20142014 it recruitment and retention...

TRANSCRIPT

IT Recruitment and Retention Report

20142014

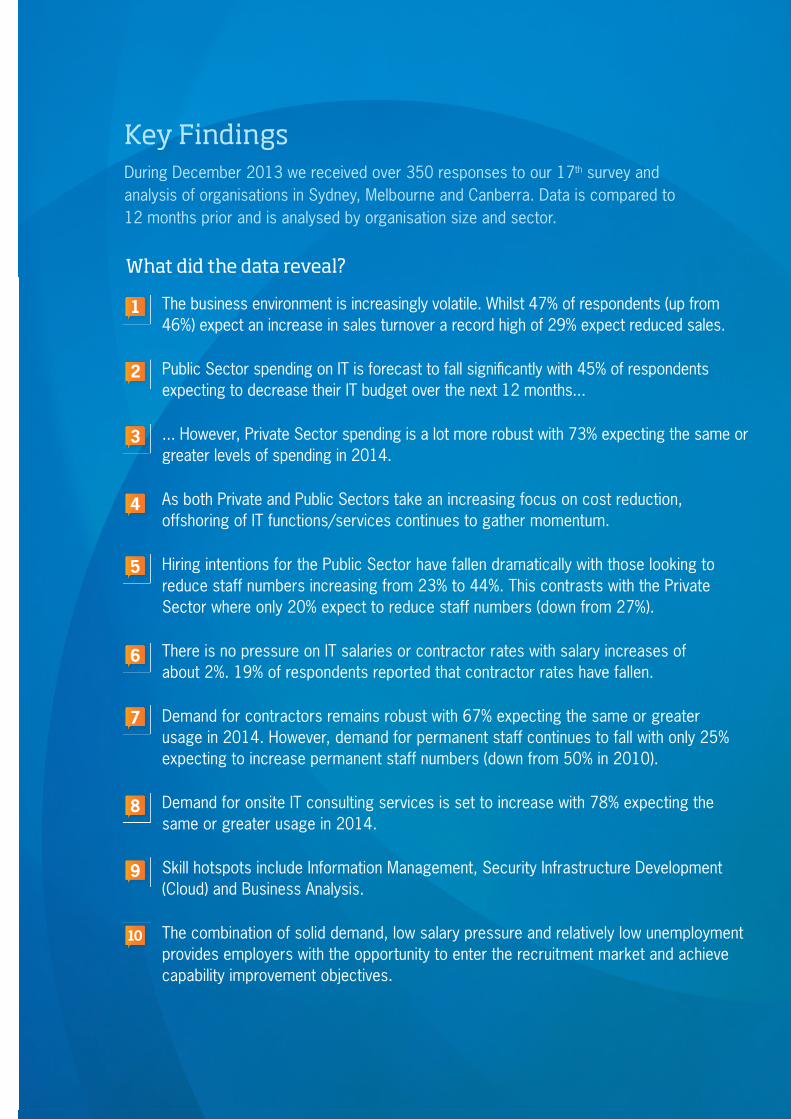

The business environment is increasingly volatile. Whilst 47% of respondents (up from 46%) expect an increase in sales turnover a record high of 29% expect reduced sales.

Public Sector spending on IT is forecast to fall signifi cantly with 45% of respondents expecting to decrease their IT budget over the next 12 months...

... However, Private Sector spending is a lot more robust with 73% expecting the same or greater levels of spending in 2014.

As both Private and Public Sectors take an increasing focus on cost reduction, offshoring of IT functions/services continues to gather momentum.

Hiring intentions for the Public Sector have fallen dramatically with those looking to reduce staff numbers increasing from 23% to 44%. This contrasts with the Private Sector where only 20% expect to reduce staff numbers (down from 27%).

There is no pressure on IT salaries or contractor rates with salary increases of about 2%. 19% of respondents reported that contractor rates have fallen.

Demand for contractors remains robust with 67% expecting the same or greater usage in 2014. However, demand for permanent staff continues to fall with only 25% expecting to increase permanent staff numbers (down from 50% in 2010).

Demand for onsite IT consulting services is set to increase with 78% expecting the same or greater usage in 2014.

Skill hotspots include Information Management, Security Infrastructure Development (Cloud) and Business Analysis.

The combination of solid demand, low salary pressure and relatively low unemployment provides employers with the opportunity to enter the recruitment market and achieve capability improvement objectives.

1

3

4

5

6

7

8

9

10

2

Key FindingsDuring December 2013 we received over 350 responses to our 17th survey and analysis of organisations in Sydney, Melbourne and Canberra. Data is compared to 12 months prior and is analysed by organisation size and sector.

What did the data reveal?

IT RECRUITMENT & RETENTION REPORT 2014

ContentsIntroduction ............................................................................................................................ 1

Business Environment: Budgets ......................................................................................... 2

Business Environment: Looking Abroad ........................................................................... 3

Staffi ng Levels: Hiring or Firing .......................................................................................... 4

Salaries: Show us the Money ............................................................................................... 7

Recruitment Strategies: Buy or Build ................................................................................. 9

Hot Spots: Who’s in Demand? ............................................................................................ 10

Staff Turnover: Revolving Doors ....................................................................................... 12

IT Health Check .................................................................................................................... 14

About you and your organisation ..................................................................................... 16

IT RECRUITMENT & RETENTION REPORT 2014 1

IntroductionFirstly, thank you to all our respondents who contributed to Clicks being voted Australia’s favourite medium IT Recruiter for 2013.

The SEEK Annual Recruitment Awards (SARAs) are the most prestigious award for the Australian recruitment industry. SARAs are voted for by both employers and job seekers and represent an unbiased recognition of exemplary and consistent service.

We are excited to share the benefi ts of our win with you and will work hard to maximise the opportunities it affords to bring you better outcomes.

In this year’s report we see an upswing in hiring intentions by the private sector and signifi cant demand for onsite IT consultants. There is also a continuing 3-year trend of workforces comprising an increasingly higher proportion of contingent workers.

The Beddison Group has responded to this demand by launching INDEX Consultants, a highly scalable solution with a quality bench of experienced, accredited consultants with specialist business and technology skills.

Finally, thank you to the many respondents who took time out to contribute information to Clicks’ 2014 IT Recruitment and Retention Report. It is your input that improves our business and makes our partnerships stronger and more effective. We are very grateful and look forward to our continued shared success in 2014.

Best wishes,

Ben WoodManaging Director

Level 35, 360 Collins Street, Melbourne VIC 300003 9963 4884 | [email protected]

Australia’s favourite medium IT recruiter ...As voted by job seekers, contractors and employers

IT RECRUITMENT & RETENTION REPORT 20142

Business Environment: Budgets

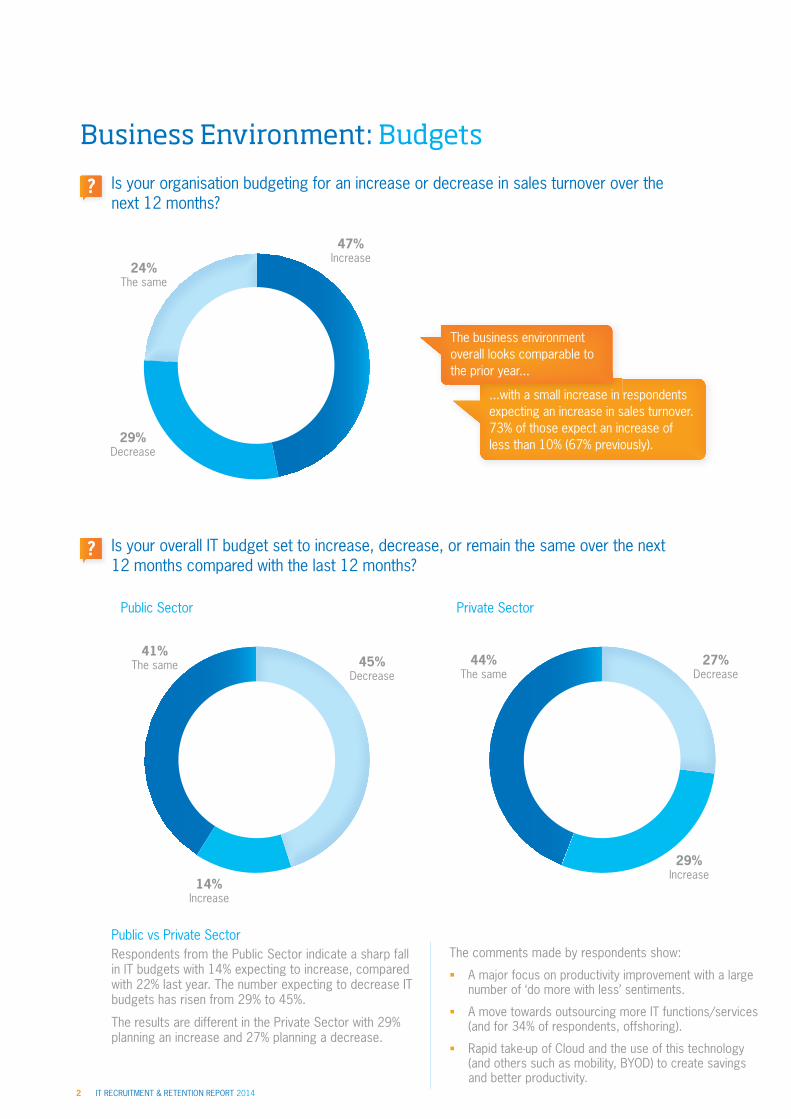

Is your organisation budgeting for an increase or decrease in sales turnover over the next 12 months?

Is your overall IT budget set to increase, decrease, or remain the same over the next 12 months compared with the last 12 months?

...with a small increase in respondents expecting an increase in sales turnover. 73% of those expect an increase of less than 10% (67% previously).29%

Decrease

47% Increase

24% The same

?

?

Public vs Private SectorRespondents from the Public Sector indicate a sharp fall in IT budgets with 14% expecting to increase, compared with 22% last year. The number expecting to decrease IT budgets has risen from 29% to 45%.

The results are different in the Private Sector with 29% planning an increase and 27% planning a decrease.

The comments made by respondents show:

A major focus on productivity improvement with a large number of ‘do more with less’ sentiments.

A move towards outsourcing more IT functions/services (and for 34% of respondents, offshoring).

Rapid take-up of Cloud and the use of this technology (and others such as mobility, BYOD) to create savings and better productivity.

The business environment overall looks comparable to the prior year...

Private Sector

27% Decrease

29% Increase

44% The same

Public Sector

45% Decrease

14% Increase

41% The same

IT RECRUITMENT & RETENTION REPORT 2014 3

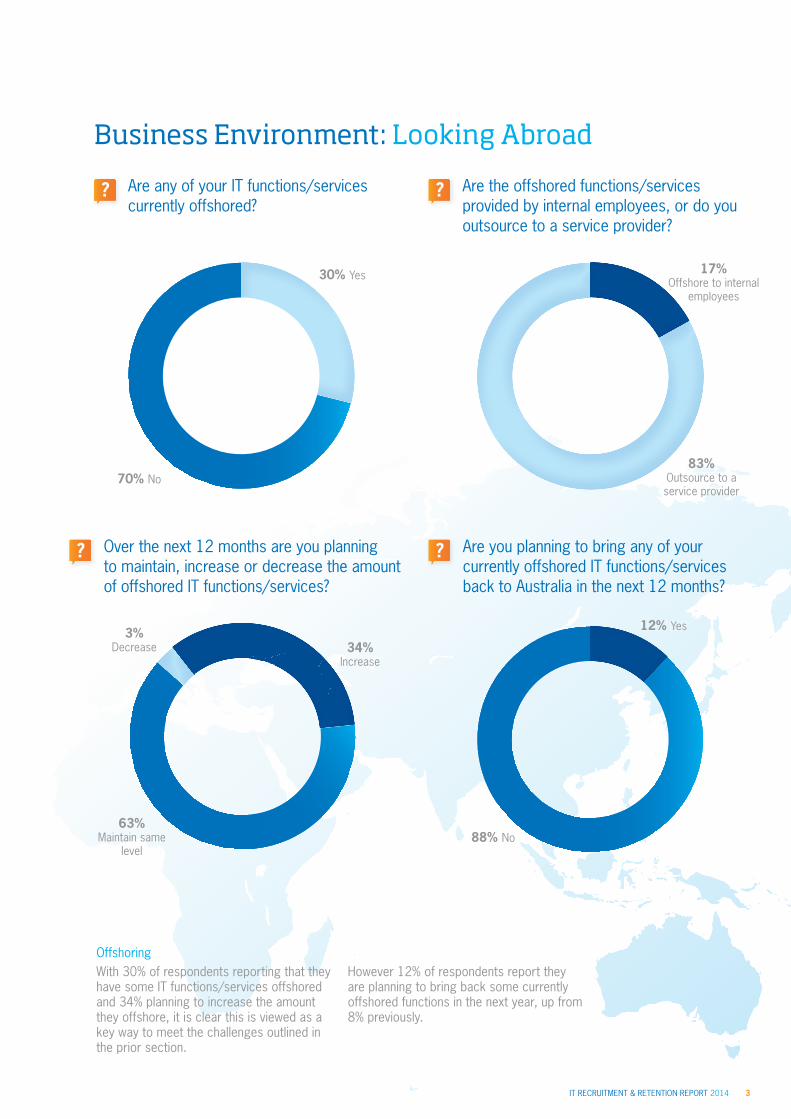

Are any of your IT functions/services currently offshored?

Are you planning to bring any of your currently offshored IT functions/services back to Australia in the next 12 months?

70% No

88% No

30% Yes

12% Yes

?

?

Business Environment: Looking Abroad

Over the next 12 months are you planning to maintain, increase or decrease the amount of offshored IT functions/services?

?

34% Increase

63% Maintain same

level

3% Decrease

OffshoringWith 30% of respondents reporting that they have some IT functions/services offshored and 34% planning to increase the amount they offshore, it is clear this is viewed as a key way to meet the challenges outlined in the prior section.

However 12% of respondents report they are planning to bring back some currently offshored functions in the next year, up from 8% previously.

Are the offshored functions/services provided by internal employees, or do you outsource to a service provider?

?

17% Offshore to internal

employees

83% Outsource to a service provider

IT RECRUITMENT & RETENTION REPORT 20144

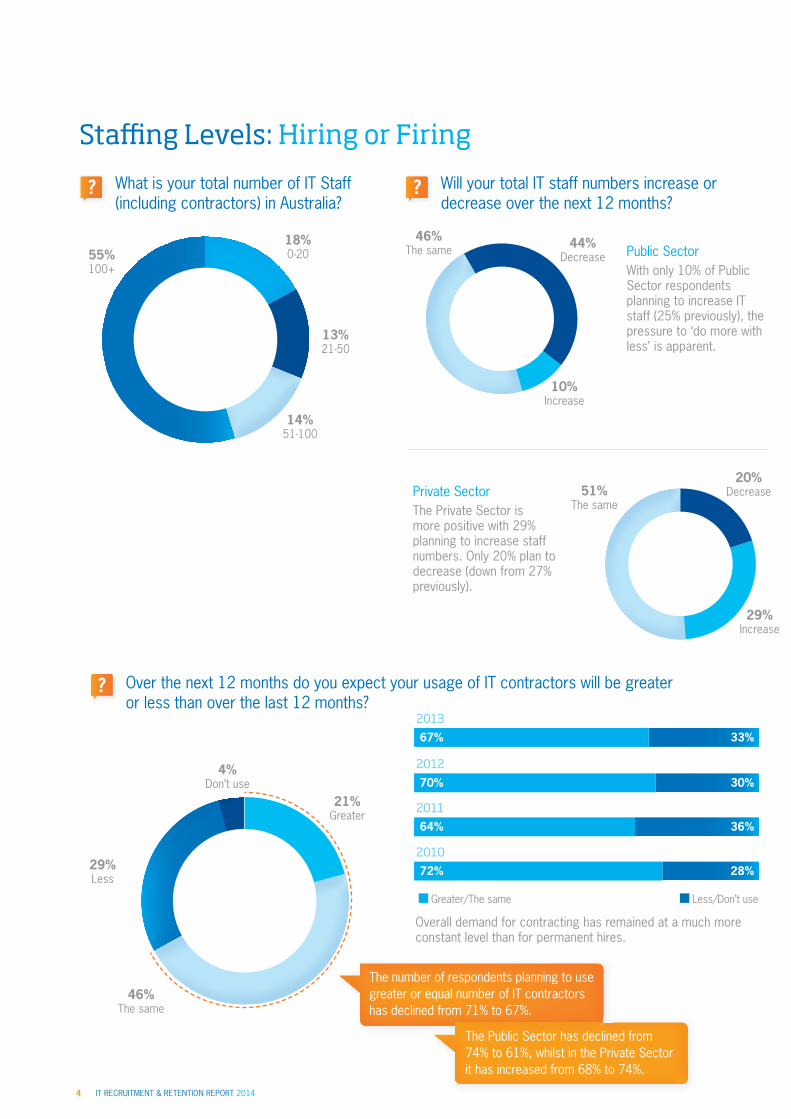

What is your total number of IT Staff (including contractors) in Australia?

Will your total IT staff numbers increase or decrease over the next 12 months?

? ?

Staffi ng Levels: Hiring or Firing

55% 100+

14% 51-100

13% 21-50

18% 0-20

Over the next 12 months do you expect your usage of IT contractors will be greater or less than over the last 12 months?

?

Overall demand for contracting has remained at a much more constant level than for permanent hires.

Private Sector The Private Sector is more positive with 29% planning to increase staff numbers. Only 20% plan to decrease (down from 27% previously).

20% Decrease

29% Increase

51% The same

Public Sector With only 10% of Public Sector respondents planning to increase IT staff (25% previously), the pressure to ‘do more with less’ is apparent.

44% Decrease

10% Increase

46% The same

67%

70%

64%

72%

2013

2012

2011

2010

36%

30%

33%

28%

Greater/The same Less/Don’t use

4% Don’t use

21% Greater

29% Less

46% The same

The Public Sector has declined from 74% to 61%, whilst in the Private Sector it has increased from 68% to 74%.

The number of respondents planning to use greater or equal number of IT contractors has declined from 71% to 67%.

IT RECRUITMENT & RETENTION REPORT 2014 5

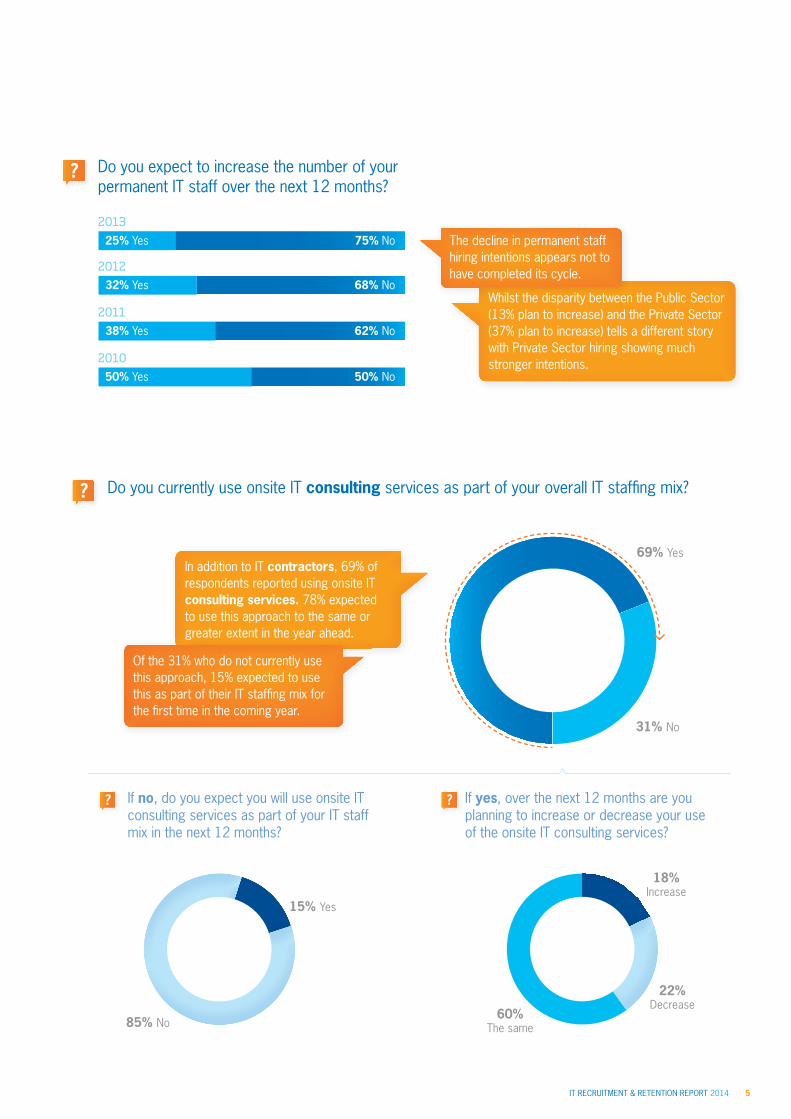

Do you expect to increase the number of your permanent IT staff over the next 12 months?

?

25% Yes 75% No

68% No

62% No

50% No

32% Yes

38% Yes

50% Yes

2013

2012

2011

2010

Whilst the disparity between the Public Sector (13% plan to increase) and the Private Sector (37% plan to increase) tells a different story with Private Sector hiring showing much stronger intentions.

The decline in permanent staff hiring intentions appears not to have completed its cycle.

15% Yes

85% No

Do you currently use onsite IT consulting services as part of your overall IT staffi ng mix? ?

69% Yes

31% No

If no, do you expect you will use onsite IT consulting services as part of your IT staff mix in the next 12 months?

? ? If yes, over the next 12 months are you planning to increase or decrease your use of the onsite IT consulting services?

22% Decrease

18% Increase

60% The same

Of the 31% who do not currently use this approach, 15% expected to use this as part of their IT staffi ng mix for the fi rst time in the coming year.

In addition to IT contractors, 69% of respondents reported using onsite IT consulting services. 78% expected to use this approach to the same or greater extent in the year ahead.

INDEX ConsultantsSpeed. Agility. Transparency. Value.

The Beddison Group recently launched INDEX Consultants, established to help our clients engage experienced ICT consultants qualified to undertake and deliver ICT projects on a consulting basis.

Our services include:

IT Strategy

Program and Project Management

Technical and Business Analysis

Business Transformation

Delivery Capability Uplift

Change Management

Process Optimisation

Application Development

Testing

The INDEX model removes costly overheads often associated with traditional consultancy services and allows the client and INDEX to agree project phases, timelines and service levels to create clear accountability, at 30%+ cost saving compared to traditional consulting services.

To discuss further please call Ben Wood on 03 9963 4884.

INDEX CONSULTANTS

index com au1300 4 INDEX

IT RECRUITMENT & RETENTION REPORT 2014 7

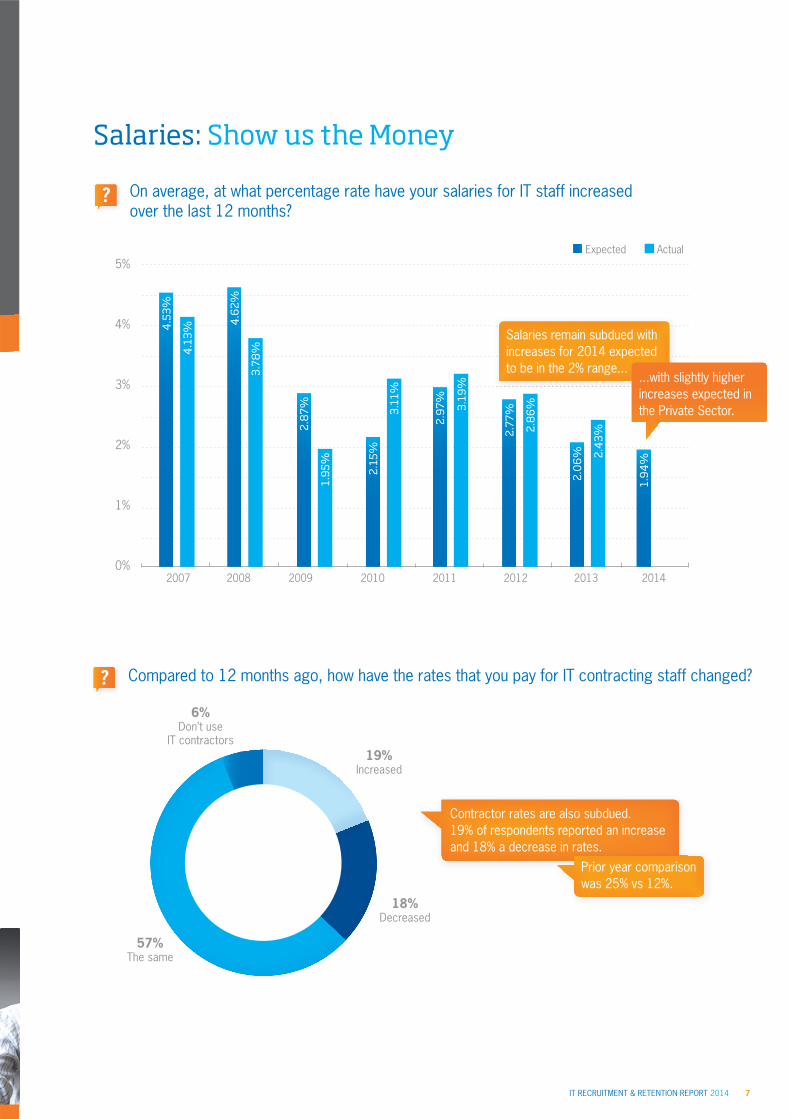

Salaries: Show us the Money

On average, at what percentage rate have your salaries for IT staff increased over the last 12 months?

?

2007 2008 20112009 20122010 2013 2014

5%

4%

3%

2%

1%

0%

Salaries remain subdued with increases for 2014 expected to be in the 2% range...

...with slightly higher increases expected in the Private Sector.

1.9

4%2.

43%

2.0

6%

2.8

6%

4.6

2%

3.78

%

2.8

7%

1.9

5% 2.15

%

3.11

%

2.9

7% 3.19

%

2.77

%

4.1

3%

4.5

3%

Expected Actual

Compared to 12 months ago, how have the rates that you pay for IT contracting staff changed? ?

19% Increased

18% Decreased

57% The same

6% Don’t use

IT contractors

Prior year comparison was 25% vs 12%.

Contractor rates are also subdued. 19% of respondents reported an increase and 18% a decrease in rates.

IT RECRUITMENT & RETENTION REPORT 20148

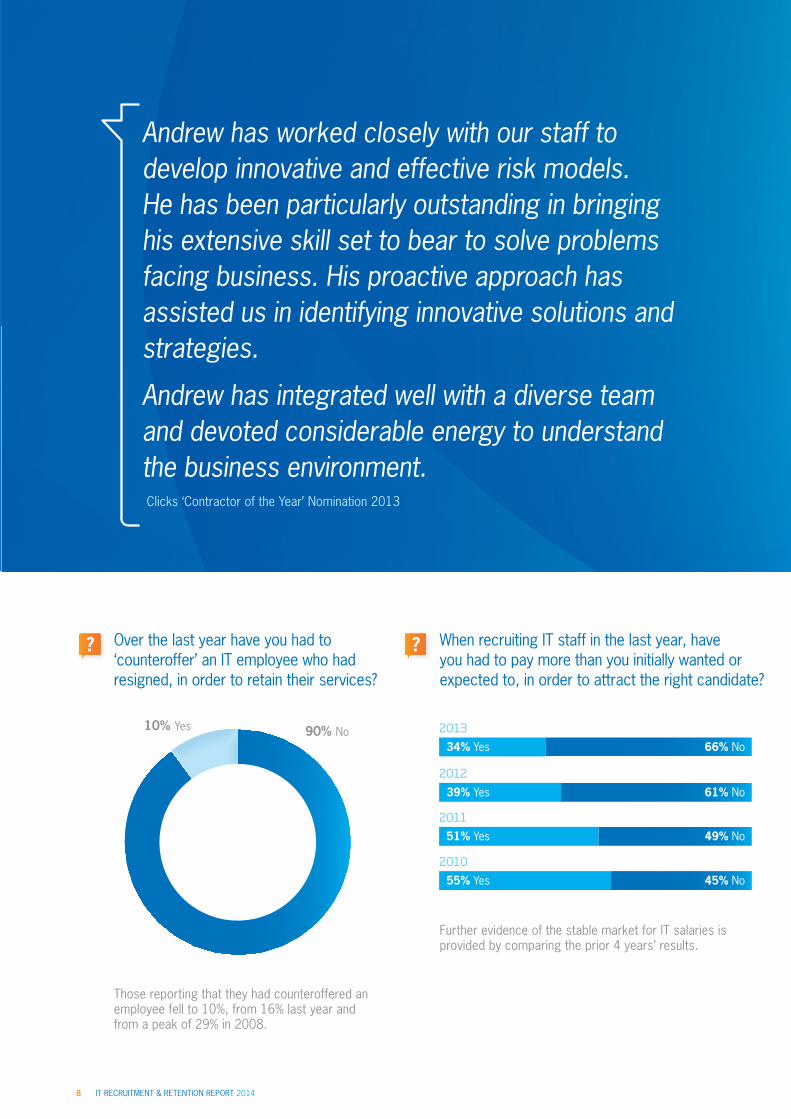

Over the last year have you had to ‘counteroffer’ an IT employee who had resigned, in order to retain their services?

When recruiting IT staff in the last year, have you had to pay more than you initially wanted or expected to, in order to attract the right candidate?

? ?

34% Yes

39% Yes

51% Yes

55% Yes

2013

2012

2011

2010

49% No

61% No

66% No

45% No

10% Yes 90% No

Those reporting that they had counteroffered an employee fell to 10%, from 16% last year and from a peak of 29% in 2008.

Further evidence of the stable market for IT salaries is provided by comparing the prior 4 years’ results.

Andrew has worked closely with our staff to develop innovative and effective risk models. He has been particularly outstanding in bringing his extensive skill set to bear to solve problems facing business. His proactive approach has assisted us in identifying innovative solutions and strategies.

Andrew has integrated well with a diverse team and devoted considerable energy to understand the business environment.Clicks ‘Contractor of the Year’ Nomination 2013

IT RECRUITMENT & RETENTION REPORT 2014 9

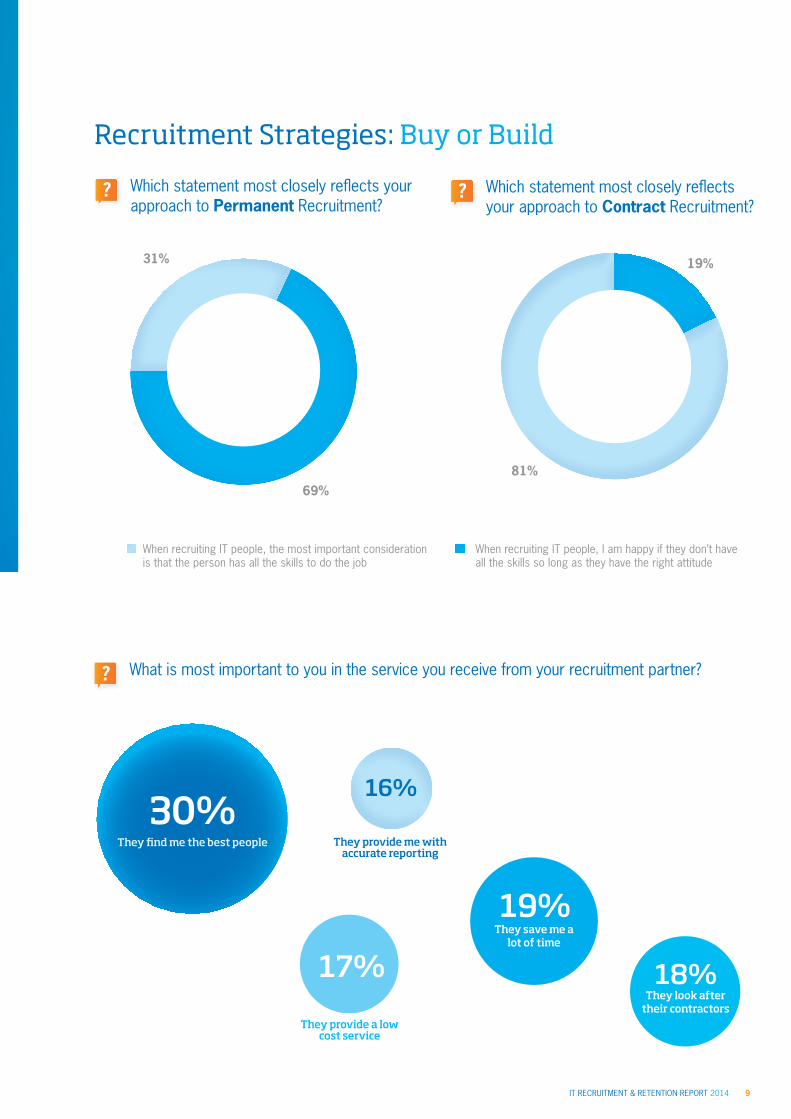

Which statement most closely refl ects your approach to Permanent Recruitment?

Which statement most closely refl ects your approach to Contract Recruitment?

? ?

Recruitment Strategies: Buy or Build

69%

31% 19%

81%

When recruiting IT people, the most important consideration is that the person has all the skills to do the job

When recruiting IT people, I am happy if they don’t have all the skills so long as they have the right attitude

What is most important to you in the service you receive from your recruitment partner??

30%16%

They fi nd me the best people

19%They save me a

lot of time

18%They look after

their contractors

They provide me with accurate reporting

17%

They provide a low cost service

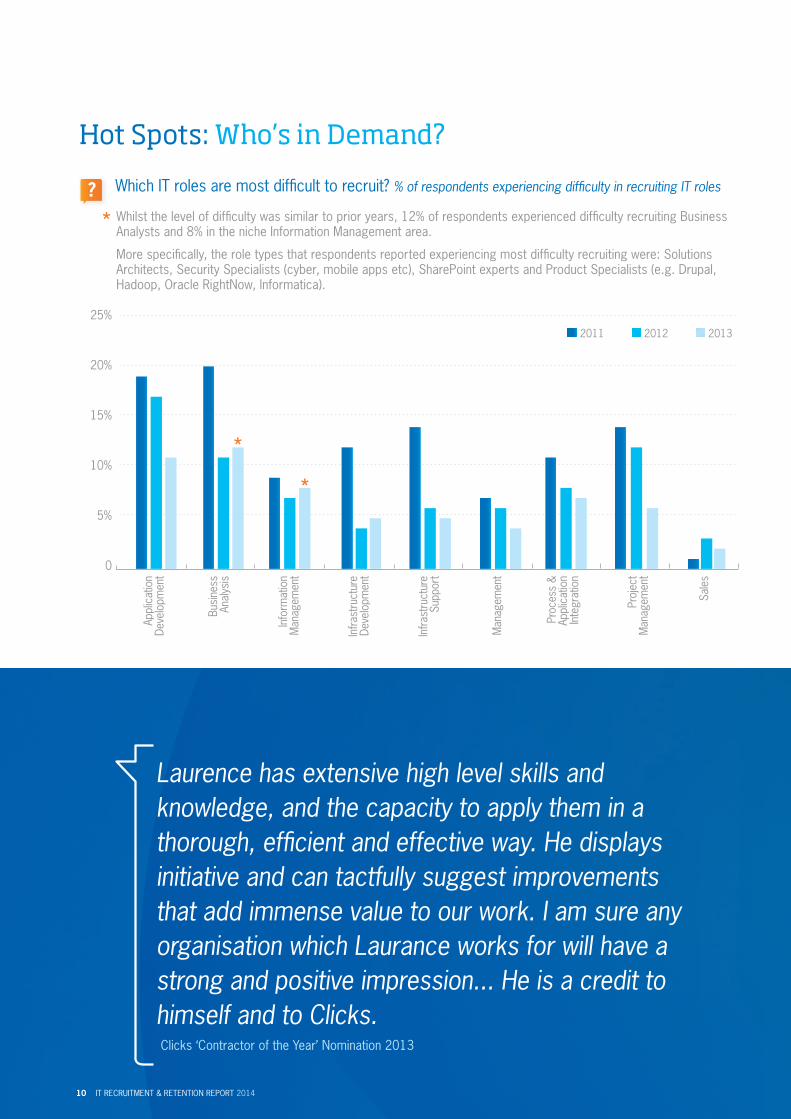

Which IT roles are most diffi cult to recruit? % of respondents experiencing diffi culty in recruiting IT roles?

Hot Spots: Who’s in Demand?

2011 2012 2013

Whilst the level of diffi culty was similar to prior years, 12% of respondents experienced diffi culty recruiting Business Analysts and 8% in the niche Information Management area.

More specifi cally, the role types that respondents reported experiencing most diffi culty recruiting were: Solutions Architects, Security Specialists (cyber, mobile apps etc), SharePoint experts and Product Specialists (e.g. Drupal, Hadoop, Oracle RightNow, Informatica).

25%

20%

15%

10%

5%

0

Appl

icat

ion

Deve

lopm

ent

Busi

ness

An

alys

is

Info

rmat

ion

Man

agem

ent

Infra

stru

ctur

e De

velo

pmen

t

Infra

stru

ctur

e Su

ppor

t

Sale

s

Proc

ess

& Ap

plic

atio

n In

tegr

atio

n

Man

agem

ent

Proj

ect

Man

agem

ent

Laurence has extensive high level skills and knowledge, and the capacity to apply them in a thorough, effi cient and effective way. He displays initiative and can tactfully suggest improvements that add immense value to our work. I am sure any organisation which Laurance works for will have a strong and positive impression... He is a credit to himself and to Clicks.Clicks ‘Contractor of the Year’ Nomination 2013

*

*

*

IT RECRUITMENT & RETENTION REPORT 201410

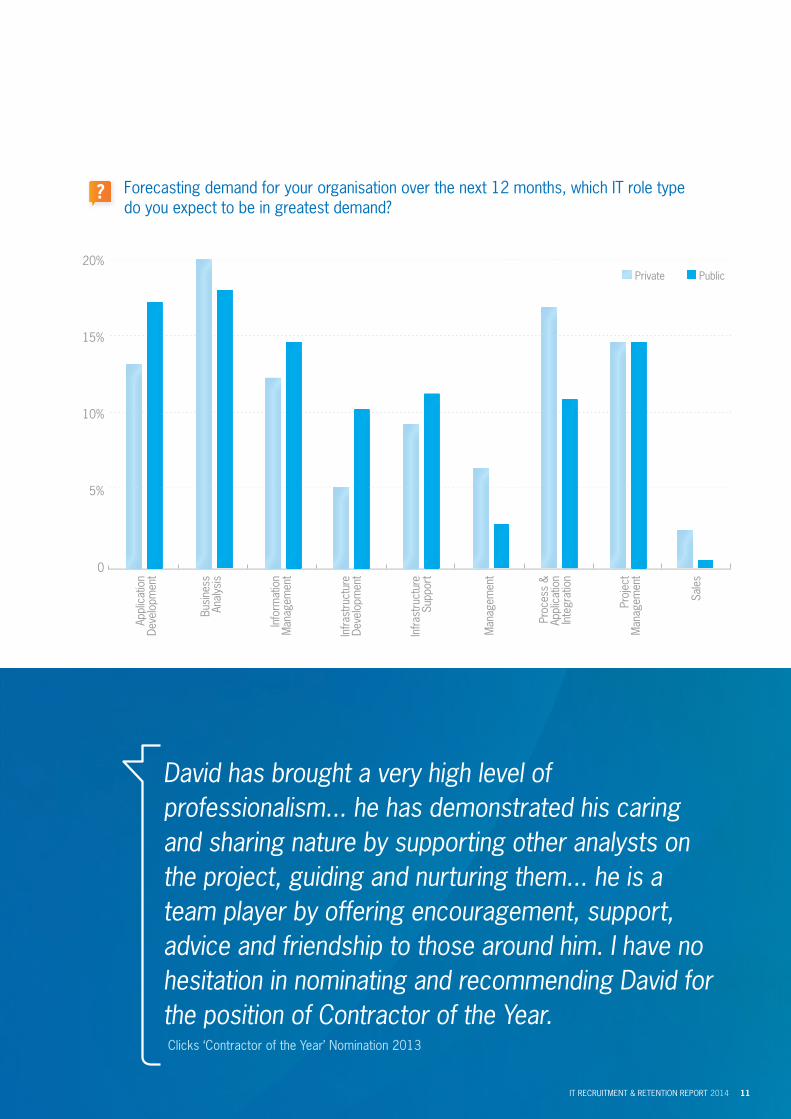

Forecasting demand for your organisation over the next 12 months, which IT role type do you expect to be in greatest demand?

?

Private Public

Appl

icat

ion

Deve

lopm

ent

Busi

ness

An

alys

is

Info

rmat

ion

Man

agem

ent

Infra

stru

ctur

e De

velo

pmen

t

Infra

stru

ctur

e Su

ppor

t

Sale

s

Proc

ess

& Ap

plic

atio

n In

tegr

atio

n

20%

15%

10%

5%

0

Man

agem

ent

Proj

ect

Man

agem

ent

David has brought a very high level of professionalism... he has demonstrated his caring and sharing nature by supporting other analysts on the project, guiding and nurturing them... he is a team player by offering encouragement, support, advice and friendship to those around him. I have no hesitation in nominating and recommending David for the position of Contractor of the Year.Clicks ‘Contractor of the Year’ Nomination 2013

IT RECRUITMENT & RETENTION REPORT 2014 11

IT RECRUITMENT & RETENTION REPORT 201412

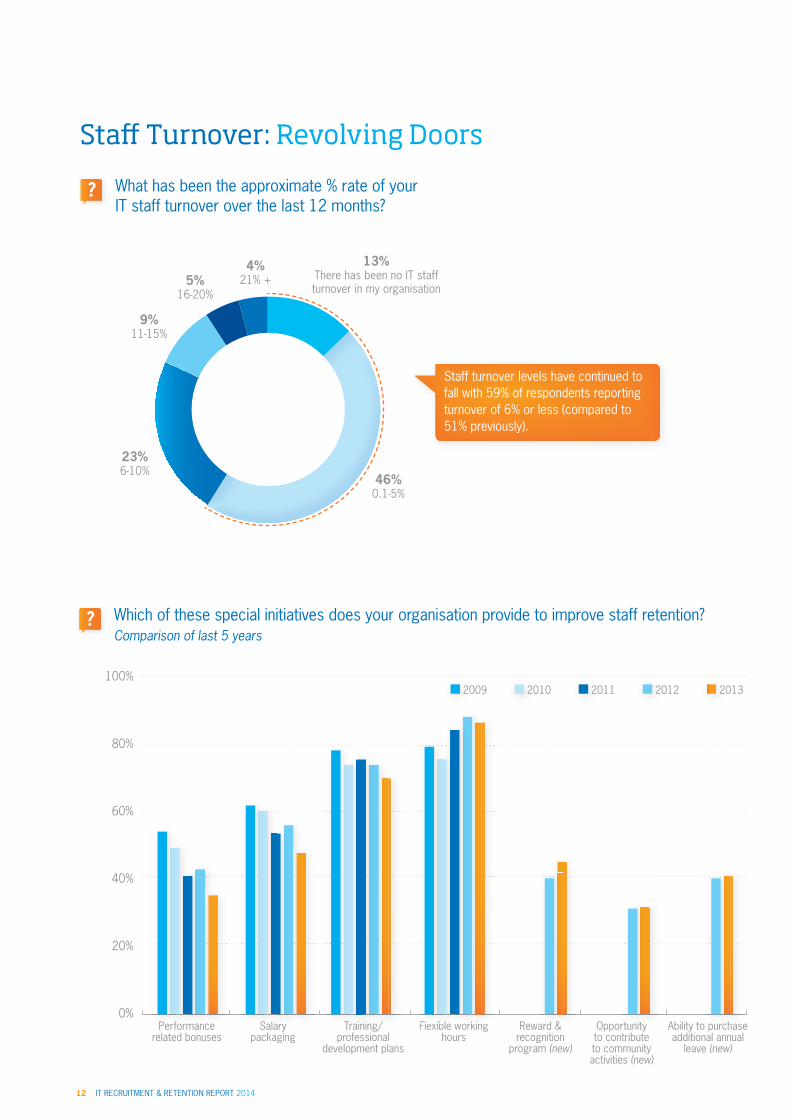

Which of these special initiatives does your organisation provide to improve staff retention?Comparison of last 5 years

?

Performance related bonuses

Salary packaging

Training/professional

development plans

Reward & recognition

program (new)

Flexible working hours

Opportunity to contribute to community activities (new)

Ability to purchase additional annual

leave (new)

100%

80%

60%

40%

20%

0%nncence ry g/ ng nit& rchasegg/ rkinkin t itd & hmanman a rainingi g wororerformorm Salaala i xible wle wPerf S TrT Fle ib

2009 2010 2011 2012 2013

What has been the approximate % rate of your IT staff turnover over the last 12 months?

?

Staff Turnover: Revolving Doors

13% There has been no IT staff turnover in my organisation

46% 0.1-5%

23% 6-10%

9% 11-15%

5% 16-20%

4% 21% +

Staff turnover levels have continued to fall with 59% of respondents reporting turnover of 6% or less (compared to 51% previously).

IT RECRUITMENT & RETENTION REPORT 2014 13

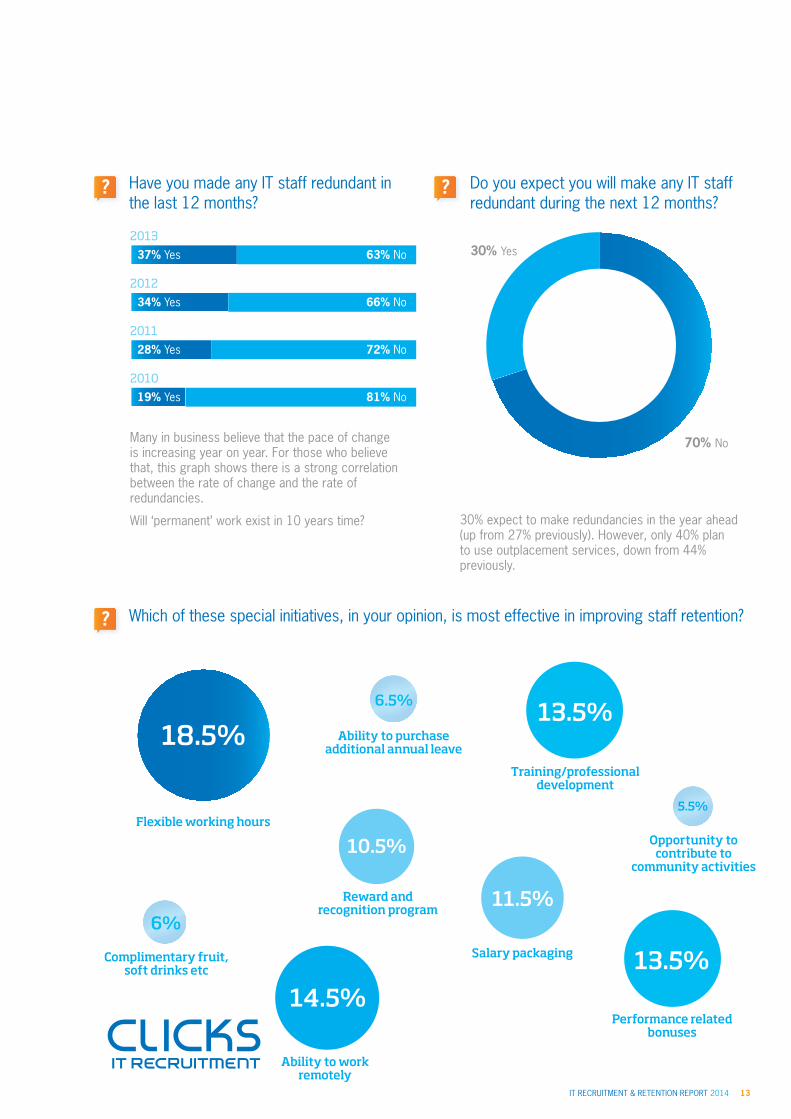

Do you expect you will make any IT staff redundant during the next 12 months?

?

70% No

30% Yes

Have you made any IT staff redundant in the last 12 months?

?

37% Yes

34% Yes

28% Yes

19% Yes

2013

2012

2011

2010

63% No

66% No

72% No

81% No

Many in business believe that the pace of change is increasing year on year. For those who believe that, this graph shows there is a strong correlation between the rate of change and the rate of redundancies.

Will ‘permanent’ work exist in 10 years time? 30% expect to make redundancies in the year ahead (up from 27% previously). However, only 40% plan to use outplacement services, down from 44% previously.

Which of these special initiatives, in your opinion, is most effective in improving staff retention??

18.5%

Flexible working hours

14.5%

Ability to work remotely

13.5%

Training/professional development

13.5%

Performance related bonuses

11.5%

Salary packaging

10.5%

Reward and recognition program

6.5%

Ability to purchase additional annual leave

6%

Complimentary fruit, soft drinks etc

5.5%

Opportunity to contribute to

community activities

IT RECRUITMENT & RETENTION REPORT 201414

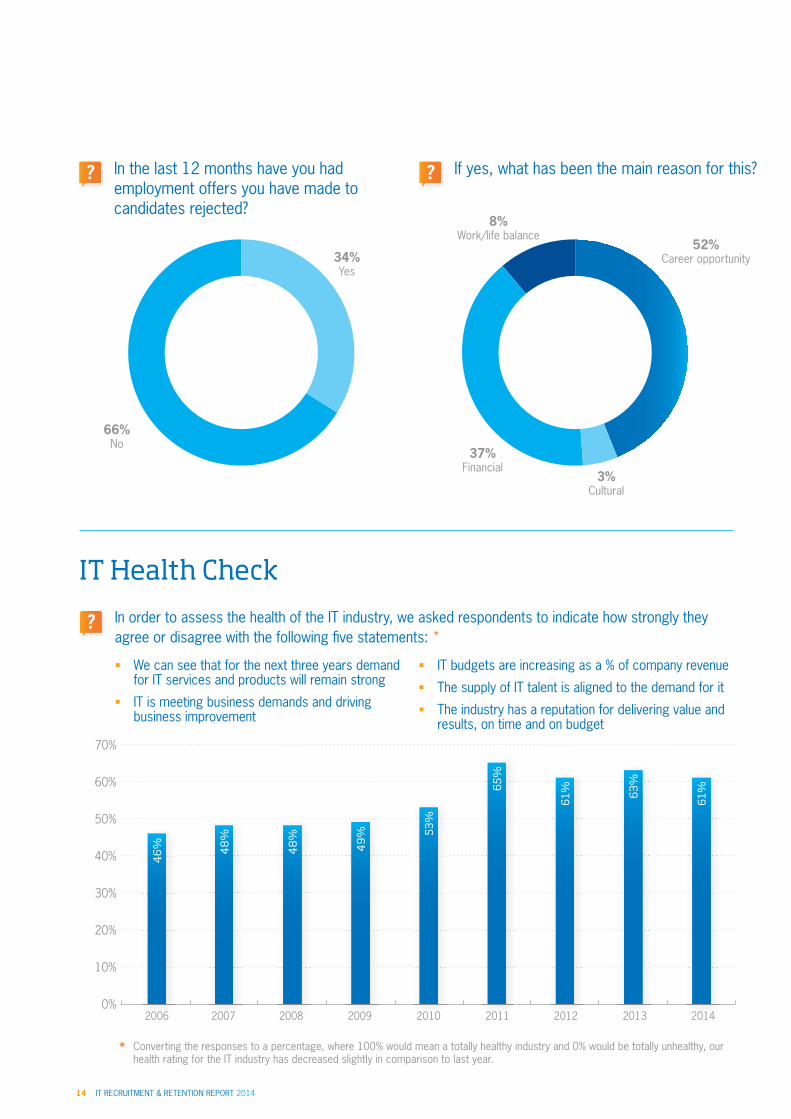

In the last 12 months have you had employment offers you have made to candidates rejected?

?

34% Yes

66% No

If yes, what has been the main reason for this? ?

52% Career opportunity

8% Work/life balance

37% Financial

3% Cultural

?

IT Health Check

In order to assess the health of the IT industry, we asked respondents to indicate how strongly they agree or disagree with the following fi ve statements: *

2006 2007 2008 20112009 20122010 2013 2014

70%

60%

50%

40%

30%

20%

10%

0%2006 2007 2008 2009 2010 2011 2012 2013 2014

We can see that for the next three years demand for IT services and products will remain strong

IT is meeting business demands and driving business improvement

IT budgets are increasing as a % of company revenue

The supply of IT talent is aligned to the demand for it

The industry has a reputation for delivering value and results, on time and on budget

Converting the responses to a percentage, where 100% would mean a totally healthy industry and 0% would be totally unhealthy, our health rating for the IT industry has decreased slightly in comparison to last year.*

46

% 48

%

48

%

49

% 53%

65%

61% 6

3%

61%

IT RECRUITMENT & RETENTION REPORT 2014 15

?

Australia’s favourite medium IT recruiter ...As voted by job seekers, contractors and employers

IT RECRUITMENT & RETENTION REPORT 201416

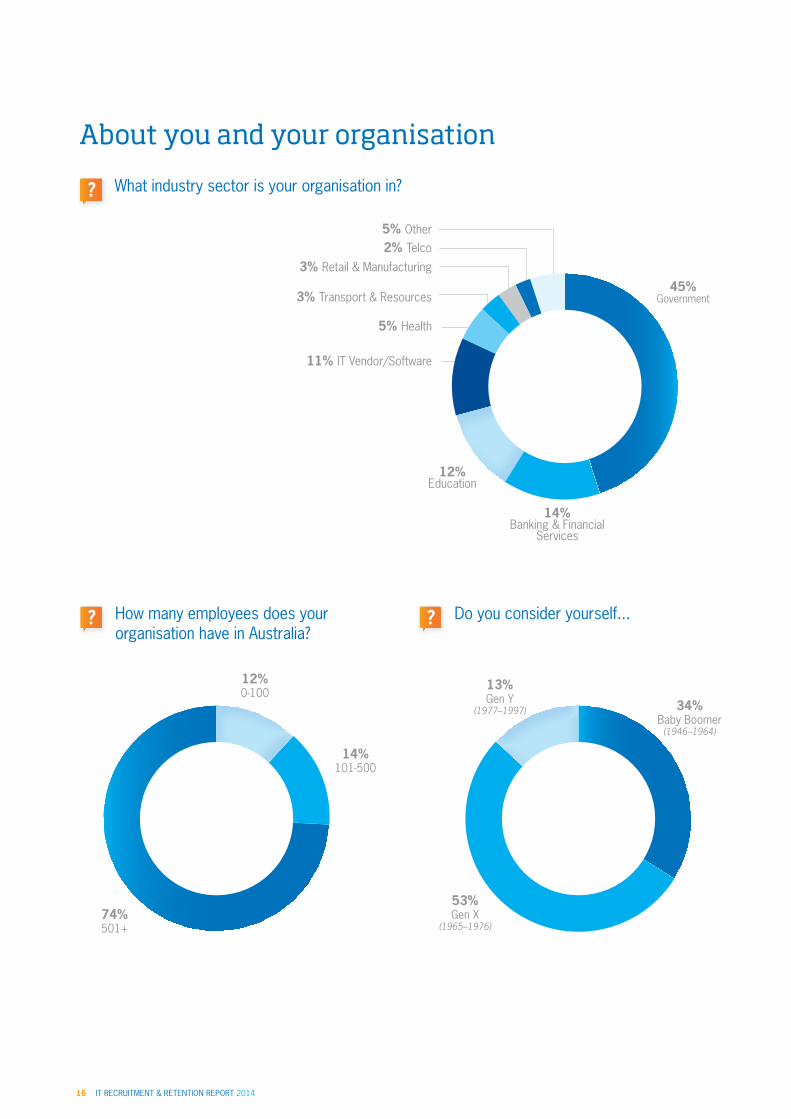

12% Education

11% IT Vendor/Software

What industry sector is your organisation in? ?

About you and your organisation

How many employees does your organisation have in Australia?

Do you consider yourself...? ?

???

12% 0-100

14% 101-500

13% Gen Y

(1977–1997) 34% Baby Boomer

(1946–1964)

53% Gen X

(1965–1976)74% 501+

2% Telco5% Other

3% Retail & Manufacturing

3% Transport & Resources

5% Health

14% Banking & Financial

Services

45% Government

RECRUITMENT & RETENTION REPORT 2014 17

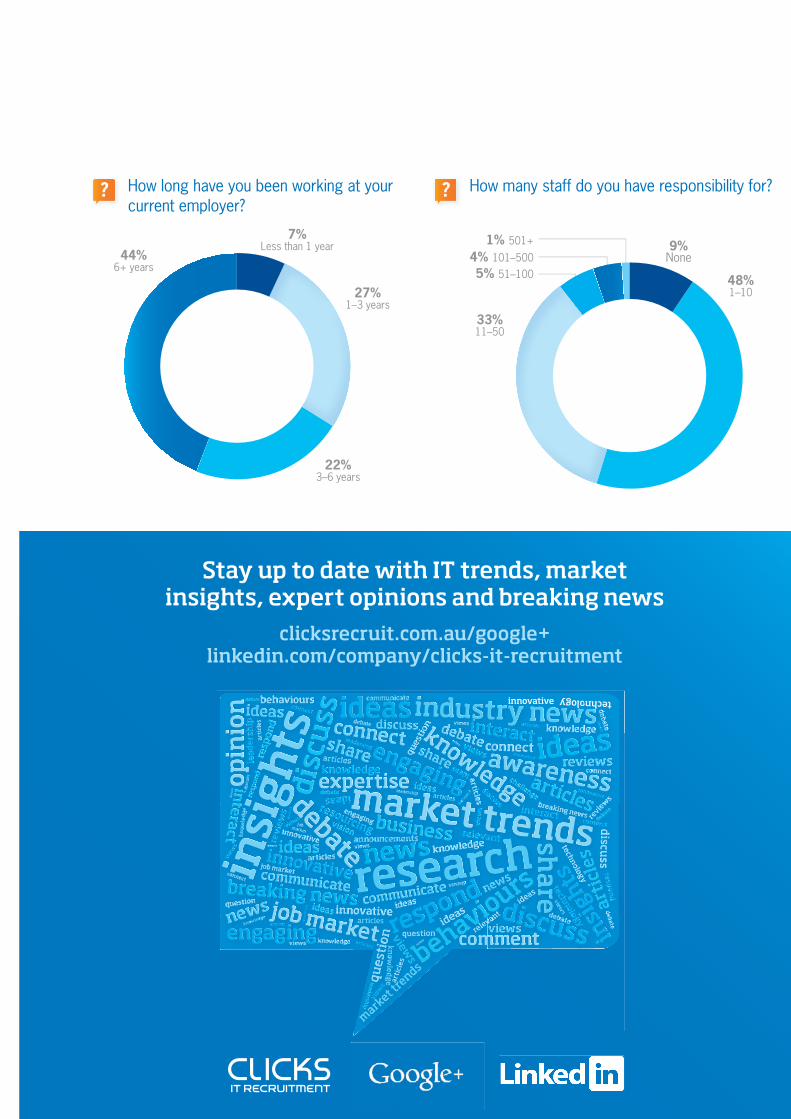

5% 51–1004% 101–500

1% 501+ 9% None

48% 1–10

33% 11–50

7% Less than 1 year

27% 1–3 years

22% 3–6 years

44% 6+ years

How long have you been working at your current employer?

How many staff do you have responsibility for? ? ?

clicksrecruit.com.au/google+ linkedin.com/company/clicks-it-recruitment

Stay up to date with IT trends, market insights, expert opinions and breaking news

Did you fi nd this report useful?

The quality of information we provide improves with every hiring manager who provides their data.

If you hire contract or permanent IT staff, your contribution is very important to us and all readers of this report.

If you’re new to Clicks please contact Sam Micich, Operations Manager, on 03 9963 4802 or [email protected] to ensure you receive your invitation to contribute to our next survey.

We look forward to sharing our mid-year update with you in July.

Clicks’ Services

Permanent Recruitment

Our team has an average of 8 years’ IT recruitment experience. For employers this means a deep understanding of your requirements and an established network of high calibre talent. For job seekers, our market knowledge, relationships and support will open the right doors for you.

Contract Recruitment

Clicks places an IT professional into a new job every hour of every day. We have over 20 years’ experience in the IT contracting market, and over 80 Preferred Supplier Agreements with some of Australia’s most respected employers. Whether you’re looking for work or looking for staff, we’re here to help you.

Contingent Workforce Engagement

Our systems guarantee that our contractors receive accurate pays on time every time. Clicks utilises robust and scaleable systems for online timesheeting, payroll management and reporting/analytics services. 95% of our contractors give us the highest ‘trust’ rating possible for our payroll management capability. We can also seamlessly interface with your systems to ensure hassle free data delivery and reporting.

Managed Services

Clicks’ Professional Services offering involves a single point of contact for all queries, resulting in increased speed and accuracy of response. You will also enjoy visible and consistent reporting, enhanced performance monitoring capabilities, and consolidation to a single invoice for both consulting and on hire labour, resulting in signifi cant cost saving in accounts payable, banking, and other fi nancial and administrative transactions.

Salary Surveys

Clicks produces regular salary reports for specifi c skill sets, sectors, and regions within Australia. Our salary data is based on actual rates/salaries being paid by employers, so is of the highest integrity. Clicks’ salary data assists employers in attracting the best talent via their knowledge of current market rates, and assists job seekers in achieving true market value for their skill set.

Master Vendor

For clients with larger-scale recruitment requirements, Clicks has a proven Master Vendor model that offers a single point of release for all roles, and the management of all downstream suppliers. Clicks is also responsible for managing compliance, job allocation, performance management, payroll, quality, and customer satisfaction.

Candidate Capability Testing and Benchmarking

Clicks has partnered with leading assessment organisations to improve the quality of information you use to make hiring decisions, establish clear capability benchmarks for your team, reduce time spent interviewing inappropriate candidates, and improve the quality of candidates you hire.

Market Reports

For over 10 years Clicks has been conducting critical research into the key issues affecting the recruitment and retention of IT professionals. Each year we survey over 500 leading Australian employers about market conditions, business confi dence, hiring intentions, emerging technologies and more, and produce a range of easy-to-read reports for employers.

MELBOURNE

Level 35, 360 Collins Street, Melbourne VIC 3000

+61 3 9963 4888 | [email protected]

SYDNEY

Level 14, 55 Clarence Street, Sydney NSW 2000

+61 2 9200 4444 | [email protected]

CANBERRA

Level 1, 15 London Circuit, Canberra ACT 2601

+61 2 6202 7700 | [email protected]

1300 CLICKS | clicksrecruit.com.au

rne VIC 3000

uit.com.au

y NSW 2000

ruit.com.au

a ACT 2601

uit.com.au