1 finance school of management chapter 3: interpreting financial statements objective contrast...

TRANSCRIPT

1

FinanceFinance School of Management School of Management

Chapter 3: Interpreting Chapter 3: Interpreting Financial StatementsFinancial Statements

ObjectiveContrast Economic and

Accounting ModelsValue of Accounting

Information

2

FinanceFinance School of Management School of Management

Chapter 3 ContentsChapter 3 Contents

Review of Financial Statements

Market Values v. Book Values

Accounting v. Economic Measures of Income

Return on Shareholders v. Return on Equity

Analysis Using Financial Ratios

The Relation Among Ratios

Limitations of Ratio Analysis

Purpose and Process of Financial Planning

Managing Working Capital

3

FinanceFinance School of Management School of Management

Review of Financial StatementsReview of Financial Statements

Financial Statements– Provide information (clues) to the owners &

creditors of a firm about the current status and past performance.

– Provide a convenient way for owners & creditors to set performance targets & to impose restrictions on the managers of the firm.

– Provide a convenient templates for financial planning.

4

FinanceFinance School of Management School of Management

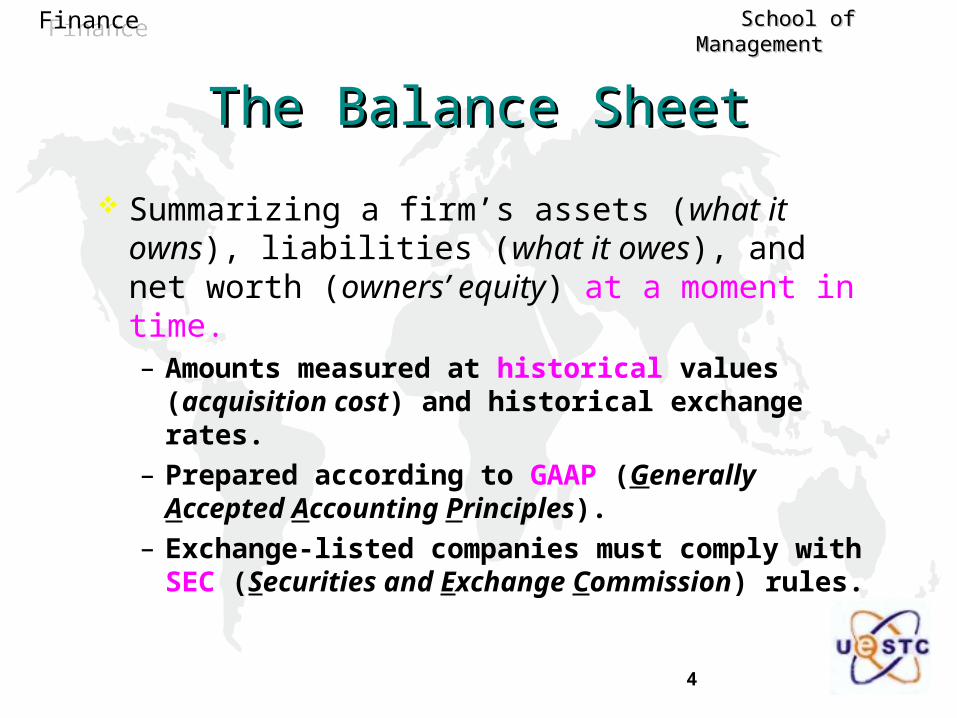

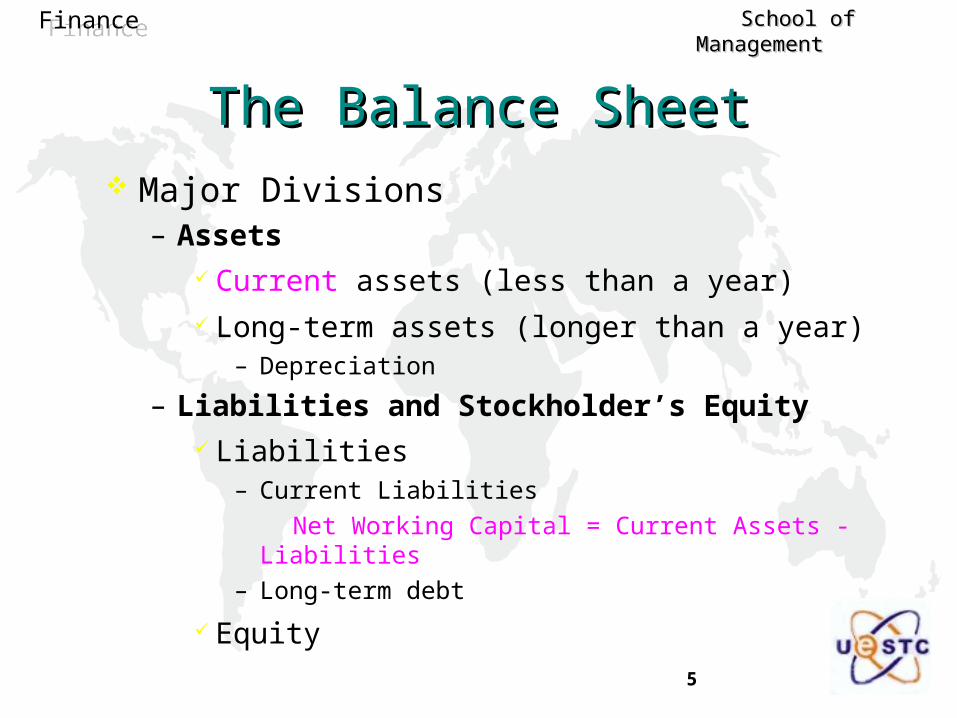

The Balance SheetThe Balance Sheet

Summarizing a firm’s assets (what it owns), liabilities (what it owes), and net worth (owners’ equity) at a moment in time.– Amounts measured at historical values (acquisition

cost) and historical exchange rates.

– Prepared according to GAAP (Generally Accepted Accounting Principles).

– Exchange-listed companies must comply with SEC (Securities and Exchange Commission) rules.

5

FinanceFinance School of Management School of Management

Major Divisions– Assets

Current assets (less than a year) Long-term assets (longer than a year)

– Depreciation

– Liabilities and Stockholder’s Equity Liabilities

– Current Liabilities

Net Working Capital = Current Assets - Liabilities

– Long-term debt

Equity

The Balance SheetThe Balance Sheet

6

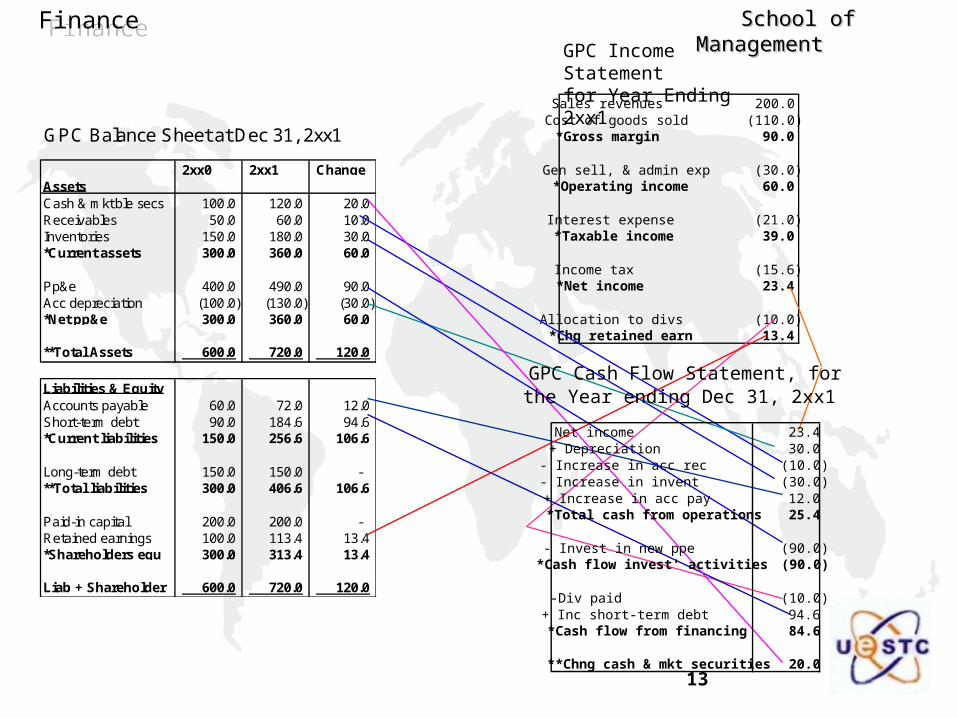

FinanceFinance School of Management School of ManagementGPC Balance Sheet at Dec 31, 2xx1

2xx12xx0

200.0 187.2

Market PricePer Share

2xx0 ChangeAssetsCash & mkt'ble secs 100.0 120.0 20.0 Receivables 50.0 60.0 10.0 Inventories 150.0 180.0 30.0 *Current assets 300.0 360.0 60.0

Pp&e 400.0 490.0 90.0 Acc depreciation (100.0) (130.0) (30.0) *Net pp&e 300.0 360.0 60.0

**Total Assets 600.0 720.0 120.0

Liabilities & EquityAccounts payable 60.0 72.0 12.0 Short-term debt 90.0 184.6 94.6 *Current liabilities 150.0 256.6 106.6

Long-term debt 150.0 150.0 - **Total liabilities 300.0 406.6 106.6

Paid-in capital 200.0 200.0 - Retained earnings 100.0 113.4 13.4 *Shareholders equ 300.0 313.4 13.4

Liab + Shareholder 600.0 720.0 120.0

2xx1

7

FinanceFinance School of Management School of Management

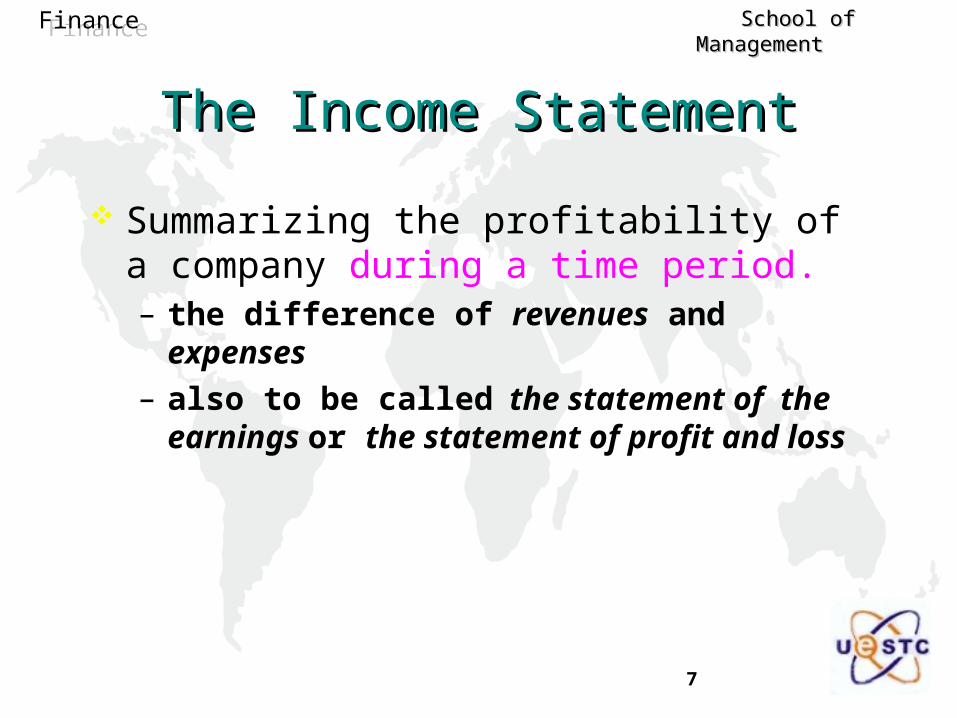

The Income StatementThe Income Statement

Summarizing the profitability of a company during a time period.– the difference of revenues and expenses

– also to be called the statement of the earnings or the statement of profit and loss

8

FinanceFinance School of Management School of Management

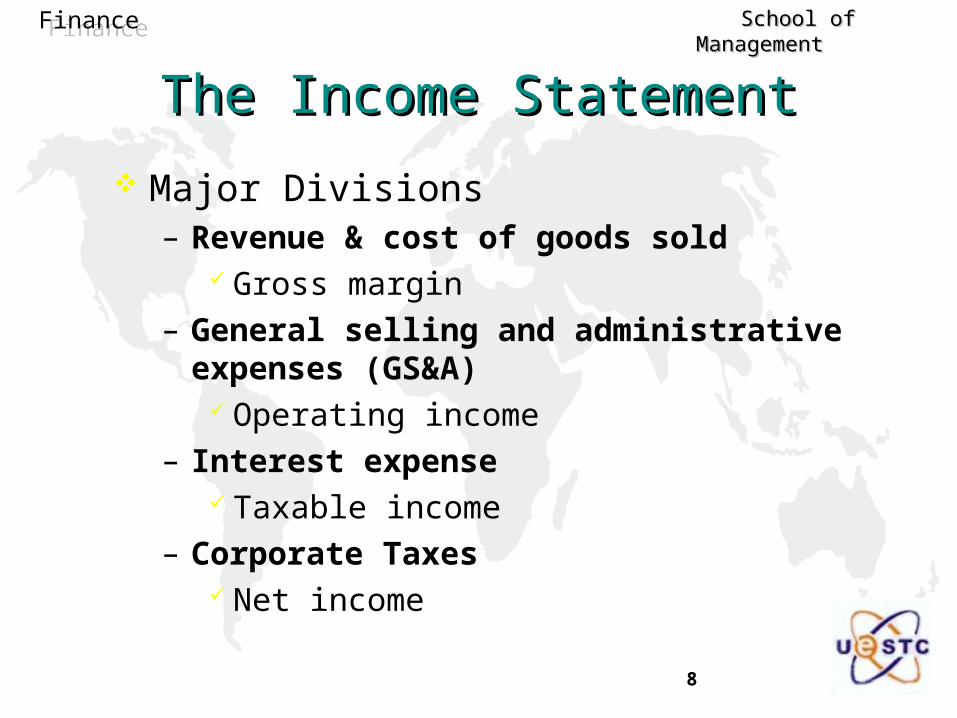

Major Divisions– Revenue & cost of goods sold

Gross margin

– General selling and administrative expenses (GS&A)

Operating income

– Interest expense Taxable income

– Corporate Taxes Net income

The Income StatementThe Income Statement

9

FinanceFinance School of Management School of Management

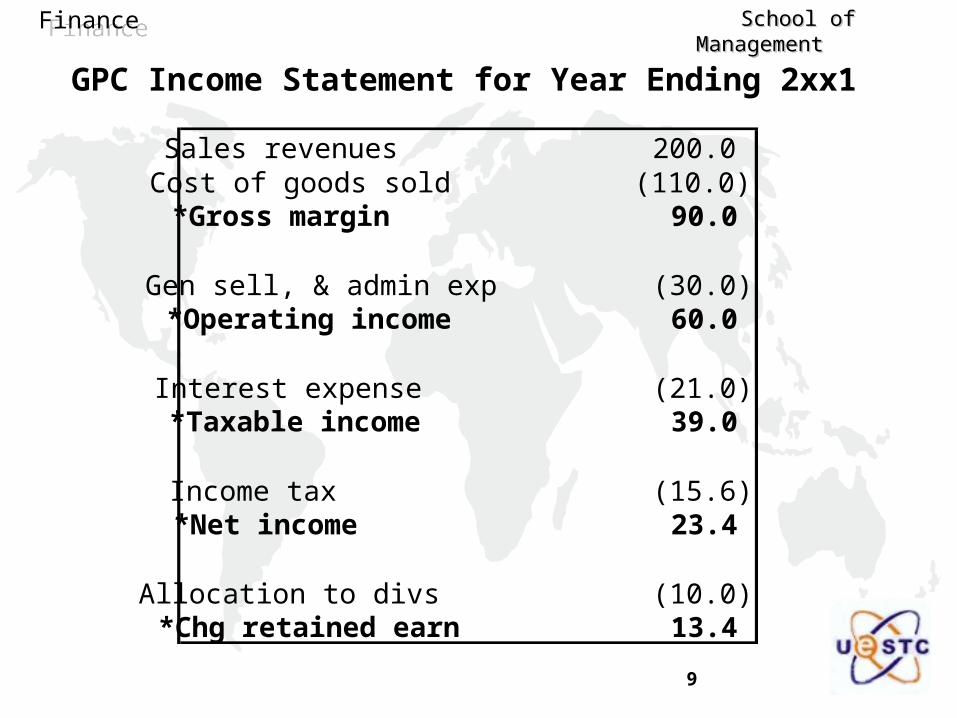

GPC Income Statement for Year Ending 2xx1

Sales revenues 200.0 Cost of goods sold (110.0) *Gross margin 90.0

Gen sell, & admin exp (30.0) *Operating income 60.0

Interest expense (21.0) *Taxable income 39.0

Income tax (15.6) *Net income 23.4

Allocation to divs (10.0) *Chg retained earn 13.4

10

FinanceFinance School of Management School of Management

It is important to remember– Retained earnings are not added to the cash

balance of the firm, but are added to shareholder’s equity.

– Accounts show historical values, not market values.

The Income StatementThe Income Statement

11

FinanceFinance School of Management School of Management

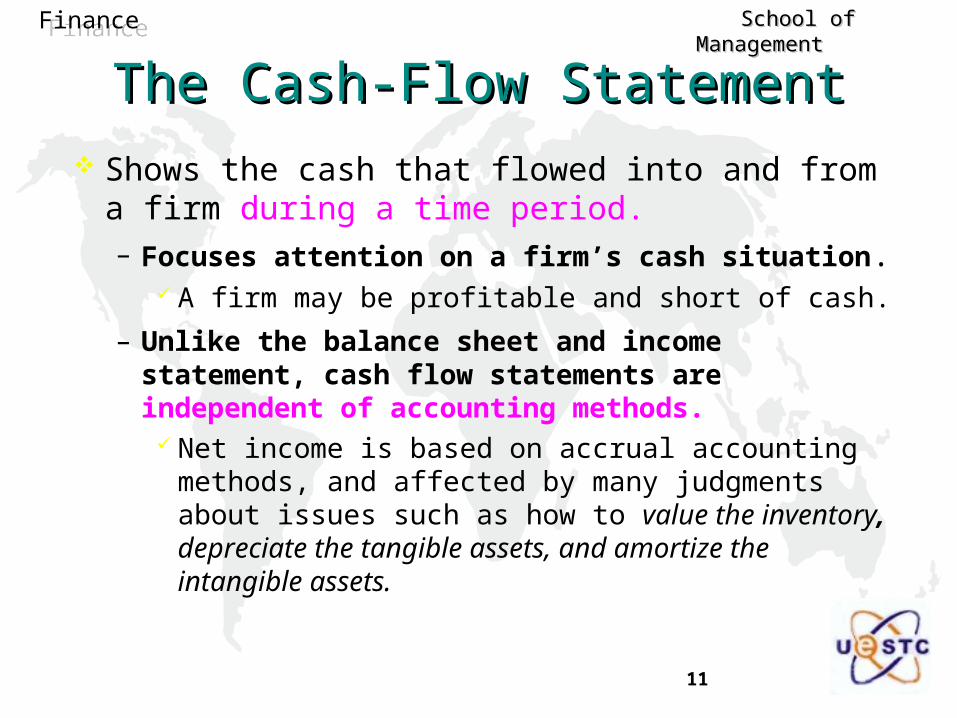

The Cash-Flow StatementThe Cash-Flow Statement

Shows the cash that flowed into and from a firm during a time period.– Focuses attention on a firm’s cash situation.

A firm may be profitable and short of cash.

– Unlike the balance sheet and income statement, cash flow statements are independent of accounting methods.

Net income is based on accrual accounting methods, and affected by many judgments about issues such as how to value the inventory, depreciate the tangible assets, and amortize the intangible assets.

12

FinanceFinance School of Management School of Management

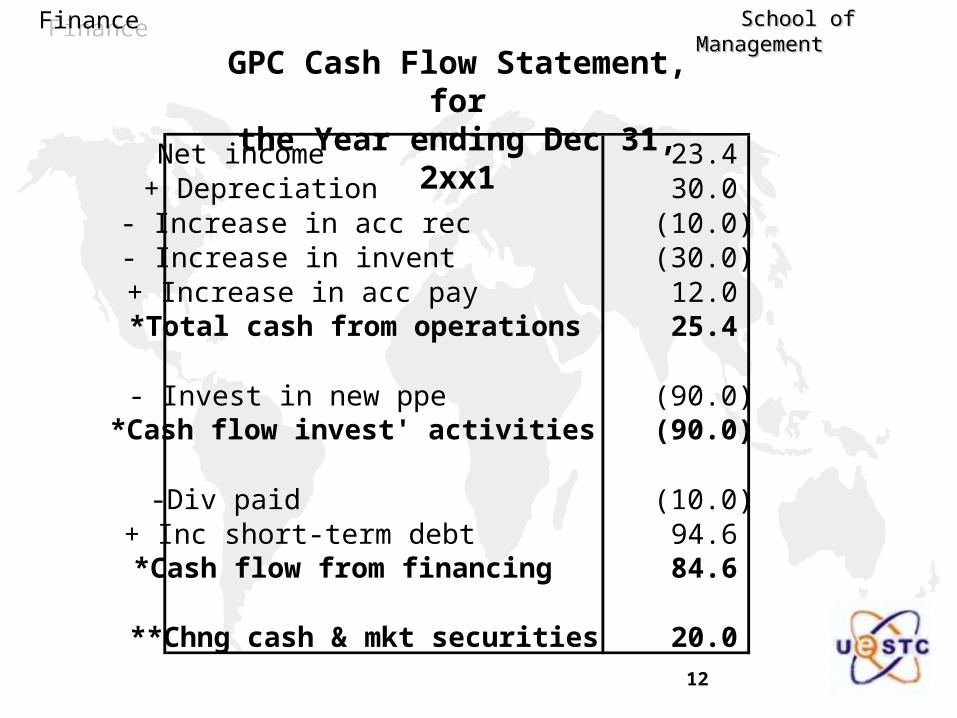

GPC Cash Flow Statement, forthe Year ending Dec 31, 2xx1

Net income 23.4 + Depreciation 30.0 - Increase in acc rec (10.0) - Increase in invent (30.0) + Increase in acc pay 12.0 *Total cash from operations 25.4

- Invest in new ppe (90.0) *Cash flow invest' activities (90.0)

-Div paid (10.0) + Inc short-term debt 94.6 *Cash flow from financing 84.6

**Chng cash & mkt securities 20.0

13

FinanceFinance School of Management School of Management

GPC Balance Sheet at Dec 31, 2xx1

2xx0 2xx1 ChangeAssetsCash & mkt'ble secs 100.0 120.0 20.0 Receivables 50.0 60.0 10.0 Inventories 150.0 180.0 30.0 *Current assets 300.0 360.0 60.0

Pp&e 400.0 490.0 90.0 Acc depreciation (100.0) (130.0) (30.0) *Net pp&e 300.0 360.0 60.0

**Total Assets 600.0 720.0 120.0

Liabilities & EquityAccounts payable 60.0 72.0 12.0 Short-term debt 90.0 184.6 94.6 *Current liabilities 150.0 256.6 106.6

Long-term debt 150.0 150.0 - **Total liabilities 300.0 406.6 106.6

Paid-in capital 200.0 200.0 - Retained earnings 100.0 113.4 13.4 *Shareholders equ 300.0 313.4 13.4

Liab + Shareholder 600.0 720.0 120.0

GPC Income Statement for Year Ending 2xx1

Sales revenues 200.0 Cost of goods sold (110.0) *Gross margin 90.0

Gen sell, & admin exp (30.0) *Operating income 60.0

Interest expense (21.0) *Taxable income 39.0

Income tax (15.6) *Net income 23.4

Allocation to divs (10.0) *Chg retained earn 13.4

GPC Cash Flow Statement, forthe Year ending Dec 31, 2xx1

Net income 23.4 + Depreciation 30.0 - Increase in acc rec (10.0) - Increase in invent (30.0) + Increase in acc pay 12.0 *Total cash from operations 25.4

- Invest in new ppe (90.0) *Cash flow invest' activities (90.0)

-Div paid (10.0) + Inc short-term debt 94.6 *Cash flow from financing 84.6

**Chng cash & mkt securities 20.0

14

FinanceFinance School of Management School of Management

Notes on Financial StatementsNotes on Financial Statements

More information relevant to understanding the true financial condition of the company in the notes to the financial statements.

–An explanation of accounting methods used

–Greater details regarding certain assets or liabilities

–Information regarding the equity structure of the firm

–Documentation of changes in operations

–Off-balance-sheet items

15

FinanceFinance School of Management School of Management

Market Values v. Book ValuesMarket Values v. Book Values

Book value: the official accounting values of assets and shareholders’ equity

Two reasons why the market price of a company’s stock does not equal its book value

–The book value does not include all of a firm’s assets and liabilities.

–The assets and liabilities included on a firm’s official balance sheet are valued at original acquisition cost less depreciation, rather than at current market value.

16

FinanceFinance School of Management School of Management

The accounting balance sheet often omits some economically significant assets.– Intangible assets: a good reputation, a knowledge base

– Goodwill: the difference between the acquisition price and the book value when a firm is acquired

The accounting balance sheet also omits some economically significant liabilities.– Contingent liabilities: costly lawsuits

Market Values v. Book ValuesMarket Values v. Book Values

17

FinanceFinance School of Management School of Management

IBM’s equipment for shell molding– Purchased for $3.9 million 3 years ago

– The book value at $2.6 million after 3 years depreciation

– The market value has fallen to $1.2 million because of technological change in the manufacture of computer shells.

Inventory of copper to be used in the manufacturing process of heating furnaces– You paid $29,000 at the beginning of the year.

– The market value has risen to $60,000.

For decision-making purposes, the correct value to use is the market value, whenever available.– Marking to market

Which is Relevant for Financial Decision-MakingWhich is Relevant for Financial Decision-Making

18

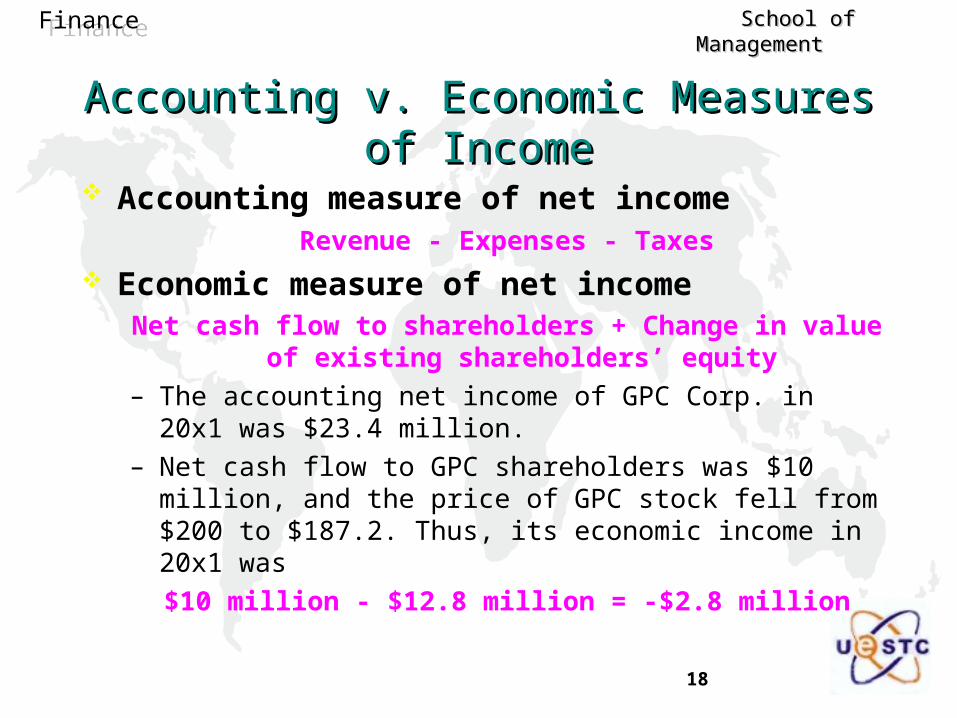

FinanceFinance School of Management School of Management

Accounting measure of net income Revenue - Expenses - Taxes

Economic measure of net income Net cash flow to shareholders + Change in value of existing

shareholders’ equity

– The accounting net income of GPC Corp. in 20x1 was $23.4 million.

– Net cash flow to GPC shareholders was $10 million, and the price of GPC stock fell from $200 to $187.2. Thus, its economic income in 20x1 was

$10 million - $12.8 million = -$2.8 million

Accounting v. Economic Measures of IncomeAccounting v. Economic Measures of Income

19

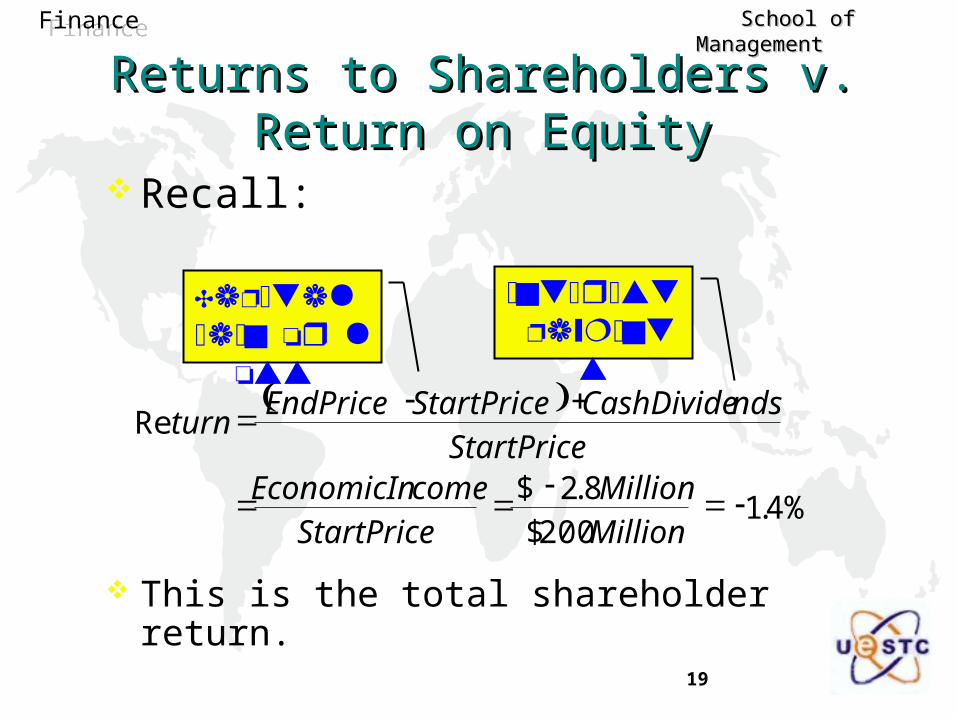

FinanceFinance School of Management School of Management

Returns to Shareholders v. Return on EquityReturns to Shareholders v. Return on Equity

Recall:

This is the total shareholder return.

4%.1200$

8.2$

Re

MillionMillion

StartPricecomeEconomicIn

StartPricendsCashDivideStartPriceEndPrice

turn

20

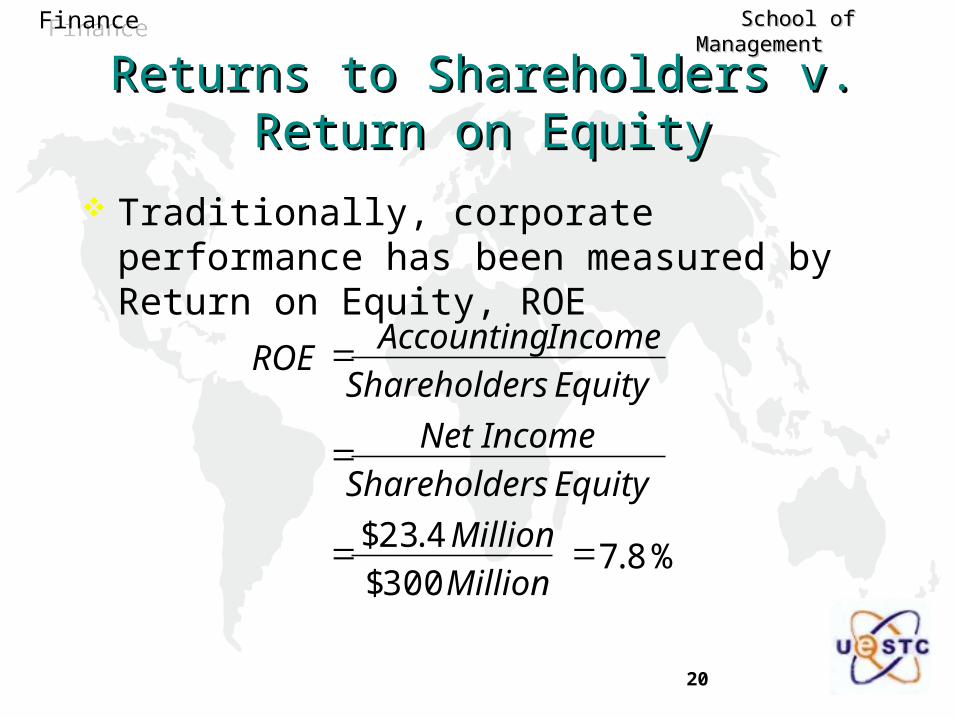

FinanceFinance School of Management School of Management

Traditionally, corporate performance has been measured by Return on Equity, ROE

%8.7300$

4.23$

Million

Million

EquityShareholders

Net Income

EquityShareholders

IncomeAccountingROE

Returns to Shareholders v. Return on EquityReturns to Shareholders v. Return on Equity

21

FinanceFinance School of Management School of Management

Analysis Using Financial RatiosAnalysis Using Financial Ratios

Despite the differences between accounting and economic financial principle, a firm’s published statements can often offer some clues about its financial condition and provide insights into its past performance that may be relevant for the future.

22

FinanceFinance School of Management School of Management

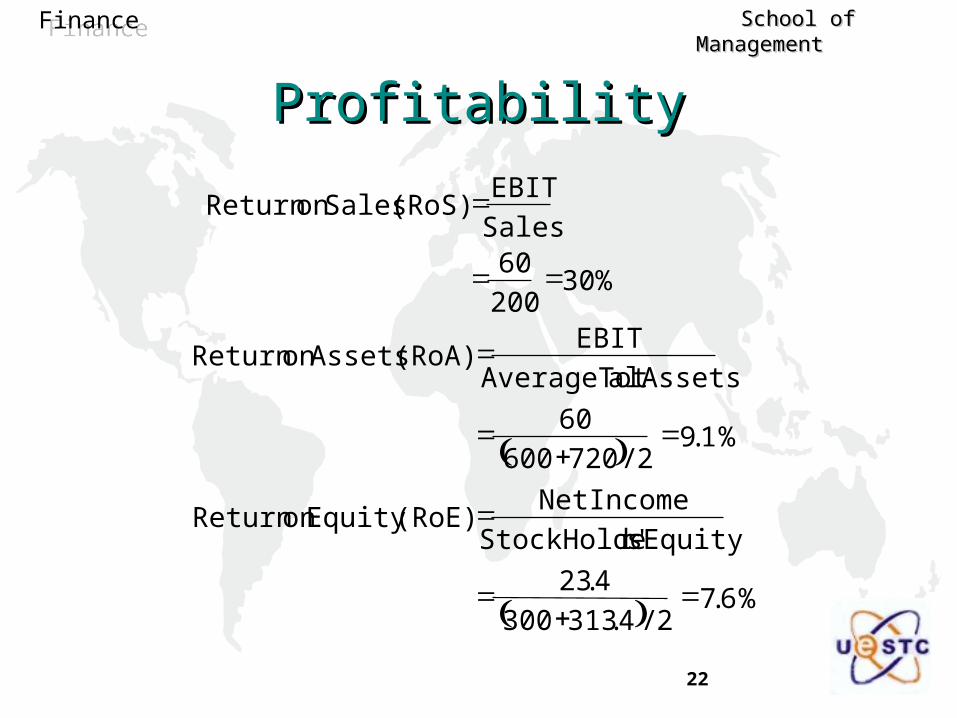

ProfitabilityProfitability

%6.72/4.313300

4.23

sEquityr'StockHolde

NetIncome (RoE)Equity on Return

%1.92/720600

60

alAssetsAverageTot

EBIT (RoA) Assetson Return

%30200

60Sales

EBIT (RoS) Saleson Return

23

FinanceFinance School of Management School of Management

Asset TurnoverAsset Turnover

Times 3.02/720600

200

Assets Total Average

Sales Turnover Asset

Times 7.02/180150

110

Inventory Average

Sold Goods ofCost Turnover Inventory

Times 6.32/6050

200

sReceivable Average

Sales Turnover sReceivable

24

FinanceFinance School of Management School of Management

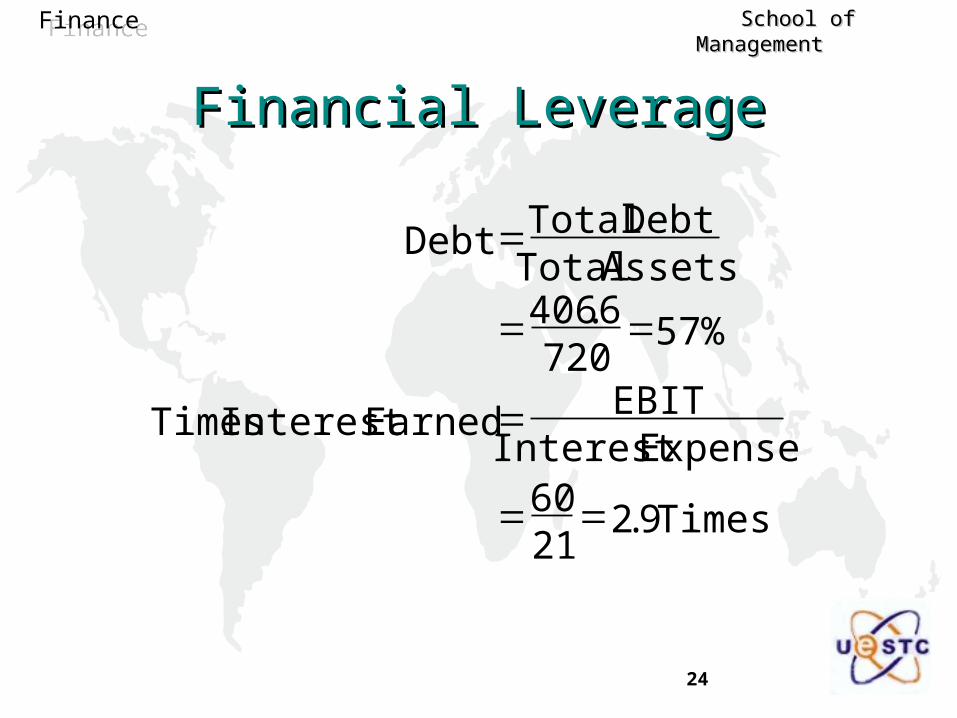

Financial LeverageFinancial Leverage

Times 9.22160

ExpenseInterest EBIT Earned Interest Times

%57720

6.406Assets TotalDebt Total Debt

25

FinanceFinance School of Management School of Management

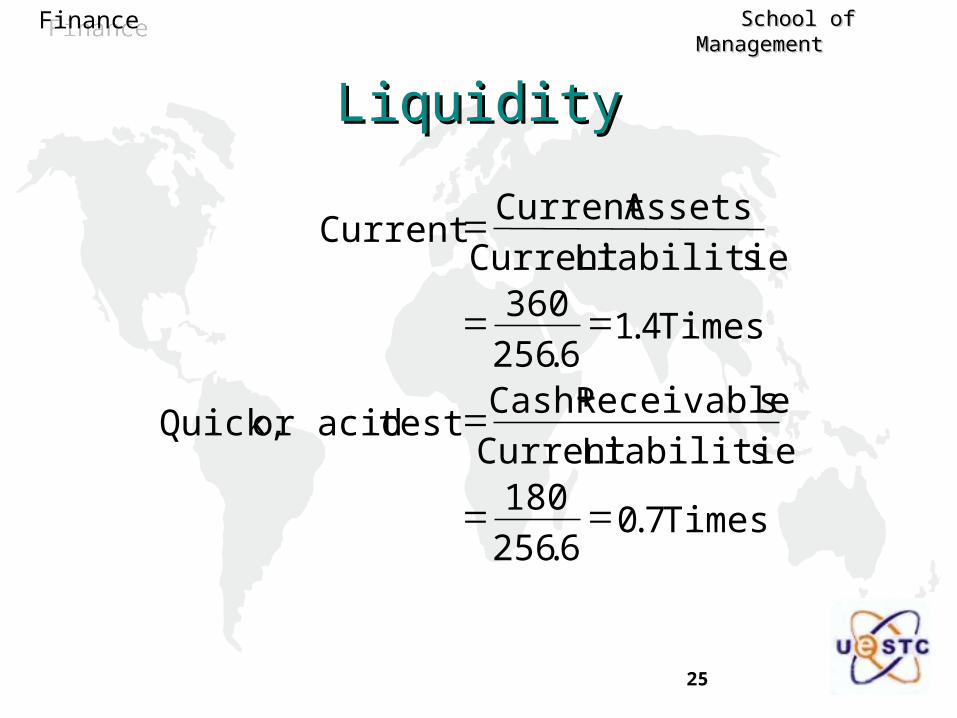

LiquidityLiquidity

Times 7.06.256

180sLiabilitieCurrent

sReceivableCash testor acid Quick,

Times 4.16.256

360sLiabilitieCurrent

AssetsCurrent Current

26

FinanceFinance School of Management School of Management

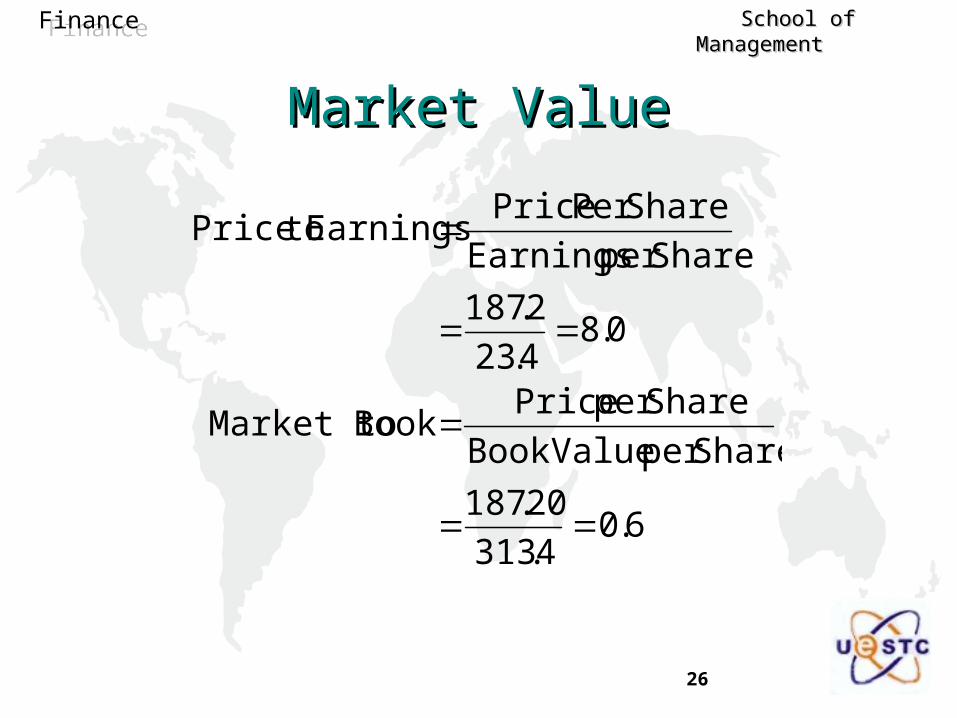

Market ValueMarket Value

6.04.313

20.187

Shareper ValueBook

Shareper Price Book Market to

0.84.23

2.187

Shareper Earnings

SharePer Price Earnings toPrice

27

FinanceFinance School of Management School of Management

Ratio ComparisonsRatio Comparisons Establish Your Perspective

– Shareholder

– Employee, Management, or Union

– Creditor

– Predator, Customer, Supplier, Competitor, Trade Association

Benchmarks– Other companies’ ratios

– The firm’s historical ratios

– Data extracted from financial markets

28

FinanceFinance School of Management School of Management

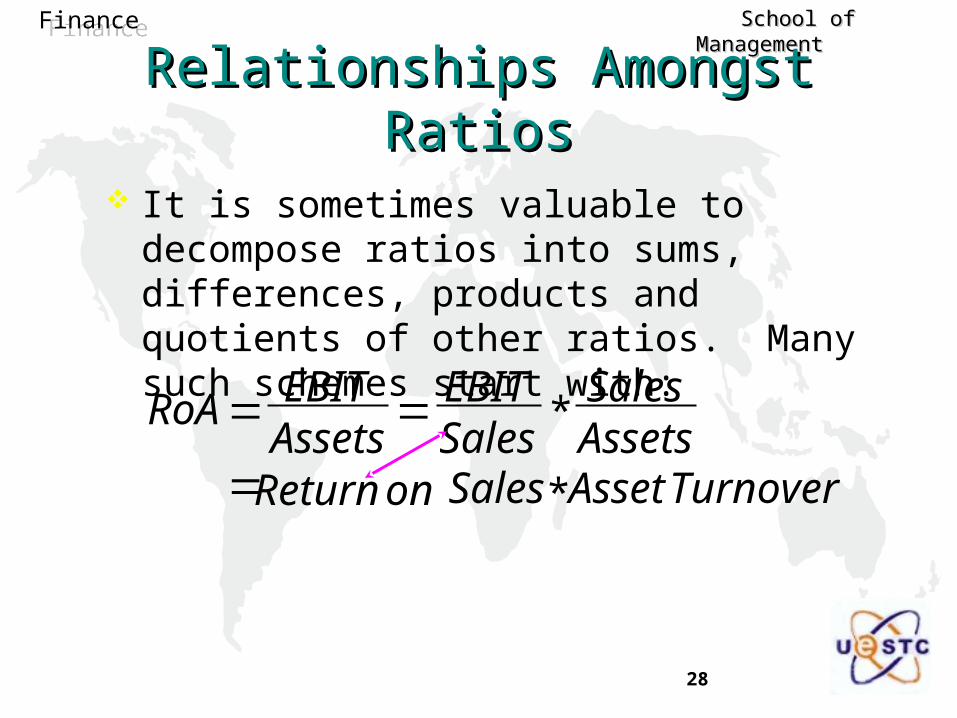

Relationships Amongst RatiosRelationships Amongst Ratios

It is sometimes valuable to decompose ratios into sums, differences, products and quotients of other ratios. Many such schemes start with:

TurnoverAsset *Saleson Return

*

AssetsSales

SalesEBIT

AssetsEBITRoA

29

FinanceFinance School of Management School of Management

Differences between ROS and ATO Differences between ROS and ATO across Industriesacross Industries

A “low” ROS or ATO ratio need not be a sign of a trouble firm.

30

FinanceFinance School of Management School of Management

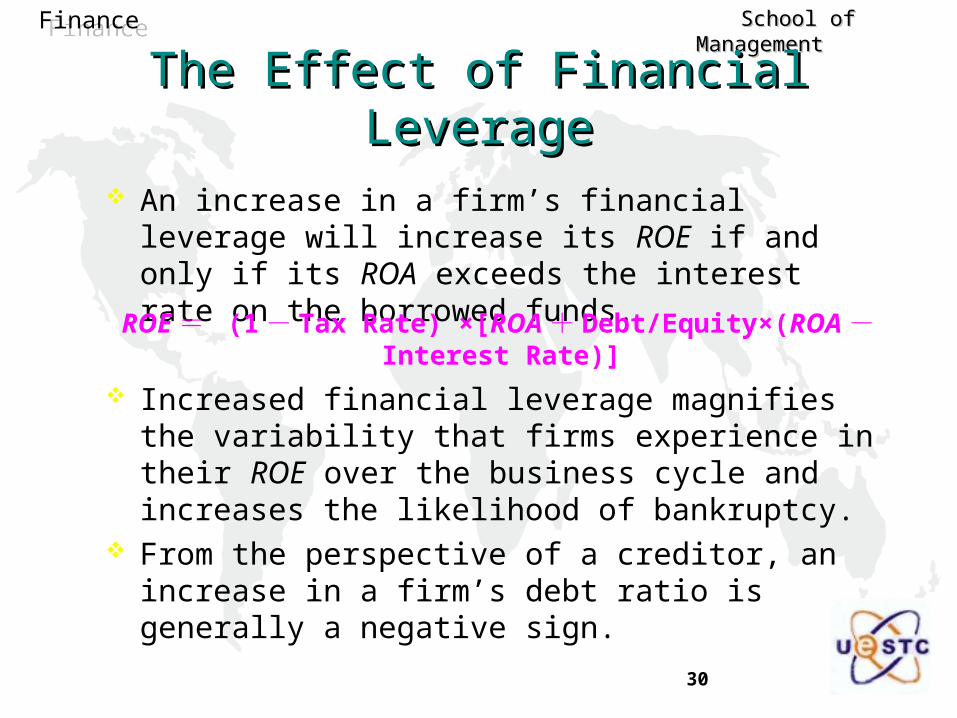

The Effect of Financial LeverageThe Effect of Financial Leverage

An increase in a firm’s financial leverage will increase its ROE if and only if its ROA exceeds the interest rate on the borrowed funds.

Increased financial leverage magnifies the variability that firms experience in their ROE over the business cycle and increases the likelihood of bankruptcy.

From the perspective of a creditor, an increase in a firm’s debt ratio is generally a negative sign.

ROE = (1 - Tax Rate) ×[ROA + Debt/Equity×(ROA - Interest Rate)]

31

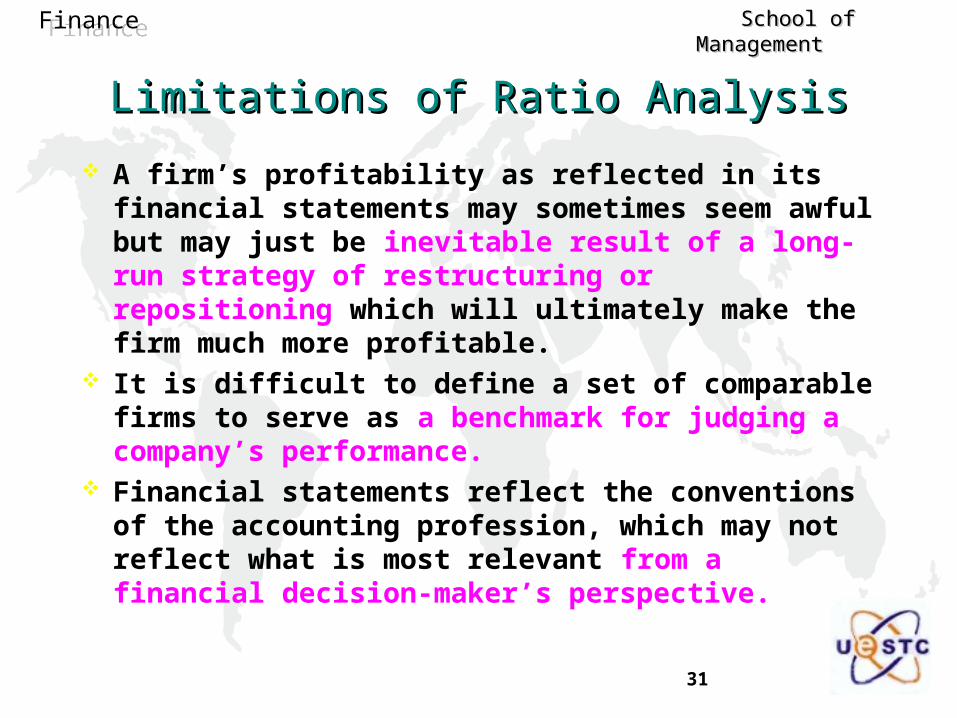

FinanceFinance School of Management School of Management

A firm’s profitability as reflected in its financial statements may sometimes seem awful but may just be inevitable result of a long-run strategy of restructuring or repositioning which will ultimately make the firm much more profitable.

It is difficult to define a set of comparable firms to serve as a benchmark for judging a company’s performance.

Financial statements reflect the conventions of the accounting profession, which may not reflect what is most relevant from a financial decision-maker’s perspective.

Limitations of Ratio AnalysisLimitations of Ratio Analysis

32

FinanceFinance School of Management School of Management

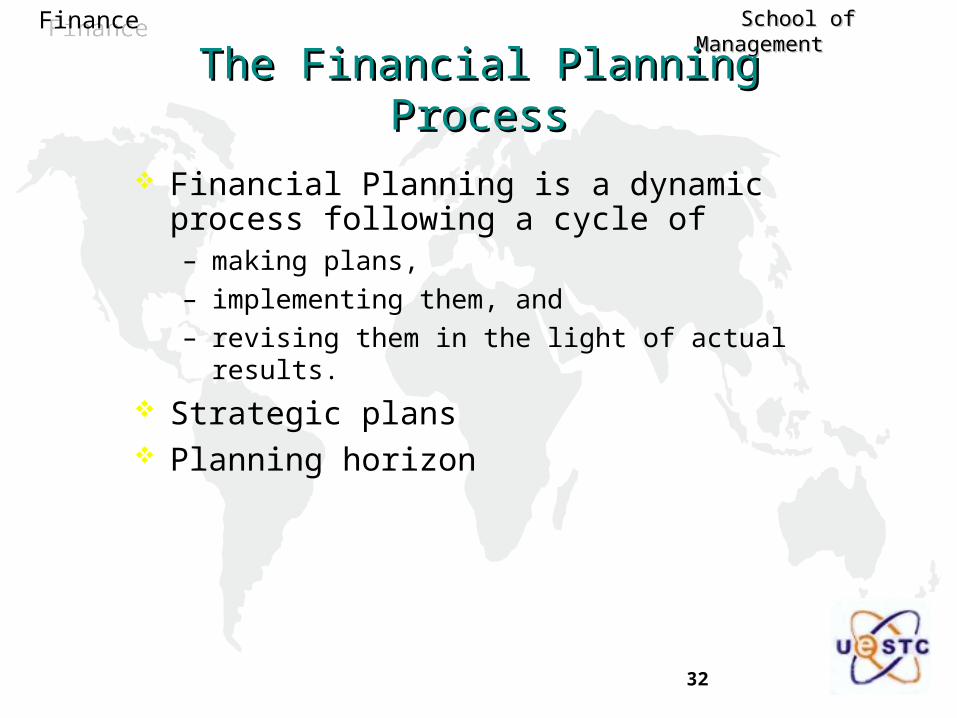

The Financial Planning ProcessThe Financial Planning Process

Financial Planning is a dynamic process following a cycle of – making plans,

– implementing them, and

– revising them in the light of actual results.

Strategic plans Planning horizon

33

FinanceFinance School of Management School of Management

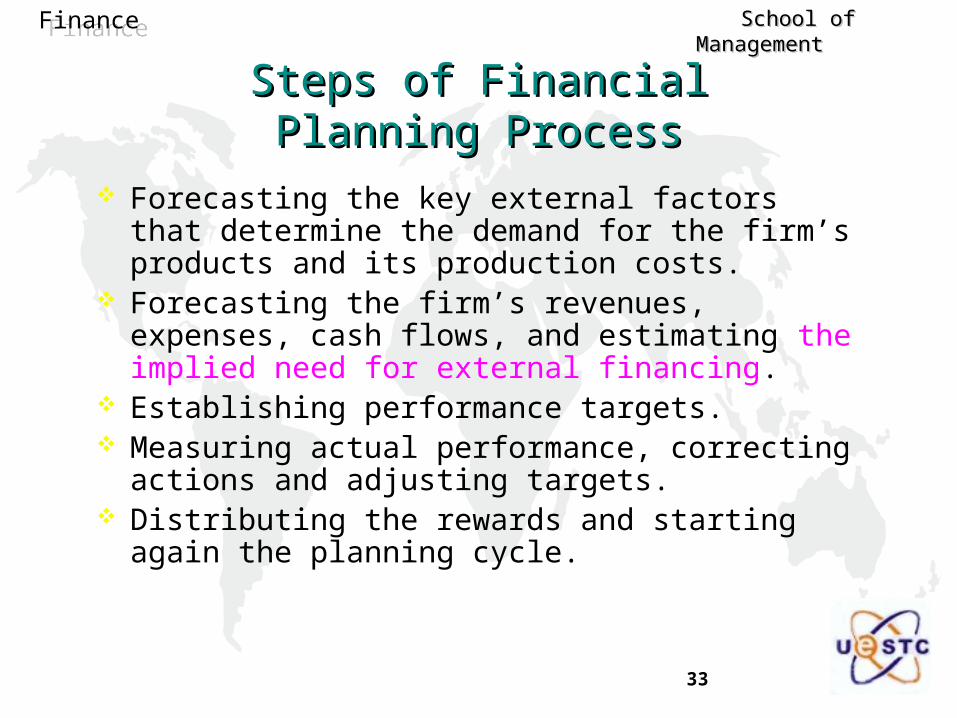

Steps of Financial Planning ProcessSteps of Financial Planning Process

Forecasting the key external factors that determine the demand for the firm’s products and its production costs.

Forecasting the firm’s revenues, expenses, cash flows, and estimating the implied need for external financing.

Establishing performance targets. Measuring actual performance, correcting actions and

adjusting targets. Distributing the rewards and starting again the planning

cycle.

34

FinanceFinance School of Management School of Management

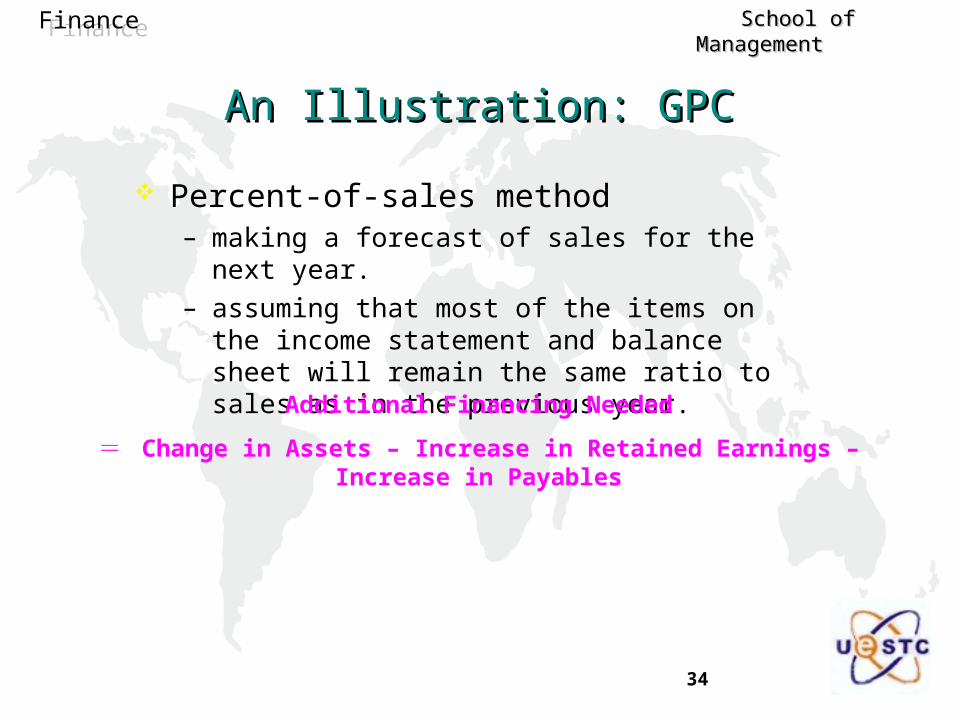

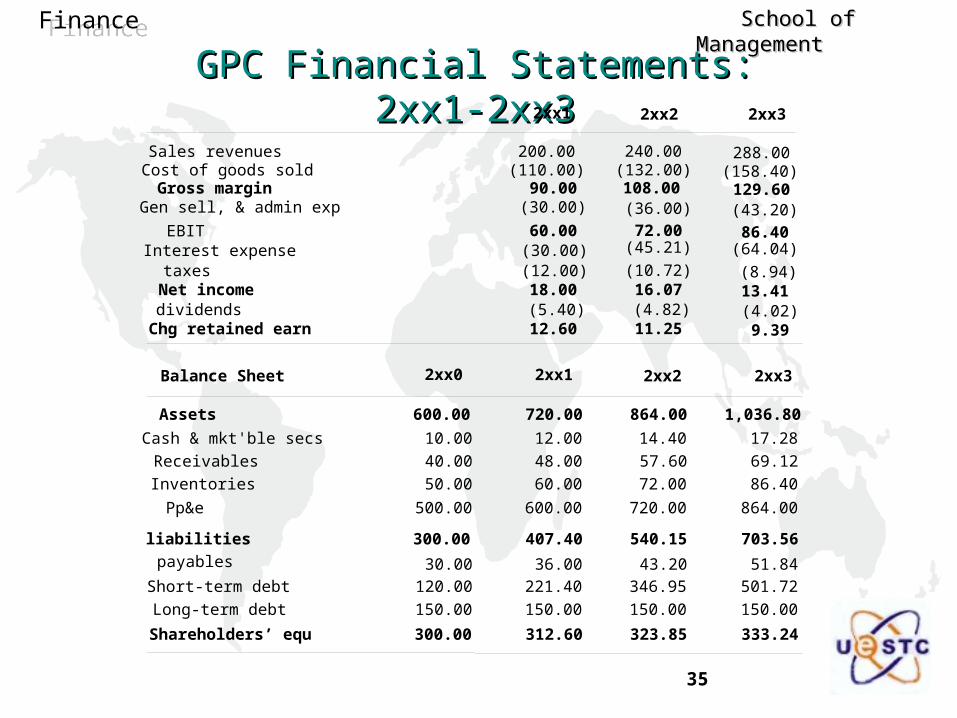

An Illustration: GPCAn Illustration: GPC

Percent-of-sales method – making a forecast of sales for the next year.

– assuming that most of the items on the income statement and balance sheet will remain the same ratio to sales as in the previous year.

Additional Financing Needed

= Change in Assets – Increase in Retained Earnings – Increase in Payables

35

FinanceFinance School of Management School of Management

GPC Financial Statements: 2xx1-2xx3GPC Financial Statements: 2xx1-2xx3

2xx0 2xx1

Cash & mkt'ble secs 10.00 12.00

Receivables 40.00 48.00

Inventories 50.00 60.00

Pp&e 500.00 600.00

Assets 600.00 720.00

payables 30.00 36.00

Short-term debt 120.00 221.40

Long-term debt 150.00 150.00

liabilities 300.00 407.40

Shareholders’ equ 300.00 312.60

14.40

57.60

72.00

720.00

864.00

43.20

346.95

150.00

540.15

323.85

2xx2

17.28

69.12

86.40

864.00

1,036.80

51.84

501.72

150.00

703.56

333.24

2xx3Balance Sheet

Sales revenuesCost of goods soldGross marginGen sell, & admin exp

EBITInterest expensetaxesNet incomedividendsChg retained earn

200.00(110.00)

90.00(30.00)

60.00(30.00)(12.00)18.00(5.40)12.60

240.00(132.00)108.00(36.00)

72.00(45.21)

(10.72)16.07(4.82)11.25

288.00(158.40)129.60(43.20)

86.40(64.04)

(8.94)13.41(4.02)9.39

2xx1 2xx2 2xx3

36

FinanceFinance School of Management School of Management

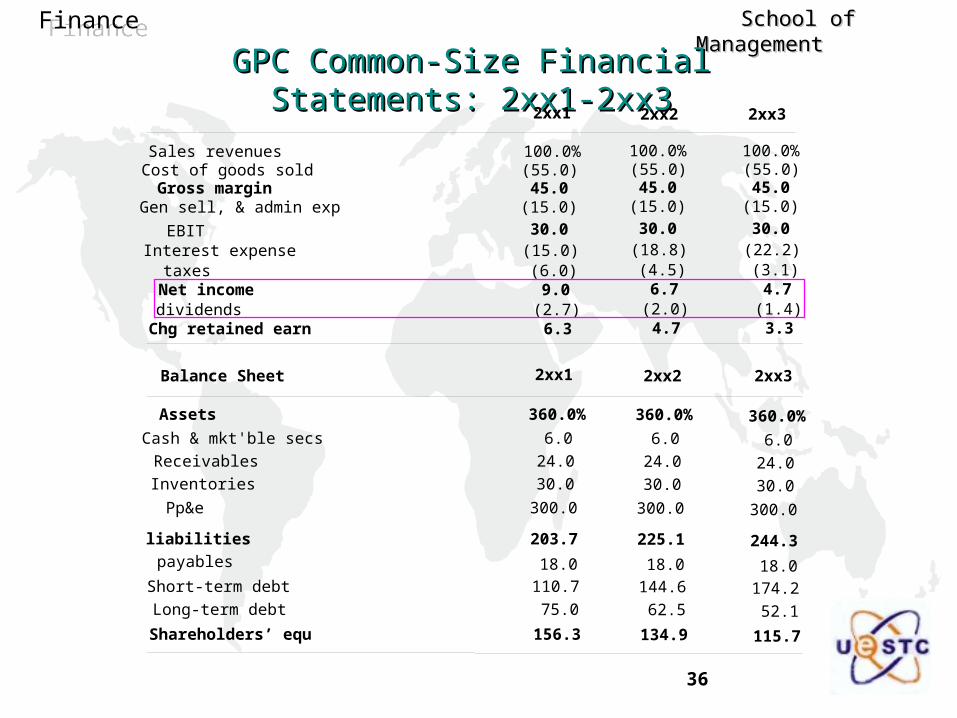

GPC Common-Size Financial Statements: 2xx1-2xx3GPC Common-Size Financial Statements: 2xx1-2xx3

2xx1

Cash & mkt'ble secs 6.0

Receivables 24.0

Inventories 30.0

Pp&e 300.0

Assets 360.0%

payables 18.0

Short-term debt 110.7

Long-term debt 75.0

liabilities 203.7

Shareholders’ equ 156.3

2xx2 2xx3Balance Sheet

Sales revenuesCost of goods soldGross marginGen sell, & admin exp

EBITInterest expensetaxesNet incomedividendsChg retained earn

100.0%(55.0)45.0

(15.0)

30.0(15.0)(6.0)9.0

(2.7)6.3

2xx1 2xx2 2xx3

100.0%(55.0)45.0

(15.0)

30.0(18.8)(4.5)6.7

(2.0)4.7

100.0%(55.0)45.0

(15.0)

30.0(22.2)(3.1)4.7

(1.4)3.3

6.0

24.0

30.0

300.0

360.0%

18.0

144.6

62.5

225.1

134.9

6.0

24.0

30.0

300.0

360.0%

18.0

174.2

52.1

244.3

115.7

37

FinanceFinance School of Management School of Management

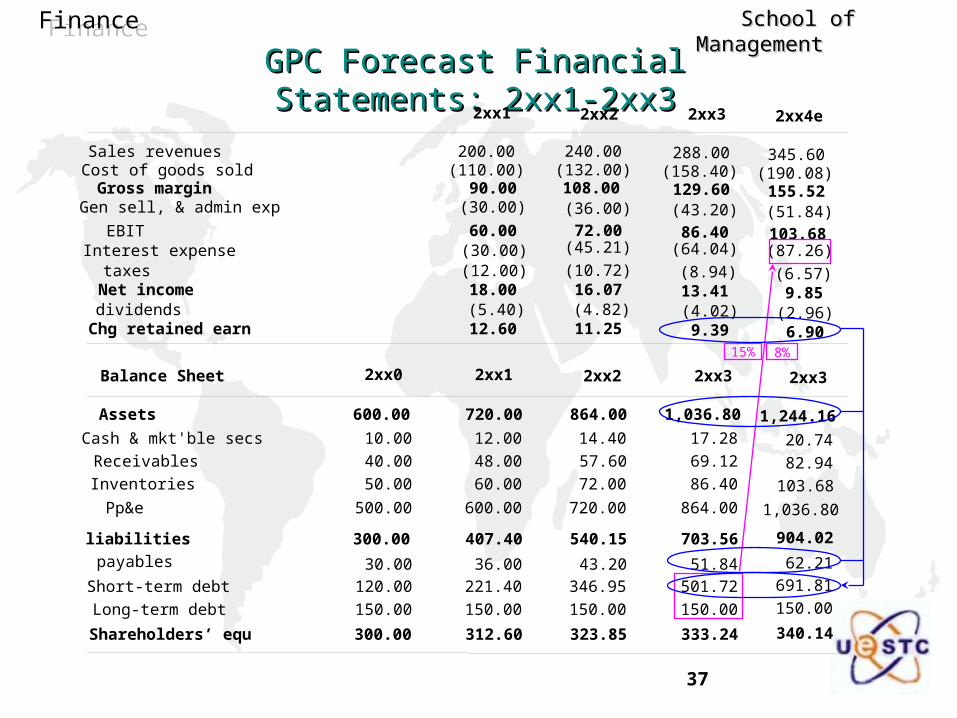

GPC Forecast Financial Statements: 2xx1-2xx3GPC Forecast Financial Statements: 2xx1-2xx3

2xx0 2xx1

Cash & mkt'ble secs 10.00 12.00

Receivables 40.00 48.00

Inventories 50.00 60.00

Pp&e 500.00 600.00

Assets 600.00 720.00

payables 30.00 36.00

Short-term debt 120.00 221.40

Long-term debt 150.00 150.00

liabilities 300.00 407.40

Shareholders’ equ 300.00 312.60

14.40

57.60

72.00

720.00

864.00

43.20

346.95

150.00

540.15

323.85

2xx2

17.28

69.12

86.40

864.00

1,036.80

51.84

501.72

150.00

703.56

333.24

2xx3Balance Sheet

Sales revenuesCost of goods soldGross marginGen sell, & admin exp

EBITInterest expensetaxesNet incomedividendsChg retained earn

200.00(110.00)

90.00(30.00)

60.00(30.00)(12.00)18.00(5.40)12.60

240.00(132.00)108.00(36.00)

72.00(45.21)

(10.72)16.07(4.82)11.25

288.00(158.40)129.60(43.20)

86.40(64.04)

(8.94)13.41(4.02)9.39

2xx1 2xx2 2xx3

20.74

82.94

103.68

1,036.80

1,244.16

62.21

691.81

150.00

904.02

340.14

2xx3

345.60(190.08)155.52(51.84)

103.68(87.26)

(6.57)9.85

(2.96)6.90

2xx4e

15% 8%

38

FinanceFinance School of Management School of Management

Sustainable Growth RateSustainable Growth Rate Assumptions:

– The firm will not issue any new equity shares, so that growth in equity capital occurs only through the retention of earnings.

– The firm will not increase its ratio of debt to equity, so that external debt financing will grow at the same rate as equity grows through retained earnings.

Sustainable Growth Rate = Earings Retention Rate × ROE

Implications: – The maximum sustainable growth rate is equal to the firm’s ROE.

– If a firm tries to grow faster than this rate, it will have to issue new shares and/or increase its debt.

39

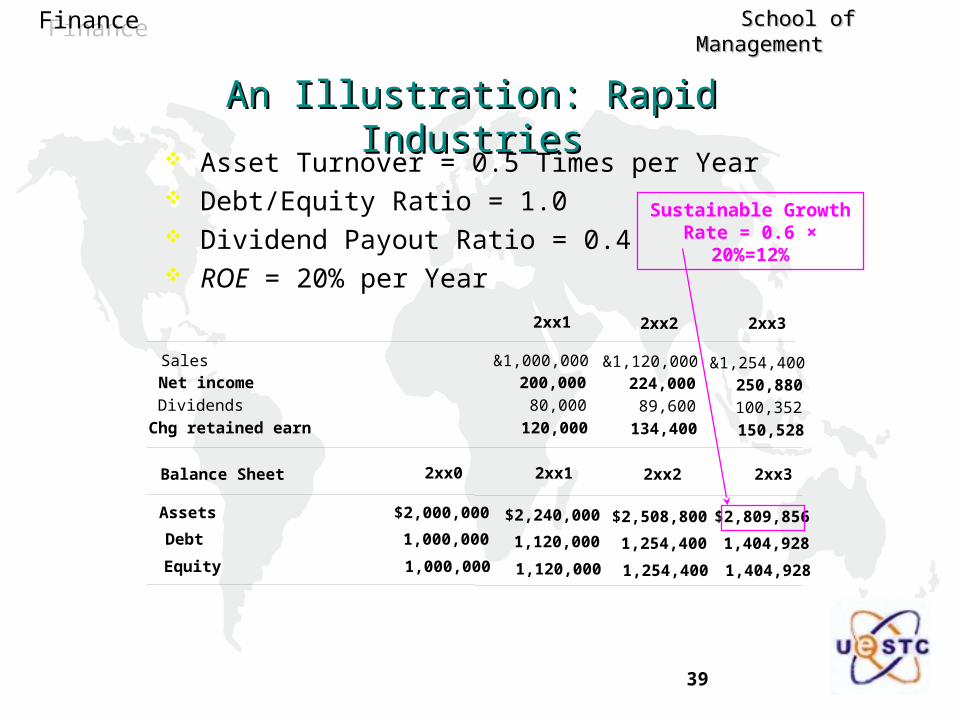

FinanceFinance School of Management School of Management

An Illustration: Rapid IndustriesAn Illustration: Rapid Industries

2xx0 2xx1

Assets $2,000,000

Debt 1,000,000

Equity 1,000,000

2xx2 2xx3Balance Sheet

Sales

Net income

Dividends

Chg retained earn

&1,000,000

200,000

80,000

120,000

2xx1 2xx2 2xx3

&1,120,000

224,000

89,600

134,400

&1,254,400

250,880

100,352

150,528

$2,240,000

1,120,000

1,120,000

$2,508,800

1,254,400

1,254,400

$2,809,856

1,404,928

1,404,928

Asset Turnover = 0.5 Times per Year Debt/Equity Ratio = 1.0 Dividend Payout Ratio = 0.4 ROE = 20% per Year

Sustainable Growth Rate = 0.6 × 20%=12%

40

FinanceFinance School of Management School of Management

In most cases cash must be paid out to cover expenses before any cash is collected from the sale of the firm’s products.– If a firm’s need for working capital is permanent rather than seasonal,

it usually seeks long-term financing for it.

– Seasonal financing needs are met through short-term financing arrangements.

The main principle of efficient working capital management – To minimize the amount of the firm’s investment in nonearning assets

such as receivables and inventories.

– To maximize the use of “free” credit such as prepayments by customers, accrued wages, and accounts payable.

Working Capital ManagementWorking Capital Management

41

FinanceFinance School of Management School of Management

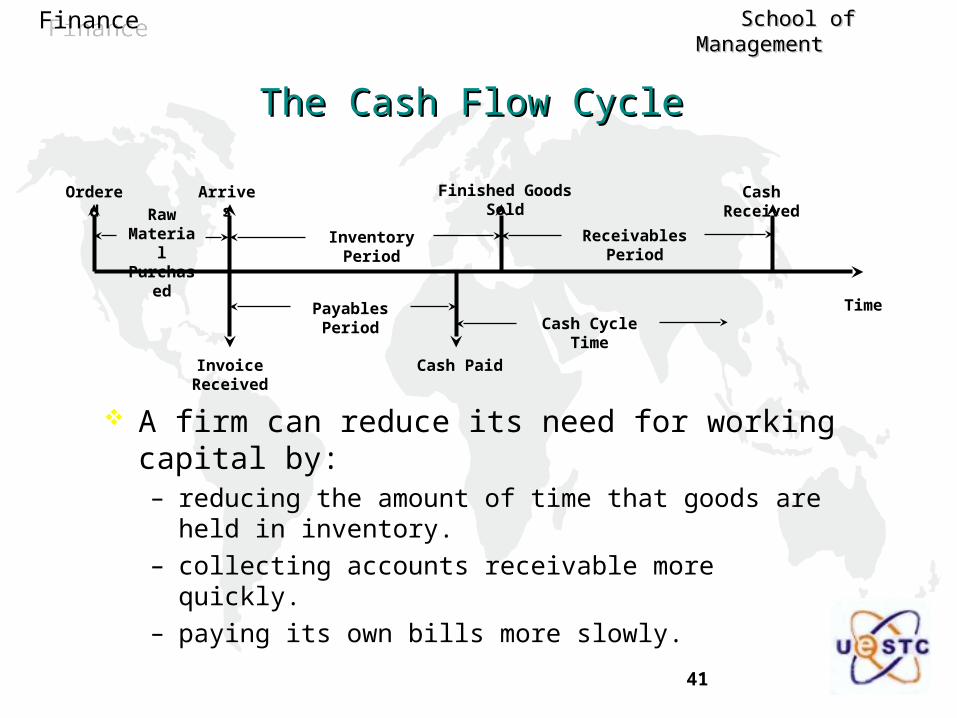

The Cash Flow CycleThe Cash Flow Cycle

Time

Ordered Arrives Finished Goods Sold Cash Received

Invoice Received Cash Paid

Payables Period

Inventory Period Receivables PeriodRaw

Material Purchased

Cash Cycle Time

A firm can reduce its need for working capital by: – reducing the amount of time that goods are held in inventory.

– collecting accounts receivable more quickly.

– paying its own bills more slowly.