w6 singeqcoint l

DESCRIPTION

Cointegration is an common phenomena in time series data. The material is about some testing procedure for cointegration, namely Augumented Dicky Fuller Test, ARS test.TRANSCRIPT

ECON3350/7350COINTEGRATION

Alicia N. Rambaldi

Week 6

1 / 28

In this lecture

Readings

IntroductionSpurious Regression vs Cointegration

Spurious Regression

CointegrationIntroduction to CointegrationDefinition of CointegrationCointegration OrderExampleTesting for CointegrationProperties of the OLS estimator in the case of cointegration.Testing the cointegration spaceNon-Uniqueness of �

Coming Up

2 / 28

Reference Materials

Author Title Chapter Call No

Enders, W AppliedEconometricTime Series,

3e

6.1-6.2

HB139 .E552015

Verbeek, M A Guide toModern

Econometrics

9.2,9.3 HB139.V465 2012

3 / 28

Spurious Regression vs Cointegration

I What are the implications for empirical economic research ofhaving I(1) variables?

I Spurious Regressions or CointegrationIt is generally true that any combination of two I (1) variableswill also be I (1).

I Spurious RegressionI Conclude there is a significant relationship when there is none.

I CointegrationI Linear combinations of I (1) variables are I (0).

4 / 28

Spurious Regression

I Assume xt

= xt�1

+ ✏x ,t and y

t

= yt�1

+ ✏y ,t where ✏

x ,t and✏y ,t are independent white noise.

I Clearly there is no relationship between xt

and yt

.I If we do not know the above and wish to ’test’ for a

relationship between xt

and yt

, we would normally estimate

yt

= ↵̂+ �̂xt

+ et

I and use a t � test to test

H0 : � = 0 against H1 : � 6= 0

If xt

and yt

were I (0), �̂ would be approximately Normal, twould be approximately Student � t or at leastT

12

⇣�̂ � �

⌘! N(0,V ).

5 / 28

Spurious Regression (cont.)

I But as xt

and yt

are I (1), the distribution of �̂ is moredisperse than Normal and the distribution of t is more dispersethat Student�t.

P(|t| > 1.96) = P(Rejected H0

) > 0.05

I Implications: Tend to reject H0

too oftenI What happens as T ! 1?

I Things get worse and there is no well defined asymptoticdistribution to which �̂ converges:

T12 (�̂ � �) ! 1 and P(|t| > 1.96) increases

6 / 28

Spurious Regression (cont.)

I Indications of a Spurious regression:Signicant t � values; Respectable (sometimes high) R2; lowDurbin-Watson (DW) statistics.

I The signicant t - values occur because the random walks tendto wander, and this wandering looks like a trend.

I If they wander in the same direction for a while (say for thetime of the observed sample), there appears to be arelationship.

I In:I y

t

= ↵+ �xt

+ ✏t

; ✏t

⇠ I (1) so the regression is meaningless.I This explains why DW is low.

7 / 28

Cointegration

I Recall the concept of the stochastic trend

st

= st�1

+ ⌘t

where ⌘t

⇠ I (0)

Any linear combination of st

will be I (1).I Thus if

xt

= ast

+ ⌫x ,t where ⌫

x ,t ⇠ I (0) then xt

⇠ I (1)

8 / 28

Common Stochastic TrendI How can two I (1) variables combine to form an I (0) variable?

I Recall

xt

= ast

+ ⌫x ,t where ⌫

x ,t ⇠ I (0) so xt

⇠ I (1)I Now assume

yt

= st

+ ⌫y ,t where ⌫

y ,t ⇠ I (0) so yt

⇠ I (1)I Then

xt

� ayt

= (ast

+ ⌫x ,t)� a(s

t

+ ⌫y ,t)

= ast

+ ⌫x ,t � as

t

� a⌫y ,t

= ⌫x ,t � a⌫

y ,t which is I (0)

I This is a case of cointegration.I The variables share a common stochastic trend: s

t

.9 / 28

Cointegration and Equilibrium

I The economic interpretation and signicance of cointegrationI We may regard the cointegrating relation

zt

= xt

� ayt

as a stable equilibrium relation.I Although x

t

and yt

are themselves unstable as they are I (1),they are attracted to a stable relationship that exists betweenthem, z

t

⇠ I (0).I For example, there is strong evidence that interest rates are

I (1). But the spread between two rates of different maturities,within the same market, appear to be I (0).

10 / 28

Common Stochastic TrendExample

CWTB3Y: Augmented Dickey-Fuller test statistic -1.253373, p-value (0.6433)

CWTB5Y: Augmented Dickey-Fuller test statistic -1.199108, p-value(0.6673)

SPREAD: Is it I (0)? We return to this question.

The expectations theory of the term structure of interest rateswould suggest that if the interest rates themselves are I (1), thespread between rates of different maturity will be I (0) (Campbelland Shiller,1991).

11 / 28

Definition of Cointegration

I It is possible for a cointegrating relation to involve manyvariables. That is, w

t

may be a (n ⇥ 1) vector. Also wt

maybe integrated of order d .

I A more formal definition of cointegration (Engle & Granger,1987):

Definition

The components of the vector wt

are said to be cointegrated oforder d , b, denoted CI (d , b), if(i) all components of w

t

are I (d),(ii) there exists a vector (� 6= 0) so that

zt

= �0wt

⇠ I (d � b), b > 0

The vector � is called the cointegrating vector.

12 / 28

Cointegration OrderI If w

t

= (w1,t ,w2,t , ...,wn,t)0 ⇠ I (1) but

w 0t

� ⇠ I (0)

I where

�0wt

= w1,t�1 + w2,t�2 + ...wn,t�n

= (�1,�2, ...,�n

)0

0

BBB@

w1,tw2,t

...wn,t

1

CCCA

I Then we say that components of the vector wt

arecointegrated of order 1, 1, denoted CI (1, 1).

I In our simple example above,

wt

=

✓xt

yt

◆and � =

✓1�a

◆

I because xt

� ayt

⇠ I (0).13 / 28

Example

King, R.G., C.I. Plosser, J.H. Stock, and M.W. Watson (1991)."Stochastic trends and economic fluctuations." The American

Economic Review, 81,819-840.

Yt

= �t

K ✓t

L1�✓t

yt

= ln(�t

) + ✓kt

+ (1 � ✓)lt

ln(�t

) = ln(�t�1

) + ✏t

Income = f (Capital , Labour) with technology/productivity shocks�t

14 / 28

Example

(cont.)The economy’s resource constraint implies that output is eitherconsumed or invested, Y

t

= Ct

+ It

, and with common stochastic

trends (�t

) the ratiosCt

Yt

andIt

Yt

(the Great Ratios) are stable.

Therefore, in logs, ct

� yt

and it

� yt

must be I (0) and ct

, yt

, andit

are I (1) but cointegrate.That is

�0wt

=

✓1 0 b

1

0 1 b2

◆0

@ct

it

yt

1

A =

✓ct

+ b1

yt

it

+ b2

yt

◆⇠ I (0)

We also know from the theory that we can restrict b1

= �1 andb2

= �1.

15 / 28

Testing for Cointegration

I Recall that if a vector of I (1) variables do not cointegrate,then no combination of them will be I (0). However, if a vectorof I (1) variables DO cointegrate, then there is a combinationof them that will be I (0).

I Simple solution: to test for cointegration.I Consider the case of three variables: x

t

, yt

, and zt

I Estimate: xt

= ↵̂+ �̂1yt + �̂2zt + et

(by OLS)I Test the residual, e

t

, for a unit root. If et

⇠ I (0), thenxt

, yt

, and zt

cointegrate.

I There are a number of ways we could perform this test. Wewill look at using the Dickey-Fuller test statistic and theDurbin-Watson statistic.

16 / 28

Testing for Cointegration (cont.)

I Because the residual et

comes from a potential cointegratingrelation, the test statistics will not have the usual distributionsso we cannot use the same critical values.

I In both tests we assume et

= ⇢et�1

+ ⌫t

(⌫t

is WN) and testH

0

: ⇢ = 1.I The Augmented Dickey-Fuller test to test for cointegration.

We proceed as usual but use critical values from Table C inEnders.

I The Durbin-Watson test to test for cointegration (CRDW).We proceed as usual but use critical values from Table 9.3 inVerbeek.

17 / 28

Example

Expectations theory of the term structure of interest rates impliesthe following empirically testable feature

If i3y ,t ⇠ I (1) then i

5y ,t ⇠ I (1) and i5y ,t � i

3y ,t ⇠ I (0)

I That is, the long and short interest rates will cointegrateI We had computed:

i3y ,t : Augmented Dickey-Fuller test statistic -1.253373, p-value (0.6433)i5y ,t : Augmented Dickey-Fuller test statistic -1.199108, p-value(0.6673)Thus, they are I (1)

I i5y ,t � i

3y ,t

I H0 : et

= i5y ,t � i3y ,t ⇠ I (1) ,I That is, the long and short interest rates will cointegrate and

we know the cointegrating relation is � = (1,�1).

18 / 28

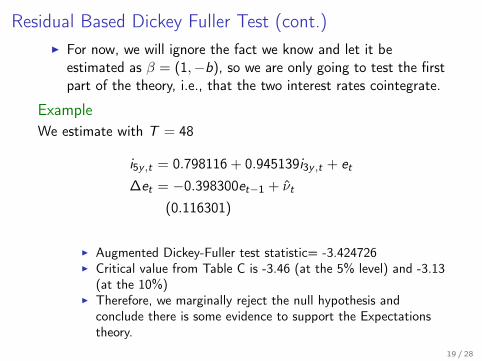

Residual Based Dickey Fuller Test (cont.)I For now, we will ignore the fact we know and let it be

estimated as � = (1,�b), so we are only going to test the firstpart of the theory, i.e., that the two interest rates cointegrate.

Example

We estimate with T = 48

i5y ,t = 0.798116 + 0.945139i

3y ,t + et

�et

= �0.398300et�1

+ ⌫̂t

(0.116301)

I Augmented Dickey-Fuller test statistic= -3.424726I Critical value from Table C is -3.46 (at the 5% level) and -3.13

(at the 10%)I Therefore, we marginally reject the null hypothesis and

conclude there is some evidence to support the Expectationstheory.

19 / 28

Residual Based CRDW

I If the first order autocorrelation is one (⇢ = 1) then theDW ! 0. Thus, the DW of the cointegrating regression goesto zero under the null hypothesis

Example

We estimate with T = 48

i5y ,t = 0.798116 + 0.945139i

3y ,t + et

DW = CRDW = 1.654472

I At the 5% the critical value (Table 9.3 in Verbeek) is 0.72 andthus we reject H

0

: et

⇠ I (1) and conclude there is evidence forthe Expectations theory of the term structure of interest rates.

20 / 28

Properties of the OLS estimator in the case of cointegrationI The OLS estimator �̂ = (↵̂, �̂

1

, �̂2

)0.I In the case of cointegration, the OLS estimator of � will be

superconsistent.I That is, although normal OLS estimates converge to N(0,V )

at the rate T12 , the OLS estimate of a cointegrating vector

converges at the rate T .

I Normally,

⇣�̂ � �

⌘! 0 and T

12

⇣�̂ � �

⌘! N(0,V )

I With cointegration

⇣�̂ � �

⌘! 0 and T

12

⇣�̂ � �

⌘! 0

T⇣�̂ � �

⌘! N(0,V )

21 / 28

Testing the cointegrating space when there is onecointegrating vector

Recall that the Expectations theory of the term structure of interestrates implied

i3y ,t ⇠ I (1) then i

5y ,t ⇠ I (1) and i5y ,t � i

3y ,t ⇠ I (0)

Put another way, if i3y ,t ⇠ I (1) then i

5y ,t ⇠ I (1) because theyshare a common stochastic trend AND the cointegrating vector forthe cointegrating relation is � = (1,�1)0.

I Thus we can test the evidence in support of this theory bysimply calculating z

t

= i5y ,t � i

3y ,t and then testing zt

⇠ I (0)with a simple ADF.

I If we Reject the null hypothesis of a unit root in zt

, then ifi5y ,t ⇠ I (1), then it must hold that i

3y ,t ⇠ I (1) because theyshare a common stochastic trend and the cointegrating vectoris � = (1,�1)0

22 / 28

Testing the more explicit economic theories

Assume wt

=

0

@ct

yt

at

1

Aconsumption

incomewealth (assets)

I If we have a theory that says the cointegrating space is completelyknown, e.g., � = (1,�1,�1)0 say, then we can test the evidence insupport of this theory by constructing the variable z

t

= �0wt

anddoing a test for z

t

⇠ I (1) against zt

⇠ I (0).

Examples

Permanent income hypothesis says

zt

= ct

-yt

= ( 1 �1 )

✓ct

yt

◆⇠ I (0).

I To test this we test for stationarity of zt

(with a simple ADF test).If there is evidence of any form of nonstationarity then this can betaken as evidence against the theory.

23 / 28

The cointegrating space is partially known

I Let the income consumption relation respond to levels ofwealth, e.g., � = (1,�1,�b)0 say, then

I We can test the evidence in support of this theory by

constructing the variable z1,t = (1,�1)0

✓ct

yt

◆= c

t

� yt

and

regressing z1,t on a

t

.

z1,t = µ̂+ b̂a

t

+ et

I Then test for stationarity of et

. If using ADF, useCointegrating ADF statistics with, in this case, two variables.-Table C Enders.

I Note that µ̂ can be interpreted as the mean of the error

correction term zt

.

24 / 28

Non-Uniqueness of �

Recall cointegration with stochastic trend st

where wt

= (xt

, yt

)0

xt

= ast

+ ⌫x ,t where ⌫

x ,t ⇠ I (0) so xt

⇠ I (1) andyt

= st

+ ⌫y ,t where ⌫

y ,t ⇠ I (0) so yt

⇠ I (1)

Then,

�0wt

= (1,�a)0✓

xt

yt

◆

= xt

� ayt

= ⌫x ,t � a⌫

y ,t which is I (0)

Here � = (1,�a)0 because this combination cancelled thestochastic trends.

25 / 28

Non-Uniqueness of � (cont.)

I However,I if 2� = (2,�2a)0 or � = (1,�a)0 for any kappa 6= 0 will also

work as �0wt

⇠ I (0).

�0wt

= (2,�2a)0✓

xt

yt

◆

= 2(xt

� ayt

)

= 2(⌫x ,t � a⌫

y ,t) which is I (0)

I Thus we normalise, � = (1,�a)0 to make � unique.

26 / 28

Example

in the Real Business Cycle model with Balanced Growth Hypthesis(King et al.,1991) we had three variables (c

t

, it

, yt

) and onecommon stochastic trend - productivity shocks.

I Thus, there are n = 3 variables, and n � r = 1 commonstochastic trends. Therefore, r = 2, cointegrating vectors:

� =

2

41 00 1b1

b2

3

5

I Although much emphasis is placed upon estimating thecointegrating vectors, except where r = 1, these vectors arenot interpretable as they are not unique.

I What is unique is the cointegrating space. The cointegratingvectors span (lie in) the cointegrating space.

27 / 28

Coming Up

ARCH, GARCH, Stochastic Volatility and Realised volatility. Testsfor ’ARCH-type’ errors and model identification.

28 / 28