corporation bank - direct research report - enam direct...

TRANSCRIPT

Corporation Bank

ENAM Securities Direct 3rd April 2012

ENAM DIRECT EQUITY RESEARCH

CO

MP

AN

Y R

EP

OR

T

For private circulation only

NIMs to Expand; Asset Quality to Remain Stable Corporation Bank is a mid-sized public sector bank all set to enter its next growth phase. During the past 5 years, Corporation Bank has exhibited robust loan growth (CAGR of 30%) and stable asset quality (average net NPA of 0.4%) in line with the best in the industry.

Corporation bank at a point of inflection: With its aggressive branch expansion plans from less than 1000 branches in FY08 to 1700 branches by FY13 (1431 in Q3FY12), Corporation Bank is all set for the next round of growth. We expect contribution from newly setup branches to start kicking in from FY13 leading to 100-125 bps improvement in CASA ratio every year till FY15. Consequently, net interest margin would bounce back to ~2.5% in FY13 and improve further during FY14.

Asset quality to remain largely stable: As Corporation Bank moved to 100% system based NPA recognition during Q2FY12, it witnessed a one-off increase in fresh slippages to 2.5% of net advances (from 0.8% in Q1FY12) and gross NPAs to 1.3% (from 1.1% in Q1FY12). However, we do not foresee further deterioration in asset quality due to the bank’s preference for low risk-low yield asset portfolio over the years. We expect gross NPAs to decline to 1.1% during FY12-13 considering policy of NPA write-offs and strong recoveries.

Valuation

At CMP of Rs 431, Corporation Bank is trading at mere 0.8x FY12E ABV and 0.7x FY13E ABV (a 30% discount to its last 5-year average P/ABV multiple of 1.0). Despite higher provisioning, we expect PAT to grow at CAGR of 11% during FY11-13 as overall performance in terms of expansion in NIMs, steady credit growth and operating efficiency is going to be quite encouraging. In addition, the bank is entering its next growth phase with its aggressive branch expansion. As majority of the negatives are already factored in our assumptions, valuation at 0.7x FY13 ABV with 4.6% dividend yield is quite compelling. We initiate a BUY on Corporation Bank with a target price of Rs 551 thus valuing it at 0.9x FY13E ABV.

CMP (Rs) 431 Target price (Rs) 551 Potential upside 28%

Stock data

No. of shares (mn) 148.1

FV (Rs) 10

Market cap (Rs bn) 62.95

52 week high/low (Rs) 658/336

Avg. daily vol.* (shares) 74409

BSE Code 532179

NSE Code CORPBANK

Bloomberg code CRPBK

Reuters Code CRBK.BO

* BSE & NSE 6 monthly

Shareholding (%)

Dec-11 QoQ Chg

Promoter 58.5 -

FIIs 4.5 (0.5)

MFs / UTI 3.5 (0.1)

Banks / Fis 27.1 -

Others 6.4 0.6

Relative performance

15000

17500

20000

Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12

0

200

400

600

800

BSE_SENSEX Corporation Bank

Source: Cline, ENAM Direct Research

Financial summary

Y/E Mar

PAT (Rs. Cr)

EPS (Rs.)

Change YoY (%)

P/E (x)

BV (Rs.)

P/BV (x)

Net NPA (%)

Adj BV (Rs.)

P/Adj.BV (x)

RoE (%)

RoA (%)

FY10 1176 82 32 5.2 403 1.1 0.3 389 1.1 22.0 1.2

FY11 1413 95 20 4.5 482 0.9 0.5 455 0.9 21.9 1.1

FY12E 1553 105 10 4.1 563 0.8 0.6 525 0.8 20.1 1.0

FY13E 1741 118 12 3.6 657 0.6 0.5 613 0.7 19.3 1.0

Source: Company, ENAM estimates

3rd April 2012 ENAM Securities Direct 2

Corporation Bank

PEER COMPARISON We compare Corporation Bank with other mid-sized PSU banks having pan-India presence with southern region focus.

Business Performance

Deposits (Rs Cr)

Advances (Rs Cr)

3 yr CAGR Loan book (%)

Return on assets (%)

Andhra Bank 92,156 71,435 27.8 1.4

Corporation Bank 116,747 86,850 30.4 1.1

Indian Bank 105,804 75,250 23.6 1.5

Indian Overseas Bank 145,229 111,833 22.8 0.7

Syndicate Bank 135,596 106,782 18.6 0.8

Source: Company, RBI; Based on FY11 financial data

Business Growth

Among its peer group, Corporation Bank has the fastest growing loan book which has grown at CAGR of 30% in last 3 years.

Return ratios

At 1.1%, return on asset (ROA) of Corporation Bank is in-line with its peer group average. However, due to higher slippages the ratio would move marginally lower in future.

Return on Assets (%)

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Source: Company, RBI, Enam Direct Research.

3rd April 2012 ENAM Securities Direct 3

Corporation Bank

Components of profitability

Interest Spread (%)

CASA Ratio (%)

Cost-to-income ratio (%)

Non-interest income (% of net total income)

Andhra Bank 5.3 26.6 41.4 21.8 Corporation Bank 4.0 21.1 38.5 31.1 Indian Bank 5.4 30.2 36.9 22.7 Indian Overseas Bank 3.7 26.2 47.3 22.5 Syndicate Bank 4.7 30.8 48.1 17.3

Source: RBI; Based on FY11 financial data; * Based on Q3FY12 data

Interest Spread

At 4%, Corporation Bank has one of the lowest interest spreads among its peers. Low interest spreads (hence NIMs) are primarily due to higher proportion of large and mid-corporate loans which have low risk and low yield. Also, higher reliance on bulk deposits on account of lower CASA put pressure on NIMs in recent period.

Interest Spread (%) Casa Ratio (%)

Andhra Bank

Corporation Bank

Indian Bank

Syndicate Bank

Indian Overseas Bank

Andhra Bank

Corporation Bank

Indian Bank

Syndicate Bank

Indian Overseas Bank

Source: Company, RBI, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 4

Corporation Bank

Cost – to- income Ratio (%)

0 5 10 15 20 25 30 35 40 45 50

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Source: Company, ENAM Direct Research.

Cost efficiency

Corporation bank has one of the lowest cost-to-income ratio at 38.5% among its peers. Going forward, we expect it to come to sub-38 levels on back of lower employee cost. During Q3FY12, the bank reported lower cost-to-income ratio ever at 36.6%.

Contribution from non-interest income

At 31.1%, Corporation bank has the highest contribution of non-interest income towards net total income among its peers. Majority of its non-interest income is fee-based thus providing stability to its non-interest income.

Proportion of non-interest income (%)

0 5 10 15 20 25 30 35

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 5

Corporation Bank

Productivity Ratios

Business per

branch (Rs Cr)

Profit per branch

(Rs lacs)

Business per employee

(Rs Cr)

Profit per employee (Rs Lacs)

Andhra Bank 99.6 77.1 11.7 0.1

Corporation Bank 159.6 110.8 15.7 10.9

Indian Bank 95.6 90.5 9.3 8.9

Indian Overseas Bank 115.1 48.0 10.1 0.0

Syndicate Bank 94.8 41.0 8.8 4.0

Source: RBI; Based on FY11 data

Productivity

Corporation Bank has the best productivity ratios at Employee and Branch level among its peers.

Productivity per branch Productivity per employee

0 50 100 150 200

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Profit per branch (Rs lacs) Business per branch (Rs Cr)

0 5 10 15 20

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Profit per employee (Rs Lacs) Business per employee (Rs Cr) Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 6

Corporation Bank

Asset Quality

CRAR (%) Gross NPA (%)* Net NPA (%)* PCR (%)*

Andhra Bank 14.4 2.4 1.2 49.2 Corporation Bank 14.1 1.4 1.0 28.9 Indian Bank 13.6 1.4 0.8 40.7 Indian Overseas Bank 14.6 3.0 1.2 59.0 Syndicate Bank 13.0 2.3 0.9 62.4

Source: RBI; Based on FY11 data, * based on Q3FY12 data

Asset Quality and Provisioning

Historically, Gross NPA levels of Corporation Bank were lower than its peer group average while provisioning coverage ratio remains close to its peer group average (i.e. ~75% respectively). Despite increase in Gross NPA during Q2FY12, gross and net NPA ratios are still low compared to its peers. However, its provision coverage ratio deteriorated to the lowest among its peers. Bank has taken steps to improve its recoveries which might show improvement in profitability from the current levels.

Gross & Net NPA (Q3FY12) Provision Coverage Ratio (%)

0 1 2 3

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Net NPA (%) Gross NPA (%)

0 10 20 30 40 50 60 70

Andhra Bank

Corporation Bank

Indian Bank

Indian Overseas Bank

Syndicate Bank

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 7

Corporation Bank

COMPANY BACKGROUND Established in 1906, Corporation Bank is one of the leading public sector banks in India. Its operations are primarily concentrated in southern and western India with over 60% of branches located in Karnataka, Maharashtra, Kerala, Tamilnadu, Andhra Pradesh and Goa. The bank has always been the first to adapt evolving financial reforms and services such as cash management services, m-commerce, 100% CBS and now low-cost branchless operations. Currently Corporation bank has nearly 14 million customers with a network of 1431 branches, 1262 ATMs and 2525 branchless banking units (Grameen Vikas Kendras).

NIMs likely to bounce back to ~2.5% in FY13

NIMs to bounce back

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY08 FY09 FY10 FY11 FY12E FY13E

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Avg yield on adv Avg Cost of Deposits NIM (Calculated)

Source: Company, ENAM Direct Research.

Aggressive branch expansion to lead future business growth

96.4116.2

135.0 149.6 155.5 170.0

981 1,054

1,3611,550

1,700

1,155

0

40

80

120

160

200

FY08 FY09 FY10 FY11 FY12E FY13E

0

400

800

1200

1600

2000

Business/Branch (Rs. Cr) Branches (Nos.) [RHS]

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 8

Corporation Bank

Corporation bank CASA ratio has been continuously falling since FY08 due to which it has to rely on high cost bulk deposits. The bank witnessed a steep fall in NIMs (calculated) from 3.07% in Q3FY11 to 2.19% in Q1FY12 as cost of deposits soared following RBI actions. However, NIMs have shown steady recovery since then as the bank increased lending rates after a lag. We expect net interest margins (NIMs) to show steady improvement in NIMs from FY13 onwards, mainly on account of:

CASA ratio set to improve from FY13 onwards by 100-125 bps every year

Corporation bank is adding nearly 200 branches a year since FY11 to expand its branch network to over 1700 by FY13. With contribution from newly setup branches starting from FY13, we expect CASA ratio to bounce back by 100-125 bps every year. This would necessitate lesser recourse to bulk deposits;

CASA to improve steadily

0

5

10

15

20

25

30

35

40

FY08 FY09 FY10 FY11 FY12E FY13E

-5.00.05.010.015.020.025.030.035.040.0

% of Low Cost Deposits Growth in CASA (%)

Source: Company, ENAM Direct Research.

Corporation Bank’s recurring failure to meet priority sector lending norms has been one of the key reasons behind lower NIMs as it has to invest in rural infrastructure development fund (RIDF) bonds (at 4%) for not meeting PSL norms or individual sub-limits. Corporation Bank’s investment in RIDF has been higher compared to its PSU peers. There is a good possibility that increased branch network is expected to help the bank in meeting its priority sector lending targets.

3rd April 2012 ENAM Securities Direct 9

Corporation Bank

Priority Sector Exposure (%)

20%

24%

28%

32%

36%

40%

FY07 FY08 FY09 FY10 FY11

Source: Company, ENAM Direct Research.

Rational pricing of loans driven by the new base rate system

We believe pricing has become much more rational with introduction of new base rate system. Banks have been swift in passing on cost of funds to customers and managed to do so in the rising interest rate cycle, when competition in general was slow in increasing lending rates. This would help Corporation Bank prevent steep slides in NIMs due to rising cost of funds.

Operational performance set to improve Corporation Bank’s loan book growing faster than industry

0.0

10.0

20.0

30.0

40.0

2008 2009 2010 2011

Industry CorpBank

Source: Company, RBI, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 10

Corporation Bank

During FY07-11, Corporation Bank’s loan book grew at CAGR of 30.5% compared to 19.5% reported by all SCBs combined. However, due to higher interest rates and increased focus on asset quality, the bank’s credit growth is likely to slow down considerably to 17.6% in FY12 though it would still remain above industry average (~16% YoY). With shift in RBI’s focus from inflation to growth, we expect 100-125 bps repo rate cut during FY13. Consequently, credit growth for the bank would bounce back a little to 19.7% in FY13. Deposit growth during FY11-13 is pegged at 19.5%.

Corporation bank has witnessed steady improvement in operational efficiency. Among its peers, the bank maintains one of the lowest cost-to-income ratio which has come down from 41% in FY07 to 38.5% in FY11 (36.6% in Q3FY12). Newly started branches would deteriorate the ratio as they would take a while to reach full efficiency. The bank is not adding employees to run new branches thus limiting impact on cost-to-income ratio. Operational efficiency is likely to improve further as number of employees per branch decreases in future. Productivity ratios such as business per branch, business per employee etc are expected to exhibit steady improvement demonstrated over last 5 years.

Cost-to-income ratio to remain low

41.3 41.6

37.4 37.1

38.5

37.137.5

34

35

36

37

38

39

40

41

42

FY07 FY08 FY09 FY10 FY11 FY12E FY13E

Operating Cost as % of Net Income

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 11

Corporation Bank

However, profitability ratios such profit per branch, profit per employee would remain largely flat during FY11-13 owing to higher provisioning and aggressive branch expansion. During the period, profit per branch would decline by 1% to Rs.1.05 Cr while profit per employee would increase by just 3% to Rs11.2 lakhs.

Employee Productivity: Ratios on continuous growth path

7.99.8

11.9

14.715.9

18.1

6.17.2

8.910.2 10.2 10.9

0

4

8

12

16

20

FY08 FY09 FY10 FY11 FY12E FY13E

Business/Employee (Rs Cr) Profit/Employee (Rs. Lakh)

Source: Company, ENAM Direct Research.

Branch Productivity: Ratios on continuous growth path

96.4116.2

135.0149.6 155.5

170.0

7585

102 104 100 102

0

40

80

120

160

200

FY08 FY09 FY10 FY11 FY12E FY13E

Business/Branch (Rs. Cr) PAT/branch ( Rs Lacs)

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 12

Corporation Bank

Return ratios to remain healthy

We expect Corporation Bank to report earnings CAGR of 11% for FY11-FY13E, aided by improvement in NIMs, credit growth of 18.6% and lower operating expenses. The Bank has consistently demonstrated its ability to maintain its ROE at ~22% despite equity dilution. While return ratios are likely to decline a bit due to higher provisioning, they would still remain healthy. We expect ROA to decline to 1% in FY12-13 from 1.1% in FY11 while ROE would decline to 19.3% in FY13 from 21.9% in FY11.

Return ratios to remain healthy

16.0

17.0

18.0

19.0

20.0

21.0

22.0

23.0

FY08 FY09 FY10 FY11 FY12E FY13E

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

ROE (%) ROA (%) [RHS]

Source: Company, ENAM Direct Research. Loan book break-up as on 31st December 2011

SME + MSME14%

Retail Credit19%

Agriculture7% Other Sectors

13%

Corporate & Mid Corporate Advances

47%

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 13

Corporation Bank

Asset quality to remain largely stable

In order to maintain superior asset quality, Corporation Bank’s loan book has always been skewed towards large and mid-corporate segment (39% in FY11) which typically has lower yields as well as lower slippages. In addition, during FY07-09, the bank increased its exposure to working capital loans from 35% to 50% while bringing down term loan proportion from 60% to 48% and maintained the asset mix over past 3 years. This along with bank’s policy to aggressively write off NPAs brought down its gross NPA from 2.1% in FY07 to 0.9% in FY11. We expect the bank to maintain the similar asset mix going forward.

Exposure to Top 10 industries as on 31.12.11

Source: Company, ENAM Direct Research. Others include chemical, rubber, transport equipment etc.

The bank also witnessed significant increase in diversification in its industry-wise loan portfolio as its exposure to top 10 industries has declined from 81% in Q3FY11 to 70% in Q3FY12. Its exposure to infrastructure sector as on 31st December 2011 at 16.1% of total advances remains close to its average exposure to the sector in recent years. Exposure to power sector has declined from 9.5% in Q3FY11 to 8.5% in Q3FY12. The bank has also increased diversification in its customer-wise loan portfolio where the percentage of exposure to top 20 largest borrowers has declined from 29% in FY10 to 25% in FY11.

Corporation Bank’s exposure to major industries including infrastructure is in line with its historical lending profile and hence do not add stress to the overall asset quality. We believe the performance of loans to power sector is set to improve and depends upon the pace of implementation of recently announced reforms in the sector.

3rd April 2012 ENAM Securities Direct 14

Corporation Bank

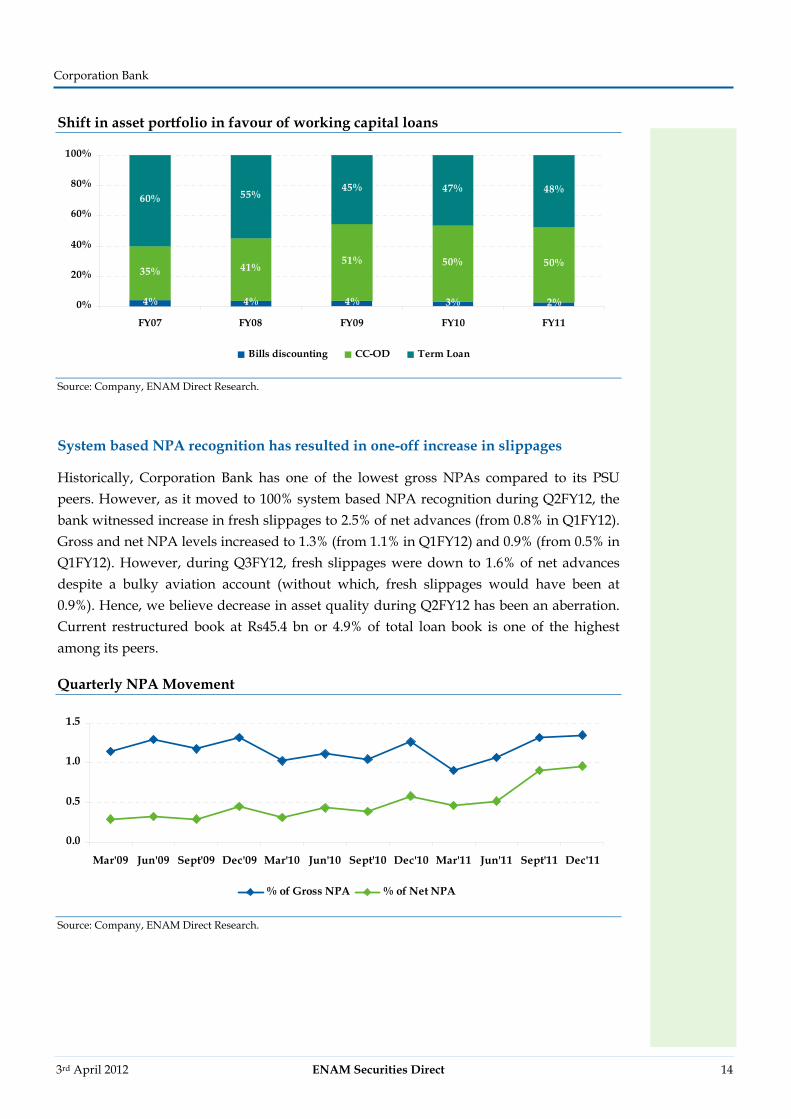

Shift in asset portfolio in favour of working capital loans

4% 4% 4% 3% 2%

35% 41%51% 50% 50%

60% 55%45% 47% 48%

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10 FY11

Bills discounting CC-OD Term Loan

Source: Company, ENAM Direct Research.

System based NPA recognition has resulted in one-off increase in slippages

Historically, Corporation Bank has one of the lowest gross NPAs compared to its PSU peers. However, as it moved to 100% system based NPA recognition during Q2FY12, the bank witnessed increase in fresh slippages to 2.5% of net advances (from 0.8% in Q1FY12). Gross and net NPA levels increased to 1.3% (from 1.1% in Q1FY12) and 0.9% (from 0.5% in Q1FY12). However, during Q3FY12, fresh slippages were down to 1.6% of net advances despite a bulky aviation account (without which, fresh slippages would have been at 0.9%). Hence, we believe decrease in asset quality during Q2FY12 has been an aberration. Current restructured book at Rs45.4 bn or 4.9% of total loan book is one of the highest among its peers.

Quarterly NPA Movement

0.0

0.5

1.0

1.5

Mar'09 Jun'09 Sept'09 Dec'09 Mar'10 Jun'10 Sept'10 Dec'10 Mar'11 Jun'11 Sept'11 Dec'11

% of Gross NPA % of Net NPA

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 15

Corporation Bank

Slippages and restructured accounts

01

23

45

6

Jun'10 Sept'10 Dec'10 Mar'11 Jun'11 Sept'11 Dec'11

As

% o

f net

adv

ance

s

Fresh slippages Restructured accounts

Source: Company, ENAM Direct Research.

Going forward, focus is likely to be on controlling asset quality and recoveries. We expect strong recoveries to follow in coming quarters. Besides, we do not foresee further deterioration in asset quality keeping the bank’s preference for low risk-low yield asset portfolio over the years in mind. We expect gross NPAs to decline to 1.1% during FY12-13 considering the bank’s aggressive policy of NPA write-offs and strong recoveries.

Despite higher provisioning, PAT to grow at 11% CAGR during FY11-13

Corporation Bank maintains provisioning coverage ratio at above 70% thus providing additional cushion against any unexpected slippages. However, increase in NPAs in recent years has impacted the provisioning coverage ratio. Conservatively we have assumed fresh slippages in FY13 to remain above historical average. This along with recent increase in NPAs would keep provisioning expenses at elevated levels during FY12-13.

Gross NPAs to remain largely stable

0.50.3 0.3 0.3

0.5 0.6 0.5

2.1

1.5

1.21.0 1.1 1.1

0.9

78 7570

50 48 50

77

0.0

0.5

1.0

1.5

2.0

2.5

FY07 FY08 FY09 FY10 FY11 FY12E FY13E

0.0

20.0

40.0

60.0

80.0

100.0

Net NPAs (%) Gross NPAs (%) PCR (%)

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 16

Corporation Bank

Capital adequacy ratio (CAR) at comfortable levels

Since 2001, Corporation Bank’s loan book has increased nearly 8 times at a CAGR of 25.8% while barring FY11, there had been no equity dilution. The bank has been funding its balance sheet growth through internal accruals which remained robust on back of prudent credit policy and healthy asset quality. The bank raised fresh capital (~Rs309 Cr) from GoI at Rs658 per share during FY11 as credit growth accelerated in recent years. CAR at ~14.1% is quite comfortable to fund mid-term growth especially in slower credit growth scenario.

Comfortable CAR levels

12.113.6

15.414.1 13.3 12.4

-2.04.06.08.0

10.012.014.016.018.0

FY08 FY09 FY10 FY11 FY12E FY13E

CAR

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 17

Corporation Bank

VALUATION

Stock Price Vs P/ABV Bands

0100200300400500600700800900

31-Mar-06 31-Mar-07 31-Mar-08 31-Mar-09 31-Mar-10 31-Mar-11

Stock Price 0.6 x 0.8 x 1 x 1.2 x 1.4 x

Source: Company, ENAM Direct Research.

Past trend in P/ABV Ratio

0.00.20.40.60.81.01.21.41.61.8

31-Mar-06 31-Mar-07 31-Mar-08 31-Mar-09 31-Mar-10 31-Mar-11

Fwd P/ABV Mean Mean - 1 *Std Dev Mean + 1 * Std Dev

Source: Company, ENAM Direct Research.

During past 5 years, Corporation Bank has exhibited robust loan growth (CAGR of 30%) and stable asset quality (average net NPA of 0.4%) in line with the bests in the industry. At CMP of Rs 431, Corporation Bank is trading at 0.8x FY12E ABV and 0.7x FY13E ABV (30% discount to its last 5-year average P/ABV multiple of 1x). The current valuation of Corporation Bank (0.7x) is at significant discount even after factoring for decline in return ratios. Despite its comparable performance with its peers, the stock is trading at reasonable discount vis-à-vis its peers thus making it an attractive buy.

3rd April 2012 ENAM Securities Direct 18

Corporation Bank

Peer Comparison

3 yr CAGR Loan growth ROA (%) Net NPA (%)* P/BV

Andhra Bank 27.8 1.4 1.2 1.1 Corporation Bank 30.4 1.1 1.0 0.9 Indian Bank 23.6 1.5 0.8 1.1 Indian Overseas Bank 22.8 0.7 1.2 0.7 Syndicate Bank 18.6 0.8 0.9 0.7

Source: RBI, Based on FY11 data, *based on Q3FY12 data

Overall performance in terms of expansion in NIMs, steady credit growth and operating efficiency is going to be satisfactory. In addition, the bank is all set for next round of growth on back of aggressive branch expansion. As majority of the negatives are already factored in our assumptions, valuation at 0.7x FY13 ABV with 4.6% dividend yield is quite compelling. We initiate a BUY on the stock with a target price of Rs551 thus valuing it at 0.9x FY13E ABV.

Dividend per share

0.0

5.0

10.0

15.0

20.0

25.0

FY07 FY08 FY09 FY10 FY11 FY12E FY13E

Source: Company, ENAM Direct Research.

3rd April 2012 ENAM Securities Direct 19

Corporation Bank

Key risks to our investment thesis

Sharp deterioration in asset quality

Any sharp deterioration in asset quality could see credit costs rising sharply, thereby impacting our earnings forecasts adversely.

Sharp slowdown in growth

We expect loan growth CAGR of 18.6% for the next two years. Any sharp deviation from our expectation could pose a risk to our investment thesis.

Sharp slowdown in fee income/non-interest income

In past 3 years, ~38% of net total income has come from non-interest income, which includes profit/loss from sale of investments, securitization fees and recoveries. Contribution from investment related non-interest income (~16% of non-interest income FY11) could be volatile depending on market conditions. If the CASA does not improve as envisaged then the margins could be impacted.

3rd April 2012 ENAM Securities Direct 20

Corporation Bank

FINANCIALS Income Statement (Rs Cr)

Particulars FY08 FY09 FY10 FY11 FY12E FY13E

Interest Earned 4,517 6,067 6,988 9,135 13,196 15,220

Interest Expended 3,073 4,376 5,084 6,196 9,831 10,934

Net Interest Income 1,443 1,691 1,903 2,940 3,366 4,286

Non-Interest Income 700 1,107 1,493 1,324 1,609 1,793

- Sale of Investments 136 442 616 209 300 300

- Other income 564 665 878 1,115 1,309 1,493

Net Total Income 2,143 2,798 3,397 4,264 4,974 6,079

Total Income 5,216 7,175 8,481 10,460 14,805 17,013

Operating Expenses 892 1,047 1,260 1,642 1,844 2,280

- Staff Costs 428 513 632 895 949 1,186

Operating Profit 767 909 946 1,651 1,937 2,503

Profit including extraordinary income 1,251 1,752 2,137 2,622 3,130 3,799

Provisions 186 365 468 689 1,140 1,312

Profit after Provisions 1,065 1,386 1,668 1,934 1,991 2,487

Tax 330 493 492 520 438 746

PAT 735 893 1,176 1,413 1,553 1,741

Balance Sheet (Rs Cr)

Particulars FY08 FY09 FY10 FY11 FY12E FY13E

Capital 143 143 143 148 148 148

Reserves and Surplus 4,085 4,753 5,631 6,990 8,196 9,590

Networth 4,229 4,897 5,775 7,138 8,344 9,738

Deposits 55,424 73,984 92,734 116,748 138,930 166,715

Borrowings 2,938 4,810 9,078 15,965 16,534 17,384

Other Liabilities & Prvsns. 4,007 3,215 4,081 3,658 3,870 3,899

Total Liabilities 66,598 86,906 111,667 143,509 167,678 197,737

Assets

Cash with RBI and Call Money 8,103 10,540 10,792 10,393 10,866 11,767

Investments 17,325 24,938 34,523 43,453 51,404 60,018

Advances 39,186 48,512 63,203 86,850 102,113 122,202

Fixed Assets 272 299 293 331 377 415

Other Assets 1,712 2,617 2,857 2,482 2,918 3,334

Total Assets 66,598 86,906 111,667 143,509 167,678 197,737

Source: Company, ENAM Direct Research

3rd April 2012 ENAM Securities Direct 21

Corporation Bank

Ratio Analysis (%)

Particulars FY08 FY09 FY10 FY11 FY12E FY13E

Growth (%)

Growth in NII 10 17 13 54 14 27

Growth in Net profit 37 21 32 20 10 12

Growth in deposits 31 33 25 26 19 20

Growth in advances 31 24 30 37 18 20

Growth in investment 20 44 38 26 18 17

Cash-flow (Rs. Cr)

(%) FY08 FY09 FY10 FY11 FY12E FY13E

Valuations

EPS (Rs.) 51 62 82 95 105 118

ROA 1.2 1.2 1.2 1.1 1.0 1.0

ROE 18.4 19.6 22.0 21.9 20.1 19.3

BV (Rs.) 295 341 403 482 563 657

Adj. BV (Rs.) 286 332 389 455 525 613

Yields & Margins

Average Yield on Investment 6.8 7.1 6.0 6.0 6.7 6.5

Average Yield on Advances 9.3 10.0 8.9 8.6 10.2 10.0

Average Cost of Deposits 5.9 6.3 5.5 5.1 6.8 6.4

NIM 2.7 2.5 2.1 2.5 2.3 2.5

Asset Quality

Net NPAs (Rs. Cr) 126.9 138.3 197.3 397.7 573.7 664.7

Net NPAs (%) 0.3 0.3 0.3 0.5 0.6 0.5

Others

Operating Cost as % of Net Income 42 37 37 39 37 38

% of current deposits 19 18 15 12 8 9

% of savings deposits 16 14 14 14 14 15

% of Low cost deposits 35 31 29 26 22 23

Dividend Per Share (Rs.) 10 13 16 20 20 20

Source: Company, ENAM Direct Research

3rd April 2012 ENAM Securities Direct 22

Corporation Bank

CONFLICT OF INTEREST DISCLOSURE

We, at ENAM, are committed to providing the most honest and transparent advice to our clients. However, given thenature of the capital markets, from time to time we are faced with situations that could give rise to potential conflict ofinterest. In order to provide complete transparency to our clients, before we make any recommendations, we arecommitted to making a disclosure of our interest and any potential conflict IN ADVANCE so that the interests of ourclients are safe- guarded at all times. In light of this policy, we have instituted what we believe to be the mostcomprehensive disclosure policy among leading investment banks/brokerages in the world so that our clients may make an informed judgment about our recommendations. Thefollowing disclosures are intended to keep you informed before you make any decision- in addition, we will be happyto provide information in response to specific queries that our clients may seek from us. Disclosure of interest statement (As of 21st March, 2012) 1. Analyst ownership of the stock No 2. Firm ownership of the stock No 3. Directors ownership of the stock No 4. MBD Relationship No 5. Broking relationship Yes

We are committed to providing completely independent and transparent recommendations to help our clients reach a better decision.

This document has been prepared by Enam Securities Direct Private Limited – Privileged Client Group. Affiliates of Enam Securities Direct Private Limited focused on Institutional Equities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating and target price of the Affiliates research report. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgement by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options and other derivatives as well as non investment grade securities - involve substantial risk and are not suitable for all investors. Enam Securities Direct Private Limited has not independently verified all the information given in this document. Accordingly, no representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Enam Securities Direct Private Limited, its affiliates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of ENAM Securities Direct Private Limited. The views expressed are those of the analyst and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. Neither this document nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the United States or Canada or distributed or redistributed in Japan or to any resident thereof. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Enam Securities Direct Private Limited to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.

Copyright in this document vests exclusively with ENAM Securities Direct Private Limited.

ENAM Securities Direct Pvt. Ltd.

201, Laxmi Towers, 'A' Wing, Bandra-Kurla Complex, Bandra East, Mumbai - 400 051. Board: 6680 3600 Helpline: 6680 ENAM Fax : 6680 3700

Website: www.enam.com / www.enamdirect.in Email: [email protected]