jindal steel and power ltd - power your trade:...

TRANSCRIPT

Jindal Steel and Power Ltd

BUY

- 1 of 34 -

Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

ST

OC

K P

OIN

TE

R

Target Price ₹ 472 CMP ₹ 155 FY20E EV/EBITDA 4.0X

Index Details We believe that the steel industry is headed for a cyclical upturn

given that China has undertaken intiatives to cut excess capacities

citing environmental issues. Following this we have seen a rebound

in global steel prices. In India too the government measures to check

dumping have resulted in prices firming up. With prices set to rally

there is always the threat of imports increasing, especially flat

products. However given the fact that JSPL is primarily into long

products it should remain unaffected.

Post capex completion at Angul, we expect JSPL to near double its

revenues by FY20. This coupled with the fact that coal linkages with

Coal India have been firmed up for five years and the domestic iron

ore prices are quoting at lows, the steel business is expected to do

well. The power business is also expected to perform well given that

FSA & PPAs are in place. Further with the sale of its power asset

Tamnar I (1,000 MW) already inked the company should be able to

leverage its gearing to a certain extent.

We expect revenues to grow at a CAGR of 22.7% to Rs. 39,184 crores

while EBITDA is expected to grow at a faster clip of 27% CAGR to Rs.

9,615 crores by FY20. Net earnings are expected to turn the corner in

FY18 and should scale to Rs.1,954 crores by FY20. We initiate with a

BUY for a price target of Rs. 472 (target 7.0X FY20 EV/EBITDA)

representing an upside of 204.5% from the CMP of Rs.155 over the

next 21 months.

We are optimistic given that :

Completion of capex at Angul should enhance crude steelmaking

capacity to 8.9 million tonnes from 6 million tonnes in FY17. Steel

volumes are expected to grow at a CAGR of 21% to 8.4 million

tonnes in FY20. On the back of improving realisations, revenues

from the steel business are expected to grow at a CAGR of 25%

from Rs. 16,280 crores in FY17 to Rs. 31,574 crores by FY20.

Sensex 32,575

Nifty 10,114

Industry Steel & Power

Scrip Details Mkt Cap(₹ cr) 14,160

BVPS (₹) 328.4

O/s Shares (Cr) 91.5

Av Vol (Lacs) 13.9

52 Week H/L 62.6/158.3

Div Yield (%) 0

FVPS (₹) 2

Shareholding Pattern

Shareholders %

Promoters 61.9

Public 38.1

Total 100

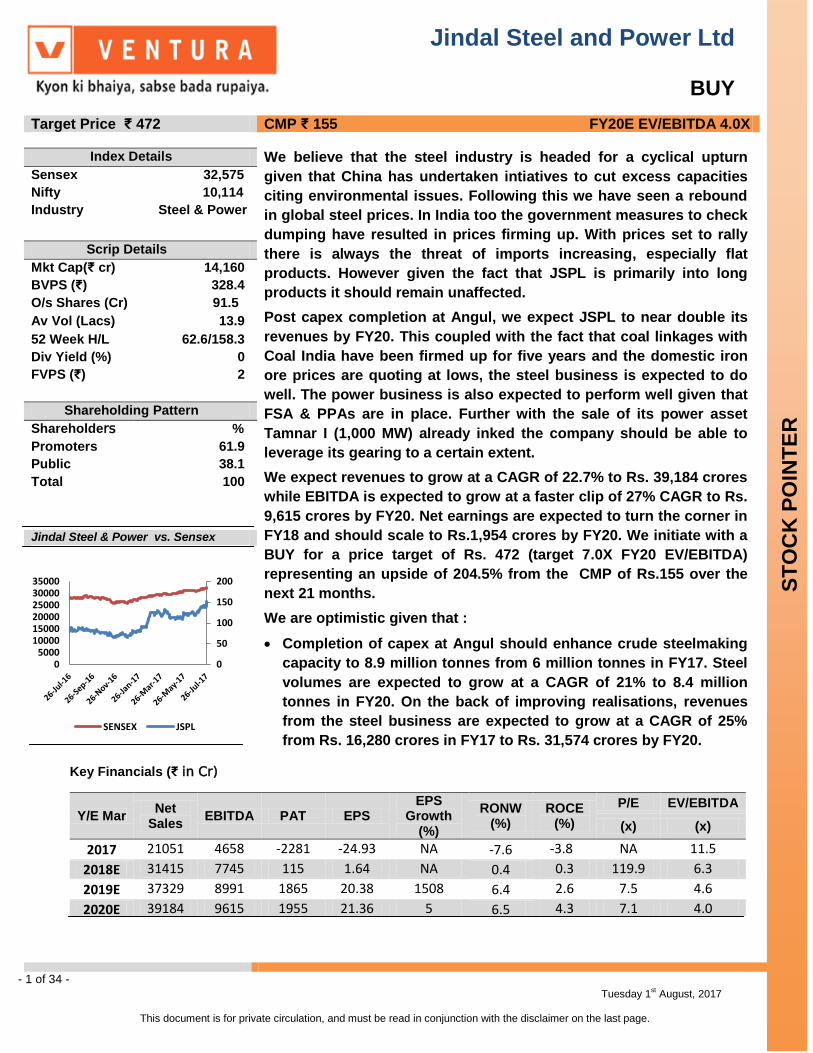

Jindal Steel & Power vs. Sensex

00000000000

0000000000000000000;/’;;.

0

50

100

150

200

0 5000

10000 15000 20000 25000 30000 35000

SENSEX JSPL

Key Financials (₹ in Cr)

Y/E Mar Net

Sales EBITDA PAT EPS

EPS Growth

(%)

RONW (%)

ROCE (%)

P/E EV/EBITDA

(x) (x)

2017 21051 4658 -2281 -24.93 NA -7.6 -3.8 NA 11.5

2018E 31415 7745 115 1.64 NA 0.4 0.3 119.9 6.3

2019E 37329 8991 1865 20.38 1508 6.4 2.6 7.5 4.6

2020E 39184 9615 1955 21.36 5 6.5 4.3 7.1 4.0

- 2 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

JSPL skipped its debt repayment schedule in FY16 as it was cash

strapped. To overcome this the company has inked an agreement to

sell its 1,000 MW power generating asset (Tamnar I) to JSW energy

for a consideration of Rs. 4,000 crores in FY19. This should help the

company deleverage. Further improving business fundamentals

should help lower debt gearing to 1.0X by FY20 from 1.3X reported

in FY17. This compares very favourably with that of peers JSW and

Tata Steel.

With signing of PPAs & FSAS (barring Tamnar I) visibility of

power business should improve. We expect overall PLF

utilizations to improve to 70% by FY20 from the current 35%. In

line with this revenues are expected to grow at a CAGR of 17% to

Rs. 5,063 crores by FY20 from the current Rs. 3120 crores.

- 3 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

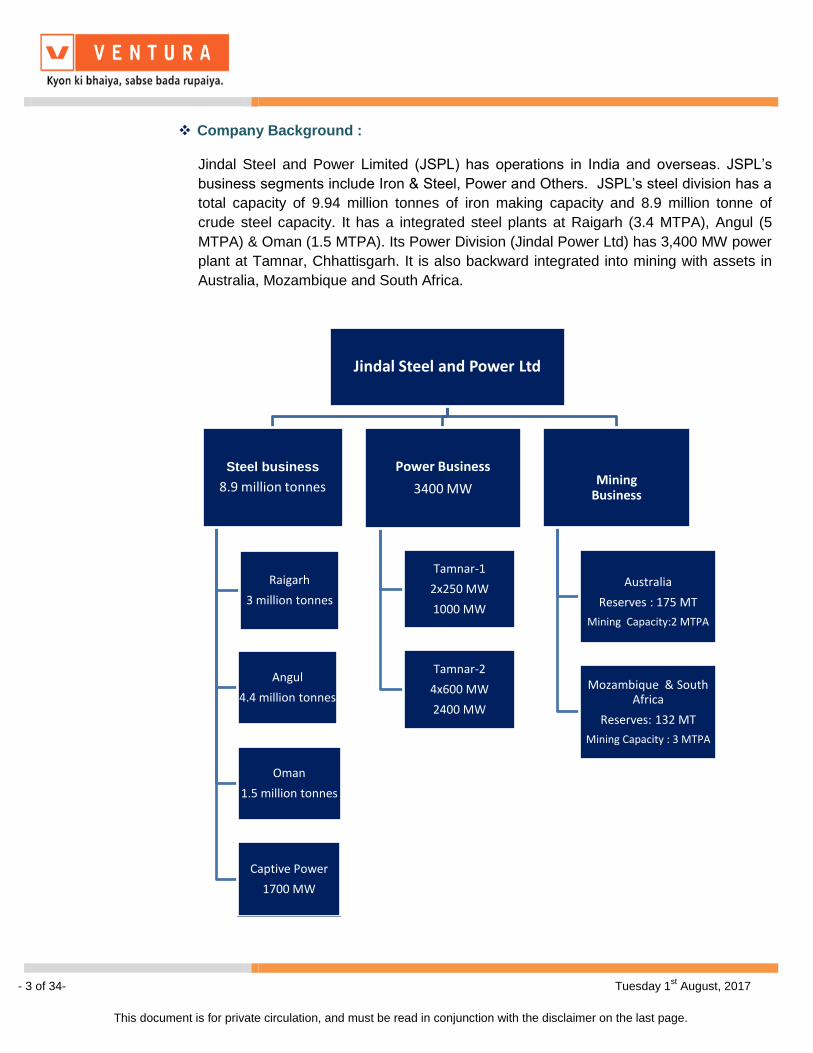

Company Background : Jindal Steel and Power Limited (JSPL) has operations in India and overseas. JSPL’s

business segments include Iron & Steel, Power and Others. JSPL’s steel division has a

total capacity of 9.94 million tonnes of iron making capacity and 8.9 million tonne of

crude steel capacity. It has a integrated steel plants at Raigarh (3.4 MTPA), Angul (5

MTPA) & Oman (1.5 MTPA). Its Power Division (Jindal Power Ltd) has 3,400 MW power

plant at Tamnar, Chhattisgarh. It is also backward integrated into mining with assets in

Australia, Mozambique and South Africa.

Jindal Steel and Power Ltd

Steel business

8.9 million tonnes

Raigarh

3 million tonnes

Angul

4.4 million tonnes

Oman

1.5 million tonnes

Captive Power

1700 MW

Power Business

3400 MW

Tamnar-1

2x250 MW

1000 MW

Tamnar-2

4x600 MW

2400 MW

Mining Business

Australia

Reserves : 175 MT

Mining Capacity:2 MTPA

Mozambique & South

Africa

Reserves: 132 MT

Mining Capacity : 3 MTPA

- 4 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

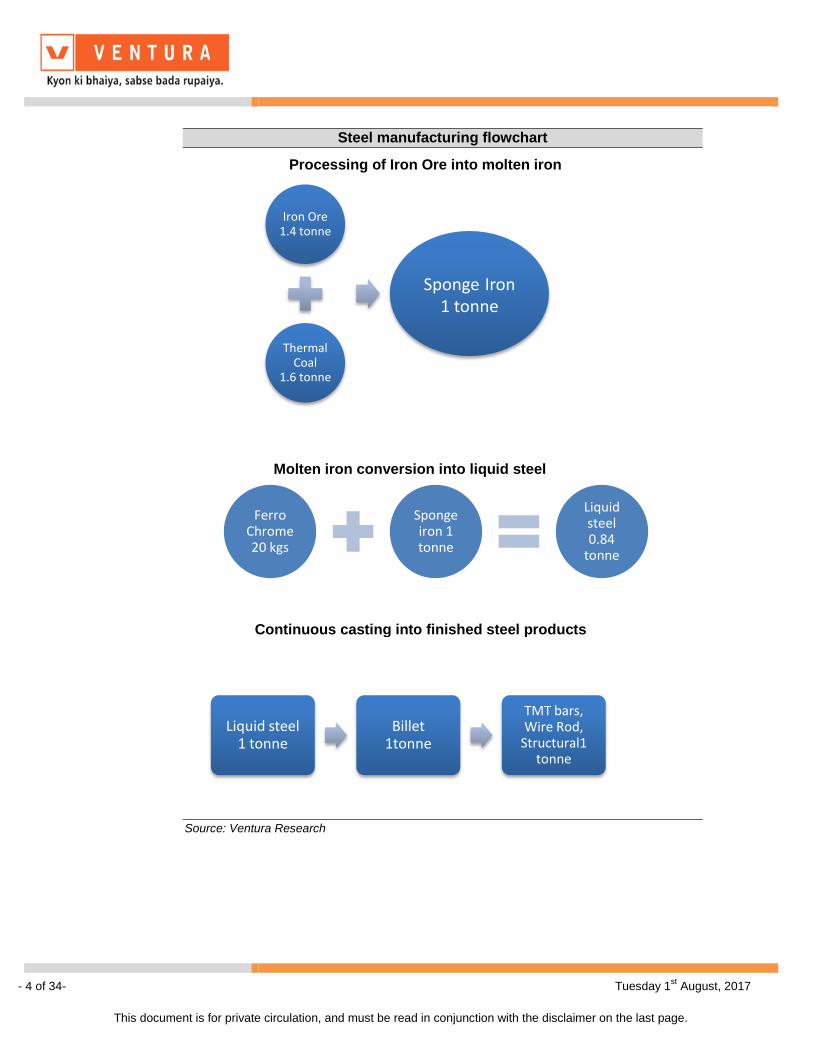

Steel manufacturing flowchart

Source: Ventura Research

Iron Ore 1.4 tonne

Thermal Coal

1.6 tonne

Sponge Iron 1 tonne

Ferro Chrome 20 kgs

Sponge iron 1 tonne

Liquid steel 0.84

tonne

Liquid steel 1 tonne

Billet 1tonne

TMT bars, Wire Rod,

Structural1 tonne

Processing of Iron Ore into molten iron

Molten iron conversion into liquid steel

Continuous casting into finished steel products

- 5 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Key Investment Highlights

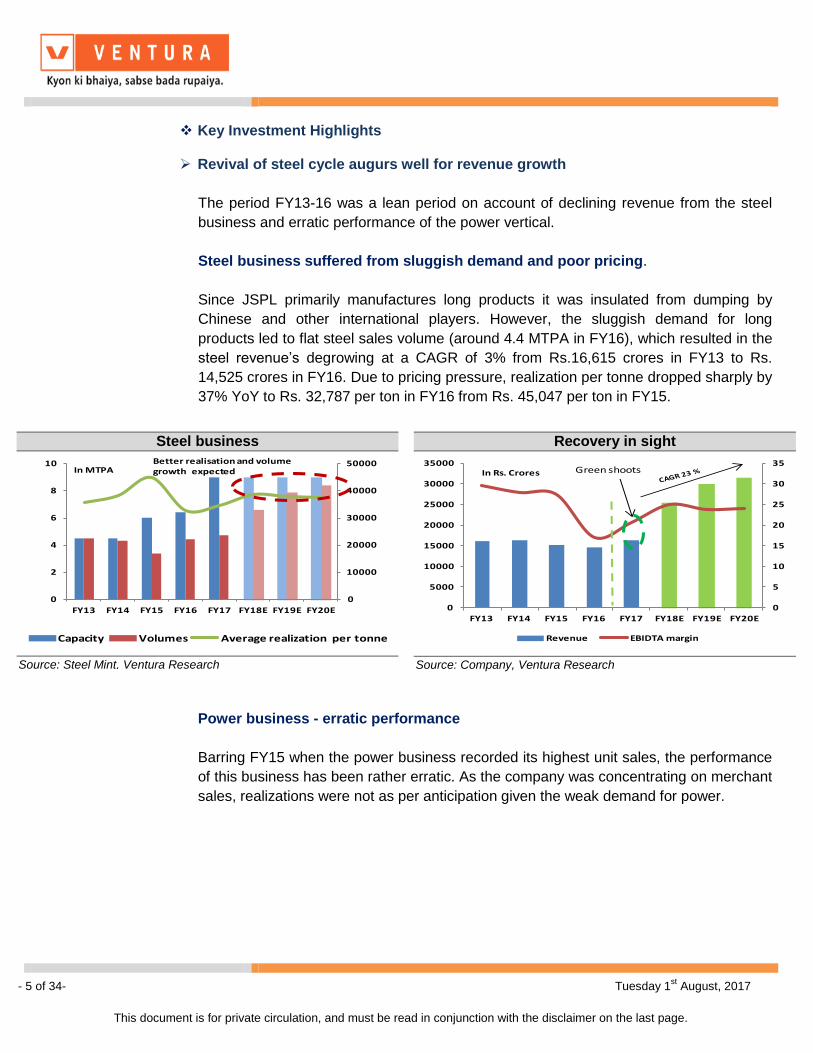

Revival of steel cycle augurs well for revenue growth

The period FY13-16 was a lean period on account of declining revenue from the steel

business and erratic performance of the power vertical.

Steel business suffered from sluggish demand and poor pricing.

Since JSPL primarily manufactures long products it was insulated from dumping by

Chinese and other international players. However, the sluggish demand for long

products led to flat steel sales volume (around 4.4 MTPA in FY16), which resulted in the

steel revenue’s degrowing at a CAGR of 3% from Rs.16,615 crores in FY13 to Rs.

14,525 crores in FY16. Due to pricing pressure, realization per tonne dropped sharply by

37% YoY to Rs. 32,787 per ton in FY16 from Rs. 45,047 per ton in FY15.

Power business - erratic performance

Barring FY15 when the power business recorded its highest unit sales, the performance

of this business has been rather erratic. As the company was concentrating on merchant

sales, realizations were not as per anticipation given the weak demand for power.

Recovery in sight

0

5

10

15

20

25

30

35

0

5000

10000

15000

20000

25000

30000

35000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Revenue EBIDTA margin

In Rs. Crores Green shoots

Source: Company, Ventura Research

Steel business

0

10000

20000

30000

40000

50000

0

2

4

6

8

10

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Capacity Volumes Average realization per tonne

In MTPABetter realisation and volume growth expected

Source: Steel Mint, Ventura Research

- 6 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

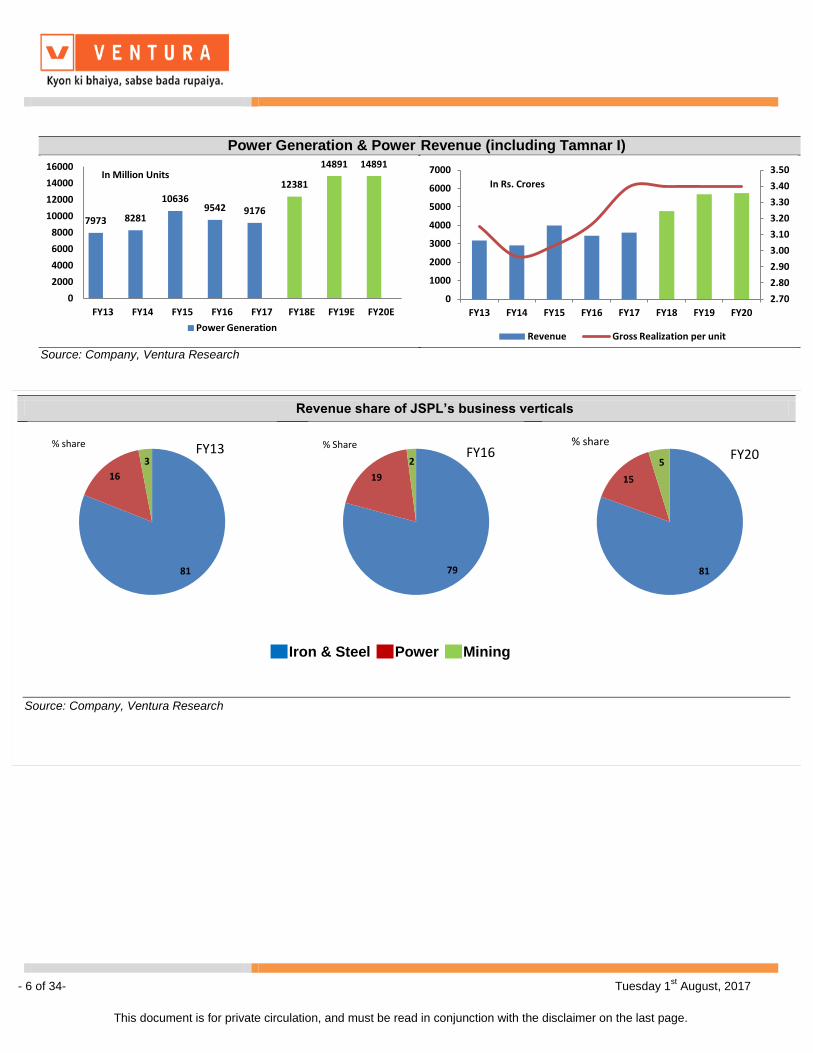

Revenue share of JSPL’s business verticals

Source: Company, Ventura Research

81

16

3

% share FY13

79

19

2

% Share FY16

81

15

5

% share FY20

Power Generation & Power

Source: Company, Ventura Research

7973 8281

10636 9542 9176

12381

14891 14891

0

2000

4000

6000

8000

10000

12000

14000

16000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Power Generation

In Million Units

Revenue (including Tamnar I)

2.70

2.80

2.90

3.00

3.10

3.20

3.30

3.40

3.50

0

1000

2000

3000

4000

5000

6000

7000

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Revenue Gross Realization per unit

In Rs. Crores

Iron & Steel Power Mining

- 7 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Steel Business - green shoots seen in FY17.

FY17 was the year of revival not only for the overall global steel cycle but also for the

Indian steel industry and JSPL. This was on account of -

1. Sharp cut backs by China in its installed capacity citing environmental concerns.

2. Anti-dumping measures undertaken by major steel importers viz. India, US & Europe on

Chinese dumping.

3. Decrease in domestic iron ore prices which have improved profitability.

4. Revival of Indian infrastructure given the measures taken by the Modi government.

5. Shrinking demand supply gap in the domestic market which has improved long term

visibility.

6. Completion of capex at the Angul plant which augurs well for JSPL’s steel revenue

growth. Long products in particular plates, rails & TMT bars which are the revenue

spinners of JSPL have strong drivers in place.

7. Existing operations at Raigarh to function at full throttle from FY19.

8. Oman facility to produce value added products (TMT bars) from FY18.

- 8 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

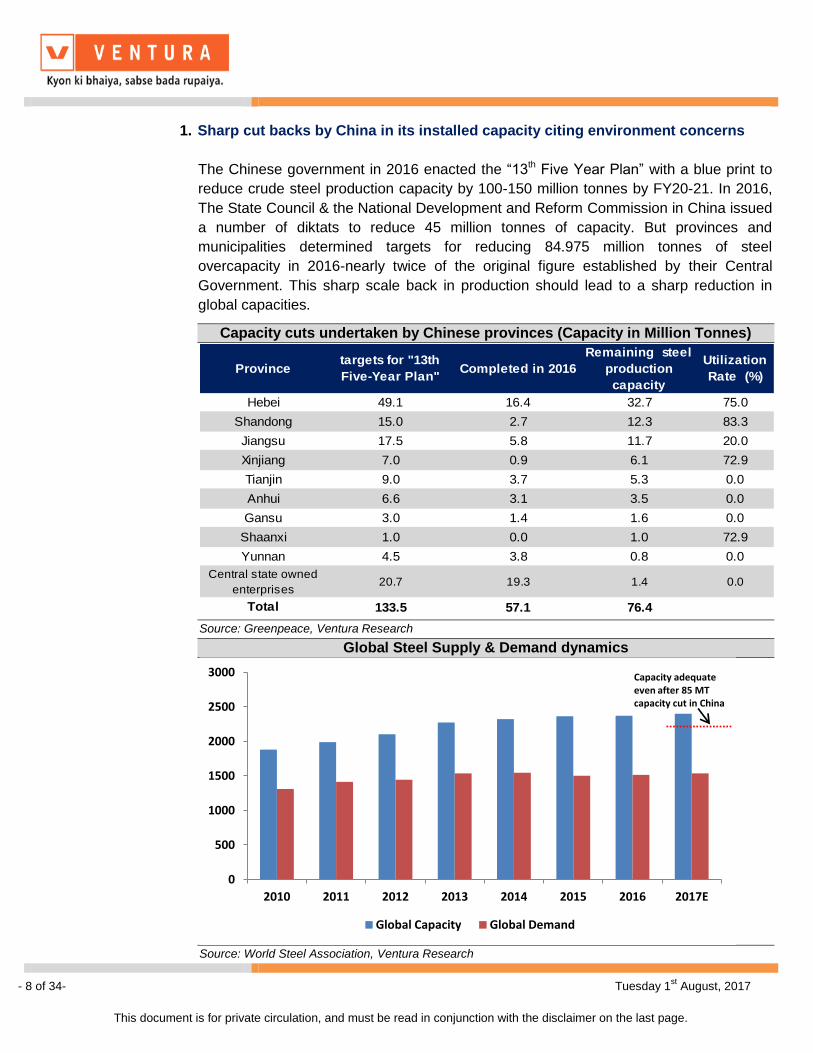

1. Sharp cut backs by China in its installed capacity citing environment concerns

The Chinese government in 2016 enacted the “13th Five Year Plan” with a blue print to

reduce crude steel production capacity by 100-150 million tonnes by FY20-21. In 2016,

The State Council & the National Development and Reform Commission in China issued

a number of diktats to reduce 45 million tonnes of capacity. But provinces and

municipalities determined targets for reducing 84.975 million tonnes of steel

overcapacity in 2016-nearly twice of the original figure established by their Central

Government. This sharp scale back in production should lead to a sharp reduction in

global capacities.

Capacity adequate even after capacity cut back in China

Capacity cuts undertaken by Chinese provinces (Capacity in Million Tonnes)

Provincetargets for "13th

Five-Year Plan"Completed in 2016

Remaining steel

production

capacity

Utilization

Rate (%)

Hebei 49.1 16.4 32.7 75.0

Shandong 15.0 2.7 12.3 83.3

Jiangsu 17.5 5.8 11.7 20.0

Xinjiang 7.0 0.9 6.1 72.9

Tianjin 9.0 3.7 5.3 0.0

Anhui 6.6 3.1 3.5 0.0

Gansu 3.0 1.4 1.6 0.0

Shaanxi 1.0 0.0 1.0 72.9

Yunnan 4.5 3.8 0.8 0.0

Central state owned

enterprises20.7 19.3 1.4 0.0

Total 133.5 57.1 76.4

Source: Greenpeace, Ventura Research

Global Steel Supply & Demand dynamics

Source: World Steel Association, Ventura Research

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014 2015 2016 2017E

Global Capacity Global Demand

Capacity adequate even after 85 MT capacity cut in China

- 9 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

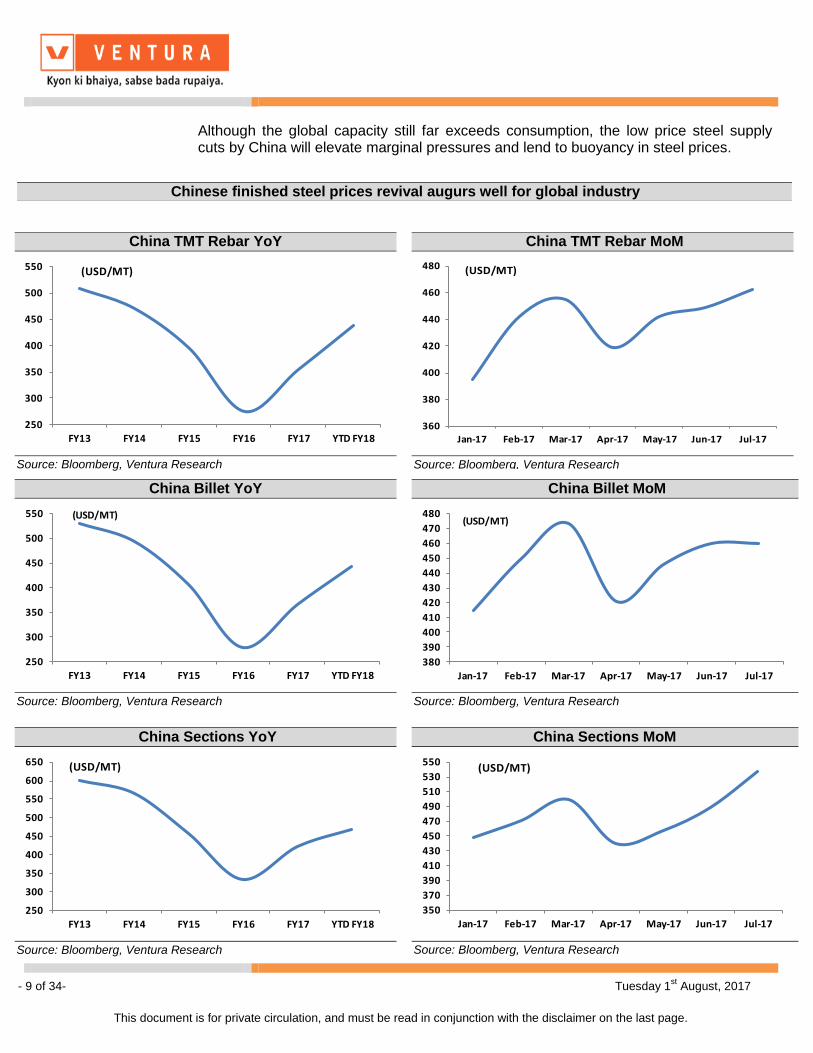

Although the global capacity still far exceeds consumption, the low price steel supply cuts by China will elevate marginal pressures and lend to buoyancy in steel prices.

China TMT Rebar YoY

250

300

350

400

450

500

550

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

China TMT Rebar MoM

360

380

400

420

440

460

480

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

China Billet YoY

250

300

350

400

450

500

550

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

China Billet MoM

380

390

400

410

420

430

440

450

460

470

480

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

China Sections YoY

250

300

350

400

450

500

550

600

650

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

China Sections MoM

350

370

390

410

430

450

470

490

510

530

550

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

Chinese finished steel prices revival augurs well for global industry

- 10 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

China HR Plate YoY

250

300

350

400

450

500

550

600

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

China HR Plate MoM

400

410

420

430

440

450

460

470

480

490

500

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

Hot Rolled Coil China YoY

250

300

350

400

450

500

550

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

Hot Rolled Coil China MoM

350

450

550

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

Cold Rolled Coil China YoY

350

400

450

500

550

600

650

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

Cold Rolled Coil China MoM

400

420

440

460

480

500

520

540

560

580

600

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

- 11 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Coking coal Australia YoY

60

80

100

120

140

160

180

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Steel Mint, Ventura Research

Coking coal Australia MoM

100

120

140

160

180

200

220

240

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Steel Mint, Ventura Research

Coking coal USA YoY

80

100

120

140

160

180

200

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Steel Mint, Ventura Research

Coking coal USA MoM

125

145

165

185

205

225

245

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Steel Mint, Ventura Research

- 12 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

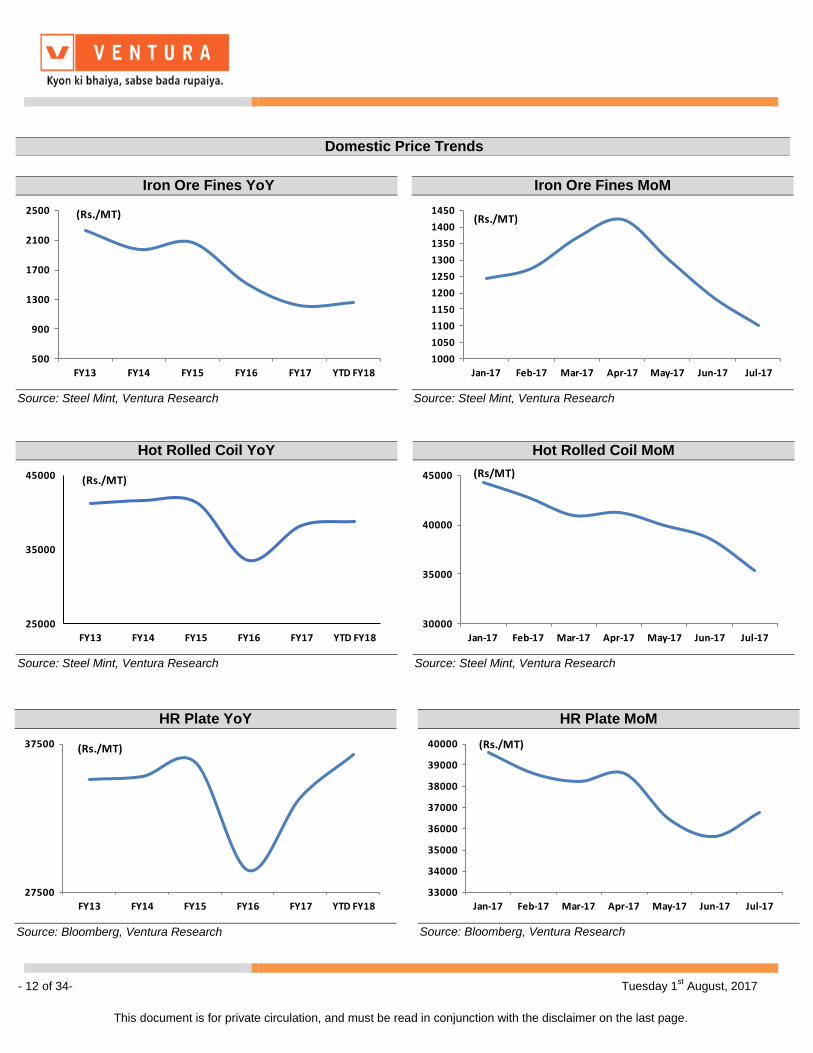

Domestic Price Trends

Iron Ore Fines YoY

500

900

1300

1700

2100

2500

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

Iron Ore Fines MoM

1000

1050

1100

1150

1200

1250

1300

1350

1400

1450

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

Hot Rolled Coil YoY

25000

35000

45000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

Hot Rolled Coil MoM

30000

35000

40000

45000

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs/MT)

Source: Steel Mint, Ventura Research

HR Plate YoY

27500

37500

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Bloomberg, Ventura Research

HR Plate MoM

33000

34000

35000

36000

37000

38000

39000

40000

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Bloomberg, Ventura Research

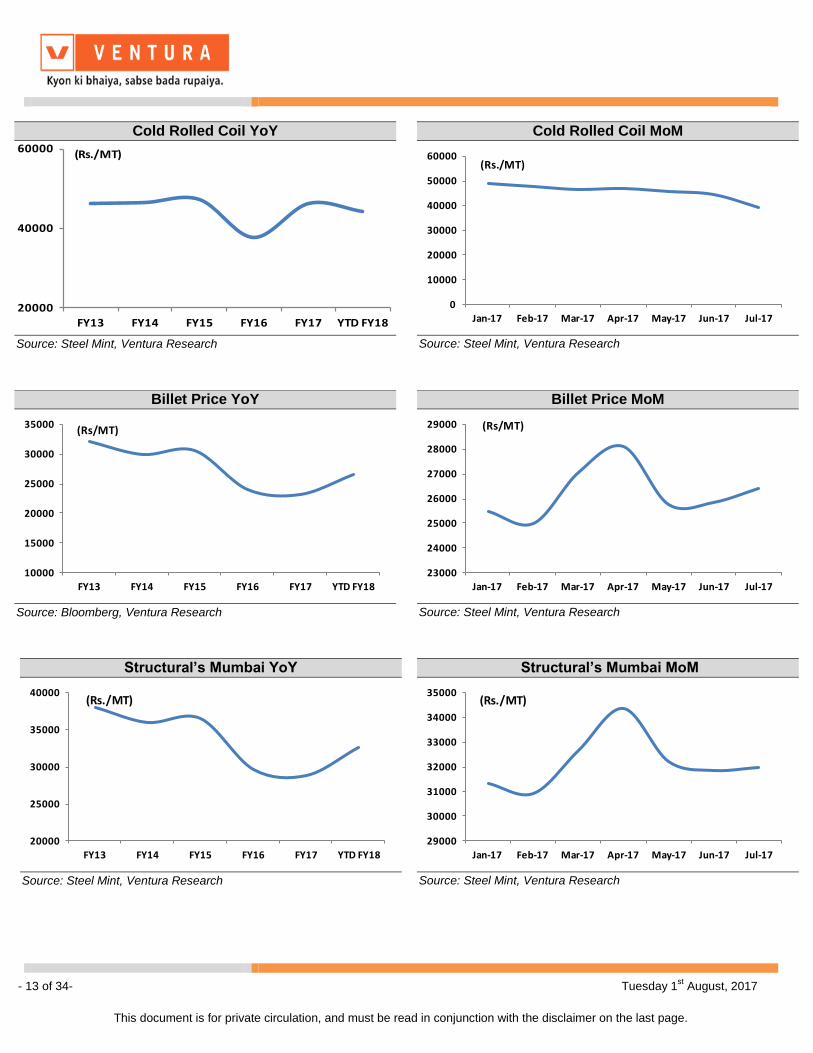

- 13 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Cold Rolled Coil YoY

20000

40000

60000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

Billet Price YoY

10000

15000

20000

25000

30000

35000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs/MT)

Source: Bloomberg, Ventura Research

Structural’s Mumbai YoY

20000

25000

30000

35000

40000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

Cold Rolled Coil MoM

0

10000

20000

30000

40000

50000

60000

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

Billet Price MoM

23000

24000

25000

26000

27000

28000

29000

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs/MT)

Source: Steel Mint, Ventura Research

Structural’s Mumbai MoM

29000

30000

31000

32000

33000

34000

35000

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

- 14 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

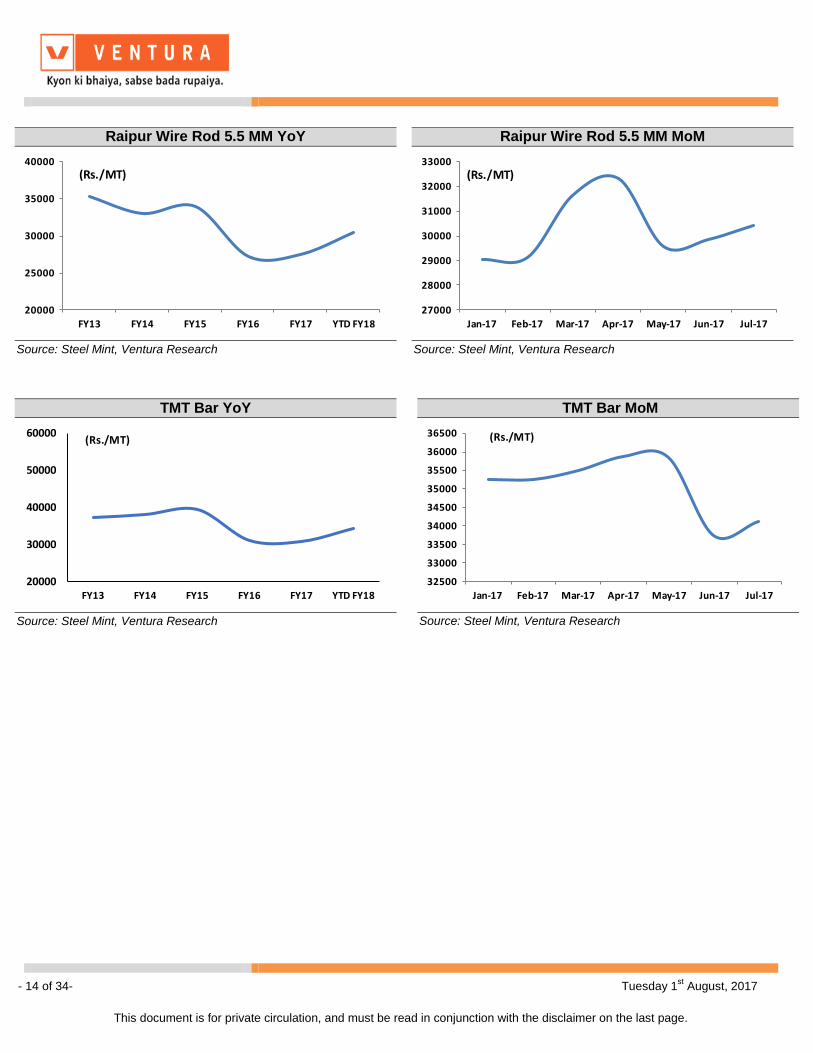

Raipur Wire Rod 5.5 MM YoY

20000

25000

30000

35000

40000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

TMT Bar YoY

20000

30000

40000

50000

60000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

Raipur Wire Rod 5.5 MM MoM

27000

28000

29000

30000

31000

32000

33000

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

TMT Bar MoM

32500

33000

33500

34000

34500

35000

35500

36000

36500

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

- 15 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

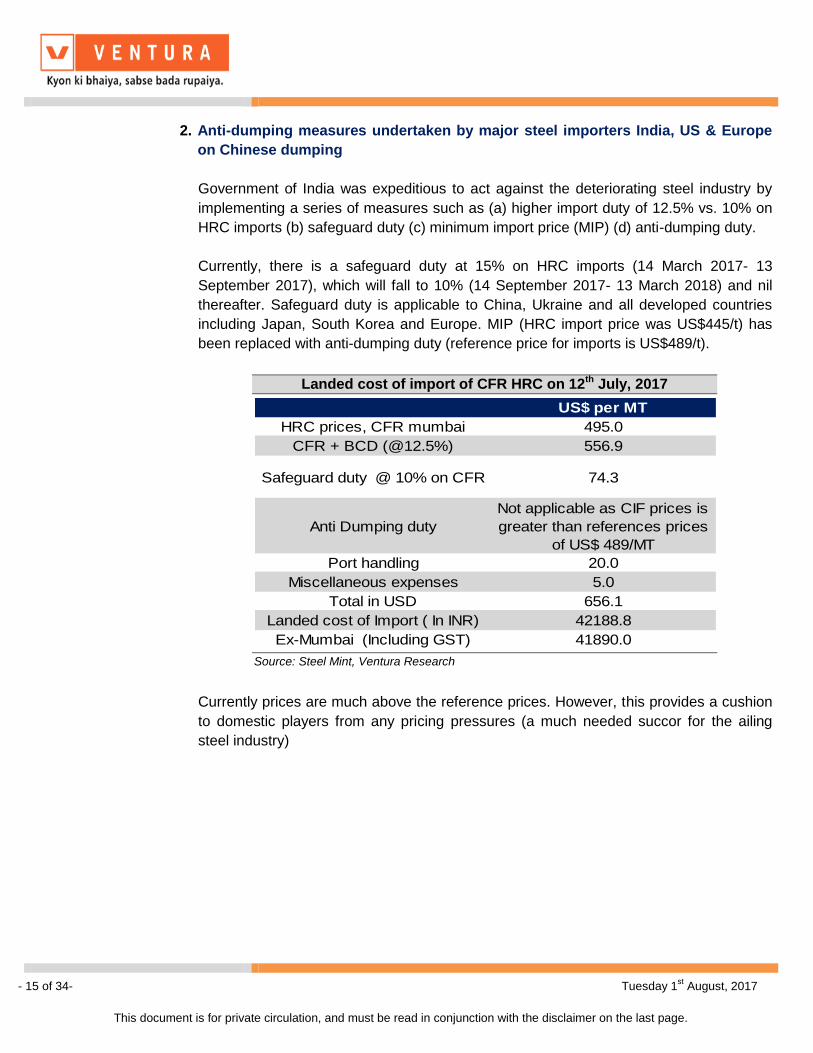

2. Anti-dumping measures undertaken by major steel importers India, US & Europe

on Chinese dumping

Government of India was expeditious to act against the deteriorating steel industry by

implementing a series of measures such as (a) higher import duty of 12.5% vs. 10% on

HRC imports (b) safeguard duty (c) minimum import price (MIP) (d) anti-dumping duty.

Currently, there is a safeguard duty at 15% on HRC imports (14 March 2017- 13

September 2017), which will fall to 10% (14 September 2017- 13 March 2018) and nil

thereafter. Safeguard duty is applicable to China, Ukraine and all developed countries

including Japan, South Korea and Europe. MIP (HRC import price was US$445/t) has

been replaced with anti-dumping duty (reference price for imports is US$489/t).

Currently prices are much above the reference prices. However, this provides a cushion

to domestic players from any pricing pressures (a much needed succor for the ailing

steel industry)

Landed cost of import of CFR HRC on 12th July, 2017

US$ per MT

HRC prices, CFR mumbai 495.0

CFR + BCD (@12.5%) 556.9

Safeguard duty @ 10% on CFR 74.3

Anti Dumping duty

Not applicable as CIF prices is

greater than references prices

of US$ 489/MT

Port handling 20.0

Miscellaneous expenses 5.0

Total in USD 656.1

Landed cost of Import ( In INR) 42188.8

Ex-Mumbai (Including GST) 41890.0

Source: Steel Mint, Ventura Research

- 16 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

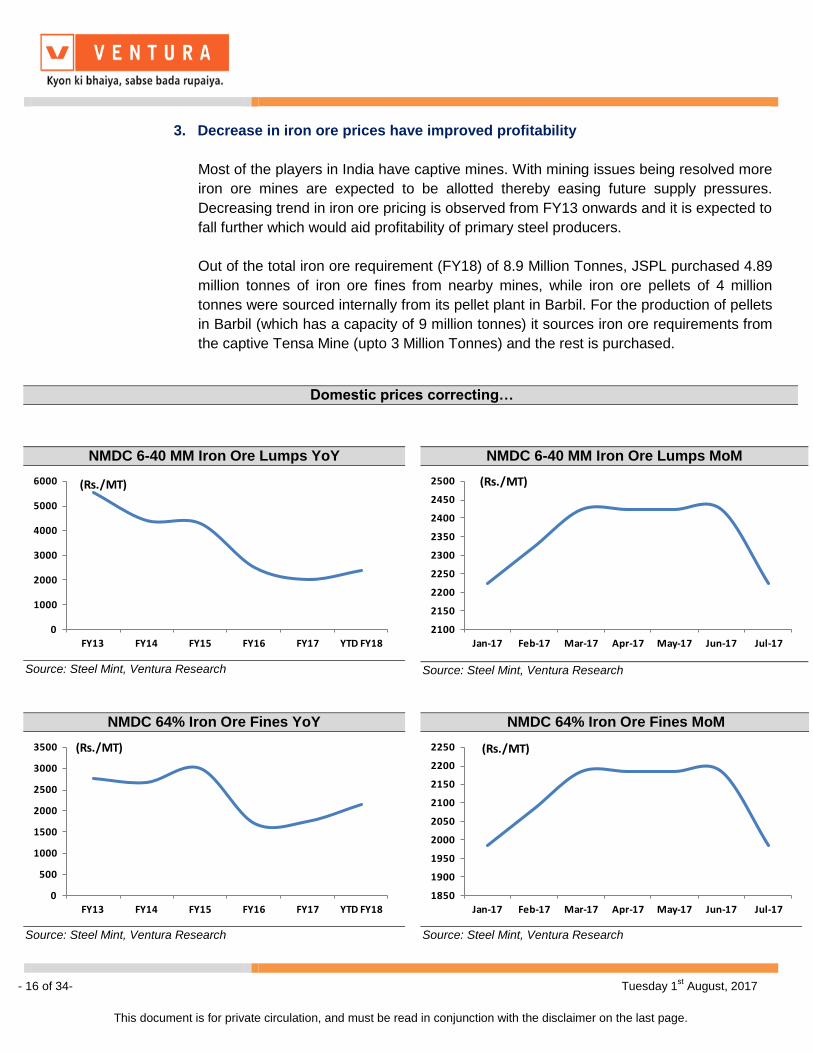

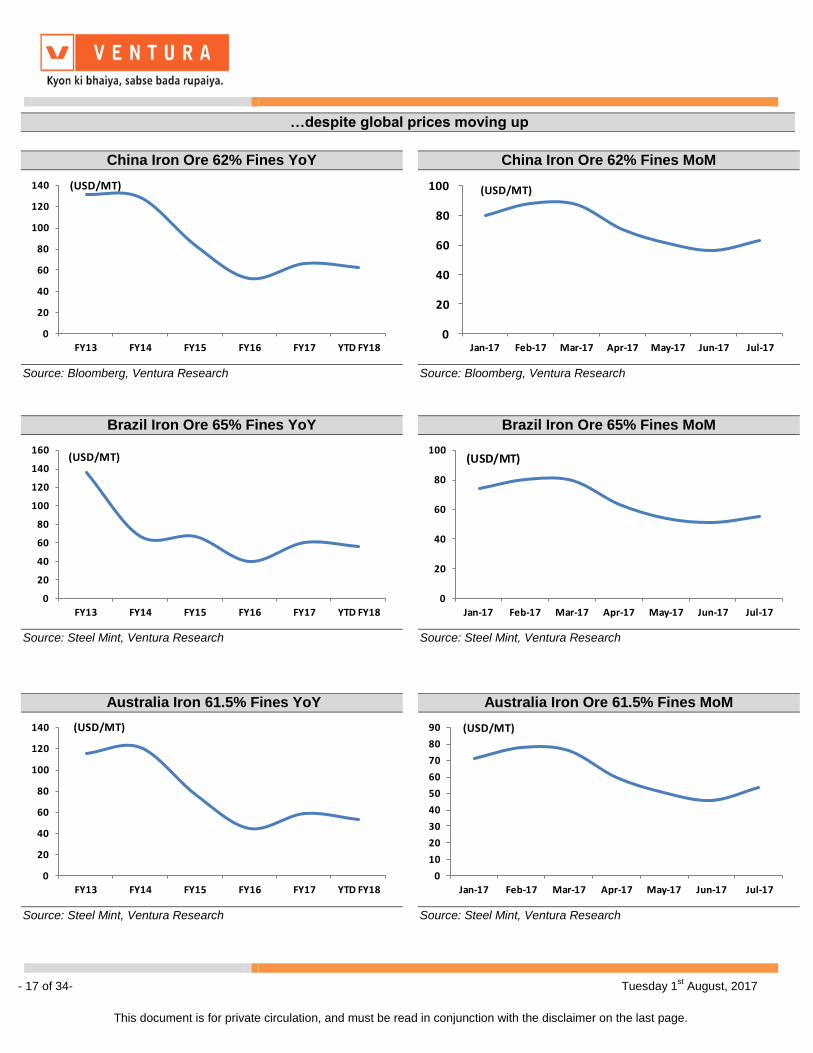

3. Decrease in iron ore prices have improved profitability

Most of the players in India have captive mines. With mining issues being resolved more

iron ore mines are expected to be allotted thereby easing future supply pressures.

Decreasing trend in iron ore pricing is observed from FY13 onwards and it is expected to

fall further which would aid profitability of primary steel producers.

Out of the total iron ore requirement (FY18) of 8.9 Million Tonnes, JSPL purchased 4.89

million tonnes of iron ore fines from nearby mines, while iron ore pellets of 4 million

tonnes were sourced internally from its pellet plant in Barbil. For the production of pellets

in Barbil (which has a capacity of 9 million tonnes) it sources iron ore requirements from

the captive Tensa Mine (upto 3 Million Tonnes) and the rest is purchased.

NMDC 6-40 MM Iron Ore Lumps YoY

0

1000

2000

3000

4000

5000

6000

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

NMDC 6-40 MM Iron Ore Lumps MoM

2100

2150

2200

2250

2300

2350

2400

2450

2500

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

NMDC 64% Iron Ore Fines YoY

0

500

1000

1500

2000

2500

3000

3500

FY13 FY14 FY15 FY16 FY17 YTD FY18

(Rs./MT)

Source: Steel Mint, Ventura Research

NMDC 64% Iron Ore Fines MoM

1850

1900

1950

2000

2050

2100

2150

2200

2250

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(Rs./MT)

Source: Steel Mint, Ventura Research

Domestic prices correcting…

- 17 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

China Iron Ore 62% Fines YoY

0

20

40

60

80

100

120

140

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Bloomberg, Ventura Research

China Iron Ore 62% Fines MoM

0

20

40

60

80

100

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Bloomberg, Ventura Research

Brazil Iron Ore 65% Fines YoY

0

20

40

60

80

100

120

140

160

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Steel Mint, Ventura Research

Brazil Iron Ore 65% Fines MoM

0

20

40

60

80

100

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Steel Mint, Ventura Research

Australia Iron 61.5% Fines YoY

0

20

40

60

80

100

120

140

FY13 FY14 FY15 FY16 FY17 YTD FY18

(USD/MT)

Source: Steel Mint, Ventura Research

Australia Iron Ore 61.5% Fines MoM

0

10

20

30

40

50

60

70

80

90

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17

(USD/MT)

Source: Steel Mint, Ventura Research

…despite global prices moving up

- 18 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

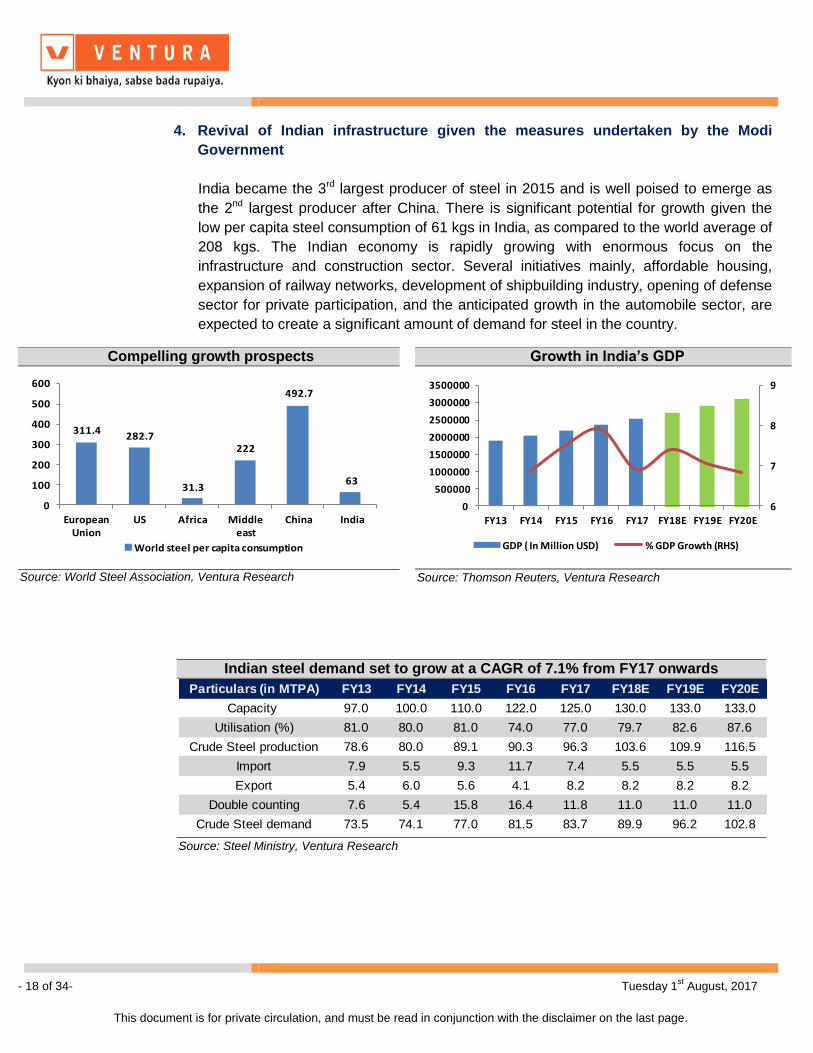

4. Revival of Indian infrastructure given the measures undertaken by the Modi

Government

India became the 3rd largest producer of steel in 2015 and is well poised to emerge as

the 2nd largest producer after China. There is significant potential for growth given the

low per capita steel consumption of 61 kgs in India, as compared to the world average of

208 kgs. The Indian economy is rapidly growing with enormous focus on the

infrastructure and construction sector. Several initiatives mainly, affordable housing,

expansion of railway networks, development of shipbuilding industry, opening of defense

sector for private participation, and the anticipated growth in the automobile sector, are

expected to create a significant amount of demand for steel in the country.

Indian steel demand set to grow at a CAGR of 7.1% from FY17 onwards

Particulars (in MTPA) FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Capacity 97.0 100.0 110.0 122.0 125.0 130.0 133.0 133.0

Utilisation (%) 81.0 80.0 81.0 74.0 77.0 79.7 82.6 87.6

Crude Steel production 78.6 80.0 89.1 90.3 96.3 103.6 109.9 116.5

Import 7.9 5.5 9.3 11.7 7.4 5.5 5.5 5.5

Export 5.4 6.0 5.6 4.1 8.2 8.2 8.2 8.2

Double counting 7.6 5.4 15.8 16.4 11.8 11.0 11.0 11.0

Crude Steel demand 73.5 74.1 77.0 81.5 83.7 89.9 96.2 102.8

Source: Steel Ministry, Ventura Research

Compelling growth prospects

311.4282.7

31.3

222

492.7

63

0

100

200

300

400

500

600

European Union

US Africa Middle east

China India

World steel per capita consumption

Source: World Steel Association, Ventura Research

Growth in India’s GDP

6

7

8

9

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

GDP ( In Million USD) % GDP Growth (RHS)

Source: Thomson Reuters, Ventura Research

- 19 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

5. Shrinking demand supply gap of domestic manufacturers

Investment in new steel capacity creation has come to a halt in India over the last three

years due to the deteriorating global steel industry environment and highly leveraged

balance sheets of Indian companies. It is estimated that Indian steel demand supply will

tighten significantly post FY19 given slowing supply and gradually improving demand.

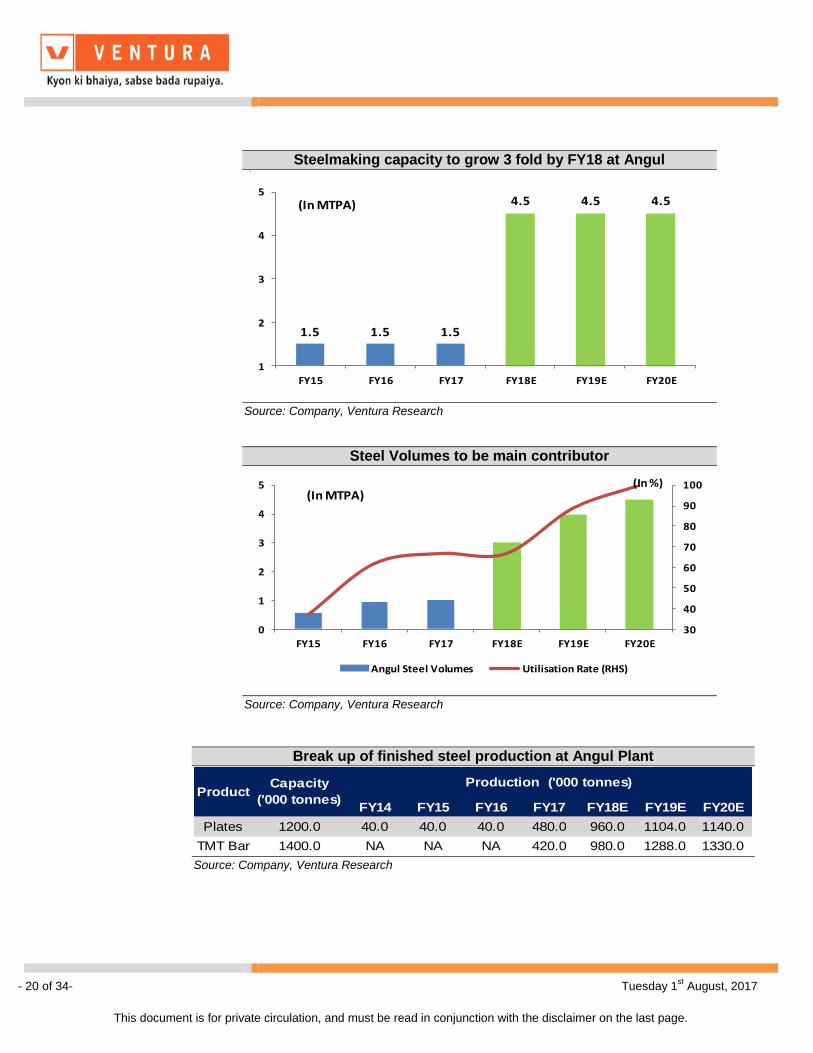

6. Culmination of capex at Angul augurs well for JSPL

The Angul plant consists of 1.8 million tonnes of a coal fired synthetic gas based DRI

plant and the recently commissioned 3.2 MTPA blast furnace. With these facilities now in

operation, crude steel capacity is expected to grow 3X to 4.5MTPA from 1.5 MTPA. We

expect steel volumes to grow at a CAGR of 65% to 4.5 MTPA by FY20.

Sector wise Steel demand growth

Sr. No. industry application

Current

Demand

2015-16

Estimated

Demand

2030-31

CAGR (%)

Current

Share

(%)

Future

Share

(%)

1 Construction & Infrastructure 50.5 138.0 7.4 62.0 60.0

2 Engineering & Fabrication 18.0 50.0 7.6 22.1 21.7

3 Automotive 8.2 28.0 9.2 10.1 12.2

4 Other Transport 2.4 8.0 9.0 2.9 3.5

5 Packaging & others 2.4 6.0 6.8 2.9 2.6

Total Finished Steel Consumption 81.5 230.0

Per Capita (Kg/Capita) 61.0 158.0

(in MTPA)

Railway material

Diversified

Product Profile

Bar & Rods, structurals,

plates and pipes

Plates, Bars & Rods

HRC , CRC, Plates

Source: Steel Ministry, Ventura Research

Indian Steel Supply

Particulars (in MTPA) FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Capacity 97.0 100.0 110.0 122.0 125.0 130.0 133.0 133.0

Utilisation (%) 81.0 80.0 81.0 74.0 77.0 79.7 82.6 87.6

Crude Steel production 78.6 80.0 89.1 90.3 96.3 103.6 109.9 116.5

Source: Steel Ministry, Ventura Research

- 20 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Break up of finished steel production at Angul Plant

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Plates 1200.0 40.0 40.0 40.0 480.0 960.0 1104.0 1140.0

TMT Bar 1400.0 NA NA NA 420.0 980.0 1288.0 1330.0

Production ('000 tonnes)Capacity

('000 tonnes)Product

Source: Company, Ventura Research

Steel Volumes to be main contributor

30

40

50

60

70

80

90

100

0

1

2

3

4

5

FY15 FY16 FY17 FY18E FY19E FY20E

Angul Steel Volumes Utilisation Rate (RHS)

(In MTPA)(In %)

Source: Company, Ventura Research

Steelmaking capacity to grow 3 fold by FY18 at Angul v

1.5 1.5 1.5

4.5 4.5 4.5

1

2

3

4

5

FY15 FY16 FY17 FY18E FY19E FY20E

(In MTPA)

Source: Company, Ventura Research

- 21 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

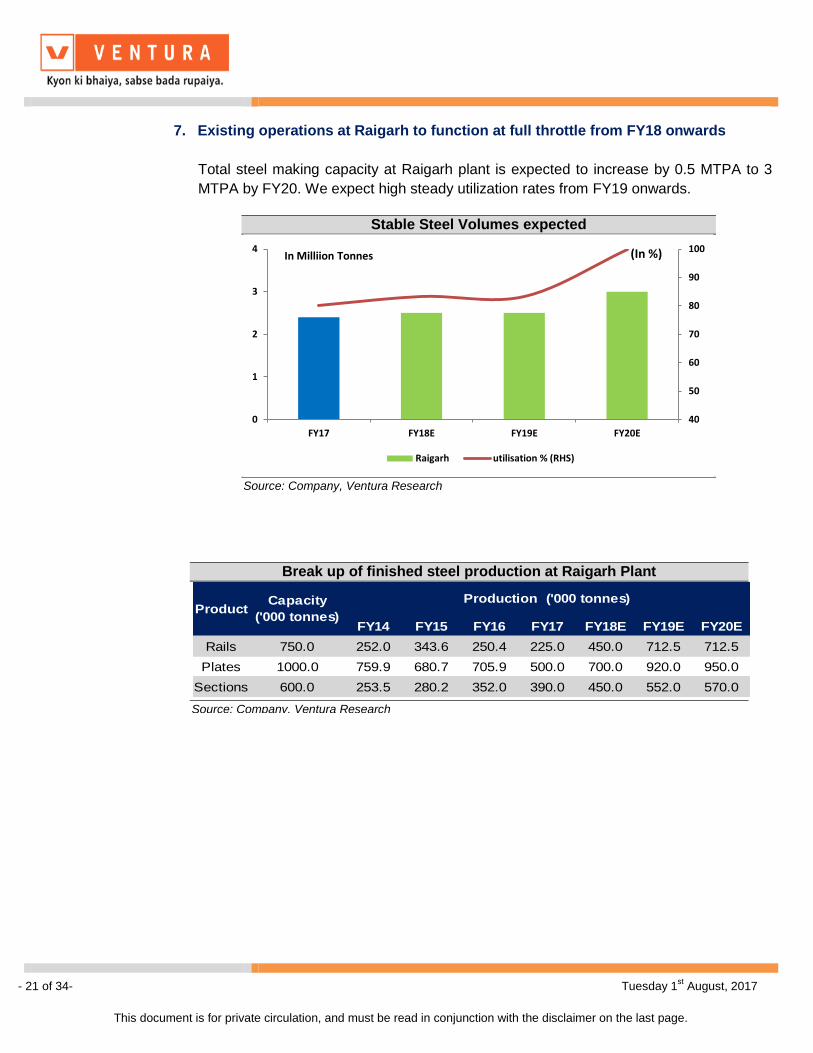

7. Existing operations at Raigarh to function at full throttle from FY18 onwards

Total steel making capacity at Raigarh plant is expected to increase by 0.5 MTPA to 3

MTPA by FY20. We expect high steady utilization rates from FY19 onwards.

Break up of finished steel production at Raigarh Plant

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rails 750.0 252.0 343.6 250.4 225.0 450.0 712.5 712.5

Plates 1000.0 759.9 680.7 705.9 500.0 700.0 920.0 950.0

Sections 600.0 253.5 280.2 352.0 390.0 450.0 552.0 570.0

Production ('000 tonnes)Product

Capacity

('000 tonnes)

Source: Company, Ventura Research

Stable Steel Volumes expected

Source: Company, Ventura Research

40

50

60

70

80

90

100

0

1

2

3

4

FY17 FY18E FY19E FY20E

Raigarh utilisation % (RHS)

In Milliion Tonnes (In %)

- 22 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

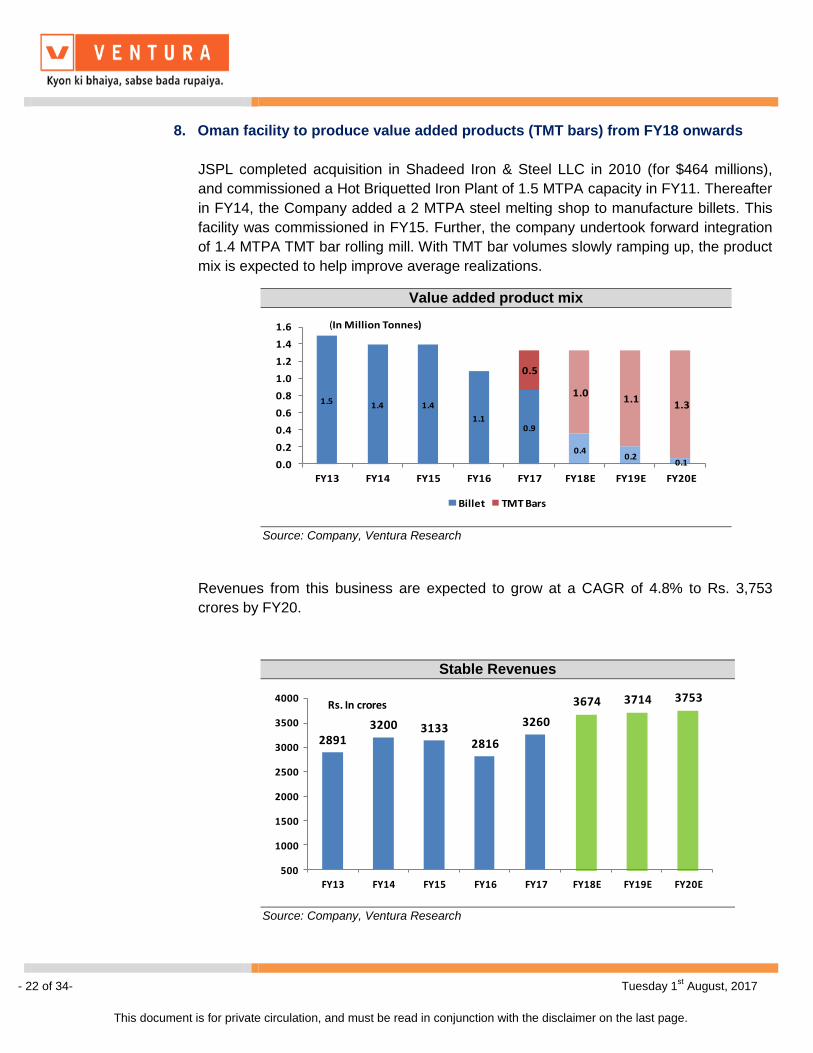

8. Oman facility to produce value added products (TMT bars) from FY18 onwards

JSPL completed acquisition in Shadeed Iron & Steel LLC in 2010 (for $464 millions),

and commissioned a Hot Briquetted Iron Plant of 1.5 MTPA capacity in FY11. Thereafter

in FY14, the Company added a 2 MTPA steel melting shop to manufacture billets. This

facility was commissioned in FY15. Further, the company undertook forward integration

of 1.4 MTPA TMT bar rolling mill. With TMT bar volumes slowly ramping up, the product

mix is expected to help improve average realizations.

Revenues from this business are expected to grow at a CAGR of 4.8% to Rs. 3,753

crores by FY20.

Value added product mix

1.5 1.4 1.4

1.10.9

0.40.2

0.1

0.5

1.01.1

1.3

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Billet TMT Bars

(In Million Tonnes)

Source: Company, Ventura Research

Stable Revenues

28913200 3133

2816

3260

3674 3714 3753

500

1000

1500

2000

2500

3000

3500

4000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rs. In crores

Source: Company, Ventura Research

- 23 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

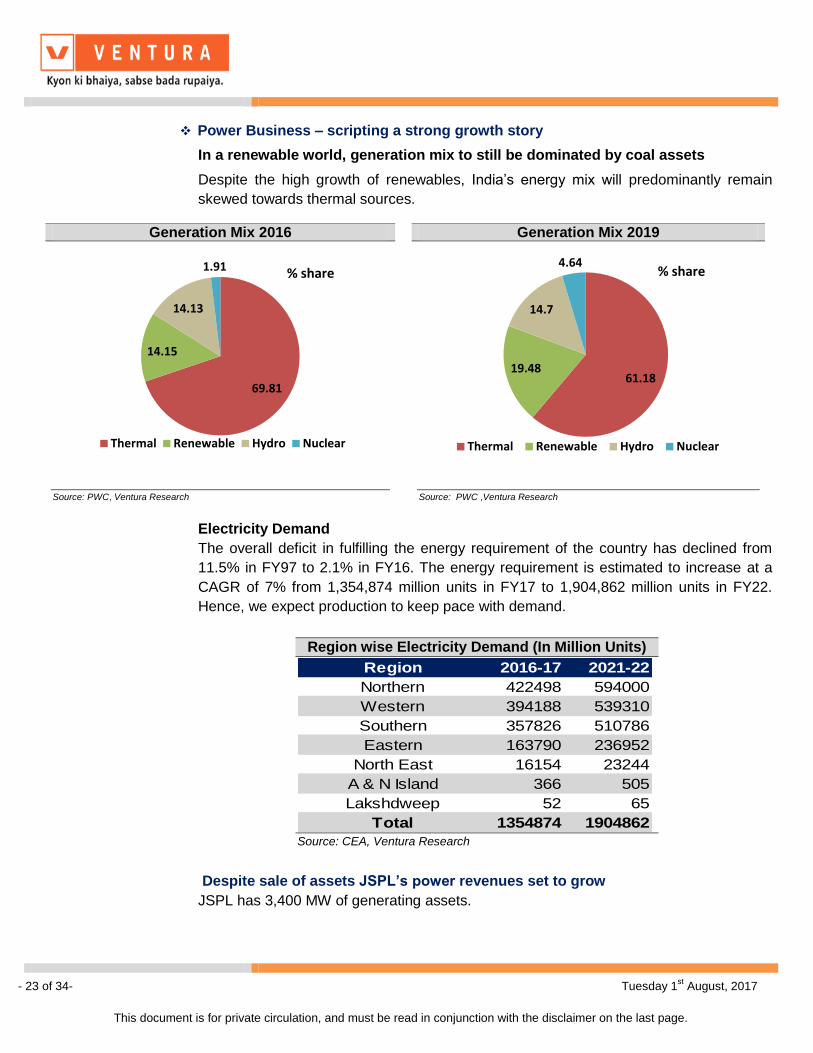

Power Business – scripting a strong growth story

In a renewable world, generation mix to still be dominated by coal assets

Despite the high growth of renewables, India’s energy mix will predominantly remain

skewed towards thermal sources.

Electricity Demand

The overall deficit in fulfilling the energy requirement of the country has declined from

11.5% in FY97 to 2.1% in FY16. The energy requirement is estimated to increase at a

CAGR of 7% from 1,354,874 million units in FY17 to 1,904,862 million units in FY22.

Hence, we expect production to keep pace with demand.

Despite sale of assets JSPL’s power revenues set to grow

JSPL has 3,400 MW of generating assets.

Generation Mix 2016 Generation Mix 2019

Source: PWC, Ventura Research

Source: PWC ,Ventura Research

69.81

14.15

14.13

1.91

Thermal Renewable Hydro Nuclear

% share

61.18 19.48

14.7

4.64

Thermal Renewable Hydro Nuclear

% share

Region wise Electricity Demand (In Million Units)

Region 2016-17 2021-22

Northern 422498 594000

Western 394188 539310

Southern 357826 510786

Eastern 163790 236952

North East 16154 23244

A & N Island 366 505

Lakshdweep 52 65

Total 1354874 1904862

Source: CEA, Ventura Research

- 24 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

However, to deleverage its balance sheet and improve liquidity, it concluded a binding

agreement for the sale of a thermal power plant worth Rs. 4,000 crores (1,000 MW plant

located at Tamnar, Chhattisgarh). This deal has two options:

Option 1: Sale of asset without Fuel Source Agreement (FSA) for Rs. 4,000 crores

Option 2: Sale of asset with FSA for Rs. 6,500 crores

This deal is expected to conclude in H1FY19. In our model we have assumed option 1

for cash flow consideration. This would mean in case of option 2, there would be an

upside risk to our EPS estimates by ~ Rs. 9.8 per share in FY19.

After the asset sale JSPL will be left with a portfolio of 2,400 MW of thermal power. We

expect the revenues to grow at a CAGR of 17.5% to Rs. 5,063 crores by FY20. We

expect the overall portfolio PLF to improve to 70% from the current 35%. We expect

EBIDTA to grow at a CAGR of 20% to Rs. 1,814 crores by FY20.

Sold to JSW energy

Details of Power purchase agreements

Project Buyer Period Quantity (MW) FSA

Tamnar I Tamil Nadu Sep 2014 to Aug 17 400 r

Tamnar IITamil Nadu Feb 2014 to Sep 2028 400 a

Tamnar IIKarnataka Jun 2016 to May 4041 200 a

Tamnar IIKarnataka Oct 2017 to Sep 2042 150 a

Tamnar IIChattisgarh From start of commercial operation 60 a

Tamnar IIChattisgarh From start of commercial operation 60 r

Total 870

Source: Company, Ventura Research

Capacity reduction with stable utilizations

Source: Company, Ventura Research

0

20

40

60

80

100

120

0

500

1000

1500

2000

2500

3000

3500

4000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Capacity Overall PLF % (RHS)

In MW Decline in capacity post sale of Tanmar I

Stable revenue from long term PPA’s

Source: Company, Ventura Research

2.7

2.8

2.9

3.0

3.1

3.2

3.3

3.4

3.5

0

1000

2000

3000

4000

5000

6000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Revenue Gross realisation Per unit

In Rs. Crores

Power generation portfolio

Tamnar I (2 unitsx250 MW) 1000 MW

Tamnar II (4 units x600 MW)2400 MW

Total 3400 MW

Source: Company, Ventura Research

Sold to JSW energy

- 25 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

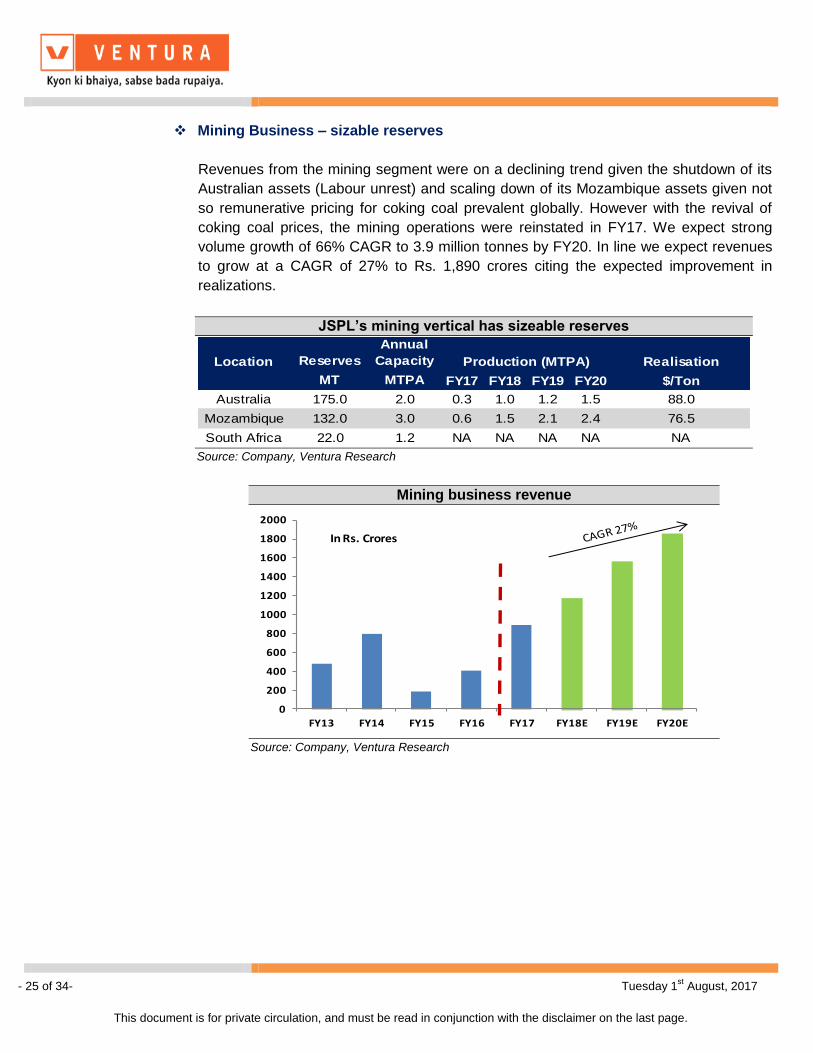

Mining Business – sizable reserves

Revenues from the mining segment were on a declining trend given the shutdown of its

Australian assets (Labour unrest) and scaling down of its Mozambique assets given not

so remunerative pricing for coking coal prevalent globally. However with the revival of

coking coal prices, the mining operations were reinstated in FY17. We expect strong

volume growth of 66% CAGR to 3.9 million tonnes by FY20. In line we expect revenues

to grow at a CAGR of 27% to Rs. 1,890 crores citing the expected improvement in

realizations.

JSPL’s mining vertical has sizeable reserves

Location Reserves

Annual

Capacity Realisation

MT MTPA FY17 FY18 FY19 FY20 $/Ton

Australia 175.0 2.0 0.3 1.0 1.2 1.5 88.0

Mozambique 132.0 3.0 0.6 1.5 2.1 2.4 76.5

South Africa 22.0 1.2 NA NA NA NA NA

Production (MTPA)

Source: Company, Ventura Research

Mining business revenue

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

In Rs. Crores

Source: Company, Ventura Research

- 26 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

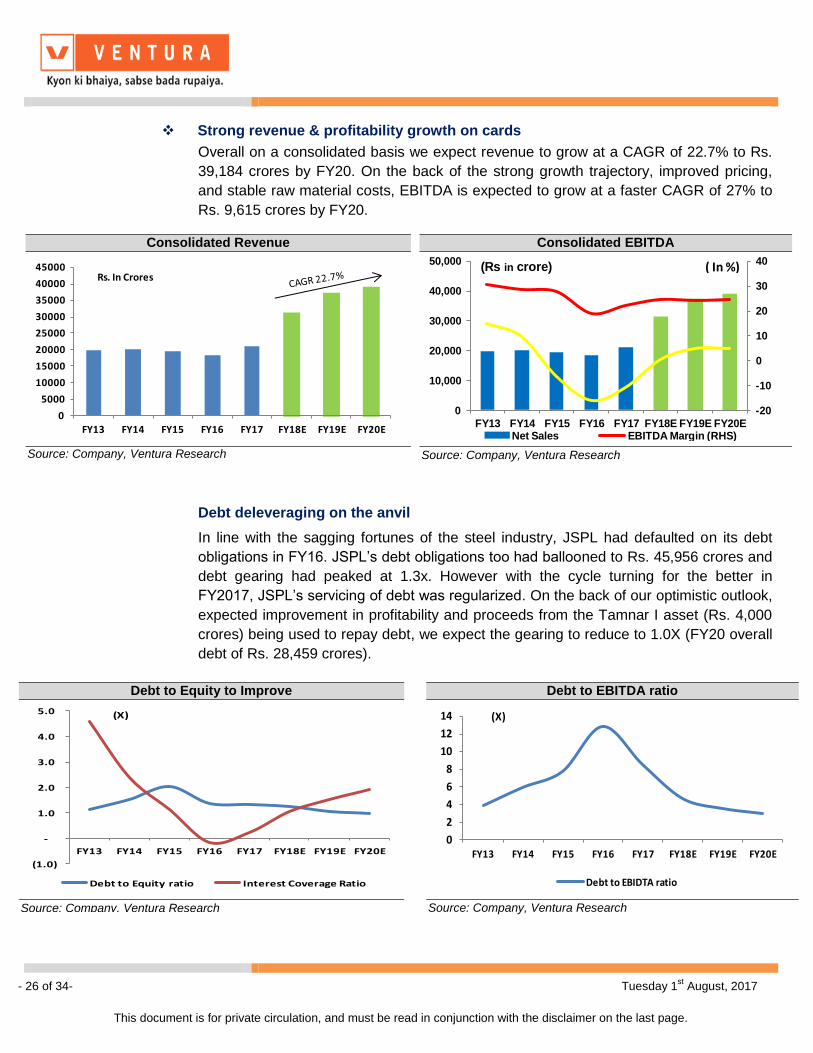

Strong revenue & profitability growth on cards

Overall on a consolidated basis we expect revenue to grow at a CAGR of 22.7% to Rs.

39,184 crores by FY20. On the back of the strong growth trajectory, improved pricing,

and stable raw material costs, EBITDA is expected to grow at a faster CAGR of 27% to

Rs. 9,615 crores by FY20.

Debt deleveraging on the anvil

In line with the sagging fortunes of the steel industry, JSPL had defaulted on its debt

obligations in FY16. JSPL’s debt obligations too had ballooned to Rs. 45,956 crores and

debt gearing had peaked at 1.3x. However with the cycle turning for the better in

FY2017, JSPL’s servicing of debt was regularized. On the back of our optimistic outlook,

expected improvement in profitability and proceeds from the Tamnar I asset (Rs. 4,000

crores) being used to repay debt, we expect the gearing to reduce to 1.0X (FY20 overall

debt of Rs. 28,459 crores).

Consolidated Revenue

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rs. In Crores

Source: Company, Ventura Research

Consolidated EBITDA

-20

-10

0

10

20

30

40

0

10,000

20,000

30,000

40,000

50,000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20ENet Sales EBITDA Margin (RHS)

(Rs in crore) ( In %)

Source: Company, Ventura Research

Debt to Equity to Improve

(1.0)

-

1.0

2.0

3.0

4.0

5.0

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Debt to Equity ratio Interest Coverage Ratio

(X)

v

Source: Company, Ventura Research

Debt to EBITDA ratio

0

2

4

6

8

10

12

14

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Debt to EBIDTA ratio

(X)

Source: Company, Ventura Research

- 27 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

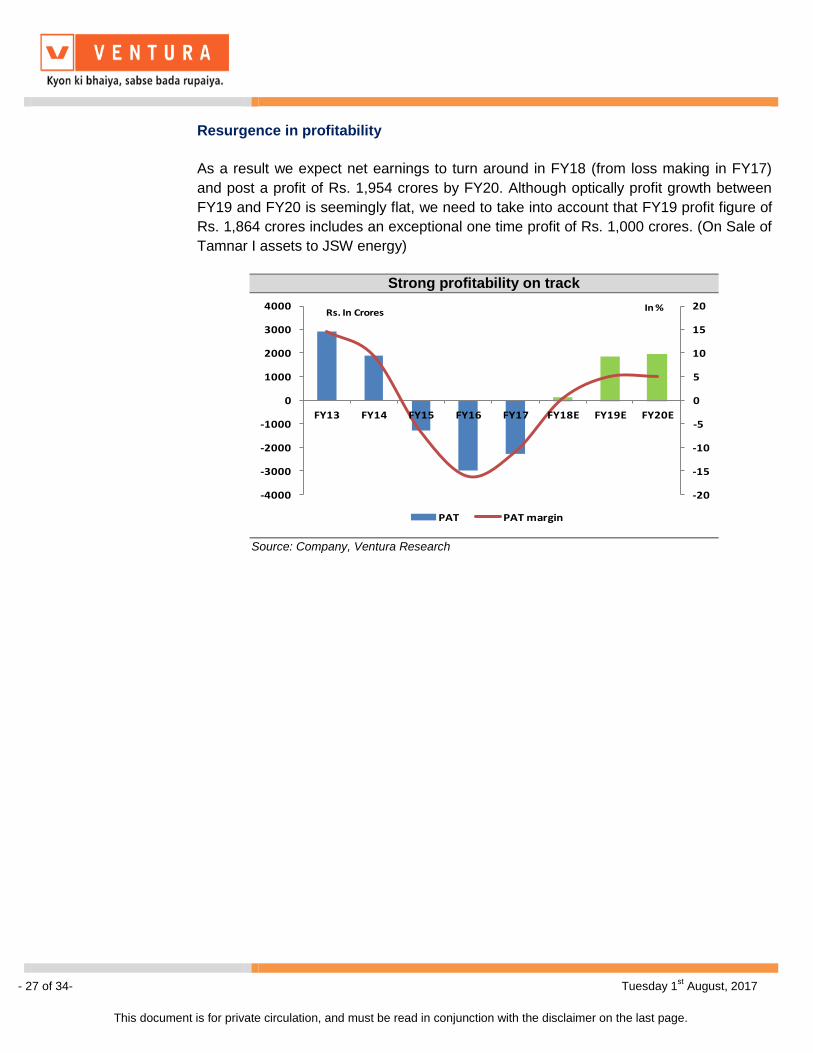

Resurgence in profitability

As a result we expect net earnings to turn around in FY18 (from loss making in FY17)

and post a profit of Rs. 1,954 crores by FY20. Although optically profit growth between

FY19 and FY20 is seemingly flat, we need to take into account that FY19 profit figure of

Rs. 1,864 crores includes an exceptional one time profit of Rs. 1,000 crores. (On Sale of

Tamnar I assets to JSW energy)

Strong profitability on track

-20

-15

-10

-5

0

5

10

15

20

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

PAT PAT margin

Rs. In Crores In %

Source: Company, Ventura Research

- 28 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

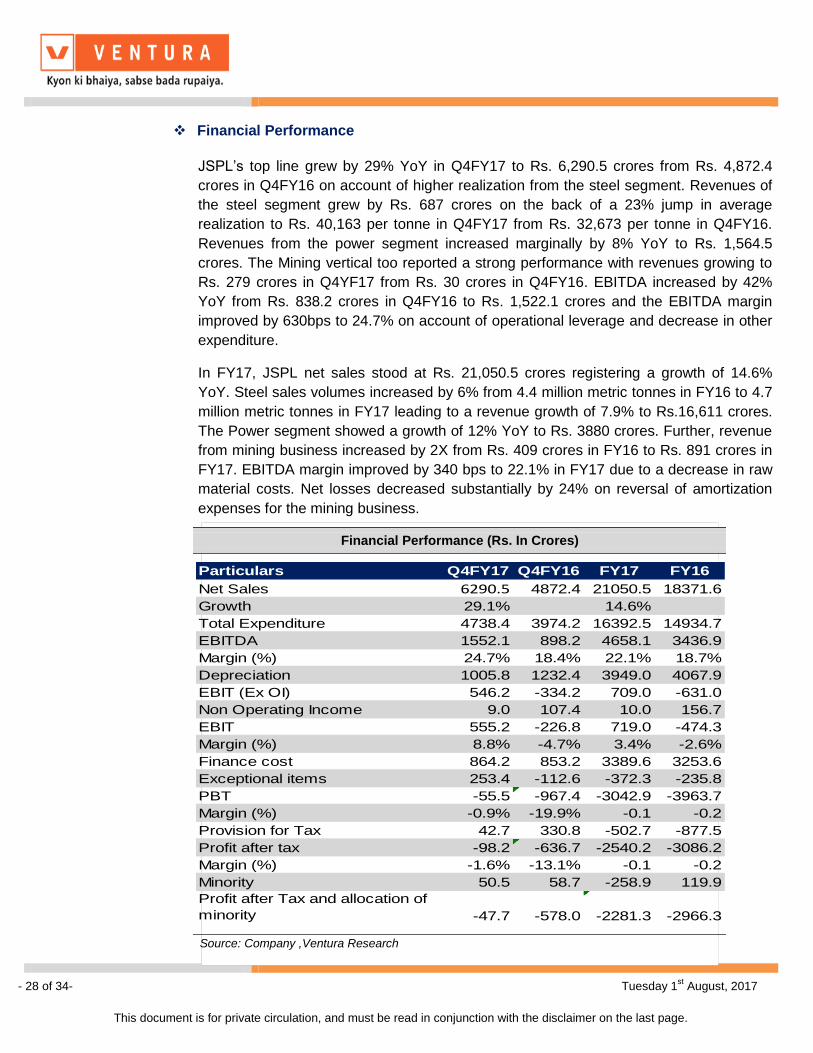

Financial Performance

JSPL’s top line grew by 29% YoY in Q4FY17 to Rs. 6,290.5 crores from Rs. 4,872.4

crores in Q4FY16 on account of higher realization from the steel segment. Revenues of

the steel segment grew by Rs. 687 crores on the back of a 23% jump in average

realization to Rs. 40,163 per tonne in Q4FY17 from Rs. 32,673 per tonne in Q4FY16.

Revenues from the power segment increased marginally by 8% YoY to Rs. 1,564.5

crores. The Mining vertical too reported a strong performance with revenues growing to

Rs. 279 crores in Q4YF17 from Rs. 30 crores in Q4FY16. EBITDA increased by 42%

YoY from Rs. 838.2 crores in Q4FY16 to Rs. 1,522.1 crores and the EBITDA margin

improved by 630bps to 24.7% on account of operational leverage and decrease in other

expenditure.

In FY17, JSPL net sales stood at Rs. 21,050.5 crores registering a growth of 14.6%

YoY. Steel sales volumes increased by 6% from 4.4 million metric tonnes in FY16 to 4.7

million metric tonnes in FY17 leading to a revenue growth of 7.9% to Rs.16,611 crores.

The Power segment showed a growth of 12% YoY to Rs. 3880 crores. Further, revenue

from mining business increased by 2X from Rs. 409 crores in FY16 to Rs. 891 crores in

FY17. EBITDA margin improved by 340 bps to 22.1% in FY17 due to a decrease in raw

material costs. Net losses decreased substantially by 24% on reversal of amortization

expenses for the mining business.

Financial Performance (Rs. In Crores)

Particulars Q4FY17 Q4FY16 FY17 FY16

Net Sales 6290.5 4872.4 21050.5 18371.6

Growth 29.1% 14.6%

Total Expenditure 4738.4 3974.2 16392.5 14934.7

EBITDA 1552.1 898.2 4658.1 3436.9

Margin (%) 24.7% 18.4% 22.1% 18.7%

Depreciation 1005.8 1232.4 3949.0 4067.9

EBIT (Ex OI) 546.2 -334.2 709.0 -631.0

Non Operating Income 9.0 107.4 10.0 156.7

EBIT 555.2 -226.8 719.0 -474.3

Margin (%) 8.8% -4.7% 3.4% -2.6%

Finance cost 864.2 853.2 3389.6 3253.6

Exceptional items 253.4 -112.6 -372.3 -235.8

PBT -55.5 -967.4 -3042.9 -3963.7

Margin (%) -0.9% -19.9% -0.1 -0.2

Provision for Tax 42.7 330.8 -502.7 -877.5

Profit after tax -98.2 -636.7 -2540.2 -3086.2

Margin (%) -1.6% -13.1% -0.1 -0.2

Minority 50.5 58.7 -258.9 119.9

Profit after Tax and allocation of

minority -47.7 -578.0 -2281.3 -2966.3

e

Source: Company ,Ventura Research

- 29 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

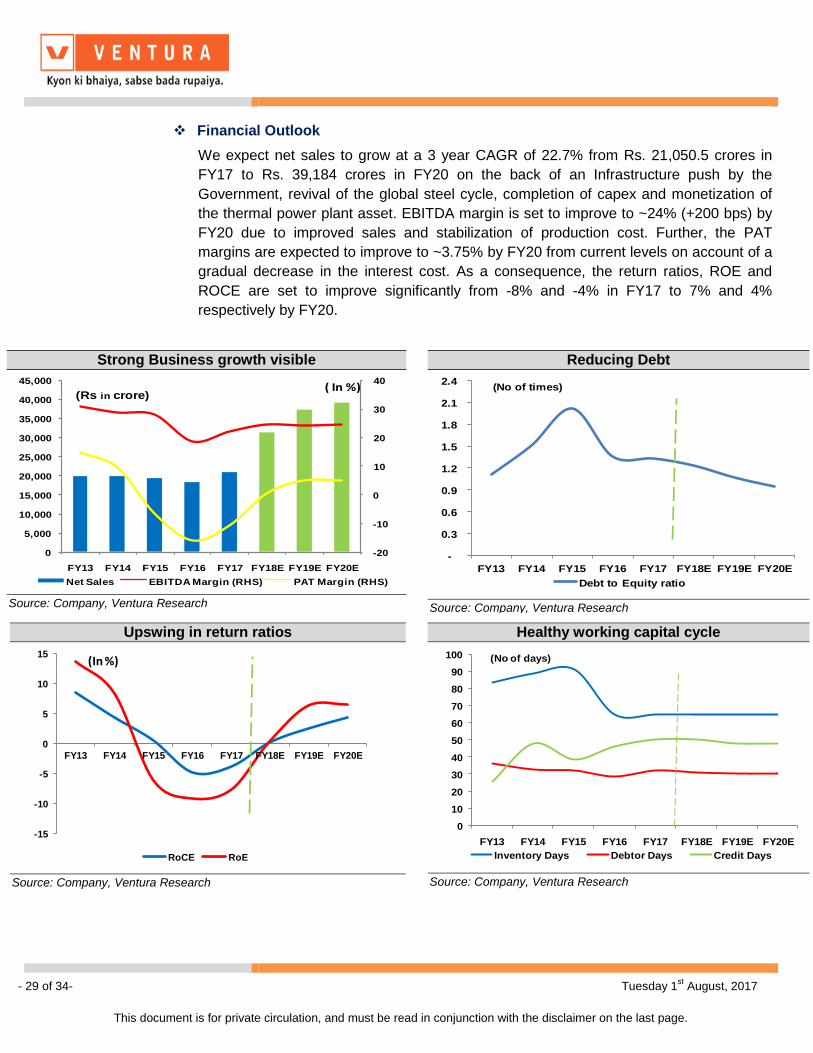

Financial Outlook

We expect net sales to grow at a 3 year CAGR of 22.7% from Rs. 21,050.5 crores in

FY17 to Rs. 39,184 crores in FY20 on the back of an Infrastructure push by the

Government, revival of the global steel cycle, completion of capex and monetization of

the thermal power plant asset. EBITDA margin is set to improve to ~24% (+200 bps) by

FY20 due to improved sales and stabilization of production cost. Further, the PAT

margins are expected to improve to ~3.75% by FY20 from current levels on account of a

gradual decrease in the interest cost. As a consequence, the return ratios, ROE and

ROCE are set to improve significantly from -8% and -4% in FY17 to 7% and 4%

respectively by FY20.

Strong Business growth visible

-20

-10

0

10

20

30

40

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Net Sales EBITDA Margin (RHS) PAT Margin (RHS)

(Rs in crore)( In %)

Source: Company, Ventura Research

Reducing Debt

-

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Debt to Equity ratio

(No of times)

Source: Company, Ventura Research

Upswing in return ratios

-15

-10

-5

0

5

10

15

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

RoCE RoE

(In %)

Source: Company, Ventura Research

Healthy working capital cycle

0

10

20

30

40

50

60

70

80

90

100

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Inventory Days Debtor Days Credit Days

(No of days)

Source: Company, Ventura Research

- 30 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Key Risk

Coal block allocation scam

CBI had registered a case against Mr. Naveen Jindal in the allocation of the Amarkonda

Murgadangal coal block in Jharkhand. On 24th April, 2017 Mr. Jindal was formally

charged with criminal misconduct & false representation of facts in the allocation of

above coal block. Further, on 10th July, 2017 CBI filed another supplementary charge

sheet against Mr. Jindal in the Urtan North coal block case. In our view, the above

mentioned cases will not have any financial impact on the company. Markets have

already priced in the impact of above cases & any adverse order will not impact the

fortunes of the company.

Slow down in Infrastructure boom

Steel demand is expected to grow at a CAGR of 7.1% on the back of a boost given to

infrastructure by the launch of “Housing for all by 2020”, infrastructure status given to

housing projects, opening up of the defence sector to private players and growth in the

automobile industry. Any delays in achieving the stipulated targets would mean a

setback to anticipated steel demand and hence impact the profitability assumption for

JSPL negatively.

- 31 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

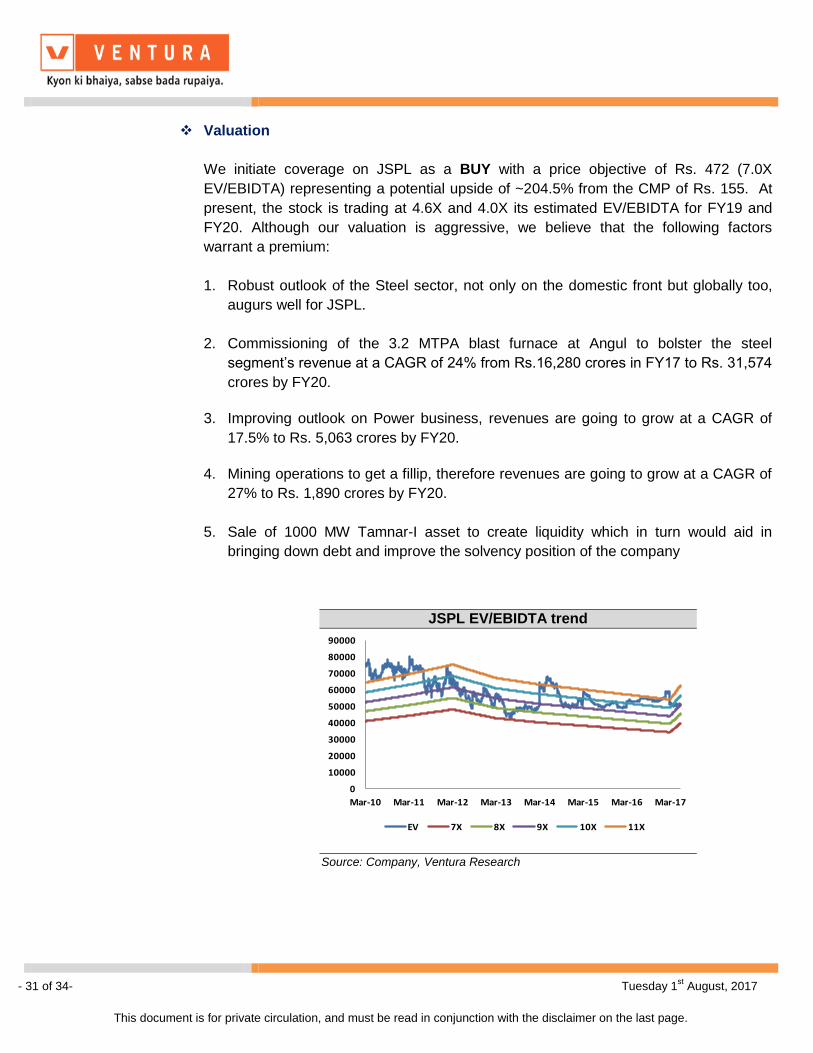

Valuation

We initiate coverage on JSPL as a BUY with a price objective of Rs. 472 (7.0X

EV/EBIDTA) representing a potential upside of ~204.5% from the CMP of Rs. 155. At

present, the stock is trading at 4.6X and 4.0X its estimated EV/EBIDTA for FY19 and

FY20. Although our valuation is aggressive, we believe that the following factors

warrant a premium:

1. Robust outlook of the Steel sector, not only on the domestic front but globally too,

augurs well for JSPL.

2. Commissioning of the 3.2 MTPA blast furnace at Angul to bolster the steel

segment’s revenue at a CAGR of 24% from Rs.16,280 crores in FY17 to Rs. 31,574

crores by FY20.

3. Improving outlook on Power business, revenues are going to grow at a CAGR of

17.5% to Rs. 5,063 crores by FY20.

4. Mining operations to get a fillip, therefore revenues are going to grow at a CAGR of

27% to Rs. 1,890 crores by FY20.

5. Sale of 1000 MW Tamnar-I asset to create liquidity which in turn would aid in

bringing down debt and improve the solvency position of the company

JSPL EV/EBIDTA trend

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

EV 7X 8X 9X 10X 11X

Source: Company, Ventura Research

- 32 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

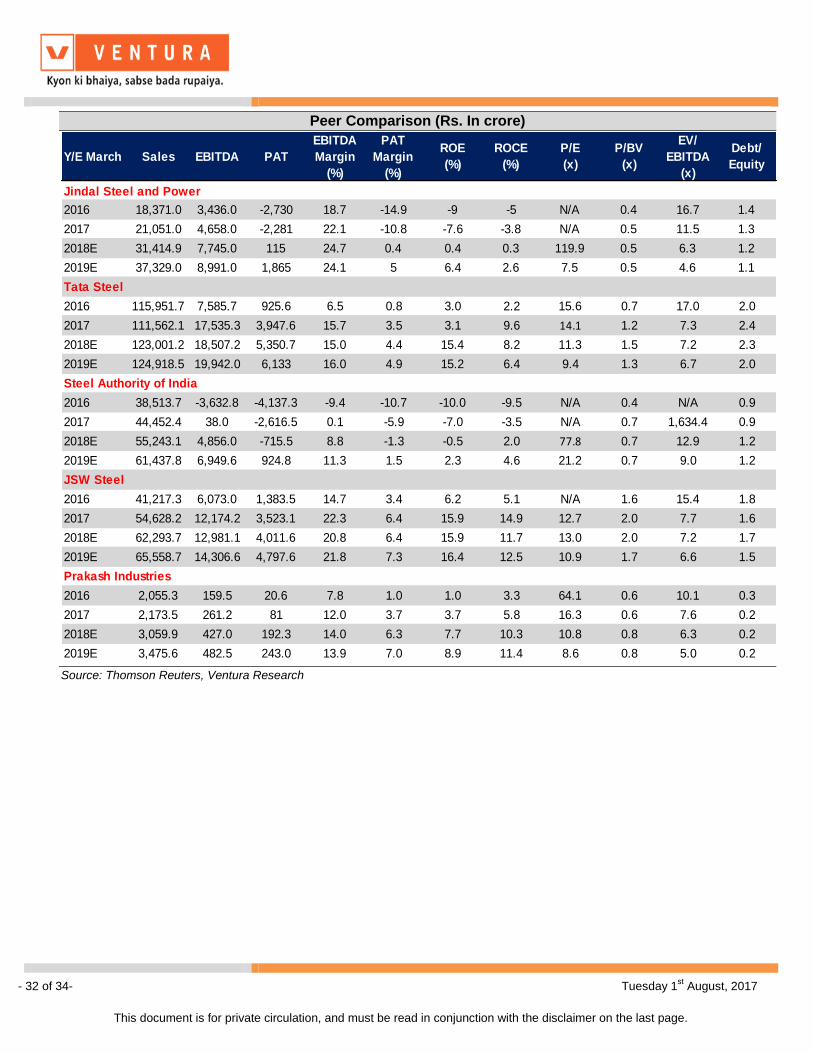

Peer Comparison (Rs. In crore)

Y/E March Sales EBITDA PAT

EBITDA

Margin

(%)

PAT

Margin

(%)

ROE

(%)

ROCE

(%)

P/E

(x)

P/BV

(x)

EV/

EBITDA

(x)

Debt/

Equity

Jindal Steel and Power 100.00%

2016 18,371.0 3,436.0 -2,730 18.7 -14.9 -9 -5 N/A 0.4 16.7 1.4

2017 21,051.0 4,658.0 -2,281 22.1 -10.8 -7.6 -3.8 N/A 0.5 11.5 1.3

2018E 31,414.9 7,745.0 115 24.7 0.4 0.4 0.3 119.9 0.5 6.3 1.2

2019E 37,329.0 8,991.0 1,865 24.1 5 6.4 2.6 7.5 0.5 4.6 1.1

Tata Steel

2016 115,951.7 7,585.7 925.6 6.5 0.8 3.0 2.2 15.6 0.7 17.0 2.0

2017 111,562.1 17,535.3 3,947.6 15.7 3.5 3.1 9.6 14.1 1.2 7.3 2.4

2018E 123,001.2 18,507.2 5,350.7 15.0 4.4 15.4 8.2 11.3 1.5 7.2 2.3

2019E 124,918.5 19,942.0 6,133 16.0 4.9 15.2 6.4 9.4 1.3 6.7 2.0

Steel Authority of India

2016 38,513.7 -3,632.8 -4,137.3 -9.4 -10.7 -10.0 -9.5 N/A 0.4 N/A 0.9

2017 44,452.4 38.0 -2,616.5 0.1 -5.9 -7.0 -3.5 N/A 0.7 1,634.4 0.9

2018E 55,243.1 4,856.0 -715.5 8.8 -1.3 -0.5 2.0 77.8 0.7 12.9 1.2

2019E 61,437.8 6,949.6 924.8 11.3 1.5 2.3 4.6 21.2 0.7 9.0 1.2

JSW Steel

2016 41,217.3 6,073.0 1,383.5 14.7 3.4 6.2 5.1 N/A 1.6 15.4 1.8

2017 54,628.2 12,174.2 3,523.1 22.3 6.4 15.9 14.9 12.7 2.0 7.7 1.6

2018E 62,293.7 12,981.1 4,011.6 20.8 6.4 15.9 11.7 13.0 2.0 7.2 1.7

2019E 65,558.7 14,306.6 4,797.6 21.8 7.3 16.4 12.5 10.9 1.7 6.6 1.5

Prakash Industries

2016 2,055.3 159.5 20.6 7.8 1.0 1.0 3.3 64.1 0.6 10.1 0.3

2017 2,173.5 261.2 81 12.0 3.7 3.7 5.8 16.3 0.6 7.6 0.2

2018E 3,059.9 427.0 192.3 14.0 6.3 7.7 10.3 10.8 0.8 6.3 0.2

2019E 3,475.6 482.5 243.0 13.9 7.0 8.9 11.4 8.6 0.8 5.0 0.2

Source: Thomson Reuters, Ventura Research

- 33 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

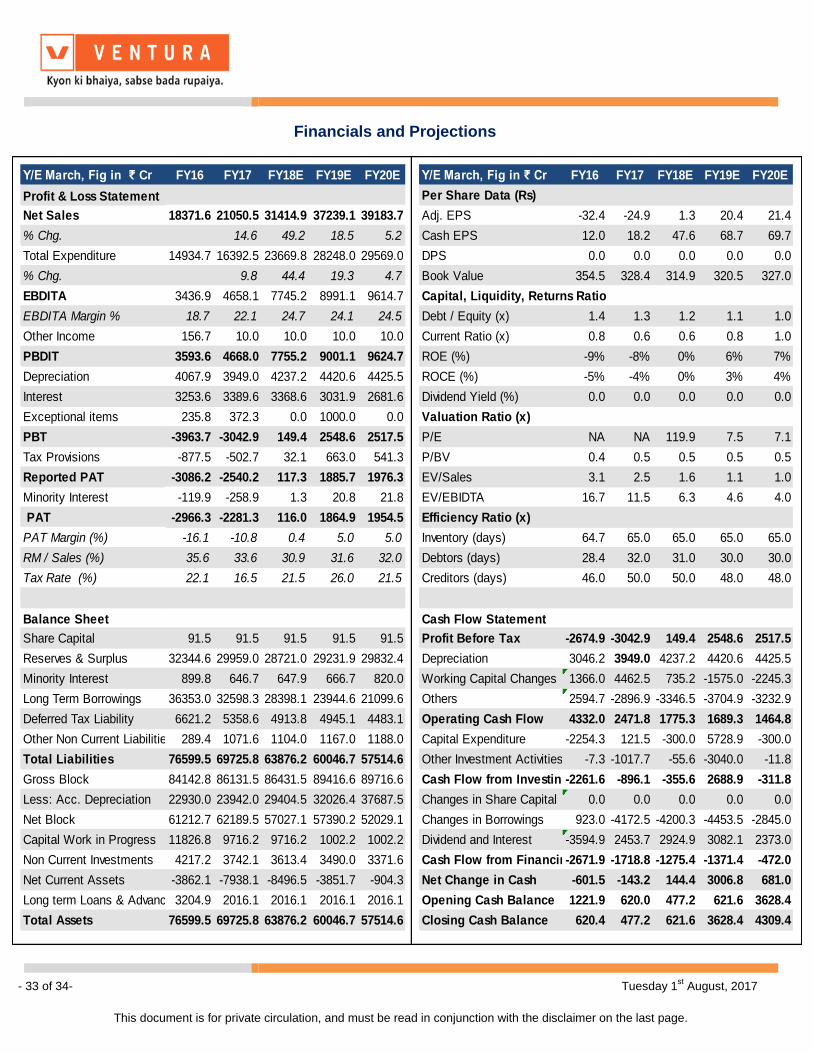

Financials and Projections

Y/E March, Fig in ₹ Cr FY16 FY17 FY18E FY19E FY20E Y/E March, Fig in ₹ Cr FY16 FY17 FY18E FY19E FY20E

Profit & Loss Statement Per Share Data (Rs)

Net Sales 18371.6 21050.5 31414.9 37239.1 39183.7 Adj. EPS -32.4 -24.9 1.3 20.4 21.4

% Chg. 14.6 49.2 18.5 5.2 Cash EPS 12.0 18.2 47.6 68.7 69.7

Total Expenditure 14934.7 16392.5 23669.8 28248.0 29569.0 DPS 0.0 0.0 0.0 0.0 0.0

% Chg. 9.8 44.4 19.3 4.7 Book Value 354.5 328.4 314.9 320.5 327.0

EBDITA 3436.9 4658.1 7745.2 8991.1 9614.7 Capital, Liquidity, Returns Ratio

EBDITA Margin % 18.7 22.1 24.7 24.1 24.5 Debt / Equity (x) 1.4 1.3 1.2 1.1 1.0

Other Income 156.7 10.0 10.0 10.0 10.0 Current Ratio (x) 0.8 0.6 0.6 0.8 1.0

PBDIT 3593.6 4668.0 7755.2 9001.1 9624.7 ROE (%) -9% -8% 0% 6% 7%

Depreciation 4067.9 3949.0 4237.2 4420.6 4425.5 ROCE (%) -5% -4% 0% 3% 4%

Interest 3253.6 3389.6 3368.6 3031.9 2681.6 Dividend Yield (%) 0.0 0.0 0.0 0.0 0.0

Exceptional items 235.8 372.3 0.0 1000.0 0.0 Valuation Ratio (x)

PBT -3963.7 -3042.9 149.4 2548.6 2517.5 P/E NA NA 119.9 7.5 7.1

Tax Provisions -877.5 -502.7 32.1 663.0 541.3 P/BV 0.4 0.5 0.5 0.5 0.5

Reported PAT -3086.2 -2540.2 117.3 1885.7 1976.3 EV/Sales 3.1 2.5 1.6 1.1 1.0

Minority Interest -119.9 -258.9 1.3 20.8 21.8 EV/EBIDTA 16.7 11.5 6.3 4.6 4.0

PAT -2966.3 -2281.3 116.0 1864.9 1954.5 Efficiency Ratio (x)

PAT Margin (%) -16.1 -10.8 0.4 5.0 5.0 Inventory (days) 64.7 65.0 65.0 65.0 65.0

RM / Sales (%) 35.6 33.6 30.9 31.6 32.0 Debtors (days) 28.4 32.0 31.0 30.0 30.0

Tax Rate (%) 22.1 16.5 21.5 26.0 21.5 Creditors (days) 46.0 50.0 50.0 48.0 48.0

Balance Sheet Cash Flow Statement

Share Capital 91.5 91.5 91.5 91.5 91.5 Profit Before Tax -2674.9 -3042.9 149.4 2548.6 2517.5

Reserves & Surplus 32344.6 29959.0 28721.0 29231.9 29832.4 Depreciation 3046.2 3949.0 4237.2 4420.6 4425.5

Minority Interest 899.8 646.7 647.9 666.7 820.0 Working Capital Changes 1366.0 4462.5 735.2 -1575.0 -2245.3

Long Term Borrowings 36353.0 32598.3 28398.1 23944.6 21099.6 Others 2594.7 -2896.9 -3346.5 -3704.9 -3232.9

Deferred Tax Liability 6621.2 5358.6 4913.8 4945.1 4483.1 Operating Cash Flow 4332.0 2471.8 1775.3 1689.3 1464.8

Other Non Current Liabilities 289.4 1071.6 1104.0 1167.0 1188.0 Capital Expenditure -2254.3 121.5 -300.0 5728.9 -300.0

Total Liabilities 76599.5 69725.8 63876.2 60046.7 57514.6 Other Investment Activities -7.3 -1017.7 -55.6 -3040.0 -11.8

Gross Block 84142.8 86131.5 86431.5 89416.6 89716.6 Cash Flow from Investing-2261.6 -896.1 -355.6 2688.9 -311.8

Less: Acc. Depreciation 22930.0 23942.0 29404.5 32026.4 37687.5 Changes in Share Capital 0.0 0.0 0.0 0.0 0.0

Net Block 61212.7 62189.5 57027.1 57390.2 52029.1 Changes in Borrowings 923.0 -4172.5 -4200.3 -4453.5 -2845.0

Capital Work in Progress 11826.8 9716.2 9716.2 1002.2 1002.2 Dividend and Interest -3594.9 2453.7 2924.9 3082.1 2373.0

Non Current Investments 4217.2 3742.1 3613.4 3490.0 3371.6 Cash Flow from Financing-2671.9 -1718.8 -1275.4 -1371.4 -472.0

Net Current Assets -3862.1 -7938.1 -8496.5 -3851.7 -904.3 Net Change in Cash -601.5 -143.2 144.4 3006.8 681.0

Long term Loans & Advances3204.9 2016.1 2016.1 2016.1 2016.1 Opening Cash Balance 1221.9 620.0 477.2 621.6 3628.4

Total Assets 76599.5 69725.8 63876.2 60046.7 57514.6 Closing Cash Balance 620.4 477.2 621.6 3628.4 4309.4

- 34 of 34- Tuesday 1st August, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Disclosures and Disclaimer

Ventura Securities Limited (VSL) is a SEBI registered intermediary offering broking, depository and portfolio management services to clients. VSL is member of BSE, NSE and MCX-SX. VSL is a depository participant of NSDL. VSL states that no disciplinary action whatsoever has been taken by SEBI against it in last five years except administrative warning issued in connection with technical and venial lapses observed while inspection of books of accounts and records. Ventura Commodities Limited, Ventura Guaranty Limited, Ventura Insurance Brokers Limited and Ventura Allied Services Private Limited are associates of VSL. Research Analyst (RA) involved in the preparation of this research report and VSL disclose that neither RA nor VSL nor its associates (i) have any financial interest in the company which is the subject matter of this research report (ii) holds ownership of one percent or more in the securities of subject company (iii) have any material conflict of interest at the time of publication of this research report (iv) have received any compensation from the subject company in the past twelve months (v) have managed or co-managed public offering of securities for the subject company in past twelve months (vi) have received any compensation for investment banking merchant banking or brokerage services from the subject company in the past twelve months (vii) have received any compensation for product or services from the subject company in the past twelve months (viii) have received any compensation or other benefits from the subject company or third party in connection with the research report. RA involved in the preparation of this research report discloses that he / she has not served as an officer, director or employee of the subject company. RA involved in the preparation of this research report and VSL discloses that they have not been engaged in the market making activity for the subject company. Our sales people, dealers, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein. We may have earlier issued or may issue in future reports on the companies covered herein with recommendations/ information inconsistent or different those made in this report. In reviewing this document, you should be aware that any or all of the foregoing, among other things, may give rise to or potential conflicts of interest. We may rely on information barriers, such as "Chinese Walls" to control the flow of information contained in one or more areas within us, or other areas, units, groups or affiliates of VSL. This report is for information purposes only and this document/material should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this document nor anything contained herein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. This document does not solicit any action based on the material contained herein. It is for the general information of the clients / prospective clients of VSL. VSL will not treat recipients as clients by virtue of their receiving this report. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of clients / prospective clients. Similarly, this document does not have regard to the specific investment objectives, financial situation/circumstances and the particular needs of any specific person who may receive this document. The securities discussed in this report may not be suitable for all investors. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives. Persons who may receive this document should consider and independently evaluate whether it is suitable for his/ her/their particular circumstances and, if necessary, seek professional/financial advice. And such person shall be responsible for conducting his/her/their own investigation and analysis of the information contained or referred to in this document and of evaluating the merits and risks involved in the securities forming the subject matter of this document. The projections and forecasts described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections and forecasts were based will not materialize or will vary significantly from actual results, and such variances will likely increase over time. All projections and forecasts described in this report have been prepared solely by the authors of this report independently of the Company. These projections and forecasts were not prepared with a view toward compliance with published guidelines or generally accepted accounting principles. No independent accountants have expressed an opinion or any other form of assurance on these projections or forecasts. You should not regard the inclusion of the projections and forecasts described herein as a representation or warranty by VSL, its associates, the authors of this report or any other person that these projections or forecasts or their underlying assumptions will be achieved. For these reasons, you should only consider the projections and forecasts described in this report after carefully evaluating all of the information in this report, including the assumptions underlying such projections and forecasts. The price and value of the investments referred to in this document/material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance. Future returns are not guaranteed and a loss of original capital may occur. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. We do not provide tax advice to our clients, and all investors are strongly advised to consult regarding any potential investment. VSL, the RA involved in the preparation of this research report and its associates accept no liabilities for any loss or damage of any kind arising out of the use of this report. This report/document has been prepared by VSL, based upon information available to the public and sources, believed to be reliable. No representation or warranty, express or implied is made that it is accurate or complete. VSL has reviewed the report and, in so far as it includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. The opinions expressed in this document/material are subject to change without notice and have no obligation to tell you when opinions or information in this report change. This report or recommendations or information contained herein do/does not constitute or purport to constitute investment advice in publicly accessible media and should not be reproduced, transmitted or published by the recipient. The report is for the use and consumption of the recipient only. This publication may not be distributed to the public used by the public media without the express written consent of VSL. This report or any portion hereof may not be printed, sold or distributed without the written consent of VSL. This document does not constitute an offer or invitation to subscribe for or purchase or deal in any securities and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document is strictly confidential and is being furnished to you solely for your information, may not be distributed to the press or other media and may not be reproduced or redistributed to any other person. The opinions and projections expressed herein are entirely those of the author and are given as part of the normal research activity of VSL and are given as of this date and are subject to change without notice. Any opinion estimate or projection herein constitutes a view as of the date of this report and there can be no assurance that future results or events will be consistent with any such opinions, estimate or projection. This document has not been prepared by or in conjunction with or on behalf of or at the instigation of, or by arrangement with the company or any of its directors or any other person. Information in this document must not be relied upon as having been authorized or approved by the company or its directors or any other person. Any opinions and projections contained herein are entirely those of the authors. None of the company or its directors or any other person accepts any liability whatsoever for any loss arising from any use of this document or its contents or otherwise arising in connection therewith. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Securities Market. Ventura Securities Limited

Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079