business design

TRANSCRIPT

Number 10 1998

Market Share Is Dead:Long Live Business DesignOnce, business leaders who increased revenue,decreased cost, fielded technically superior products,and expanded their market share could expect to reapenviable increases in shareholder value. No longer.Achieving sustained value growth requires a strategyframework that reflects today’s marketplace of rapidlyshifting customer priorities. It requires the disciplineof Business Design, which helps companies find andcapture tomorrow’s “profit zones.”

Table of contents, page 4; executive summaries, page 69.

Management Consulting

An elaboration on the themesof Mercer’s best-selling book, The Profit Zone

Mercer Management Journal

Management Consulting

Achieving Shareholder Value GrowthThrough Business Design

4

Mercer Management JournalAchieving Shareholder Value GrowthThrough Business Design

7 Letter to readersby James A.Quella and James W. Down

9 Achieving sustained shareholder value growthStrategy in the age of Value Migration®

by Adrian J. Slywotzky, David J. Morrison, and James A. Quella

Once, business leaders who increased revenue, decreased cost, fielded

technically superior products, and expanded their market share could

expect to reap enviable increases in shareholder value. No longer.

Achieving sustained value growth requires a new strategy framework

that reflects the times: Business Design.

16 Value Migration in the communications industry

23 “Changing the hand instead of the glove”An executive roundtable on shareholder value growth

A discussion by five top executives from a variety of industries

highlights some of the issues facing business leaders as they strive to

achieve sustained value growth. One conclusion: Companies can’t just

continue to do what they do now, only better. They have to reinvent

themselves—to “change the hand,” as one panelist says, “as opposed to

changing the glove.”

31 Identifying the opportunities of the futureStrategic AnticipationSM through marketing science

by Eric Almquist and Gordon Wyner

A winning Business Design is founded on an insightful understanding

of rapidly shifting customer priorities. In 1995, Mercer Management

Consulting used two rigorous marketing science tools to conclude—

correctly, it turns out—that much of the conventional wisdom about

the future of multimedia “broadband” networks was wrong.

37 Targeting the profitable rail passenger

Number 10

1998

5

41 A blueprint for shareholder value growthWinning through strategic Business Design

by Rick Wise

The discipline of Business Design, with its customer-centric rather

than product-centric view of business and its explicit focus on

shareholder value growth, recognizes and embraces the demanding

requirements of today’s volatile marketplace.

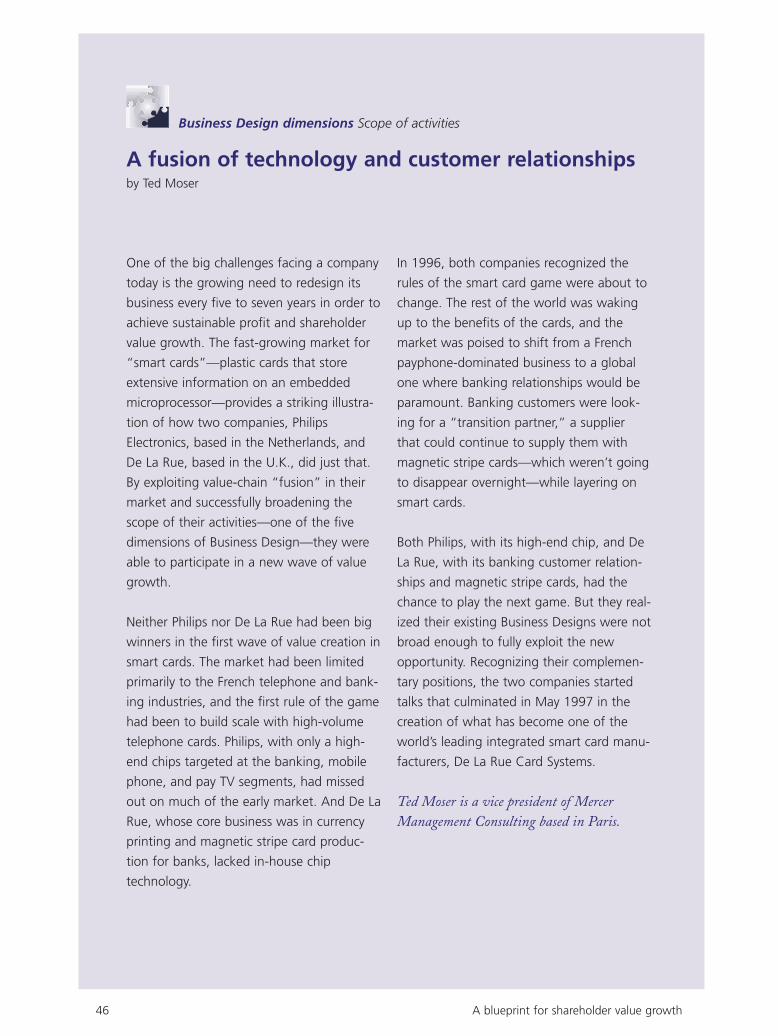

46 A fusion of technology and customer relationships

48 Tomorrow’s Business Designs in financial services

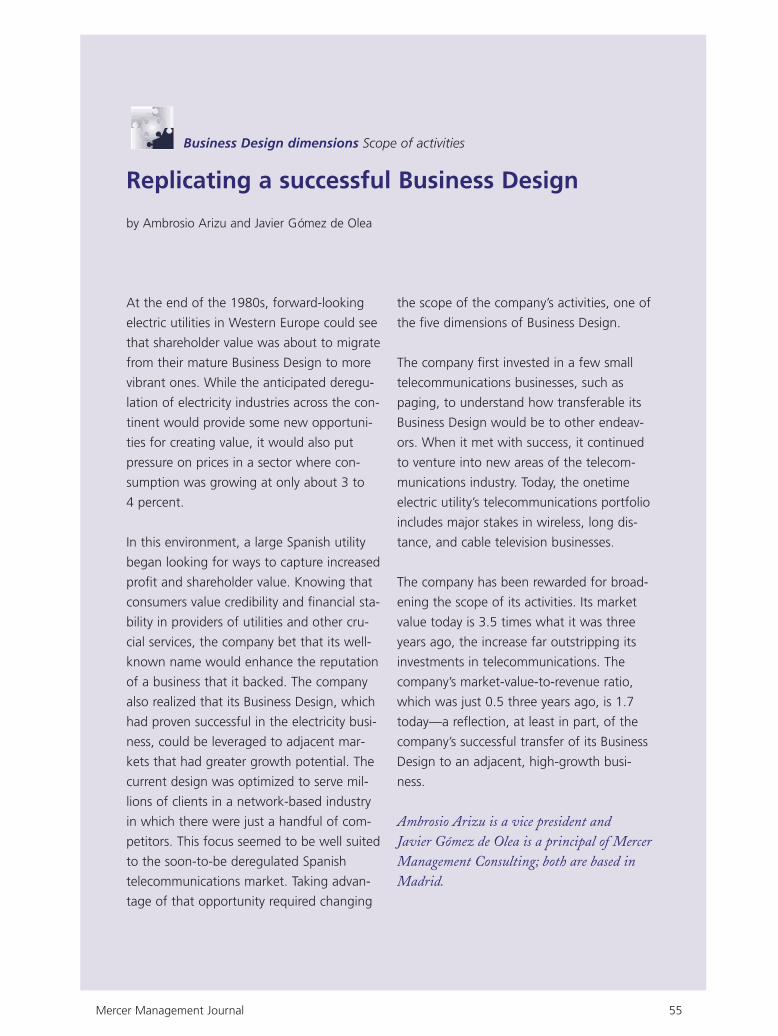

55 Replicating a successful Business Design

57 Reaping the fruits of Business DesignValue growth realization through rapid organizational change

by Diane MacDiarmid, Hanna Moukanas, and Rainer Nehls

A company may have created a Business Design perfectly suited to

capturing future value-creation opportunities. But unless the company

can get its organization to rapidly move from its current Business

Design to the new one, it will miss what these days is often little more

than a fleeting opportunity.

65 The overhaul of an auto components supplier

69 Executive summariesAbstracts of the main articles of this issue in English, French, German,

Spanish, and Portuguese.

To join a discussion on howcompanies can achievesustained shareholder valuegrowth, visit ourMercer ManagementJournal Forumat www.mercermc.com.

Mercer Management Consulting helps leading enterprises anticipate

rapidly changing customer priorities, economics, and environments and

then design their businesses to seize the opportunities created by those

changes. Our proprietary Business Design techniques, combined with

our specialized industry knowledge and global reach, enable us to help

clients develop innovative strategies for achieving sustained shareholder

value growth.

Mercer Management Journal

Mercer Management Journal is published twice yearly by Mercer

Management Consulting, Inc., for its clients and friends. The contents

are copyright © 1998 by Mercer Management Consulting.

All rights reserved. Excerpts can be reprinted with attribution to

Mercer Management Consulting. Article summaries can be found on

our web site: www.mercermc.com.

For information on reprinting articles and all other correspondence,

including change of address notification, please contact the editor at:

Mercer Management Journal

33 Hayden Avenue

Lexington, Massachusetts 02173

781-674-3276

Paul_Hemp @MercerMC.com

Editorial Board

Matthew A. Clark, co-chair

Carla Heaton, co-chair

João P. A. Baptista

James W. Down

Jean-Pierre Gaben

August Joas

David J. Morrison

Patrick A. Pollino

James A. Quella

Adrian J. Slywotzky

Editor

Paul Hemp

Designer

Trina Teele

7

To our readers,Market share is dead?

Certainly, the link between market share and attractive gains in

shareholder value—once strong and certain—is increasingly ten-

uous, if not severed entirely. The traditional management focus

on building market share, increasing revenue, decreasing costs,

and building superior products just doesn’t guarantee the results

it did only a short time ago. In more and more industries, the

lion’s share of shareholder, or stock market, value is owned by

enterprises that have a relatively small share of industry revenue.

In our work with clients, we bear daily witness to the fact that

the time-honored approaches to strategic planning no longer

work in today’s discontinuous world. If the future is no longer a

linear progression of the past, then linear, deterministic, incre-

mental thinking no longer suffices. In this environment, strategy

can no longer be built from the inside out, tweaking yesterday’s

assumptions for tomorrow’s business plan. And with the cycles of

value creation rapidly shortening, companies that continue to

play by the old rules risk over-investing in an outdated business

model, while ceding to upstarts the opportunity to build tomor-

row’s. Errors are costly and hard to overcome.

Today, strategy requires a new, outside-in perspective, one provid-

ed by the discipline of Business Design. This approach demands

that managers ask themselves three deceptively simple questions:

How do I anticipate and identify the “profit zones” where cus-

tomers will allow me to create value in the future? What

Business Design will allow me to capture that value? How do

I harness the power of my entire organization to seize this

opportunity?

And these questions aren’t for pondering when an executive finds

the time. Given the rapidly shortening cycles of value creation,

even a business that is prospering must constantly reexamine its

current Business Design. Otherwise, managers will wake up one

day to find that the design has become obsolete and that some-

one else has seized what these days is often little more than a

fleeting value-creation opportunity.

8

This issue of the Mercer Management Journal is in essence a man-

ifesto. From the first article, which argues that today’s market-

place demands a new, more dynamic approach to strategy, to the

last, which shares some of our thinking on how to rapidly move

an organization from yesterday’s Business Design to tomorrow’s,

this Journal outlines a powerful new approach for strategy devel-

opment, one that we call Value-Driven Business Design. As

such, the issue is best read in its entirety.

Mercer Management Consulting is uniquely positioned to assist

clients in achieving sustained growth in shareholder value. Not

only has our proven process of Value-Driven Business Design

consistently helped clients to identify and benefit from new

opportunities, but no other firm can claim our continued

thought leadership on the topics of profitable growth and share-

holder value growth. Over the past several years, our best-selling

business books have set the agenda. Grow to Be Great declared, at

the height of the downsizing and reengineering movement, the

imperative of growth. Value Migration® laid out the threats to

growth. The Profit Zone offers perspectives for business leaders

on how to achieve value growth in the face of these threats. The

Journal, too, has helped develop this continuum of thinking. Last

issue, for example, we examined one of the key tools for achiev-

ing sustained value growth: Customer Relationship

Management. Future issues will address other value growth

topics.

Just as this issue of the Mercer Management Journal introduces

our newest thinking on the topic of value growth, it also intro-

duces a new editorial design. We think we’ve succeeded in mak-

ing the Journal easier to read and more engaging. We hope you

agree.

Sincerely yours,

James A. Quella James W. Down

Vice Chairman Vice Chairman

Mercer Management Journal Copyright © 1998 by Mercer Management Consulting, Inc. 9

Wars were traditionally won by those who marshaled the

largest fighting force. It was a zero-sum game. The goal

of the advancing army was to keep driving the opponent back,

capturing the ceded territory. Size mattered, perhaps more than

fighting prowess: You won if you were the last person standing.

The assumption that size counted was central even to the large-

scale computerized war games that officers used for training and

strategy.

The Vietnam war dramatically illustrated that military strategy

could no longer rely on the old rules of the game. Despite over-

whelming firepower and mass, the United States and South

Vietnamese troops were unable to prevail over the North

Vietnamese army, whose clear objectives were informed by a

superior understanding of geography, local resources, and psy-

chology. Building on the lessons of Vietnam, Desert Storm was

the first really modern war. The United States and its allies,

despite being the smaller on-site force, harnessed advanced tech-

nology—from satellites to smart bombs—to provide unparal-

leled information to generals. This enabled them to conduct a

complex, highly choreographed, multi-fronted war that rewrote

the rules for military strategy. These new rules require that old-

line generals make the transition to a new way of thinking:

— from a static to a dynamic view of battle, where thinking

several moves ahead is now essential rather than merely

desirable;

— from a monolithic, mass-based approach, waged on a limited

number of fronts, to one that focuses on fighting several

simultaneous battles, each using a different mix of troops,

artillery, and air power;

Once, business leaders

who increased revenue,

decreased cost, fielded

technically superior

products, and expanded

their market share could

expect to reap enviable

increases in shareholder

value. No longer. Achieving

sustained value growth

requires a new strategy

framework that reflects the

times: Business Design.

Achieving sustained shareholder value growth

Strategy in the age of Value Migration®

by Adrian J. Slywotzky,

David J. Morrison,

and James A. Quella

Achieving sustained shareholder value growth10

— from a focus on simple territorial objectives to more subtle

and sophisticated definitions of success.

As a result, military strategy has become simultaneously more

critical and more difficult.

We are on the cusp of an equally profound reshaping of the role

of and requirements for business strategy. Able commanders

such as Jack Welch of GE, Bill Gates of Microsoft, and the late

Roberto Goizueta of Coca-Cola, having mastered the new

strategic order, have achieved stunning victories for their share-

holders and employees.

When Strategy Didn’t Matter

It may seem hard to believe, but for much of the post-World

War II period, customer and marketplace strategy didn’t matter.

In the 1950s and early 1960s, customer demand often out-

stripped capacity, and the resulting high systemic growth rates

“lifted all boats.” This was especially true for the U.S. economy,

which enjoyed a strong relative competitive advantage during

the period. Moreover, regulation, global trade management, and

outright protectionism created relatively stable industry environ-

ments within which large-scale players had hegemony.

As the 1960s progressed, the “if you build it, they will come”

euphoria was supplanted by a need for more rigorous business

thinking. Dominant strategic approaches centered around organ-

ization economics: improving organization structure and com-

mand-control functions.

With the advent of the 1970s, and the balancing of supply to

demand, the focus changed again. As exemplified by the “experi-

ence curve” and the “five forces model,” the core of business

thinking became the identification and building of structural

advantage based on a rigorous understanding of relative supply

economics.

In the early 1980s—and even persisting to some extent today—

global competition, corporate raiders, and activist shareholders

drove another shift, toward a focus on efficiency economics.

Downsizing and reengineering became the mantras of business;

balance sheet and income statement restructuring became man-

agement’s core concerns.

Throughout these periods, strategic thinking was a narrow, eso-

teric discipline practiced by a few corporate staff types. It was

In the last 30 years, the

focus of strategy has

shifted, from organization

economics, which empha-

sized the improvement

of organization and

command-control func-

tions; to relative eco-

nomics, which made use

of tools like the

“experience curve” and

the “five forces” model;

to efficiency economics,

characterized by

downsizing and reengi-

neering. Now, the focus

has shifted again.

Mercer Management Journal 11

also largely operations-driven: How can we achieve a low-cost

position through manufacturing economies of scale? How do we

optimize capital allocation trade-offs between business units?

How do we manage a portfolio of businesses?

In this world, the rules for success were fairly predictable: Target

a high-growth market. Develop superior products through a dis-

ciplined R&D capability. Build high relative market share

through rapid roll-out, aggressive capacity expansion, and pow-

erful marketing and sales. Harness scientific management prac-

tices—planning, budgeting, and control systems—to sustain and

enhance this position. The inevitable result would be revenue

growth, scale economies, barriers to competition—and growth in

shareholder value. As in traditional warfare, scale would win.

The Rules of Strategy Have Changed Forever

Beginning in the second half of the 1980s, the rules of success

began to change. Manufacturing scale and product share were

no longer, on their own, enough to drive value growth. Strategic

success was now defined by a company’s ability to gain and act

upon a superior understanding of customer economics. Value-

growth companies of the 1990s have become the ones that can

anticipate rapidly-changing customer priorities and design their

businesses to seize the opportunities created by those dynamic

changes.

Look at the period from 1990 to 1996 and compare the top fif-

teen companies ranked by absolute dollars of revenue growth,

operating profit growth, and shareholder value growth (see

Exhibit 1). Only two of the top fifteen revenue growers were

Only includes those companies that had values for both 1990 and 1996.SOURCE: Mercer Management Consulting Value Growth Database

Top 15 Shareholder Value Growers1990-1996

21%

27%

57%

50%

18%

18%

31%

11%

14%

12%

27%

16%

37%

102%

18%

$113BB

$100BB

$100BB

$90BB

$68BB

$62BB

$58BB

$57BB

$52BB

$46BB

$44BB

$44BB

$43BB

$41BB

$41BB

GENERAL ELECTRIC

COCA-COLA

INTEL

MICROSOFT

TOYOTA

MERCK

ROCHE

EXXON

ROYAL DUTCH SHELL

PHILIP MORRISPHILIP MORRIS

HONGKONG SHANGHAI BANK

PROCTER & GAMBLE

HEWLETT-PACKARD

CISCO SYSTEMS

JOHNSON & JOHNSON

Top 15 Operating Profit Growers1990-1996

INTEL

FORD MOTOR

GENERAL ELECTRIC

AT&T

NOVARTIS

PHILIP MORRISPHILIP MORRIS

CHRYSLER

GLAXO WELLCOME

COLUMBIA/HCA

MICROSOFT

HEWLETT-PACKARD

HONDA

PROCTER & GAMBLE

WAL-MART

MERCK

Top 15 Revenue Growers1990-1996

WAL-MART

FORD MOTOR

TOYOTA

ALLIANZ

GENERAL MOTORS

NIPPON TELEPHONE & TELEGRAPH

CHRYSLER

METRO

AXA-UAP

CREDIT SUISSE

SIEMENS

HEWLETT-PACKARD

VOLKSWAGEN

SONY

MATSUSHITA

CAGR

Exhibit 1 Revenue andprofit growth don’t alwayscorrelate with value growth

Achieving sustained shareholder value growth12

also top value growers. Only seven of the top operating profit

growers were also top value growers. Clearly, biggest is no longer

necessarily best.

More and more in our research, we see three sorts of struggling

enterprises. The first, firms with empty revenue or market share, are

characterized by continued profitless growth. Many consumer

electronics and PC sales and distribution companies are prime

examples. The second, bottle rockets, are companies that climb

rapidly to vertiginous heights of stock market success and then

just as rapidly fall back to earth. Netscape—relying on ubiquity

and evanescent product superiority as its sources of sustainability

instead of working to build in sources of continuing strategic

control—is an example. The third, asset monsters, are asset-inten-

sive firms that earn insufficient returns on their capital employed,

either because of flaws in their original business model or because

they are blindsided by rapid change. These companies find that

achieving market share goals—sometimes even with profitable

growth—demands more fixed assets and working capital than can

be deployed at attractive returns. Big steel and store-based com-

puter and software retailers are historical examples. Some utili-

ties, because of deregulation, will soon join their ranks.

We’re not suggesting that the challenges faced by such companies

are new. But their incidence is increasing, which suggests that

traditional strategy approaches no longer apply. So what hap-

pened? The old rules were overthrown by five quiet revolutions:

— The globalization of regional players, which has led to

worldwide overcapacity, price pressure, and product com-

moditization.

— The blurring of traditional industry boundaries, catalyzed by

the emergence of economically advantaged substitute tech-

nologies and materials (for example, plastics and aluminum

vs. steel), which has led to increased customer options and

overcapacity.

— The industrialization of distribution channels, driven by infor-

mation technology, branding, and consolidation plays, which

has led to a shift in the balance of power from suppliers to

the channel.

— The rise of entrepreneurial support systems, powered by the

explosion of seed and mezzanine financing, which has led to

Increasingly, we see three

sorts of struggling enter-

prises: firms with empty

revenue or market share,

characterized by continued

profitless growth; bottle

rockets, the companies

that enjoy rapid stock

market success and then

crash back to earth; and

asset monsters, businesses

that earn insufficient

returns on their capital

employed.

Mercer Management Journal 13

a lowering of barriers for the creation of innovative new

business models.

— The democratization of information, which has led to a broad-

er group of more educated customers, greater pricing trans-

parency, and the creation of new information-based compet-

itive business models that, by their very nature, can be

highly customer-responsive.

The direct impact of these revolutions is rapidly changing cus-

tomer priorities and a broader set of competitive alternatives (see

Exhibit 2). These revolutions have contributed substantially to

the decreased importance of scale and market share. For exam-

ple, increased availability of capital has made it easier to achieve

scale. Information technology has enabled knowledge-based and

service-based value-added to become more important in many

industries than product-centric factors such as cost and

capabilities.

A by-product of these revolutions is Value Migration®. We

define this as the flow of shareholder value from increasingly

outmoded Business Designs—the entire system by which a

company delivers utility to its customers and thereby generates

sustained value growth for its shareholders—to other Business

Designs better calibrated to satisfy critical customer priorities. In

computing, value flowed from traditional integrated players such

as IBM and Digital Equipment to value chain specialists such as

Intel, Microsoft, Oracle, and EDS (see Exhibit 3).

Value Migration is not new. It occurs whenever new Business

Designs arise that better satisfy changing customer priorities.

Value Migration®

Value Sector Rivalry

BoundaryBlurring

EntrepreneurialSupportSystems

GlobalizationChanging

Role ofInformation

IndustrializingDistribution

Channels

Change Drivers

DynamicCustomerDecisionMaking

ChangingCustomerPriorities

EmergingBusinessDesigns

Exhibit 2 Shiftingcustomer priorities andnew Business Designalternatives drive ValueMigration®

Achieving sustained shareholder value growth14

Value migrated from Ford’s vertically integrated, single-car-

focused Business Design to GM’s price-laddered design in the

1920s. It moved from corner grocery stores to supermarkets in

the 1930s, from fragmented merchandisers to national catalogue

retailers, such as Sears, in the 1890s, and to national merchan-

dise chains—again, Sears—in the 1920s. Business Designs have

been moving into and out of phase for decades, creating and

destroying fortunes in the process.

While not new, the pace of Value Migration® is accelerating. In

industry after industry, we see value creation cycles, the lifecycle

of any given Business Design, shortening. Every Business

Design—if it remains static as customer priorities shift—travels

through a three-phased lifecycle (see Exhibit 4). In Value Inflow,

a company’s Business Design is both well-calibrated to its cho-

sen customers’ priorities and well-differentiated from competi-

tors; in this stage, it is a magnet for value and a beneficiary of

Value Migration. In Stability, customer priorities have begun to

change, but no major competitive alternative has emerged.

Business Designs in the stability phase usually have good oper-

ating results, but growth has slowed and customers are starting

to bid down prices. In Value Outflow, changing priorities have

engendered new, highly attractive Business Design alternatives,

and the original Business Design falls victim to Value

Migration.

Consider the pharmaceutical industry. Twenty-five to 30 years

ago, Business Designs for a new pharmaceutical product could

0

20

40

60

80

100

120

140

160

Market capitalization through December 31, 1997, in billions of (1995) dollars.Source: Mercer Management Consulting Value Growth Database

0

5

10

15

20

25

30

Digital

IBM

0

20

40

60

80

100

120

140

160

0

5

10

15

20

25

30

Oracle/EDS

Oracle

EDS

Intel

Intel/Microsoft

Microsoft

1977 1987 1997 1977 1987 1997

1977 1987 19971977 1987 1997

Exhibit 3 Market valueincreasingly flows fromoutmoded BusinessDesigns to newer onesbetter calibrated to satisfycritical customer priorities

Mercer Management Journal 15

expect to enjoy a long economic life. Why? Speedier Food and

Drug Administration review cycles meant that the remaining

patent life at launch could be as long as 12 to 15 years. In addi-

tion, the generics industry was embryonic; it took more than a

decade for generic substitution to erode a product’s market

position.

By the 1980s, the growing complexity of drug approval reduced

remaining patent life at launch to 10 years, and the generics

industry had come of age. Today, it is not uncommon for a

branded pharmaceutical to lose half its share of prescriptions to

generics within nine months of patent expiration. What was

once a nearly 30-year value creation cycle has been compressed

to little more than a decade.

In this increasingly dynamic business environment, the role of

top management has changed. It is no longer enough to focus on

operational excellence alone. In order to sustain the firm’s value

growth, managers must answer the following questions: How

much life remains in our current Business Design? Where will

we be allowed to create shareholder value? How do we seize

these opportunities as rapidly as possible?

Despite the sea change in the rules of business success, many

companies still struggle to apply traditional strategy processes

and frameworks to these new problems. They build projections

based on extrapolations of the current situation rather than eval-

uating the likelihood of discontinuous change. They use “core

competency” thinking to identify the foundations for future

growth. And when all else fails, they

Value Migration®, the flow

of shareholder value from

increasingly outmoded

Business Designs to others

better calibrated to satisfy

critical customer priorities,

is not new. But the pace

of Value Migration is accel-

erating. In industry after

industry, we see value

creation cycles—the life-

cycle of any given Business

Design—shortening.

Market Value to Revenue Ratio

<1

2 - 10

1 - 2

ValueInflow

ValueOutflow

The company captures a disproportionateshare of value because its Business Designis superior in satisfying customers’ priorities.

The company maintains its value either becauseits Business Design remains powerful (thoughmature) or because no credible alternatives exist.

Value flows away from the company towardBusiness Designs that more effectively meetevolving customer priorities.

DANGER POINT

Stability

Reinvention

Exhibit 4 Business Designshave a finite lifecycle [continued on page 18]

16 Achieving sustained shareholder value growth

Value Migration® in the communications industry Business Designs, not technology, are driving the shift

by Richard S. Christner

The communications services

industry has, in recent years,

been an area of steady share-

holder value growth. Since

1991, the combined market

value for firms competing in

communications services has

increased by about 120 per-

cent, slightly higher than the

increase for the S&P 500 Index.

But the majority of new value

growth has come not from the

traditional service providers—

AT&T, MCI, Sprint, GTE, the

“Baby Bells”—but from non-

traditional providers. Indeed,

those companies’ share of

industry market value grew

from under 25 percent in 1991

to over 45 percent by the end

of 1997, reflecting the migra-

tion of value to them from tra-

ditional providers (see exhibit).

These non-traditional service

providers are generating value

growth primarily in three areas.

The unprecedented rise of the

Internet is driving value growth

in data communications ser-

vices. Beneficiaries have been

non-traditional service providers

such as WorldCom, America

Online, Qwest, and @Home.

The need for more flexible com-

munications connectivity than

traditional wireline provides is

driving value growth in digital

wireless services, including

those that are satellite-based.

This change is behind the value

growth of providers such as

Nextel and PanAmSat. The

explosion of communications

volume—resulting from the

reduction of cost-per-communi-

cation to nearly zero in areas

such as E-mail and voice mail—

is driving value growth in con-

text services, which organize

and provide meaning to a cus-

1991 1992 1993 1994 1995 1996 1997

Non-traditionalProviders•Data

- Internet -Broadband

•Wireless/ Satellite

•Context

AT&T,MCI, andSprint

Baby Bellsand GTE

Market values include long-term debt.SOURCE: Mercer Management Consulting Value Growth Database

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$361BB $402BB $465BB $456BB $615BB $664BB $803BB

Providers’ shares of

communications

services industry

market value

17Mercer Management Journal

tomer’s communications.

Winners in this category are

Yahoo! and Premiere

Technologies.

These three areas of value

growth reflect new areas of

technology innovation. For

example, new packet-switching

and compression technologies

have allowed some non-tradi-

tional providers to greatly

expand the amount of informa-

tion transmitted on an existing

line. But even though new

technology has given upstart

providers a source of competi-

tive advantage, traditional

providers are quickly able to

replicate this technology.

Technology alone is insufficient

to generate significant creation

of shareholder value.

Instead, according to a recent

study of the communications

services industry by Mercer

Management Consulting, it is

the non-traditional players with

innovative Business Designs that

have captured the majority of

value growth over the past six

years. Nextel has prospered by

refocusing on a well-defined set

of customers: business work-

groups. WorldCom’s end-to-end

fiber network, assembled

through several acquisitions,

gives it the advantage in provid-

ing low-cost, seamless service

to business customers. Yahoo!’s

focus on providing navigation

and context assistance for

Internet users has given it

shareholder value multiples

higher than firms with greater

revenue that merely provide

access to the ‘Net.

The danger for established ser-

vice providers is to ignore the

power of newly created

Business Designs such as these.

As regulatory barriers come

down, many Baby Bells and

long distance providers are

focusing on strategies built

around improving their current

Business Designs, through cost

cutting and expansion of scale.

Like the steelmakers, airlines,

and automakers before them,

these companies risk missing

the true competition and the

true opportunity. Instead, the

established players should look

toward redesigning their busi-

nesses for the customer priori-

ties, technologies, and econom-

ics of the future.

The stakes for developing a

Business Design that will cap-

ture future value creation

opportunities are high. The

communications and related

technology industries show an

increasing propensity toward

“winner-take-all” competitive

battles, where the player with

the superior Business Design

gets an overwhelmingly dispro-

portionate share of the value

growth. For example, America

Online’s Business Design

focused on creating an online

“community” that was easy for

even technology novices to join,

on building subscriber volume

through free trial software, and

on generating revenue through

advertising and transaction

fees. CompuServe, AOL’s early

rival, had a Business Design that

focused on providing informa-

tion to more sophisticated users

and generating revenue

through subscription fees. AOL’s

superior design helped it

reverse CompuServe’s early lead

and leave later-comers like

Prodigy, Microsoft Network,

and AT&T, along with

CompuServe, in the dust. This

battle was won very early by

choices AOL made in its

Business Design. The winners

in the next battles for commu-

nications services are creating

their winning Business Designs

right now.

Richard S. Christner is a vice

president of Mercer Management

Consulting based in

Washington, D.C.

Achieving sustained shareholder value growth18

reengineer to make up for the shrinking operating profit growth

delivered by a declining Business Design. These are fundamen-

tally company-centric, “inside-out” approaches.

Wanted: A new paradigm for sustained value growth

So how should companies think about creating sustained value

growth? As part of our ongoing research into the topic of value

growth, we studied companies that have successfully delivered

increases in shareholder value. These “grandmasters” of value

growth—ABB, Coca-Cola, Disney, GE, Intel, Microsoft,

Schwab, SMG (the maker of Swatch watches), and Thermo

Electron—collectively created $700 billion in value over the last

20 years. Together, this group represents more than 10 percent of

the value creation in the U.S. equity market over that period.

We found that all of the grandmasters excelled at a discipline we

call Value-Driven Business Design. It demands three broad

capabilities:

— Strategic AnticipationSM: the identification of future “profit

zones,” those places where customers will allow companies to

earn attractive returns. Identifying and occupying these

zones requires a robust understanding of customers’ changing

priorities, economics, and behavior; an “outside-in” approach

CAGR1980-1997

23.3%

12.3%

7.7%

BusinessDesignGrandmasters1

S&P 500

Market ShareLeaders2

1 ABB, Coca-Cola, Disney, GE, Intel, Microsoft, Schwab, SMG, and Thermo Electron. Without Microsoft and Intel, the Grandmasters had a 19.9 percent compoundannual growth rate.

2 Market share leaders include American Airlines, Bethlehem Steel, Digital Equipment, Ford, GM, IBM, Kmart, Sears, United Airlines, and U.S. Steel.

SOURCE: Mercer Management Consulting Value Growth Database

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1980 1982 1984 1986 1988 1990 1992 1994 1996

Indexed to 1980 Values

Exhibit 5 Companies thatmaster the discipline ofBusiness Design are wellrewarded

Mercer Management Journal 19

to strategy development; and a disciplined effort to under-

stand the implication of these insights.

— Business Design: the development of the enterprise blueprint

that will best capture the identified profit zone(s). This

requires making internally consistent and mutually

reinforcing decisions along a number of critical dimensions:

What customers do I wish to serve, and what will I have to

offer them? How will I capture my fair share of the value I

create for customers? What features do I need to build into

my business in order to protect my profit stream? What

activities should I own versus outsource? How do we increase

the likelihood of success through our organizational systems?

— Value growth realization: the strategy, systems, and processes

to galvanize the organization to create the new Business

Design.

The grandmasters also shared the fundamental recognition that

no Business Design is forever, and that continual vigilance and

reinvention are essential ingredients of sustained value growth.

The rewards of this approach to strategy are staggering. We

compared the value growth of grandmasters with that of market

share leaders still playing by the old rules. From 1980 to 1997,

the grandmasters have generated 23.3 percent compound annual

growth in shareholder value, compared with 7.7 percent for the

market share leaders and 12.3 percent for the S&P 500 (see

Exhibit 5).

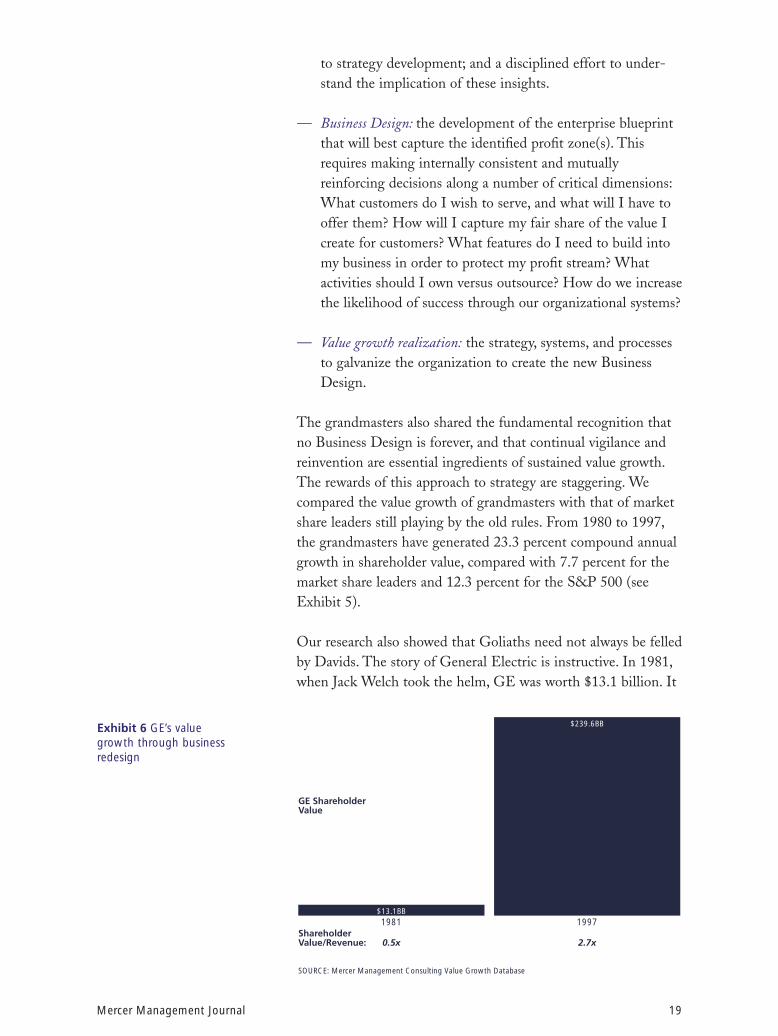

Our research also showed that Goliaths need not always be felled

by Davids. The story of General Electric is instructive. In 1981,

when Jack Welch took the helm, GE was worth $13.1 billion. It

1981 1997

GE ShareholderValue

SOURCE: Mercer Management Consulting Value Growth Database

ShareholderValue/Revenue: 0.5x 2.7x

$13.1BB

$239.6BBExhibit 6 GE’s valuegrowth through businessredesign

Achieving sustained shareholder value growth20

was a diversified manufacturer of both industrial and consumer

products, from light bulbs to jet engines to locomotives to plastic

resin. GE’s shareholder-value-to-revenue ratio—its market capi-

talization divided by its annual sales—was 0.5. By 1997, GE had

grown to become the most valuable company in the world, with

a market value of $239.6 billion and a shareholder-value-to-rev-

enue ratio of 2.7 (see Exhibit 6).

How did Welch achieve this feat? He worked smarter as well as

harder. Over 16 years, he reinvented GE, transforming it from a

classic product-oriented manufacturer into a services company

where products are viewed as just a component of the total solu-

tion provided to customers. Welch’s capacity for Strategic

Anticipation is exceptional; based on his customer-driven under-

standing of where the profit zone will be tomorrow, he has guid-

ed the company through an evolution of Business Design phases

(see Exhibit 7).

His talents for Business Design and value growth realization are

no less impressive. In the early 1980s, Welch saw that occupying

the profit zone for most of GE’s businesses meant capturing

dominant share in chosen product markets. In response, he gave

the organization a challenge: Be Number 1 or Number 2 in a

sector or exit the business. As the mid-1980s arrived—and based

on his frequent interactions with the CEOs of GE’s customers—

Welch saw the profit zone shifting. Increasingly powerful cus-

tomers facing more intense competition were beginning to seek

price concessions. In such an environment, GE’s sustained prof-

itability and value growth would be challenged if it continued to

view itself as a manufacturer—even one with a Number 1 or 2

market position. While good products would continue to be

essential to building good customer relationships, the new profit

zone would be solutions, services, and outsourcing.

Legendary value creators

excel in three broad areas:

Strategic AnticipationSM,

the identification of future

“profit zones”; Business

Design, the development

of the enterprise blueprint

that will best capture the

identified profit zone(s);

and value growth

realization, the galvanizing

of the organization to

create the new Business

Design.

• Achieving marketshare leadership toincrease profit perproduct sold

• Exit any productarea where GE isneither #1 nor #2

#1 or #2

Services and Solutions for Profit Growth

• Capturing “beyond the product” profit by improvingcustomers’ systems economics through solutions selling

• Product plus:- Financing- Maintenance- Service

Early 1980s

Early 1990sExhibit 7 GE’s evolvingBusiness Design focus

Mercer Management Journal 21

To occupy the customer solutions profit zone, GE thought

beyond the product to the entire economic equation of the cus-

tomer’s use of the product. Harnessing product and process

knowledge to optimize these systems economics for customers

was key to unlocking downstream profits. Welch aggressively

expanded GE Capital Services, which provided financing to cus-

tomers of its own, and others’, products. By 1995, through both

acquisition and internal development, GE Capital had amassed

$186 billion in assets, making the company as large as the third

largest bank in the United States. Simultaneously, Welch ramped

up GE’s maintenance and outsourcing businesses. These moves

were all essential to delivering complete solutions to customers.

The reward for these reinventions has been extraordinary, as can

be seen from a comparison of GE with United Technologies,

another traditional manufacturing company that could have

made similar choices. From 1981 forward, GE delivered

19.9 percent annual shareholder value growth, while United

Technologies delivered 13.5 percent. Importantly, the power of

GE’s customer solutions Business Design has won it a much

higher shareholder-value-to-revenue ratio (see Exhibit 8).

Living by the new rules

Our study of leading value creators offers critical lessons for

business leaders. To achieve sustained value growth in today’s

marketplace requires four mindset shifts:

SOURCE: Mercer Management Consulting Value Growth Database

GE

United Technologies 0.2

0.50.7

2.7

UnitedTechnologies

GE1981 1997

$0

$50

$100

$150

$200

$250

$300

Shareholder Value ($BB) Shareholder-Value-to-Revenue Ratio

1981 19970

1

2

3

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Exhibit 8 Workingsmarter: GE vs. UnitedTechnologies

Achieving sustained shareholder value growth22

— From inside-out to outside-in. Understanding customers is the

cornerstone of effective strategy. With Business Design life-

cycles shortening, winning strategies are rarely based on yes-

terday’s core competencies.

— From revenue to profit. Top-line growth is not always good.

Sometimes a more focused approach to customer selection

creates a smaller, yet more profitable and more valuable,

enterprise.

— From product and technology to Business Design. Great products

and technologies are insufficient to guarantee success. They

must be embedded in a comprehensive Business Design that

is calibrated to deliver competitively superior utility to cus-

tomers.

— From market share to value share. Size still matters, but the

metric has changed. Business leaders must create strategies

that not only create shareholder value, but also enable the

company to capture an increasing share of its sector’s total

market value.

The rate of change in customers and industries demands that we

abandon traditional approaches to planning and strategy.

Extrapolation of the past no longer works. To win, business lead-

ers must inform their current investment decisions with an “out-

side-in” perspective on where customers will allow suppliers to

make a profit in the future. Just as the generals of the Gulf War

decimated a much larger force by waging war in a different way,

so must business leaders—the ones, at least, who hope to achieve

victory—embrace a new paradigm for business strategy.

Adrian J. Slywotzky is a vice president of Mercer Management

Consulting based in Boston. He is the co-author of The Profit Zone:

How Strategic Business Design Will Lead You to Tomorrow’s

Profits and the author of Value Migration: How to Think Several

Moves Ahead of the Competition. David J. Morrison is a vice

president of Mercer Management Consulting based in Boston and the

co-author of The Profit Zone. James A. Quella is a vice chairman of

Mercer Management Consulting based in New York.

Mercer Management Journal 23

No one is more familiar with the challenge of achieving sus-

tained shareholder value growth than senior executives who

wrestle with it in the decisions they make every day. They know

that simplistic solutions and outdated strategies will do little for

them as they work toward that goal in a competitive, rapidly

changing global marketplace.

With that in mind, Mercer Management Journal conducted a “vir-

tual” roundtable discussion designed to glean value-growth

insights from top executives in a number of industries. The dis-

cussion took the form of individual interviews in which the exec-

utives responded to a set list of questions. The participants

included:

Dr. A. B. Fred Bok, chairman and chief

executive officer, Philips Business

Electronics, one of nine product divi-

sions of Philips Electronics N.V. The

division sells information products, sys-

tems, and services. Philips, with 1997

revenue of 76.5 billion Dutch guilders

($37.3 billion) and 265,000 employees,

is based in Eindhoven, the

Netherlands.

Donald L. Boudreau, vice chairman for

consumer banking at Chase Manhattan

Corp., one of the largest banks in the

United States. Chase, the product of the

1996 merger of Chemical Bank and

Chase, had 1997 revenue of $30.4 bil-

lion. The company, which has 68,000

employees, is based in New York.

A discussion by five top

executives from a variety of

industries highlights some

of the issues facing business

leaders as they strive to

achieve sustained value

growth. One conclusion:

Companies can’t just

continue to do what they do

now, only better. They have

to reinvent themselves—

to “change the hand,” as one

panelist says, “as opposed

to changing the glove.”

“Changing the hand instead of the glove”An executive roundtable on shareholder value growth

“Changing the hand instead of the glove”24

Kenneth W. Freeman, chairman and

chief executive officer of Quest

Diagnostics Inc., one of the leading

clinical laboratories in the U.S. Quest

Diagnostics, known as Corning

Clinical Laboratories before it was

spun off from Corning Inc. last year,

had 1997 revenue of $1.5 billion. The

company, which has 15,000 employ-

ees, is based in Teterboro, New Jersey.

Raymond W. LeBoeuf, chairman and

chief executive officer of PPG

Industries Inc., one of the world’s

leading glass and paint manufacturers.

PPG, founded in 1883, had 1997

revenue of $7.4 billion. The company,

which has 31,900 employees, is based

in Pittsburgh.

Didier Pineau-Valencienne, chairman

and chief executive officer of

Schneider Electric S.A., a worldwide

leader in the electrical distribution,

industrial control, and automation

industries. Schneider, founded in

1836, had 1997 revenue of 47.4 billion

French francs ($8.2 billion). The com-

pany, which has 61,500 employees, is

based outside Paris.

Mercer Management Journal: Thank you for taking the time to share

your thoughts with us. As a starting point, where does sustained

shareholder value growth fall on your list of priorities?

LeBoeuf (PPG): Along with sustained and consistent earnings

growth, it’s right at the top of our priorities. We recognize that

shareholders can move with great swiftness, that investment cap-

ital is highly fungible, and that a company like ours can’t be sat-

isfied with just comparing ourselves to peers in the businesses in

which we operate. We’ve defined our peers today as “everyone

out there competing for capital.” And when you look at it that

way, you find that the Microsofts, the Intels, the General

Electrics, the Pepsicos, the Emersons fall onto investors’ comput-

Mercer Management Journal 25

“Our customers are no

longer satisfied with merely

competitive products. They

also want services and

solutions adapted to their

problems. . . . Products alone

no longer drive our

business.”

—Didier Pineau-Valencienne

er screens as being competitors that you’re going to be measured

against on an ongoing basis. So, coming back to your question,

shareholder value becomes preeminent in terms of driving a

company.

MMJ: Is it getting harder to achieve this kind of growth?

LeBoeuf: If you take the macro, long-term look at it, you’d say,

“Well, it gets increasingly difficult as you mature in the

businesses in which you operate.” But I think there are some

reasons to believe that it can get easier, in the sense that your

people are more directed toward these issues today than they’ve

ever been before. So for driving shareholder value, in terms of

marshaling your resources—principally your people—I think

we’re in better shape today than we were 20 years ago. But,

again, if you look at it in terms of certain external forces, of

course it’s more difficult, because everybody’s getting better at

doing it. More people today are focusing on the shareholder as

being a principal, if not the principal, scorekeeper in evaluating

your performance as a corporation.

MMJ: How widely accepted is a value growth philosophy in Europe?

Pineau-Valencienne (Schneider): Only in the last two or three

years has the concept of shareholder value begun to spread in

France, where many enterprises have long operated under state

control—although, like other large French corporations,

Schneider adopted this approach earlier because of its sharehold-

er base, which includes Anglo-Saxon investors, in particular.

Bok (Philips): Europe is clearly behind the U.S. Penetration is not

high here; it is just beginning. I think it will take three to five

years to get sufficient penetration among the more important

firms. In faster-moving industries—electronics, for example—

change is happening relatively fast, as management thinking is

globalizing. In more traditional and in more regional European

industries—textiles, some engineering-driven industries, etc.—I

don’t see change happening for a while. The biggest change fac-

tor there will be demographic, as the older generation retires and

younger individuals take over.

MMJ: One of the challenges of achieving sustained shareholder value

growth these days is the rate and relentlessness of change, as value

migrates from one company or industry to another. How are you

affected by that?

“Changing the hand instead of the glove”26

“A lot of older companies,

in particular, think they’re

solving the problem by

trying harder and running

along the same curve faster.

And all they’re doing is

flattening the curve faster.”

—Raymond W. LeBoeuf

Boudreau (Chase): The rate of change has been dramatic. If you

go back twenty years, someone wanting a loan to buy a car went

to a bank; if you wanted a mortgage you went to a bank. Bank

cards were defined by banks. Begin to fast forward that. Little

changes began to take place, some of which seemingly facilitated

banks doing the business better. But, as often happens—and will

continue to happen as technology continues to redesign business

systems—those changes cleared the tracks for non-entrenched

players. What that’s doing is repositioning in the minds of cus-

tomers who the providers are for financial services. You used to

have to go to a branch to do a lot of stuff that today no longer

requires going to a branch, or even to a bank. So we can hang a

lot of bunting on branches, but customers aren’t coming back to

us there. To stay there is a destruction of shareholder value.

MMJ: How does a business cope with this kind of change?

Freeman (Quest Diagnostics): We think an awful lot about what

the world will look like in five to ten years, and how we need to

anticipate that and get in front of it. But, at the same time, we

often get tangled up in the web of: “Okay, well, who is the cus-

tomer, really? What business are we in?” There’s a lot of dialogue

about what it is that customers may or may not want. Probably

not unlike a lot of industries, we have a complex web of cus-

tomers. We’ve got patients—every person in America is, ulti-

mately, potentially a client of ours. We’ve also got the physician

who, in most places, has to say, “I’d like you to have lab tests per-

formed,” before we can actually perform them. And then also, at

the same time, we have customers called “the payors”—federal

and state governments, insurance companies, managed care com-

panies, etc. So, not unlike a lot of industries, where you’ve got

wholesalers and retailers and the end consumer, we’ve got to

please all elements of the chain to be successful.

Pineau-Valencienne: There is one important thing that we’ve

learned: Our customers are no longer satisfied with merely com-

petitive products. They also want services and solutions adapted

to their problems. So that means we need to understand the cus-

tomer and the customer’s business and the customer’s markets,

all with the aim of understanding the customer’s present and

future needs. Products alone no longer drive our business.

Boudreau: The old system in our industry was sort of a branch-

centric notion. The new paradigm, the one that we’re so busy

implementing, is what we call “an information-based business

Mercer Management Journal 27

system.” It essentially has every element of our business support-

ed by an information capability that is constantly reflecting the

insights we gain about our customers and is continuously iterat-

ing that through every aspect of our doing business. This gives us

the ability to recognize a complete customer relationship at any

point a customer shows up. One of the things that this informa-

tion-based business does for us—without question, in every

application—is to empower our people to do more to satisfy cus-

tomers. And it costs us less at the end of the day to have done

so. We make better decisions, we make them in a more timely

way, and we make customers happier. That gives us a retention

benefit, which, again, is a way to maintain shareholder value.

MMJ: We have talked about the changing business environment.

What degree of change must a business itself be prepared to make?

LeBoeuf: One of the things that has allowed a 115-year-old com-

pany like ours to survive is our ability to re-pot ourselves every so

many years, to know when the trendline we’ve been on is begin-

ning to plateau and to move ourselves from that trendline onto

the next one. If the trendline you’re on flattens out, and you’ve

done nothing but continue to move along it, or just try to move

along it at a faster pace, you’re going to die. Conventional ortho-

doxies can be absolutely deadly. They keep you on the same line.

A lot of older companies, in particular, think they’re solving the

problem by trying harder and running along the same curve

faster. And all they’re doing is flattening the curve faster.

Boudreau: There are a couple of things that can happen when

you get into an industry that is rapidly changing, with new cus-

tomer expectations, new competitors, new channels, new ways of

putting packages together. One is, you can redouble your efforts

to recreate the past and try to withstand the market forces. And

essentially, while this works over the short term, it ends up dissi-

pating shareholder value, because what you end up doing is erod-

ing the franchise. The other way to approach it is to anticipate

where the end game is going to be played, what it’s going to look

like, and then to take the position that you’re going to make the

journey with your franchise and your customers. Rather than

railing against change, you begin to say, “We’ve got to be part of

it, and try as best we can to get in front of it, and to not only

participate in it but lead with it.”

Freeman: I think that you always need to strive to do what you’re

doing better, just to keep up with a kind of natural inertia in a

competitive situation. So you still have to keep working to do

“The other way to

approach [change] is

to anticipate where the end

game is going to be played,

what it’s going to look like,

and then to . . . make the

journey with your franchise

and your customers.”

—Donald L. Boudreau

“Changing the hand instead of the glove”28

things better: standardizing your processes, deploying best prac-

tices, all that sort of stuff. But in a situation like this, that’s not

nearly enough. The other piece you have to do is redefine the

game. And redefining the game can come in a number of differ-

ent ways. You can start thinking about how you segment the

market. You can think about geographic market participation.

You can think about acquisitions. But all of those are relatively

conventional answers, and to some degree I think can redefine

the game for only a short period of time. The bigger challenge,

I think, is to actually change the offering—to change the hand,

as opposed to changing the glove.

MMJ: How does a management team go about identifying future

opportunities for shareholder value growth?

Pineau-Valencienne: As a company thinks about change, it’s

important to remember that the concept of shareholder value

cannot be disassociated from what we call “competitive growth,”

or profitable growth. Increasing shareholder value through a

purely financial approach—for example, through cost-cutting

alone—is a sign of short-term vision. You may increase your

share price in the short term, but you won’t get sustained growth

in shareholder value. I prefer the concept of “francs of value cre-

ated for each franc of competitive growth.” This concept is moti-

vating for employees and fits into a long-term vision.

LeBoeuf: One of the things that we’ve tried to do is move from

being a more reactive, inside-out company to a more proactive,

outside-in company, with more of a marketplace focus than in

the past. If you go back twenty to twenty-five years, we were an

“invent it, manufacture it, and then it will sell” company. Very

much inside-out. We looked at: What was the next invention?

Could we make it? And if we could make it, “I’m sure some-

body’s going to buy it.” Then, in the early ’80s, we saw that that

wasn’t good enough—that the customer was damned important.

And we became more of a customer-obsessed company. Now

we’re trying to recognize that the customer and the marketplace

aren’t always the same thing. The customer is a part of the mar-

ketplace, but the marketplace transcends the customer. We try to

be out there understanding the marketplace in which our cus-

tomers deal, and in which we deal, and try to anticipate the

dynamics of that marketplace as we move forward. We think the

next move on the trendline will be built around the marketplace.

So we’re trying to be a proactive, market-sensitive company, and

be out there not just with our customers, but also with our cus-

tomers’ customers, and right down through the chain.

“I think that you always

need to strive to do what

you're doing better, just

to keep up with a kind of

natural inertia in a competi-

tive situation. . . . But that's

not nearly enough. The

other piece you have to do

is redefine the game . . .

change the hand, as

opposed to changing

the glove.”

—Kenneth W. Freeman

Mercer Management Journal 29

Boudreau: We don’t believe just listening to the customer is going

to be good enough going forward. That’s important, but some-

times the customer isn’t able to articulate exactly what new prod-

uct or service improvement they want or need. What we should

be doing continuously is understanding what consumers are try-

ing to do in terms of achieving a financial goal or mitigating a

concern. Our job, it seems to me, is to frame up a response that

meets that requirement in a cost-effective and convenient way.

If we do this well and continuously, it will give our customers a

Chase brand experience that will provide us with a competitive

advantage.

MMJ: How do you get value-growth thinking placed front and center

among your company’s priorities, get it integrated into the organiza-

tional consciousness, and create a dynamic environment for change?

Bok: In one way it’s simple, really. The key to success is clarity.

A CEO needs to pass along a clear vision of what he wants his

management team to do, then hold them accountable for it and

incentivize them on it. Because in Philips Business Electronics

we structure our business units as entrepreneurial companies,

there is transparency about how each unit performs. However,

one big challenge that can arise from value-oriented strategies is

business unit leadership. If a company is value-growth oriented,

it may follow value opportunities to new business designs that

challenge its management team’s perceptions of their businesses.

How do you convince them to follow aggressively? Another

challenge is how a company organizes itself for new business

designs. In technology industries, it is difficult to create an orga-

nizational bridge from the way technologies are nurtured to the

way strong customer relationships are built. Managing both cul-

tures—technology-centric for product performance and cus-

tomer-centric for relevance in the marketplace—is a key success

factor.

Boudreau: The guy running our mortgage business isn’t a mort-

gage banker. He’s got an engineering background. The guy that’s

running the credit card business wasn’t in the credit card business

two years ago. Again, he’s an engineer by background. The rea-

son they were so valuable is that they showed up with a lot of

questions and were willing to search for the answers—as opposed

to being stocked with answers because they had grown up in the

way the business used to be done. In addition, my managers

know that thinking about the future isn’t someone else’s job. It’s

what we all get paid to do all the time. And it never ends. It

“In technology industries, it

is difficult to create an

organizational bridge

from the way technologies

are nurtured to the way

strong customer relation-

ships are built.”

—Dr. A. B. Fred Bok

“Changing the hand instead of the glove”30

seems to me—and I suspect we’re not unique—that you need

excellent people, and then you need a framework and a set of

expectations that empowers them to make decisions. And if you

don’t take that step, if you try to operate the way it used to be—

with a hierarchy, where every decision has got to get signed off

by the level above—you won’t succeed. A command-and-control

management structure is an anathema to an information-based,

empowered system. In the old days, only the people in mortgages

worried about mortgage questions. In the world we’re in today,

customers contact us by PC, by phone, by fax, by ATMs—even

still in branches. We’re going to have channels that’ll be all over

the place. There is no way you’re going to say, “Only ask these

questions in this channel, or these questions in that channel.”

Those days are over.

Freeman: We’ve looked at some radical changes in how we do

business—for example, creating a retail arm and going “direct to

the consumer.” And, as you might expect, there are a lot of rea-

sons why people think it can’t be done. But that’s not a reason to

stop working at it. My guess is, and my belief is, that if the ideas

that we’re working on, to get out of the value migration trap,

aren’t outlandish enough that a fair number of people say up

front, “It can’t be done,” then the odds are we’re not thinking

radically enough.

If you would like to join a discussion on how companies can achieve

sustained shareholder value growth, visit our Mercer Management

Journal Forum, at www.mercermc.com.

Mercer Management Journal 31

Hockey great Wayne Gretzky has explained his phenomenal

success on the ice by saying that, while other players skate

to where the puck is, he skates to where the puck is going to be.

Similarly, we have seen that those companies that are most

skilled at identifying where new business opportunities are going

to be tend to be rewarded with substantial growth in shareholder

value.

Our experience suggests that the customer can represent the

most reliable compass to help a business leader plot his or her

company’s course. But gaining an understanding of the future

through customers is not easy. Businesses have a long history of

missing upcoming trends because they—and the consumers they

query—fail to envision the future environment in which a new

product or technology will be introduced. A 19th century farmer

would have said he needed a stronger and faster horse, not a

tractor. Mercedes-Benz concluded in 1900 that the worldwide

market for automobiles would never exceed 1 million, primarily

because of the limited number of available chauffeurs. Similar

faulty predictions were made in the early history of computers,

photocopy machines, telephones—and, more recently, in the

“broadband” marketplace.

The broadband opportunity

Back in 1995, it was clear that the communications, informa-

tion, and entertainment industries were entering a period of

blistering change and convergence. Technological advances had

made it possible to send enormous quantities of digitized infor-

mation over fiber-optic cables, and the planned broadband net-

works promised both to bring new multimedia services to con-

sumer households and to usher in head-to-head competition

between telephone and cable services.

A winning Business Design

is founded on an insightful

understanding of rapidly

shifting customer priorities.

In 1995, Mercer Manage-

ment Consulting used two

rigorous marketing science

tools to conclude—

correctly, it turns out—that

much of the conventional

wisdom about the future

of multimedia “broad-

band” networks was

wrong.

Identifying the opportunities of the futureStrategic AnticipationSM through marketing science

by Eric Almquist

and Gordon Wyner

Identifying the opportunities of the future32

The signs of change were many: America Online was becoming

a darling of Wall Street; the Internet had reached a 2 percent

household penetration level and was starting to make business

press headlines; MCI had just invested $2 billion in media giant

News Corporation, one of a number of multimedia megadeals;

and local phone companies were projecting they would have

broadband services to 20 percent of U.S. households by the

year 2000.

It was clear that Value Migration®—the shifting of profits and

stock market value between companies or industries—was about

to accelerate. But its rate, direction, and magnitude were clouded

in uncertainty. In this volatile environment, Mercer Manage-

ment Consulting undertook to find out where customers would

allow companies to make a profit in the coming years and which

Business Designs would prevail.

Industry experts and technology pundits had already built up a

body of predictions concerning the broadband marketplace:

— Video-on-demand services would boom. Substantial demand

for enhanced pay-per-view services would largely justify the

cost to build out the broadband network.

— The Internet would remain a power-user curiosity. The

Internet would not—in the short term—achieve meaningful

penetration outside of a limited group of sophisticated,

high-end users.

— Video telephones would not be a short- to medium-term opportu-

nity. Consumers would not embrace videophones—which

had died a thousand deaths since the New York World’s Fair

of 1964—until quality was high.

— One-stop shopping from well-known brands would prevail.

Consumers would seek to minimize the complexity of the

numerous communication, entertainment, and information

services offerings by relying on branded consolidators, either

cable or telephone companies.

To evaluate these assumptions, as well as to identify areas of

opportunity within the broadband universe, Mercer turned to

customers. The firm’s 1995 study, “Colliding Worlds: Separating

the Virtual from the Reality,” combined customer research, com-

petitive economic analysis, and game theory to address the

problem.

Mercer Management Journal 33

Marketing science for Strategic AnticipationSM

This was clearly a challenging task. Estimating the future

demand and profit power of new and emerging products and

technologies with which consumers had no familiarity wouldn’t

be easy. We were fortunate to have at our disposal a number of

proprietary marketing science tools that enabled us to develop a

fact-based, robust picture of future customer segment priorities,

behaviors, and values. These tools enabled us to condition cus-

tomers to a future world and then—in the context of this new

world—to evaluate their decision-making process.

The consumer demand research started with a national sample

of 850 randomly chosen consumers, all with household incomes

greater than $10,000. Mercer introduced these consumers to a

world of broadband capability, showed them examples of new

broadband-related services, and asked them to choose between

available offerings at various prices. This research project relied

heavily on two research techniques: Information Acceleration™

and Strategic Choice Analysis®, both developed at academic

institutions and adopted by Mercer over the last 15 years.

Information Acceleration “accelerates” consumers into an all-

encompassing future market environment. Sitting at an interac-

tive multimedia workstation that uses video, graphics, sound,

motion, and text, consumers are able to experience an array of

new products and services. They see and hear simulated testimo-

nials, advertisements, in-store displays, sales presentations, prod-

uct literature, and other elements of the marketing mix. Glenn

Urban, of MIT’s Sloan School of Management, developed

Information Acceleration based on methodologies he created

for forecasting demand for consumer packaged goods. This

approach is now licensed exclusively to Mercer.

Once consumers are conditioned to the future, the use of

Strategic Choice Analysis provides the tools to develop a power-

ful consumer decision model. This model allows us to estimate

market sizes, provider shares, product penetration, demand elas-

ticities, and profitability. Discrete choice theory, the backbone of

Strategic Choice Analysis, was developed at several academic

institutions in the 1960s; the first practical applications were in

the field of public transportation, including estimating the

demand for San Francisco’s Bay Area Rapid Transit system.

Mercer drew on the literature of discrete choice theory to devel-

op Strategic Choice Analysis, which we have used in over

300 mainstream marketing applications across the transporta-

tion, financial services, and communications industries.

Information Acceleration™

drops consumers into an

all-encompassing future

marketplace. Once they are

conditioned to the future,

Strategic Choice Analysis®

gauges their preferences.

In the 1995 broadband

study, consumers were

asked to consider how they

would use the new

technology—not in the

context of 1995, but in a

richer, more “futuristic”

environment of 2000

to 2005.

Identifying the opportunities of the future34

In Mercer Management Consulting’s broadband study, con-

sumers were asked to consider how they would use the new

technology—not in the context of 1995, but in a richer, more

“futuristic” environment of 2000 to 2005. First, consumers were

placed in a future of electronic media and made familiar with

how these media might change their lives. They were then

introduced to numerous multimedia and electronic broadband

applications—from home banking to video-on-demand to time-

shifted television—at different price points and asked to choose

whether they would buy any of these new services or stick with

the ones they currently had (see Exhibit 1).

Because brands have a significant influence over buying deci-

sions, we also asked the consumers to choose among six

providers whose names were familiar to them, ranging from

their local telephone companies to national cable providers.

They were asked to make their decisions based on price, per-

formance options, and various product bundles—as well as

brand.

While these tools—Information Acceleration™ and Strategic

Choice Analysis®—can be used independently, their power is

enhanced when they are used together. This is particularly true

when evaluating a market like broadband, where the future is

uncertain, the required investment is huge, the products and

services are unfamiliar, and the potential Business Design

options are plentiful.

Identifying “profit zones” in the broadband marketplace

The three years that have passed since this research was com-

pleted enable us to evaluate just how prescient these tools can

be—and how valuable they can be in providing executives with

the information needed to invest in attractive customer-driven

opportunities ahead of the curve.

Information Acceleration™

• “Accelerate” consumerinto the future

• Illustrate the newcompetitive landscape

• Voice and videophone

• Traditional cable, video-on-demand, near video-on-demand, time-shifted TV,interactive TV

• Information, shopping,banking, chat, and otheronline services

From among future offerings:

• Six brands

• Different prices

• Performance options (e.g.,picture quality)

• Bundling options

Future Market

Strategic Choice Analysis®

Future Conditioning Future Services Consumer Choices

• Size

• Provider shares

• Product penetration