Macro/Demographic Model China Wealthy Consumer StudyChina Mass Consumer Studies

1 2 3

▪ Pre-profiled 12,000 panelists from mass consumer surveys and ~1,000 panelists from wealthy consumer surveys

Chinese consumer panel

4

McKinsey & Company 3|SOURCE: Global Insight; McKinsey Insights China - August 2010 update

China’s GDP has rebounded well, and is expected to stayrobust to 2025

CONTINUED MACROECONOMIC RESILIENCE

Growth of China real GDP – YearlyGrowth of China real GDP – Quarterly (YoY)

11.9

10.7

6.2

0

2

4

6

8

10

12

14

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

10.3

Q2

2007 08 09 2010

9.8

8.7

5

6

7

8

9

10

11

12

13

14

2025 2015102005

History Forecast

>9% 8~9% <8%

China’s GDP is expected to grow at around 10% in 2010 and between 8-10% through the current decade

McKinsey & Company 4|

1 Includes 650 official cities, 165 counties that are identified as hidden cities and new cities

SOURCE: McKinsey Insights China - August 2010 update

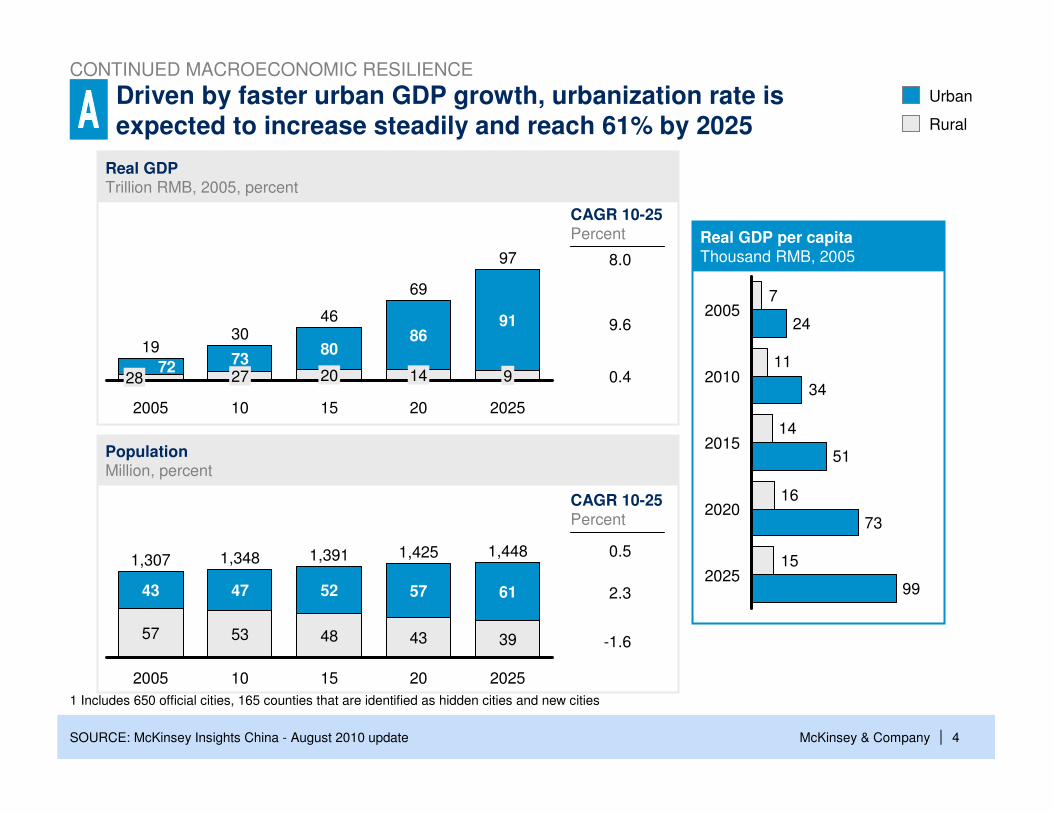

Driven by faster urban GDP growth, urbanization rate is expected to increase steadily and reach 61% by 2025

CONTINUED MACROECONOMIC RESILIENCE

Real GDP Trillion RMB, 2005, percent

PopulationMillion, percent

Real GDP per capitaThousand RMB, 2005

73

2005

19

2872

10

27

30

69

20

91

2025

97

914

86

15

46

20

80

2025

1,448

39

20

1,425

61

43

52

10

57

15

1,348

53

1,391

48

47

2005

43

1,307

57

15

16

14

11

7

99

73

51

34

24

2025

2015

2020

2010

20059.6

0.4

8.0

2.3

-1.6

0.5

CAGR 10-25Percent

CAGR 10-25Percent

Urban

Rural

McKinsey & Company 5|

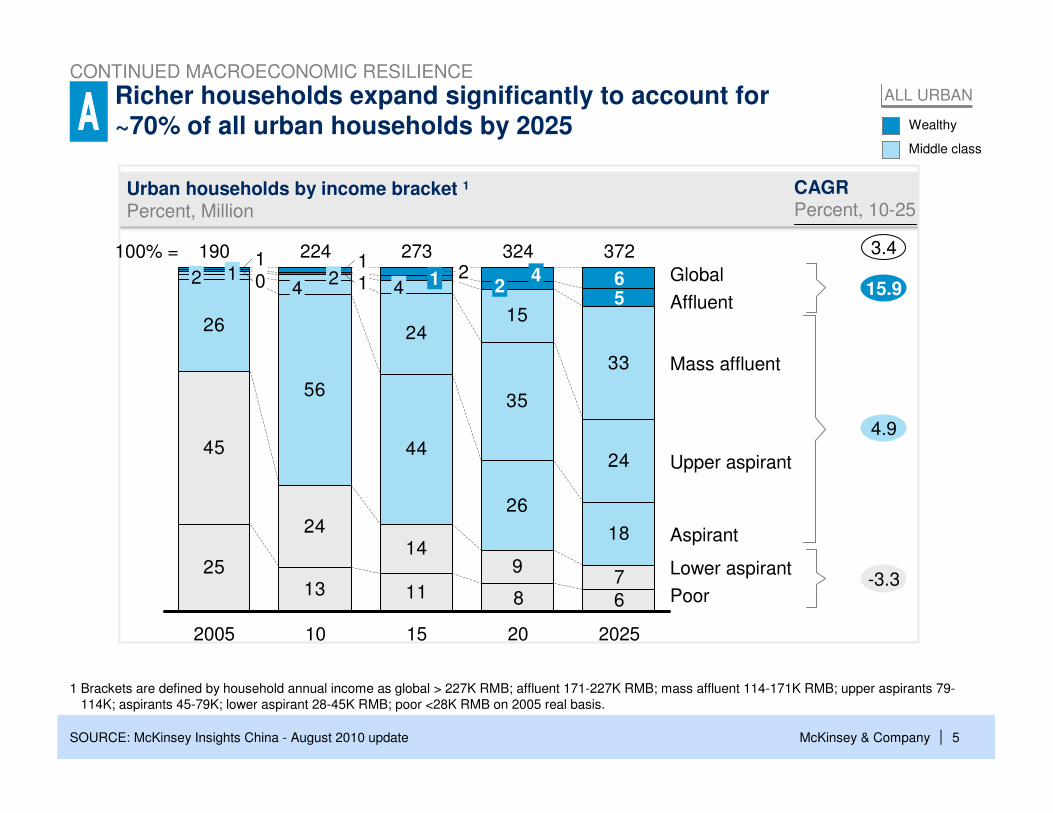

1 Brackets are defined by household annual income as global > 227K RMB; affluent 171-227K RMB; mass affluent 114-171K RMB; upper aspirants 79-

114K; aspirants 45-79K; lower aspirant 28-45K RMB; poor <28K RMB on 2005 real basis.

ALL URBAN

SOURCE: McKinsey Insights China - August 2010 update

Richer households expand significantly to account for~70% of all urban households by 2025

Urban households by income bracket 1

Percent, Million

CONTINUED MACROECONOMIC RESILIENCE

2513 11 6

45

2414

97

26

56

44

26

18

24

35

24

8

33

15

102

11100% = 324

224

5

224

10

14

273

15

372

Global

Affluent

Mass affluent

Upper aspirant

Aspirant

2025

Lower aspirant

Poor

12 4

20

6

190

2005

15.9

3.4

4.9

-3.3

Middle class

Wealthy

CAGRPercent, 10-25

McKinsey & Company 6|

Presentation Outline

Role of Internet in lifestyle & consumption

Increasing consumer sophistication

▪ Continued shift towards discretionary spend categories

▪ City-tiers no longer the best business opportunity framework in China; city-clusters more effective & efficient

▪ Brands remain important, but loyalty is falling; moreover loyalty is largely to a suite of brands rather than a single brand

▪ While some consumers are upgrading, a majority are “trading-off”to manage their share of wallet

Chinese market & consumers

Continued macroeconomic resilience

▪ Macroeconomic fundamentals remain strong

▪ Continued drive towards urbanization results in majority of economic activity to be concentrated in urban centers

▪ The explosive growth of internet is causing significant shifts in lifestyles, research process and purchase channels in China & India

▪ Consumers are turning into “smart-shoppers” at accelerated pace

McKinsey & Company 7|

20

7081

45-65

18-45

Japan3

19

US2

30

China1

80

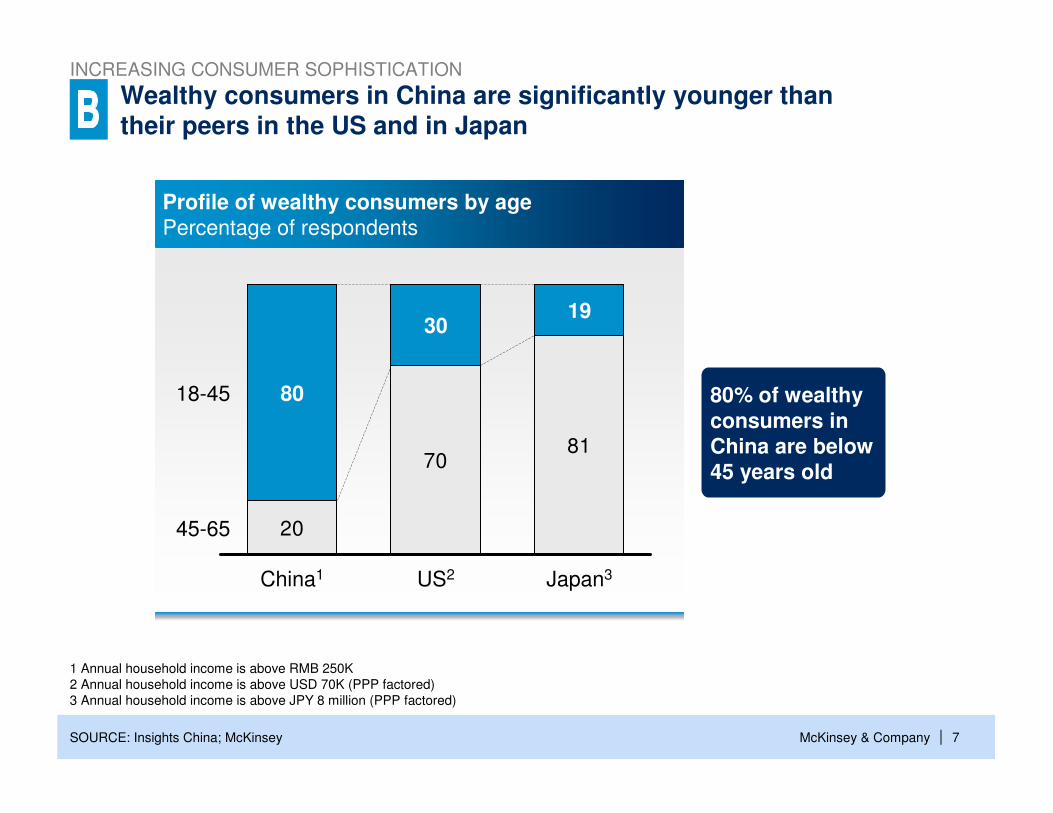

Profile of wealthy consumers by agePercentage of respondents

80% of wealthy consumers in China are below 45 years old

1 Annual household income is above RMB 250K

2 Annual household income is above USD 70K (PPP factored)

3 Annual household income is above JPY 8 million (PPP factored)

SOURCE: Insights China; McKinsey

Wealthy consumers in China are significantly younger than their peers in the US and in Japan

INCREASING CONSUMER SOPHISTICATION

McKinsey & Company 8|SOURCE: McKinsey Insights China - March 2010 update

Urban China's share of wallet will continue to shift towards discretionary categories

ALL URBAN

INCREASING CONSUMER SOPHISTICATION

Thousand RMB, 2005, percent CAGRPercent, 10-25

Necessities Semi-necessities Discretionary

1010

1112

14

66

589

1011

11

1012

1110

937

29 24 20 18

13

14

3

26

20

95

21

Recreation, edu-cationand cultural

100% =

Personal items

18

5

5Housing and utility

Household product

Health care

Transportation, communication

2025

Food

Apparel

73

20

15

52

16

5

5

14

4

2005

5

18

15

2010

36

16

6.8

3.3

6.9

8.8

McKinsey & Company 9| 9

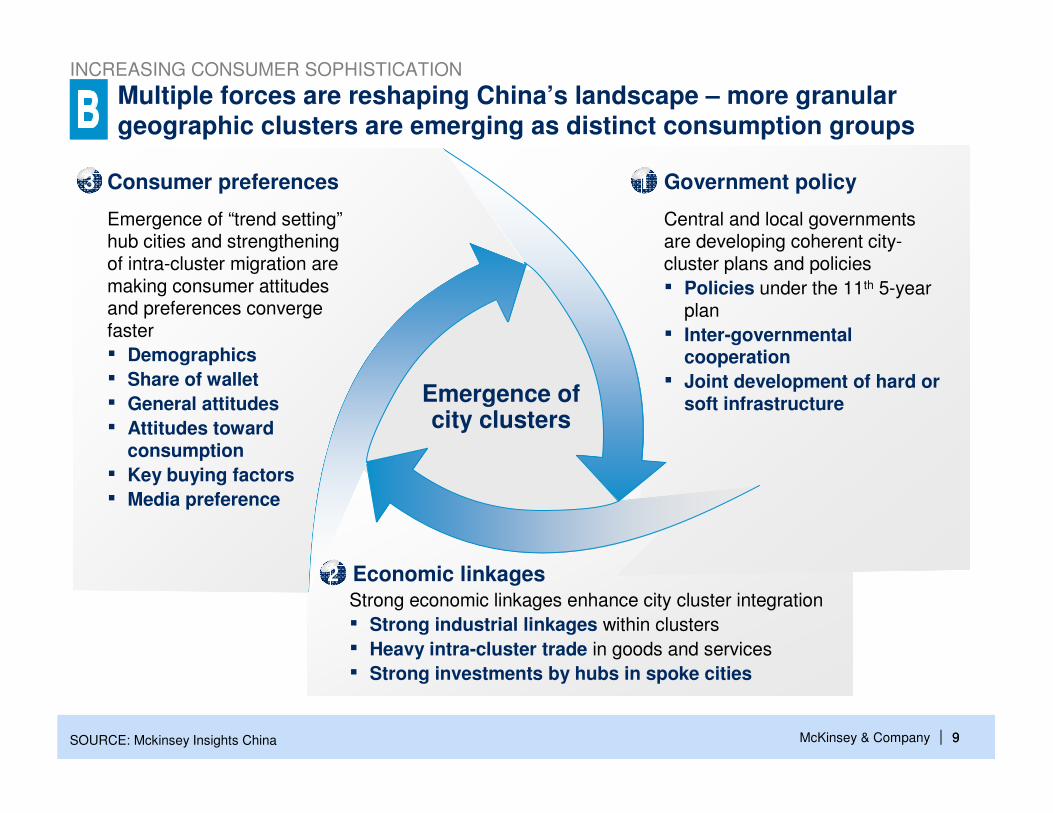

Multiple forces are reshaping China’s landscape – more granular geographic clusters are emerging as distinct consumption groups

Central and local governments are developing coherent city-cluster plans and policies

▪ Policies under the 11th 5-year plan

▪ Inter-governmental cooperation

▪ Joint development of hard or soft infrastructure

Strong economic linkages enhance city cluster integration

▪ Strong industrial linkages within clusters

▪ Heavy intra-cluster trade in goods and services

▪ Strong investments by hubs in spoke cities

Emergence of “trend setting”hub cities and strengthening of intra-cluster migration are making consumer attitudes and preferences converge faster

▪ Demographics

▪ Share of wallet

▪ General attitudes

▪ Attitudes toward consumption

▪ Key buying factors

▪ Media preference

Emergence of city clusters

Government policy

Economic linkages

Consumer preferences 13

2

SOURCE: Mckinsey Insights China

INCREASING CONSUMER SOPHISTICATION

McKinsey & Company 10|

xx (xx)

xx% | xx%

Cluster name # of cities

Cluster GDP & Hub city GDP

Large MegaSmall

22 is not a magic number! Each

company should tailor clusters to meet its

unique requirements

重庆重庆重庆重庆Chongqing

Chongqing (15)

2.3% | 1.5%

南宁南宁南宁南宁Nanning

Nanning (28)

1.8% | 0.3%

昆明昆明昆明昆明Kunming

Kunming (15)

1.0% | 0.5%

呼和浩特呼和浩特呼和浩特呼和浩特Huhehaote

Huhehaote (10)

1.3% | 0.4%

杭州杭州杭州杭州Hangzhou

Hangzhou (35)

6.6% | 1.6%

长春长春长春长春Changchun

哈尔滨哈尔滨哈尔滨哈尔滨Haerbin Changchun-Haerbin (36)

3.6 | 1.6%

南昌南昌南昌南昌Nanchang

Nanchang (21)

1.7% | 0.6%深圳深圳深圳深圳Shenzhen

Shenzhen (2)

4.3% |2.9%

大连大连大连大连Dalian

沈阳沈阳沈阳沈阳Shenyang

Liao central south (30)

4.3% | 2.4%

西̀安西安西安西安Xian

Guanzhong (15)

1.9% | 1.2%

Taiyuan (19)

1.4% | 0.5%

太原太原太原太原Taiyuan

Central (39)

3.6% | 0.7%

郑州郑州郑州郑州Zhengzhou

Chengdu (25)

2.7% | 1.6% 成都成都成都成都Chengdu

Hefei (29)

2.8% | 0.8% 合肥合肥合肥合肥Hefei

Yangzi mid-lower (42)

4.1% | 1.8%Changzhutan (29)

2.2% | 0.8%

长沙长沙长沙长沙Changsha

Coast West (38)

3.9 | 1.4%

福州福州福州福州Fuzhou厦门厦门厦门厦门

Xiamen

Jingjinji (37)

10.8% | 8.5%北京北京北京北京Beijing天津天津天津天津

Tianjin

石家庄石家庄石家庄石家庄Shijiazhuang

Shandong byland (67)

9.0% | 2.1%青岛青岛青岛青岛Qingdao济南济南济南济南

Jinan

Nanjing (28)

5.5% | 1.8%南京南京南京南京Nanjing

Shanghai (19)

10.1% | 6.2%上海上海上海上海Shanghai

Guangzhou (28)

6.9% | 2.6%

广州广州广州广州Guangzhou

武汉武汉武汉武汉Wuhan

We divided China into 22 city clusters accountingfor 92% of China’s GDP

SOURCE: Mckinsey Insights China

INCREASING CONSUMER SOPHISTICATION

McKinsey & Company 11|

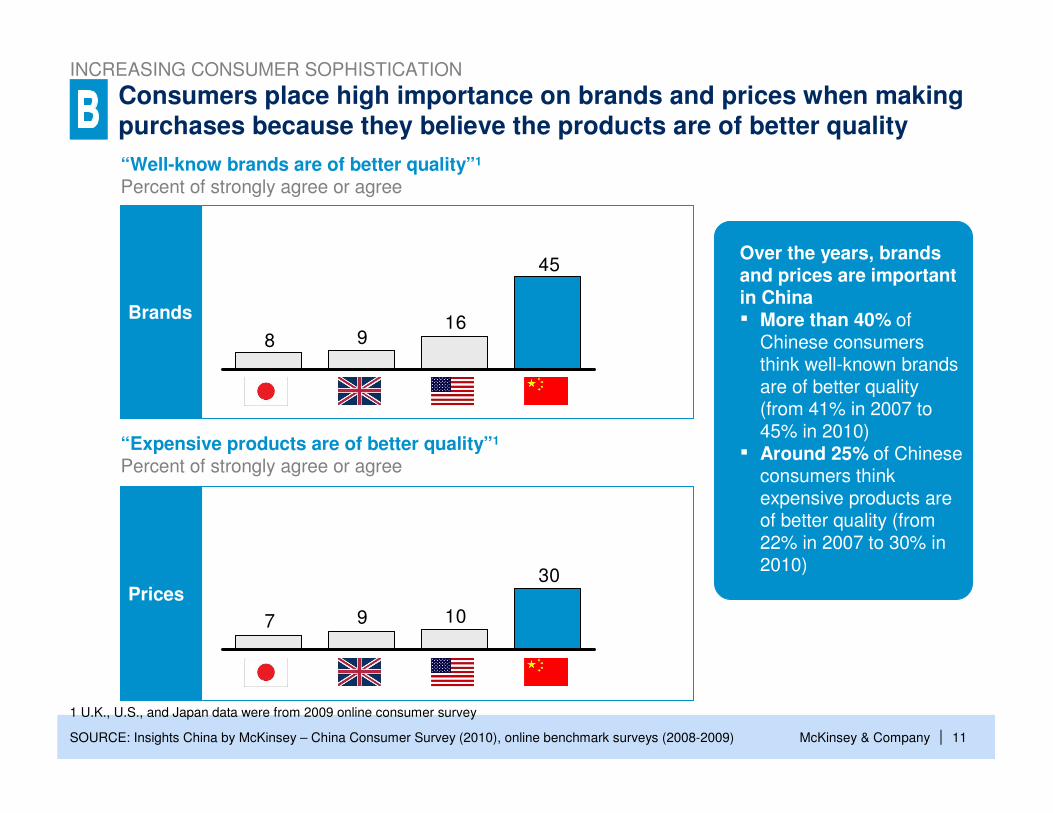

Consumers place high importance on brands and prices when makingpurchases because they believe the products are of better quality

“Well-know brands are of better quality”1

Percent of strongly agree or agree

“Expensive products are of better quality”1

Percent of strongly agree or agree

Brands

Prices

45

1698

30

1097

SOURCE: Insights China by McKinsey – China Consumer Survey (2010), online benchmark surveys (2008-2009)

1 U.K., U.S., and Japan data were from 2009 online consumer survey

Over the years, brands and prices are important in China▪ More than 40% of

Chinese consumers think well-known brands are of better quality (from 41% in 2007 to 45% in 2010)

▪ Around 25% of Chinese consumers think expensive products are of better quality (from 22% in 2007 to 30% in 2010)

INCREASING CONSUMER SOPHISTICATION

McKinsey & Company 12|

However, single brand loyalty is declining rapidly

SOURCE: McKinsey Insights China – 2007-2010 China consumer surveys

1 Weighted average of 5 F&B (UHT/fresh milk, yogurt, chocolate, beer, and carbonated soft drink)

2 Among respondents who claim to consider a few brands and decide which one to buy in the store or consider a few brands but are open to others if it is

on promotions in the store 3 Weighted average of 17 F&B 4 Weighted average of 13 HPC products 5 Weighted average of 7 CE products

1821

2927

44

48

4646

3626

20 24

53Always buy the best deal

Consider a few brandsbut are open to othersif they are on sale

Consider a few brandsand decide among theconsideration set

Only buy the preferred brand

2010

3

20092008

5

2007

Percent of respondents

Decreasing brand loyalty but increasing consideration from a repertoire of brands

F&B CATEGORY EXAMPLE1

Brand loyalty

Repertoire of brands

INCREASING CONSUMER SOPHISTICATION

McKinsey & Company 13|

Laptop exampleHome/ personal care example1

Purchase decisions are now increasingly influenced by “emotional” considerations – Comparison vs. US and UK

SOURCE: McKinsey Insights China – Annual Chinese Consumer Studies (2008, 2010); Online benchmark survey (2008)

12

434

15

36

14

105

2125

U.K. (2008)

U.S.(2008)

China (2010)

China (2008)

1 Facial moisturizer data for “status” and “what fits me”; laundry detergent data for “family”

2 Purchasing this brand can show my status

3 Using this brand makes me feel like my family is better off

4 It is a brand for people like me

Status2

Family3

What fits me4

10

122

6244

106

1115

China (2010)

China (2008)

U.K. (2008)

U.S.(2008)

INCREASING CONSUMER SOPHISTICATION

McKinsey & Company 14|

As consumers get more sophisticated, importance of Package Design is getting increasingly important over the years for FMCG categories

Importance of “Attractive Packaging Design”(percent)

SOURCE: Source

INCREASING CONSUMER SOPHISTICATION

16

12

2010

2008

Yogurt

24

9

Beer

24

17

30

23

ChocolateCarbonatedSoft Drink

20

14

Facial Moisturizer

21

16

Haircare

McKinsey & Company 15|

Presentation Outline

Role of Internet in lifestyle & consumption

Increasing consumer sophistication

▪ Continued shift towards discretionary spend categories

▪ City-tiers no longer the best business opportunity framework in China; city-clusters more effective & efficient

▪ Brands remain important, but loyalty is falling; moreover loyalty is largely to a suite of brands rather than a single brand

▪ While some consumers are upgrading, a majority are “trading-off”to manage their share of wallet

Chinese market & consumers

Continued macroeconomic resilience

▪ Macroeconomic fundamentals remain strong

▪ Continued drive towards urbanization results in majority of economic activity to be concentrated in urban centers

▪ The explosive growth of internet is causing significant shifts in lifestyles, research process and purchase channels in China & India

▪ Consumers are turning into “smart-shoppers” at accelerated pace

McKinsey & Company 16|SOURCE: CNNIC; Strategy Analytics (2008); Tech Crunchies; Internet World Status (2009); McKinsey

Total number of internet users1

Millions

17374347548196

228

384

AustraliaKoreaFranceUKGermanyIndiaJapanUSChina2Global

1,734

26 29 74 76 7 66 76 69 77 80

1 Including people access internet via PC and mobile phone. Data as of the end of 2009

2 For overall China population ≥ 6 years old

China has already had the world’s largest internet user base

Internet penetration,

percent

xx

420 million by June, 2010, a penetration of 32%

ROLE OF INTERNET

McKinsey & Company 17|

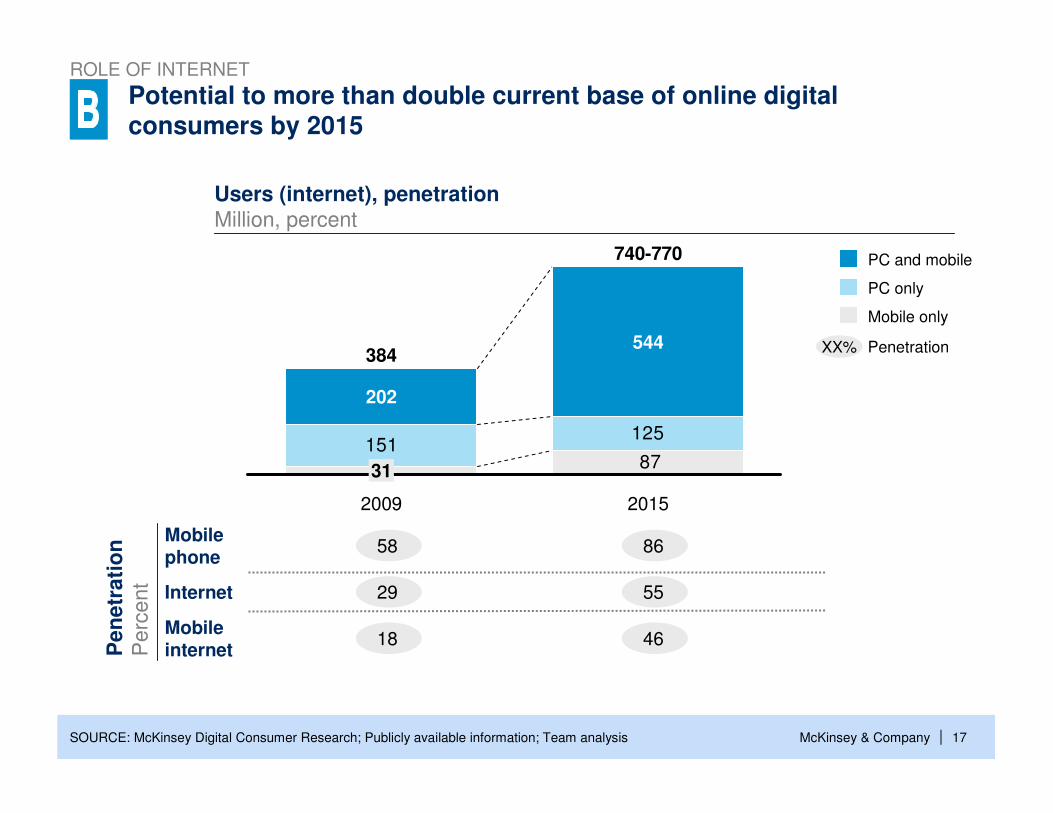

Potential to more than double current base of online digital consumers by 2015

Users (internet), penetrationMillion, percent

SOURCE: McKinsey Digital Consumer Research; Publicly available information; Team analysis

15187

125

2015

740-770

544

2009

384

31

202

29 55Internet

18 46Mobile internet

58 86Mobile phone

Pe

ne

tra

tio

nP

erc

en

t

XX% Penetration

Mobile only

PC only

PC and mobile

ROLE OF INTERNET

McKinsey & Company 18|

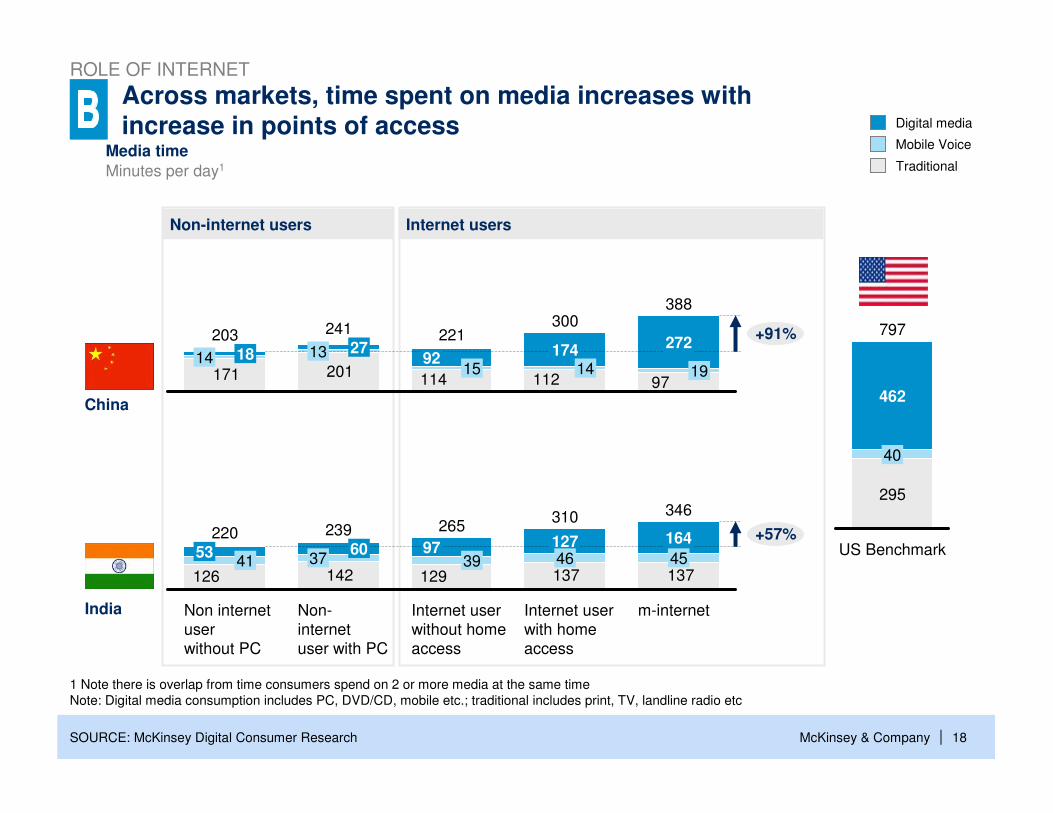

Across markets, time spent on media increases withincrease in points of access

Traditional

Mobile Voice

Digital media

97112114201171

388

19

272

300

14174

221

1592

241

13 27203

14 18

+91%

US Benchmark

797

295

40

462

SOURCE: McKinsey Digital Consumer Research

1 Note there is overlap from time consumers spend on 2 or more media at the same time

Note: Digital media consumption includes PC, DVD/CD, mobile etc.; traditional includes print, TV, landline radio etc

137137129142126

346

m-internet

45

164

Internet user

with home

access

310

46127

Internet user

without home

access

265

3997

Non-

internet

user with PC

239

3760

Non internet

user

without PC

220

4153

+57%

Non-internet users Internet users

India

China

Media time

Minutes per day1

ROLE OF INTERNET

McKinsey & Company 19|

“Have you surfed the internet in the past 6 months?”

While internet penetration in China is largely dependenton age …

URBAN CHINA

1 Among age 15-65

2 Weighted average of absolute deviation in each group from mean, sample size as weighting

SOURCE: Insights China by McKinsey – China Consumer Survey (2010)

Internet penetration clearly differs by agePercent of respondents (N = 13,271)

In fact, age is the most significant differentiator%; Weighted average deviation from mean2

11

20

47

76

91

Average internet

penetration rate: 531

55-65

45-54

35-44

25-34

18-24

2

4

9

11

26

Gender

Tier

Cluster

Income

Age

ROLE OF INTERNET

McKinsey & Company 20|

“How many hours do you spend on the Internet each week for personal reasons?”

URBAN CHINA

Time online does not differ much by ageAverage hours per week among internet

users (N = 7,079)

In fact, usage time is also similar across others macro-demographics%; Weighted average deviation from mean2

17

16

17

19

21

Average time

online: 191

55-65

45-54

35-44

25-34

18-24

3

5

4

Gender

Tier

Cluster 12

Income

Age 11

… once online, the amount of time people spent on internet doesn’t differ much by demographics

SOURCE: Insights China by McKinsey – China Consumer Survey (2010)

1 Among age 15-65

2 Weighted average of absolute deviation in each group from mean, sample size as weighting

ROLE OF INTERNET

McKinsey & Company 21|

“Before purchasing new products, I always check the Internet for other people's

usage experience/comments/feedback”

2010 25

2008 16

Total

45

N/A

Automotive

27

23

20

12

ApparelConsumerElectronics

19

14

Home/ Personal Care

▪ The proportion of consumers checking online for product information before purchasing is growing steadily over past 2 years

▪ This trend is especially strong for high value & high involvement categories

When in the market to make a purchase, Chinese consumers are increasingly using social media for checking product information

20

12

Food & Beverages

SOURCE: Insights China by McKinsey – China Consumer Survey (2010)

Percent of internet users who choose “strongly agree” or “agree” (N = 7,079)

ROLE OF INTERNET

McKinsey & Company 22|

In Summary…

Role of Internet in lifestyle & consumption

Increasing consumer sophistication

▪ Continued shift towards discretionary spend categories

▪ City-tiers no longer the best business opportunity framework in China; city-clusters more effective & efficient

▪ Brands remain important, but loyalty is falling; moreover loyalty is largely to a suite of brands rather than a single brand

▪ While some consumers are upgrading, a majority are “trading-off”to manage their share of wallet

Chinese market & consumers

Continued macroeconomic resilience

▪ Macroeconomic fundamentals remain strong

▪ Continued drive towards urbanization results in majority of economic activity to be concentrated in urban centers

▪ The explosive growth of internet is causing significant shifts in lifestyles, research process and purchase channels in China & India

▪ Consumers are turning into “smart-shoppers” at accelerated pace