2014 afr workshop presentation final.ppt - home - the texas a&m university system · ·...

TRANSCRIPT

FY 2014A l Fi i l R ti Annual Financial Reporting

Workshop

August 5-6, 2014

Agenda - Tuesday, August 5th

Time Topic Presenter

8:30 Introduction/Accounting Update Teresa Bass3 / g p

10:30 Reporting Update and Deadlines Tracy Crowley

12:00 Lunch Break

1:15 APS011 Benefits Proportional Teresa Bass

3:00 Net Position Categories Tracy Crowley

3:30 NACUBO Function Reporting Teresa Bass3 3 p g

4:00 OMB Uniform Guidance Update

Cl i C5:00 Closing Comments

Agenda - Wednesday, August 6th

Time Topic Presenter

8:30 Introduction/Previous Day Questions Teresa Bass

8:45 FAMIS Year-End Processing Melissa Ray

AFR M d l B i T C l10:30 AFR Module Basics Tracy Crowley

11:15 Cash Flow Statement Workpaper Teresa Bass

Noon Adjourn/Closing Comments

Introduction/Introduction/Accounting Updateg p

Teresa Bass, CPAComptroller Comptroller

Texas A&M System Office

Introduction

Accounting Team Re-organized in FY 2014 Tracy Crowley Senior Manager of Financial Reporting Tracy Crowley, Senior Manager of Financial Reporting -

Investment Reporting & AFR Wanda Roof-Senior Financial Analyst-Investment

Reporting & AFR Monica Poehl, Senior Manager of Accounting-System Office

Operations, Sources/Uses Reporting, Indirect Cost & AFRp , / p g, Rekha Joshi, Senior Accountant-Construction Accounting &

IntraSystem ActivityT i S jk l I t di t A t t I t t & Tori Smejkal, Intermediate Accountant- Investments & Operations

Open Position-Senior Financial Analyst-Construction Accounting & Assisting Facilities team

2013 Consolidated AFR

Consolidated AFR Consolidation Process went well Comptroller’s Office did have some changes/adjustments

Unrealized Gain/Loss on Investments Moved to Investment Income and ties to Cash Flow Statement NonCash Section

USAS Certification Form Note 22-Donor Restricted Endowments Note 24-Disaggregation of Accounts Receivable

Member Desk Reviews Member Desk Reviews Overall very good 79% Blue Ribbons

USAS Certification Form

After submitting the USAS certification forms, members k d h h kb i were asked to correct the checkboxes on question 1

The USAS box should not be checked since Benefits Paid on Behalf are on the GR recon and not in USAS on Behalf are on the GR recon and not in USAS (Corrected form shown below)

Questions about Note 22

Note 22 - Donor Restricted Endowmentsd h l i Required to report the “cumulative net appreciation on

investments of donor-restricted endowments available for authorization for expenditure”

Hi i ll h d h A i i R hi h Historically, we have reported the Appreciation Reserve, which is the accumulated realized gains/losses

State Comptroller disagreed, and we changed this year’s Note 22 to reflect the unrealized fair value for True Endowments22 to reflect the unrealized fair value for True Endowments

Expendable vs. NonExpendable Net Position Nonexpendable classification is only appropriate when the net

position is required to be retained in perpetuity (for example position is required to be retained in perpetuity (for example, endowment corpus)

Comptroller’s Office has stated the unrealized belongs in expendablep

Questions about Note 24

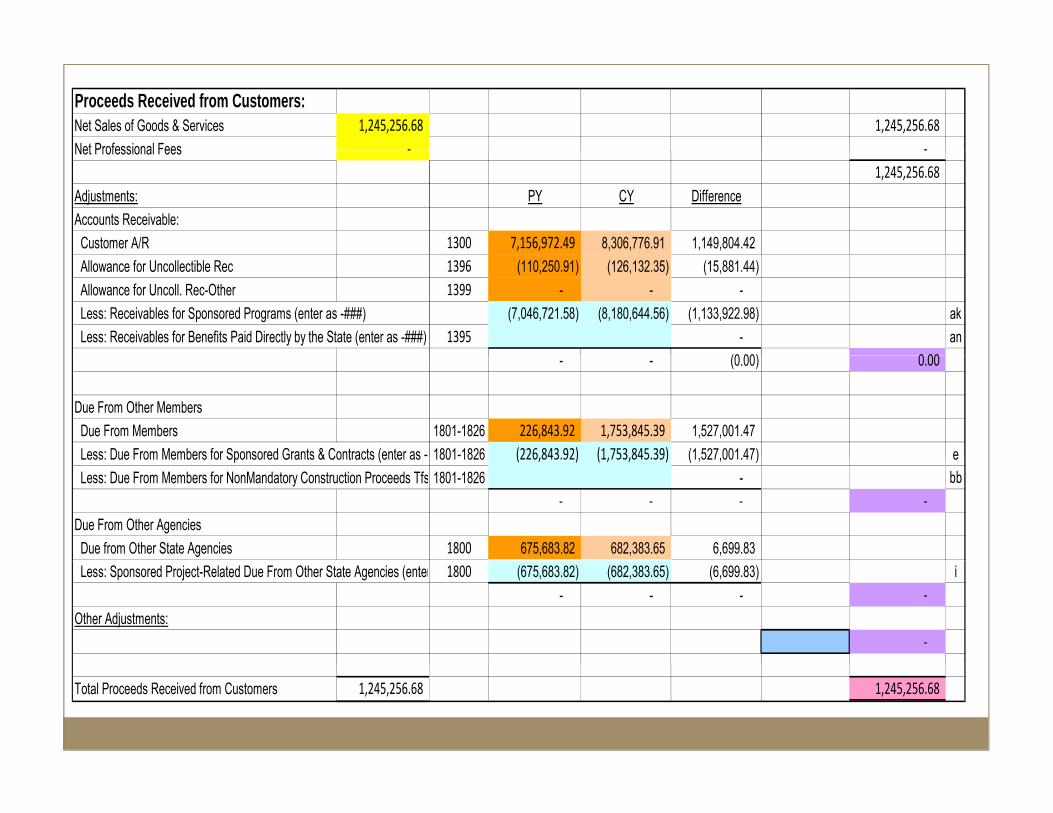

Note 24 - Disaggregation of Receivables System-wide, the total Other Receivables was less than 5%

of the total current receivables. Since the total exceeded $10M, we were asked to provide details.$ , p

Other Receivables AmountGrants and Contracts Receivable 2,546,671.08

State Receivables 4,752,466.40

Departmental Receivables 1,231,310.75

Deferred Compensation Plans 506,199.88p 99

Other 2,761,116.46

Allowance for Doubtful Accounts (193,243.43)

Total Other Receivables 11 604 530 14Total Other Receivables 11,604,530.14

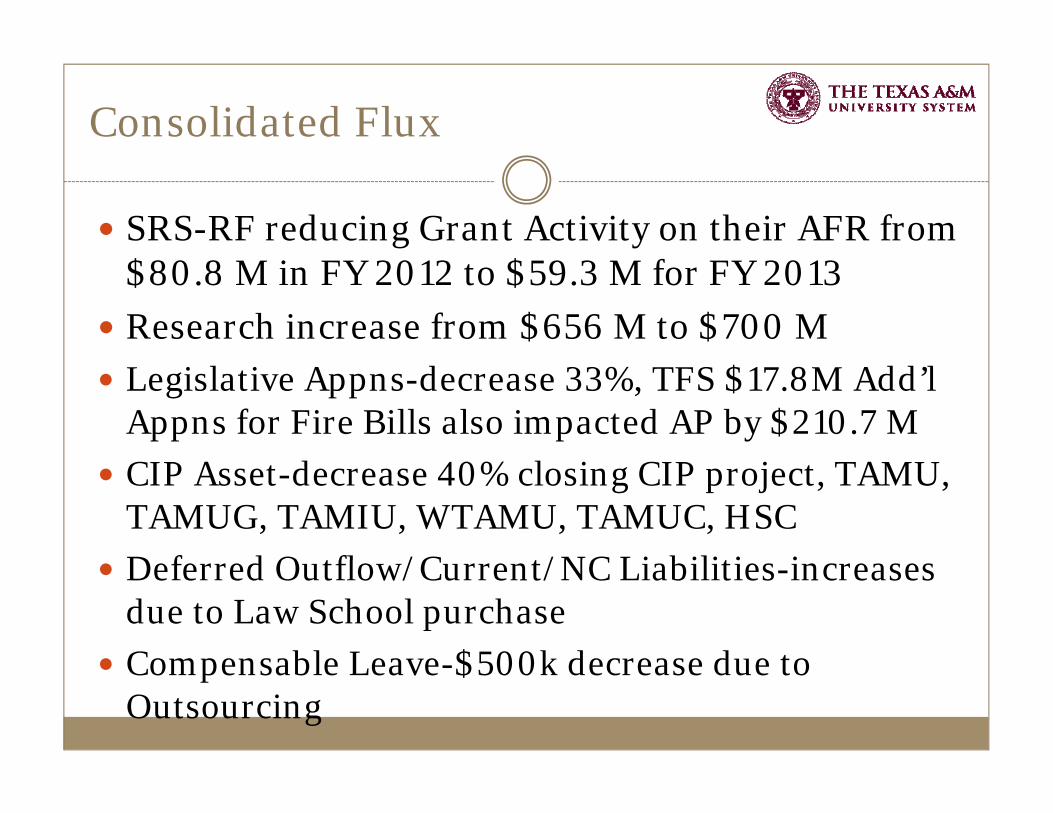

Consolidated Flux

SRS-RF reducing Grant Activity on their AFR from $80.8 M in FY 2012 to $59.3 M for FY 2013

Research increase from $656 M to $700 M Legislative Appns-decrease 33%, TFS $17.8M Add’l

Appns for Fire Bills also impacted AP by $210.7 M CIP Asset-decrease 40% closing CIP project, TAMU,

TAMUG, TAMIU, WTAMU, TAMUC, HSCD f d O tfl /C t/NC Li biliti i Deferred Outflow/Current/NC Liabilities-increases due to Law School purchase

Compensable Leave $500k decrease due to Compensable Leave-$500k decrease due to Outsourcing

Consolidated Flux, cont.

Tuition/Fees-22% increase attributable to TAMU /and HSC enrollment, TAMUT, TAMUCT, TAMUSA

Hospital Revenue-New Line item HSC patient income

Federal PT Revenue-262% increase, TFS $83.2M fi bill2011-2012 fire season bills

COGS-$9M decrease, outsourcingP f i l F & S i $ M i Professional Fees & Services-$34M outsourcing, TAMU/TAMUC/PVAMU, TAMIU related to Gear Up Grant TAMUCT Ellucian contract Grant, TAMUCT Ellucian contract

Analysis of Review Points-79% Blue Ribbon

•Members with <5 Review Pts -31% •TTITVMDL•TVMDL

•TFS•TEES•HSCSC•SO/SRS

•Members between 6-10 Rev Pts-48%•TAMUKTAMU/TAMUG•TAMU/TAMUG

•TAMUT•AgriLife Extension Service•TAMIU•TAMUCT•TAMUSA•TEEX•WTAMU•WTAMU•Research Foundation

Happy System Office AFR Team!!

Member AFR Review Process

Reviews went well As members continue to improve begin focusing on bigger As members continue to improve begin focusing on bigger

accounting theory issues and less focus on the checklist because the statements depict the position of the entity

Common Issues Still Present Clearing Accounts Service Centers Accruals and accurate account controls Staff being reduced and requirements haven’t changed Strong Reconciliation team needed Strong Reconciliation team needed

Improved fluctuation explanations this year Math plus explanations Math plus explanations Still had to ask for some additional explanations

2014 Accounting Update

2014 Board Update & Budgeting UpdateBudgeting Update Board Update Still concerned about the III 1 Net Position Reserves for Still concerned about the III-1 Net Position Reserves for

Unrestricted Ending Balance of Unrealized Gain/Losses on Investments added Due from’s will be reserved

Reduce Overall Debt OPEB Liability-Retirement Insurance-FY 2013 $719 million OPEB Liability Retirement Insurance FY 2013 $719 million Reviewing Functions in the Budget Process More concentration on Strategic Budgeting Analytics http://analytics.tamus.edu/ website still being used

Students asked for a breakdown of the consolidated fee Website being updated for this additional detail Website being updated for this additional detail

2014 Board Update & Budgeting UpdateBudgeting Update

Resume the normal budget calendar for Legislative year BPP will roll prep to active for Budgeted positions on

August 16th and Wage positions the following week on August 16 and Wage positions the following week on August 23rd

Budget Module open late Spring

Members will present to the Board their budgets Members will present to the Board their budgets

Budgets due June, 2015

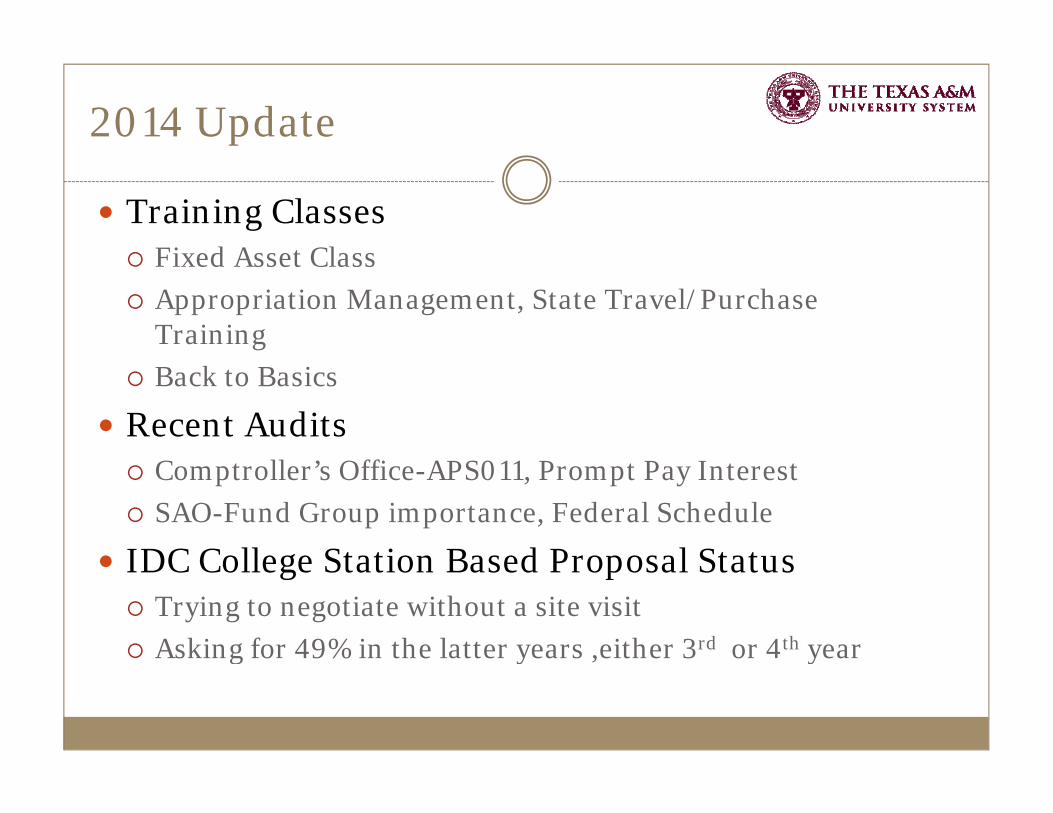

2014 Update

Training Classes Fixed Asset Class Fixed Asset Class Appropriation Management, State Travel/Purchase

Training Back to Basics

Recent Auditsll ff Comptroller’s Office-APS011, Prompt Pay Interest

SAO-Fund Group importance, Federal Schedule

IDC College Station Based Proposal Status IDC College Station Based Proposal Status Trying to negotiate without a site visit Asking for 49% in the latter years ,either 3rd or 4th yearg 49 y , 3 4 y

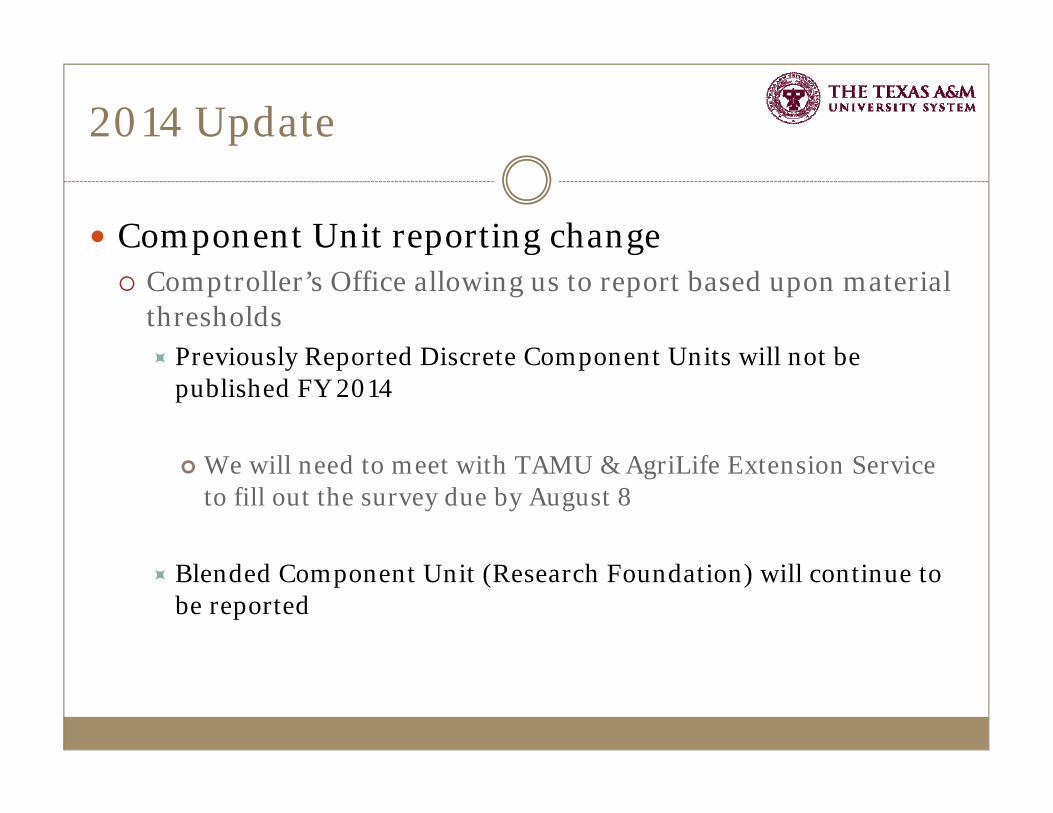

2014 Update

Component Unit reporting changep p g g Comptroller’s Office allowing us to report based upon material

thresholds Previously Reported Discrete Component Units will not be Previously Reported Discrete Component Units will not be

published FY 2014

W ill d t t ith TAMU & A iLif E t i S i We will need to meet with TAMU & AgriLife Extension Service to fill out the survey due by August 8

Blended Component Unit (Research Foundation) will continue to be reported

Accounting Update Topics

2014 Site Visits- PVAMU, TAMUC, WTAMU

Employee Reimbursement Policy (Safe Harbor)

TASSCUBO Accounting Principles Committee

GASB update – FY15 could see changes for i GASB 68pensions, GASB 68

NACUBO U d NACUBO Updates

2014 Site Visits

PVAMU Improving Coordination and Training internally Recon Team working through variances Privatized Housing contract unique Privatized Housing contract unique

TAMUC New Staff Members New Staff Members

WTAMU Building new teamg Reporting Challenges when comparing Internal System to

FAMIS Taught us their Accounting System Taught us their Accounting System

Employee Reimbursement Policy

Change implemented at all A&M members FY 2015g p 5

IRS looking to collect additional taxes from gschools/agencies if we do not treat employee reimbursements properly

Starting 9/1 employee reimbursements will be taxed if h l d b i h h i hi if the employee does not submit the voucher within 90 days of the Ending travel date Ending travel date Date expense incurred

3Ps

Public Private Partnership=Privatized Housingp g Board does not want us to increase debt for capital

projects, if possible Across the nation Companies/Foundations are

constructing assets and managing dorms, parking tgarages, etc.

PVAMU started these years agoTAMIU h TAMIU has a contract

Now TSU, and TAMU

3Ps

Accounting Researchg GASB 60 Service Concession Agreements-usually fails third

criteria-level of control over prices/management GASB 60 Appendix B Service Management Agreements GASB 60 Appendix B Service Management Agreements

Similar to Outsourcing Vendor is selected to manage a function on campus Vendor begins making management decisions regarding the

function GASB stated there are no additional reporting requirements Treat as a Contract Revenue recognized when earned Asset title usually stays with company until 30 year life ends Asset title usually stays with company until 30 year life ends

3Ps

Accounting Treatment-each contract is a little gdifferent PVAMU-Service Management Agreement with the gifting of

the buildings (no longer writing these contracts to gift the the buildings (no longer writing these contracts to gift the assets)

TSU-Setup agency fund with SLs-Collegiate Housing Foundation is managing the facilities, TSU will be managing the activity, issuing FASB statements for CHF, allocate interest to the agency funds, employees paid from Designated and these costs can be charged to CHF

TAMU-should be similar working with Janet Guillory and her teamteam

TASSCUBO Accounting Principles

Pressure to issue white papers and meet more oftenp p

Considering analyzing g y g Service Centers NACUBO Functions

Defining whether Lab Fees are mandatory or not

Future GASB Statement 68

Ohio State University Steps to Prepare for FY 2015 y p p 5Reporting change for Pensions1. Read GASB 68 Accounting & Reporting for Pensions

l i l l li bl f h f d d i2. Multi-employers plan are liable for the unfunded pension3. Estimate unfunded pension liability

Unfunded liability for each $1 of salaryy $ y Liability may vary once Pensions implement GASB 67 Communicate with Management, Boards, Auditors and Rating

AgenciesAgencies4. Differs from OPEB, since we are funding Pension plans5. Opportunity to discuss this complex issue and help others

d d hi l i b fiunderstand this complex, expensive benefit

Future GASB Statement 68

Teacher’s Retirement System is considered a cost h i lti l d fi d b fit l ith sharing multi-employer defined benefit plan with

special funding situation (most common)

Since the State funded the contributions, TRS is reported more like a sole employerreported more like a sole employer This is important and could be the determining factor whether

we have to report at the member/agency level Once the Comptroller’s Office makes a decision, we may need

to gear up for recording this new liability (May, 2015)

Future GASB Statement 68

According to 2013 CAFR-Pension Noteg 3 TRS Actuarial Assets $122 billion; Liability $150 billion TRS Unfunded Actuarial Accrued Liability $28 billion for

2013; Covered payroll $36 billion2013; Covered payroll $36 billion $28 billion divided by $36 billion is $.77, for every dollar of

salary multiply by $.77 to calculate an estimated liability Our Eligible TRS Covered Wages was $741 million in FY 2013 Estimated Texas A&M System Liability could be $570 million

(from BPP report BP219-02 covered wages $741 million)(from BPP report BP219 02, covered wages $741 million) GASB 67 will require a change in the unfunded pension liability, so

this number could be significantly different for FY 2015 We need to be aware of this looming liability (OPEB liability was We need to be aware of this looming liability (OPEB liability was

$719 million for FY 2013)

Future GASB Statement 68

After talking with TRS appears the liability will g pp yincrease after GASB 67 is implemented in FY 2014

Comptroller’s Office is leaning towards the State reporting most of the liability

However, still a potential that each i i i / ill h f h h l institution/agency will report our share of the whole liability less the state’s portion

GASB 34 Up for Review

In 2013, GASB researching with users of the 3, gfinancial statements effectiveness of GASB34, June, 2014 NACUBO Business Officer Magazine

Users were not satisfied with comparability of Enterprise funds and Higher Ed BTAs (handout)Di ti fi d ith O ti St t t l it i Dissatisfied with Operating Statement unless it is a fund of the primary government, doesn’t tell the story of BTAs must operate within their means and story of BTAs must operate within their means and generate many diverse revenue streams that support complex programs

NACUBO Updates

Reduction of Debt Across the Nation, March, 2014, , 4 Reaching debt capacity

B d f R d d b Board of Regents want to reduce debt

Shift the burden of capital facilities to Foundations/ Shift the burden of capital facilities to Foundations/ Corporations

M t h t b l b t i i th f iliti Management has to balance between improving the facilities and reducing debt

NACUBO Updates

Funding Accounting dead? 1995 Articleg g 995 Stanford says yes University of Oklahoma says no

Implementing new software packages starting to see some changessome changes

Stronger Reporting Solutions reducing the number Stronger Reporting Solutions reducing the number of funds

NACUBO Updates

UC Berkeley-April, 2014 Business Officer articley p , 4 Went from 22,000 funds to 160 funds

If department spent more than 5% of its budget on a particular fund then kept itfund, then kept it

Consolidate into higher-level fund types Unrestricted

Gif Gifts Endowments Contracts & Grants

State funded in 2004 was 28%, in 2012 dropped to 12% Shared services initiative

If more then 50% of their time as HR IT research or finance If more then 50% of their time was HR, IT, research or finance, they were moved into a service center

NACUBO Updates

UC Berkeley-April, 2014 B i Offi ti lBusiness Officer article 3 Types of Funding

Good-UnrestrictedGood Unrestricted Bad-Restrictions for certain

purposes, financial aid or specific departmentdepartment

Ugly-rarely spendable because of being restricted to narrow purposespurposes

Use first dollar principle-concentrate on spending ‘ugly’ funds first to manage flexibility in the ‘good’ unrestricted funds

Analyze the ‘bad’ funding and see if restrictions can be lifted if they are too strict

NACUBO Updates

New chair of the Financial Accounting Standards gBoard (FASB) strives for consistency on technical issues between FASB, Governmental (GASB) & I t ti l (IASB) M International (IASB)-May, 2014

D t i h t i f ti i t t t i Determine what information investors want to see in the financial statements Add some data that is needed Add some data that is needed Remove data that is no longer relevant

NACUBO Updates

Split-rating is where an institution’s credit is rated by p g yMoody’s and Standards & Poor’s-June, 2014

Becoming more common due to variances in methodologies

80% Public Universities use Moody’s Moody’s recalibrated all municipal bonds in FY

2010, most were ranked higherT A&M S i k d b i i Texas A&M System is ranked by 3 rating agencies Moody’s: Aaa S&P: AA++ S&P: AA++ Fitch: AA+

NACUBO Updates

Moody’s: Aaa:y The bonds and stocks which are given this rating are regarded

as of the highest class, both as regards security and general convertibilityconvertibility

S&P: AA++ ‘AAA’—Extremely strong capacity to meet financial y g p y

commitments-Highest Rating ‘AA’—Very strong capacity to meet financial commitments

Fit h AA Fitch: AA+ AAA: Highest credit quality AA: Very high credit quality Very low default risk Very strong AA: Very high credit quality. Very low default risk. Very strong

capacity for payment of financial commitments.

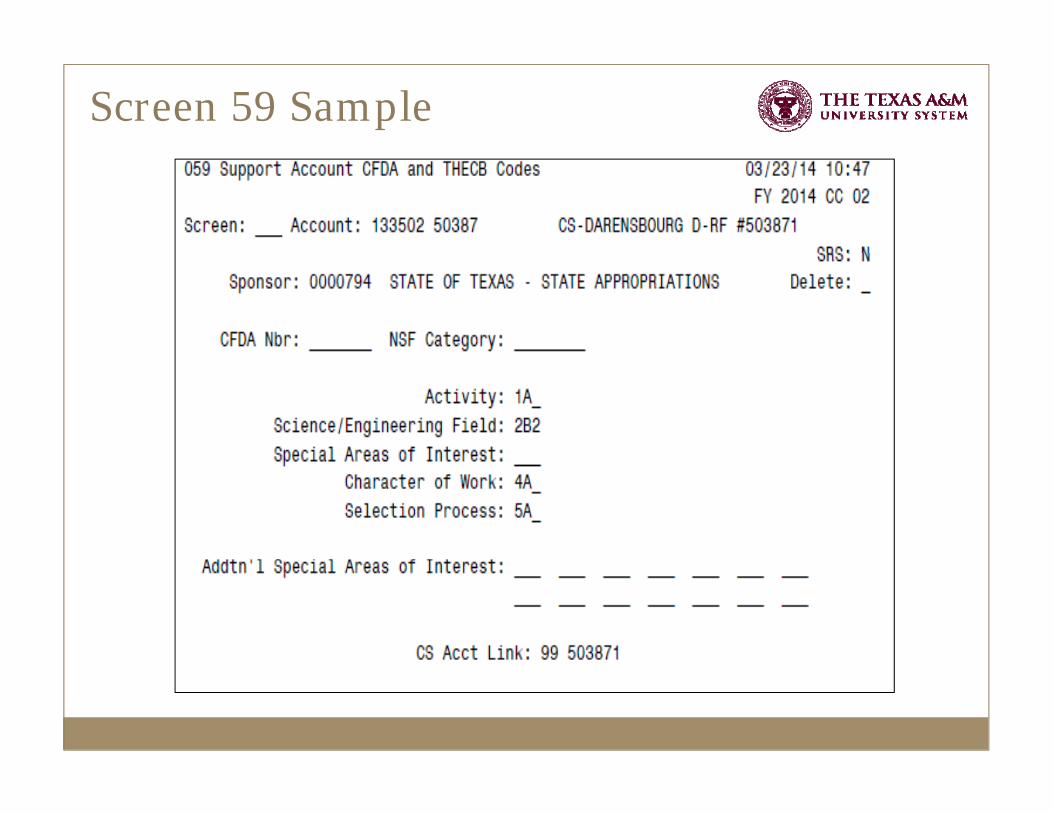

FAMIS 59 Screen

Provides reporting attributes for SL accounts, and p gsupport accounts, included in the THECB or NSF HERD Survey of research expenses

M t NOT t l d j t b t i l d d Many accounts are NOT actual sponsored projects, but are included in research reports, such as state appropriations allocated for a research program or initiative, indirect cost funds spent for “research” purposes faculty start-up packages or research giftsresearch purposes, faculty start-up packages, or research gifts

CFDA Codes – federal funds paid to an institution (FEMA reimbursements) not considered part of a sponsored project

When ne attributes are added to data arehouse for Business When new attributes are added to data warehouse for Business Objects reports, will have ability to associate the account/support account with a sponsor and reporting codes

Screen 59 Sample

15 Minute Break

R i U d d Reporting Updates and DeadlinesDeadlines

Tracy CrowleySenior Manager Financial ReportingSenior Manager, Financial Reporting

Texas A&M System Office

Overview

State Comptroller Update Highlights from July 17 AFR Update Webinar

Deadlines Status of follow-up items from FY13 Discussed at March workshop

FY Ch t AFR M d l d W k FY14 Changes to AFR Module and Workpapers Supplemental Packet

R i bl d W it Off’ Receivables and Write-Off’s Cash and Investment Entries

It t S b it ith AFR Items to Submit with AFR

State Comptroller Update

Financial Reporting Analyst assigned to Texas A&M System - Selena Meyers

Minor changes for FY14d GASB Updates

Changes to online Web Applications

Review Interagency Transactions Contact List for Review Interagency Transactions Contact List for accuracy Begin preliminary pass-through confirmationsg p y p g

USAS Reminders

GASB Statements Effective FY14

GASB 65 - Items Previously Reported as Assets & Li bilitiLiabilities Reclassifies some assets and liabilities as Deferred Inflows

& Outflows, in addition to Derivatives and SCA’s, Reclassifies certain items reported as assets and liabilities

as expenses or revenues Comptroller’s online req irements pdated Comptroller’s online requirements updated Use of the term “deferred”

The use of the term deferred should be limited to items freported as deferred outflows of resources or deferred inflows of resources. Deferred revenue is unearned revenue Deferred expense is prepaid expense

GASB Statements Effective FY14

GASB 65, continuedf l l d Specific transactions, examples include

Sale-Leaseback transactions Bond reportingp g Gain/loss on refunding recognized as deferred

outflow/inflow, not a component of bonds payable Issue costs expensed in year bond issued, not amortized Issue costs expensed in year bond issued, not amortized

Non-Exchange transactions – related to time and eligibility Resources received before time requirements are met, but

after all other eligibility requirements have been met after all other eligibility requirements have been met, should be reported as a deferred outflow of resources by the provider and a deferred inflow of resources by the recipientrecipient.

GASB Statements Effective FY14

GASB 66 - Technical Corrections GASB 67 - Financial Reporting for Pension Plans Applicable to plan administrators, TRS and ERS

GASB 69 - Government Combinations and Disposals of Government Operations

l i l d i i i f l h l Early implemented, acquisition of law school

GASB 70 - Accounting and Financial Reporting for Nonexchange of Financial GuaranteesNonexchange of Financial Guarantees Financial guarantees extended to another government, not-

for-profit organization, private entity or individual Potential to recognize a liability

GASB Update – FY15

GASB 68 – Accounting and Financial Reporting for Pensions

h f f h ll Waiting to hear from State of Texas on how it will impact TRS participants

Determine how liability will be reported

GASB Exposure Drafts

Exposure Draft – Fair Value Measurement and pApplication Proposes three acceptable valuation approaches

C ld i h l i i l d Could impact how alternative investments are valued Hedge funds and limited partnerships, not able to readily

determine market value Additional disclosures for methods used

Exposure Draft – OPEBh h li bili d l Changes to how OPEB liability and annual expense are

calculated Single actuarial cost allocation method “entry age g y g

actuarial cost method” (we already use this method)

Web Application Systems

Several only applicable to System Officesd h l Bond Reporting, Investments, Cash Flow, Long Term

Liability Note

Web applications for MembersWeb applications for Members CANSS (Capital Assets Note 2) GR Recon SEFA (Federal Expenditures) SPTR (State Pass-Through’s)

Pl h d Plan ahead Request access for individuals responsible for these items Verify beginning balance in CANSS is correct Verify beginning balance in CANSS is correct

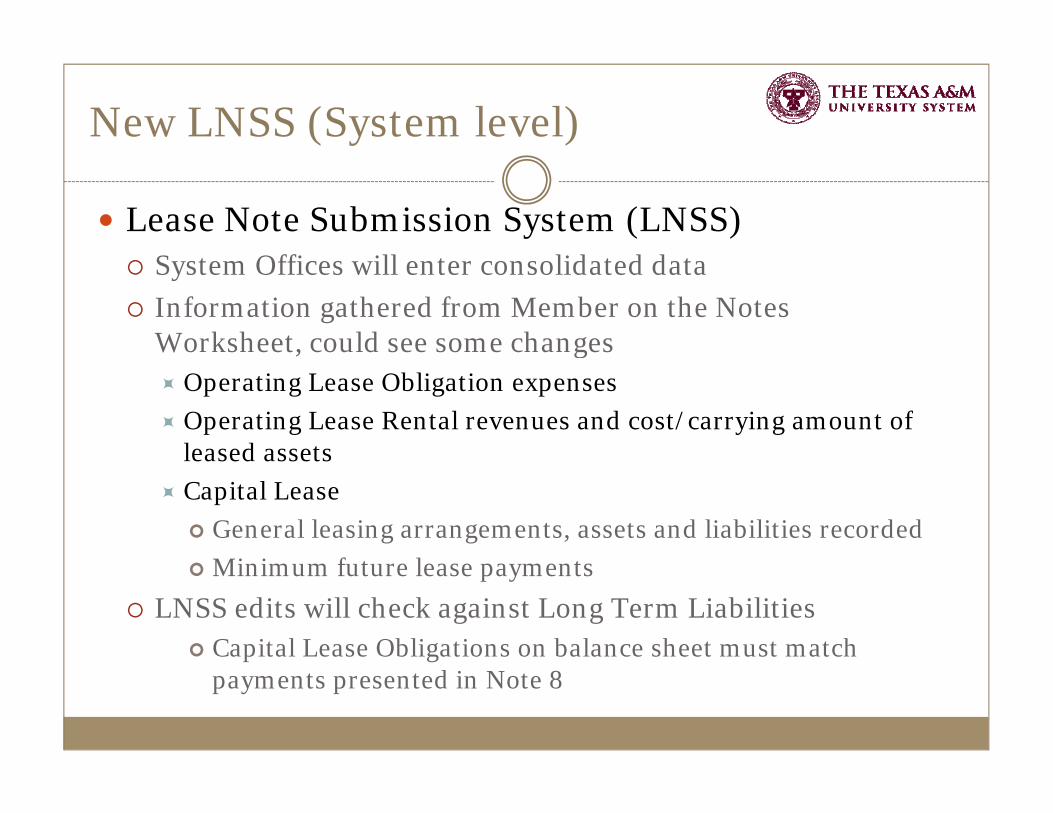

New LNSS (System level)

Lease Note Submission System (LNSS)ff ll l d d d System Offices will enter consolidated data

Information gathered from Member on the Notes Worksheet, could see some changes, g Operating Lease Obligation expenses Operating Lease Rental revenues and cost/carrying amount of

leased assetsleased assets Capital Lease General leasing arrangements, assets and liabilities recorded

Mi i f t l t Minimum future lease payments LNSS edits will check against Long Term Liabilities

Capital Lease Obligations on balance sheet must match payments presented in Note 8

CANSS Note 2 Capital Assets

Comptroller changes – CANSS certification i t l ifi drequirements clarified

Encountered new CANSS edits FY13 Example Additions column amount per Depreciation row Example - Additions column, amount per Depreciation row

cannot be higher than the related asset row

Verify CANSS matches AFR N-2 Schedule, by y , ycolumn (activity) and by row (asset type)

October 20th deadline comes fast, avoid waiting until last day to certify

CANSS/N-2 ColumnsColumn What to reviewBeginning balance Populated from USAS, should match PY

publishedN-2 schedule

Adjustments Net Restatement for Investment in Plant, consider materiality for restatements

Completed CIP Must net to zero

Interagency Transactions Includes intra-system transfers and transfers with other state agencies see transfers with other state agencies, see AFR report N-2-FN for breakdown

Additions Verify Depreciation/Amortization t h ti t t tmatches operating statement

Deletions Includes gain/loss on sale or disposal of assets

di l h b l ifEnding Balance Must match USAS balance to certify

Capital Asset Transfers

Verify IntraSystem transfersl b b Capital asset business objects query

AFR schedules N-2SYTR and N-2SYST2 match N-2

Transfers to/from internal SPA agency requires Transfers to/from internal SPA agency requires SPA entry – provide documentation with AFR Both agencies must agree and book the same value and g g

asset type (vehicle, equipment, etc.)

Transfers to/from external (non-SPA) agency Submit External to External transfer worksheet

Email to [email protected], and copy System Offices Not applicable for intra-system Not applicable for intra system

SEFA Update

Schedule of Expenditure of Federal Awardsll f d l f d d d b Captures all federal funds expended by an agency

Total Pass-Through from and Direct must equal Total Pass-Through To and Expendituresg p

Accrue revenues for cost-reimbursable contracts

Identify CFDA’s that need to be added to SEFA Send requests to add to SEFA as soon as possible

Note 7 Deferred Revenue no longer required for U i itiUniversities All System Members exempt Used for CMIA (Cash Management Improvement Act) Used for CMIA (Cash Management Improvement Act)

calculation, only applies to a few state agencies

Applicable SEFA Notes

Note 1 NonMonetary Assistance Federal Surplus Property varies each year Federal Surplus Property, varies each year

System Office will request reports and send to Members

Note 2 ReconciliationNote eco c at o Required for all Members Reconciling items for RF activity excluded from SEFA

Note 3 Student Loans Applicable to academics and HSC

N D i Lib i f G P bl Note 4 Depository Libraries for Govt. Publ. Only some have this program (historically. TAMU, TAMIU,

TAMUK, and TAMU)TAMUK, and TAMU)

SEFA Notes 5-8 Not Applicable

SEFA New Screens Added

SEFA Verification Screens

Verification B – R&D Clusterf b d l dd Verify CFDA number used is correctly overridden as R&D

R&D tag is manually selected when entering SEFA data

Verification C – NSE(Non-State Entity) Verification C NSE(Non State Entity) Do not list Texas state agencies or federal agencies as NSE Use proper titles for NSE, do not abbreviate ID number - award or contract assigned by grantor

May see a change on FAMIS reports used to prepare SEFA Award number per Screen 9 is MAESTRO reference number Award number per Screen 9 is MAESTRO reference number

Verification D – Large negative balance Review large negative balances, provide explanationg g , p p Certify the balance is correct

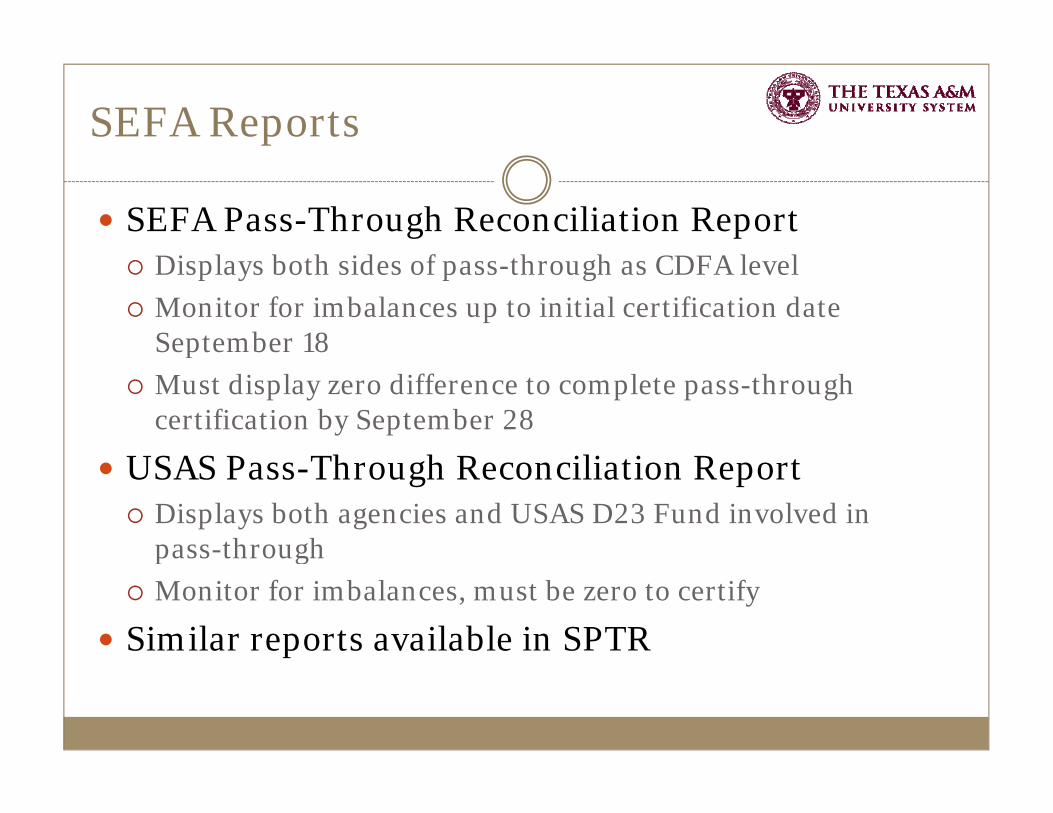

SEFA Reports

SEFA Pass-Through Reconciliation Reportl b h d f h h l l Displays both sides of pass-through as CDFA level

Monitor for imbalances up to initial certification date September 18p

Must display zero difference to complete pass-through certification by September 28

USAS P Th h R ili ti R t USAS Pass-Through Reconciliation Report Displays both agencies and USAS D23 Fund involved in

pass-throughp g Monitor for imbalances, must be zero to certify

Similar reports available in SPTR

SPTR State Pass-Through

State Grant funds passed between agencies Identify state grant award numbers that need to

be added to SPTR, send request to add Intra-system activity included in SPTR Valid exception to USAS reconciliation report, SPTR edits

won’t allow certificationwon t allow certification Send request to financial reporting analyst to certify

AFR Review – Operating statementp g State pass-through’s are reported as Operating Explanation required for State Pass-through NonOperating

SEFA and SPTR Timeline

Both web applications available July 31st

Deadline Item

September 18 Initial Certification

September 19 Intra-System Pass-Through and Due to/From Schedules Due to System Offices

September 19-25 Interagency Reconciliation Period

September 26 Interagency Activity in USAS(excludes intra-system activity)

September 28 Pass-Through Certification

November 1 Federal SEFA Schedule Final Confirmation

USAS Year-End Close

USAS Close August 29th at 7:00 PMb k d h Cannot back-date cash entries

Review IT File (USAS 53 screen) Correct batches with errors Correct batches with errors Balance and release batches before August 29th & when

post additional batches for the AFR release Nov. 20th

Pending transactions should be as minimum as possible

Clear Default Funds (9000 & 9001)i f f d b l Review USAS 69 screen for fund balances

Make corrections as needed to clear balances

USAS available for normal processing September USAS available for normal processing September 2nd

FY14 Important Deadlines

Deadline Item

August 8 CU Questionnaires due to System Office (Comptroller deadline 08/15)

August 15 Last day to accept intra-system property transfersAugust 15 Last day to accept intra system property transfers

August 28 Last day to enter data for to be FTP’d to USAS

August 29 USAS deadline for cash, IT file clean up

September 1 GASB 49 Pollution Remediation Survey

September 2 Last day to submit FY14 equity transfers to System

September 5 August FAMIS Close (TAMRF closes Sept 4)September 5 August FAMIS Close (TAMRF closes Sept 4)

September 18 Initial SEFA and SPTR Certifications

Due to/From Transfer and Intrasystem Pass-thru Worksheets due September 19 to System Office

FY14 Important Deadlines (cont’d)

Deadline Item

September 26 Interfund activities entered in USAS(Intra-system activity is entered in SEFA and SPTR web applications, not in USAS.)

S t b 8 SEFA d SPTR P th h tifi tiSeptember 28 SEFA and SPTR Pass-through certification

Property transfers with internal SPA agencies–SPA entry deadline

October 20 CANSS certification due for capital asset note

October 30 Binding Encumbrance and Payables USAS Entry and Certification

November 1 GR certification

SEFA Final CertificationSEFA Final Certification

External to External Agency Property Transfer template due

November 19 APS-011 Benefits Proportional(will be reviewed as part of AFR review this year)(will be reviewed as part of AFR review this year)

November 21 THECB Sources & Uses template due to System Offices

USAS/AFR Reconciliation

Due to System Offices by November 18thy y Component Higher Education Agencies Template from State

Comptroller’s web site (Excel)

USAS and Interagency Activity Certification Form —Component Universities (see State Comptroller website) PDF file of signed certification

System will collect documents and transmit to State System will collect documents and transmit to State Comptroller’s office by the November 20th deadline

FY13 AFR Follow Up

Results of pending items from March workshop Changes for Service Departments Proposed change not implemented in FY14

Still not a perfect solution would require significant changes to Still not a perfect solution, would require significant changes to AFR reports

Same process as last year, except post journal entries i t d f l t iinstead of manual entries Correct function and reclassify negative expense as revenue AFR Instructions updated with details on required entries

Use Schedule IV-4 and business objects query to analyze accounts

New tab added in Notes template describe what entries New tab added in Notes template, describe what entries were made

Service Department Entry 1

Net Income reported as negative expensef h h $ If the net income is greater than $25,000, or creates a

negative expense, post a journal entry to recognize the income as revenue Increase expense and revenue in Designated year-end

adjustment account Use Institutional Support function when increasing expense to pp g p

offset the negative expense

Entry Fund Group Function

Debit Operating Expense Designated Institutional Support

Credit Operating Revenue Designated Institutional Support

Service Department Entry 2

Net Loss reported as Institutional Supportf h l b l f h h l If the net loss belongs in a function other than Institutional

Support, post a journal entry using year-end adjustment Designated accounts coded with correct functions. Move expense between the year-end accounts with different

functions

d G iEntry Fund Group Function

Debit Operating Expense Designated Correct Function (such as Research))

Credit Operating Expense Designated Institutional Support

Suggested Expense Codes

For entries 1 & 2, select an expense that d ith th S i D t t AFR corresponds with the Service Department AFR

Fund Group

Fund Suggested SL Expense Group Description Code for Adjustment Entry 21 Professional Fees & Service 5453

l22 Travel 303023 Materials & Supplies 4010 24 Communications & Utilities 5010 25 Repairs & Maintenance 5512 26 Rentals & Leases 584027 Printing & Reproduction 5615 28 Claims & Losses 6457 (System only) 29 Other Operating Expense 6335

Service Department Analysis

Use Schedule IV-4 to analyze Service Department ti it d di b lactivity and ending balances

Review Non-Operating activity, should be minimal Review rates for losses fund negative balances Review rates for losses, fund negative balances Monitor large balances for reasonableness

Journal entries is an improvement over manual pentries

Technically should be allocating the net losses according to natural classification of expensenatural classification of expense Current design relies on AFR fund group to determine natural

classification, very challenging to change the current structure Since we aren’t bringing in all expense, just the net loss, impact is

somewhat limited

Endowment Survey Results

Received feedback from Members on three questions about Endowments Endowment AFR Fund Groups, each endowment category

(True Term Quasi Quasi-Restricted) has a code for (True, Term, Quasi, Quasi Restricted) has a code for General Purpose and for Student Aid Informational only, not used in any financial reports

I t t t d t t t GP SA t iti l Important to code to correct category, GP vs. SA not critical Definition for Quasi-Restricted

Agree this represents fund with external restrictions internally designated as a quasi-endowment.

Corpus could be spent, must follow the restricted purpose Examples include funds donated to provide scholarships that p p p

the university elected to invest as a quasi-endowment

Net Position-Restricted for EndowmentsRestricted for Endowments

Note 22 - Donor Restricted Endowments Revised FY13 amounts during State Comptroller review

Researched what belongs in Expendable vs. U d blUnexpendable

Per GASB 34, paragraph 35 “ h d f d i i l“When permanent endowments or permanent fund principal amounts are included, “restricted net assets” should be displayed in two additional components—expendable and nonexpendable. Nonexpendable net assets are those that are required to be retained in perpetuity.”

Revised Note 22

Net Appreciation of Donor-Restricted Endowments

Donor-Restricted Amount of Reported in Endowments Net Appreciation* Net Position

True Endowments 36,193,118.75$ Restricted for Expendablep

* The current year fair value adjustment was $995,858.13.

$36M Net appreciation represents the unrealized gain/loss for True endowmentsgain/loss for True endowments

Historically, we have reported the Appreciation Reserve, which is the accumulated realized

i /lgains/losses

FY13 Restricted for Endowments

Nonexpendable is only appropriate when the net positionis required to be held in perpetuity, such as endowment corpuscorpus

AFR Module Change – IV-Fund

Realized Gain/Loss moved to Investment Income Previously netted with Unrealized Gain/Loss on the Net

Increase/Decrease in Fair Value row Since this was a CAFR adjustment PY column was adjusted Since this was a CAFR adjustment, PY column was adjusted

PY query updated in AFR module, automatically updated Detail rows on IV-Fund distinguish Realized Gain/Loss

f I t t/Di id d Ifrom Interest/Dividend Income

Investment Income

Interest/Dividends/Other Income

Summarized on Investment Income row for single column E IV

Interest/Dividends/Other Income

Realized Gain(Loss) on Sale of Investments

Ex IV

AFR Module Change - III-1

New row added to Reserves section of III-1l d ( ) Unrealized Gain (Loss) on Investments

Use existing reserve code 2772 Reserve amount for ending unrealized gain (loss) allocated ese e a ou o e d g u ea ed ga ( oss) a oca ed

to unrestricted current funds 08/31 market value adjustment Reconciliation of Assets Held

by System Officesby System Offices This is not net change reported on operating statement.

Instructions for Reserved for Receivable updated to include Due from Other Members Include with reserve entry T t l h ld t h b l h t i bl Total should match balance sheet receivable rows

AFR Module Changes – Ex III

New row for Student Liabilities Use existing account control 2155, Student Liabilities Identified as the most significant balance in Other

M i ill d f bl Moving to separate row will reduce amount of payables to detail in Note 24

Remove rows for Security Lending Collateral/Obligations

Workpaper Changes

Fluctuation Analysish d h h ld f l Changed threshold for explanations

Required for fluxes greater than 20% and $100,000 (increased from $25,ooo)( $ 5, )

AFR Instructions Updated Accounts Receivable accounts controls added to Chapter 5 Reserve codes added to Net Position section, Chapter 8

APS011 Benefits Proportional will be reviewed ith AFR thi with AFR this year

Will see “APS011 Review” items listed on point log Won’t be numbered as actual points may require some Won t be numbered as actual points, may require some

explanations

Change for ACAP by Fund Group

ACAP worksheet provided by System Officesll d bl b b f d Allocate accrued compensable absences by fund group

Estimate current and non-current Based on LeaveTraq data Based on LeaveTraq data

Historically instructed Members to report Restricted portion in E&G columnp Change for FY14, worksheet will show Restricted separately Members use judgment to decide whether to report in

Restricted or E&G columnRestricted or E&G column Acceptable if expenses are allowable from the Restricted

funds funding the related payroll

Payroll Posted to Agency Funds

New item added to AFR review checklist to check f l i t d t f dfor salaries posted to agency funds Per Regulation 21.01.07 Not Allowed

Payments for employee salaries belong on the Payments for employee salaries belong on the operating statement

Processing through agency funds results in Processing through agency funds results in understated salary expenses

This year, will require explanation on point log for y , q p p gsalaries posted to agency funds

Plan to build business objects query, will share in AFR Reports folder

Supplemental Packet

When will templates/worksheets be provided? Supplemental packets will be distributed by System Offices

containing information needed to complete year-end items. Part 1 - Mid-August Part 1 Mid August Due/To From Transfer worksheet Intra-System Pass Through worksheet

P t I P i l i f ti Property Insurance Premium accrual information Tuition Discounting Template TPEG worksheet SEFA (Schedule 1A) Notes worksheet and instructions Fluctuation Analysis workpaper Member review checklist Member review checklist AFR Title Page

Supplemental Packet, cont’d.

Part 2 – distributed in Mid-September Reconciliation of Assets Held by System Offices

Year-end investment entries ACAP Worksheet ACAP Worksheet

Compensable absences payable entries TRS/ORP Data for GR Recon GASB 51 Land Use Rights (easements) Cash Flow Workpaper Notes Worksheet Notes Worksheet Federal Surplus Property (if applicable) USAS Cash in State Treasury

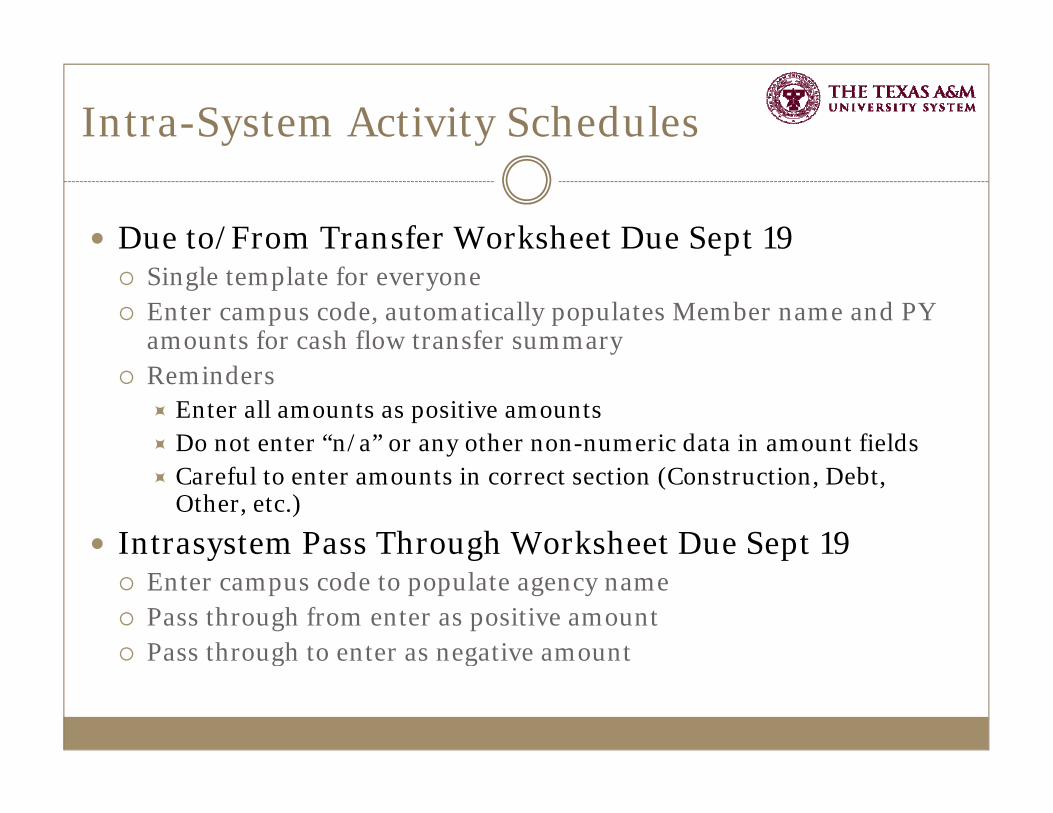

Intra-System Activity Schedules

Due to/From Transfer Worksheet Due Sept 19/ p 9 Single template for everyone Enter campus code, automatically populates Member name and PY

amounts for cash flow transfer summary Reminders

Enter all amounts as positive amounts Do not enter “n/a” or any other non-numeric data in amount fields Careful to enter amounts in correct section (Construction, Debt,

Other, etc.)

Intrasystem Pass Through Worksheet Due Sept 19y g p Enter campus code to populate agency name Pass through from enter as positive amount Pass through to enter as negative amountg g

Pre-AFR Review/Preparation

Run AFR Reports Verify Balance Sheet is in balance, and ties to operating y , p g

statement Run frozen code/budget pool queries R i f t b l Review for contra balances Review TANDF-TD and tie out Exemptions & waiver lines

Clean up reconciling items banks & clearing Clean up reconciling items, banks & clearing accounts

Preliminary pass-through confirmationsy p g Review contract and grant revenue codes Review accounts for correct function/effort codes/ Review Reimbursements Due from State Treasury

Year-End Receivable Entries

Resources added to Ch. 5 of AFR Instructions to 5assist in selecting the correct codes receivables, allowances, and bad debt expenses

l l b ll /b d d b Several review points last year about allowances/bad debt entries that didn’t relate to original revenue stream of the receivable

Balances were reported in other that belonged in A/R Questions during the year about proper write-off procedures

A/R M d l l i bl b l i t A/R Module places receivable balance in account control 1300 Entries required to move to correct row such as Federal Entries required to move to correct row, such as Federal

Receivables

Allowance for Doubtful Accounts

Review receivable trends, estimate percentage and , p gadjust allowance balances

Bad Debt Expense contra-revenue Select appropriate codes based on type of receivable

Contra-RevenueRevenue Line Item Bad Debt Expense Codes Receivable Allowance CodesRevenue Line Item Bad Debt Expense Codes Receivable Allowance Codes

Tuition Revenue 6310 Tuition 1397 Student ReceivablesFee Revenue 6316 Fees 1397 Student ReceivablesNet Professional Fees 6311 Professional Fees 1396 Accounts ReceivableNet Professional Fees 6311 Professional Fees 1396 Accounts ReceivableOther Sales Revenue 6312 Other Sales 1396 Accounts Receivable

1396 Accounts Receivable, or1399 Other Receivable

Other Grants & Contracts 6313 Contracts & Grants, Private and Other

Gift Revenue 6314 Pledges 1398 Pledge Receivable

Receivable Write-Off’s

System Policy 21.01.04 Extension of Credit Coordinate with General Counsel to set threshold for

receivable write-off’sh b h h ld l Anything above threshold require OGC approval

Write-off entry – Debit Allowance, Credit Receivable

Does not constitute a forgiveness of debt Does not constitute a forgiveness of debt Vendor remains on state hold (if applicable)

Questions about write-off procedures?Questions about write off procedures? Special considerations for student receivables? Write-off’s remain in student record system for tracking y g

purposes, not reported on balance sheet

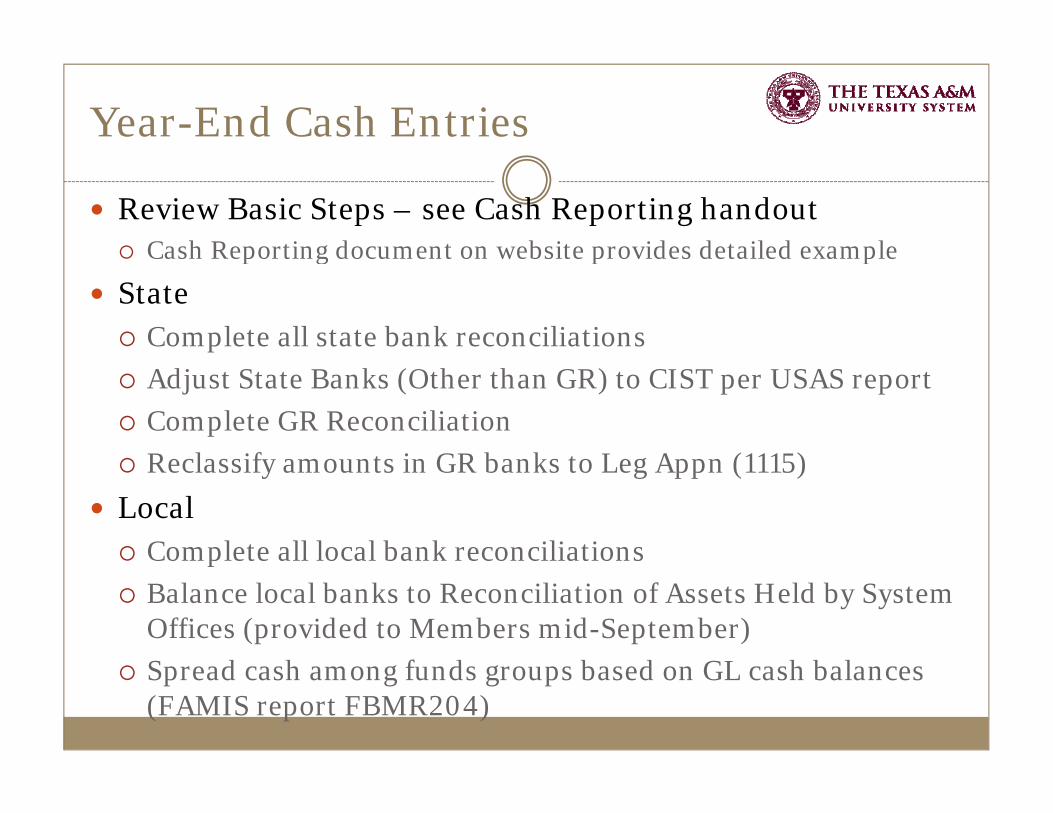

Year-End Cash Entries

Review Basic Steps – see Cash Reporting handout Cash Reporting document on website provides detailed example Cash Reporting document on website provides detailed example

State Complete all state bank reconciliations Adjust State Banks (Other than GR) to CIST per USAS report Complete GR Reconciliation R l if t i GR b k t L A (1115) Reclassify amounts in GR banks to Leg Appn (1115)

Local Complete all local bank reconciliations Complete all local bank reconciliations Balance local banks to Reconciliation of Assets Held by System

Offices (provided to Members mid-September)S d h f d b d GL h b l Spread cash among funds groups based on GL cash balances (FAMIS report FBMR204)

Negative Cash or Investments

Review cash and investments by fund group for negative balances balances

This can happen in Restricted if there is a large number of cost-reimbursable grants or contractsg Record Due to/from between fund groups if activity is

temporarily funded from another source

U k t l t i d k Use a workpaper to plan entries and make adjustments as needed

Cash/investment allocation by fund group are some Cash/investment allocation by fund group are some of the last entries posted

AS OF AUGUST 31, 2014SYSTEM MEMBER:_______

C h C i P l F d L d▪ Cash Concentration Pool Fund Ledgers:8/31 Balance - Current Investments (Short Term) 21,541,354.828/31 Balance - Non-Current Investments (Long Term) 70,867,969.21

YE Adjustments - Short Term (ST):ST July Bank Charges (1,926.73)

SampleReconciliation

f A H ld ST Realized LossST August Interest/Dividend Earnings 278.564th Quarter SEF Income Distribution 131,708.44LT August Interest/Dividend Earnings 88,383.37LT August Realized Gain (Loss) (10,886.99)LT A t E t l M F (16 093 42)

of Assets Held by System

LT August External Manager Fees (16,093.42)

Total Assets Held by SO - Book Value 92,600,787.26

Adjustment for Fair Value Increase (Decrease) 3,525,896.52

Total Assets Held by SO - Market Value 96,126,683.78

Assets Held by SO - Market Value - Non-Current 74,455,268.69

Assets Held by SO - Market Value - Current 21,671,415.09

Cash Concentration Pool Adjustments (Current Only):In-Transit Items

Outstanding Checks (5,810,841.55)

Adj t d A t H ld b SO C t 15 860 573 54Adjusted Assets Held by SO - Current 15,860,573.54

Adjusted Total Assets Held by SO 90,315,842.23

Investment Reporting

Highlights from AFR Instructions Chapter 4 Investments Held by System Offices

Reconciliation of Assets Held by System Officesl l b k l h dEnter local bank reconciling items, such as outstanding

checks, to balance CCP carrying amount per books Year-End Entries Recorded in Month 13 Year End Entries Recorded in Month 13

August Cash Concentration Pool (CCP) Income & Fees 4th Quarter Endowment Fund Income Distribution 4 Q

• SO will request automated entries post in in Month 13• Review XR051 error report

Investment AFR Entries

AFR Entries – Reverse in September Market Value Adjustments and SEF Appreciation Reserve Endowments

Year End Appreciation Reserve Allocation by endowment type Year-End Appreciation Reserve Allocation by endowment type Market Value Adjustment by endowment type Report portions related to True Endowments as Expendable

Cash Concentration Pool Cash Concentration Pool Use workpaper to allocate balance across fund groups Wait until all other entries are posted, entries could change allocation

P t M k t V l dj t t b f d Post Market Value adjustment by fund group Classify between Current and NonCurrent Use appropriate account controls for Restricted or UnRestricted

S l H ld I MV Adj b A Separately Held Investments MV Adjustment by Account

Assets Held by System Workpaper

Instructions for Completing the Reconciliation of Assets H ld f I B S Offi (d il d i Ch )Held for Investment By System Offices (detailed in Ch. 4) Enter Cash Concentration Pool Reconciling Items

Based on local bank reconased o oca ba eco Complete Balance Sheet Category Summary (below the

Reconciliation) Update Balance Sheet Summary for each Column Update Balance Sheet Summary for each Column Verify Grand Total Equals Total per SO Verify Total Column Equals AFR Reports

Complete AFR Check Figure Sheet Verify Net Increase/Decrease in Fair Market Value Verity Statement of Cash Flows-Net Purchases/Sales of Verity Statement of Cash Flows Net Purchases/Sales of

Investments

I l d f t t t l d AFR h d l

Balance Sheet Category Summary:

Includes references to account controls and AFR schedules, summarizes how balances are reported.

Balance Sheet Category Summary:FAMIS GL Acct Ctrl:

Title per AFR line item: CCP Per AFR:Unrestricted Assets Held - Short Term 1110 14,100,507.50 Sch ThreeR t i t d A H ld Sh T 1111 1 760 066 04 S h ThRestricted Assets Held - Short Term 1111 1,760,066.04 Sch Three

Subtotal - Current Assets 15,860,573.54 CCP | Sep.| SEF

Restricted Assets Held - Long Term 1204| 1205| 1210 122 15,852,076.30 Ex IIIUnrestricted Assets Held - Long Term 1206| 1207| 1207 58,603,192.39 Ex III

Subtotal - Non-Current Assets 74,455,268.69

Grand Total - Investments Held by SO 90,315,842.23 Check formula, value must be zero -------->

AFR Check figures - reconciling items used forconsolidated elimination entries

SECTION 2: Exhibit V: Statement of Cash FlowsNet Sales/Purchases of Investments Held by SO

co so dated e at o e t es

Amounts per System Office:CY Net Incr/Decr in FMV per Exhibit IV 3,776,181.94 Pulls from abovePlus: Beginning NonCurrent Market Value 71,664,926.34Less: Ending NonCurrent Market Value (85,664,657.36) Pulls from Asset Recon sheet

Net Sales/Purchases of Investment per SO (10,223,549.08)

Member: reconcile to AFR line item - add/change lines as needed:

Adjusted Net Sales/Purchases of Investments (10,223,549.08)

PER EXHIBIT V: CASH FLOWS FROM INVESTINGNet Sales/Purchases of Investments Held by System (10,223,549.08) <--Enter from Ex V

Difference 0.00

Resources

System Office of Budgets & Accounting website http://www.tamus.edu/offices/budget-acct/acct/resources/

AFR Preparation Guidance Workshop Presentation Preparation Instructions

Added list of Reservation codes Added reference for Receivable/Payable codes

Ch kli t f i t t t i Checklist for investment entries NACUBO function descriptions

Cash Reporting allocation example AFR Review Checklist AFR Review Checklist Deadlines Financial Reporting Contacts Sample AFR Reportsp p

Items to Submit with AFR

List of Items to submit with the AFR Title Page (remember to update names in bottom section) Schedule 1-A (download from SEFA web application) Schedule 1 A Notes (System provides template) Schedule 1-A Notes (System provides template) Schedule 1-B (download from SPTR web application) Fluctuation Analysis (III, III-1, IV, IV-1) Notes worksheet (System provides template) Tuition Discounting workpaper (System provides template,

Academics & HSC)Academics & HSC) GR Reconciliation Contra Financial Statement Amount Explanation worksheet Cash Flow workpaper (System provides template)

Items to Submit with AFR (cont’d)

FMQuery Interagency/Interfund ReportQ y g y/ p Verify activity to financial statements and schedules Due to/from, Transfers, SEFA, SPTR Valid differences for Intra System activity excluded from USAS Valid differences for Intra-System activity excluded from USAS

Completed APS011 Benefits Proportional plus workpapers TPEG Worksheet (System provides template, Academics &

HSC) Note 2 from CANSS Member review checklist Member review checklist Reconciliation of Assets Held by System (template provided) Investments by Fund Group (applies only to Investments not

held by System)

AFR Lock Request

Ready to submit AFR? Send AFR Lock Request via Ready to submit AFR? Send AFR Lock Request via email to Tracy Crowley [email protected] Wanda Roof [email protected]

AFR cannot be locked until 3 FAMIS items are completed (n/a for non-FAMIS campuses)

MDEP Monthly Depreciation1. MDEP Monthly Depreciation2. RR200 Indirect Cost3. YR412 Close budget (marked final)g

Certifications Due after Final Review

After review is complete, final confirmation will p ,include reminder to submit required certifications.

USAS Reconciliation Certification GR Certification SEFA (Schedule 1A) Final Certification SEFA (Schedule 1A) Final Certification CANSS Certification Signed CEO Certification (email acceptable, hard copy not g p py

required)

Return at 1:15

APS011APS011Benefits Proportional

Teresa Bass, CPAComptroller Comptroller

Texas A&M System Office

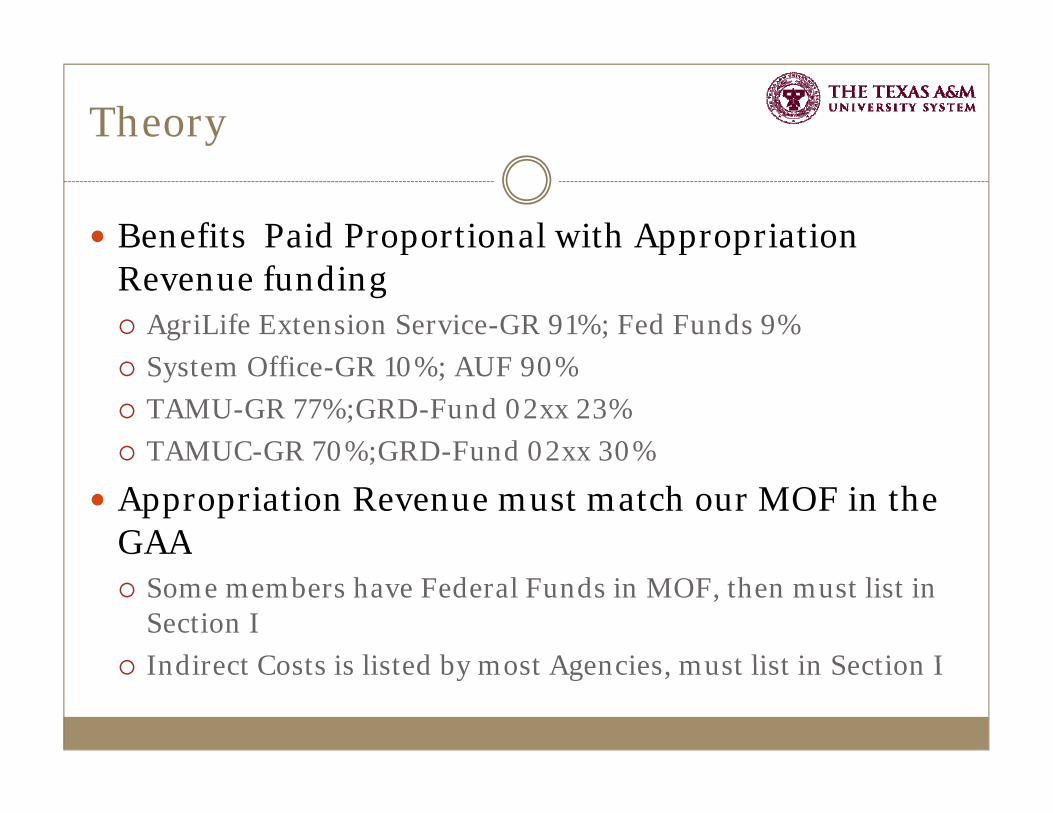

Theory

Benefits Paid Proportional with Appropriation p pp pRevenue funding AgriLife Extension Service-GR 91%; Fed Funds 9%

S Offi % % System Office-GR 10%; AUF 90% TAMU-GR 77%;GRD-Fund 02xx 23% TAMUC-GR 70%;GRD-Fund 02xx 30% TAMUC GR 70%;GRD Fund 02xx 30%

Appropriation Revenue must match our MOF in the GAA Some members have Federal Funds in MOF, then must list in

Section I Indirect Costs is listed by most Agencies must list in Section I Indirect Costs is listed by most Agencies, must list in Section I

APS011 Benefits Proportional

Overview of the Issue University of North Texas Over Charged Benefits

Can only charge salaries/wages and benefits for strategies listed in the GAA-Library was not listedthe GAA-Library was not listed

SAO and Internal Audit analyzing the calculations Must list Legal Cites for all Exclusions Education Code was changed to exclude Indirect Cost

Recovery for Higher Ed; need to ask Lauri Deviney to help us exclude this for Higher Ed Agencies as wellg g

APS011 Benefits Proportional

Contracted with Selena Meyers, former ACOy , If Appropriations are listed in the GAA, must list in Section I Do not include 3777 Default Fund Voided Warrant

I R i /C Interagency Receipts/Contracts Pass-through grants must pay for both the salaries and benefits

(change) Budget Transfers will allow the agency receiving the

appropriations to also receive the benefit appropriations (this is the preferred method by the Comptroller’s Office now)

Do not automatically use pass-through grant object codes Fund 02xx Revenue should be greater than amount listed on

the USAS 49a Screenthe USAS 49a Screen

APS011 Benefits Proportional

Revenue Exclusions-We might be excluding too g gmany items from the revenue Centers/Institutes-only exclude if federally funded

d l d l d if i d f Federal Funds-exclude if restricted for a purpose Should not exclude just because payroll wasn’t paid from funds Indirect Costs should not be excluded for agencies Indirect Costs should not be excluded for agencies Private/Local Grants-exclude if restricted for a purpose Supplemental Appropriations should be excluded or not

i l d dincluded Restricted funds that carry their own benefit costs should be

excluded-TRB, Feed & Fertilizer

APS011 Benefits Proportional

Revenue Exclusions, cont., TRB Bond Debt Interagency Receipts, NSRP grants & Family Practice

D l d h d b i i i Do not exclude other debt service appropriations Do not exclude scholarship appropriations Do not exclude/include pass-throughs (not in MOF) Do not exclude/include pass throughs (not in MOF) Exclude waivers, TPEG, Doctoral Incentive Set Asides, Tuition

Rebates, Bad Debt (can’t be the same percentage each year), Unrealized Gains/LossesUnrealized Gains/Losses

APS011 Benefits Proportional

Expense Exclusionsp Significantly reduced exclusions Some are excluding the 90 day wait, which should not be

included in Column 2 so we do not have to exclude in Column included in Column 2 so we do not have to exclude in Column 3

No longer allowed to back-out ARP

AFR Desk Review

New Procedures for APS011 Verify Appropriations to MOF in GAA

V if R & E E l i Verify Revenue & Expense Exclusions

Ask Members to submit USAS/FAMIS recon for Benefit Ask Members to submit USAS/FAMIS recon for Benefit Expenses

V if L l Cit Verify Legal Cites

Comptroller’s Office

ACO asked to look into Allowing all A&M agencies to use the System Agency form-she

must verify with management Why the APS011 Statement is listed as Pending? Will there be Why the APS011 Statement is listed as Pending? Will there be

changes to this statement before we submit AFR? Kristalle stated that the certification statement might be edited to

dd t t tadd more statements The majority of the statement can’t be edited; the statutes would

need to change She stated the procedures would potentially change in 2016-2017

and maybe 2015 if they are allowed to backdate the change

15 Minute Break

Net Position Categories

Tracy CrowleyTracy CrowleySenior Manager of Financial Reporting

Texas A&M System Office

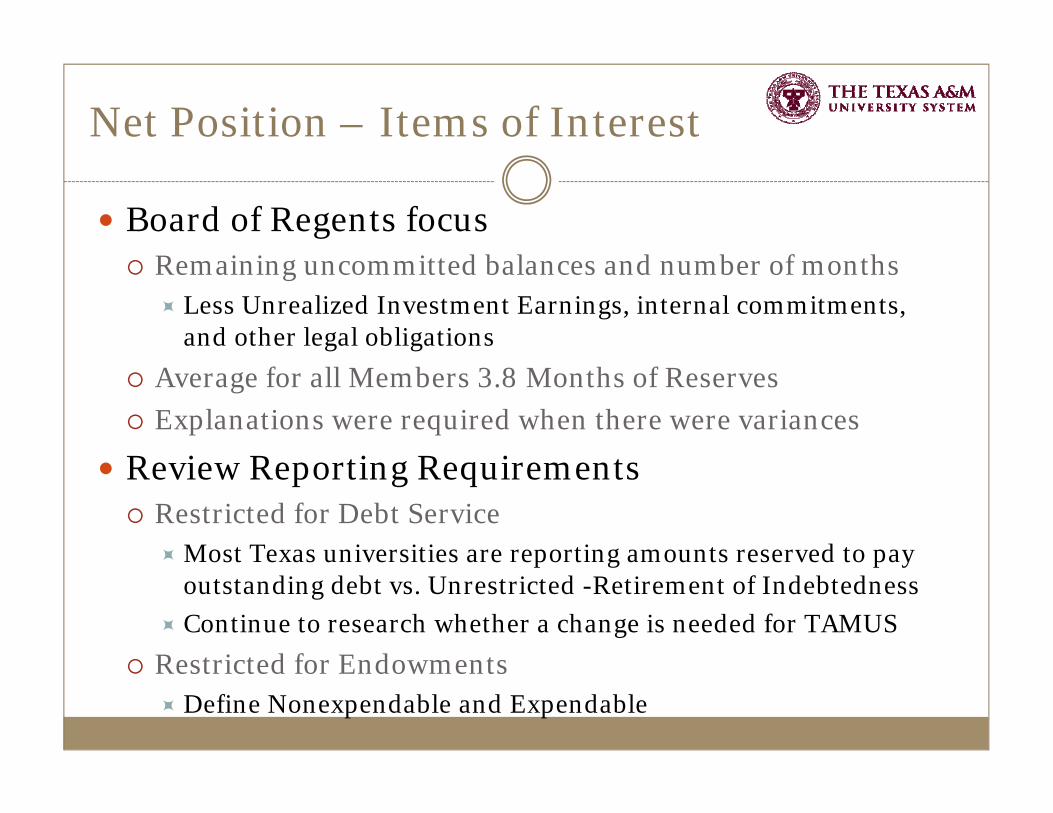

Net Position – Items of Interest

Board of Regents focusd b l d b f h Remaining uncommitted balances and number of months

Less Unrealized Investment Earnings, internal commitments, and other legal obligations

Average for all Members 3.8 Months of Reserves Explanations were required when there were variances

R i R ti R i t Review Reporting Requirements Restricted for Debt Service

Most Texas universities are reporting amounts reserved to pay Most Texas universities are reporting amounts reserved to pay outstanding debt vs. Unrestricted -Retirement of Indebtedness

Continue to research whether a change is needed for TAMUS Restricted for Endowments Restricted for Endowments

Define Nonexpendable and Expendable

Net Position per Balance Sheet

Exhibit III

Categories defined by accounting standards

The Texas A&M University SystemCombined Statement Of Net PositionFor The Year Ended August 31, 2013

Current Year Prior YearNet Position Net Investment In Capital Assets 1,307,774,114.02$ 1,284,223,421.32$ Restricted for Capital Projects 40,433,189.27 84,372,806.48 Education 281,666,779.08 263,085,114.96

Endowment and Permanent Funds Endowment and Permanent Funds Nonexpendable 420,073,627.66 404,634,119.29 Expendable 170,847,122.44 133,894,137.14 Unrestricted 2,351,859,958.84 2,062,776,988.65

Total Net Position 4,572,654,791.31$ 4,232,986,587.84$

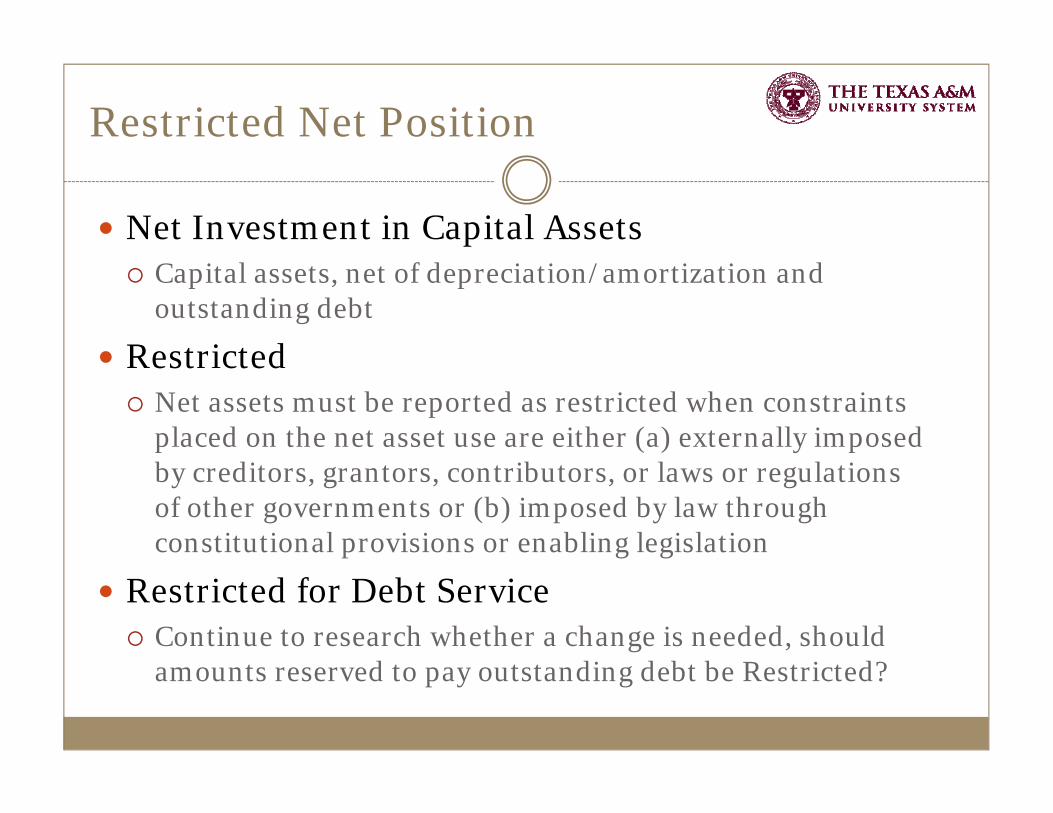

Restricted Net Position

Net Investment in Capital Assets Capital assets, net of depreciation/amortization and

outstanding debt

Restricted Restricted Net assets must be reported as restricted when constraints

placed on the net asset use are either (a) externally imposed by creditors, grantors, contributors, or laws or regulations of other governments or (b) imposed by law through constitutional provisions or enabling legislation

Restricted for Debt Service Continue to research whether a change is needed, should

t d t t t di d bt b R t i t d?amounts reserved to pay outstanding debt be Restricted?

Restricted Net Position, cont’d.

Restricted for Capital ProjectsUnspent bond proceeds (net of related debt) Restricted funds reserved to fund capital projects

Restricted for EducationRestricted fund group (excluding Capital Projects) Federal E&G Funds (AgriLife)

Restricted for Endowment and Permanent FundsNonexpendable – endowment corpus Expendable - appreciation

Restricted for Endowments

Non-Expendablep Corpus of a donor-restricted True Endowment includes

donor gifts Fair value of fund when received Fair value of fund when received Plus subsequent gifts Plus other addition specified by the donor

Expendable Appreciation

Rein ested reali ed gains/losses (Appreciation Reser e) Reinvested realized gains/losses (Appreciation Reserve) Unrealized gains/losses (Market Value Adjustment)

Restricted Quasi-Endowments

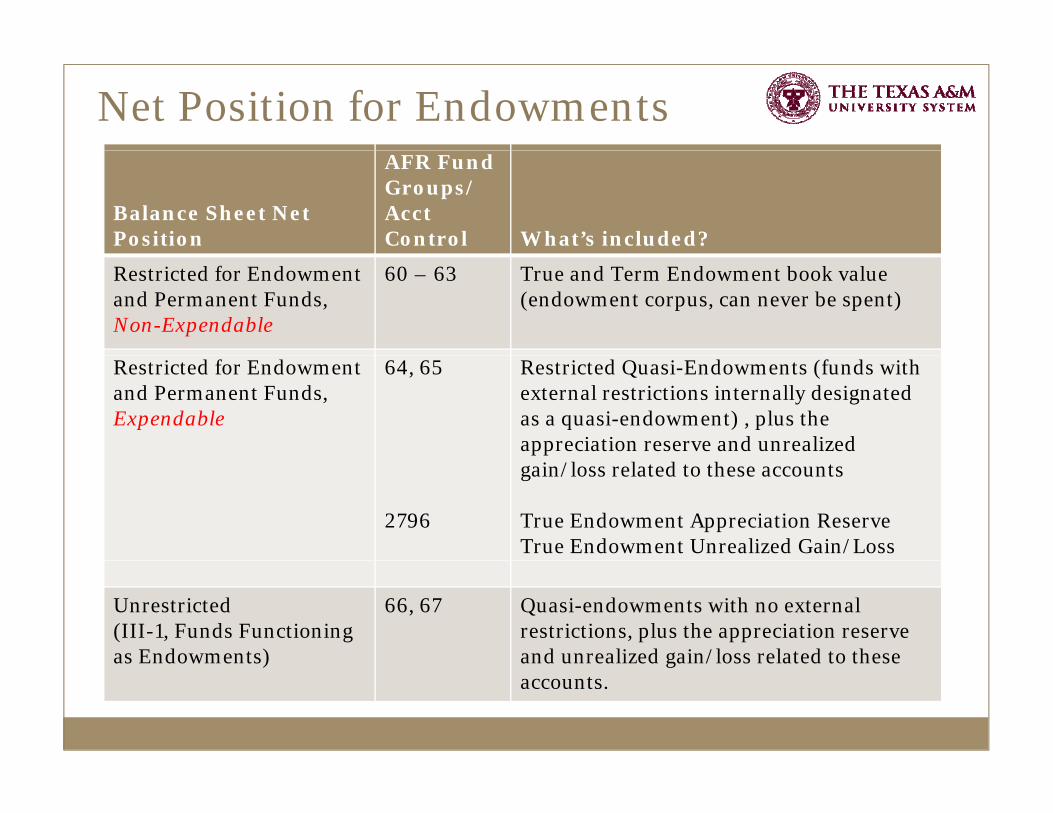

Net Position for Endowments

Balance Sheet NetPosition

AFR Fund Groups/AcctControl What’s included?

Restricted for Endowment and Permanent Funds,Non-Expendable

60 – 63 True and Term Endowment book value (endowment corpus, can never be spent)

Restricted for Endowment and Permanent Funds, Expendable

64, 65 Restricted Quasi-Endowments (funds with external restrictions internally designated as a quasi-endowment) , plus the appreciation reserve and unrealized

2796

gain/loss related to these accounts

True Endowment Appreciation ReserveTrue Endowment Unrealized Gain/Loss

Unrestricted (III-1, Funds Functioning as Endowments)

66, 67 Quasi-endowments with no external restrictions, plus the appreciation reserve and unrealized gain/loss related to these as Endowments) and unrealized gain/loss related to these accounts.

Unrestricted Net Position

Schedule III-1 Unrestricted Net Position Detail Categories not prescribed by accounting standards System Office can add/changes rows

S i i Separate into two sections Reserved Unreserved

If no Reserve or Allocation is made, remaining fund balance (net position) flows to Unreserved Unallocated

Totals on III 1 must match III Fund Unrestricted Net Totals on III-1 must match III-Fund Unrestricted Net Position by fund group

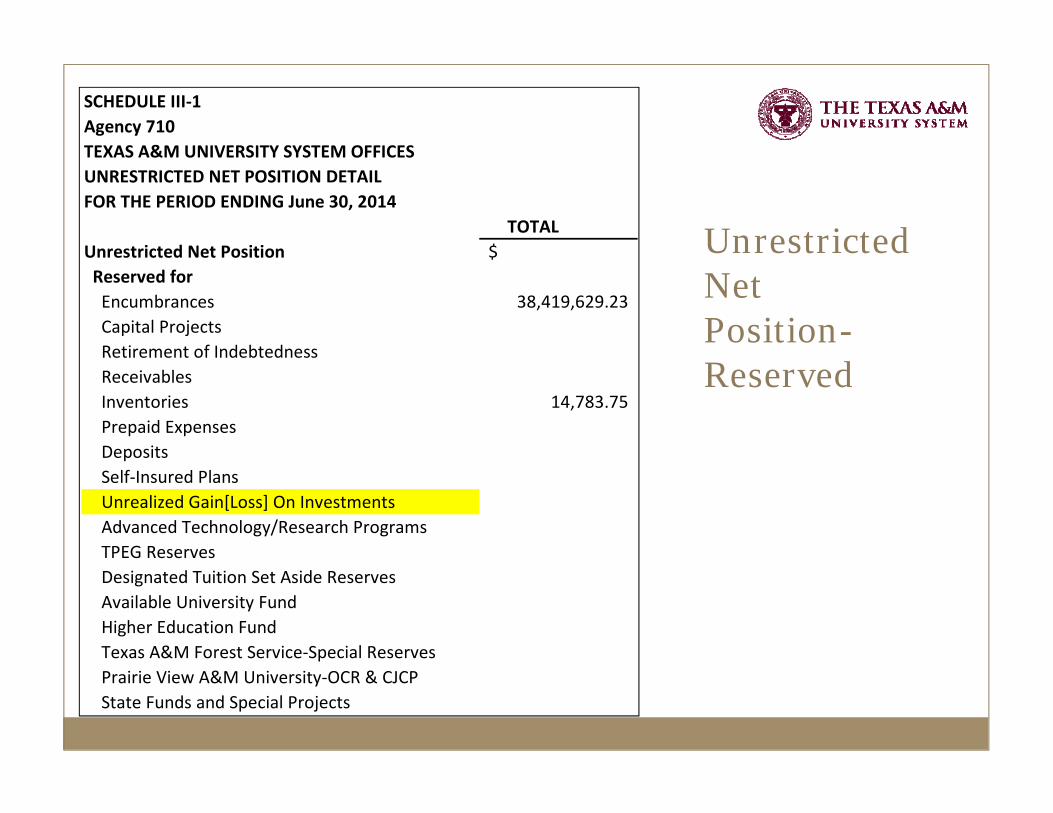

SCHEDULE III‐1 Agency 710 TEXAS A&M UNIVERSITY SYSTEM OFFICES

Unrestricted

TEXAS A&M UNIVERSITY SYSTEM OFFICES UNRESTRICTED NET POSITION DETAIL FOR THE PERIOD ENDING June 30, 2014

TOTAL Unrestricted Net Position $ Unrestricted

Net Position-

Unrestricted Net Position $ Reserved for Encumbrances 38,419,629.23 Capital Projects Retirement of Indebtedness

Reserved Retirement of Indebtedness Receivables Inventories 14,783.75 Prepaid Expenses Deposits p Self‐Insured Plans Unrealized Gain[Loss] On Investments Advanced Technology/Research Programs TPEG Reserves Designated Tuition Set Aside Reserves Available University Fund Higher Education Fund Texas A&M Forest Service‐Special Reserves Prairie View A&M University‐OCR & CJCP State Funds and Special Projects

III-1 Reserved

Group 1 – third-party claims against resources that do not qualify as liabilities Encumbrances

FAMIS encumbrance account controls 9610 9620 etc FAMIS encumbrance account controls 9610, 9620, etc. Capital Projects

Contracts entered into for construction projects, not yet b dencumbered

Retirement of Indebtedness Next year’s debt service transfer to System, net of appropriated y y , pp p

tuition revenue bond debt service funding

III-1 Reserved, cont’d.

Group 2 - Assets are not available for current appropriation or expenditure because of their non-monetary nature or lack of liquidity Receivables Receivables

Receivable balances, including Due from Other Members Exclude Loans & Contracts

Inventories - both consumable and merchandise Prepaid Expenses - goods & services paid in advance Deposits assets held by others such as a utility deposit Deposits – assets held by others, such as a utility deposit Self Insured Plans

Primarily System Offices reserves for Health/Dental plans Members may report UCI balances here (not much reserves)

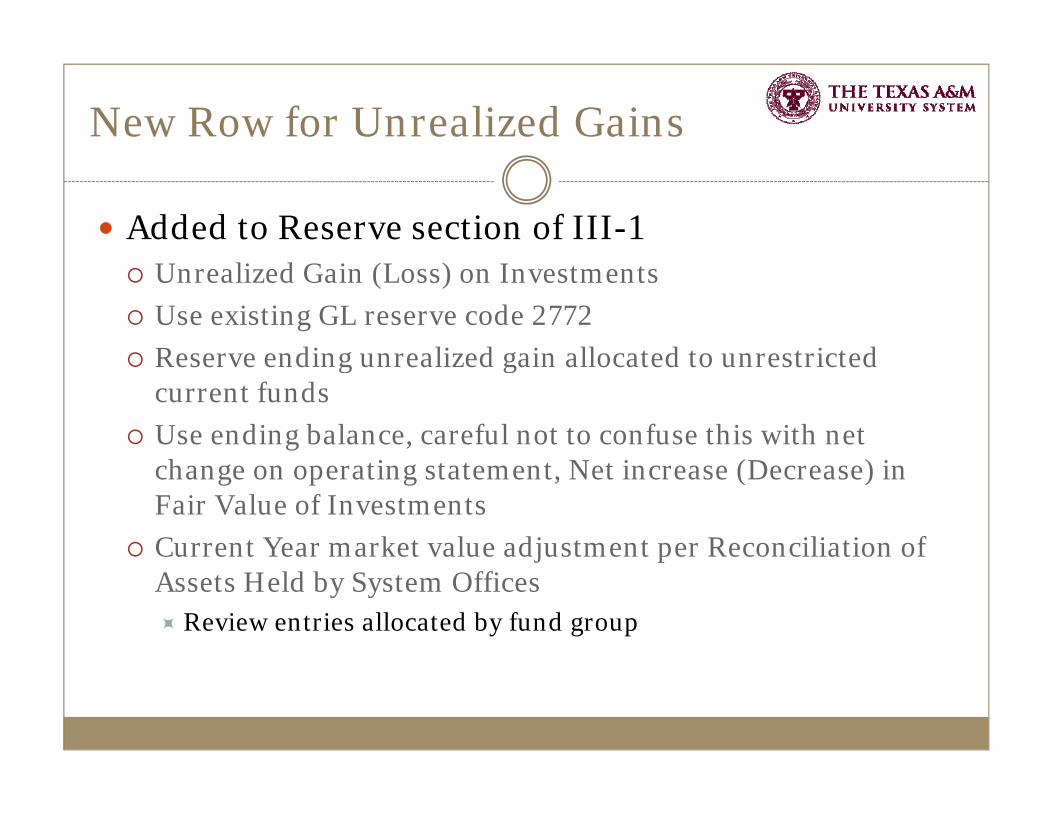

New Row for Unrealized Gains

Added to Reserve section of III-1 Unrealized Gain (Loss) on Investments Use existing GL reserve code 2772 Reserve ending unrealized gain allocated to unrestricted Reserve ending unrealized gain allocated to unrestricted

current funds Use ending balance, careful not to confuse this with net

h i i ( ) ichange on operating statement, Net increase (Decrease) in Fair Value of Investments

Current Year market value adjustment per Reconciliation of j pAssets Held by System Offices Review entries allocated by fund group

RECONCILIATION OF ASSETS HELD BY SYSTEM OFFICES (SO)AS OF AUGUST 31, 2013SYSTEM MEMBER: TAMUSSYSTEM MEMBER: TAMUS

CASHCONCENTRATION

POOL▪ Cash Concentration Pool Fund Ledgers:

8/31 Balance - Current Investments (Short Term) 102 202 753 92 Sample8/31 Balance - Current Investments (Short Term) 102,202,753.928/31 Balance - Non-Current Investments (Long Term) 95,567,330.23Total 197,770,084.15

YE Adjustments - Short Term (ST):ST July Bank Charges (634 54)

SampleReconciliation of Assets Held by System, showing ST July Bank Charges (634.54)

ST Realized LossST August Interest/Dividend Earnings 11,103.704th Quarter SEF Income Distribution 1,243,379.94

System, showing CurrentYear marketvalue

YE Adjustments - Long Term (LT):LT August Interest/Dividend Earnings 122,089.89LT August Realized Gain (Loss) (15,038.93)LT August Gain (Loss) on Sale of UnitsLT August External Manager Fees (22 230 92)

adjustment, or Unrealized Gains

LT August External Manager Fees (22,230.92)

Total Assets Held by SO - Book Value 199,108,753.29

Adjustment for Fair Value Increase (Decrease) 7,197,932.49

Total Assets Held by SO - Market Value 206,306,685.78

Fund Group Amount

Designated 6,556,493.57Review activity in account controls 4008/4009, and subcode 0355, to

Restricted 553,270.10

Agency 88,168.82

Total 7,197,932.49

4 /4 9, 355,identify Unrestricted Current Funds portion of Unrealized Gain/Loss to reserve on III-1

III-1 Reserved, cont’d.

Group 3 - Balances with state imposed limitationsd d h l h Advanced Technology/Research Programs

Designated Tuition Set Aside Reserves Used for grants to students, not for general operations Used for grants to students, not for general operations

TPEG should match TPEG Worksheet Exclude amounts already reserved as Prepaid ExpensesA il bl U i i F d (AUF) Available University Fund (AUF)

Higher Education Fund, unencumbered HEF balances Texas A&M Forest Service-Special Reserve Texas A&M Forest Service Special Reserve Prairie View – OCR & CJCP State Funds and Special Projects

Intended for specific expenses, not for general operations

III-1 Unrestricted Net PositionUnreservedUnreserved

SCHEDULE III‐1 Agency 710Agency 710 TEXAS A&M UNIVERSITY SYSTEM OFFICES UNRESTRICTED NET POSITION DETAIL FOR THE PERIOD ENDING June 30, 2014 Allocated Allocated for Operations Funds Functioning As Endowments 234,981,552.79

Research/Sponsored Project Commitments Research/Sponsored Project Commitments Endowment Commitment Faculty/Researcher/Staff Capital Plan and Major Purchases Maintenance and Repair Other Unallocated 122,783,777.94 Total Unrestricted [III‐Fund Unrestr Net Position] 396,199,743.71$ [ ] , ,$

Unreserved - Allocated

Amounts reported on these rows are more user defined, the methodologies used will vary Document allocation amounts when possible

All ti f l d h t d t t d Allocations for planned purchases not under contract, and not yet encumbered

Allocated for Operationsp Funds for next year’s operating budget, used to cover

budget costs greater than estimated revenue

F d F i i E d Funds Functioning as Endowments Unrestricted Quasi-Endowments, including related

Appreciation Reserve and market value adjustmentAppreciation Reserve and market value adjustment

Unreserved – Allocated, cont’d.

Research/Sponsored Project Commitments Matching funds internally committed as part of a sponsored

project grant

Endowment Commitment Endowment Commitment Faculty/Researcher/Staff Internal commitment to meet faculty reinvestment goals Internal commitment to meet faculty reinvestment goals

Capital Plan and Major Purchases Capital projects and funds set aside for major purchasesp p j j p

Maintenance and Repair Other

Unreserved - Unallocated

UnAllocated Remaining fund balance after reserved and allocated Remaining fund balance after reserved and allocated

balances

Allocated for Operations is combined with UnAllocated for the purposes of analyzing how many months reserves could support operationspp p Review balances Are new Reserve or Allocation categories needed on III-1?

If Unallocated balance is negative, Allocated section should be zero

FAMIS Reservation Codes

GL accounts controls and SL subcodes used to reserve or allocate balances Chapter 8 of AFR Instructions provides list

SL ti d SL reservation codes, 9450-9499 Budget entries, no actuals Excludes from budget available Excludes from budget available Generates GL entry to related account control

GL reservation codes, 2758-27969 Some entries generate from SL codes Year-End fund balance reclassification entries, offset to

5700 (such as Receivables)5700 (such as Receivables)

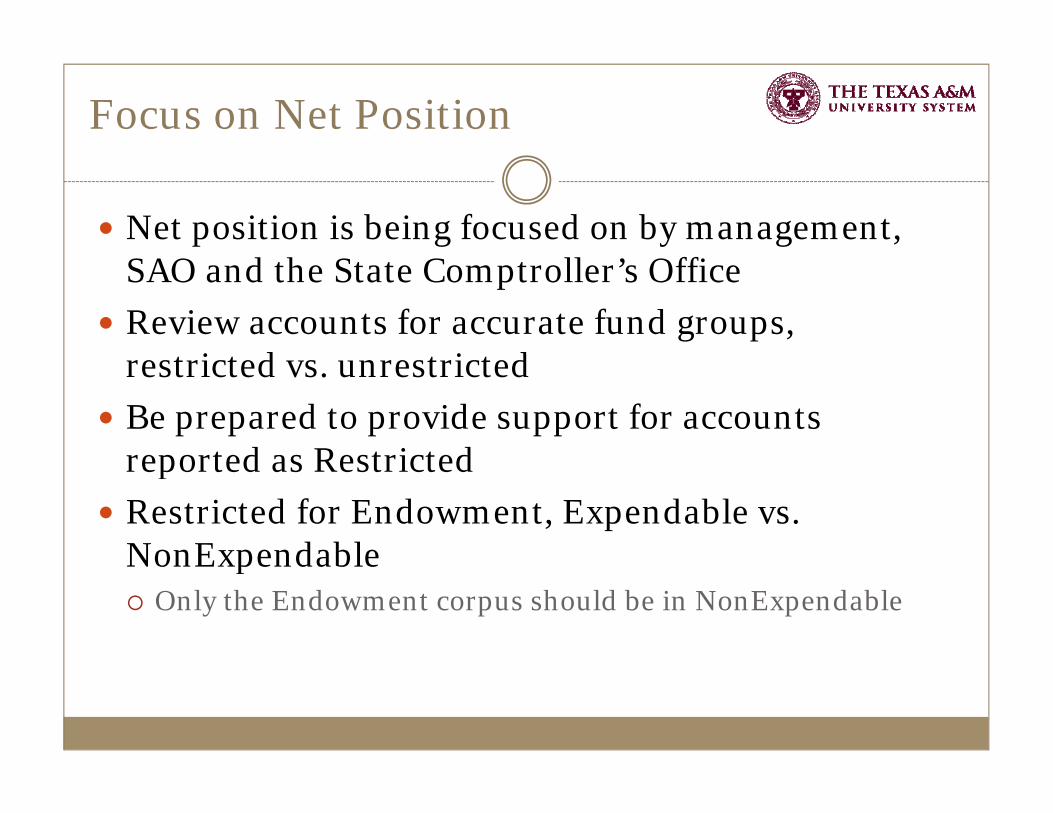

Focus on Net Position

Net position is being focused on by management, SAO and the State Comptroller’s Office

Review accounts for accurate fund groups, t i t d t i t drestricted vs. unrestricted

Be prepared to provide support for accounts reported as Restrictedreported as Restricted

Restricted for Endowment, Expendable vs. NonExpendableNonExpendable Only the Endowment corpus should be in NonExpendable

NACUBO Function Reporting

Teresa Bass, CPA

NACUBO Functions

Initially appeared 1968 of College & University y pp 9 g yBusiness Administration (CUBA)

NACUBO adopted these definitions in the Financial Accounting and Reporting Manual (FARM)

Functions used in the Integrated Post secondary Ed i D S (IPEDS) i f Education Data System (IPEDS)-primary source for data on colleges & universities

NACUBO Functions

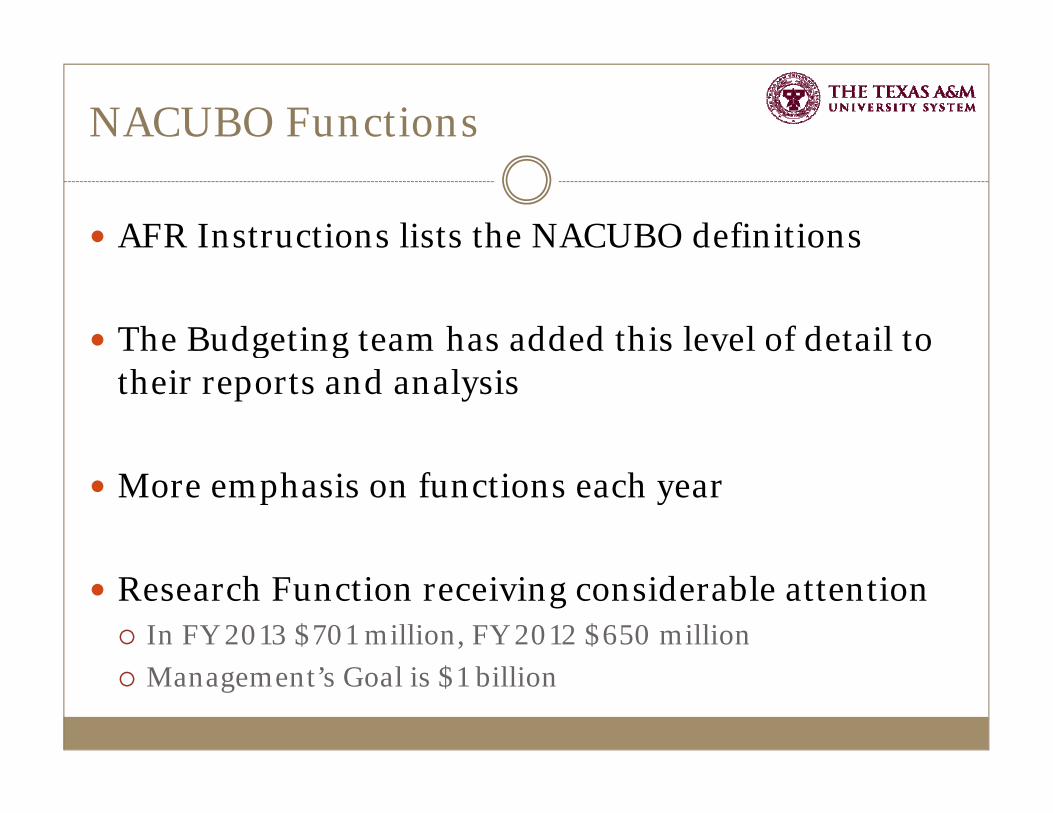

AFR Instructions lists the NACUBO definitions

The Budgeting team has added this level of detail to g gtheir reports and analysis

More emphasis on functions each year

Research Function receiving considerable attention In FY 2013 $701 million, FY 2012 $650 million Management’s Goal is $1 billion

Changes in FY 2014

Ensure Service Centers are classified in the correct function, no longer acceptable to just record in Institutional Support

Added text in the AFR Instructions for the Instruction Function Adult classes that do not lead to a certification or can be used Adult classes that do not lead to a certification or can be used

as credits for a degree should be recorded in Public Support AgriLife Extension Service analyzed their activity and

determined some of their activity needs to moved to Public Support

For institutes or centers all costs with that center can For institutes or centers all costs with that center can be placed in the Research function

NACUBO Article

NACUBO Article in the February Business Officer Maga ineMagazine Page 23 states that the Accounting Principles Committee is

considering recommending to consolidate functions down to g gjust six to make institutions more comparable. Allocating O&M and Depreciation to the most appropriate function.

Education and General Education and General-Instruction - Student Services-Research -Institutional Support-Public Service -Scholarships & FellowshipsPublic Service Scholarships & Fellowships-Academic Support

Auxiliaries Hospitals Hospitals Independent Operations

Issues

NACUBO Guidelines are flexible; GASB has not ;weighed in on this issue The definitions provide general guidelines but then allow for

adjustmentsadjustments

Institutions are evaluated nationally by these functionsy y

National Center for Educational Statistics Integrated Post Secondary Education Data System (IPEDs) ReportingSecondary Education Data System (IPEDs) Reporting

Issues

Operations & Maintenance function is probably p p yunderstated This is in line with some other Texas Universities, but not UT

di h b b d i d d h Depending on how members are budgeting depends on where the O&M is recorded, FY 2013 $229 million

IPEDs has us allocate these costs (based upon salary or square ( p y qfootage)

NACUBO article says they might eliminate these costs F&A rate won’t be impacted as we pull these costs out of the F&A rate won t be impacted, as we pull these costs out of the

function based upon the object code More research is needed on this topic

What can we do differently?

This is a project for next year and the Accounting p j y gteam would like to review our definitions and compare them to other universities, or at least

t i b t A&M bcompare topics between A&M members

A th th ld h? Are there are other areas we could research?

R h F i i i ? Research Function is important, any concerns?

OMB Uniform Guidance Update

Teresa Bass, CPA

Overview

Biggest Change in the last 50 years to Research gg g 5 yAdministration

Office of Management & Budget (OMB) Changes To Be Implemented December, 2014

Consolidates A-87, A-21 and A-122 Adds some confusion since Higher Ed/State agencies different

than local governments

All Federal Agencies have to provide their plan to All Federal Agencies have to provide their plan to OMB by December Federal Agencies are implementing the OMB requirements

differently

Changes

Program Income-Patents and licenses are now greported as program income Reduce Revenue for PI

i j / /li Ensure can tie project/grant to patent/license revenue

Procurement Standards new burden (BIG) Anything over $3k requires quotes Anything over $3k requires quotes Increase time Increase HUB

Fixed Award Contract requires approval if over $150k

Changes

Depreciation Cost Share must be considered and preduce the F&A Proposal In the Past, if purchased with Fed funds marked in FFX and we

ensure we do not charge the Feds for depreciation now need ensure we do not charge the Feds for depreciation, now need to track cost sharing costs on Fed funded buildings (BARDA)

Can directly charge the grant for exchange rates y g g g Discourage agency deviations from the F&A Rate If Feds reduce the rate we can notify OMB OMB will track these

Confirmed Voluntary Cost Share not a factor

Changes

Computing devices can be charged directly to grantsp g g y g Short-form schools still at $10 million, there was

debate on increasing the threshold TAMUCC will be converted in FY 2014

Close outs could take longer, more costs allowed Admin & Clerical staff can be charged directly to

grants, but cannot be included in the F&A Rate Already had this issue with major projects where admin costs Already had this issue with major projects where admin costs

were charged directly, exclusions can be made in the F&A proposal

F&A Proposal Changes

F&A Proposal Impactll dd l All universities get to add Utility Cost

Remove Admin & Clerical costs charged directly Extensions can be granted, give rate for an additional 4 years Extensions can be granted, give rate for an additional 4 years Participant Support costs removed from MTDC base Can not use depreciation on fully depreciated assets Depending on impact of Fringe Benefits Consider Cost Sharing costs to build Federally funded

buildingsbuildings

DS-2 Disclosure Stmt Changes

DS-2-required for proposals over $25 million-Only C ll St ti B h i DSCollege Station Base has issue a DS-2 Dates Threshold raised to $50 million Threshold raised to $50 million Changes must be submitted 6 months prior to making the

operational changei fi Fringe Benefits

Procurement Depreciation Depreciation Utility Allocation

Procurement & Fringe Benefits

COGR Letter Dated June 17th Raised these two issues 7as significant burdens asked for a change

Procurement changes-too prescriptive IT Changes Required Not Following state thresholds/rules Increase the time to purchase a supply/tool Increase the time to purchase a supply/tool

Fringe Benefits in some circumstances are treated as indirect costindirect cost Accounting Violation Potential Change to Accounting Systems Impact to F&A Proposal

Next Steps

Michele Lacey’s workgroup summarizing the impact y g p g pfor A&M members

Review Processes

Wait for additional guidance

Keep attending webinars

Additional Insight

Open forump

Go around the room and discuss Biggest concern by each agency & campus How to implement

i l i Potential impacts

Adjourn

Final Questions?

Closing Comments

Day 2 will begin at 8:30am FAMIS Year-End processing AFR Module Basics Cash Flow Statement Workpaper Cash Flow Statement Workpaper

Thank you for attending!Thank you for attending!

Agenda - Wednesday, August 6th

Time Topic Presenter

8:30 Introduction/Previous Day Questions Teresa Bass

8:45 FAMIS Year-End Processing Melissa Ray

10:30 AFR Module Basics Tracy Crowley

11 15 C h Fl St t t W k T B11:15 Cash Flow Statement Workpaper Teresa Bass

Noon Adjourn/Closing Comments Teresa Bass

dIntroduction/Previous Day QuestionsQuestions

Teresa Bass, CPAComptroller

Texas A&M System OfficeTexas A&M System Office

FAMIS Year-End Processing

Melissa RayLead Software Support Analyst

FAMIS ServicesFAMIS Services

15 Minute Break

AFR Module BasicsAFR Module Basics

Tracy CrowleySenior Manager of Financial Reporting

Texas A&M System OfficeTexas A&M System Office

AFR Module

Accessing the AFR moduleg Log into FAMIS and type “AFR” in the Screen field

Navigation Use Screen 882 to change the fiscal year or campus code

(defaults to current year)(defaults to current year)

Main Menu Screen 001 Useful to find screen numbers

View PF keys at bottom of screens for cues View PF keys at bottom of screens for cues

AFR Module ScreensAFR Module Screens

AFR Module Key Screensy Screen 172 – Print Group Reports Screen 175 – Defines report columns

S D fi Screen 179 – Defines report rows Screen 180 – Manual entries, queries, updates Screen 193 – Manual entry summaryScreen 193 Manual entry summary Screen 194 – Report print status

Screen 172 Print Group Reports

Generate a complete set of AFR reportsk l Use F8 key to view GASB reports; select ‘X’ to print ALL

Month = 13 for year-end (Calendar months, 4 = April, etc.) Other fields – leave default values Change print priority from 3 to 4 to print immediately Always leave report specifications blank

Select F9 to print to default printerSelect F9 to print to default printer

OR Select Specific Reports to Run/Print Select from GASB Reports or User Reports using F8 or F10 Pop up box will prompt to run pre-requisites Selected reports are marked with an ‘X’ All pre-requisites should be run p e equ s tes s ou d be u

Screen 172 Print Selected Reports

Can omit printing step for pre-requisites by changing ‘X’ to ‘R’ for Run Only

Screen 172 Priority Field Default is Priority 3 Requests remain in queue until next priority 3 print window (before

9am, noon, or after 4pm

For urgent requests, change to Priority 4

View Status of Print Jobs

Screen 194 –View Report Print Status O-Open request O-Open request R-Running Report C-Complete and in print queue

AFR Module Report Inquiry

Report inquiry screens M l E t S 193 Manual Entry Summary