moody’s analytics ifrs 9 for insurersma.moodys.com/rs/961-kcj-308/images/moodys webinar... ·...

TRANSCRIPT

Moody’s Analytics

IFRS 9 for Insurers

Roshni Patel and Nadja Roos Wednesday, 26 September 2018

IFRS9 for Insurers, London, September 26, 2018 2

Moody's Analytics operates independently of the credit ratings activities of Moody's Investors Service. We do not comment on credit ratings or potential rating changes,

and no opinion or analysis you hear during this presentation can be assumed to reflect those of the ratings agency.

IFRS9 for Insurers, London, September 26, 2018 3

AgendaKey elements for discussion

1. Current trends in the insurance market

2. Best practices in gearing up for implementation

3. Acceptable model methodologies and level of granularity

4. A solution considering the challenges and linkages to IFRS 17

IFRS9 for Insurers, London, September 26, 2018 4

Accounting Standard Timelines

2022

CECL - SEC Filers

IFRS17 adoption*

IFRS9 exemption for Insurers

CECL - Other Co.’s

202120202019

IFRS9 General

adoption

2018

CECL - Public Co.’s

* IFRS 17 general adoption. Early adoption possible. Some regulators might decide to accelerate timelines.

IFRS9 for Insurers, London, September 26, 2018 5

Stages to IFRS9 complianceSmall steps achieving greater affect

IFRS9 for Insurers, London, September 26, 2018 6

Implementation Timeline – an Insurance view

IFRS 9: Automation and

Workflow

Integration with

IFRS17/Solvency II

IFRS 9 compliance –

tactical approach

Methodology development

/ enhancement

IFRS 9 compliance –

tactical approach

Q3 2018 Q1 2019 Q3 2019

Q4 2018 Q2 2019 Q4 2019

Gap assessment / Impact Study

Diagnostic Phase

Business Model and SPPI tests

IFRS9 for Insurers, London, September 26, 2018 7

Current market themes

Results of Gap Analysis / Impact Study

» What were some of the key findings?

» What existing methodologies, tools are recommended for use in IFRS9 implementation?

» If Impact study, what are the initial provision estimations, communication around the analysis?

Path to Implementation

» With late Q1 2019 / early Q2 2019 start, when is the parallel run targeted to begin?

» What is the planned scope of the parallel run?

» Is the firm planning to engage external support for implementation assistance, model validation, accounting advisory?

Applicable portfolio and materiality compared to IFRS17?

» Investment vs applicable portfolio

» Others standard, implementation unclear, i.e. UK GAAP?

1 Advantages of early

Implementation

IFRS9 for Insurers, London, September 26, 2018 9

Advantages of early ImplemetationBest Practices – Incorporating lessons learned

1Accountability / Responsibility

Institutions identifying a ‘Super user’ early on in the implementation project saw

considerable synergies.

2Governance

Strong Project Governance with Senior Management involvement and clear

escalation procedures made projects more efficient from the start.

3Validation / Audit

Early engagement of internal validation and external audit teams brought

everyone on the same level simultaneously and focused the formal process.

4Global / Local

Local Workshops with detailed user training across the end to end calculation

process.

IFRS9 for Insurers, London, September 26, 2018 10

Advantages of early ImplemetationBest Practices – Modelling

1Scenarios

Explore the use of internal macroeconomic scenarios for consistency with

Stress Test / ICAAP.

2PD / LGD

Use internal LGD models for consistency if available. Incorporate conditional PiT

PD / LGD term structures into existing accounting systems.

3Consistency

Consistency with internal process (Credit process, watch list approach, ICAAP,

Stress Testing).

4Validation

Incorporating new models in existing operating model (e.g. expanding current

Validation Framework).

IFRS9 for Insurers, London, September 26, 2018 11

Advantages of early ImplemetationInternal communication and Incorporating results

1Parallel Run

Opportunity for a longer parallel run phase.

2IFRS9 Impact

Analysing the impact of IFRS9 and determining potential mitigants (credit review of

stage 3, determining impact of staging in stress scenarios, QoQ volatility).

3Internal Communication

Providing Senior Management (CEO, CRO, CFO, CTO) with frequent and tailored

information especially around the QoQ volatility.

4Infrastructure

Assessing possible solutions in the context of existing infrastructure and potential

technical POCs. Enhance data systems and resources to source and link all data

requirements.

IFRS9 for Insurers, London, September 26, 2018 12

Advantages of early Implemetation

» Type of resources is changing

» Bringing skills into BAU

» Understanding of Risk and Finance data and

processes

» New sub teams for reporting across

stakeholders (CFO, CRO, CTO)

Resource Mix

Global Resources and Local Resources

» Addressing and assessing Group requirements

vs. Subsidiary requirements

» Implementing / communicating local changes

Consistency

» Have resources / skill sets that look across a

number of different requirememts (ST, ICAAP,

IFRS9)

People Cost

» Data – enhancing Risk and Finance data

» Personnel cost

» Methodology changes, re-calibration annually and

assumptions reflections

Operational Cost

Infrastructure

» New IT infrastructure vs. building/ re-using current

IT Infrastructure

» Tactical vs. Automated solution

Business Cost » Adopting new regulation / modifying existing processes

» Increased internal validation efforts

» Ongoing maintanance of models / documentation

» Enhancing business requirements (e.g. Origination,

RAROC)

Considering Operational Aspects of IFRS9

2 Portfolio Coverage

IFRS9 for Insurers, London, September 26, 2018 14

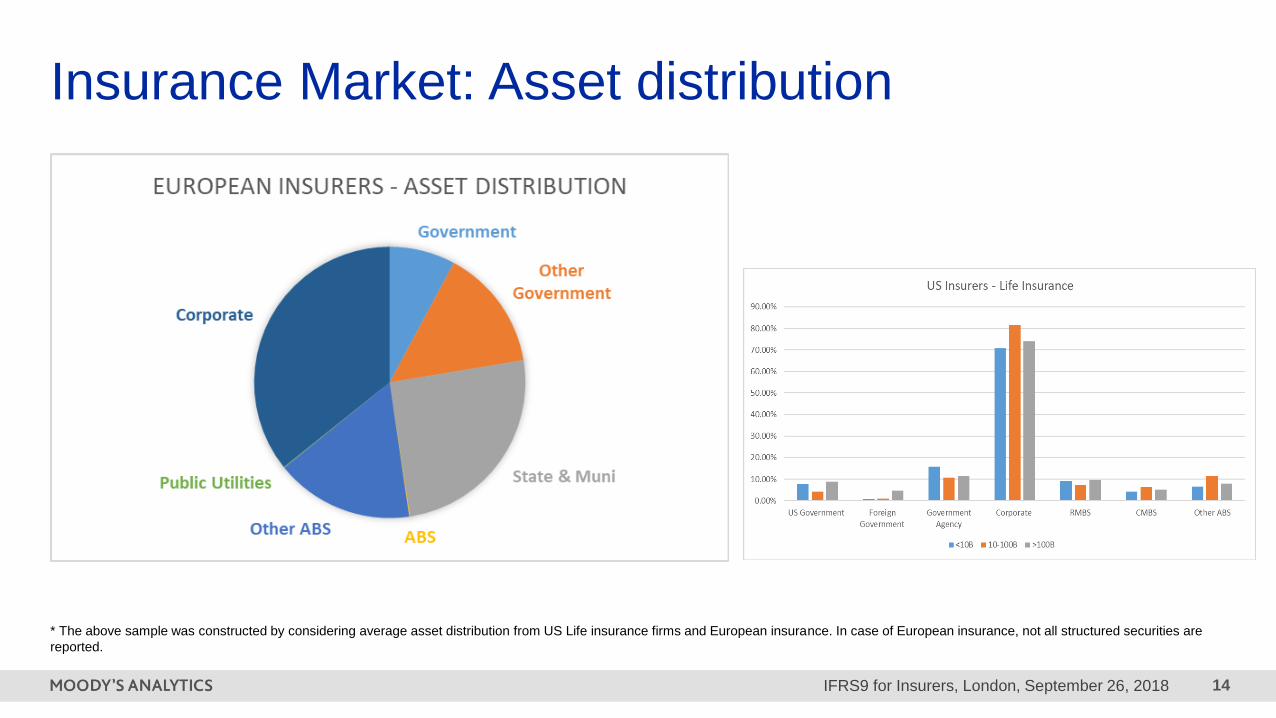

Insurance Market: Asset distribution

* The above sample was constructed by considering average asset distribution from US Life insurance firms and European insurance. In case of European insurance, not all structured securities are

reported.

IFRS9 for Insurers, London, September 26, 2018 15

Business Model and Classification & Measurement

• Perform Business model (BM) Assessment

• Test Criteria for Solely Payment of Principal and Interest (SPPI)

• Coverage: Products and investments and discuss the future balance sheet structure with key stakeholders

• Identify new policies and procedures e.g. business model policy that needs to be developed

BM and SPPI Test

• Assessment of systems, policies and procedures for BMA and SPPI test

• Content and structure of business concept; definition of benchmark test including business requirement description

Accounting Processes Revision

• Advise on implementation of models, data requirements, policies & procedures for BM and SPPI Test

• Automation to perform BM and SPPI test

Implementation

3 Impairment Modelling

Requirements

IFRS9 for Insurers, London, September 26, 2018 17

Impairment Process Experience – IFRS9Typical Process Steps

Data

Management

Portfolio

Segmentation

Methodology/

Models Selection

Scenario

Design/

Selection

Model(s) &

Accounting

Execution

Qualitative

Adjustments

Framework

Data preparation, Data Load,

ETL/Manual, Exception

reporting, Data substitution,

Rules Engine

CECL/IFRS9-allowable

Methodologies and Models

feeding these methodologies,

Assumptions

Model and Accounting Engines

execution

Ad hoc and/or pre-approved

segmentation at any level of

granularity

One or multiple Scenarios and

their weights, Reversion (if

desired)

Management Override at any

level, interagency and CECL

qualitative factors, entity-

specific factors

Real time reporting on input and output data, trending, roll forwards, audit trails, preparer/approver for any changes, attribution, disclosures, GL

aggregate and instrument-level entries

Pu

blis

h a

nd

Extra

ct (D

ata

an

d G

L)

IFRS9 for Insurers, London, September 26, 2018 18

IFRS 9 Impairment Calculation StepsAn end-to-end process

1Macroeconomic Scenarios

• Minimum of 3 Scenarios – Benign, Baseline and Adverse

• Include factors that are credit explanatory

• Quantitative Weights for each scenario (e.g., 50% weight for Baseline)

• Forecast Horizon: Cover full portfolio maturity (typically > 30 years)

3Stage Allocation

• Separate Allocation criteria per portfolio (Stage1 – 12m ECL, Stage 2/3 – L/time ECL)

• Analyse portfolio migration across stages to choose most optimal criteria per segment

• Absolute and Relative Thresholds

• Comply with minimum standards and best practice

4ECL calculation

ECL Calculation and Calibration

• Define and calibrate Effective Interest (Profit) Rate and discount factors

• Forward exposure method for ECL calculation

• Review and qualitative adjustments

2

PD & LGD Modelling

Forward-looking PIT PD Term Structure

• Derive TTC PDs from historical ratings, mapping to Moody's Analytics default study

• Convert TTC PDs to PIT

• Induce Scenario dependence to convert PIT PDs to Forward Looking PIT PDs

Forward-looking PIT LGD Term Structure

• TTC LGD based on historical recoveries, collateral and/or off-the-shelf models

• Lifetime LGD and Moody's Analytics PD – LGD Correlation model

IFRS9 for Insurers, London, September 26, 2018 19

Impairment Model Overview

Macroeconomic Scenario Forecasts

Scenario Probability Weights

Macro-Conditioned, Point-in-Time, Forward-Looking Default Probabilities

Credit Stage

PIT Conversion

Default Risk Measure

» Forecasts of GDP, unemployment, prices, etc.» Minimum 3 alternative scenarios: baseline, upside, downside» Business relevant scenarios

» Expected probabilities of scenarios

» Stage 1, 2, or 3 based on credit risk

» If TTC, need to convert to PIT

» PD Model» External or internal rating

Expected Credit Loss

Loss Given

Default

Exposure at

Default

Discount Factor

XX =

IFRS9 for Insurers, London, September 26, 2018 20

Forward Looking & Probability-Weighted Outcomes

» Requires expected credit losses (ECL) to account for forward-looking information

» Requires probability-weighted outcomes when measuring expected credit losses

– Estimates should reflect the possibility that a credit loss occurs and the possibility that no credit loss occurs

Macroeconomic modelling satisfies both requirements above

IFRS 9

IFRS9 for Insurers, London, September 26, 2018 22

Macroeconomic ScenariosProbability-weighted expected loss

2007Q1 2010Q4 2014Q3 2018Q2 2022Q1 2025Q4

2012Q1 2014Q1 2016Q1 2018Q1 2020Q1

S1 S3Baseline

Multiple Scenario Forecasts

Derive probability-weighted ECL

Scenario probabilities

S2 Mild Second Recession

Protracted SlumpS4

Baseline / Most LikelyBL

New Upside ScenarioS0

Stronger Near-Term ReboundS1

S3 Deeper Second Recession

IFRS9 for Insurers, London, September 26, 2018 23

United Kingdom Unemployment rate, %

United Kingdom Inflation, % change yr ago United Kingdom House price, 2010=100

United Kingdom IFRS9 Scenario Forecasting

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

S4 S3

S1 S0

BL

2

3

4

5

6

7

8

9

S4 S3 S1

S0 BL

90

110

130

150

170

190

S4 S3

S1 S0

BL

United Kingdom Real GDP, 2015 bil GBP

1600.00

1700.00

1800.00

1900.00

2000.00

2100.00

2200.00

2300.00

2400.00

2500.00

S4 S3

S1 S0

BL

Sources: ONS, Moody's Analytics Analytics

IFRS9 for Insurers, London, September 26, 2018 24

Expected Credit Loss CalculationCalculations steps

Moody's Analytics Analytics IFRS 9 Proposal

TTC ratings

• TTC assessment of creditworthiness

• Rating based on financial information of the obligor

TTC PD calibration

• Calibrate TTC ratings to TTC PDs for each obligor

• Calibration needs to use the historical default experience of the bank

• For portfolios with low number of defaults, Moody's Analytics can augment the data with its own datasets

Translation to PiT PDs

• Adjust TTC PDs for the point in the credit cycle

• Typically banks do not have enough data to extract the credit cycle

• Moody's Analytics can use its own data to get a robust estimate of the credit cycle

Forward-looking PiT PDs

• Add dependence of PiT PDs to macroeconomic variables

• Combine with macroeconomic scenario forecasts and probabilities to get forward-looking estimates

IFRS9 for Insurers, London, September 26, 2018 25

What is the Rating to PD Converter?

PD by

Rating

Country

adjustment

Sector

adjustment

Point-in-Time

PDs

» Use the public firm PD database to

estimate the typical PD given the rating

» Adjust for sector and country trends

» Use the PD term structure to generate a

Point-in-Time PD term structure

» Can be applied to a financial institution’s

internal rating

IFRS9 for Insurers, London, September 26, 2018 26

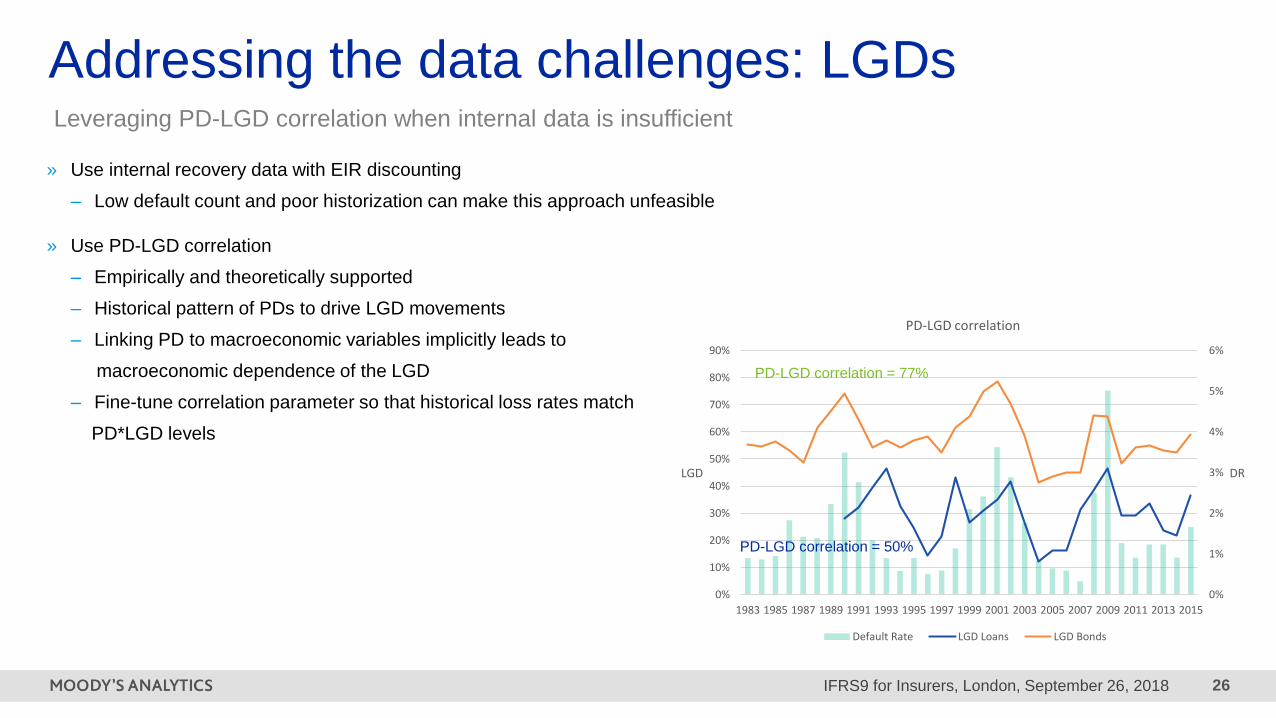

Addressing the data challenges: LGDsLeveraging PD-LGD correlation when internal data is insufficient

IFRS 9 and beyond: Implementation challenges and what lies ahead

» Use internal recovery data with EIR discounting

– Low default count and poor historization can make this approach unfeasible

» Use PD-LGD correlation

– Empirically and theoretically supported

– Historical pattern of PDs to drive LGD movements

– Linking PD to macroeconomic variables implicitly leads to

macroeconomic dependence of the LGD

– Fine-tune correlation parameter so that historical loss rates match

PD*LGD levels

0%

1%

2%

3%

4%

5%

6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

DRLGD

PD-LGD correlation

Default Rate LGD Loans LGD Bonds

PD-LGD correlation = 50%

PD-LGD correlation = 77%

IFRS9 for Insurers, London, September 26, 2018 27

Stage Allocation Criteria

Absolute Criteria

PD Master Scale

Future Default Rate

under each scenario

Portfolio Distribution

Possibility to segment by model,

rating scale or industry

Define

Absolute

Rating

Threshold

Relative to

Inputs

Possibility to

differentiate

by Maturity /

Lifetime PD

Horizon

Absolute Criteria

Rating is less than XX AND / OR PD is > XX%

Last allocated stage

Terms Modified With Adverse Impact on the

bank

Watch list account

Relative Criteria

Decrease in Ratings by XX notches AND / OR Increase in PD by XX

percentage points

XX number of Movements across Stages in the last

XX months

Decrease in collateral coverage ratio

4 IFRS17

IFRS9 for Insurers, London, September 26, 2018 29

Connecting IFRS 9 and IFRS 17Consistent credit modelling / Infrastructure

IFRS 9

Modelling impairments

1. Insurers are looking for consistent approach to credit modelling across both sides of the balance sheet i.e. IFRS 9 and IFRS17.

2. Consistent modelling could reduce the probability / likelihood of accounting mismatches arising and leading to spurious volatility in the net financial results reported by insurer.

3. Future linkages for infrastructure and reporting purposes

» Impairment modelling is required for

assets classified at amortised cost of

FVOCI

» IFRS9 tool / model deployment

» Leveraging In-house and/or Vendor data

(i.e. PD, LGD engine)

» Derive the ECL at the granular level for

each exposure in the portfolio

IFRS 17

Top Down approach for the liability discount rate

Credit risk premium

for unexpected losses

Yield

Curve

based on

actual or

reference

portfolio

Expected credit

losses

Mismatch

IFRS 17

Discount

Rate

Methodology may

require PD and

granular LGD

IFRS9 for Insurers, London, September 26, 2018 30

IFRS 9 & 17 Thought Leadership Papers

Actuarial Models in an IFRS 17 World

Compliance with this standard promises to

bring the greatest disruption ever seen to

insurers’ financial reporting systems and

processes, by forcing companies to integrate

actuarial models deeply within reporting

processes.

Discount Rate Curves

In his IFRS17 Insight whitepaper, Nick

Jessop – Senior Director Research, decodes

the impact, significance and use of discount

curves in the IFRS 17 reporting process.

Getting IFRS 17 Implementation Right

InsuranceERM recently published a Q&A

interview with Moody's Analytics Analytics

that provides practical insights on some

aspects of the IFRS 17 implementation.

moodysanalytics.com/ifrs17

Level of Aggregation in IFRS 17

Massimiliano Neri shares his thoughts about

the level of contract aggregation required by

IFRS17 in his latest publication. Read his

whitepaper now to learn more about this core

requirement of IFRS17.

IFRS9 getting ready for the challenge

November 2018 will see the release of the

experiences learnt from IFRS9 banking

implementations and what this means for

Insurers.

Impact for Asset Managers

5 Q&A

Appendix

IFRS9 for Insurers, London, September 26, 2018 33

» 100+ IFRS9 ECL

engagements in Europe,

Asia and Americas (exclu.

Americas)

» Working with institutions of

various sizes and

sophistication levels sizes

(Tier 1 to New banks)

» Banks, Development

Banks, Corporates and

Insurers

Moody's Analytics Analytics experience

IFRS9 for Insurers, London, September 26, 2018 34

Moody's Analytics and Thomson Reuters

joint SPPI solution

700K

Fixed Income

Securities

1M

Mortgage Backed

Security Pools

300K

Asset Backed

Securities

The partnership merges two core competences in one solution, offering the most competitive

approach in the market in terms of instrument coverage and functionality.

Clients will benefit from more than 30 SPPI related value and transparency fields and

documentation within one auditable solution delivered by Moody's Analytics Analytics and

Thomson Reuters.

IFRS9 for Insurers, London, September 26, 2018 35

ImpairmentStudioTM for Insurance CompaniesA CECL/IFRS9 orchestration platform to ensure a well governed and efficient period end process for

the new impairment accouting standards

Model Inventory for in house or

Moody's Analytics provided models

Scenario library with Moody's Analytics

documented and validated

methodology

Analysis project repository to run

production and ad hoc analysis

Full set of reports and disclosures to

support the analysis and review process

SUPPORT FOR

Risk, finance and

accounting analysts

Moody's Analytics, Internal

and external models

Scenario weighting

Attribution analysis

Audit tracking at loan level

Full disclosure set

Accounting entries (GL and

loan level)

Q-factor analysis support

for review challenge

SOC 1 Type 2 from Big 4

Interest Rate Risk in the Banking Book, Sep 2017 36

© 2018 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All

rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT

OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND

MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET

ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT.

CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR

PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF

CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT

RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S

PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S

PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES.

NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR

INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND

UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS

UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE

RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN

MAKING AN

INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF

SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED,

DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART,

IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human

or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S

adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers

to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance

independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to

any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the

information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents,

representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of

present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating

assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for

any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud,

willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or

beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in

connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR

ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY

FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of

debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors

Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it

fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s

ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities

who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at

www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of

MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105

136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the

Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the

document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this

document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to

the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail

investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment

decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which

is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit

rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned

by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated

obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the

Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2

and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and

commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or

MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.