10 january 2018 india reliance … profile... · reliance communications ... rcom in september 2016...

TRANSCRIPT

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

10 January 2018

Debtwire.com

India

BankruptcyProfile

Reliance Communications Limited

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com Page 2

India Bankruptcy Profile | 10-Jan-18

Reliance Communications Limited

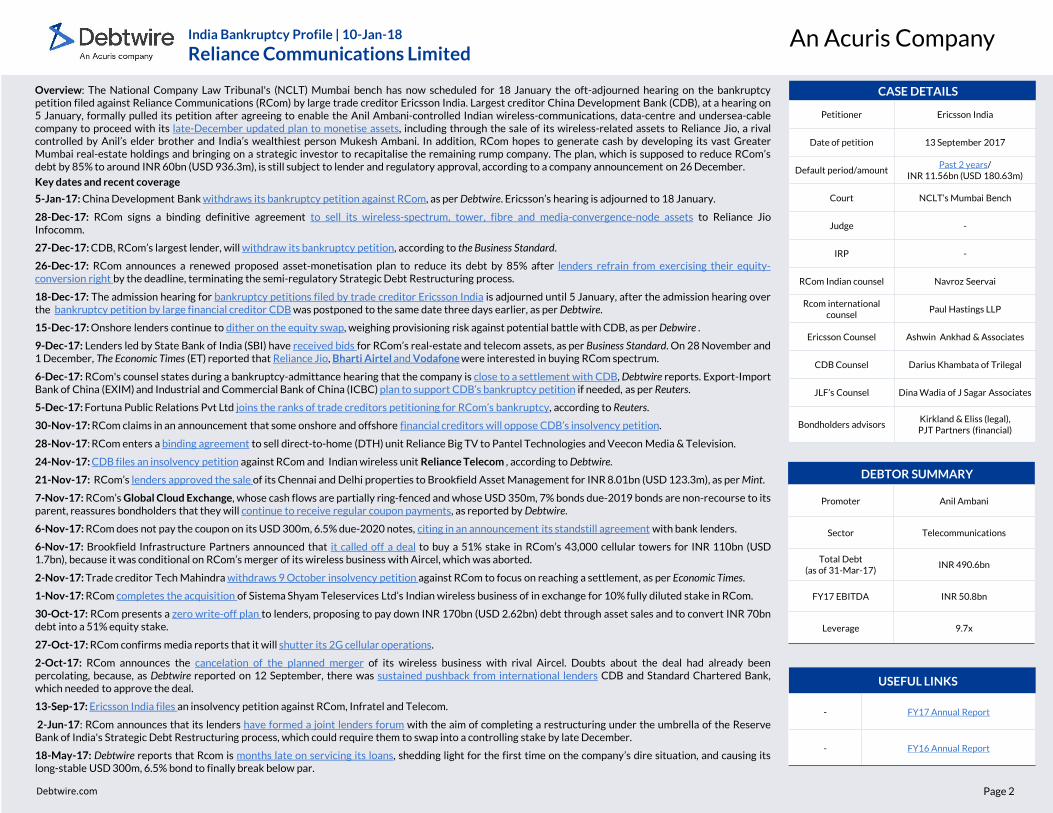

CASE DETAILS

Petitioner Ericsson India

Date of petition 13 September 2017

Default period/amountPast 2 years/

INR 11.56bn (USD 180.63m)

Court NCLT’s Mumbai Bench

Judge -

IRP -

RCom Indian counsel Navroz Seervai

Rcom international counsel

Paul Hastings LLP

Ericsson Counsel Ashwin Ankhad & Associates

CDB Counsel Darius Khambata of Trilegal

JLF’s Counsel Dina Wadia of J Sagar Associates

Bondholders advisorsKirkland & Eliss (legal), PJT Partners (financial)

DEBTOR SUMMARY

Promoter Anil Ambani

Sector Telecommunications

Total Debt(as of 31-Mar-17)

INR 490.6bn

FY17 EBITDA INR 50.8bn

Leverage 9.7x

Overview: The National Company Law Tribunal's (NCLT) Mumbai bench has now scheduled for 18 January the oft-adjourned hearing on the bankruptcypetition filed against Reliance Communications (RCom) by large trade creditor Ericsson India. Largest creditor China Development Bank (CDB), at a hearing on5 January, formally pulled its petition after agreeing to enable the Anil Ambani-controlled Indian wireless-communications, data-centre and undersea-cablecompany to proceed with its late-December updated plan to monetise assets, including through the sale of its wireless-related assets to Reliance Jio, a rivalcontrolled by Anil’s elder brother and India’s wealthiest person Mukesh Ambani. In addition, RCom hopes to generate cash by developing its vast GreaterMumbai real-estate holdings and bringing on a strategic investor to recapitalise the remaining rump company. The plan, which is supposed to reduce RCom’sdebt by 85% to around INR 60bn (USD 936.3m), is still subject to lender and regulatory approval, according to a company announcement on 26 December.

Key dates and recent coverage

5-Jan-17: China Development Bank withdraws its bankruptcy petition against RCom, as per Debtwire. Ericsson’s hearing is adjourned to 18 January.

28-Dec-17: RCom signs a binding definitive agreement to sell its wireless-spectrum, tower, fibre and media-convergence-node assets to Reliance JioInfocomm.

27-Dec-17: CDB, RCom’s largest lender, will withdraw its bankruptcy petition, according to the Business Standard.

26-Dec-17: RCom announces a renewed proposed asset-monetisation plan to reduce its debt by 85% after lenders refrain from exercising their equity-conversion right by the deadline, terminating the semi-regulatory Strategic Debt Restructuring process.

18-Dec-17: The admission hearing for bankruptcy petitions filed by trade creditor Ericsson India is adjourned until 5 January, after the admission hearing overthe bankruptcy petition by large financial creditor CDB was postponed to the same date three days earlier, as per Debtwire.

15-Dec-17: Onshore lenders continue to dither on the equity swap, weighing provisioning risk against potential battle with CDB, as per Debwire .

9-Dec-17: Lenders led by State Bank of India (SBI) have received bids for RCom’s real-estate and telecom assets, as per Business Standard. On 28 November and1 December, The Economic Times (ET) reported that Reliance Jio, Bharti Airtel and Vodafone were interested in buying RCom spectrum.

6-Dec-17: RCom's counsel states during a bankruptcy-admittance hearing that the company is close to a settlement with CDB, Debtwire reports. Export-ImportBank of China (EXIM) and Industrial and Commercial Bank of China (ICBC) plan to support CDB’s bankruptcy petition if needed, as per Reuters.

5-Dec-17: Fortuna Public Relations Pvt Ltd joins the ranks of trade creditors petitioning for RCom’s bankruptcy, according to Reuters.

30-Nov-17: RCom claims in an announcement that some onshore and offshore financial creditors will oppose CDB’s insolvency petition.

28-Nov-17: RCom enters a binding agreement to sell direct-to-home (DTH) unit Reliance Big TV to Pantel Technologies and Veecon Media & Television.

24-Nov-17: CDB files an insolvency petition against RCom and Indian wireless unit Reliance Telecom , according to Debtwire.

21-Nov-17: RCom’s lenders approved the sale of its Chennai and Delhi properties to Brookfield Asset Management for INR 8.01bn (USD 123.3m), as per Mint.

7-Nov-17: RCom’s Global Cloud Exchange, whose cash flows are partially ring-fenced and whose USD 350m, 7% bonds due-2019 bonds are non-recourse to itsparent, reassures bondholders that they will continue to receive regular coupon payments, as reported by Debtwire.

6-Nov-17: RCom does not pay the coupon on its USD 300m, 6.5% due-2020 notes, citing in an announcement its standstill agreement with bank lenders.

6-Nov-17: Brookfield Infrastructure Partners announced that it called off a deal to buy a 51% stake in RCom’s 43,000 cellular towers for INR 110bn (USD1.7bn), because it was conditional on RCom’s merger of its wireless business with Aircel, which was aborted.

2-Nov-17: Trade creditor Tech Mahindra withdraws 9 October insolvency petition against RCom to focus on reaching a settlement, as per Economic Times.

1-Nov-17: RCom completes the acquisition of Sistema Shyam Teleservices Ltd’s Indian wireless business of in exchange for 10% fully diluted stake in RCom.

30-Oct-17: RCom presents a zero write-off plan to lenders, proposing to pay down INR 170bn (USD 2.62bn) debt through asset sales and to convert INR 70bndebt into a 51% equity stake.

27-Oct-17: RCom confirms media reports that it will shutter its 2G cellular operations.

2-Oct-17: RCom announces the cancelation of the planned merger of its wireless business with rival Aircel. Doubts about the deal had already beenpercolating, because, as Debtwire reported on 12 September, there was sustained pushback from international lenders CDB and Standard Chartered Bank,which needed to approve the deal.

13-Sep-17: Ericsson India files an insolvency petition against RCom, Infratel and Telecom.

2-Jun-17: RCom announces that its lenders have formed a joint lenders forum with the aim of completing a restructuring under the umbrella of the ReserveBank of India's Strategic Debt Restructuring process, which could require them to swap into a controlling stake by late December.

18-May-17: Debtwire reports that Rcom is months late on servicing its loans, shedding light for the first time on the company’s dire situation, and causing itslong-stable USD 300m, 6.5% bond to finally break below par.

USEFUL LINKS

- FY17 Annual Report

- FY16 Annual Report

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com Page 3

RISE, FALL AND SALVATION

Reliance Communications Limited (RCom) is a Maharashtra, India-headquartered wireless-communications, data-centre and undersea-cable company in the process of trying to monetise assets to ward off abankruptcy process. Once India’s second-largest wireless-communications player in what was expected to be a booming market, the company -- controlled by tycoon Anil Ambani -- is the most high-profile loser in thebrutal war for users that reached its apex with the aggressive entry into the space in September 2016 by Reliance Jio Infocomm (RJIO). Under a late-December definitive agreement, Jio will buy RCom’s wirelessassets, bringing the business back to its original corporate home – Reliance Industries, the conglomerate controlled by Anil’s big brother and frequent foil, Mukesh Ambani.

The sale is part of a revised monetisation plan RCom announced on Boxing Day 2017 that is supposed to reduce its debt to around INR 60bn (USD 936.3m) eventually, compared with INR 490.6bn (USD 7.56bn) as of31 March 2017. The announcement ended management’s desperate attempts for the past year to save the core wireless business. Following a Debtwire report in May that RCom was months late on servicing its loans,its lenders in early June formed a so-called Joint Lenders Forum with the aim of completing a restructuring by late December under the Reserve Bank of India's Strategic Debt Restructuring (SDR) process. Attempts tomerge the flagging wireless business with a rival’s and to sell the communications-tower business collapsed in October and November under the weight of objections from key creditors China Development Bank(CDB) and Standard Chartered Bank. Bankruptcy petitions from CDB and large trade creditor Ericsson India finally forced Anil’s hands.

Monetisation plan: RJIO will purchase most of RCom's assets, including 122.4 Mhz of 4G spectrum, around 43,000 towers, around 178,000 kilometres of fibre-optic cable, 248 media-convergence nodes, as per a 28December announcement that doesn’t state a price. Indian press have reported a price range of INR 200bn-INR 240bn (USD 3.12bn-USD 3.75bn). As part of the 26 December plan, RCom also intends to sell real estatein New Delhi, Chennai, Kolkata, Jigni and Tirupati. It expects the sale of the wireless and property assets will reduce its debt by INR 250bn (USD 3.93bn), according to the 26 December announcement.

RCom also plans to monetise its 125 acre IT Park in Navi Mumbai, which houses RCom’s network operations centre. The property, which is held by an SPV, is expected to be further developed after RCom finds apartner and eventually lead to an additional INR 100bn debt reduction.

Leftovers: The residual company will mainly comprise RCom’s internet data centres, its landline service catering to Indian enterprises and its submarine cable and data centre unit Global Cloud Xchange (GCX). GCX’scash flows are partially ring-fenced, as per the terms of its USD 350m secured due-2019 bonds, restricting dividends to RCom if debt-to-EBITDA is above 3.75x or if interest coverage is below 1.75x. Under the 26December plan, the rump company would be recapitalised by a strategic investor. Credit Suisse was appointed to find an investor, according to RCom.

How it got here: RCom was incorporated in July 2004 and then listed on the Indian stock exchanges on 6 March 2006, not long after being split off from Reliance Industries. The spin off was part of a deal between thefeuding Amabani brothers that divided the vast conglomerate built by their late father. In the years following the split, RCom experienced significant growth in revenue and profit, fuelled in part by eager borrowingand a rapidly growing market, sending the stock price soaring to an eventual peak of INR 803 in January 2008. The shares closed at INR 32.45 on 9 January.

The mix of debt and intense competition eventually caught up to RCom, particularly once Reliance Jio entered the market in September 2016 and began slashing prices. After a strong decade-long run following thesplit from Reliance Industries, RCom’s growth in revenue and EBITDA leveled off in FY14 through 31 March 2014, and then in FY17 the bottom fell out, with adjusted EBITDA declining 31% YoY to INR 50.8bn onrevenue that fell 11.2% YoY to INR 194.9bn. Free cash flow burn intensified, at negative INR 107bn versus negative INR 43.8bn in the year prior. The trend continued into 1H18, with revenue falling 41% YoY to INR61.1bn and EBITDA swinging to negative INR 0.8bn, a INR 31.1bn fall from the year-prior period.

To deal with the competition and liquidity challenges, RCom in September 2016 inked the ill-fated deals to merge its wireless business with struggling rival Aircel Ltd and in April 2017 agreed to sell of its tower assetsto Canadian alternative-asset manager Brookfield Infrastructure Partners. These transactions were supposed to help RCom reduce its debt by 60%. With completion of the deals dragging, RCom's bank lenders formeda Joint Lenders Forum with the purpose of putting the company through the Reserve Bank of India's so-called SDR process, which effectively gave management a late December deadline for finalising a resolution planor face the loss of control of the company. If that wasn’t pressure enough, bankruptcy petitions from CDB, Ericsson and some other trade creditors appears to have done the trick.

India Bankruptcy Profile | 10-Jan-18

Reliance Communications Limited

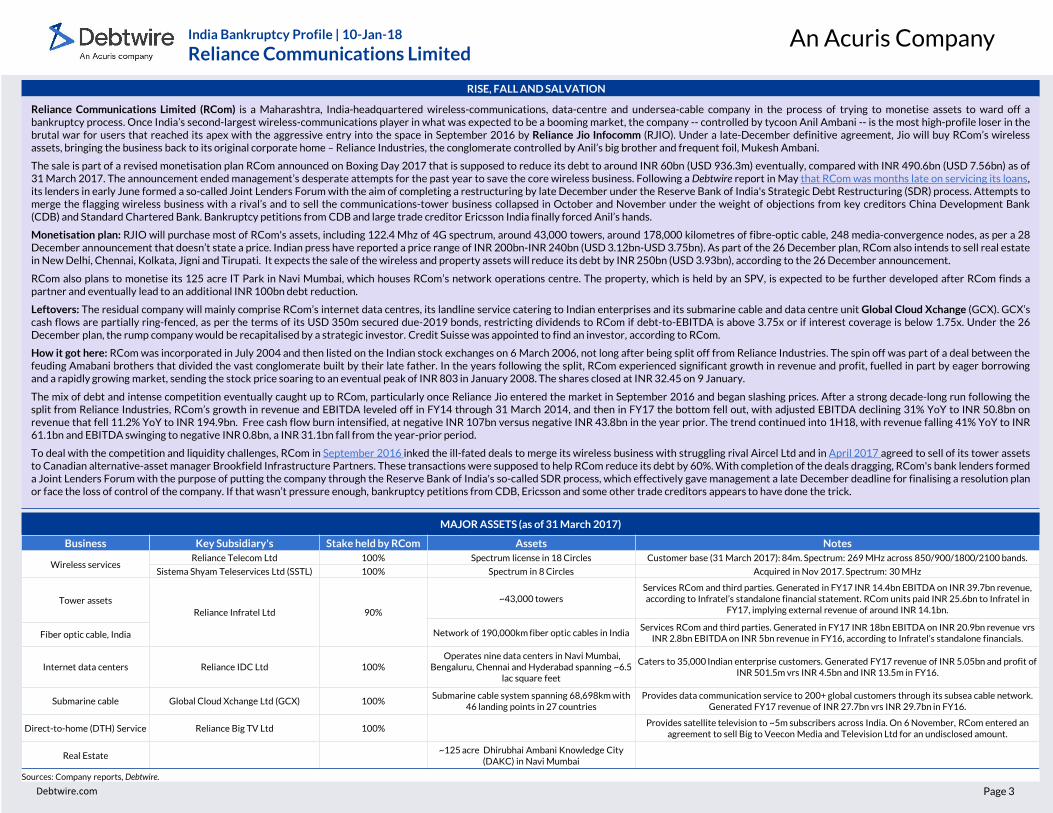

MAJOR ASSETS (as of 31 March 2017)

Business Key Subsidiary's Stake held by RCom Assets Notes

Wireless servicesReliance Telecom Ltd 100% Spectrum license in 18 Circles Customer base (31 March 2017): 84m. Spectrum: 269 MHz across 850/900/1800/2100 bands.

Sistema Shyam Teleservices Ltd (SSTL) 100% Spectrum in 8 Circles Acquired in Nov 2017. Spectrum: 30 MHz

Tower assets

Reliance Infratel Ltd 90%

~43,000 towersServices RCom and third parties. Generated in FY17 INR 14.4bn EBITDA on INR 39.7bn revenue,according to Infratel’s standalone financial statement. RCom units paid INR 25.6bn to Infratel in

FY17, implying external revenue of around INR 14.1bn.

Network of 190,000km fiber optic cables in IndiaServices RCom and third parties. Generated in FY17 INR 18bn EBITDA on INR 20.9bn revenue vrs

INR 2.8bn EBITDA on INR 5bn revenue in FY16, according to Infratel’s standalone financials. Fiber optic cable, India

Internet data centers Reliance IDC Ltd 100%Operates nine data centers in Navi Mumbai,

Bengaluru, Chennai and Hyderabad spanning ~6.5 lac square feet

Caters to 35,000 Indian enterprise customers. Generated FY17 revenue of INR 5.05bn and profit of INR 501.5m vrs INR 4.5bn and INR 13.5m in FY16.

Submarine cable Global Cloud Xchange Ltd (GCX) 100%Submarine cable system spanning 68,698km with

46 landing points in 27 countriesProvides data communication service to 200+ global customers through its subsea cable network.

Generated FY17 revenue of INR 27.7bn vrs INR 29.7bn in FY16.

Direct-to-home (DTH) Service Reliance Big TV Ltd 100%Provides satellite television to ~5m subscribers across India. On 6 November, RCom entered an

agreement to sell Big to Veecon Media and Television Ltd for an undisclosed amount.

Real Estate~125 acre Dhirubhai Ambani Knowledge City

(DAKC) in Navi Mumbai

Sources: Company reports, Debtwire.

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com Page 4

Issuer group security providers of the due-2020 notes

Restricted subsidiaries under RCom’s due-2020 notes

RELIANCE COMMUNICATION LTD(1)(2)

—Wireless and other telecom operations

Reliance Communication Inc. (USA) (100%)- Int’l voice & data

services

GCX Limited(Bermuda) (100%)

-Investment Holding

USD 300m 6.5% senior secured notes due 2020

21.20%

99%

10.74%

79.71%

Reliance Big TV Limited (100%)

- Direct o Home (DTH)

Reliance Webstore Limited (100%)

- Trading & Marketing

Reliance IDC Limited (100%)

- Internet data centers

Reliance InfocommInfrastructure

Limited(3) (100%) -Investment Holding

Reliance Telecom Limited(1)(3)

- Wireless operation

Reliance Communications Infrastructure Limited(1)

(100%) -Investment Holding

Reliance InfratelLimited(1)

- Telecom tower and Optic fiber cable

Reliance Globalcom BV (The Netherlands)

(100%)-Investment Holding

Global Cloud Xchange Limited (Bermuda)

(100%)-Investment Holding

78.80%

USD 350m 7.0% senior secured notes due 2019

Anil D. Ambani & family and other promotor group

(53.08%)

Life Insurance Corporation of India

(5.97%)

Sistema ShyamTeleservices Ltd (SSTL)

(Person acting in Concert) (10.02%)

Other shareholders (29.40%)

CLSA Global Markets PTE Ltd (1.53%)

Reliance GlobalcomLimited

(Bermuda) (99.965%)- Investment Holding

FLAG Telecom Group Services Limited

(Bermuda) (100%)- Investment Holding

Restricted group under GCX’s due-2019 notes

Flag Telecom Group- Capacity leasing and

internet protocol

Vanco Group- Capacity leasing and

internet protocol

Collaterals for the due-2020 notes:(1) Charge over present and future movables of RCom, Reliance Telecom Limited, Reliance Infratel Limited and Reliance Communications Infrastructure Limited(2) Assignment of 20 unified access service licenses and one national long distance and one International long distance license of RCom(3) Pledge of entire shareholding of Reliance Telecom Limited and Reliance Infocomm Infrastructure Limited held by RCom

Source: Offering circular of USD 300m 6.5% senior secured notes dated 27 April 2015

Indian Subsidiaries

Overseas Subsidiaries

On 6 November, RComentered into an agreementwith Veecon Media andTelevision Ltd for sale of it'sDTH business for anundisclosed amount.

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com Page 5

Organization structure of GCX Group

GCX Limited (Bermuda)

Reliance GlobalcomBV

(Netherlands)

Global Cloud Xchange Limited

(Bermuda)

USD 350m 7.0% senior secured notes due 2019

Reliance GlobalcomLimited

(Bermuda)

GCX Services Limited (Bermuda)

FLAG Telecom Group Services Limited

(Bermuda)

Reliance Globalcom

(UK) Limited (UK)

FLAG Atlantic UK

Limited (UK)

FLAG Telecom

Asia Limited (Hong Kong)

Reliance Globalcom

Limited (India)

Reliance FLAG

Atlantic France SAS

(France)

FLAG Telecom

Singapore Pte Limited (Singapore)

Seoul Telenet Inc. (49%)

(South Korea)

FLAG Telecom Taiwan Limited

(Taiwan)FLAG

Telecom Netherland

B.V. (Netherlands)

FLAG Telecom

Deutschland GmbH

(Germany)

FLAG Telecom

Development Limited

(Bermuda)

FLAG Holdings (Taiwan) Limited (50%) (Taiwan)

FLAG Telecom Network Services Limited (Ireland)

Reliance FLAG Telecom Ireland Limited (Ireland)

FLAG Telecom Ireland Network Limited (Ireland)

FLAG Telecom Network USA

Limited (Delware)

FLAG Telecom Development

Services Company LLC

(Egypt)

FLAG Telecom Espana Network

SAU (Spain)

FLAG Telecom Japan Limited

(Japan)

80%20%

0.01%99.99%

1%99%

FLAG Telecom

Hellas AE (Greece)

Reliance Vanco Group Limited (UK)

VancoGmbH

(Germany)VNO Direct

Limited (UK)

Vanco UK Limited (UK)

Vanco Australasia Pty Limited (Australia)

Vanco US, LLC (Delaware)

VancoDeutschland

GmbH (Germany)

VancoSolutions Inc.

(Delware)

Vanco South America Ltda

(Brazil)

Vanco SpZoo(Poland)

Vanco NV (Belgium)

Vanco Japan KK (Japan)

Vanco (Shanghai) Co., Ltd (China)

Vanco SAS (France)

Vanco Global Limited (UK)

Vanco BV (Holland)

Vanco ROW Limited (UK)

Vanco Asia Pacific PTE

Limited (Singapore

VancoInternational Limited (UK)

VancoSwitzerland A.G.

(Switzerland)

VancoBenelux BV

(Netherlands)

Net Direct SA (Proprietary)

Ltd. (South Africa)

Vanco Srl (Italy)

Euronet Spain SA

(Spain)

VancoSweden AB

(Sweden)

Subsidiary guarantors* under USD 350m due-2019 notes

Restricted group under USD 350m due-2019 notes

* cash, trade receivables and fixed assets of subsidiary guarantors are pledged to the notes

Source: Offering circular of GCX’s USD 350m 7% senior secured bonds due-2019Note: all shareholdings are at least 99.9% unless otherwise stated.

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com Page 6

India Bankruptcy Profile | 10 -Jan-18

Reliance Communications Limited

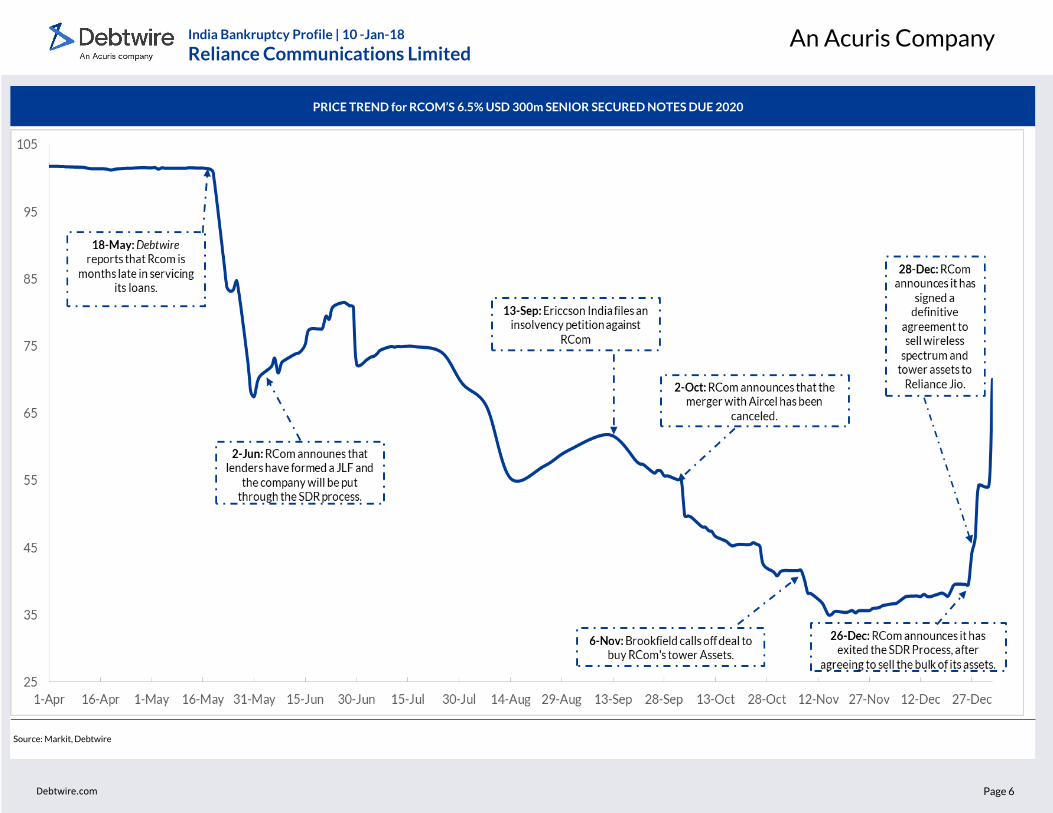

PRICE TREND for RCOM’S 6.5% USD 300m SENIOR SECURED NOTES DUE 2020

Source: Markit, Debtwire

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com Page 7

India Bankruptcy Profile | 10-Jan-18

Reliance Communications Limited

CONTACT INFORMATION

Luc Mongeon Managing Editor, Asia Pacific

+65 6349 8054 [email protected]

Chaim Estulin Senior Editor, Asia Pacific

+852 2158 9725 [email protected]

Ryan PatwellHead of Research, Asia Pacific

+852 2158 [email protected]

Rajiv SavardekarSenior Credit Analyst, Asia Pacific

Anjali AgarwalCredit Analyst, Asia Pacific

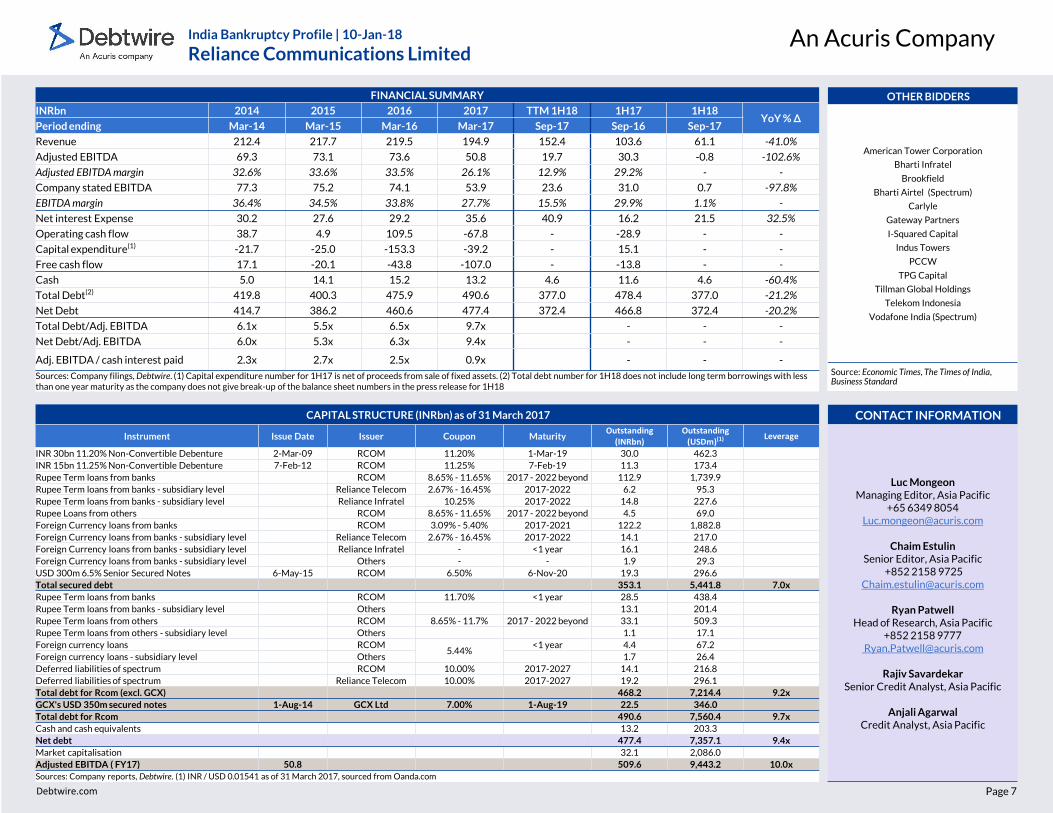

FINANCIAL SUMMARY

INRbn 2014 2015 2016 2017 TTM 1H18 1H17 1H18YoY % ∆

Period ending Mar-14 Mar-15 Mar-16 Mar-17 Sep-17 Sep-16 Sep-17

Revenue 212.4 217.7 219.5 194.9 152.4 103.6 61.1 -41.0%

Adjusted EBITDA 69.3 73.1 73.6 50.8 19.7 30.3 -0.8 -102.6%

Adjusted EBITDA margin 32.6% 33.6% 33.5% 26.1% 12.9% 29.2% - -

Company stated EBITDA 77.3 75.2 74.1 53.9 23.6 31.0 0.7 -97.8%

EBITDA margin 36.4% 34.5% 33.8% 27.7% 15.5% 29.9% 1.1% -

Net interest Expense 30.2 27.6 29.2 35.6 40.9 16.2 21.5 32.5%

Operating cash flow 38.7 4.9 109.5 -67.8 - -28.9 - -

Capital expenditure(1) -21.7 -25.0 -153.3 -39.2 - 15.1 - -

Free cash flow 17.1 -20.1 -43.8 -107.0 - -13.8 - -

Cash 5.0 14.1 15.2 13.2 4.6 11.6 4.6 -60.4%

Total Debt(2) 419.8 400.3 475.9 490.6 377.0 478.4 377.0 -21.2%

Net Debt 414.7 386.2 460.6 477.4 372.4 466.8 372.4 -20.2%

Total Debt/Adj. EBITDA 6.1x 5.5x 6.5x 9.7x - - -

Net Debt/Adj. EBITDA 6.0x 5.3x 6.3x 9.4x - - -

Adj. EBITDA / cash interest paid 2.3x 2.7x 2.5x 0.9x - - -

Sources: Company filings, Debtwire. (1) Capital expenditure number for 1H17 is net of proceeds from sale of fixed assets. (2) Total debt number for 1H18 does not include long term borrowings with less than one year maturity as the company does not give break-up of the balance sheet numbers in the press release for 1H18

CAPITAL STRUCTURE (INRbn) as of 31 March 2017

Instrument Issue Date Issuer Coupon MaturityOutstanding

(INRbn)Outstanding

(USDm)(1) Leverage

INR 30bn 11.20% Non-Convertible Debenture 2-Mar-09 RCOM 11.20% 1-Mar-19 30.0 462.3

INR 15bn 11.25% Non-Convertible Debenture 7-Feb-12 RCOM 11.25% 7-Feb-19 11.3 173.4

Rupee Term loans from banks RCOM 8.65% - 11.65% 2017 - 2022 beyond 112.9 1,739.9

Rupee Term loans from banks - subsidiary level Reliance Telecom 2.67% - 16.45% 2017-2022 6.2 95.3

Rupee Term loans from banks - subsidiary level Reliance Infratel 10.25% 2017-2022 14.8 227.6

Rupee Loans from others RCOM 8.65% - 11.65% 2017 - 2022 beyond 4.5 69.0

Foreign Currency loans from banks RCOM 3.09% - 5.40% 2017-2021 122.2 1,882.8

Foreign Currency loans from banks - subsidiary level Reliance Telecom 2.67% - 16.45% 2017-2022 14.1 217.0

Foreign Currency loans from banks - subsidiary level Reliance Infratel - <1 year 16.1 248.6

Foreign Currency loans from banks - subsidiary level Others - - 1.9 29.3

USD 300m 6.5% Senior Secured Notes 6-May-15 RCOM 6.50% 6-Nov-20 19.3 296.6

Total secured debt 353.1 5,441.8 7.0x

Rupee Term loans from banks RCOM 11.70% <1 year 28.5 438.4

Rupee Term loans from banks - subsidiary level Others 13.1 201.4

Rupee Term loans from others RCOM 8.65% - 11.7% 2017 - 2022 beyond 33.1 509.3

Rupee Term loans from others - subsidiary level Others 1.1 17.1

Foreign currency loans RCOM5.44%

<1 year 4.4 67.2

Foreign currency loans - subsidiary level Others 1.7 26.4

Deferred liabilities of spectrum RCOM 10.00% 2017-2027 14.1 216.8

Deferred liabilities of spectrum Reliance Telecom 10.00% 2017-2027 19.2 296.1

Total debt for Rcom (excl. GCX) 468.2 7,214.4 9.2x

GCX's USD 350m secured notes 1-Aug-14 GCX Ltd 7.00% 1-Aug-19 22.5 346.0

Total debt for Rcom 490.6 7,560.4 9.7x

Cash and cash equivalents 13.2 203.3

Net debt 477.4 7,357.1 9.4x

Market capitalisation 32.1 2,086.0

Adjusted EBITDA ( FY17) 50.8 509.6 9,443.2 10.0x

Sources: Company reports, Debtwire. (1) INR / USD 0.01541 as of 31 March 2017, sourced from Oanda.com

OTHER BIDDERS

American Tower Corporation

Bharti Infratel

Brookfield

Bharti Airtel (Spectrum)

Carlyle

Gateway Partners

I-Squared Capital

Indus Towers

PCCW

TPG Capital

Tillman Global Holdings

Telekom Indonesia

Vodafone India (Spectrum)

Source: Economic Times, The Times of India, Business Standard

Debtwire.com

An Acuris CompanyAsia-Pacific Restructuring Advisory Mandates An Acuris Company

Debtwire.com

EMEA10 Queen Street PlaceLondonEC4R 1BEUnited Kingdom+44 203 741 [email protected]

AsiaSuite 1602-6Grand Millennium Plaza 181 Queen’s Road, Central Hong Kong+ 612 9002 [email protected]

Americas330 Hudson St. 4th FloorNew York, NY 10013 USA+1 212 500 [email protected]

Disclaimer

We have obtained the information provided in this report in good faith from publicly available data as well as Debtwire proprietary data and intelligence. This information is not intended to provide tax, legal or investment advice. You should seek independent tax, legal and/or investment advice before acting on information obtained from this report. We shall not be liable for any mistakes, errors, inaccuracies or omissions in, or incompleteness of, any information contained in this report, and not for any delays in updating the information.

We make no representations or warranties in regard to the contents of and materials provided on this report and exclude all representations, conditions, and warranties, express or implied arising by operation of law or otherwise, to the fullest extent permitted by law. We shall not be liable under any circumstances for any trading, investment, or other losses which may be incurred as a result of use of or reliance on information provided by this report. All such liability is excluded to the fullest extent permitted by law.

Any opinions expressed herein are statements of our judgment at the date of publication and are subject to change without notice. Reproduction without written permission is prohibited.

India Bankruptcy Profile | 10-Jan-18

Reliance Communications Limited