an assessment of customer centric strategy on the

TRANSCRIPT

AN ASSESSMENT OF CUSTOMER CENTRIC STRATEGY ON THE

PERFORMANCE OF COMMERCIAL BANKS IN KENYA

BY

GIKUHE TIMOTHY WAITITU

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2014

i

AN ASSESSMENT OF CUSTOMER CENTRIC STRATEGY ON THE

PERFORMANCE OF COMMERCIAL BANKS IN KENYA

BY

GIKUHE TIMOTHY WAITITU

A Project Report Submitted to the Chandaria School of Business in Partial Fulfillment

of the Requirement for the Degree of Masters of Business Administration (MBA).

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2014

ii

DECLARATION PAGE

I, the undersigned, declare that this is my original work and has not been submitted to any

other college, institution or university other than the United States International University in

Nairobi for academic credit.

Signed: ________________________ Date: _________________________

Gikuhe Timothy Waititu

This research report has been presented for examination with my approval as the appointed

supervisor.

Signed: ________________________ Date: _________________________

Dr. Peter Kiriri

Signed: _______________________ Date: ___________________________

Dean, Chandaria School of Business

iii

COPYRIGHT

GIKUHE TIMOTHY WAITITU © 2014

All rights reserved. This report may not be copied, replaced, recorded or transmitted by any

electronic or mechanical means without the consent of the copyright owner.

iv

ACKNOWLEDGEMENTS

I am greatly obliged to my supervisor, Dr. Kiriri, whose perceptive comments, scholarly

supervision and assistance reinvigorated and saw me through this research report. His

awareness and direction was also very helpful during my report writing and I would not have

achieved without his direction and patience.

My appreciation also goes to all the library personnel at USIU-A and fellow students who

provided me with direction on the proposal. The library staff who offered me journals and

textbooks and other sources of information that were used in the collecting of this proposal, I

will not forget to be gratifying for your support during this research study.

No research is complete without the help of the respondents from the population. I extend my

sincere gratitude to all the members of the banking industry that took part in this research

study and for taking your time and filling the questionnaires.

Thank you all for all your help for this research study would not have been possible without

your help.

v

ABSTRACT

This study focused on the assessment of customer centric strategy on the performance of

commercial banks in Kenya. It was driven to determine the impact of customer centric

strategy on acquisition and retention of customers in commercial banks; the impact of

customer centric strategy on the profitability of commercial banks; and the challenges facing

customer centric strategies in commercial banks and a way forward for improving these

strategies.

The research design that was used for this study was descriptive research design. The

descriptive technique aided in creating priorities definite to areas under research. The target

population for this study was all commercial banks in Nairobi - Kenya. This population

included all banks that operate in Nairobi. The total number of the population was 43 banks

in Nairobi. The sample size was determined using a census which covered all banks. The

researcher selected three respondents from each bank to bring the sample size to 129

respondents.

Primary data for the study was collected using a structured questionnaire that was developed

by the researcher on the basis of research objectives. The questionnaires were estimated to

take forty five minutes to complete. A letter of introduction was attached to the questionnaire

explaining the purpose of the study. The researcher sought for an approval to conduct the

study within the organization before the questionnaires were administered. Data was

analyzed using descriptive statistics. Data was run through the Statistical Package for Social

Science (SPSS) for a thorough statistical analysis. Analyzed data was presented using tables

and pie charts in order to give a clear picture of the research findings. Percentages, means

and standard deviations were used to discuss the data meaning and correctional analysis was

done based on the feedback from the respondents in order to ensure objectivity and efficiency

of the process.

The study has determined that customer centric strategy creates trust between the

organizations and customers and this trust built in customers‟ leads to continued patronage

between them and the organizations. It has also been determined that customer centric

vi

strategy used in financial institutions ensures that customers are satisfied. From the study, it

can be concluded that building trust in customers is the main drive that enables the

organizations to retain them and this evokes positive feelings from customers leading to their

long-term commitment with the organizations.

The study determined that customer centric strategy enables banks to develop better

relationships with existing clients as well as acquire new customers. The study concludes that

customer centric strategy enables organizations to serving the customer‟s needs and hence

increase customer satisfaction and thus strengthen the organization in terms of growth and

profitability. The study has determined that customer centric strategy creates boundary

conditions for banks to serve their niche markets profitably since the customer centric

strategy offers a clear-cut attitudinal segmentation which is formed on the basis of

identifying attractive segments and it gives a detailed knowledge about the market segments

which allow the banks to determine segment profitability.

The study has determined that the current banks do not face challenges of linking all

accounts associated with customers and neither do they have a difficulty in achieving an

integrated view of accounts due to the different operating platforms and systems. The

challenge of capturing secondary or co-signer accounts is not a daunting task and neither is

identifying parent/child accounts across affiliated businesses and handling probable customer

matches. The study concludes that Kenyan banks have enough agents who have the

appropriate level of knowledge of all products and that customer centric strategy in the

Kenyan banks offers customer-level treatment and not account-level treatment.

This study recommends the adoption of competitive intelligence practices in the banks. The

main four competitive intelligence practices that should be considered for greater

profitability are market intelligence, product intelligence, technology intelligence and

strategic alliance intelligence. In applying competitive intelligence the banks and the rest of

the banking sector will stand to be more profitable and competitive in the international

market.

vii

TABLE OF CONTENTS

DECLARATION PAGE ........................................................................................................ ii

COPYRIGHT ......................................................................................................................... iii

ACKNOWLEDGEMENTS .................................................................................................. iv

ABSTRACT ............................................................................................................................. v

TABLE OF CONTENTS ..................................................................................................... vii

LIST OF TABLES ................................................................................................................. ix

LIST OF FIGURES ................................................................................................................ x

LIST OF ABBREVIATIONS ............................................................................................... xi

CHAPTER ONE ..................................................................................................................... 1

1.0 INTRODUCTION............................................................................................................. 1

1.1 Background of the Study .................................................................................................... 1

1.2 Problem Statement .............................................................................................................. 5

1.3 General Objective ............................................................................................................... 6

1.4 Specific Objectives ............................................................................................................. 6

1.5 Importance of the Study ...................................................................................................... 6

1.6 Scope of the Study .............................................................................................................. 7

1.7 Definition of Terms............................................................................................................. 8

1.8 Chapter Summary ............................................................................................................... 8

CHAPTER TWO .................................................................................................................. 10

2.0 LITERATURE REVIEW .............................................................................................. 10

2.1 Introduction ....................................................................................................................... 10

2.2 Impact of Customer Centric Strategy on Acquisition and Retention of Customers ......... 10

2.3 Impact of Customer Centric Strategy on the Profitability ................................................ 14

2.4 Challenges Facing Customer Centric Strategies in Commercial Banks ........................... 18

2.5 Chapter Summary ............................................................................................................. 22

CHAPTER THREE .............................................................................................................. 23

3.0 RESEARCH METHODOLOGY .................................................................................. 23

viii

3.1 Introduction ....................................................................................................................... 23

3.2 Research Design................................................................................................................ 23

3.3 Population and Sampling Design ...................................................................................... 24

3.4 Data Collection Methods .................................................................................................. 25

3.5 Research Procedures ......................................................................................................... 26

3.6 Data Analysis Methods ..................................................................................................... 26

3.7 Chapter Summary ............................................................................................................. 27

CHAPTER FOUR ................................................................................................................. 28

4.0 RESULTS AND FINDINGS .......................................................................................... 28

4.1 Introduction ....................................................................................................................... 28

4.2 Demographics ................................................................................................................... 28

4.3 Impact of Customer Centric Strategy on Acquisition and Retention of Customers ......... 32

4.4 Impact of Customer Centric Strategy on the Profitability ................................................ 39

4.5 Challenges Facing Customer Centric Strategies in Commercial Banks ........................... 45

4.6 Chapter Summary ............................................................................................................. 49

CHAPTER FIVE .................................................................................................................. 50

5.0 DISCUSSIONS, CONCLUSIONS AND RECOMMENDATIONS ........................... 50

5.1 Introduction ....................................................................................................................... 50

5.2 Summary ........................................................................................................................... 50

5.3 Discussions ....................................................................................................................... 52

5.4 Conclusions ....................................................................................................................... 59

5.5 Recommendations ............................................................................................................. 60

REFERENCES ...................................................................................................................... 63

APPENDIX I: COVER LETTER ....................................................................................... 68

APPENDIX II: QUESTIONNAIRE ................................................................................... 69

ix

LIST OF TABLES

Table 4.1: Respondents Organization ..................................................................................... 29

Table 4.2: Impact of Customer Centric Strategy on Customer Relation ................................ 33

Table 4.3: Impact of Customer Centric Strategy on Building Customer Trust ...................... 34

Table 4.4: Impact of Customer Centric Strategy on Understanding Customers..................... 35

Table 4.5: Impact of Customer Centric Strategy on Customer Satisfaction from Products and

Services ................................................................................................................................... 36

Table 4.6: Impact of Customer Centric Strategy on Data Mining .......................................... 37

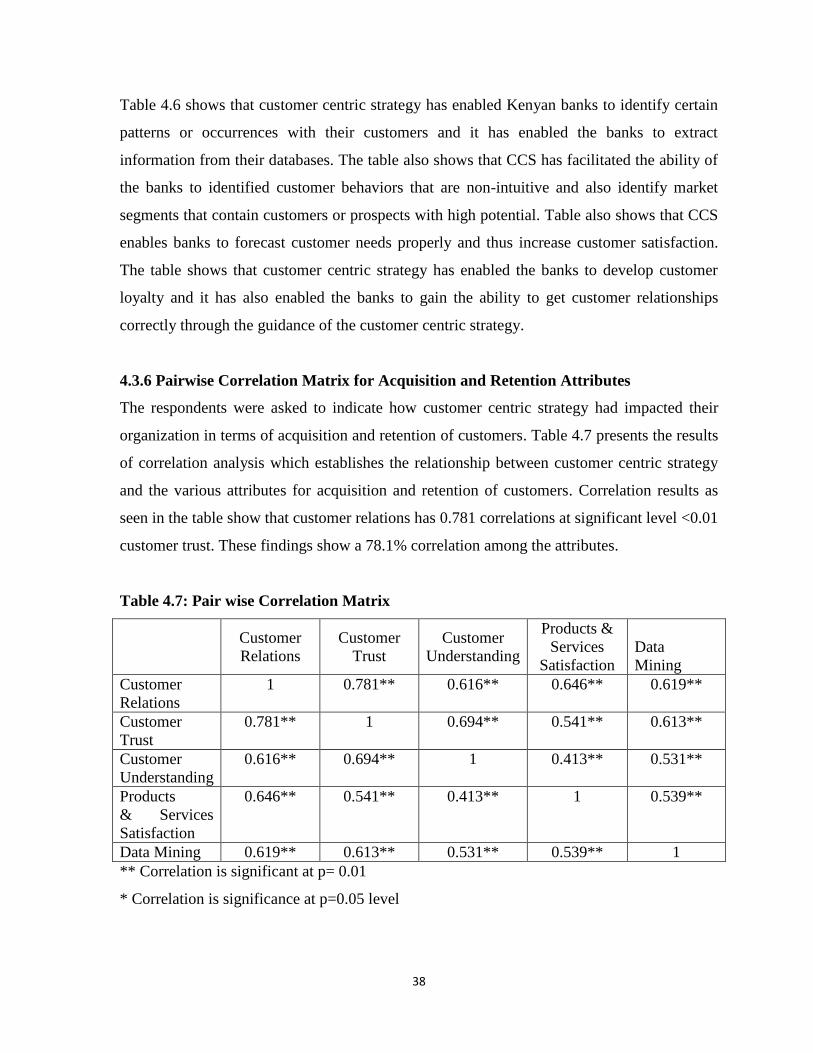

Table 4.7: Pair wise Correlation Matrix ................................................................................. 38

Table 4.8: Impact of Customer Centric Strategy on Organization Profitability ..................... 39

Table 4.9: Impact of Customer Centric Strategy on Creating Niche Segments ..................... 41

Table 4.10: Impact of Anchoring Customer Centric Strategy on Organization‟s Values ...... 42

Table 4.11: Impact of Customer Centric Strategy on Growth in Returns .............................. 44

Table 4.12: Pair wise Correlation Matrix for Profitability Attributes .................................... 44

Table 4.13: Challenges of Customer Data .............................................................................. 45

Table 4.14: Challenges of Treatment and Workflow .............................................................. 46

Table 4.15: Contact Channels in the Organizations................................................................ 47

Table 4.16: Organizational Challenges ................................................................................... 48

Table 4.17: Core Banking Systems ......................................................................................... 49

x

LIST OF FIGURES

Figure 4.1: Respondents Gender ............................................................................................. 28

Figure 4.2: Level of Education ............................................................................................... 29

Figure 4.3: Management Level ............................................................................................... 31

Figure 4.4: Involvement in Customer Centric Strategy .......................................................... 32

xi

LIST OF ABBREVIATIONS

ATMs: Automated Teller Machines

CBK: Central Bank of Kenya

CCS: Customer Centric Strategy

CRM: Customer Relationship Management

FMCG: Fast-Moving Consumer Goods

ICB: Independent Commission on Banking

KBA: Kenya Bankers Association

NAB: National Australia Bank

NSE: Nairobi Securities Exchange

RBC: Royal Bank of Canada

SPSS: Statistical Package for Social Sciences

UK: United Kingdom

US: United States

VIP: Very Important person

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

Intensifying competition and growing customer expectations have made it increasingly

difficult in recent years for companies to keep their customers and do it profitably. Now, new

economic concerns pose new threats to break down the bonds of customer loyalty even

further. Trust is an essential component of loyalty; as consumer confidence wanes, so too

does the basis on which loyalty can be fostered (Bhattacharya, 2011).

To survive and even thrive in today‟s difficult economic environment, many organizations

should take a fresh look at their strategies and methods for retaining customers - and if

necessary renew their commitment to customer centricity (Izquierdo et al., 2005). The threat

of declining customer revenues and defection is real and must be addressed - at the same

time, however, the economic climate creates new opportunities to strengthen market position

and position for growth by building customer trust, providing meaningful brand

differentiation, tailoring offers in light of new customer needs and, if appropriate, negotiating

new terms (Lindgreen et al., 2006). Companies that not only keep but deepen relationships

with their best customers during this weak phase of the economic cycle will be well

positioned to eclipse their rivals when the economy reignites.

Customer Centricity has been defined as an approach to doing business in which a company

focuses on creating a positive and consistent consumer experience at the point of sale,

through the call center, online and via all communications, including mobile, email and print

(Galbraith, 2011). A Customer Centric approach can add value to a company by

differentiating themselves from competitors who do not offer the same experience. A

Customer Centric framework requires connectivity across every channel of the organization,

allowing the consistent delivery of the most appropriate level of service, benefits, and

customer care to each segment of the customer base (Fader, 2012; Kaufmann & Mohammed,

2012).

2

To become customer centric, companies must first become expert in their target markets,

understanding the specific needs of different customers and being clear about how to

combine core products with new services to add value to their customers. This means

recognizing that customers want individual solutions, not generic responses (Wang & Lo,

2004). As one investment bank told a market leading technology supplier, “Your products

and people were great – but your competitor knew more about applying them in an

investment banking environment” (Rogers, 2005).

The second requirement for companies moving to become customer centric is to restructure

to respond to customer needs. In traditional companies, resource deployment, management

controls, core processes and profitability measures are all aligned to products (Christopher et

al., 1991). By contrast, customer centric businesses align all these elements to adding value

to customers, and measure how this converts into profit for the business.

The third requirement recognizes that customer centric businesses need a very different

culture to product centric businesses. Selling and delivering new solutions often means

recruiting new people with different mindsets – who think less „plan and build‟ and more

„sense and respond‟ to react to customer needs. Customer centric companies must reward

people for creating value for customers rather than simply following agreed plans (Fader,

2012).

Retail banks today face significant challenges to growth and profitability. The erosion of

customer trust, the slow economic recovery and margin pressure stemming from a variety of

sources are among the many factors that account for the current difficulties (Wang & Lo,

2004). In search of growth opportunities, many banks are focusing on deepening their share

of wallet with existing customers. In all regions – the United States, Europe, Asia-Pacific and

Africa – financial institutions are launching marketing campaign slogans such as reinventing

the banking industry and deepening customer relationships (Szczepańska & Gawron, 2011).

The goal is to make customers feel that their needs are being looked after – to become in a

nutshell, more „customer centric.‟

3

In the UK, the government has fully accepted the findings of the Independent Commission

on Banking (ICB), set up to investigate the possibility of permanently separating retail from

investment banking. Many banks have already begun the process of transforming their

operating models by decentralizing operations, slashing costs and introducing more cost

efficient processes and technologies (Mohsan et al., 2011).

In Asia-Pacific, authorities are developing a stricter regulatory approach and encouraging

local banks to develop stronger standalone capabilities. With lower labor costs, the major

focus for banks here is on process standardization and efficiency. In the US, banks are

repositioning their products and routes to market to replace lost revenues. Central to this is

moving more low-value transactions to self-service channels such as ATMs, online banking

and mobile. More flexible and user-friendly treasury management systems are also being

introduced to support a renewed focus on corporate in place of retail banking. Australia,

meanwhile, has seen banks looking to customer-centric industries such as fast-moving

consumer goods (FMCG), with beginning-to-end lines of responsibility (Gee et al., 2008;

Mohsan et al., 2011). Staff must accept new skills, training, cultures and behaviors; otherwise

it is the banks which will suffer.

The banking sector in Kenya is facing many challenges posed by the competitive

environment in the industry. The banking sector was liberalised in 1995 and exchange

controls lifted. The Central Bank of Kenya (CBK), which falls under the Minister for

Finance‟s docket, is responsible for formulating and implementing monetary policy and

fostering the liquidity, solvency and proper functioning of the financial system. The CBK

publishes information on Kenya‟s commercial banks and non-banking financial institutions,

interest rates and other publications and guidelines (Thuo, 2010).

The banks have come together under the Kenya Bankers Association (KBA), which serves as

a lobby for the banks‟ interests and addresses issues affecting its members (Kenya Bankers

Association annual Report, 2008). There are forty-six bank and non-bank financial

institutions, fifteen micro finance institutions and forty-eight foreign exchange bureaus in

Kenya. Thirty-five of the banks, most of which are small to medium sized, are locally owned

4

(Central Bank of Kenya annual report 2007). The industry is dominated by a few large banks

most of which are foreign-owned, though some are partially locally owned. Nine of the major

banks are listed on the Nairobi Stock Exchange (NSE). The commercial banks and non-

banking financial institutions offer corporate and retail banking services but a small number,

mainly comprising the larger banks, offer other services including investment banking,

insurance services and custodial services among others (Dikken & Hoeksema, 2001).

Despite the intense growth in the acquisition of CCS in the last 10 years and widely accepted

conceptual underpinnings of CCS/ CRM strategy, critics point to the high failure rate of

implementations as evidenced by commercial market research studies (Foss, Stone & Ekinci,

2008; Petty, 2008). For instance, in one survey of senior executives across five continents

(North and South America, Europe, Asia and Africa), Bain and Company found that the use

of CRM tools had increased from 35 to 78 percent between the years 2000 and 2002, but

satisfaction with the performance of CCS/ CRM was below 50 percent (Ang & Buttle 2006).

An equally elaborate international survey by CSO Insights of 1,337 companies who have

implemented CRM systems to support their sales force has estimated that only 25 percent

reported significant improvements in their performance (Raman, Wittmann & Rauseo, 2006).

According to Jain et al., (2007), 60-70 percent of CCS/ CRM programs have resulted in

either losses or no bottom line improvement in company performance.

However, much as CCS/ CRM initiatives at many companies have failed, more and more

organizations worldwide continue to implement CCS/ CRM strategy (Young 2003).

Conflicting opinions and increased pessimism about the value of CCS/ CRM abound the

marketing literature. Given that CRM is widely adopted by many organizations as a strategic

orientation, the conflicting academic and practitioner opinions on the performance of CRM

strategy adversely affects the development of CCS/ CRM theory and strategic marketing

practice. It is therefore important to study the phenomenon of CCS/ CRM in greater depth

and especially its contributions to organizational performance.

5

1.2 Problem Statement

The retail banking industry is in the midst of a seismic shift. But it‟s not the ups and downs

of the markets that cause the shift. It is the rising power of the customers and changing

regulatory conditions across the globe (Ryals & Payne, 2001). Customers now hold the

power in their relationships with banks. They are more connected, vocal, and on the lookout

for stronger relationships than ever before. They do not just want a place to put their money.

Today‟s consumers want to be understood as people. They are looking for financial advice

and guidance, as well as transparency and trust in these turbulent times. And if they do not

find that in one bank, they simply move on to another. It is much easier for consumers to

switch banks or use multiple banks for their monetary needs than it was in the past (Kotler &

Armstrong, 2011). This newly empowered customer base makes for an uncertain future for

many banks, which in the past were primarily focused inward.

Regulators are also defining new rules for banks about controlling leverage of individuals,

limiting the amount of fees and commissions levied by banks and reinforcing more

transparent communication (Sivadass & Baker-Prewitt, 2000). This time of uncertainty is

also a time of opportunity. Consumers will reward banks with their loyalty and

recommendations if they meet their needs and help them as advisors. Banks can increase

their profitability by balancing their customers‟ needs and expectations with the costs of

doing business. This means providing better products, services, and prices, while also

improving cross-sell ratios and internal efficiencies. This makes being relevant more

important than ever (Hanley & Leahy, 2008). Customer management became one of the most

critical components to economic survival and sustainable growth.

In this time of volatility and unpredictability among financial services companies, the one

constant is customers (Kotler & Armstrong, 2011). Companies that have aligned their

businesses to get, keep, and grow customers have weathered the recent economic turmoil.

The connection between customer centricity and economic strength is no coincidence

(Dikken & Hoeksema, 2001; Sivadass & Baker-Prewitt, 2000; Ryals & Payne, 2001). The

retail banking space is shifting to focus on building relationships with existing customers

through customer-focused operating models.

6

Done right, revenue shall increase while costs decrease, creating sustainable growth. The

following study assesses the effect of customer centric strategy on the performance of

commercial banks in Kenya. It indicates how CCS/ CRM affect customer retention,

organization profitability and the challenges that exist in CCS implementation.

1.3 General Objective

The general objective of this study was to assess customer centric strategy on the

performance of commercial banks in Kenya.

1.4 Specific Objectives

This study focused and was guided by the following specific objectives:

1.4.1 To determine the impact of customer centric strategy on acquisition and retention of

customers in commercial banks.

1.4.2 To examine the impact of customer centric strategy on the profitability of commercial

banks.

1.4.3 To determine the challenges facing customer centric strategies in commercial banks and

a way forward for improving these strategies.

1.5 Importance of the Study

1.5.1 Organization

This research gives an insight on how CCS/ CRM affect organizations when implemented.

The results of the study show organizations the importance of focusing on consumers/

customers and hence will encourage organizations that do not employ CCS/ CRM to adopt

the strategy.

1.5.2 Policy Makers

This research is beneficial to the entire banking industry as it has elicited a need for being

proactive in managing and adapting to the changing environment. The industry is

characterized by intense competition among the market players. It may enable them move

away from the wait and see attitude, which reduces most of them to playing second fiddle. As

7

a result, there may be increased competition originating from all the banks as opposed to the

current top five in the country.

1.5.2 Academicians

This research has added to the immense pool of research work that is already available. To

the academicians, this may be a source of new knowledge in terms of further research to the

one already available. They may use this research for reference and as a motivator for more

or new research on issue not covered.

1.6 Scope of the Study

The study was conducted in all the banks in Kenya, according to the listing that was obtained

from Central Bank of Kenya (CBK) and Kenya Bankers Association (KBA) in April 2014.

This gave a good outlook of how banks are managed change. This study sought to find a link

between CCS/ CRM and performance of banks. The results of this study were therefore

limited to the financial institutions in Kenya given the fact that the study was carried out in

Kenya. The results are limited to all commercial banks that operate in Nairobi since the study

was limited to the capital city geographically.

The researcher targeted the operations managers, financial managers, and customer care

representatives in all banks. This population was selected by the researcher since they had the

idea of what CCS/ CRM strategies they employed and were best placed to give information

in the outcome of their strategies. The collection of data presented a lot of challenges since

getting the targeted population was difficult. The researcher used appointments, some of

which were cancelled at the last minute. To mitigate the challenge, the researcher called in

advance and informed the respondents that questionnaire(s) had been dropped off in their

office in cases where the respondents were not available.

8

1.7 Definition of Terms

1.7.1 Customer Centricity

This is an approach to doing business in which a company focuses on creating a positive and

consistent consumer experience at the point of sale, through the call center, online and via all

communications, including mobile, email and print (Galbraith, 2011).

1.7.2 Customer Relationship Management

This is a model for managing a company‟s interactions with current and future customers. It

involves using technology to organize, automate, and synchronize sales, marketing, customer

service, and technical support (Fader, 2012).

1.7.3 Customer Satisfaction

This is a measure of how products and services supplied by a company meet or surpass

customer expectation (Lindgreen et al., 2006). Customer satisfaction can also be defined the

number of customers, or percentage of total customers, whose reported experience with a

firm, its products, or its services (ratings) exceeds specified satisfaction goals (Bhattacharya,

2011).

1.7.4 Customer Loyalty

Customer loyalty is both an attitudinal and behavioral tendency to favor one brand over all

others, whether due to satisfaction with the product or service, its convenience or

performance, or simply familiarity and comfort with the brand (Fader, 2012).

1.7.5 Customer Retention

Customer retention is the activity a company undertakes to prevent customers from defecting

to alternative companies. Successful customer retention starts with the first contact and con-

tinues throughout the entire lifetime of the relationship (Galbraith, 2011).

1.8 Chapter Summary

This chapter brings out a clear and elaborate overview of the background of the study. The

main highlights brought out in this chapter are the key elements involved in analyzing CCS/

9

CRM. The chapter has introduced readers to what CCS/ CRM is and it has shown the gap the

study aims to fill. The chapter also highlights the scope and importance and finally gives

readers the definition of key terms. The next chapter discusses the literature review of the

study. The third chapter discusses the research methodology adopted for the study. The

fourth chapter presents the results and findings of the study. The fifth chapter gives the

discussions of the study and it gives the study conclusion and offers recommendations for

improvement and further studies.

10

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

This chapter deals with the literature review of past studies on the study topic. The literature

discusses the assessment of customer centric strategy on the performance of commercial

banks in Kenya. It discusses the impact of customer centric strategy on acquisition and

retention of customers in commercial banks; the impact of customer centric strategy on the

profitability of commercial banks; and the challenges facing customer centric strategies in

commercial banks and a way forward for improving these strategies.

2.2 Impact of Customer Centric Strategy on Acquisition and Retention of Customers

One of the basic elements of modern marketing understanding is customer satisfaction

(Fader, 2012). Businesses can survive as long as they can meet the customers‟ needs and

enable customer satisfaction. Determining the consumer‟s wishes and needs and meeting

them is one of the ways of enabling consumer satisfaction. For this reason, it is pretty

important in our intensively competitive environment to be in regular contact with the

customers and to follow the changes in them closely (Gee, Coates & Nicholson, 2008).

One of the sectors in which competition is experienced intensively is that of banking. Banks

are the finance institutions that meet the economic needs of the individuals and businesses

and that perform such economic activities as collecting bank deposits, giving credits,

providing capital, and etc. In recent years there have appeared important developments in the

understanding of modern banking. With the transition to automation, customer satisfaction

and management of customer relationships have taken place among the subjects spoken of in

the banking sector (Fader, 2012).

Customer satisfaction means that customer needs, wishes and expectations are met or

overcome during the product/service period, giving way to re-purchasing and customer

loyalty. In other words, customer satisfaction is the assessment of the pre-purchasing

expectations from the product, with the results reached after the act of purchasing (Mohsan et

al., 2011). A highly satisfied customer according to Kotler and Armstrong (2011) continues

11

his shopping for a long time, buys more as long as the firm produces new products and the

existing products are improved, speaks of the firm and its products with praise, keeps

indifferent to the trademarks that are in competition with the products of the firm and does

not place the emphasis on the price, and offers the firm suggestions and ideas about products

and services.

It is possible to secure the customer loyalty through customer satisfaction. However, the fact

that there are many enterprises that offer products and services of the same quality and at the

same price interval makes it difficult for the enterprises to secure customer satisfaction. It

may even be easy to let the satisfied customer go to the rival enterprises. Today the most

important thing to do about the reduced customer satisfaction is the customer-centred

practices adapted to each customer‟s needs and values. By treating different customers in

different manners, firms can achieve customer loyalty. Customer loyalty is the long and

uninterrupted retention of the relationship by offering service that meets and even goes

beyond the customer needs (Mohsan et al., 2011).

Whether enterprises can make their current customers loyal depends on whether they can

manage the customer relationships well. As customers have grown to be more conscious

consumers, enterprises have had to pay the prices of the errors and faults they do in customer

relationships. The most important quality of the 1990s is that customers revealed their power

then. They realized that they themselves had something to say and have themselves listened

to. The firms, then, understood that they had to listen to their customers so as to be able to

sustain their presence in the market (Raman, Wittmann & Rauseo, 2006). After the 2000s,

with the increased use and effect of the internet and such platforms as discussion groups,

customers had the opportunity to be more powerful and effective against the enterprises.

Thus, enterprises noticed that they could only be successful if they adopted customer-based

marketing.

To retain customers, organizations must focus on customer satisfaction. Organizations must

work at creating and maintaining an ongoing relationship with their customers (Kotler &

Armstrong, 2011). Customer expectations are always high. According to Horowitz, (2004) to

12

keep a customer, you need to get close to the customer and understand his or her wants and

needs. CCS offers organizations the ability to understand their customers and therefore,

enhance retention.

2.2.1 Building Trust

The first strategy employed by CCS is to create trust between the buyer and the organization.

Customer trust plays a major role in customer retention but it does not always guarantee

continued customer patronage (Jones & Sasser, 1995). According to Crosby et al. (2002)

customer satisfaction is a main driver of customer retention and it evokes positive feelings

from the customer. Even though the customer is satisfied it does not mean that they

automatically assume that they will receive the same service or product at all times - it takes

time to build the trust.

Ranaweera & Prabhu (2003) state that satisfaction neither may nor ensure a long-term

commitment, but that organizations who look beyond satisfaction for the customer and allow

the customer to develop trust in the organization do establish long-term relationships with the

customer. Once the trust had been placed, the relationship formed, the likelihood of either

party ending the relationship decreases (Morgan & Hunt, 1994).

2.2.2 Handling Complaints

Research has shown that customers who perceive their complaint has been dealt with

satisfactorily are amongst the most loyal thereafter. Addressing a customer‟s grievance with

honesty and integrity is as good a path to retaining customers (Crosby et al., 2002). A

growing number of customer complaints are caused by fragmentation within a large

organization. According to Gale (1994), there is nothing more annoying that ringing up to

complain and being passed onto another department, it immediately causes a customer to get

angry before they even give their complaint.

Most dissatisfied customers do not complain - they just leave - taking their business with

them. Organizations will not even know they have disappeared until they notice a decrease in

profit. After this the customer will inform business partners and other customers of their

13

experience, about how incompetent the organization is (Gale, 1994). The idea put forward is

to set up a link on a web page, or even something as simple as a grievances box in store to

allow customers vent their annoyances and complaints about the organization, the product or

the service.

2.2.3 Specify Products for Specific Customers

Another strategy presented is to create a specific product for a specific customer (Wyner,

2002). Organizations would identify a niche in the market, and produce the service or

product (Porter, 1995). The difference with this approach is that organizations would find it

easier to retain their customers due to the fact that nobody else would be selling the product

or service in that particular area – it must be noted that organizations should not let their

standards drop because customers will always find an alternative (Conlon, 1999).

2.2.4 Prioritizing the Needs of Key Customers

Another strategy that may be put forward is to ensure that the organization prioritizes the

needs of key customers. Focusing on these customers‟ needs, is not about giving them

everything they want or need, it is about understanding what they are willing to pay for,

delivering that efficiently and capturing the value back through the price (Jamieson, 1994).

The researcher puts forward that it must be clear to the organization who the key customers

are and what exactly they want, this could be achieved through data mining.

2.2.5 Data Mining

Data mining is the process of exploration and analysis by automatic or semiautomatic mean,

of large quantities of data in order to discover meaningful pattern and rules (Berry et al.,

1999). Data mining digs down through data until it finds a certain pattern or occurrence

which will help the organization get to know their customers better through CCS (Story,

1998). Data mining extracts information from a database that the organization did not know

existed. Relationships between customer patterns and customer behaviors that are non-

intuitive are the jewels that data mining hopes to find (Thearling et al., 2000).

14

Through the use of data mining organizations can learn critical information about their

customers. It allows them to identify market segments containing customers or prospects

with high potential (Au et al., 2003). Because organizations can see what customers want

before the customers know themselves, they are able to present this to the customer and

therefore increase satisfaction; this leads to the customer trusting the organization to know

what they want followed by customer retention (Lejeune, 2001).

2.2.6 Securing Loyal Customers

The strategy of securing loyal customers is about locking in valuable customer relationships

(Kale, 2004). He also suggests that it will not be enough to satisfy customers satisfied

customers may leave or switch for no good reason, and loyalty must be built through getting

customers to trust the organization. According to Kendrick and Fletcher (2002), getting

customer relationships correct leads to loyalty; this should ensure that competitors will not

get the organizations customers. Loyalty has a direct link to customer satisfaction and

customer trust. It can be seen that each of these strategies mentioned is unique but they do

require the support of other suggested strategies in order to achieve an overall strategy when

retaining customers (Bowden, 1998).

Despite the apparent absence of an empirical link between satisfaction and behavioral

customer loyalty, several studies show that satisfaction affects customer retention (Bolton,

1998; Bolton, Kannan & Bramlett, 2000). The underlying rationale is that customers aim to

maximize the subjective utility they obtain from a particular supplier (Oliver & Winer,

1987). This depends on, among other things, the customer‟s satisfaction level. As a

consequence, customers who are more satisfied are more likely to remain customers. Thus,

satisfaction positively affects customer retention.

2.3 Impact of Customer Centric Strategy on the Profitability

Becoming customer centric should be a means, not an end. A customer-centric

transformation needs an agenda to further develop existing clients and acquire new ones

(Petty, 2008). Better serving customer needs enables a bank to increase the satisfaction and

loyalty of its customers as well as strengthen the bank‟s economics, both in terms of growth

15

and profitability. It is therefore essential that banks translate all their customer activities into

clear actions that boost revenues (Bohling et al., 2006). When resources are limited, banks

need to give priority to customer segments with the greatest profit potential. Interestingly, it

is not the case that there are just a few large segments that are attractive. The largest profit

potential often resides in smaller niche segments.

2.3.1 Niche Segments

Coulter and Coulter (2002) research has shown that there are many niche segments that may

be financially attractive but cannot currently be served due to their small size. McKinsey has

developed an approach to tap the potential of these segments despite their small size. The

approach is not about enlarging the segments or merging them, but accepting their size and

creating boundary conditions to serve them profitably. This requires market segment

specialists who continuously seek out new niche segments in the market, as well as modular

systems that can rapidly tailor products to the needs of segments (and without additional IT

capacity) (Hanley & Leahy, 2008). Brand management is a further element that is vital for

developing concepts on how to address individual customer segments at low cost. Agile sales

staff is also needed who can swiftly identify and adapt to the needs of niche segments

(Khaligh, 2012).

Clear-cut attitudinal segmentation represents the basis for identifying attractive segments.

Quantitative market research derives this kind of segmentation (Sivadass et al., 2000;

Zineldin, 2006; Gee et al., 2008). Banks can use this to decide which segments are

particularly financially attractive or strategically relevant for the future. Detailed knowledge

about the segments allows you to determine segment profitability, and which marketing and

sales concepts are most suitable for each segment.

Royal Bank of Canada (RBC) pursues this kind of a niche strategy with great success. After

identifying attractive customer groups via micro-segmentation, RBC tailors products for each

group. Their approach comprises three layers of segmentation. First, “basic segmentation”

defines five customer groups using demographic criteria (Foss et al., 2008). Next, “strategic

segmentation” cuts the customer base into a multitude of sub-segments by factors such as

16

profitability, risk profile, or customer life time value. Finally, “tactical segmentation” focuses

primarily on product sales, drawing on parameters such as probability of purchase, risk of

cancellation, or frequency with which products are used (Ang & Buttle, 2006).

2.3.2 Micro-Segments

This micro-segmentation helped RBC detect a previously neglected customer segment:

senior citizens spending the winter in Florida. The bank developed a “VIP Banking” account

for this segment that includes a senior rebate for eligible clients above 60, travel discounts,

easy access to Canadian funds, a consolidated account review online, ability to leverage a

Canadian credit history for mortgages in the US, and a toll-free number for cross-border

banking questions. As a result, over the last five years sales per customer have more than

doubled, the attrition rate has dropped by nearly 50 percent, and net income has grown by 75

percent. Other examples are the Swiss Bank Coop‟s financial advice for women, the Dutch

Rabobank‟s package for the divorced, or Wells Fargo‟s offer for soldiers. Managing all these

opportunities systematically will create a sustainable development agenda (Rogers, 2005;

Ryals & Payne, 2001; Kaufmann & Mohammed, 2012).

2.3.3 Anchoring Customer Centricity Deep within the Company

Customer centricity needs anchoring within the organization to last. This is vital for the

paradigm shift to unfold its full impact. To achieve this, banks need to install customer-

centric core functions, align their governance and adapt their incentive systems accordingly

to initiate real change (Kendrick & Fletcher, 2002).

Key to a higher degree of customer centricity within a bank is having an excellent customer

insights unit. Profound knowledge of customer needs and preferences is an essential input for

decisions. One best-practice example is the National Australia Bank (NAB Europe), which

has pursued a CRM strategy for over 10 years, and has won numerous awards for its efforts

(Morgan & Hunt, 1994). One of the main takeaways from this long-term project has been the

importance of educating the front line to drive employee buy-in. NAB considers a

partnership approach crucial for driving adoption via a staged approach. This includes

gaining executive buy-in by embedding the concept within the group strategy, introducing

17

rigorous measurement and coaching/mentoring, and pursuing a carefully planned process of

cultural change. NAB also understands that this cannot be a “one-off” effort: it requires

continual focus and development (Zineldin, 2006).

To drive and support this task, NAB developed a central Customer Knowledge and

Analytical Marketing team that worked closely with all parts of the organization to develop

and implement its strategy. This customer perspective is applied right up to senior executive

level, with a scorecard that includes customer and community as well as employees and

culture metrics (Szczepańska & Gawron, 2011). A Customer Council (chaired by the Group

Chief Executive Officer) also meets on a monthly basis to ensure an ongoing focus on

customer relations and service.

The core functions need to be designed to represent customer focus within the organization.

It is important that they have the power to implement solutions to the customer‟s benefit. If

this is not the case, there is a danger they will become just an appendage, which could

quickly weaken the newly won trust of the customer (Raman et al., 2006). Besides such

powerful core functions, banks also need overarching customer and product management.

Only interface functions of this kind can ensure that the voice of the customer will be

integrated in all core business processes. Last but not least, anchoring customer centricity in

employees‟ hearts and minds is crucial. A transformation can only be successful if staff live

and breathe this dedication to the customer (Jain et al., 2007). To support this, the balanced

scorecard and incentive systems for each employee need to be targeted towards customer

centricity. Anchoring customer centricity deep within the company implements the

transformation consistently, from the vision and operational processes through to individual

targets for every employee (Bohling et al., 2006; Brown & Gulycz, 2002).

2.3.4 Growth and Returns

Customer centricity, when conceived and implemented correctly, is not just a sentiment – it

makes a clear difference to the bottom line. McKinsey experience and research show that a

customer-centric view leads to greater loyalty, higher cross-selling, less attrition, and

ultimately to higher sales and profits.

18

It will come as no surprise that a lack of public and client trust is one of the biggest

challenges this industry is facing, although a recent McKinsey survey conducted in 2008

shows that customer intimacy and trust are the most important loyalty drivers (77 percent),

ahead of staff (though still rated extremely high, at 75 percent), service (66 percent), and

price (57 percent). Related surveys (Coulter & Coulter, 2002; Khaligh et al., 2012; Wang &

Lo, 2004; Zineldin, 2006) also revealed that improved customer knowledge and a 360°

customer perspective correlates with an increase in money in balances and accounts of 150

percent, four times the improvement in customer experience scores and almost twice the

number of referrals and leads to branches/financial advisers (Baker, 2003). In total, a

customer-centric structured needs assessment leads to 30 percent higher cross-selling of non-

deposit products. As a result, bank branches that use a customer-centric structured needs

assessment; derive profits 2.5 times above those with a minimal needs assessment. Banks can

achieve sustainable growth and above-average profitability by embarking on a customer-

centric transformation (Gee, 2008).

Successful transformation towards a customer-centric company starts with a diagnosis of the

status quo. McKinsey‟s customer-centric transformation framework can provide a first grid

for a thorough assessment. The “timeless tests of customer centricity” can serve as an

objective discussion platform for such an endeavor. The answers provide clear indications of

the bank‟s current status on the way to its customers‟ hearts and minds. McKinsey has

developed a short three-week diagnostic tool along these questions to determine the answers

using a sound fact base. Having this diagnostic in place could be the starting shot to

embarking on a both exciting and profitable journey into the future.

2.4 Challenges Facing Customer Centric Strategies in Commercial Banks

There are a number of the key challenges that banks face in developing and implementing

customer-centric operations. Difficulties are focused in the areas of customer data,

treatment/workflow, contact channels and organization. While they are addressing these

challenges to some degree, there is significant opportunity for further improvement.

19

2.4.1 Customer Data Challenges

The ability to link all accounts associated with a customer is essential to customer centricity

because it allows lenders to manage interactions holistically. Zineldin (2006) states that, an

integrated view of accounts is difficult to achieve due to different operating platforms and

systems. He also states that capturing secondary or co-signer accounts, identifying

parent/child accounts across affiliated businesses, and handling probable customer matches

were among their key challenges.

In response, some companies are addressing this procedurally by asking customers for other

accounts and then linking them to customer IDs, while others are using automated matching

algorithms. There is also a trend toward moving to a single default management platform for

collections, recovery and loss mitigation, allowing organizations to interact with the

customer from a single, integrated source (Galbraith, 2011).

2.4.2 Treatment and Workflow Challenges

Determining the right actions to take for multi-account customers requires access to

customer-level account information, agents with an appropriate level of knowledge of all

products, and treatment strategies that are executed using customer-level, rather than

account-level, workflows (Berry, 1999; Conlon, 1999).

Multiple platforms make it difficult for organizations to get a full view of the customer

relationship. Kale (2004) states that, such a view is available only through a separate system,

which slows down collector responsiveness. Where companies attempt to collect in a

customer-centric manner, different accounts are routed to different work queues, resulting in

disjointed or redundant treatments. In addition, collecting across multiple accounts and

products at once presents the challenge of how to allocate available dollars to pay the various

accounts.

Organizations these challenges by starting with a customer-centric approach across a subset

of related products (for example mortgages and home equity), which reduces the training

challenge. Another first step is to work around the limitations of account-level workflow with

20

procedures such as checking for accounts already in treatment before contacting the customer

(Kendrick & Fletcher, 2002; Story, 1998; Wyner, 2002). It should be noted that several

organizations have moved beyond these initial approaches to make more fundamental

changes, including agents trained on all products, customer-level workflow, cross-product

negotiation and payments, and an integrated default management platform (Gale, 1994;

Bolton et al., 2000). In most cases, payment allocation determination is being left to the

customer.

2.4.3 Contact Channel Challenges

As consumers seek greater ease of access and higher levels of personalization from their

creditors, they are moving their transactions to an ever-growing spectrum of channels - and

the providers that best support their preferences. Ryals and Payne (2001) identified a lack of

prime channels for younger customers, capturing and using customer preferences and

permissions, measuring channel effectiveness, and regulatory compliance as their main

customer contact challenges.

As the market shifts, these organizations are adding channels such as e-mail, text, mobile and

web-based services including chat and virtual agent, making self-service options available,

and focusing on making the best use of each contact (Kaufmann & Mohammed, 2012). To

that end, they are using experimental design and business intelligence tools to understand the

impact of these contact methods for different customer segments.

2.4.4 Organizational Challenges

A siloed organization creates inconsistencies in customer treatment and misalignment with

customer needs. Organizational challenges for customer-centric default management include

recent regulatory changes and senior managers who are more focused on revenue generation

(Izquierdo, 2005). Another frequently raised issue was lines of business with “siloed

thinking” and misaligned incentives. The lines of business are incented to focus on

maximizing collections on their products, as opposed to the entire relationship.

21

To address these challenges, some companies are conducting focus groups with customers to

determine the target experience and then tracking performance vs. target. Additionally, they

are trying to prove relationship concepts by starting with a subset of similar products. Finally,

some managers are aligning their initiatives with enterprise-level, customer-centric projects

to raise visibility and priority with senior management (Ang & Buttle, 2006).

2.4.5 Core Banking Systems

Today, several banks in the US are bleeding due to their rigid legacy systems. It has been a

challenge for the banks to live with these systems because the process is painful, right from

accessing information to integrating new channels, products and services. Maintaining these

systems (finding and retaining the skill set to maintain outdated technology platform) is

another challenge for the banks (Raman et al., 2006). Considering all these factors, several

banks are moving on to new core banking platforms.

Given the magnitude and nature of such transformations, many a time key issues such as

customer-centricity are overlooked or compromised. In several cases, decision makers are

under the impression that core banking replacement will enable them to achieve customer-

centricity (Coulter & Coulter, 2002; Gee et al., 2008). The reasons why core banking

applications fall short of achieving customer-centricity are: though core banking allows

banks to consolidate their deposits, loans, transfers, payments, liquidity and other lines of

business, they prefer specialized product processors for specialized businesses such as FX

Trading, Wealth Management, Trade Finance, and so on. Due to the multiplicity of

applications, banks are unable to get a single view of the relationships with their customers;

and core banking applications do not provide the capability to create and manage

relationship-based offerings (Baker, 2003).

2.4.6 Integrated Data Hub / Data Warehousing

In most banks, each business line operates in a silo, and even within each line of business

there are multiple product processors. A classic example would be the Payments business.

Almost each department in the bank deals with Payment and most of them (if not all) have

their own payment processing applications. This leads to the creation of disparate silos of

22

information inside the organization (Brown & Gulycz, 2002; Wang & Lo, 2004). With deep-

rooted legacy systems and resistance to change, it is not easy to replace these systems to

create a homogeneous infrastructure.

Several banks have created, or are in the process of creating an integrated data hub to get

information in the de-normalized form, to support the decision making process. With an

integrated data hub combined with state-of-the-art business intelligence solutions, banks may

have the answer to their immediate requirements, but are still far from implementing

customer centric strategies. In order to extend this approach to customer centricity, banks

need to translate the intelligence assembled into customized product offerings with

personalized pricing (Sivadass & Baker-Prewitt, 2000; Hanley & Leahy, 2008).

2.4.7 Price Optimization

Price Optimization is the method of finding the right price for a specific customer by

channel, segment, geography, market or product. With predictive capabilities such as price

elasticity of customer segment, price optimization systems have proved to be good decision

support tools. The scope of these systems has by far been restricted to the retail lending

business (Rogers, 2005).

According to Gartner research, out of the 34 banks surveyed worldwide (more than half were

based in the US), 55 per cent have adopted some form or the other of price optimization

systems. Price optimization is a very specialized tool for deciding the price of a particular

product for a target customer segment (Petty, 2008). However, it is only a small component

in the implementation of overall customer-centric strategies.

2.5 Chapter Summary

This chapter has relied on secondary data to explain in detail the opportunities provided by

CCS to organizations as well as showing how CCS is profitable to organizations. The chapter

has highlighted the challenges that exist in implementing CCS and the various strategies that

various banking units around the world are coping with these challenges. The next chapter

discusses the research methodology.

23

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

3.1 Introduction

This section presents the tactics of research methodology that were embraced by the

researcher during the study. It comprises of a blue print for the collection, measurement and

analysis of data. It therefore analyses the research design, population and sampling design,

data collection methods, research procedures and data analysis methods.

3.2 Research Design

Kumar (2008) outlines research design as methods used in conducting research. The

appropriateness of a research technique depends on numerous issues including but not

limited to the research problem and the complexity of knowledge necessary for the

phenomena in question. Allyn and Bacon (2007) define research design as the overall

strategy that you choose to integrate the different components of the study in a coherent and

logical way, thereby, ensuring one effectively addresses the research problem; it constitutes

the blueprint for the collection, measurement, and analysis of data. They also state that the

research problem determines the type of design one can use, not the other way around.

The research design that was used for this study was descriptive. Descriptive research is

intended to obtain data that defines the features of the topic of concern in the research (Hair,

Money, Samouel & Page, 2007). The descriptive technique aided in creating priorities

definite to areas under research such as assessing customer centric strategy on the

performance of commercial banks in Kenya. The investigation design was suitable as it gave

decisive results on the objectives of the study as well as enabled the researcher to use the

survey method. The design enabled the researcher to determine how customer centric

strategy (independent variable) impacted the performance of commercial banks (dependent

variable).

24

3.3 Population and Sampling Design

3.3.1 Population

Population is a collection of knowledgeable persons also known as universe (Hair et al.,

2007). According to Cooper and Schindler (2003), a population is the entire collection of

fundamentals about which a researcher needs to make implications. The target population for

this study was all commercial banks in Nairobi - Kenya. The total number of the population

was therefore, all 43 banks in Nairobi.

3.3.2 Sampling Design

3.3.2.1 Sampling Frame

Sampling is a way of choosing some part of the group to symbolize and represent the entire

group of the population of concern (Yin, 2003). It decreases the research period required to

complete the study, it is controllable, cut costs, and it is virtually a mirror to the population.

Sample frame is a broad list of the elements from which the trial is drawn (Hair et al., 2007).

It is a goals list of the population from which the researcher can create a selection. Allyn and

Bacon (2007) define a sample frame as a set of information used to identify a sample

population for statistical treatment. A sampling frame includes a numerical identifier for each

individual, plus other identifying information about characteristics of the individuals, to aid

in analysis and allow for division into further frames for more in-depth analysis. The

sampling frame for this study was the list of all licensed commercial banks in Kenya that

operate in Nairobi; the listing that was obtained from Central Bank of Kenya (CBK) and the

Kenya Bankers Association (KBA) in April 2014.

3.3.2.2 Sampling Technique

According to Coopers and Schindler (2003) a census is an attempt to collect data from every

member of the population being studied rather than choosing a sample. Kumar (2008), states

that some populations can be easily identified, such as every member participating in a

particular event at a particular time. However, censuses can also be taken of less obvious

groups such as research that collects data from every person entering a specified supermarket

between 2 pm and 4 pm on a specified day would be a form of census (Coopers and

25

Schindler (2003). In this study, the researcher employed a census study where all commercial

banks in Nairobi were sampled.

3.3.2.3 Sample Size

Meredith (2008) defines a sample as a small part of anything or one of a number, intended to

show the quality, style, or nature of the whole; specimen. In statistics, a sample is defined as

a subset of a population to study a sample of the total population (Ronet, 2007). Cooper and

Schindler (2003) poised that, the sample must be warily selected to be representative of the

population and the researcher also desires to certify that the subdivisions involved in the

analysis are correctly catered for. The researcher selected three respondents from each bank

to bring the sample size to 129 respondents. The distribution was as shown in the table.

3.4 Data Collection Methods

The choice of research tools hinge on the kind of data to be composed. This study comprised

of both primary and secondary data. Secondary data was used to form the foundation of the

study while primary data was gathered by questionnaires in order to successfully achieve the

set objectives. Instruments like observations interviews, and document reviews are good for

qualitative studies while questionnaires standardized measuring schedules and observation

schedules are valuable in quantitative studies (Stake, 1995; Stillwell & Clarke, 2011). Data

was collected using a structured questionnaire that was developed by the researcher on the

basis of research objectives.

According Wilkinson and Birmingham (2003), questionnaires are fairly low-priced to

administer, can be established with slight training and are easy to examine and analyze once

they are finished. The questionnaire was divided into various parts that were guided by the

study objectives. The questionnaire had a five point like scale that contained a series of

statements that expressed the various impacts observed by the respondents. A likert measure

permits the respondent to ratio a question on a gauge of ranges given. A likert scale is

boundless for consenting respondents to rate a precise item (Cargan, 2007; Silver et al.,

2012). The likert scale was used by the researcher since the researcher wanted the

26

respondents to give a view on specific items of the study. The likert measure was specific for

graphical control and comfort of analysis.

3.5 Research Procedures

The questionnaire that was used in the study based on the research objectives was pre-tested

to establish the appropriateness of the tool before the real administration. According to

Mugenda and Mugenda (2003), pre-testing enhances the reliability of the data collected for

the research. This was done by administering the questionnaire to three different respondents

who were selected randomly from the population of the study but were not be part of the

final study sample.

The questionnaires were estimated to take forty five minutes to complete. A letter of

introduction was attached to the questionnaire explaining the purpose of the study. The

researcher sought for an approval to conduct the study within the organization before the

questionnaires were administered. The researcher then administered the refined

questionnaires to the target population. The questionnaires were administered through a drop

and pick format. Follow up reminders were sent through emails, text messages and phone

calls in order to achieve a high response rate.

3.6 Data Analysis Methods

The quantitative technique of data analysis is supported by statistical tools which are

beneficial when the researcher seeks to generalize the results after collection of data is

organized and analyzed (Splitzlinger, 2006). According to Mugenda and Mugenda (2003),

expressive statistics includes a procedure of changing a mass of underdone data into charts,

tables, with frequency distribution and fractions which are a vital part of making logic of the

data. To ensure easy analysis, the questionnaires were coded according to each variable of

the study to ensure the margin of error was minimized and to ensure accuracy during

analysis.

The data was run through a computer program known as Statistical Package for Social

Sciences (SPSS) for computation of the mean, standard deviation, and frequency distribution

27

for analysis. Data was analyzed using descriptive statistics. Analyzed data was presented

using tables and figures in order to give a clear picture of the research findings at a glance.

3.7 Chapter Summary

The chapter describes the methodology that was used in carrying out the study. The research

design was descriptive in nature. The population of the study was the staff members working

in the various commercial banks in Kenya. The sample size was 129, the sampling

techniques used was census. The chapter has also indicated that, data was analyzed with the

help of a computer programme SPSS for statistical computations such as the mean and

standard deviation and presented in inform of charts and tables. The next chapter presents the

findings of the research.

28

CHAPTER FOUR

4.0 RESULTS AND FINDINGS

4.1 Introduction

This chapter presents the results and findings of the study on the „assessment of customer

centric strategy on the performance of Commercial Banks in Kenya. The first section

presents the background information of the respondents, while the second section presents

findings in the impact of customer centric strategy on acquisition and retention of customers.

The third section looks at the relationship between Customer Centric Strategy and the

profitability of the organization while the forth section focusses on the challenges facing

customer centric strategies in Commercial Banks in Kenya.

The researcher gave out 129 questionnaires to the selected respondents for the study. The

researcher received a total of 98 questionnaires that were completely filled. This gave the

research a response rate of 75.9% which is above the required threshold of 51% for a study

research.

4.2 Demographics

4.2.1 Respondents Gender

The researcher wanted to determine the gender divide of the respondents and as shown in

Figure 4.1, 64.3% were male and 35.7% were female; this showed that majority of the

respondents were male.

Figure 4.1: Respondents Gender

63

35

29

4.2.2 Level of Education

The researcher wanted to determine the level of education of the respondents and their

response was as shown in Figure 4.2. From the figure most of the respondents had attained

their degree and masters since 44.9% had degrees and 36.8% had a master‟s degree. The

figure also shows that 12.2% had their diploma and 6.1% had their PhD. The results indicate

that the respondents were well educated and could easily understand the questions making

them practical for the study.

Figure 4.2: Level of Education

4.2.3 Organization Worked

The respondents were asked to indicate the organizations they worked for and the results

received indicated that all banks were represented in the study. Majority of the banks had at

least two representatives while some had all three representatives. These results go hand-in-

hand with the initial target set by the researcher where a representative was selected from all

banks in the country.

Table 4.1: Respondents Organization

Banks

Distribution

Number Percent

Victoria Commercial Bank 2 2

Prime Bank (Kenya) 2 2

Oriental Commercial Bank 2 2

PhD 6

Masters 36

Degree 44

Diploma 12

30

Jamii Bora Bank 2 2

Gulf African Bank 4 3.6

Guaranty Trust Bank 2 2

First Community Bank 2 2

Equatorial Commercial Bank 2 2

Development Bank of Kenya 4 3.6

Citibank 2 2.4

ABC Bank (Kenya) 2 2

Bank of Baroda 4 3.6

FINA Bank 4 3.6

NIC Bank 1 1.6

Imperial Bank Kenya 4 3.6

Ecobank 1 1.6

Consolidated Bank of Kenya 2 2

CFC Stanbic Holdings 4 3.6