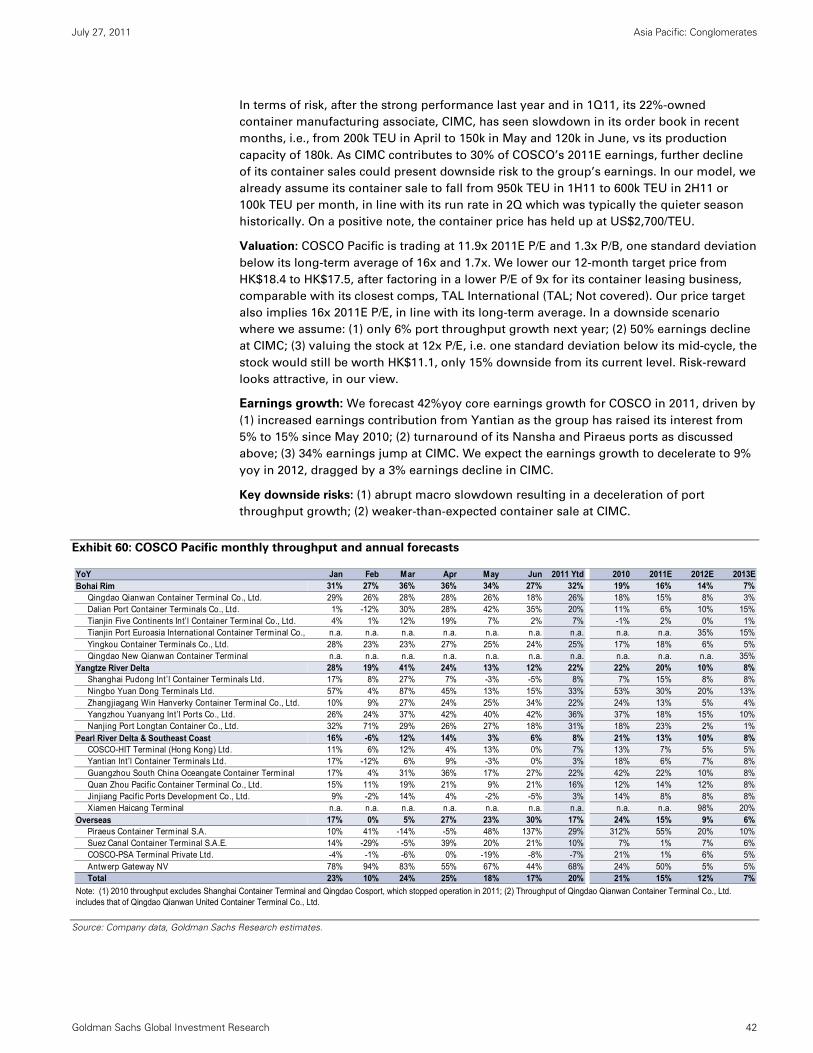

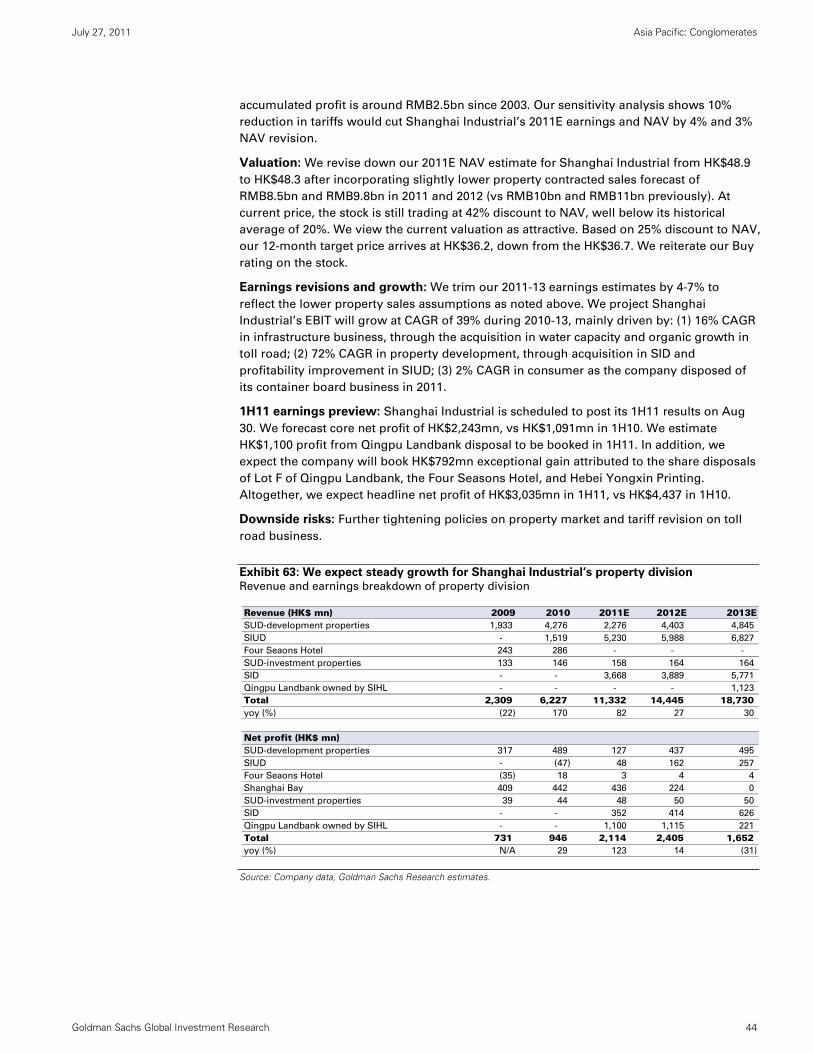

asia pacific: conglomerates - · pdf filestock picks by themes, stress test on valuation and...

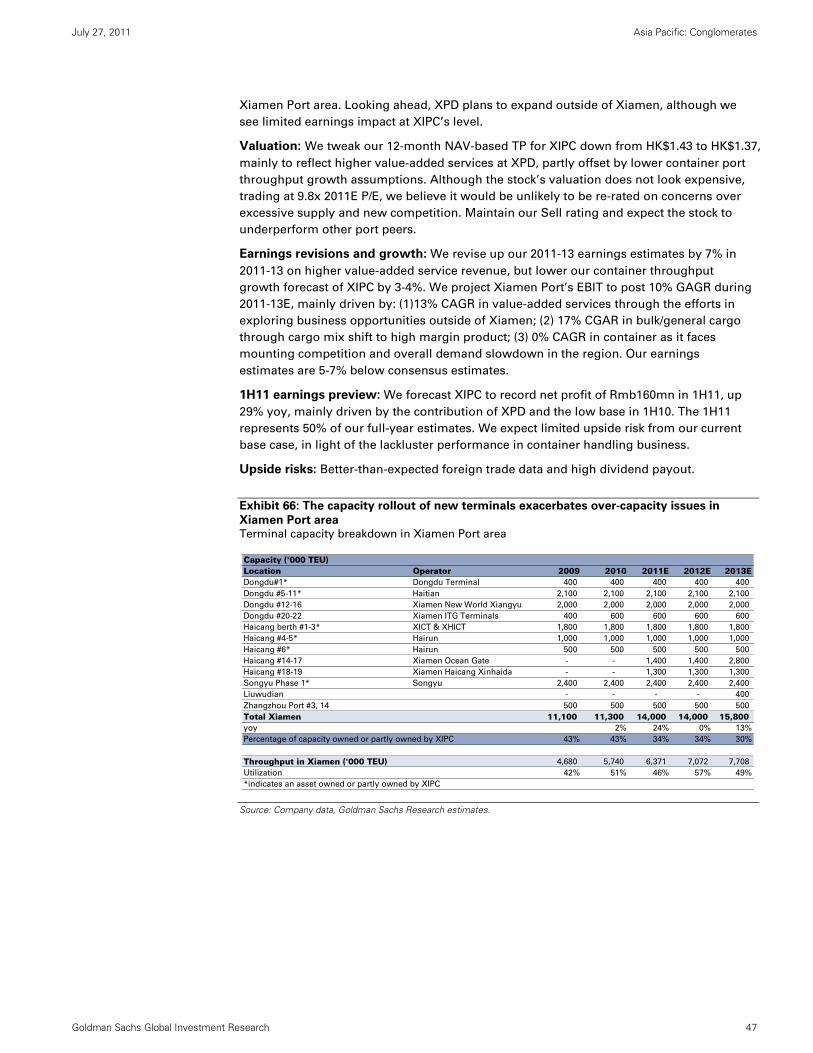

TRANSCRIPT

July 27, 2011

Asia Pacific: Conglomerates

Equity Research

Stock picks by themes, stress test on valuation and results preview

Top ideas: Buy Hutch, Wharf and COSCO Pacific; Sell Jardine

Market sell-down on macro concerns has given back much of the price gain

in 1Q, with HK/China conglomerates trading sideways or down ytd. While

their valuations look attractive, our stress test suggests an average

downside of 18% if macro deteriorates and the stocks de-rate to one-

standard deviation below mid-cycle valuation. This said, risk-reward looks

favorable for selective stocks, e.g., COSCO, HPHT and Shanghai Industrial,

in our view. We also see buying opportunities for those that benefit from

sector themes and offer potential surprises in upcoming results.

Investment themes and rating changes

(1) Prefer exposure to Bohai region, and container over bulk ports - Given

the fragility of macro recovery and retailers’ cautious stance as reflected by

their lean inventory levels, shorter restocking cycles would translate to

more volatile trading data in coming months, in our view. We prefer ports

in Bohai Rim which are more leveraged to fast-growing domestic and intra-

Asia trades. We also prefer container over bulk ports for their better

demand and supply outlook. We downgrade Dalian Port from Buy to

Neutral, as we believe slower-than-expected oil throughput growth ytd

could present downside risk to its earnings. We recommend investors

switch to COSCO.

(2) HK rental upcycle to continue and appreciation in capital value – We

expect the cap rate to remain low, as (1) its spread over long-term rates

has been 2-3%, inline with historical avg; (2) our ECS team believes the US

will not raise the Fed rate until at least end-2013. In the meantime, hiring

expectations, though moderate slightly, remain strong. Coupled with a lack

of new supply, we expect HK’s rental upcycle to continue and forecast 25%

office and 10-15% retail rental growth in 2011. We downgrade MTRC from

Buy to Neutral on concerns over policy risk, and upgrade Wharf from

Neutral to Buy, as the stock has underperformed MSCI HK Index by 4%ytd

despite robust rental growth. We expect market to react positively if Wharf

confirms its 2011 property sale target at its interim results in August, and

see significant upside risk to consensus estimates in 2012-13.

(3) Acquisition opportunities for cash-rich conglomerates – Less revenue

from land sales as developers turn more cautious on their replenishment

plans would prompt local government to seek other ways to reduce their

debt burden, which may create acquisition opportunities for cash-rich

companies, e.g. Shanghai Industrial or CRE.

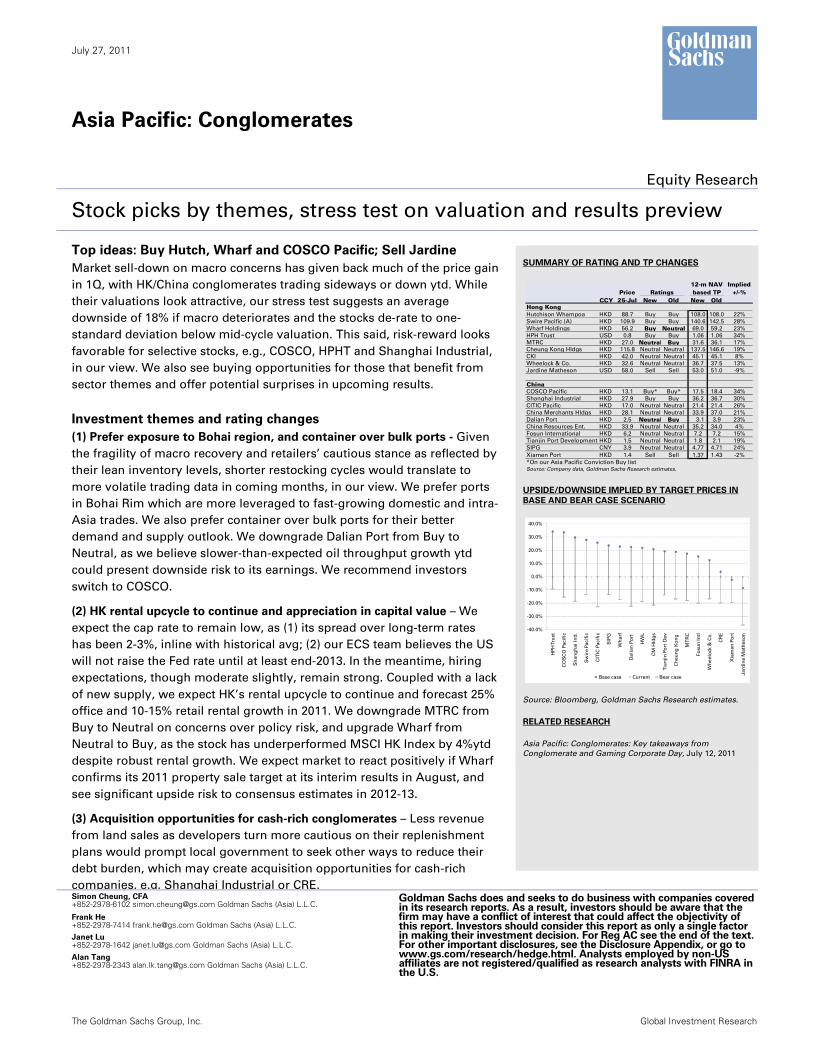

SUMMARY OF RATING AND TP CHANGES

UPSIDE/DOWNSIDE IMPLIED BY TARGET PRICES IN

BASE AND BEAR CASE SCENARIO

Source: Bloomberg, Goldman Sachs Research estimates.

RELATED RESEARCH

Asia Pacific: Conglomerates: Key takeaways from

Conglomerate and Gaming Corporate Day, July 12, 2011

Simon Cheung, CFA +852-2978-6102 [email protected] Goldman Sachs (Asia) L.L.C.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC see the end of the text. For other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

Frank He +852-2978-7414 [email protected] Goldman Sachs (Asia) L.L.C. Janet Lu +852-2978-1642 [email protected] Goldman Sachs (Asia) L.L.C. Alan Tang +852-2978-2343 [email protected] Goldman Sachs (Asia) L.L.C.

The Goldman Sachs Group, Inc. Global Investment Research

ImpliedPrice +/-%

CCY 25-Jul New Old New OldHong KongHutchison Whampoa HKD 88.7 Buy Buy 108.0 108.0 22%

Swire Pacific (A) HKD 109.9 Buy Buy 140.6 142.5 28%

Wharf Holdings HKD 56.2 Buy Neutral 69.0 59.2 23%

HPH Trust USD 0.8 Buy Buy 1.06 1.06 34%

MTRC HKD 27.0 Neutral Buy 31.6 36.1 17%

Cheung Kong Hldgs HKD 115.8 Neutral Neutral 137.5 146.6 19%

CKI HKD 42.0 Neutral Neutral 45.1 45.1 8%

Wheelock & Co. HKD 32.6 Neutral Neutral 36.7 37.5 13%

Jardine Matheson USD 58.0 Sell Sell 53.0 51.0 -9%

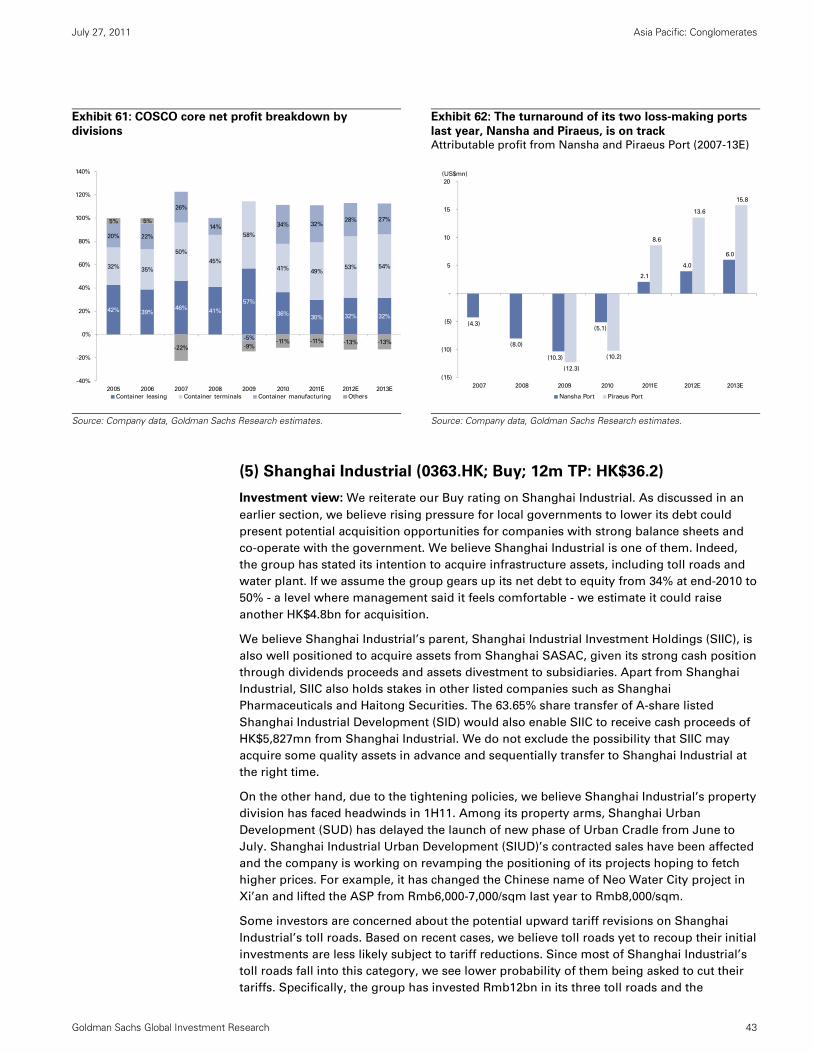

ChinaCOSCO Pacific HKD 13.1 Buy* Buy* 17.5 18.4 34%

Shanghai Industrial HKD 27.9 Buy Buy 36.2 36.7 30%

CITIC Pacific HKD 17.0 Neutral Neutral 21.4 21.4 26%

China Merchants Hldgs HKD 28.1 Neutral Neutral 33.9 37.0 21%

Dalian Port HKD 2.5 Neutral Buy 3.1 3.9 23%

China Resources Ent. HKD 33.9 Neutral Neutral 35.2 34.0 4%

Fosun International HKD 6.2 Neutral Neutral 7.2 7.2 15%

Tianjin Port Development HKD 1.5 Neutral Neutral 1.8 2.1 19%

SIPG CNY 3.9 Neutral Neutral 4.77 4.71 24%

Xiamen Port HKD 1.4 Sell Sell 1.37 1.43 -2%

*On our Asia Pacific Conviction Buy listSource: Company data, Goldman Sachs Research estimates.

12-m NAVRatings based TP

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

HP

H T

rust

CO

SC

O P

acif

ic

Sh

an

gh

ai

Ind

.

Sw

ire P

acif

ic

CIT

IC P

acif

ic

SIP

G

Wh

arf

Dali

an

Po

rt

HW

L

CM

Hld

gs

Tia

nji

n P

ort

Dev

Ch

eu

ng

Ko

ng

MT

RC

Fo

su

n In

tl

Wh

eelo

ck &

Co

.

CR

E

Xia

men

Po

rt

Ja

rdin

e M

ath

eso

n

Base case Current Bear case

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 2

Table of Contents

Summary of our latest sector view and rating changes 3

Sector themes, stress-test our assumptions and earnings preview 3

(1) Prefer container over bulk ports, and exposure to Bohai Rim 7

(2) Capital value appreciation in HK rental properties 14

(3) Acquisition opportunities for cash-rich conglomerates 20

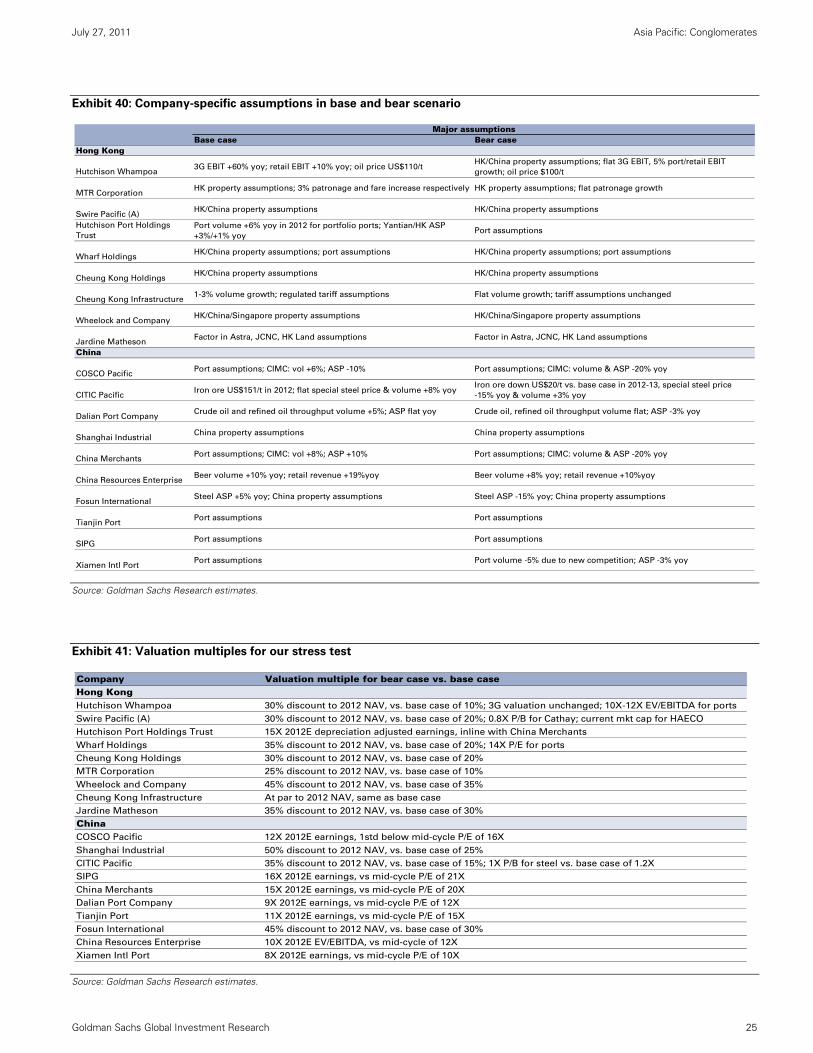

Downside scenario - stress-test our key assumptions 23

Conclusion: earnings impact and valuation implication 26

Potential surprises and trading ideas around the results season 29

Stock implications and investment views 32

Stocks with rating changes 32

Other Buy rated stocks 37

Sell-rated stocks 45

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 3

Summary of our latest sector view and rating changes

Sector themes, stress-test our assumptions and earnings preview

Similar to what we had experienced last year, the Hong Kong and Chinese conglomerate

stocks staged a sharp rally along with the broader market in the early part of this year on

expectation of a sustainable macro recovery, especially for those more leveraged to the

export-driven sectors (e.g., port, commodity). Given a firmer US outlook and greater

inflation/policy tightening concerns in Asia, our strategist also recommended DM

(developed market) over EM (emerging market) trades. But toward the end of 1Q, weaker

macro data in the US and debt crisis concern in Europe started to weigh on market

sentiment. Coupled with the higher-than-expected inflation data released from China and

other emerging economies, these had triggered a sell-down across the Hong Kong and

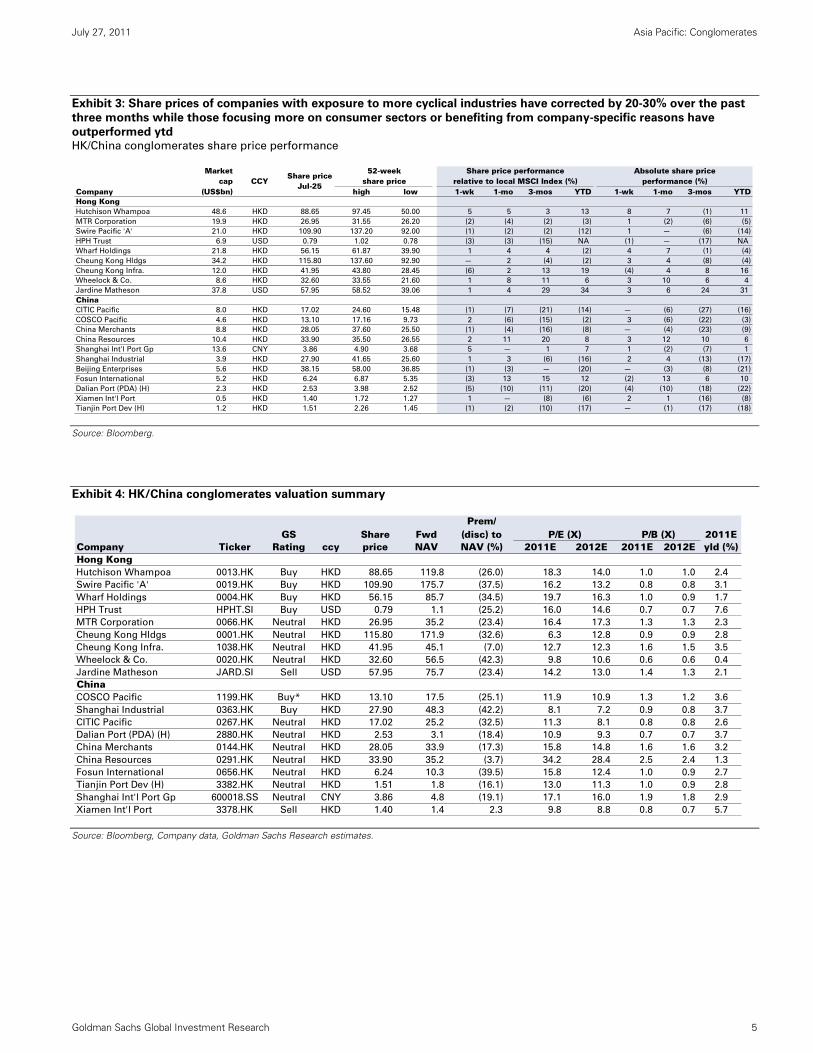

China markets in recent weeks. As shown in Exhibit 3, share prices of the HK/China

conglomerates with exposure to the more cyclical industries, such as CITIC Pacific and

China Merchants, have corrected by 20-30% over the past three months. On the other hand,

those that focus more on consumer sectors (i.e., CRE, Jardine Matheson) or benefit from

company-specific reasons (i.e., Hutch for HPHT IPO, CKI for EDF acquisition, Fosun for the

privatization of Forte Land and proposed listing of Hainan Mining) have outperformed ytd.

Looking into 2H2011, as most of the stocks have traded either sideways or fallen ytd, we

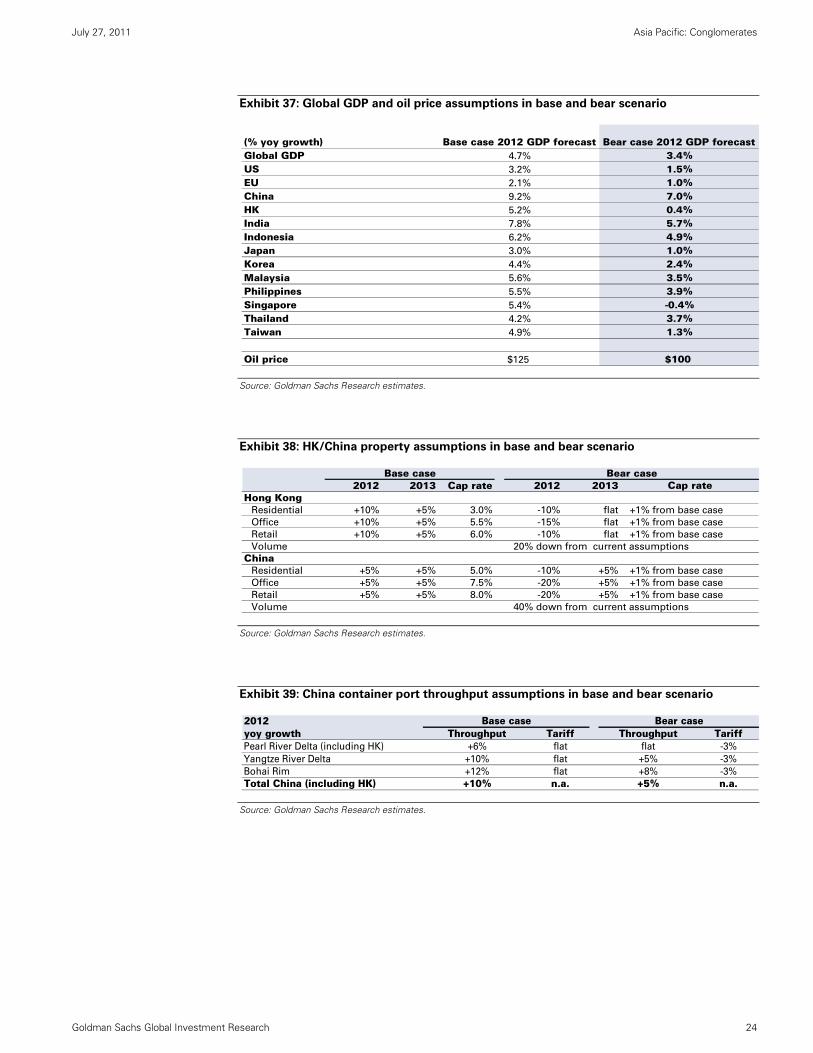

generally find the sector valuation attractive. In a bear case where we stress-test our key

assumptions based on a downside scenario by our ECS team (i.e., 3.4% global, 1.5% US,

1.0% Europe, 7% China and 0.4% Hong Kong GDP growth forecasts in 2012) and value the

stocks at one-standard deviation below their mid-cycle valuation, there could be 9%-37% or

an average of 18% potential downside from the share prices of stocks in our coverage

universe. That said, risk-reward looks favorable for selective stocks, such as COSCO Pacific

(on Conviction List), HPHT and Shanghai Industrial, both rated Buy. We also see

investment opportunities for those which benefit from the several sector themes we

identify below:

Prefer port operators with exposure to the Bohai Rim region, and container over bulk

ports.

Further capital value appreciation of Hong Kong rental properties on favorable

demand-supply outlook and our expectation that the cap rate is unlikely to widen for a

period of time.

Acquisition opportunities for cash-rich conglomerates with strong local relationship

with local governments, given mounting pressure for them to lower their debt burden.

We upgrade Wharf from Neutral to Buy, and downgrade MTRC from Buy to Neutral. After

trading sideways ytd in spite of the strong fundamentals of Hong Kong’s retail rental

market, Wharf shares trade at a 35% discount to NAV, below the mid-cycle valuation. We

see a buying opportunity at this level. If the group continues to execute well on its China

investment, we expect a step-up in its property sale profit and see significant upside risk to

consensus estimates in 2012-13E. Confirmation of its full-year property sale target by

management is likely to be taken positively by the market.

For MTRC, several developments in recent months led us to turn more cautious on its

business outlook, i.e., a substantial capex increase which raises concerns about further cost

overruns and the return of its new rail projects. MTRC agreed to offer an additional

HK$100mn fare promotion, wiping off close to 40% of the revenue increase from previous

fare hikes, in response to Hong Kong locals’ protest against the fare increase. With HK CPI

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 4

rising to 5.6% in June, the magnitude of the fare hike will likely be even higher. MTRC may

face more of a challenge then. In addition, there may be a risk that the existing Fare

Adjustment Mechanism (FAM) formula may be revised when it is reviewed in 1H 2012.

We also downgrade Dalian Port from Buy to Neutral and prefer COSCO Pacific. We see

downside risk on consensus earnings estimates on weaker-than-expected crude oil

throughput growth ytd and potential dilution after the completion of the China-Russia

pipeline. The recent fire accident at PetroChina’s Dalian Petrochemical plan may also delay

the launch of PetroChina’s 4.2mn oil storage facility.

Our top buys are COSCO Pacific, Hutch and Wharf. Our top Sell is Jardine Matheson.

Exhibit 1: Summary of rating, target price and net asset value changes

Source: Company data, Goldman Sachs Research estimates.

Exhibit 2: Summary of core net profit estimate revisions

Source: Company data, Goldman Sachs Research estimates.

Price Implied

Ticker Ccy 25-Jul New Old New Old Chg New Old New Old % +/-% Comments

Hong KongHutchison Whampoa 0013.HK HKD 88.7 Buy Buy 119.8 120.0 0% -10% -10% 108.0 108.0 0% 22% NAV-basedSwire Pacific (A) 0019.HK HKD 109.9 Buy Buy 175.7 178.1 -1% -20% -20% 140.6 142.5 -1% 28% NAV-basedWharf Holdings 0004.HK HKD 56.2 Buy Neutral 85.7 78.9 9% -20% -25% 69.0 59.2 17% 23% NAV-based Narrower discount on solid China property executionHPH Trust HPHT.SI USD 0.8 Buy Buy 1.1 1.1 0% 0% 0% 1.06 1.06 0% 34% DCF-based

MTRC 0066.HK HKD 27.0 Neutral Buy 35.2 36.1 -3% -10% 0% 31.6 36.1 -12% 17% NAV-basedWider discount on concern over the new projects' return and its ability to raise fare

Cheung Kong Hldgs 0001.HK HKD 115.8 Neutral Neutral 171.9 172.5 0% -20% -15% 137.5 146.6 -6% 19% NAV-basedWider discount on de-rating of property developers and HK property policy risks

CKI 1038.HK HKD 42.0 Neutral Neutral 45.1 45.1 0% 0% 0% 45.1 45.1 0% 8% NAV-basedWheelock & Co. 0020.HK HKD 32.6 Neutral Neutral 56.5 53.6 5% -35% -30% 36.7 37.5 -2% 13% NAV-based Wider discount on HK/Singapore property policy risksJardine Matheson JARD.SI USD 58.0 Sell Sell 75.7 72.9 4% -30% -30% 53.0 51.0 4% -9% NAV-based

ChinaCOSCO Pacific 1199.HK HKD 13.1 Buy* Buy* 17.5 18.4 -5% 0% 0% 17.5 18.4 -5% 34% NAV-basedShanghai Industrial 0363.HK HKD 27.9 Buy Buy 48.3 48.9 -1% -25% -25% 36.2 36.7 -1% 30% NAV-basedCITIC Pacific 0267.HK HKD 17.0 Neutral Neutral 25.2 25.2 0% -15% -15% 21.4 21.4 0% 26% NAV-basedChina Merchants Hldgs 0144.HK HKD 28.1 Neutral Neutral 33.9 37.0 -8% 0% 0% 33.9 37.0 -8% 21% NAV-basedDalian Port 2880.HK HKD 2.5 Neutral Buy 3.1 3.9 -21% 0% 0% 3.1 3.9 -21% 23% DCF-based SOTPChina Resources Ent. 0291.HK HKD 33.9 Neutral Neutral 35.2 34.0 4% 0% 0% 35.2 34.0 4% 4% NAV-basedFosun International 0656.HK HKD 6.2 Neutral Neutral 10.3 10.4 -1% -30% -30% 7.2 7.2 0% 15% NAV-basedTianjin Port Development 3382.HK HKD 1.5 Neutral Neutral 1.8 2.1 -15% 0% 0% 1.8 2.1 -15% 19% DCF-based SOTPSIPG 600018.SS CNY 3.9 Neutral Neutral 4.8 4.7 1% 0% 0% 4.77 4.71 1% 24% DCF-based SOTPXiamen Port 3378.HK HKD 1.4 Sell Sell 1.4 1.4 -4% 0% 0% 1.37 1.43 -4% -2% DCF-based SOTP* On Conviction List.

Target price2011E NAV / shareRating Target disc. Valuation methodology

Ticker Ccy New Old Chg New Old Chg New Old ChgHong KongHutchison Whampoa 0013.HK HKD 20,694 23,086 -10% 27,049 29,906 -10% 31,489 33,137 -5% Factor in deferral of proeprty profit booking and higher earnings at HuskSwire Pacific (A) 0019.HK HKD 10,225 10,941 -7% 12,536 13,325 -6% 13,592 14,083 -3% Factor in lastest GS estimates of Cathay Pacific and HAECOWharf Holdings 0004.HK HKD 8,493 8,482 0% 10,456 10,293 2% 13,198 10,659 24% Factor in higher HK retail rental growth & China property sales assumptHPH Trust HPHT.SI HKD 2,314 2,314 0% 2,514 2,514 0% 2,834 2,834 0% n.a.

MTRC 0066.HK HKD 9,599 9,818 -2% 9,382 10,795 -13% 11,127 11,795 -6%Factor in lower margin for its rail business and deferral of profit booking at Lohas Park Phase 3 from 2012 to 2013

Cheung Kong Hldgs 0001.HK HKD 42,393 39,255 8% 21,027 28,854 -27% 27,582 31,863 -13% Factor in Hutch's latest estimates and latest proeprty scheduleCKI 1038.HK HKD 7,458 7,458 0% 7,695 7,695 0% 7,957 7,957 0% n.a.Wheelock & Co. 0020.HK HKD 6,726 6,588 2% 6,250 6,060 3% 9,181 6,764 36% Factor in Wharf's latest estimatesJardine Matheson JARD.SI USD 1,470 1,406 5% 1,598 1,538 4% 1,859 1,751 6% Factor in latest GS estimates for HK Land, JCNC and Astra

ChinaCOSCO Pacific 1199.HK USD 385 385 0% 417 417 0% 469 469 0% n.a.Shanghai Industrial 0363.HK HKD 3,727 2,774 34% 4,162 3,288 27% 3,700 3,862 -4% Reclassify the Qingpu landbank sales as recurrent earningsCITIC Pacific 0267.HK HKD 5,493 5,493 0% 7,662 7,662 0% 11,561 11,561 0% n.a.China Merchants Hldgs 0144.HK HKD 4,373 4,422 -1% 4,661 4,827 -3% 5,130 5,476 -6% Factor in lower container throughput growth in PRD Dalian Port 2880.HK CNY 846 941 -10% 960 1,096 -12% 1,068 1,227 -13% Slower throughput growth in oil handling divisionChina Resources Ent. 0291.HK HKD 2,379 2,387 0% 2,861 2,822 1% 3,487 3,404 2% Factor in higher sales growth for retail business in 2012-13Fosun International 0656.HK CNY 2,101 2,116 -1% 2,675 2,706 -1% 3,332 3,360 -1% Factor in higher interest expensesTianjin Port Development 3382.HK HKD 718 691 4% 823 793 4% 904 875 3% Factor in higher coal and container throughput growth assumptionsSIPG 600018.SS CNY 5,032 5,094 -1% 5,486 5,695 -4% 6,169 6,567 -6% Factor in lower container throughput and tariff forecastXiamen Port 3378.HK CNY 320 298 7% 345 321 8% 367 343 7% Lower container throughput and tariff forecast

**Core net profit excluding exceptional items except for Cheung Kong

CommentRecurring net profits (mn)**

2011E 2012E 2013E

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 5

Exhibit 3: Share prices of companies with exposure to more cyclical industries have corrected by 20-30% over the past

three months while those focusing more on consumer sectors or benefiting from company-specific reasons have

outperformed ytd HK/China conglomerates share price performance

Source: Bloomberg.

Exhibit 4: HK/China conglomerates valuation summary

Source: Bloomberg, Company data, Goldman Sachs Research estimates.

Marketcap

Company (US$bn) high low 1-wk 1-mo 3-mos YTD 1-wk 1-mo 3-mos YTDHong KongHutchison Whampoa 48.6 HKD 88.65 97.45 50.00 5 5 3 13 8 7 (1) 11

MTR Corporation 19.9 HKD 26.95 31.55 26.20 (2) (4) (2) (3) 1 (2) (6) (5)

Swire Pacific 'A' 21.0 HKD 109.90 137.20 92.00 (1) (2) (2) (12) 1 — (6) (14)

HPH Trust 6.9 USD 0.79 1.02 0.78 (3) (3) (15) NA (1) — (17) NA

Wharf Holdings 21.8 HKD 56.15 61.87 39.90 1 4 4 (2) 4 7 (1) (4)

Cheung Kong Hldgs 34.2 HKD 115.80 137.60 92.90 — 2 (4) (2) 3 4 (8) (4)

Cheung Kong Infra. 12.0 HKD 41.95 43.80 28.45 (6) 2 13 19 (4) 4 8 16

Wheelock & Co. 8.6 HKD 32.60 33.55 21.60 1 8 11 6 3 10 6 4

Jardine Matheson 37.8 USD 57.95 58.52 39.06 1 4 29 34 3 6 24 31

ChinaCITIC Pacific 8.0 HKD 17.02 24.60 15.48 (1) (7) (21) (14) — (6) (27) (16)

COSCO Pacific 4.6 HKD 13.10 17.16 9.73 2 (6) (15) (2) 3 (6) (22) (3)

China Merchants 8.8 HKD 28.05 37.60 25.50 (1) (4) (16) (8) — (4) (23) (9)

China Resources 10.4 HKD 33.90 35.50 26.55 2 11 20 8 3 12 10 6

Shanghai Int'l Port Gp 13.6 CNY 3.86 4.90 3.68 5 — 1 7 1 (2) (7) 1

Shanghai Industrial 3.9 HKD 27.90 41.65 25.60 1 3 (6) (16) 2 4 (13) (17)

Beijing Enterprises 5.6 HKD 38.15 58.00 36.85 (1) (3) — (20) — (3) (8) (21)

Fosun International 5.2 HKD 6.24 6.87 5.35 (3) 13 15 12 (2) 13 6 10

Dalian Port (PDA) (H) 2.3 HKD 2.53 3.98 2.52 (5) (10) (11) (20) (4) (10) (18) (22)

Xiamen Int'l Port 0.5 HKD 1.40 1.72 1.27 1 — (8) (6) 2 1 (16) (8)

Tianjin Port Dev (H) 1.2 HKD 1.51 2.26 1.45 (1) (2) (10) (17) — (1) (17) (18)

CCYShare price

Jul-25

Absolute share priceperformance (%)

52-weekshare price

Share price performancerelative to local MSCI Index (%)

Prem/GS Share Fwd (disc) to 2011E

Company Ticker Rating ccy price NAV NAV (%) 2011E 2012E 2011E 2012E yld (%)Hong KongHutchison Whampoa 0013.HK Buy HKD 88.65 119.8 (26.0) 18.3 14.0 1.0 1.0 2.4

Swire Pacific 'A' 0019.HK Buy HKD 109.90 175.7 (37.5) 16.2 13.2 0.8 0.8 3.1

Wharf Holdings 0004.HK Buy HKD 56.15 85.7 (34.5) 19.7 16.3 1.0 0.9 1.7

HPH Trust HPHT.SI Buy USD 0.79 1.1 (25.2) 16.0 14.6 0.7 0.7 7.6

MTR Corporation 0066.HK Neutral HKD 26.95 35.2 (23.4) 16.4 17.3 1.3 1.3 2.3

Cheung Kong Hldgs 0001.HK Neutral HKD 115.80 171.9 (32.6) 6.3 12.8 0.9 0.9 2.8

Cheung Kong Infra. 1038.HK Neutral HKD 41.95 45.1 (7.0) 12.7 12.3 1.6 1.5 3.5

Wheelock & Co. 0020.HK Neutral HKD 32.60 56.5 (42.3) 9.8 10.6 0.6 0.6 0.4

Jardine Matheson JARD.SI Sell USD 57.95 75.7 (23.4) 14.2 13.0 1.4 1.3 2.1

ChinaCOSCO Pacific 1199.HK Buy* HKD 13.10 17.5 (25.1) 11.9 10.9 1.3 1.2 3.6

Shanghai Industrial 0363.HK Buy HKD 27.90 48.3 (42.2) 8.1 7.2 0.9 0.8 3.7

CITIC Pacific 0267.HK Neutral HKD 17.02 25.2 (32.5) 11.3 8.1 0.8 0.8 2.6

Dalian Port (PDA) (H) 2880.HK Neutral HKD 2.53 3.1 (18.4) 10.9 9.3 0.7 0.7 3.7

China Merchants 0144.HK Neutral HKD 28.05 33.9 (17.3) 15.8 14.8 1.6 1.6 3.2

China Resources 0291.HK Neutral HKD 33.90 35.2 (3.7) 34.2 28.4 2.5 2.4 1.3

Fosun International 0656.HK Neutral HKD 6.24 10.3 (39.5) 15.8 12.4 1.0 0.9 2.7

Tianjin Port Dev (H) 3382.HK Neutral HKD 1.51 1.8 (16.1) 13.0 11.3 1.0 0.9 2.8

Shanghai Int'l Port Gp 600018.SS Neutral CNY 3.86 4.8 (19.1) 17.1 16.0 1.9 1.8 2.9

Xiamen Int'l Port 3378.HK Sell HKD 1.40 1.4 2.3 9.8 8.8 0.8 0.7 5.7

P/E (X) P/B (X)

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 6

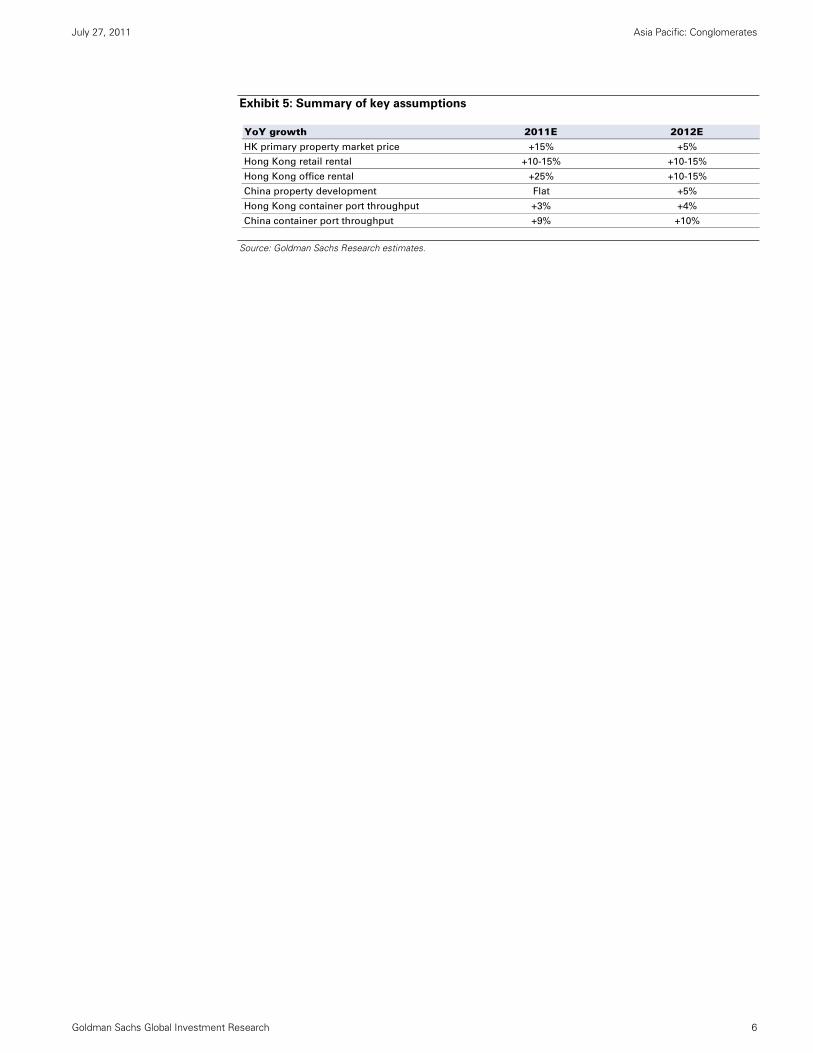

Exhibit 5: Summary of key assumptions

Source: Goldman Sachs Research estimates.

YoY growth 2011E 2012EHK primary property market price +15% +5%

Hong Kong retail rental +10-15% +10-15%

Hong Kong office rental +25% +10-15%

China property development Flat +5%

Hong Kong container port throughput +3% +4%

China container port throughput +9% +10%

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 7

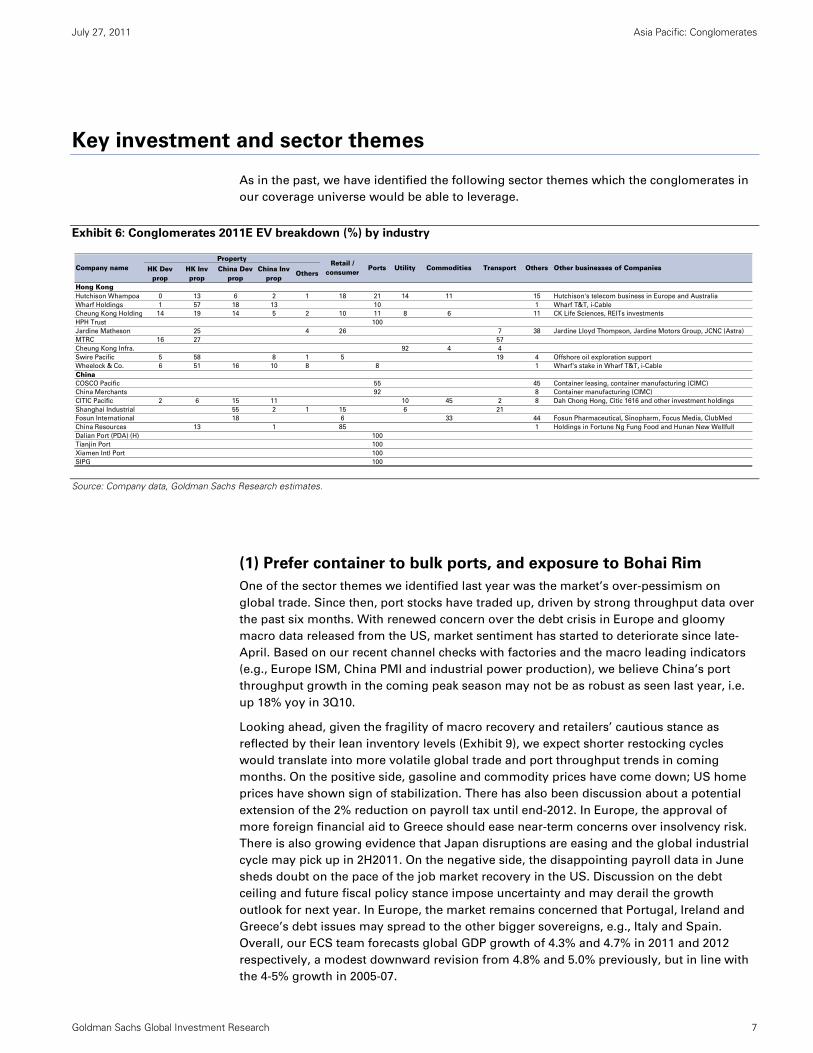

Key investment and sector themes

As in the past, we have identified the following sector themes which the conglomerates in

our coverage universe would be able to leverage.

Exhibit 6: Conglomerates 2011E EV breakdown (%) by industry

Source: Company data, Goldman Sachs Research estimates.

(1) Prefer container to bulk ports, and exposure to Bohai Rim

One of the sector themes we identified last year was the market’s over-pessimism on

global trade. Since then, port stocks have traded up, driven by strong throughput data over

the past six months. With renewed concern over the debt crisis in Europe and gloomy

macro data released from the US, market sentiment has started to deteriorate since late-

April. Based on our recent channel checks with factories and the macro leading indicators

(e.g., Europe ISM, China PMI and industrial power production), we believe China’s port

throughput growth in the coming peak season may not be as robust as seen last year, i.e.

up 18% yoy in 3Q10.

Looking ahead, given the fragility of macro recovery and retailers’ cautious stance as

reflected by their lean inventory levels (Exhibit 9), we expect shorter restocking cycles

would translate into more volatile global trade and port throughput trends in coming

months. On the positive side, gasoline and commodity prices have come down; US home

prices have shown sign of stabilization. There has also been discussion about a potential

extension of the 2% reduction on payroll tax until end-2012. In Europe, the approval of

more foreign financial aid to Greece should ease near-term concerns over insolvency risk.

There is also growing evidence that Japan disruptions are easing and the global industrial

cycle may pick up in 2H2011. On the negative side, the disappointing payroll data in June

sheds doubt on the pace of the job market recovery in the US. Discussion on the debt

ceiling and future fiscal policy stance impose uncertainty and may derail the growth

outlook for next year. In Europe, the market remains concerned that Portugal, Ireland and

Greece’s debt issues may spread to the other bigger sovereigns, e.g., Italy and Spain.

Overall, our ECS team forecasts global GDP growth of 4.3% and 4.7% in 2011 and 2012

respectively, a modest downward revision from 4.8% and 5.0% previously, but in line with

the 4-5% growth in 2005-07.

HK Dev prop

HK Inv prop

China Dev prop

China Inv prop

Others

Hong KongHutchison Whampoa 0 13 6 2 1 18 21 14 11 15 Hutchison's telecom business in Europe and Australia

Wharf Holdings 1 57 18 13 10 1 Wharf T&T, i-Cable

Cheung Kong Holding 14 19 14 5 2 10 11 8 6 11 CK Life Sciences, REITs investments

HPH Trust 100

Jardine Matheson 25 4 26 7 38 Jardine Lloyd Thompson, Jardine Motors Group, JCNC (Astra)

MTRC 16 27 57

Cheung Kong Infra. 92 4 4

Swire Pacific 5 58 8 1 5 19 4 Offshore oil exploration support

Wheelock & Co. 6 51 16 10 8 8 1 Wharf's stake in Wharf T&T, i-Cable

ChinaCOSCO Pacific 55 45 Container leasing, container manufacturing (CIMC)

China Merchants 92 8 Container manufacturing (CIMC)

CITIC Pacific 2 6 15 11 10 45 2 8 Dah Chong Hong, Citic 1616 and other investment holdings

Shanghai Industrial 55 2 1 15 6 21

Fosun International 18 6 33 44 Fosun Pharmaceutical, Sinopharm, Focus Media, ClubMed

China Resources 13 1 85 1 Holdings in Fortune Ng Fung Food and Hunan New Wellfull

Dalian Port (PDA) (H) 100

Tianjin Port 100

Xiamen Intl Port 100

SIPG 100

Transport Others Other businesses of CompaniesCompany nameProperty

Retail / consumer

Ports Utility Commodities

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 8

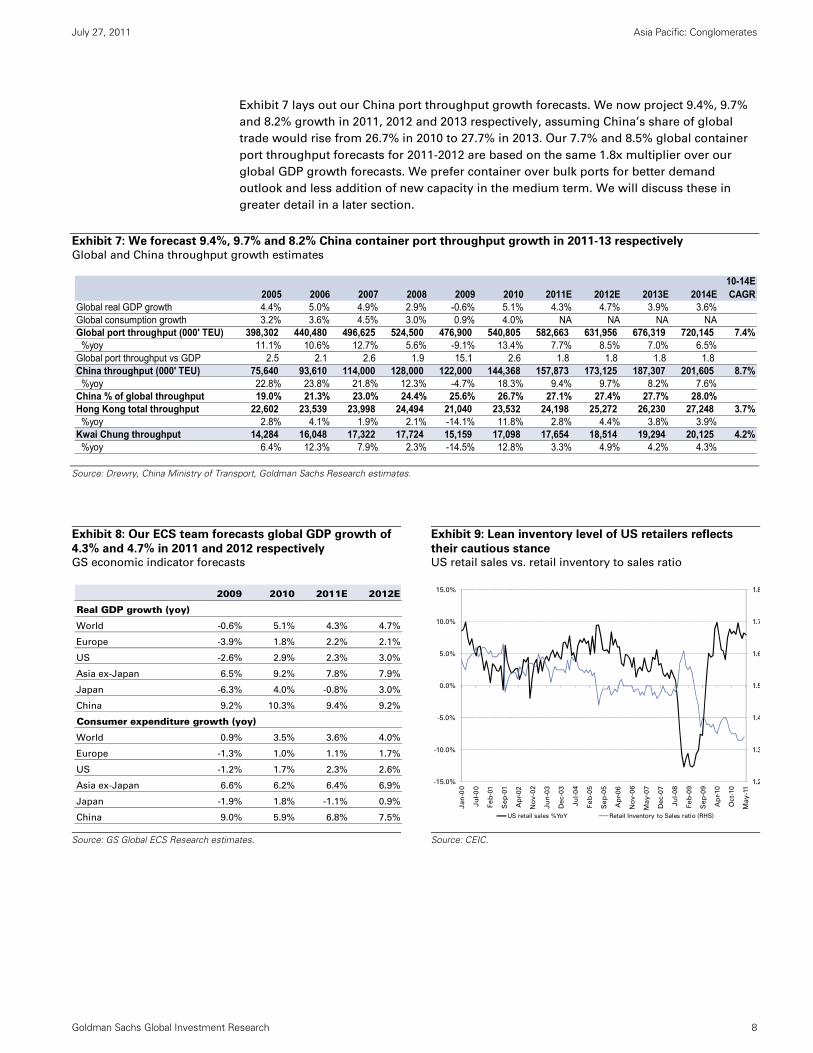

Exhibit 7 lays out our China port throughput growth forecasts. We now project 9.4%, 9.7%

and 8.2% growth in 2011, 2012 and 2013 respectively, assuming China’s share of global

trade would rise from 26.7% in 2010 to 27.7% in 2013. Our 7.7% and 8.5% global container

port throughput forecasts for 2011-2012 are based on the same 1.8x multiplier over our

global GDP growth forecasts. We prefer container over bulk ports for better demand

outlook and less addition of new capacity in the medium term. We will discuss these in

greater detail in a later section.

Exhibit 7: We forecast 9.4%, 9.7% and 8.2% China container port throughput growth in 2011-13 respectively

Global and China throughput growth estimates

Source: Drewry, China Ministry of Transport, Goldman Sachs Research estimates.

Exhibit 8: Our ECS team forecasts global GDP growth of

4.3% and 4.7% in 2011 and 2012 respectively GS economic indicator forecasts

Exhibit 9: Lean inventory level of US retailers reflects

their cautious stance US retail sales vs. retail inventory to sales ratio

Source: GS Global ECS Research estimates.

Source: CEIC.

2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014E10-14E CAGR

Global real GDP growth 4.4% 5.0% 4.9% 2.9% -0.6% 5.1% 4.3% 4.7% 3.9% 3.6%Global consumption growth 3.2% 3.6% 4.5% 3.0% 0.9% 4.0% NA NA NA NAGlobal port throughput (000' TEU) 398,302 440,480 496,625 524,500 476,900 540,805 582,663 631,956 676,319 720,145 7.4% %yoy 11.1% 10.6% 12.7% 5.6% -9.1% 13.4% 7.7% 8.5% 7.0% 6.5%Global port throughput vs GDP 2.5 2.1 2.6 1.9 15.1 2.6 1.8 1.8 1.8 1.8 China throughput (000' TEU) 75,640 93,610 114,000 128,000 122,000 144,368 157,873 173,125 187,307 201,605 8.7% %yoy 22.8% 23.8% 21.8% 12.3% -4.7% 18.3% 9.4% 9.7% 8.2% 7.6%China % of global throughput 19.0% 21.3% 23.0% 24.4% 25.6% 26.7% 27.1% 27.4% 27.7% 28.0%Hong Kong total throughput 22,602 23,539 23,998 24,494 21,040 23,532 24,198 25,272 26,230 27,248 3.7% %yoy 2.8% 4.1% 1.9% 2.1% -14.1% 11.8% 2.8% 4.4% 3.8% 3.9%Kwai Chung throughput 14,284 16,048 17,322 17,724 15,159 17,098 17,654 18,514 19,294 20,125 4.2% %yoy 6.4% 12.3% 7.9% 2.3% -14.5% 12.8% 3.3% 4.9% 4.2% 4.3%

2009 2010 2011E 2012E

Real GDP growth (yoy)

World -0.6% 5.1% 4.3% 4.7%

Europe -3.9% 1.8% 2.2% 2.1%

US -2.6% 2.9% 2.3% 3.0%

Asia ex-Japan 6.5% 9.2% 7.8% 7.9%

Japan -6.3% 4.0% -0.8% 3.0%

China 9.2% 10.3% 9.4% 9.2%

Consumer expenditure growth (yoy)

World 0.9% 3.5% 3.6% 4.0%

Europe -1.3% 1.0% 1.1% 1.7%

US -1.2% 1.7% 2.3% 2.6%

Asia ex-Japan 6.6% 6.2% 6.4% 6.9%

Japan -1.9% 1.8% -1.1% 0.9%

China 9.0% 5.9% 6.8% 7.5%

1.2

1.3

1.4

1.5

1.6

1.7

1.8

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Ja

n-0

0

Ju

l-0

0

Fe

b-0

1

Se

p-0

1

Ap

r-0

2

No

v-0

2

Ju

n-0

3

De

c-0

3

Ju

l-0

4

Fe

b-0

5

Se

p-0

5

Ap

r-0

6

No

v-0

6

Ma

y-0

7

De

c-0

7

Ju

l-0

8

Fe

b-0

9

Se

p-0

9

Ap

r-10

Oct-

10

Ma

y-1

1

US retail sales %YoY Retail Inventory to Sales ratio (RHS)

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 9

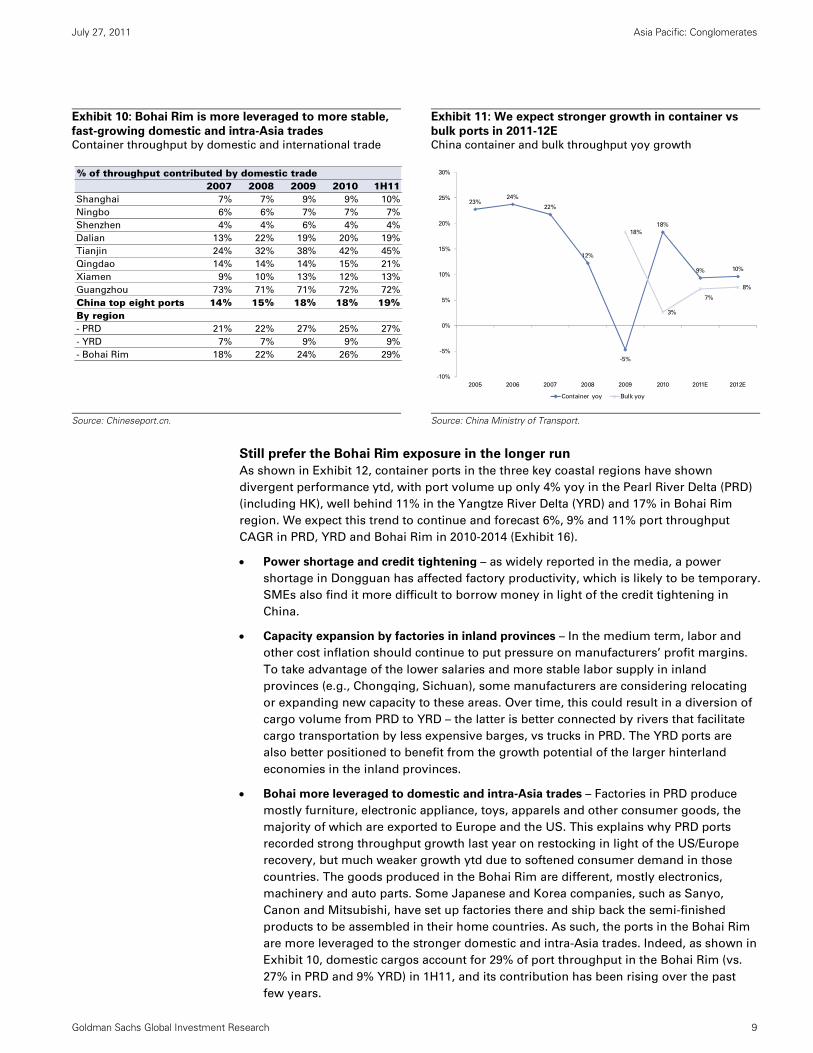

Exhibit 10: Bohai Rim is more leveraged to more stable,

fast-growing domestic and intra-Asia trades Container throughput by domestic and international trade

Exhibit 11: We expect stronger growth in container vs

bulk ports in 2011-12E China container and bulk throughput yoy growth

Source: Chineseport.cn.

Source: China Ministry of Transport.

Still prefer the Bohai Rim exposure in the longer run

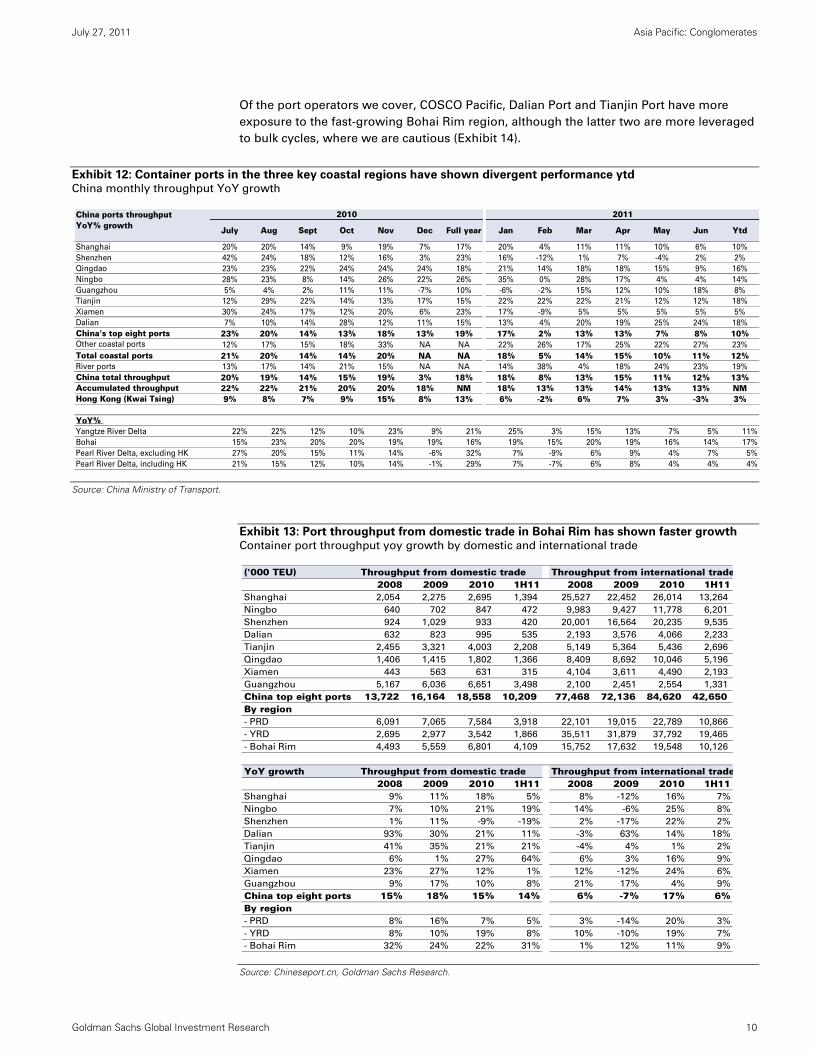

As shown in Exhibit 12, container ports in the three key coastal regions have shown

divergent performance ytd, with port volume up only 4% yoy in the Pearl River Delta (PRD)

(including HK), well behind 11% in the Yangtze River Delta (YRD) and 17% in Bohai Rim

region. We expect this trend to continue and forecast 6%, 9% and 11% port throughput

CAGR in PRD, YRD and Bohai Rim in 2010-2014 (Exhibit 16).

Power shortage and credit tightening – as widely reported in the media, a power

shortage in Dongguan has affected factory productivity, which is likely to be temporary.

SMEs also find it more difficult to borrow money in light of the credit tightening in

China.

Capacity expansion by factories in inland provinces – In the medium term, labor and

other cost inflation should continue to put pressure on manufacturers’ profit margins.

To take advantage of the lower salaries and more stable labor supply in inland

provinces (e.g., Chongqing, Sichuan), some manufacturers are considering relocating

or expanding new capacity to these areas. Over time, this could result in a diversion of

cargo volume from PRD to YRD – the latter is better connected by rivers that facilitate

cargo transportation by less expensive barges, vs trucks in PRD. The YRD ports are

also better positioned to benefit from the growth potential of the larger hinterland

economies in the inland provinces.

Bohai more leveraged to domestic and intra-Asia trades – Factories in PRD produce

mostly furniture, electronic appliance, toys, apparels and other consumer goods, the

majority of which are exported to Europe and the US. This explains why PRD ports

recorded strong throughput growth last year on restocking in light of the US/Europe

recovery, but much weaker growth ytd due to softened consumer demand in those

countries. The goods produced in the Bohai Rim are different, mostly electronics,

machinery and auto parts. Some Japanese and Korea companies, such as Sanyo,

Canon and Mitsubishi, have set up factories there and ship back the semi-finished

products to be assembled in their home countries. As such, the ports in the Bohai Rim

are more leveraged to the stronger domestic and intra-Asia trades. Indeed, as shown in

Exhibit 10, domestic cargos account for 29% of port throughput in the Bohai Rim (vs.

27% in PRD and 9% YRD) in 1H11, and its contribution has been rising over the past

few years.

% of throughput contributed by domestic trade2007 2008 2009 2010 1H11

Shanghai 7% 7% 9% 9% 10%

Ningbo 6% 6% 7% 7% 7%

Shenzhen 4% 4% 6% 4% 4%

Dalian 13% 22% 19% 20% 19%

Tianjin 24% 32% 38% 42% 45%

Qingdao 14% 14% 14% 15% 21%

Xiamen 9% 10% 13% 12% 13%

Guangzhou 73% 71% 71% 72% 72%

China top eight ports 14% 15% 18% 18% 19%By region- PRD 21% 22% 27% 25% 27%

- YRD 7% 7% 9% 9% 9%

- Bohai Rim 18% 22% 24% 26% 29%

23%24%

22%

12%

-5%

18%

9% 10%

18%

3%

7%

8%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2005 2006 2007 2008 2009 2010 2011E 2012E

Container yoy Bulk yoy

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 10

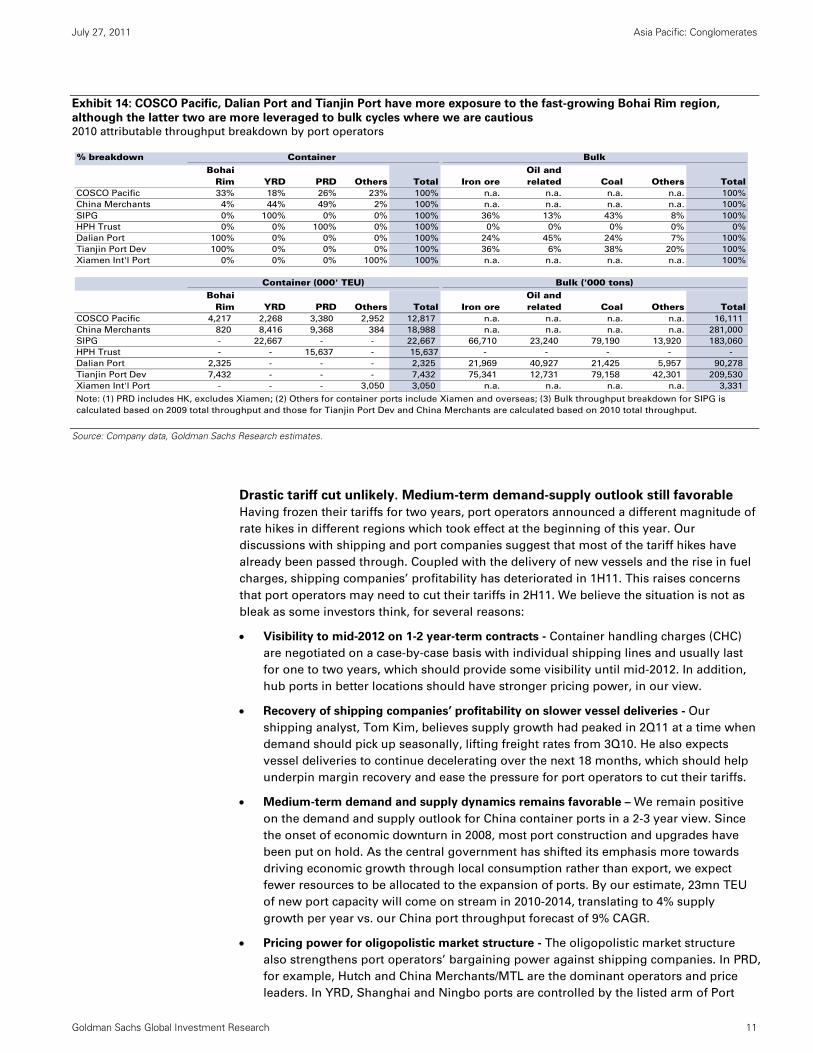

Of the port operators we cover, COSCO Pacific, Dalian Port and Tianjin Port have more

exposure to the fast-growing Bohai Rim region, although the latter two are more leveraged

to bulk cycles, where we are cautious (Exhibit 14).

Exhibit 12: Container ports in the three key coastal regions have shown divergent performance ytd China monthly throughput YoY growth

Source: China Ministry of Transport.

Exhibit 13: Port throughput from domestic trade in Bohai Rim has shown faster growth Container port throughput yoy growth by domestic and international trade

Source: Chineseport.cn, Goldman Sachs Research.

China ports throughputYoY% growth

Shanghai 20% 20% 14% 9% 19% 7% 17% 20% 4% 11% 11% 10% 6% 10%

Shenzhen 42% 24% 18% 12% 16% 3% 23% 16% -12% 1% 7% -4% 2% 2%

Qingdao 23% 23% 22% 24% 24% 24% 18% 21% 14% 18% 18% 15% 9% 16%

Ningbo 28% 23% 8% 14% 26% 22% 26% 35% 0% 28% 17% 4% 4% 14%

Guangzhou 5% 4% 2% 11% 11% -7% 10% -6% -2% 15% 12% 10% 18% 8%

Tianjin 12% 29% 22% 14% 13% 17% 15% 22% 22% 22% 21% 12% 12% 18%

Xiamen 30% 24% 17% 12% 20% 6% 23% 17% -9% 5% 5% 5% 5% 5%

Dalian 7% 10% 14% 28% 12% 11% 15% 13% 4% 20% 19% 25% 24% 18%

China's top eight ports 23% 20% 14% 13% 18% 13% 19% 17% 2% 13% 13% 7% 8% 10%Other coastal ports 12% 17% 15% 18% 33% NA NA 22% 26% 17% 25% 22% 27% 23%

Total coastal ports 21% 20% 14% 14% 20% NA NA 18% 5% 14% 15% 10% 11% 12%River ports 13% 17% 14% 21% 15% NA NA 14% 38% 4% 18% 24% 23% 19%

China total throughput 20% 19% 14% 15% 19% 3% 18% 18% 8% 13% 15% 11% 12% 13%Accumulated throughput 22% 22% 21% 20% 20% 18% NM 18% 13% 13% 14% 13% 13% NMHong Kong (Kwai Tsing) 9% 8% 7% 9% 15% 8% 13% 6% -2% 6% 7% 3% -3% 3%

YoY% Yangtze River Delta 22% 22% 12% 10% 23% 9% 21% 25% 3% 15% 13% 7% 5% 11%

Bohai 15% 23% 20% 20% 19% 19% 16% 19% 15% 20% 19% 16% 14% 17%

Pearl River Delta, excluding HK 27% 20% 15% 11% 14% -6% 32% 7% -9% 6% 9% 4% 7% 5%

Pearl River Delta, including HK 21% 15% 12% 10% 14% -1% 29% 7% -7% 6% 8% 4% 4% 4%

2010

Full year FebJanSeptAug DecNovOctJuly

2011

Mar Apr May Jun Ytd

('000 TEU) Throughput from domestic trade Throughput from international trade2008 2009 2010 1H11 2008 2009 2010 1H11

Shanghai 2,054 2,275 2,695 1,394 25,527 22,452 26,014 13,264

Ningbo 640 702 847 472 9,983 9,427 11,778 6,201

Shenzhen 924 1,029 933 420 20,001 16,564 20,235 9,535

Dalian 632 823 995 535 2,193 3,576 4,066 2,233

Tianjin 2,455 3,321 4,003 2,208 5,149 5,364 5,436 2,696

Qingdao 1,406 1,415 1,802 1,366 8,409 8,692 10,046 5,196

Xiamen 443 563 631 315 4,104 3,611 4,490 2,193

Guangzhou 5,167 6,036 6,651 3,498 2,100 2,451 2,554 1,331

China top eight ports 13,722 16,164 18,558 10,209 77,468 72,136 84,620 42,650 By region- PRD 6,091 7,065 7,584 3,918 22,101 19,015 22,789 10,866

- YRD 2,695 2,977 3,542 1,866 35,511 31,879 37,792 19,465

- Bohai Rim 4,493 5,559 6,801 4,109 15,752 17,632 19,548 10,126

YoY growth Throughput from domestic trade Throughput from international trade2008 2009 2010 1H11 2008 2009 2010 1H11

Shanghai 9% 11% 18% 5% 8% -12% 16% 7%

Ningbo 7% 10% 21% 19% 14% -6% 25% 8%

Shenzhen 1% 11% -9% -19% 2% -17% 22% 2%

Dalian 93% 30% 21% 11% -3% 63% 14% 18%

Tianjin 41% 35% 21% 21% -4% 4% 1% 2%

Qingdao 6% 1% 27% 64% 6% 3% 16% 9%

Xiamen 23% 27% 12% 1% 12% -12% 24% 6%

Guangzhou 9% 17% 10% 8% 21% 17% 4% 9%

China top eight ports 15% 18% 15% 14% 6% -7% 17% 6%By region- PRD 8% 16% 7% 5% 3% -14% 20% 3%

- YRD 8% 10% 19% 8% 10% -10% 19% 7%

- Bohai Rim 32% 24% 22% 31% 1% 12% 11% 9%

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 11

Exhibit 14: COSCO Pacific, Dalian Port and Tianjin Port have more exposure to the fast-growing Bohai Rim region,

although the latter two are more leveraged to bulk cycles where we are cautious 2010 attributable throughput breakdown by port operators

Source: Company data, Goldman Sachs Research estimates.

Drastic tariff cut unlikely. Medium-term demand-supply outlook still favorable

Having frozen their tariffs for two years, port operators announced a different magnitude of

rate hikes in different regions which took effect at the beginning of this year. Our

discussions with shipping and port companies suggest that most of the tariff hikes have

already been passed through. Coupled with the delivery of new vessels and the rise in fuel

charges, shipping companies’ profitability has deteriorated in 1H11. This raises concerns

that port operators may need to cut their tariffs in 2H11. We believe the situation is not as

bleak as some investors think, for several reasons:

Visibility to mid-2012 on 1-2 year-term contracts - Container handling charges (CHC)

are negotiated on a case-by-case basis with individual shipping lines and usually last

for one to two years, which should provide some visibility until mid-2012. In addition,

hub ports in better locations should have stronger pricing power, in our view.

Recovery of shipping companies’ profitability on slower vessel deliveries - Our

shipping analyst, Tom Kim, believes supply growth had peaked in 2Q11 at a time when

demand should pick up seasonally, lifting freight rates from 3Q10. He also expects

vessel deliveries to continue decelerating over the next 18 months, which should help

underpin margin recovery and ease the pressure for port operators to cut their tariffs.

Medium-term demand and supply dynamics remains favorable – We remain positive

on the demand and supply outlook for China container ports in a 2-3 year view. Since

the onset of economic downturn in 2008, most port construction and upgrades have

been put on hold. As the central government has shifted its emphasis more towards

driving economic growth through local consumption rather than export, we expect

fewer resources to be allocated to the expansion of ports. By our estimate, 23mn TEU

of new port capacity will come on stream in 2010-2014, translating to 4% supply

growth per year vs. our China port throughput forecast of 9% CAGR.

Pricing power for oligopolistic market structure - The oligopolistic market structure

also strengthens port operators’ bargaining power against shipping companies. In PRD,

for example, Hutch and China Merchants/MTL are the dominant operators and price

leaders. In YRD, Shanghai and Ningbo ports are controlled by the listed arm of Port

% breakdownBohai

Rim YRD PRD Others Total Iron oreOil and related Coal Others Total

COSCO Pacific 33% 18% 26% 23% 100% n.a. n.a. n.a. n.a. 100%

China Merchants 4% 44% 49% 2% 100% n.a. n.a. n.a. n.a. 100%

SIPG 0% 100% 0% 0% 100% 36% 13% 43% 8% 100%

HPH Trust 0% 0% 100% 0% 100% 0% 0% 0% 0% 0%

Dalian Port 100% 0% 0% 0% 100% 24% 45% 24% 7% 100%

Tianjin Port Dev 100% 0% 0% 0% 100% 36% 6% 38% 20% 100%

Xiamen Int'l Port 0% 0% 0% 100% 100% n.a. n.a. n.a. n.a. 100%

Bohai Rim YRD PRD Others Total Iron ore

Oil and related Coal Others Total

COSCO Pacific 4,217 2,268 3,380 2,952 12,817 n.a. n.a. n.a. n.a. 16,111

China Merchants 820 8,416 9,368 384 18,988 n.a. n.a. n.a. n.a. 281,000

SIPG - 22,667 - - 22,667 66,710 23,240 79,190 13,920 183,060

HPH Trust - - 15,637 - 15,637 - - - - -

Dalian Port 2,325 - - - 2,325 21,969 40,927 21,425 5,957 90,278

Tianjin Port Dev 7,432 - - - 7,432 75,341 12,731 79,158 42,301 209,530

Xiamen Int'l Port - - - 3,050 3,050 n.a. n.a. n.a. n.a. 3,331

Container Bulk

Container (000' TEU) Bulk ('000 tons)

Note: (1) PRD includes HK, excludes Xiamen; (2) Others for container ports include Xiamen and overseas; (3) Bulk throughput breakdown for SIPG is

calculated based on 2009 total throughput and those for Tianjin Port Dev and China Merchants are calculated based on 2010 total throughput.

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 12

Authorities, namely SIPG and Ningbo Port. Shanghai’s pricing strategy is indicative of

the trend and Ningbo is usually a price follower.

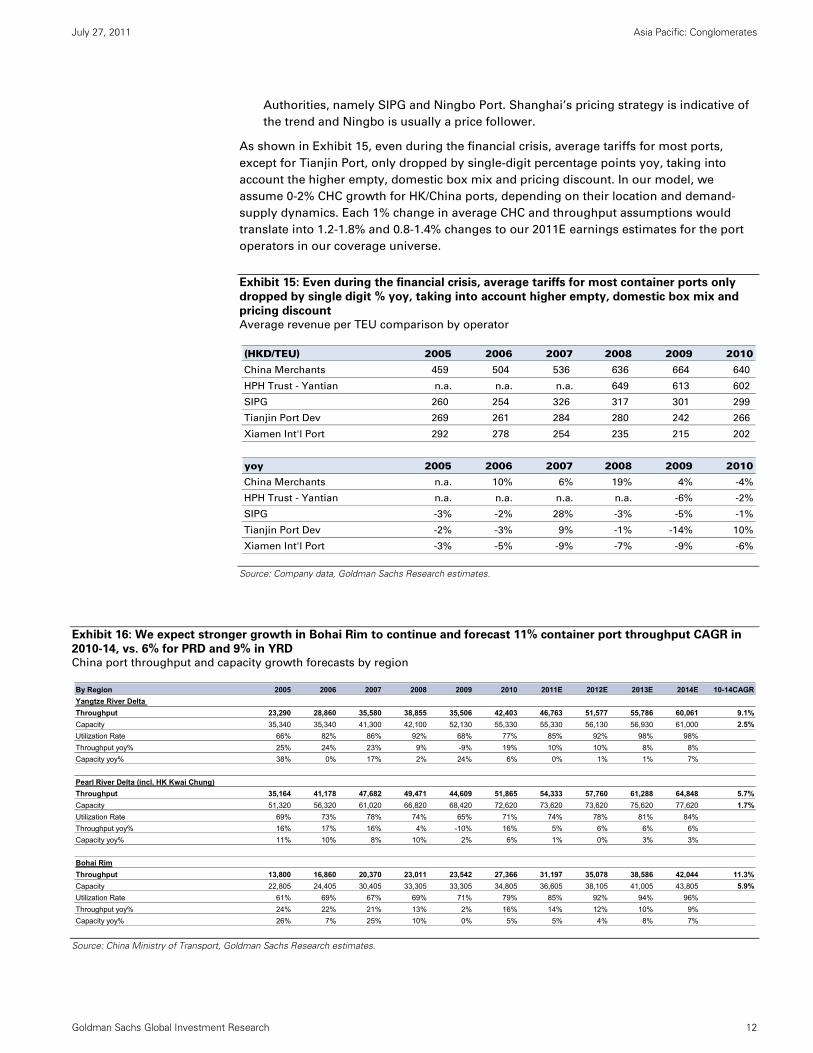

As shown in Exhibit 15, even during the financial crisis, average tariffs for most ports,

except for Tianjin Port, only dropped by single-digit percentage points yoy, taking into

account the higher empty, domestic box mix and pricing discount. In our model, we

assume 0-2% CHC growth for HK/China ports, depending on their location and demand-

supply dynamics. Each 1% change in average CHC and throughput assumptions would

translate into 1.2-1.8% and 0.8-1.4% changes to our 2011E earnings estimates for the port

operators in our coverage universe.

Exhibit 15: Even during the financial crisis, average tariffs for most container ports only

dropped by single digit % yoy, taking into account higher empty, domestic box mix and

pricing discount Average revenue per TEU comparison by operator

Source: Company data, Goldman Sachs Research estimates.

Exhibit 16: We expect stronger growth in Bohai Rim to continue and forecast 11% container port throughput CAGR in

2010-14, vs. 6% for PRD and 9% in YRD China port throughput and capacity growth forecasts by region

Source: China Ministry of Transport, Goldman Sachs Research estimates.

(HKD/TEU) 2005 2006 2007 2008 2009 2010

China Merchants 459 504 536 636 664 640

HPH Trust - Yantian n.a. n.a. n.a. 649 613 602

SIPG 260 254 326 317 301 299

Tianjin Port Dev 269 261 284 280 242 266

Xiamen Int'l Port 292 278 254 235 215 202

yoy 2005 2006 2007 2008 2009 2010

China Merchants n.a. 10% 6% 19% 4% -4%

HPH Trust - Yantian n.a. n.a. n.a. n.a. -6% -2%

SIPG -3% -2% 28% -3% -5% -1%

Tianjin Port Dev -2% -3% 9% -1% -14% 10%

Xiamen Int'l Port -3% -5% -9% -7% -9% -6%

By Region 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014E 10-14CAGR

Yangtze River Delta

Throughput 23,290 28,860 35,580 38,855 35,506 42,403 46,763 51,577 55,786 60,061 9.1%

Capacity 35,340 35,340 41,300 42,100 52,130 55,330 55,330 56,130 56,930 61,000 2.5%

Utilization Rate 66% 82% 86% 92% 68% 77% 85% 92% 98% 98%

Throughput yoy% 25% 24% 23% 9% -9% 19% 10% 10% 8% 8%

Capacity yoy% 38% 0% 17% 2% 24% 6% 0% 1% 1% 7%

Pearl River Delta (incl. HK Kwai Chung)

Throughput 35,164 41,178 47,682 49,471 44,609 51,865 54,333 57,760 61,288 64,848 5.7%

Capacity 51,320 56,320 61,020 66,820 68,420 72,620 73,620 73,620 75,620 77,620 1.7%

Utilization Rate 69% 73% 78% 74% 65% 71% 74% 78% 81% 84%

Throughput yoy% 16% 17% 16% 4% -10% 16% 5% 6% 6% 6%

Capacity yoy% 11% 10% 8% 10% 2% 6% 1% 0% 3% 3%

Bohai Rim

Throughput 13,800 16,860 20,370 23,011 23,542 27,366 31,197 35,078 38,586 42,044 11.3%

Capacity 22,805 24,405 30,405 33,305 33,305 34,805 36,605 38,105 41,005 43,805 5.9%

Utilization Rate 61% 69% 67% 69% 71% 79% 85% 92% 94% 96%

Throughput yoy% 24% 22% 21% 13% 2% 16% 14% 12% 10% 9%

Capacity yoy% 26% 7% 25% 10% 0% 5% 5% 4% 8% 7%

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 13

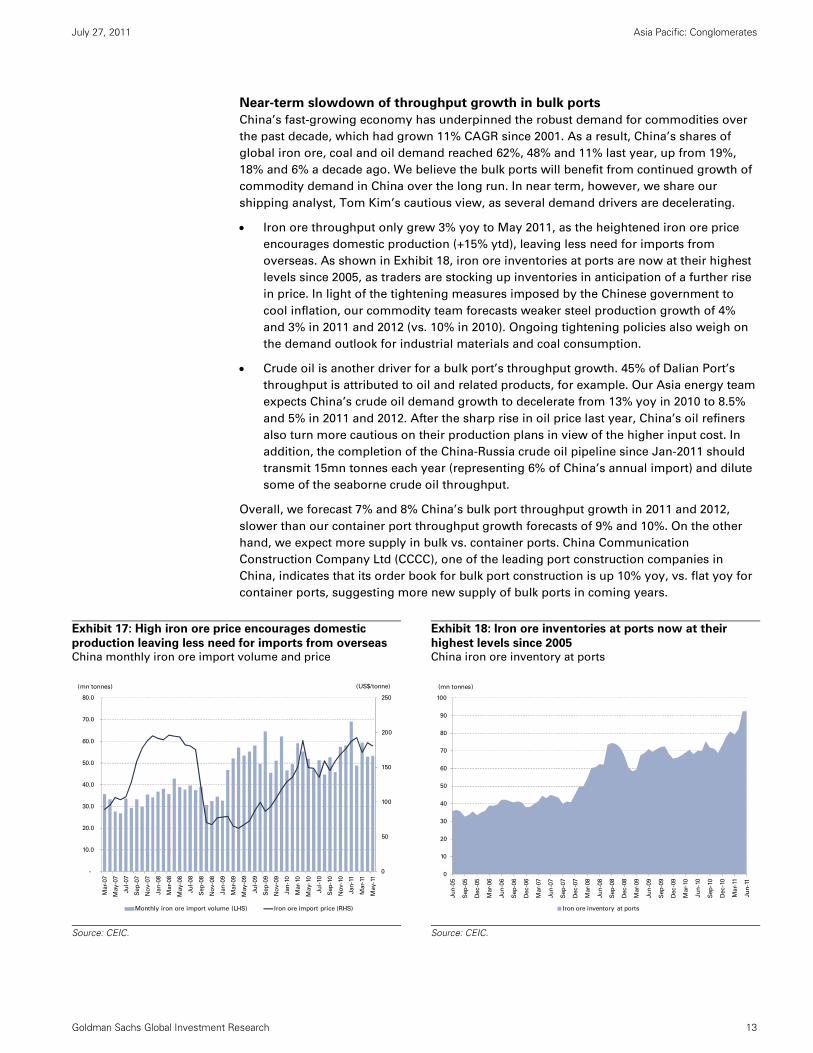

Near-term slowdown of throughput growth in bulk ports

China’s fast-growing economy has underpinned the robust demand for commodities over

the past decade, which had grown 11% CAGR since 2001. As a result, China’s shares of

global iron ore, coal and oil demand reached 62%, 48% and 11% last year, up from 19%,

18% and 6% a decade ago. We believe the bulk ports will benefit from continued growth of

commodity demand in China over the long run. In near term, however, we share our

shipping analyst, Tom Kim’s cautious view, as several demand drivers are decelerating.

Iron ore throughput only grew 3% yoy to May 2011, as the heightened iron ore price

encourages domestic production (+15% ytd), leaving less need for imports from

overseas. As shown in Exhibit 18, iron ore inventories at ports are now at their highest

levels since 2005, as traders are stocking up inventories in anticipation of a further rise

in price. In light of the tightening measures imposed by the Chinese government to

cool inflation, our commodity team forecasts weaker steel production growth of 4%

and 3% in 2011 and 2012 (vs. 10% in 2010). Ongoing tightening policies also weigh on

the demand outlook for industrial materials and coal consumption.

Crude oil is another driver for a bulk port’s throughput growth. 45% of Dalian Port’s

throughput is attributed to oil and related products, for example. Our Asia energy team

expects China’s crude oil demand growth to decelerate from 13% yoy in 2010 to 8.5%

and 5% in 2011 and 2012. After the sharp rise in oil price last year, China’s oil refiners

also turn more cautious on their production plans in view of the higher input cost. In

addition, the completion of the China-Russia crude oil pipeline since Jan-2011 should

transmit 15mn tonnes each year (representing 6% of China’s annual import) and dilute

some of the seaborne crude oil throughput.

Overall, we forecast 7% and 8% China’s bulk port throughput growth in 2011 and 2012,

slower than our container port throughput growth forecasts of 9% and 10%. On the other

hand, we expect more supply in bulk vs. container ports. China Communication

Construction Company Ltd (CCCC), one of the leading port construction companies in

China, indicates that its order book for bulk port construction is up 10% yoy, vs. flat yoy for

container ports, suggesting more new supply of bulk ports in coming years.

Exhibit 17: High iron ore price encourages domestic

production leaving less need for imports from overseas China monthly iron ore import volume and price

Exhibit 18: Iron ore inventories at ports now at their

highest levels since 2005 China iron ore inventory at ports

Source: CEIC.

Source: CEIC.

0

50

100

150

200

250

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Mar-

07

May-0

7

Ju

l-07

Sep

-07

No

v-0

7

Jan

-08

Mar-

08

May-0

8

Ju

l-08

Sep

-08

No

v-0

8

Jan

-09

Mar-

09

May-0

9

Ju

l-09

Sep

-09

No

v-0

9

Jan

-10

Mar-

10

May-1

0

Ju

l-10

Sep

-10

No

v-1

0

Jan

-11

Mar-

11

May-1

1

Monthly iron ore import volume (LHS) Iron ore import price (RHS)

(US$/tonne)(mn tonnes)

0

10

20

30

40

50

60

70

80

90

100

Ju

n-0

5

Sep

-05

Dec-0

5

Mar-

06

Ju

n-0

6

Sep

-06

Dec-0

6

Mar-

07

Ju

n-0

7

Sep

-07

Dec-0

7

Mar-

08

Ju

n-0

8

Sep

-08

Dec-0

8

Mar-

09

Ju

n-0

9

Sep

-09

Dec-0

9

Mar-

10

Ju

n-1

0

Sep

-10

Dec-1

0

Mar-

11

Ju

n-1

1

Iron ore inventory at ports

(mn tonnes)

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 14

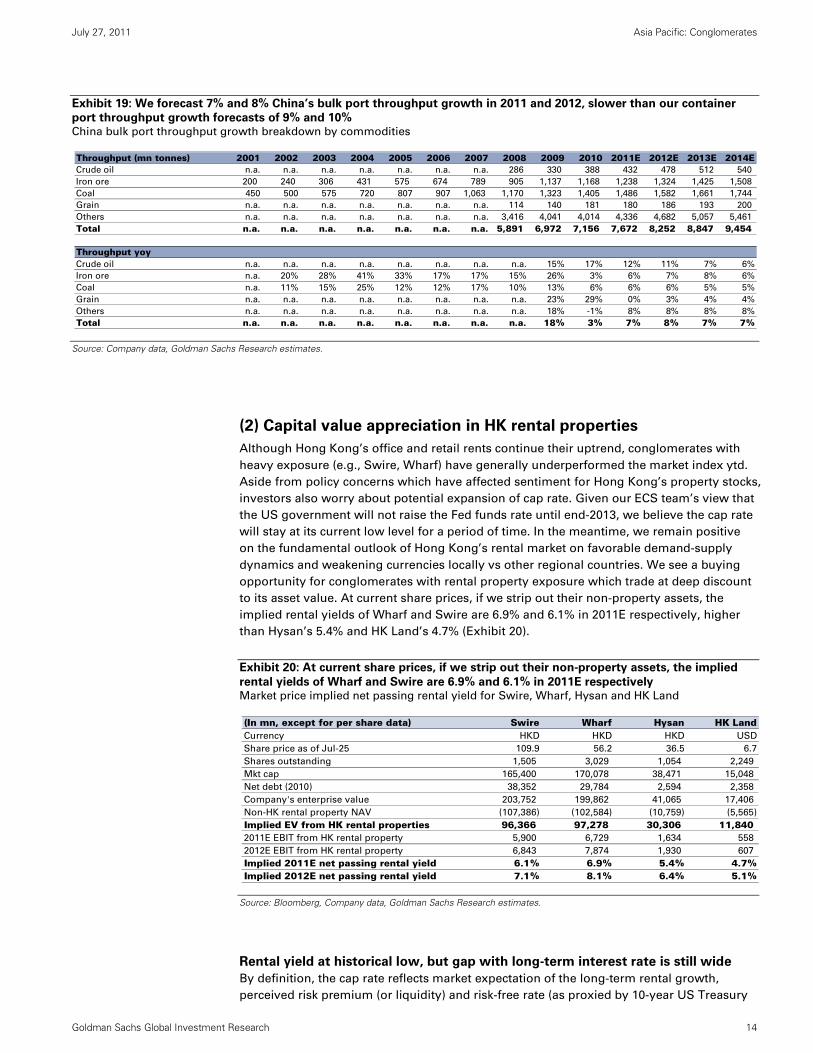

Exhibit 19: We forecast 7% and 8% China’s bulk port throughput growth in 2011 and 2012, slower than our container

port throughput growth forecasts of 9% and 10% China bulk port throughput growth breakdown by commodities

Source: Company data, Goldman Sachs Research estimates.

(2) Capital value appreciation in HK rental properties

Although Hong Kong’s office and retail rents continue their uptrend, conglomerates with

heavy exposure (e.g., Swire, Wharf) have generally underperformed the market index ytd.

Aside from policy concerns which have affected sentiment for Hong Kong’s property stocks,

investors also worry about potential expansion of cap rate. Given our ECS team’s view that

the US government will not raise the Fed funds rate until end-2013, we believe the cap rate

will stay at its current low level for a period of time. In the meantime, we remain positive

on the fundamental outlook of Hong Kong’s rental market on favorable demand-supply

dynamics and weakening currencies locally vs other regional countries. We see a buying

opportunity for conglomerates with rental property exposure which trade at deep discount

to its asset value. At current share prices, if we strip out their non-property assets, the

implied rental yields of Wharf and Swire are 6.9% and 6.1% in 2011E respectively, higher

than Hysan’s 5.4% and HK Land’s 4.7% (Exhibit 20).

Exhibit 20: At current share prices, if we strip out their non-property assets, the implied

rental yields of Wharf and Swire are 6.9% and 6.1% in 2011E respectively Market price implied net passing rental yield for Swire, Wharf, Hysan and HK Land

Source: Bloomberg, Company data, Goldman Sachs Research estimates.

Rental yield at historical low, but gap with long-term interest rate is still wide

By definition, the cap rate reflects market expectation of the long-term rental growth,

perceived risk premium (or liquidity) and risk-free rate (as proxied by 10-year US Treasury

Throughput (mn tonnes) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014ECrude oil n.a. n.a. n.a. n.a. n.a. n.a. n.a. 286 330 388 432 478 512 540

Iron ore 200 240 306 431 575 674 789 905 1,137 1,168 1,238 1,324 1,425 1,508

Coal 450 500 575 720 807 907 1,063 1,170 1,323 1,405 1,486 1,582 1,661 1,744

Grain n.a. n.a. n.a. n.a. n.a. n.a. n.a. 114 140 181 180 186 193 200

Others n.a. n.a. n.a. n.a. n.a. n.a. n.a. 3,416 4,041 4,014 4,336 4,682 5,057 5,461

Total n.a. n.a. n.a. n.a. n.a. n.a. n.a. 5,891 6,972 7,156 7,672 8,252 8,847 9,454

Throughput yoyCrude oil n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 15% 17% 12% 11% 7% 6%

Iron ore n.a. 20% 28% 41% 33% 17% 17% 15% 26% 3% 6% 7% 8% 6%

Coal n.a. 11% 15% 25% 12% 12% 17% 10% 13% 6% 6% 6% 5% 5%

Grain n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 23% 29% 0% 3% 4% 4%

Others n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 18% -1% 8% 8% 8% 8%

Total n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. 18% 3% 7% 8% 7% 7%

(In mn, except for per share data) Swire Wharf Hysan HK LandCurrency HKD HKD HKD USD

Share price as of Jul-25 109.9 56.2 36.5 6.7

Shares outstanding 1,505 3,029 1,054 2,249

Mkt cap 165,400 170,078 38,471 15,048

Net debt (2010) 38,352 29,784 2,594 2,358

Company's enterprise value 203,752 199,862 41,065 17,406

Non-HK rental property NAV (107,386) (102,584) (10,759) (5,565)

Implied EV from HK rental properties 96,366 97,278 30,306 11,840 2011E EBIT from HK rental property 5,900 6,729 1,634 558

2012E EBIT from HK rental property 6,843 7,874 1,930 607

Implied 2011E net passing rental yield 6.1% 6.9% 5.4% 4.7%Implied 2012E net passing rental yield 7.1% 8.1% 6.4% 5.1%

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 15

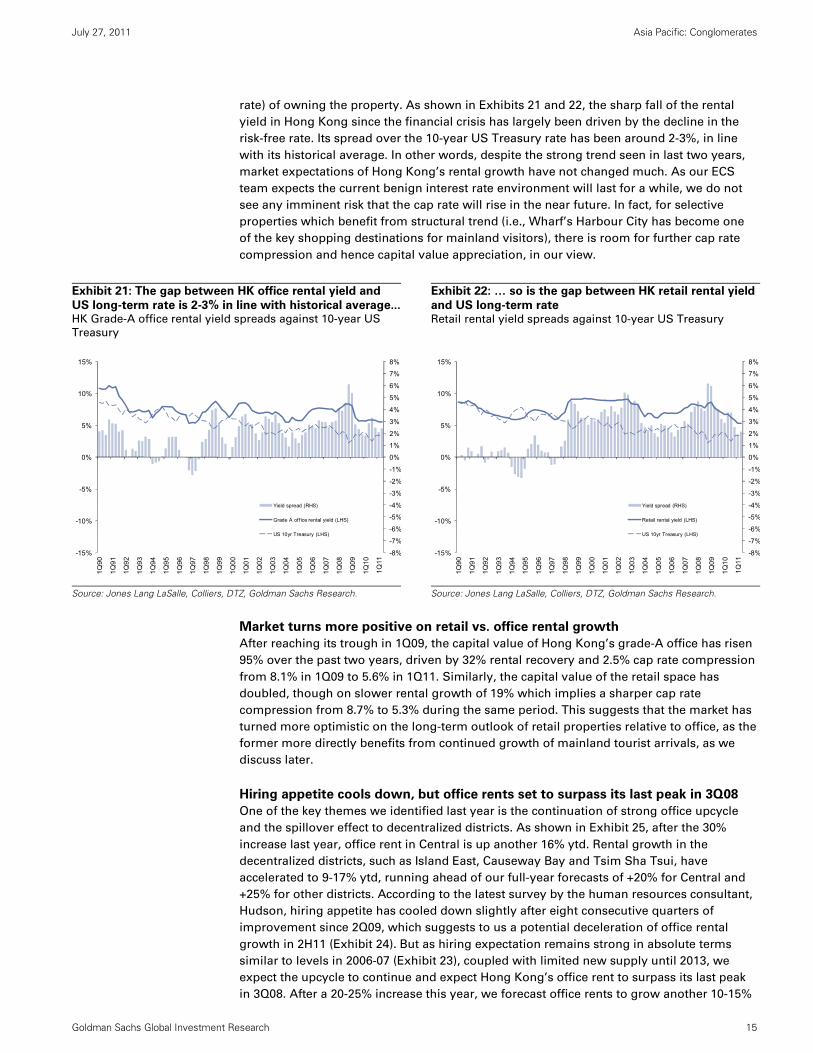

rate) of owning the property. As shown in Exhibits 21 and 22, the sharp fall of the rental

yield in Hong Kong since the financial crisis has largely been driven by the decline in the

risk-free rate. Its spread over the 10-year US Treasury rate has been around 2-3%, in line

with its historical average. In other words, despite the strong trend seen in last two years,

market expectations of Hong Kong’s rental growth have not changed much. As our ECS

team expects the current benign interest rate environment will last for a while, we do not

see any imminent risk that the cap rate will rise in the near future. In fact, for selective

properties which benefit from structural trend (i.e., Wharf’s Harbour City has become one

of the key shopping destinations for mainland visitors), there is room for further cap rate

compression and hence capital value appreciation, in our view.

Exhibit 21: The gap between HK office rental yield and

US long-term rate is 2-3% in line with historical average...HK Grade-A office rental yield spreads against 10-year US

Treasury

Exhibit 22: … so is the gap between HK retail rental yield

and US long-term rate Retail rental yield spreads against 10-year US Treasury

Source: Jones Lang LaSalle, Colliers, DTZ, Goldman Sachs Research.

Source: Jones Lang LaSalle, Colliers, DTZ, Goldman Sachs Research.

Market turns more positive on retail vs. office rental growth

After reaching its trough in 1Q09, the capital value of Hong Kong’s grade-A office has risen

95% over the past two years, driven by 32% rental recovery and 2.5% cap rate compression

from 8.1% in 1Q09 to 5.6% in 1Q11. Similarly, the capital value of the retail space has

doubled, though on slower rental growth of 19% which implies a sharper cap rate

compression from 8.7% to 5.3% during the same period. This suggests that the market has

turned more optimistic on the long-term outlook of retail properties relative to office, as the

former more directly benefits from continued growth of mainland tourist arrivals, as we

discuss later.

Hiring appetite cools down, but office rents set to surpass its last peak in 3Q08

One of the key themes we identified last year is the continuation of strong office upcycle

and the spillover effect to decentralized districts. As shown in Exhibit 25, after the 30%

increase last year, office rent in Central is up another 16% ytd. Rental growth in the

decentralized districts, such as Island East, Causeway Bay and Tsim Sha Tsui, have

accelerated to 9-17% ytd, running ahead of our full-year forecasts of +20% for Central and

+25% for other districts. According to the latest survey by the human resources consultant,

Hudson, hiring appetite has cooled down slightly after eight consecutive quarters of

improvement since 2Q09, which suggests to us a potential deceleration of office rental

growth in 2H11 (Exhibit 24). But as hiring expectation remains strong in absolute terms

similar to levels in 2006-07 (Exhibit 23), coupled with limited new supply until 2013, we

expect the upcycle to continue and expect Hong Kong’s office rent to surpass its last peak

in 3Q08. After a 20-25% increase this year, we forecast office rents to grow another 10-15%

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

-15%

-10%

-5%

0%

5%

10%

15%

1Q

90

1Q

91

1Q

92

1Q

93

1Q

94

1Q

95

1Q

96

1Q

97

1Q

98

1Q

99

1Q

00

1Q

01

1Q

02

1Q

03

1Q

04

1Q

05

1Q

06

1Q

07

1Q

08

1Q

09

1Q

10

1Q

11

Yield spread (RHS)

Grade A office rental yield (LHS)

US 10yr Treasury (LHS)

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

-15%

-10%

-5%

0%

5%

10%

15%

1Q

90

1Q

91

1Q

92

1Q

93

1Q

94

1Q

95

1Q

96

1Q

97

1Q

98

1Q

99

1Q

00

1Q

01

1Q

02

1Q

03

1Q

04

1Q

05

1Q

06

1Q

07

1Q

08

1Q

09

1Q

10

1Q

11

Yield spread (RHS)

Retail rental yield (LHS)

US 10yr Treasury (LHS)

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 16

in 2012. After all, our ECS team remains positive on Hong Kong’s job market and forecasts

3.2% unemployment rate by year-end, settling at this low level in 2012 (vs 3.5% in 2Q11).

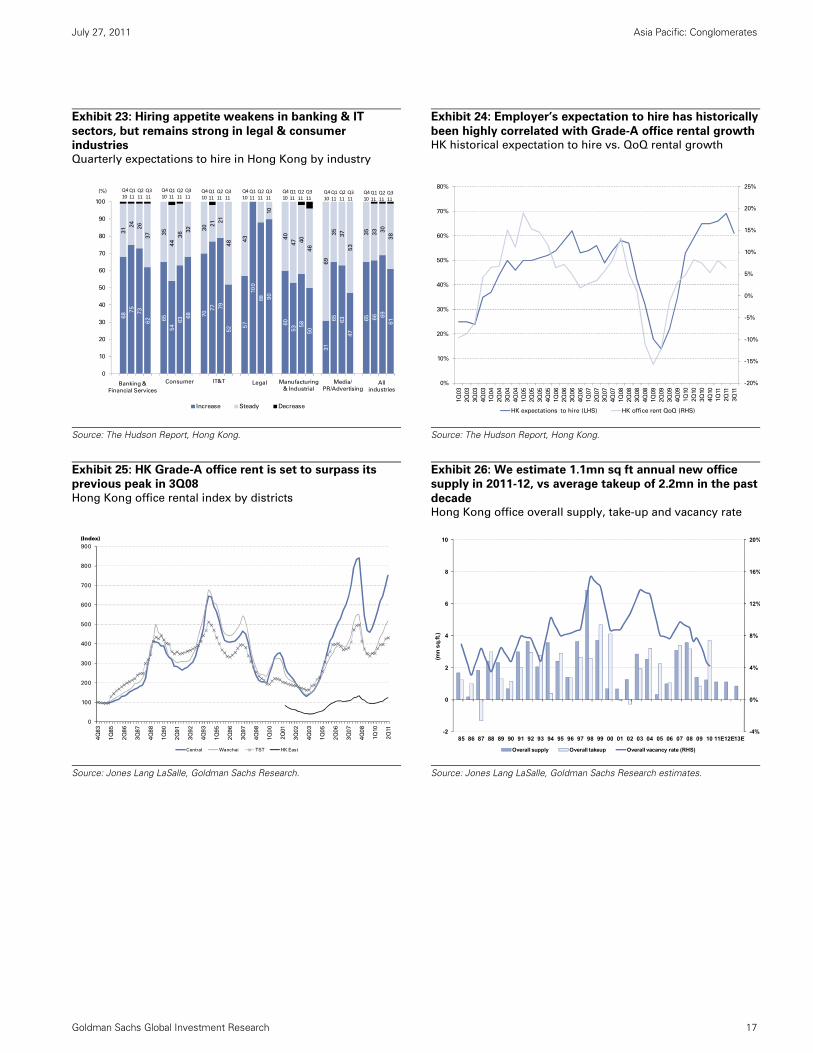

Hiring appetite weakens in banking & IT sectors, but remains strong in legal &

consumer industries – Among the different industries that Hudson has surveyed, the

employers in banking & IT industries have turned more cost cautious. The former was

ahead of the other sectors in starting to hire aggressively since 2Q09 and by now,

much of their post-downturn hiring has been completed. For the latter, some

consolidation is taking place in the IT vendor space causing the hiring managers to

turn more cautious in their expansion plans. On the other hand, the robust

consumption market has led to greater demand for sale and marketing roles in the

consumer and FMCG industries. Leading law firms are also actively looking for lawyers

with experience in corporate finance and M&A, given the large number of companies

seeking IPOs in Hong Kong. These trends should bode better for decentralized districts

in our view, e.g., Island East, Causeway Bay and Tsim Sha Tsui, where many PR and

consumer companies set up their offices.

Demand from smaller, newly set up corporates in Central – As hiring activities in large

investment banks starts to slow down, more of the office take-up in Central will come

from the newly set-up small to mid-sized companies (e.g., branches of PRC corporate

and hedge funds) who typically need less office space (i.e., 1,000-2,000 sq ft) and hence

can afford higher rents on a per square foot basis. At IFC Two, for example, headline

average spot rents of recent committed transactions are over HK$150psf, surpassing

its previous high of around HK$140 psf in 2Q08. This trend should continue, as more

overseas companies are setting up their offices in Hong Kong.

Decentralization trend to continue – Given the surge of Central’s office rent and the

widened rental gap between Central and other districts (Exhibit 28), more companies

(e.g., insurance, audit firms, bank office of investment banks) are seeking to relocate or

expand their office space in decentralized districts. Among all, HK Island and Kowloon

East are more popular locations for financial institutions, as the newly completed

buildings are of premium quality comparable with the Grade-A buildings in Central.

We estimate that around 40% of the tenants in Kowloon East are in the financial

industry this year, vs. 10-15% in 2008. In Island East, banks which have set up back-

offices there include DBS, Citibank and HSBC.

Tight office supply to last till 2013 – The average vacancy of Grade-A office in Hong

Kong remains low at 4.8% in the end of 1H2011. Based on the existing construction

schedule, there will only be 1.1mn sq ft of new office supply in both 2011 and 2012,

below the 2.2mn sq ft of annual average office take-up in the past two decades. By

assuming office demand sustains at its historical level, we estimate Hong Kong’s

overall office vacancy would drop to 2.2% by end-2012E, giving landlords greater

bargaining power to ask for steady rental increase. In medium term, we expect more

redevelopment of existing aged buildings, e.g., Hutchison House in Central,

Warwick/Somerset/Cornwall Houses in Island East.

Since the redevelopment of old buildings and construction of the new ones will take at

least 1-2 years to finish, we believe the key risks to our rental growth forecasts are not

supply but demand, i.e., deterioration in macro and job market condition. We present our

bear-case scenario and its impact on Wharf and Swire in the next section.

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 17

Exhibit 23: Hiring appetite weakens in banking & IT

sectors, but remains strong in legal & consumer

industries Quarterly expectations to hire in Hong Kong by industry

Exhibit 24: Employer’s expectation to hire has historically

been highly correlated with Grade-A office rental growthHK historical expectation to hire vs. QoQ rental growth

Source: The Hudson Report, Hong Kong.

Source: The Hudson Report, Hong Kong.

Exhibit 25: HK Grade-A office rent is set to surpass its

previous peak in 3Q08

Hong Kong office rental index by districts

Exhibit 26: We estimate 1.1mn sq ft annual new office

supply in 2011-12, vs average takeup of 2.2mn in the past

decade Hong Kong office overall supply, take-up and vacancy rate

Source: Jones Lang LaSalle, Goldman Sachs Research.

Source: Jones Lang LaSalle, Goldman Sachs Research estimates.

68

65 7

0

57 60

31

65

31

35 3

0

43 40

69

35

75

54

77

10

0

53

65 66

24

44

21

47

35

33

73

63

79

88

58 6

3 69

26

36

21

40

37 3

0

62 6

8

52

90

50

47

61

37

32

48

10

46 53

38

0

10

20

30

40

50

60

70

80

90

100

Increase Steady Decrease

IT&TConsumerBanking &

Financial Services

Legal Manufacturing

& Industrial

Media/

PR/AdvertisingAll

industries

Q410

Q111

Q211

Q311

(%) Q410

Q111

Q211

Q311

Q410

Q111

Q211

Q311

Q410

Q111

Q211

Q311

Q410

Q111

Q211

Q311

Q410

Q111

Q211

Q311

Q410

Q111

Q211

Q311

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1Q

03

2Q

03

3Q

03

4Q

03

1Q

04

2Q

04

3Q

04

4Q

04

1Q

05

2Q

05

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

HK expectations to hire (LHS) HK office rent QoQ (RHS)

0

100

200

300

400

500

600

700

800

900

4Q

83

1Q

85

2Q

86

3Q

87

4Q

88

1Q

90

2Q

91

3Q

92

4Q

93

1Q

95

2Q

96

3Q

97

4Q

98

1Q

00

2Q

01

3Q

02

4Q

03

1Q

05

2Q

06

3Q

07

4Q

08

1Q

10

2Q

11

(Index)

Central Wanchai TST HK East

-4%

0%

4%

8%

12%

16%

20%

-2

0

2

4

6

8

10

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11E12E13E

(mn

sq

.ft.)

Overall supply Overall takeup Overall vacancy rate (RHS)

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 18

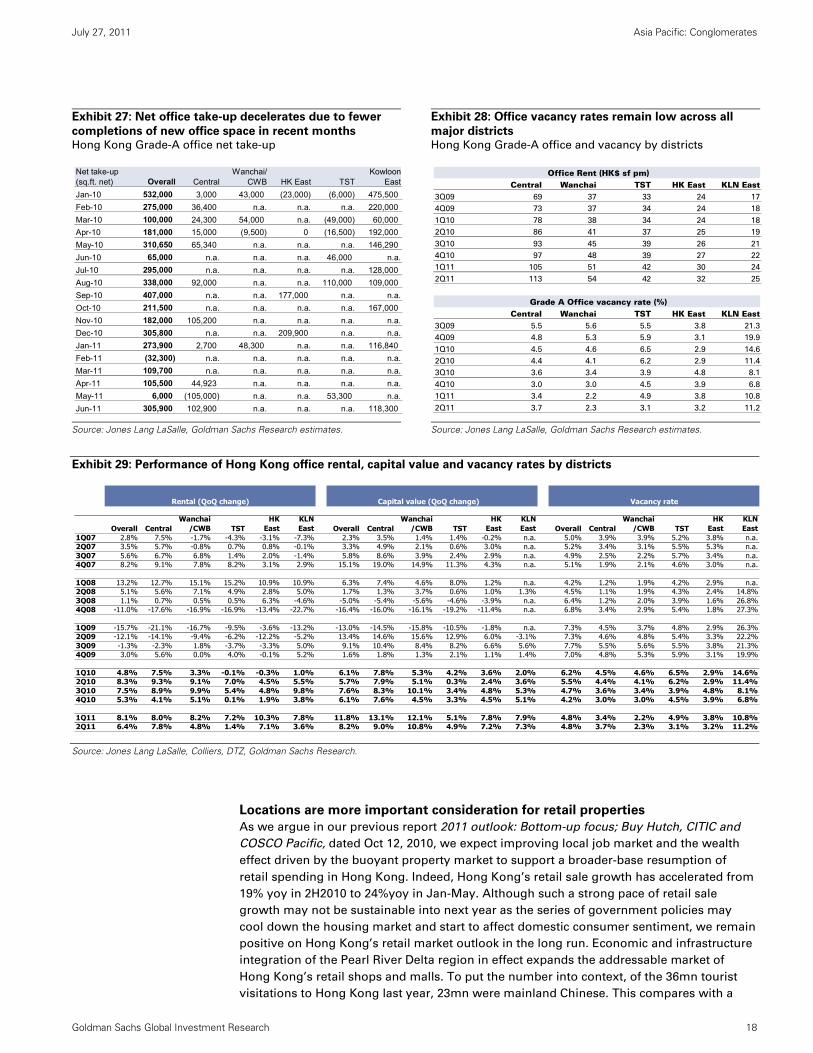

Exhibit 27: Net office take-up decelerates due to fewer

completions of new office space in recent months Hong Kong Grade-A office net take-up

Exhibit 28: Office vacancy rates remain low across all

major districts Hong Kong Grade-A office and vacancy by districts

Source: Jones Lang LaSalle, Goldman Sachs Research estimates.

Source: Jones Lang LaSalle, Goldman Sachs Research estimates.

Exhibit 29: Performance of Hong Kong office rental, capital value and vacancy rates by districts

Source: Jones Lang LaSalle, Colliers, DTZ, Goldman Sachs Research.

Locations are more important consideration for retail properties

As we argue in our previous report 2011 outlook: Bottom-up focus; Buy Hutch, CITIC and

COSCO Pacific, dated Oct 12, 2010, we expect improving local job market and the wealth

effect driven by the buoyant property market to support a broader-base resumption of

retail spending in Hong Kong. Indeed, Hong Kong’s retail sale growth has accelerated from

19% yoy in 2H2010 to 24%yoy in Jan-May. Although such a strong pace of retail sale

growth may not be sustainable into next year as the series of government policies may

cool down the housing market and start to affect domestic consumer sentiment, we remain

positive on Hong Kong’s retail market outlook in the long run. Economic and infrastructure

integration of the Pearl River Delta region in effect expands the addressable market of

Hong Kong’s retail shops and malls. To put the number into context, of the 36mn tourist

visitations to Hong Kong last year, 23mn were mainland Chinese. This compares with a

Net take-up(sq.ft. net) Overall Central

Wanchai/ CWB HK East TST

Kowloon East

Jan-10 532,000 3,000 43,000 (23,000) (6,000) 475,500

Feb-10 275,000 36,400 n.a. n.a. n.a. 220,000

Mar-10 100,000 24,300 54,000 n.a. (49,000) 60,000

Apr-10 181,000 15,000 (9,500) 0 (16,500) 192,000

May-10 310,650 65,340 n.a. n.a. n.a. 146,290

Jun-10 65,000 n.a. n.a. n.a. 46,000 n.a.

Jul-10 295,000 n.a. n.a. n.a. n.a. 128,000

Aug-10 338,000 92,000 n.a. n.a. 110,000 109,000

Sep-10 407,000 n.a. n.a. 177,000 n.a. n.a.

Oct-10 211,500 n.a. n.a. n.a. n.a. 167,000

Nov-10 182,000 105,200 n.a. n.a. n.a. n.a.

Dec-10 305,800 n.a. n.a. 209,900 n.a. n.a.

Jan-11 273,900 2,700 48,300 n.a. n.a. 116,840

Feb-11 (32,300) n.a. n.a. n.a. n.a. n.a.

Mar-11 109,700 n.a. n.a. n.a. n.a. n.a.

Apr-11 105,500 44,923 n.a. n.a. n.a. n.a.

May-11 6,000 (105,000) n.a. n.a. 53,300 n.a.

Jun-11 305,900 102,900 n.a. n.a. n.a. 118,300

Central Wanchai TST HK East KLN East3Q09 69 37 33 24 17

4Q09 73 37 34 24 18

1Q10 78 38 34 24 18

2Q10 86 41 37 25 19

3Q10 93 45 39 26 21

4Q10 97 48 39 27 22

1Q11 105 51 42 30 24

2Q11 113 54 42 32 25

Central Wanchai TST HK East KLN East3Q09 5.5 5.6 5.5 3.8 21.3

4Q09 4.8 5.3 5.9 3.1 19.9

1Q10 4.5 4.6 6.5 2.9 14.6

2Q10 4.4 4.1 6.2 2.9 11.4

3Q10 3.6 3.4 3.9 4.8 8.1

4Q10 3.0 3.0 4.5 3.9 6.8

1Q11 3.4 2.2 4.9 3.8 10.8

2Q11 3.7 2.3 3.1 3.2 11.2

Grade A Office vacancy rate (%)

Office Rent (HK$ sf pm)

Overall CentralWanchai

/CWB TSTHK

EastKLNEast Overall Central

Wanchai/CWB TST

HKEast

KLNEast Overall Central

Wanchai/CWB TST

HKEast

KLNEast

1Q07 2.8% 7.5% -1.7% -4.3% -3.1% -7.3% 2.3% 3.5% 1.4% 1.4% -0.2% n.a. 5.0% 3.9% 3.9% 5.2% 3.8% n.a.2Q07 3.5% 5.7% -0.8% 0.7% 0.8% -0.1% 3.3% 4.9% 2.1% 0.6% 3.0% n.a. 5.2% 3.4% 3.1% 5.5% 5.3% n.a.3Q07 5.6% 6.7% 6.8% 1.4% 2.0% -1.4% 5.8% 8.6% 3.9% 2.4% 2.9% n.a. 4.9% 2.5% 2.2% 5.7% 3.4% n.a.4Q07 8.2% 9.1% 7.8% 8.2% 3.1% 2.9% 15.1% 19.0% 14.9% 11.3% 4.3% n.a. 5.1% 1.9% 2.1% 4.6% 3.0% n.a.

1Q08 13.2% 12.7% 15.1% 15.2% 10.9% 10.9% 6.3% 7.4% 4.6% 8.0% 1.2% n.a. 4.2% 1.2% 1.9% 4.2% 2.9% n.a.2Q08 5.1% 5.6% 7.1% 4.9% 2.8% 5.0% 1.7% 1.3% 3.7% 0.6% 1.0% 1.3% 4.5% 1.1% 1.9% 4.3% 2.4% 14.8%3Q08 1.1% 0.7% 0.5% 0.5% 6.3% -4.6% -5.0% -5.4% -5.6% -4.6% -3.9% n.a. 6.4% 1.2% 2.0% 3.9% 1.6% 26.8%4Q08 -11.0% -17.6% -16.9% -16.9% -13.4% -22.7% -16.4% -16.0% -16.1% -19.2% -11.4% n.a. 6.8% 3.4% 2.9% 5.4% 1.8% 27.3%

1Q09 -15.7% -21.1% -16.7% -9.5% -3.6% -13.2% -13.0% -14.5% -15.8% -10.5% -1.8% n.a. 7.3% 4.5% 3.7% 4.8% 2.9% 26.3%2Q09 -12.1% -14.1% -9.4% -6.2% -12.2% -5.2% 13.4% 14.6% 15.6% 12.9% 6.0% -3.1% 7.3% 4.6% 4.8% 5.4% 3.3% 22.2%3Q09 -1.3% -2.3% 1.8% -3.7% -3.3% 5.0% 9.1% 10.4% 8.4% 8.2% 6.6% 5.6% 7.7% 5.5% 5.6% 5.5% 3.8% 21.3%4Q09 3.0% 5.6% 0.0% 4.0% -0.1% 5.2% 1.6% 1.8% 1.3% 2.1% 1.1% 1.4% 7.0% 4.8% 5.3% 5.9% 3.1% 19.9%

1Q10 4.8% 7.5% 3.3% -0.1% -0.3% 1.0% 6.1% 7.8% 5.3% 4.2% 3.6% 2.0% 6.2% 4.5% 4.6% 6.5% 2.9% 14.6%2Q10 8.3% 9.3% 9.1% 7.0% 4.5% 5.5% 5.7% 7.9% 5.1% 0.3% 2.4% 3.6% 5.5% 4.4% 4.1% 6.2% 2.9% 11.4%3Q10 7.5% 8.9% 9.9% 5.4% 4.8% 9.8% 7.6% 8.3% 10.1% 3.4% 4.8% 5.3% 4.7% 3.6% 3.4% 3.9% 4.8% 8.1%4Q10 5.3% 4.1% 5.1% 0.1% 1.9% 3.8% 6.1% 7.6% 4.5% 3.3% 4.5% 5.1% 4.2% 3.0% 3.0% 4.5% 3.9% 6.8%

1Q11 8.1% 8.0% 8.2% 7.2% 10.3% 7.8% 11.8% 13.1% 12.1% 5.1% 7.8% 7.9% 4.8% 3.4% 2.2% 4.9% 3.8% 10.8%2Q11 6.4% 7.8% 4.8% 1.4% 7.1% 3.6% 8.2% 9.0% 10.8% 4.9% 7.2% 7.3% 4.8% 3.7% 2.3% 3.1% 3.2% 11.2%

Rental (QoQ change) Capital value (QoQ change) Vacancy rate

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 19

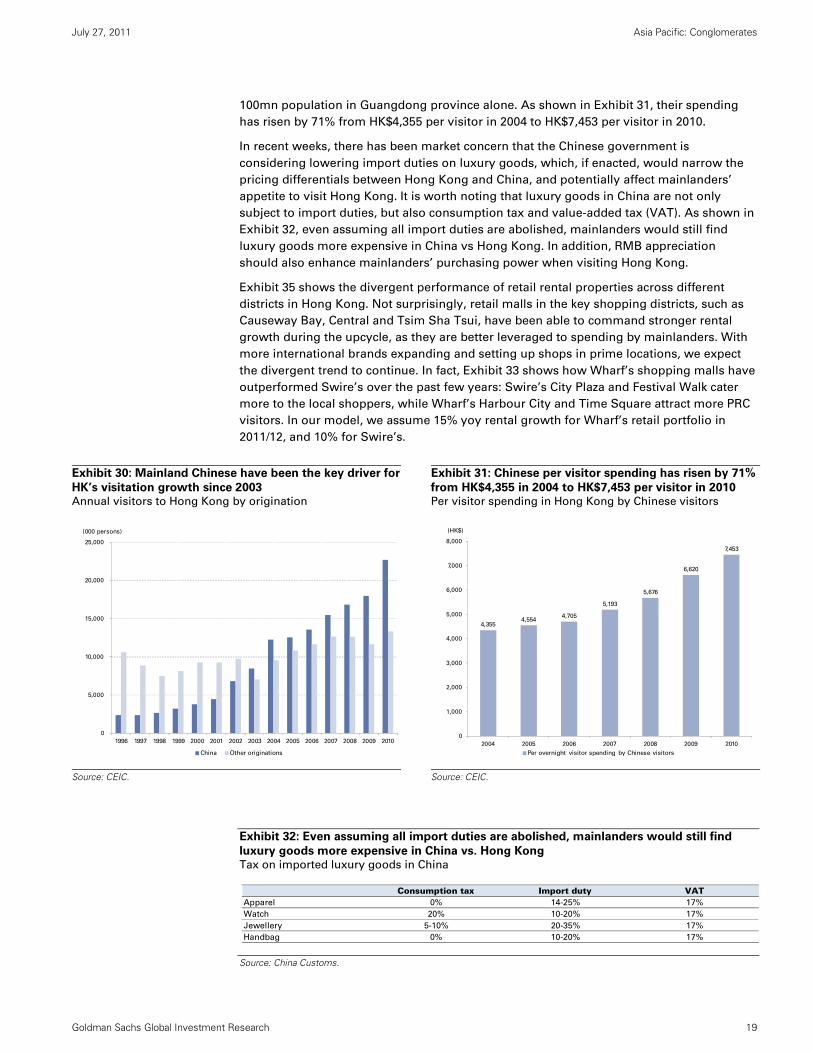

100mn population in Guangdong province alone. As shown in Exhibit 31, their spending

has risen by 71% from HK$4,355 per visitor in 2004 to HK$7,453 per visitor in 2010.

In recent weeks, there has been market concern that the Chinese government is

considering lowering import duties on luxury goods, which, if enacted, would narrow the

pricing differentials between Hong Kong and China, and potentially affect mainlanders’

appetite to visit Hong Kong. It is worth noting that luxury goods in China are not only

subject to import duties, but also consumption tax and value-added tax (VAT). As shown in

Exhibit 32, even assuming all import duties are abolished, mainlanders would still find

luxury goods more expensive in China vs Hong Kong. In addition, RMB appreciation

should also enhance mainlanders’ purchasing power when visiting Hong Kong.

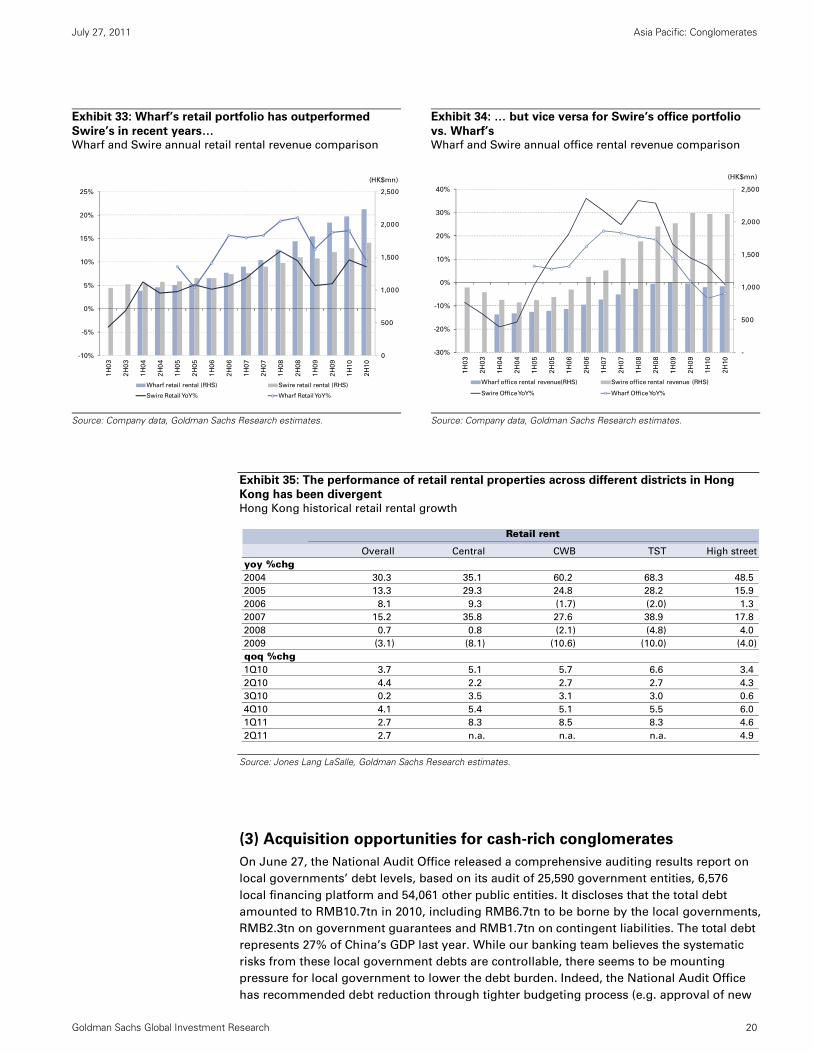

Exhibit 35 shows the divergent performance of retail rental properties across different

districts in Hong Kong. Not surprisingly, retail malls in the key shopping districts, such as

Causeway Bay, Central and Tsim Sha Tsui, have been able to command stronger rental

growth during the upcycle, as they are better leveraged to spending by mainlanders. With

more international brands expanding and setting up shops in prime locations, we expect

the divergent trend to continue. In fact, Exhibit 33 shows how Wharf’s shopping malls have

outperformed Swire’s over the past few years: Swire’s City Plaza and Festival Walk cater

more to the local shoppers, while Wharf’s Harbour City and Time Square attract more PRC

visitors. In our model, we assume 15% yoy rental growth for Wharf’s retail portfolio in

2011/12, and 10% for Swire’s.

Exhibit 30: Mainland Chinese have been the key driver for

HK’s visitation growth since 2003 Annual visitors to Hong Kong by origination

Exhibit 31: Chinese per visitor spending has risen by 71%

from HK$4,355 in 2004 to HK$7,453 per visitor in 2010 Per visitor spending in Hong Kong by Chinese visitors

Source: CEIC.

Source: CEIC.

Exhibit 32: Even assuming all import duties are abolished, mainlanders would still find

luxury goods more expensive in China vs. Hong Kong Tax on imported luxury goods in China

Source: China Customs.

0

5,000

10,000

15,000

20,000

25,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

China Other originations

(000 persons)

4,3554,554

4,705

5,193

5,676

6,620

7,453

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004 2005 2006 2007 2008 2009 2010

Per overnight visitor spending by Chinese visitors

(HK$)

Consumption tax Import duty VATApparel 0% 14-25% 17%

Watch 20% 10-20% 17%

Jewellery 5-10% 20-35% 17%

Handbag 0% 10-20% 17%

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 20

Exhibit 33: Wharf’s retail portfolio has outperformed

Swire’s in recent years… Wharf and Swire annual retail rental revenue comparison

Exhibit 34: … but vice versa for Swire’s office portfolio

vs. Wharf’s Wharf and Swire annual office rental revenue comparison

Source: Company data, Goldman Sachs Research estimates.

Source: Company data, Goldman Sachs Research estimates.

Exhibit 35: The performance of retail rental properties across different districts in Hong

Kong has been divergent

Hong Kong historical retail rental growth

Source: Jones Lang LaSalle, Goldman Sachs Research estimates.

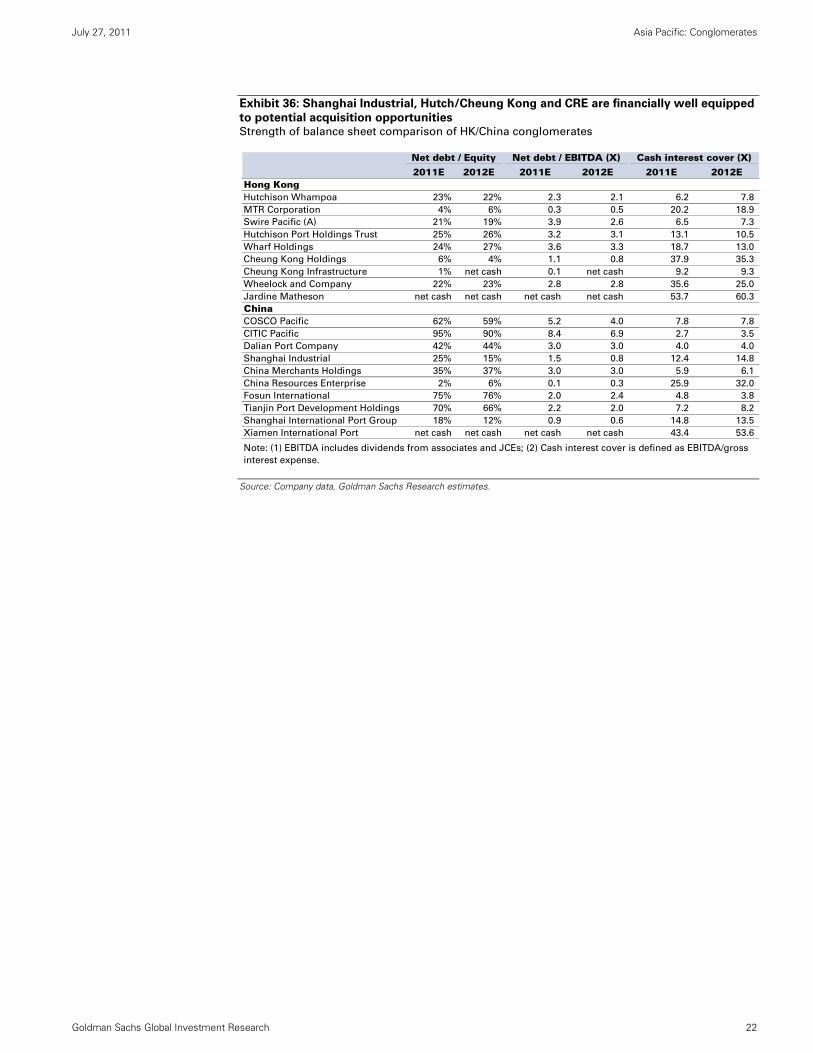

(3) Acquisition opportunities for cash-rich conglomerates

On June 27, the National Audit Office released a comprehensive auditing results report on

local governments’ debt levels, based on its audit of 25,590 government entities, 6,576

local financing platform and 54,061 other public entities. It discloses that the total debt

amounted to RMB10.7tn in 2010, including RMB6.7tn to be borne by the local governments,

RMB2.3tn on government guarantees and RMB1.7tn on contingent liabilities. The total debt

represents 27% of China’s GDP last year. While our banking team believes the systematic

risks from these local government debts are controllable, there seems to be mounting

pressure for local government to lower the debt burden. Indeed, the National Audit Office

has recommended debt reduction through tighter budgeting process (e.g. approval of new

0

500

1,000

1,500

2,000

2,500

-10%

-5%

0%

5%

10%

15%

20%

25%

1H

03

2H

03

1H

04

2H

04

1H

05

2H

05

1H

06

2H

06

1H

07

2H

07

1H

08

2H

08

1H

09

2H

09

1H

10

2H

10

Wharf retail rental (RHS) Swire retail rental (RHS)

Swire Retail YoY% Wharf Retail YoY%

(HK$mn)

-

500

1,000

1,500

2,000

2,500

-30%

-20%

-10%

0%

10%

20%

30%

40%

1H

03

2H

03

1H

04

2H

04

1H

05

2H

05

1H

06

2H

06

1H

07

2H

07

1H

08

2H

08

1H

09

2H

09

1H

10

2H

10

Wharf office rental revenue(RHS) Swire office rental revenue (RHS)

Swire Office YoY% Wharf Office YoY%

(HK$mn)

Retail rent

Overall Central CWB TST High street

yoy %chg2004 30.3 35.1 60.2 68.3 48.5

2005 13.3 29.3 24.8 28.2 15.9

2006 8.1 9.3 (1.7) (2.0) 1.3

2007 15.2 35.8 27.6 38.9 17.8

2008 0.7 0.8 (2.1) (4.8) 4.0

2009 (3.1) (8.1) (10.6) (10.0) (4.0)

qoq %chg1Q10 3.7 5.1 5.7 6.6 3.4

2Q10 4.4 2.2 2.7 2.7 4.3

3Q10 0.2 3.5 3.1 3.0 0.6

4Q10 4.1 5.4 5.1 5.5 6.0

1Q11 2.7 8.3 8.5 8.3 4.6

2Q11 2.7 n.a. n.a. n.a. 4.9

渐飞研究报告 - http://bg.panlv.net

July 27, 2011 Asia Pacific: Conglomerates

Goldman Sachs Global Investment Research 21

projects), more closely monitoring of fiscal disciplines and issuance of local government

debts.

In recent years, land sales have been an important source of revenue streams for municipal

governments. According to the Ministry of Land and Resources, China’s land sale revenue

amounted to RMB2.7tn in 2010, representing 37% of its tax-related revenue. In light of the

tightening policies implemented in the property sector since last year, developers have

generally turned more cautious on their landbank replenishment. In Shanghai and Beijing,

for example, land sales have fallen by 48% and 80% yoy in 1H2011 respectively. As local

governments find other ways to relieve their debt burden and lower their fiscal spending, it