2016 hostile m&a and activism - practising law...

TRANSCRIPT

Copyright ©2017 Sullivan & Cromwell LLP

0

Stephen M. Kotran

March 8, 2017

2016 Hostile M&A and Activism

Copyright ©2017 Sullivan & Cromwell LLP

Copyright ©2017 Sullivan & Cromwell LLP

1

Hostile M&A

2

Copyright ©2017 Sullivan & Cromwell LLP

2016 Global Hostile M&A

Target

Acquirer

Equity Value ($m)

Transaction Status

1. Reading International, Inc. Patton Vision, LLC 432 Pending

2. Alliance HealthCare Services, Inc. Tahoe Investment Group Co., Ltd. 50 Pending

3. Sky plc Twenty-First Century Fox, Inc. 14,217 Pending

4. OCI Partners LP OCI N.V. 136 Pending

5. SciClone Pharmaceuticals, Inc. Ally Bridge Group Capital Partners, GL Capital Management GP Limited 518 Pending

6. Digi International Inc. Belden Inc. 359 Pending

7. SunCoke Energy Partners, L.P. SunCoke Energy, Inc. 380 Pending

8. Reynolds American Inc. British American Tobacco p.l.c. 49,129 Pending

9. Alon USA Energy, Inc. Delek US Holdings, Inc. 459 Pending

10. Cheniere Energy Partners LP Holdings, LLC Cheniere Energy, Inc. 1,010 Withdrawn

11. Columbia Pipeline Partners LP TransCanada Corporation 915 Completed

12. Affinity Gaming Z Capital Partners, L.L.C. 209 Completed

13. Premier Farnell plc Avnet, Inc. 903 Completed

14. Blue Bird Corporation American Securities LLC 118 Withdrawn

15. Concord Medical Services Holdings Limited Blue Ocean Management Limited 126 Pending

16. The Hershey Company Mondelez International, Inc. 22,831 Withdrawn

17. InterOil Corporation Exxon Mobil Corporation 2,236 Completed

18. Skullcandy, Inc. Mill Road Capital Management LLC 164 Completed

19. Qunar Cayman Islands Limited Ocean Imagination L.P. 4,383 Pending

20. SolarCity Corporation Tesla Motors, Inc. 2,589 Completed

21. Patriot National, Inc. Ebix, Inc. 255 Withdrawn

22. Ashford Hospitality Prime, Inc. Weisman Group, LLC 548 Pending

23. eFuture Holding Inc. Beijing Shiji Information Technology Co., Ltd 16 Completed

24. iKang Healthcare Group, Inc. Yunfeng Capital 1,466 Pending

25. Monsanto Company Bayer AG 55,916 Pending

26. Polycom, Inc. Siris Capital Group, LLC 1,674 Completed

27. Actions Semiconductor Co., Ltd. Embona Holdings (Malaysia) Limited, Middlesex Holdings Corporation Inc, Nutronics Technology Corporation, Rich Dragon Consultants Limited, Surrey Glory Investments Inc., Tongtong Investment Holding Co. Ltd., Uniglobe Securities Limited

33 Completed

28. The Andersons, Inc. HC2 Holdings, Inc. 1,043 Pending

29. Zhaopin Limited Management Buyout 1,078 Pending

3

Copyright ©2017 Sullivan & Cromwell LLP

2016 Global Hostile M&A

Target

Acquirer

Equity Value ($m) Transaction Status

30. Medivation, Inc Sanofi SA 10,018 Withdrawn

31. Tribune Publishing Company Gannett Co., Inc. 475 Withdrawn

32. Autohome Inc. Management Buyout 3,465 Withdrawn

33. Integrated Device Technology, Inc. Investor 4,140 Pending

34. LeapFrog Enterprises, Inc. Investor 78 Withdrawn

35. Premier Foods plc McCormick & Company, Incorporated 768 Withdrawn

36. Affymetrix Inc. Origin Technologies Corporation, LLC 1,359 Withdrawn

37. Starwood Hotels & Resorts Worldwide, Inc. Anbang Insurance Group Co., Ltd., J.C. Flowers & Co., Primavera Capital Limited 13,965 Withdrawn

38. E-Commerce China Dangdang Inc. iMeigu Capital Management Ltd. 724 Withdrawn

39. National Interstate Corporation American Financial Group, Inc. 311 Completed

40. Federal-Mogul Holdings Corporation Icahn Enterprises L.P. 304 Completed

41. United Technologies Corporation Honeywell International Inc. 90,335 Withdrawn

42. Jumei International Holding Limited Management Buyout 467 Pending

43. Sinovac Biotech Ltd. Beijing Sinobioway Group Co., Ltd., CICC Qianhai Development Fund, Fuerde Global Investment Limited, Heng Feng Investments (International) Limited, PKU V-Ming (Shanghai) Investment Holdings, Shandong Sinobioway Biomedicine Co., Ltd.,

391 Pending

44. Ku6 Media Co., Ltd. Shanda Interactive Entertainment Limited 15 Completed

45. Amaya Inc. Management Buyout 1,905 Withdrawn

46. Sinovac Biotech Ltd. Management Buyout 308 Pending

47. Agria Corporation Management Buyout 66 Withdrawn

48. Axiall Corporation Westlake Chemical Corporation 2,329 Completed

49. Terex Corporation Zoomlion Heavy Industry Science and Technology Co. 3,364 Withdrawn

50. Zhaopin Limited CDH Investments, Shanghai Goliath Investment Management L.P. 495 Pending

51. Rouse Properties, Inc. Brookfield Asset Management Inc. 705 Completed

52. Synutra International, Inc. Management Buyout 125 Pending

TOTAL: $299,305

4

Copyright ©2017 Sullivan & Cromwell LLP

2016 Hostile M&A

• Majority of hostile bids are withdrawn as companies remain independent or sell to a third party:

1. Includes hostile M&A transactions since January 1, 2011, above $500 million transaction value at announcement; excludes pending transactions. Percentages are based on the number of deals. Sold to hostile bidder includes transactions where a revised bid was accepted.

5

Copyright ©2017 Sullivan & Cromwell LLP

2016 Hostile M&A

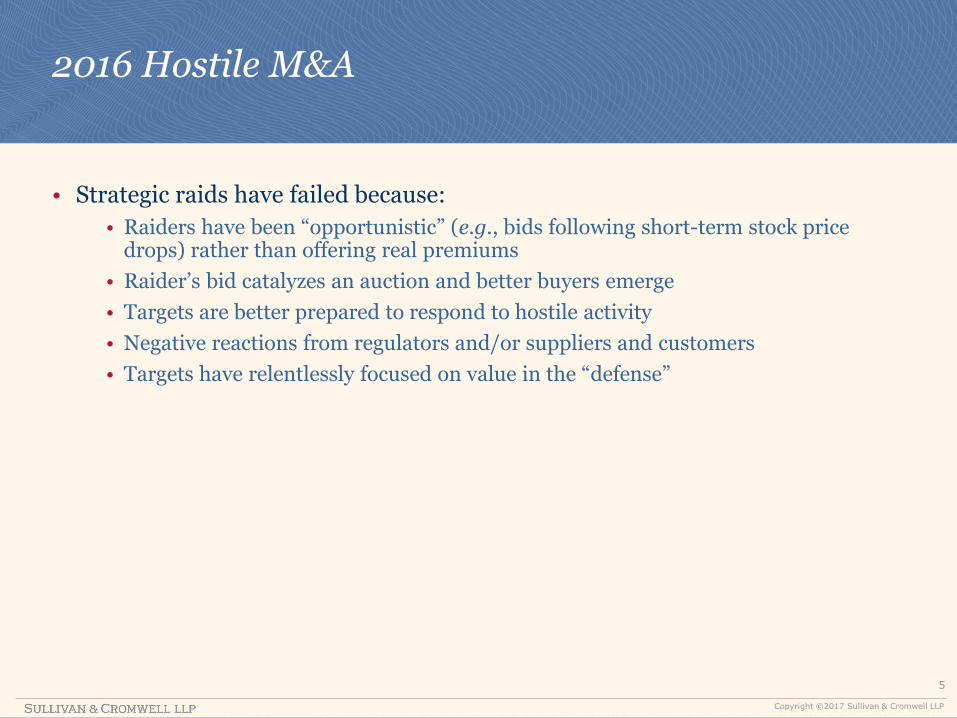

• Strategic raids have failed because:

• Raiders have been “opportunistic” (e.g., bids following short-term stock price drops) rather than offering real premiums

• Raider’s bid catalyzes an auction and better buyers emerge

• Targets are better prepared to respond to hostile activity

• Negative reactions from regulators and/or suppliers and customers

• Targets have relentlessly focused on value in the “defense”

6

Copyright ©2017 Sullivan & Cromwell LLP

2016 Hostile M&A

7

Copyright ©2017 Sullivan & Cromwell LLP

Allergan SEC Administrative Order

• In January 2017, the SEC ordered Allergan to pay $15 million and cease and desist violations of Section 14(d) of the Exchange Act and Rule 14d-9 due to Allergan’s failure to disclose negotiations with third parties that it conducted in response to a tender offer.

• After filing a Schedule 14D-9 in response to a tender offer by Valeant Pharmaceuticals International and Pershing Square, in which Allergan stated that the tender offer was inadequate, Allergan failed to disclose that it was “in negotiations” with two third parties regarding potential extraordinary transactions.

• The SEC stated that at the time Allergan or a third party provided a counterproposal on price for an extraordinary transaction, Allergan was required by Schedule 14D-9 to disclose that Allergan was engaged “in negotiations” regarding an extraordinary transaction and by Rule 14d-9 to update its previously filed Schedule 14D-9 to reflect this material change.

• Allergan did not make such disclosures in a timely manner, despite multiple communications from SEC staff (following market rumors and news reports) that it should update the Schedule 14D-9 if it was in negotiations regarding a potential extraordinary transaction.

8

Copyright ©2017 Sullivan & Cromwell LLP

Allergan SEC Administrative Order

• Generally, companies are not required to disclose M&A negotiations unless the disclosure is necessary to correct prior disclosure or public statements, but this serves as a reminder that the disclosure rules regarding negotiations in the context of tender offers differ from the disclosure rules in the context of other transactions.

• The SEC will consider a target company to be “in negotiations” when it or a third party provides a counterproposal with regard to the acquisition price for a potential transaction.

• It is important to be mindful of this trigger in the tender offer context and carefully monitor when the SEC may consider negotiations to have had occurred, particularly as the offer/counteroffer chronology will be detailed in the background section of any proxy filed in connection with a transaction.

• The identity of the third party and terms of the proposed transaction are not necessarily required to be disclosed at an early stage, but only the fact that preliminary negotiations with a third party are occurring.

• The language included by Allergan in Item 7 of Schedule 14D-9, stating the Allergan board’s position that Allergan would not disclose a potential transaction unless and until an agreement had been reached, is ineffective in the Schedule 14D-9 context.

Copyright ©2017 Sullivan & Cromwell LLP

9

Activism

10

Copyright ©2017 Sullivan & Cromwell LLP

Activist

11

Copyright ©2017 Sullivan & Cromwell LLP

Overview of the Current Environment

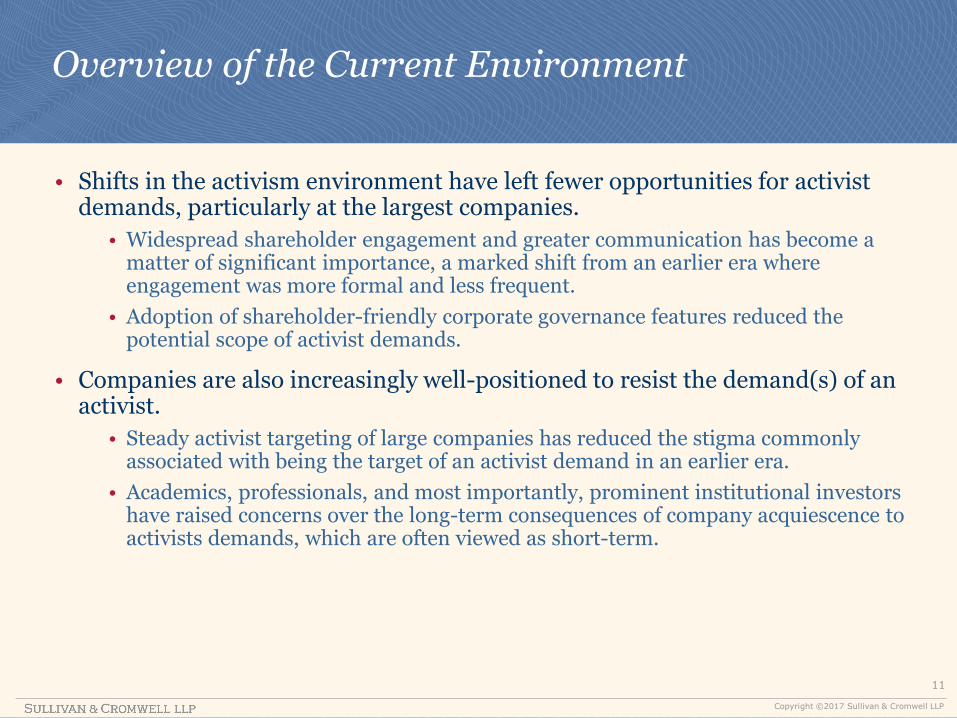

• Shifts in the activism environment have left fewer opportunities for activist demands, particularly at the largest companies.

• Widespread shareholder engagement and greater communication has become a matter of significant importance, a marked shift from an earlier era where engagement was more formal and less frequent.

• Adoption of shareholder-friendly corporate governance features reduced the potential scope of activist demands.

• Companies are also increasingly well-positioned to resist the demand(s) of an activist.

• Steady activist targeting of large companies has reduced the stigma commonly associated with being the target of an activist demand in an earlier era.

• Academics, professionals, and most importantly, prominent institutional investors have raised concerns over the long-term consequences of company acquiescence to activists demands, which are often viewed as short-term.

12

Copyright ©2017 Sullivan & Cromwell LLP

84 93

111 119

129 122

112

H12013

H22013

H12014

H22014

H12015

H22015

H12016

Fewer Campaigns and Dollars Invested

• Between 2013 and 2015, activist campaigns were publicly announced at increasing rates. This growth trend flattened in 2016 and the total number of public activist campaigns announced fell slightly compared to 2015.

• Prior to H1 2015, assets under management by activist hedge funds were growing consistently. This trend has reversed, which reflects both investor withdrawals and negative activist hedge fund performance.

221

272 300

254

2013 2014 2015 2016

Total Activist Hedge Fund AUM ($bn) Publicly Announced Activist Campaigns

13

Copyright ©2017 Sullivan & Cromwell LLP

Higher Returns

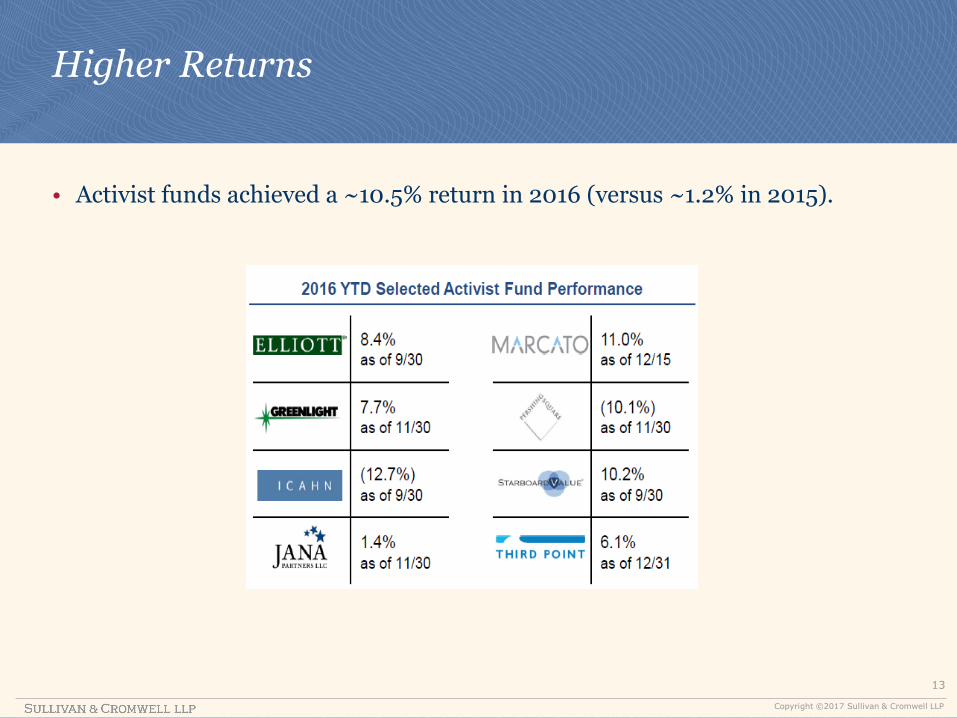

• Activist funds achieved a ~10.5% return in 2016 (versus ~1.2% in 2015).

14

Copyright ©2017 Sullivan & Cromwell LLP

New Activists on the Rise

• The changes in the activist environment have caused an increase in the number of activist campaigns by new and less frequent activists:

• For example, Citron, Viex Capital

• 95 activists with no prior activism between 2013 and 2015 made demands at U.S. public companies in 2016.

• Record number of shareholders initiated campaigns for the first time.

• Only 5% of proxy fights in 2016 were announced by activists who brought more than 5 campaigns from 2013 to 2016, down from 14% in 2013.

15

Copyright ©2017 Sullivan & Cromwell LLP

Different Activist Strategies and Objectives

• Smaller, younger funds can be more aggressive with their approach and demands because:

• they have less campaign experience and thus a less nuanced approach

• they want a public “win” early on to establish a track record and gain credibility

• smaller target companies are generally more prone to activist approaches (less prepared, less informed, fewer resources, e.g., IR/PR firm)

• it’s easier to exert influence at smaller target companies with fewer dollars at risk

• Activists’ investment horizons can range from very short-term to somewhat longer term.

• An activist hedge fund’s redemption policy (e.g., quarterly redemption vs. longer-term “lock-up” commitments) may also have an impact on its investment strategy.

16

Copyright ©2017 Sullivan & Cromwell LLP

Shift to Small and Mid-Cap Targets

• All companies across the market cap spectrum remain subject to activism.

• Smaller companies were targeted more frequently than larger companies in 2016, partially a response to the shifts in the activism environment and the increasing number of campaigns announced by less frequent activists.

• Since 2013, companies with market caps between $100 million and $500 million have represented 38–45% of campaigns, but only 28% of public companies.

17

Copyright ©2017 Sullivan & Cromwell LLP

Target Company Industries

• Activists have targeted a wide variety of industries, with certain isolated industries being particularly prevalent in a given year.

• Most common industries targeted since 2013:

INDUSTRY NUMBER OF CAMPAIGNS

Investment Trusts/Mutual Funds 55

Packaged Software 44

Miscellaneous Commercial Services 41

Major Pharmaceuticals 31

Restaurants 28

• In 2016, particular industries that were targeted more than in prior years include: real estate development (11), financial conglomerates (8), semiconductors (7), medical specialties (7), and movies & entertainment (7).

• Expectations for coming year targets: energy, retail and restaurant industries. • Oil, gas and energy companies are becoming healthier as commodities prices rise,

which will allow well-positioned and well-run companies to begin to regain their footing and make it easier to spot those that are struggling.

• Retail stores are facing pressure from online shopping.

• Restaurants are facing pressure due to meal-kits (e.g., Blue Apron) and declining grocery prices.

18

Copyright ©2017 Sullivan & Cromwell LLP

Increasing Institutional Investor Importance

• Activists generally hold only a small stake in target companies and instead depend on the support of large institutional investors to gain traction in proxy contests and other activist campaigns.

• As retail ownership declines and institutional ownership concentration increases, activists can rapidly garner support from other shareholders with less engagement and smaller costs.

• The importance of this concept is exemplified by the increasing shareholder ownership concentration among U.S. public companies held by only the largest four institutional investors: Vanguard, State Street Global Advisors, Fidelity, and Blackrock.

Retail Ownership of Public Company Shares

35%

33%

31% 32%

30%

2012 2013 2014 2015 2016

• Activists may also have increased support due to a shift in investment philosophy: investors are shifting away from active investment strategies and relying more on passive holdings, such as index funds.

• Index funds are long-term investors — their inability to nimbly exit investments increases their willingness to directly express their views on governance matters and support activism campaigns that on average, increase enterprise value.

Average Total Stake in S&P 500 by Four Largest

Asset Managers

17% 19% 20% 20% 21%

2012 2013 2014 2015 2016

19

Copyright ©2017 Sullivan & Cromwell LLP

Institutional Investor Engagement Efforts

• Institutional investors have developed robust internal proxy advisory functions and have emphasized that responsiveness to activist investor demands is no substitute for direct engagement with significant shareholders.

• In January 2012, BlackRock began sending letters to public company chairs and CEOs, highlighting BlackRock’s detailed voting policies and governance expertise, and encouraging companies not to rely solely on proxy advisory firm recommendations.

• Vanguard sent similar letters to portfolio companies emphasizing the importance of corporate governance engagement and emphasis on certain corporate governance principles.

• Other important institutional investors have raised concerns over the potential for activist demands to focus on short-term value rather than long-term growth.

• In October 2016, State Street Global Advisors issued a memo and press release expressing concern that quick settlements with activists may harm long-term shareholders.

20

Copyright ©2017 Sullivan & Cromwell LLP

Settlement Agreements

• Increased Frequency: The percentage of completed activist campaigns with SEC-filed settlement agreements has increased significantly in 2016.

• In 2015, 81 settlement agreements were filed with the SEC, representing only 25% of completed campaigns. This percentage increased to more than 40% in 2016.

• Increased Speed:

• Through Nov. 2016, 30% of settlements were reached in less than 1 month after the initiation of the campaign (versus 15% in 2015).

• The increased frequency and speed of settlements is consistent with recent concerns by institutional investors that some companies may be settling too quickly without broad consultation.

21

Copyright ©2017 Sullivan & Cromwell LLP

Institutional Investor Engagement Efforts

State Street Global Advisors memo and press release (October 2016):

• Settlements that are entered into quickly and without appropriate consultation with other shareholders deprive long-term shareholders of the opportunity to express their views.

• State Street’s review of the actions of the largest activists identified several red flags that raise questions about the long-term effects of activism, including increases in CEO pay and tying CEO pay to earnings per share, as well as undue focus on share repurchases, spin-offs and other financial engineering.

• Settlement agreements should include terms that protect the interests of long-term investors:

• Longer Duration: Typical settlement agreement duration of 6–18 months may not be long enough to incentivize the company and activist to be sensitive to long-term factors.

• Long-Term Shareholding Commitment: Specify minimum ownership levels of activists and/or nominees for long periods in exchange for any board representation, and require directors who are affiliated with an activist to tender their resignation if the activist’s ownership in the company falls below the minimum threshold.

• Restrictions on Pledging: Activist investors often pledge a significant portion of their stake in margin accounts. Boards should evaluate carefully the pledging practices of activists and develop robust mechanisms to oversee and mitigate any potential risk from the pledge positions to the stock price.

22

Copyright ©2017 Sullivan & Cromwell LLP

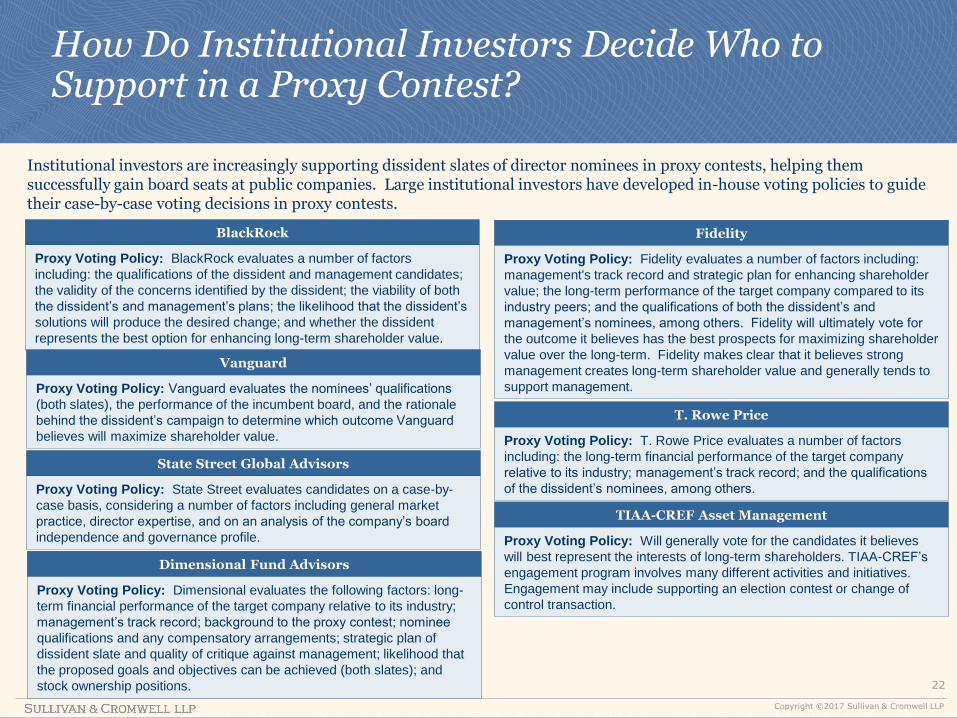

How Do Institutional Investors Decide Who to Support in a Proxy Contest?

Institutional investors are increasingly supporting dissident slates of director nominees in proxy contests, helping them successfully gain board seats at public companies. Large institutional investors have developed in-house voting policies to guide their case-by-case voting decisions in proxy contests.

BlackRock

Proxy Voting Policy: BlackRock evaluates a number of factors

including: the qualifications of the dissident and management candidates;

the validity of the concerns identified by the dissident; the viability of both

the dissident’s and management’s plans; the likelihood that the dissident’s

solutions will produce the desired change; and whether the dissident

represents the best option for enhancing long-term shareholder value.

Vanguard

Proxy Voting Policy: Vanguard evaluates the nominees’ qualifications

(both slates), the performance of the incumbent board, and the rationale

behind the dissident’s campaign to determine which outcome Vanguard

believes will maximize shareholder value.

TIAA-CREF Asset Management

Proxy Voting Policy: Will generally vote for the candidates it believes

will best represent the interests of long-term shareholders. TIAA-CREF’s

engagement program involves many different activities and initiatives.

Engagement may include supporting an election contest or change of

control transaction.

T. Rowe Price

Proxy Voting Policy: T. Rowe Price evaluates a number of factors

including: the long-term financial performance of the target company

relative to its industry; management’s track record; and the qualifications

of the dissident’s nominees, among others.

Dimensional Fund Advisors

Proxy Voting Policy: Dimensional evaluates the following factors: long-

term financial performance of the target company relative to its industry;

management’s track record; background to the proxy contest; nominee

qualifications and any compensatory arrangements; strategic plan of

dissident slate and quality of critique against management; likelihood that

the proposed goals and objectives can be achieved (both slates); and

stock ownership positions.

Fidelity

Proxy Voting Policy: Fidelity evaluates a number of factors including:

management's track record and strategic plan for enhancing shareholder

value; the long-term performance of the target company compared to its

industry peers; and the qualifications of both the dissident’s and

management’s nominees, among others. Fidelity will ultimately vote for

the outcome it believes has the best prospects for maximizing shareholder

value over the long-term. Fidelity makes clear that it believes strong

management creates long-term shareholder value and generally tends to

support management.

State Street Global Advisors

Proxy Voting Policy: State Street evaluates candidates on a case-by-

case basis, considering a number of factors including general market

practice, director expertise, and on an analysis of the company’s board

independence and governance profile.

23

Copyright ©2017 Sullivan & Cromwell LLP

Proxy Advisory Firms in Contested Elections

• As institutional investors develop their own proxy advisory functions internally, the impact of proxy advisory firms, such as Institutional Shareholder Services (ISS) and Glass Lewis & Co., wanes.

• In 2013, ISS recommendations matched the proxy outcome in 77% of proxy contests. In 2016, that figure declined to 63%.

• Nonetheless, the proxy advisory firms still have a notable effect on the outcome of a contested election. Their recommendations still match the outcome of the election in a majority of cases and therefore, issuers should be mindful of their policy positions.

• ISS votes on a case-by-case basis on the election of directors in contested director elections.

• ISS considers the following factors, among others: • Long-term financial performance of the issuer relative to its industry peers

• Management’s track record

• Background to the proxy contest

• Nominee qualifications and any compensatory arrangements

• Strategic plan of dissident slate and quality of critique against management

• Likelihood that the proposed goals and objectives can be achieved (both sides)

• Stock ownership positions

FACTORS CONSIDERED IN PROXY CONTESTS FOR DIRECTOR ELECTIONS

24

Copyright ©2017 Sullivan & Cromwell LLP

Tactics Used by Activists

• Activists have utilized a variety of tactics to pursue different objectives.

• The most common activist campaign tactics are putting forth (or threatening to put forth) a slate of director nominees in a full scale proxy contest and initiating a publicity campaign.

• Publicity campaigns include public letters to the company disclosing certain demands or press releases expressing certain positions and desired objectives.

• Public disclosure has recently been less prevalent, perhaps as a result of increased company engagement with activists before campaigns become public.

• In 2013, publicity campaigns were used in 53% of activist campaigns. This figure fell to 37% in 2016.

• Other activism tactics include putting forth binding or precatory shareholder proposals, initiating lawsuits, calling a special meeting, or acting by written consent. In 2016, these tactics have appeared in fewer than 7% of announced campaigns.

25

Copyright ©2017 Sullivan & Cromwell LLP

Standard Activist “Playbook”

Activists often follow a standard playbook of escalation tactics; key objective is to create an impression of inevitability

• Activist engages in private dialogue with management/board

• Activist conducts background checks on directors and management

• Management/Board often receptive, seeking to preempt public agitation

• Discussions can avoid further agitation or lead to settlement; if unsuccessful, activist could escalate

• Nothing is gained by refusing to meet with activists

• Activist files a Schedule 13D disclosing its stake and an intention to pursue activism

• But activists are also successfully using smaller stakes (~1%) to press for change

• Activist initiates a high-profile public campaign designed to put pressure on Board

• Tactics employed vary: public statements, letters to management and shareholders, presentations (white papers), etc. — activists increasingly adept at using media

• Typically attracts like-minded investors/other activist funds — “wolf pack”

• Activist threatens a proxy fight — activists announced 73 contests in 2015, and 38 in 2016.

• Activist may ultimately engage in a proxy contest, seeking to elect minority slate of directors or force/encourage specific action (shareholder proposal)

• Large percentage of proxy fights results in activist winning one or more board seats (or achieving settlement)

• 138 publicly filed settlements between companies and activists in 2016

• 24% of proxy contests that went to a vote in 2016 resulted in at least 1 board seat

• If activist is well-funded, activist commences lawsuit (sometimes in conjunction with other tactics) to obtain information, reverse board decision, redeem poison pill, etc.

O V E R V I E W O F T A C T I C S SELECTED EXAMPLES

• With some notable exceptions (e.g., Icahn, Elliot, Pershing Square), an activist does not often make an offer for the entire company

• Hedge funds have made approximately 100 unsolicited bids since 2005

INCREASINGLY

HOSTILE

PRIVATE

DISCUSSIONS

MEDIA AND

PR CAMPAIGN

PROXY CONTEST

LAWSUIT

“HOSTILE OFFER”

26

Copyright ©2017 Sullivan & Cromwell LLP

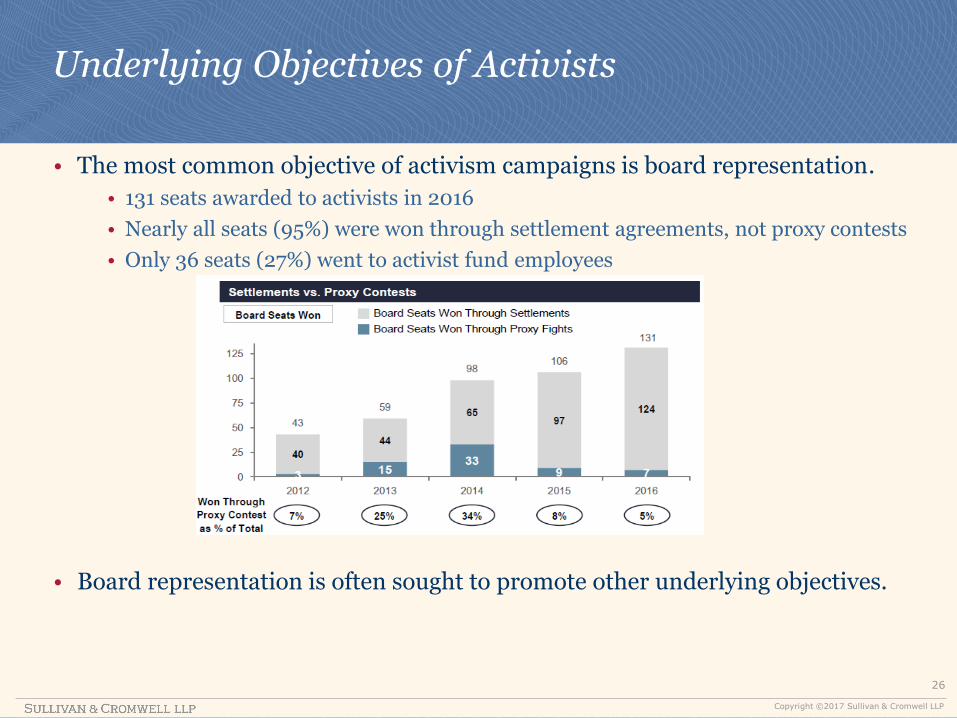

Underlying Objectives of Activists

• The most common objective of activism campaigns is board representation.

• 131 seats awarded to activists in 2016

• Nearly all seats (95%) were won through settlement agreements, not proxy contests

• Only 36 seats (27%) went to activist fund employees

• Board representation is often sought to promote other underlying objectives.

27

Copyright ©2017 Sullivan & Cromwell LLP

Underlying Objectives of Activists

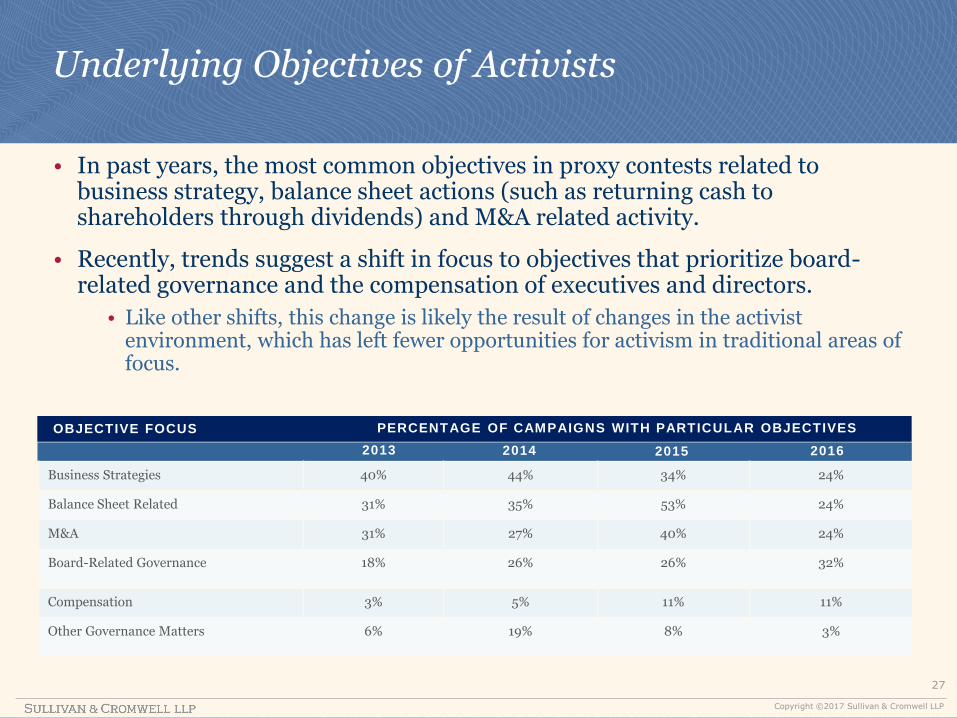

• In past years, the most common objectives in proxy contests related to business strategy, balance sheet actions (such as returning cash to shareholders through dividends) and M&A related activity.

• Recently, trends suggest a shift in focus to objectives that prioritize board-related governance and the compensation of executives and directors.

• Like other shifts, this change is likely the result of changes in the activist environment, which has left fewer opportunities for activism in traditional areas of focus.

OBJECTIVE FOCUS

2013

PERCENTAGE OF CAMPAIGNS WITH PARTICULAR OBJECTIVES

Business Strategies 40% 44% 34% 24%

Balance Sheet Related 31% 35% 53% 24%

M&A 31% 27% 40% 24%

Board-Related Governance 18% 26% 26% 32%

Compensation 3% 5% 11% 11%

Other Governance Matters 6% 19% 8% 3%

2014 2015 2016

28

Copyright ©2017 Sullivan & Cromwell LLP

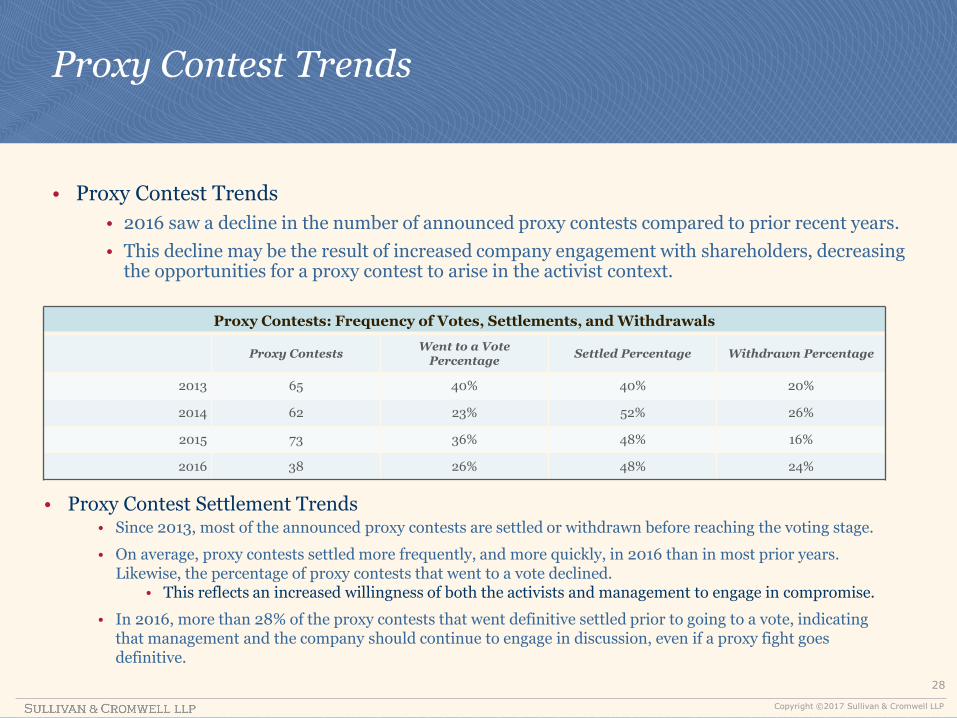

Proxy Contest Trends

• Proxy Contest Trends

• 2016 saw a decline in the number of announced proxy contests compared to prior recent years.

• This decline may be the result of increased company engagement with shareholders, decreasing the opportunities for a proxy contest to arise in the activist context.

• Proxy Contest Settlement Trends • Since 2013, most of the announced proxy contests are settled or withdrawn before reaching the voting stage.

• On average, proxy contests settled more frequently, and more quickly, in 2016 than in most prior years. Likewise, the percentage of proxy contests that went to a vote declined.

• This reflects an increased willingness of both the activists and management to engage in compromise.

• In 2016, more than 28% of the proxy contests that went definitive settled prior to going to a vote, indicating that management and the company should continue to engage in discussion, even if a proxy fight goes definitive.

Proxy Contests: Frequency of Votes, Settlements, and Withdrawals

Proxy Contests Went to a Vote

Percentage Settled Percentage Withdrawn Percentage

2013 65 40% 40% 20%

2014 62 23% 52% 26%

2015 73 36% 48% 16%

2016 38 26% 48% 24%

29

Copyright ©2017 Sullivan & Cromwell LLP

Short Slate v. Control Slate Proxy Contests

• Activists have aggressively sought control of the board in most proxy contests over recent years. Since 2013, short slate contests have made up approximately one-third of the proxy contests in each year.

• In short slate contests, activists usually seek between 30% and 50% of the board seats represented, which usually accounts for three or four nominees.

• Activists have been more successful in reaching pre-vote settlement agreements in the context of a control slate proxy contest.

• Since 2013, an average of 57% of control slate contests settled before the vote, compared to a significantly lower 30% for short slate contests.

• Management may be predisposed to settling in control slate contests, where costs are higher.

• Activists may be predisposed to settling, in order to avoid the higher costs for running a control slate campaign or the higher burden of persuasion to receive support.

• In both short slate and control slate contests, the activist usually wins at least one board seat. Activists have won control of the board in less than 15% of proxy contests since 2013.

30

Copyright ©2017 Sullivan & Cromwell LLP

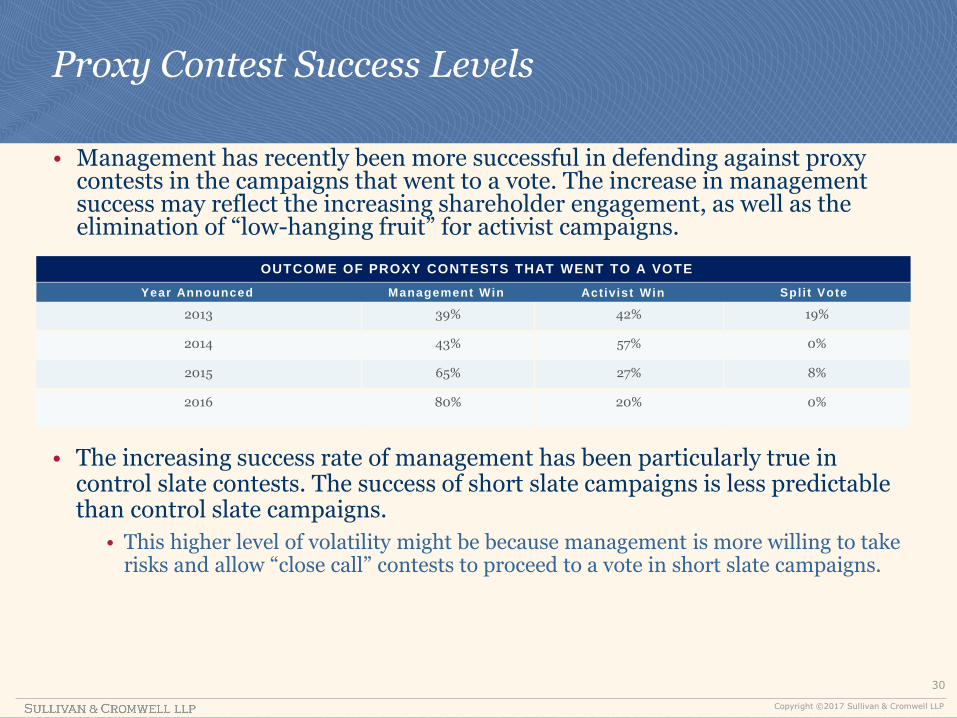

Proxy Contest Success Levels

• Management has recently been more successful in defending against proxy contests in the campaigns that went to a vote. The increase in management success may reflect the increasing shareholder engagement, as well as the elimination of “low-hanging fruit” for activist campaigns.

2013 39% 42% 19%

2014 43% 57% 0%

2015 65% 27% 8%

2016 80% 20% 0%

OUTCOME OF PROXY CONTESTS THAT WENT TO A VOTE

Management Win Activist Win Spl i t Vote

• The increasing success rate of management has been particularly true in control slate contests. The success of short slate campaigns is less predictable than control slate campaigns.

• This higher level of volatility might be because management is more willing to take risks and allow “close call” contests to proceed to a vote in short slate campaigns.

Year Announced

31

Copyright ©2017 Sullivan & Cromwell LLP

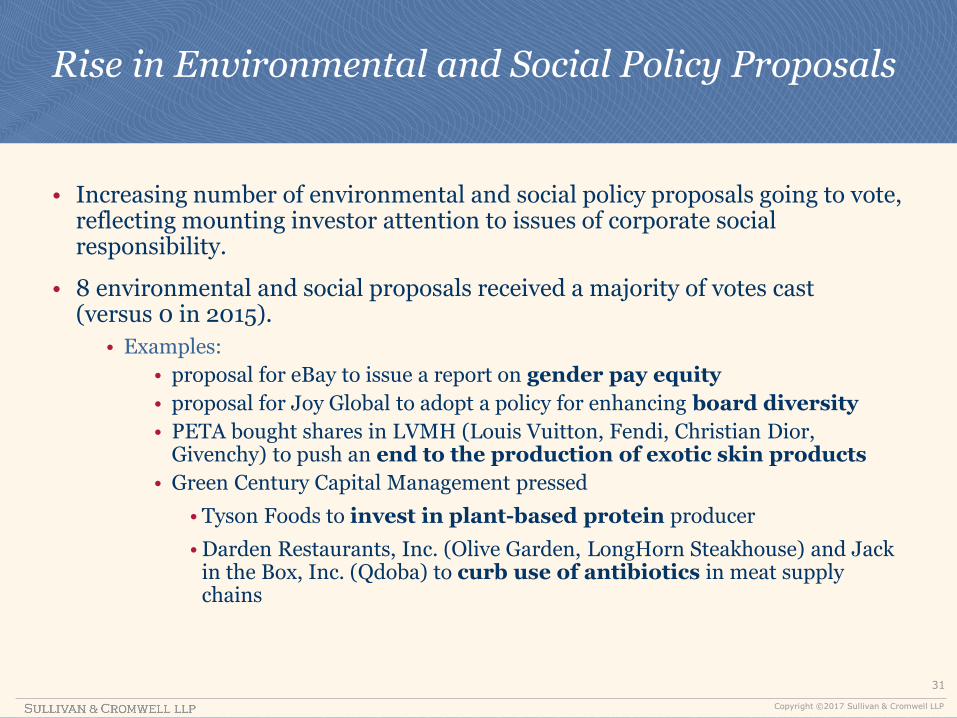

Rise in Environmental and Social Policy Proposals

• Increasing number of environmental and social policy proposals going to vote, reflecting mounting investor attention to issues of corporate social responsibility.

• 8 environmental and social proposals received a majority of votes cast (versus 0 in 2015).

• Examples:

• proposal for eBay to issue a report on gender pay equity

• proposal for Joy Global to adopt a policy for enhancing board diversity

• PETA bought shares in LVMH (Louis Vuitton, Fendi, Christian Dior, Givenchy) to push an end to the production of exotic skin products

• Green Century Capital Management pressed

• Tyson Foods to invest in plant-based protein producer

• Darden Restaurants, Inc. (Olive Garden, LongHorn Steakhouse) and Jack in the Box, Inc. (Qdoba) to curb use of antibiotics in meat supply chains

32

Copyright ©2017 Sullivan & Cromwell LLP

Proxy Contest Aftermath

• It’s quite common to observe significant events taking place at target companies after a proxy contest has concluded. Frequent changes include changes to senior management, merger or spin-off transactions, or the development of further proxy contests.

2013 23% 19% 31%

2014 44% 31% 0%

2015 11% 14% 11%

YEAR ANNOUNCED

CEO Change

OCCURRENCES IN YEAR FOLLOWING PROXY CONTEST

Merger or Spin-Off Further Proxy Contests

• The outcome of the proxy contest does not appear to have a significant effect on the frequency of the events above.

• In proxy contests where the management slate won, the percentages were very similar to those campaigns in which the activist won.

• Companies should be aware of the issues raised during the activist campaign and engage with shareholders accordingly. Management may wish to implement certain changes, even if management won the proxy contest.

• In light of these trends, issuers should consider certain actions or response steps, even in the aftermath of a proxy contest.

33

Copyright ©2017 Sullivan & Cromwell LLP

Settlement Agreements

• Activist campaign settlement agreements vary greatly based on the particular campaign. Certain settlement agreement provisions are nearly universal, while others appear less frequently.

• Nearly every settlement agreement contains one or more standstill provisions. While certain provisions are less frequent, the provisions below are the most common:

COMMON STANDSTILL PROVISIONS FREQUENCY (2015–2016)

Prohibition on public negative comments about the company 100%

Prohibition on the solicitation of proxies or consents 99%

Prohibition on forming a group or voting trust or entering into a voting agreement 97%

Prohibition on seeking or recommending the company engage in mergers or other unusual transactions

95%

Prohibition on seeking board membership or director removal 94%

Prohibition on the presentation of a shareholder proposal 90%

Prohibition on calling shareholder meetings 77%

Prohibition on acquiring more shares 72%

34

Copyright ©2017 Sullivan & Cromwell LLP

Proxy Access

SEC Issues Universal Ballot Proposal: The SEC proposed the mandatory use of universal proxy cards in all contested director elections at annual meetings of listed U.S. public companies.

• Current System: Competing cards sent by the issuer and the dissident shareholder, each with only their nominees

• Proposal: One proxy card that allows shareholders to vote by selecting any mix of directors from slates proposed both by the issuer and a dissident shareholder

• Concerns:

• Undesired Election Outcomes: Each shareholder could vote for a mix of directors that differs from that preferred by either the company or the dissident.

• Invalid Voting: There may be more invalid votes due to shareholders voting for more candidates than there are available seats. (But this isn’t a big concern.)

• Benefits for Activists: Would provide a less costly process to put forth nominees and making a vote for individual nominees more appealing to shareholders due to the flexibility in selecting the exact mix of directors a shareholder wants to elect.

• Could lead to more proxy contests and therefore higher costs and greater disruptions for reporting companies and their shareholders generally.

• May also encourage the use of dissident proxy cards in “vote no” campaigns and campaigns on proposals other than director elections.

• Comments on this proposal were due January 9, 2017. Given this timing, it is unlikely that the proposed rules, if adopted, will be effective for the 2017 proxy season.

35

Copyright ©2017 Sullivan & Cromwell LLP

Proxy Access

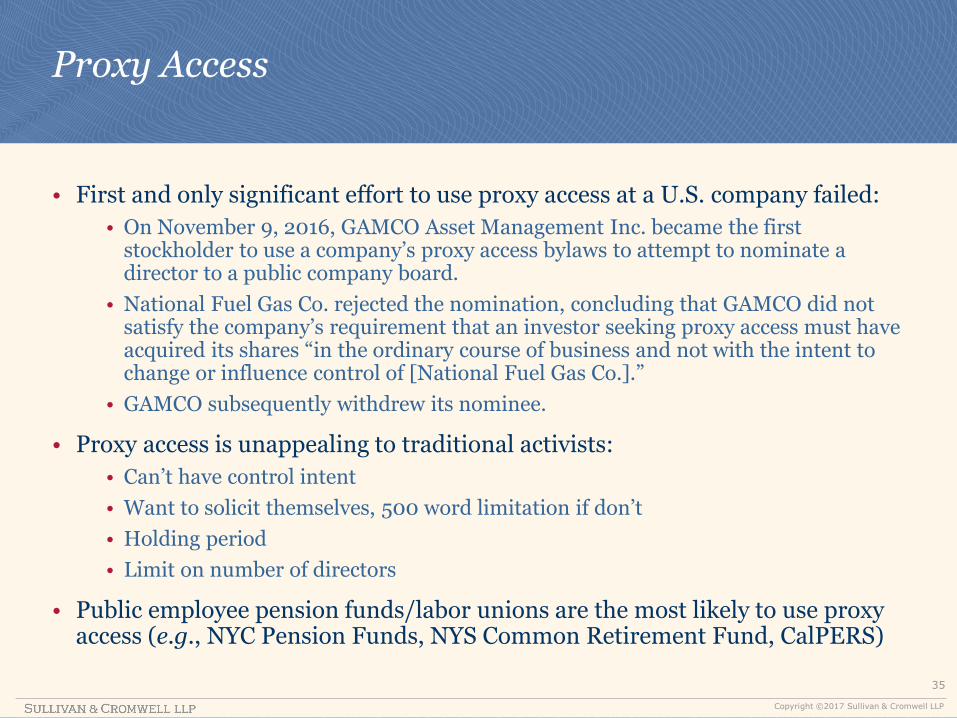

• First and only significant effort to use proxy access at a U.S. company failed:

• On November 9, 2016, GAMCO Asset Management Inc. became the first stockholder to use a company’s proxy access bylaws to attempt to nominate a director to a public company board.

• National Fuel Gas Co. rejected the nomination, concluding that GAMCO did not satisfy the company’s requirement that an investor seeking proxy access must have acquired its shares “in the ordinary course of business and not with the intent to change or influence control of [National Fuel Gas Co.].”

• GAMCO subsequently withdrew its nominee.

• Proxy access is unappealing to traditional activists:

• Can’t have control intent

• Want to solicit themselves, 500 word limitation if don’t

• Holding period

• Limit on number of directors

• Public employee pension funds/labor unions are the most likely to use proxy access (e.g., NYC Pension Funds, NYS Common Retirement Fund, CalPERS)

36

Copyright ©2017 Sullivan & Cromwell LLP

Potential Developments

• The Trump presidency may significantly impact the activism environment through new tax policies and appointments.

• Trump’s tax policies (potential tax holiday and rollback of regulatory environment) could significantly increase the amount of free cash available to U.S. companies, potentially resulting in increased criticism by activists over capital allocation strategies.

• Trump’s proposed policies include a tax holiday which would allow U.S. companies to repatriate offshore earnings at a 10% tax rate and the reduction of the statutory corporate tax rate from 35% to 15%.

• On December 21, 2016, Trump named Carl Icahn (major activist) as special adviser to the President on overhauling federal regulations.

• The new SEC Chairman may decide whether activists must disclose their stakes more quickly after acquiring them and whether those disclosures must include certain derivatives.

• The new SEC Chairman may decide whether to adopt the universal proxy card proposal and the SEC’s proposal to rewrite the rules for proxy fights, which might supplant proxy access entirely as a means for sophisticated investors like pension funds to secure board seats with limited expense and effort.

• Repeal of Dodd-Frank may reduce the current level of transparency which may reduce opportunities for activism.

Copyright ©2017 Sullivan & Cromwell LLP

37

Global Trends in Activism

38

Copyright ©2017 Sullivan & Cromwell LLP

Global Trends in Activism

• Increased activism in Europe, the Middle East and Africa (“EMEA”).

• Despite historical preference for privacy in European and Asian countries (investment communities are historically averse to public spats, shareholders don’t have stringent disclosure requirements for their plans and most activism has taken the form of behind-the-scenes negotiations)

• Brexit

• Increasing presence of foreign institutional investors in Germany and Italy

• But nearly 80% of public demands in Europe are by investors based in Europe

39

Copyright ©2017 Sullivan & Cromwell LLP

Global Trends in Activism Companies Subject to Activism by Country: 2015 v. 2016

40

Copyright ©2017 Sullivan & Cromwell LLP

Global Trends in Activism

Rising activism in other international markets, perhaps because global activist investors may be running out of targets in the U.S., incentivizing them to chase opportunities in new markets.

41

Copyright ©2017 Sullivan & Cromwell LLP

Global Trends in Activism

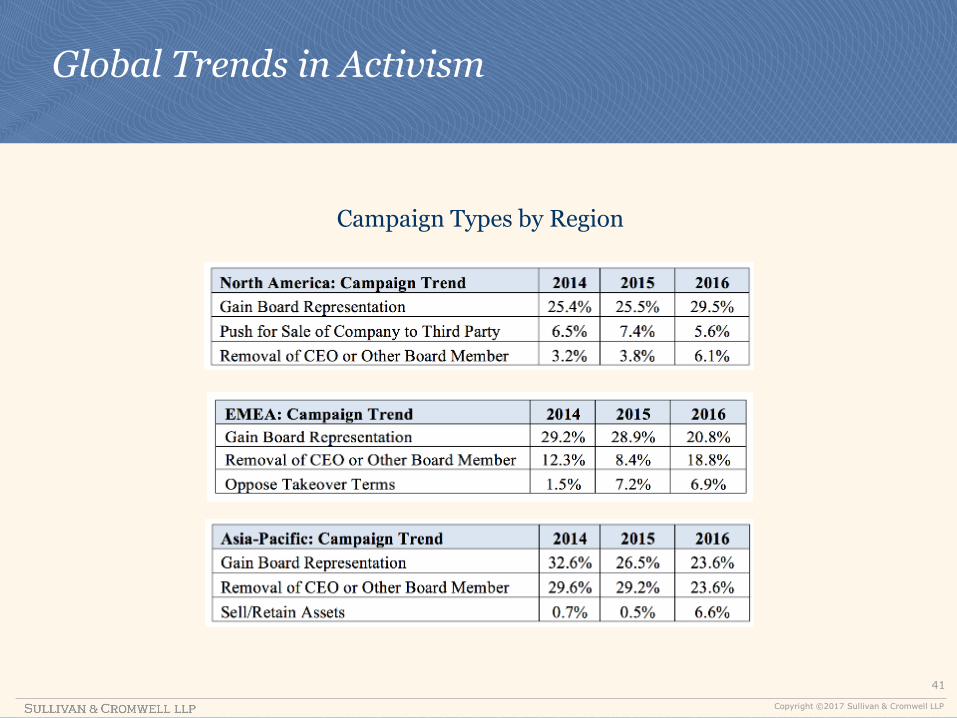

Campaign Types by Region

Copyright ©2017 Sullivan & Cromwell LLP

42