what will keep insurance ceos awake at night in 2001? an update & outlook for the us &...

TRANSCRIPT

What Will Keep Insurance CEOs Awake at Night in 2001?

An Update & Outlook for the US & Pennsylvania Property/Casualty Insurance

Industry for 2001 and Beyond

Pennsylvania Association of Mutual Insurance CompaniesUnderwriting & Loss Prevention Seminar

Harrisburg Hilton & Towers HotelHarrisburg, PA

November 15, 2000

Robert P. Hartwig, Ph.D. Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 669-9214 Fax: (212) 732-1916 [email protected] www.iii.org

Highlights: First Half 2000($ Millions)

2000 1999 Change

Net Written Prem. 149,301 143,335 +4.2%

Loss & LAE 115,154 106,065 +8.6%

Net UW Gain (Loss) (14,730) (7,788) +89.1%

Net Inv. Income 19,405 19,114 +1.5%

Net Income (a.t.) 10,031 14,865 -32.5%

Surplus 326,708 334,348 -2.3%

Combined Ratio 109.2 104.8 +4.4 pts.

Presentation Outline

Insomnia: Major Problem Among

Insurance CEOs

• Top 10 Reasons for Losing Sleep

• Q&A

#1PROFITS

Return on Equity (Profitability)

-2.1%

8.3%

10.5%

7.7%

9.0%

13.0%

-5% 0% 5% 10% 15%

Fortune 500

US All P/C Lines

PA Workers Comp

PA PP Auto

PA All P/C Lines

PA Homeowners

*Insurers: 1989-1998; and Fortune 500: 1990-1999.Source: NAIC, Insurance Information Institute

10-Year Average*

P/C Net Income After Taxes1993-2000* ($ Billions)

$19,316

$10,870

$20,598

$24,404

$36,819

$30,773

$22,170$20,062

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

1993 1994 1995 1996 1997 1998 1999 2000**Estimate based on First Half 2000 data.Sources: A.M. Best, ISO.

0%

5%

10%

15%

20%

25%

US P/C Insurers All US Industries LifeDiversified Finl. Comm. Banks

ROE: Financial Services Industry Segments, 1987–2000*

* 2000 figures are estimates.Source: Insurance Information Institute

Return on Net Worth,Selected Lines in Pennsylvania

Source: NAIC, Insurance Information Institute

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

Auto Homeowners Workers' Comp

10-Year Averages

Auto +10.5%

Home -2.1%

WC +7.7

Sagging Profits are the Symptom, not the Cause

•Capital/Capacity•Pricing•Fundamentals•Investments•Competition•Consolidation•Distribution•Class Action•Wall Street

#2CAPITAL/CAPACITY

$0

$50

$100

$150

$200

$250

$300

$350

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

*

Policyholder Surplus: 1975-2000* (Capital, Total P/C)

Source: A.M. Best, Insurance Information Institute

Bil

lion

s

(US

$)

•1999 Surplus = $336.3 Billion Is it a Peak?

•Increase of 0.9% over 1998, smallest gain since 1984

•Surplus decreased 2.3% in First Half 2000 to $326.7 Billion

* First Half 2000

0.5

1.3

2.0

2.8

US

Net Premiums Written to Policyholder Surplus

Source: A.M. Best, ISO, Insurance Information Institute

1998: 0.84

1999: 0.85

2000 (Forecast): 0.94

Berkshire Hathaway

12.3%

Other67.2%

USAA1.8%

Farmers1.3%

Nationwide3.1%

State Farm12.2%

Liberty2.1%

Distribution of Industry Surplus

Source: PaineWebber

Excess Capital: What to Do?

• CEOs: Buy It, Build It--They Will Come

• Policyholders: Lower my rates! Pay my dividend!

• Shareholders: Show me the money!

• Regulators: Keep your hands off of it!

• Rating Agencies: Keep your hands off of it and give it

back!

#3PRICING

Average Price Change of Commercial Insurance Renewals

1.4%

0.8%

-1.6%

-1.2%

-0.4%

-5.0%

-4.4%

-7.0%

-6.0%

-11.0%

-6.0%

-10.0%

-7.0%

-3.0%

3.5%

3.2%

3.2%

2.8%

4.1%

-2.1%

-2.8%

-1.8%

0.2%

-3.5%

-4.3%

-6.6%

-4.1%

-2.0%

-16% -14% -12% -10% -8% -6% -4% -2% 0% 2%

E&S

Umbrella

Workers' Comp

Commercial Property

CMP

General Liability

Commercial Auto

Spring 2000 Fall 99 Spring 99 Fall 98Source: Conning

Policy Renewal Premiums in Standard Commercial Lines

0.2%

0.2%

3.9%

53.5%

28.2%

12.8%

0.9%

0.2%

0.2%

0.0%

1.8%

19.6%

62.3%

14.8%

1.3%

0.3%

0.0%

0.0%

0% 10% 20% 30% 40% 50% 60% 70%

Up Over 30%

Up 21-30%

Up 11-20%

Up 1-10%

No Change

Down 1-10%

Down 11-20%

Down 21-30%

Down Over 30%

Jan-00 Jul-00

Source: Goldman Sachs

Policy Renewal Premiums in Workers’ Compensation

0.7%

1.5%

8.8%

38.0%

34.3%

13.1%

2.9%

0.0%

0.7%

2.4%

4.7%

29.9%

37.8%

22.0%

3.1%

0.0%

0.0%

0.0%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Up Over 30%

Up 21-30%

Up 11-20%

Up 1-10%

No Change

Down 1-10%

Down 11-20%

Down 21-30%

Down Over 30%

Jan-00 Jul-00

Source: Goldman Sachs

-6.0%

-8.8%

-14.0%

-20.6%

-24.8%-26.6%

-30%

-20%

-10%

0%

Cumulative Workers Comp Rate/Loss Cost Changes*

Source: NCCI*Advisory Loss Costs

Average Expenditures on Auto Insurance: US vs. PA

572

596

618

637 65

166

869

170

770

4

697 70

272

272

0

687

667

657

645

642

610

634

$500

$550

$600

$650

$700

$750

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

*

2000

*

* III estimates; Sources: NAIC, Insurance Information Institute

Countrywide rates fell by 2.8% in 1998, 3.2% in

1999 (est.)

Nearby States’ Auto Insurance Expenditures & Rank, 19981138

960

769722

581

704

$0

$300

$600

$900

$1,200

Expenditures/Rank

New Jersey New York Maryland Pennsylvania Ohio US

Source: NAIC (March 2000 release), Insurance Information Institute

1 2 14 19 37

Nearby States’ Average Homeowners Insurance Premium, 1997

513469

379355

289

455

$0

$300

$600

Expenditures/Rank

New York New Jersey Pennsylvania Maryland Ohio US

Source: NAIC (March 2000 release), Insurance Information Institute

11 18 34 38 50

#4FUNDAMENTALS

95

100

105

110

115

120

Combined Ratio

P/C Industry Combined Ratio

1999 = 107.9

2000 (Est)* = 109.6

2001 Forecast* = 108.7

Combined Ratios

1970s: 100.3

1980s: 109.2

1990s: 107.7

* Based on III Earlybird Forecast

2001*

Direct Loss Ratio Trends, Selected Lines, Pennsylvania

Source: NAIC, Insurance Information Institute

40%

60%

80%

100%

120%

140%

Auto Homeowners Workers Comp

($40)

($30)

($20)

($10)

$0

$10

Underwriting Gain (Loss)1975-2000*

*I.I.I. estimate based on First Half 2000 data.Source: A.M. Best, Insurance Information Institute

Bil

lion

s

(US

$)

In 2000, P-C insurers will pay out nearly $30 billion more in claims and

expenses than they collected in premiums

U.S. InsuredCatastrophe Losses

$7.5

$2.7$4.7

$22.9

$5.5

$16.9

$8.3 $7.3

$2.6

$10.1$8.3

$3.2

0

5

10

15

20

25

89 90 91 92 93 94 95 96 97 98 99 00*

* First Half 2000.Source: Property Claims Service, Insurance Information Institute

CATs in 1990s caused

$90B in insured losses

$ Billions CATs cost insurers $750 million per month during the 1990s

3% 3%

-4%-3%

-2%

0%

-6% -6%

-4%

-1%

-10%

-5%

0%

5%

Lost-Time Claim Frequency Per Worker: On the Rise?

Source: NCCI

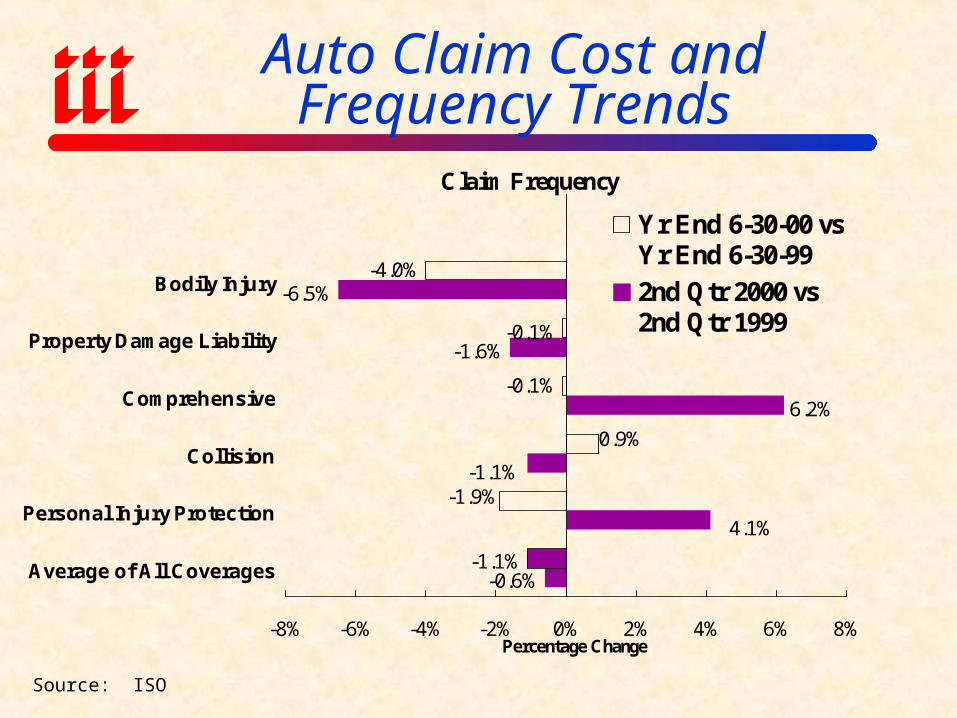

Auto Claim Cost andFrequency Trends

Claim Frequency

-0.6%

6.2%

-1.6%

-6.5%

-0.1%

4.1%

-1.1%

-1.1%

-1.9%

0.9%

-0.1%

-4.0%

-8% -6% -4% -2% 0% 2% 4% 6% 8%

Average of All Coverages

Personal Injury Protection

Collision

Comprehensive

Property Damage Liability

Bodily Injury

Percentage Change

Yr End 6-30-00 vsYr End 6-30-99

2nd Qtr 2000 vs2nd Qtr 1999

Source: ISO

Auto Claim Cost andFrequency Trends

Average Loss

10.6%

15.0%

6.0%

4.2%

5.9%

15.4%

7.8%

5.9%

13.5%

6.2%

5.5%

2.1%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Average of All Coverages

Personal Injury Protection

Collision

Comprehensive

Property Damage Liability

Bodily Injury

Percentage Change

Yr End 6-30-00 vs YrEnd 6-30-99

2nd Qtr 2000 vs 2ndQtr 1999

Source: ISO

Auto Claim Cost andFrequency Trends

Combined Frequency and Severity

10.0%

22.1%

4.3%

-2.6%

5.8%

20.1%

6.6%

4.8%

11.3%

7.2%

5.4%

-2.0%

-5% 0% 5% 10% 15% 20% 25%

Average of All Coverages

Personal Injury Protection

Collision

Comprehensive

Property Damage Liability

Bodily Injury

Percentage Change

Yr End 6-30-00 vs YrEnd 6-30-99

2nd Qtr 2000 vs 2ndQtr 1999

Source: ISO

#5INVESTMENTS

$0

$9

$18

$27

$36

$45

Net Investment Income

Facts

1997 Peak = $41.5B

1998 = $39.9B

1999 = $38.6B

2000 (Forecast)* = $39.2B

Source: A.M. Best, Insurance Information Institute

Bil

lion

s

(US

$)

Pricing & underwriting problems were exacerbated by declining investment income

* Estimate based on First Half 2000 results.

Interest Rates: Up, Up,But Not Away

2%

4%

6%

8%

10%

12%

14%

16%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00**

3-Month T-Bills 10 Year Notes

**Forecast

Source: Federal Reserve Board of Governors.

Rising interest rates reduced the market value of the

industry’s bond portfolio by $55 billion in 1999

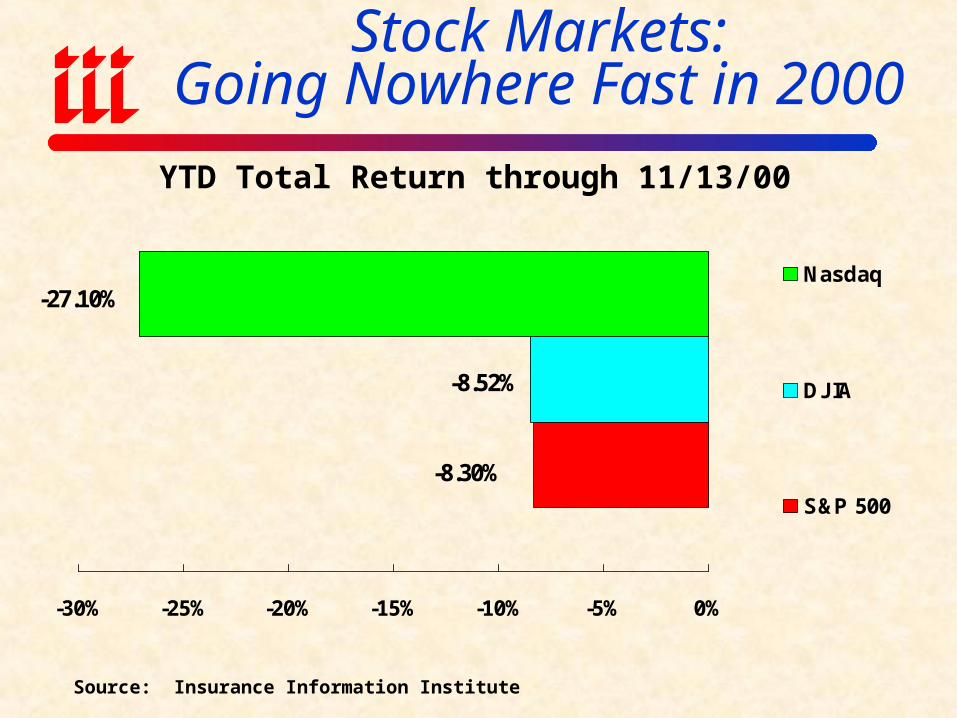

Stock Markets:Going Nowhere Fast in 2000

-8.52%

-8.30%

-27.10%

-30% -25% -20% -15% -10% -5% 0%

Nasdaq

DJIA

S&P 500

Source: Insurance Information Institute

YTD Total Return through 11/13/00

#6COMPETITION

Competition—Still on the Rise: Number of Insurers: 1970-1998

1095 1059

15751702

2406 2430 2485 2480

1802 17461958

2261 2195

17151563

0

500

1,000

1,500

2,000

2,500

3,000

1970 1975 1980 1985 1990 1995 1998 1999

Property/Casualty

Life/Health

Sources: P/C: A.M. Best; L/H: NAIC.

Market Share of Top 5 P/C Insurers

30.2%

29.7%

29.3%

28.5%

1995 1997 1998 1999

Source: Insurance Information Institute Fact Book (annual issues)

Market Share of Top 5 Life/Health Insurers

14.0%

17.0%18.0%

1997 1998 1999

Source: Insurance Information Institute Fact Book (annual issues)

0%

5%

10%

15%

20%

25%

U.S.

Source: A.M. Best, ISO, Insurance Information Institute

Growth in Net Premiums Written (All P/C Lines)

2000 est.; 2001 forecast from III Earlybird Survey

1999: 1.9%

2000 Est: 5.2%

2001 Forecast: 7.0%

The underwriting cycle went AWOL in the 1990s.

Is it Back?

2001*

#7CONSOLIDATION

Insurance Mergers and Acquisitions

7.1 6.9 8.6 5 8.5 12.527

40.856.2

41.6

11.3

243 246

171 188149

221

349382

433

161

472

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

89 90 91 92 93 94 95 96 97 98 99 00*

Val

ue

of M

& A

s ($

bill

ion

s)

0

100

200

300

400

500

600

Nu

mb

er o

f M

& A

s

Value of Deals Number of Deals

*First Half 2000Source: Compiled from Conning & Company reports.

1998: 565 deals valued at $165.4 B

Number of Deals: First Half 2000 vs. First Half 1999

3034

18 2016

2824

57

73

105

P/C Life Health/MC Service Distribution

Source: Conning

19992000

Total = 161 Total = 244

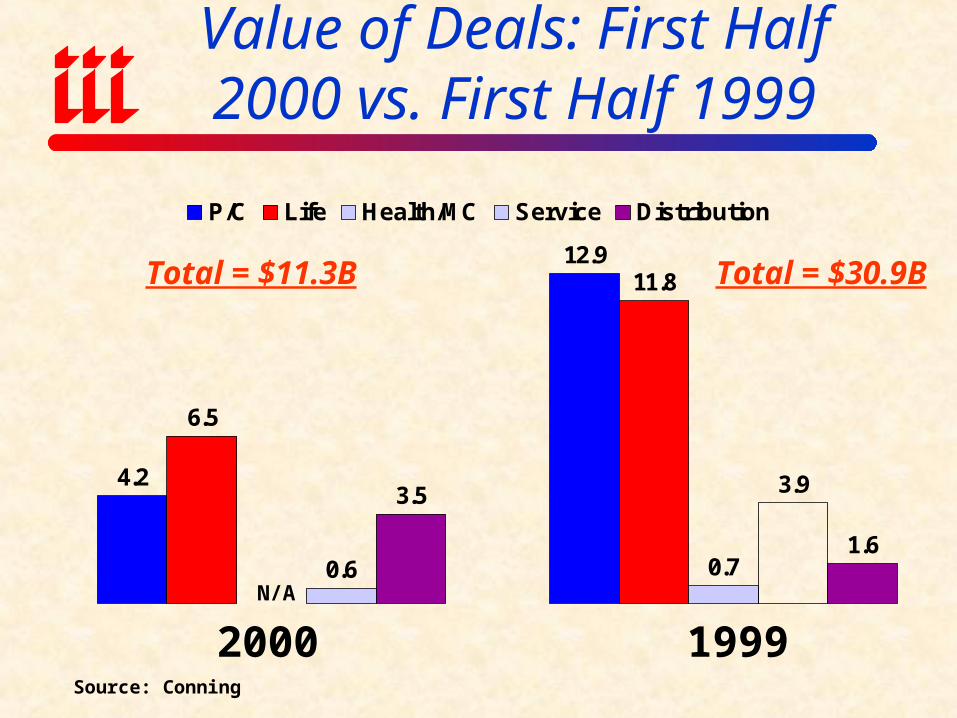

Value of Deals: First Half 2000 vs. First Half 1999

4.2

12.9

6.5

11.8

0.70.6

3.5

1.6

3.9

P/C Life Health/MC Service Distribution

Source: Conning

19992000

Total = $11.3B Total = $30.9B

N/A

#8DISTRIBUTION

Small Insurance Firms Lag in Web Access and Exposure

Source: The Industry Standard, Summer 2000

Percentage of Small Firms with Internet Access

82%

70%

56%

0%10%20%30%40%50%60%70%80%90%

Real EstateAgencies

Law Firms InsuranceFirms andAgencies

Percentage of Small Firms with Their Own Web Site

30%

41%

23%

0%5%

10%15%20%25%30%35%40%45%

Real EstateAgencies

Law Firms InsuranceFirms andAgencies

Web Presence of the Nation's 250 Largest P/C Companies

Source: John P. Franzis, PricewaterhouseCoopers Management

No Web Site Whatsoever

27.5%

Transaction Sites: Real Time Quotes

but No Sales7.2%

Rudimentary E-Mail Quote

Forms4.0%

Processor Sites: Quotes, Sales, and

Claims Online0.4%

Billboard Sites: No Quotes or

Transactions60.9%

Shifting Distribution Channels: Property/Casualty Insurers

Source: Datamonitor

20031998

Direct Response

10.0%Banks8.1%

Internet7.3%

Other2.5%

Independent Agents23.3%

Captive Agents48.8%

Direct Response

9.8%Banks2.8%

Internet0.9%

Other3.0%

Independent Agents27.0%

Captive Agents56.5%

Projected Online Sales of Auto, Home & Term Life Insurance

0

500

1000

1500

2000

2500

3000

3500

Auto Home Term Life

1998

1999

2000

2001

2002

2003

Source: Forrester Research

$ Millions

Life = $1.3B27%

Home = $0.3B6%

Auto = $3.2B67%

Internet Insurance Sales Forecast, 2003

Source: Conning & Co. (Life), Forrester Group (Auto & Home)

(Online-closed sales=Total $4.8 Billion)

Small-Commercial Market’s Internet Potential

Source: Connings MarketStance

Extremely Interested

($.8 B)1.5%

Very Interested

($2.3 B)4.6%

Not at All Interested($23.0 B)

45.9%

Somewhat Interested

($7.5 B)14.9%

Not Very Interested($ 16.7 B)

33.2%Total Written Premium

($50.2 Billion)

Internet Ready Small-Commercial Market Written Premium Potential

Source: Connings MarketStance

Retail Trade($1,252 Mil)

14.9%

TCPU($700 Mil)

8.3%

Mfg($767 Mil)

9.1%Construction($1,622 Mil)

19.3%

Agriculture($96 Mil)

1.1%

Services($1,665 Mil)

19.8%

FIRE($433 Mil)

5.2%

Wholesale Trade

($1,858 Mil)22.1%

Total Written Premium($8.4 Billion)

Distribution Channels Continue to Proliferate

Customer InsurerAgent Broker

Mail Telephone

Bank

Internet Dealerships Payroll Plans

Stock Exchanges

Online Auctions (e.g. Priceline.com)

????

Insurers: Tangled in the Web?

#9CLASS ACTION

ABUSE

TORT-ure

• Aftermarket Parts• Medical Claims Review• Totaled Cars (CCC/ADP)• Guns• Genetically Modified Foods (Corn)• Y2K Sue & Labor• HMOs• Nursing Homes/Med Mal• Tobacco• Technology (Toshiba/Microsoft)• Redlining• Toxic Mold

Median Jury Award for Personal Injury Cases

50,000

45,000

48,096

39,054

45,000

50,000 50,000

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

93 94 95 96 97 98 99

Source: Jury Verdict Research

Average Jury Awards1993 vs.1999

520759

175 324 249

1,9531,444

1,004

1,727

316 457

2,9593,495

7,361

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Overall BusinessNegligence

VehicularLiability*

PremisesLiability

PersonalNegligence

MedicalMalpractice

ProductsLiability

($00

0)

1993 1999

*Comparison is between 1994 and 1999.Source: Jury Verdict Research; Insurance Information Institute.

Median Jury Award for Product Liability Cases

500,300 434,247 497,000

702,500550,000

1,257,000

1,806,000

$200,000

$500,000

$800,000

$1,100,000

$1,400,000

$1,700,000

$2,000,000

93 94 95 96 97 98 99

Source: Jury Verdict Research

Median Punitive Damage Award by Case Type

1,229,080

956,470

652,000

277,875194,180

94,700

250,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

Securities OtherCommercial

Insurance OtherContracts

Employment Real Property Overall

(1985-1994, $1992)

Source: Jury Verdict Research

#10WALL STREET

Insurer 1999 Stock Performance

-25.65%

-9.62%

-6.54%

-3.08%

20.95%

-30% -20% -10% 0% 10% 20% 30%

S&P 500

Banks

All Insurers

L/H

P/C

Source: SNL Securities, Insurance Information Institute

Total Return

IPO Champs

458%

474%

482%

483%

525%

606%

698%VA Linux

Theglobe.com

Foundry Networks

FreeMarkets

Cobalt Networks

Marketwatch.com

Akamai Technologies

Source: Hoover’s

Biggest First-Day Jumps from Offer Price to Close

$145 31610/29/99

$97 ½1/15/99

$128 1811/5/99

$28012/10/99

$156 ¼9/28/99

$63 ½11/13/99

$239 ¼12/9/99

1st Day CloseDate

Insurance Stock Performance:What a Difference a Year Makes

26.95%

28.52%

32.32%

39.25%

10.89%

-7.03%

-7.78%

-25.57%

-30% -20% -10% 0% 10% 20% 30% 40% 50%

Nasdaq

DJIA

S&P 500

Banks

Multiline

All Insurers

Life/Health

P/C

Source: SNL Securities, Insurance Information Institute

YTD Total Return through November 10, 2000

Insurance Stock Performance:Since Tech Crash Began

57.6%

-2.1%

74.0%

67.2%

69.6%

57.6%

24.5%

-40.0%

-50% -40% -30% -20% -10% 0% 10% 20% 30% 40% 50% 60% 70% 80%

Nasdaq

S&P 500

Banks

P/C

Brokers

Life/Health

All Insurers

Multiline

* NASDAQ peaked on March 10, 2000 at 5048.62Source: Insurance Information Institute, SNL Securities

Total Return: March 10 through November 10, 2000*

Insurance Stock Performance:Since Tech Crash Began

-4.0%

48.6%

44.3%

41.0%

36.2%

35.7%

13.3%

-27.4%

-40% -20% 0% 20% 40% 60%

Nasdaq

S&P 500

Banks

Life/Health

P/C

All Insurers

Brokers

Multiline

* NASDAQ peaked on March 10, 2000 at 5048.62Source: Insurance Information Institute, SNL Securities

Total Return: March 10 through July 28, 2000*

Dot-Com to Dot-Gone?

Source: Stockpoint.com, Insurance Information Institute.

Price: June 8 52-Week High Low

QUOT: $2.91 $13.63 $2.91

INSW: $3.00 $44.00 $2.09

Insurance Information Institute On-Line

Download this presentation at: http://www.iii.org/media/pennsylvania/index.htm