1 chapter 3: interpreting financial statements copyright © prentice hall inc. 1999. author: nick...

Post on 22-Dec-2015

217 views

TRANSCRIPT

1

Chapter 3: Interpreting Financial Statements

Copyright © Prentice Hall Inc. 1999. Author: Nick Bagley

ObjectiveContrast Economic and

Accounting Models<=>

Value of Accounting Information

2

Chapter 3 ContentsChapter 3 Contents

• 3.1 Functions of Financial 3.1 Functions of Financial StatementsStatements

• 3.2 Review of Financial 3.2 Review of Financial StatementsStatements

• 3.3 Market values v. Book 3.3 Market values v. Book ValuesValues

• 3.4 Accounting v. Economic 3.4 Accounting v. Economic Measures of IncomeMeasures of Income

• 3.5 Return on Shareholders 3.5 Return on Shareholders v. Return on Equityv. Return on Equity

• 3.6 Analysis Using Financial 3.6 Analysis Using Financial RatiosRatios

• 3.7 The Financial Planning 3.7 The Financial Planning ProcessProcess

• 3.8 Constructing a Financial 3.8 Constructing a Financial Planning ModelPlanning Model

• 3.9 Growth & the Need for 3.9 Growth & the Need for External FinancingExternal Financing

• 3.10 Working Capital Mgmt.3.10 Working Capital Mgmt.

• 3.11 Liquidity & Cash Mgmt.3.11 Liquidity & Cash Mgmt.

3

3.1 Functions of Financial Statements• Financial Statements:

– Provide information to the owners & creditors of a firm about the current status and past performance

– Provide a convenient way for owners & creditors to set performance targets & to impose restrictions of the managers of the firm

– Provide a convenient templates for financial planning

4

The Balance Sheet• Summarizes a firms assets, liabilities, and

owner’s equity at a moment in time

• Amounts measured at historical values and historical exchange rates

• Prepared according to GAAP, Generally Accepted Accounting Principles– GAAP modified occasionally by the Financial

Accounting Standards Board

• Exchange-listed companies must comply with Securities and Exchange Commission (SEC) rules

5

The Balance Sheet

• Major Divisions:– Assets

• Current assets (less than a year)

• Long-term assets (longer than a year– Depreciation

– Liabilities and Stockholder’s Equity• Liabilities

– Current Liabilities– Long-term debt

• Equity

6

GPC Balance Sheet at Dec 31, 2xx1

2xx0 2xx1 ChangeAssetsCash & mkt'ble secs 100.0 120.0 20.0 Receivables 50.0 60.0 10.0 Inventories 150.0 180.0 30.0 *Current assets 300.0 360.0 60.0

Pp&e 400.0 490.0 90.0 Acc depreciation (100.0) (130.0) (30.0) *Net pp&e 300.0 360.0 60.0

**Total Assets 600.0 720.0 120.0

Liabilities & EquityAccounts payable 60.0 72.0 12.0 Short-term debt 90.0 184.6 94.6 *Current liabilities 150.0 256.6 106.6

Long-term debt 150.0 150.0 - **Total liabilities 300.0 406.6 106.6

Paid-in capital 200.0 200.0 - Retained earnings 100.0 113.4 13.4 *Shareholders equ 300.0 313.4 13.4

Liab + Shareholder 600.0 720.0 120.0

7

The Income Statement• Summarizes the profitability of a

company during a time period

• Major Divisions:– Revenue & cost of goods sold

» Gross margin

– General administrative and selling expenses (GS&A)

» Operating income

– Debt service » Taxable income

– Corporate Taxes » Net income

8

The Income Statement

• Important Reminders:– Retained earnings are not added to the

cash balance in the balance sheet, but are added to shareholder’s equity

– Accounts show historical values, not market values• The shareholder’s equity may be much

higher or lower than the market value of the firm

– The value of the firm’s land may have halved or doubled, but this would not be reported in the balance sheet

9

GPC Income Statement for Year Ending 2xx1

Sales revenues 200.0 Cost of goods sold (110.0) *Gross margin 90.0

Gen sell, & admin exp (30.0) *Operating income 60.0

Interest expense (21.0) *Taxable income 39.0

Income tax (15.6) *Net income 23.4

Allocation to divs (10.0) *Chg retained earn 13.4

10

The Cash-Flow Statement

• Show the cash that flowed into and from a firm in during a time period– Focuses attention on a firm’s cash situation

• A firm may be profitable and short of cash

– Unlike the balance sheet and income statement, cash flow statements are independent of accounting methods • The IRS uses accounting income to compute

tax, so accounting rules have a second order effect on cash flows through taxes

11

GPC Cash Flow Statement, forthe Year ending Dec 31, 2xx0

Net income 23.4 + Depreciation 30.0 - Increase in acc rec (10.0) - Increase in invent (30.0) + Increase in acc rec 12.0 *Total cash from operations 25.4

- Invest in new ppe (90.0) *Cash flow invest' activities (90.0)

-Div paid (10.0) + Inc short-term debt 94.6 *Cash flow from financing 84.6

**Chng cash & mkt securities 20.0

12

GPC Balance Sheet at Dec 31, 2xx1

2xx0 2xx1 ChangeAssetsCash & mkt'ble secs 100.0 120.0 20.0 Receivables 50.0 60.0 10.0 Inventories 150.0 180.0 30.0 *Current assets 300.0 360.0 60.0

Pp&e 400.0 490.0 90.0 Acc depreciation (100.0) (130.0) (30.0) *Net pp&e 300.0 360.0 60.0

**Total Assets 600.0 720.0 120.0

Liabilities & EquityAccounts payable 60.0 72.0 12.0 Short-term debt 90.0 184.6 94.6 *Current liabilities 150.0 256.6 106.6

Long-term debt 150.0 150.0 - **Total liabilities 300.0 406.6 106.6

Paid-in capital 200.0 200.0 - Retained earnings 100.0 113.4 13.4 *Shareholders equ 300.0 313.4 13.4

Liab + Shareholder 600.0 720.0 120.0

GPC Income Statement for Year Ending 2xx1

Sales revenues 200.0 Cost of goods sold (110.0) *Gross margin 90.0

Gen sell, & admin exp (30.0) *Operating income 60.0

Interest expense (21.0) *Taxable income 39.0

Income tax (15.6) *Net income 23.4

Allocation to divs (10.0) *Chg retained earn 13.4

GPC Cash Flow Statement, forthe Year ending Dec 31, 2xx0

Net income 23.4 + Depreciation 30.0 - Increase in acc rec (10.0) - Increase in invent (30.0) + Increase in acc pay 12.0 *Total cash from operations 25.4

- Invest in new ppe (90.0) *Cash flow invest' activities (90.0)

-Div paid (10.0) + Inc short-term debt 94.6 *Cash flow from financing 84.6

**Chng cash & mkt securities 20.0

13

3.3 Market v. Book Values

• Not all assets and liabilities are included, and others are understate and/or overstated– Intangible assets such as patents may have

some value included, but brand loyalty, technological know-how, or a highly trained loyal workforce will not be valued. Goodwill may be included, but soon loses its connection to market value because of accounting depreciation and market fluctuations

– Some contingent liabilities such as law-suits are not routinely disclosed, or only disclosed in the notes

– Accountants are beginning to mark-to-market the assets of pension funds

14

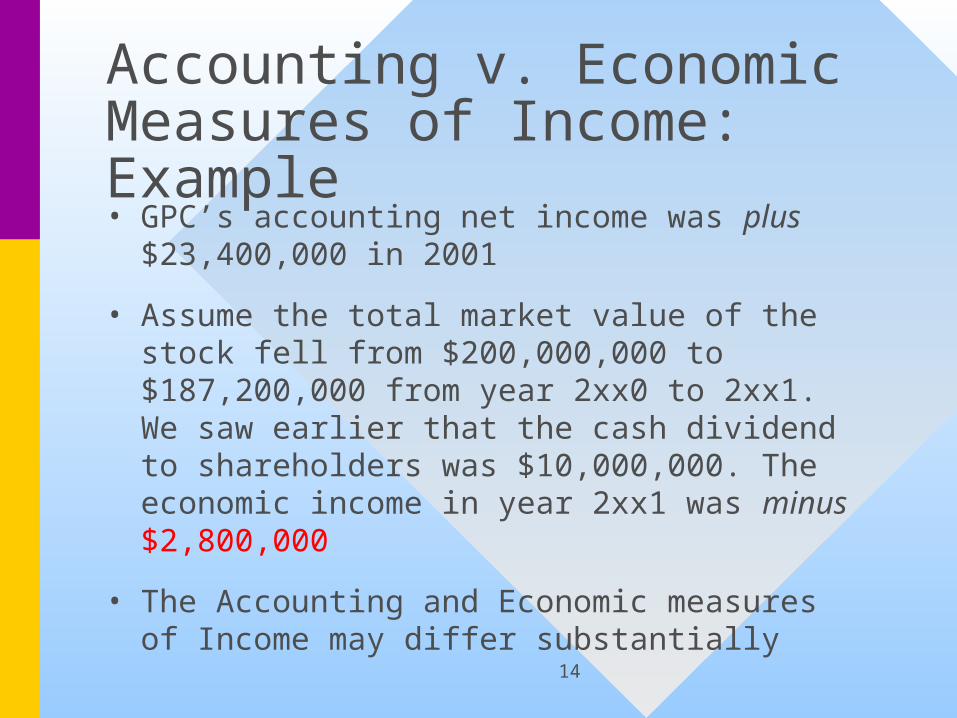

Accounting v. Economic Measures of Income: Example• GPC’s accounting net income was plus

$23,400,000 in 2001

• Assume the total market value of the stock fell from $200,000,000 to $187,200,000 from year 2xx0 to 2xx1. We saw earlier that the cash dividend to shareholders was $10,000,000. The economic income in year 2xx1 was minus $2,800,000

• The Accounting and Economic measures of Income may differ substantially

15

3.5 Returns to Shareholders v. Return on Equity• Recall our definition in Chapter 2 of the

holding period return, and compare this with the economic measure of income

4.1200$

8.2$

Re

MillionMillion

StartPricecomeEconomicIn

StartPricendsCashDivideStartPriceEndPrice

turn

• This is the Total Shareholder Return

16

Returns to Shareholders v. Return on Equity (Continued)• Traditionally, corporate performance has

been measured by Return on Equity, ROE

%8.7300$

4.23$

Million

Million

rsEquityShareHolde

NetIncome

rsEquityShareHolde

IncomeAccountingROE

17

Returns to Shareholders v. Return on Equity (Conclusion)

• Thus, we see that there is no correspondence between a firm's ROE in any year & the total rate of return earned by shareholders on their investment in the company’s stock

18

3.6 Analysis using Financial Ratios• Despite the differences in accounting

and financial principles, the published accounts of a firm yield clues about its financial condition

• Five aspects of a firms performance:• Profitability

• Asset turnover

• Financial leverage

• Liquidity

• Market value

19

Profitability

%6.72/4.313300

4.23

sEquityr'StockHolde

NetIncome (RoE)Equity on Return

%1.92/720600

60

alAssetsAverageTot

EBIT (RoA) Assetson Return

%30200

60Sales

EBIT (RoS) Saleson Return

20

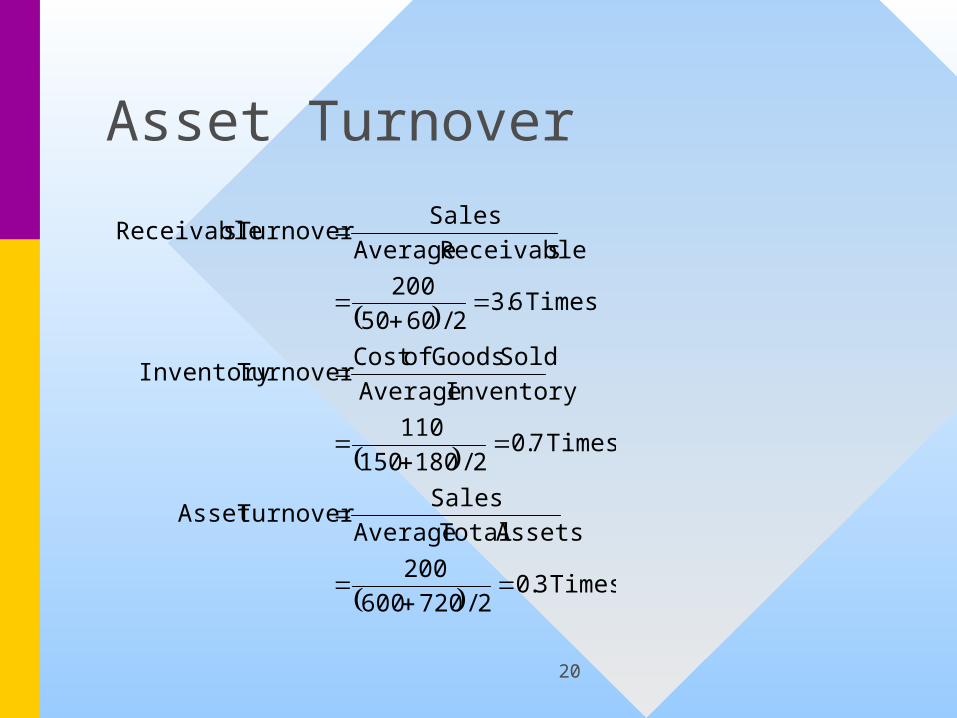

Asset Turnover

Times 3.02/720600

200

Assets Total Average

Sales Turnover Asset

Times 7.02/180150

110

Inventory Average

Sold Goods ofCost Turnover Inventory

Times 6.32/6050

200

sReceivable Average

Sales Turnover sReceivable

21

LiquidityLiquidity

CCurrent Assets

Ciurrent Liabilities

Quick or Acid TestCash REC.

Current Liab.

Times

urrent Times

360

256 614

180

256 6

0 7

..

.

.

22

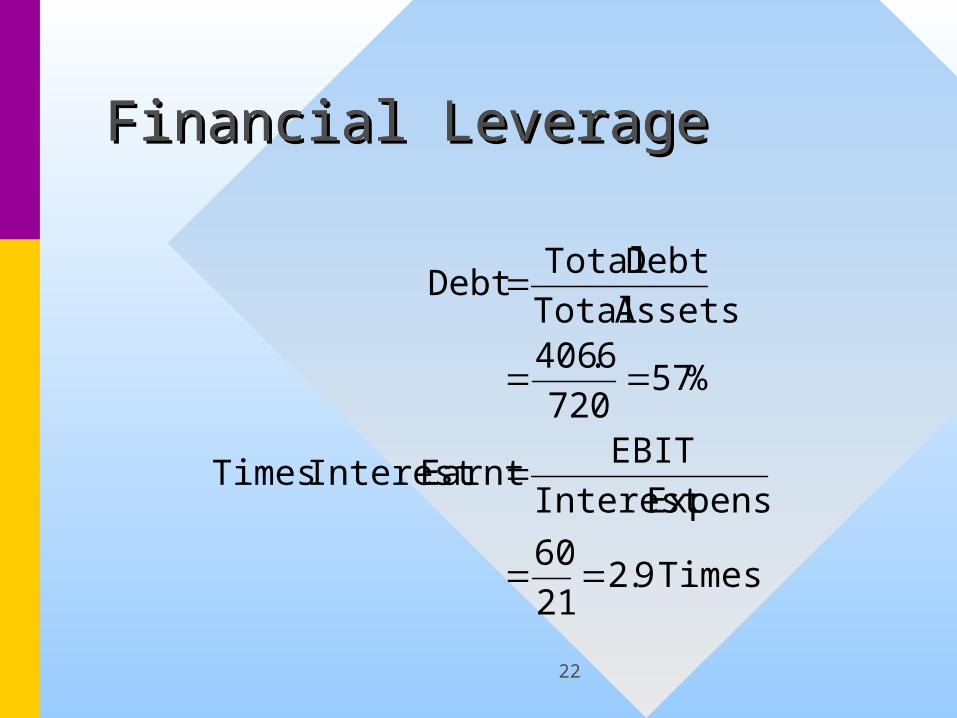

Financial LeverageFinancial LeverageFinancial Leverage

Times 9.221

60

ExpenseInterest

EBIT Earnt Interest Times

%57720

6.406Assets Total

Debt Total Debt

23

Market Value

6.04.313

20.187

Shareper ValueBook

Shareper Price Book Market to

0.84.23

2.187

Shareper Earnings

SharePer Price Earnings toPrice

24

Ratio Comparisons• Establish Your Perspective

• Shareholder

• Employee, Management, or Union

• Creditor

• Predator, Customer, Supplier, Competitor, Trade Association

• Benchmarks• Other companies ratios

• The firm’s historical ratios

• Data extracted from financial markets

• Sources• Dun & Bradstreet, Robert Morris, Commerce

Department's Quarterly Financial Report, Trade Associations

25

Relationships Amongst Ratios• It is sometimes valuable to decompose

ratios into sums, differences, products and quotients of other ratios. Many such schemes start with:

TurnoverAsset * saleson Return

*

Assets

Sales

Sales

EBIT

Assets

EBITRoA

26

Ratio Analysis Limitations

• Ratio analysis indicates where you might profitably focus your attention, but it can also mislead you– Look for collaborating evidence for the hypotheses you

form from the ratios

• Sound long-term goals of a firm may cause ratios to look awful. Management-by-ratios may not be in the firms long-term interest

• Companies in the same industry may have very different distribution channels, and accounting methods, leading to markedly different ratios that are none-the-less appropriate to each company

27

Comment:

• Always keep in mind that financial statements are prepared according to accounting standards and traditions, and that they do not fully satisfy the needs of a financial analysts

• They do yield useful information if used with care and understanding

28

Effect of Financial Effect of Financial LeverageLeverage

• Financial leverage simply means the Financial leverage simply means the use of borrowed moneyuse of borrowed money– Shareholders of a firm use financial Shareholders of a firm use financial

leverage to boost their ROEleverage to boost their ROE• This increases the sensitivity of ROE to This increases the sensitivity of ROE to

fluctuations in the firm’s underlying fluctuations in the firm’s underlying profitability as measured by its ROAprofitability as measured by its ROA

29

IllustrationIllustration

• (Table 3.7 & 3.8 of textbook)(Table 3.7 & 3.8 of textbook)– Consider two firms that are identical Consider two firms that are identical

except that Nodebt is financed using except that Nodebt is financed using $1,000,000 of equity and Halfdebt is $1,000,000 of equity and Halfdebt is financed using $500,000 of equity and financed using $500,000 of equity and $500,000 of debt$500,000 of debt

– further assume that the EBIT of both further assume that the EBIT of both firms is $120,000 and tax is 40%firms is $120,000 and tax is 40%

30

Case: Borrow at 10%Case: Borrow at 10%

Nodebt HalfdebtEBIT 120,000 120,000Interest 0 50,000Taxable Income 120,000 70,000Tax 48,000 28,000Net Income 72,000 42,000Equity 1,000,000 500,000ROE 7.20% 8.40%

31

Case: Borrow at 10%: Case: Borrow at 10%: Effect of Business Cycle Effect of Business Cycle on ROEon ROE

Economic ROA ROE ROEConditions Nodebt Halfdebt Bad Year 1% 0.6% -4.8% Normal Year 12% 7.2% 8.4% Good Year 30% 18.0% 30.0%

32

Conclusion:Conclusion:

• From the perspective ofFrom the perspective of– Creditors: increasing debt is Creditors: increasing debt is

unambiguously harmful, and bond unambiguously harmful, and bond rating agencies will downgrade the rating agencies will downgrade the firm’s securitiesfirm’s securities

– Shareholders: may benefit, depending Shareholders: may benefit, depending on the sign of (ROA-interest rate) and on the sign of (ROA-interest rate) and ROAROA

33

3.7 Financial Planning 3.7 Financial Planning ProcessProcess

• This section navigates us through the This section navigates us through the financial planning process, using the financial planning process, using the historical financial statements for a historical financial statements for a manufacturing firm as our manufacturing firm as our embarkation pointembarkation point

• Later, we discuss short-term planning Later, we discuss short-term planning and the management of working and the management of working capitalcapital

34

The Financial Planning The Financial Planning ProcessProcess

– Financial planning is a Financial planning is a dynamicdynamic process process that follows a cycle of making plans, that follows a cycle of making plans, implementing them, and revising them implementing them, and revising them in the light of actual resultsin the light of actual results

35

The Financial Planning The Financial Planning ProcessProcess

– Starting point is the strategic planStarting point is the strategic plan• Strategy guides the financial planning Strategy guides the financial planning

process by establishing overall business process by establishing overall business development guidelines and growth targetsdevelopment guidelines and growth targets

• Which businesses does the firm want to Which businesses does the firm want to – enterenter– expandexpand– contractcontract– exitexit

• and how quickly?and how quickly?

36

The Financial Planning The Financial Planning ProcessProcess

– Length of the planning horizonLength of the planning horizon• The longer the financial plan, the less The longer the financial plan, the less

detailed it should be (in general)detailed it should be (in general)

• The revision of a financial plan is The revision of a financial plan is generally a function of the length of the generally a function of the length of the planning horizonplanning horizon

– Short-term plans are revised frequently, Short-term plans are revised frequently, long-term plans are revised much less long-term plans are revised much less frequentlyfrequently

37

The Financial Planning The Financial Planning ProcessProcess

– The financial planning horizon may be The financial planning horizon may be broken down into several steps:broken down into several steps:• Management forecasts the key external Management forecasts the key external

factors, including level of economic factors, including level of economic activity, inflation, interest rates, and the activity, inflation, interest rates, and the competition’s output and pricescompetition’s output and prices

• Based on above, they next forecast Based on above, they next forecast revenues, expenses, cash flows, and revenues, expenses, cash flows, and implied need for external financingimplied need for external financing

38

The Financial Planning The Financial Planning ProcessProcess

• Specific performance targets are Specific performance targets are generated for the divisions, functions and generated for the divisions, functions and key individuals of the firmkey individuals of the firm

• Periodic measurements of performance Periodic measurements of performance are made, and compared to the plan in are made, and compared to the plan in order to correct either the plan or order to correct either the plan or performanceperformance

• Periodically, key personnel are Periodically, key personnel are counseled, rewarded or punished, and a counseled, rewarded or punished, and a new iteration is instigatednew iteration is instigated

39

The Financial Planning The Financial Planning Process: NotesProcess: Notes

– Some variables must be forecast well Some variables must be forecast well in advance because exploitation in advance because exploitation requires a long lead-time, others may requires a long lead-time, others may be reacted to immediatelybe reacted to immediately

– Some variables are highly volatile, and Some variables are highly volatile, and can’t be forecast effectively, so the can’t be forecast effectively, so the best we can do is to plan for the best we can do is to plan for the unknown (contingency planning)unknown (contingency planning)

40

The Financial Planning The Financial Planning Process: NotesProcess: Notes

– Planning horizons must be appropriatePlanning horizons must be appropriate

– For a magazine stand, a two year planning For a magazine stand, a two year planning horizon may be far too longhorizon may be far too long

– A pharmaceutical business (with long new-A pharmaceutical business (with long new-plant construction lead-times, and long plant construction lead-times, and long drug development/testing/approval drug development/testing/approval procedures) needs a planning horizon that procedures) needs a planning horizon that may be as long a ten yearsmay be as long a ten years

41

The Financial Planning The Financial Planning Process: NotesProcess: Notes

– A plan should always lead to A plan should always lead to decisionsdecisions that justify the cost of its preparationthat justify the cost of its preparation• Proper planning is, in essence, part of Proper planning is, in essence, part of

the process of decision making. Any the process of decision making. Any part of a plan that does not lead to a part of a plan that does not lead to a decision is probably a waste of decision is probably a waste of managerial resourcesmanagerial resources

42

3.8 Constructing a 3.8 Constructing a Financial Planning ModelFinancial Planning Model

• The next slide shows the history of The next slide shows the history of GPCGPC

43

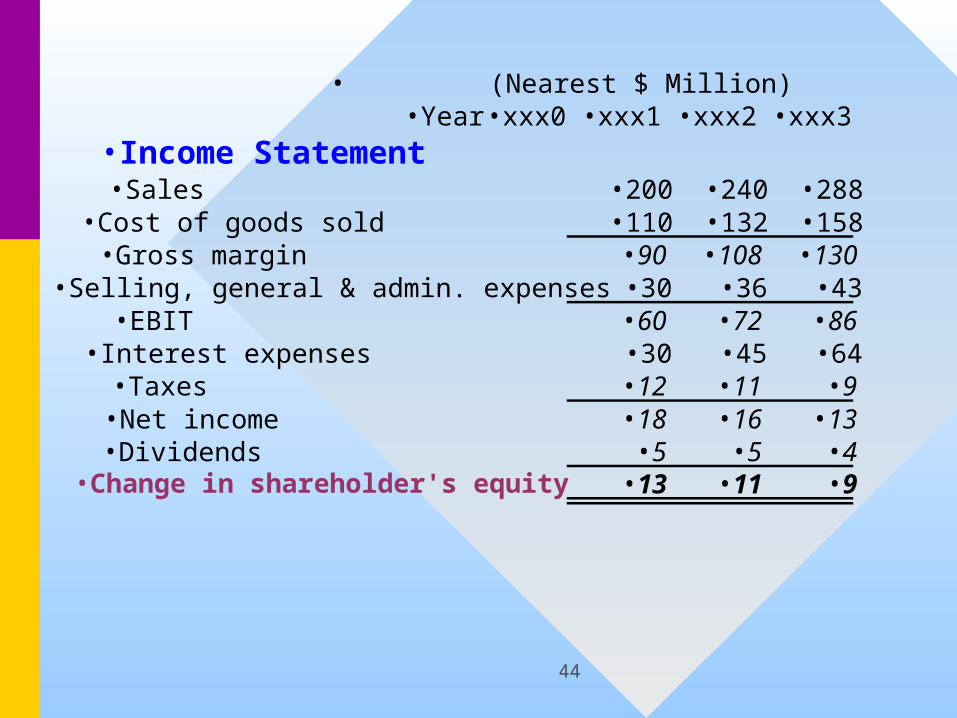

•GPC Financial Statements, Years xxx1 - xxx3• (Nearest $ Million) • (Percent of Year's Sales)

•Year •xxx0 •xxx1 •xxx2 •xxx3 •xxx1 •xxx2 •xxx3•Income Statement

•Sales •200 •240 •288 •100.0% •100.0% •100.0%•Cost of goods sold •110 •132 •158 •55.0% •55.0% •55.0%•Gross margin •90 •108 •130 •45.0% •45.0% •45.0%•Selling, general & admin. expenses •30 •36 •43 •15.0% •15.0% •15.0%•EBIT •60 •72 •86 •30.0% •30.0% •30.0%•Interest expenses •30 •45 •64 •15.0% •18.8% •22.2%•Taxes •12 •11 •9 •6.0% •4.5% •3.1%•Net income •18 •16 •13 •9.0% •6.7% •4.7%•Dividends •5 •5 •4 •2.7% •2.0% •1.4%•Change in shareholder's equity •13 •11 •9 •6.3% •4.7% •3.3%

•Balance Sheet•Assets:• Cash & equivalents •10 •12 •14 •17 •6.0% •6.0% •6.0%• Receivables •40 •48 •58 •69 •24.0% •24.0% •24.0%• Inventories •50 •60 •72 •86 •30.0% •30.0% •30.0%• Property, Plant & equipment •500 •600 •720 •864 •300.0% •300.0% •300.0%• Total Assets •600 •720 •864 •1037 •360.0% •360.0% •360.0%•Liabilities:• Payables •30 •36 •43 •52 •18.0% •18.0% •18.0%• Short-term debt •120 •221 •347 •502 •110.7% •144.6% •174.2%• Long-term debt •150 •150 •150 •150 •75.0% •62.5% •52.1%• Total Liabilities •300 •407 •540 •704 •203.7% •225.1% •244.3%•Shareholder's equity •300 •313 •324 •333 •156.3% •134.9% •115.7%

44

• (Nearest $ Million) •Year •xxx0 •xxx1 •xxx2 •xxx3

•Income Statement•Sales •200 •240 •288•Cost of goods sold •110 •132 •158•Gross margin •90 •108 •130•Selling, general & admin. expenses •30 •36 •43•EBIT •60 •72 •86•Interest expenses •30 •45 •64•Taxes •12 •11 •9•Net income •18 •16 •13•Dividends •5 •5 •4•Change in shareholder's equity •13 •11 •9

45

Balance SheetAssets: Cash & equivalents 10 12 14 17 Receivables 40 48 58 69 Inventories 50 60 72 86 Property, Plant & equipment 500 600 720 864 Total Assets 600 720 864 1037Liabilities: Payables 30 36 43 52 Short-term debt 120 221 347 502 Long-term debt 150 150 150 150 Total Liabilities 300 407 540 704Shareholder's equity 300 313 324 333

46

• (Percent of Year's Sales)•Year •xxx1 •xxx2 •xxx3

•Income StatementSales •100.0% •100.0% •100.0%Cost of goods sold •55.0% •55.0% •55.0%Gross margin •45.0% •45.0% •45.0%Selling, general & admin exp. •15.0% •15.0% •15.0%EBIT •30.0% •30.0% •30.0%Interest expenses •15.0% •18.8% •22.2%Taxes •6.0% •4.5% •3.1%Net income •9.0% •6.7% •4.7%Dividends •2.7% •2.0% •1.4%Change in equity •6.3% •4.7% •3.3%

47

Balance SheetAssets: Cash & equivalents 6.0% 6.0% 6.0% Receivables 24.0% 24.0% 24.0% Inventories 30.0% 30.0% 30.0% Property, Plant & equipment 300.0% 300.0% 300.0% Total Assets 360.0% 360.0% 360.0%Liabilities: Payables 18.0% 18.0% 18.0% Short-term debt 110.7% 144.6% 174.2% Long-term debt 75.0% 62.5% 52.1% Total Liabilities 203.7% 225.1% 244.3%Shareholder's equity 156.3% 134.9% 115.7%

48

Constructing a Financial Constructing a Financial Planning ModelPlanning Model

• Percent-of-sales methodPercent-of-sales method– First examine which items in the First examine which items in the

income statement have maintained a income statement have maintained a fixed ratio to salesfixed ratio to sales• This enables us to decide which items This enables us to decide which items

should be forecast on projected sales, should be forecast on projected sales, and which need to be forecast on and which need to be forecast on another basisanother basis

49

Constructing a Financial Constructing a Financial Planning ModelPlanning Model

• Percent-of-sales methodPercent-of-sales method– The second step is to forecast salesThe second step is to forecast sales

• This is a major exercise, but we will This is a major exercise, but we will assume that sales will continue to grow assume that sales will continue to grow at 20% next year (as it has in the past)at 20% next year (as it has in the past)

50

Constructing a Financial Constructing a Financial Planning ModelPlanning Model

• Percent-of-sales methodPercent-of-sales method– The third step is to forecast those The third step is to forecast those

items that have been assumed to vary items that have been assumed to vary with saleswith sales

51

Constructing a Financial Constructing a Financial Planning ModelPlanning Model

• Percent-of-sales methodPercent-of-sales method– The fourth and final step is to forecast The fourth and final step is to forecast

the missing items that have the missing items that have notnot been been assumed to vary with salesassumed to vary with sales

– We need some assumptions:We need some assumptions:

52

Constructing a Financial Constructing a Financial Planning ModelPlanning Model

• Assumptions:Assumptions:– Interest rate on long-term debt is 8%, and Interest rate on long-term debt is 8%, and

on short-term debt is 15%on short-term debt is 15%

– To avoid complexity, we assume that To avoid complexity, we assume that interest is computed on the yearend long- interest is computed on the yearend long- and short-term balances (we can re-address and short-term balances (we can re-address this later)this later)

– interest = 0.08*501.72 + 0.15*150 = 87.26interest = 0.08*501.72 + 0.15*150 = 87.26

53

Constructing a Financial Constructing a Financial Planning ModelPlanning Model

– The income statement may now be The income statement may now be constructed given the dividend pay-out constructed given the dividend pay-out ratio and tax rate (30% and 40%)ratio and tax rate (30% and 40%)

– The change in equity is added to the The change in equity is added to the equity for year xxx3, to give the new equity for year xxx3, to give the new balance for year xxx4balance for year xxx4

– ““Total assets” is available, so the “Total Total assets” is available, so the “Total liabilities” may now be computedliabilities” may now be computed

54

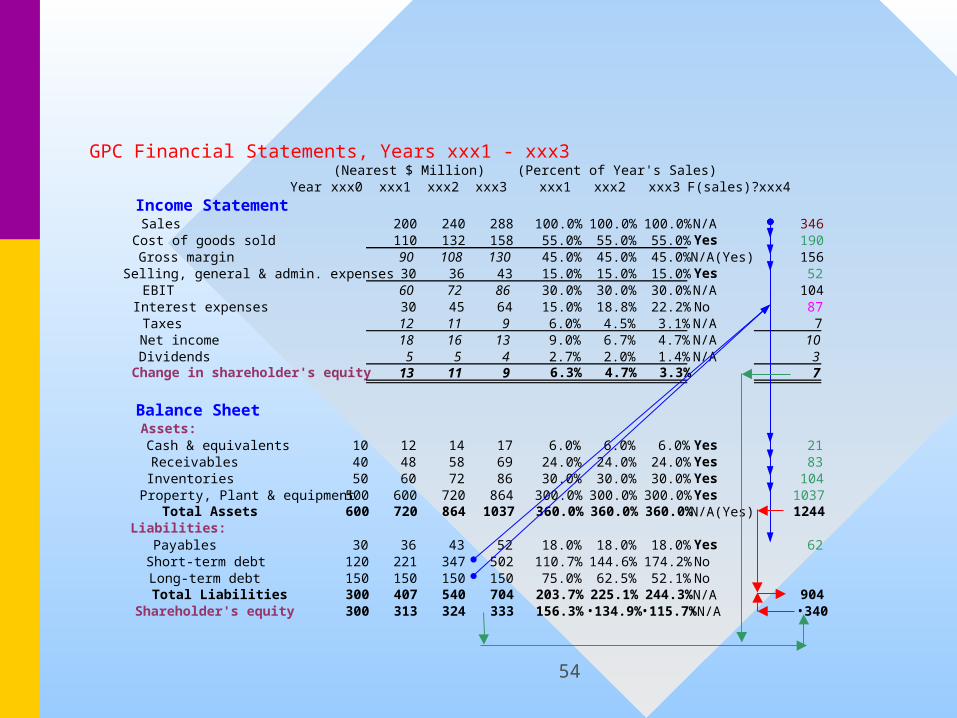

GPC Financial Statements, Years xxx1 - xxx3 (Nearest $ Million) (Percent of Year's Sales)

Year xxx0 xxx1 xxx2 xxx3 xxx1 xxx2 xxx3 F(sales)? xxx4

Income StatementSales 200 240 288 100.0% 100.0% 100.0% N/A 346Cost of goods sold 110 132 158 55.0% 55.0% 55.0% Yes 190Gross margin 90 108 130 45.0% 45.0% 45.0% N/A(Yes) 156

Selling, general & admin. expenses 30 36 43 15.0% 15.0% 15.0% Yes 52EBIT 60 72 86 30.0% 30.0% 30.0% N/A 104Interest expenses 30 45 64 15.0% 18.8% 22.2% No 87

Taxes 12 11 9 6.0% 4.5% 3.1% N/A 7Net income 18 16 13 9.0% 6.7% 4.7% N/A 10Dividends 5 5 4 2.7% 2.0% 1.4% N/A 3Change in shareholder's equity 13 11 9 6.3% 4.7% 3.3% 7

Balance SheetAssets: Cash & equivalents 10 12 14 17 6.0% 6.0% 6.0% Yes 21 Receivables 40 48 58 69 24.0% 24.0% 24.0% Yes 83 Inventories 50 60 72 86 30.0% 30.0% 30.0% Yes 104 Property, Plant & equipment 500 600 720 864 300.0% 300.0% 300.0% Yes 1037

Total Assets 600 720 864 1037 360.0% 360.0% 360.0% N/A(Yes) 1244Liabilities: Payables 30 36 43 52 18.0% 18.0% 18.0% Yes 62 Short-term debt 120 221 347 502 110.7% 144.6% 174.2% No Long-term debt 150 150 150 150 75.0% 62.5% 52.1% No Total Liabilities 300 407 540 704 203.7% 225.1% 244.3% N/A 904Shareholder's equity 300 313 324 333 156.3% •134.9% •115.7%•N/A •340

55

Example CompletedExample Completed

– We complete the balance sheet by We complete the balance sheet by recognizing that there are only two recognizing that there are only two accounts that need to be estimated, Short-accounts that need to be estimated, Short-term debt, and Long-term debtterm debt, and Long-term debt

– The sum is then 904 (Liabilities) - 62 The sum is then 904 (Liabilities) - 62 (Payables) = $842 Million(Payables) = $842 Million

– Assume no change in long-term debtAssume no change in long-term debt

– Short-term debt =$842 - 150 = $692 Short-term debt =$842 - 150 = $692 millionmillion

56

GPC Financial Statements, Years xxx1 - xxx3 (Nearest $ Million)

Year xxx0 xxx1 xxx2 xxx3 xxx4

Income StatementSales 200 240 288 346Cost of goods sold 110 132 158 190Gross margin 90 108 130 156Selling, general & admin. expenses 30 36 43 52EBIT 60 72 86 104Interest expences 30 45 64 87Taxes 12 11 9 7Net income 18 16 13 10Dividends 5 5 4 3Change in shareholder's equity 13 11 9 7

57

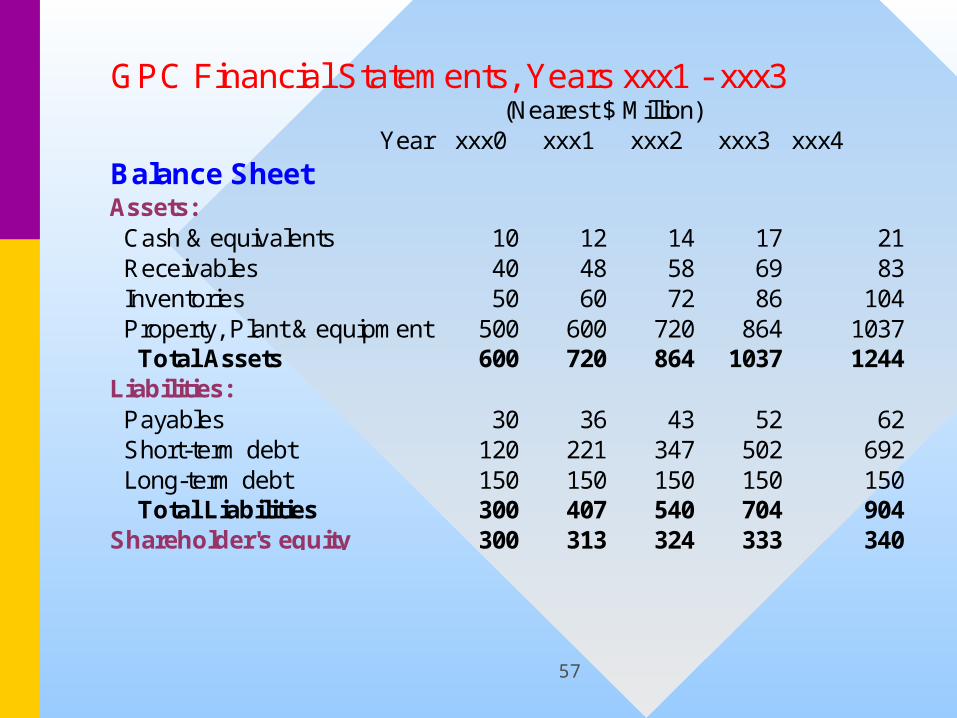

GPC Financial Statements, Years xxx1 - xxx3 (Nearest $ Million)

Year xxx0 xxx1 xxx2 xxx3 xxx4

Balance SheetAssets: Cash & equivalents 10 12 14 17 21 Receivables 40 48 58 69 83 Inventories 50 60 72 86 104 Property, Plant & equipment 500 600 720 864 1037 Total Assets 600 720 864 1037 1244Liabilities: Payables 30 36 43 52 62 Short-term debt 120 221 347 502 692 Long-term debt 150 150 150 150 150 Total Liabilities 300 407 540 704 904Shareholder's equity 300 313 324 333 340

58

3.9 Growth & Need for 3.9 Growth & Need for External FinanceExternal Finance

• In order to grow by 20%, the firm In order to grow by 20%, the firm will need an additional 692 - 502 = will need an additional 692 - 502 = $190 million in external funding (all $190 million in external funding (all short-term funding in the example)short-term funding in the example)

59

Some Questions:Some Questions:

• What external funds are required to What external funds are required to support a sales growth rate, g, of 30%?support a sales growth rate, g, of 30%?

• If I have external funds available equal If I have external funds available equal to $30 million, what level of sales to $30 million, what level of sales growth does this support?growth does this support?

60

External Funds Needed for Growth

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Growth Rate

Ext

ern

al F

un

ds

Nee

ded

61

3.10 Working Capital 3.10 Working Capital ManagementManagement

• Many businesses that fail do so Many businesses that fail do so because of poor management of because of poor management of working capital, not poor working capital, not poor profitability profitability

• Working capitalWorking capital Current assets - current liabilitiesCurrent assets - current liabilities

62

Efficient Management of Efficient Management of Working Capital Principle:Working Capital Principle:

– Minimize the investment in non-earning Minimize the investment in non-earning assets such as assets such as • receivablesreceivables• inventoriesinventories

– Maximizing the use of free credit such Maximizing the use of free credit such as as • prepayments by customersprepayments by customers• accrued wagesaccrued wages• accounts payableaccounts payable

63

Cash Cycle TimeCash Cycle Time

• Cash Cycle Time = Inventory period Cash Cycle Time = Inventory period + receivable period - payables + receivable period - payables periodperiod

64

3.11 Liquidity and Cash 3.11 Liquidity and Cash BudgetingBudgeting

– A firm may be profitable, and have a A firm may be profitable, and have a sizable net worth, but if it is illiquid it will sizable net worth, but if it is illiquid it will be damaged by forced assets sales and be damaged by forced assets sales and by laying-off trained workersby laying-off trained workers

– Banks are much more receptive to Banks are much more receptive to funding a funding a plannedplanned cash shortfall than cash shortfall than funding a shortfall that should have been funding a shortfall that should have been forecastforecast

– Construct a Cash BudgetConstruct a Cash Budget