managing capital and stress testing for traded book assetsma.moodys.com/rs/961-kcj-308/images/moodys...

TRANSCRIPT

Managing Capital and Stress Testing for

Traded Book Assets

Abinash Arulanandam, Alexis Hamar and Roshni Patel Thursday 4 October 2018

Managing Capital and Stress Testing for Traded Book Assets 2

AgendaKey elements for discussion

1. Overview and the current market demands

2. Impacts for trading book assets

a. Fundamental Review of Trading Book - Linkage to Incremental Risk Charge (IRC) and Default Risk Charge

(DRC)

b. Risk coverage

3. Focus on Reverse Stress Testing

4. Q&A

1 Overview and the current

market demands

Managing Capital and Stress Testing for Traded Book Assets 4

Market trends

CONSOLIDATED VIEW

Group structures require a strong coordination of activities aimed to:

• Set rules for estimation of traded assets and banking books at group level.

• Have a consolidated and consistent view of the Group risk profile

• Increase the efficiency of risk-capital allocation over the entire Group perimeter

• Risk Appetite and Hedging Strategies Implementation

NEW PARADIGM FOR TRADED ASSETS

• More Regulatory emphasis on economic risks of traded assets treated

• Risk and Emergence of Collateral Risk – Spread Risk - Settlement Risk – Wrong Way Risk Stress Testing

reinforcement in context of ICAAP and future FRTB rules

Traditionally, analysis of trading book and banking book is viewed as distinct from the analysis of the different nature and

dynamics of risks.

However, some joint dynamics are required to capture the emergence of collateral risk

Exploring both Regulatory and Internal Risk Capital

• Concentration and correlation affects for concentration risk

• Capital allocation across both measures

• Trend to enhance and integrate measures

Managing Capital and Stress Testing for Traded Book Assets 5

What is the market saying?Comments in 2018

1Quantification soundnessCurrent approaches adopted by clients are viewed to not be quantitative, and are more expert or

qualitatively based/driven. This is predominantly led by ICAAP findings and internal committee reviews.

2GovernanceThe banking book, its models have known to have strong governance frameworks but the trading book

needs to have consistent and common governance structures, enhancing controls for models.

3Greater need for Validation / AuditRevisions to regulation, models and feedback on prior regulatory submissions has meant greater

interactions for internal / external validation and providing Auditors with proof on the submissions.

4Global / LocalThe need for global consistency but accounting for local nuisances and how to manage branches,

subsidiaries and group level consolidations. Common reporting and model framework.

Managing Capital and Stress Testing for Traded Book Assets 6

The financial crisis and the regulatory evolution

on Trading Book

Financial Crisis

2007 - Subprime

Crisis

2008 - Default Lehman Brothers

2010 - EuropeanSovereign debtcrisis

Issues posed by regulators

Advantage of Internal Models vs Standard

VaR and credit risk in the Trading Book

Low sensitivity to extreme events

Banking Book vs Trading Book Arbitrage

Basel 2.5

Stressed VaR

IRC/CRM

Hypo vs Actual Backtesting

Impact of Basel 2.5

Capital charge for wider asset classes (i.e Sovereign

Increase of capital requirement for Internal Model

Banking Book vs Trading Book

Next evolution: FRTB Basel 4

Expected Shorftall / Liquidity Horizon

Regulator imposed correlations

Market dynamics representation

News for Model Validation

PnL Attribution

Backtesting

Validation of IMM at Desk level

Floor Standard Method / Reduction of gap Internal Model vs Std

Default Risk Charge(DRC)

Arbitrage between

Banking and Trading

Book

Capital Volatility for

Trading Assets

Market VaR RWA

Model Validation for

Complex and

Structured Instruments

Comprehensive

Risk Coverage

Managing Capital and Stress Testing for Traded Book Assets 7

Banking & Trading Books Funds T

ransfe

r Pri

ce

Commercial Margin

Concentration Premium

Option Spread

Funding Liquidity Spread

Credit Spread Residual

Reference Rate

Spread Risk Premium

Commercial Margin

Capital Value Adjustment

Margin Value Adjustment

Funding Value

Adjustment

Credit Value Adjustment

Reference Rate

Collateral Value

Adjustment

INTERSECTIONS

» New Accounting standards to

impact both Pricing and Regulatory

Capital landscapes

» CET 1 increases due to IFRS rules

will reduce upcoming FRTB

required ones

» Common Components - Spread

Risk across Trading and Banking

Books

COMMON

COMPONENTS

Common Components and Intersections

2Fundamental Review of

Trading Book Linkage to DRC and IRC

Managing Capital and Stress Testing for Traded Book Assets 9

Risk factor identification

BB & TB segregation for instruments

Intraday limit monitoring

P&L reports

Inventory ageing reports

Disclosures

Strategy/profitability Investments GovernanceSenior Management

Front office

Desk1

Desk2

Desk n Trading BookDe

sk

re

org

an

isa

tio

n

(elig

ible

de

sk

s)

Banking Book

IRT

desk

Well defined

boundary

Internal Model Approach (IMA) Standardized Approach

Expected

ShortfallNMRF

DEFAULT RISK

CHARGE

Sensitivity based

charge

Default risk

charge

Residual risk add-

on

Front office

Middle office/data

management

Monte Carlo Farms

Distributed Computing

Data Warehousing

Technology

FRTB Implementation

Managing Capital and Stress Testing for Traded Book Assets 10

Stress Testing Emphasis in FRTB » Stress Testing is a transversal imposed practice

– Stressed calibration period (period of significant financial stress) for Expected Shortfall

– Liquidity Horizon : no price movement for instrument hedging in stressed period

– Curvature in Standardized approach is estimated through 2 stress scenarios per risk factors

– Non Modellable Risk factors where there is a stress capital charge

– Default Risk Charge : Based on a 1 year period of stress taken from a 10 year historical data using a 250 Liquidity Horizon

“Stressed” period means:

– 12 months period of stress over the observation horizon in which the portfolio experiences the largest loss

– Span at least back to 2007

– Observation equally weighted

– At least an update once a month

– And updates done as soon as there is a significant move in the market

Managing Capital and Stress Testing for Traded Book Assets 12

IRC Principles

IRC

PRINCIPLES

01

0205

06

04 03

Concentration Risk» Issuer and Market (Country/Industry)

concentration

Correlations» Correlation between default& migrations

» Capture Listed, Unlisted, Emerging Markets

& Sovereign correlations

Migration» Spread and Ratings

Risk Mitigation and

Diversification» Long/Short Positions

» Hedging Strategies

Optionality» Non Linear relationships

Coverage» Debt Instruments

» Sovereigns

» Corporates/Financials

» Credit & IR Derivatives

Managing Capital and Stress Testing for Traded Book Assets 13

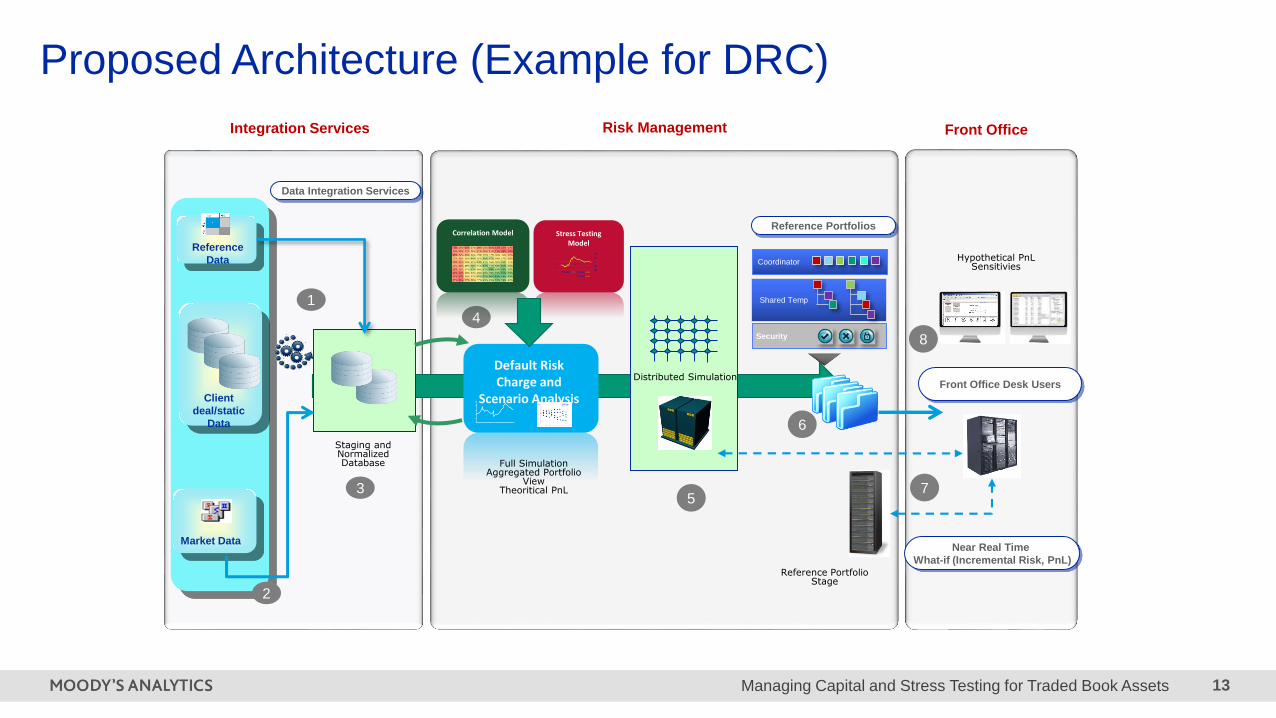

Proposed Architecture (Example for DRC)

Integration Services Risk Management

Default Risk Charge and

Scenario AnalysisClient

deal/static

Data

Reference

Data

Market Data

1

2

3

4

6

Distributed Simulation

Correlation Model Stress Testing Model

Staging and NormalizedDatabase

Reference Portfolios

Near Real Time

What-if (Incremental Risk, PnL)

Security

Coordinator

Full SimulationAggregated Portfolio

ViewTheoritical PnL

Front Office Desk Users

Data Integration Services

Front Office

7

8

5

Shared Temp

Hypothetical PnLSensitivies

Reference PortfolioStage

Managing Capital and Stress Testing for Traded Book Assets 14

FRTB, DRC – Correlation pain point

What banks are looking

for

Granular level that allows client to better understand risk in their portfolios

Multi-factor model allows to capture different aspects of firms, economy and the relevant relations

+10 years of data satisfying FRTB requirements and providing robust estimates

Partner with external vendor or create a combined external and internal data model

Sovereigns included with state of the art methodology due to scarce data

Corporate correlations included in model ensuring maximum completeness

Extensive research in model development for different sectors

Data cleaning not needed on the client’s side, painless bind with system

Recognized vendor ensuring quality, standards and support if needed

Correlation is one of the pain points due to modelling complexity, data requirements and inclusion of equities in FRTB

FRTB REQUIREMENTS

MODEL

Correlation model is a requirement

Correlation needs to be measured over a liquidity horizon of one year

Validation of correlation model must be in place

Choice & weights of systematic risk factors must be well documented and validated

DATA

Calibration to at least 10 years of data

Equity data must be included

Must include periods of stress

Objective and transparent data

Managing Capital and Stress Testing for Traded Book Assets 15

IRC vs DRC SummaryTopics IRC DRC

Scope IR Instruments (Bonds, Sovereigns,

CDS) Equities (optional)

IR Instruments + Equities

Modeling Approach VaR 1 year @99.9% VaR 1 year @99.9%

Default Risk Multi-Factor approach 2 types of Factor Approach

Correlations horizon 3 years 10 years including a 12 months of

stress

Correlations source Any (asset returns, equity returns, cds

spreads)

Based on CDS spreads and equity

returns

Migration Risk Included Excluded. Included in Spread Risk

Liquidity Horizons 3 month or 1 year horizon 1 year and 60 day for Equity

PD No floor 3 bps floor

LGD Deterministic, stochastic (optional) Stochastic and correlated to

systematic factors

2b Other risk types

Managing Capital and Stress Testing for Traded Book Assets 17

Counterparty Credit Risk considerations

Multi-period Valuation Portfolio Models Correlation

» Valuation (optionality and pricing proxies etc)

» Credit Migration and Spread Risk Effects

» Liquidity Value adjustments/ funding liquidity adjustments

» Wrong way risk (specific)

» Monte Carlo simulation approximations

» CVA VaR and allocation

» Re/calibration

» Benchmarking

» Back-testing

» Risk Factor Analysis (multi factor asset correlation models)

» Cross asset correlation (IR, Credit, FX etc)

» Wrong way risk (general)

» Stress testing and scenario construction

Strategy and Business Considerations

» Best practices processes

» Data, System infrastructure and reporting requirements

» Front office (FO) vs CCR model reconciliation

» CVA Hedging

» Capital Optimisation

» Integration of loan and trading portfolios

Modeling Considerations

Managing Capital and Stress Testing for Traded Book Assets 18

Wrong Way Risk

» Wrong-Way Risk

– An unfavourable dependence between exposure and counterparty credit quality: the exposure is high when the counterparty is more likely to default and

vice versa.

» General Wrong-Way Risk

– Arises when the probability of default of counterparties is positively correlated with general market risk factors.

» Specific Wrong-Way Risk

– Arises when the exposure to a particular counterpart is positively correlated with the probability of default of the counterparty due to the nature of the

transactions with the counterparty.

» Wrong Way Risk includes the following ingredients:

– Joint simulation of Market-Credit factors

– Utilizes Economic Portfolio Models as it is designed by nature with correlations effects

– Migration, Default and to some extent Recovery for systematic LGD

– Conditional scenarios

– Funding Spread in FVA

Managing Capital and Stress Testing for Traded Book Assets 19

» There are two types of correlation to consider:

– The correlation between the underlying asset and the counterparty of the trade.

– The correlation between the trades.

» A firm has to typically take into account both types of correlation.

» The correlation between the instrument and trade counterparty can increase (WWR/wrong way

risk) or decrease (RWR/right way risk) the capital requirements.

» Example of an use cases (other use cases also available:

Wrong Way Risk and correlations

Case 1 Case 2Correlation (Counterparty and underling asset) Positive NegativeBank A position on the underling asset will receive will deliver will receive will deliverRisk (wrong way risk/ right way risk) RWR WWR WWR RWR

Managing Capital and Stress Testing for Traded Book Assets 20

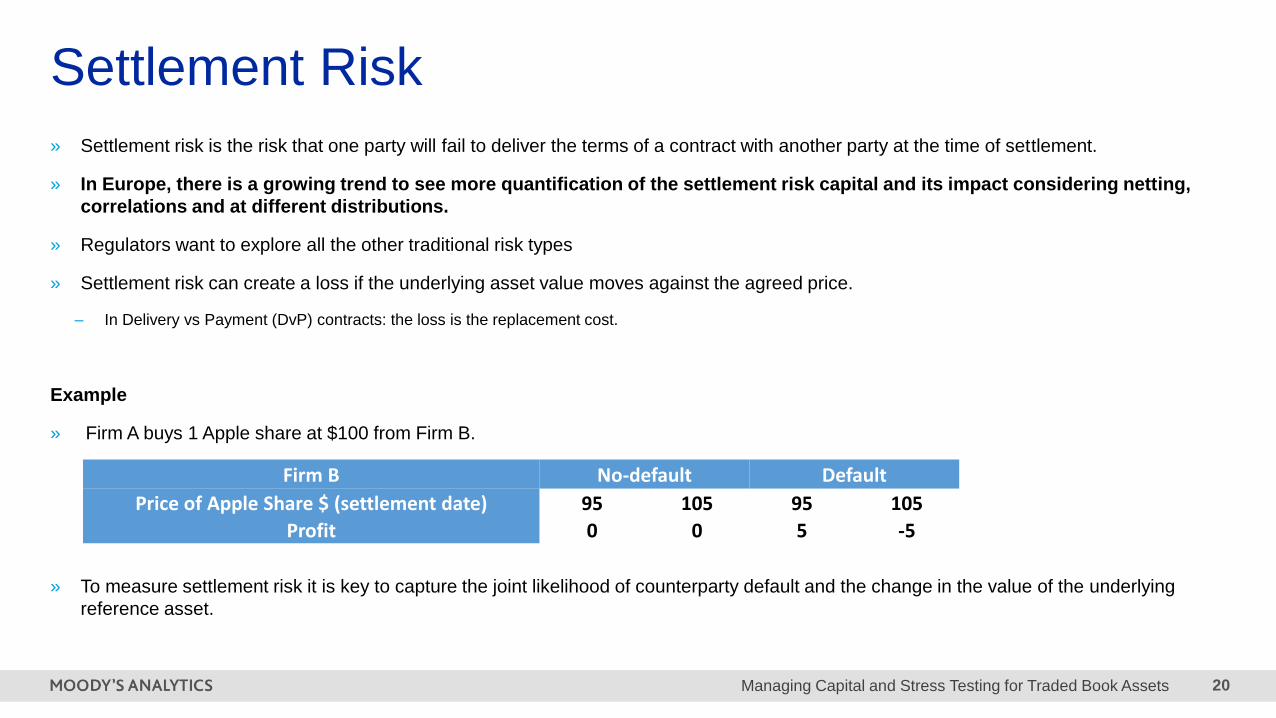

» Settlement risk is the risk that one party will fail to deliver the terms of a contract with another party at the time of settlement.

» In Europe, there is a growing trend to see more quantification of the settlement risk capital and its impact considering netting,

correlations and at different distributions.

» Regulators want to explore all the other traditional risk types

» Settlement risk can create a loss if the underlying asset value moves against the agreed price.

– In Delivery vs Payment (DvP) contracts: the loss is the replacement cost.

Example

» Firm A buys 1 Apple share at $100 from Firm B.

» To measure settlement risk it is key to capture the joint likelihood of counterparty default and the change in the value of the underlying

reference asset.

Settlement Risk

Firm B No-default Default

Price of Apple Share $ (settlement date) 95 105 95 105

Profit 0 0 5 -5

3 Focus on Reverse Stress

Testing

Managing Capital and Stress Testing for Traded Book Assets 22

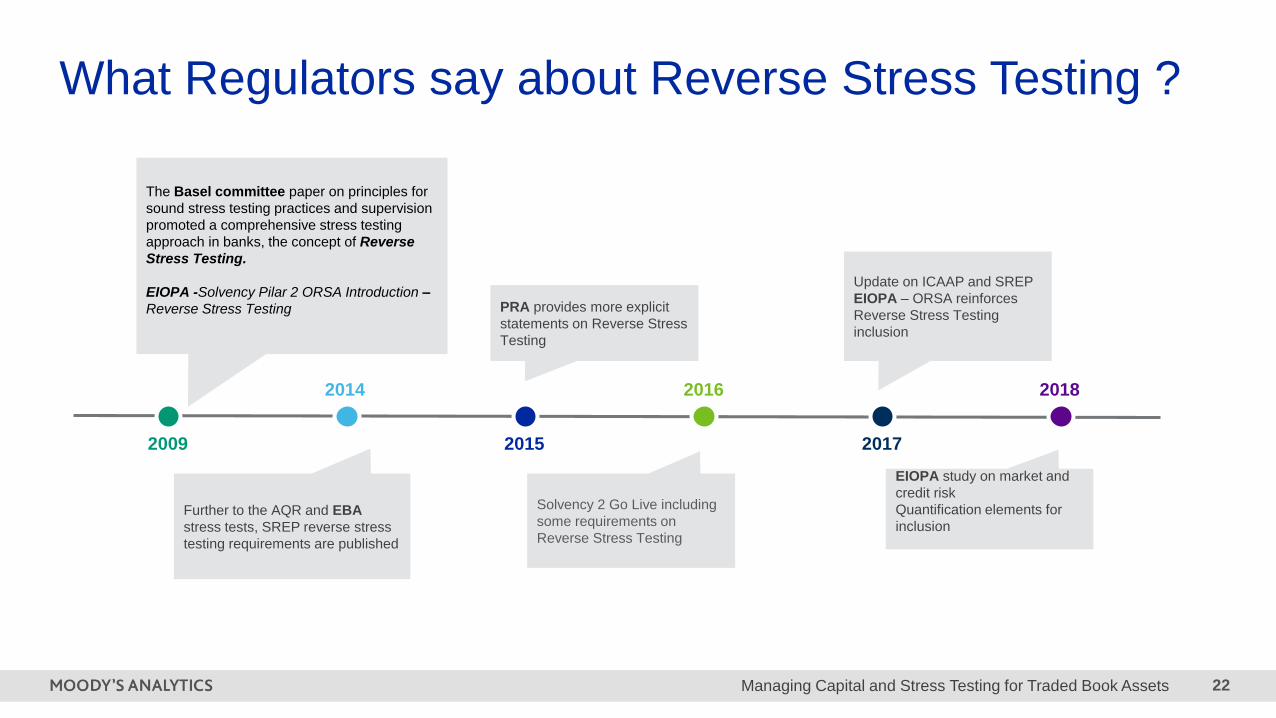

What Regulators say about Reverse Stress Testing ?

EIOPA study on market and

credit risk

Quantification elements for

inclusion

Solvency 2 Go Live including

some requirements on

Reverse Stress Testing

PRA provides more explicit

statements on Reverse Stress

Testing

Update on ICAAP and SREP

EIOPA – ORSA reinforces

Reverse Stress Testing

inclusion

2009 2015 2017

2014 2016 2018

The Basel committee paper on principles for

sound stress testing practices and supervision

promoted a comprehensive stress testing

approach in banks, the concept of Reverse

Stress Testing.

EIOPA -Solvency Pilar 2 ORSA Introduction –

Reverse Stress Testing

Further to the AQR and EBA

stress tests, SREP reverse stress

testing requirements are published

Managing Capital and Stress Testing for Traded Book Assets 23

Reverse Stress Testing: Trends

1Reverse Stress Testing – Nothing new

• In the UK, this has been around for a number of years, Europe has become more advanced and developed, a new re-focus

• Require firm to assess scenarios and circumstances that would render its business model unviable

• More understanding for the ICAAP submission as per regulatory requirements

3

Example approach

• Range of qualitative and quantitative approaches to determine those weaknesses

• Explore correlations between credit risk factors and macroeconomic variables to help draw impacts

• Different risk types will also have different triggers, look at asset class specific influences

• Leverage macro-scenario approach, which is key input for the firm to explore cause of trigger points.

• Estimating conditional mean of the risk factors and macro variables conditional on portfolio loss exceeding a given loss level

• Reducing dimension of risk and macro factors by ranking the most influential risk/macro factors that determine losses

• Solving for the inversion problem to find the set of risk/macro factors values with regards to the hypothetical scenario (the most likely

scenario)

2

Core elements

Determining scenarios

• Be able to macroeconomic variable related terms for loss points defined

• Explore idiosyncratic weaknesses

• Uncover which risks contribute the most to expected loss and capital and use that information to design plausible stress scenarios

• For instance By how much does GDP have to fall for my portfolio to lose 10% in value?

Q&A

Appendix

Managing Capital and Stress Testing for Traded Book Assets 26

Joining the Building Blocks

CONSOLIDATED RISK

CREDIT RISK

COUNTERPARTY CREDIT

RISK

» Challenges in setting the correlation between credit risk, market risk, spread risk

and CCR

» Spread Risk presence in both trading and banking books and unique counting

– Margin Period of Risk – Settlement Risk

– Migration Risk - Spread

BANKING BOOK

RISK DUE TO DEFAULT RISK DUE TO CREDIT MIGRATION

TRADING BOOK

RISK DUE TO MARKET RISK RISK DUE TO CCR

RISK DUE TO SPREAD RISKRISK DUE TO SPREAD

RISK

Managing Capital and Stress Testing for Traded Book Assets 27

Advantage of an Integrated Solution

A SINGLE CREDIT RISK SYSTEM

RISK DUE TO DEFAULT

RISK DUE TO CREDIT MIGRATION

INTEGRATED RISK

from an Integrated Model

of Risk Factors

» Ability to set more accurate and granular risk correlation parameters

» Straightforward risk decomposition

» Avoids double counting

» Improved operational efficiency

Better captures diversification – more accurate capital numbers

RISK DUE TO SPREAD RISK

RISK DUE TO MARKET RISK

RISK DUE TO CCR

Managing Capital and Stress Testing for Traded Book Assets 28

Credit Risk Framework

3 sub-portfolio to be considered: » Non Securitization

» Securitization-Non CTP incl. its hedges

» Securitization-CTP incl. its hedges

Modeling of the Default Risk by Jump-to-default (JTD)» LGD equity, non senior debt = 100%; LGD senior debt = 75%, LGD

covered bonds = 25%

» Limitation in terms of seniority for offsetting positions (long/short) : Netting

is allowed only if short position has the same seniority of the long one

» JTD (long) = Max {LGD X Notional +PnL; 0}

» JTD (short) = Max {LGD X Notional + PnL; 0}

» RW = default risk weight * JTD

Wts = σ 𝐽𝑇𝐷 𝑙𝑜𝑛𝑔

σ 𝐽𝑇𝐷 𝑙𝑜𝑛𝑔+σ 𝐽𝑇𝐷 𝑠ℎ𝑜𝑟𝑡

DRC Charge Non Securitization (by bucket)

= M𝐚𝐱 [∑𝑹𝑾𝑙𝑜𝑛𝑔 net JTD - 𝑾𝒕𝑺 * ∑𝑹𝑾𝒔𝒉𝒐𝒓𝒕 net JTD, 𝟎]

DRC Charge Securitization CTP (by bucketed DRCb)

= M𝐚𝐱 [∑[Max[DRCb,0] + 0.5 x Min [DRCb,0],0]

Standardized ApproachDRC – Internal Model Approach

Credit VaR based approach :» Stochastic LGD and 0% recovery for equities

» Dependance of recovery rates and systematic risk factors

» 2 types of systematic factors for simulating defaults

» Correlations based on equity prices or CDS spreads

» Floored PD @3bps

» One year liquidity horizon and 60 day for Equities

The new default risk charge should capture the risk arising

from long/short positions from the timing of defaults within

a one-year capital horizon :» For example a long 1-year bond position hedged with a 3month

CDS should take into account loss scenarios generated by the

issuer defaulting between months four and twelve months.

Managing Capital and Stress Testing for Traded Book Assets 29

Modeling Credit Correlations Using Macroeconomic Variables is also Core to Understand Portfolio-Specific Tail Risk under Stress

Σ curent covariance matrix

φ

?

??

MVs

φM

Vs

The parameters to be estimated are the entries of the correlations matrix linking macroeconomic variables and systematic creditrisk factors, as well as correlations among macroeconomic variables

Define metrics and

target survival valuesPerform tail risk factor

analysis

Identify

macroeconomic

variables

Enterprise –wide

sensitivity analysis

Take actions and

create contingency

plans

Identify unviable

scenarios & hidden

vulnerabilities

Correlations of systematic factors and macroeconomic variables (MVs):

Managing Capital and Stress Testing for Traded Book Assets 30

Counterparty Credit RiskRiskFrontier in conjunction with GCorr Macro and a market risk system can be used to construct Wrong Way Exposure, along with the portfolio referent risk of each particular counterparty.1)Run RiskFrontier with GCorr Macro and the Expected Exposure Profile (from market system that accounts for netting)

2)Using the MC Output (which provides trial-by-trial detailed distributions on exposure and factor level) one can calculate the expected WW PD and expected WW market factor realizations conditional on the portfolio realizing losses in the region of the capital threshold

3)Compute WW Exposure using the market risk system along with the expected WW market factor from step (2)

4)Calculate portfolio referent risk of each counterparty using WW Exposure from (3)

5)In some cases the WW Exposure is substantial and may impact the capital threshold to the point where steps (1)-(4) need to be iterated, with the WW Exposure replacing Expected exposure in step (1)

Expected

shock φMV

conditional on

portfolio loss

Market Risk

System

Calculates

Wrong Way

Exposure

Wrong Way

Exposure

analyzed in

RiskFrontier

Managing Capital and Stress Testing for Traded Book Assets 31

Expanded GCorrTM and Macro Variables Covariance Matrix:

Modeling Overview

*For further information: “Modeling Credit Correlations using Macro Economic Variables”, Nihil Patel, RPC 2012

TrialSimulated macroeconomic

factorsSimulated GCorrTM systematic

credit risk factors Portfolio Loss

1 φMV1, φMV2, … φ1, φ2, … L

2 φMV1, φMV2, … φ1, φ2, … L

Economic scenario

Losses Economic scenarios

Specified loss level

Inputs

Outputs

Analysis

Expanded Cov. Matrix Mapping MV and MV Factors

MV MC Trial-by-Trial File

Scenario Analysis: Impact MV

on LossesStress Testing Reverse Stress Testing

RiskFrontier TM

MC Simulation

Engine

Managing Capital and Stress Testing for Traded Book Assets 32

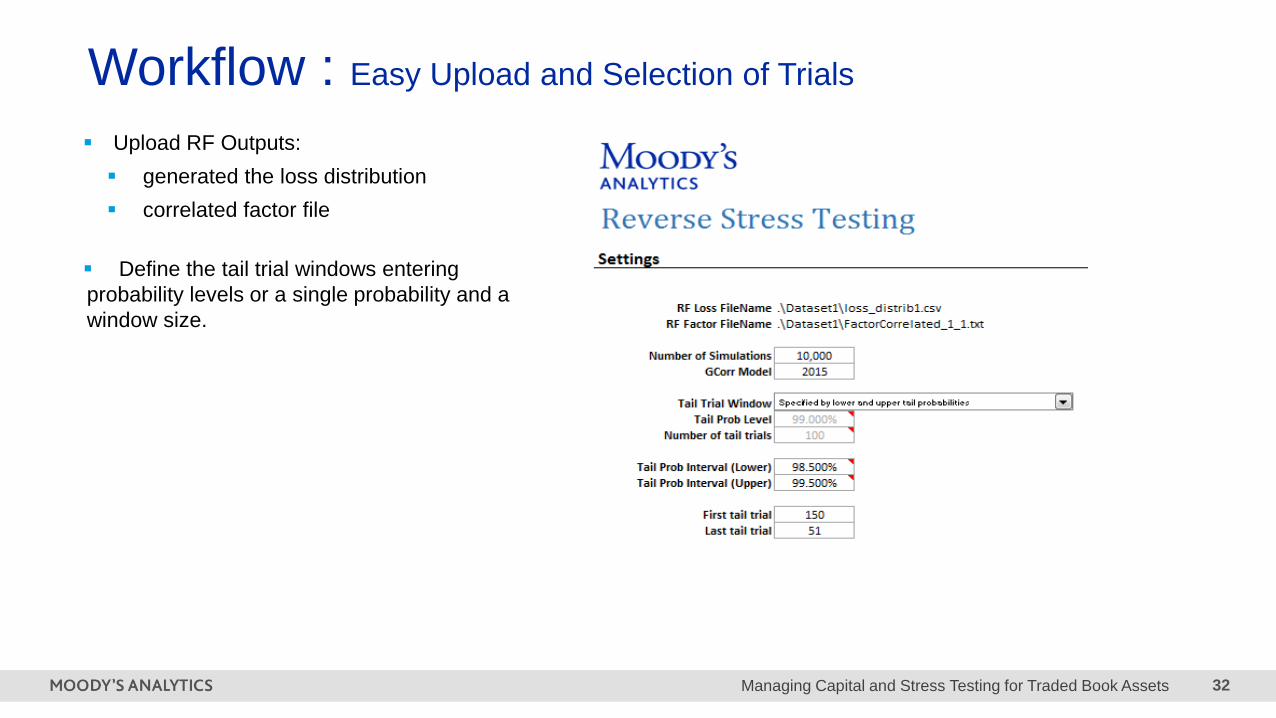

Workflow : Easy Upload and Selection of Trials

Upload RF Outputs:

generated the loss distribution

correlated factor file

Define the tail trial windows entering

probability levels or a single probability and a

window size.

Managing Capital and Stress Testing for Traded Book Assets 33

Workflow: Set the starting macro environment

Managing Capital and Stress Testing for Traded Book Assets 34

Workflow: Factor and MV Tail Mean Analysis

4. Trials Sorting in R or Excel

5. Attribution Reports – Outputs

Factor Means

Macro and Financial Variable Means

Macro and Financial Variable Density

» Conditional Systematic Factor Ranking Tail Mean

» Conditional Macro and Financial Variables Tail

Mean

» Macro and Financial Variable Density Probability

Managing Capital and Stress Testing for Traded Book Assets 35

Scenarios that Generate a Loss Level

» The key to this approach is an approximation of the

portfolio loss function 𝐿𝐻 𝑟 as a linear function of asset

returns.

» The linearization is done around the asset returns ҧ𝑟 that

generate the pre-defined loss level ത𝐿.

» We can then analytically search for the scenarios that give

that level of loss

» We need the Monte Carlo output around the pre-defined

loss level to identify the asset returns ҧ𝑟.

Managing Capital and Stress Testing for Traded Book Assets 36

Scenarios that Generate a Loss LevelExample

» Consider a well-diversified portfolio made of US and Canadian exposures.

» We want macroeconomic scenarios that lead to a loss of 6% of mark-to-model

value in this portfolio at a 1-year horizon.

– This loss level corresponds to the 47bp percentile of the loss distribution.

– Analysis date: 30/09/2016.

» We focus only on scenarios with the following macroeconomic variables:

– US Unemployment, US Equity, US VIX, US BBB Spread, Canada Equity, Canada Unemployment, Oil Price.

Managing Capital and Stress Testing for Traded Book Assets 37

Scenarios that Generate a Loss LevelExample: Focus on the scenario with a 6% loss level

Macroeconomic VariableAnalysis Date

Q3-2016

Average Scenario Q3-2017

US Unemployment 4.9% 10%

US Equity 100 25

US VIX 13.34 39.87

US BBB Spread 1.85% 9.36%

Canada Equity 100 33

Canada Unemployment 7% 20.51%

Oil Price 100 41

The scenarios should lead to a conditional loss distribution whose

expected loss is close to the desired level of loss

Percentiles Target Expected Conditional

Loss

672 bp 2% 4%

154 bp 4% 6.33%

46 bp 6% 8.19%

Managing Capital and Stress Testing for Traded Book Assets 38

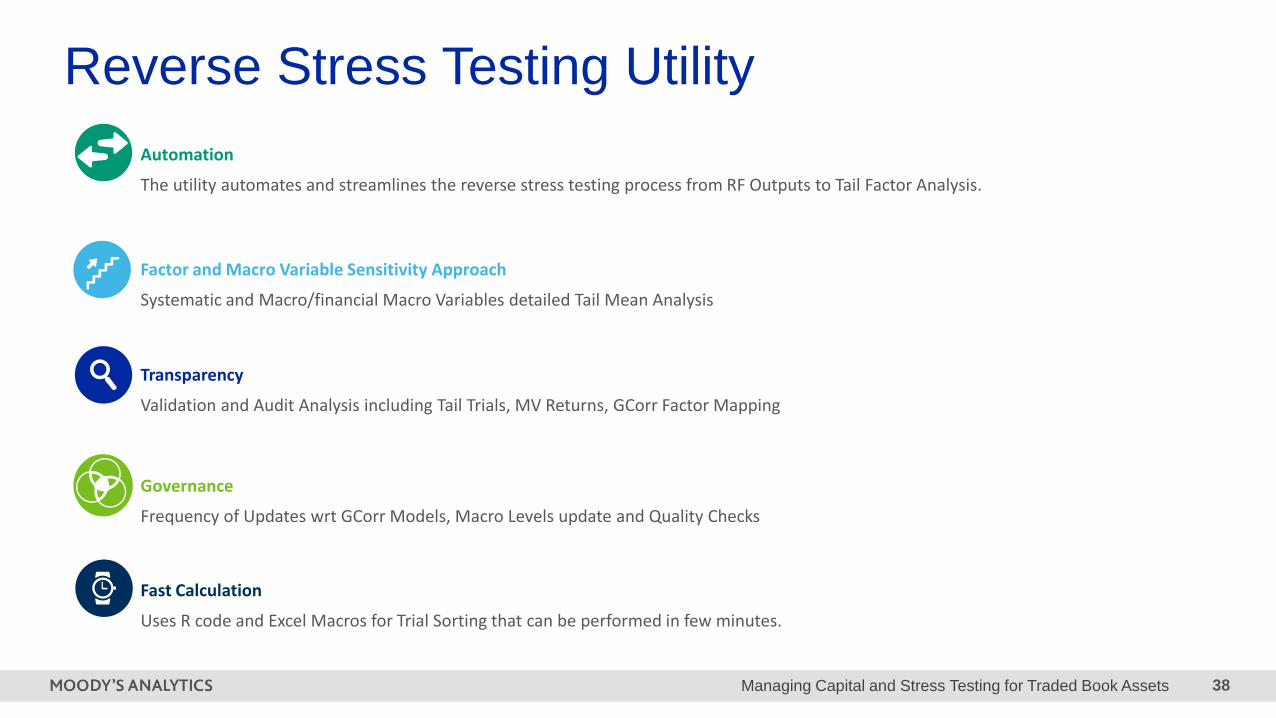

Reverse Stress Testing Utility

Automation

The utility automates and streamlines the reverse stress testing process from RF Outputs to Tail Factor Analysis.

Factor and Macro Variable Sensitivity Approach

Systematic and Macro/financial Macro Variables detailed Tail Mean Analysis

Transparency

Validation and Audit Analysis including Tail Trials, MV Returns, GCorr Factor Mapping

Governance

Frequency of Updates wrt GCorr Models, Macro Levels update and Quality Checks

Fast Calculation

Uses R code and Excel Macros for Trial Sorting that can be performed in few minutes.

Interest Rate Risk in the Banking Book, Sep 2017 39

© 2018 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All

rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT

OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND

MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET

ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT.

CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR

PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF

CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT

RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S

PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S

PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES.

NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR

INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND

UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS

UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE

RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN

MAKING AN

INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF

SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED,

DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART,

IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human

or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S

adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers

to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance

independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to

any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the

information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents,

representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of

present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating

assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for

any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud,

willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or

beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in

connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR

ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY

FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of

debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors

Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it

fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s

ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities

who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at

www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of

MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105

136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the

Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the

document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this

document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to

the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail

investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment

decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which

is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit

rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned

by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated

obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the

Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2

and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and

commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or

MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.