del moral-penev - stochastic processes from applications

TRANSCRIPT

Stochastic Processes

From Applications to Theory

CHAPMAN & HA LL/CRC Texts in Statis tical Sc ience Se riesSeries EditorsFrancesca D ominici, Harvard Sc hool of Public H ealth, U SAJulian J . F araway, University of Bath, U KMartin Tanner, N orthwestern U niversity, U SAJim Zide k, U niversity of Br itish C olumbia, C anada

Statistical !eory: A Concise Introduction F. Abramovich and Y. Ritov Practical Multivariate Analysis, Fifth EditionA. A!!, S. May, and V.A. ClarkPractical Statistics for Medical ResearchD.G. AltmanInterpreting Data: A First Course in StatisticsA.J.B. AndersonIntroduction to Probability with R K. BaclawskiLinear Algebra and Matrix Analysis for StatisticsS. Banerjee and A. RoyMathematical Statistics: Basic Ideas and Selected Topics, Volume I, Second EditionP. J. Bickel and K. A. DoksumMathematical Statistics: Basic Ideas and Selected Topics, Volume IIP. J. Bickel and K. A. DoksumAnalysis of Categorical Data with RC. R. Bilder and T. M. LoughinStatistical Methods for SPC and TQMD. BissellIntroduction to ProbabilityJ. K. Blitzstein and J. HwangBayesian Methods for Data Analysis, !ird Edition B.P. Carlin and T.A. LouisSecond EditionR. Caulcutt!e Analysis of Time Series: An Introduction, Sixth Edition C. Chat!eld Introduction to Multivariate Analysis C. Chat!eld and A.J. Collins Problem Solving: A Statistician’s Guide, Second Edition C. Chat!eld

Statistics for Technology: A Course in Applied Statistics, !ird EditionC. Chat!eldAnalysis of Variance, Design, and Regression : Linear Modeling for Unbalanced Data, Second Edition R. ChristensenBayesian Ideas and Data Analysis: An Introduction for Scientists and Statisticians R. Christensen, W. Johnson, A. Branscum, and T.E. HansonModelling Binary Data, Second EditionD. CollettModelling Survival Data in Medical Research, !ird EditionD. CollettIntroduction to Statistical Methods for Clinical Trials T.D. Cook and D.L. DeMets Applied Statistics: Principles and Examples D.R. Cox and E.J. SnellMultivariate Survival Analysis and Competing RisksM. CrowderStatistical Analysis of Reliability DataM.J. Crowder, A.C. Kimber, T.J. Sweeting, and R.L. SmithAn Introduction to Generalized Linear Models, !ird EditionA.J. Dobson and A.G. BarnettNonlinear Time Series: !eory, Methods, and Applications with R ExamplesR. Douc, E. Moulines, and D.S. Sto"erIntroduction to Optimization Methods and !eir Applications in Statistics B.S. EverittExtending the Linear Model with R: Generalized Linear, Mixed E"ects and Nonparametric Regression Models, Second EditionJ.J. Faraway

Linear Models with R, Second EditionJ.J. FarawayA Course in Large Sample !eoryT.S. FergusonMultivariate Statistics: A Practical ApproachB. Flury and H. RiedwylReadings in Decision Analysis S. FrenchDiscrete Data Analysis with R: Visualization and Modeling Techniques for Categorical and Count Data M. Friendly and D. MeyerMarkov Chain Monte Carlo: Stochastic Simulation for Bayesian Inference, Second EditionD. Gamerman and H.F. LopesBayesian Data Analysis, !ird Edition A. Gelman, J.B. Carlin, H.S. Stern, D.B. Dunson, A. Vehtari, and D.B. RubinMultivariate Analysis of Variance and Repeated Measures: A Practical Approach for Behavioural ScientistsD.J. Hand and C.C. TaylorPractical Longitudinal Data AnalysisD.J. Hand and M. CrowderLogistic Regression Models J.M. Hilbe Richly Parameterized Linear Models: Additive, Time Series, and Spatial Models Using Random E"ects J.S. Hodges Statistics for Epidemiology N.P. JewellStochastic Processes: An Introduction, Second EditionP.W. Jones and P. Smith !e !eory of Linear ModelsB. JørgensenPragmatics of UncertaintyJ.B. KadanePrinciples of UncertaintyJ.B. KadaneGraphics for Statistics and Data Analysis with RK.J. KeenMathematical Statistics K. Knight Introduction to Multivariate Analysis: Linear and Nonlinear ModelingS. Konishi

Nonparametric Methods in Statistics with SAS ApplicationsO. KorostelevaModeling and Analysis of Stochastic Systems, Second EditionV.G. KulkarniExercises and Solutions in Biostatistical !eoryL.L. Kupper, B.H. Neelon, and S.M. O’BrienExercises and Solutions in Statistical !eoryL.L. Kupper, B.H. Neelon, and S.M. O’BrienDesign and Analysis of Experiments with RJ. LawsonDesign and Analysis of Experiments with SASJ. LawsonA Course in Categorical Data Analysis T. Leonard Statistics for AccountantsS. LetchfordIntroduction to the !eory of Statistical Inference H. Liero and S. ZwanzigStatistical !eory, Fourth EditionB.W. Lindgren Stationary Stochastic Processes: !eory and Applications G. LindgrenStatistics for Finance E. Lindström, H. Madsen, and J. N. Nielsen!e BUGS Book: A Practical Introduction to Bayesian Analysis D. Lunn, C. Jackson, N. Best, A. #omas, and D. SpiegelhalterIntroduction to General and Generalized Linear ModelsH. Madsen and P. #yregodTime Series AnalysisH. MadsenPólya Urn ModelsH. MahmoudRandomization, Bootstrap and Monte Carlo Methods in Biology, !ird Edition B.F.J. ManlyIntroduction to Randomized Controlled Clinical Trials, Second Edition J.N.S. MatthewsStatistical Rethinking: A Bayesian Course with Examples in R and Stan R. McElreath

Statistical Methods in Agriculture and Experimental Biology, Second EditionR. Mead, R.N. Curnow, and A.M. HastedStatistics in Engineering: A Practical ApproachA.V. MetcalfeStatistical Inference: An Integrated Approach, Second EditionH. S. Migon, D. Gamerman, and F. LouzadaBeyond ANOVA: Basics of Applied Statistics R.G. Miller, Jr.A Primer on Linear ModelsJ.F. MonahanStochastic Processes: From Applications to !eoryP.D Moral and S. PenevApplied Stochastic Modelling, Second Edition B.J.T. MorganElements of Simulation B.J.T. MorganProbability: Methods and MeasurementA. O’HaganIntroduction to Statistical Limit !eoryA.M. PolanskyApplied Bayesian Forecasting and Time Series AnalysisA. Pole, M. West, and J. HarrisonStatistics in Research and Development, Time Series: Modeling, Computation, and InferenceR. Prado and M. WestEssentials of Probability !eory for Statisticians M.A. Proschan and P.A. ShawIntroduction to Statistical Process Control P. Qiu Sampling Methodologies with Applications P.S.R.S. RaoA First Course in Linear Model !eoryN. Ravishanker and D.K. DeyEssential Statistics, Fourth Edition D.A.G. ReesStochastic Modeling and Mathematical Statistics: A Text for Statisticians and Quantitative ScientistsF.J. Samaniego Statistical Methods for Spatial Data AnalysisO. Schabenberger and C.A. Gotway

Bayesian Networks: With Examples in RM. Scutari and J.-B. DenisLarge Sample Methods in StatisticsP.K. Sen and J. da Motta SingerSpatio-Temporal Methods in Environmental EpidemiologyG. Shaddick and J.V. ZidekDecision Analysis: A Bayesian ApproachJ.Q. SmithAnalysis of Failure and Survival DataP. J. SmithApplied Statistics: Handbook of GENSTAT Analyses E.J. Snell and H. Simpson Applied Nonparametric Statistical Methods, Fourth Edition P. Sprent and N.C. SmeetonData Driven Statistical Methods P. Sprent Generalized Linear Mixed Models: Modern Concepts, Methods and ApplicationsW. W. StroupSurvival Analysis Using S: Analysis of Time-to-Event DataM. Tableman and J.S. KimApplied Categorical and Count Data Analysis W. Tang, H. He, and X.M. Tu Elementary Applications of Probability !eory, Second Edition H.C. TuckwellIntroduction to Statistical Inference and Its Applications with R M.W. Trosset Understanding Advanced Statistical MethodsP.H. Westfall and K.S.S. HenningStatistical Process Control: !eory and Practice, !ird Edition G.B. Wetherill and D.W. BrownGeneralized Additive Models: An Introduction with RS. WoodEpidemiology: Study Design and Data Analysis, !ird EditionM. WoodwardPractical Data Analysis for Designed ExperimentsB.S. Yandell

Texts in Statistical Science

Pierre Del MoralUniversity of New South Wales

Sydney, Australia and

INRIA Sud Ouest Research Center Bordeaux, France

Spiridon PenevUniversity of New South Wales

Sydney, Australia

With illustrations by Timothée Del Moral

Stochastic Processes

From Applications to Theory

CRC PressTaylor & Francis Group6000 Broken Sound Parkway NW, Suite 300Boca Raton, FL 33487-2742

© 2014 by Taylor & Francis Group, LLCCRC Press is an imprint of Taylor & Francis Group, an Informa business

No claim to original U.S. Government works

Printed on acid-free paperVersion Date: 20161005

International Standard Book Number-13: 978-1-4987-0183-9 (Hardback)

!is book contains information obtained from authentic and highly regarded sources. Reasonable e"orts have been made to publish reliable data and information, but the author and publisher cannot assume responsibility for the valid-ity of all materials or the consequences of their use. !e authors and publishers have attempted to trace the copyright holders of all material reproduced in this publication and apologize to copyright holders if permission to publish in this form has not been obtained. If any copyright material has not been acknowledged please write and let us know so we may rectify in any future reprint.

Except as permitted under U.S. Copyright Law, no part of this book may be reprinted, reproduced, transmitted, or uti-lized in any form by any electronic, mechanical, or other means, now known or hereafter invented, including photocopy-ing, micro#lming, and recording, or in any information storage or retrieval system, without written permission from the publishers.

For permission to photocopy or use material electronically from this work, please access www.copyright.com (http://www.copyright.com/) or contact the Copyright Clearance Center, Inc. (CCC), 222 Rosewood Drive, Danvers, MA 01923, 978-750-8400. CCC is a not-for-pro#t organization that provides licenses and registration for a variety of users. For organizations that have been granted a photocopy license by the CCC, a separate system of payment has been arranged.

Trademark Notice: Product or corporate names may be trademarks or registered trademarks, and are used only for identi#cation and explanation without intent to infringe.Visit the Taylor & Francis Web site athttp://www.taylorandfrancis.comand the CRC Press Web site athttp://www.crcpress.com

To Laurence, Tiffany and Timothée;to Tatiana, Iva and Alexander.

Contents

Introduction xxi

I An illustrated guide 1

1 Motivating examples 31.1 Lost in the Great Sloan Wall . . . . . . . . . . . . . . . . . . . . . . . . . . 31.2 Meeting Alice in Wonderland . . . . . . . . . . . . . . . . . . . . . . . . . 61.3 The lucky MIT Blackjack Team . . . . . . . . . . . . . . . . . . . . . . . . 71.4 Kruskal’s magic trap card . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101.5 The magic fern from Daisetsuzan . . . . . . . . . . . . . . . . . . . . . . . 121.6 The Kepler-22b Eve . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151.7 Poisson’s typos . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171.8 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

2 Selected topics 252.1 Stabilizing populations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252.2 The traps of reinforcement . . . . . . . . . . . . . . . . . . . . . . . . . . . 282.3 Casino roulette . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 312.4 Surfing Google’s waves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342.5 Pinging hackers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 362.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3 Computational and theoretical aspects 433.1 From Monte Carlo to Los Alamos . . . . . . . . . . . . . . . . . . . . . . . 433.2 Signal processing and population dynamics . . . . . . . . . . . . . . . . . . 453.3 The lost equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 493.4 Towards a general theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563.5 The theory of speculation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 603.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

II Stochastic simulation 69

4 Simulation toolbox 714.1 Inversion technique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 714.2 Change of variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 744.3 Rejection techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 754.4 Sampling probabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

4.4.1 Bayesian inference . . . . . . . . . . . . . . . . . . . . . . . . . . . . 774.4.2 Laplace’s rule of successions . . . . . . . . . . . . . . . . . . . . . . . 794.4.3 Fragmentation and coagulation . . . . . . . . . . . . . . . . . . . . . 79

4.5 Conditional probabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . 804.5.1 Bayes’ formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 804.5.2 The regression formula . . . . . . . . . . . . . . . . . . . . . . . . . . 81

ix

x Contents

4.5.3 Gaussian updates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 824.5.4 Conjugate priors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

4.6 Spatial Poisson point processes . . . . . . . . . . . . . . . . . . . . . . . . . 854.6.1 Some preliminary results . . . . . . . . . . . . . . . . . . . . . . . . . 854.6.2 Conditioning principles . . . . . . . . . . . . . . . . . . . . . . . . . 884.6.3 Poisson-Gaussian clusters . . . . . . . . . . . . . . . . . . . . . . . . 91

4.7 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

5 Monte Carlo integration 995.1 Law of large numbers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 995.2 Importance sampling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

5.2.1 Twisted distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . 1025.2.2 Sequential Monte Carlo . . . . . . . . . . . . . . . . . . . . . . . . . 1025.2.3 Tails distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

5.3 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

6 Some illustrations 1076.1 Stochastic processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1076.2 Markov chain models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1086.3 Black-box type models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1086.4 Boltzmann-Gibbs measures . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

6.4.1 Ising model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1106.4.2 Sherrington-Kirkpatrick model . . . . . . . . . . . . . . . . . . . . . 1116.4.3 The traveling salesman model . . . . . . . . . . . . . . . . . . . . . . 111

6.5 Filtering and statistical learning . . . . . . . . . . . . . . . . . . . . . . . . 1136.5.1 Bayes’ formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1136.5.2 Singer’s radar model . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

6.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

III Discrete time processes 119

7 Markov chains 1217.1 Description of the models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1217.2 Elementary transitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1227.3 Markov integral operators . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1237.4 Equilibrium measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1247.5 Stochastic matrices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1257.6 Random dynamical systems . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

7.6.1 Linear Markov chain model . . . . . . . . . . . . . . . . . . . . . . . 1267.6.2 Two-states Markov models . . . . . . . . . . . . . . . . . . . . . . . 127

7.7 Transition diagrams . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1287.8 The tree of outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1287.9 General state space models . . . . . . . . . . . . . . . . . . . . . . . . . . . 1297.10 Nonlinear Markov chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

7.10.1 Self interacting processes . . . . . . . . . . . . . . . . . . . . . . . . 1327.10.2 Mean field particle models . . . . . . . . . . . . . . . . . . . . . . . . 1347.10.3 McKean-Vlasov diffusions . . . . . . . . . . . . . . . . . . . . . . . . 1357.10.4 Interacting jump processes . . . . . . . . . . . . . . . . . . . . . . . 136

7.11 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

Contents xi

8 Analysis toolbox 1418.1 Linear algebra . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141

8.1.1 Diagonalisation type techniques . . . . . . . . . . . . . . . . . . . . . 1418.1.2 Perron Frobenius theorem . . . . . . . . . . . . . . . . . . . . . . . . 143

8.2 Functional analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1458.2.1 Spectral decompositions . . . . . . . . . . . . . . . . . . . . . . . . . 1458.2.2 Total variation norms . . . . . . . . . . . . . . . . . . . . . . . . . . 1498.2.3 Contraction inequalities . . . . . . . . . . . . . . . . . . . . . . . . . 1528.2.4 Poisson equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1568.2.5 V-norms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1568.2.6 Geometric drift conditions . . . . . . . . . . . . . . . . . . . . . . . . 1608.2.7 V -norm contractions . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

8.3 Stochastic analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1668.3.1 Coupling techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . 166

8.3.1.1 The total variation distance . . . . . . . . . . . . . . . . . . 1668.3.1.2 Wasserstein metric . . . . . . . . . . . . . . . . . . . . . . . 169

8.3.2 Stopping times and coupling . . . . . . . . . . . . . . . . . . . . . . 1728.3.3 Strong stationary times . . . . . . . . . . . . . . . . . . . . . . . . . 1738.3.4 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

8.3.4.1 Minorization condition and coupling . . . . . . . . . . . . . 1748.3.4.2 Markov chains on complete graphs . . . . . . . . . . . . . . 1768.3.4.3 A Kruskal random walk . . . . . . . . . . . . . . . . . . . . 177

8.4 Martingales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1788.4.1 Some preliminaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1788.4.2 Applications to Markov chains . . . . . . . . . . . . . . . . . . . . . 183

8.4.2.1 Martingales with fixed terminal values . . . . . . . . . . . . 1838.4.2.2 Doeblin-Ito formula . . . . . . . . . . . . . . . . . . . . . . 1848.4.2.3 Occupation measures . . . . . . . . . . . . . . . . . . . . . 185

8.4.3 Optional stopping theorems . . . . . . . . . . . . . . . . . . . . . . . 1878.4.4 A gambling model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 191

8.4.4.1 Fair games . . . . . . . . . . . . . . . . . . . . . . . . . . . 1928.4.4.2 Unfair games . . . . . . . . . . . . . . . . . . . . . . . . . . 193

8.4.5 Maximal inequalities . . . . . . . . . . . . . . . . . . . . . . . . . . . 1948.4.6 Limit theorems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

8.5 Topological aspects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2038.5.1 Irreducibility and aperiodicity . . . . . . . . . . . . . . . . . . . . . . 2038.5.2 Recurrent and transient states . . . . . . . . . . . . . . . . . . . . . 2068.5.3 Continuous state spaces . . . . . . . . . . . . . . . . . . . . . . . . . 2108.5.4 Path space models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 211

8.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212

9 Computational toolbox 2219.1 A weak ergodic theorem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2219.2 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 224

9.2.1 Parameter estimation . . . . . . . . . . . . . . . . . . . . . . . . . . 2249.2.2 Gaussian subset shaker . . . . . . . . . . . . . . . . . . . . . . . . . 2259.2.3 Exploration of the unit disk . . . . . . . . . . . . . . . . . . . . . . . 226

9.3 Markov Chain Monte Carlo methods . . . . . . . . . . . . . . . . . . . . . 2269.3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2269.3.2 Metropolis and Hastings models . . . . . . . . . . . . . . . . . . . . 2279.3.3 Gibbs-Glauber dynamics . . . . . . . . . . . . . . . . . . . . . . . . . 229

xii Contents

9.3.4 Propp and Wilson sampler . . . . . . . . . . . . . . . . . . . . . . . 2339.4 Time inhomogeneous MCMC models . . . . . . . . . . . . . . . . . . . . . 236

9.4.1 Simulated annealing algorithm . . . . . . . . . . . . . . . . . . . . . 2369.4.2 A perfect sampling algorithm . . . . . . . . . . . . . . . . . . . . . . 237

9.5 Feynman-Kac path integration . . . . . . . . . . . . . . . . . . . . . . . . . 2399.5.1 Weighted Markov chains . . . . . . . . . . . . . . . . . . . . . . . . . 2399.5.2 Evolution equations . . . . . . . . . . . . . . . . . . . . . . . . . . . 2409.5.3 Particle absorption models . . . . . . . . . . . . . . . . . . . . . . . 2429.5.4 Doob h-processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2449.5.5 Quasi-invariant measures . . . . . . . . . . . . . . . . . . . . . . . . 2459.5.6 Cauchy problems with terminal conditions . . . . . . . . . . . . . . . 2479.5.7 Dirichlet-Poisson problems . . . . . . . . . . . . . . . . . . . . . . . 2489.5.8 Cauchy-Dirichlet-Poisson problems . . . . . . . . . . . . . . . . . . . 250

9.6 Feynman-Kac particle methodology . . . . . . . . . . . . . . . . . . . . . . 2529.6.1 Mean field genetic type particle models . . . . . . . . . . . . . . . . 2529.6.2 Path space models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2549.6.3 Backward integration . . . . . . . . . . . . . . . . . . . . . . . . . . 2559.6.4 A random particle matrix model . . . . . . . . . . . . . . . . . . . . 2579.6.5 A conditional formula for ancestral trees . . . . . . . . . . . . . . . . 258

9.7 Particle Markov chain Monte Carlo methods . . . . . . . . . . . . . . . . . 2609.7.1 Many-body Feynman-Kac measures . . . . . . . . . . . . . . . . . . 2609.7.2 A particle Metropolis-Hastings model . . . . . . . . . . . . . . . . . 2619.7.3 Duality formulae for many-body models . . . . . . . . . . . . . . . . 2629.7.4 A couple particle Gibbs samplers . . . . . . . . . . . . . . . . . . . . 266

9.8 Quenched and annealed measures . . . . . . . . . . . . . . . . . . . . . . . 2679.8.1 Feynman-Kac models . . . . . . . . . . . . . . . . . . . . . . . . . . 2679.8.2 Particle Gibbs models . . . . . . . . . . . . . . . . . . . . . . . . . . 2699.8.3 Particle Metropolis-Hastings models . . . . . . . . . . . . . . . . . . 271

9.9 Some application domains . . . . . . . . . . . . . . . . . . . . . . . . . . . 2729.9.1 Interacting MCMC algorithms . . . . . . . . . . . . . . . . . . . . . 2729.9.2 Nonlinear filtering models . . . . . . . . . . . . . . . . . . . . . . . . 2769.9.3 Markov chain restrictions . . . . . . . . . . . . . . . . . . . . . . . . 2769.9.4 Self avoiding walks . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2779.9.5 Twisted measure importance sampling . . . . . . . . . . . . . . . . . 2799.9.6 Kalman-Bucy filters . . . . . . . . . . . . . . . . . . . . . . . . . . . 280

9.9.6.1 Forward filters . . . . . . . . . . . . . . . . . . . . . . . . . 2809.9.6.2 Backward filters . . . . . . . . . . . . . . . . . . . . . . . . 2819.9.6.3 Ensemble Kalman filters . . . . . . . . . . . . . . . . . . . 2839.9.6.4 Interacting Kalman filters . . . . . . . . . . . . . . . . . . . 285

9.10 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 286

IV Continuous time processes 297

10 Poisson processes 29910.1 A counting process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29910.2 Memoryless property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30010.3 Uniform random times . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30110.4 Doeblin-Ito formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30210.5 Bernoulli process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30410.6 Time inhomogeneous models . . . . . . . . . . . . . . . . . . . . . . . . . . 306

10.6.1 Description of the models . . . . . . . . . . . . . . . . . . . . . . . . 306

Contents xiii

10.6.2 Poisson thinning simulation . . . . . . . . . . . . . . . . . . . . . . . 30910.6.3 Geometric random clocks . . . . . . . . . . . . . . . . . . . . . . . . 309

10.7 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311

11 Markov chain embeddings 31311.1 Homogeneous embeddings . . . . . . . . . . . . . . . . . . . . . . . . . . . 313

11.1.1 Description of the models . . . . . . . . . . . . . . . . . . . . . . . . 31311.1.2 Semigroup evolution equations . . . . . . . . . . . . . . . . . . . . . 314

11.2 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31711.2.1 A two-state Markov process . . . . . . . . . . . . . . . . . . . . . . . 31711.2.2 Matrix valued equations . . . . . . . . . . . . . . . . . . . . . . . . . 31811.2.3 Discrete Laplacian . . . . . . . . . . . . . . . . . . . . . . . . . . . . 320

11.3 Spatially inhomogeneous models . . . . . . . . . . . . . . . . . . . . . . . . 32211.3.1 Explosion phenomenon . . . . . . . . . . . . . . . . . . . . . . . . . . 32411.3.2 Finite state space models . . . . . . . . . . . . . . . . . . . . . . . . 328

11.4 Time inhomogeneous models . . . . . . . . . . . . . . . . . . . . . . . . . . 32911.4.1 Description of the models . . . . . . . . . . . . . . . . . . . . . . . . 32911.4.2 Poisson thinning models . . . . . . . . . . . . . . . . . . . . . . . . . 33111.4.3 Exponential and geometric clocks . . . . . . . . . . . . . . . . . . . . 332

11.5 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 332

12 Jump processes 33712.1 A class of pure jump models . . . . . . . . . . . . . . . . . . . . . . . . . . 33712.2 Semigroup evolution equations . . . . . . . . . . . . . . . . . . . . . . . . . 33812.3 Approximation schemes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34012.4 Sum of generators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34212.5 Doob-Meyer decompositions . . . . . . . . . . . . . . . . . . . . . . . . . . 344

12.5.1 Discrete time models . . . . . . . . . . . . . . . . . . . . . . . . . . . 34412.5.2 Continuous time martingales . . . . . . . . . . . . . . . . . . . . . . 34612.5.3 Optional stopping theorems . . . . . . . . . . . . . . . . . . . . . . . 349

12.6 Doeblin-Ito-Taylor formulae . . . . . . . . . . . . . . . . . . . . . . . . . . 35012.7 Stability properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 351

12.7.1 Invariant measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35112.7.2 Dobrushin contraction properties . . . . . . . . . . . . . . . . . . . . 353

12.8 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 356

13 Piecewise deterministic processes 36313.1 Dynamical systems basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363

13.1.1 Semigroup and flow maps . . . . . . . . . . . . . . . . . . . . . . . . 36313.1.2 Time discretization schemes . . . . . . . . . . . . . . . . . . . . . . . 366

13.2 Piecewise deterministic jump models . . . . . . . . . . . . . . . . . . . . . . 36713.2.1 Excursion valued Markov chains . . . . . . . . . . . . . . . . . . . . 36713.2.2 Evolution semigroups . . . . . . . . . . . . . . . . . . . . . . . . . . 36913.2.3 Infinitesimal generators . . . . . . . . . . . . . . . . . . . . . . . . . 37113.2.4 Fokker-Planck equation . . . . . . . . . . . . . . . . . . . . . . . . . 37213.2.5 A time discretization scheme . . . . . . . . . . . . . . . . . . . . . . 37313.2.6 Doeblin-Ito-Taylor formulae . . . . . . . . . . . . . . . . . . . . . . . 376

13.3 Stability properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37713.3.1 Switching processes . . . . . . . . . . . . . . . . . . . . . . . . . . . 37713.3.2 Invariant measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . 379

13.4 An application to Internet architectures . . . . . . . . . . . . . . . . . . . . 379

xiv Contents

13.4.1 The transmission control protocol . . . . . . . . . . . . . . . . . . . 37913.4.2 Regularity and stability properties . . . . . . . . . . . . . . . . . . . 38113.4.3 The limiting distribution . . . . . . . . . . . . . . . . . . . . . . . . 383

13.5 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 384

14 Diffusion processes 39314.1 Brownian motion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 393

14.1.1 Discrete vs continuous time models . . . . . . . . . . . . . . . . . . . 39314.1.2 Evolution semigroups . . . . . . . . . . . . . . . . . . . . . . . . . . 39514.1.3 The heat equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39714.1.4 Doeblin-Ito-Taylor formula . . . . . . . . . . . . . . . . . . . . . . . 398

14.2 Stochastic differential equations . . . . . . . . . . . . . . . . . . . . . . . . 40114.2.1 Diffusion processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40114.2.2 Doeblin-Ito differential calculus . . . . . . . . . . . . . . . . . . . . . 402

14.3 Evolution equations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40514.3.1 Fokker-Planck equation . . . . . . . . . . . . . . . . . . . . . . . . . 40514.3.2 Weak approximation processes . . . . . . . . . . . . . . . . . . . . . 40614.3.3 A backward stochastic differential equation . . . . . . . . . . . . . . 408

14.4 Multidimensional diffusions . . . . . . . . . . . . . . . . . . . . . . . . . . . 40914.4.1 Multidimensional stochastic differential equations . . . . . . . . . . . 40914.4.2 An integration by parts formula . . . . . . . . . . . . . . . . . . . . 41114.4.3 Laplacian and orthogonal transformations . . . . . . . . . . . . . . . 41214.4.4 Fokker-Planck equation . . . . . . . . . . . . . . . . . . . . . . . . . 413

14.5 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 413

15 Jump diffusion processes 42515.1 Piecewise diffusion processes . . . . . . . . . . . . . . . . . . . . . . . . . . 42515.2 Evolution semigroups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42615.3 Doeblin-Ito formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42815.4 Fokker-Planck equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43315.5 An abstract class of stochastic processes . . . . . . . . . . . . . . . . . . . . 434

15.5.1 Generators and carré du champ operators . . . . . . . . . . . . . . . 43415.5.2 Perturbation formulae . . . . . . . . . . . . . . . . . . . . . . . . . . 437

15.6 Jump diffusion processes with killing . . . . . . . . . . . . . . . . . . . . . 43915.6.1 Feynman-Kac semigroups . . . . . . . . . . . . . . . . . . . . . . . . 43915.6.2 Cauchy problems with terminal conditions . . . . . . . . . . . . . . . 44015.6.3 Dirichlet-Poisson problems . . . . . . . . . . . . . . . . . . . . . . . 44215.6.4 Cauchy-Dirichlet-Poisson problems . . . . . . . . . . . . . . . . . . . 447

15.7 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45015.7.1 One-dimensional Dirichlet-Poisson problems . . . . . . . . . . . . . . 45015.7.2 A backward stochastic differential equation . . . . . . . . . . . . . . 451

15.8 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 451

16 Nonlinear jump diffusion processes 46316.1 Nonlinear Markov processes . . . . . . . . . . . . . . . . . . . . . . . . . . 463

16.1.1 Pure diffusion models . . . . . . . . . . . . . . . . . . . . . . . . . . 46316.1.2 Burgers equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46416.1.3 Feynman-Kac jump type models . . . . . . . . . . . . . . . . . . . . 46616.1.4 A jump type Langevin model . . . . . . . . . . . . . . . . . . . . . . 467

16.2 Mean field particle models . . . . . . . . . . . . . . . . . . . . . . . . . . . 46816.3 Some application domains . . . . . . . . . . . . . . . . . . . . . . . . . . . 470

Contents xv

16.3.1 Fouque-Sun systemic risk model . . . . . . . . . . . . . . . . . . . . 47016.3.2 Burgers equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47116.3.3 Langevin-McKean-Vlasov model . . . . . . . . . . . . . . . . . . . . 47216.3.4 Dyson equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 473

16.4 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 474

17 Stochastic analysis toolbox 48117.1 Time changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48117.2 Stability properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48217.3 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 483

17.3.1 Gradient flow processes . . . . . . . . . . . . . . . . . . . . . . . . . 48317.3.2 One-dimensional diffusions . . . . . . . . . . . . . . . . . . . . . . . 484

17.4 Foster-Lyapunov techniques . . . . . . . . . . . . . . . . . . . . . . . . . . 48517.4.1 Contraction inequalities . . . . . . . . . . . . . . . . . . . . . . . . . 48517.4.2 Minorization properties . . . . . . . . . . . . . . . . . . . . . . . . . 486

17.5 Some applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48717.5.1 Ornstein-Uhlenbeck processes . . . . . . . . . . . . . . . . . . . . . . 48717.5.2 Stochastic gradient processes . . . . . . . . . . . . . . . . . . . . . . 48717.5.3 Langevin diffusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 488

17.6 Spectral analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49017.6.1 Hilbert spaces and Schauder bases . . . . . . . . . . . . . . . . . . . 49017.6.2 Spectral decompositions . . . . . . . . . . . . . . . . . . . . . . . . . 49317.6.3 Poincaré inequality . . . . . . . . . . . . . . . . . . . . . . . . . . . . 494

17.7 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 495

18 Path space measures 50118.1 Pure jump models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 501

18.1.1 Likelihood functionals . . . . . . . . . . . . . . . . . . . . . . . . . . 50418.1.2 Girsanov’s transformations . . . . . . . . . . . . . . . . . . . . . . . 50518.1.3 Exponential martingales . . . . . . . . . . . . . . . . . . . . . . . . . 506

18.2 Diffusion models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50718.2.1 Wiener measure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50718.2.2 Path space diffusions . . . . . . . . . . . . . . . . . . . . . . . . . . . 50818.2.3 Girsanov transformations . . . . . . . . . . . . . . . . . . . . . . . . 509

18.3 Exponential change twisted measures . . . . . . . . . . . . . . . . . . . . . 51218.3.1 Diffusion processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51318.3.2 Pure jump processes . . . . . . . . . . . . . . . . . . . . . . . . . . . 514

18.4 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51418.4.1 Risk neutral financial markets . . . . . . . . . . . . . . . . . . . . . . 514

18.4.1.1 Poisson markets . . . . . . . . . . . . . . . . . . . . . . . . 51418.4.1.2 Diffusion markets . . . . . . . . . . . . . . . . . . . . . . . 515

18.4.2 Elliptic diffusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51618.5 Nonlinear filtering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 517

18.5.1 Diffusion observations . . . . . . . . . . . . . . . . . . . . . . . . . . 51718.5.2 Duncan-Zakai equation . . . . . . . . . . . . . . . . . . . . . . . . . 51818.5.3 Kushner-Stratonovitch equation . . . . . . . . . . . . . . . . . . . . 52018.5.4 Kalman-Bucy filters . . . . . . . . . . . . . . . . . . . . . . . . . . . 52118.5.5 Nonlinear diffusion and ensemble Kalman-Bucy filters . . . . . . . . 52318.5.6 Robust filtering equations . . . . . . . . . . . . . . . . . . . . . . . . 52418.5.7 Poisson observations . . . . . . . . . . . . . . . . . . . . . . . . . . . 525

18.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 527

xvi Contents

V Processes on manifolds 533

19 A review of differential geometry 53519.1 Projection operators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53519.2 Covariant derivatives of vector fields . . . . . . . . . . . . . . . . . . . . . . 541

19.2.1 First order derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . 54319.2.2 Second order derivatives . . . . . . . . . . . . . . . . . . . . . . . . . 546

19.3 Divergence and mean curvature . . . . . . . . . . . . . . . . . . . . . . . . 54719.4 Lie brackets and commutation formulae . . . . . . . . . . . . . . . . . . . . 55419.5 Inner product derivation formulae . . . . . . . . . . . . . . . . . . . . . . . 55619.6 Second order derivatives and some trace formulae . . . . . . . . . . . . . . 55919.7 Laplacian operator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56219.8 Ricci curvature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56319.9 Bochner-Lichnerowicz formula . . . . . . . . . . . . . . . . . . . . . . . . . 56819.10Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 576

20 Stochastic differential calculus on manifolds 57920.1 Embedded manifolds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57920.2 Brownian motion on manifolds . . . . . . . . . . . . . . . . . . . . . . . . . 581

20.2.1 A diffusion model in the ambient space . . . . . . . . . . . . . . . . 58120.2.2 The infinitesimal generator . . . . . . . . . . . . . . . . . . . . . . . 58320.2.3 Monte Carlo simulation . . . . . . . . . . . . . . . . . . . . . . . . . 584

20.3 Stratonovitch differential calculus . . . . . . . . . . . . . . . . . . . . . . . 58420.4 Projected diffusions on manifolds . . . . . . . . . . . . . . . . . . . . . . . 58620.5 Brownian motion on orbifolds . . . . . . . . . . . . . . . . . . . . . . . . . 58920.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 591

21 Parametrizations and charts 59321.1 Differentiable manifolds and charts . . . . . . . . . . . . . . . . . . . . . . 59321.2 Orthogonal projection operators . . . . . . . . . . . . . . . . . . . . . . . . 59621.3 Riemannian structures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59921.4 First order covariant derivatives . . . . . . . . . . . . . . . . . . . . . . . . 602

21.4.1 Pushed forward functions . . . . . . . . . . . . . . . . . . . . . . . . 60221.4.2 Pushed forward vector fields . . . . . . . . . . . . . . . . . . . . . . . 60421.4.3 Directional derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . 606

21.5 Second order covariant derivative . . . . . . . . . . . . . . . . . . . . . . . 60921.5.1 Tangent basis functions . . . . . . . . . . . . . . . . . . . . . . . . . 60921.5.2 Composition formulae . . . . . . . . . . . . . . . . . . . . . . . . . . 61221.5.3 Hessian operators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 613

21.6 Bochner-Lichnerowicz formula . . . . . . . . . . . . . . . . . . . . . . . . . 61721.7 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 623

22 Stochastic calculus in chart spaces 62922.1 Brownian motion on Riemannian manifolds . . . . . . . . . . . . . . . . . . 62922.2 Diffusions on chart spaces . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63122.3 Brownian motion on spheres . . . . . . . . . . . . . . . . . . . . . . . . . . 632

22.3.1 The unit circle S = S1 ⊂ R2 . . . . . . . . . . . . . . . . . . . . . . . 63222.3.2 The unit sphere S = S2 ⊂ R3 . . . . . . . . . . . . . . . . . . . . . . 633

22.4 Brownian motion on the torus . . . . . . . . . . . . . . . . . . . . . . . . . 63422.5 Diffusions on the simplex . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63522.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 637

Contents xvii

23 Some analytical aspects 63923.1 Geodesics and the exponential map . . . . . . . . . . . . . . . . . . . . . . 63923.2 Taylor expansion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64323.3 Integration on manifolds . . . . . . . . . . . . . . . . . . . . . . . . . . . . 645

23.3.1 The volume measure on the manifold . . . . . . . . . . . . . . . . . . 64523.3.2 Wedge product and volume forms . . . . . . . . . . . . . . . . . . . 64823.3.3 The divergence theorem . . . . . . . . . . . . . . . . . . . . . . . . . 650

23.4 Gradient flow models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65723.4.1 Steepest descent model . . . . . . . . . . . . . . . . . . . . . . . . . 65723.4.2 Euclidian state spaces . . . . . . . . . . . . . . . . . . . . . . . . . . 658

23.5 Drift changes and irreversible Langevin diffusions . . . . . . . . . . . . . . 65923.5.1 Langevin diffusions on closed manifolds . . . . . . . . . . . . . . . . 66123.5.2 Riemannian Langevin diffusions . . . . . . . . . . . . . . . . . . . . . 662

23.6 Metropolis-adjusted Langevin models . . . . . . . . . . . . . . . . . . . . . 66523.7 Stability and some functional inequalities . . . . . . . . . . . . . . . . . . . 66623.8 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 669

24 Some illustrations 67324.1 Prototype manifolds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 673

24.1.1 The circle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67324.1.2 The 2-sphere . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67424.1.3 The torus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 678

24.2 Information theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68124.2.1 Nash embedding theorem . . . . . . . . . . . . . . . . . . . . . . . . 68124.2.2 Distribution manifolds . . . . . . . . . . . . . . . . . . . . . . . . . . 68224.2.3 Bayesian statistical manifolds . . . . . . . . . . . . . . . . . . . . . . 68324.2.4 Cramer-Rao lower bound . . . . . . . . . . . . . . . . . . . . . . . . 68524.2.5 Some illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 685

24.2.5.1 Boltzmann-Gibbs measures . . . . . . . . . . . . . . . . . . 68524.2.5.2 Multivariate normal distributions . . . . . . . . . . . . . . 686

VI Some application areas 691

25 Simple random walks 69325.1 Random walk on lattices . . . . . . . . . . . . . . . . . . . . . . . . . . . . 693

25.1.1 Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69325.1.2 Dimension 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69325.1.3 Dimension 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69425.1.4 Dimension d ≥ 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 694

25.2 Random walks on graphs . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69425.3 Simple exclusion process . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69525.4 Random walks on the circle . . . . . . . . . . . . . . . . . . . . . . . . . . . 695

25.4.1 Markov chain on cycle . . . . . . . . . . . . . . . . . . . . . . . . . . 69525.4.2 Markov chain on circle . . . . . . . . . . . . . . . . . . . . . . . . . . 69625.4.3 Spectral decomposition . . . . . . . . . . . . . . . . . . . . . . . . . 696

25.5 Random walk on hypercubes . . . . . . . . . . . . . . . . . . . . . . . . . . 69725.5.1 Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69725.5.2 A macroscopic model . . . . . . . . . . . . . . . . . . . . . . . . . . 69825.5.3 A lazy random walk . . . . . . . . . . . . . . . . . . . . . . . . . . . 698

25.6 Urn processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69925.6.1 Ehrenfest model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 699

xviii Contents

25.6.2 Pólya urn model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70025.7 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 701

26 Iterated random functions 70526.1 Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70526.2 A motivating example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70726.3 Uniform selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 708

26.3.1 An ancestral type evolution model . . . . . . . . . . . . . . . . . . . 70826.3.2 An absorbed Markov chain . . . . . . . . . . . . . . . . . . . . . . . 709

26.4 Shuffling cards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71226.4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71226.4.2 The top-in-at-random shuffle . . . . . . . . . . . . . . . . . . . . . . 71226.4.3 The random transposition shuffle . . . . . . . . . . . . . . . . . . . . 71326.4.4 The riffle shuffle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 716

26.5 Fractal models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71926.5.1 Exploration of Cantor’s discontinuum . . . . . . . . . . . . . . . . . 72026.5.2 Some fractal images . . . . . . . . . . . . . . . . . . . . . . . . . . . 723

26.6 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 725

27 Computational and statistical physics 73127.1 Molecular dynamics simulation . . . . . . . . . . . . . . . . . . . . . . . . . 731

27.1.1 Newton’s second law of motion . . . . . . . . . . . . . . . . . . . . . 73127.1.2 Langevin diffusion processes . . . . . . . . . . . . . . . . . . . . . . . 734

27.2 Schrödinger equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73727.2.1 A physical derivation . . . . . . . . . . . . . . . . . . . . . . . . . . . 73727.2.2 Feynman-Kac formulation . . . . . . . . . . . . . . . . . . . . . . . . 73927.2.3 Bra-kets and path integral formalism . . . . . . . . . . . . . . . . . . 74227.2.4 Spectral decompositions . . . . . . . . . . . . . . . . . . . . . . . . . 74327.2.5 The harmonic oscillator . . . . . . . . . . . . . . . . . . . . . . . . . 74527.2.6 Diffusion Monte Carlo models . . . . . . . . . . . . . . . . . . . . . . 748

27.3 Interacting particle systems . . . . . . . . . . . . . . . . . . . . . . . . . . . 74927.3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74927.3.2 Contact process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75127.3.3 Voter process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75127.3.4 Exclusion process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 752

27.4 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 753

28 Dynamic population models 75928.1 Discrete time birth and death models . . . . . . . . . . . . . . . . . . . . . 75928.2 Continuous time models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 762

28.2.1 Birth and death generators . . . . . . . . . . . . . . . . . . . . . . . 76228.2.2 Logistic processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76228.2.3 Epidemic model with immunity . . . . . . . . . . . . . . . . . . . . . 76428.2.4 Lotka-Volterra predator-prey stochastic model . . . . . . . . . . . . 76528.2.5 Moran genetic model . . . . . . . . . . . . . . . . . . . . . . . . . . . 768

28.3 Genetic evolution models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76928.4 Branching processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 770

28.4.1 Birth and death models with linear rates . . . . . . . . . . . . . . . 77028.4.2 Discrete time branching processes . . . . . . . . . . . . . . . . . . . 77228.4.3 Continuous time branching processes . . . . . . . . . . . . . . . . . . 773

28.4.3.1 Absorption-death process . . . . . . . . . . . . . . . . . . . 774

Contents xix

28.4.3.2 Birth type branching process . . . . . . . . . . . . . . . . . 77528.4.3.3 Birth and death branching processes . . . . . . . . . . . . . 77728.4.3.4 Kolmogorov-Petrovskii-Piskunov equation . . . . . . . . . . 778

28.5 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 780

29 Gambling, ranking and control 78729.1 Google page rank . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78729.2 Gambling betting systems . . . . . . . . . . . . . . . . . . . . . . . . . . . 788

29.2.1 Martingale systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78829.2.2 St. Petersburg martingales . . . . . . . . . . . . . . . . . . . . . . . 78929.2.3 Conditional gains and losses . . . . . . . . . . . . . . . . . . . . . . . 791

29.2.3.1 Conditional gains . . . . . . . . . . . . . . . . . . . . . . . 79129.2.3.2 Conditional losses . . . . . . . . . . . . . . . . . . . . . . . 791

29.2.4 Bankroll management . . . . . . . . . . . . . . . . . . . . . . . . . . 79229.2.5 Grand martingale . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79429.2.6 D’Alembert martingale . . . . . . . . . . . . . . . . . . . . . . . . . 79429.2.7 Whittacker martingale . . . . . . . . . . . . . . . . . . . . . . . . . . 796

29.3 Stochastic optimal control . . . . . . . . . . . . . . . . . . . . . . . . . . . 79729.3.1 Bellman equations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79729.3.2 Control dependent value functions . . . . . . . . . . . . . . . . . . . 80229.3.3 Continuous time models . . . . . . . . . . . . . . . . . . . . . . . . . 804

29.4 Optimal stopping . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80729.4.1 Games with fixed terminal condition . . . . . . . . . . . . . . . . . . 80729.4.2 Snell envelope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80929.4.3 Continuous time models . . . . . . . . . . . . . . . . . . . . . . . . . 811

29.5 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 812

30 Mathematical finance 82130.1 Stock price models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 821

30.1.1 Up and down martingales . . . . . . . . . . . . . . . . . . . . . . . . 82130.1.2 Cox-Ross-Rubinstein model . . . . . . . . . . . . . . . . . . . . . . . 82430.1.3 Black-Scholes-Merton model . . . . . . . . . . . . . . . . . . . . . . . 825

30.2 European option pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82630.2.1 Call and put options . . . . . . . . . . . . . . . . . . . . . . . . . . . 82630.2.2 Self-financing portfolios . . . . . . . . . . . . . . . . . . . . . . . . . 82730.2.3 Binomial pricing technique . . . . . . . . . . . . . . . . . . . . . . . 82830.2.4 Black-Scholes-Merton pricing model . . . . . . . . . . . . . . . . . . 83030.2.5 Black-Scholes partial differential equation . . . . . . . . . . . . . . . 83130.2.6 Replicating portfolios . . . . . . . . . . . . . . . . . . . . . . . . . . 83230.2.7 Option price and hedging computations . . . . . . . . . . . . . . . . 83330.2.8 A numerical illustration . . . . . . . . . . . . . . . . . . . . . . . . . 834

30.3 Exercises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 835

Bibliography 839

Index 855

0Introduction

A brief discussion on stochastic processesThese lectures deal with the foundations and the applications of stochastic processes alsocalled random processes.

The term "stochastic" comes from the Greek word "stokhastikos" which means a skillfulperson capable of guessing and predicting. The first use of this term in probability theorycan be traced back to the Russian economist and statistician Ladislaus Bortkiewicz (1868-1931). In his paper Die Iterationen published in 1917, he defines the term "stochastik" asfollows: "The investigation of empirical varieties, which is based on probability theory, and,therefore, on the law of the large numbers, may be denoted as stochastic. But stochastic isnot simply probability theory, but above all probability theory and its applications".

As their name indicates, stochastic processes are dynamic evolution models with randomingredients. Leaving aside the old well-known dilemma of determinism and freedom [26, 225](solved by some old fashion scientific reasoning which cannot accommodate any piece ofrandom "un-caused causations"), the complex structure of any "concrete" and sophisticatedreal life model is always better represented by stochastic mathematical models as a first levelof approximation.

The sources of randomness reflect different sources of model uncertainties, includingunknown initial conditions, model uncertainties such as misspecified kinetic parameters, aswell as the external random effects on the system.

Stochastic modelling techniques are of great importance in many scientific areas, toname a few:

• Computer and engineering sciences: signal and image processing, filtering and inverseproblems, stochastic control, game theory, mathematical finance, risk analysis and rareevent simulation, operation research and global optimization, artificial intelligence andevolutionary computing, queueing and communication networks.

• Statistical machine learning: hidden Markov chain models, frequentist and Bayesianstatistical inference.

• Biology and environmental sciences: branching processes, dynamic population models,genetic and genealogical tree-based evolution.

• Physics and chemistry: turbulent fluid models, disordered and quantum models, sta-tistical physics and magnetic models, polymers in solvents, molecular dynamics andSchrödinger equations.

A fairly large body of the literature on stochastic processes is concerned with the prob-abilistic modelling and the convergence analysis of random style dynamical systems. Asexpected these developments are closely related to the theory of dynamical systems, topartial differential and integro-differential equations, but also to ergodic and chaos theory,

xxi

xxii Stochastic Processes

differential geometry, as well as the classical linear algebra theory, combinatorics, topology,operator theory, and spectral analysis.

The theory of stochastic processes has also developed its own sophisticated probabilistictools, including diffusion and jump type stochastic differential equations, Doeblin-Ito calcu-lus, martingale theory, coupling techniques, and advanced stochastic simulation techniques.

One of the objectives of stochastic process theory is to derive explicit analytic type resultsfor a variety of simplified stochastic processes, including birth and death models, simplerandom walks, spatially homogeneous branching processes, and many others. Nevertheless,most of the more realistic processes of interest in the real world of physics, biology, andengineering sciences are "unfortunately" highly nonlinear systems evolving in very highdimensions. As a result, it is generally impossible to come up with any type of closed formsolutions.

In this connection, the theory of stochastic processes is also concerned with the modellingand with the convergence analysis of a variety of sophisticated stochastic algorithms. Thesestochastic processes are designed to solve numerically complex integration problems thatarise in a variety of application areas. Their common feature is to mimic and to use repeatedrandom samples of a given stochastic process to estimate some averaging type property usingempirical approximations.

We emphasize that all of these stochastic methods are expressed in terms of a partic-ular stochastic process, or a collection of stochastic processes, depending on the precisionparameter being the time horizon, or the number of samples. The central idea is to approx-imate the expectation of a given random variable using the empirical averages (in space orin time) based on a sequence of random samples. In this context, the rigorous analysis ofthese complex numerical schemes also relies on advanced stochastic analysis techniques.

The interpretation of the random variables of interest depends on the application. Insome instances, these variables represent the random states of a complex stochastic process,or some unknown kinetic or statistical parameters. In other situations, the random variablesof interest are specified by a complex target probability measure. Stochastic simulation andMonte Carlo methods are used to predict the evolution of given random phenomena, aswell as to solve several estimation problems using random searches. To name but a few:computing complex measures and multidimensional integrals, counting, ranking, and ratingproblems, spectral analysis, computation of eigenvalues and eigenvectors, as well as solvinglinear and nonlinear integro-differential equations.

This book is almost self-contained. There are no strict prerequisites but it is envisagedthat students would have taken a course in elementary probability and that they have someknowledge of elementary linear algebra, functional analysis and geometry. It is not possibleto define rigorously stochastic processes without some basic knowledge on measure theoryand differential calculus. Readers who lack such background should instead consult someintroductory textbook on probability and integration, and elementary differential calculus.

The book also contains around 500 exercises with detailed solutions on a variety oftopics, with many explicit computations. Each chapter ends with a section containing aseries of exercises ranging from simple calculations to more advanced technical questions.This book can serve as a reference book, as well as a textbook. The next section providesa brief description of the organization of the book.

On page xxxii we propose a series of lectures and research projects which can be devel-oped using the material presented in this book. The descriptions of these course projectsalso provide detailed discussions on the connections between the different topics treated inthis book. Thus, they also provide a reading guide to enter into a given specialized topic.

Introduction xxiii

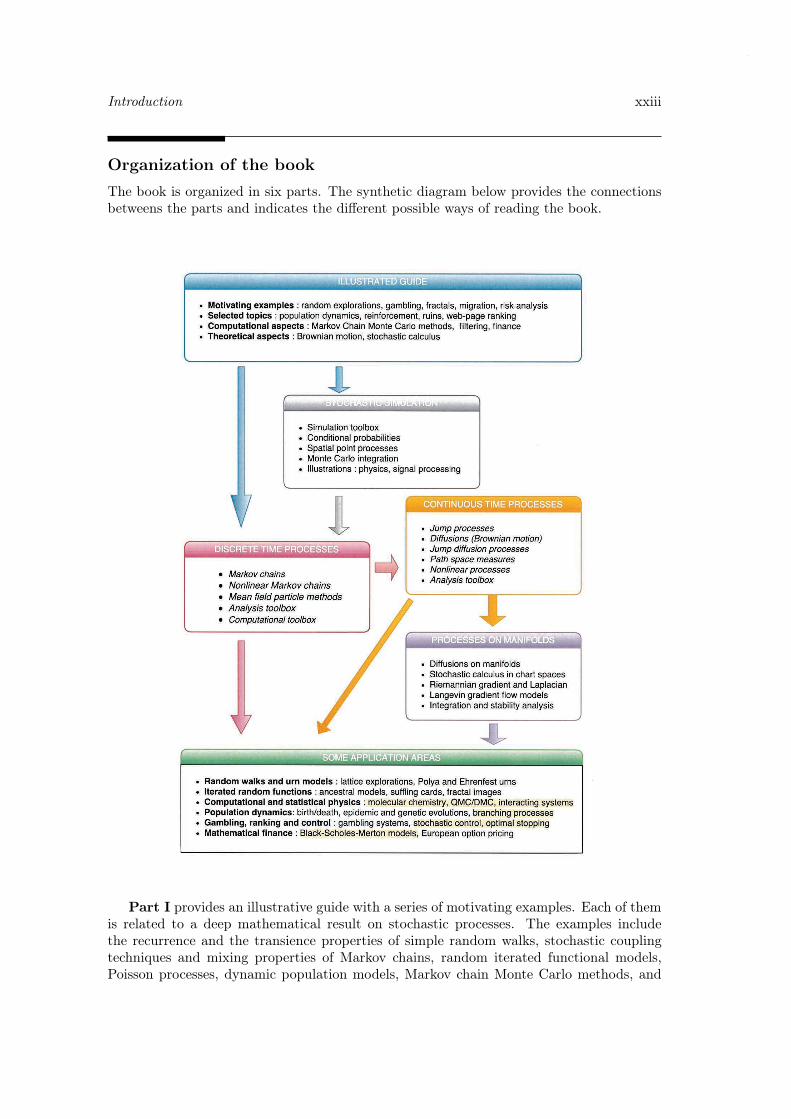

Organization of the bookThe book is organized in six parts. The synthetic diagram below provides the connectionsbetweens the parts and indicates the different possible ways of reading the book.

Part I provides an illustrative guide with a series of motivating examples. Each of themis related to a deep mathematical result on stochastic processes. The examples includethe recurrence and the transience properties of simple random walks, stochastic couplingtechniques and mixing properties of Markov chains, random iterated functional models,Poisson processes, dynamic population models, Markov chain Monte Carlo methods, and

xxiv Stochastic Processes

the Doeblin-Ito differential calculus. In each situation, we provide a brief discussion on themathematical analysis of these models. We also provide precise pointers to the chaptersand sections where these results are discussed in more details.

Part II is concerned with the notion of randomness, and with some techniques to "sim-ulate perfectly" some traditional random variables (abbreviated r.v.). For a more thoroughdiscussion on this subject, we refer to the encyclopedic and seminal reference book of LucDevroye [92], dedicated to the simulation of nonuniform random variables. Several concreteapplications are provided to illustrate many of the key ideas, as well as the usefulness ofstochastic simulation methods in some scientific disciplines.

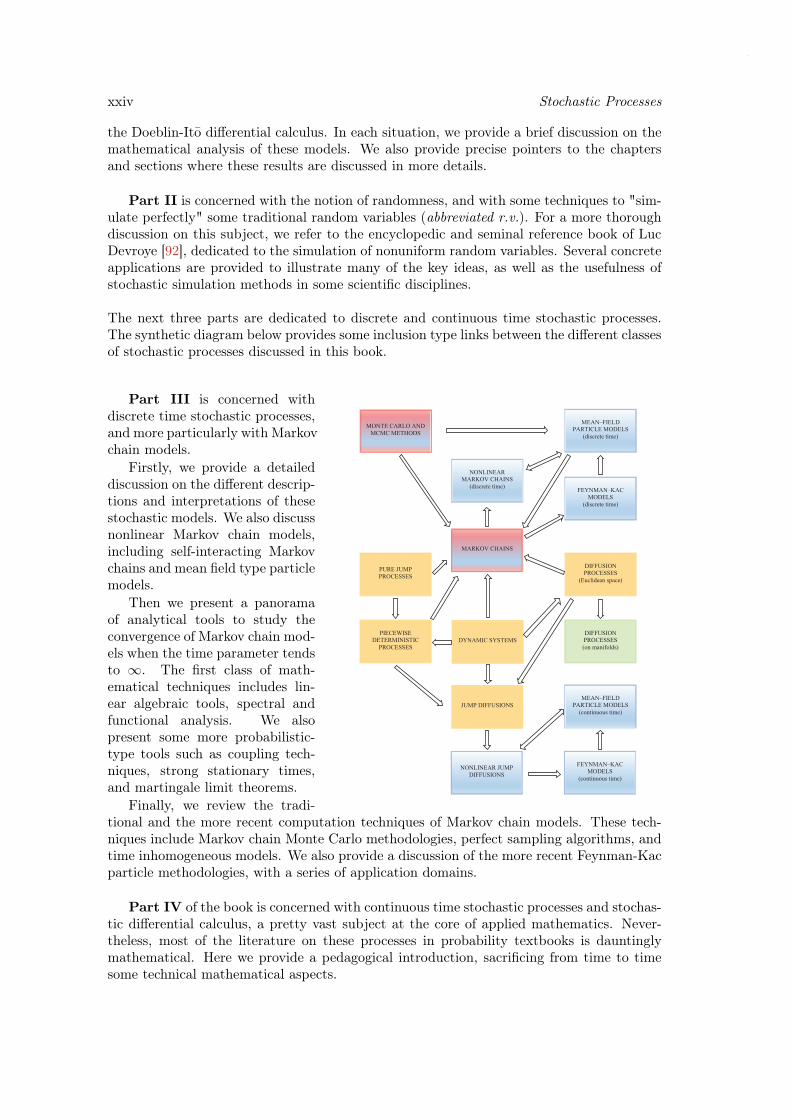

The next three parts are dedicated to discrete and continuous time stochastic processes.The synthetic diagram below provides some inclusion type links between the different classesof stochastic processes discussed in this book.

MONTE CARLO AND MCMC METHODS

MEAN–FIELD PARTICLE MODELS

(discrete time)

MARKOV CHAINS

NONLINEAR MARKOV CHAINS

(discrete time) FEYNMAN–KAC MODELS

(discrete time)

FEYNMAN–KAC MODELS

(continuous time)

MEAN–FIELD PARTICLE MODELS

(continuous time)

NONLINEAR JUMP DIFFUSIONS

DIFFUSION PROCESSES (on manifolds)

JUMP DIFFUSIONS

DYNAMIC SYSTEMS PIECEWISE

DETERMINISTIC PROCESSES

PURE JUMP PROCESSES

DIFFUSION PROCESSES

(Euclidean space)

Part III is concerned withdiscrete time stochastic processes,and more particularly with Markovchain models.

Firstly, we provide a detaileddiscussion on the different descrip-tions and interpretations of thesestochastic models. We also discussnonlinear Markov chain models,including self-interacting Markovchains and mean field type particlemodels.

Then we present a panoramaof analytical tools to study theconvergence of Markov chain mod-els when the time parameter tendsto ∞. The first class of math-ematical techniques includes lin-ear algebraic tools, spectral andfunctional analysis. We alsopresent some more probabilistic-type tools such as coupling tech-niques, strong stationary times,and martingale limit theorems.

Finally, we review the tradi-tional and the more recent computation techniques of Markov chain models. These tech-niques include Markov chain Monte Carlo methodologies, perfect sampling algorithms, andtime inhomogeneous models. We also provide a discussion of the more recent Feynman-Kacparticle methodologies, with a series of application domains.

Part IV of the book is concerned with continuous time stochastic processes and stochas-tic differential calculus, a pretty vast subject at the core of applied mathematics. Never-theless, most of the literature on these processes in probability textbooks is dauntinglymathematical. Here we provide a pedagogical introduction, sacrificing from time to timesome technical mathematical aspects.

Introduction xxv

Continuous time stochastic processes can always be thought as a limit of a discrete gen-eration process defined on some time mesh, as the time step tends to 0. This viewpointwhich is at the foundation of of stochastic calculus and integration is often hidden in purelytheoretical textbooks on stochastic processes. In the reverse angle, more applied presenta-tions found in textbooks in engineering, economy, statistics and physics are often too farfrom recent advances in applied probability so that students are not really prepared to enterinto deeper analysis nor pursue any research level type projects.

One of the main new points we have adopted here is to make a bridge between appli-cations and advanced probability analysis. Continuous time stochastic processes, includingnonlinear jump-diffusion processes, are introduced as a limit of a discrete generation processwhich can be easily simulated on a computer. In the same vein, any sophisticated formulain stochastic analysis and differential calculus arises as the limit of a discrete time mathe-matical model. It is of course not within the scope of this book to quantify precisely andin a systematic way all of these approximations. Precise reference pointers to articles andbooks dealing with these questions are provided in the text.

All approximations treated in this book are developed through a single and systematicmathematical basis transforming the elementary Markov transitions of practical discretegeneration models into infinitesimal generators of continuous time processes. The stochas-tic version of the Taylor expansion, also called the Doeblin-Ito formula or simply the Itoformula, is described in terms of the generator of a Markov process and its correspondingcarré du champ operator.

In this framework, the evolution of the law of the random states of a continuous timeprocess resumes to a natural weak formulation of linear and nonlinear Fokker-Planck typeequations (a.k.a. Kolmogorov equations). In this interpretation, the random paths of a givencontinuous time process provide a natural interpolation and coupling between the solutionsof these integro-differential equations at different times. These path-space probability mea-sures provide natural probabilistic interpretations of important Cauchy-Dirichlet-Poissonproblems arising in analysis and integro-partial differential equation problems. The limit-ing behavior of these functional equations is also directly related to the long time behaviorof a stochastic process.

All of these subjects are developed from chapter 10 to chapter 16. The presentationstarts with elementary Poisson and jump type processes, including piecewise deterministicmodels, and develops forward to more advanced jump-diffusion processes and nonlinearMarkov processes with their mean field particle interpretations. An abstract and universalclass of continuous time stochastic process is discussed in section 15.5.

The last two chapters, chapter 17 and chapter 18 present respectively a panorama ofanalytical tools to study the long time behavior of continuous time stochastic processes,and path-space probability measures with some application domains.

Part V is dedicated to diffusion processes on manifolds. These stochastic processes arisewhen we need to explore state spaces associated with some constraints, such as the sphere,the torus, or the simplex. The literature on this subject is often geared towards purelymathematical aspects, with highly complex stochastic differential geometry methodologies.This book provides a self-contained and pedagogical treatment with a variety of examplesand application domains. Special emphasis is given to the modelling, the stability analysis,and the numerical simulation of these processes on a computer.

The synthetic diagram below provides some inclusion type links between the differentclasses of stochastic computational techniques discussed in this book.

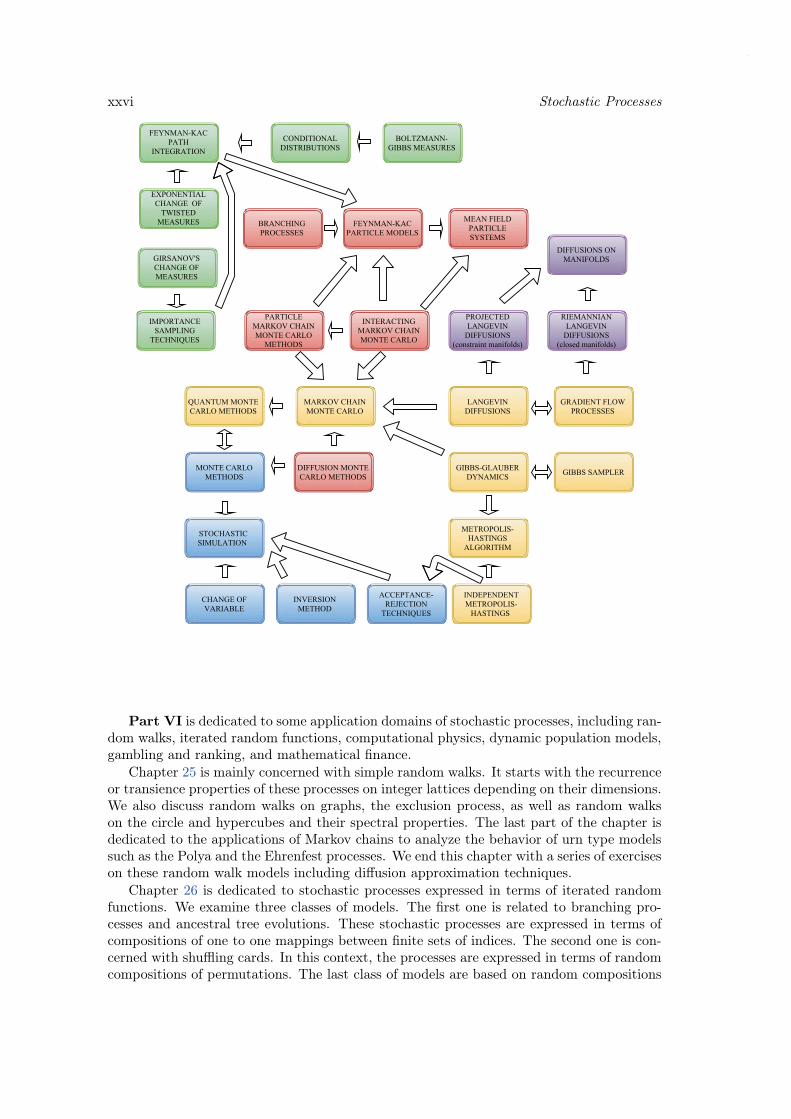

xxvi Stochastic Processes

Part VI is dedicated to some application domains of stochastic processes, including ran-dom walks, iterated random functions, computational physics, dynamic population models,gambling and ranking, and mathematical finance.

Chapter 25 is mainly concerned with simple random walks. It starts with the recurrenceor transience properties of these processes on integer lattices depending on their dimensions.We also discuss random walks on graphs, the exclusion process, as well as random walkson the circle and hypercubes and their spectral properties. The last part of the chapter isdedicated to the applications of Markov chains to analyze the behavior of urn type modelssuch as the Polya and the Ehrenfest processes. We end this chapter with a series of exerciseson these random walk models including diffusion approximation techniques.

Chapter 26 is dedicated to stochastic processes expressed in terms of iterated randomfunctions. We examine three classes of models. The first one is related to branching pro-cesses and ancestral tree evolutions. These stochastic processes are expressed in terms ofcompositions of one to one mappings between finite sets of indices. The second one is con-cerned with shuffling cards. In this context, the processes are expressed in terms of randomcompositions of permutations. The last class of models are based on random compositions

Introduction xxvii

of linear transformations on the plane and their limiting fractal image compositions. Weillustrate these models with the random construction of the Cantor’s discontinuum, andprovide some examples of fractal images such as a fractal leaf, a fractal tree, the Sierpinskicarpet, and the Highways dragons. We analyze the stability and the limiting measures asso-ciated with each class of processes. The chapter ends with a series of exercises related to thestability properties of these models, including some techniques used to obtain quantitativeestimates.

Chapter 27 explores some selected applications of stochastic processes in computationaland statistical physics.

The first part provides a short introduction to molecular dynamics models and to theirnumerical approximations. We connect these deterministic models with Langevin diffusionprocesses and their reversible Boltzmann-Gibbs distributions.

The second part of the chapter is dedicated to the spectral analysis of the Schrödingerwave equation and its description in terms of Feynman-Kac semigroups. We provide anequivalent description of these models in terms of the Bra-kets and path integral formalismscommonly used in physics. We present a complete description of the spectral decompositionof the Schrödinger-Feynman-Kac generator, the classical harmonic oscillator in terms of theHermite polynomials introduced in chapter 17. Last but not least we introduce the reader tothe Monte Carlo approximation of these models based on the mean field particle algorithmspresented in the third part of the book.

The third part of the chapter discusses different applications of interacting particlesystems in physics, including the contact model, the voter and the exclusion process. Thechapter ends with a series of exercises on the ground state of Schrödinger operators, quasi-invariant measures, twisted guiding waves, and variational principles.

Chapter 28 is dedicated to applications of stochastic processes in biology and epidemiol-ogy. We present several classes of deterministic and stochastic dynamic population models.We analyse logistic type and Lotka-Volterra processes, as well as branching and geneticprocesses. This chapter ends with a series of exercises related to logistic diffusions, bimodalgrowth models, facultative mutualism processes, infection and branching processes.

Chapter 29 is concerned with applications of stochastic processes in gambling and rank-ing. We start with the celebrated Google page rank algorithm. The second part of thechapter is dedicated to gambling betting systems. We review and analyze some famousmartingales such as the St Petersburg martingale, the grand martingale, the D’Alembertand the Whittaker martingales. The third part of the chapter is mainly concerned withstochastic control and optimal stopping strategies. The chapter ends with a series of exer-cises on the Monty Hall game show, the Parrondo’s game, the bold play strategy, the ballotand the secretary problems.

The last chapter, chapter 30, is dedicated to applications in mathematical finance. Wediscuss the discrete time Cox-Ross-Rubinstein models and the continuous Black-Scholes-Merton models. The second part of the chapter is concerned with European pricing options.We provide a discussion on the modelling of self-financing portfolios in terms of controlledmartingales. We also describe a series of pricing and hedging techniques with some nu-merical illustrations. The chapter ends with a series of exercises related to neutralizationtechniques of financial markets, replicating portfolios, Wilkie inflation models, and life func-tion martingales.

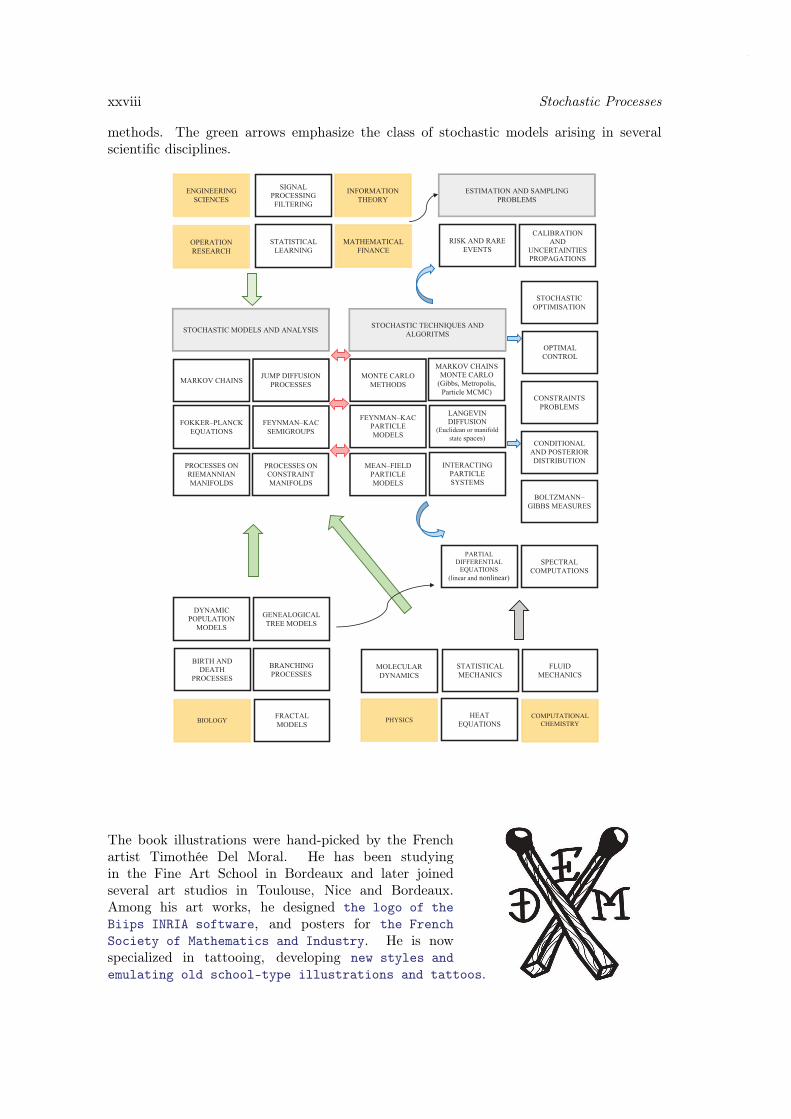

The synthetic diagram below provides some inclusion type links between the stochasticprocesses and the different application domains discussed in this book. The black arrowsindicate the estimations and sampling problems arising in different application areas. Theblue arrows indicate the stochastic tools that can be used to solve these problems. Thered arrows emphasize the modelling, the design and the convergence analysis of stochastic

xxviii Stochastic Processes

methods. The green arrows emphasize the class of stochastic models arising in severalscientific disciplines.

ENGINEERING SCIENCES

SIGNAL PROCESSING FILTERING

INFORMATION THEORY

OPERATION RESEARCH

STATISTICAL LEARNING

MATHEMATICAL FINANCE

CALIBRATION AND

UNCERTAINTIES PROPAGATIONS

RISK AND RARE EVENTS

ESTIMATION AND SAMPLING PROBLEMS

STOCHASTIC OPTIMISATION

OPTIMAL CONTROL

CONSTRAINTS PROBLEMS

CONDITIONAL AND POSTERIOR DISTRIBUTION

BOLTZMANN–GIBBS MEASURES

SPECTRAL COMPUTATIONS

COMPUTATIONAL CHEMISTRY

FLUID MECHANICS

HEAT EQUATIONS PHYSICS

MOLECULAR DYNAMICS

STATISTICAL MECHANICS

FRACTAL MODELS BIOLOGY

BIRTH AND DEATH

PROCESSES

BRANCHING PROCESSES

GENEALOGICAL TREE MODELS

PARTIAL DIFFERENTIAL

EQUATIONS (linear and nonlinear)

DYNAMIC POPULATION

MODELS

STOCHASTIC TECHNIQUES AND ALGORITMS

MARKOV CHAINS MONTE CARLO

(Gibbs, Metropolis, Particle MCMC)

MONTE CARLO METHODS

LANGEVIN DIFFUSION

(Euclidean or manifold state spaces)

FEYNMAN–KAC PARTICLE MODELS

MEAN–FIELD PARTICLE MODELS

INTERACTING PARTICLE SYSTEMS

STOCHASTIC MODELS AND ANALYSIS

MARKOV CHAINS JUMP DIFFUSION PROCESSES

FOKKER–PLANCK EQUATIONS

FEYNMAN–KAC SEMIGROUPS

PROCESSES ON RIEMANNIAN MANIFOLDS

PROCESSES ON CONSTRAINT MANIFOLDS

The book illustrations were hand-picked by the Frenchartist Timothée Del Moral. He has been studyingin the Fine Art School in Bordeaux and later joinedseveral art studios in Toulouse, Nice and Bordeaux.Among his art works, he designed the logo of theBiips INRIA software, and posters for the FrenchSociety of Mathematics and Industry. He is nowspecialized in tattooing, developing new styles andemulating old school-type illustrations and tattoos.

Introduction xxix

Preview and objectivesThis book provides an introduction to the probabilistic modelling of discrete and continuoustime stochastic processes. The emphasis is put on the understanding of the main mathemat-ical concepts and numerical tools across a range of illustrations presented through modelswith increasing complexity.

If you can’t explain it simply, you don’t understand it well enough.Albert Einstein (1879-1955).

While exploring the analysis of stochastic processes, the reader will also encounter avariety of mathematical techniques related to matrix theory, spectral analysis, dynamicalsystems theory and differential geometry.

We discuss a large class of models ranging from finite space valued Markov chains tojump diffusion processes, nonlinear Markov processes, self-interacting processes, mean fieldparticle models, branching and interacting particle systems, as well as diffusions on con-straint and Riemannian manifolds.

Each of these stochastic processes is illustrated in a variety of applications. Of course,the detailed description of real-world models requires a deep understanding of the physicalor the biological principles behind the problem at hand. These discussions are out of thescope of the book. We only discuss academic-type related situations, providing precisereference pointers for a more detailed discussion. The illustrations we have chosen are veryoften at the crossroads of several seemingly disconnected scientific disciplines, includingbiology, mathematical finance, gambling, physics, engineering sciences, operations research,as well as probability, and statistical inference.

The book also provides an introduction to stochastic analysis and stochastic differentialcalculus, including the analysis of probability measures on path spaces and the analysis ofFeynman-Kac semigroups. We present a series of powerful tools to analyze the long time be-havior of discrete and continuous time stochastic processes, including coupling, contractioninequalities, spectral decompositions, Lyapunov techniques, and martingale theory.

The book also provides a series of probabilistic interpretations of integro-partial differ-ential equations, including stochastic partial differential equations (such as the nonlinearfiltering equation), Fokker-Planck equations and Hamilton-Jacobi-Bellman equations, aswell as Cauchy-Dirichlet-Poisson equations with boundary conditions.

Last but not least, the book also provides a rather detailed description of some tradi-tional and more advanced computational techniques based on stochastic processes. Thesetechniques include Markov chain Monte Carlo methods, coupling from the past techniques,as well as more advanced particle methods. Here again, each of these numerical techniquesis illustrated in a variety of applications.

Having said that, let us explain some other important subjects which are not treated inthis book. We provide some precise reference pointers to supplement this book on some ofthese subjects.

As any lecture on deterministic dynamical systems does not really need to start witha fully developed Lebesgue, or Riemann-Stieltjes integration theory, nor with a special-ized course on differential calculus, we believe that a full and detailed description ofstochastic integrals is not really needed to start a lecture on stochastic processes.

For instance, Markov chains are simply defined as a sequence of random variables indexedby integers. Thus, the mathematical foundations of Markov chain theory only rely on ratherelementary algebra or Lebesgue integration theory.

xxx Stochastic Processes

It is always assumed implicitly that these (infinite) sequences of random variables aredefined on a common probability space; otherwise it would be impossible to quantify, norto define properly limiting events and objects. From a pure mathematical point of view,this innocent technical question is not so obvious even for sequences of independent randomvariables. The construction of these probability spaces relies on abstract projective lim-its, the well known Carathéodory extension theorem and the Kolmogorov extensiontheorem. The Ionescu-Tulcea theorem also provides a natural probabilistic solution on gen-eral measurable spaces. It is clearly not within the scope of this book to enter into theserather well known and sophisticated constructions.

As dynamical systems, continuous time stochastic processes can be defined as the limitof a discrete generation Markov process on some time mesh when the time step tendsto 0. For the same reasons as above, these limiting objects are defined on a probabilityspace constructed using projective limit techniques and extension type theorems to definein a unique way infinite dimensional distributions from finite dimensional ones defined oncylindrical type sets.