wrong way risk - silverman tanaka · what is the wrong way risk? epe and pd are not independent •...

TRANSCRIPT

Wrong Way Risk: Short Gamma Exposures

© Silverman Tanaka

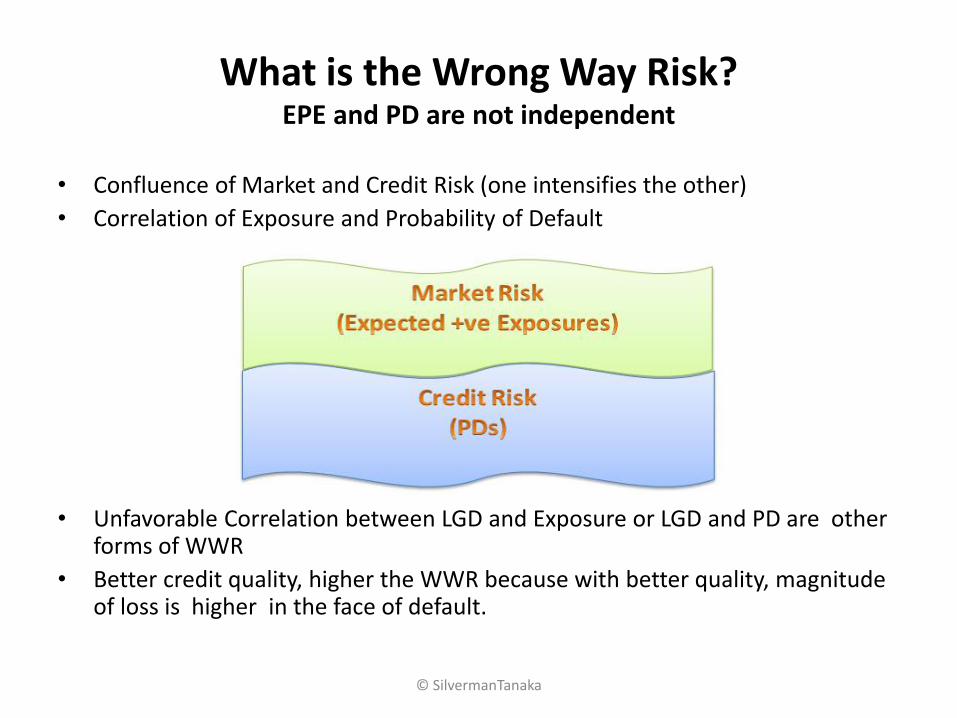

What is the Wrong Way Risk? EPE and PD are not independent

• Confluence of Market and Credit Risk (one intensifies the other)

• Correlation of Exposure and Probability of Default

• Unfavorable Correlation between LGD and Exposure or LGD and PD are other forms of WWR

• Better credit quality, higher the WWR because with better quality, magnitude of loss is higher in the face of default.

© SilvermanTanaka

What is the Wrong Way Risk? +ve Correlation between EPE and PD

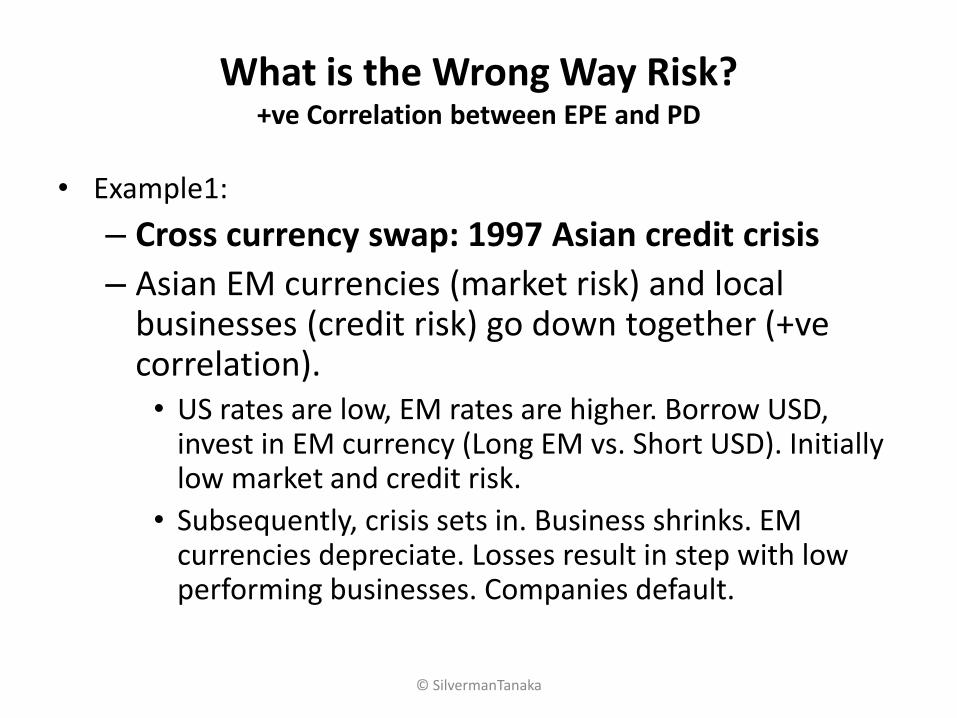

• Example1:

– Cross currency swap: 1997 Asian credit crisis

– Asian EM currencies (market risk) and local businesses (credit risk) go down together (+ve correlation). • US rates are low, EM rates are higher. Borrow USD,

invest in EM currency (Long EM vs. Short USD). Initially low market and credit risk.

• Subsequently, crisis sets in. Business shrinks. EM currencies depreciate. Losses result in step with low performing businesses. Companies default.

© SilvermanTanaka

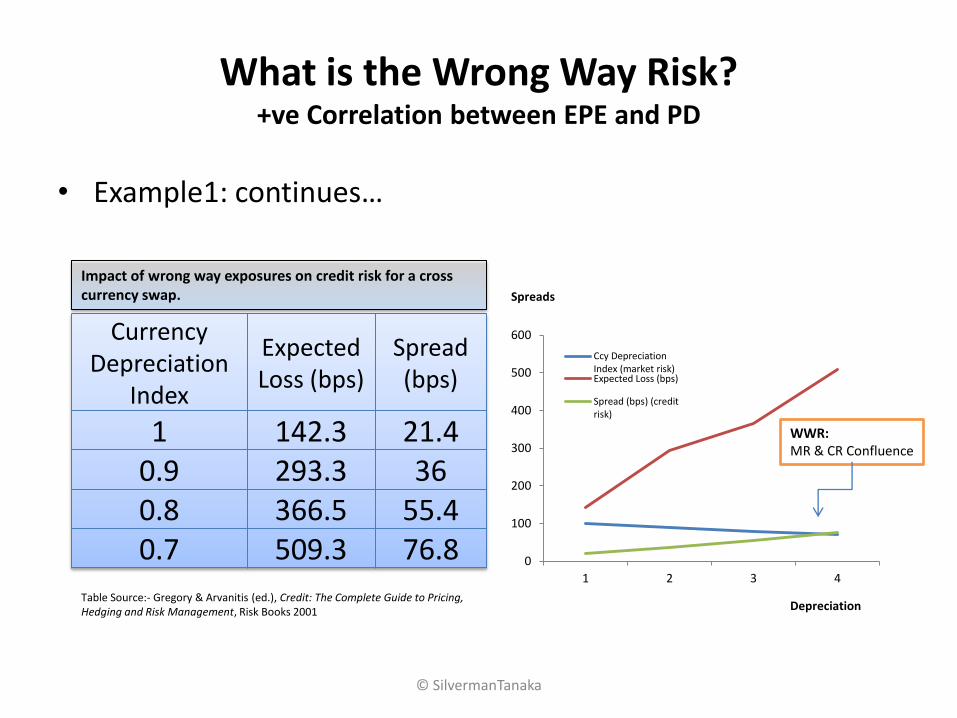

What is the Wrong Way Risk? +ve Correlation between EPE and PD

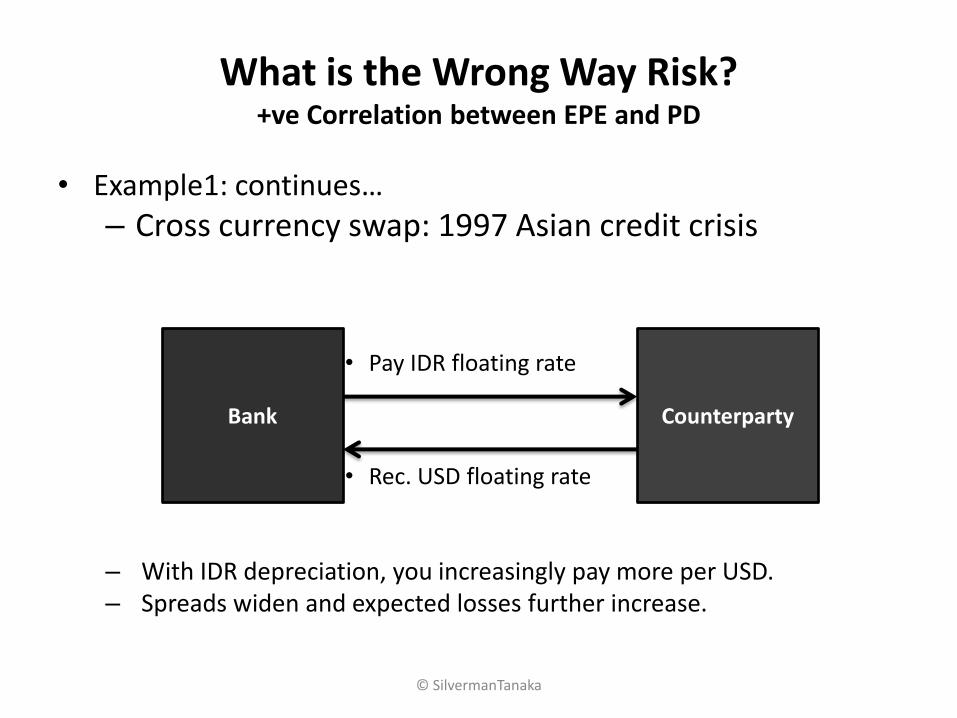

• Example1: continues…

– Cross currency swap: 1997 Asian credit crisis

• Pay IDR floating rate

• Rec. USD floating rate

– With IDR depreciation, you increasingly pay more per USD. – Spreads widen and expected losses further increase.

© SilvermanTanaka

Bank Counterparty

What is the Wrong Way Risk? +ve Correlation between EPE and PD

• Example1: continues…

© SilvermanTanaka

Currency Depreciation

Index

Expected Loss (bps)

Spread (bps)

1 142.3 21.4 0.9 293.3 36 0.8 366.5 55.4 0.7 509.3 76.8 0

100

200

300

400

500

600

1 2 3 4

Ccy DepreciationIndex (market risk)Expected Loss (bps)

Spread (bps) (creditrisk)

Spreads

Depreciation Table Source:- Gregory & Arvanitis (ed.), Credit: The Complete Guide to Pricing, Hedging and Risk Management, Risk Books 2001

Impact of wrong way exposures on credit risk for a cross currency swap.

WWR: MR & CR Confluence

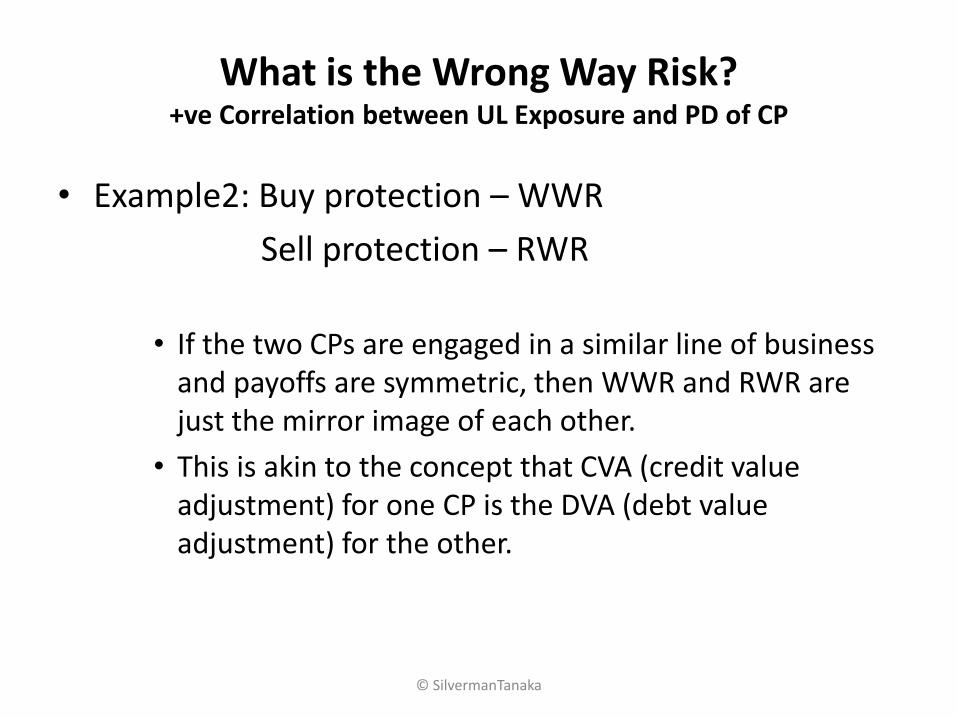

What is the Wrong Way Risk? +ve Correlation between UL Exposure and PD of CP

• Example2: Buy protection – WWR

Sell protection – RWR

© SilvermanTanaka

What is the Wrong Way Risk? +ve Correlation between UL Exposure and PD of CP

• Example2: Buy protection – WWR

Sell protection – RWR

• If the two CPs are engaged in a similar line of business and payoffs are symmetric, then WWR and RWR are just the mirror image of each other.

• This is akin to the concept that CVA (credit value adjustment) for one CP is the DVA (debt value adjustment) for the other.

© SilvermanTanaka

What is the Wrong Way Risk? +ve Correlation between IR Exposure and PD

• Example3: Interest Rate Exposure – double edged sword

– Higher rates scenario: Mortgage pre-payments => Defaults

– Lower rates scenario: Deflationary/recessionary pressure => Defaults

© SilvermanTanaka

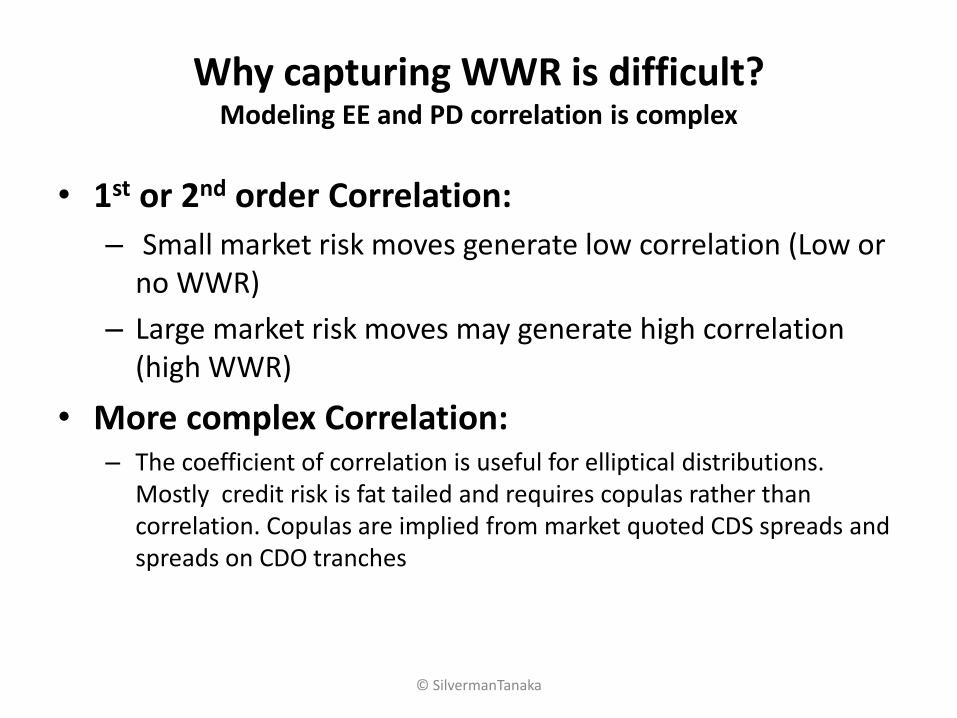

Why capturing WWR is difficult? Modeling EE and PD correlation is complex

• 1st or 2nd order Correlation:

– Small market risk moves generate low correlation (Low or no WWR)

– Large market risk moves may generate high correlation (high WWR)

• More complex Correlation: – The coefficient of correlation is useful for elliptical distributions.

Mostly credit risk is fat tailed and requires copulas rather than correlation. Copulas are implied from market quoted CDS spreads and spreads on CDO tranches

© SilvermanTanaka

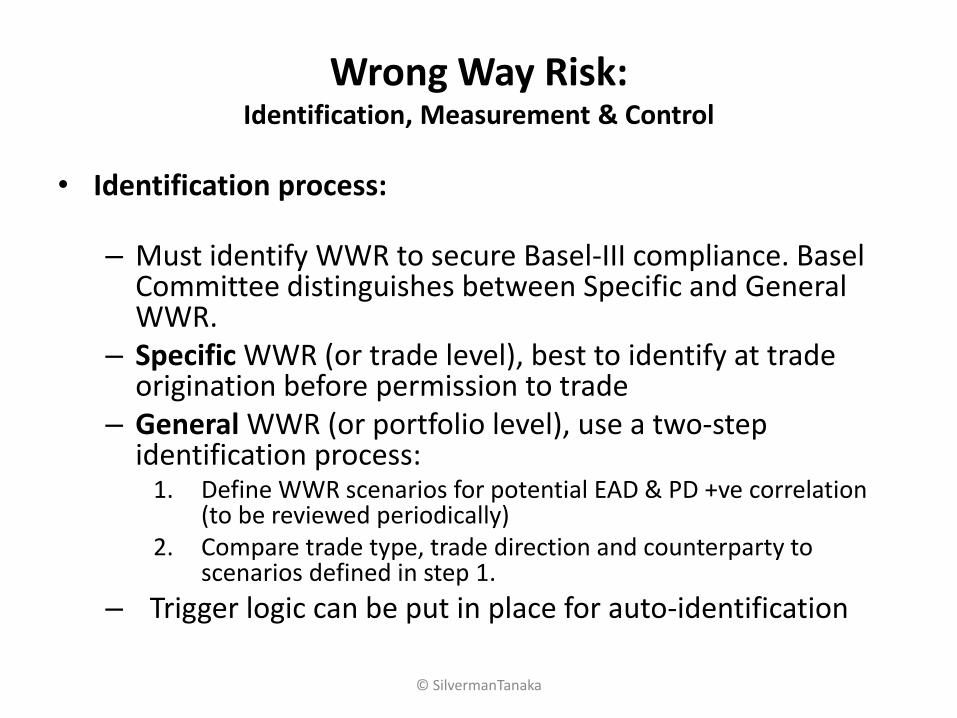

Wrong Way Risk: Identification, Measurement & Control

• Identification process:

– Must identify WWR to secure Basel-III compliance. Basel Committee distinguishes between Specific and General WWR.

– Specific WWR (or trade level), best to identify at trade origination before permission to trade

– General WWR (or portfolio level), use a two-step identification process:

1. Define WWR scenarios for potential EAD & PD +ve correlation (to be reviewed periodically)

2. Compare trade type, trade direction and counterparty to scenarios defined in step 1.

– Trigger logic can be put in place for auto-identification

© SilvermanTanaka

Wrong Way Risk: Identification, Measurement & Control

• Measurement:

– Specific WWR: Typically adjustments are made to Potential Credit Exposure (PCE) to account for WWR – initial adjustment being a percentage of market value, based on observation and experience.

– Separate netting set is defined for the segregated WWR trades at: EAD = 100% x Notional

– General WWR: More difficult to capture.

© SilvermanTanaka

Wrong Way Risk: Identification, Measurement & Control

• Measurement: Data limitations make it difficult to estimate correlations that drive WWR.

– Deterministic measurement of PD & EAD correlation

– Stochastic measurement of PD & EAD correlation

– It may be more cost effective to specifically concentrate on trades that are strongly impacted by WWR rather than trying to measure the entire portfolio.

– Another approach is to measure WWR via stress testing the PD and exposure correlation.

© SilvermanTanaka

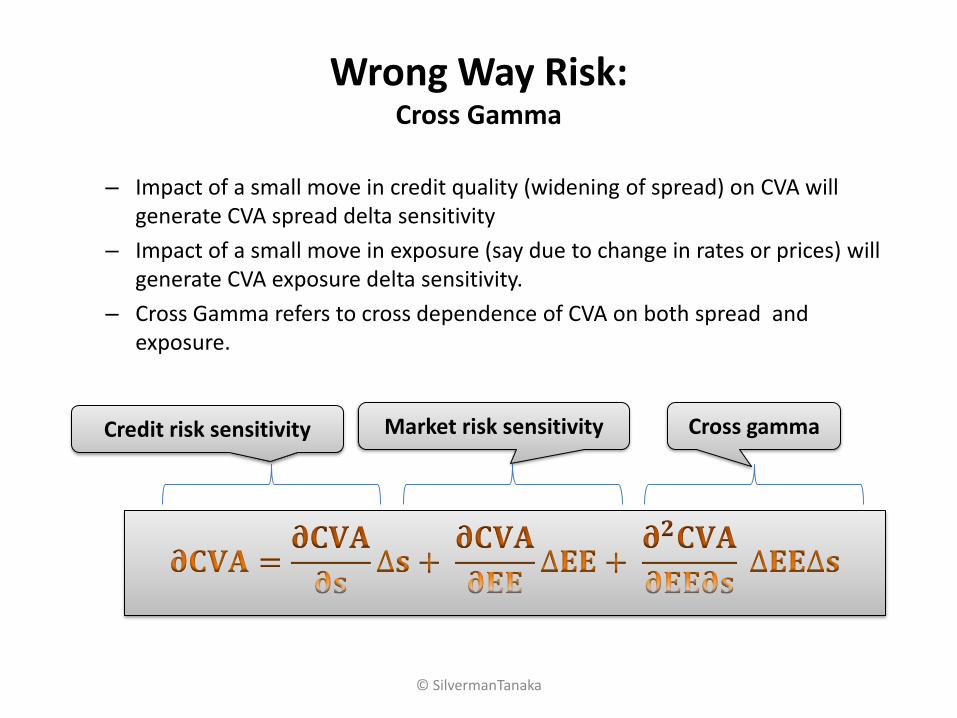

Wrong Way Risk: Cross Gamma

– Impact of a small move in credit quality (widening of spread) on CVA will generate CVA spread delta sensitivity

– Impact of a small move in exposure (say due to change in rates or prices) will generate CVA exposure delta sensitivity.

– Cross Gamma refers to cross dependence of CVA on both spread and exposure.

© SilvermanTanaka

Cross gamma Market risk sensitivity Credit risk sensitivity

Wrong Way Risk: Identification, Measurement & Control

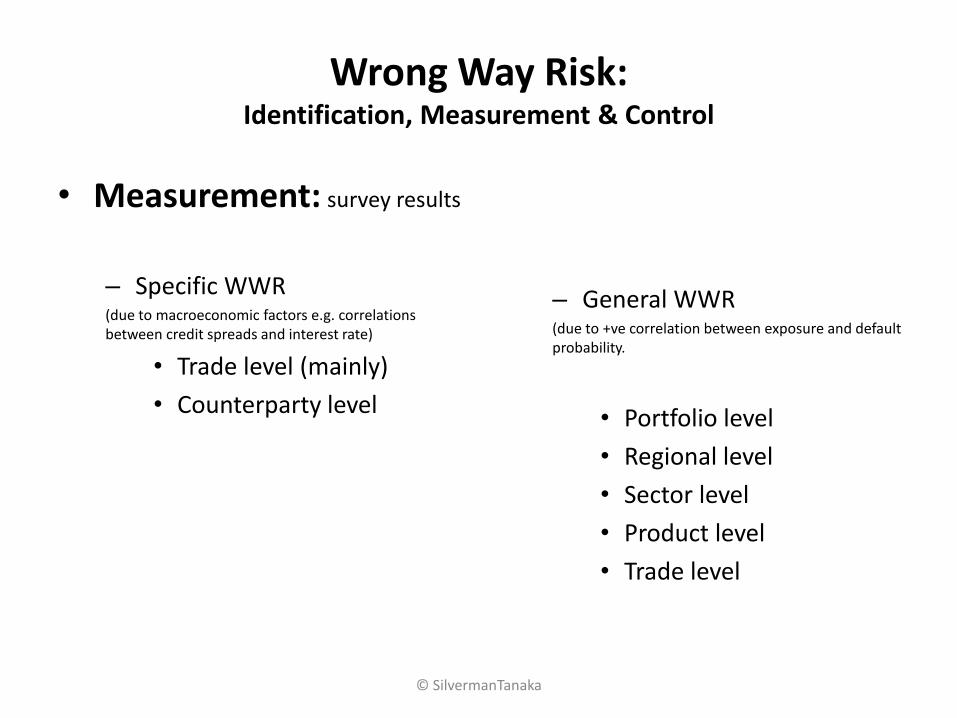

• Measurement: survey results

– Specific WWR (due to macroeconomic factors e.g. correlations between credit spreads and interest rate)

• Trade level (mainly)

• Counterparty level

© SilvermanTanaka

– General WWR (due to +ve correlation between exposure and default probability.

• Portfolio level

• Regional level

• Sector level

• Product level

• Trade level

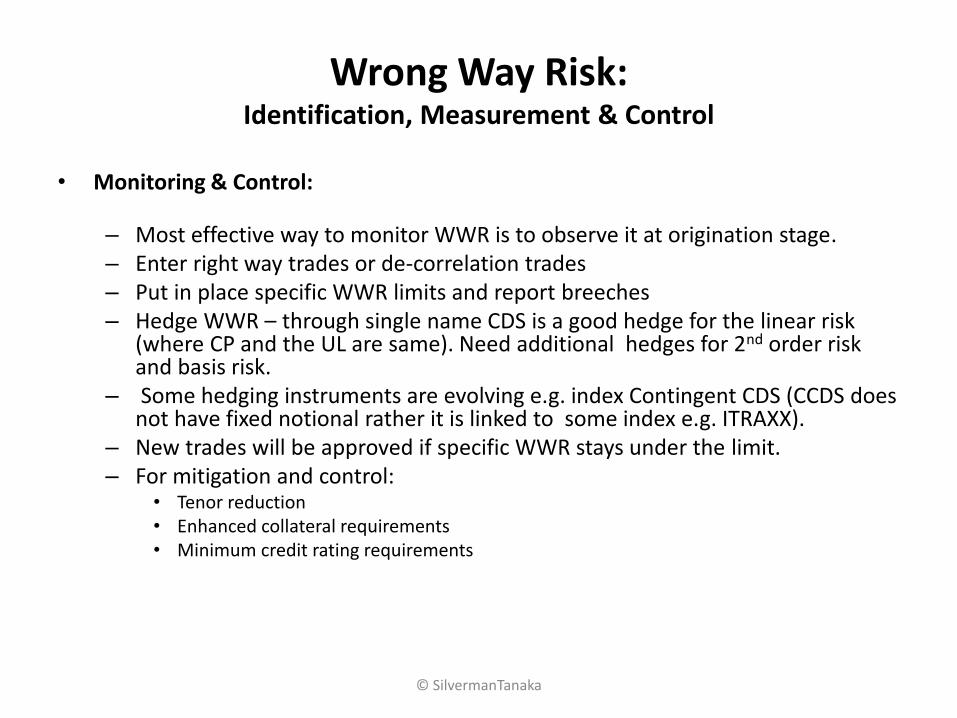

Wrong Way Risk: Identification, Measurement & Control

• Monitoring & Control:

– Most effective way to monitor WWR is to observe it at origination stage. – Enter right way trades or de-correlation trades – Put in place specific WWR limits and report breeches – Hedge WWR – through single name CDS is a good hedge for the linear risk

(where CP and the UL are same). Need additional hedges for 2nd order risk and basis risk.

– Some hedging instruments are evolving e.g. index Contingent CDS (CCDS does not have fixed notional rather it is linked to some index e.g. ITRAXX).

– New trades will be approved if specific WWR stays under the limit. – For mitigation and control:

• Tenor reduction • Enhanced collateral requirements • Minimum credit rating requirements

© SilvermanTanaka

References

– Deloitte and Solum: “Counterparty risk and CVA Survey” http://bit.ly/16oTPIR

– Gregory and Arvanitis, Credit: The Complete Guide to Pricing, Hedging and Risk Management, Risk Waters 2001

– Gregory, Jon, Counterparty Credit Risk and Credit Value Adjustment, 2nd Ed., Wiley 2012

– Christian Redon, “Wrong way risk modeling”, Risk, April 2006 http://bit.ly/aOVTmH

– Goldman Sachs, “Wrong-way CVA done right”, Risk Library, 26 April 2012 http://bit.ly/16Nqvuc

– Inamura, Kouki, et.al., “Wrong way risk in OTC derivatives and its implication for Japan’s financial institutions”, Bank of Japan Review, June 2012

–

© SilvermanTanaka