daily credit briefing

TRANSCRIPT

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 1 See last pages for disclaimer.

Credit Market Snapshot

Amid fresh monetary stimulus signaled by the ECB, European credit and equity markets experienced a rollercoaster ride on Thursday. The ECB left key interest rates unchanged but the central bank sent dovish signals of additional monetary policy easing ahead. However, it disappointed market participants with regard to the details and timing of the stimulation package. In the view of our economists, the ECB is increasingly worried about the downturn in the manufacturing sector and inflation remaining persistently below its goal. ECB President Mario Draghi emphasized determination to act. In an unambiguous sign that stimulus is in the pipeline, the rate guidance was changed to include a formal easing bias, while technical committees have been tasked to consider a broad range of options to relax policy. As a result, our economists think that the ECB has opened the door for a 10bp rate cut in the deposit rate in September as the ECB expects rates to “remain at their present or lower levels at least through the first half of 2020”. Furthermore, a tiered system for excess reserves, benefiting banks in particular is very likely, along with a resumption of a QE program in the form of asset purchases. Given Mr. Draghi’s rhetoric in the press conference, it seems that potential new net asset purchases could be announced some time between September and December.

Right after the release of the ECB decision, credit markets rallied but pared earlier gains during the press conference as Mr. Draghi made also a few statements that were regarded as less dovish: the monetary policy decision was not taken unanimously, recession risk was regarded as “pretty low”, there was no discussion to cut rates at Thursday’s policy meeting and there was no discussion of raising the issue/issuer limit in a renewed QE program. In the end, the Main widened 0.5bp to 46bp, the XO was up 3bp to 240bp, and the FinSen (+1bp to 55bp) and FinSub (+2bp to 121bp) both followed suit. Given that spreads in the credit market have adjusted to the expectation of a more-dovish ECB in recent weeks, we think that markets will now likely move sideways over the next weeks.

The prospects of additional monetary stimulus also spurred European equities at the beginning, while stock markets turned sour across the broad during the ECB press conference. The STOXX Europe 600 was down 0.6% in the end with only three industry sectors closing on a positive note (Travel & Leisure +0.3%, Health Care +0.1% and Food & Beverage 0.01%). In particular, Automobiles & Parts (-1.75%) and Chemicals (-1.6%) ended lower. Expectations of a so-called tiered deposit rate spurred Bank stocks (+1.9%) before the ECB decision but the rally faltered afterwards and Bank stocks closed 0.3% lower at the end of the session. A tiered deposit rate would partially exempt banks from paying the deposit rate (currently -40bp) on their excess reserves, thus improving their profits. German stocks experienced the biggest drop (DAX -1.3%), a disappointing release of the Ifo index adding to the view. The Ifo index plunged to its lowest level since April 2013 with the business expectations component reaching its lowest level since 2009. Following mixed earnings results, all major US benchmark stock indices dropped (S&P 500 -0.5%).

This morning, Asian markets are trading lower on mixed US earnings results (Nikkei and Hang Seng both down by 0.5%, while the CSI 300 is unchanged). In terms of economic releases, US 2Q GDP data will be out today. Our economists expect a slowdown in GDP growth to 1.7% qoq annualized from 3.1% qoq annualized growth in 1Q19. This likely reflects a slump in inventories and net exports, and a decline in non-residential investment, while an expected pickup in consumer spending should partly offset the slowdown. In Italy, consumer and manufacturing confidence will be released. Furthermore, the ECB will publish its Survey of Professional Forecasters. In yesterday’s press conference, Mario Draghi indicated that the survey would show a decline in inflation expectations. For this reason, attention will mainly be on this variable, especially that for the longer term.

Holger Kapitza, Credit & High Yield Strategist (UniCredit Bank, Munich) +49 89 378 28745, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 2 See last pages for disclaimer.

Investment GradeENERGY

EnBW Good operational results, net debt substantially higher on acquisitions, signals potential new hybrid

INDUSTRIALS

Saint-Gobain Solid 1H19 results

Anglo American Anil Agarwal to exit Anglo American

Stora Enso Termination of coverage

AUTOS

FCE Bank Reports adj. automotive gross leverage in 2Q19 as stable yoy but still too high

Hella Makes special dividend proposal and reports weak FY19/20 guidance

Renault 1H19 revenues down 6.4%, operating profit margin down 50bp to 5.9% and adjusted automotive gross leverage up

Valeo Reports that credit metrics weakened further in 2Q19

TMT

AT&T Well on track to achieve net leverage target

Comcast 2Q19 results slighly above consensus, deleveraging continues

Deutsche Telekom T-Mobile US reports strong 2Q19 results and raises outlook

RELX Group 1H19 results show growth deceleration, but trends still positive

Vivendi 1H19 results show strong results for UMG, IPO on track

CONSUMER

Roche 1H19 results better than expected , guidance for 2019 increased

Danone 1H19 results in line with expectations, outlook 2019 confirmed - no surprises

Diageo FY18/19 results

LVMH 1H19 results in line with estimates

BANKS

Banco de Sabadell 2Q19 results below consensus estimates

CaixaBank Better-than expected 2Q19 results impacted by one-off restructuring costs of almost EUR 1bn

INSURANCE

Mapfre Reports mixed 1H19 results

SUB-SOVEREIGNS

Deutsche Bahn Revenue up by 2.2% yoy in 1H19, EBIT down to EUR 757mn

High Yield HIGH YIELD

Ardagh Weaker underlying performance in 2Q19

Jaguar Land Rover Reports JLR 1Q19/20 revenue down by 2.8% and EBITDA margin down by 200bp to 4.2%

LKQ Reports net leverage in 2Q19 slightly down qoq and increases FY19 FCF guidance

Quick links Market Data Page Rating Actions Recent Credit Research Publications

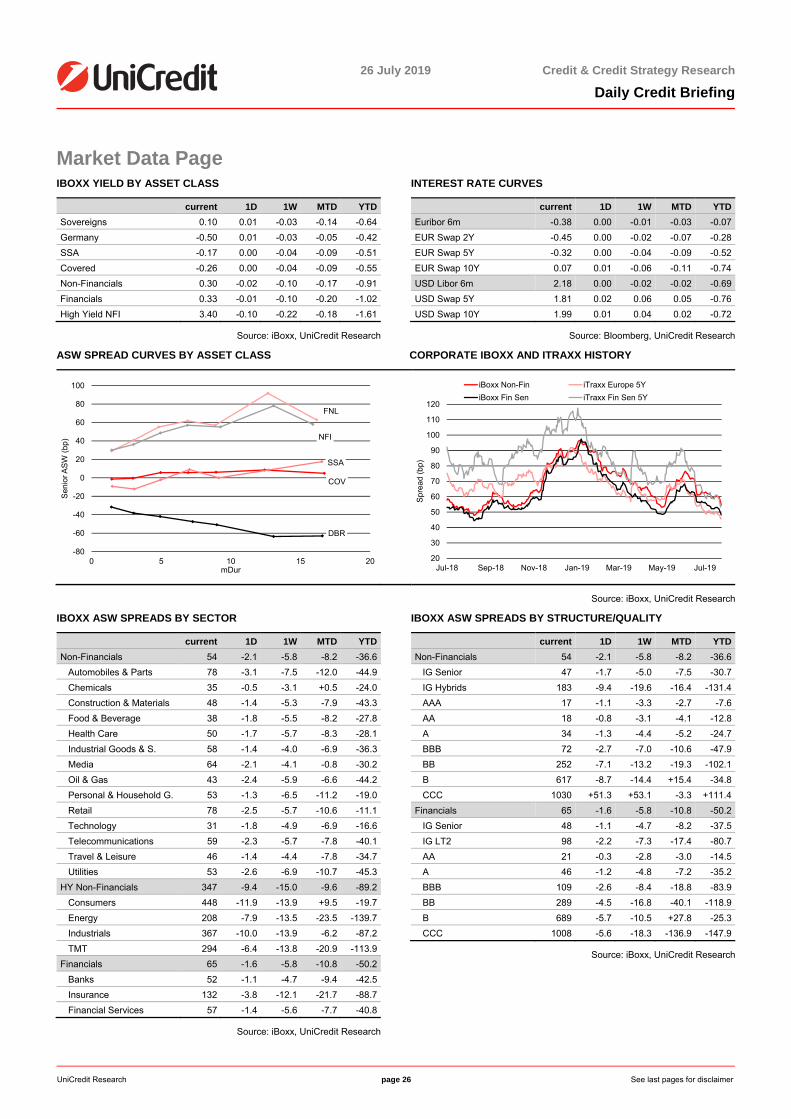

MARKET DATA

Credits 1D Govies 1D FX/FI 1D Equities 1D Other

iBoxx NFI Sen 47 -1.7 Bund Ft 174.13 -0.17 3m Euribor -0.38 -0.002 Euro STOXX 50 3,510 -23 VSTOXX 13

iBoxx NFI Hyb 183 -9.4 Germany 5Y -0.67 +0.01 2Y EUR Swap -0.45 +0.002 DAX 12,362 -161 VDAX 18

iBoxx FIN Sen 48 -1.1 France 5Y -0.58 +0.01 5Y EUR Swap -0.32 -0.001 CAC 5,578 -28 VIX 13

iBoxx FIN Sub 133 -3.4 Italy 5Y 0.79 +0.03 10Y EUR Swap 0.07 +0.005 MSCI Italy 60.4 +0.3 Brent Future 63

iBoxx NFI HY 347 -9.4 Spain 5Y -0.23 +0.01 EUR-USD 1.11 +0.001 IBEX 35 9,290 -40 Gold Spot 1,417

Source: Bloomberg, iBoxx, Markit, UniCredit Research

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 3 See last pages for disclaimer.

Energy

EnBW (Marketweight) EnBW (A3n/A-/A-) posted good 1H19 results that benefited from the strong performance of

Generation and Renewables activities, offsetting weakness at Sales. Adjusted EBITDA camein at EUR 1.28bn for the period, up by 11% yoy. Sales, however, posted a decrease to EUR 109mn, down by 31.5% yoy, mainly due to higher electricity and gas procurement costs.Generation and Trading registered an 87% increase to EUR 261mn, supported by higherforward power prices compared to the prior year (the German baseload 1Y forward average in 1H18 was EUR 37/MWh compared to EUR 48/MWh in 1H19) as well as the more-beneficial timing of nuclear plant shutdowns for inspection, resulting in higher production(however, this will even out in 2H19). Renewables EBITDA came in at EUR 205mn, up by 24% yoy thanks to better wind conditions. Grids also increased by 5% to EUR 720mn, mainly from higher investments to ensure resiliency of the network, confirming the stable businessprofile of these activities.

Despite the increase in EBITDA, cash flow from operating activities was reported almost flat, mainly as a consequence of strong cash absorption from NWC due to an increase in thestock of receivables and inventories (related to CO2 purchases). With about EUR 450mn innet investments, free cash flow after capex was negative at EUR -376mn. This operational development, along with the acquisition of Valeco and Plusnet, brought net financial debt toEUR 5.8bn (including IFRS 16 impact of EUR 521mn), compared to EUR 3.7bn at FYE 2018, and net debt (including pensions and nuclear obligations) to EUR 12.7bn from EUR 9.6bn atFYE 2018. In the investor call, CFO Thomas Andreas Kusterer stated that the level of debtshould remain stable over 2H19, as low rates will continue to put pressure on the valuation of pension and nuclear liabilities. This is higher than the previous guidance of a stock ofEUR 10.8-11.8bn. He also reiterated the importance of a solid investment-grade rating, and he mentioned that EnBW might find a partner for future investments and that additional funding through the capital market might come in the form of a hybrid bond to support ratings.

EnBW hybrids have underperformed Ørsted hybrids YTD by some 30-60bp depending on the maturity. The ORSTED 6.25% 6/13 (first call 6/23) now trades more or less flat to the ENBW 3.375% 4/77 (first call 1/22), which has a better rating and also one-year shorter duration. We keep a marketweight recommendation on EnBW.

Gianfranco Arcovito, CFA, Credit Analyst (UniCredit Bank, Munich) +49 89 378-15449, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 4 See last pages for disclaimer.

Industrials

Saint-Gobain (Marketweight) Event Saint-Gobain (Baa2s/BBBs/BBBs) released solid 1H19 results slightly above market

expectations. The company confirmed its full-year forecast and raised its cost savings target for the full-year. Top-line growth decelerated in 2Q compared to 1Q, which benefitted,however, from a weak comparison base in Europe as well as a positive calendar effect. Salesof EUR 21.7bn were up by 3.5% organically in 1H19, driven by volumes (+1.2%) but alsoprices (+2.3%) in an overall slightly less inflationary environment. EBITDA advanced by 8.4%to EUR 2.4bn

Expected development of credit profile/rating

Saint-Gobain confirmed its full-year objectives and for the second half of the year, albeit in aless supportive market overall, and expects a like-for-like increase in operating income compared to 2H18.

It expects the following trends: 1. satisfactory industrial markets, particularly in the US, despite the contraction in the automotive market in Europe and China for its HighPerformance Solutions division; 2. progress in Northern Europe, despite a tougher environment in the UK; 3. growth for Southern Europe, the Middle East and Africa, with a lower contribution from new construction (as expected) and a solid renovation market in2H19, in particular in France; 4. stabilization in North America and a less certain environment in Latin America (the company has become more cautious here) and 5. further growth in Asia.

The targeted improved operating performance should be further supported by a continuedfocus on sales prices and ongoing cost savings, with the target as part of its Transform &Growth program for FY19 being raised from over EUR 50mn to more than EUR 80mn. Capex is forecast to be close to its FY18 level, and the company remains focused on FCFgeneration. Saint-Gobain further stated that it is making good progress with its portfolio-optimization program and will exceed EUR 3bn in sales divested by the end of 2019 (divestments already completed or signed represent over EUR 2.8bn in sales).

Name recommendation We have a marketweight recommendation on SGOFP issues and do not expect the solidresults to be a driver for spread levels this morning. Spread levels remain supported by astrong French bid, but we see little reason for the bonds to underperform.

Jana Schuler, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13211, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 5 See last pages for disclaimer.

Anglo American (Underweight) Volcan Investments, a holding company wholly owned by the family trust of Anil

Agarwal, currently the biggest shareholder in Anglo American (around 20% stake),announced that it will exit its stake. In a statement Volcan announced that it intends to call its two issues of mandatory exchangeable bonds and settle them with its underlying AngloAmerican plc shares. In a separate statement, Vedanta Ltd (a subsidiary of Volcan) said its overseas subsidiary Cairn India Holdings Ltd (CIHL) will exit its investments in Anglo American. Following these transactions, neither Volcan nor its subsidiaries will hold any AngloAmerican shares, the company stated. The stake sale is positive as it removes uncertainty about Mr. Agrawal’s intentions with regard to Anglo. The announcement should hence beslightly positive for spread levels this morning. We have an underweight recommendation onAnglo American.

Jana Schuler, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13211, [email protected]

Stora Enso (No recommendation from Hold) We are ceasing coverage of Stora Enso and change our recommendation on the name from

hold to no recommendation.

Jana Schuler, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13211, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 6 See last pages for disclaimer.

Autos

FCE Bank (Underweight); Ford Motor Credit (Underweight) Event Ford (Baa3n/BBBn/BBBn), the ultimate parent of both Ford Motor Credit and FCE Bank

(Baa3n/BBBn/BBBn), has reported its 2Q19/1H19 results (see presentation). The following are some highlights: automotive wholesales were -9%/-12% yoy, revenue was 0%/-3% yoyand its automotive EBIT margin was up to 3.8%/4.6% (compared to 3.2%/3.9% yoy [with North America down to 7.1%/7.9%, compared to 7.4%/7.6% yoy]). Ford’s global market share decreased by 50bp to 6.2%/6.1% yoy. In South America, margin decreased by 880bp/-740bp to -21.0%/-19.1% yoy. In Europe, it was up by 170bp/+40bp, to 0.7%/0.7%. Outside NorthAmerica in 2Q19, Ford Automotive had an EBIT of USD 323mn, which was down from USD596mn yoy, with losses in South America, China, the Middle East and Africa. The Mobility segment reported adjusted EBIT of USD -264mn. Automotive debt was up to USD 14.6bn,compared to USD 14.1bn at FYE 2018.

Expected development of credit profile/rating

Ford remains committed to maintaining its IG rating and aims to achieve cash balances and liquidity that are at or above USD 20bn (2Q19: USD 23.2bn) and USD 30bn (2Q19: USD 37.3bn)respectively. For 2019, Ford has projected for adj. FCF to be above the USD 2.8bn from FY18 (1H19: USD 2.1bn), for adj. EBIT of USD 7-7.5bn (1H19: USD 4.1bn; FY18: USD 7.0bn) and for adj. EPS of USD 1.2-1.35 (FY18: USD 1.3). Recently, Ford provided details concerning itsrestructuring program in Europe, where it has a longer-term goal of delivering a 6% EBIT margin. These measures are part of Ford’s announced restructuring of its automotive divisions outside North America. This restructuring involves potential EBIT charges of USD11bn (2019E: USD 3-3.5bn) with cash-related effects of USD 7bn (2019E: USD 1.5-2bn) over the next three to five years. Unfortunately, Ford did not provide leverage numbers, which it had previously provided. Adjusted debt/EBITDA (Ford’s calculation) in 1Q19 was 3.2x, whichwas above Ford’s longer-term target of less than 2.5x. Guidance for leverage in FY19 (as of the 1Q19 release) was expected to be higher than in FY18 (3.2x). We calculate that Ford’sautomotive gross debt/EBITDA (UniCredit Research) ratio in 2Q19 was stable, at 3.6x(compared to 3.6x yoy). However, it improved slightly from 3.7x qoq. If gross leverage of roughly 3x is the hurdle ratio for an IG rating, it is likely that Ford will keep its leverage ratio inthe low-BBB area should it achieve its longer-term deleveraging target of greater than 0.7x(see above). Therefore, we still expect the mid-BBB ratings by S&P and Fitch to come under pressure but do not expect a downgrade to junk by Moody’s as long as Ford is on the waytowards meeting its leverage and guidance targets. Ford’s increased leverage compares toGM’s lower leverage of 2.3x in 1Q19, which remained stable after the disposal of GM Europe. Ford’s unsecured term funding plan for 2019 amounts to USD 14-19bn (2018: USD 13bn). Of this, approximately USD 3-4bn (2018: USD 4bn) is denominated in EUR/GBP, USD 9-12bn (USD 6bn) is denominated in USD and USD 13-15bn (2018: USD 27bn) is in securitizations.

Name recommendation FCE Bank’s and Ford Motor Credit’s EUR-denominated cash curves are trading wider than FCA’s (Ba1s/BB+p/BBB-s), close to Volvo Car’s (Ba1s/BB+p) and roughly 50bp wider thanPeugeot’s (Baa3s/BBB-s/BBB-s). Ford’s 2019 guidance in terms of a slight EBIT improvement but negative FCF (after global redesign cash charges and USD 2.6bn individends) does not seem indicate an improvement in credit metrics in FY19 over FY18. We are keeping our underweight recommendation. More-conservative IG investors should wait until credit metrics start to improve on a yoy basis and return closer to IG leverage ratios.Given crossover spread levels, the bonds might however be attractive for IG investors with HY buckets. On the Ford Credit euro-denominated curve, we recommend a switch from FC 2/25 into FC 3/24 for a reduction in duration at a higher spread. None of FCE Bank’s/Ford Motor’s bonds are eligible for the CSPP. Details on FCE’s credit profile can be found inour Automotive Credit Conference Handbook, 25 May 2018.

Dr. Sven Kreitmair, CFA (UniCredit Bank); +49 89 378-13246; [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 7 See last pages for disclaimer.

Hella (Hold) Event Ahead of its FY18/19 results (ending 31 May) release on 9 August, Hella (Baa1s/--)

reported preliminary FY18/19 figures, proposed a special dividend of EUR 255mn andprovided weak FY19/20 guidance. The key figures for FY18/19 were as follows: 1. Organic growth of +5.0% was achieved in light of the disposal of the wholesale distribution business and after FX-rate effects were taken into account, and reported sales declined to EUR 7.0bn,compared to EUR 7.1bn yoy. 2. Adjusted EBIT was up by 5.9% to EUR 585mn, with the adjusted EBIT margin up by 10bp to 8.4% yoy, and the reported EBIT margin was 11.6%,compared to 8.1% yoy. Hella plans to propose paying out a special dividend of EUR 2.30 per share in addition to a regular dividend of EUR 1.05 per share (previous year: EUR 1.05). Thespecial dividend is based on a strong balance-sheet performance over the past few years and the sale of the wholesale distribution business. The amount of the dividend approximatelycorresponds to the accounting profit of EUR 255mn, which Hella realized by disposing of the wholesale distribution business – or to around two-thirds of the cash proceeds from this transaction. On the assumption that the markets will continue to decline, that significant investments in R&D will be required and that material and labor costs will further increase, Hella’s guidance for FY19/20 is for currency and portfolio-adjusted sales in the range of EUR 6.5-7.0bn (FY18/19: EUR 6.8bn) and for an EBIT margin, adjusted for restructuring measures and portfolio effects, in the range of 6.5-7.5% (FY18/19: 8.4%).

Expected development of credit profile/rating

Hella’s medium-to-long-term target is net debt/EBITDA of below 1x (3Q18/19: 0.0x). Netfinancial debt at end-3Q18/19 amounted to EUR 48mn (compared to EUR -187mn at FYE) and the equity ratio was up to 45.7% (compared to 41.9% at FYE). In an interview with Handelsblatt, which was cited by Bloomberg, Hella CEO Rolf Breidenbach stated that the company had great interest in acquisitions in the field of special applications. Sensors andcontrol electronics for electric motors are also potential targets. In an article inAutomobilwoche, Mr. Breidenbach said that Hella wanted to speed up growth by acquiring companies in such areas as electronics, sensors, aftermarket and special applications. Available funds for possible deals total around EUR 1bn, while the majority owners do not allow Hella to undertake what they refer to as “financial adventures” when buying companies. For our comment on this, see our Daily Credit Briefing, 2 October 2017. For credit details regarding Hella, see our Automotive Credit Conference Handbook, 25 May 2018. For details and peer comparisons, see our Sector Report “Automobiles & Parts/German auto suppliers: Transformation needs in volatile times”, 4 July.

Name recommendation We think that the special dividend and FY19/20 guidance for margin reduction are credit negative. Adjusted gross (net) debt/EBITDA (UniCredit Research) at 9M18/19 was up to 1.9x(1.0x), compared to 1.5x (0.9x) yoy. Given the company’s leverage target (companydefinition) of less than 1.0x (compared to 0.0x at 3Q), this ratio might increase, in the worst case, by up to 1.0x in case of any larger debt-financed acquisitions, which would put pressure on the current rating. The retail-sized HELLA 2.375% 1/20 bond, which was Hella’s only benchmark bond, left the iBoxx in February. The bond has some scarcity value, and the ECB’s CSPP holds both Hella bonds (1/20 and 5/24). Given their tight spreads (but also due to the short duration), the lack of tightening potential and M&A plans, and as we do not thinkHella plans to enter the single-A rating category any time soon, we have a hold recommendation.

Dr. Sven Kreitmair, CFA, Head of Credit Research (UniCredit Bank, Munich) +49 89 378-13246, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 8 See last pages for disclaimer.

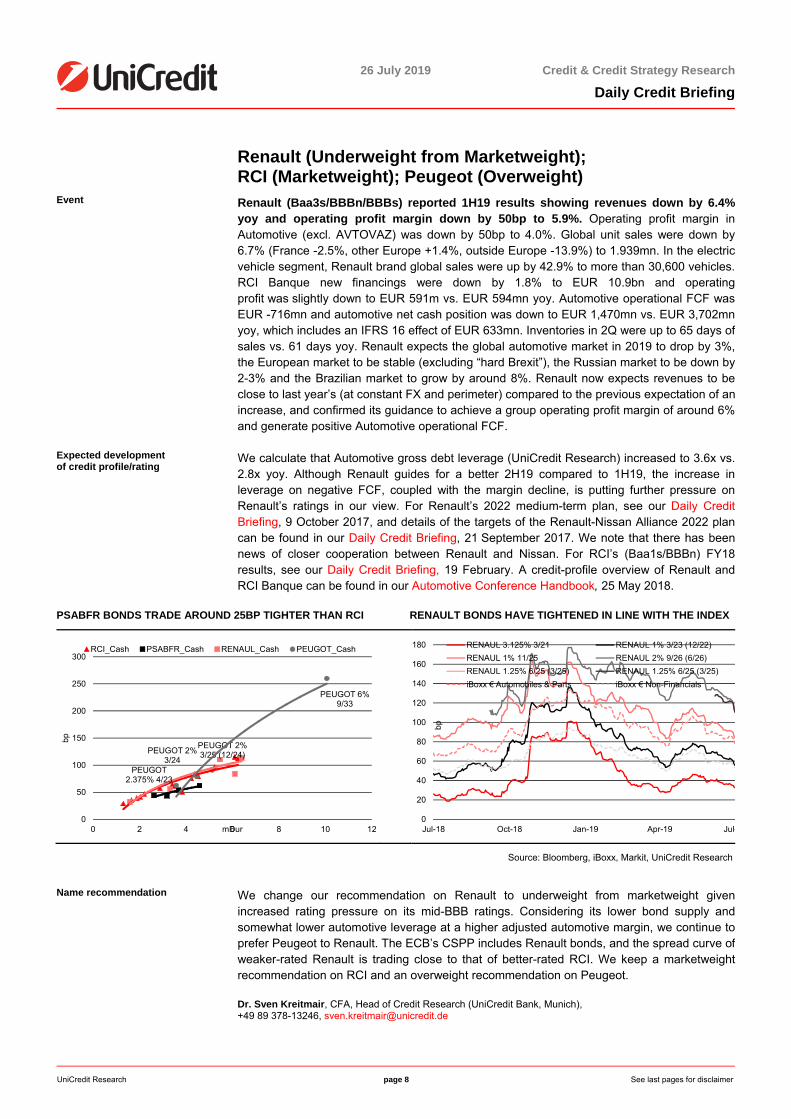

Renault (Underweight from Marketweight); RCI (Marketweight); Peugeot (Overweight)

Event Renault (Baa3s/BBBn/BBBs) reported 1H19 results showing revenues down by 6.4%yoy and operating profit margin down by 50bp to 5.9%. Operating profit margin in Automotive (excl. AVTOVAZ) was down by 50bp to 4.0%. Global unit sales were down by6.7% (France -2.5%, other Europe +1.4%, outside Europe -13.9%) to 1.939mn. In the electric vehicle segment, Renault brand global sales were up by 42.9% to more than 30,600 vehicles. RCI Banque new financings were down by 1.8% to EUR 10.9bn and operating profit was slightly down to EUR 591m vs. EUR 594mn yoy. Automotive operational FCF wasEUR -716mn and automotive net cash position was down to EUR 1,470mn vs. EUR 3,702mnyoy, which includes an IFRS 16 effect of EUR 633mn. Inventories in 2Q were up to 65 days ofsales vs. 61 days yoy. Renault expects the global automotive market in 2019 to drop by 3%,the European market to be stable (excluding “hard Brexit”), the Russian market to be down by 2-3% and the Brazilian market to grow by around 8%. Renault now expects revenues to beclose to last year’s (at constant FX and perimeter) compared to the previous expectation of anincrease, and confirmed its guidance to achieve a group operating profit margin of around 6% and generate positive Automotive operational FCF.

Expected development of credit profile/rating

We calculate that Automotive gross debt leverage (UniCredit Research) increased to 3.6x vs.2.8x yoy. Although Renault guides for a better 2H19 compared to 1H19, the increase in leverage on negative FCF, coupled with the margin decline, is putting further pressure on Renault’s ratings in our view. For Renault’s 2022 medium-term plan, see our Daily Credit Briefing, 9 October 2017, and details of the targets of the Renault-Nissan Alliance 2022 plan can be found in our Daily Credit Briefing, 21 September 2017. We note that there has been news of closer cooperation between Renault and Nissan. For RCI’s (Baa1s/BBBn) FY18 results, see our Daily Credit Briefing, 19 February. A credit-profile overview of Renault and RCI Banque can be found in our Automotive Conference Handbook, 25 May 2018.

PSABFR BONDS TRADE AROUND 25BP TIGHTER THAN RCI RENAULT BONDS HAVE TIGHTENED IN LINE WITH THE INDEX

Source: Bloomberg, iBoxx, Markit, UniCredit Research

Name recommendation We change our recommendation on Renault to underweight from marketweight givenincreased rating pressure on its mid-BBB ratings. Considering its lower bond supply and somewhat lower automotive leverage at a higher adjusted automotive margin, we continue toprefer Peugeot to Renault. The ECB’s CSPP includes Renault bonds, and the spread curve ofweaker-rated Renault is trading close to that of better-rated RCI. We keep a marketweight recommendation on RCI and an overweight recommendation on Peugeot.

Dr. Sven Kreitmair, CFA, Head of Credit Research (UniCredit Bank, Munich), +49 89 378-13246, [email protected]

PEUGOT 2% 3/24

PEUGOT 2% 3/25 (12/24)

PEUGOT 2.375% 4/23

PEUGOT 6% 9/33

0

50

100

150

200

250

300

0 2 4 6 8 10 12

bp

mDur

RCI_Cash PSABFR_Cash RENAUL_Cash PEUGOT_Cash

0

20

40

60

80

100

120

140

160

180

Jul-18 Oct-18 Jan-19 Apr-19 Jul-

bp

RENAUL 3.125% 3/21 RENAUL 1% 3/23 (12/22)

RENAUL 1% 11/25 RENAUL 2% 9/26 (6/26)

RENAUL 1.25% 6/25 (3/25) RENAUL 1.25% 6/25 (3/25)

iBoxx € Automobiles & Parts iBoxx € Non-Financials

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 9 See last pages for disclaimer.

Valeo (Underweight) Event Valeo (Baa3s/BBBn) has reported 1H19 results, with sales down by 0.9% (like-for-like -2%)

and its operating margin down to 5.3%, compared to 7.7% yoy. Sales of original equipment (OE) were down 2% (like for like: -3%) and outpaced global automotive production by four percentage points. Aftermarket sales were down by 4% as reported and on a like-for-like basis. Automotive production in 1H19 was as follows: globally -7%, China -22%, North America -3% and Europe/Africa -5%. Asian customers accounted for 31% of OE sales, and German customers for 31%. By business group, Visibility Systems generated 30% of group sales, Thermal Systems 24%,Powertrain Systems 26% and Comfort/Driving Assistance Systems 20%. OE sales in each of thefour segments outperformed automotive production by 3pp and in Comfort/Driving Assistance by 6pp. The EBITDA margin of the group was 12.5% in 1H19, with Comfort & Driving AssistanceSystems reporting the highest EBITDA margin, of 14.6%. Net debt (company definition) increasedto EUR 2,877mn, compared to EUR 629mn after the dividend payment was taken into accountand lease liabilities were recognized following the application of IFRS 16 (EUR 442mn at the endof 1H19). Including the impact of IFRS 16, the leverage ratio (net debt/EBITDA) was 1.26x, compared to the 3.25x covenant.

Expected development of credit profile/rating

Order intake in 1H19 amounted to EUR 11.1bn, 42% of which (or 1.3x OE sales) was associated with innovative production. Thanks to the rolling out of a program to reduce costs and capex, a favorable trend in raw-material prices and the start of production on new contracts, Valeo confirmed its guidance despite a stronger-than-anticipated decline in the automotive market, which is expected to contract by around 4% in 2019 (versus a previously forecast decrease of between 1% and 0%). Its guidance is based on the following: its market outperformance, which was stronger than in 2H18 and is anticipated to increase graduallyduring the year (driven by production start-ups for projects in the camera, electrical and transmission systems, and lighting segments); the continued roll-out of a program, announced in February, to reduce costs by more than EUR 100mn and capex by more than EUR 100mn(the main impact of this program is expected to be felt in 2H19). Valeo also expects to achieve EBITDA growth (in value terms) and an operating margin (excluding the share in netearnings of equity-accounted companies [as a percentage of sales]) of between 5.8% and6.5% (FY18: 6.3%; FY17: 7.8%), depending on trends in automotive production and on the prices of raw materials and of electronic components. In addition, Valeo has set itself the objective of maintaining FCF generation in 2H19. Lastly, the “share in net earnings of equity-accounted companies” line is expected to have a similar impact (in millions of euros) onValeo’s statement of income in 2H as it did in 1H, due to the Valeo Siemens eAutomotive JVand to the weak performance of Chinese subsidiaries.

Name recommendation In 1H19, Valeo’s adjusted net debt/EBITDA (UniCredit Research) ratio weakened to 2.9x, compared to 2.0x yoy. As a result of Valeo’s 2019 guidance, there is a risk that credit metricswill weaken further in 2H19, and we believe that the recently weakened credit metrics do not leave much headroom in Valeo’s BBB ratings.

At the longer end, Valeo’s cash curve is trading at the tighter end of automotive BBBs in theiBoxx index. Valeo’s bonds are held in the ECB’s CSPP portfolio. The company has EUR350mn in bond maturities in November 2019. We are keeping our underweight recommendation on the name given the negative credit-metric momentum that is a result of a combination of acquisitions and the risk of weaker 2019 margins and/or lower-than-currently expected light-vehicle production.

Dr. Sven Kreitmair, CFA, Head of Credit Research (UniCredit Bank, Munich) +49 89 378-13246, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 10 See last pages for disclaimer.

TMT

AT&T (Overweight) Event AT&T’s (Baa2s/BBBs/A-s) 2Q19 results came in close to market expectations. The

company raised its free cash flow guidance by USD 2bn to the USD 28bn range.

Revenue in the quarter came to USD 45.0bn (consensus: USD 44.0bn), up 0.6% on a pro forma basis (for the consolidation of Warner Media). Adjusted EBITDA was up 1.1% pro forma toUSD 15.0bn (consensus: USD 15.1bn), driven by strong growth in mobility and continued improvement in the Entertainment Group. OCF increased by 40% yoy to USD 14.3bn with capex of USD 5.4bn (USD 6.5bn including USD 1.0bn in vendor financing), bringing FCF (before dividends) to USD 8.8bn. Net debt was down by USD 6.8bn to USD 162bn, bringing net leverage to 2.7x and marking an improvement by 0.2x qoq.

In the Mobility segment, revenue was up 1.3% yoy to USD 17.5bn (-0.3% qoq), with wireless services revenue up by a stronger 2.4% to USD 14.0bn. Adjusted EBITDA at Mobility was up3.1% yoy to USD 7.9bn (+6.4% qoq). Postpaid subscriber additions were up 72,000, compared to 70,000 in 1Q19 and to 51,000 in 2Q18. The Entertainment Group reported revenue that was down 1.0% yoy to USD 11.4bn (+0.4% qoq), while EBITDA slightly gained 1.1% yoy to USD 2.8bn (+1.9% qoq). Premium-video net adds were down by 778,000, and DIRECTV NOW (OTT) subscribers were down by 168,000, which the company attributed to fewer promotions and price increases (ARPU up 2.5% qoq and up 4.7% yoy). The company reported 34,000 broadband net losses (318,000 fiber net adds) and ARPU that was up 3.6% qoq and 5.2% yoy. Business Wireline reported revenue as being down 0.3% yoy to USD 6.6bn (+2.0% qoq), with EBITDA up 1.3% yoy to USD 2.6bn (+7.6% qoq). Revenue at Warner Media amounted toUSD 8.4bn, with EBITDA of USD 2.4bn.

Expected development of credit profile/rating

AT&T raised its free cash flow guidance by USD 2.0bn to the USD 28bn range. The companysaid that it is on track to reach its target of USD 150bn in net debt and net leverage of 2.5x bythe end of 2019. Beyond the 2.5x range, AT&T will consider opportunistic share repurchaseswhile continuing to pay down debt.

Name recommendation We continue to appreciate AT&T’s focus on debt reduction, though the company has nowsignaled opportunistic share buy backs after achieving its net leverage target. We see low M&A risk for the company in the near term given its deleveraging focus. We therefore confirm ouroverweight recommendation on the name.

Ulrich Scholz, CFA, FRM, Credit Analyst (UniCredit Bank, Munich) [email protected] Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 11 See last pages for disclaimer.

Comcast (Overweight) Event Comcast (A3s/A-n/A-s) reported 2Q19 results that slightly exceeded consensus

estimates in terms of profitability. Revenue came to USD 26,858 (consensus: USD 27,098mn), an increase of 23.6%, driven to a large degree by the Sky acquisition.Adjusted EBITDA rose by 17.5% to USD 8,716mn (consensus: USD 8,654mn). On the segment level, all segments contributed to growth. Cable Communications reported a 7.4%increase in EBITDA to USD 5,854mn. The segment gained a total of 152,000 customers, ofwhich 123,000 were residential customers. High-speed internet customers increased by 209,000 but could not offset video losses of 224,000 and voice losses of 65,000. Wirelessadditions of 181,000 drove total customer additions into positive territory, although thisremains a negligible business for Comcast. Despite the significant subscriber losses, video revenue was down only 0.6% yoy due to price increases. Revenue growth in CableCommunications was mainly driven by high-speed internet (+9.4%) and business services (+9.8%). NBCUniversal reported EBITDA up 8.1% to USD 2,324mn despite revenue being down 0.8%. All sub-segments showed positive EBITDA growth, but broadcast TV (+28.3%)and filmed entertainment (+33%) were the main growth drivers. Lower programming andproduction costs drove these increases, such as the absence of broadcasting expense for the 2018 FIFA World Cup. Sky reported a strong EBITDA increase of 19.9% in constant currency(CC) to USD 772mn despite a 2.4% revenue increase in CC. Sky benefitted from loweroperating expenses as contract termination costs and a settlement in 2Q18 negatively impacted EBITDA in that quarter (pro forma +3.2% in 1H19). Sky gained 304,000 customers(+4.4%) in 2Q19, which Comcast attributed to new content launches. OCF for the group in2Q19 was down slightly by 0.3% to USD 7,040mn and capex was up by 0.6% to USD 2,263mn, resulting in a 1.3% decline in FCF (before dividends) to USD 4,246mn. Thisbrings FCF to USD 8,838mn through 1H19. The company paid USD 1,823mn in dividends in1H19. Net debt was down to USD 103.5bn from USD 105.5bn in 1Q19 and leverage improved further to 3.1x compared to 3.2x in 1Q19 and 3.3x as of FYE 2018.

Expected development of credit profile/rating

Although Comcast continues to show weak video and voice customer trends in the US due tocord-cutting, price increases on video products and sustained strength in the highly profitable internet business has so far been able to more than offset this weakness. Sky, on the otherhand, continues to show strong subscriber trends. Comcast’s core businesses are highly cashgenerative, and both EBITDA growth and FCF generation are driving a sustaineddeleveraging trend. We think that further deleveraging in 2H19 would cause S&P to revise itsnegative outlook to stable. The agency set a threshold of 3.0x within two years as a target for the outlook revision. This should help to solidify SKYLN bonds as the strongest positionedwithin the high-grade media peer group.

Name recommendation We reiterate our overweight recommendation on Comcast’s SKYLN bonds. The bondscontinue to trade in line with those of BBB+ peers that do not show the same capacity orwillingness to improve their credit profile that Comcast has. We therefore see further potentialfor spread tightening as this is increasingly recognized in the market.

Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 12 See last pages for disclaimer.

Deutsche Telekom (Underweight) Event Deutsche Telekom (DT, Baa1n/BBB+wn/BBB+s) subsidiary T-Mobile US (63% stake)

reported strong 2Q19 results and raised its 2019 guidance. In 2Q19, revenues increased by 4% yoy to USD 11.0bn (consensus USD 11.1bn) and adjusted EBITDA went up by 7% yoyto EUR 3.5bn (consensus USD 3.4bn). Operating cash flow amounted to USD 2.1bn and resulted in free-cash-flow growth by 51% yoy to USD 1.2bn. All key figures hit a record levelfor a second quarter. Net debt excluding tower obligations came slightly down from USD26.5bn as of 31 March 2019 (2.1x leverage) to USD 26.4bn as of 30 June 2019 (2.0x leverage). Sales were supported by 1.8mn in total net additions in 2Q19 (+11% yoy) and1.1mn in branded postpaid net additions (+9% yoy). Postpaid branded phone churn fell by17bp yoy to 0.78%, an all-time record low.

T-Mobile US raised its FY19 outlook and now expects branded postpaid net additions of 3.5mn to 4.0mn, up from prior guidance of 3.1mn to 3.7mn. The adjusted EBITDA target isnow USD 12.9-13.3bn, which includes leasing revenues of USD 550-600mn, up from prior guidance of USD 12.7-13.2bn (consensus USD 12.4bn).

Expected development of credit profile/rating

The operating performance of T-Mobile US itself is supportive of DT’s credit profile but our focus remains on the impact the planned T-Mobile US/Sprint merger would have on DT. The decision by the US Justice Department (DoJ) is expected to be announced in the near term, perhaps even today.

Name recommendation The increased likelihood of approval of the T-Mobile US/Sprint transaction was a major reason for our recommendation change for DT bonds from marketweight to underweight(see Sector Flash, 6 June 2019). In a merger, DT’s exposure to a BB rated subsidiary would increase. As DT will continue to consolidate T-Mobile US, DT’s net leverage development will be affected. We believe that a T-Mobile US/Sprint merger would raise the ratio to the 3.00-3.50x range. The ratio is currently at the higher end of DT’s 2.25-2.75x net leverage target corridor.

Ulrich Scholz, CFA, FRM, Credit Analyst (UniCredit Bank, Munich) [email protected] Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 13 See last pages for disclaimer.

RELX Group (Marketweight) Event RELX Group (Baa1s/BBB+s/BBB+s) reported 1H19 results that showed a slight

deceleration in organic revenue and operating profit growth. Revenue of GBP 3,888mn was up 3% in underlying terms, but down from 4% growth recorded in 2018. Adjusted operating profit increased 4% to GBP 1,240mn, down from 6% growth in 2018. At thesegment level, Scientific, Technical & Medical showed a 1% increase in revenue toGBP 1,244mn (FY18: +2%) and 2% growth in operating profit to GBP 445mn (FY18: +2%). InRisk & Business Analytics, revenue was up 7% to GBP 1,149mn (FY18: +8%) and operatingprofit was up 8% to GBP 422mn (FY18: +8%). In Legal, revenue was up 2% to GBP 811mn(FY18: +2%) and operating profit was up 5% to GBP 149mn (FY18: +10%). In Exhibitions,revenue was up 5% to GBP 684mn (FY18: +6%) and operating profit was up 1% toGBP 231mn (FY18: +10%). At the segment level, RELX’s guidance confirmed that all segments should see similar trends in 2019 to those seen in 2018. Only in Exhibitions didRELX note that “cycling-out effects” would reduce the reported rate of revenue growth by 5pp.Through 1H19, RELX has completed eight acquisitions for GBP 246mn (1H18: GBP 710mn).The company completed GBP 400mn in share buybacks in 1H19 (1H18: GBP 500mn), with afurther GBP 200mn to come in 2H19. FCF (after dividends) came to GBP 216mn, up fromGBP 176mn in 1H18. However, the acquisition spending and share buybacks contributed to a GBP 463mn increase in net debt. Net leverage came to 2.6x (based on IFRS 16), and was upfrom 2.5x in the prior year (FYE 2018: 2.4x). RELX attributed this increase to a higher pensiondeficit, driven by lower discount rates. Excluding pensions and leases, leverage was stableyoy at 2.3x. RELX announced a 10% increase in its interim dividend after 12% growth in itsEPS (+8% in constant currency; operating profit was also +8% in reported terms).

Expected development of credit profile/rating

RELX confirmed its standard (vague) guidance, calling for positive underlying revenue andoperating profit growth in 2019. Based on the segment performance, it appears that cyclingeffects in the Exhibitions business are a major factor behind the slower growth rates andtherefore do not reflect an underlying weakening in the long-term growth trend. The Legal business continues to recover and generate solid profit growth, while the core Scientific,Technical & Medical business remains a solid – although not a dynamic – performer. This eases concerns of a forthcoming structural decline in this business from changing academicpublishing practices. It appears that RELX is managing these changes by continuallydeveloping its product portfolio in this key segment. We see the slight growth slowdown asprobably temporary and the modest increase in leverage as unproblematic given the solidcash flow trends in 1H19 relative to 1H18. We still see publishing companies with highly developed digital/subscription product portfolios, such as RELX, as facing some of the loweststructural risk among high-grade media peers.

Name recommendation We confirm our marketweight recommendation on RELLN bonds. The bonds have performedwell in recent months and we think they now trade fairly relative to key peers.

Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 14 See last pages for disclaimer.

Vivendi (Underweight) Event Vivendi (Baa2s/BBBs/BBBs) reported 1H19 results that again showed surging growth

at Universal Music Group (UMG) and lackluster results in the other segments. Like-for-like (lfl) group revenue grew 6.7% to EUR 7,353mn. EBITA was up disproportionately by 27.6% to EUR 718mn. The group results were driven by another strong quarter at UMG,which reported an 18.6% lfl revenue increase to EUR 3,258mn and EBITA up 43.6% toEUR 481mn. Subscription streaming revenue (+25.5%) and physical sales (+15%) continued to more than offset the decline in revenue from music downloads (-19.7%). Music publishing (+10.5%) and merchandising (+82.3%) also contributed to UMG’s revenue growth. Canal+showed a mixed picture, with revenue down 2.2% in lfl terms to EUR 2,518mn. Revenue from TV in mainland France weakened on the back of a further decline in subscribers (-263,000), although this was largely offset by a rise in subscribers in the international business(+361,000). The broadcasting of the Africa Cup of Nations provided support here. ARPU in France was also down by EUR 1 to EUR 44.5. EBITA at Canal+ before restructuring came toEUR 236mn in 1H19, or a decline of 4.8% yoy. This segment is working to furtherinternationalize its business while restructuring in mainland France. Havas reported organic net revenue growth of 0.2% to EUR 1,061mn. EBITA of EUR 108mn was up 2.0% in 1H19.The recently consolidated Editis business posted revenue growth of 1.2% to EUR 260mn withEBITA of EUR 4mn (since 1 February). The other segments – Gameloft (EUR -11mn), Vivendi Village (EUR -9mn) and New Initiatives (EUR -29mn) – continue to be loss-making on the EBITA level. In 1H19, net debt rose to EUR 2.1bn compared to EUR 0.2bn in net cash as of FYE 2018 due mainly to the acquisition of Editis for EUR 0.8bn, dividends of EUR 0.6bn and the EUR 0.9bn share buyback program.

Expected development of credit profile/rating

The main driver of Vivendi’s credit profile in the medium term will be the outcome of thecompany’s plan to sell a stake of up to 50% in UMG through an IPO. So far, Vivendi hasrepeatedly said that it would use the proceeds from the stake sale for acquisitions and for“significant" shareholder remuneration. Vivendi confirmed that it has selected banks to leadthe stake sale and thinks that the process could be completed by early 2020. Since Vivendihas not indicated that any of the proceeds would be used to pay down debt, we view thestake sale as credit negative as Vivendi would lose proportionate control of its only strongly growing asset. Vivendi has a mixed track record with acquisitions, so we think that hit-and-miss results of the ensuing M&A are likely to leave the group with a weakened credit profile.Beyond M&A, Vivendi reiterated in the conference call that shareholder remuneration is a “priority” and that buybacks would account for a “significant” share of the use of proceedsfrom the IPO, which is also clearly credit negative.

Name recommendation We confirm our underweight recommendation on VIVFP. VIVFP bonds have not performed well relative to peers after shareholder remuneration and acquisitions in 1H19 erased the company’s net cash position and drove up net debt. We remain cautious toward Vivendi untilfinal details on the UMG sale are released and assume that boosting shareholder returns remains paramount to Vivendi’s ongoing portfolio management strategy.

Jonathan Schroer, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13212, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 15 See last pages for disclaimer.

Consumer

Roche (Marketweight) Event Roche’s (Aa3s/AAs/AAs) 1H19 results were boosted by its new drug pipeline and came

in better than anticipated (Bloomberg consensus). The outlook for 2019 has beenincreased. In 1H19, group sales increased by 8% in CHF and 9% at constant currency toCHF 30,469mn. Core operating profit increased by 11% to CHF 12,363mn (margin 40.6%).Sales in the Pharmaceuticals division increased by 10% to CHF 24.2bn. The company’s keygrowth drivers were the multiple sclerosis medicine Ocrevus, the new hemophilia medicineHemlibra and cancer medicines Tecentriq, Perjeta and Avastin. The strong uptake of newlyintroduced medicines more than offset lower sales of Herceptin (down 8% yoy) andMabThera/Rituxan (down 4%). The Diagnostics division sales increased by 2% to CHF 6.3bn.At 30 June 2019, operating free cash flow of CHF 7.5bn (-9% yoy) was lower yoy due tohigher net working capital and higher investment in intangible assets. At 30 June 2019, net debt was CHF 8.4bn (30 June 2018: CHF 11.7bn) and higher than it was at the end of 2018due to dividend payments (31 December 2018: CHF 5.7bn).

Expected development of credit profile/rating

Management increased its outlook for 2019 to mid-to-high-single-digit sales growth (previously: mid-single-digit growth). The outlook for core EPS growth to be broadly in linewith sales and further increase in dividend in CHF was maintained. This guidance still seemsbe conservative compared to Bloomberg consensus.

In our view, patent cliff (for Avastin, Herceptin and Rituxan) will be manageable because thegrowth of its new products (particularly Perjeta, Ocrevus and Tecentriq) will offset revenuelost to biosimilar competition over the next two to three years. In 1H19, the strong performance of Ocrevus (up 63% yoy to CHF 1,735mn), Perjeta (up 34% yoy toCHF 1,755mn), Alencensa (up 50% yoy to CHF 421mn) and Tecentriq (up 141% yoy toCHF 782mn) more than outweighed the pressure on MabThera (down 4%) and Herceptin (down 9%) following the entry of biosimilar competition. Roche has ten products that eachgenerated more than USD 1.0bn in 2018. This portfolio of strong brands benefits from solidmargins, which we believe to be significantly higher than the overall group EBITA margin, enabling Roche to generate healthy free cash flow (FCF) amounting to CHF 5.3bn (30 June2019). For 2019, we estimate further slight deleveraging to 1.1x (FY18: 1.2x).

Name recommendation Despite the tight spread levels, we confirm our marketweight recommendation on Roche. We like Roche’s strong cash flow generation, its deleveraging since the Genentech acquisition in2019 and its strong pipeline.

Dr. Silke Stegemann, CEFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-18202, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 16 See last pages for disclaimer.

Danone (Marketweight) Yesterday, Danone reported its 1H19 key results and confirmed its outlook for 2019. In

1H19, sales increased by 1.7% (like-for-like) to EUR 12,498mn and recurring operating income by 6.4% to EUR 1,858mn. As of 30 June 2019, free cash flow had remained more orless stable yoy at EUR 1,083mn and net debt (reported) had slightly increased to EUR 13.9bn (FY18: EUR 12.7bn).

Danone’s management confirmed its outlook for 2019 with like-for-like sales growth of around 3% and a recurring operating income margin above 15%. The company’s 2020 objectiveshave been confirmed: accelerate like-for-like sales growth, maximize efficiencies and allocate capital with discipline. We expect further growth in the profitable specialized nutritionbusinesses and stable earnings from bottled water. Since the 2016 Whitewave acquisition,cash flow has been largely dedicated to repaying debt. We estimate that Danone’s adjustednet leverage will remain in the 3.0-3.5x range (FY18: 3.3x).

We confirm our marketweight recommendation on Danone, supported by its strong businessrisk profile as a leading global player in fresh diary and plant-based products, infant milk nutrition and water bottling. In our FOB universe, Danone is the only company with anoutstanding perp. We prefer the BNFP perp versus the outstanding BNFP seniorsdenominated in EUR.

Dr. Silke Stegemann, CEFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-18202, [email protected]

Diageo (Marketweight) Diageo (A3s/A-s/A-s) has published its FY19 preliminary results (year ended 30 June 2019),

which showed a slight increase in net leverage as expected. In FY19, reported net sales grew 5.8% yoy to GBP 12.9bn, mainly driven by organic growth and favorable exchangerates, and partly offset by acquisitions and disposals. All regions and categories contributed to broad-based organic net sales growth of 6.1%, which is above 5% in FY18, 4.3% in FY17 and2.8% in FY16. Operating profit before exceptional items was GBP 4,116mn (FY17/18:GBP 3,819mn). The reported operating margin increased to 32% (FY18: 31.4%). Net cash from operating activities was GBP 3.2bn (up GBP 164mn). Free cash flow continued to bestrong at GBP 2.6bn, an increase of GBP 85mn yoy (FY18: GBP 2.5bn; FY17: GBP 2.7bn; FY16:GBP 2.1bn; FY15: GBP 2.0bn). In FY19, Diageo returned GBP 2.8bn to shareholders through share buybacks. Adjusted net debt/EBITDA came in at 2.5x (FY18: 2.2x). The company’sadjusted net debt includes post-employment-plan-benefit liabilities.

Diageo’s management remains committed to its leverage policy of adjusted net debt/EBITDA in the range of 2.5-3.0x. We assume stable net leverage in FY20 and a slight decreasein FY21. As part of its medium-term guidance, Diageo assumes consistent mid-single-digit organic net sales growth and sustainable organic operating profit growth about 1% ahead of net sales, within a range of 5-7%. On 25 July 2019, the board approved plans for a further return of up to GBP 4.5bn in capital to shareholders in the period FY20 to FY22.

We confirm our marketweight recommendation on Diageo. Diageo’s business-risk profile is supported by its position as the number one global player in the alcoholic beverage sector withsound diversity by products, brands, and regions. The company owns world-leading brands (including Johnnie Walker, Smirnoff, Tanqueray, and Guinness) and operates in the majority ofproduct categories (such as vodka, rum, gin, whiskey, and beer). Diageo enjoys also a strongbalance in terms of exposure to emerging markets (about 40% of sales). Its EBITDA margin(35-38%) is higher than that of peers such as Pernod Ricard. Since 1 January 2019, DGELN issues denominated in EUR have slightly outperformed the iBoxx EUR FOB index. Only the

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 17 See last pages for disclaimer.

DGELN 0.25% 10/21 and DGELN 0% 11/20 issues have underperformed.

Dr. Silke Stegemann, CEFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-18202, [email protected]

LVMH (Marketweight) LVMH (A1s/A+s/--) reported 1H19 results that were in line with Bloomberg consensus

estimates. Profit from recurring operations was EUR 5.3bn (up from EUR 4.6bn in 1H18) compared to the Bloomberg consensus estimate of EUR 5.37bn.

The Fashion & Leather Goods segment reported the highest yoy growth, to EUR 3.2bn fromEUR 2.8bn. Revenues in the segment increased to EUR 10.4bn from EUR 8.6bn but theoperating margin fell by 1pp to 31.2%.

LVMH’s cash flows were negatively impacted by higher working capital outflows of EUR 1.9bn yoy on the back of higher inventory requirements and cash required for the decline in trade accounts payables. Company-adjusted operating FCF declined by EUR 262mn to EUR 1.7bn. In addition, LVMH paid EUR 1.9bn for the acquisition of Belmond and around EUR 2.4bn in dividends. Company-adjusted net financial debt (which does not include capitalized leases due to IFRS 16) increased to EUR 8.7bn from EUR 5.5bn, while gearing was at 25% at end-1H19,up from 16% in 1H18.

We maintain our marketweight recommendation on the name and positively note thecompany’s strong position in the global personal luxury industry and its strong businessprofile. Nevertheless, from a credit-investor point of view, we see the relatively high dividend payments and business-risk exposure to fashion as a downside. We think the MCFP cashcurve is trading at fair levels in relation to the company’s credit profile.

Mehmet Dere, Credit Analyst (UniCredit Bank, Munich) +49 89 378 11294, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 18 See last pages for disclaimer.

High Yield

Ardagh (Hold) Event Ardagh reported 2Q19 results that revealed weaker underlying operating performance.

The company confirmed its full-year guidance. Adjusted EBITDA was USD 395mn, in linewith the company’s guidance for the quarter, but slightly below market consensus. EBITDA wasup by 5% excluding exchange-rate impacts; however, excluding the positive impacts from IFRS16 of USD 24mn, EBITDA would have been lower yoy. In the quarter, the company reported 1%higher beverage can volumes globally with volume/mix growth of 6%. Glass Packaging NorthAmerica continued to be impacted by lower volumes, while Metal Packaging Europe wasweighed down by higher input costs. Company-adjusted FCF turned negative in the quarter(minus USD 50mn), mainly due to higher working capital outflows. Net leverage (excluding thePiKs) stood at 5.3x at the end of 2Q (secured net leverage at 1.9x), slightly up qoq.

Expected development of credit profile/rating

For FY19, the company confirmed its outlook, which includes the expectation of adjustedEBITDA of at least USD 1.5bn (pro forma the divestment: of at least USD 1.15bn). This isexpected to be driven by organic growth in three of the company’s four segments, as well asa positive accounting impact of USD 80mn (resulting from the capitalization of operatingleases on the balance sheet due to IFRS 16) that should more than offset FX headwind andsome inflationary headwinds (which might be passed on to some extent). For 3Q, thecompany expects adjusted EBITDA of USD 410-420mn. Full-year adjusted FCF is forecast atabout USD 450mn (FY18: USD 441mn), with the forecast for capex at USD 590mn, includingUSD 90mn of short payback projects.

Pro forma the divestment of its Food & Specialty Metal packaging business to form Trivium, thecompany will deleverage by around 0.5x. Given Ardagh’s track record, we assume that leveragewill not remain at these levels, and we expect re-leveraging of the business either through M&Aor – less attractive from a bondholder perspective – by taking out a special dividend.

Name recommendation We have a hold recommendation on Ardagh.

Jana Schuler, CFA, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-13211, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 19 See last pages for disclaimer.

Jaguar Land Rover (Sell) Event Tata Motors (Ba3n/B+wn/BB-n), parent of Jaguar Land Rover Automotive Plc

(B1n/B+wn/BB-n), has reported JLR’s 1Q19/20 key figures: retail sales (including CJLR) down by 11.6%, wholesales (including CJLR) -9.9% yoy, revenues -2.8% yoy, EBITDA down to GBP 213mn (compared to GBP 324mn yoy), EBIT margin down to -5.5% (compared to -3.7% yoy), EBITDA margin down to 4.2% (compared to 6.2% yoy), EBT (before exceptional items) down to GBP -383mn (compared to GBP -264mn yoy) and FCF to GBP -719mn (compared to GBP -1,674mn yoy).

Expected development of credit profile/rating

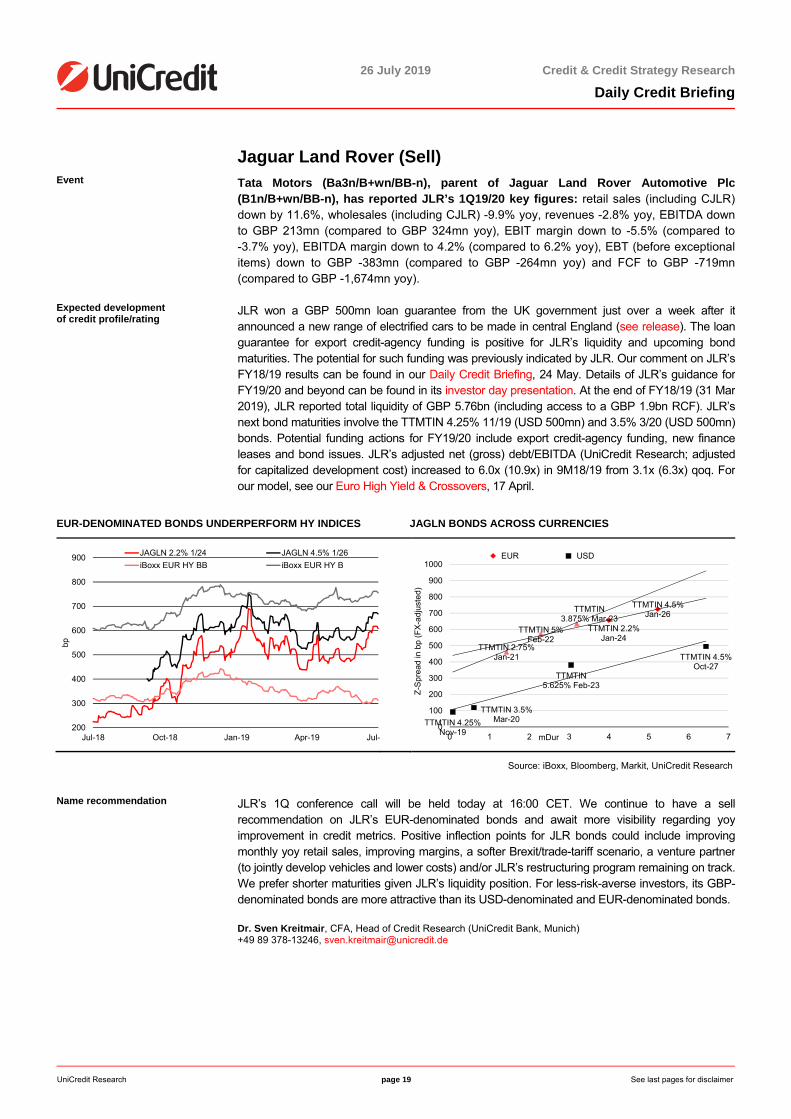

JLR won a GBP 500mn loan guarantee from the UK government just over a week after it announced a new range of electrified cars to be made in central England (see release). The loan guarantee for export credit-agency funding is positive for JLR’s liquidity and upcoming bondmaturities. The potential for such funding was previously indicated by JLR. Our comment on JLR’s FY18/19 results can be found in our Daily Credit Briefing, 24 May. Details of JLR’s guidance forFY19/20 and beyond can be found in its investor day presentation. At the end of FY18/19 (31 Mar 2019), JLR reported total liquidity of GBP 5.76bn (including access to a GBP 1.9bn RCF). JLR’s next bond maturities involve the TTMTIN 4.25% 11/19 (USD 500mn) and 3.5% 3/20 (USD 500mn)bonds. Potential funding actions for FY19/20 include export credit-agency funding, new finance leases and bond issues. JLR’s adjusted net (gross) debt/EBITDA (UniCredit Research; adjusted for capitalized development cost) increased to 6.0x (10.9x) in 9M18/19 from 3.1x (6.3x) qoq. For our model, see our Euro High Yield & Crossovers, 17 April.

EUR-DENOMINATED BONDS UNDERPERFORM HY INDICES JAGLN BONDS ACROSS CURRENCIES

Source: iBoxx, Bloomberg, Markit, UniCredit Research

Name recommendation JLR’s 1Q conference call will be held today at 16:00 CET. We continue to have a sell recommendation on JLR’s EUR-denominated bonds and await more visibility regarding yoy improvement in credit metrics. Positive inflection points for JLR bonds could include improvingmonthly yoy retail sales, improving margins, a softer Brexit/trade-tariff scenario, a venture partner (to jointly develop vehicles and lower costs) and/or JLR’s restructuring program remaining on track. We prefer shorter maturities given JLR’s liquidity position. For less-risk-averse investors, its GBP-denominated bonds are more attractive than its USD-denominated and EUR-denominated bonds.

Dr. Sven Kreitmair, CFA, Head of Credit Research (UniCredit Bank, Munich) +49 89 378-13246, [email protected]

200

300

400

500

600

700

800

900

Jul-18 Oct-18 Jan-19 Apr-19 Jul-

bp

JAGLN 2.2% 1/24 JAGLN 4.5% 1/26

iBoxx EUR HY BB iBoxx EUR HY B

TTMTIN 4.5% Jan-26

TTMTIN 2.2% Jan-24

TTMTIN 4.5% Oct-27

TTMTIN 5.625% Feb-23

TTMTIN 3.5% Mar-20TTMTIN 4.25%

Nov-19

TTMTIN 3.875% Mar-23

TTMTIN 5% Feb-22

TTMTIN 2.75% Jan-21

0

100

200

300

400

500

600

700

800

900

1000

0 1 2 3 4 5 6 7

Z-S

pre

ad in

bp

(FX

-adj

uste

d)

mDur

EUR USD

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 20 See last pages for disclaimer.

LKQ (Buy) Event LKQ’s (Ba2s/BBs) 2Q19 results (see presentation) showed total revenues up by 7.2%

(organic -2.4%, acquisitions +12.0%, FX -2.4%), with organic growth for parts and services down by 2.1%. Organic growth in North America was down 0.4% and was -4.3% in Europe (and +0.1% at Specialty). Its segment EBITDA margin in 2Q was down by 30bp to 11.0% yoy, primarily as a result of its mix, as Europe is now LKQ’s largest segment by revenue. That of North America (53% of segment EBITDA and generating the highestmargins among LKQ’s segments) in 2Q was up by 130bp to 14.4% given an increase in grossmargin by 100bp. That of Europe was down to 7.7%, compared to 8.6% yoy, and that of Specialty was down to 12.7% (13.6% yoy), as the gross margin was down by 30bp. FCF (before special items) in 1H19 amounted to USD 537mn (USD 213n yoy), and net debt (company definition) decreased to USD 3,710mn, compared to USD 3,948mn qoq at an effective borrowing rate of 3.3% in 2Q19. At the end of 2Q19, LKQ’s cash and cash equivalents amounted to USD 376mn, compared to USD 316mn, and total revolver availability amounted to USD 1,574mn.

Expected development of credit profile/rating

Net debt/EBITDA (company definition) was slightly down to 2.8x, compared to 2.9x qoq.At 3.8x qoq, adjusted net leverage (UniCredit Research, not adjusted for acquisitions) was flat but up compared to 3.7x yoy.

LKQ’s FY19 guidance was adjusted to a lower (but still positive) organic-growth rate but higher FCF: organic revenue growth of 0.5-2.0% (previously 2.0-4.0%) at Parts and Services (FY18: 4.4%); cash flow from operations of USD 800-875mn (previously: USD 775-850mn; FY18: USD 711mn) and capex of USD 225-275mn (previously USD 250-300mn; FY18: USD 250mn), resulting in FCF of USD 525-650mn (previously: USD 475-600mn; FY18: USD 461mn). For more details on LKQ’s credit profile and on our financial model, see our latest Euro High Yield & Crossovers publication (17 April).

Organic growth at Parts and Services is expected to be more resilient in downturns than thatof the Auto manufacturers and Suppliers businesses overall. This is credit-positive for LKQ, which also does not pay any dividends, generated USD 397mn on average of annual FCF(before M&A) in 2015-18 and had a low capex/sales ratio of 2.1% in FY18 (and of between1.8% and 2.6% in 2011-18) – in addition to decent EBITDA margins of 10-13% (2011-18). We believe LKQ’s bonds would outperform in a cyclical downturn. Despite its very strong FCF-generation capacity, deleveraging or a rating upgrade are quite unlikely given LKQ’sacquisition and growth strategies. LKQ’s net leverage covenants in its senior secured facilitiesare for a maximum of 3.5x net debt/EBITDA (2Q19: 2.8x) and a minimum of 3.0x interestcoverage. The net leverage covenant is, however, allowed to increase to 4.0x followingacquisitions of more than USD 200mn. However, it must revert back to 3.5x over fourconsecutive fiscal quarters.

Name recommendation We are keeping our buy recommendation on LKQ’s euro-denominated bonds. Leverage in 2Q19 was slightly down, and FCF guidance was increased. Organic growth at LKQ’s Partsand Services business was negative in 2Q19, but it should still continue to be more resilient during downturns than that of the cyclical automotive sector. Now that LKQ generates FCF ofaround USD 500mn p.a., it has regained some covenant headroom. A major risk for LKQbondholders is whether LKQ will pursue its next larger acquisition (however, within the covenants). In line with its recent acquisition history and a USD 500mn share-repurchase program, we do not expect its ratings to be upgraded. We prefer LKQ’s longest-dated bond,LKQ 4/28 (which is quite small and less-liquid, at EUR 250mn). We note that the USD-denominated 5/23 bond (USD 600mn) has been callable and that its call price, at 101.583, has decreased since 15 May 2019.

Dr. Sven Kreitmair, CFA, Head of Credit Research (UniCredit Bank, Munich) +49 89 378-13246, [email protected]

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 21 See last pages for disclaimer.

Banks

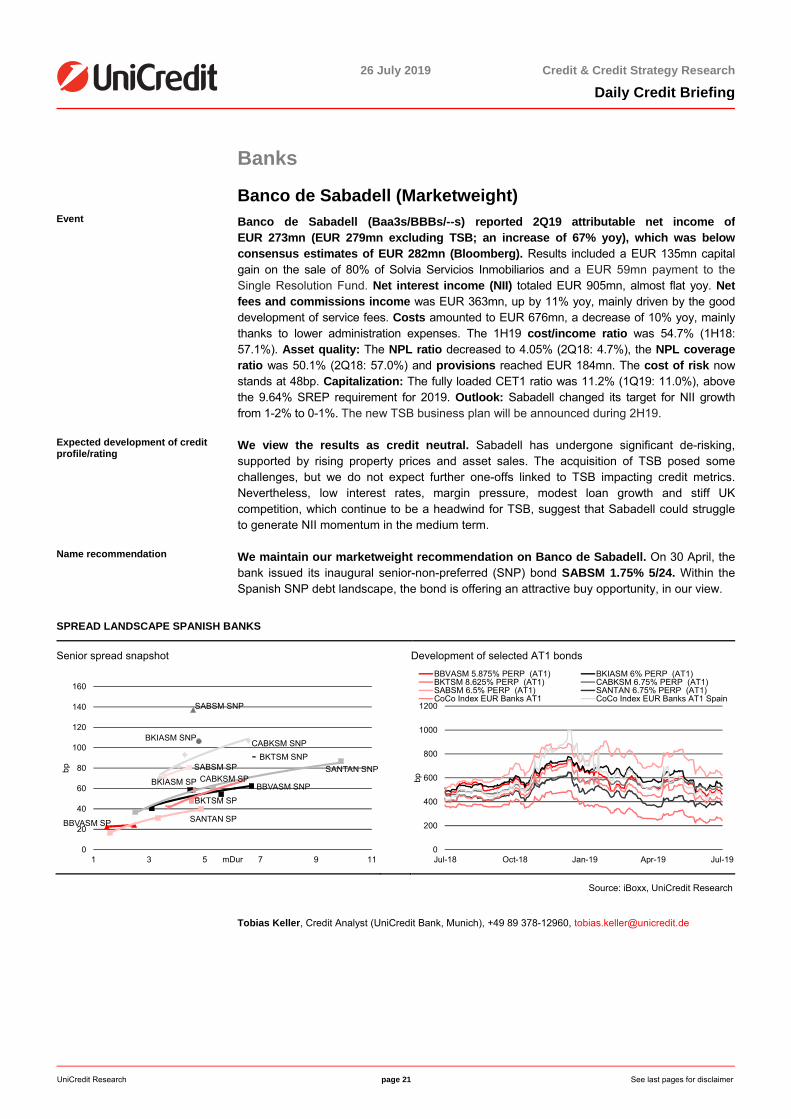

Banco de Sabadell (Marketweight) Event Banco de Sabadell (Baa3s/BBBs/--s) reported 2Q19 attributable net income of

EUR 273mn (EUR 279mn excluding TSB; an increase of 67% yoy), which was belowconsensus estimates of EUR 282mn (Bloomberg). Results included a EUR 135mn capital gain on the sale of 80% of Solvia Servicios Inmobiliarios and a EUR 59mn payment to the Single Resolution Fund. Net interest income (NII) totaled EUR 905mn, almost flat yoy. Net fees and commissions income was EUR 363mn, up by 11% yoy, mainly driven by the good development of service fees. Costs amounted to EUR 676mn, a decrease of 10% yoy, mainly thanks to lower administration expenses. The 1H19 cost/income ratio was 54.7% (1H18: 57.1%). Asset quality: The NPL ratio decreased to 4.05% (2Q18: 4.7%), the NPL coverage ratio was 50.1% (2Q18: 57.0%) and provisions reached EUR 184mn. The cost of risk now stands at 48bp. Capitalization: The fully loaded CET1 ratio was 11.2% (1Q19: 11.0%), above the 9.64% SREP requirement for 2019. Outlook: Sabadell changed its target for NII growth from 1-2% to 0-1%. The new TSB business plan will be announced during 2H19.

Expected development of credit profile/rating

We view the results as credit neutral. Sabadell has undergone significant de-risking, supported by rising property prices and asset sales. The acquisition of TSB posed somechallenges, but we do not expect further one-offs linked to TSB impacting credit metrics. Nevertheless, low interest rates, margin pressure, modest loan growth and stiff UK competition, which continue to be a headwind for TSB, suggest that Sabadell could struggleto generate NII momentum in the medium term.

Name recommendation We maintain our marketweight recommendation on Banco de Sabadell. On 30 April, the bank issued its inaugural senior-non-preferred (SNP) bond SABSM 1.75% 5/24. Within the Spanish SNP debt landscape, the bond is offering an attractive buy opportunity, in our view.

SPREAD LANDSCAPE SPANISH BANKS

Senior spread snapshot Development of selected AT1 bonds

Source: iBoxx, UniCredit Research

Tobias Keller, Credit Analyst (UniCredit Bank, Munich), +49 89 378-12960, [email protected]

BKIASM SP

BKIASM SNP

BKTSM SP

BKTSM SNP

SABSM SNP

BBVASM SP

BBVASM SNPCABKSM SP

CABKSM SNP

SABSM SP

SANTAN SP

SANTAN SNP

0

20

40

60

80

100

120

140

160

1 3 5 7 9 11

bp

mDur0

200

400

600

800

1000

1200

Jul-18 Oct-18 Jan-19 Apr-19 Jul-19

bp

BBVASM 5.875% PERP (AT1) BKIASM 6% PERP (AT1)BKTSM 8.625% PERP (AT1) CABKSM 6.75% PERP (AT1)SABSM 6.5% PERP (AT1) SANTAN 6.75% PERP (AT1)CoCo Index EUR Banks AT1 CoCo Index EUR Banks AT1 Spain

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 22 See last pages for disclaimer.

CaixaBank (Marketweight) Event 2Q19 results presentation

CaixaBank (Baa1s/BBB+s/BBB+s) reported 2Q19 net attributable income of EUR 89mn (down 85.1% yoy but up by 30.3% adjusted), well above consensus expectations of a loss of EUR 21mn. The performance was adversely impacted by the labor agreement reached in 2Q19 regarding a plan of 2,023 compensated terminations, which entailed an expense of EUR 978mn. Excluding the extraordinary expenses, attributable profit grew by 30.3%yoy. Net interest income (NII) totaled EUR 1.24bn, up by 1% yoy, driven by an increase in income from loans and lower retail and institutional financing expenses. Net fees and commissions income was EUR 636mn, down by 5% yoy, impacted by lower one-off fees and commissions from investment banking. Recurring administrative expenses, depreciation and amortization amounted to EUR 1.2bn, up by 4% yoy, largely due to higher personnel expenses. RoE was 4.9%. The cost/income ratio was 67.0% (55.4% not considering extraordinary expenses). Asset quality: The NPL ratio decreased by 0.4pp to 4.2%, close tothe bank’s target of 4% for FY19 (below 3% by FYE 2021). The NPL coverage ratio was 54%.Capitalization: The fully loaded CET1 ratio remained flat qoq at 11.6%, well above the 8.75% SREP requirement for 2019. The leverage ratio was 5.5%. CaixaBank stated that its MREL of 21.2% at 2Q19 represented a solid base to achieve the 22.5% requirement (in 2021).TheBPI segment, which relates to Banco BPI (Ba1s/BBBs/BBBs) and excludes Banco BPI’s minority stakes, contributed 2Q19 consolidated profit of EUR 40mn, compared to EUR 36mn in 2Q18 (up by 11%). Outlook: The restructuring will result in cost savings (approximate savings of EUR 200mn on an annual basis and EUR 80mn in 2Q19.

Expected development of credit profile/rating

We view the results as credit neutral. The underlying operating performance of CaixaBank looks strong, in particular NII. We expect the bank to continue to gradually enhance its credit profile, and asset quality in particular, by reducing its NPL exposure and progressively improving its core profitability. Further improvement may be challenged by persistently low interest rates. Due to its relatively large IRPH exposure (EUR 6.7bn at 1Q19), CaixaBank ismore exposed than peers to the European ruling on the IRPH mortgage case. A preliminary ruling is expected by 10 September 2019. However, this ruling will not be binding and we donot expect a final judgment before year-end 2019 or early 2020. Possible outcomes range from confirming that IRPH is a correct way to price mortgages to making Spanish banks pay back part of the excess interest paid by customers. In any case, we expect CaixaBank to beable to manage the potential impact, thanks to its sound fundamentals.

Name recommendation We maintain our marketweight recommendations on CaixaBank and Banco BPI. Within the Spanish senior non-preferred (SNP) debt landscape, CABKSM 2.375% 2/24 looksattractive in our view. We think it is trading relatively wide, considering the strong creditfundamentals of the bank, which compare well with the Spanish average. CaixaBank’s business is geographically focused on Spain and Portugal, meaning it is less exposed thanthe two national champions to potential risks inherent in operating in emerging markets. Considering CaixaBank’s MREL ratio, we expect the bank to continue issuing SNP instruments in line with its 2019-2021 funding plan. As Banco BPI has no major subordinated or senior bonds outstanding, we do not have any trade or relative-value considerations on the subsidiary.

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 23 See last pages for disclaimer.

SPREAD LANDSCAPE, SPANISH BANKS

Senior spread snapshot Development of selected AT1 bonds

Source: iBoxx, UniCredit Research

Tobias Keller, Credit Analyst (UniCredit Bank, Munich) +49 89 378-12960, [email protected]

BKIASM SP

BKIASM SNP

BKTSM SP

BKTSM SNP

SABSM SNP

BBVASM SP

BBVASM SNPCABKSM SP

CABKSM SNP

SABSM SP

SANTAN SP

SANTAN SNP

0

20

40

60

80

100

120

140

160

1 3 5 7 9 11

bp

mDur0

200

400

600

800

1000

1200

Jul-18 Oct-18 Jan-19 Apr-19 Jul-19

bp

BBVASM 5.875% PERP (AT1) BKIASM 6% PERP (AT1)BKTSM 8.625% PERP (AT1) CABKSM 6.75% PERP (AT1)SABSM 6.5% PERP (AT1) SANTAN 6.75% PERP (AT1)CoCo Index EUR Banks AT1 CoCo Index EUR Banks AT1 Spain

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 24 See last pages for disclaimer.

Insurance

Mapfre (Marketweight) Event 1H19 results

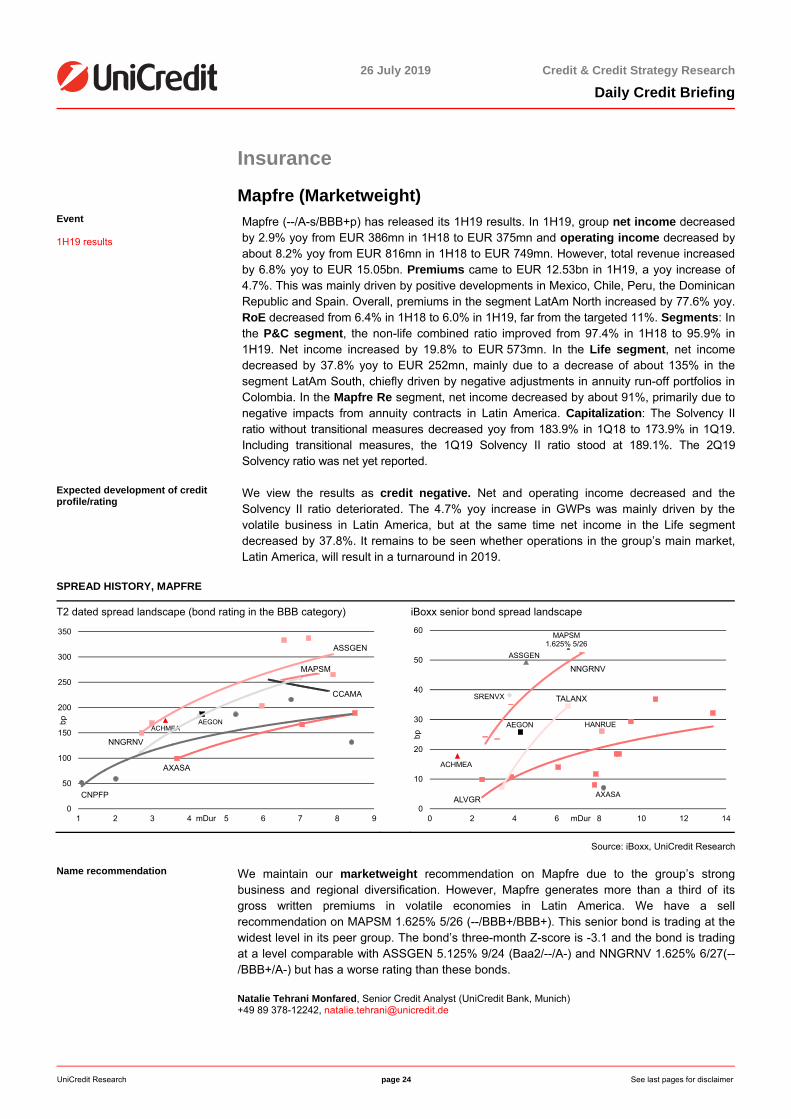

Mapfre (--/A-s/BBB+p) has released its 1H19 results. In 1H19, group net income decreased by 2.9% yoy from EUR 386mn in 1H18 to EUR 375mn and operating income decreased by about 8.2% yoy from EUR 816mn in 1H18 to EUR 749mn. However, total revenue increased by 6.8% yoy to EUR 15.05bn. Premiums came to EUR 12.53bn in 1H19, a yoy increase of 4.7%. This was mainly driven by positive developments in Mexico, Chile, Peru, the Dominican Republic and Spain. Overall, premiums in the segment LatAm North increased by 77.6% yoy. RoE decreased from 6.4% in 1H18 to 6.0% in 1H19, far from the targeted 11%. Segments: In the P&C segment, the non-life combined ratio improved from 97.4% in 1H18 to 95.9% in 1H19. Net income increased by 19.8% to EUR 573mn. In the Life segment, net income decreased by 37.8% yoy to EUR 252mn, mainly due to a decrease of about 135% in the segment LatAm South, chiefly driven by negative adjustments in annuity run-off portfolios in Colombia. In the Mapfre Re segment, net income decreased by about 91%, primarily due to negative impacts from annuity contracts in Latin America. Capitalization: The Solvency II ratio without transitional measures decreased yoy from 183.9% in 1Q18 to 173.9% in 1Q19. Including transitional measures, the 1Q19 Solvency II ratio stood at 189.1%. The 2Q19 Solvency ratio was net yet reported.

Expected development of credit profile/rating

We view the results as credit negative. Net and operating income decreased and the Solvency II ratio deteriorated. The 4.7% yoy increase in GWPs was mainly driven by the volatile business in Latin America, but at the same time net income in the Life segment decreased by 37.8%. It remains to be seen whether operations in the group’s main market, Latin America, will result in a turnaround in 2019.

SPREAD HISTORY, MAPFRE

T2 dated spread landscape (bond rating in the BBB category) iBoxx senior bond spread landscape

Source: iBoxx, UniCredit Research

Name recommendation We maintain our marketweight recommendation on Mapfre due to the group’s strong business and regional diversification. However, Mapfre generates more than a third of itsgross written premiums in volatile economies in Latin America. We have a sellrecommendation on MAPSM 1.625% 5/26 (--/BBB+/BBB+). This senior bond is trading at the widest level in its peer group. The bond’s three-month Z-score is -3.1 and the bond is trading at a level comparable with ASSGEN 5.125% 9/24 (Baa2/--/A-) and NNGRNV 1.625% 6/27(--/BBB+/A-) but has a worse rating than these bonds.

Natalie Tehrani Monfared, Senior Credit Analyst (UniCredit Bank, Munich) +49 89 378-12242, [email protected]

ACHMEA AEGON

AXASA

CNPFP

ASSGEN

CCAMA

MAPSM

NNGRNV

0

50

100

150

200

250

300

350

1 2 3 4 5 6 7 8 9

bp

mDur

ACHMEA

AEGON

AXASA

HANRUE

MAPSM 1.625% 5/26

SRENVX

ASSGEN

ALVGR

NNGRNV

TALANX

0

10

20

30

40

50

60

0 2 4 6 8 10 12 14

bp

mDur

26 July 2019 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 25 See last pages for disclaimer.

Sub-Sovereigns

Deutsche Bahn (Marketweight) Event 1H19 results press release

Yesterday, Deutsche Bahn (Aa1s/AA-s/AAs) announced its 1H19 financial results. DB Group’s adjusted revenue in 1H19 increased to EUR 22bn (+2.2% yoy). Adjusted earnings before interest and taxes (EBIT) declined to EUR 757mn compared to EUR 974mn in 1H18 (decrease of 22% yoy), which was, according to DB, primarily driven by investment in additional measures to improve quality and performance.

DB’s net financial debt rose to EUR 25.4bn by the end of 1H19 (FY18: EUR 19.5bn). This was primarily driven by new accounting standards, which include operating leases in debt. According to DB, the company’s debt would have been flat at around EUR 20bn without theaccounting changes.

In terms of passengers, DB achieved another record in its long-distance transport segment. In 1H19, 71.8mn passengers used ICE and IC services, the fifth increase in a row. For FY19, DB expects to transport 150mn long-distance passengers. Long-distance punctuality has risen to 77.2% in 1H19 (FY18: 74.9%) and is above the FY19 target of 76.5%.

DB expects to record FY19 revenue of more than EUR 45bn and adjusted EBIT of atleast EUR 1.9bn, and for net capital expenditure to rise to over EUR 5.5bn compared toEUR 4.0bn in the previous year (up by 37.5% yoy). DB will invest in new trains, in improving quality and punctuality, improving travel comfort and in hiring staff. With the new “Powerful Rail” strategy, published in June 2019, DB plans to expand its rail infrastructurecapacity by 30% and will hire 100,000 new employees in the coming years (22,000 in 2019).The strategy also includes the plan to sell DB Arriva, as it has little strategic relevance, according to the company. According to yesterday’s release, preparations for a sale ofDB Arriva are going well and a number of parties have expressed interest.

Expected development of credit profile/rating

We view the results as credit neutral. Deutsche Bahn is a government-related issuer because it is wholly owned by the Federal Republic of Germany (Aaas/AAAs/AAAs). DB does not benefitfrom an explicit or implicit guarantee from the German government, but government support isstrong and the government has a constitutional obligation to provide functional rail infrastructure,which ensures a stable operating environment. It is likely that the German government wouldgrant support to DB should the issuer need it. We do not expect any negative rating pressure from the higher debt level, since the increase is driven by accounting changes, in particular theinclusion of operating leases. Rating agencies already factor in this adjustment in the adjusteddebt measure under their corporate rating methodologies.

Name recommendation We keep our recommendation at marketweight relative to the iBoxx EUR Sub-sovereign index. Benchmark investors can gain sovereign-related exposure through the name at spread levels that are more attractive than guaranteed German SSA issuers. Longer-dated DBHNGR bonds currently trade with a 40bp spread premium to German agencies (government guaranteed) and at roughly 100bp over Bunds.