world trade - 08 aug 2009

DESCRIPTION

The Authority for Supply Chain Decision MakersTRANSCRIPT

SM

Hyundai, a natural resource for your growing business.

Hyundai Merchant Marine. On time. Online.

2001-2009

Whether the core of your business is in raw materials or finished goods, HMM understands the importance of ocean transportation to your supply chain. Depend on us for reliable, on time multimodal transportation service

1.800.regions | regions.com/business

YES, we’re here for small businesses.

YES, we’re here for big businesses.

YES, we’re lending to both.

LET’S TALK ABOUT YOUR LENDING NEEDS TODAY. STOP BY A BRANCH TO SPEAK TO A REGIONS BANKER.

© 2009 Regions Bank.

At Regions, we’ve always put our customers fi rst. And in tough

economic times, that’s not going to change. We know that

businesses need resources to stay strong and explore new

opportunities. And we’re determined to help businesses grow –

both large and small alike. To put it simply, Regions remains a

safe harbor for your deposits – and we are lending.

Regions works for business.• Regions is currently ranked #3 on the list of Top

Small Business Lenders in the U.S. by the SmallBusiness Administration.

• Every day, Regions bankers are meeting with businesses toconduct the free Regions CashCOR analysis – designed to help you optimize your business’ cash fl ow.

• Over 1.3 million business owners across 16 states turn to Regions for their business deposit and lending needs.

©2009 The Port of Long Beach

We’re striving for perfection every day—with our proactive

customer service, fast transit times, huge capacity, vast

network of distribution centers and unparalleled cross-

country rail access. But of course there’s always room for

improvement. Th at’s why we’re so committed to smart

upgrades and expansion projects. We want to stay on the

forefront of goods movement. And on our winning streak.

www.POLB.com

Why did we get the

Best Seaport Award 13 times

in 14 years?

Hey, nobody’s perfect.

Thinking outside the docks

W W W . W O R L D T R A D E W T 1 0 0 . C O M 5

COVER STORY:

16 The Top U.S. Trade PartnersOur annual survey of the top U.S. trade partners and our leading imports and exports.

28 Taking Supply Chain Securityto the Next LevelMobile security is playing a big part, but it’s not a silver bullet.By Dan McCue

34 Staples Nails SustainabilityThe office company’s embrace of environmentalism is paying off.By Gail Dutton

38 Is Trade with Cuba a Reality?Recent developments in the Obama administration could open the door wider.By Dan McCue

REGION44 NAFTA: Two Sides of the Coin

Mexican manufacturing bounces back while Canada frets over U.S. protectionism.By Lara L. Sowinski

TRANSLATION47 Talk About a Tough Sell

Making the case for spending on translationservices in a slow economy.By Jeffrey Jorgensen

WORLD TRADE, WT100 Volume 22, Number 8 (ISSN 1949-9159) is published 12 times annually, monthly, by BNP Media II, L.L.C., 2401 W. Big Beaver Rd., Suite 700, Troy, MI 48084-3333. Telephone: (248) 362-3700, Fax: (248) 362-0317. No charge for subscriptions to qualified individuals. Annual rate for subscriptions to nonqualified individuals in the U.S.A.: $104.00 USD. Annual rate for subscriptions to nonqualified individuals in Canada: $137.00 USD (includes GST & postage); all other countries: $154.00 (int’l mail) payable in U.S. funds. Printed in the U.S.A. Copyright 2009, by BNP Media II, L.L.C. All rights reserved. The contents of this publication may not be reproduced in whole or in part without the consent of the publisher. The publisher is not responsible for product claims and representations. Periodicals Postage Paid at Troy, MI and at additional mailing offices. POSTMASTER: Send address changes to: WORLD TRADE, P.O. Box 2144, Skokie, IL 60076. Canada Post: Publications Mail Agreement #40612608. GST account: 131263923. Send returns (Canada) to Bleuchip International, P.O. Box 25542, London, ON, N6C 6B2. Change of address: Send old address label along with new address to WORLD TRADE, P.O. Box 2144, Skokie, IL 60076.

F E A T U R E S

16

August 2009Inside

V O L U M E 2 2 N U M B E R 8

10 Green Matters12 Supply Chain Watch13 Tradewinds

INSIDE WORLD TRADE8 Out with the Old,

in with the NewTurning the page at World Trade while entering a new chapter of world trade.By Lara L. Sowinski

SCI-FI50 The Cargo-Screening Robotic Ferret

Scientists at the University of Sheffield, England unleash a new ‘animal’ for screening cargo.By Jeremy N. Smith

C O LU M N S

EXE C UT I V E B R I E F I N G

34

28

38

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 96

www.worldtradeWT100.com Online

DigitalEdition

CLICK ON

LTL/Motor Freight

CLICK ON

WhitePapers

CLICK ON

Calendar of Events

CLICK ON

Are you a subscriber of the World Trader? You should be — choose from one or more of the following E-Newsletters from World Trade 100:

China EditionEurope EditionLatin America EditionIndia EditionGlobal Edition

Sign up today at www.WorldTrademag.com/enews.

Check out current and archivedissues of World Trade 100Never miss a must read article. Plus, you can share it with colleagues and click on web links to get further resources. It’s all at your

fi ngertips!

Get linked to LTL and Motor Freight: Articles Newsletters Industry News Vendors Expert Knowledge

Are you looking for more information on 3PLs?Then look no further than World Trade 100’s White Papers online.

SCOPE WestAugust 19-21, Las Vegas, NV

CSCMP Annual Global Conference 2009September 20-23, Chicago, IL

IMPORTANT CONSUMER INFORMATION: Subject to your Major Account Agreement, Calling Plan and credit approval. Offer available for corporate subscribers only. Up to $175 early termination fee and other charges. Device capabilities: Add’l charges apply. Push to Talk requires compatible phone and is available only with other Verizon Wireless Push to Talk subscribers. Largest claim based on comparison of carrier-owned/operated Push to Talk coverage areas. Offers and coverage, varying by service, not available everywhere. Network details and coverage maps at verizonwireless.com. While supplies last. Shipping charges may apply. Limited time offer. ©2009 Verizon Wireless.

Call 1.800.VZW.4BIZ Click verizonwireless.com/pushtotalk Visit a Verizon Wireless store

America’s Largest Push to Talk Coverage Area. Delivered.Switch to Verizon Wireless, owner of the nation’s largest Push to Talk Network coverage area, plus get America’s Most Reliable Voice Network. Make your business more productive at the push of a button.

With new 2-yr. activation on any Nationwide voice plan with Push to Talk feature when you have 5 or more business lines.

Add Push to Talk for only $5

Motorola Adventure™ V750Ruggedly Refined.

FREE

G’zOne Boulder™ Built to Survive.

$2999

Verizon Wireless 8975On-the-Go Communications System.

FREE

a month to any Nationwide voice plan and get these great deals!

I N S I D E W O R L D T R A D E

As we turn the page at World Trade, you’ll notice that

aside from our new name—WT100—we’ve begun to make some editorial changes too.

Our Policy Perspec-tives column has been replaced with Green Matters—a column summarizing ‘green’ news in the logis-tics sector as well as

broader sustainability initiatives.Great Moments, which highlighted

historical milestones in world trade, has been swapped out for SCI-fi (the “SCI” standing for Supply Chain Innovations), a column profi ling cutting edge, radical, and in some cases ‘still on the drawing board’ developments and technologies that have potential for future supply chains.

In this month’s annual survey of the U.S.’ leading trade partners and biggest imports and exports, one thing stayed the same, however, and that’s Canada’s posi-tion as our top trade partner. We again consulted Coface for their assessment of the risk associated with these trade part-ners and also added several new indices, like the Heritage Foundation’s Index of Economic Freedom and the World Eco-nomic Forum’s Global Competitiveness Ranking, to see how our top 15 trade part-ners fared on other fronts.

It’s worth mentioning that our trade relationship with Canada isn’t entirely rosy at the moment, with the ‘Buy American’ provision contained within the American Recovery and Reinvestment Act causing a bit of friction with our northern neighbor.

Susan Kohn Ross, International Trade Counsel with Mitchell Silberberg & Knupp LLP addressed this issue recently, calling into question the three arguments that are typically used to defend Buy American provisions.

The fi rst argument states that most other countries have similar provisions. “But, since when did the fact that lots of folks do some-thing make it right?” she asks. Moreover, tax-payer money shouldn’t be spent on foreign products, and third, using American-made inputs supports American jobs, say support-ers of the Buy American provision. “Cer-tainly, we all want to see full employment, but there are four industries that the U.S. has historically protected through high tariffs and non-tariff barriers (such as quotas)—automo-biles, wearing apparel and textile products, footwear, and steel and steel products. How many of them are competitive in today’s world market?” Ross responds. She adds that, “As to spending taxpayer money for these infrastructure projects, shouldn’t the goal be to get the best return on our invest-ment? All things being equal, including the safety and effi cacy of the fi nished product, shouldn’t we use the cheapest inputs, even if they are foreign? Doesn’t the government have a fi duciary duty to get the best bang for the taxpayer buck?”

And yet, just when it looks like rising pro-tectionism is getting a foothold, our trade relations with Cuba are showing the earliest signs of reparation, as contributing editor Dan McCue reports this month. President Obama’s easing of family travel restrictions and remittances earlier this year has given hope to many in the trade community that the long-standing trade embargo will even-tually be dismantled too.

Administrations change. Trade policies change. World trade (and World Trade) changes.

As always, we welcome your view. Drop us an email or visit us on Facebook and let us know what you see.

LARA L. SOWINSKI

Out with the Old, in with the New

Lara L. Sowinski, [email protected]

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 88

Group Publisher Tom EspositoPublisher Sarah Harding

Managing Editor Lara L. SowinskiArt Director Michael T. Powell

Contributing WritersMark Bernstein, Richard Barovick, Gail Dutton, Joshua Kurlantzick,

Andrea MacDonald, Clay Risen, Jeremy Smith, April Terreri, Amy Zuckerman

SALES

Grant BelangerFord Motor Company

Director South America Operations

Steve PalagyiDirector, Pacifi c Region

PRTM Consulting

Erik AutorVice President and

International CounselNational Retail Federation

Susan G. EssermanChair, International Department

Steptoe & Johnson

Beth EnslowGlobal Supply Chain Resiliency

Marsh, Inc.

Kurt Cavano, Chairman and CEO,

TradeCard

Frank Vogl, Vogl Communications,

Washington D.C.

Thomas E. CrockerCo-Chair International Trade and

Regulatory Group, Alston & Bird LLP

Publisher Sarah Harding/West & Midwest Sales 216.991.4861

National Sales Director-East Randi Giambruno 516.377.3906 [email protected]

Inside Sales Manager/Print Vito Laudati 630.694.4018 Fax: 248.283.6618 [email protected]

Asia Hong Kong Offi ce Publicitas Wendy Lin Tel: 852.2527.3525, Fax: 852.2528.3260

Director Custom Media Steve Beyer Tel: 847.516.1977, Cell: 630.699.7625 [email protected]

Production Manager John Talan, 248.244.8253Marketing Coordinator Amanda Podina

Web Seminar Project Manager Danielle Belmont, 248.786.1613Reprint Manager & Cindy Williams

Trade Show Coordinator 610.436.4220 ext. 8516 [email protected]

Group Audience Development Manager Christopher Sheehy Multimedia Manager Katie Jabour

Corp. Audience Audit Manager Catherine Ronan Postal List Rental Robert Liska, 800.223.2194 [email protected]

E-mail List Rental Shawn Kingston, 800.409.4443 [email protected] Single Copy & Back Issue Sales Ann Kalb, 248.244.6499 [email protected]

600 Willowbrook LaneSte. 610

West Chester, Pa. 19382www.worldtradeWT100.com

CORPORATE DIRECTORSPublishing Timothy A. Fausch Publishing John R. Schrei

Audience Development Christine A. BalogaCustom Media Steve M. Beyer

Corporate Strategy Rita M. Foumia Information Technology Scott Kesler

Production Vincent M. Miconi Finance Lisa L. PaulusCreative Michael T. Powell

Marketing Michele Weston-Rowe Directories Nikki Smith

Human Resources Marlene J. WitthoftConferences & Events Scott A. WoltersClear Seas Research John E. Thomas

BNP Media Helps People Succeed in Business with Superior Information

BNP Media Corporate Telephone: 248. 244.6400

For subscription information or service, please contact Customer Service at: Tel: 847.763.9534 or Fax: 847.763.9538 or e-mail [email protected]

PRINTED IN THE USA

OPERATIONS STAFF

WORLD TRADE HEADQUARTERS

CORPORATE

WORLD TRADE MAGAZINE EDITORIAL ADVISORY BOARD

®

Serec provides an exceptional array of fulfi llment ser-vices thanks to our 45+ year history and impeccable compliance rating with virtually all retailers. Some of the many services we offer include: EDI order process-ing, pick and pack, labeling, pricing, and ticketing: light assembly, kitting, and promo packs; e-fulfi llment con-sumer direct; inventory visibility; custom status reports; RFID if required; custom thermoforming; compliance consulting and outsource service; EDI services; UCC – 128 Bar code printing and labeling. If you do not see what you need, please ask as we accommodate most requests. Serec pro-vides its clients with nearly 100 percent compliance. Our dedicated staff is a vital component of this astounding compliance statistic. One hundred percent compliance is more than just a number. A perfect record means that chargebacks are practically eliminated and it guarantees our clients will save money on their distribution and fulfi llment. We pride ourselves on our fl exibility and responsive-ness. Whatever you need, whenever you need it, we ensure that your needs are met in a timely and accurate fashion.

Tom FarrellOwner/DirectorTom Farrell, son of the founder, has provided an excel-lent bridge from the operational expertise available at Serec to the clients currently held at Serec and those interested in acquiring third party fulfi llment/import distribution service offered by Serec. The company’s 45+ years experience in the industry has allowed for a historical evolution including growth and service to some great retail stores including Trader Joe’s, Sears, Adidas, Nike, LA Gear and Wilson.

ALL Things to Some PeopleSEREC

626-961-3666

FAX: 626-330-8458

WWW.SEREC.COM

15351 E. STAFFORD STREET

CITY OF INDUSTRY, CA 91744

TOM FARRELLOwner/Director

T: 312-659-6818

INDUSTRIES SERVEDB2B & B2C Manufacturing: Apparel,

non durable consumer goods, Bath &

Beauty, Toys….

REGIONS SERVEDUSA via Southern CA

WEB HIGHLIGHTS“Things we DO” section of

www.SEREC.com

CATEGORIES 3PL Warehousing

Fulfi llment

Replenishment

Pick/Pack

EDI

E-Fulfi llment

Import Distribution

Crossdocking

Sub-Assembly

Reverse logistics

E-commerce

Product visibility

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 910

Port of Indiana Handling Equipment for Massive Wind Farm The Port of Indiana-Burns Harbor has begun handling shipments of wind turbines and blades, which will be used to construct one of the world’s largest wind farms in the north-western part of the state.

The Meadow Lake Wind Farm—a 26,000-acre “clean energy” project—could eventu-ally contain 600 turbines supply-ing power to more than 250,000 homes.

On June 1, the port received the fi rst shipment of generators and hubs built by Denmark-based Vestas Wind Systems. Later that month, 94 blades measuring 132-feet long by 10-feet high and 6-feet wide were unloaded at the port, along with more generators and hubs.

Cold-ironing for Crowley at the Port of LACrowley tugboats operating at the Port of Los Angeles have begun using newly installed shore-side electrical power when not on the job to cut fuel con-sumption and reduce carbon dioxide emissions. Shore-side electrical power, also known as cold ironing, is expected to reduce Crowley’s carbon dioxide emissions by more than 486,180 pounds in the fi rst year alone, while significantly saving on fuel that was previously used to run the tugs’ generators.

Crowley already has cold ironing capabilities in Seattle, Jacksonville, Pennsauken and Puerto Rico.

“We are very pleased to be a part of this important green ini-tiative with the Port of Los Ange-les,” said Frosty Leonard, Crowley manager of marine operations in California. “Using shore-side power is not only the environ-mentally friendly thing to do, it’s just good business.”

As an added benefi t, Leonard said shore-side power eliminates the constant noise from the engines that disrupts the crews’ rest periods and provides engi-neers a quieter engine room in which to work.

PepsiCo Opens First Green Beverage Plant in ChinaBeverage giant PepsiCo has opened the fi rst green beverage plant in China that complies with the Green Building Council’s Lead-ership in Energy and Environmen-tal Design (LEED) standards.

The beverage facility, located in the western city of Chongq-ing, “is important to the com-pany’s ongoing strategy to expand in emerging markets and broaden its portfolio of locally relevant products,” the company said.

Compared to the average Pep-siCo plant in China, the Chongq-ing plant uses 22 percent less water and 23 percent. To save energy, 75 percent of the plant’s indoor areas feature natural lighting, including a skylight in the packing area and warehouse, while a roof garden insulates the offi ce building and saves energy for cooling and heating.

Dow Chemical in Pilot Project to Create Fuel from Algae, CO2

Dow Chemical has announced plans to partner with Algenol Biofuels in a pilot project to use algae and carbon dioxide to produce ethanol fuel. The site of the project will likely be located at Dow’s Freeport, Texas facility.

The project will be based on Algenol’s technology, which mixes carbon dioxide and saltwa-ter with algae in photobioreactors to produce the biofuel.

Dow said the project aims for “a breakthrough process for etha-nol production” that does not use food sources such as corn.

The U.S. is the world’s top producer of corn-based ethanol, but critics say this diverts needed food supplies and land resources for fuel, while raising food prices on world markets.

NYK Vessel Gets its Power from SolarThe world’s first solar-assisted auto carrier, the NYK Auriga Leader, called the Port of Long Beach last month with a ship-ment of Toyota automobiles.

According to NYK Line execu-tives, the shipment represents the fi rst step towards a distant goal of developing a zero-emis-sion vessel.

The top deck of the NYK Auriga Leader is equipped with 328 solar panels. The panels generate 40 kilowatts of power that feed into the vessel’s auxiliary engine, which in turn supplies the ship’s electricity and other internal power requirements.

Although solar power accounts for only about 0.8 percent of the

vessel’s total electrical energy consumption, it can be combined with other energy-saving mea-sures to reduce energy consump-tion and limit the vessel’s carbon footprint.

Green Technologies to Comprise 40 Percent of Siemens’ OrdersGovernment economic stimulus plans are expected to result in 15 billion euros ($21 billion) in orders worldwide between 2010-2012 for Siemens, with about 40 percent of that amount for envi-ronmental or “green” technolo-gies, the company said recently.

Already, the company’s pro-duction of such products as low-consumption light bulbs and wind turbines accounted for roughly 19 billion euros in Sie-mens’ 2007/2008 fi scal year.

Meanwhile, in 2011, orders for green products are forecast to climb to 25 billion euros, Siemens said. WT

KCS Railroad Greens its LocomotivesKansas City Southern railroad is adding 27 locomotives to its fl eet that utilize Electro-Motive Diesel (EMD) technology. The locomotives minimize fuel consumption while maintain-ing emissions compliance, producing 25 percent fuel savings, 50 percent lube oil reductions, and 70 percent reduction in greenhouse gas emissions, which makes them U.S. Environ-mental Protection Agency (EPA) Tier II compliant and eligible for both state and federal funding as clean air projects.

Eleven locomotives will be in service on the Kansas City Southern Railway Company network, while 16 locomotives will be in service on the Kansas City Southern de Mexico, S.A. de C.V.

GREENMATTERS

This conference will provide you best practices and solutions from leading supply chain practitioners and thought leaders that your organization can use to drive improvements.

Choose from over 100 professional education sessions in 20 tracks including: transportation, warehousing, inventory management and demand planning, third party logistics, supply chain integration, and global infrastructure management. Representatives from over 40 countries and leading FORTUNE 500 companies will be attending.

Network with over 3,000 like profession-als. To register and see who is attending, go to cscmpconference.org.

Register before August 15 and SAVE $150 US!

The World’s Leading Source for the Supply Chain Profession.™

KEYNOTE SPEAKER:Gary Maxwell, Senior Vice President of International

Supply Chain for Wal-Mart Stores, Inc.

Attend Supply Chain’s Premier Event™

September 20-23 in Chicago. Take HomeIdeas and Tools that will Help Drive

Improvements Within Your Organization.

SUPPLY CHAINT R U C K I N G A I R O C E A N T E C H N O L O G Y T R A D E F I N A N C E 3 P L W A R E H O U S I N G

Watch

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 912

AIR

Freight Demand Stabilizing, Says IATAThe International Air Transport Association (IATA) said recently that demand for airfreight has begun to stabilize, with May’s volumes posting a modest 3 per-cent increase over April’s fi gures.

According to IATA, the latest fi gures represent a “fi rst sign” of economic recovery in equity markets.

Nonetheless, the industry group says the long-term outlook for airfreight remains grim.

“Even if we look beyond the [economic] crisis, it is diffi cult to see a return to business as usual. This crisis is re-shaping the industry,” stated IATA director-general Giovanni Bisignani.

The impact of airline debt and low asset prices will also delay any recovery, according to IATA, which estimates the industry may lose $9 billion this year.

UPS, FedEx to Trim Fuel Costs

United Parcel Service (UPS) and FedEx have both announced fuel saving measures that will not only trim costs but boost sus-tainability efforts too.

For its part, UPS aims to cut its airline fl eet’s greenhouse gas emissions 42 percent from 1990 levels during the next decade by using less fossil fuel in its jets.

The company operates the world’s ninth-largest private air-line fleet with 228 jumbo jets in service and 314 more char-tered aircraft. UPS is planning to invest in more fuel-effi cient air-craft models, introduce biofuels, reduce runway idling and opti-

mize fl ight routes, among other things, to slash its fuel costs and emissions of carbon dioxide and other heat-trapping gases.

“Our customers are asking us to do this and are looking for green partners,” said Lynnette McIntire, a company spokes-woman. “We are a huge part of their supply chain.”

On the other hand, rival FedEx says it plans to get 30 percent of its fuel from petroleum alterna-tives by 2030. According to the company’s CEO Fred Smith, FedEx will soon switch from MD-11s to Boeing 777s for its long-range, international routes. The com-pany will also phase-out Boeing 727s for 757 models, which are 47 percent more fuel-effi cient.

Aviation accounts for about 10 percent of U.S. greenhouse gas emissions from transporta-tion, or about 2.7 percent of the nation’s overall carbon footprint, according to the U.S. Department of Transportation.

OCEAN

Major Shipping Lines Hike Asia-U.S. RatesThe 14 shipping lines of the Transpacifi c Stabilization Agree-ment (TSA) say they will hike rates by $500 per 40-foot con-tainer on the eastbound Asia-U.S. route to end a price war caused by slumping demand, overcapac-ity and “panic.”

The increase will take effect on August 10.

Average revenue per container dropped as much as $1,200 from October to May, the TSA said.

“The lines are taking the opportunity of the peak season to reduce losses,” remarked a shipping analyst. “That doesn’t mean demand has come back.”

Maersk to Open Chassis Pool in NY/NJ Region

Maersk Line is planning to open a chassis pool in the New York/New Jersey port region during the third quarter—the first in a number of sites the company plans to unveil.

The NY/NJ location will offer over 5,000 chassis, however Maersk will eventually make its total U.S. fl eet of 90,000 chassis available throughout the U.S.

The company said the new business model for its chassis fl eet will fundamentally change its carbon footprint. It estimates that the program will cut carbon dioxide emissions by over 4,000 tons a year when the program is rolled out nationwide.

The U.S. Environmental Pro-tection Agency’s SmartWay Trans-port Partnership recommends the use of common chassis to reduce the environmental impact of drayage. “According to SmartWay, common chassis pools can help trucking companies save fuel and reduce greenhouse gas emissions by minimizing unnecessary truck movements and idling associ-ated with switching chassis,” explained Lee Kindberg, Maersk Line’s environmental director.

RAIL

UP Investments Boosting Intermodal Union Pacifi c Railroad says that improvements on its network over the past few years are help-ing boost intermodal capacity and on-time performance, which is now at an all-time high.

According to the railroad, recent routing upgrades have

reduced mileage and prevented congestion in certain lanes, such as a northern California-to-Dal-las route that’s more than 1,000 miles shorter and takes 30 fewer hours to travel through compared with a previous route.

The Omaha, Nebraska-based railroad plans to invest $1.7 bil-lion during this year to strengthen the track infrastructure across its more than 32,000-mile system.

TRUCKING

Mexican Truck Ban Costly for Some U.S. BusinessesThe U.S. government’s decision this past spring to ban funding for a pilot program allowing Mexican trucks full access to U.S. highways prompted Mexico to impose retal-iatory tariffs on U.S. exports to Mexico, which is making it costlier for many U.S. businesses.

According to a report in the Dallas Morning News, eighty-fi ve of the 90 U.S. exports targeted by the retaliatory tariffs are made or grown in Texas. And one company, Dallas-based cosmetics manufacturer Mary Kay, says the tariffs are costing the company an additional $450,000 each month.

Mary Kay has joined with other companies to urge the Obama administration to fi nd a solution that would allow Mexican trucks back onto U.S. highways.

“Since the tariffs were imposed, we have worked non-stop to affect this issue,” noted Anne Crews, Mary Kay’s vice president for government rela-tions. “This is having a real effect on U.S. companies and needs a quick resolution.”

Transportation Secretary Ray LaHood has stated that he is optimistic that a solution could be found very soon. WT

W W W . W O R L D T R A D E W T 1 0 0 . C O M 13

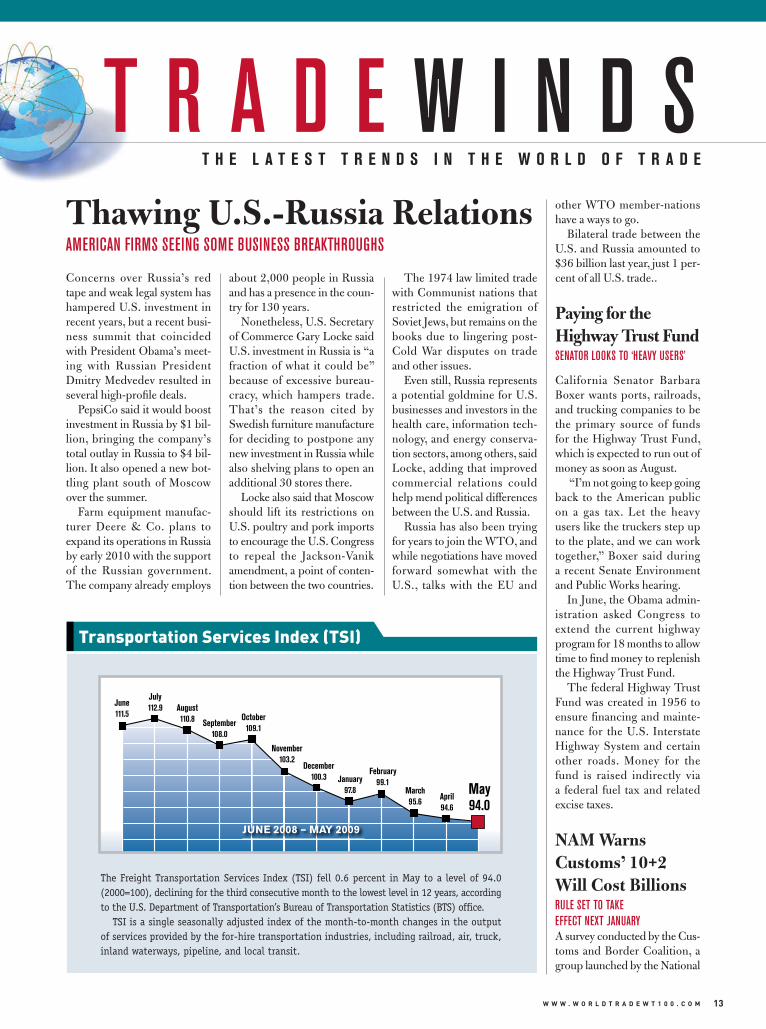

Concerns over Russia’s red tape and weak legal system has hampered U.S. investment in recent years, but a recent busi-ness summit that coincided with President Obama’s meet-ing with Russian President Dmitry Medvedev resulted in several high-profi le deals.

PepsiCo said it would boost investment in Russia by $1 bil-lion, bringing the company’s total outlay in Russia to $4 bil-lion. It also opened a new bot-tling plant south of Moscow over the summer.

Farm equipment manufac-turer Deere & Co. plans to expand its operations in Russia by early 2010 with the support of the Russian government. The company already employs

about 2,000 people in Russia and has a presence in the coun-try for 130 years.

Nonetheless, U.S. Secretary of Commerce Gary Locke said U.S. investment in Russia is “a fraction of what it could be” because of excessive bureau-cracy, which hampers trade. That’s the reason cited by Swedish furniture manufacture for deciding to postpone any new investment in Russia while also shelving plans to open an additional 30 stores there.

Locke also said that Moscow should lift its restrictions on U.S. poultry and pork imports to encourage the U.S. Congress to repeal the Jackson-Vanik amendment, a point of conten-tion between the two countries.

The 1974 law limited trade with Communist nations that restricted the emigration of Soviet Jews, but remains on the books due to lingering post-Cold War disputes on trade and other issues.

Even still, Russia represents a potential goldmine for U.S. businesses and investors in the health care, information tech-nology, and energy conserva-tion sectors, among others, said Locke, adding that improved commercial relations could help mend political differences between the U.S. and Russia.

Russia has also been trying for years to join the WTO, and while negotiations have moved forward somewhat with the U.S., talks with the EU and

other WTO member-nations have a ways to go.

Bilateral trade between the U.S. and Russia amounted to $36 billion last year, just 1 per-cent of all U.S. trade..

Paying for the Highway Trust FundSENATOR LOOKS TO ‘HEAVY USERS’

California Senator Barbara Boxer wants ports, railroads, and trucking companies to be the primary source of funds for the Highway Trust Fund, which is expected to run out of money as soon as August.

“I’m not going to keep going back to the American public on a gas tax. Let the heavy users like the truckers step up to the plate, and we can work together,” Boxer said during a recent Senate Environment and Public Works hearing.

In June, the Obama admin-istration asked Congress to extend the current highway program for 18 months to allow time to fi nd money to replenish the Highway Trust Fund.

The federal Highway Trust Fund was created in 1956 to ensure financing and mainte-nance for the U.S. Interstate Highway System and certain other roads. Money for the fund is raised indirectly via a federal fuel tax and related excise taxes.

NAM Warns Customs’ 10+2 Will Cost BillionsRULE SET TO TAKE EFFECT NEXT JANUARYA survey conducted by the Cus-toms and Border Coalition, a group launched by the National

June111.5

July112.9 August

110.8 September108.0

October109.1

November103.2

December100.3 January

97.8

February99.1

March95.6 April

94.6

May94.0

The Freight Transportation Services Index (TSI) fell 0.6 percent in May to a level of 94.0 (2000=100), declining for the third consecutive month to the lowest level in 12 years, according to the U.S. Department of Transportation’s Bureau of Transportation Statistics (BTS) offi ce.

TSI is a single seasonally adjusted index of the month-to-month changes in the output of services provided by the for-hire transportation industries, including railroad, air, truck, inland waterways, pipeline, and local transit.

JUNE 2008 – MAY 2009

Transportation Services Index (TSI)

Thawing U.S.-Russia RelationsAMERICAN FIRMS SEEING SOME BUSINESS BREAKTHROUGHS

T R A D E W I N D ST H E L A T E S T T R E N D S I N T H E W O R L D O F T R A D E

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 914

T R A D E W I N D S

Association of Manufacturers (NAM), fi nds that U.S. Customs and Border Protection’s (CBP) 10+2 rule will end up costing the U.S. economy more than $20 billion annually.

“The potential impact of this rule is huge,” warned John Engler, president of NAM. “To put the cost in perspective, it is virtually the equivalent of doubling the import tariffs that manufacturers now pay to bring

products and components into the United States.”

CBP’s Importer Security Filing rule, known as 10+2, requires importers to provide 10 data elements and ocean carriers an additional 2 ele-ments to CBP no later than 24 hours before ocean cargo is laden on board a vessel des-tined to the U.S.

The rule will be fully imple-mented on January 26, 2010.

At that time, CBP plans to enforce the rule with penalties of $5,000 per violation.

U.S. Logistics Costs DroppingFIRST TIME IN 6 YEARS, FINDS CSCMP REPORT

The latest “State of Logistics Report” released by the Council of Supply Chain Management

Professionals (CSCMP) reveals that logistics costs fell to 9.4 percent of U.S. gross domes-tic product (GDP) in 2008—a stark contrast to the previous 5 years that saw logistics costs rise 50 percent overall.

Inventory-carrying costs experienced a 13 percent drop in 2008, and were the driving force behind the year’s decline in logistics costs. The decrease in carrying costs was due to both a 2.2 percent drop in inventories and an 11.2 percent decrease in the inventory-carrying rate.

Since 1988, the report has tracked and measured all costs associated with moving goods through the U.S. supply chain. The report benchmarks key metrics in logistics, such as trans-portation and inventory-carrying costs, freight volumes, and reve-nues, giving practitioners a big-picture view of the performance of the supply chain process.

Commenting on the report, Rick Blasgen, CSCMP president and CEO, said, “The economy will eventually recover, and when it does, those companies that use the statistics and industry insight contained in this report will be better prepared for the busi-ness boom ahead. This research details ways that company lead-ers can capitalize on the recovery when it occurs, such as restructur-ing their distribution networks to maximize effi ciency and minimize miles, investing in technologies to facilitate ‘green’ transportation, and improving real-time data flows to increase visibility and enhance productivity.”

Asia-Pacifi c Primed for SaaSSTRONG GROWTH FORECAST FOR ON-DEMAND APPS

A survey by Springboard research shows that the Asia-Pacifi c market for Software-as-a-Service (SaaS) will grow from $35 million in 2008 to $193 million by 2012.

Kurz, Widdows Receive AwardsThe United Seamen’s Service (USS) 2009 40th Annual Admi-ral of the Ocean Sea Awards (AOTOS) will be presented to Donald Kurz, President and CEO of Keystone Shipping Co., headquartered in Philadelphia, and to Ronald Widdows, Group President and CEO of NOL (Nep-tune Orient Lines) of Singapore, parent company of American President Lines (APL).

The maritime industry’s most prestigious honors will be awarded at a gala industry dinner and dance to be held at the Sheraton New York Hotel and Towers, New York City, on November 13, 2009.

Echo Global Logistics’ Waggoner RecognizedEcho Global Logistics, a technol-ogy-driven transportation man-agement fi rm, has announced that CEO Douglas Waggoner received the Ernst & Young Entrepreneur Of The Year® 2009 Award in the Emerging Compa-nies category in the Midwest region. According to Ernst & Young LLP, the award recog-nizes outstanding entrepreneurs who are building and leading dynamic, growing businesses.

MOL Appoints AnMOL has appointed Andrew An to the position of assistant vice president North America China sales. An joined MOL’s Atlanta offi ce in 1997 as an account executive, and has since served in various sales assignments throughout the country.

Ryan in New Role at CEVA LogisticsCEVA Logistics has appointed Matthew Ryan to the newly cre-ated position of Chief Operat-ing Offi cer. This role will focus on ensuring CEVA continues to provide industry leading opera-tional and supply chain service excellence.

Chipman Next CEO for Grant Thornton Stephen Chipman will assume the CEO spot at accounting fi rm Grant Thornton on Janu-ary 1, 2010. Chipman was most recently chief executive offi -cer, Greater China Management Corporation, responsible for leading the development and growth of services for Grant Thornton in China.

TMCA Awards AbernathyThe Transportation Market-ing & Communications Asso-

ciation (TMCA) has awarded George Abernathy, executive vice president and chief oper-ating offi cer for Transplace, as the “2009 TMCA Transpor-tation Marketing Executive of the Year.” This honor was awarded June 2 at TMCA’s Annual Conference in San Diego, Calif.

Freese to Succeed Newsome at Hapag-LloydHapag-Lloyd, the German ocean container carrier, announced that Wolfgang Freese will suc-ceed Jim Newsome as president of Hapag-Lloyd (America) on September 1.

Newsome will leave the com-pany after 12 years to take a new job as president and chief executive offi cer of South Caro-lina State Ports Authority.

Sky-Trax Chooses McDonnellWilliam H. McDonnell has been hired by Sky-Trax Inc. to serve as the company’s Chief Finan-cial Offi cer. McDonnell will be responsible for the company’s financial controls, financial reporting, financial plan-ning, day-to-day management of financial operations, and human resources.

Names News&

W W W . W O R L D T R A D E W T 1 0 0 . C O M 15

The survey revealed that 35 percent of the respon-dents intended to purchase SaaS-based ERP (enterprise resource planning) in the next 12 months. Around 20 percent of those surveyed were already using SaaS ERP.

Analysts predict the SaaS market to grow faster in Asia, especially in the markets of China and India, than in U.S. or any Western market.

SaaS is a model of software deployment whereby a pro-vider licenses an application to customers for use as a service on demand.

Japan to Recognize U.S. Trade Security ProgramsMUTUAL RECOGNITION WILL HELP EXPEDITE CARGO CLEARANCESOffi cials from Japan and the U.S. have agreed to mutually recog-nize their respective trade secu-rity and facilitation programs to expedite bilateral trade.

The U.S. trade security and facilitation program is the Customs-Trade Partnership Against Terrorism program, or C-TPAT.

According to Japanese offi -cials, the mutual recognition agreement is the second of its kind for Japan and the fi fth of its kind in the world. The coun-try already has a similar pact in place with New Zealand, while the U.S. has established agreements with New Zealand, Canada, and Jordan.

Tightening Security at India’s Top Box PortRECENT SNAFUS HIGHLIGHTED LAPSESCustoms officials at the Port of Jawaharlal Nehru—India’s biggest container port—have issued new security regulations to improve container-screening procedures.

The move follows a string of incidents where containers, specifi cally those identifi ed for scanning, evaded the customs agency’s scrutiny. “It has been noticed that sometimes con-tainers, which are selected for scanning, are not presented for scanning and are being taken directly to respective freight stations without scanning. This non-reporting of selected containers to the scanners is defeating the very purpose of scanning in the heightened security scenario,” customs offi cials explained.

The new procedures stipu-late that once a container is selected for scanning, it will not be exempted from the process.

India’s Port of Jawaharlal Nehru handles nearly 60 per-cent of India’s container traffi c. In fi scal 2008-09, total volume handled by its three terminals was 3.95 million TEUs, com-pared with 4.06 million TEUs the previous year.

Seizures of Fake Goods Up 125% in EUMORE THAN HALF FROM CHINAThe European Commission says the number of counterfeit seizures jumped 125 percent between 2007 and 2008, with over half coming from China.

Customs offi cers seized 178 million counterfeit items last year that were headed for the 27 nations in the European Union, including CDs, DVDs, cigarettes, and clothing.

In fact, CDs and DVDs accounted for 44 percent of confi scated items followed by cigarettes at 23 percent and clothing at 10 percent.

The Commission found that more than half of the fake goods confi scated in 2008 came from China. Furthermore, a signifi -cant portion of the confi scated products were potentially dan-gerous for European consum-

ers, the governing body said.Fake medicine came from

India, forged food and drink products were from Indone-sia, while the United Arab Emirates was listed as the main source of counterfeit cigarettes, said offi cials.

EU, U.S. Challenge China’s Export RestraintsWTO CALLED IN TO INVESTIGATETrade officials from the EU and U.S. have requested inves-tigations from the WTO over China’s export restraints on several important raw materials, including bauxite, coke, fl uor-spar, magnesium, manganese, silicon metal, silicon carbide, yellow phosphorus, and zinc.

China is a major global pro-ducer of these raw materials.

According to U.S. Trade Representative Ron Kirk, his agency “is very concerned that China appears to be restricting the exports of these materials at the expense of U.S. industries that need these materials, and their workers. This appears to be occurring despite strong WTO rules designed to disci-pline export restraints.”

For her part, EU Trade Com-missioner Catherine Ashton said, “The Chinese restrictions on raw materials distort compe-tition and increase global prices, making things even more diffi -cult for our companies in this economic downturn.”

Athens Airport Improving Customs ClearancesOLYMPIC GAMES PROVIDED THE PUSH

The Athens Airport is working with the EU to improve cus-toms clearances and automate the cargo system to bring it up to par with other European airports.

“It is vital that we provide a fast and flexible service to encourage more freight traffi c at this airport,” said Vasiliki Kalamara, who took over as head of Airport Customs some eighteen months ago.

Since the Olympic Games four years ago, Athens Airport has gradually introduced more fl exible procedures and oper-ating hours, particularly for freighters, which mostly oper-ate at night. WT

SCOPE WestLas Vegas, NevadaAugust 19-21www.scopewest.com

Third International Conference on Energy Solutions for TransportReykjavik, IcelandSeptember 14-15www.drivingsustainability.org

CSCMP Annual Global Conference 2009Chicago, IllinoisSeptember 20-23http://cscmpconference.org

Cool LogisticsHamburg, GermanySeptember 28-30www.coollogisticsconference.com

MARK YOUR

Calendar

World Trade Magazine will be publishing announcements of forthcoming global supply chain events in every issue. For inclusion, please forward event details to [email protected]

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 916

COVER STORY

While the downturn in the global economy is affecting trade partners across the board, some have higher risk factors than others.

D T RD T R AD T R AD T R AAD T R ATD TDD D E 1DDDDDDDDDDD EE D E E E D E 1D E 1DDDDDD ED 0 00000000

Trade PartnersTop U.S.

The Outlook for the

For this year’s snapshot of the risk factors associated with the top U.S. trade partners, we again turned to Coface, a world leader in trade-credit information and protection, for their expertise and analysis. The sobering news is that the 2008-2009 credit crisis, defi ned as a sub-stantial rise in corporate defaults stemming from an economic shock, is quite serious, with simultaneous recessions in the world’s three major industrialized regions: Japan, Western Europe, and the United States. Furthermore, dwindling demand coupled with a credit crunch brought on by the banking crisis is a vicious cycle that can only be broken by a restoration of confi dence, according to Coface. On a better note, the credit crisis should end by late 2009, Coface believes, and if the global economy has indeed reached the proverbial ‘bottom’ and has begun to stabilize, then we can say with assurance that we are setting foot on the path to recovery. –Lara Sowinski, Editor

W W W . W O R L D T R A D E W T 1 0 0 . C O M 17

W W W . W O R L D T R A D E W T 1 0 0 . C O M 19

CanadaThe economy sagged slightly in the second half of 2008, a trend expected to continue in early 2009 before giving way to a period of stabilization and then a modest recov-ery toward year-end. The economic decline is attributable to persistently poor export performance—with a quarter of Canada’s growth dependent on economic conditions in the United States—and the downturn of investment. Although consumption has shown some strength, it has not suffi ced to reverse the negative trend.

Exports will continue to decline due to weaken-ing demand from the United States for manufactured products, the Canadian dollar depreciation against the U.S. dollar notwithstanding. Amid falling world prices, meanwhile, raw material sales will decline more sharply in value than in volume.

Investment will in general also trend down. Corporate investment will suffer from both sluggish demand and less favorable credit conditions. The downturn will be sharper in the western provinces—especially Alberta—which have suffered most from the bursting of the raw-materials speculative bubble. The collapse of oil prices will moreover likely jeopardize several oil shale explora-tion and exploitation projects.

Households are expected to invest slightly less on housing but that trend will be unlikely reach the pro-portions observed in the United States thanks to a more tightly supervised system of fi nancing and the absence of past excesses. Sharp declines could nonetheless develop in major western urban areas.

Consumption by households will likely manifest some strength refl ecting their generally good fi nancial health and limited indebtedness, the continued growth of real wages, and an unemployment rate that, although rising, remains at historically low levels. Public spending is sim-ilarly expected to remain an anchor of economic stability thanks to the public sector’s good fi nancial health.

ChinaAfter peaking in 2007 with 11.9 percent annual growth, the Chinese economy cooled in 2008 amid a slowdown of exports and domestic demand. Export growth slowed somewhat mainly as a result of sagging demand from industrialized countries, which absorb 46 percent of total sales abroad. Consumption declined, meanwhile, essentially as a result of growing infl ation in 2008 and rising unemployment. Furthermore, a slowdown of investment is partly attributable to the narrowing of cor-porate margins, particularly in sectors with overcapacity (steel, car industry, real estate, etc.).

To deal with the slowdown, the government has adopted a more expansionary monetary policy. Since late 2008, offi cials have similarly shifted gears on exchange rate policy to foster stabilization or depreciation of the yuan and bolster export sectors in diffi culty. And with the leeway afforded by low public sector debt (15 per-cent of GDP) and a high savings rate, the government has decided to implement a $586 billion fi scal stimulus plan devoted to major infrastructure projects—with invest-ments in transportation and electricity, reconstruction of areas devastated by the earthquake, among others—and

social measures (education, subsidies to rural populations, housing aid, etc.). The plan is intended to avert a severe-slowdown scenario that could cause a significant upsurge of payment defaults and an increase in social unrest.

Despite the fi scal stimulus, the risk of payment failures in particular sectors will nonetheless remain substantial. Low-end export sectors with tight margins, like textiles, shoes, and toys, suffered from the acceleration of the yuan appreciation in the fi rst nine months of 2008, the rise of wages, and problems with product quality. Sectors like automotives and property where sales transactions are commonly made on credit have also been in diffi-culty. According to Coface monitoring records, payment behavior has been deteriorating—a trend likely to worsen in 2009 as the economic slowdown tightens its grip.

MexicoAffected mainly by the economic recession in the U.S. along with the international fi nancial crisis, Mexico is expected to suffer a severe economic downturn in 2009, despite fi scal stimulus measures taken by the govern-ment. Monetary authorities will also experience diffi cul-ties in controlling infl ation, attributable mainly to the peso depreciation and pessimistic expectations.

Public debt remains moderate with its foreign com-

uraln

fllnd

extiles,

Country Value

Canada1. $596.9

China2. $409.2

Mexico3. $367.5

Japan4. $205.8

Germany5. $152.3

United Kingdom6. $112.4

South Korea7. $82.9

France8. $73.2

Saudi Arabia9. $67.3

Venezuela10. $64.0

Brazil11. $63.4

Taiwan12. $61.6

Netherlands13. $61.4

Italy 14. $51.6

Belgium15. $46.4

TOP 15 U.S. TRADE PARTNERS (total goods imported/exportedin 2008; US$ billions)

Source: U.S. Census Bureau

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 920

COVER STORY

ponent in decline. But improvement in public fi nances, still dependent on oil revenues, will

require further efforts on reform of both the tax system and the state-run oil company PEMEX. It will thus be a very slow pro-cess. With a steady decline in oil produc-tion compounded by the fall of oil prices

and the downturn of exports to the U.S. and transfers from emigrant workers, the

external account defi cit will widen. To cover its very large and strongly growing financing

needs and also to compensate for a signifi cant drop in foreign direct investment, Mexico will have to turn not only to international fi nancial institutions, but also to fi nancial markets, though at a high cost. But the stable and moderate level of short-term debt and the fl exibility of the exchange rate will tend to mitigate, albeit increas-ing, liquidity crisis risk. The relatively modest size of the banking sector has moreover sheltered it from exposure to risks resulting from the sub-prime crisis in the U.S.

After the adoption of a limited reform of PEMEX in 2008, modernization of the economy continues to come up against strong social and political resistance. Too, the climate of insecurity and violence resulting from the organized criminal activities associated with narcot-ics traffi cking moreover constitutes a challenge to the

authority of President Felipe Calderon, whose success will partly depend on improvement in this area.

In this context, the business environment leaves room for improvement and the credit crunch handicaps com-panies. Large private fi rms are faced with the drying up of international liquidity. The diffi culties faced by the textile, clothing and shoe industries are, however, the traditional ones and result from an inability to compete with their Asian rivals.

JapanThe spectacular fall of economic growth during the fi rst quarter of 2009 (down an annualized 14.2 percent quarter-on-quarter and down 9.1 percent year-on-year), resulting from the decline in both exports and invest-ment, bears out that of all industrialized countries Japan will likely suffer the most severe recession this year with GDP contracting by 7 percent. The lack of reaction by companies in failing to reduce their stocks and costs in the fourth quarter of 2008 paved the way for the fall of corporate profi ts to their lowest level since 1983. They will therefore have to revise their investment projects downward and adjust production. But production could, however, benefit temporarily from a technical recovery: The vast economic support plan implemented by China and focused chiefl y on investment will likely

Country Value% of Total Imports

China1. $337.8 16.1%

Canada2. $335.6 16.0%

Mexico3. $215.9 10.3%

Japan4. $139.2 6.6%

Germany5. $97.6 4.6%

United Kingdom6. $58.6 2.8%

Saudi Arabia7. $54.8 2.6%

Venezuela8. $51.4 2.4%

South Korea9. $48.1 2.3%

France10. $44.0 2.1%

Nigeria11. $38.1 1.8%

Taiwan12. $36.3 1.7%

Italy13. $36.1 1.7%

Ireland14. $31.6 1.5%

Malaysia15. $30.7 1.5%

Total, Top 15 Countries $1,555.8 74.1%

Total, All Countries $2,100.4 100.0%

Country Value% of Total Exports

Canada1. $261.4 20.1%

Mexico2. $151.5 11.7%

China3. $71.5 5.5%

Japan4. $66.6 5.1%

Germany5. $54.7 4.2%

United Kingdom6. $53.8 4.1%

Netherlands7. $40.2 3.1%

South Korea8. $34.8 2.7%

Brazil9. $32.9 2.5%

France10. $29.2 2.2%

Belgium11. $29.0 2.2%

Singapore12. $28.8 2.2%

Taiwan13. $25.3 1.9%

Australia14. $22.5 1.7%

Switzerland15. $22.0 1.7%

Total, Top 15 Countries $924.2 71.1%

Total, All Countries $1,300.5 100.0%

TOP 15 COUNTRIES FOR U.S. IMPORTS (total goods imported in 2008; US$ billions)

TOP 15 COUNTRIESFOR U.S. EXPORTS (total goods exported in 2008; US$ billions)

Source: U.S. Census Bureau

ponentfi na

ret

aex

its veneeds and

W W W . W O R L D T R A D E W T 1 0 0 . C O M 21

Commodity ExportsVehicles1. $32,341Electrical machinery 2. $27,752Airplanes, engines, and parts 3. $27,443General industrial machines4. $17,995Specialized industrial machines5. $17,340Petroleum preparations6. $14,704Scientifi c instruments 7. $14,007Chemicals - plastics8. $13,586Chemicals - organic9. $12,007Chemicals - medicinal10. $11,619Power generating machines 11. $10,711ADP equipment and offi ce machines12. $9,746Metal ores and scrap13. $8,836Chemicals - n.e.s.14. $8,454Gold, nonmonetary15. $8,196TVs, VCRs, etc. 16. $8,145Soybeans17. $6,434Metal manufactures, n.e.s.18. $6,145Iron and steel mill products19. $5,641Corn20. $5,110Paper and paperboard21. $4,774Vegetables and fruits22. $4,196Textile yarn, fabric23. $4,011Chemicals - inorganic24. $4,006Wheat25. $3,931Chemicals - cosmetics26. $3,712Meat and preparations27. $3,543Plastic articles, n.e.s.28. $3,158Pulp and waste paper29. $2,668Animal feeds30. $2,618Basketware, etc.31. $2,474Gem diamonds32. $2,292Coal33. $2,112Aluminum34. $2,085Printed materials35. $2,032Artwork and antiques36. $2,015Chemicals - dyeing37. $2,006Metalworking machines38. $1,954Mineral fuels, other39. $1,951Natural gas40. $1,946Records and magnetic media41. $1,734Furniture and bedding 42. $1,653Toys, games, and sporting goods43. $1,620Jewelry44. $1,605Cotton, raw and linters45. $1,593Chemicals - fertilizers46. $1,503Cork, wood, and lumber47. $1,419Copper48. $1,327Fish and preparations49. $1,309Rubber tires and tubes 50. $1,261

Top 50 U.S. Goods Exports

Commodity ImportsCrude oil1. $110,014Vehicles2. $69,829TVs, VCRs, etc. 3. $40,719Electrical machinery4. $37,171ADP equipment and offi ce machines5. $31,965Petroleum preparations6. $28,539Clothing7. $23,834General industrial machines8. $22,672Chemicals - medicinal9. $19,434Chemicals - organic10. $16,254Power generating machines 11. $15,954Natural gas12. $12,798Specialized industrial machines13. $12,368Scientifi c instruments 14. $12,250Iron and steel mill products15. $10,856Furniture and bedding 16. $10,789Metal manufactures, n.e.s.17. $9,783Airplanes, engines, and parts 18. $9,222Toys, games, and sporting goods19. $8,056Vegetables and fruits20. $7,346Textile yarn, fabric21. $7,275Gem diamonds22. $6,699Chemicals - plastics23. $6,319Footwear24. $6,292Paper and paperboard25. $5,835Chemicals - inorganic26. $5,052Plastic articles, n.e.s.27. $5,043Aluminum28. $4,269Chemicals - n.e.s.29. $4,256Fish and preparations30. $4,002Basketware, etc.31. $3,924Copper32. $3,603Rubber tires and tubes 33. $3,270Chemicals - cosmetics34. $3,099Artwork and antiques35. $3,052Metal ores and scrap36. $2,931Jewelry37. $2,868Platinum38. $2,861Metalworking machines39. $2,860Wood manufactures40. $2,819Chemicals - fertilizers41. $2,644Gold, nonmonetary42. $2,495Lighting and plumbing43. $2,385Travel goods44. $2,296Records and magnetic media45. $2,181Cork, wood, and lumber46. $2,039Liquefi ed propane and butane47. $1,751Optical goods48. $1,711Printed materials49. $1,704Meat and preparations50. $1,596

Top 50 U.S. Goods Imports

TOP 100 U.S. IMPORTS & EXPORTS(goods traded in 2008; in US$ millions)

Source: U.S. Census Bureau

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 922

COVER STORY

enable Japanese mechanicals and metal processing sectors to limit the deterioration of their busi-

ness activity. That temporary relief from the overall trend will, however, remain marginal since Japanese exports to China correlate with Chinese exports to the U.S. and Euro-pean Union.

The improvement in consumer con-fidence recorded in May was largely

attributable to various stimulus measures implemented by the government in the second

quarter, particularly for purchases of vehicles and home furnishings. Despite these measures, household consumption—already relatively fl at before the crisis—will decline in 2009 (down 2 percent), undermined by the rise of unemployment (5.9 percent) and the decline in disposable income (with fi nancial assets constituting 70 percent of net wealth), and savings are expected to increase to 7.6 percent of disposable income.

GermanyUndermined by the marked weakening of exports, the German economy slipped into recession in spring 2008, a trend expected to continue until autumn 2009 with a timid recovery possibly developing thereafter. Persis-tently sluggish household consumption will provide little backup support to the economy.

In the context of a severe slowdown of the world econ-omy and trade, exports, which had been the main growth engine (41 percent of GDP) until early 2008, are now proving to be the main vector of the recession. Half capi-tal goods (including automotive vehicles) and half con-sumer goods, the export trend refl ects both the end of the investment boom in emerging and raw material producing countries and the downturn of household demand from the major European and American trading partners.

Faced with stagnating exports, eroding margins, and

tightening credit, German industry will likely put its invest-ments on hold. Nonetheless, household consumption will make a slightly positive contribution to growth despite the drop in capital goods purchases like automotives.

In this context, corporate payment behavior, while sat-isfactory in 2008, could deteriorate in 2009 particularly in sectors heavily dependent on exports, like automotive and aeronautical subcontracting, textiles and clothing, mari-time and river transport, and,to a lesser extent, metallurgy, chemicals, and industrial capital equipment.

United KingdomWith the growing impact of the fi nancial and property crisis on household and corporate spending, the eco-nomic downturn will intensify in 2009.

Households have been facing a rapid decline in home prices, which could ultimately fall 30 percent, and tight-ening credit conditions with their debt representing 170 percent of disposable income. A slumping employment market and the concomitant rise of unemployment—not only in fi nancial services and construction but also in other sectors—will also be a drag on the economy.

Only foreign trade is expected to make a slightly posi-tive contribution to GDP growth, thanks to the drop in imports. Exports, meanwhile, are also expected to decline, but to a lesser extent, due to the sluggishness of foreign demand despite a weakening pound sterling, since a high proportion of sales abroad involve special-ties, like pharmaceuticals, software, and IT services that are by nature relatively insensitive to price fl uctuations.

In a deteriorating environment, corporate health has been weakening, particularly in construction, property services, transport, machinery rental, distribution (home furnishings, automotives, consumer electronics, cloth-ing), and outbound tourism: all sectors suffering from the defection of consumers. The highly competitive retail sector has been the riskiest of all. Greater London,

Water Value

Los Angeles1. $180.2

New York-New Jersey2. $165.2

Long Beach3. $147.1

Houston4. $114.6

Charleston5. $60.9

Savannah6. $49.6

Norfolk7. $49.5

Baltimore8. $42.0

Seattle9. $37.6

Oakland10. $34.8

Air Value

New York (JFK)1. $161.2

Chicago O'Hare2. $86.6

Los Angeles3. $79.6

San Francisco4. $61.6

Anchorage5. $45.3

Dallas-Fort Worth6. $41.5

New Orleans7. $41.1

Atlanta8. $35.4

Miami9. $34.5

Cleveland10. $27.3

Land Value

Detroit, MI1. $136.6

Laredo, TX2. $110.4

Buffalo-Niagara Falls, NY3. $78.6

Port Huron, MI4. $77.1

El Paso, TX5. $49.1

Otay Mesa, CA6. $30.7

Hidalgo, TX7. $21.9

Champlain-Rouses Pt., NY8. $21.5

Nogales, AZ9. $18.2

Blaine, WA10. $17.9

TOP 10 U.S. FOREIGN TRADE GATEWAYS (by Value of Shipment, in US$ billions)

Source: U.S. Department of Transportation, Bureau of Transportation Statistics

enable Jsect

neo

fatt

implequarter p

W W W . W O R L D T R A D E W T 1 0 0 . C O M 23

with the preponderant role played by fi nance and con-struction, will be the hardest hit metropolitan area. The positive factors are few in number but nonetheless noteworthy: the pound sterling depreciation benefi ting exporters, public sector support for short-term fi nanc-ing, the ongoing preparations for the 2012 Olympic Games, and an acceleration of public infrastructure and housing programs benefi ting construction.

South KoreaDespite adoption of expansionary monetary and fi scal policy, economic growth slowed in 2008 due mainly to sagging domestic demand affected by the rise of infl a-tion, deterioration of the labor market, and bursting of speculative bubbles in the stock, property, and credit markets. The rationing of credit also undermined investment by smaller companies. The chaebols, South Korea’s family-controlled conglomerates, remained solid, however, benefi ting from suffi cient resources to continue investing. Exports decelerated to industrialized and Asian countries—which represent, respectively, 35 percent and 47 percent of sales abroad.

In 2009, the economic slowdown could intensify, with domestic demand remaining fl at. Consumption could

decline again amid a negative wealth effect linked to the collapse of the property and stock markets and the rationing of credit, with household debt representing 140 percent of disposable income. Moreover, compa-nies also burdened with heavy foreign currency debt will suffer from the credit crunch. Construction, automotive, and ship owners will again be the sectors to suffer most. In addition, the export slowdown is expected to con-tinue, particularly in electronics. Therefore, corporate payment behavior could deteriorate in 2009.

FranceThe contraction of economic activity in 2008—down a marked 1.2 per cent in the fourth quarter—will continue in 2009 with a further decline of 2 percent expected. Industrial production will likely continue to fall, notably affected by the automotive sector’s diffi culties. To cope with the decline in demand from the main European trading partners (the EU provides a market for 65 per-cent of export sales and Germany 14 percent) and from domestic customers, companies will go on postponing investments and adjusti ng their costs. Explosive growth of unemployment, erosion of fi nancial assets, and limited increases in wage will prompt households to keep their

ON THE TOP OR IN THE TANK?Here’s How Our Top Trade Partners Stack Up on Other Indices

(Note: Hong Kong ranked fi rst on this index, and North Korea last) (Note: The U.S. ranked fi rst on this index, and Chad last) (Note: Denmark, New Zealand, and Sweden tied for fi rst on this index, and Somalia last)

Country Index

Canada1. Free

Japan2. Mostly free

Germany3. Mostly free

UK4. Mostly free

France5. Mostly free

Netherlands6. Mostly free

Belgium7. Mostly free

Mexico8. Moderately free

South Korea9. Moderately free

Saudi Arabia10. Moderately free

Taiwan11. Moderately free

Italy12. Moderately free

China13. Mostly unfree

Brazil14. Mostly unfree

Venezuela15. Repressed

Country Ranking

Germany1. 7

Netherlands2. 8

Japan3. 9

Canada4. 10

UK5. 12

South Korea6. 13

France7. 16

Taiwan8. 17

Belgium9. 19

Saudi Arabia10. 27

China11. 30

Italy12. 49

Mexico13. 60

Brazil14. 64

Venezuela15. 105

Country Index

Netherlands1. 7

Canada2. 9

Germany3. 14

UK4. 16

Japan5. 18 (tied)

Belgium6. 18 (tied)

France7. 23

Taiwan8. 39

South Korea9. 40

Italy10. 55

China11. 72 (tied)

Mexico12. 72 (tied)

Saudi Arabia13. 80 (tied)

Brazil14. 80 (tied)

Venezuela15. 158

Heritage Foundation’s 2009 Index of Economic Freedom

World Economic Forum’s 2008-2009 Global Competitiveness Ranking

Transparency International’s 2008 Corruption Perceptions Index

W O R L D T R A D E 1 0 0 A U G U S T 2 0 0 924

COVER STORY

buying in check and to replenish emergency savings. Exports will tread water, particularly in the automo-

tive and intermediate goods sectors. The current account defi cit will nonetheless narrow with sluggish household consumption and the drop in investment undermin-ing imports. The public sector defi cit will widen sig-nifi cantly, (to a negative 5.3 percent) as a result of the economic downturn and the rescue measures taken by the government: bank-fi nancing guarantees, support to companies and sectors in diffi culty, and public invest-ment spending. Public sector debt will grow meanwhile to nearly 74 per cent of GDP.

Saudi ArabiaDriven by booming oil prices, the revenues raked in these past years have facilitated implementation of vast infra-structure projects, an increase in oil production capacity, a reduction in government debt, and a build-up of fi nancial assets. The kingdom is now in a very strong economic and fi nancial position expected to allow it to cope with the consequences of the world economic crisis that began to appear in 2008 with the fall of stock market indices and capitalizations, the drop in oil prices from July on, in conjunction with a shortage of liquidity and a weak-ening of foreign demand. In this context, strong growth in the first half, buoyed moreover by a sharp increase in oil production, subsequently gave signs of slowing down, particularly in the petrochemical and oil sectors. The economic downturn and the credit crunch affected household consumption and prompted private investors to cancel or postpone some projects. With infl ation easing late in the year, offi cials took measures to increase liquidity and to stimulate the economy. Bank deposits, meanwhile, are guaranteed by the government.

The leading OPEC oil-producing country, Saudi Arabia will likely continue in 2009 to make the most

of the adjustment effort for the downward world-demand trend. Oil production could thus

decline compared to 2008. The business climate improved with

Saudi Arabia’s admission to the WTO late 2005. But, it continues to suffer from persistent weaknesses in governance terms.

The performance of companies could suffer from the economic slowdown with deteriora-

tion of their payment behavior, not unlikely in view of their traditional vulnerability to a downturn

of barrel prices.With barrel prices substantially below their average

levels in 2008, a decline in hydrocarbon production will likely result in a sharp drop in export earnings and fi scal revenues, which still derive mainly from oil.

VenezuelaGDP growth is expected to collapse in 2009 with world oil prices and national production falling. The priority given to redistribution of oil export earnings to the detri-ment of productive investment has moreover jeopardized growth sustainability.

Meanwhile, ill-advised fi scal and monetary policies, in conjunction with inadequate production capacity, have

kept infl ation very high despite price controls. In view of the resulting huge differential in inflation between Venezuela and its main trading partners in conjunction with falling oil prices, a devaluation of the bolivar in 2009 seems necessary. However, the government is still seeking to delay the timing of a move that will only fan the fl ames of infl ation even more.

The trade surplus is expected to shrink markedly as a result of the decline in oil prices, the stagnation of production, the slowdowns affecting the main trading partners, and the country’s dependence on imports of consumer goods.

In addition, the “21st century socialism” advocated by President Hugo Chávez has resulted in growing eco-nomic interventionism by the State, nationalizations, and increased barriers to private initiative in an unpredict-able business environment. The President’s victory in the February 2009 referendum reinforces his position in allowing him to stand again for the late 2012 presi-dential election. Before that date, the November 2010 parliamentary elections will be a new test for President Chávez, whose popularity could be undermined by a prolonged deterioration of the economic situation.

BrazilAfter remaining strong in 2008, (and exceeding the 5 per-cent rate targeted by Brazil’s Growth Acceleration Program), the economy will suffer a very sharp contraction in 2009, dragged down by the effects of the world economic and fi nancial crisis, despite government stimulus measures.

Weaker export performance attributable to the marked deterioration of the international environment, in conjunction with import vigor, is expected to exacer-bate the current account defi cit. Liquidity crisis risk will increase due to the very sharp growth of already large external fi nancing needs. Although foreign direct invest-ment should cover nearly half of those needs, Brazilian companies will experience greater diffi culty in obtaining fi nancing abroad in 2009 than in past years.

Overall, companies are being hampered by credit restrictions (particularly small- and medium-sized enter-prises) and/or the exchange rate trend in regular busi-ness transactions, or due to debt contracted in foreign currencies, and their payment behavior will likely suffer in consequence. Some sectors continue to face chronic diffi culties, such as garment and footwear industries, which are grappling with foreign competition. In other sectors, the more difficult economic conditions have taken their toll on agribusiness, the mining and steel industries, construction, automotives (car makers, parts manufacturers, dealers), and mass distribution (particu-larly in home appliances and information technology).

TaiwanAfter the strong 5.7 percent growth achieved in 2007, and even stronger 6.3 percent in the 2008 fi rst quarter, the Taiwanese economy slowed dramatically for the remainder of the year. This slowdown is mainly attrib-utable to the weakening of foreign demand, particularly from China, Hong Kong, and above all, the United States, the island’s main trading partner, considering that

Arabia wiof the

ded

Tfro

tionview of t

W W W . W O R L D T R A D E W T 1 0 0 . C O M 25

it is the ultimate re-export destination for about 70 per-cent of Taiwan’s exports to mainland China. Electronics exports, representing 76 percent of Taiwan’s GDP, and tourism have particularly suffered. Domestic demand has also sagged with several adverse trends undermining consumption: the upsurge of infl ation (with the island importing all its energy and food), the negative wealth effect associated with the fall of stock market prices, and the rise of unemployment. Meanwhile, tightening credit conditions and dimmer sales prospects have prompted companies to postpone investments. Despite adoption of more expansionary policies, both monetary (interest rate reductions) and fi scal, the slowdown will likely tighten its grip on the economy in 2009 amid weaker perfor-mance by industrialized and emerging Asian economies. Taiwan’s economic growth could thus be negative in 2009. In this context, corporate payment behavior has continued to deteriorate and the narrowing margins of Taiwanese companies will bear watching.

NetherlandsProduction and exports continued to deteriorate in the fi rst quarter of 2009 with full year growth expected to contract 4.7 percent. Given its open economy, the coun-try is very dependent on demand from its four traditional trading partners (Germany, Belgium, France and the UK). Exports and investment will continue to decline, down respectively16.2 percent and 14.7 percent. With wage growth remaining very moderate and unemploy-ment rising, the contraction of the disposable incomes of private individuals compounded by the erosion of their fi nancial and property asset values will prompt house-holds strained by very heavy debt (170 percent of dis-posable income) to cut back considerably on spending.

The plans for rescuing the banking sector and stimu-lating the economy in conjunction with a slowdown in revenues from gas will wipe out the fiscal surplus the country has run since 2005 and increase the debt, nonetheless expected to remain relatively low (nearly 60 percent of GDP). Bankruptcies accelerated these past months, surging 96.4 per cent in the fi rst quarter.

The global credit crunch will further undermine weaker companies in the manufacturing sector, par-ticularly electronics, information technology, and metal processing. Smaller companies that are reliant on the domestic market could be hurt by the slowdown in household consumption.

ItalyThe sluggishness that began to grip the Italian economy in 2007 has continued with growth likely to slacken for most of 2009 before giving way to a timid recovery.

Household consumption is expected to remain on even keel despite the large wage increases won in 2008 and the fall of prices for energy and, to a lesser extent, food. Nonetheless, households will be facing higher unemployment, refl ecting the stagnation of job creation and the growth of the working population. Although the government has provided underprivileged households with cards for making purchases at reduced prices and extended family allowances to wage earners with tem-

porary employment contracts, they should not expect signifi cant aid from a government that has made a com-mitment to Brussels to bring public sector fi nances back into balance by 2010.

Although the competitiveness of exports is expected to stop deteriorating thanks to the light weakening of the euro against the dollar and the moderate growth of the cost of labor in phase with productiv-ity gains, sales abroad will be unlikely to show any sign of recovery before end 2009. They will be faced with weak demand in developed countries, their primary market.

Investment will only grow in the public sector thanks to the accelerated use of European subsidies for infrastructure, research, and environmental protection. Companies meanwhile will make further reductions in spending amid sluggish demand, tightening credit, and a drop in profi tability.

Moreover, corporate payment behavior, already below the world average, has deteriorated further. The benefi t derived from the euro depreciation, if sustained, and the fall of prices for energy and raw materials, are being can-celled out by the drop in demand.

BelgiumThe economic downturn that began materializing during the fourth quarter of last year will continue in 2009 and growth will contract by 1.9 percent. The decline in demand from the main trading partners (with the Euro-pean Union representing over 73 percent of Belgium’s export market), under way since the third quarter of 2008, will continue to undermine the country’s exports, which have also become less competitive due to high payroll costs (and are above the euro zone average).

Industrial production will continue to fall, down about 4 percent, a trend that will only exacerbate the decline of the production capacity utilization rate, already down sharply in the fourth quarter of last year. Corporate investment will slow, also down about 4 percent, especially with the severe shocks that battered the banking sector in 2008, which prompted banks to tighten loan conditions.

On a positive note, Belgium is a highly multicultural and multilingual country that enjoys a unique geo-graphic location and the presence of European insti-tutions, which have been assets to attracting foreign companies and developing foreign trade. The country is also at the heart of a major economic region and serves as the crossroads of many channels, whether road, rail, or water transport. WT

Risk assessments were excerpted from the Coface Handbook of Coun-

try Risk 2009. Additional information is available online at www.

trade-safely.com.

pto the

the he

herated t t

For reprints of this article, please contact Cindy Williams at [email protected] or 610-436-4220 ext. 8516.

©2009. OHL, the OHL logo and “Count on us.” are the trademarks of Ozburn-Hessey Logistics, LLC.

In today’s economy, reliability can take you places.

Reliability is the key to success in the global marketplace. As one of the most established logistics companies in the world, OHL leads the way, with locations in dozens of countries. From transportation and warehousing to import and export services, duty drawback and freight management, our team of skilled professionals can deliver your goods as well as peace of mind. We have the flexibility to adapt to any distribution needs, with dynamic solutions and innovative value-added services. Today more than ever, you need the reliability of OHL.

www.ohl.com/countonus or 800-401-6400

Taking Supply ChainSecurity to the Next Level