a private investor's guide to gilts - london stock exchange · this booklet is intended to...

TRANSCRIPT

1

PRIVATE INVESTORS GUIDE

Header

1

Header

A Private Investor's Guide to Gilts

Fourth EditionDecember 2004

United KingdomDebtManagementOffice

2

PRIVATE INVESTORS GUIDE

Disclaimer

This booklet is intended to help those who may have an interest in investingin gilts. It covers the main features of buying, selling and holding gilts. Thebooklet does not constitute a recommendation to buy, sell or hold gilts, nordoes it offer investment advice.

The United Kingdom Debt Management Office (DMO) has tried to ensurethat the legal and factual information is accurate. Except where specificallyindicated, the booklet describes the position as at 30 November 2004. Thereader should not assume that anything described in it is still accurate at alater date.

This booklet cannot be a comprehensive statement of the intricacies of lawand practice relating to gilts, nor can it take account of the circumstances ofevery investor. Therefore, reliance should not be placed on the booklet:investors who want advice on which gilt or other investment may be bestsuited to them, or on trading strategies, should consult a professional adviser.

As gilts are marketable securities, their market value may go down as well asup. The DMO issues gilts to the market on behalf of the Government of theUnited Kingdom, and holds gilts itself for market management purposes.

The DMO does not in any way guarantee the liabilities of the commercialinstitutions referred to in this booklet.

3

PRIVATE INVESTORS GUIDE

1. What are gilts?

1.1 Conventional gilts 4• Information on a gilt certificate• Double-dated gilts• Undated gilts

1.2 Index-linked gilts 61.3 Gilt strips 8

2. Gilt prices and yields

2.1 Gilt prices 10• What causes prices to change?

2.2 Gilt yields 12

3. Buying and selling gilts

3.1 Buying and selling in the market 143.2 The Approved Group of investors 163.3 Buying from the DMO at auctions 173.4 Buying and selling through the DMO Gilt Purchase and Sale Service 18

4. Registration of gilts 21

5. Taxation of gilts 22

6. Conversion offers 24

7. Euro re-denomination 24

Appendices

a) Gilts in issue 25b) Index-linked gilt cash flows 28c) Frequently Asked Questions 29d) Glossary 30e) List of Gilt-edged Market Makers 32f) Useful contacts and websites 33

Contents

4

PRIVATE INVESTORS GUIDE

What are gilts?

Gilts are marketable securities issued byHer Majesty’s Government through theUK Debt Management Office (DMO) –an Executive Agency of HM Treasury.Gilts are issued to finance the CentralGovernment Net Cash Requirements andto refinance maturing debt.

The name ‘Gilts’ is short for ‘Gilt-edgedstock’. The market has given this name toBritish Government securities because oftheir reputation as one of the safestinvestments.

Gilts cannot be cashed in before theirofficial maturity date. However, aninvestor can always sell them in themarket (section 3.1) or via the DMO GiltPurchase and Sale Service (section 3.4).This service is offered on an executiononly basis. Individuals should ensure thatit meets their own requirements. If youare unsure of what action to take youshould seek financial advice.

Dealers are prepared to buy and sell mostgilts at any time. Prices may change fromday to day, and it is important toremember that you may not be able to sellyour gilts for the same price as you boughtthem.

There are many different kinds of gilt (seeAppendix A for a full list). Some have onlya few years to run; others will continue topay interest for over 30 years. Some are‘index-linked’, meaning that the interestand capital payments are adjusted forinflation as measured by the Retail PricesIndex (RPI) (section 1.2).

Others are ‘strippable’ which means thatthe individual interest and redemptionpayments may be separately bought andsold in the market (section 1.3).

This booklet explains the main kinds ofgilts available, how to buy and sell them,and other issues that may be of interest tothe potential investor.

This is the fourth edition of thispublication and the first to be publishedsince Computershare Investor ServicesPLC (‘Computershare’) succeeded theBank of England as Gilts Registrar.

1.1 Conventional gilts

Conventional gilts are the simplest form ofUK Government bond and represent thelargest part of the gilt portfolio (75% at 30November 2004). A conventional gilt re-presents a guarantee by the Government topay the holder a fixed cash interest payment(half of the coupon) every six1 months untilthe bond matures. On maturity the holderreceives the final coupon payment and thenominal capital amount invested.

A conventional gilt is denoted by its annualcoupon rate and maturity (e.g. 5%Treasury Stock 2014). The coupon rateusually reflects the market interest rate atthe time of first issue of the gilt. As a result,there is a wide range of coupon ratesavailable – reflecting how rates ofborrowing have varied in the past.

Information on a gilt certificateA lot of the key information relating to an

1 Three ‘rump’ gilts pay coupons quarterly (see Appendix A).

5

PRIVATE INVESTORS GUIDE

What are gilts?

investment in gilts is available on thecertificate you will be sent after purchase(pictured). Suppose you have a holding of£1,000 nominal of 5% Treasury Stock2014. What does that mean?

• Nominal amount£1,000 nominal is the face value amount ofthe gilt you hold. It is not necessarily howmuch it is worth now, or how much itwould cost you to buy now. A £1,000 nom-inal holding of that gilt may be worth moreor less than £1,000 in the market. But whenthis gilt finally matures, on 7 September2014, £1,000 is the capital repayment thatthe holder will receive at that time.

There is no particular significanceabout the £1,000 used in theexample above. You can holdlarger or smaller amounts, £100,or £100,000, if you choose. Giltsare actually transferable inmultiples of a penny. However, ifyou buy gilts at a DMO auction(section 3.3), £1,000 (nominal) isthe minimum amount you mayapply for.

• The coupon5% is the ‘coupon’, or the annualrate of interest that is applied tothe nominal value of the holdingto determine the size of yourinterest payment, or ‘dividend’,each year. In most cases dividendson gilts are paid six-monthly so the investor will receive halfof the dividend twice a year; in this example, £25.00 gross oftax on both 7 March and 7 September.

• The name‘Treasury Stock’ is the name given to thegilt when it was first issued. Gilts have avariety of names – Treasury Stock,Exchequer Stock, Conversion Stock, WarLoan and Consolidated Stock. The nameshave no significance as far as theunderlying obligation to repay isconcerned. All new gilts issues in recentyears have been named ‘Treasury Stock’.

• Maturity Year2014 is the ‘maturity’ year i.e. the year inwhich the holder at that time will receivethe capital repayment (£1,000 in theexample above). The gilt cannot be cashed

6

PRIVATE INVESTORS GUIDE

What are gilts?

in before September 2014, although it canbe sold in the market at any stage duringits life. At any time, the value in themarket may be higher or lower than£1,000 depending on how attractive the5% coupon is relative to other prevailinginterest rates (see page 12).

Market convention is to divide gilts intothe following maturity categories:

• Shorts: 1-7 years • Mediums: 7-15 years• Longs: Over 15 years

Double-dated conventional giltsIn the past the UK Government has issuedgilts which have two repayment dates in thetitle, e.g. ‘73/4% Treasury Stock 2012–2015’.This means that the Government canchoose to repay the gilt at any time from2012 onwards with three months’ notice,but must repay the gilt by 2015 at the latest.It is important to remember that the choiceof redemption date is the Government’s,not the investor’s. There are currently onlythree double-dated gilts still remaining.

Undated giltsUndated gilts (which have no fixedredemption date) are the oldest in the port-folio – some date back to the 19th century.The redemption of these bonds is at thediscretion of the Government, but becauseof their age they all have low coupons andso there is little current incentive for theGovernment to redeem them.

1.2 Index-linked gilts

These are gilts on which both the interestpayments and the capital repayment onredemption are adjusted in line withinflation, as measured by the Retail PricesIndex (or RPI), which is published byNational Statistics.

Whereas for conventional gilts anassumption about expected inflation overthe life of the gilt is effectively orimplicitly included in the fixed annualcoupon rate, index-linked gilts removethe risk of actual inflation turning out tobe different from the expectation byapplying an updated inflation adjustmentfactor as each cash flow (twice a year) ispaid. Index-linked coupons and yieldstend to look much lower than onconventional gilts. However, this isbecause their coupons and yields are thevalues in addition to inflation (notincluding inflation, as with coupons andyields for conventional gilts).

Inflation adjusted cash flows from index-linked gilts are determined by a ‘Base RPI’– this is the level of the RPI eight monthsbefore the gilt was first issued2. Theinflation adjustment is made bycalculating the ratio of the RPI level eightmonths before a cash flow is due, to theBase RPI for the gilt in question. Thecoupon rate (or 100 for the capitalrepayment) is then multiplied by thisratio. The eight-month lag ensures thatthe cash value of the next interestpayment is always known with certaintyat any time.

2 A list of Base RPIs for each index-linked gilt is available at www.dmo.gov.uk/gilts/indexlink/uk/igtable.htm

7

PRIVATE INVESTORS GUIDE

Index-linked gilt arithmeticTake an example. 41/8% Index-linked Treasury Stock 2030 was first issued on 12 June1992. Interest is paid on 22 January and 22 July each year. The gilt will be redeemedon 22 July 2030, at which time the final interest payment will also be made.

The base month for the Retail Prices Index for the gilt is October 1991, i.e. the montheight months before the gilt’s issue in June 1992. The RPI in October 1991 was 135.1.Each semi-annual interest payment (except the first, which related to a period of morethan six months) comprises £2.0625 (half the 41/8% annual coupon) adjusted for themovement in the RPI, as per the following formula:

Amount of interest per £100 nominal of stock = half the annual coupon x RPI eightmonths before the dividend is due/Base RPI.

Therefore for the interest payment made on 22 January 2001 for this index-linked gilt,the amount paid was

£2.0625 x 170.7135.1

= £2.6059863064…per £100 nominal of stock

(170.7 was the level of the RPI in May 2000).

This was then rounded down to £2.6059 per £100 nominal in accordance with thisindex-linked gilt’s prospectus.

The actual principal repayment on redemption (also called the ‘uplifted redemptionvalue’) depends on the level of the RPI eight months before the repayment date of thegilt and is calculated in the following way:

Uplifted redemption value per £100 nominal of stock = 100 x RPI eight months before therepayment date / Base RPI.

We do not, of course, know yet what the RPI will be in November 2029 (eight monthsbefore the repayment date of 41/8% Index-linked Treasury Stock 2030). Suppose that thelatest RPI figure available is that for December 2000 (172.2). In order to produce anestimate for the value of the November 2029 RPI it is necessary to make an assumptionabout RPI inflation over the period from December 2000 to November 2029 (a periodof 28 years and 11 months). If we suppose that RPI inflation over this period averages3% per annum, then this would give an estimate for the RPI for November 2029 of:

= 172.2 x ((1.03)2811/12) = 172.2 x ((1.03)28.916…) = 172.2 x 2.35076…. = 404.80222. ,which would be published as 404.8.

Making this assumption about future RPI inflation, the sum repaid to investors in thisindex-linked gilt in July 2030 would then be estimated as:£100 x 404.8 = £299.6299….

135.1per £100 nominal of the gilt.

A list of recent index-linked payments appears in Appendix B.

What are gilts?

8

PRIVATE INVESTORS GUIDE

What are gilts?

It should be noted that, since the RPI cango down as well as up, cash flows onindex-linked gilts may also fall. Forexample, cash flows paid in April andOctober 2002 for 21/2% Index-linkedTreasury Stock 2020 would have used theRPI values for August 2001 (174.0) andFebruary 2002 (173.8) respectively to fixthe cash flows. Hence, although the RPIincreased from April to October 2002, itdecreased from August 2001 to February2002 and the interest payment rate wasadjusted downwards accordingly (from£2.6215 to £2.6185 per £100 nominal). Inthe event that the RPI which fixes theredemption payment is less than the BaseRPI for an index-linked gilt (implyingnegative inflation over the life of the gilt),then the final redemption payment wouldbe less than £100 per £100 nominal (i.e.there is no ‘deflation floor’).

The UK Government has no current plansto issue new index-linked gilts linked tothe UK Harmonised Index of ConsumerPrices (now referred to as the ConsumerPrice Index (CPI)) despite this measure ofinflation being substituted for RPIX forinflation targeting purposes. This is keptunder review, but the DMO wouldconsult with the market were it at anytime to consider a move to a substituteindex for new index-linked gilts. The RPIwill continue to be published andpayments for existing index-linked giltswill continue to be linked to the RPI.

The DMO website includes a table withmonthly RPI data going back to 1980(this can be found at www.dmo.gov.uk/gilts/indexlink/uk/rpiseries.htm).

Index-linked gilts may be particularlyattractive to UK taxpayers since, undercurrent legislation, the gain arising fromthe inflation uplift on the principal (orcapital) value is generally not taxed in thehands of UK private investors. Suchinvestments will, however, be taxable onthe full amount of interest received,including any inflation uplift.

1.3 Gilt strips

Stripping a gilt is the process of separatinga standard interest-bearing gilt into itsindividual interest (or coupon) andredemption (or principal) paymentswhich can then be separately held andtraded in their own right as non-interestbearing (or zero-coupon) bonds.

For example, in June 2004 a holding of5% Treasury Stock 2008 could be dividedinto nine strips; one for the principalrepayment or strip on 7 March 2008 andeight coupon strips for the half yearlyinterest payments running from 7 September 2004 through to 7 March2008.

Strips are referred to as ‘zero-coupon’instruments because they do not payinterest on the maturity date of the strip;the holder simply receives a payment forthe strip’s nominal value. They thereforetrade at a discount to face value prior tomaturity.

An official strips facility was introduced inDecember 1997 and until 2002, allstrippable gilts had coupon dates of 7June and 7 December. From 2 April 2002,a second series, with coupon dates of 7

9

PRIVATE INVESTORS GUIDE

March and 7 September, was opened. Notall gilts, however, are eligible to bestripped. Those gilts that may be strippedare identified in Appendix A. The range of strippable gilts may be extended by theDMO.

At 30 November 2004 there were 17strippable gilts in issue in the two series,with a total of £207.6 billion (nominal) inissue, of which 1.1% was held in strippedform.

In order to hold strips directly an investormust be a member of CREST and theprocess of stripping will need to beundertaken through a GEMM3. Investors

who hold gilt strips on 5 April in any yearof assessment will be treated as havingtransferred and reacquired the strip at themarket value on 5 and 6 April of therelevant year respectively, and may betaxed on any increase in that value overthe previous year. The prices of gilt stripsmay behave differently to other gilts.Potential investors may wish to seekprofessional advice before buying strips.Further information on gilt strips may beobtained from the DMO website.

0

40

50

60

70

80

90

100

110

What are gilts?

Strips of 5% Treasury Stock 2008

3 A Gilt-edged Market-Maker (see section 3.1 and Appendix E).

Please note: If you are not a member ofCREST and you wish to hold a strip youshould consult your stockbroker orfinancial adviser.

10

PRIVATE INVESTORS GUIDE

Gilt prices and yields

Gilts are actively traded securities and theprice of a gilt can change continuallywhilst the capital markets are trading. Thetitle of a gilt does not tell you its value inthe market; neither does it tell you howmuch you would have to pay to buy it orhow much you would receive if you sold it(rather than waiting for repayment atmaturity).

• Gilts prices in newspapersIf you are looking for price information innewspapers you will find prices for mostgilts with the share price lists, usuallyunder the heading ‘UK Gilts’ or‘Government Securities’. The examplehere is taken from the Financial Times of30 November 2004.

The easiest way to find out the price ofa gilt is to look in the financial pages of the newspapers or on the gilts prices pages of the DMO website atwww.dmo.gov.uk/gilts/f2gilts.htmwhere close of business reference pricesand redemption yields for the previousday for all gilts are published.

In addition, the Financial Times publishesa full list of gilt prices each day at www.ft.com/gilts Gilt prices shown innewspapers are usually the closingmiddle-market prices, i.e. halfwaybetween the indicative buying and sellingprice. As noted above gilt prices canfluctuate continuously and the price maywell have changed by the time you look in the newspaper on the followingmorning. A broker can give you up-to-date prices for buying andselling.

Newspapers often show the price changerelative to the previous day (or theprevious month) per £100 nominal of thegilt. In addition, a high/low price indicatesthe movement of the gilt’s price over theprevious year. The price published bynewspapers is the clean price, i.e. it does not include accrued interest (section3.1).

• Price information on the DMO websiteClosing prices and redemption yields forall gilts and gilt strips are published on theDMO website on every business day atwww.dmo.gov.uk/gilts/f2gilts.htm Thefollowing example is taken from theDMO website for 30 November 2004 andshows close of business data for 5%Treasury Stock 2014. The first three fields are all means of identifying the gilt. The first is the DMO’s internalidentifier code and the second a shortenedform of the gilt’s name. The third field isthe ISIN number (the InternationalSecurity Identification Number – anidentifier number used by the LondonStock Exchange). The next three fieldsgive price and yield information.

11

PRIVATE INVESTORS GUIDE

The two prices shown of £103.17 and£104.344033 are known as the ‘clean’ and‘dirty’ price respectively. Clean prices donot include accrued interest whereas dirtyprices do (see the section on accruedinterest on page 15). The clean price istypically the price, which is quoted whenagreeing a purchasing or selling price.However, the actual amount of moneywhich will change hands is based on thedirty price and will reflect settlement onthe business day after the transaction(T+1)4.

So, on the basis of the reference price on30 November 2004, every £1,000 nominalof 5% Treasury Stock 2014 was worth£1,043.44.

• Sale and purchase pricesIt is worth noting that the price you willactually pay (if you are buying) or receive(if you are selling) will probably bedifferent to the mid-prices describedabove. This is because:

• prices move all the time, and theDMO website and newspapers quoteclose of business prices from theprevious day.

• in the market, dealers will offer to sellgilts at a higher price than they areready to pay for it. The differencebetween their buying and sellingprices is known as the ‘spread’, and isa dealer’s charge for conducting thetransaction. There may, however, beother charges which are not based on

the price of the gilt (see below). Theprice shown in the newspapers is inthe middle of the spread. If you are abuyer you will pay a little more; if aseller you will receive a little less.

• The price you actually pay willinclude some allowance for accruedor rebate interest (see pages 15-16).

• Investors will also pay commission toa broker or bank for the arrangementof the purchase or sale.

The gilt prices that appear on the DMOwebsite and newspapers assume next daysettlement. This means that someone whopurchases a gilt today will be expected topay for it on the following business day.This is the standard convention in the giltsmarket for wholesale investors (e.g.insurance companies). However, tradesconducted for retail customers may notsettle on a T+1 basis. For instance, theDMO’s Gilt Retail Purchase and SaleService will use a T+3 settlementconvention.

What causes gilt prices to change?As noted above, gilt prices do fluctuate.Why should this be the case when gilts areregarded as free of any default risk?

Gilt prices do not change like companyshares do, where people change theirviews about the earning power orcreditworthiness of the borrower. Withgilts, the coupon is fixed and it is widelyassumed that the UK Government will

Gilt prices and yields

5TY14 5 Treasury 2014 GB0031829509 103.170000 104.344033 4.592604

4 Settlement convention

12

PRIVATE INVESTORS GUIDE

Gilt prices and yields

not default on its obligations to pay thecoupons through the life of the gilt or thecapital amount on redemption.

Prices change because people change theirviews about interest rate prospects. Acoupon fixed at 6% may look unattractivewhen market interest rates are at 8%; andit may look generous when market interestrates are at 4%. Prices in the gilts marketwill adjust to reflect that. This is why, forexample, the clean price of 5% TreasuryStock 2014 at the close of business on 30November 2004 was £103.17 (i.e. above£100.00) - with market interest rates (forthat maturity) at that time of around4.60%, the coupon (of 5.0%) lookedslightly generous and the price of the giltper £100 nominal had risen above par(£100.00) to reflect that. Equally, the priceof 31/2% War Loan, with a coupon (31/2%)below current market interest rates, closedat £78.17, well below par.

However, it is not just the comparisonwith today’s interest rates that matters.The prices will also reflect the market’scollective view of what will happen tointerest rates over future years. The priceof a gilt with many years to run will reflectboth the coupon, and the collective viewof the market on how attractive that fixedcoupon rate is likely to be over theremaining years of the gilt’s life. That inturn will be affected by the view thatpeople take about both the level and theuncertainty of inflation in the future.Prices will of course behave differentlywhere the interest and capital payment isprotected against changes in inflation, asmeasured by the RPI. Index-linked giltsare described earlier in section 1.2.

Other issues, such as the levels of outrightsupply and the strength and nature ofdemand from investors, can also affect giltprices.

2.2 Gilt yields

Some of the most important informationabout gilts is given in the second columnof the newspaper table and the finalcolumn of the DMO website table(opposite) – ‘the gross redemption yield’.This figure gives an indication of theactual return which the investor willreceive from buying the gilt at the priceshown and holding it to maturity.

The redemption yield is different from thecoupon. The coupon is the fixed interestrate paid on the nominal amount of thegilt – in the case of 5% Treasury Stock2014, £5.00 on each £100 (paid in twoequal amounts of £2.50). In the exampleabove, to receive the 5% annual interestand the £100 capital repayment onredemption, you would have had to pay aclean price of £103.17 (per £100 nominal)on 30 November. The yield will change asprices change because the cash flows fromthe gilt are fixed. As prices rise you areeffectively paying more for a series offixed cash flows so the yield falls, and ifprices fall the yield rises.

The redemption yield reflects the netpresent value of the future flow of interestand includes the effect of the capital gainor loss from holding the gilt untilmaturity, at a given price. This is thestandard measure used in bond marketsfor assessing the rate of return on aninvestment. For example, if you buy a

13

PRIVATE INVESTORS GUIDE

high coupon gilt which pays interest wellabove current interest rates (e.g. 9%Conversion Loan 2011) you would havepaid some £125 per £100 nominal on 30November and, assuming you held toredemption, you would make a capitalloss of £25 per £100 nominal on theinvestment. Offsetting this loss, however,is the fact that you would be receivingabove (current) market related interestpayments. The redemption yieldcalculation also assumes that the investorreinvests the interest payments received bybuying more of the gilt at the sameredemption yield.

For index-linked gilts, ‘real’ grossredemption yields are calculated. Unlikethe ‘nominal’ gross redemption yields

which are calculated for conventional gilts,real yields do not include an allowance forinflation. Hence yields for index-linkedgilts tend to look lower than forconventional gilts. For example, in theexample above, the 4.71% yield includes anallowance for RPI inflation. However, foran index-linked gilt the ‘real’ yield shownwould be the yield which would be addedto actual future RPI inflation. The yieldshown on the DMO website for 30November for 21/2% Index-linked TreasuryStock 2013, for example, was 1.81%.

Formulae for calculating redemptionyields, appear on the DMO website atwww.dmo.gov.uk/gilts/public/technical/yldeqns_v2.pdf

Gilt prices and yields

5TY14 5 Treasury 2014 GB0031829509 103.170000 104.344033 4.592604

_

14

PRIVATE INVESTORS GUIDE

Buying and selling gilts

3.1 Buying and selling gilts in themarket

Gilts are traded in a very active marketcentred on a group of firms known as‘Gilt-edged Market Makers’ (GEMMs). Alist of GEMMs appears in Appendix E.The GEMMs deal continuously withmajor professional investors like pensionfunds and insurance companies, acrossthe entire range of gilts. GEMMs, alongwith institutional investors andcustodians who may hold stock on behalfof private investors, hold gilts incomputerised form using the CRESTsettlement system5. Some of the GEMMsmake special provision for deals in smallamounts.

If a private investor wishes to purchasegilts other than via the DMO at outrightgilt auctions, the secondary market can beaccessed through a stockbroker or bank orthe DMO’s Retail Purchase and SalesService (section 3.4). A member of thepublic who wishes to use a stockbroker orbank will need to have opened an accountwith the broker or bank before they canbuy or sell gilts.

Stockbrokers and banksStockbrokers are members of the LondonStock Exchange, and a list may beobtained by writing to the London StockExchange, 10 Paternoster Square LondonEC4M 7LS or by accessing its websitewww.londonstockexchange.com. Several

of the high street banks also offerstockbroking services to their bankingcustomers, or will put them in contactwith their own stockbroking arm. It isworth remembering that a broker chargescommission for buying and selling gilts.The services the broker provides are toseek out the best price available for you,the client, and to organise the paperwork.Many brokers will offer advice on whichgilt is best suited to the client’s particularcircumstances. An example of the dealingprocess is given below.

How to buy through a stockbrokerA client telephones their stockbroker orbank and asks them to buy £1,000nominal of 5% Treasury Stock 2014 in themarket. The broker obtains the best price,and if acceptable to the client, deals at thatprice. At this stage this is an oral contractbetween all parties. The broker will thensend the client a contract note setting outthe amount bought, the price, and anyadjustments (e.g. for accrued or rebateinterest – see pages 15-16). It will alsoinclude the broker’s commission. If thebroker does not already hold funds for theclient, he/she will want a cheque for thebalance immediately.

A GEMM, who may be the seller of thegilt, will then debit the £1,000 nominal ofthe 5% Treasury Stock 2014 from theirCREST account in order to rematerialisethe gilt into the client’s own name. TheGEMM will do this by sending a ‘stock

5 The CREST system is a computerised system for settlement, registration and transfer of dematerialised securitiesincluding UK and Irish corporate securities, UK government securities and international securities. Holdings andtransfers are made under the Uncertificated Securities Regulations 1995 which permit transfers without the need for aninstrument in writing or the issuance of certificates. Sponsored membership of CREST for personal investors isavailable through commercial stockbrokers. Sponsored members do not receive stock certificates.

15

PRIVATE INVESTORS GUIDE

withdrawal’ instruction to CRESTcomprising of the withdrawal details andthe details of the client’s name andaddress in which the certificate is to beproduced. An electronic instruction willthen automatically be sent toComputershare in order to complete theregistration process. Once the client’sholding is registered with Computershare,dividends will be sent direct to the client’sbank or building society account or bycheque to the client if preferred. If noinstructions are received to the contrary,payment will be made by cheque. Theclient will receive a ‘certificate’ if the gilt isregistered in their own name; this will beneeded if the gilt is later sold.Alternatively, the broker or a custodianmay arrange for the stock to be held inCREST on the client’s behalf.

…and how to sellSales can be arranged in much the sameway. The broker will find the best priceoffered in the market, agree the sale anddeliver the ‘stock certificate’ toComputershare, together with a stocktransfer form signed by the client. If the giltis held in CREST, the broker or custodianwill arrange for the gilt to be transferred tothe relevant GEMM. The GEMM will paythe broker the agreed price, and the brokerwill deduct their commission and pay thebalance to the client.

• General points to note when buying orselling giltsWhen buying or selling gilts investorsneed to be aware in particular of two

conventions associated with gilts – ruleson accrued interest and ex-dividendperiods.

• Accrued interest When you are buying or selling a gilt youwill generally have to pay or receive anamount of money representing theaccrued interest on that gilt. Interest ongilts accrues on a daily basis between onecoupon (or dividend) date and the next.

For example, if you bought a holding of5% Treasury Stock 2008 for settlement on7 April 2004, i.e. a month after theprevious coupon payment (on 7 March)you are also buying 31 days accruedinterest which entitled you to receive thefull coupon payment on 7 September. Thepurchase price would therefore have beenincreased by (5%/2) x (31/184) =£0.421196 per £100 nominal of the gilt6.Here 184 is the number of calendar daysbetween 7 March 2004 and 7 September2004.

Equally you will generally receive acorresponding amount of accrued interestif you are selling a gilt.

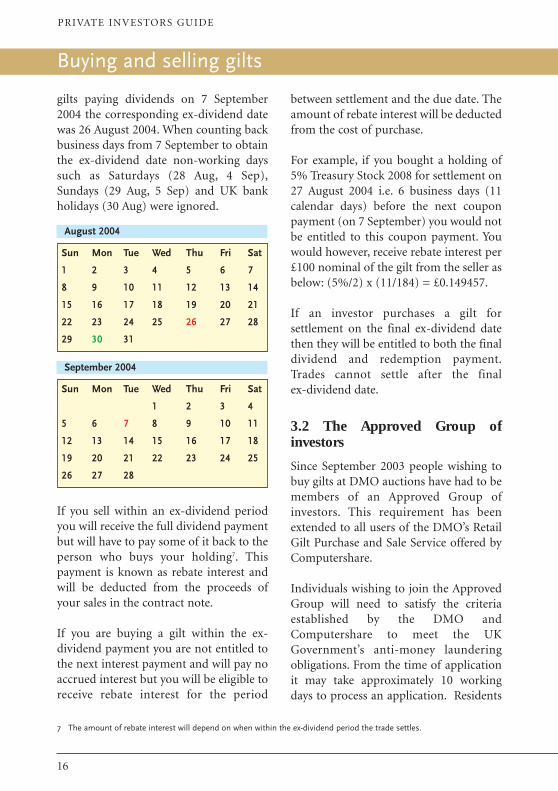

• Ex-dividend periodsInterest payments are usually made to the person who is the registered holder of a gilt 7 business days before thecoupon payment date (10 business daysfor 31/2% War Loan) unless alternativeinstructions have been given to theRegistrar. These periods are known as theex-dividend periods. For example, for

Buying and selling gilts

6 Half the coupon rate multiplied by the number of days on which interest has accrued divided by the total number ofdays in the coupon period.

16

PRIVATE INVESTORS GUIDE

Buying and selling gilts

gilts paying dividends on 7 September2004 the corresponding ex-dividend datewas 26 August 2004. When counting backbusiness days from 7 September to obtainthe ex-dividend date non-working dayssuch as Saturdays (28 Aug, 4 Sep),Sundays (29 Aug, 5 Sep) and UK bankholidays (30 Aug) were ignored.

between settlement and the due date. Theamount of rebate interest will be deductedfrom the cost of purchase.

For example, if you bought a holding of5% Treasury Stock 2008 for settlement on27 August 2004 i.e. 6 business days (11calendar days) before the next couponpayment (on 7 September) you would notbe entitled to this coupon payment. Youwould however, receive rebate interest per£100 nominal of the gilt from the seller asbelow: (5%/2) x (11/184) = £0.149457.

If an investor purchases a gilt forsettlement on the final ex-dividend datethen they will be entitled to both the finaldividend and redemption payment.Trades cannot settle after the final ex-dividend date.

3.2 The Approved Group ofinvestors

Since September 2003 people wishing tobuy gilts at DMO auctions have had to bemembers of an Approved Group ofinvestors. This requirement has beenextended to all users of the DMO’s RetailGilt Purchase and Sale Service offered byComputershare.

Individuals wishing to join the ApprovedGroup will need to satisfy the criteriaestablished by the DMO andComputershare to meet the UKGovernment’s anti-money launderingobligations. From the time of applicationit may take approximately 10 workingdays to process an application. Residents

7 The amount of rebate interest will depend on when within the ex-dividend period the trade settles.

Sun Mon Tue Wed Thu Fri Sat

1 2 3 4 5 6 7

8 9 10 11 12 13 14

15 16 17 18 19 20 21

22 23 24 25 26 27 28

29 30 31

August 2004

Sun Mon Tue Wed Thu Fri Sat

1 2 3 4

5 6 7 8 9 10 11

12 13 14 15 16 17 18

19 20 21 22 23 24 25

26 27 28

September 2004

If you sell within an ex-dividend periodyou will receive the full dividend paymentbut will have to pay some of it back to theperson who buys your holding7. Thispayment is known as rebate interest andwill be deducted from the proceeds ofyour sales in the contract note.

If you are buying a gilt within the ex-dividend payment you are not entitled tothe next interest payment and will pay noaccrued interest but you will be eligible toreceive rebate interest for the period

17

PRIVATE INVESTORS GUIDE

abroad (in selected overseas jurisdictions)who wish to buy and sell gilts must alsojoin the Approved Group, but eligibilitycriteria may differ from country tocountry.

The introduction of these arrangementsreflects the Government’s commitment tocombating financial crime in all its forms.In this context, gilts are recognisedthroughout the world as some of thesafest and, consequently, most desirableforms of investment. The Governmentbelieves that it would be detrimental tothe UK’s policy of combating financialcrime and to its contribution to theinternational fight against terrorism if itsown instruments were used to laundermoney.

One way of preventing money launderingis to institute stricter checks on peoplebuying financial services and it is nowcommon practice for banks and buildingsocieties to enquire much morethoroughly about potential customers.This is a requirement imposed on them bylegislation. By clearly establishing theiridentity, individuals can help to make itmuch harder for potential criminals tooperate.

Once accepted into the Approved Group,individuals will not have to provideevidence of identity and address on eachoccasion they wish to use the Purchase

An application form to apply formembership is available from the DMOand Computershare. Completed formsshould be sent to Computershare at theaddress at Appendix F.

and Sale Service or apply at gilt auctions.Only the new issue application forms sentout by the Registrar to Approved Groupmembers will be accepted at auctions heldby the DMO.

3.3 Buying from the DMO atauctions

Members of the public can only buy giltsoutright from the DMO at gilt auctions,when a further amount of a particular giltis issued. However, in order to do this, aperson must be a member of the ApprovedGroup of investors (section 3.2).

At the end of every quarter, (i.e. March,June, September and December) theDMO announces which gilts it willauction on each date in the followingquarter. On the Tuesday of the weekbefore the auction is scheduled, finaldetails are announced, including the sizeof the auction. At this time members ofthe Approved Group of investors can (ifthey choose) receive a Prospectus and anApplication Form for the auction fromComputershare.

Non-competitive bidsMembers of the public who bid at auctionscan bid non-competitively, meaning thatsuccessful applications will be met in fullat the average accepted competitive bidprice at the auction (i.e. the weighedaverage price paid by successfulcompetitive bidders). Below is an example

The DMO’s auction calendar ispublished up to a year in advance: seethe website page www.dmo.gov.uk/gilts/issuance/isucal.htm.

Buying and selling gilts

18

PRIVATE INVESTORS GUIDE

Buying and selling gilts

of a non-competitive application form, itrelates to an auction on of 5% TreasuryStock 20149.

People bidding non-competitively atauctions are asked to enclose a cheque fora specified amount per £100 nominal bid

The minimum amount that a member ofthe public may bid for in this way is£1,000 nominal of the gilt and themaximum is £500,000 for conventionalgilts and £250,000 for index-linked gilts.Each bid must be a multiple of £1,000.

for (a non-competitive bid price).This price is set above theprevailing market price so as toavoid the possibility of investorsbeing asked to pay a further sum ifthe auction price is higher thanthe price paid upfront – a processwhich would delay dispatch of giltcertificates. If, as is usual, theauction price is lower than theprice paid upfront, the differenceis automatically refunded to theinvestor.

Competitive bidsInvestors who wish to bid formore than £500,000 nominal (or£250,000 for index-linked gilts)must submit their bids through aGEMM (Appendix E) stating theprice they are prepared to pay. Ifan investor submits a competitivebid which is too low, they riskreceiving none, or only aproportion of, the amount of thegilt bid for.

3.4 Buying and selling through theDMO Gilt Purchase and SaleService

Computershare, as Agent for the DMO,offers an execution only service for privateinvestors who wish to purchase and sell giltsby post. People wishing to use the servicemust be members of the Approved Groupof investors (section 3.2).

No commission is payable on purchasesat gilt auctions.

9 Amended to asssume Computershare was Registrar.

19

PRIVATE INVESTORS GUIDE

Commission charges, particularly forsmaller transactions, may be lower thancharges made for buying or sellingthrough a stockbroker or bank (section3.1).

Gilts may be bought or sold bycompleting the relevant form(s), availablefrom Computershare by telephoning 0870703 0143 and sending it (with theappropriate payment) to Computersharein Bristol (address in Appendix F). Alltrades (purchases and sales) through theService settle three days after thetransaction date.

A brief summary of how to complete therelevant form(s) is outlined below.

• BuyingA list of gilts available for purchase isenclosed with each purchase form. An up-to-date list can also be accessed on theDMO website www.dmo.gov.uk/gilts/data/stock/stklst.htm (but note that thisincludes ‘rump’ gilts9, which are notavailable for purchase). Updated lists ofgilts for purchase can also be obtained byphoning Computershare on 0870 703 0143.

When purchasing gilts using the service,applications must be made in money, notnominal, terms – cheques must be madepayable to Computershare InvestorServices PLC and crossed ‘A/C Payee’. It isnot possible to specify the nominalamount of a gilt you wish to buy andpresent a blank cheque to be completed bythe Registrar after a purchase has been

made, nor is it possible to specify themaximum price at which your purchase isto be made. Computershare will notaccept third party cheques and paymentsout can only be sent to accounts in thesame name as the purchaser.

On receipt of a completed purchase formComputershare will normally instruct theDMO to execute the purchase on the sameday and will do so at the latest by thefollowing business day. The price paid forthe gilt will be the prevailing market priceas determined by the DMO at the time ofthe purchase.

• CommissionsThe purchase form will also specify thecommission charges applicable to theamount being invested. In completing thecheque investors should be aware that acommission charge will be deducted fromthe funds used to purchase the gilt.

On confirmation of receipt of clearedfunds (typically three days after receipt ofthe postal instruction) Computersharewill settle the purchase of the specifiedgilts from the DMO and will aim to sendyou the gilt certificate four business daysafter the purchase was transacted. You willalso receive a contract note showing thedetailed statement of the costs.

Commission rates for the Retail GiltPurchase and Sale Service will be published on the DMO website at www.dmo.gov.uk/gilts/buysell/purchase-sale.htm

Buying and selling gilts

9 Rump gilts are small illiquid gilts in which gilt-edged market makers are not obliged to make markets. The DMO ishowever prepared to buy rump gilts (Appendix C).

20

PRIVATE INVESTORS GUIDE

Buying and selling gilts

• SellingOn receipt of a completed sale formComputershare will normally instruct theDMO to sell your holding of gilts on thesame day and will do so at the latest by thefollowing business day. You are not able tospecify a price at which your sale is to bemade. The price received for the gilt will bethe prevailing market price as determinedby the DMO at the time of the sale.

Computershare will make payment to youonce it has received settled funds from theDMO. You may choose to receive proceedsby cheque or by automated transfer(BACS). You will also receive a contractnote showing the detailed statement of thecosts and proceeds.

The Computershare website atwww.computershare.com/uk/investor/gilts includes brokerage information,Frequently Asked Questions,downloadable forms (paymentinstructions, gross payment of interest,deduction of income tax, stocktransfer form, change of name andchange of address) and upcomingpayment information.

Further information on buying andselling gilts may be obtained byaccessing Computershare’s website atwww.computershare.com/uk/investor/gilts alternatively, you can call 0870 703 0143.

21

PRIVATE INVESTORS GUIDE

Computershare maintains the mainregister of holdings of gilt-edgedsecurities under a contract from HMTreasury (and administered by theDMO). It will send out dividends to arriveon the due dates, and redemption monieswhen each gilt matures. Gilt holders areadvised to ensure that Computershareholds a record of their current address. Allpersonal records are held in compliancewith the requirements of the DataProtection Act 1998.

Further information may be obtained byvisiting Computershare’s websitewww.computershare.com/uk/investor/giltsor by calling 0870 703 0143.

Holding of gilts in dematerialised formA buyer of gilts held within the CRESTsystem in dematerialised form receivesimmediate and irrevocable legal title totheir securities at the point of transfer.The effect of this is that the register oflegal ownership of dematerialised gilts isnow kept by CrestCo. However,Computershare acts as the paying andreceiving agent for dematerialised giltsand keeps a parallel record of the CRESTregister to enable it to discharge thesefunctions.

Registration of gilts

22

PRIVATE INVESTORS GUIDE

Taxation of gilts

Gilts are a straightforward investment forUK private investors. What follows aimsonly to be a general introduction to themain taxation rules applying to gilts at thetime of writing. The exact treatmentapplied in any individual case depends onthe particular circumstances of eachtaxpayer. If in doubt, investors shouldseek professional advice.

UK individualsa) Conventional and index-linked gilts

• UK individual investors are taxableon interest receivable on gilts(including the interest uplift onindex-linked gilts). Interest isnormally payable gross, but investorsmay opt for net payment onapplication to the Gilts Registrar,Computershare.

• UK individual investors may betaxable on accrued or rebate intereston transfers of gilts.

• Individuals are not liable to capitalgains tax or income tax on thedisposal of gilts.

• No stamp duty or stamp duty reservetax is payable on purchases or sales ofgilts.

b) Gilt strips• All gains and losses on gilt strips held

by individuals are taxed as income onan annual basis. At the end of the taxyear, individuals are deemed for taxpurposes to have disposed of andreacquired their holdings of giltstrips at their then prevailing marketvalue. Any resulting gain (or loss)arising during the year on theholding should be added to the gain(or loss) on any strips actually

maturing in the tax year. The overallgain (or loss) is taxed (relieved) asincome.

c) Individual Savings Accounts (ISAs)• It is possible to hold gilts (conven-

tional, index-linked or strips) in anISA, in which case income andcapital gains from investments heldin ISAs are exempt from income taxand capital gains tax and should notbe shown on tax returns. Should youwish to hold gilts in an ISA they willneed to be purchased through anapproved ISA manager. Any gilt heldin an ISA must have at least five yearsto maturity at the time of purchase.

Further information is available on the Inland Revenue’s website atwww.inlandrevenue.gov.uk

Overseas investorsGilts held on FOTRA (Free of Tax toResidents Abroad) terms, and the intereston them, are generally exempt from tax ifthey are held by persons who are notordinarily resident in the UK. The preciseterms depend on the prospectus underwhich the gilts were issued; but under themost recent version (post -1996), incomeon FOTRA gilts is exempt from tax if theholder is non-resident, unless the incomeis received as part of a trade conducted inthe UK. In April 1998, all existing non-FOTRA gilts were made FOTRA gilts onpost -1996 terms.

• Annual Statements of Interest (ASIs)Investors having their interest paid directto a bank or building society account arenormally sent an Annual Statement of

23

PRIVATE INVESTORS GUIDE

Interest (ASI) at the beginning ofthe following financial year. Anexample is shown opposite. Thisshows the total amount ofinterest received and any tax paidduring the previous tax year. Ifappropriate, investors can opt,instead, for an ASI relating to acalendar tax year.

As an alternative to directpayment, interest can be paid bymeans of a warrant (cheque)which will be sent by post at therisk of the investor. In thisinstance a tax voucher will beattached.

Taxation of gilts

Your tax adviser, your own taxoffice, or your local InlandRevenue Tax Enquiry Centreare all sources of advice andinformation on the taxation ofgilts, should you need it.

Gilts continue to be denominated insterling. However, if in the future, the UKwere to adopt the euro the assumption isthat holdings of gilts would be convertedor redenominated from pounds andpence into euros and cents on entry toEMU, i.e. the day that the £/€ conversionrate becomes effective for the wholesalemarkets.

Details of the redenomination ofindividual gilt holders’ holdings would bemade available in the event of any futureredenomination.

24

PRIVATE INVESTORS GUIDE

Conversion offers

Euro redemonination

From time to time the DMO announcesoffers to holders of gilts to exchange orconvert their holdings of one gilt intoanother at a fixed rate (the ‘conversion’rate) based on the prevailing marketprices of each gilt. The main purpose ofsuch conversion offers is to provide anopportunity for gilt holders to switch outof an existing less liquid gilt into a moreliquid, possibly strippable, gilt withoutincurring transaction costs. Conversionoffers are typically more likely to be heldin times of low outright gilt issuancewhen it is more difficult for the DMO tobuild up large benchmark issues byoutright issuance alone.

Acceptance of such offers is voluntary andgilt holders are free to retain their existing

gilt, although this may become less liquid(less frequently traded) if the bulk ofother holders choose to accept an offer.Should the amount outstanding of a giltwhich has been subject to a conversionoffer be too small to expect a two-waymarket to exist, it becomes known as a‘rump gilt’. See Appendix C for anexplanation of ‘rump gilts’.

Investors who hold a gilt which becomessubject to a conversion offer shouldconsult their stockbroker, solicitor,accountant or other professional adviser ifthey are uncertain as to the best course tofollow.

25

PRIVATE INVESTORS GUIDE

Appendix A

Gilts in issue 30 November 2004Total amount in issue (inc IL uplift) £mn: 340,282

Conventional Gilts Redemption Dividend Amount Amount held in DMO/CRNDDate Dates in issue stripped form Holdings

(£mn norm) at (DMO &2 Dec 2004 CRND) at

30 Nov 2004

Shorts: (maturity up to 7 years)

91/2% Conversion 2005 18-Apr-05 18 Apr/Oct 4,469 - 97

81/2% Treasury 2005 07-Dec-05 7 Jun/Dec 10,486 157 312

73/4% Treasury 2006 08-Sep-06 8 Mar/Sep 3,955 - 441

71/2 % Treasury 2006 07-Dec-06 7 Jun/Dec 11,807 159 276

41/2% Treasury 2007 07-Mar-07 7 Mar/Sep 11,500 1 22

81/2% Treasury 2007 16-Jul-07 16 Jan/Jul 4,638 - 371

71/4% Treasury 2007 07-Dec-07 7 Jun/Dec 11,103 133 247

5% Treasury 2008 07-Mar-08 7 Mar/ Sep 14,221 45 163

51/2% Treasury 2008/2012 10-Sep-08 10 Mar/Sep 1,026 182

4% Treasury 2009 07-Mar-09 7 Mar/Sep 13,250 26 18

53/4% Treasury 2009 07-Dec-09 7 Jun/Dec 11,437 120 358

43/4% Treasury 2010 07-Jun-10 7 Jun/Dec 3,500 1

61/4% Treasury 2010 25-Nov-10 25 May/Nov 4,958 - 477

9% Conversion 2011 12-Jul-11 12 Jan/Jul 5,396 - 205

Mediums: (maturity 7 to 15 years)

73/4% Treasury 2012/2015 26-Jan-12 26 Jan/Jul 805 - 339

5% Treasury 2012 07-Mar-12 7 Mar/ Sep 13,346 183 235

8% Treasury 2013 27-Sep-13 27 Mar/Sep 6,181 - 386

5% Treasury 2014 07-Sep-14 7 Mar/Sep 13,050 21 57

43/4% Treasury 2015 07-Sep-15 7 Mar/Sep 13,000 143 8

8% Treasury 2015 07-Dec-15 7 Jun/Dec 7,377 220 172

83/4% Treasury 2017 25-Aug-17 25 Feb/Aug 7,751 - 380

Longs: (maturity over 15 years)

8% Treasury 2021 07-Jun-21 7 Jun/Dec 16,741 272 346

5% Treasury 2025 07-Mar-25 7 Mar/Sep 12,922 46 177

6% Treasury 2028 07-Dec-28 7 Jun/Dec 11,756 197 309

41/4% Treasury 2032 07-Jun-32 7 Jun/Dec 13,829 557 251

41/4% Treasury 2036 07-Mar-36 7 Mar/Sep 12,250 70 3

43/4% Treasury 2038 07-Dec-38 7 Jun/Dec 9,500 15 5

26

PRIVATE INVESTORS GUIDE

Appendix A

Index-Linked Gilts Redemption Dividend Amount Nominal Central GovtDate Dates in issue including Holdings

(£mn norm) Inflation Uplift (DMO &CRND) at

29 Oct 2004

2% I-L Treasury 2006 19-Jul-06 19 Jan/Jul 2,037 5,412 37

21/2% I-L Treasury 2009 20-May-09 20 May/Nov 3,098 7,261 74

21/2% I-L Treasury 2011 23-Aug-11 23 Feb/Aug 4,342 10,752 70

21/2% I-L Treasury 2013 16-Aug-13 16 Feb/Aug 6,022 12,462 105

21/2% I-L Treasury 2016 26-Jul-16 26 Jan/Jul 6,805 15,391 170

21/2% I-L Treasury 2020 16-Apr-20 16 Apr/Oct 5,568 12,389 68

21/2% I-L Treasury 2024 17-Jul-24 17 Jan/Jul 5,751 10,870 112

41/8% I-L Treasury 2030 22-Jul-30 22 Jan/Jul 3,521 4,811 72

2% I-L Treasury 2035 26-Jan-35 26 Jan/Jul 5,550 5,902 1

27

PRIVATE INVESTORS GUIDE

Undated Gilts Redemption Dividend Amount in Central Govt Holdings(non-rump) Date Dates issue (DMO & CRND) at

30 Nov 2004

21/2% Treasury Undated 1 Apr/Oct 493 22

31/2% War Undated 1 Jun/Dec 1939 30

‘Rump’ Gilts Redemption Dividend Amount in Central Govt HoldingsDate Dates issue (DMO & CRND) at

30 Nov 2004

101/2% Exchequer 2005 20-Sep-05 20 Mar/Sep 24 16

93/4% Conversion 2006 15-Nov-06 15 May/Nov 6 3

9% Treasury 2008 13-Oct-08 13 Apr/Oct 687 154

8% Treasury 2009 25-Sep-09 25 Mar/Sep 393 126

9% Treasury 2012 06-Aug-12 6 Feb/Aug 403 158

12% Exchequer 2013/2017 12-Dec-13 12 Jun/Dec 58 9

4% Consolidated Undated 1 Feb/Aug 358 62

21/2% Consolidated Undated 5 Jan/Apr/Jul/Oct 272 48

31/2% Conversion Undated 1 Apr/Oct 88 73

3% Treasury Undated 5 Apr/Oct 53 7

21/2% Annuities Undated 5 Jan/Apr/Jul/Oct 3 0.5

23/4% Annuities Undated 5 Jan/Apr/Jul/Oct 1 0.3

Appendix A

28

PRIVATE INVESTORS GUIDE

Appendix B

Gilt Dividend Dividend Dividend Dividend Date per £100 Date per £100

2% IL 2006 19-Jan-05 £2.68 19-Jul-05 N/A

21/2% IL 2009 20-May-05 £2.9854 20-Nov-05 N/A

21/2% IL 2011 23-Feb-05 £3.13 23-Aug-05 N/A

21/2% IL 2013 16-Feb-05 £2.6176 16-Aug-05 N/A

21/2% IL 2016 26-Jan-05 £2.8561 26-Jul-05 N/A

21/2% IL 2020 16-Apr-05 £2.8234 16-Oct-05 N/A

21/2% IL 2024 17-Jan-05 £2.3869 17-Jul-05 N/A

41/8% IL 2030 22-Jan-05 £2.8471 22-Jul-05 N/A

2% IL 2035 26-Jan-05 £1.074309 26-Jul-05 N/A

Cash flows for 2005:Gilt Dividend Dividend Dividend Dividend

Date per £100 Date per £100

43/8% IL 2004 21-Apr-04 £2.9295 21-Oct-04 2.9650 (+135.5457redemption

payment)

2% IL 2006 19-Jan-04 £2.61 19-Jul-04 2.62

21/2% IL 2009 20-May-04 £2.8965 20-Nov-04 2.9298

21/2% IL 2011 23-Feb-04 £3.03 23-Aug-04 3.07

21/2% IL 2013 16-Feb-04 £2.5405 16-Aug-04 2.5714

21/2% IL 2016 26-Jan-04 £2.7795 26-Jul-04 2.7979

21/2% IL 2020 16-Apr-04 £2.7360 16-Oct-04 2.7692

21/2% IL 2024 17-Jan-04 £2.3229 17-Jul-04 2.3382

41/8% IL 2030 22-Jan-04 £2.7708 22-Jul-04 2.7891

2% IL 2035 26-Jan-04 £1.045507 26-Jul-04 1.052419

Index-linked gilt cash flowsCash flows for 2005:

Note: The latest relevant RPI available when these tables were produced was that for September 2004 published in October 2004.

29

PRIVATE INVESTORS GUIDE

Frequently Asked Questions

Q1: What is a ‘rump’ gilt?

A ‘rump’ gilt is a gilt, declared by the DMO, in which GEMMs are not required to maketwo-way markets. The current list of rump gilts is available on the DMO websitewww.dmo.gov.uk/gilts/data/stock/stklst.htm. Current Rump gilts are identified inAppendix A; any changes to the list will be published on the DMO website.

The Government will not sell further amounts of ‘rump’ gilts to the market, but theDMO is prepared, when asked by a GEMM, to bid a price of its own choosing for suchgilts. Members of the public who are members of the Approved Group can sell ‘rump’gilts via the DMO Gilts Purchase and Sale Service (see section 3.4 above) but not buythem.

Q2: Some newspapers quote interest and redemption yields for gilts. What is thedifference? And why are redemption yields so low?

The interest yield is simply a yield derived by dividing the coupon by the price paid. It isof use only as a short-term indicator of return over a short period of time. Theredemption yield - or yield to maturity - is the standard way for measuring the return ongilts. It is a complex net present value calculation which assumes that the gilt is held tomaturity and repaid at par and that all future income streams from the coupons arereinvested at current redemption yields. Where a gilt is high coupon and trading wellabove par, this calculation reflects the capital loss involved in holding to redemption(although this loss is mitigated by the receipt of coupon payments above prevailinginterest rates). Similarly, the calculation takes into account the effect of capital gain for agilt trading well below par (at a discount).

Q3: Why are yields on index-linked gilts so much lower than those on conventionals?

Because yields on index-linked gilts are ‘real’ yields, that is they represent the return tothe holder of the gilt after taking account of inflation. All real yields published by theDMO assume an annual inflation rate of 3%, although some newspapers also assume a5% rate.

Appendix C

30

PRIVATE INVESTORS GUIDE

Appendix D

Glossary

Accrued interest. Interest earned on a giltsince the last interest payment date, whichis paid and received at the time of atransaction in addition to the clean priceof the gilt.

Approved Group. See section 3.2.

Auction (Gilt). Conventional gilts: Opento all bidders, although only GEMMs areallowed to make telephone bids -individuals can make non-competivepostal bids. Successful bidders inconventional gilt auctions are allotted giltson a bid price basis, paying the price theybid. There is also a limited facility fornon-competitive bids.

Auction (Index-linked gilts). Open toIndex-linked GEMMs only (forcompetitive bids) and conducted on auniform price basis, based on the lowestaccepted price. There is also a limitedfacility for non-competitive bids.

Basis point (bp). One hundredth of onepercent.

Benchmarks. Informal term for liquid gilts,usually with a large outstanding amountand coupons in line with the prevailinggeneral level of interest rates, which areused by participants in other markets toprice other instruments of correspondingmaturity, e.g. corporate bonds.

Clean price. Quoted price of a gilt whichexcludes accrued interest.

Competitive bid. A bid for the gilt which,

if successful, would be allotted at the pricemade by a bidder in an auction for aconventional gilt.

Non-competitive bid. A bid where noprice is specified; such bids are allotted atthe weighted average price of successfulcompetitive bid prices.

Conventional gilts (including double-dated). Gilts on which interest paymentsand principal repayments are fixed.

Coupon. Annual interest paid on giltholding, usually in two equal, semi-annual instalments. Expressed as inpercentage terms.

Cum dividend. The trading status of abond where the purchaser of the bond isentitled to receive the next interest ordividend payment. The alternative is exdividend, where the seller of the bondretains the right to receive the nextinterest or dividend payment.

DMO. The United Kingdom DebtManagement Office.

Duration. A measure of a bond’svolatility or the sensitivity of the bond’sprice to changes in interest rates (definedas the weighted average of the number ofyears in the bond’s life, the weightingfactor being the present value of the cashflows discounted at the bond’sredemption yield).

GEMMs. Gilt-edged Market Makers –primary dealers in gilts.

Gilt. A UK Government security issued

31

PRIVATE INVESTORS GUIDE

by HM Treasury. The term ’gilt’ (or ‘gilt-edged’) is a reference to the primarycharacteristic of gilts as an investment:their security.

IGs. Index-linked gilts whose couponsand final redemption payment are relatedto movements in the Retail Prices Index(RPI).

Liquidity. A term describing the ease withwhich one can undertake transactions in aparticular market or instrument. Amarket where there are always buyers andsellers willing to transact at competitiveprices is regarded as liquid.

Maturity date. Date on which a dated giltis redeemed i.e. the capital is repaid.

Nominal amount/value. The face valueor amount of a gilt, i.e. the amount ofcapital a holder receives when the giltredeems.

Nominal amount/value (uplifted).Applicable to index linked-gilts: this is thenominal amount uplifted by inflationsince the gilt was first issued.

Primary market. The issuance by theDMO (typically by auction) of a new giltor a new tranche of an existing gilt.

Redemption yield. The redemption yieldis the measure of the return implicit in thecurrent market price assuming the gilt isheld to redemption and all cash flows arere-invested back into the bond.

Register. Record of ownership ofsecurities. For gilts, excluding bearerbonds, entry in an official register conferstitle.

Secondary market. Where existingsecurities are traded by marketparticipants.

Spread. Difference between a marketmaker’s buying and selling prices.

Strips. Separate Trading of RegisteredInterest and Principal Securities; for some(‘strippable’) gilts, the coupons andprincipal can be traded separately.

Undated gilts. Gilts for which there is nofixed redemption date.

Yield. The DMO quotes only grossredemption yields. See redemption yield.

Yield curve. The mathematicalrelationship computed across all giltsbetween maturity and yield.

Appendix D

32

PRIVATE INVESTORS GUIDE

Appendix E

List of Gilt-edged market makers (GEMMs)ABN Amro Bank NV JP Morgan Securities Limited250 Bishopsgate 125 London WallLondon EC2M 4AA London EC2Y 5AJ

Barclays Capital* Lehman Brothers International (Europe)*5 The North Colonnade 25 Bank StreetCanary Wharf DocklandsLondon E14 4BB London E14 5LE

Citigroup Global Markets Limited Merrill Lynch International*Citigroup Centre Merrill Lynch Financial Centre33 Canada Square 2 King Edward StreetLondon E14 5LB London EC1A 1HQ

CS First Boston Limited* Morgan Stanley & Co. InternationalOne Cabot Square Limited*London E14 4QJ 20 Cabot Square

Canary WharfDeutsche Bank AG (London Branch)* London E14 4QWWinchester House1 Great Winchester Street Royal Bank of Canada Europe Limited*London EC2N 2DB Thames Court

One QueenhitheDresdner Bank AG (London Branch)* London EC4V 4DEPO Box 18075 Riverbank House Royal Bank of Scotland* 2 Swan Lane 135 BishopsgateLondon EC4R 3UX London EC2M 3UR

Goldman Sachs International Limited* UBS Limited*Peterborough Court 1 Finsbury Avenue133 Fleet Street London EC2M 2PPLondon EC4A 2BB

Winterflood Securities Limited*HSBC Bank PLC* The Artrium Building8 Canada Square Cannon BridgeLondon E14 5HQ 25 Dowgate Hill

London EC4R 2GA

*Index-linked Gilt-edged Market Makers.

33

PRIVATE INVESTORS GUIDE

Useful contacts andwebsites

UK DEBT MANAGEMENT OFFICEFor general enquiries and planned giltissuance: Eastcheap Court 11 Philpot LaneLondon EC3M 8UDTelephone 020 7862 6500Website address: www.dmo.gov.uk

COMPUTERSHARE INVESTORSERVICES PLC Registered in England No 3498808For enquiries about individual holdings,giltholder services and Approved Groupforms: The PavilionsBridgwater RoadBristolBS13 8AETelephone 0870 703 0143Website address:www.computershare.com

BANK OF ENGLAND STERLINGMARKETS DIVISIONFor enquiries on index-linked interestpayments on index-linked gilt first issuedbefore 2002 and the calculation ofredemption proceeds on such gilts: Threadneedle StreetLondon EC2R 8AHTelephone 020 7601 4444Website address:www.bankofengland.co.uk

THE LONDON STOCK EXCHANGEFor information on stockbrokers who willarrange transactions in gilts: 10 Paternoster SquareLondon EC4M 7LS Telephone 020 7797 1000Website address:www.londonstockexchange.com

INDEPENDENT COMPLAINTSSERVICEIf you have a complaint about the serviceprovided by a stockbroker: The Financial OmbudsmanSouth Quay Plaza183 March WallLondon E14 9SRTelephone 0845 080 1800Website address:www.financial-ombudsman.org.uk

Appendix F

34

PRIVATE INVESTORS GUIDE

Notes

35

PRIVATE INVESTORS GUIDE

PRIVATE INVESTORS GUIDE

Header United KingdomDebtManagementOffice

Eastcheap Court11 Philpot LaneLondon EC3M 8UD