busi 163 notes

TRANSCRIPT

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 1/22

Chapter 1 2/2/2013 11:23:00 AM

3 Kinds of FX Markets:

Spot Market - By and sell based on current price

Forward Market – By currency today at pre-determined price, but

complete transaction at a time specified in the future

Swap Market – Return to this topic later in class

FX Market has no physical location (trade in OTC market)

Open 24 hours on weekdays (flexible)

How money – invest for speculative returns vs. long-run return

If you do not have regulations in place, you should not open your

market to speculators (East Asian Crisis of 1998)

Indirect quote => foreign currency/home currency

Direct quote => home currency/foreign currency

Banks or airports

Easier for a domestic person to understand

Cross-rate => foreign currency/foreign currency

0.0001 = 1 basis point = .01%

Spot Market

Cross-rate example: Derive CAD/EUR cross-rate

$0.98 USD/CAD

$1.22 USD/EUR

(1.22 USD/EUR) / (0.98 USD/CAD)

= 1.2449 CAD/EUR

Sometimes in the business world, it is possible to find cross-rate that does

not match the mathematical derivative

Way to make profit by taking advantage of the difference

Arbitrage = risk-free profit

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 2/22

Now that trading is done by computer, arbitrage is no longer

possible

Currency change given a direct quote:

(Ending Price – Opening Price) / Opening Price If given an indirect quote, convert to direct quote first

o 1 / indirect quote

If given a cross-rate, ensure that your are consistent

FX Currency Change Example 1:

Day 1: 0.98 USD/CAD

Day 2: 1.02 USD/CAD

(1.02-0.98)/0.98 = .0408 (4 decimal places)

CAD appreciated against USD by 4.08%

FX Currency Change Example 2 (cross-rate):

Day 1: 1.23 CAD/EUR

Day 2: 1.19 CAD/EUR

(1.19-1.23)/1.23 = -.0325

EUR depreciated against CAD by 3.25%

Absolute Bid-Ask Spread Example: Dealer buys at 1.2000 USD/EUR (Bid Price)

Dealer sells at 1.2200 USD/EUR (Ask Price)

1.22 – 1.20 = $0.02 USD profit (Absolute Bid-Ask Spread)

If turnover/volume is low, the dealer will charge higher commission to make

profit

If currency is very liquid, profit margin is small but turnover/volume is high

(allowing them to make profits)

Relative Bid-Ask Spread

(Ask price – Bid price) / Ask price

Used to standardize the bid-ask spread because it gives a

percentage value

Allows you to measure transaction cost

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 3/22

Relative Bid-Ask Spread Example:

Dealer buys at 1.2000 USD/EUR (Bid Price)

Dealer sells at 1.2200 USD/EUR (Ask Price)

(1.22-1.2)/1.22 = 1.64% (Relative Bid-Ask Spread) If trading $1000 USD,

o $1000 * 1.64% = $16.40 (Transaction Cost)

Relative Bid-Ask Spread (transaction cost) Example:

Buy EUR, sell 1000 USD to the dealer

1000 USD / (1.22 USD/EUR) = 819.67 EUR

Sell 819.67 EUR back to the dealer and buy USD

819.67 EUR * 1.20 USD/EUR = $983.60 USD

$983.60 - $1000 = -$16.40 (transaction cost)

Transaction cost is round trip

OANDA FX Game

Example: EUR/USD

o EUR = primary currency

o USD = secondary currency

Buying/selling the primary currency for/with the secondary currency

XAU = gold XAG = silver

Short sell – selling an asset that you do not have

Borrow from the dealer

Sell acquired asset in the market for current (market) price

(Hopefully) when the asset drops in the market, you buy back the

asset and return it to the dealer (plus interest)

Margin Account

Only have to pay a portion of the price (borrow the rest)

Have to put more into your account (margin call) if you losses

exceed the amount you put in

o If you do not put more money into your account, the dealer

will close it

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 4/22

Dealer charges interest for the time you buy on margin

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 5/22

8/30/2012 4:57:00 PM

Goal of financial management?

Maximize Cash flow

Maximize Profit

Maximize Market share

Corporate company structure

Assets (controlled by mangers/employees)

Debt holders (liability)

Shareholders (equity)

Must act in the best interest of shareholders

Shareholder’s value

Stock price * #shares outstanding

Firm value = CF1 /(1+i) + CF2 /(1+i)2+…+CFn /(1+i)n

i=discount rate

discount rate reflects rate of return you are expecting given the risk

of the company

Increase firm value by increasing cash flows and/or decreasing risk

Reason’s for going abroad

Develop new markets Cheap labor

Outsourcing (costs, strengths of labor force)

Regulation at home

Risk diversification

Natural resources

International risks

Political risk

Foreign market risk

Cultural difference

Natural disaster

Differing management style

Control

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 6/22

Corporation benefits

Limited liability

Easier to raise capital

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 7/22

8/30/2012 4:57:00 PM

Current Account

Trade Balance = Export – Import

Surplus (if positive) or Deficit (if negative) GDP = Consumption + Investment + Government Spending +

Trade Balance

1) Inflation

Inflation of U.S.

o Inversely related with U.S. export

o Directly related with U.S. import

Inflation of foreign country

o Directly related with U.S. export

o Inversely related with U.S. import

2) FX Rate

US FX Rate

o Inversely related with U.S. export

o Directly related with U.S. import

Depreciation alone is an ineffective policy

o Competitors cut their own price/depreciate their own currencyo Transfer price / Inter-firm trade

International trade between subsidiaries of single MNC

Not effected by external exchange rate

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 8/22

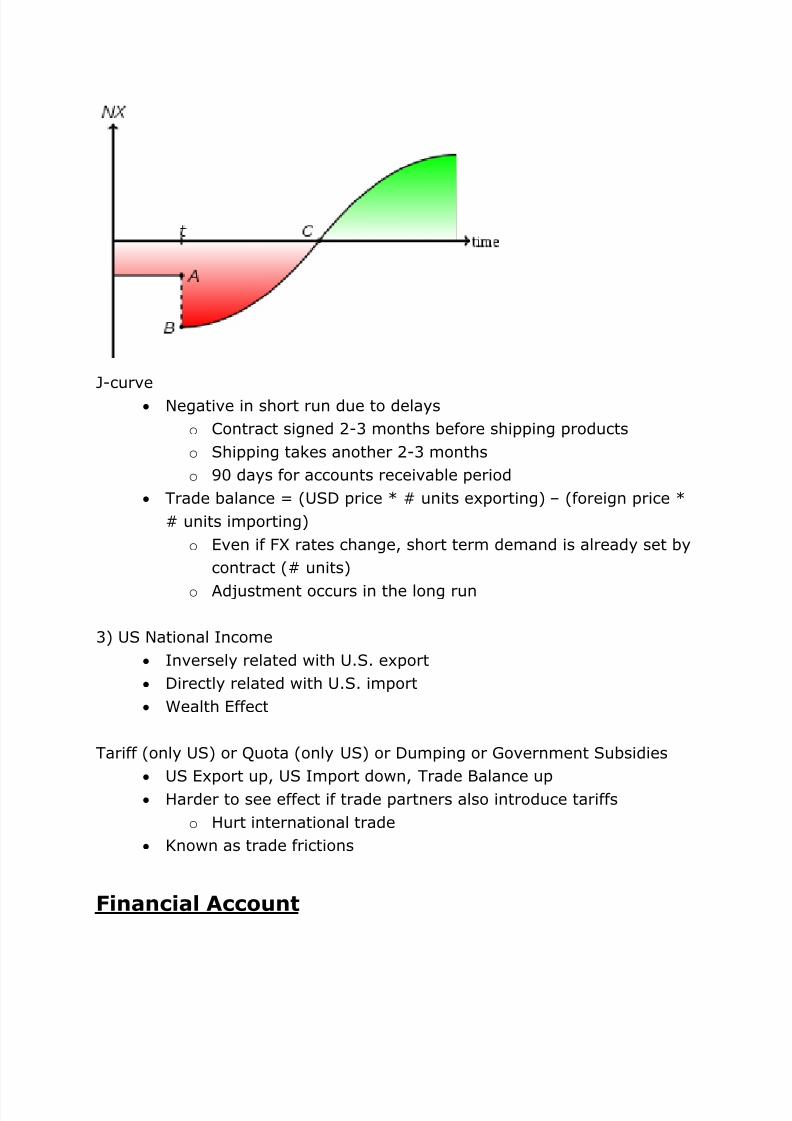

J-curve

Negative in short run due to delays

o Contract signed 2-3 months before shipping products

o Shipping takes another 2-3 months

o 90 days for accounts receivable period

Trade balance = (USD price * # units exporting) – (foreign price *

# units importing)

o Even if FX rates change, short term demand is already set by

contract (# units)

o Adjustment occurs in the long run

3) US National Income

Inversely related with U.S. export

Directly related with U.S. import

Wealth Effect

Tariff (only US) or Quota (only US) or Dumping or Government Subsidies

US Export up, US Import down, Trade Balance up

Harder to see effect if trade partners also introduce tariffs

o Hurt international trade

Known as trade frictions

Financial Account

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 9/22

Foreign Direct Investment Economic growth/strength

Institutions (government/culture)

Tax

Government PolicyInternational Portfolio Investment

Interest rate

o Attracts “Hot money” – not good for economy

Tax

Government Policy

Others

Fixed exchange regime All countries fix their exchange rates to USD

After WWII

o US had the gold to support the currencies

Bretton Woods Agreement

Ends in 1971

o France first to say USD is overvalued

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 10/22

8/30/2012 4:57:00 PM

Unholy Trinity – Can only achieve 2 at once

Currency stability

Open capital market

Independent monetary policy

Effects of having a fixed rate currency

Exporting inflation

o Hong Kong rate fixed to USD

Inflation in US goes up

Demand for Hong Kong products go up

Prices in Hong Kong go up

Exporting unemployment

o US unemployment goes up

Imports go down

o Demand for Hong Kong products goes down

Hong Kong job cuts up

Unemployment up

Examples of FX Markets (Japan Perspective)

Spot market

o Sell yeno Buy dollar

Forward market

o Buy yen

o Sell dollar

Swap market

o Selling today

o Repurchase in the future at a fixed price

Currency Inventory Cost

Opportunity cost of keeping cash in banks

The higher the interest rate on currency, the higher the opportunity

cost

Euro prefix – describe offshore currencies

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 11/22

Eurodollar – name to describe offshore US dollars

Euroeuro – name to describe offshore euros

Syndicator

Group of banks that share risk/loans given to client Lead bank to organize administration between banks

International bond market

Loan maturity generally greater than 5 years

o Due to large size of the bond

2 Types of bonds

o Eurobond – currency denomination of bond is different from

the issuing county’s currency

Bearer form – anonymous owner / amount of bond

Attractive for investors looking to avoid taxes on

income generated from investment

o Foreign bond - currency denomination of bond is same as the

domestic market’s currency

Capital Reserve

Amount that banks have on hand

Focus on standardization reserve requirementso Basel Accord – 8%

ADR – American Depository Receipt

Foreign firm -> US Depository Bank -> ADR -> US Investors

ARD I only traded in OTC market

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 12/22

Financial Derivatives 2/2/2013 11:23:00 AM

Hedging strategy to reduce risk

Foreign exchange rate risk

o Exporting

Receive foreign currency

If FX rate depreciates, revenue goes downo Importing

Pay foreign currency

If FX rate appreciates, cost to import goes up

Forward Contract

o Example:

Forward Contract for 3 months later at $1.00/euro

Current FX rate $1.00/euro

Future FX rate $1.50/euro

($1.50/euro - $1.00/euro) * 10,000 euro = $5,000 =

price of contract

Buy 10,000 euro at $1.00/euro using contract for

$10,000

Sell 10,000 euro in the market and get $15,000

$5,000 profit

o Both buyer and seller are bound to the contract

Hedging Strategies Payable of foreign currency (import)

o Buy forward

o Buy futures

o Buy call option

Receivable of foreign currency (export)

o Sell forward

o Sell futures

o Buy put options

Need to make payment of Euros in three months (hedge against

euro rising)

o Buy euro forward (for large institutional investors)

o Buy euro futures

o Buy call option

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 13/22

Forwards & Futures 8/30/2012 4:57:00 PM

Parts of a Forward Contract

1. Quantity

2. Future Date

3. Type of Assets

4. Price of Assets5. Buyer and Seller

i. Obligation to buy and sell at agreed upon date in the future at

agreed upon price

ii. Can only be traded OTC

Forward rate = rate 3 months in the future

Forward premium (When Forward rate > Spot rate)

Expectation of how much the currency will appreciate in the future

Forward discount (When Forward rate < Sport rate)

Expectation of how much the currency will depreciate in the future

(Forward rate – Spot rate) / Spot rate = Forward premium or discount

Annualized forward premium or discount

Multiple by 4

Calculate Profit/Loss in Forward Contract

Buyer: (Forward rate – Spot rate) * Contract Size

Seller: (Spot rate – Forward rate) * Contract Size

Assuming no transaction cost

Futures contract is similar to a forward contract, but can be traded publically

on an organized securities exchange

Very liquid (can buy/sell in secondary market)

Highly structured

Mark-to-Market

Margin account – do not need to pay 100% of amount for the trade

Margin call if your account balance drops below maintain amount

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 14/22

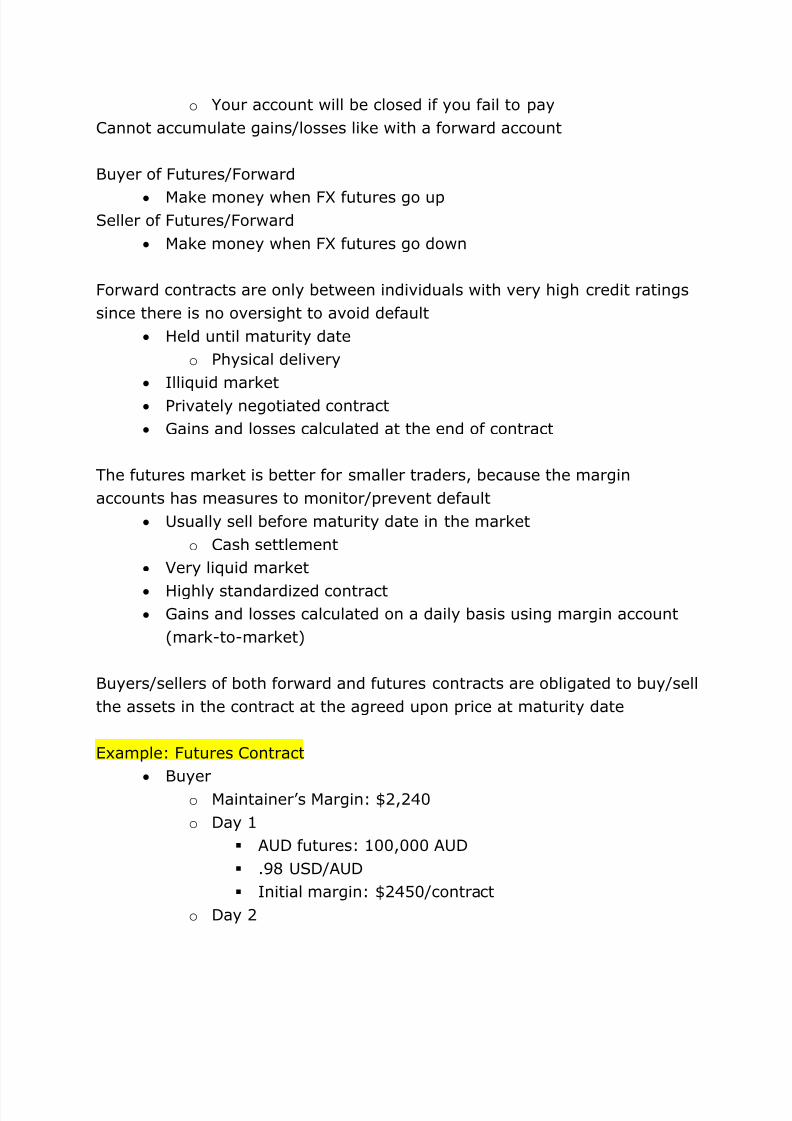

o Your account will be closed if you fail to pay

Cannot accumulate gains/losses like with a forward account

Buyer of Futures/Forward

Make money when FX futures go upSeller of Futures/Forward

Make money when FX futures go down

Forward contracts are only between individuals with very high credit ratings

since there is no oversight to avoid default

Held until maturity date

o Physical delivery

Illiquid market

Privately negotiated contract

Gains and losses calculated at the end of contract

The futures market is better for smaller traders, because the margin

accounts has measures to monitor/prevent default

Usually sell before maturity date in the market

o Cash settlement

Very liquid market

Highly standardized contract Gains and losses calculated on a daily basis using margin account

(mark-to-market)

Buyers/sellers of both forward and futures contracts are obligated to buy/sell

the assets in the contract at the agreed upon price at maturity date

Example: Futures Contract

Buyer

o Maintainer’s Margin: $2,240

o Day 1

AUD futures: 100,000 AUD

.98 USD/AUD

Initial margin: $2450/contract

o Day 2

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 15/22

1.00 USD/AUD

(1.00 – 0.98) * 100,000 * 100 = $200,000

Margin = 200,000 + (2,450*100) = $445,000

o Day 3

.97 USD/AUD (0.97 – 1.00) * 100,000 *100 = -$300,000

Margin = -300,000 + $445,000 = $145,000

(Margin Call)

$224,000 - $145,000 = $79,000 to margin

account to maintain

Cross-hedging (in futures contract)

Due to standardization, you may not be able to find the exact asset

you are looking to hedge against

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 16/22

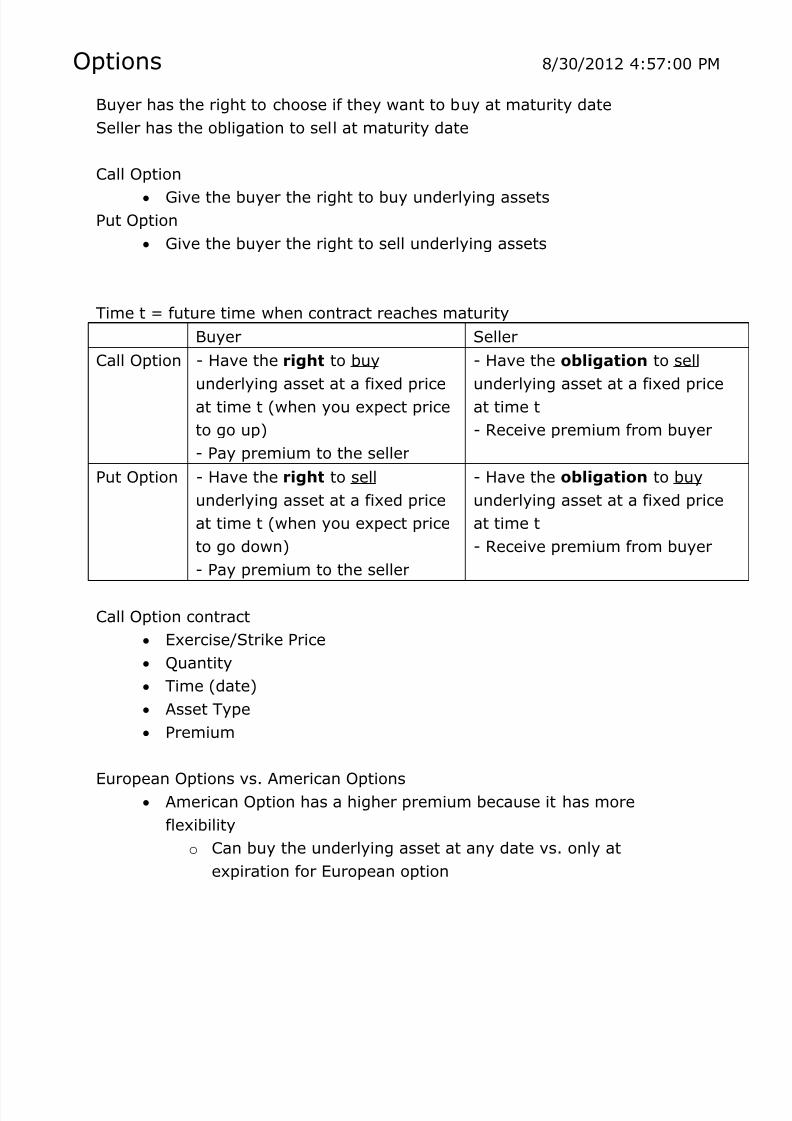

Options 8/30/2012 4:57:00 PM

Buyer has the right to choose if they want to buy at maturity date

Seller has the obligation to sell at maturity date

Call Option

Give the buyer the right to buy underlying assetsPut Option

Give the buyer the right to sell underlying assets

Time t = future time when contract reaches maturity

Buyer Seller

Call Option - Have the right to buy

underlying asset at a fixed price

at time t (when you expect price

to go up)

- Pay premium to the seller

- Have the obligation to sell

underlying asset at a fixed price

at time t

- Receive premium from buyer

Put Option - Have the right to sell

underlying asset at a fixed price

at time t (when you expect price

to go down)

- Pay premium to the seller

- Have the obligation to buy

underlying asset at a fixed price

at time t

- Receive premium from buyer

Call Option contract

Exercise/Strike Price

Quantity

Time (date)

Asset Type

Premium

European Options vs. American Options American Option has a higher premium because it has more

flexibility

o Can buy the underlying asset at any date vs. only at

expiration for European option

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 17/22

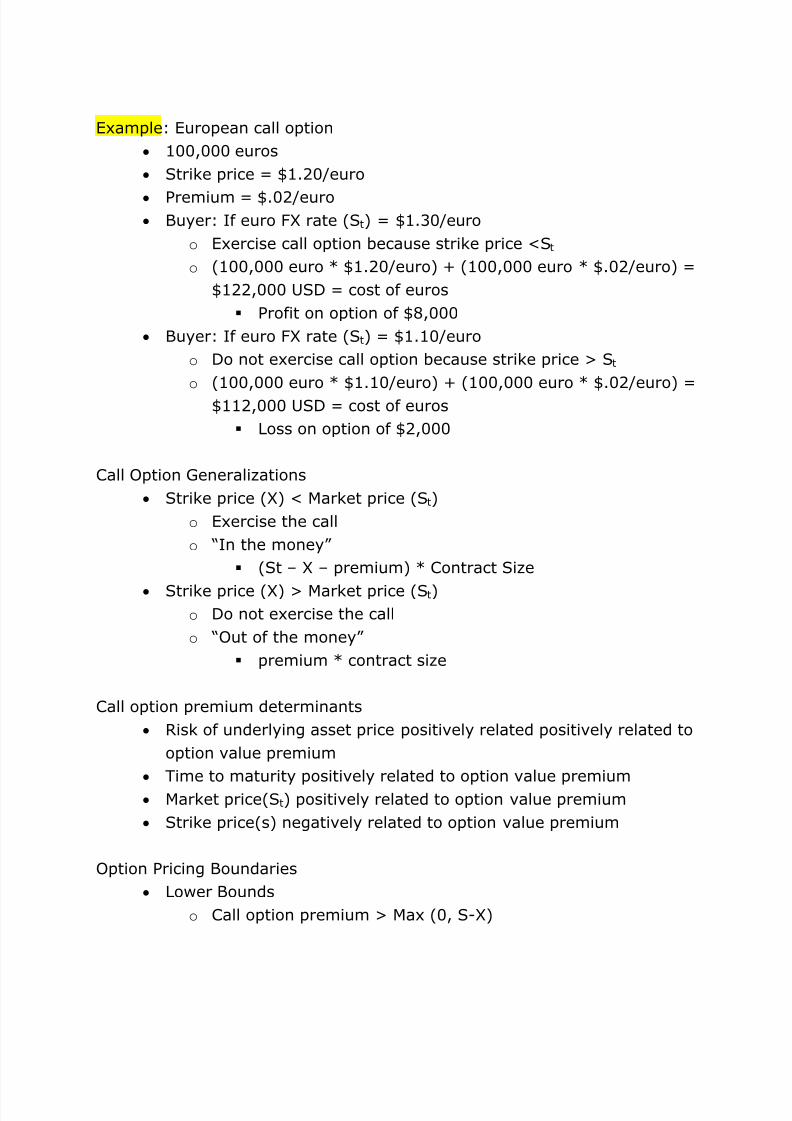

Example: European call option

100,000 euros

Strike price = $1.20/euro

Premium = $.02/euro Buyer: If euro FX rate (St) = $1.30/euro

o Exercise call option because strike price <St

o (100,000 euro * $1.20/euro) + (100,000 euro * $.02/euro) =

$122,000 USD = cost of euros

Profit on option of $8,000

Buyer: If euro FX rate (St) = $1.10/euro

o Do not exercise call option because strike price > St

o (100,000 euro * $1.10/euro) + (100,000 euro * $.02/euro) =

$112,000 USD = cost of euros

Loss on option of $2,000

Call Option Generalizations

Strike price (X) < Market price (St)

o Exercise the call

o “In the money”

(St – X – premium) * Contract Size

Strike price (X) > Market price (St)o Do not exercise the call

o “Out of the money”

premium * contract size

Call option premium determinants

Risk of underlying asset price positively related positively related to

option value premium

Time to maturity positively related to option value premium

Market price(St) positively related to option value premium

Strike price(s) negatively related to option value premium

Option Pricing Boundaries

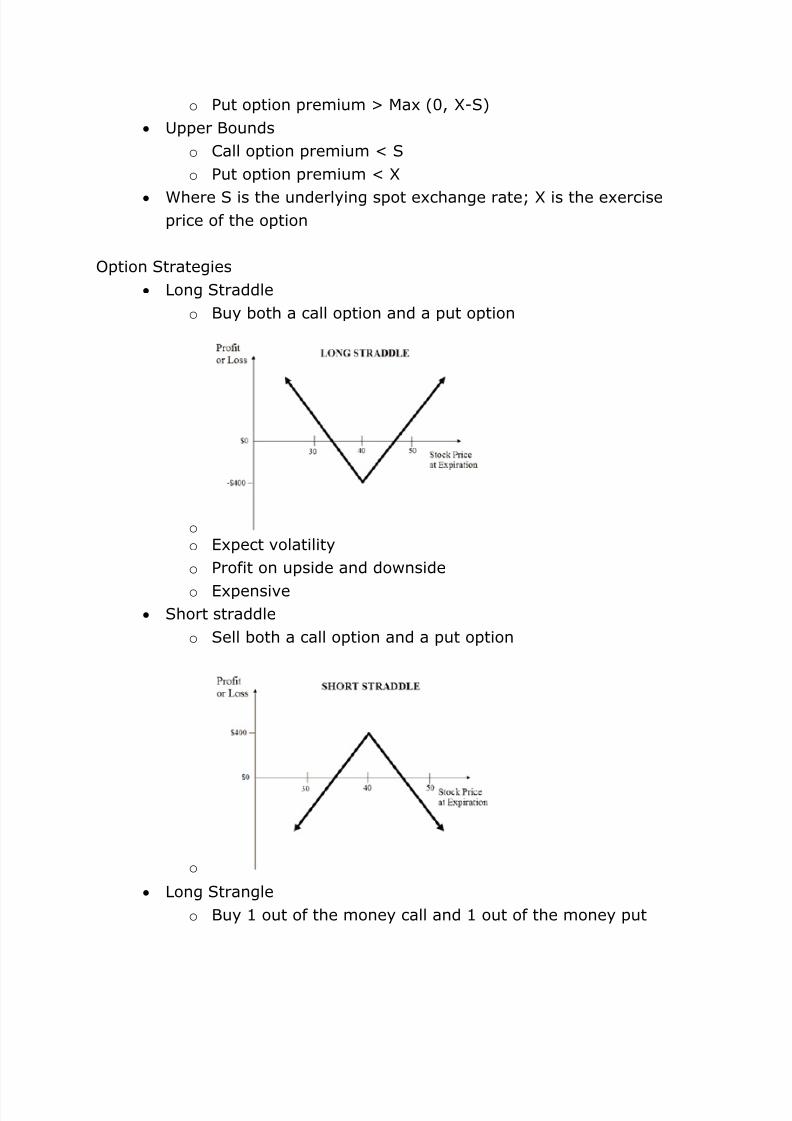

Lower Bounds

o Call option premium > Max (0, S-X)

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 18/22

o Put option premium > Max (0, X-S)

Upper Bounds

o Call option premium < S

o Put option premium < X

Where S is the underlying spot exchange rate; X is the exerciseprice of the option

Option Strategies

Long Straddle

o Buy both a call option and a put option

o o Expect volatility

o Profit on upside and downside

o Expensive Short straddle

o Sell both a call option and a put option

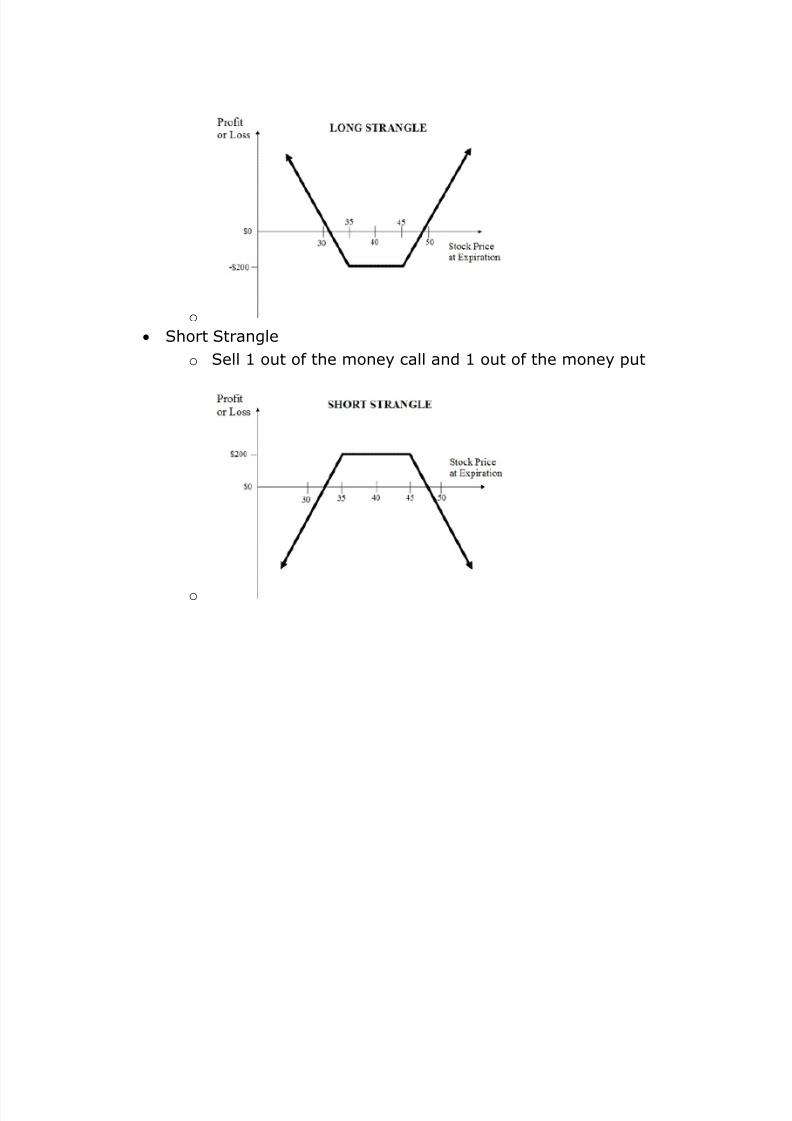

o Long Strangle

o Buy 1 out of the money call and 1 out of the money put

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 19/22

o Short Strangle

o Sell 1 out of the money call and 1 out of the money put

o

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 20/22

Swaps 8/30/2012 4:57:00 PM

Exchange cash flows at periodic intervals

Interest rate swap

Decide you want to switch between fixed or floating rate without

refinancing

Currency swap Switch currencies based on specific exchange rates an fixed or

floating interest rates

Example

US firm wants to finance 1000000 euro plant in UK

British firm wants to borrow $1.6 million

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 21/22

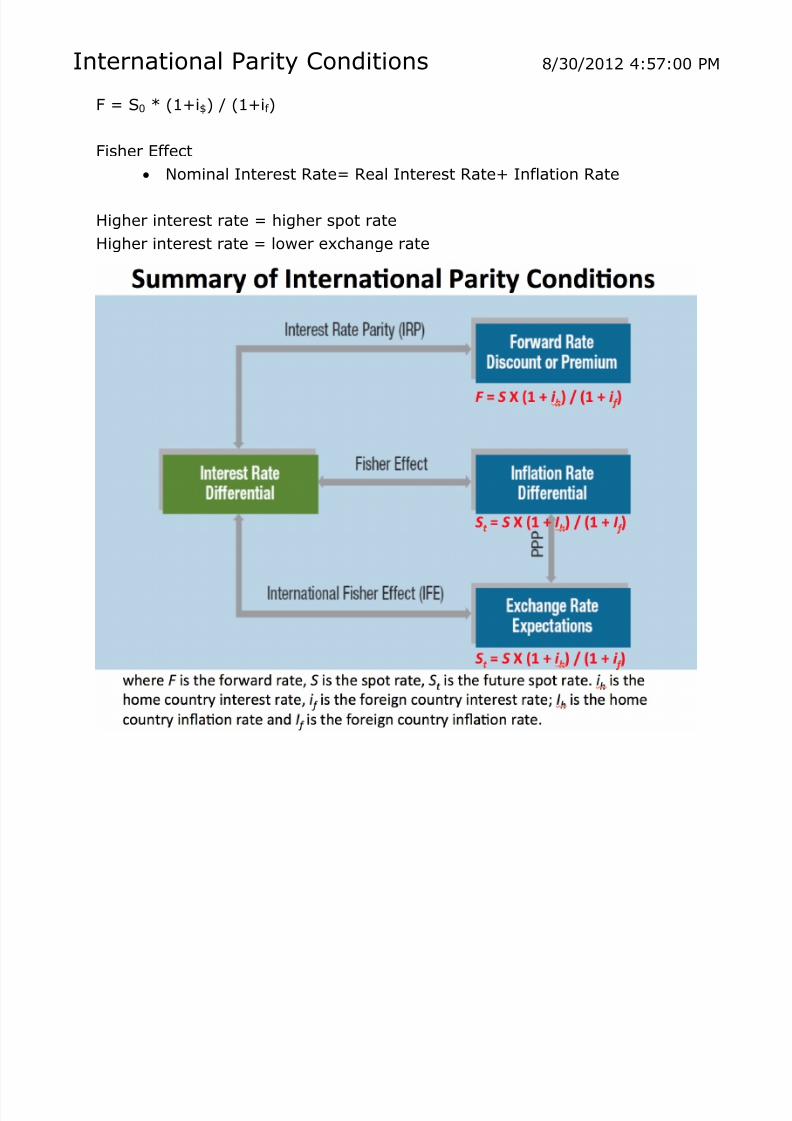

International Parity Conditions 8/30/2012 4:57:00 PM

F = S0 * (1+i$) / (1+if )

Fisher Effect

Nominal Interest Rate= Real Interest Rate+ Inflation Rate

Higher interest rate = higher spot rate

Higher interest rate = lower exchange rate

7/29/2019 BUSI 163 Notes

http://slidepdf.com/reader/full/busi-163-notes 22/22

Risk Exposure 8/30/2012 4:57:00 PM

USD FX Rate Up

Company A Net Income Down 2%

Company B Net Income Down 2%

o More exposed to risk

3 Types of Exposure in FX Market

Transactional Exposure

o Hedge with Contracts

o Amount and Timing

o Receivable (Fear depreciation of foreign currency)

Buy put option to lock rate at fixed price at future time

Sell futures of foreign currency

Sell forward of foreign currency

o Payable (Fear appreciation of foreign currency)

Buy call option to lock rate at fixed price at future time

Buy futures of foreign currency

Buy forward of foreign currency

o Translation Exposure

FX Rates affect numbers on accounting statements