“sushil finance wishes you and your family a very happy...

TRANSCRIPT

“Sushil Finance wishes you and your family a very Happy Diwali and a Prosperous New Year ahead”

2

Y/E Mar (Consol.)

Revenues(Rs. mn)

EBITDA(Rs. mn)

RPAT(Rs. mn)

NPM (%)

REPS*(Rs.)

PER(x)

P/S (x)

P/BV(x)

FY12 19,538 1,564 595 3.0 8.2 6.1 0.2 1.0FY13 21,305 1,737 695 3.3 9.6 5.2 0.2 0.8FY14E 23,015 1,866 781 3.4 10.7 4.7 0.2 0.7FY15E 25,406 2,210 882 3.5 12.1 4.1 0.1 0.6

SHARE HOLDING (%)Promoters 69.37FII 11.54FI/Bank 0.08Body Corporate 3.73Public & Others 15.28

Transport Corporation of India Ltd. Market Cap. 52 Week H/L CMP Target Price

Rs. 3,639 mn Rs. 90/44 Rs. 50 Rs. 73

STOCK DATA

Recommendation BUY

Reuters Code Bloomberg Code

TCIL.BO TRPC IN

BSE CodeNSE Symbol

532349TCI

Face Value Rs. 2

Shares Outstanding* 72.8 mn

Avg. Daily Volume (6m)

2,714 shares

Price Performance (%)1M 3M 6M4 4 (5)

200 Days EMA Rs. 55* On fully diluted equity Shares

This report based on Techno Funda Research and our View / Target Price has been derived accordingly. Please refer to the disclaimer on the last page.

Emerging trends in the Indian logistics space and shift towards organized logistics: The Indianlogistics space is 90% commanded by the unorganized segment. Over the past few years, thissector is experiencing a shift towards the organized segment. It is witnessing the emergence ofnew concepts in automated warehousing, third party logistics, express cargo and logistics parks.The industrial warehousing is expected to be driven by rising domestic and export‐import freightvolumes, investments in infrastructure, organized retail, focus towards manufacturing and theanticipated implementation of goods and services tax. Additionally, other aspects such as thirdparty logistics and logistics parks are also gaining significance in the Indian logistics space therebypromising relatively lower costs and smoother connectivity to multiple markets, going forward.Growing investments in infrastructure and rising attention towards logistics: The Indian logisticssector which is said to have a market size of nearly $230 bn, has been growing at 8‐10%. Accordingto various agencies, it is expected to grow at ~15%, once the capex cycle revives. However, the costof logistics in the country currently stands at roughly 13% of GDP as compared to the usual 8‐9%that prevails in the developed economies. The total consumption expenditure is expected to jumpthree‐folds to $3,600 bn by 2020 largely driven by food, housing and consumer durables. Webelieve, factors including shift from unorganized to organized, FDI in retail and e‐commerce,increasing industrial activities, growing exports and imports, planned expenditure towardsinfrastructure and rising demand for cost‐efficiencies and effective operations by the corporatespromises for a consistent evolution of the Indian logistics space.Investment Thesis: The company currently trades at 5.2x of FY13 EPS (Rs.9.6) and 4.1x of FY15 EPSof Rs.12.1. The debt‐equity ratio stands at comfortable 0.71x; we expect the company to registertop‐line of Rs.25,406 mn in FY15 with 3.5% of net margin that translates into an EPS of Rs.12.1 asagainst Rs.9.6 in FY13. We believe, the current valuations provide a decent margin of safety and thecurrent investments promises robust growth going forward, thereby, presenting a lucrativeinvestment opportunity at these levels. In addition, the company has never missed out on dividendpayout in last 13 years. For past two years, the company has increased its dividend payout to 50%.

November 01, 2013

3

Company Overview

Founded by Mr. Prabhu Dayal Agarwal in Kolkata during 1958, Transport Corporation of India Ltd. (TCIL) has now evolved into a leadingmulti‐modal (road, rail, air, sea) integrated supply‐chain and logistics solutions provider in the global cargo transportation. With continuousand strategic diversification in value added and new areas of logistics, customer centric‐approach and extensive infrastructure, TCILdeveloped an expertise over these five decades. The company now through its more than 1,400 branches operates with a fleet of 7,000vehicles, 9.75 mn sq.ft. of warehousing space and a skilled work force of 6,500 with 20,000 outsourced positions while covering over 17,000positions in the country. Moreover, the company has got a strong distribution network provides access to large and growing aftermarket.

The other group companies include TCI Industries and TCI Developers which got demerged and listed during the course of time. The groupwhich achieved a turnover of Rs.10,000 mn in 2006 doubled the turnover over the next five years and reaching a top‐line mark of Rs.22,000mn in 2012.

TCIL reports it’s revenues under five business segments namely ‐ TCI Seaways, TCI Freight, TCI Supply Chain Solutions, TCI XPS and TCIGlobal. The key management team which is headed by the Chairman, Mr. S.M. Datta is as follows:

The group has got a couple of unlisted subsidiaries including Infinite Logistics Solutions Pvt. Ltd., TCI Distribution Centers Ltd. and TCI Properties (Pune) Ltd. besides several other associate companies.

November 01, 2013

Transport Corporation of India Ltd.

Vice Chairman & MD Mr. D.P. Agarwal CEO – TCI Seaways Mr. R.U. Singh

Managing Director Mr. Vineet Agarwal CEO – TCI Freight Mr. I.S. Sagar

Jt. Managing Director Mr. Chander Agarwal CEO – TCI SCS Mr. Jasjit Sethi

Group CFO Mr. A.K.Bansal CEO – TCI XPS Mr. P. C. Sharma

Company Secretary Mr. A.K.Bansal CEO – TCI Global Mr. P. K. Jain

4

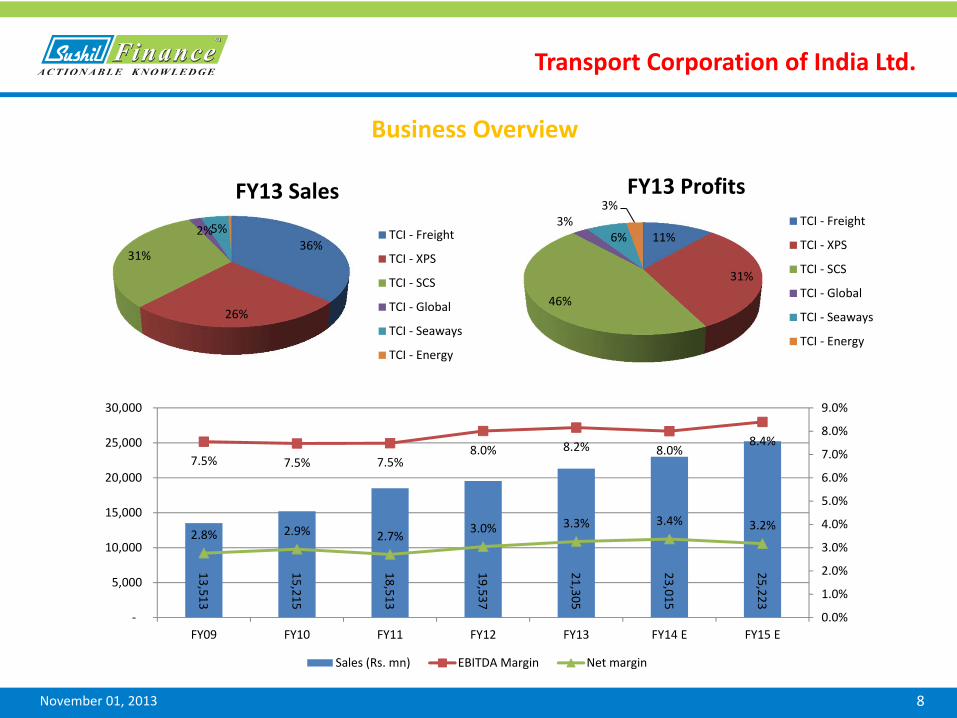

Business OverviewThe company has five major business divisions TCI Freight, TCI XPS, TCI Supply Chain Solutions, TCI Seaways and TCI Global Logistics.

TCI Freight: TCI Freight, the largest division of the group is the country’s leading surface transport entity. It has an extensive andstrategically located branch network and trained work force. This segment of the industry is characterized as mature, highly fragmentedwith low barriers of entry and thereby, high competition and low margin. This division is fully equipped to provide total transport solutionsfor cargo of any dimension or product segment. It transports cargo on FTL (Full Truck Load)/ LTL(Less than truck load)/ Small Packages andconsignments/Over Dimensional Cargoes. It handles a fleet of 2,400 trucks and trailers (both owned and leased) providing freightmovement services. Apart from road, the division also provides rail transportation using bulk rakes, containers etc. TCI Freight through itsmulti‐modal solutions provides services linking north to south and east to west. The company has clients from across the industries thatinclude FMCG, electrical, engineering, pharmaceutical, chemicals, etc.

The segment of the industry has been growing at 5‐7% while the company’s business has been de‐growing moderately for the last twofiscals. For FY13, the division registered de‐growth of 1.0% y‐o‐y contributing Rs.7774.8 mn to the top‐line consisting ~40% of the overallrevenues with an EBITDA of Rs.232.7 mn. In recent years, the growth has been hampered on account of severe slowdown in the economyand constant rise in fuel cost.

TCI XPS: This segment across the industry is one of the fast growing and has high‐entry barriers with cost‐efficiency is the key factor. Thisdivision provides express door‐to‐door service for time‐sensitive and high value documents and parcels across 3,000 pick up and over13,000 delivery locations in India and other 207 countries. The company operates through dedicated XPS trucks and vendors. In order togain customer traction, the company provides several value‐added services such as diplomat delivery (i.e. non‐service location), holidayservice, freight on delivery and money‐back guarantee scheme. (contd. on next page)

Transport Corporation of India Ltd.

November 01, 2013

5

Business OverviewThis segment of the industry has been growing at 8‐12% and the company is managing to match the pace with the industry. During FY13,this business division registered a growth of 12.2% y‐o‐y to Rs.5,556.7 mn to the top‐line consisting 28% of the overall sales with an EBITDAof Rs.454.9 mn. Over the past few years, the demand for express cargo services has outgrown the traditional set‐ups, particularly in thecorporate sector.

TCI Supply Chain Solutions: This segment provides inbound/outbound logistics and supply chain solutions right from the conceptualizationto implementation. The services include supply‐chain design and re‐engineering, lead logistics, specialized logistics, warehousemanagement, yard management, information management and record management. It operates with a customized fleet of 1,046 trucksincluding 38 refrigerated trucks. Currently, auto sector contributes to 70% of the revenues from the segment though its services are beingoffered to retail, telecom, healthcare and chemical industries. The segment has esteemed and vast clientele that includes Maruti, GeneralMotors, Tata Motors, Hero, Bajaj, Hindustan Unilever, Samsung, Scoda and others.

This segment of the industry is poised to grow at 20‐25% over the next few years and the company cloaked in turnover of Rs.5,189.2 mnthat consisted nearly 26% of FY13 sales, with an EBITDA of Rs.600.1 mn during FY13.

TCI Global Logistics: TCI Global Logistics provides a single window solutions across all major South East Asian countries through a networkof international offices in the region besides having strategic presence in high growth and emerging markets in Asia, Brazil (Latin America)and Africa. The customized end‐to‐end services ranging from customs clearance, international in‐bound and out‐bound freight handlingboth, air and sea, primary and secondary warehousing and redistribution, third party logistics, multimodal (air, road and sea) services, overdimensional cargo movements, mining logistics and project cargo. These services have been segregated as ocean freight, air freight,express and courier, warehousing, transportation and supply chain management. This segment of the industry can be characterized asmature with medium entry barriers that usually grows at 10‐12% per annum. The current contribution from this segment is miniscule andnegligible.

Transport Corporation of India Ltd.

November 01, 2013

6

Business Overview

TCI Seaways: This division started as an independent sea cargo division in February 1995. The division is well equipped with 1200containers and four vessels namely TCI Arjun, TCI XPS, TCI Prabhu and TCI Surya (2500‐4500 DWT and total capacity of 15634 DWTcumulative capacities). This division provides services such as coastal services, ship chartering, international shipping and project cargo.The domestic services include costal shipping, agency service while the international services include break bulk, project cargo andcontainerized businesses. TCI Seaways caters to the coastal cargo requirements for transporting container and bulk cargo from ports onthe east coast to Port Blair in the Andaman and Nicobar Islands and further distribution within the islands. The cargo largely consists of avariety of products including cattle, perishables and general goods to the islands. It usually ferries back timber, wood products, and betelnuts to the mainland from the islands. Moreover, a substantial cargo relates to the defense equipment and movement of vehicles. Thesegment is considering diversification beyond the Port Blair sector and augmenting its existing fleet by adding another ship.

This segment of the industry is experiencing a growth phase in the country and has been growing at 10‐15%. During FY13, the segmentearned revenue of Rs.939.0 mn and an EBITDA of Rs.132.6 mn. This division contributed to nearly 5% of the FY13 revenues of the company.

Associate Company

The real estate arm of TCI Group has been created to look into the development of commercial properties of TCI. These properties will be developed into office complexes, residential buildings, etc. depending on the best use of the property. It is also undertaking development of large modern warehouses, logistics parks etc.

Transport Corporation of India Ltd.

November 01, 2013

7

Business OverviewJoint Ventures

The company also has a rail logistics joint‐venture called Infinite Logistics Solutions in consortium with Container Corporation of India (CCI)in which the company owns 51% stake while the remaining 49% is owned by CCI. The JV which integrates rail and road cargo movementestablishes synergy between two rail and road giants and provides end‐to‐end multi‐modal solutions with reduced turnaround timesignificantly for movement of goods. The total paid‐up equity capital is Rs.30 mn; during FY13, the JV registered a revenue of Rs.176.6 mnwith marginal profit.

The company also has an auto‐logistics JV in collaboration with Japanese company, Mitsui & Co. Ltd., Transystem International Ltd.(founded in 1999) in which the company holds 49% stake. The JV is the lead logistics partner for Toyota Kirloskar Motors Ltd. in India andprovides complete logistics solutions from inbound to outbound transportation across the world. For FY13, the JV company paid dividendon the paid‐up equity capital of Rs.80 mn.

Transport Corporation of India Ltd.

November 01, 2013

8

Business Overview

Transport Corporation of India Ltd.

November 01, 2013

36%

26%

31%

2%5%

FY13 Sales

TCI ‐ Freight

TCI ‐ XPS

TCI ‐ SCS

TCI ‐ Global

TCI ‐ Seaways

TCI ‐ Energy

13,513

15,215

18,513

19,537

21,305

23,015

25,223

7.5% 7.5% 7.5%8.0% 8.2% 8.0%

8.4%

2.8% 2.9% 2.7% 3.0% 3.3% 3.4% 3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

‐

5,000

10,000

15,000

20,000

25,000

30,000

FY09 FY10 FY11 FY12 FY13 FY14 E FY15 E

Sales (Rs. mn) EBITDA Margin Net margin

11%

31%

46%

3%6%

3%FY13 Profits

TCI ‐ Freight

TCI ‐ XPS

TCI ‐ SCS

TCI ‐ Global

TCI ‐ Seaways

TCI ‐ Energy

9

Industry OverviewIndia is emerging as one of the world’s leading consumer market with the expanding middle class and improving affordability. Reportedly,the total consumption expenditure is expected to more than triple from $991 bn in 2010 to $3,600 bn in 2020. Food, housing andconsumer durables coupled with transport and communications are expected to drive the growth in coming years while accounting fornearly two‐third of the aforesaid consumption expenditure. In order to cater to such growing market, the logistics sector is expected toplay a key role. The Indian logistics sector which is said to have a market size of nearly $230 bn and has been growing at 8‐10% p.a. overthe past few years and according to various agencies, it is expected to grow at ~15%, once the capex cycle revives. However, the cost oflogistics in the country currently stands at roughly 13% of GDP as compared to the usual 8‐9% that prevails in the developed economies.Since, the cost of logistics is a key factor in the overall cost of a product and service, manufacturers and service providers continuouslyhunts for efficient and effective logistics solutions which could make them more competitive in the global markets.

The anticipated growth in manufacturing industries is likely to further intensify the competition in this space which will require companiesto augment their supply chain mechanisms. Manufacturing companies may place greater focus on their production activities, with theresult that many of them may begin outsourcing the transportation and logistics processes to third parties. The Indian logistics sector isstill in the nascent stage and dominated by unorganized sector. The factors which have been assisting the growth of logistics industry in thecountry over the past few years includes rapid growth in industries such as automobile, pharmaceuticals, consumer goods and onlineretailing alongwith relaxation in FDI investments and evolving tax system. In addition, increasing competition and cost, rising importance ofoutsourcing, entry of foreign players have contributed substantially to the growth of this sector. All the major industries including aviation,mining, retail, automobile, pharmaceuticals and others have been investing substantially in improvising their logistics. All these factorshave resulted in a significant rise in the volume of freight traffic, which has resulted in opportunities in all features of logistics includingtransportation, warehousing, freight forwarding, express cargo delivery, container services, shipping services and others. Going forward, itis needless to mention that the logistics is likely to be one of the key determinants of the pace of future growth. Thus, logistics havebecome an area of focus and priority in the last few years.

India continued to hold the second ranking in the Agility1 Emerging Markets Logistics Index 2013 (which conveys the opportunities andpotential growth) on account of huge potential and increased market compatibility and an increase in foreign direct investment andimprovements in security levels .1 Agility is one of the leading providers of integrated logistics. It is a publicly traded company with $4.8 bn revenue and more than 22,000 employees in 500 offices across 100 countries.

Transport Corporation of India Ltd.

November 01, 2013

10

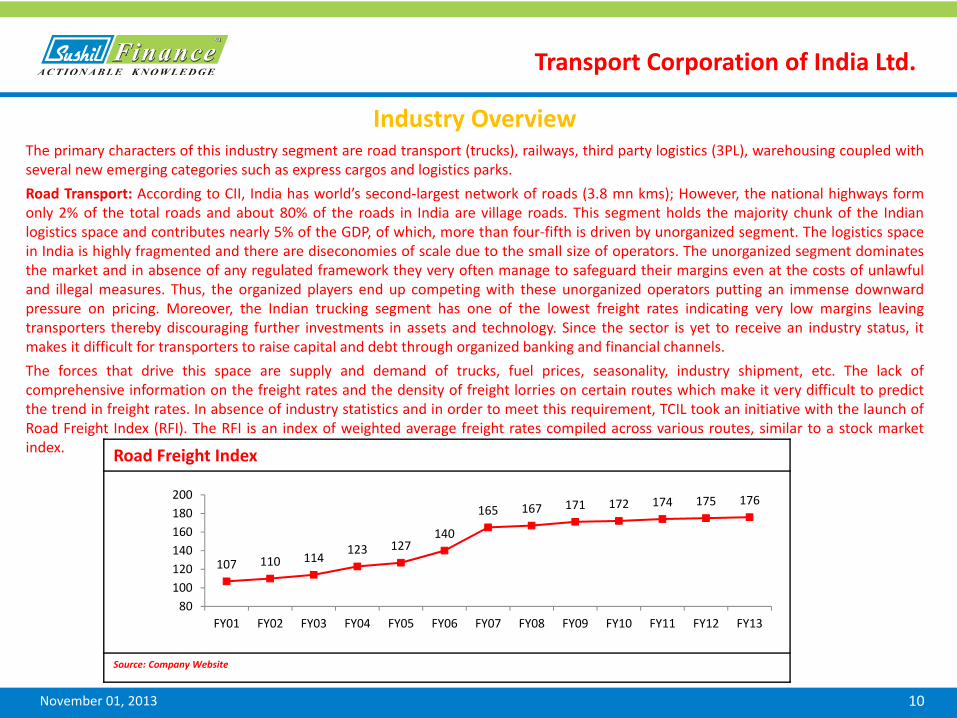

Industry OverviewThe primary characters of this industry segment are road transport (trucks), railways, third party logistics (3PL), warehousing coupled withseveral new emerging categories such as express cargos and logistics parks.Road Transport: According to CII, India has world’s second‐largest network of roads (3.8 mn kms); However, the national highways formonly 2% of the total roads and about 80% of the roads in India are village roads. This segment holds the majority chunk of the Indianlogistics space and contributes nearly 5% of the GDP, of which, more than four‐fifth is driven by unorganized segment. The logistics spacein India is highly fragmented and there are diseconomies of scale due to the small size of operators. The unorganized segment dominatesthe market and in absence of any regulated framework they very often manage to safeguard their margins even at the costs of unlawfuland illegal measures. Thus, the organized players end up competing with these unorganized operators putting an immense downwardpressure on pricing. Moreover, the Indian trucking segment has one of the lowest freight rates indicating very low margins leavingtransporters thereby discouraging further investments in assets and technology. Since the sector is yet to receive an industry status, itmakes it difficult for transporters to raise capital and debt through organized banking and financial channels.The forces that drive this space are supply and demand of trucks, fuel prices, seasonality, industry shipment, etc. The lack ofcomprehensive information on the freight rates and the density of freight lorries on certain routes which make it very difficult to predictthe trend in freight rates. In absence of industry statistics and in order to meet this requirement, TCIL took an initiative with the launch ofRoad Freight Index (RFI). The RFI is an index of weighted average freight rates compiled across various routes, similar to a stock marketindex.

Transport Corporation of India Ltd.

November 01, 2013

107 110 114123 127

140

165 167 171 172 174 175 176

80100120140160180200

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Road Freight Index

Source: Company Website

11

Industry OverviewRail Transportation: Railways is the second important link of industrial transportation in the Indian logistics space. It is one of the world'slargest railway networks comprising 115,000 kms of track over a route of 65,000 kms. It moves nearly one‐third of the total nationalfreight in terms of volumes, however, the trend is different in US and China where railways carry nearly half of the total freight volumes.The lag is primarily due to limited supporting railway infrastructure and absence of last‐mile reach. This raises the requirement forextension of rail‐network and multimodal transportation. Multi‐modal transportation in‐line with the developed countries should beencouraged where long distance transportation services may be provided by railways and the last‐mile‐connectivity may be provided byroads. However, victimized to the bureaucratic situation that prevails in the country, the concept has not been able to attain desiredresults. Going forward, we believe that the enhanced industrial activities coupled with emergence of new players and growing existingplayers in the organized segment will eventually bid for the requirement of multimodal transportation.

Third‐Party Logistics (3PL): It is an industrial activity of outsourcing logistics activities such as transportation, distribution and sometimesentire supply chain solutions to an outsourced or third party logistics service provider. Third party logistics providers typically specialize inintegrated operations, warehousing and transportation services that can be scaled and customized to customers' requirements based onmarket conditions and the demands and delivery service requirements for their products and materials. This concept has been growingsubstantially all over the world. Factors such as global sourcing, widening customer markets and growing competition amongmanufacturers have made the material movement complex giving enhanced attention to third party logistics players. According to thecompany, India’s 3PL market is estimated to reach revenues of Rs.190‐195 bn by FY15 and is expected to play a much important role in theyears to come.Warehousing: The anticipated growth in transportation and logistics market calls for aid from the other arms of the logistics space such astechnological implementations, network optimization and improved warehousing. In the recent times, the warehousing has continuouslybeen evolving from traditional godowns or stores to modern facilities with modern, efficient and fully automated set ups and multi‐rackand palletization infrastructure, etc. However, there are several key challenges such as high price sensitivity of customers and limitedinfrastructure connectivity constraints a service provider’s capability to offer world‐class services apart from other problems like capitalintensive and land requirements. Currently, nearly 90% of the Indian warehousing industry is dominated by the unorganized sector.Nevertheless, according to several industry reports this segment of the logistics industry is growing at above 30%.

Express Freight: The requirement of cost and time efficiency combined with expected growth in document shipments and high valueproducts have resulted into a high speed express segment using road and air network. This segment has been growing above 20%.

Transport Corporation of India Ltd.

November 01, 2013

12

Transport Corporation of India Ltd.

November 01, 2013

Industry Estimates that indicate growth going forwardAccording to various industry sources, the following facts showcases the anticipated upsurge in the trade and commerce in the country:

• According to Automotive Component Manufactures Association (ACMA), the Indian auto component industry’s turnover is reportedto be $41 bn in FY13 and is projected to touch $115 bn by FY21. The industry is expected to invest around Rs.70 bn ($1.2 bn) overthe next three years on new projects, as indicated by the rating agency ICRA.

• According to India Brand Equity Foundation (IBEF), the production of cement increased at 10% CAGR over FY07‐11. Going forward,the market size of the industry is expected to grow from 223 MTPA during FY12 to 550 MTPA by FY20.

• According to a report titled 'India Food Service Report 2013' by National Restaurant Association of India (NRAI), the Indian foodindustry currently stands at Rs.2,476,800 mn and is expected to touch Rs.4,080,400 mn by 2018, registering a growth of 11%.

• The Indian textile and apparel industry is expected to triple from $78 bn currently to $221 bn by 2020, according to Technopak'sTextile and Apparel Compendium 2012.

• Accounting for around 14‐15% of the gross domestic product, the Indian retail industry is estimated to be worth around $500 bncurrently and is expected to increase to $750‐850 bn by FY15, according to a report by Deloitte. The share of organized retail isexpected to increase from 5‐7% currently to 24% by 2020.

• India’s industrial energy consumption is expected to double by 2020. In this scenario, the country will need to mine 2 bn tonnes ofcoal by 2030 and transport 75% of mined coal. Further, around 30% of total transported coal will have to be imported through ports.

• Finished consumer goods, both imported and those produced in India, will have to be transported to the country’s middle‐classconsumers, which is expected to quadruple from 160 mn by 2030.

• The export‐import cargo at Indian ports is projected to increase from 890 MMT1 currently to 2,800 MMT by 2020.

• Agricultural output is expected to increase to 295 MMT by 2020.

• India Ratings & Research (Ind‐Ra) anticipates that growth in Indian steel sector will gain momentum FY14 onwards on the back ofgrowth in other economic segments; by 2030, India’s crude steel production is expected to increase by a factor of 4.

• The Government has planned infrastructure investment worth Rs.65,79,463 crores for twelfth 5 year plan (2012‐2017);1 MMT ‐million metric tonnes Source: Various Industry Reports

13

Growth DriversEmerging trends in the Indian logistics space and shift to organized logistics market: As mentioned earlier, the Indian logistics space iswitnessing a surge in the emergence of new concepts and improvisation, innovation and inspiration in some of the fastest emergingsegments including warehousing storage, third party logistics, express cargo and logistics parks. The demand for industrial warehousingspace is estimated to be growing at a CAGR of 6.8% over the past few years taking to nearly 476 mn sq. ft. in 2013. The share of modernwarehousing is anticipated to grow to 30% (178 mn sq. ft.) by 2015. In value terms, it is expected to reach beyond Rs.1,200 bn by FY15.This sharp growth is expected to be driven by rising domestic and export‐import freight volumes, strengthened investment ininfrastructure, organized retail, focus towards manufacturing and the implementation of goods and services tax. Moreover, 3PL is gainingimportance in the Indian logistics space and as mentioned earlier this business dynamic is expected to reach Rs.190‐195 bn by FY15.Furthermore, over hundred logistics parks spread over approximately 1.4 lakh sq. mt at an estimated cost over Rs.55,000 mn areexpected to be operational in close proximity to state capitals and some Tier II and Tier III cities promising relatively lower costs andbetter connectivity to multiple markets.

Growing investments in infrastructure and rising attention towards logistics: The logistics sector is gaining momentum as the country isgradually moving on to become a manufacturing hub. On the other front, the latest development in this space, e‐commerce has gainedimportance. The consumption patterns have changed thereby giving push to e‐tailing, which will eventually be a crucial milestone in thesector. The emergence of dedicated freight corridors across the country will further strengthen the logistics; in such a move, seven newcities have been finalized under the Delhi‐Mumbai Industrial Corridor project and plans for two new smart industrial cities are on thecards. This five lakh crore plus project will elevate the freight distribution to new levels and there will be industrial parks and logisticsbases with well‐developed infrastructures setting up. Moreover, FDI in retail will impact the economy as well as logistic sector as it willincrease productivity and ensure an efficient distribution network. Furthermore, with Goods and Services Tax (GST) the entire logisticsindustry can be assured of a unified tax structure and help in bringing down overall costs considerably. To conclude, factors including theplanned expenditure towards infrastructure, shift from unorganized to organized, FDI in retail and e‐commerce, increasing industrialactivities, growing exports and imports and rising demand for cost‐efficiencies and effective operations by the corporates promises for aconsistent evolution of the Indian logistics space.

Transport Corporation of India Ltd.

November 01, 2013

14

Investment ThesisThe past couple of years have been lacklustre for most of the industries on account of general economic slowdown driven by liquiditycrunch and subdued product demand that resulted into cost‐overruns, lower profitability and decisions relating postponement of capitalexpenditure. Similarly, Indian logistics space was also impacted and witnessed a tough and stagnant phase. Nevertheless, the companymanaged to continue with the gradual and steady growth. Over the past five years, TCIL ‘s business has grown at a CAGR of 11.3% andthe operating profits have grown at a 14.2%. During this period, the company incurred a capex of nearly Rs.5,000 mn of which majoritywas spent over enhancing the fleet of trucks and cars coupled with investments into hub centers and small warehouses. Approximately,one‐fourth of this total expenditure flowed towards wind‐power, ships and containers and others. These investments helped thecompany to reach a top‐line of Rs.21,305 mn in FY13 with nearly 8.2% EBITDA margin and 3.3% bottom‐line profitability. Going forward,the company has proposed a capital expenditure budget of Rs.2,300 mn (including the unspent funds of Rs.900 mn of previous fiscal.)

The logistics space in India is in its initial phase as almost 90% of this space is commanded by unorganized sector and is yet to achieve thestatus of an industry. The shift towards organized segment and need for efficiency by the corporates will play a major role in the growthphase. In addition, the economic reforms, implementation of goods and services tax, investments in infrastructure, wideninggeographical horizons for the distribution of products are likely to keep the logistics sector in higher trajectory. With this vision, thecompany is focusing on diversification into emerging businesses and growing the traditional segments. The current investments by thecompany will help in gaining the scalability and maintain its leading position amongst its peers, going forward. The company has alsoimproved its operating profitability through several cost‐cutting measures. The debt‐equity ratio stands at comfortable 0.71x; we expectthe company to register a top‐line of Rs.25,406 mn in FY15 with 3.5% of net margin that translates into an Earnings Per Share of Rs.12.1as against Rs.9.6 in FY13.

On the valuations front, the company is trading at substantial discount to its peers. At current price of Rs.50, the company trades at 5.2xconsidering FY13 EPS and 4.1x FY15 EPS of Rs.12.1. The company is trading at 0.6x its FY15E book value of Rs.80. Looking at our estimatesfor FY15, the company is trading at attractive valuations of 0.1x Price‐to‐sales and 2.8x EV/EBITDA. We believe, these valuations provide adecent margin of safety and the current investments promises strong growth going forward, thereby, presenting a lucrative investmentopportunity with a long‐term investment horizon. In addition, the company has never missed out on dividend payout in last 13 years. Forpast two years, the company has increased its dividend payout to 50%.

Transport Corporation of India Ltd.

November 01, 2013

15

Peer Comparison

Transport Corporation of India Ltd.

The above companies may not be directly comparable in terms of their business profiles but since they belongs to the Indian logistics space, we have considered them for the purpose of a broader sense of relative valuations

November 01, 2013

Gateway Distriparks Ltd. TTM FY13 FY12 FY11 FY10 FY09 FY08 FY07 CMP 116 Price Earning (P/E) 9.0 11.9 13.7 15.2 18.6 7.9 17.1 20.8 Mkt Cap 12,598 Price to Book Value ( P/BV) 1.4 1.7 2.2 1.9 2.0 0.9 1.8 2.0 EV 14,191 EV/EBIDTA 4.9 5.8 6.2 7.5 10.7 4.6 9.0 12.5 Sales 9,541 Market Cap/Sales 1.1 1.4 2.0 2.2 2.6 1.3 4.2 9.5 FV 10

Container Corporation Of India Ltd TTM FY13 FY12 FY11 FY10 FY09 FY08 FY07 CMP 753 Price Earning (P/E) 15.0 15.0 14.8 18.7 22.6 12.4 15.9 18.2 Mkt Cap 146,835 Price to Book Value ( P/BV) 3.4 1.4 2.2 3.2 3.9 2.5 1.8 2.4 EV 117,760 EV/EBIDTA 8.0 7.6 7.2 11.1 13.1 6.7 9.4 11.6 Sales 44,450 Market Cap/Sales 3.1 3.0 3.0 4.0 4.5 2.7 3.3 4.1 FV 10

Allcargo Logistics Ltd. TTM FY13 FY12 FY11 FY10 FY09 FY08 FY07 CMP 93 Price Earning (P/E) 7.5 8.7 7.8 NA 12.1 19.2 13.4 24.5 Mkt Cap 11,692 Price to Book Value ( P/BV) 0.7 0.9 1.2 NA 1.6 2.5 0.5 0.8 EV 17,623 EV/EBIDTA 4.2 4.9 4.2 NA 7.2 10.5 7.4 12.8 Sales 39,268 Market Cap/Sales 0.3 0.4 0.4 NA 0.7 1.2 0.6 1.1 FV 2

Transport Corporation of India Ltd. TTM FY13 FY12 FY11 FY10 FY09 FY08 FY07 CMP 50 Price Earning (P/E) 7.1 6.0 7.5 13.1 18.2 7.6 19.4 NA Mkt Cap 3,669 Price to Book Value ( P/BV) 1.0 1.0 1.2 2.3 2.3 0.9 2.4 NA EV 6,302 EV/EBIDTA 2.8 2.3 4.6 6.9 8.4 4.3 9.1 NA Sales 21,305 Market Cap/Sales 0.2 0.2 0.2 0.4 0.5 0.2 0.5 NA FV 2

Blue Dart Express Ltd. TTM FY13 FY12 FY11 FY10 FY09 FY08 FY07 CMP 2,795 Price Earning (P/E) 39.9 42.3 NA 30.7 29.3 27.4 13.0 25.0 Mkt Cap 66,242 Price to Book Value ( P/BV) 9.7 8.5 NA 5.7 5.1 3.7 2.6 5.5 EV 63,825 EV/EBIDTA 23.9 17.3 NA 18.6 17.0 14.6 7.0 13.0 Sales* 21,717 Market Cap/Sales 3.4 2.6 NA 2.5 2.4 1.8 1.0 2.2 FV 10

Gati Ltd. TTM FY13 FY12 FY11 FY10 FY09 FY08 FY07 CMP 29 Price Earning (P/E) NA 22.9 8.8 39.6 63.9 NA 33.0 34.4 Mkt Cap 2,481 Price to Book Value ( P/BV) NA 0.5 0.9 1.9 2.2 1.6 2.1 4.2 EV 5,775 EV/EBIDTA NA 6.0 4.1 9.4 11.1 18.9 13.4 16.9 Sales 12,730 Market Cap/Sales NA 0.2 0.3 0.4 0.6 0.5 0.8 1.2 FV 2 SOURCE: Capitaline

16

PROFIT & LOSS STATEMENT (Consol.) (Rs.mn) BALANCE SHEET STATEMENT (Consol.) (Rs.mn)

Source: Company, Sushil Finance Research Estimates

Y/E Mar. FY12 FY13 FY14E FY15E

Net Sales 19,537.5 21,305.3 23,041.7 25,406.5

Other operating expense 15,685.8 17,184.3 18,617.7 20,401.0

Staff cost 1,015.3 1,120.9 1,244.2 1,397.3

Other costs 1,271.9 1,262.7 1,313.4 1,397.3

Total Expenditure 17,973.1 19,567.9 21,175.3 23,195.7

EBITDA 1,564.4 1,737.4 1,866.4 2,210.3

Depreciation 415.7 464.0 464.7 564.2

Interest 350.0 336.3 324.8 429.6

Other Income 56.7 73.4 84.4 92.9

Exceptional ‐ ‐ ‐ ‐

PBT 855.4 1,010.5 1,165.0 1,317.8

Tax 262.0 315.2 384.4 434.9

RPAT 595.1 695.1 780.5 882.9

As on 31st Mar. FY12 FY13 FY14E FY15E

Share Capital 145.4 145.7 145.7 145.7

Reserves & Surplus 3,637.2 4,224.2 4,908.8 5,691.0

Net Worth 3,782.6 4,346.9 5,045.5 5,836.6

Total Loan funds 2,992.6 3,092.9 4,296.3 4,377.5

Deferred Tax 317.3 314.8 314.8 314.8

Trade Payables 873.5 877.6 879.2 906.7

Other Long Term Liabilities 0.2 7.0 7.0 7.0

Other Current Liabilities 514.4 561.3 620.6 680.0

Short Term Liabilities 227.5 415.7 517.2 566.7

Fixed Assets 4,237.1 4,224.7 5,372.9 5,952.0

Non‐current Investments 16.6 79.7 79.7 79.7

Trade Receivables 3,364.5 3,951.1 4,352.3 4,869.5

Cash & Bank Bal. 307.3 460.0 892.3 696.6

LT Loans & Advances 108.6 237.0 253.2 279.5

Inventory 19.6 21.5 21.5 21.5

ST Loans & Advances 664.9 662.3 714.3 787.6

Others 17.9 14.2 14.2 14.2

Total Assets 8,736.5 9,650.4 11,700.6 12,700.5

November 01, 2013

Transport Corporation of India Ltd.

17

CASH FLOW STATEMENT (Consol.) (Rs.mn) FINANCIAL RATIO STATEMENT (Consol.)Y/E Mar. FY12 FY13 FY14 FY15

Profit 595.1 695.1 780.5 882.9

Depreciation & Amortization 415.7 464.0 464.7 564.2

Chg. in Working Capital (24.2) (473.2) (307.4) (479.9)

Cash Flow from Operating 986.6 685.9 937.8 967.2

(Incr)/ Decr in LT Investments (1.6) (64.7) ‐ ‐

(Incr)/Decr In Fixed Assets (1,127.4) (451.6) (1,612.9) (1,143.3)

Cash Flow from Investing (1,128.8) (516.3) (1,612.9) (1,143.3)

(Decr)/Incr in Debt 334.5 100.4 1,203.4 81.2

(Decr)/Incr in Share Capital + 0.3 0.2 ‐ ‐

Dividend & Related Taxes (80.6) (91.4) (96.0) (100.8)

Cash Flow from Financing 253.2 10.3 1,107.4 (19.6)

Opening Cash 418.3 307.3 460.0 892.3

Cashflow during the year 111.0 179.9 432.3 (195.7)

Cash at the End of the Year 307.3 460.0 892.3 696.6

Y/E Mar. FY11 FY12 FY13E FY14E

Growth (%)Net Sales 5.5 9.0 8.2 10.3

EBITDA 12.9 11.1 7.4 18.4

Reported Net Profit 18.7 16.8 12.3 13.1

Profitability (%)EBIDTA Margin (%) 8.0 8.2 8.1 8.7

Net Profit Margin (%) 3.0 3.3 3.4 3.5

ROCE (%) 17.0 17.1 15.0 16.1

ROE (%) 15.7 15.9 15.4 15.1

Per Share Data (Rs.)EPS (Rs.) 8.2 9.6 10.7 12.1

CEPS (Rs.) 13.9 15.9 17.1 19.9

BVPS (Rs) 52.1 60.0 69.4 80.2

ValuationPER (x) 6.1 5.2 4.7 4.1

P/BV (x) 1.0 0.8 0.7 0.6

EV/EBITDA (x) 4.0 3.6 3.4 2.8

P/ Sales (x) 0.2 0.2 0.2 0.1

TurnoverDebtor Days 62 67 68 69

Creditor Days 20 18 17 16

Inventory Days ‐ ‐ ‐ ‐

Gearing RatioD/E 0.8 0.7 0.9 0.8

Source: Company, Sushil Finance Research Estimates

November 01, 2013

Transport Corporation of India Ltd.

18

Outlook & ValuationOver the past five years, TCIL’s topline has been growing at a CAGR of ~11.4% and the operating profits have grown at a CAGR of ~14.2%during the same period. Currently, in‐line with the industry, the company is going through challenging times on account of generaleconomic slowdown that has impacted the top‐line growth and profitability. However, the company has significant expansion plans whichwill benefit the company going forward. We expect several factors such as shift towards organized segment, investments ininfrastructure, anticipated economic reforms, implementation of goods and services tax, widening geographical horizons for thedistribution of products alongwith rising demand for cost‐efficiencies and effective operations by the corporates are likely to play a vitalrole in the development of Indian logistics space. Moreover, considering the company’s capex plans, comfortable debt levels, diversifiedbusiness portfolio and focus on high‐margin business of supply chain solutions and current valuations indicates a good investmentopportunity. At current price of `50, the company is trading at 4.1x its FY15 EPS of ` 12.1. By allocating a target multiple of 6.0x to itsFY15 EPS, we derive a target price of `73 for the stock.

Positives

Leading position in road transportStrong clientele relationshipRising focus on high margin businessesDiversified businessesSubstantial expansion plansComfortable valuationsStable profits and top‐line growthConsistent dividend

Negatives

Market largely dominated by unorganized playersIntensifying competitionEntry of new players in various segmentsLower bargaining power in freight business

November 01, 2013

Transport Corporation of India Ltd.

19

Stock Review Reports:These are Soft coverage’s on companies where Management access is difficult. Views and recommendation on such companies may not necessarily be based on managementmeeting but may be based on the publicly available information and/or attending Company AGMs. Hence Stock Reviews may be just one‐time coverage’s with an occasionalUpdate, wherever possible.

Disclaimer:This report is prepared for the exclusive use of Sushil Group clients only and should not be reproduced, re‐circulated, published in any media, website or otherwise, in anyform or manner, in part or as a whole, without the express consent in writing of Sushil Financial Services Private Limited. Any unauthorized use, disclosure or publicdissemination of information contained herein is prohibited. This report is to be used only by the original recipient to whom it is sent.

This is for private circulation only and the said document does not constitute an offer to buy or sell any securities mentioned herein. While utmost care has been taken inpreparing the above, we claim no responsibility for its accuracy. We shall not be liable for any direct or indirect losses arising from the use thereof and the investors arerequested to use the information contained herein at their own risk.

This report has been prepared for information purposes only and is not a solicitation, or an offer, to buy or sell any security. It does not purport to be a complete descriptionof the securities, markets or developments referred to in the material. The information, on which the report is based, has been obtained from sources, which we believe to bereliable, but we have not independently verified such information and we do not guarantee that it is accurate or complete. All expressions of opinion are subject to changewithout notice.

Sushil Financial Services Private Limited and its connected companies, and their respective directors, officers and employees (to be collectively known as SFSPL), may, fromtime to time, have a long or short position in the securities mentioned and may sell or buy such securities. SFSPL may act upon or make use of information contained hereinprior to the publication thereof.

ANALYSTSaurabh Jain| +91 22 4093 [email protected]

November 01, 2013

Transport Corporation of India Ltd.