abundance and opportunity: u.s. natural gas...historic data source: eia natural gas monthly, april...

TRANSCRIPT

Abundance and Opportunity: U.S. Natural Gas Paul Hartman Regional Director January 22, 2015

Driving Demand for Natural Gas

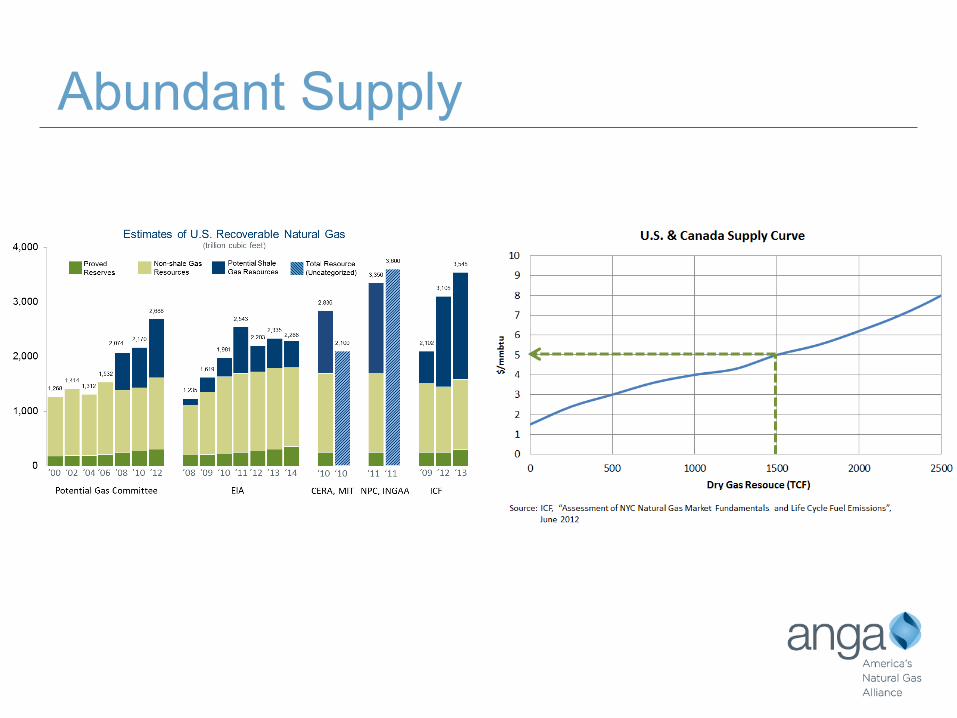

Abundant Supply

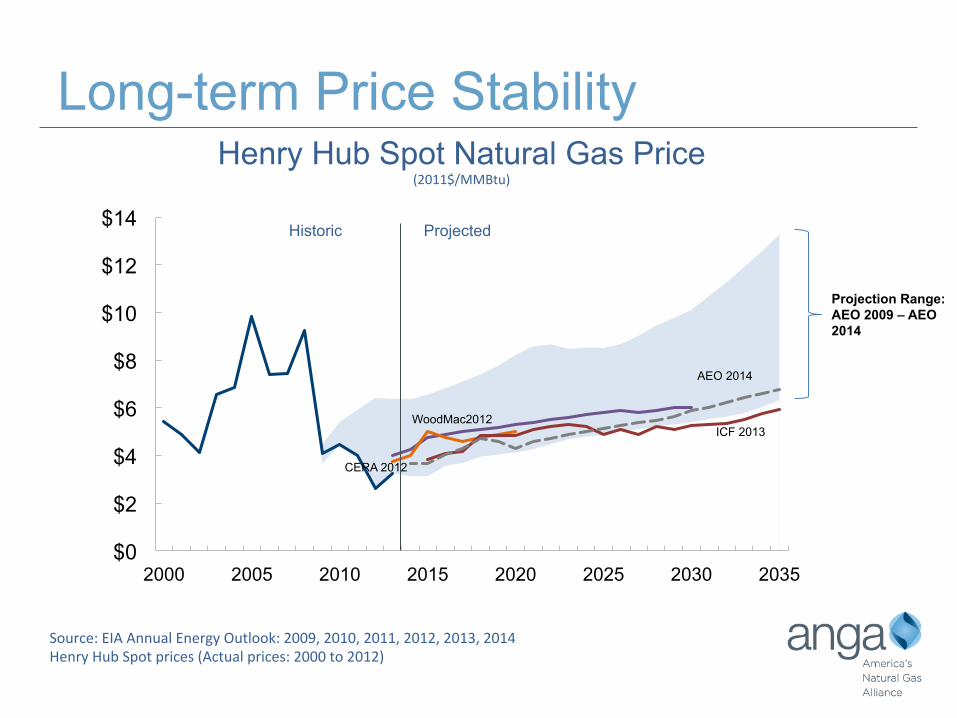

Long-term Price Stability

$0

$2

$4

$6

$8

$10

$12

$14

2000 2005 2010 2015 2020 2025 2030 2035

CERA 2012

WoodMac2012 ICF 2013

AEO 2014

Historic Projected

Henry Hub Spot Natural Gas Price (2011$/MMBtu)

Source: EIA Annual Energy Outlook: 2009, 2010, 2011, 2012, 2013, 2014 Henry Hub Spot prices (Actual prices: 2000 to 2012)

Projection Range: AEO 2009 – AEO 2014

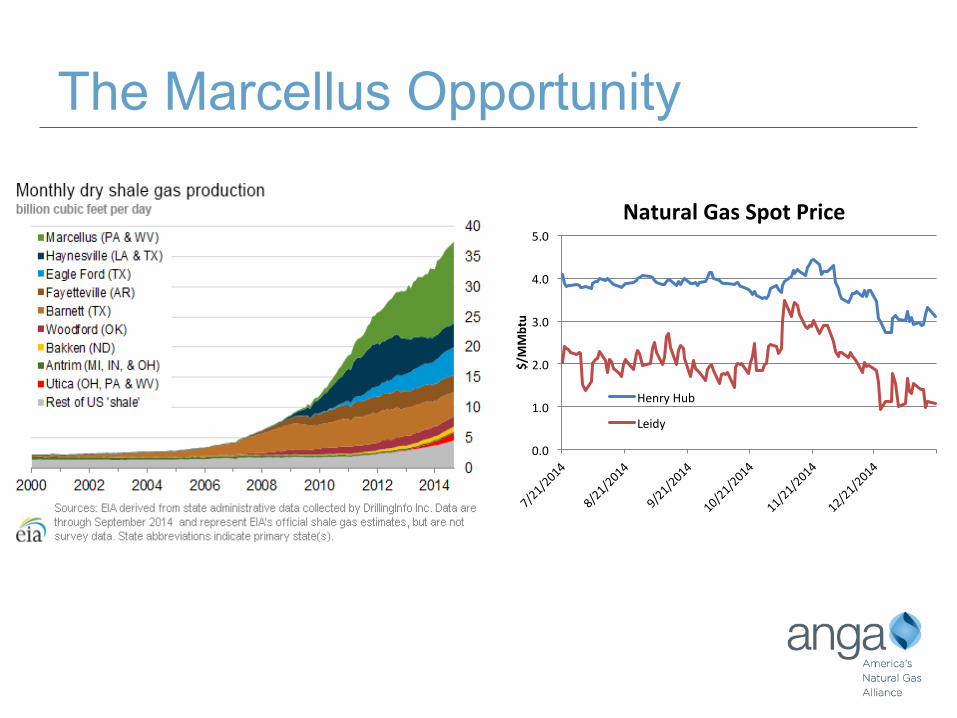

The Marcellus Opportunity

0.0

1.0

2.0

3.0

4.0

5.0

$/MMbtu

Natural Gas Spot Price

Henry Hub

Leidy

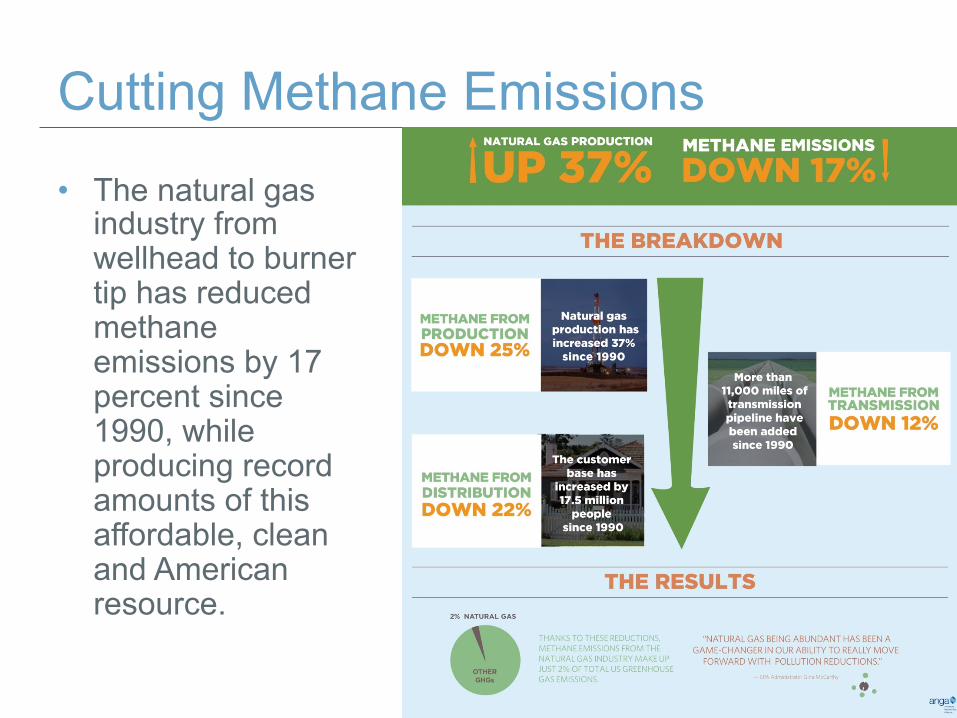

Cutting Methane Emissions

• The natural gas industry from wellhead to burner tip has reduced methane emissions by 17 percent since 1990, while producing record amounts of this affordable, clean and American resource.

6

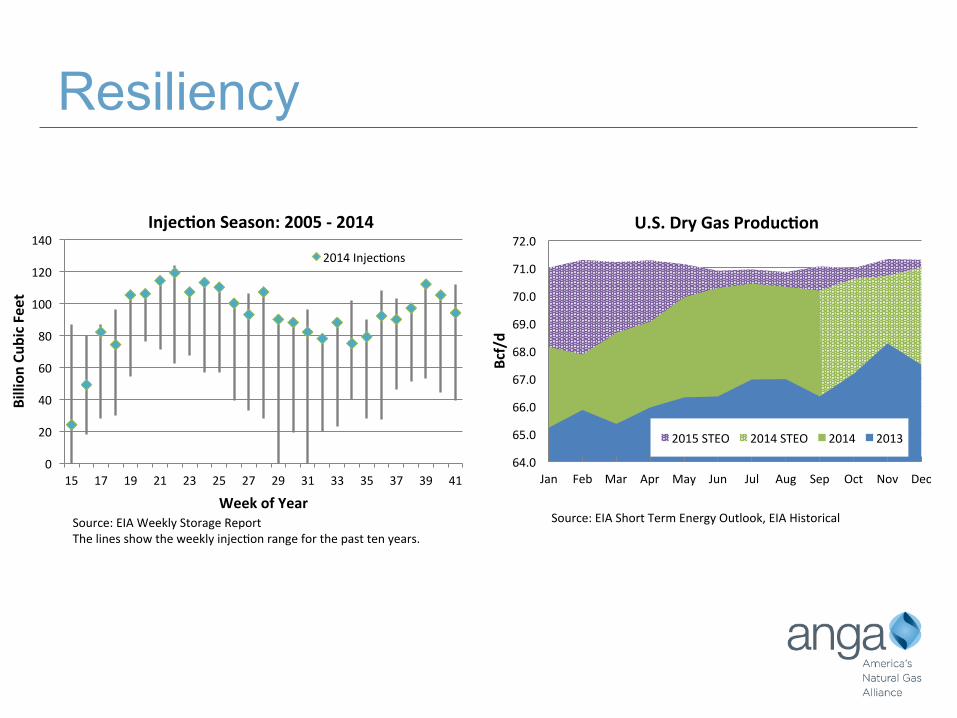

Resiliency

0

20

40

60

80

100

120

140

15 17 19 21 23 25 27 29 31 33 35 37 39 41

Billion

Cub

ic Feet

Week of Year

Injec?on Season: 2005 -‐ 2014

2014 InjecNons

64.0

65.0

66.0

67.0

68.0

69.0

70.0

71.0

72.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Bcf/d

U.S. Dry Gas Produc?on

2015 STEO 2014 STEO 2014 2013

Source: EIA Weekly Storage Report The lines show the weekly injecNon range for the past ten years.

Source: EIA Short Term Energy Outlook, EIA Historical

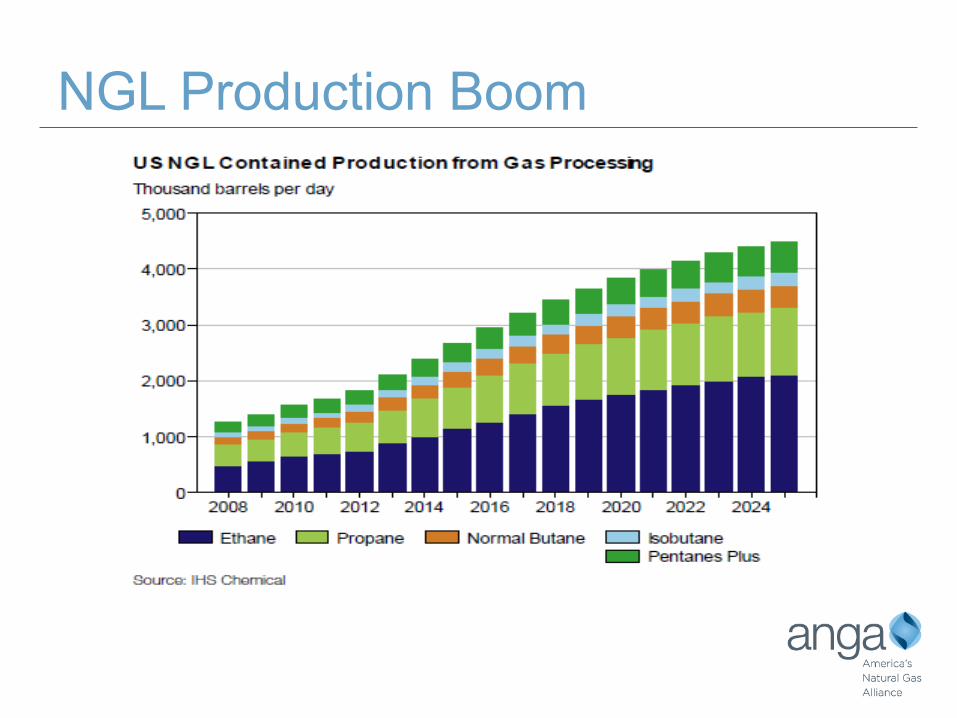

NGL Production Boom

0

10

20

30

40

50

60

70

80

90

100

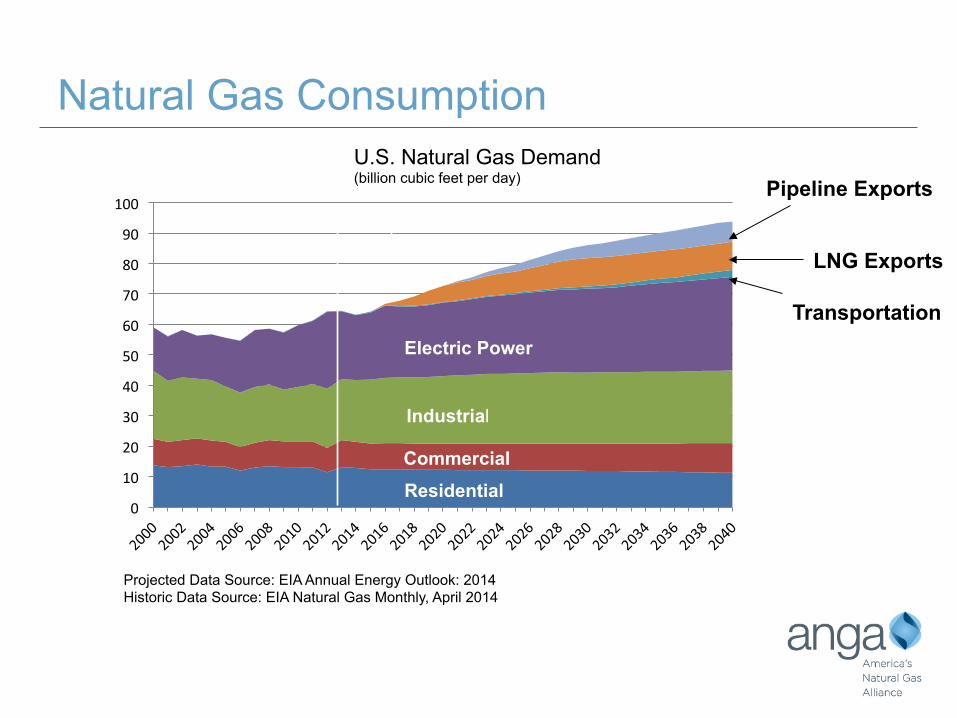

Natural Gas Consumption

Projected Historic

Projected Data Source: EIA Annual Energy Outlook: 2014 Historic Data Source: EIA Natural Gas Monthly, April 2014

U.S. Natural Gas Demand (billion cubic feet per day)

Electric Power

Industrial

Residential Commercial

Transportation

LNG Exports

Pipeline Exports

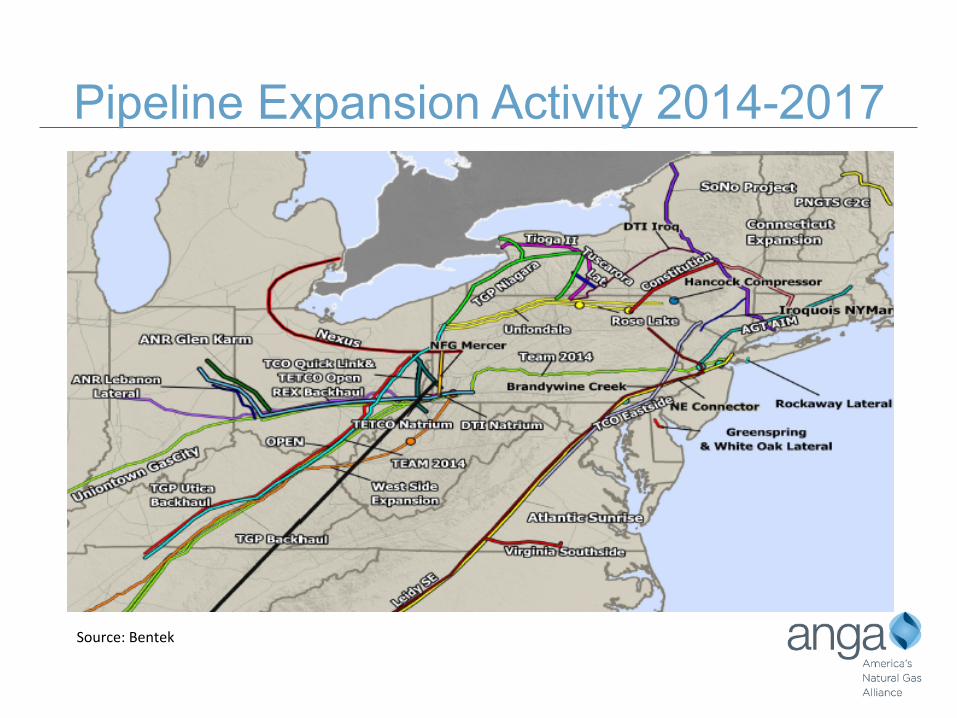

Pipeline Expansion Activity 2014-2017

Source: Bentek Source: Bentek

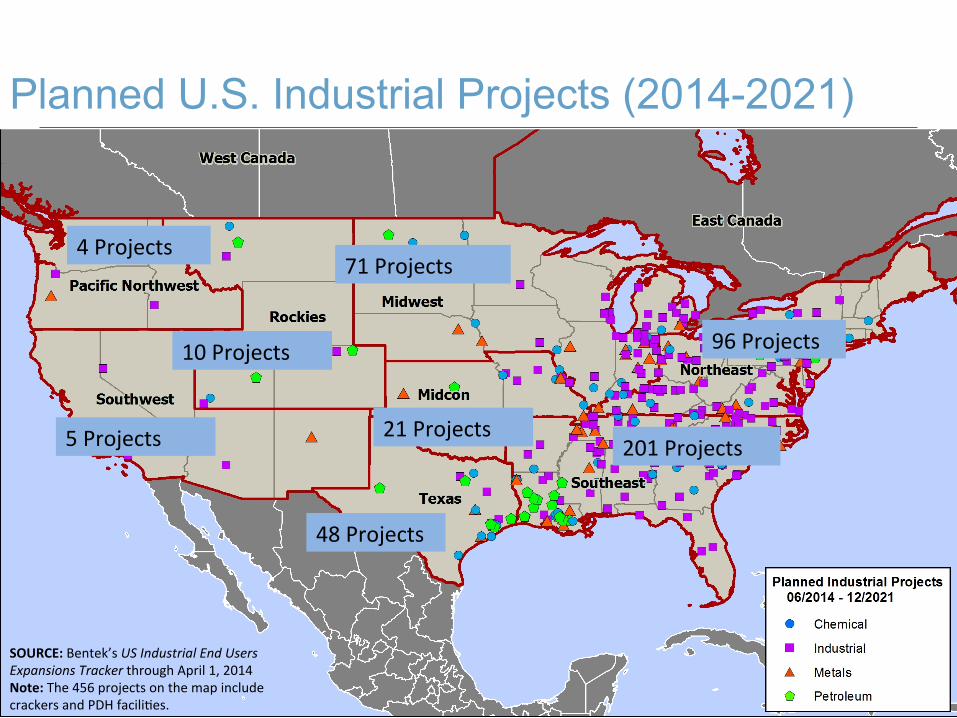

Planned U.S. Industrial Projects (2014-2021)

4 Projects

5 Projects

10 Projects

71 Projects

21 Projects

48 Projects

96 Projects

201 Projects

SOURCE: Bentek’s US Industrial End Users Expansions Tracker through April 1, 2014 Note: The 456 projects on the map include crackers and PDH faciliNes.

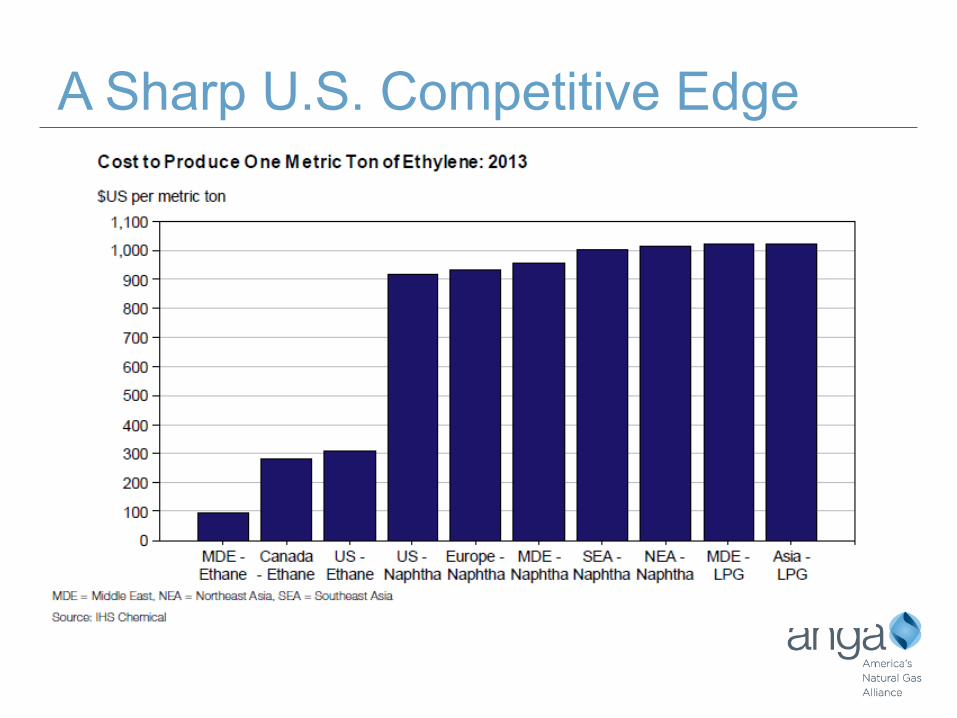

A Sharp U.S. Competitive Edge

-4

-2

0

2

4

6

8

10

1973 1983 1993 2003 2013 2023 2033

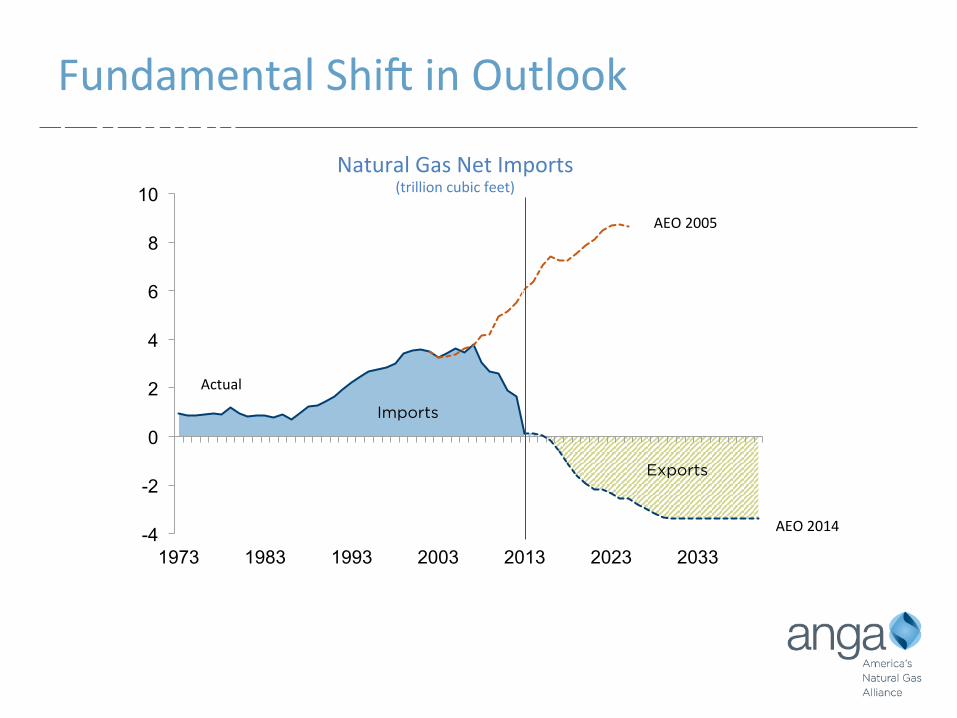

Fundamental Shi] in Outlookame Change

Source: EIA, Annual Energy Outlook 2005 & 2013 Early Release

Natural Gas Net Imports (trillion cubic feet)

Imports

Exports

AEO 2005

Projected Historic

AEO 2013

AEO 2005

AEO 2014

Actual

LNG Export Study Comparison

Modeler Release Date

U.S. Natural Gas Supply

Assump?on

LNG Exports Volume Range

(Bcf/d) Price Change from Baseline Case

EIA October, 2014 Reference 12.0 -‐ 20.0 $0.10 -‐ $0.80

ICF May, 2013 High 4.0 -‐ 16.0 $0.32 -‐ $1.02

CRA February, 2013 Low 20.0 -‐ 35.0 $1.60 -‐ $3.10

NERA December, 2012 Reference 0.0 -‐ 15.8 $0.00 -‐ $1.09

Navigant January, 2012 Reference 0.9 -‐ 6.6 $0.04 -‐ $0.41

Deloiae 2011 Reference 6 $0.22

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Landed UK Landed Japan Landed China Landed India U.S. Exports

Regasify Cost

Shipping Cost

Liquefy Cost

Henry Hub Price

U.S. LNG Export Price Components

LNG Landed Prices and Cost of Delivered U.S. Exports

Source: FERC

EsNmated June 2014 ($/mmbtu)

U.S. Exports – Global Context

1. ICF esNmate for year end 2011. 2. FTA & non-‐FTA ApplicaNons to DOE as of Mar 31, 2014 3. Dec 2012 ICF esNmate based on current worldwide project list. ~Poten, BG Group, Credit Suisse, Facts Global Source: API, ANGA

0

20

40

60

80

100

120

140

Bcf/d

Proposed U.S. Capacity 2

Under Construc?on, Planned & Proposed Non-‐U.S. World Capacity 3

Current World Capacity 1

Range in Projected Worldwide LNG Demand: 2020-‐2025~

www.anga.us twitter @ANGAus