by sandra lizarazo - uc3mmkredler/readgr/aristizabalonlizarazo13.pdf · by sandra lizarazo journal...

TRANSCRIPT

Default risk and risk averse international investorsBy Sandra Lizarazo

Journal of International Economics, 2013

Presented by Danilo Aristizabal

June 14, 2017

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 1 / 14

Outline

1 Introduction

2 Model

3 Quantitative analysis

4 Results

5 Conclusion

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 2 / 14

Introduction

There is a strong correlation between domestic fundamentals of emergingeconomies and their access to international credit markets. However,investor’s characteristics...

Develop an endogenous default risk model for small open economiesthat interact with risk averse international investors.

Explain a larger proportion and volatility of the spread betweensovereign bonds and riskless assets than the standard model with riskneutral investors.

The risk premium in the asset prices of sovereign countries can bedecomposed into two components: a base premium qRN , and anexcess premium ζRA(b′, y ,W ).

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 3 / 14

Stylized facts

Emerging economies estimated default probabilities do not accountfor all the spreads in their sovereign bonds.

The risk premium is higher for riskier countries.

Investors financial performance and their net foreign assetposition in emerging economies are positively correlated.

Emerging economies credit spreads are positively correlated withspreads of corporate junk bonds from developed countries(Longstaff, 2011).

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 4 / 14

Model I

Emerging country

Preferences

E0

∞∑t=0

βtu(ct) u(ct) =c1−γt

1− γ

Income is non-storable and follows a Markov process with transitionf (y ′|y).

If the government chooses to repay, resource constraint

c = y − q(b′, y ,W )b′ + b

If the government chooses to default, resource constraint

c = ydef where ydef = h(y)

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 5 / 14

Model II

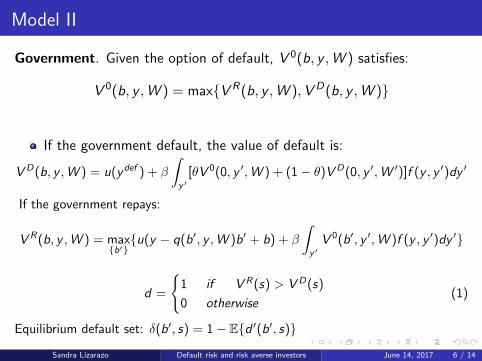

Government. Given the option of default, V 0(b, y ,W ) satisfies:

V 0(b, y ,W ) = max{V R(b, y ,W ),VD(b, y ,W )}

If the government default, the value of default is:

V D(b, y ,W ) = u(ydef ) + β

∫y ′

[θV 0(0, y ′,W ) + (1− θ)V D(0, y ′,W ′)]f (y , y ′)dy ′

If the government repays:

V R(b, y ,W ) = max{b′}{u(y − q(b′, y ,W )b′ + b) + β

∫y ′V 0(b′, y ′,W )f (y , y ′)dy ′}

d =

{1 if V R(s) > V D(s)

0 otherwise(1)

Equilibrium default set: δ(b′, s) = 1− E{d ′(b′, s)}

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 6 / 14

Model III

International investors. There is a representative risk averse investor

Preferences

E0

∞∑t=0

βtLv(cLt ) v(cL) =(cL)1−γ

1− γ

The representative investor is endowed with some initial wealth W0, andreceives an exogenous income X .

If the government does NOT default:

cL,ndef = X + W − qf ϑTB′ − qϑ′

If the government does default:

cL,def = X + ϑTB − qf ϑTB′

LOM: W ′ = d ′ϑ′ + ϑTB′

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 7 / 14

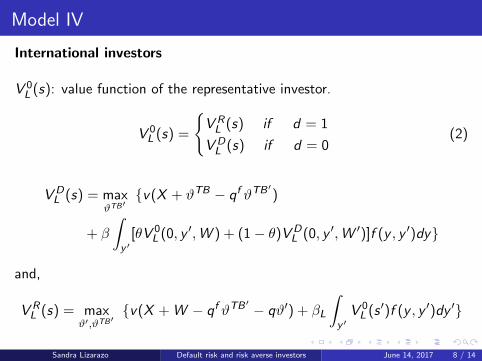

Model IV

International investors

V 0L (s): value function of the representative investor.

V 0L (s) =

{V RL (s) if d = 1

VDL (s) if d = 0

(2)

VDL (s) = max

ϑTB′{v(X + ϑTB − qf ϑTB

′)

+ β

∫y ′

[θV 0L (0, y ′,W ) + (1− θ)VD

L (0, y ′,W ′)]f (y , y ′)dy}

and,

V RL (s) = max

ϑ′,ϑTB′{v(X + W − qf ϑTB

′ − qϑ′) + βL

∫y ′V 0L (s ′)f (y , y ′)dy ′}

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 8 / 14

Model V

The representative investor faces W < 0 that prevents Ponzi schemes.W ≥W. Additionally, the investor asset position in bonds of the emergingeconomy is non-negative, i.e. ϑ ≥ 0.

From FOC

q = βL

∫y ′

vcL(cL)d ′

vcL(cL)f (y , y ′)dy ′

= βLCov(vcL(cL), d ′)

vcL(cL)+ qRN

= ζRA + qRN

where qRN = qf (1− δ).

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 9 / 14

Recursive Equilibrium

It is defined as a set of policy functions for (i) the emerging economy’sconsumption c(s), (ii) government asset holdings b′(s), (iii) thegovernment’s default decisions d(s) and default sets D(b|W ), (iv) therepresentative investor’s consumption cL(s), (v) representative investor’sholdings ϑ′(s) and ϑTB

′(s), and (vii) the emerging economy’s bond price

function q(b′, s) such that:

Given q(b′, s) and the investor’s policies, c(s), b′(s), d(s) solve theproblem of the emerging economy.

Given q(b′, s) and the government’s policies, cL(s), ϑ′(s), and ϑTB′

solves the problem of the representative investor.

Given q(b′, s), markets for the emerging economy’s bonds clear:b′(s) = −ϑ′(s) if b′(s) < 00 = −ϑ′(s) if b′(s) ≥ 0.

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 10 / 14

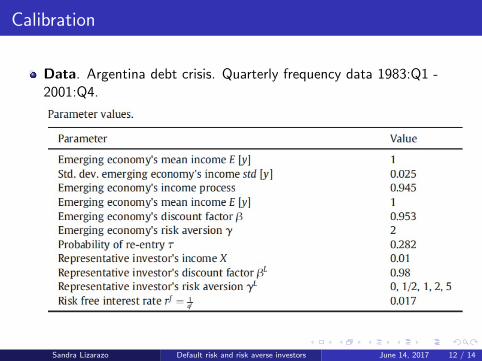

Quantitative analysis

Data. Argentina debt crisis. Quarterly frequency data 1983:Q1 -2001:Q4.

Most of the parameters for the emerging economy are taken from thecalibration of Arellano (2008).

GDP is assumed to follow a log-normal AR(1) process:

log(yt) = ρlog(yt−1) + εy and E[εy ] = 0, E[εy2] = σ2y

There is an asymmetrical function for output loss:

φ(y) =

{y if y > y

y if y ≤ y(3)

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 11 / 14

Calibration

Data. Argentina debt crisis. Quarterly frequency data 1983:Q1 -2001:Q4.

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 12 / 14

Business cycle statistics: the model and the data

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 13 / 14

Conclusion

The model quantitatively characterizes the role of internationalinvestor’s characteristics in the determination of SOE’s optimal plans.

The model accounts better for the sovereign spreads levels and itsvolatility.

Including risk averse investors does not help at explaining the highlevels of debt observed in the data.

Sandra Lizarazo Default risk and risk averse investors June 14, 2017 14 / 14