week ahead – the end of the beginning

TRANSCRIPT

13 March 2020

Week ahead – Theend of the beginning

Martin Enlund | Andreas Steno Larsen

• How deep and long-lasting will the recession be?• Oil price plunge definitely not good news• NY Fed brought an aircraft carrier to a knife fight.

If you want to receive a copy of Week ahead directly in your inbox, you can sign up via thislink.

Main Releases

How deep and long-lasting will the recession be?

In the eyes of many market participants, it’s no longer a question if we are heading towards a new virus-triggered recession, but rather how deep and long-lasting it will be. The sudden oil price war has alsomade matters worse. Lower oil prices used to be good news for global growth as it would boost realincomes for households and profit margins for energy-using businesses. However, the drop in oil prices in2014-2015 taught us otherwise …

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

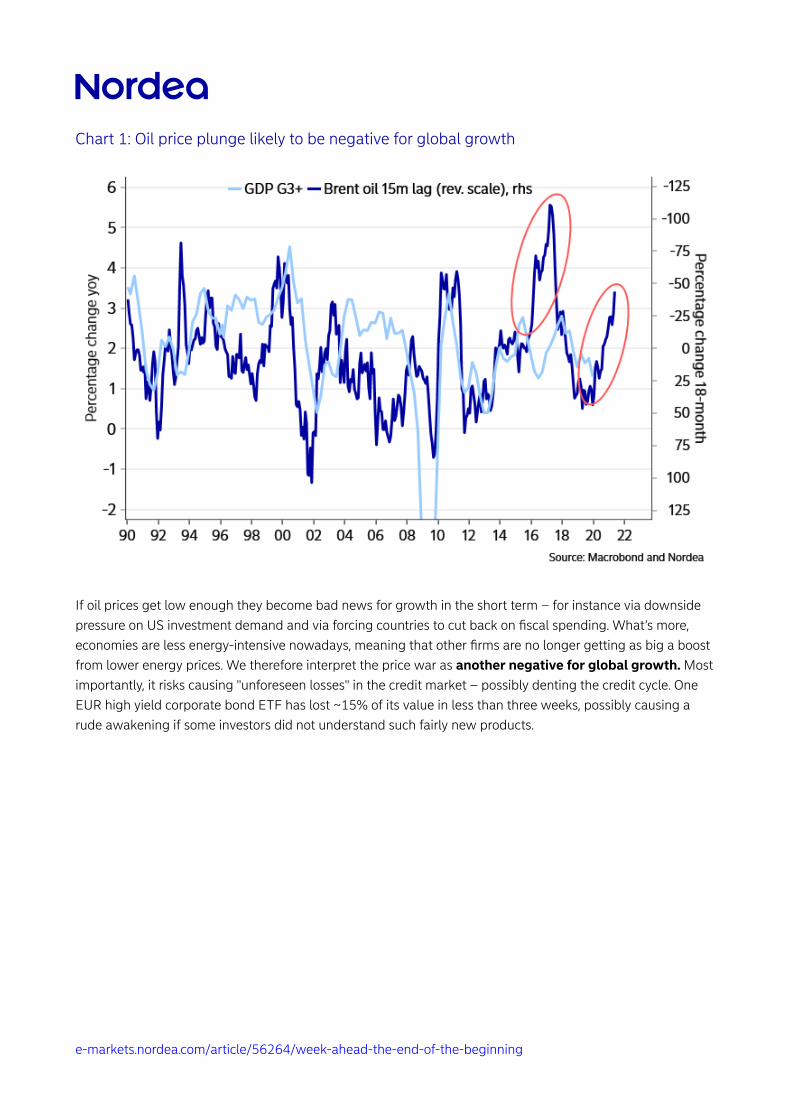

Chart 1: Oil price plunge likely to be negative for global growth

If oil prices get low enough they become bad news for growth in the short term – for instance via downsidepressure on US investment demand and via forcing countries to cut back on fiscal spending. What’s more,economies are less energy-intensive nowadays, meaning that other firms are no longer getting as big a boostfrom lower energy prices. We therefore interpret the price war as another negative for global growth. Mostimportantly, it risks causing "unforeseen losses" in the credit market – possibly denting the credit cycle. OneEUR high yield corporate bond ETF has lost ~15% of its value in less than three weeks, possibly causing arude awakening if some investors did not understand such fairly new products.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

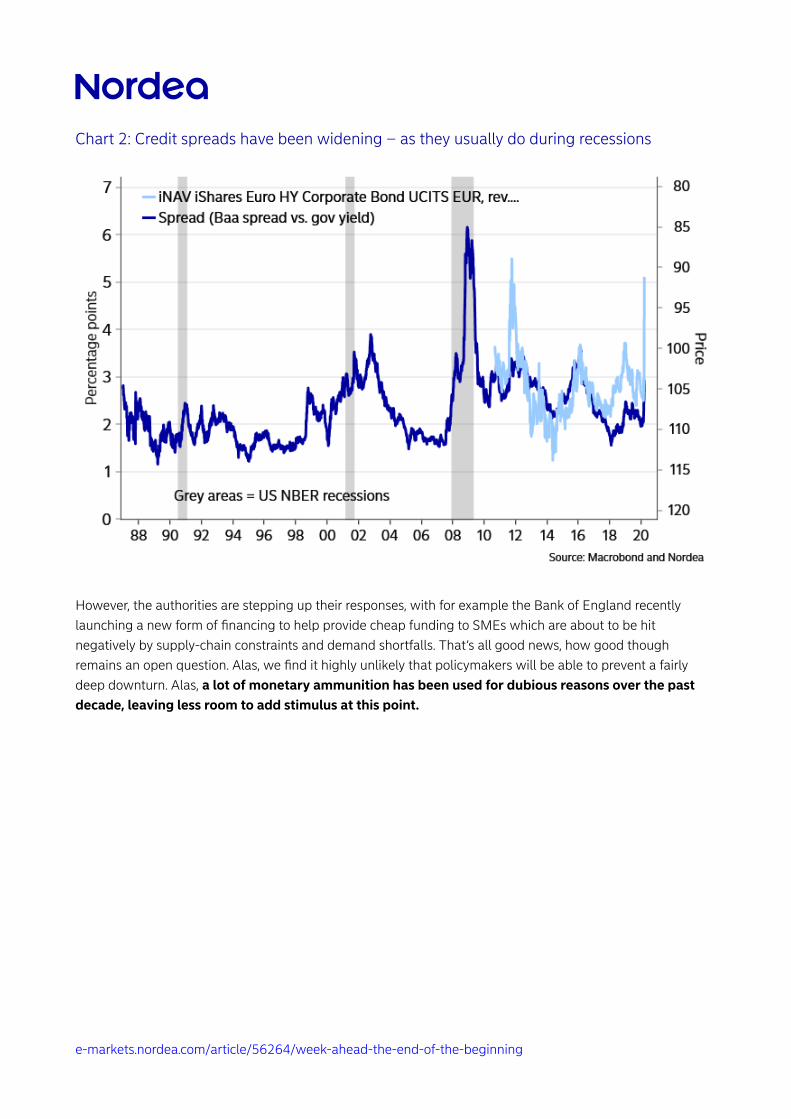

Chart 2: Credit spreads have been widening – as they usually do during recessions

However, the authorities are stepping up their responses, with for example the Bank of England recentlylaunching a new form of financing to help provide cheap funding to SMEs which are about to be hitnegatively by supply-chain constraints and demand shortfalls. That’s all good news, how good thoughremains an open question. Alas, we find it highly unlikely that policymakers will be able to prevent a fairlydeep downturn. Alas, a lot of monetary ammunition has been used for dubious reasons over the pastdecade, leaving less room to add stimulus at this point.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

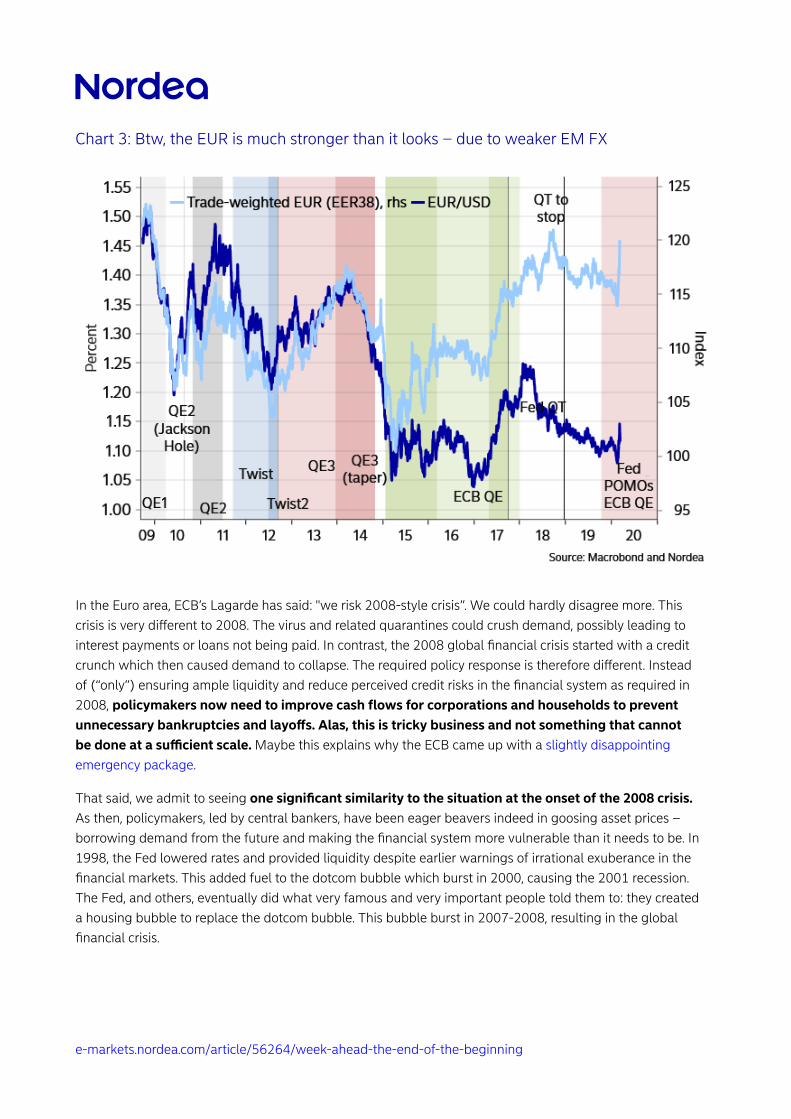

Chart 3: Btw, the EUR is much stronger than it looks – due to weaker EM FX

In the Euro area, ECB’s Lagarde has said: "we risk 2008-style crisis”. We could hardly disagree more. Thiscrisis is very dierent to 2008. The virus and related quarantines could crush demand, possibly leading tointerest payments or loans not being paid. In contrast, the 2008 global financial crisis started with a creditcrunch which then caused demand to collapse. The required policy response is therefore dierent. Insteadof (“only”) ensuring ample liquidity and reduce perceived credit risks in the financial system as required in2008, policymakers now need to improve cash flows for corporations and households to preventunnecessary bankruptcies and layos. Alas, this is tricky business and not something that cannotbe done at a sucient scale. Maybe this explains why the ECB came up with a slightly disappointingemergency package.

That said, we admit to seeing one significant similarity to the situation at the onset of the 2008 crisis.As then, policymakers, led by central bankers, have been eager beavers indeed in goosing asset prices –borrowing demand from the future and making the financial system more vulnerable than it needs to be. In1998, the Fed lowered rates and provided liquidity despite earlier warnings of irrational exuberance in thefinancial markets. This added fuel to the dotcom bubble which burst in 2000, causing the 2001 recession.The Fed, and others, eventually did what very famous and very important people told them to: they createda housing bubble to replace the dotcom bubble. This bubble burst in 2007-2008, resulting in the globalfinancial crisis.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

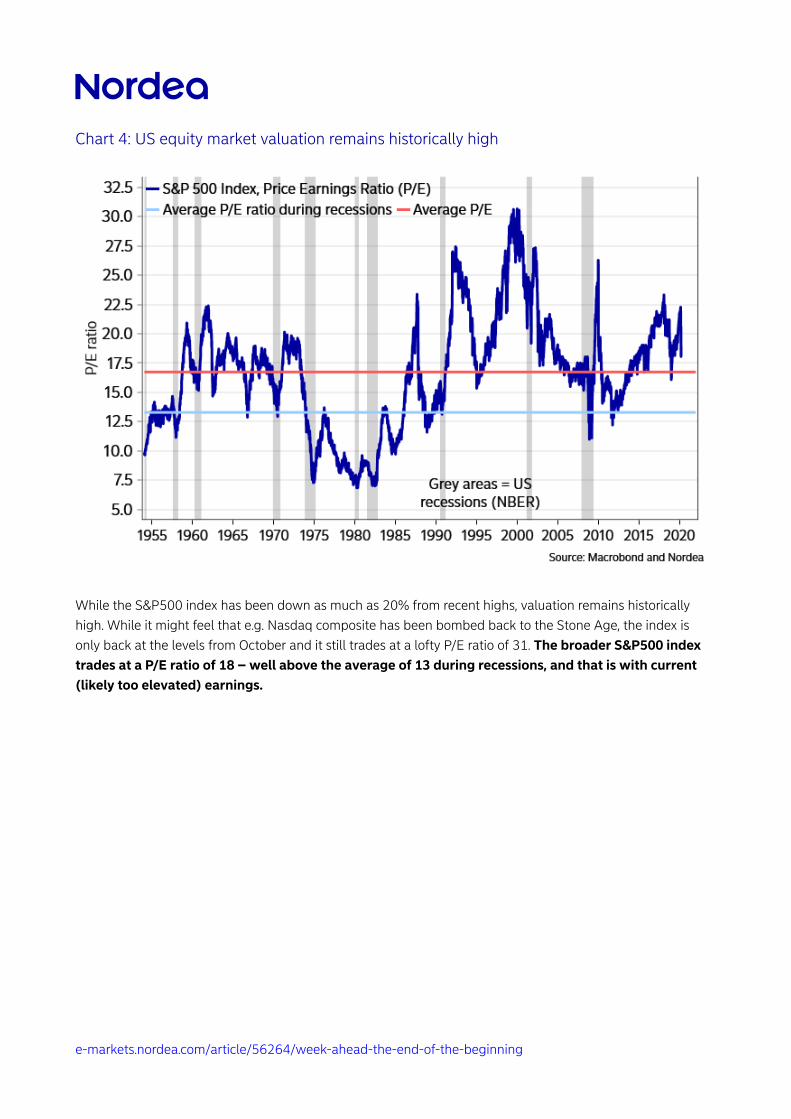

Chart 4: US equity market valuation remains historically high

While the S&P500 index has been down as much as 20% from recent highs, valuation remains historicallyhigh. While it might feel that e.g. Nasdaq composite has been bombed back to the Stone Age, the index isonly back at the levels from October and it still trades at a lofty P/E ratio of 31. The broader S&P500 indextrades at a P/E ratio of 18 – well above the average of 13 during recessions, and that is with current(likely too elevated) earnings.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

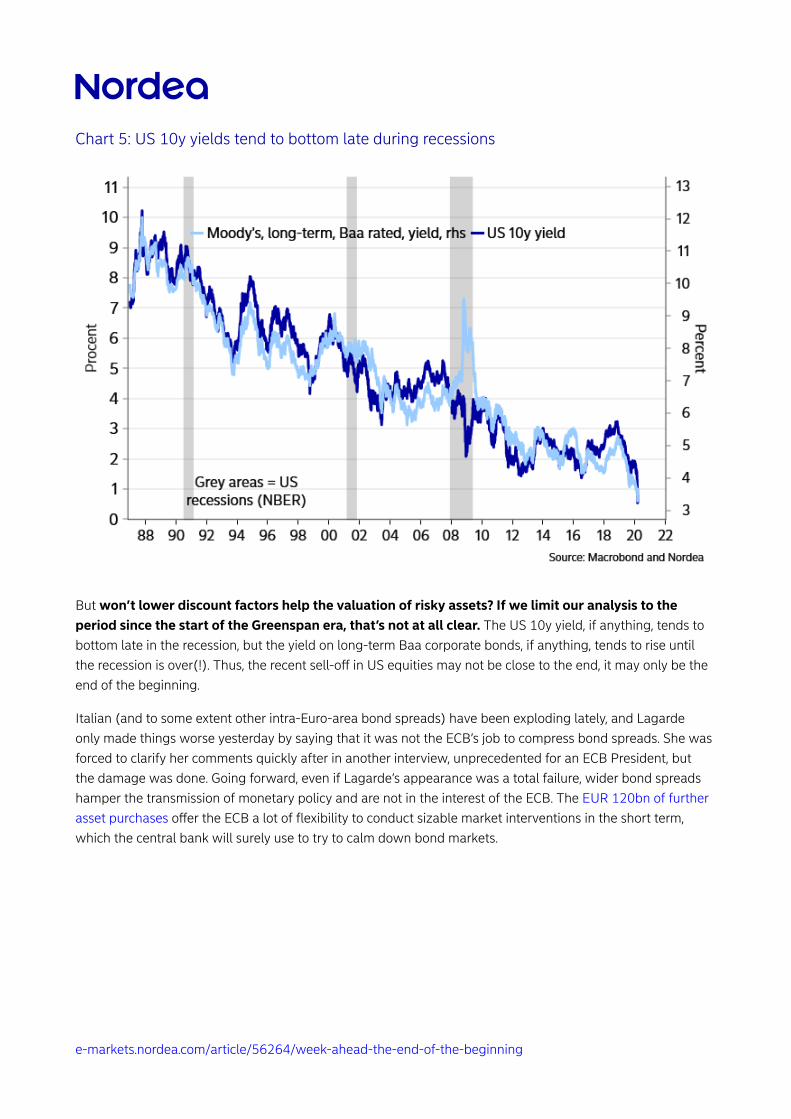

Chart 5: US 10y yields tend to bottom late during recessions

But won’t lower discount factors help the valuation of risky assets? If we limit our analysis to theperiod since the start of the Greenspan era, that’s not at all clear. The US 10y yield, if anything, tends tobottom late in the recession, but the yield on long-term Baa corporate bonds, if anything, tends to rise untilthe recession is over(!). Thus, the recent sell-o in US equities may not be close to the end, it may only be theend of the beginning.

Italian (and to some extent other intra-Euro-area bond spreads) have been exploding lately, and Lagardeonly made things worse yesterday by saying that it was not the ECB’s job to compress bond spreads. She wasforced to clarify her comments quickly after in another interview, unprecedented for an ECB President, butthe damage was done. Going forward, even if Lagarde’s appearance was a total failure, wider bond spreadshamper the transmission of monetary policy and are not in the interest of the ECB. The EUR 120bn of furtherasset purchases oer the ECB a lot of flexibility to conduct sizable market interventions in the short term,which the central bank will surely use to try to calm down bond markets.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

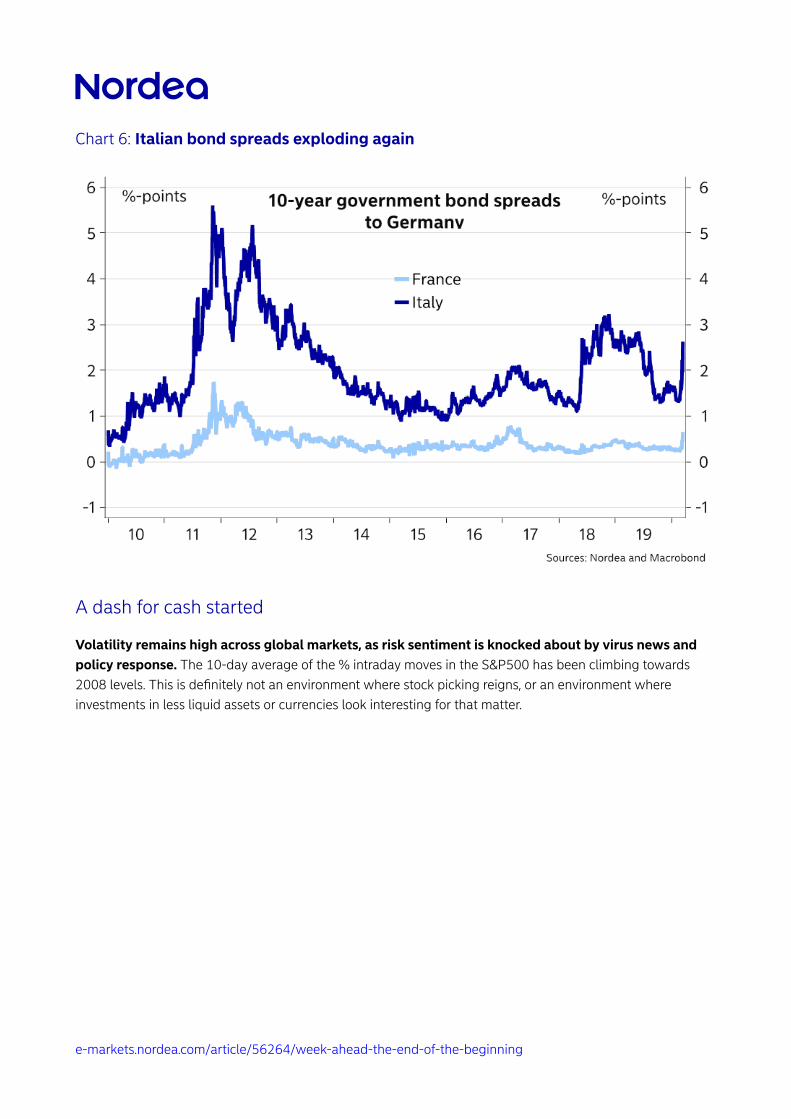

Chart 6: Italian bond spreads exploding again

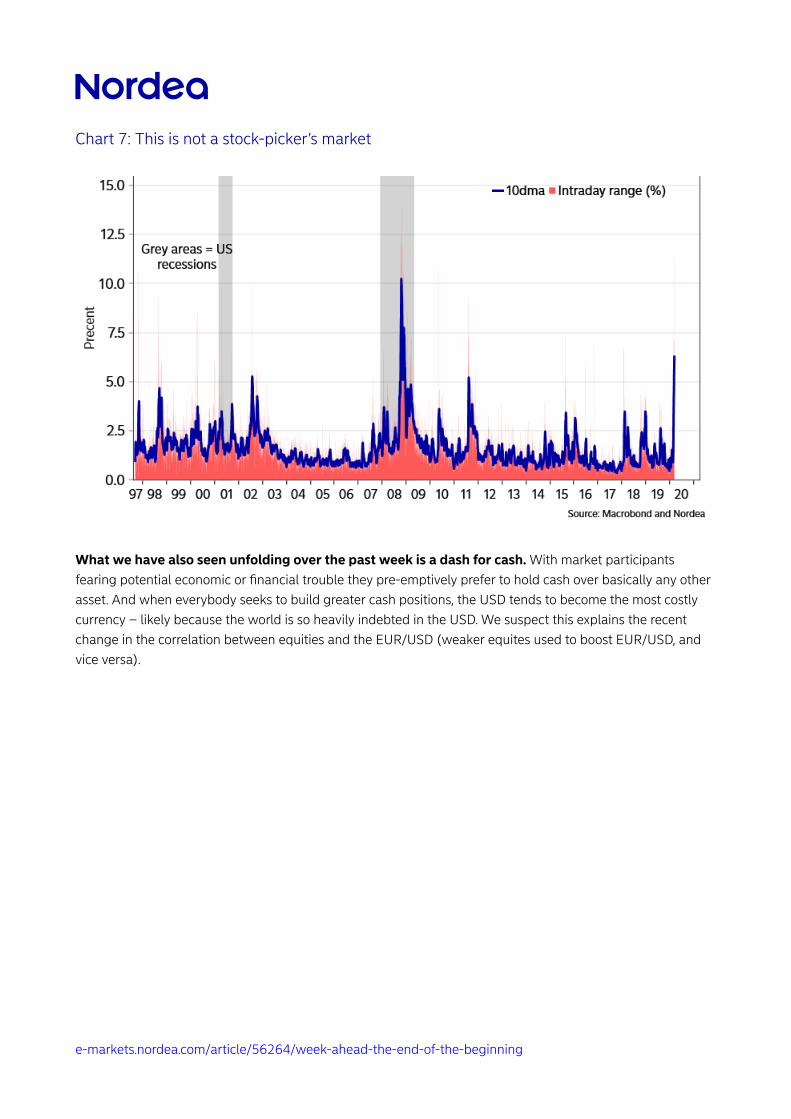

A dash for cash started

Volatility remains high across global markets, as risk sentiment is knocked about by virus news andpolicy response. The 10-day average of the % intraday moves in the S&P500 has been climbing towards2008 levels. This is definitely not an environment where stock picking reigns, or an environment whereinvestments in less liquid assets or currencies look interesting for that matter.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

Chart 7: This is not a stock-picker’s market

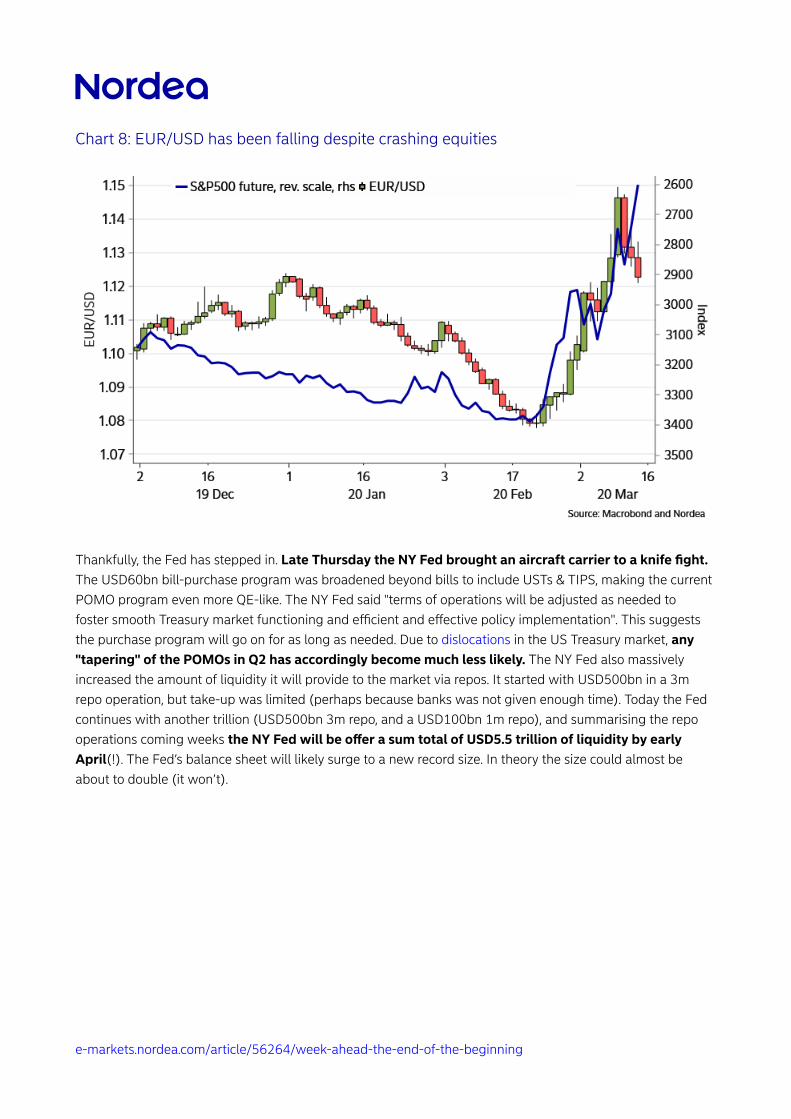

What we have also seen unfolding over the past week is a dash for cash. With market participantsfearing potential economic or financial trouble they pre-emptively prefer to hold cash over basically any otherasset. And when everybody seeks to build greater cash positions, the USD tends to become the most costlycurrency – likely because the world is so heavily indebted in the USD. We suspect this explains the recentchange in the correlation between equities and the EUR/USD (weaker equites used to boost EUR/USD, andvice versa).

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

Chart 8: EUR/USD has been falling despite crashing equities

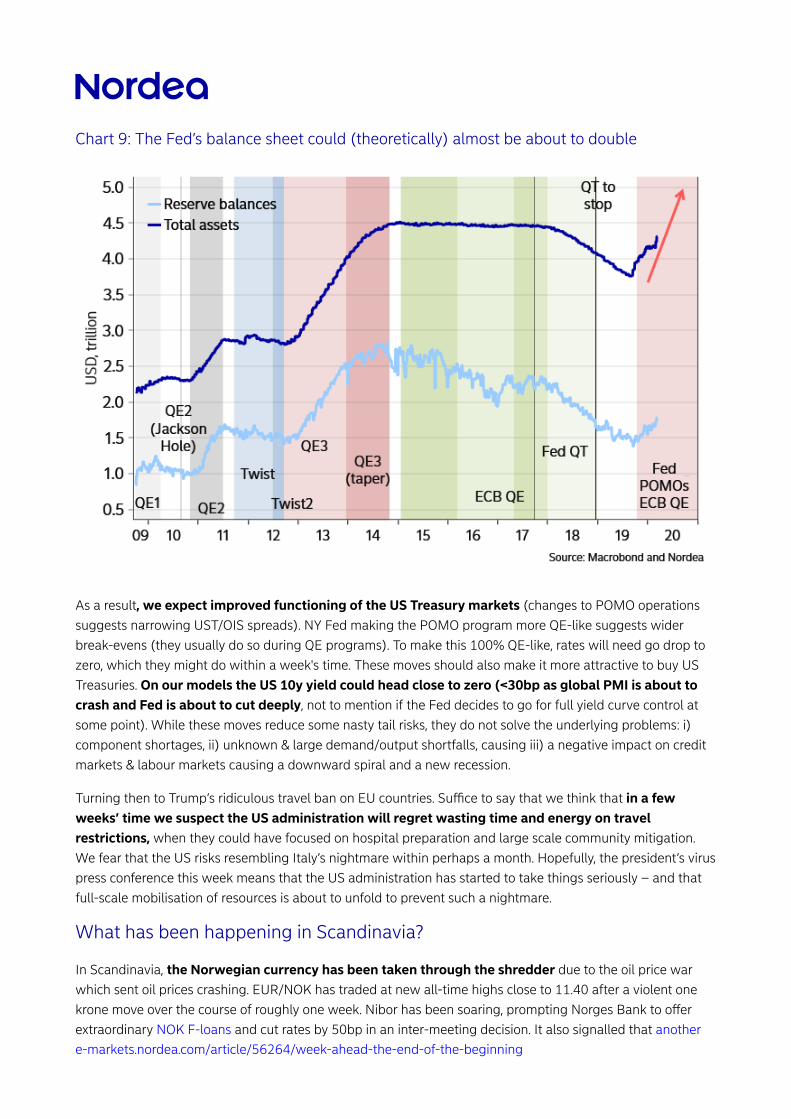

Thankfully, the Fed has stepped in. Late Thursday the NY Fed brought an aircraft carrier to a knife fight.The USD60bn bill-purchase program was broadened beyond bills to include USTs & TIPS, making the currentPOMO program even more QE-like. The NY Fed said "terms of operations will be adjusted as needed tofoster smooth Treasury market functioning and ecient and eective policy implementation". This suggeststhe purchase program will go on for as long as needed. Due to dislocations in the US Treasury market, any"tapering" of the POMOs in Q2 has accordingly become much less likely. The NY Fed also massivelyincreased the amount of liquidity it will provide to the market via repos. It started with USD500bn in a 3mrepo operation, but take-up was limited (perhaps because banks was not given enough time). Today the Fedcontinues with another trillion (USD500bn 3m repo, and a USD100bn 1m repo), and summarising the repooperations coming weeks the NY Fed will be oer a sum total of USD5.5 trillion of liquidity by earlyApril(!). The Fed’s balance sheet will likely surge to a new record size. In theory the size could almost beabout to double (it won’t).

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

Chart 9: The Fed’s balance sheet could (theoretically) almost be about to double

As a result, we expect improved functioning of the US Treasury markets (changes to POMO operationssuggests narrowing UST/OIS spreads). NY Fed making the POMO program more QE-like suggests widerbreak-evens (they usually do so during QE programs). To make this 100% QE-like, rates will need go drop tozero, which they might do within a week's time. These moves should also make it more attractive to buy USTreasuries. On our models the US 10y yield could head close to zero (<30bp as global PMI is about tocrash and Fed is about to cut deeply, not to mention if the Fed decides to go for full yield curve control atsome point). While these moves reduce some nasty tail risks, they do not solve the underlying problems: i)component shortages, ii) unknown & large demand/output shortfalls, causing iii) a negative impact on creditmarkets & labour markets causing a downward spiral and a new recession.

Turning then to Trump’s ridiculous travel ban on EU countries. Suce to say that we think that in a fewweeks’ time we suspect the US administration will regret wasting time and energy on travelrestrictions, when they could have focused on hospital preparation and large scale community mitigation.We fear that the US risks resembling Italy’s nightmare within perhaps a month. Hopefully, the president’s viruspress conference this week means that the US administration has started to take things seriously – and thatfull-scale mobilisation of resources is about to unfold to prevent such a nightmare.

What has been happening in Scandinavia?

In Scandinavia, the Norwegian currency has been taken through the shredder due to the oil price warwhich sent oil prices crashing. EUR/NOK has traded at new all-time highs close to 11.40 after a violent onekrone move over the course of roughly one week. Nibor has been soaring, prompting Norges Bank to oerextraordinary NOK F-loans and cut rates by 50bp in an inter-meeting decision. It also signalled that anothere-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

rate cut is on the cards. The crashing NOK has weighed on the SEK, which has traded to new local highs(the high close to ~11.80 in EUR/SEK from 2009 remains far away, for now). In Sweden, the Riksbank hasunveiled a program to “ensure ample credit supply”. Up to SEK500bn will be lent to banks for a period of2y, at the variable repo rate, conditional on banks increasing the loan stock to the non-financial sector.

What is most important in the week ahead?

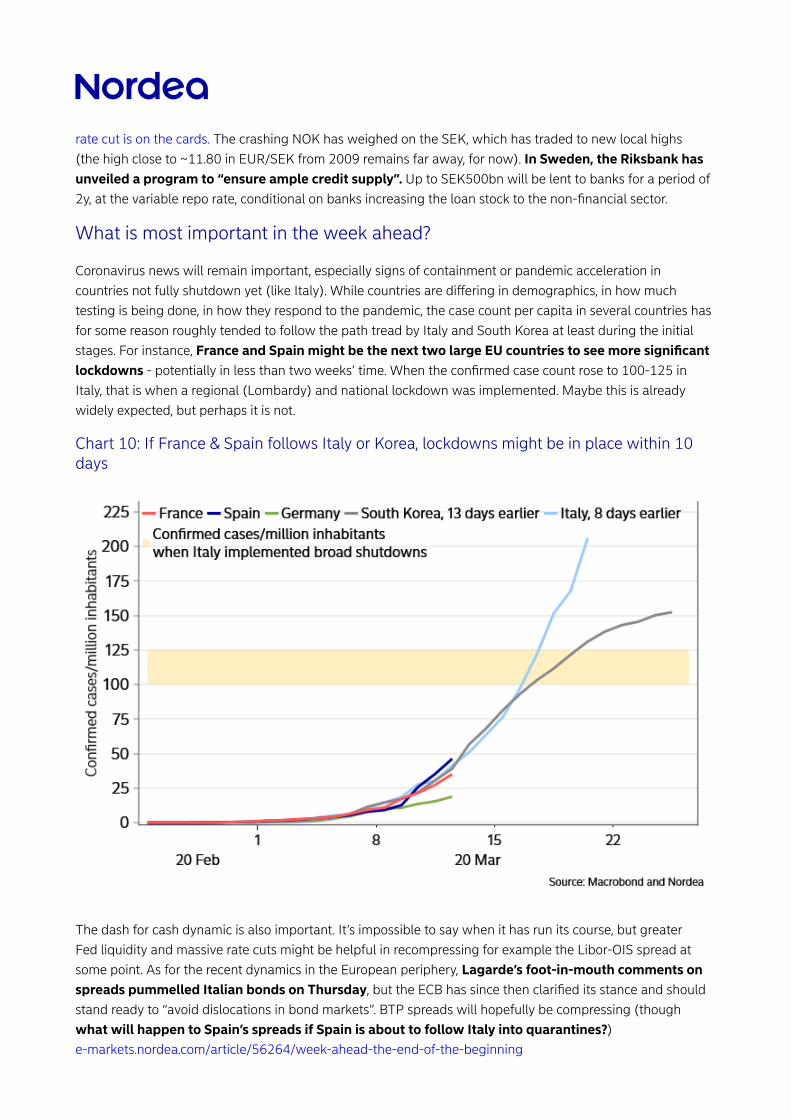

Coronavirus news will remain important, especially signs of containment or pandemic acceleration incountries not fully shutdown yet (like Italy). While countries are diering in demographics, in how muchtesting is being done, in how they respond to the pandemic, the case count per capita in several countries hasfor some reason roughly tended to follow the path tread by Italy and South Korea at least during the initialstages. For instance, France and Spain might be the next two large EU countries to see more significantlockdowns - potentially in less than two weeks’ time. When the confirmed case count rose to 100-125 inItaly, that is when a regional (Lombardy) and national lockdown was implemented. Maybe this is alreadywidely expected, but perhaps it is not.

Chart 10: If France & Spain follows Italy or Korea, lockdowns might be in place within 10days

The dash for cash dynamic is also important. It’s impossible to say when it has run its course, but greaterFed liquidity and massive rate cuts might be helpful in recompressing for example the Libor-OIS spread atsome point. As for the recent dynamics in the European periphery, Lagarde’s foot-in-mouth comments onspreads pummelled Italian bonds on Thursday, but the ECB has since then clarified its stance and shouldstand ready to “avoid dislocations in bond markets”. BTP spreads will hopefully be compressing (thoughwhat will happen to Spain’s spreads if Spain is about to follow Italy into quarantines?)e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

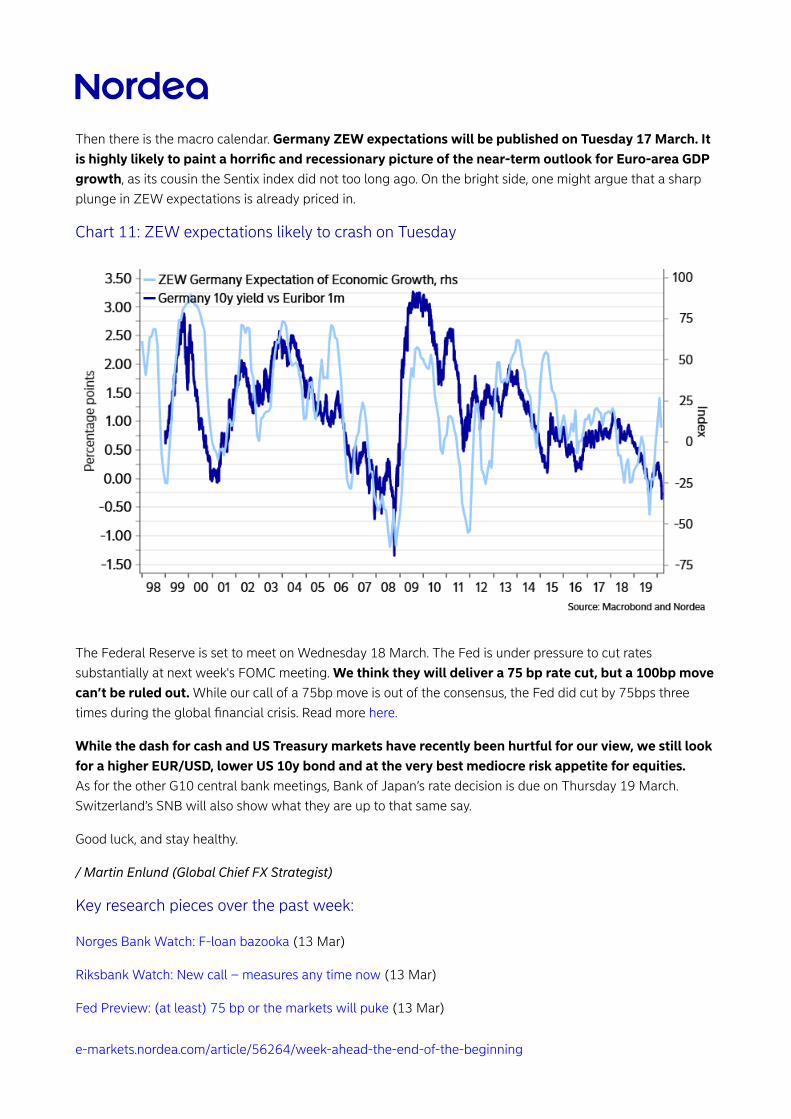

Then there is the macro calendar. Germany ZEW expectations will be published on Tuesday 17 March. Itis highly likely to paint a horrific and recessionary picture of the near-term outlook for Euro-area GDPgrowth, as its cousin the Sentix index did not too long ago. On the bright side, one might argue that a sharpplunge in ZEW expectations is already priced in.

Chart 11: ZEW expectations likely to crash on Tuesday

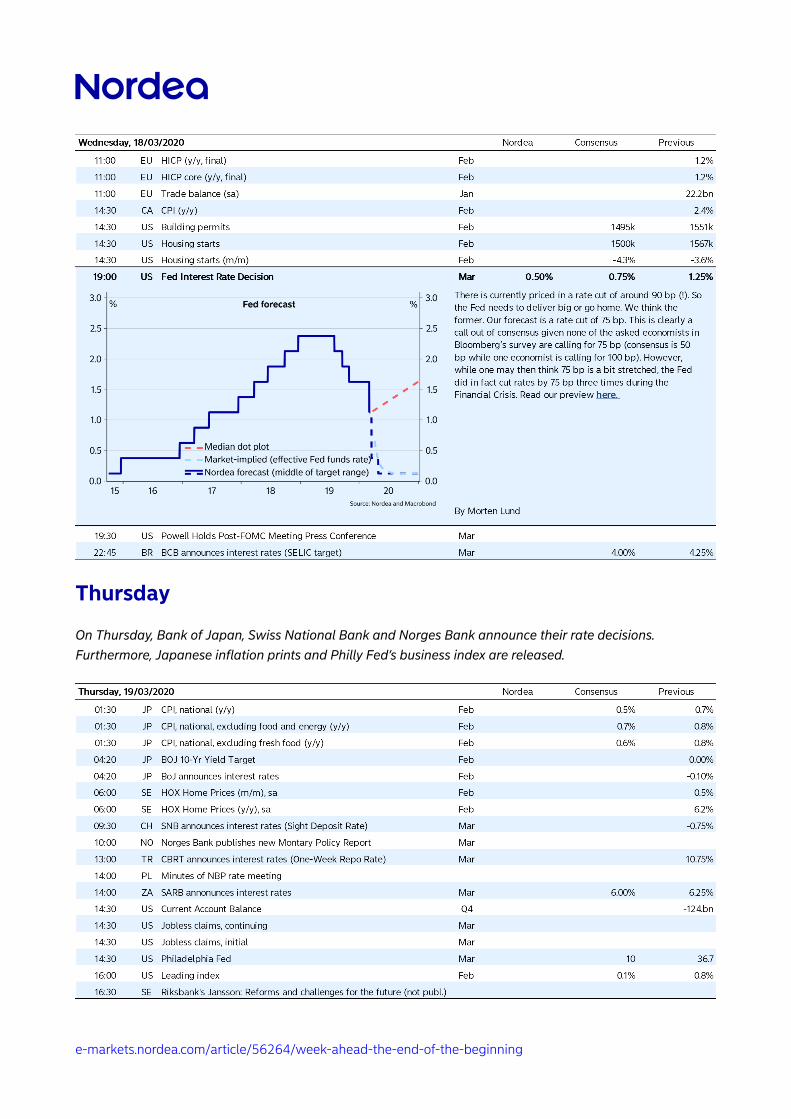

The Federal Reserve is set to meet on Wednesday 18 March. The Fed is under pressure to cut ratessubstantially at next week's FOMC meeting. We think they will deliver a 75 bp rate cut, but a 100bp movecan’t be ruled out. While our call of a 75bp move is out of the consensus, the Fed did cut by 75bps threetimes during the global financial crisis. Read more here.

While the dash for cash and US Treasury markets have recently been hurtful for our view, we still lookfor a higher EUR/USD, lower US 10y bond and at the very best mediocre risk appetite for equities.As for the other G10 central bank meetings, Bank of Japan’s rate decision is due on Thursday 19 March.Switzerland’s SNB will also show what they are up to that same say.

Good luck, and stay healthy.

/ Martin Enlund (Global Chief FX Strategist)

Key research pieces over the past week:

Norges Bank Watch: F-loan bazooka (13 Mar)

Riksbank Watch: New call – measures any time now (13 Mar)

Fed Preview: (at least) 75 bp or the markets will puke (13 Mar)

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

ECB Watch: Targeted measures on temporary problems (12 Mar)

Denmark's lockdown (12 Mar)

Global consequences of the coronavirus outbreak (12 Mar)

No negative interest rates in Norway (12 Mar)

Could the ECB hike the tiering multiplier? (11 Mar)

Major forecasts update: Ground zero (10 Mar)

Global markets: Trying to make sense of the seemingly senseless (9 Mar)

FX weekly: A great big bucket of bummerballs (8 Mar)

Monday

The week starts o with industrial output data for China in the morning and the NY Fed manufacturingactivity index in the evening.

Tuesday

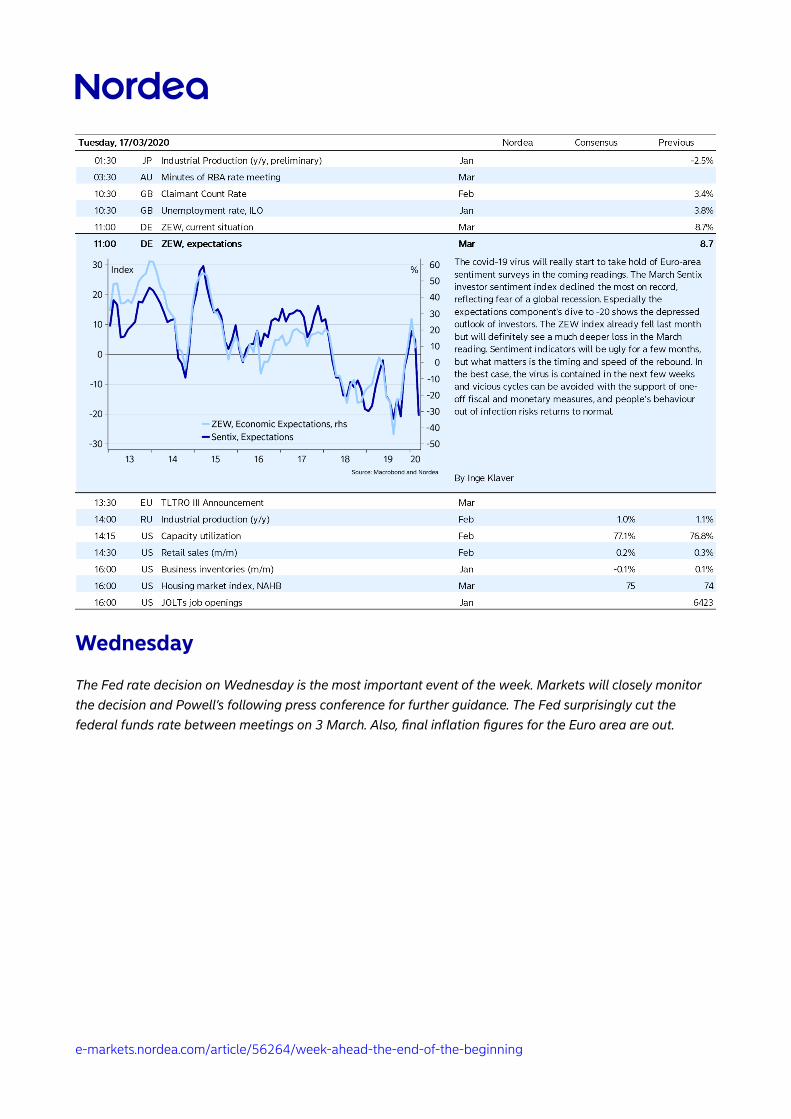

Tuesday’s main events are the UK job report and the ZEW sentiment index for Germany and the Euro area. Inthe US, the latest retail sales print and industrial production figures are published.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

Wednesday

The Fed rate decision on Wednesday is the most important event of the week. Markets will closely monitorthe decision and Powell’s following press conference for further guidance. The Fed surprisingly cut thefederal funds rate between meetings on 3 March. Also, final inflation figures for the Euro area are out.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

Thursday

On Thursday, Bank of Japan, Swiss National Bank and Norges Bank announce their rate decisions.Furthermore, Japanese inflation prints and Philly Fed’s business index are released.

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning

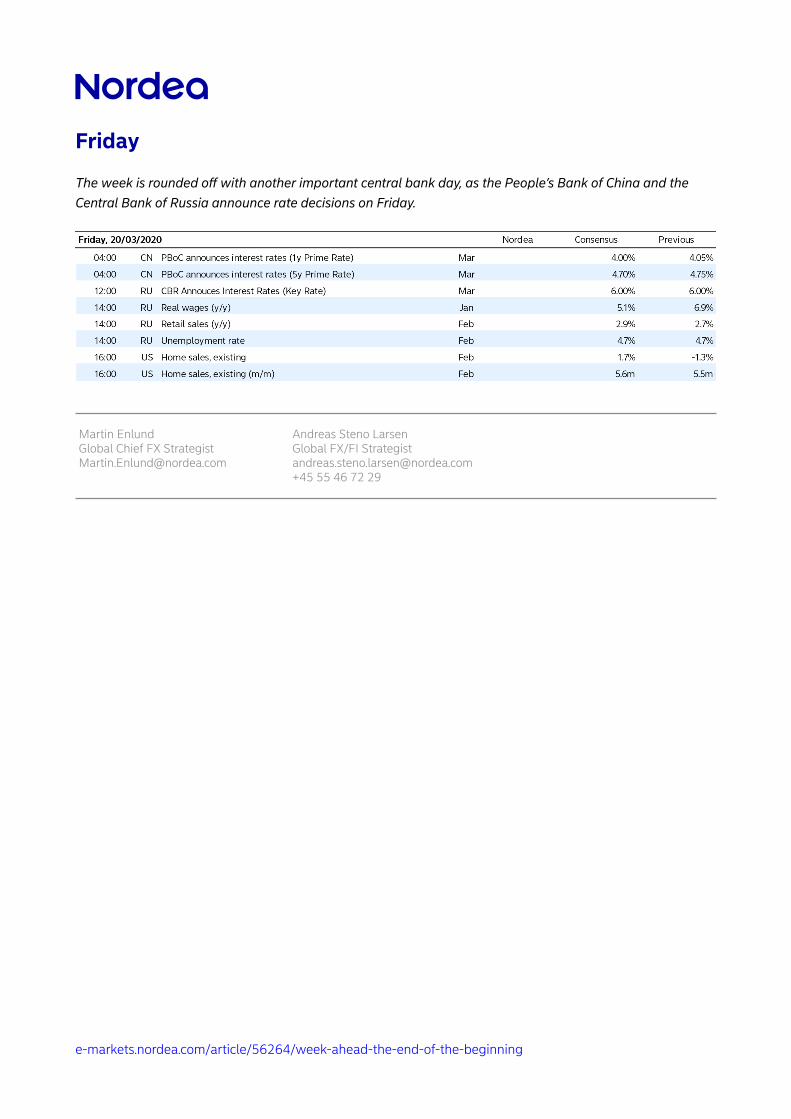

Friday

The week is rounded o with another important central bank day, as the People’s Bank of China and theCentral Bank of Russia announce rate decisions on Friday.

Martin EnlundGlobal Chief FX [email protected]

Andreas Steno LarsenGlobal FX/FI [email protected]+45 55 46 72 29

e-markets.nordea.com/article/56264/week-ahead-the-end-of-the-beginning