accelerating digital transformation in latin american_ la_dx_en_… · · 2016-11-30responsive...

TRANSCRIPT

Why are 3rd Platform Technologies Important to Successful Digital Transformation

Accelerating Digital Transformation in Latin America:

Agenda

ICT Industry in Transition

3rd Platform: Business evolution

Digital Transformation

Threat of new entrants

New buyers in Technology

13rd Platform:

Business evolution

Source: Economist Intelligence Unit, June 2016

2.1%

-3.8%

2.1%3.1%

0.3%

2.5% 3.2%

-5.7%

-0.8%-3.0%

1.8%2.2%

-2.8%

2.6%3.9%

-13.9%

3.0%

1.0%2.3% 2.8%

-0.1%

3.0%4.5%

-8.3%

Argentina Brazil Chile Colombia Ecuador Mexico Peru Venezuela

GDP growth (%)

2015 2016 2017

5

So how is the big picture looking?

Source: IDC Black Book Q2 2016

6

IT Spending by Country

Total IT Market by Country, Current USD (Δ) 2015-2016

LA

Argentina Brazil Chile Colombia Mexico Peru Venezuela

-13.4%

27.6%

-2.6%

-7.8%

-0.2%-2.1%

-9.6%

-7.5%

-14.2%-12.0%

-5.2%

-8.6%-6.6%

9.3%

2015 2016

© IDC Visit us at IDC.com and follow us on Twitter: @IDC

7

The Move to Digital Transformation (DX)

Source: IDC Latin America Buyer Pulse, 2016 Q2

8

The 2nd Platform remains the bread and butter of IT

• $5.2 billion in total TCV (2015)

• 500 IT outsourcing contracts

• 173 vendors (HW, SW and Services)

– 355 end users represent 35% total

TCV

• 10% contracts utilize cloud — potential for

between $500 million and $600 millon

reduction in total TCV

TCV

$250 Million - $1 Billion

$100 Million - $250 Million

$10 Million - $100 Million

$10 Million and under

Source: IDC Latin America Quarterly Mobile Phone, Tablet and PC Tracker, 2015 Q3

9

Has the smartphone fever ended?

0

20

40

60

80

100

120

140

160

180

200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Mill

ion

s

Unit shipments by device type, Latin America

Desktop PC Laptop PC Tablet Smartphone

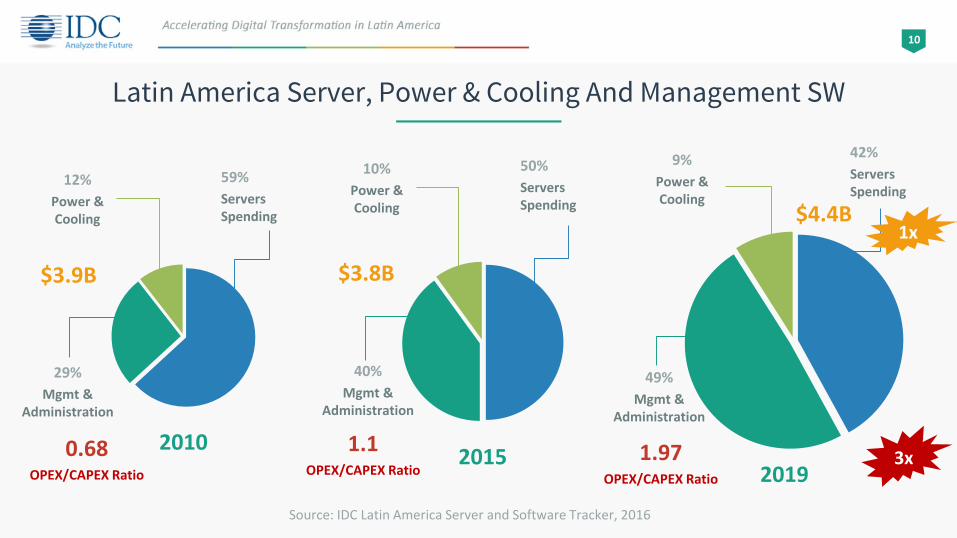

Source: IDC Latin America Server and Software Tracker, 2016

10

Latin America Server, Power & Cooling And Management SW

2010

59%

Servers Spending

12%

Power & Cooling

29%

Mgmt & Administration

$3.9B

0.68OPEX/CAPEX Ratio

2015

50%

Servers Spending

10%

Power & Cooling

40%

Mgmt & Administration

$3.8B

2019

42%

Servers Spending

9%

Power & Cooling

49%

Mgmt & Administration

$4.4B1x

3x1.1

OPEX/CAPEX Ratio1.97

OPEX/CAPEX Ratio

Source: IDC Latin America Cloud Services Tracker, 2015

11

Private Cloud will stand out in size but Hybrid Cloud appears with higher CAGR by 2018

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2014 2015 2016 2017 2018

LA Total Cloud Services Market, 2014 - 2018 MUSD Constant

Public Cloud Private Cloud Hybrid Cloud

2014 – 2018 CAGR 43.6%

2014 – 2018 CAGR 28.9%

2014 – 2018 CAGR 38.5%

Source: Latin America ICT Business Services Tracker 2015

12

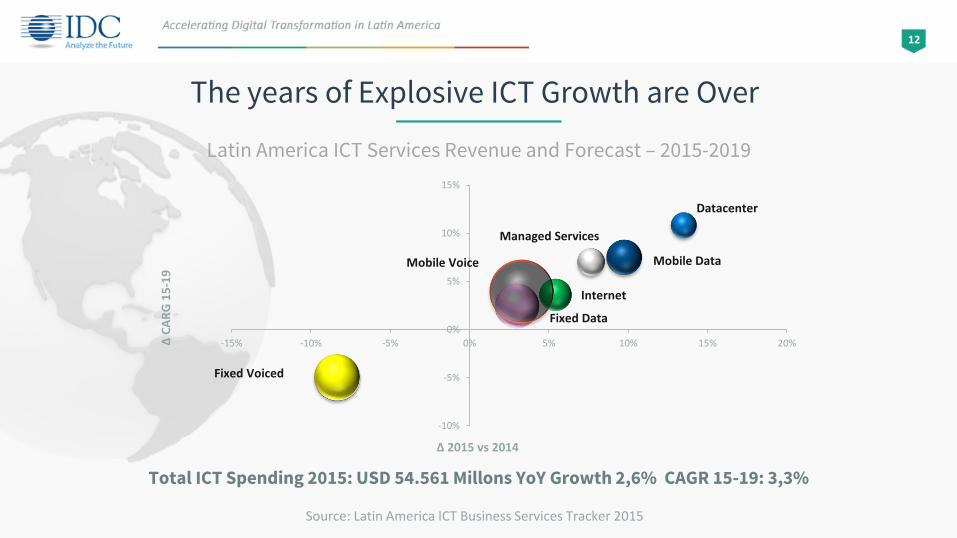

The years of Explosive ICT Growth are Over

Latin America ICT Services Revenue and Forecast – 2015-2019

Fixed Voiced

Fixed Data

Internet

Mobile Voice Mobile Data

Datacenter

Managed Services

-10%

-5%

0%

5%

10%

15%

-15% -10% -5% 0% 5% 10% 15% 20%ΔC

AR

G 1

5-1

9

Δ 2015 vs 2014

Total ICT Spending 2015: USD 54.561 Millons YoY Growth 2,6% CAGR 15-19: 3,3%

Source: IDC Latin America SW Tracker, 2015

13

3rd Platform Opportunity Scorecard

388 US$M

Mobile Market

YOY

17%

301 US$M

Virtualization

YOY

9%

2,430 US$M

Private Cloud

YOY

20%

616 US$M

Management

YOY

7%

365 US$M

Data Storage

YOY

6%

Mobile Market: Enterprise Mobility Management + Enterprise Mobile App Development SW + Mobile Enterprise Security SW

Y0Y: 2016-2017

Source: IDC Latin America Buyer Pulse, 2016 Q2

14

The Intersection of Technology and Business with 3rd Platform and DX

Leadership

Operatingmodel Worksource

InformationOmni-

experience

Source: IDC Latin America IT Investment Trends, 2016 Q1

15

Aligning the CIO Office with the C-Suite

Organization’s Top ICT Priorities

Reduce Organization Cost

Improve Organization Business Process

New and/or improved products and services

Customer acquisition and retention

Improve organization's ability to attract and retain workforce

25%

23%

13%

12%

11%

2Digital

Transformation

Source: IDC Latin America IT Investment Trends, 2016 Q1

17

Addressing the Gaps with DX

Leadership Transformation

Omni-Experience

Transformation

InformationTransformation

Operating ModelTransformation

WorkSourceTransformation

Develop a vision for the digital

transformation of the business

Attract and grow loyalty

with customers

Leverage information for

competitive advantage

Make business operations more responsive and

effective

Transform the way talent is accessed,

connected, and leveraged

Managed

Digital TransformerOpportunistic

Digital Explorer

Ad Hoc

Digital Resister

Repeatable

Digital Player

Optimized

Digital Disrupter

Digital Transformer

Digital Explorer

Digital Resister

Digital Player

Digital Disrupter

7.0%

30.6%

35.9%

70%

Source: IDC Latin America IT Investment Trends, 2016 Q1

70% of enterprises in LATAM are in the early stages of the (DX) journey

Digital Transformation is the approach by which enterprises drive changes in their business models and ecosystems by leveraging digital competencies.

1.Digital transformation initiatives are disconnected and poorly aligned with the enterprise strategy, not focused on customer experiences. 2. The organization has identified a need to develop digitally enhanced customer business strategies but execution is on an isolated project basis.3. Digital Transformation goals are aligned at the enterprise level to a near-term strategy, and include digital customer product and experience initiatives4. Integrated, synergistic transformation management disciplines to deliver digitally enabled customer-centric products, services, and experiences on a continuous basis5. Enterprise is aggressively disruptive in the use of new digital technologies and business models to impact the market and create new businesses.

18

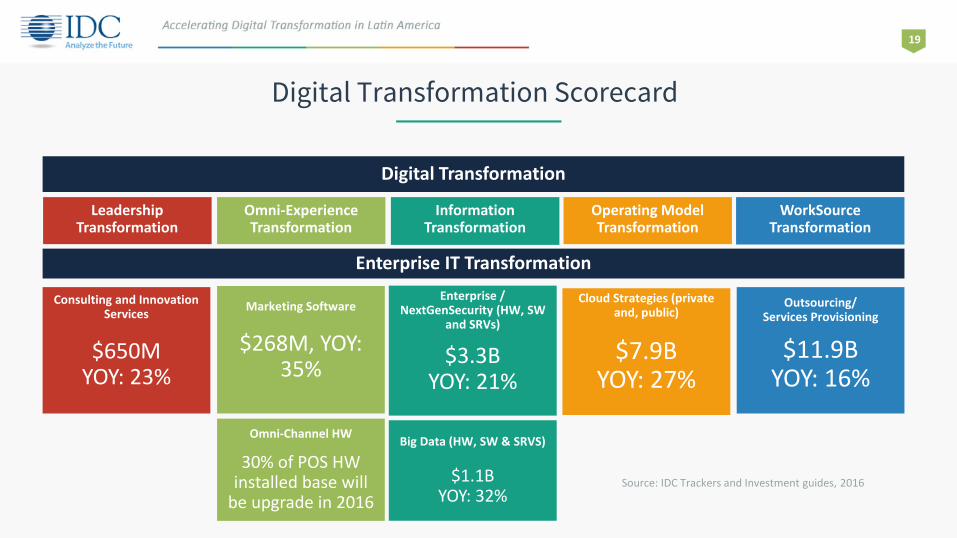

Digital Transformation Scorecard

Big Data (HW, SW & SRVS)

$1.1BYOY: 32%

Leadership Transformation

Omni-Experience Transformation

InformationTransformation

Operating ModelTransformation

WorkSourceTransformation

Digital Transformation

Omni-Channel HW

30% of POS HW installed base will

be upgrade in 2016

Enterprise / NextGenSecurity (HW, SW

and SRVs)

$3.3BYOY: 21%

Cloud Strategies (private and, public)

$7.9BYOY: 27%

Outsourcing/ Services Provisioning

$11.9BYOY: 16%

Consulting and Innovation Services

$650MYOY: 23%

Marketing Software

$268M, YOY: 35%

Enterprise IT Transformation

Source: IDC Trackers and Investment guides, 2016

19

3Threat of new

entrants

21

3rd Platform on Service Providers

Source: IDC Latin America IT Investment Trends, 2016 Q1

• Return to the networks• Compete in cloud, security

via SoC, workspace via collaboration suite, video/immersive experience including AR/VR

• ‘App’-aware/optimization is the competitive edge

• Midsize to large enterprises are target markets as SMBs go to AWS and other 3rd Platform cloud providers

• Complementary SI/ISV capabilities required to stay relevant/competitive

Telcos DC providers and hosters

Factors Impacting CAPEX Evolution into Service Providers

Latin America 2015-2016 $ 4,637

20

14

20

15

20

16

10%

$ 3,626

$ 4,234

Service Providers Networks continue to experience severe bandwidth constraints because of the high data transit driven by OTT, Mobile data and Big Data, long with the pressure by Web 2.0 companies, and cloud service providers

Major Broadband network and expansion of datacenter deployments create significant demands of critical infrastructure, mostly of networks

The next few years will result into significant adoption of IT technology aimed to improve efficiency in the largely vertical integrated world of telecommunications infrastructure

Service providers will continue to invest heavily in their networks to cope connectivity and convergence challenge in the region. This boosts 4G/LTEnetwork implementations

CSP Investments in upgrade to Metro network infrastructure that combines packet optical transportation and IP Routing/Ethernet Switching will be necessary to support high metro data growth rates and emerging WAN-Cloud Connecting services

SDN, NFV & Network Virtualization architectures are becoming crucial to service provider’s ability to improve capacity planning and offer to enable new private virtual enterprise cloud service offerings

17%

Million of Dollars

Total IT SP Spending & DriversLatin America 2014-2016

22

Mobility continued growth drives Cloud Computing adoption

-

50

100

150

200

250

2008 2012 2016Land Voice Mobile Voice Land Data Mobile Data

42%

13%15%

20%9%

16%

23%

43% 42%

Land voice declining | Steady growth of mobile voice | Land & mobileData keep growing

Latin America Telecomm Services Revenues

The future is mobile data

Land Voice

Land Data

Mobile Voice

Mobile Data

-3%

5%

4.6%

15.0%

Argentina2015 – 2018 CAGR

-7%

3%

-3%

10.2%

Brazil

0%

2.1%

3%

15.0%

Chile

1%

6%

15%

11.1%

Colombia

2%

3%

6%

11.0%

Mexico

Latin America Telecomm Services Revenues by Country

US$ Billions

24

35% 25% 18%

Public Cloud Services in Latin America by Business Model (US$M current), 2015

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0% 10% 20% 30% 40% 50%

Shar

e (%

)

Growth (% YoY)

25

Source: IDC Latin America Cloud Services Tracker, 2015

Local/ Regional DCTelco companies

Software Companies

System Integrators (SI)

Cloud born companies (AWS/Azure)

3rd Generation of Digital Commerce is Here

26

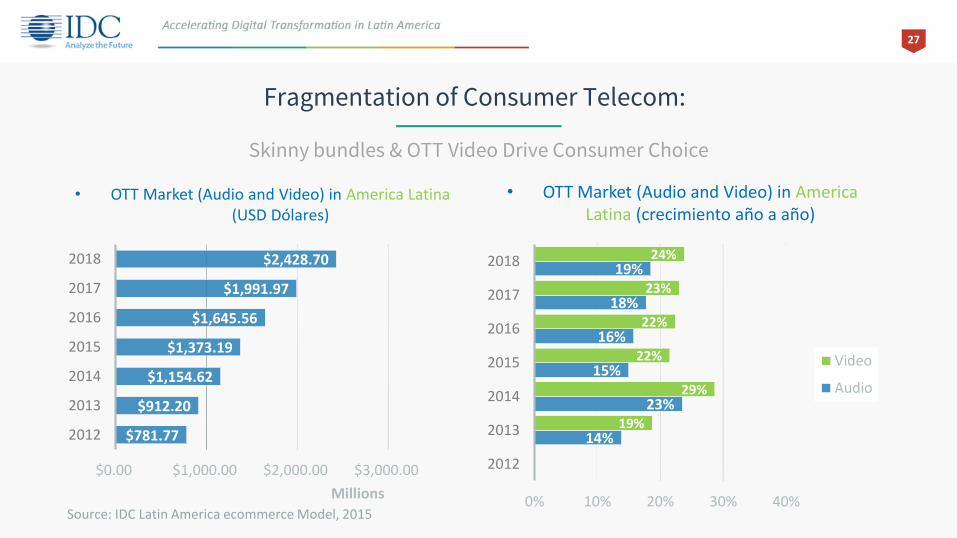

Fragmentation of Consumer Telecom:

Skinny bundles & OTT Video Drive Consumer Choice

• OTT Market (Audio and Video) in America Latina(USD Dólares)

$781.77

$912.20

$1,154.62

$1,373.19

$1,645.56

$1,991.97

$2,428.70

$0.00 $1,000.00 $2,000.00 $3,000.00

2012

2013

2014

2015

2016

2017

2018

Millions

• OTT Market (Audio and Video) in America Latina (crecimiento año a año)

14%

23%

15%

16%

18%

19%

19%

29%

22%

22%

23%

24%

0% 10% 20% 30% 40%

2012

2013

2014

2015

2016

2017

2018

Video

Audio

27

Source: IDC Latin America ecommerce Model, 2015

IoT Installed Base will grow 5 fold in just 6 years in Latin America

300.3 M

2014

1.45 B

2020

30.1% CAGR

28

Source: IDC Latin IoT Spending Guide, 2015

4New buyers in

Technology

30

New Buyer in Technology

LOB

…defines IT needs and their correspondent

financing.

…pushing for 3rd platform

initiatives

…LOB budgets are emerging for

strategic initiatives, such as digital transformation

… LOB does no think in terms of Cloud or Big Data, they thinks on costumer retention,

cross-selling, etc.

…even more “pushy” than IT for adopting 3rd

platform technologies

$

Source: IDC Latin America IT Investment Trends, 2016 Q1

New Buyer in Technology

33%

40%

12%33% IT evaluates, makes decision

& IT pay$

40% IT evaluates & recommends, but LOB pay$

12% IT & LOB evaluate solution. IT pay$

31

Source: IDC Latin America IT Investment Trends, 2016 Q1

Where to Focus?

CEO

Tech CxO CFO

CMO CDO

CIO

CTO IT?

32

IT Solution Opportunity Scorecard

US$M2016-2017 Short-term

OpportunityDriver

Container Infrastructure Software

The primary drivers for enterprise use of containers willfocus on agility and infrastructure optimization.

Infrastructure SW 2,343 6% Increasing Adoption of Private Cloud

Modern application development

2,163 8% Shift to Next-Generation Cloud-Native Applications

Integration SW 1,201 5% As quickly as cloud B2B integration is growing,customers are also interested in solutions where theycan maintain some control over their B2B processes

Business process automation

108 7% Building self-service tools that allow customers tobecome discoverable and participate in social network–like business networks encourages collaboration,innovation, and adoption

Security SW 589 9% Security in the cloud is of paramount importance,especially when dealing with B2B transactions

35

Source: IDC Latin America SW Tracker, 2015

Creating Your Digital Pitch

Business Transformation Digital Transformation

1. CUSTOMER CONVERSATION

Business Process Automation & Transformation (Internal)

Innovation and Ecosystem (External)

2. CUSTOMERS KPIs Cost and Risk New Revenue Streams

3.TECHNOLOGY Applications Driven Digital Platform with Apps

4. DECISION MAKERS CFO and CIO COO, CFO, CMO, CIO and CEO

5. PARTNERS System Integrators (SIs)Digital Influencers (agencies, start-ups and digital SIs)

6. SALES MOTION Big Bang - Solution & ValueIterative - Use Cases & PoVCloud = Accelerator

7. COMPETITION Stack-players (Traditional) Born in the Cloud vendors

36

Thank you