will russia face labor force shortage in the next 20...

TRANSCRIPT

DRAFT, NOT FOR DISTRIBUTION

20

Growth and Labor Sufficiency in Russia:

Will Russia Face Labor Force Shortage in the Next 20 Years?

Background Note1

Draft, July 2011

The World Bank

1 This background note prepared by Toru Nishiuchi and Yulia Mironova (ECSPE Consultants) under the guidance of

Sudharshan Canagarajah (ECSPE Lead Economist). We are grateful to Sergey Ulatov, Karlis Smiths, Victor Sulla, Shoghik

Hovhannisyan and Matin Kholmatov for helpful comments and suggestions. Authors’ e-mail address:

DRAFT, NOT FOR DISTRIBUTION

2

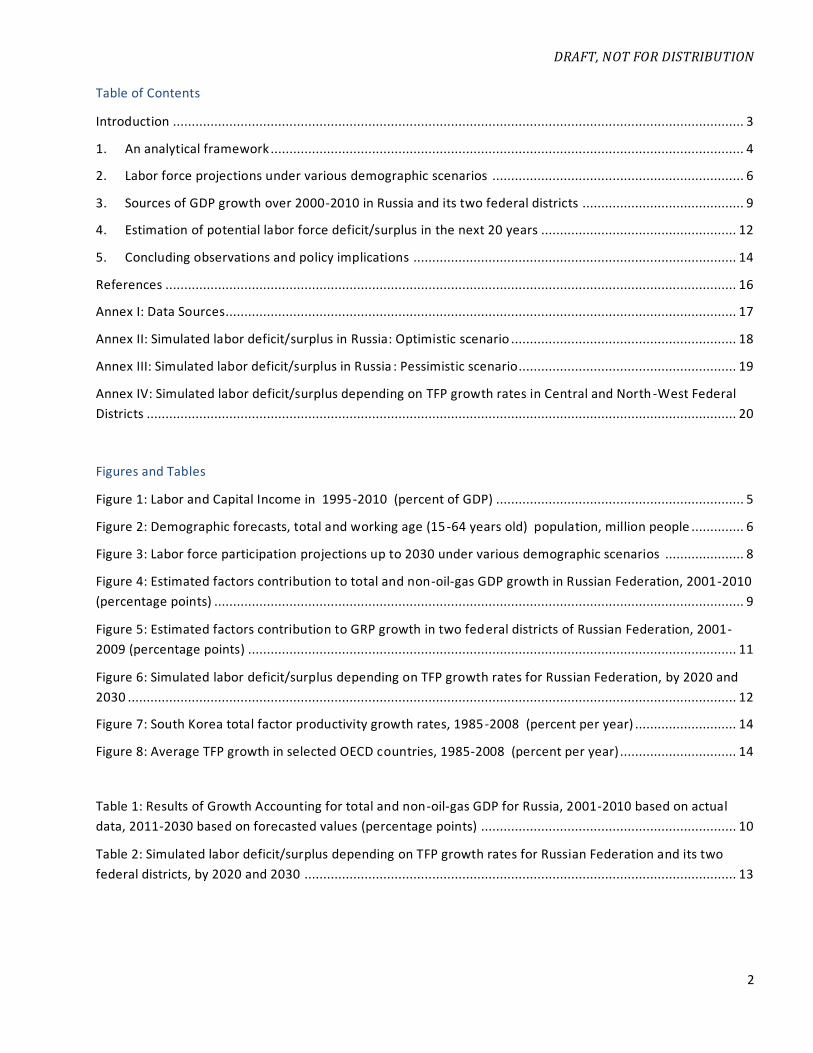

Table of Contents

Introduction ........................................................................................................................................................ 3

1. An analytical framework .............................................................................................................................. 4

2. Labor force projections under various demographic scenarios ................................................................... 6

3. Sources of GDP growth over 2000-2010 in Russia and its two federal districts ........................................... 9

4. Estimation of potential labor force deficit/surplus in the next 20 years .................................................... 12

5. Concluding observations and policy implications ...................................................................................... 14

References ........................................................................................................................................................ 16

Annex I: Data Sources........................................................................................................................................ 17

Annex II: Simulated labor deficit/surplus in Russia: Optimistic scenario ............................................................ 18

Annex III: Simulated labor deficit/surplus in Russia : Pessimistic scenario.......................................................... 19

Annex IV: Simulated labor deficit/surplus depending on TFP growth rates in Central and North -West Federal

Districts ............................................................................................................................................................. 20

Figures and Tables

Figure 1: Labor and Capital Income in 1995-2010 (percent of GDP) .................................................................. 5

Figure 2: Demographic forecasts, total and working age (15-64 years old) population, million people .............. 6

Figure 3: Labor force participation projections up to 2030 under various demographic scenarios ..................... 8

Figure 4: Estimated factors contribution to total and non-oil-gas GDP growth in Russian Federation, 2001-2010

(percentage points) ............................................................................................................................................. 9

Figure 5: Estimated factors contribution to GRP growth in two federal districts of Russian Federation, 2001-

2009 (percentage points) .................................................................................................................................. 11

Figure 6: Simulated labor deficit/surplus depending on TFP growth rates for Russian Federation, by 2020 and

2030 .................................................................................................................................................................. 12

Figure 7: South Korea total factor productivity growth rates, 1985-2008 (percent per year) ........................... 14

Figure 8: Average TFP growth in selected OECD countries, 1985-2008 (percent per year) ............................... 14

Table 1: Results of Growth Accounting for total and non-oil-gas GDP for Russia, 2001-2010 based on actual

data, 2011-2030 based on forecasted values (percentage points) .................................................................... 10

Table 2: Simulated labor deficit/surplus depending on TFP growth rates for Russian Federation and its two

federal districts, by 2020 and 2030 ................................................................................................................... 13

DRAFT, NOT FOR DISTRIBUTION

3

Introduction

ussian economy demonstrated strong economic performance over the decade prior to the global

economic crisis in 2008 and 2009. Economic growth averaged 6.9 percent per year and GDP per capita

increased almost nine times in nominal US dollars terms over the period from 1999 to 2008. This growth

episode began as a bounce-back after the 1998 financial collapse. With a weakened ruble, domestic

manufacturers were better positioned to compete with imports. Then, as oil prices climbed, the country

saw a large inflow of foreign exchange, further fueling growth and centering the Russian economic growth

model on high prices of hydrocarbons, which generated about 20 percent of total GDP, half of the budget

revenues and accounted for about 60 percent of Russian merchandise exports.

Strong economic growth in Russia created vast economic opportunities for neighboring countries which

benefited from exports expansion at the Russian market, incomes generated by labor migrants attracted

to Russia by substantial wage differentials, and Russian investments. Total Russian imports from CIS

countries more than tripled between 2001 and 2008. Exports of labor to Russia from the poorest CIS

countries – Tajikistan, Kyrgyzstan and Moldova - appeared to be even more critical for their welfare than

the trade-in-goods linkage. Remittances from labor migrants working in Russia constituted a very

significant source of incomes for population in those countries, accounting for 30 -50 percent of their GDP

in 2008. Estimated total number of foreign labor migrants working in Russia was about 2.5 million people,

or 3.4 percent of total employment; at that labor migrants accounted for over 10 percent of total

employment in Moscow city2, major center of economic activities in Russia, where jobs for migrants were

mainly created in non-tradable sectors, including construction, retail trade, and selected types of services.

Following a decade of strong economic growth, the country was hit hard by the crisis. Even though the

authorities saved significant portion of the oil revenues in the Russian Stabilization Fund, they gradually

began to spend more and more of it in the years preceding the crisis. At the same time, private sector

activity was also very dynamic. So when the crisis hit and oil prices collapsed, the economy was

overheated, and therefore output declined by more than in other countries (IMF, 2010). The government

implemented massive fiscal stimulus of about 10 percent of GDP to protect the economy. Despite large

stimulus and favorable commodity prices, growth has been modest - 4.0 percent in 2010 and 4.1 percent

in Q1-2011. Ministry of Economic Development of Russian Federation forecast average real GDP growth of

4.1 percent per year over 2011-2014, which is broadly in line with the WB, IMF and EIU outlook for Russia.

The crisis demonstrated again external vulnerability of the Russian economy. Economic team of the

Russian Government recognized that new drivers of growth are needed for Russia to sustain steady

economic growth in future. Economic modernization to boost productivity and export diversification is

among the top priorities on the Russian economic policy agenda.

However, this task is complicated by demographic situation in Russia, which po pulation has been declining

over the last decade and which implies declining working age population in the next decade or two. This

means that in order to achieve targeted economic growth rates the country may need to attain even

higher productivity gains.

2 http://mirpal.org/Статистика/Сводные%20таблицы%20за%202005-2008%20гг..html

R

DRAFT, NOT FOR DISTRIBUTION

4

This note therefore attempts to quantify relationship between economic growth and growth of labor

force, using growth accounting relationship, in order to clarify the gap between projected number of labor

force of Russian nationals under various demographic scenarios and required number of labor force to

achieve targeted level of GDP under various assumptions on total factor productivity (TFP) growth,

population’s participation rates in labor force and capital accumulation level.

The note is organized as follows. Section 1 presents an analytical framework. Section 2 provide s

projections of labor force under several demographic scenarios. Section 3 analyses sources of growth in

Russia and in two Russian Federal Districts during 2000-2010, differentiating between total GDP growth

and non-oil-gas GDP growth. This analysis underlines assumptions in scenarios used in simulations to

estimate labor force deficit/surplus in Russia in the next twenty years presented in Section 4. Policy

implications and concluding remarks follow.

1. An analytical framework

e use a standard growth accounting framework to analyse sources of growth in Russia,

differentiating between growth generated by labor and capital inputs contribution and

contribution from the increases in total factor productivity (TFP). We consider a model of an open

economy that evolves in discrete time and each time period, denoted by an index, represents one year

(World Bank, 2011). We assume that the economy has access to a technology to produce output by

combining capital and labor inputs according to the Cobb-Douglas production function with constant

returns to scale defined by equation (1):

(1)

where denotes output, is the stock of physical capital, denotes the amount of labor input, is a

measure of the productivity level of capital and labor, and the technology parameter which

measures the relative contribution of capital to the production of output and which in a competitive

economy coincides with the share of output distributed as payments to capital. Capital depreciates at a

constant rate of between time periods and can be augmented through investment evolving according to

the equation (2):

(2)

where denotes aggregate investment. We assume that capital depreciation rate is 0.05, which is

commonly used in the literature. Imposing various assumptions on targeted GDP growth, TFP growth, and

investment-to-GDP ratio we simulate required labor force growth rate under various scenarios using the

equation (3):

(3)

W

DRAFT, NOT FOR DISTRIBUTION

5

Finally, we estimate potential labor force deficit/surplus as a difference between projected labor force

under various demographic scenarios and required labor force estimated using growth rates obtained by

equation (3).

We understand various limitations of this framework as well as of the data. Growth accounting

methodology has been criticized, among others, for “residual” nature of the TFP growth, for the

underlying assumptions about production function and for that it cannot identify whether the productivity

growth caused the capital accumulation, or whether the capital accumulation made additional innovations

possible. The other concerns refer to measures of changes in output and the inputs and to choice of

parameters, including possible underutilization of available capital stock or employed labor, and sensitivity

of the results to the choice of the technology parameter α which as empirical evidence demonstrate varies

substantially across the countries (Gollin, 2002). However, there are studies (Bosworth and Collins, 2003

and Caselli, 2004), which we rely on, arguing that growth accounting is a valuable tool that can - and have

- improved understanding of growth experiences across countries.

We address some of the limitations. First we use data on capital stock adjusted for capital utilization (see

World Bank, 2007a and IMF, 2006). Second, we use observable estimate for parameter measured as

share of profits and mixed incomes in total value added (see Figure 1 a). Third, though this simple growth

accounting framework as it currently stands does not include other growth determinants – such as the

savings rate - we incorporate sensitivity analysis of labor requirement various combinations of investment

rate which is highly correlated with savings rate (see Figure 1b).

Finally, with all limitation, we believe that this framework is still useful to demonstrate how labor force

needs in Russian Federation may change in future depending on targeted economic growth rates,

improvements in factors productivity, level of participation of working age population in labor force and

investment levels; so the Government could address potential labor force shortage beforehand.

The analysis presented in this note is conducted in three steps. First, we project labor force in the next

twenty years for the three demographic scenarios provided by the National Statistics Committee of

Russian Federation (NSC RF) and imposing several alternative assumptions on expected labor participation

Figure 1a: Labor and Capital Income in 1995-2010 (percent of GDP)

Figure 2b: National savings and investment rate, average 1980-2008

Source: NSC RF Source: Savings and Growth in Egypt, World Bank (2011)

DRAFT, NOT FOR DISTRIBUTION

6

rate (LPR). Second, we use presented above framework to estimate TFP contribution to GDP growth in

Russia over the last decade, differentiating between oil-gas and non-oil-gas GDP. We also analyse sources

of growth using this framework for two Russia’s regions . Third, we estimate the gap between projected

number of labor force of Russian nationals and required number of labor force to achieve targeted level of

GDP under various assumptions on TFP growth, LPR and investment-to-GDP ratio.

2. Labor force projections under various demographic scenarios

ussian Federation has been undergoing though the period of sharp demographic decline over the last

decade. Despite strong and robust economic growth, Russia over these years has been facing

exceptional population decline fueled by low fertility and high mortality in large part due to untimely

deaths from heart disease and traffic accidents. Between 1992 and 2009 Russia’s population declined by

approximately 7 million from 149 in 1992 to an estimated 142 million people, which is corresponding to

Russia’s population in 1984. Migration has become the only source of population growth. According to

UNFPA (2010) total natural population decline for these years amounted to 12.6 million, which implies

that migration compensated for approximately half of it.

Recent years recorded however assuring population increase up to estimated 142.9 million in 2010. The

natural decline of Russia's population in 2009 went down by almost a third; birth r ate grew by 2.9 and

death rate reduced by 3 percentage points. Improved health outcomes also contributed, so that child

mortality in Russia decreased by 3.5 percent, cardiovascular diseases' toll went down by 4.6 percent, and

the TB death rate declined 7.8 percent in 2010.

Unfortunately reduction of population decline rate in recent years is likely to be only a temporary trend

for a number of reasons. First, a significant increase in the number of women of childbearing age as a

result improved fertility in the 80s, contributed to an increase in the number of births. Second, starting

from 2001 the 60-year mark was passes by a smaller generation born during the war, which inhibited the

growth of the number of deaths. The influence of both factors will weaken in the next few years, i.e. the

number of potential mothers will return to the level of the early 90s, and the number of elderly will start

growing at expense of the most

numerous post-war generations.

As a result favorable impact of

these structural factors on the

population growth in the first

decade of XXI century, in its

second decade will reverse (see

UNFPA, 2010 for details). Almost

all the forecasts predict a further

reduction Russia's population,

although at different rate of

reduction. This will lead to a

decline of working age

population. Figure 2 illustrates

potential decline of working age

R

Figure 3: Demographic forecasts, total and working age (15-64 years old) population, million people

Source: NSC RF

DRAFT, NOT FOR DISTRIBUTION

7

population for three demographic scenarios based on the forecast prepared by N SC RF. This shows that

number if working age population may decline from about 103 million people as of 2010 up to 86.4 million

in 2030. The direct economic consequence of this decline is a reduction of productive labor force which

may potentially have negative implication for economic growth.

In this section we present estimated labor force participation (measured as number of employed) in the

next twenty years for the three demographic scenarios and imposing several alternative assumptions on

expected labor participation rates as in the situation of declining population increasing labor participation

rates could partially solve the problem of shrinking labor force. We use population projections by age

group and sex provided by NSC RF. In projecting the number of labor force, we rely on three demographic

scenarios - baseline, optimistic and pessimistic (see Figure 2) and impose following assumptions on labor

force participation rates:

(a) Base case: participation rates by age and gender will remain at average level observed over

2006-2008; we exclude 2009 as there was increase in unemployment in 2009 due to the crisis

(b) EU25 convergence: participation rates for all age-gender groups will move toward those of the

current average of the 25 members of the European Union, converging by 2030; currently EU25

LPRs are substantially higher than in Russia for younger and older people (15-24 years old and

over 60 years old)

(c) 2.5 percent across the board: gradual increase in labor force participation rates for all age-

gender groups, reaching a level 2.5 percentage points higher than they were in 2006-2008

(d) Older workers: gradually increasing participation rates for workers, age 60 to 64, so that the

rates are 5 percentage points higher in 2030 than in 2006-2008

(e) 40 to 59 year olds: gradually increased participation rates for both men and women in this age

group, so that the rates are 5 percentage points higher in 2030 than in 2006-2008

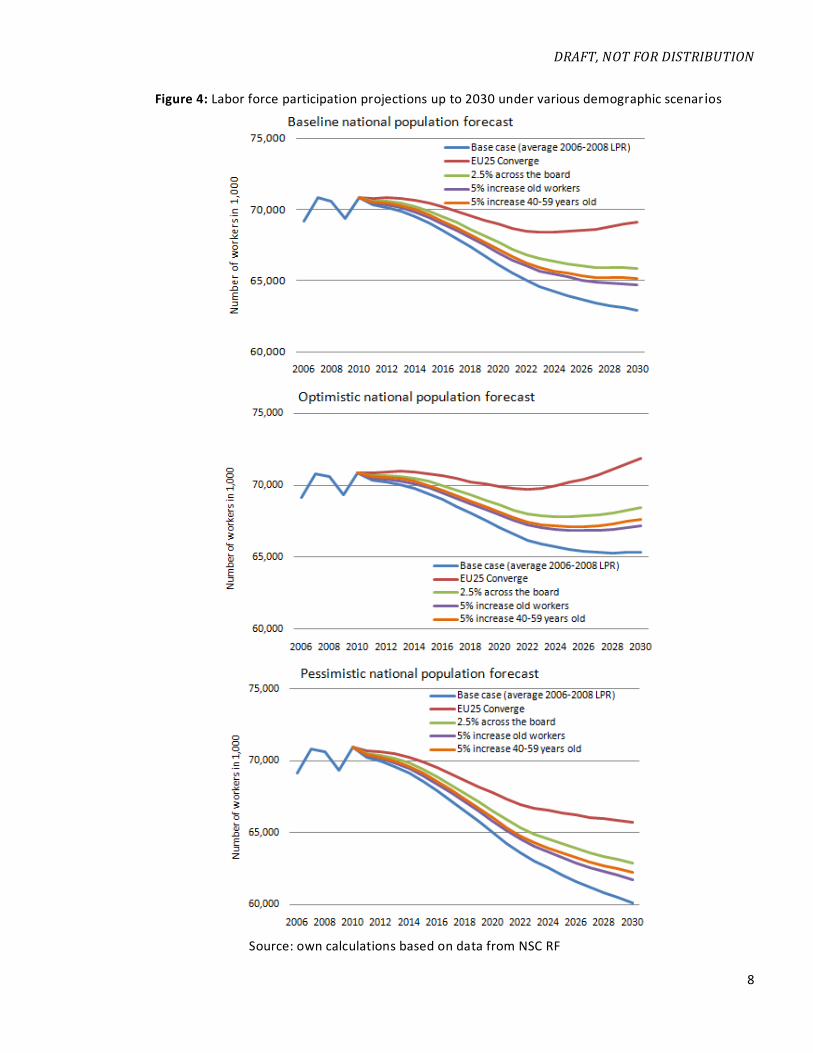

Labor force participation projections for the three scenarios are presented in Figure 3. In 2006-2008 total

employment averaged at 70.2 million people. Our estimate for labor force participation by the year 2030

varies from 62.9 to 69.1 million for the baseline demographic scenario, from 65.3 to 71.8 million for the

optimistic demographic scenario, and from 60.1 to 65.7 million under pessimistic scenario. This means

that if pessimistic demographic scenario realizes and labor participation rates will remain unchanged at

the level of 2006-2008, labor force participation may decline by as much as 10 million people or by 14.3

percent from the current level. This will be a fairly substantial burden on economic growth as it will be

more difficult to sustain high growth rates.

Figure 3 shows that beyond promoting across the board increase in labor participation rates decline in

labor force is mitigated by policies encouraging higher participation of younger people (15-24 years old) in

the labor force and promoting middle-age workers (40-59 years old and older) to stay longer in labor

market. The later could be practically implemented through postponing retirement age, but given the low

levels of life expectancy in Russia, this seems to be politically difficult to implement.

In addition to declining labor force in Russia, its quality is deteriorating in terms of education. 2011 Global

Competitiveness Report for Russia (WEF, 2011) argues that although the country’s highly educated

population is now among its key advantages; Russia will most likely not be able to maintain this advantage

DRAFT, NOT FOR DISTRIBUTION

8

Figure 4: Labor force participation projections up to 2030 under various demographic scenar ios

Source: own calculations based on data from NSC RF

DRAFT, NOT FOR DISTRIBUTION

9

over the medium to longer term without major investment into improving the quality of educational

system. The past five years have seen a significant deterioration in the quality of education in Russia, even

in math and science - which had been one of the key strengths of the Russian education while educational

outcomes in India, China, and Brazil have been improving and OECD countries show stable results. Though

in our further analysis we do not account for the deteriorating quality of labor force, as measured by its

education, we believe that this argument makes our findings stronger.

3. Sources of GDP growth over 2000-2010 in Russia and its two federal districts

nalysis of sources of growth obviously is not the main focus of the exercise presented in this note as it

can add little value to the existing rich literature studying the drivers of growth in Russia. We

decompose sources of growth in Russia here primarily to see what happened in very recent years and

whether they (sources) were different for non-oil-gas and overall economy. The later is important as

contribution of oil and gas sectors in overall growth is expected to be zero or negative in the next decade,

which is already captured in the medium-term economic forecast for Russian Federation for 2011-20143.

This implies that economic growth will have to be generated in non-oil-gas sectors, and those potentially

could require higher labor inputs.

Overall GDP growth in Russia during the period from 2001 to 2008 was mainly driven by increased

productivity, whereas the accumulation of labor and capital played a minor role. World Bank flagship

report on productivity in Europe and Central Asia (ECA) explains that large part of the productivity gains in

Russia were derived from increased capacity utilization, particularly in manufacturing. As firms began

using their excess labor and capital, which had become idle during the deep transitional recession, output

increased, and this is captured in TFP estimates (see Figure 2).

During the first half of the past decade TFP contribution to growth in non-oil-gas sectors was slightly lower

than for total economy. This implies that productivity gains were higher in oil and gas sectors. Few years

3 http://www.economy.gov.ru/minec/activity/sections/macro/prognoz/doc20110422_010

A

Figure 5: Estimated factors contribution to total and non-oil-gas GDP growth in Russian Federation, 2001-2010 (percentage points)

Source: own calculations based on data from NSC RF, WB WDI database, and dataset from World Bank (2008)

DRAFT, NOT FOR DISTRIBUTION

10

before the crisis, during 2006-2008, TFP contribution in non-oil-gas sectors was higher than for total

economy. Recent Global Competitiveness Report for Russia (WEF 2011) also shows that recently

productivity in supporting sectors (which are mostly market services, including construction, retail trade,

hospitality and etc.) grew faster than in many basic sectors (mining and manufacturing, where the

government is the main proponent and owner). However, dynamic development of supporting sectors

was fueled by oil incomes, which cannot drive the future growth.

Results of the growth accounting illustrate that even moderate rates of economic growth in the next two

decades will require sustaining high TFP growth rates between 2.5 and 4.1 percent per year, particularly in

non-oil-gas sectors. Table 1 shows estimated average contribution of TFP to growth (total and non-oil-gas)

over 2001-2010 and required TFP gains in order to generate targeted economic growth in the next two

decades under the following assumptions:

(a) Economy will grow at average rate of 4.5 percent per year. This rate corresponds to recently

announced medium term targets of the Russian government and also equal to the weighted average

annual growth rate of the top four developing recourse-rich countries (Brazil, Chile, China and South

Africa) during 2000-2009;

(b) Oil and gas sector contribution to overall growth will be on average negative 0.5 percent per year for

2011-2020 and zero percent for 2021-2030;

(c) Capital stock will grow at the rate generated by investment-to-GDP ratio equal to 2005-2010 average

of 24.1 percent of GDP;

(d) Labor force growth rate as defined by three scenarios selected from those presented and discussed in

the section 2.

In the most optimistic case from the three labor force scenarios considered (Table 1) achievement of the

targeted economic growth rate of 4.5 percent per year in the next two decided will require TFP growth of

about 3 percent per year on average, with slightly higher requirement in the non-oil-gas sectors.

Table 1: Results of Growth Accounting for total and non-oil-gas GDP for Russia, 2001-2010 based on actual

data, 2011-2030 based on forecasted values (percentage points)

Actual

Scenario 1: Base case

LPR est. for baseline

population forecast

Scenario 2: 2.5 %

increase LPR est. for

optimistic population

forecast

Scenario 3: Base case

LPR est. for pessimistic

population forecast

2001-2005

2006-2010 2011-2020 2021-2030 2011-2020 2021-2030 2011-2021 2021-2030

Total GDP

Output 6.4 2.3 4.5 4.5 4.5 4.5 4.5 4.5

Capital 0.7 1.5 1.6 2.0 1.6 2.0 1.6 2.0

Labor 0.8 0.4 -0.4 -0.3 -0.2 0.0 -0.5 -1.0

TFP 5.0 0.4 3.3 2.8 3.1 2.5 3.4 3.5

Non-oil-gas GDP

Output 5.2 2.1 5.0 4.5 5.0 4.5 5.0 4.5

Capital 0.4 1.2 1.4 1.9 1.4 1.9 1.4 1.9

Labor 0.8 0.3 -0.4 -0.3 -0.2 0.0 -0.5 -0.4

TFP 4.1 0.6 4.0 2.8 3.8 2.5 4.1 3.0

Source: own calculations based on data from NSC RF, WB WDI database, and dataset from World Bank (2008)

DRAFT, NOT FOR DISTRIBUTION

11

We also repeat growth accounting exercise to see if sources of growth differ between the regions

currently facing labor shortage and regions with adequate labor supply. We use lower share of foreign

labor migrants in overall employment as a proxy for labor sufficiency . We chose Central Federal District (as

the largest recipient of labor migrants, which could indicate existing shortage of domestic labor) and

North-West Federal District (as region with lower share of labor migrant in total employment). Both

regions account for the bulk of economic activity in the co untry and both feature post-industrial economic

structure. We use data on Gross Regional Product (GRP) growth and employment available in the official

statistics and capital stock is estimated applying actual shares of respective regions in total capital stock at

remaining balance sheet value also available in the official statistics.

Results of the growth accounting at regional level are presented at Figure 5:

Pattern of TFP contribution to GRP growth in North-Western federal district is broadly the same as at

the country level, i.e. GRP growth between 2000 and 2008 was mainly driven by increased

productivity, whereas the accumulation of labor and capital played a secondary role.

Sources of growth in the Central Federal District reveal somewhat different picture. GRP growth,

particularly in 2007 and 2008, was driven by capital accumulation and productivity gains during these

years were marginal. Given that this region accommodates large number of foreign migrants, this may

indicate that low skilled labor (as majority of labor migrants are low-skilled employed in supporting

sectors) impedes productivity growth. From the other point of view it may signal that low productivity

is compensated by cheap low-skilled labor. But it is also likely that the capital stock in this region is

overestimated due to large share of non-productive investments (housing and commercial real

estate). Therefore, it is not appropriate to conclude that this region has different patterns of

Figure 6: Estimated factors contribution to GRP growth in two federal districts of Russian Federation, 2001-

2009 (percentage points)

2001-2005 2006-2009

Output 8.4 1.5

Capital 2.0 4.3

Labor 0.6 0.1

TFP 5.8 -2.9

2001-2005 2006-2009

Output 7.7 2.7

Capital 0.9 0.5

Labor 0.8 0.0

TFP 6.1 2.3

Source: own calculations based on data from NSC RF, WB WDI database, and dataset from World Ban k (2008)

DRAFT, NOT FOR DISTRIBUTION

12

productivity growth, but given its significance for economy, it may well deserve more in -depth analysis

of growth drivers.

4. Estimation of potential labor force deficit/surplus in the next 20 years

n this section we present results of the estimation of the gap between projected number of labor force

of Russian nationals (as described in Section 2) and simulated required number of labor force to achieve

targeted level of GDP under various assumptions on TFP growth, LPR and investment-to-GDP ratio for the

optimistic and pessimistic scenarios defined as follows:

Optimistic scenario:

- 6 percent average annual GDP growth, - 2.5 percent increase in labor participation rate based

on optimistic population forecast, - average investment ratio 25 percent of GDP

- TFP annual growth varies from 0.5 to 5.0 percent

Pessimistic scenario:

- 3.0 percent average annual GDP growth, - baseline labor participation rate,

- average investment ratio 15 percent of GDP - TFP average annual growth varies from 0.5 to

5.0 percent

We conduct growth accounting exercise at national level for non-oil-gas GDP by adjusting GDP growth

rates, labor force and investments on estimated contribution of oil and gas sectors, assuming that:

Oil and gas sector contribution to overall growth will be on average negative 0.5 percent per year for

2011-2020 and zero percent for 2021-2030,

Share of employed in these sectors will remain at average level of 2005-2009 (1.8 percent of total) ,

Share of oil-gas investments will remain at average level of 2005-2009 (20 percent of total) during

2011-2020 and will slightly decline during 2021-2030 (up to 15 percent of total).

I

Figure 7: Simulated labor deficit/surplus depending on TFP growth rates for Russian Federation, by 2020 and 2030

Source: own calculations based on data from NSC RF, WB WDI database, and dataset from World Bank (2008)

Labor, required

annual growth

rate

TFP, annual growth rate

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

-180,000

-150,000

-120,000

-90,000

-60,000

-30,000

0

30,000

60,000

90,000

%

tho

usand

peo

ple

Russia: Optimistic Scenario

Labor force def icit "-"/surplus "+" by 2020Labor force def icit "-"/surplus "+" by 2030

Labor, required annual growth

rate

TFP, annual growth rate

-15

-12

-9

-6

-3

0

3

6

-100,000

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

%

tho

usand

peo

ple

Russia: Pessimistic Scenario

Labor force def icit "-"/surplus "+" by 2020

Labor force def icit "-"/surplus "+" by 2030

DRAFT, NOT FOR DISTRIBUTION

13

We do not do oil-gas adjustment at regional level as none of these two regions is major oil or gas

producer. By solving the growth accounting equation for growth rate in labor force (see equation (3) in

section 1), we obtain required growth rate in labor force using hypothetical range for TFP growth rate

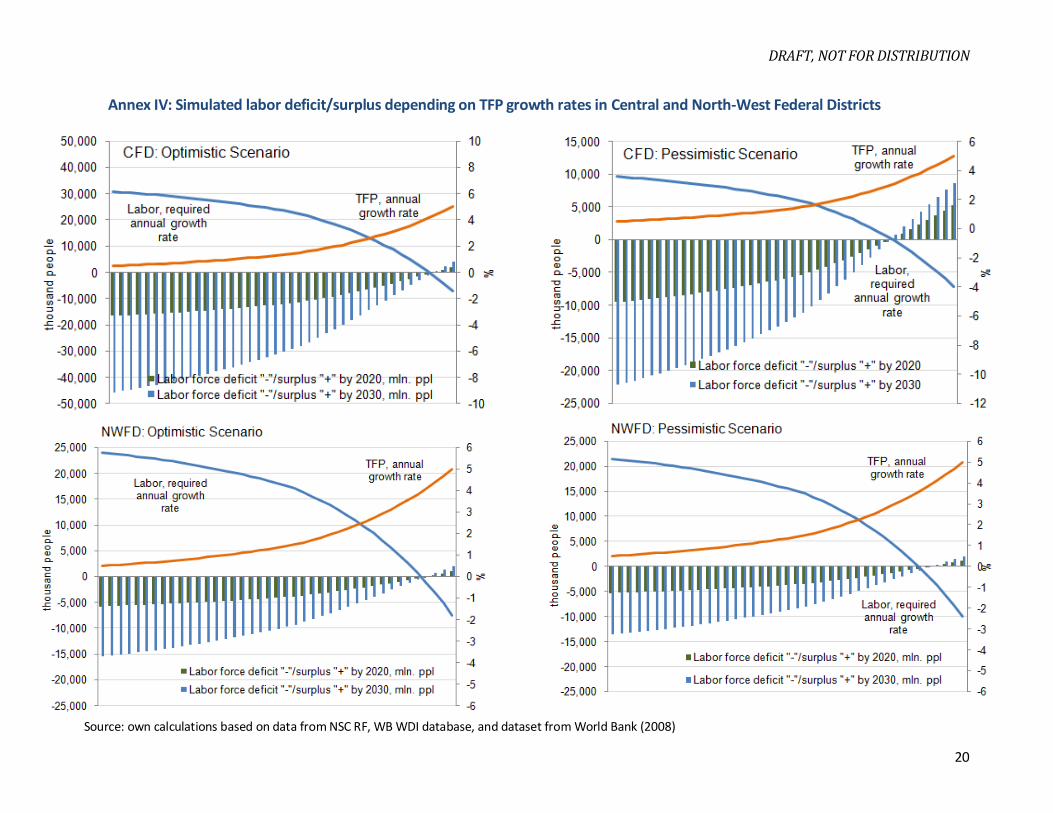

from 0.5 to 5.0 percent. The results of the simulations at national level are presented in Figure 6. Table 2

summarizes results of the simulations at national and regional level; detailed simulations results at

national level are presented in Annex II and Annex III, simulations results regional level are included in

Annex IV.

Table 2: Simulated labor deficit/surplus depending on TFP growth rates for Russian Federation and its two

federal districts, by 2020 and 2030

Central

Federal District

North-West

Federal District

Russian

Federation

Population, 2009, mln. ppl 37.1 13.4 141.9

Employment, 2009, mln. ppl 19.1 7.2 68.1

Share of labor migrants in total employment, 2008, % 5.4 2.8 3.4

Optimistic case

Est. hypothetical labor force deficit "-"/surplus "+" under

conservative long-term TFP growth of 0.5 percent per year

by 2020, mln. ppl -16.6 -5.8 -63.3

by 2030, mln. ppl -45.7 -15.5 -178.1

TFP growth at which domestic labor supply will be about sufficient, % 4.4 4.1 4.5

Pessimistic case

Est. hypothetical labor force deficit "-"/surplus "+" under

conservative long-term TFP growth of 0.5 percent per year

by 2020, mln. ppl -9.6 -5.3 -36.5

by 2030, mln. ppl -22.2 -13.6 -86.2

TFP growth at which domestic labor supply will be sufficient, % 3.0 4.0 3.2

Source: own calculations based on data from NSC RF, WB WDI database, and dataset from World Bank (2008)

The main findings of the analysis are the following:

Domestic supply of labor in Russian Federation could be sufficient to ensure long-term non-oil-gas

growth rate of above 3.0 percent with moderate level of investments in non-oil-gas sectors (of 15% of

GDP) if the country is able to sustain strong productivity growth rates of above 3.2 percent per year in

a long-term.

Above 6.0 percent long-term non-oil-gas growth rate combined with investment rate of 25% of GDP

in non-oil-gas sectors will require stronger TFP growth of about 4.5 percent per year in long term,

which could be feasible for the country like Russia – example of Korea over the period of 1985-2008,

when annual TFP growth averaged at about 4 percent (Figure 7), demonstrates that this is feasible.

Yet, one should note that Korea’s experience is exceptional. Average TFP growth rate in the last two

decades in the most of OECD countries have been modest (See Figure 8). The large difference in

productivity levels between Russia and the advanced economies may phase out as rapid productivity

gains acquired through the catch-up effect, which took place in Russia, does not last long. As labor and

capital efficiency increases, room for capacity utilization and labor adjustment decreases, resulting in

decline in TFP growth. Historically, no country has sustained high level of TFP growth in the long run

(see Englander and Mittelstadt, 1988).

DRAFT, NOT FOR DISTRIBUTION

14

The lower TFP growth rates or higher economic growth targets in a long-term could require larger

capital investments or higher growth rates of labor force. The later will likely lead to a shortage of

labor (see Table 2 and Annexes II-IV for details), which can be addressed through various policy

interventions, including among others measures aimed at increasing LPRs, improving health/education

outcomes, or attracting labor migrants from abroad.

The exercise yields results which are consistent at country and regional levels.

5. Concluding observations and policy implications

he findings of the simple growth accounting exercise presented in this note demonstrate that given

difficult current demographic situation in Russia, the country may face labor shortage in the next 20

years. We found that if pessimistic population forecast realizes labor force participation by the year 2030

may decline by as much as 10 million people or by 14.3 percent from the current le vel. This will be a fairly

substantial burden on economic growth as it will be more difficult to sustain high economic growth rates.

Russian government fully recognizes importance of demographic problems and implements combination

of policies aimed at improving demographic situation, including complex measures to improve health

(longer life expectancy, higher birth rates, lower level of diseases, etc.) and education outcomes under the

national programs “Health” and “Education” and to provide better living conditions under the national

program “Affordable and Comfortable Housing”. However these measures will not likely yield quick

results, i.e. improve demographic satiation, in the next 10-20 years.

Russian policy makers have various instruments available to address the decline in the population of

working age in sort- and medium-term. Increasing labor participation rates, postponing retirement ages,

stimulating the labor market participation of women and migration policies are among those instruments.

Increased immigration has the advantage of having an immediate effect on the age and composition of

the population because of the younger age structure of net migration. In addition, fertility rates of

immigrant women are often relatively high, which can boost fertility and hence long-term population

growth. The role of migration policies, however, in addressing demographic challenges can only be

complementary to other policies and is subject to a number of practical and political constraints.

Figure 8: South Korea total factor productivity growth rates, 1985-2008 (percent per year)

Figure 9: Average TFP growth in selected OECD countries, 1985-2008 (percent per year)

Source: OECD

T

DRAFT, NOT FOR DISTRIBUTION

15

Russia has been already receiving large inflows of labor migrants which partially offset decline in total

population (see paragraph 1 in section 2). But these massive migrant inflows featured mostly un-skilled

labor which was attracted by large wage differentials fueled by country’s oil wealth. With envisaged

decline of oil and gas sectors output, the needs in this type of labor will subside. Now the Government

may consider setting up new requirements for recruitment of foreign labor (e.g. education, skills, age

groups, etc.) to be able to attract labor of higher quality to specific sectors or regions. This will not only

help to close the labor market gap, but contribute to overall labor productivity and country

competitiveness improvement. This will, however, require substantial preparatory work, including labor

needs assessment at sectoral and regional level.

We show that domestic supply of labor in Russian Federation under current demographic trends and

maintaining current level of investments could be sufficient to ensure sustainable long-term non-oil-gas

growth rate of above 3.0 percent only if the country is able to sustain strong productivity growth rates of

about 3-4 percent per year in a long-term.

These are high rates, but feasible. First, there are examples demonstrating that this is possible - South

Korea sustained 3.9 percent average total factor productivity growth rates over the period from 1985 to

2008. Second, strong productivity gains in Russia over the last decade were derived at large extent from

increased capacity utilization. Macroeconomic stability, better governance and business environment,

financial deepening, and investments in infrastructure, particularly in information and communication

technology (ICT), were other drivers of productivity growth (see WEF, 2011). However, it is commonly

agreed that Russian economy still has substantial potential to improve its productivity. The Russian

government is inclined to realize this potential using traditional industrial policy instruments. A number of

analytical/policy studies, however, warn that productivity growth may require more fundamental

structural reforms.

For example, WB RER (2011) discusses factors with the strongest positive impact on productivity of

Russian firms, which include investment climate, competition policy, innovations and skills level of labor.

WEF GCR (2011) suggests that Russia can realize its potential and improve competitiveness by building on

the three key advantages - large domestic and foreign market size, its stock of well-educated population,

and its undisputable wealth in natural resources - and by addressing the five key challenges - rule of law

and the institutional framework, eroding quality of education, week competition environment, financial

market supervision, outdated business/management processes. Finally, Gaddy and Ickes (2010) argue that

Russia’s growth strategy cannot succeed only through eradicating the “typical set” of efficiency problems,

i.e. weak property rights, corruption, etc. They argue that the country needs to eliminate systematic

misuse of assets rooted in the inherited production structure and “oil rent addiction”. The former refers to

the particular kinds of physical and human capital that were accumulated in the Soviet era and the

manner in which they were allocated, including their spatial allocation. The later implies that there is an

imperative to distribute a large share of Russia’s oil and gas rents to the production enterprises that

employ this inherited physical and human capital.

DRAFT, NOT FOR DISTRIBUTION

16

References

Bosworth and Collins (2003), The Empirics of Growth: An Update, Brookings Institution, Washington DC

Caselli (2004), Accounting for Cross-Country Income Differences, Handbook of Economic Growth, Harvard

Englander and Mittelstadt (1988), Total Factor Productivity: Macroeconomic and Structural Aspects of the

Slowdown, OECD Economic Studies

Fischer, Sahay and Vegh (1998), How far is Eastern Europe from Brussels? IMF working paper

Gaddy and Ickes (2010) Bear Traps: Can Russia Avoid the Pitfalls on the Road to Sustainable Economic

Growth? Center for Research on International Financial and Energy Security, Pennsylvania State University

Gollin (2002), Getting income shares right. Journal of Political Economy 110, 458–74

Gurvich et al. (2008), Cyclical Fiscal Policy in Resource Rich Countries, High School of Economics, Moscow

IMF (2010) Economic Health Check, Russia: Fragile Recovery from Crisis

IMF (2006), The Utilization-Adjusted Output Gap: Is the Russian Economy Overheating?

IMF (2004), Domestic and global perspectives of migration to the United States, country report to the

United States

Doudeijns and Dumont (2003), Immigration and Labor shortages: Evaluation of needs and limits of

selection policies in recruitment of foreign labor, OECD Working Paper

World Bank (2007a), Unleashing Prosperity: Productivity Growth in Eastern Europe and Former Soviet

Union

World Bank (2007b), From Red to Gray - The "Third Transition" of Aging Populations in Eastern Europe and

the Former Soviet Union

World Bank (2005), Russian Federation Country Economic Memorandum

World Bank (2005), Dying Too Young: Addressing Premature Mortality and Ill Health Due to Non -

Communicable Diseases and Injuries in the Russian Federation

World Economic Forum (WEF) (2011), The Russia Competitiveness Report 2011: Laying the Foundation for

Sustainable Prosperity

UNFPA (2010), Social and Demographic Development in Russia: 15 Years beyond Cairo Program

DRAFT, NOT FOR DISTRIBUTION

20

Annex I: Data Sources

1. Population by age and territory Official, NSC RF

2. Population projections 2010-2030 Official as of 2010, NSC RF

3. Labor participation rates Based on official employment statistics by age group, NSC RF

4. Non-oil GDP Estimated based on World Bank CEM (2005) and Gurvich et. al (2007) “Cyclical Fiscal

Policy in Resource Rich Countries"

5. Output GDP, PPP (constant 2000 US$), WB WDI

6. Investments Gross Fixed Capital Formation, PPP (constant 2000 US$), WB WDI

7. Capital, national Level

Capital Stock adjusted for capital utilization, PPP (constant 2000 US$), “Unleashing

Prosperity: Productivity Growth in Eastern Europe and Former Soviet Union, World

Bank; after 2005 calculated using perpetual inventory method

8. Capital, regional level Calculated using actual shares obtained from official data on accounting (remaining)

value of capital stocks

9. Employment by sector and territory Official, NSC RF

10. Labor migration by territory and sector "21 Century" Foundation/MIRPAL

11. Labor and capital shares Official input-output table, NSC RF

DRAFT, NOT FOR DISTRIBUTION

20

Annex II: Simulated labor deficit/surplus in Russia: Optimistic scenario

6.0 percent average non-oil-gas GDP growth, 2.5% increase in labor participation rate for

optimistic population forecast, average non-oil-gas investment ratio 25 percent of GDP

Output,

annual

average

growth rate

Capital stock,

annual

average

growth rate*

Labor, required

annual growth

rate

TFP,

hypothetical

annual growth

rate

Labor force deficit "-

"/surplus "+" by 2020,

thousand ppl.

Labor force deficit "-

"/surplus "+" by 2030,

thousand ppl.

6.0 4.0 6.5 0.5 -63,253.9 -178,120.3

6.0 4.0 6.5 0.5 -62,730.0 -176,156.9

6.0 4.0 6.4 0.5 -62,181.4 -174,109.0

6.0 4.0 6.4 0.6 -61,606.8 -171,973.7

6.0 4.0 6.3 0.6 -61,005.3 -169,748.3

6.0 4.0 6.3 0.6 -60,375.6 -167,430.0

6.0 4.0 6.2 0.7 -59,716.7 -165,016.0

6.0 4.0 6.2 0.7 -59,027.3 -162,503.8

6.0 4.0 6.1 0.7 -58,306.2 -159,890.6

6.0 4.0 6.0 0.8 -57,552.1 -157,173.9

6.0 4.0 6.0 0.8 -56,763.7 -154,351.3

6.0 4.0 5.9 0.9 -55,939.7 -151,420.2

6.0 4.0 5.8 0.9 -55,078.8 -148,378.7

6.0 4.0 5.7 1.0 -54,179.6 -145,224.6

6.0 4.0 5.7 1.0 -53,240.7 -141,956.0

6.0 4.0 5.6 1.1 -52,260.6 -138,571.4

6.0 4.0 5.5 1.1 -51,238.1 -135,069.4

6.0 4.0 5.4 1.2 -50,171.7 -131,449.0

6.0 4.0 5.3 1.2 -49,059.8 -127,709.3

6.0 4.0 5.2 1.3 -47,901.2 -123,850.1

6.0 4.0 5.1 1.3 -46,694.4 -119,871.3

6.0 4.0 5.0 1.4 -45,438.0 -115,773.5

6.0 4.0 4.8 1.5 -44,130.6 -111,557.6

6.0 4.0 4.7 1.6 -42,291.0 -105,709.0

6.0 4.0 4.5 1.7 -40,353.9 -99,655.3

6.0 4.0 4.3 1.8 -38,316.3 -93,403.9

6.0 4.0 4.1 2.0 -36,175.5 -86,964.5

6.0 4.0 3.8 2.1 -33,929.1 -80,349.4

6.0 4.0 3.6 2.2 -31,575.3 -73,573.4

6.0 4.0 3.3 2.4 -29,112.4 -66,654.0

6.0 4.0 3.0 2.6 -26,539.6 -59,611.8

6.0 4.0 2.7 2.7 -23,856.4 -52,470.3

6.0 4.0 2.4 2.9 -21,063.3 -45,256.1

6.0 4.0 2.1 3.1 -18,161.4 -37,998.5

6.0 4.0 1.7 3.3 -15,152.9 -30,729.9

6.0 4.0 1.3 3.6 -12,041.0 -23,485.2

6.0 4.0 0.9 3.8 -8,830.0 -16,301.7

6.0 4.0 0.5 4.1 -5,525.6 -9,218.6

6.0 4.0 0.0 4.4 -2,134.8 -2,276.6

6.0 4.0 -0.5 4.7 1,334.1 4,483.2

6.0 4.0 -1.1 5.0 4,870.9 11,019.2

*Simulated to generate average investment ratio over 2011-2030 of 15 percent of GDP

DRAFT, NOT FOR DISTRIBUTION

19

Annex III: Simulated labor deficit/surplus in Russia: Pessimistic scenario

3.0 percent average non-oil-gas GDP growth, baseline labor participation rate, average non-

oil-gas investment ratio 15 percent of GDP

Output,

annual

average

growth rate

Capital stock,

annual

average

growth rate*

Labor, required

annual growth

rate

TFP,

hypothetical

annual growth

rate

Labor force deficit "-

"/surplus "+" by 2020,

thousand ppl.

Labor force deficit "-

"/surplus "+" by 2030,

thousand ppl.

3.0 0.5 3.8 0.5 -36,535.4 -86,214.0

3.0 0.5 3.8 0.5 -36,118.2 -84,999.3

3.0 0.5 3.8 0.5 -35,681.2 -83,732.5

3.0 0.5 3.7 0.6 -35,223.6 -82,412.0

3.0 0.5 3.7 0.6 -34,744.6 -81,036.1

3.0 0.5 3.6 0.6 -34,243.2 -79,603.0

3.0 0.5 3.6 0.7 -33,718.6 -78,111.2

3.0 0.5 3.5 0.7 -33,169.8 -76,559.1

3.0 0.5 3.4 0.7 -32,595.8 -74,945.0

3.0 0.5 3.4 0.8 -31,995.7 -73,267.5

3.0 0.5 3.3 0.8 -31,368.3 -71,525.1

3.0 0.5 3.2 0.9 -30,712.8 -69,716.3

3.0 0.5 3.2 0.9 -30,027.9 -67,840.0

3.0 0.5 3.1 1.0 -29,312.8 -65,894.9

3.0 0.5 3.0 1.0 -28,566.1 -63,880.0

3.0 0.5 2.9 1.1 -27,787.0 -61,794.4

3.0 0.5 2.8 1.1 -26,974.2 -59,637.3

3.0 0.5 2.7 1.2 -26,126.6 -57,408.2

3.0 0.5 2.6 1.2 -25,243.2 -55,106.7

3.0 0.5 2.5 1.3 -24,322.8 -52,732.9

3.0 0.5 2.4 1.3 -23,364.3 -50,286.7

3.0 0.5 2.3 1.4 -22,366.7 -47,768.7

3.0 0.5 2.2 1.5 -21,328.9 -45,179.5

3.0 0.5 2.0 1.6 -19,869.2 -41,590.2

3.0 0.5 1.8 1.7 -18,332.7 -37,878.1

3.0 0.5 1.6 1.8 -16,717.1 -34,048.4

3.0 0.5 1.4 2.0 -15,020.5 -30,107.3

3.0 0.5 1.2 2.1 -13,241.2 -26,063.0

3.0 0.5 0.9 2.2 -11,377.8 -21,925.0

3.0 0.5 0.7 2.4 -9,429.1 -17,704.6

3.0 0.5 0.4 2.6 -7,394.7 -13,414.9

3.0 0.5 0.1 2.7 -5,274.5 -9,070.8

3.0 0.5 -0.2 2.9 -3,068.9 -4,689.1

3.0 0.5 -0.6 3.1 -779.3 -288.2

3.0 0.5 -0.9 3.3 1,592.5 4,111.6

3.0 0.5 -1.3 3.6 4,043.6 8,488.6

3.0 0.5 -1.7 3.8 6,570.3 12,819.8

3.0 0.5 -2.2 4.1 9,167.8 17,081.2

3.0 0.5 -2.7 4.4 11,830.3 21,247.7

3.0 0.5 -3.2 4.7 14,550.7 25,294.5

3.0 0.5 -3.7 5.0 17,320.9 29,196.6

*Simulated to generate average investment ratio over 2011-2030 of 15 percent of GDP

DRAFT, NOT FOR DISTRIBUTION

20

Annex IV: Simulated labor deficit/surplus depending on TFP growth rates in Central and North-West Federal Districts

Source: own calculations based on data from NSC RF, WB WDI database, and dataset from World Bank (2008)