updates on the automotive industry on the automotive industry • pwc automotive pwc autofacts ® in...

TRANSCRIPT

Updates on the Automotive IndustryPwC Automotive

www.pwc.com

7. June 2017

Automotive Logistics 2017

PwC

7. June 2017

Transformation of the automotive industry

2

Updates on the Automotive Industry • PwC Automotive

PwC Autofacts ®

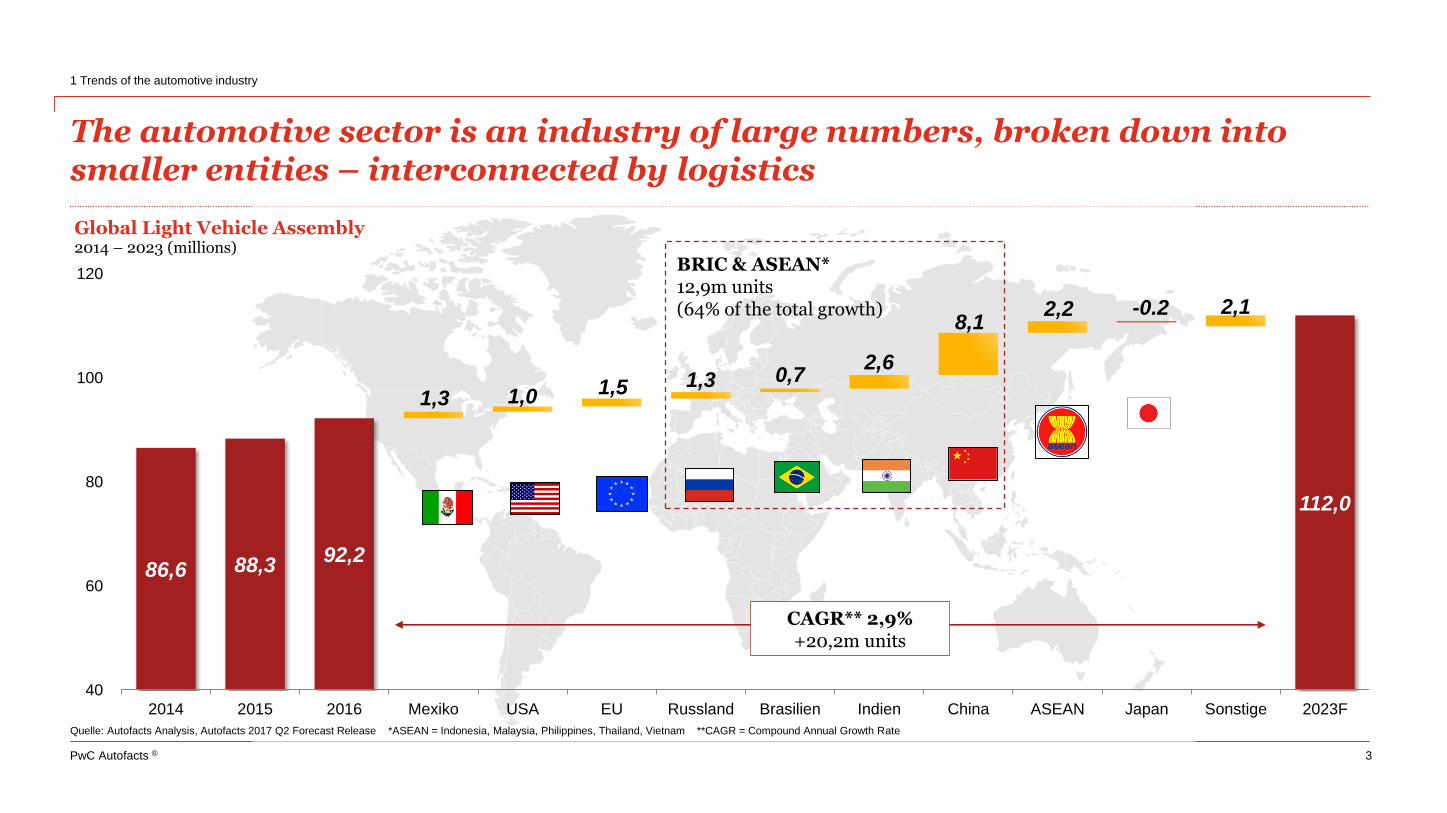

CAGR** 2,9%+20,2m units

BRIC & ASEAN*12,9m units (64% of the total growth)

Quelle: Autofacts Analysis, Autofacts 2017 Q2 Forecast Release *ASEAN = Indonesia, Malaysia, Philippines, Thailand, Vietnam **CAGR = Compound Annual Growth Rate

The automotive sector is an industry of large numbers, broken down into smaller entities – interconnected by logistics

1 Trends of the automotive industry

3

86,6 88,392,2

112,0

1,3 1,0 1,5 1,3 0,72,6

8,12,2 -0.2 2,1

40

60

80

100

120

2014 2015 2016 Mexiko USA EU Russland Brasilien Indien China ASEAN Japan Sonstige 2023F

Global Light Vehicle Assembly2014 – 2023 (millions)

PwC Autofacts ®

electrified

autonomous

shared

connected

yearly updated

The vision is clear: The car of the future is “eascy”

1 Trends of the automotive industry

4

Picture source: Volkswagen

PwC Autofacts ®

Numerous challenges mark the way to the future of the global economy and of the global automotive industry - mobility and welfare are connected

1 Trends of the automotive industry

5

Protectionism Political instability

Environmental factors Industry transformation

• Brexit – Reorganization of the relations between the UK and global markets

• USA – possible protectionism of the American economy against other countries in consequence of the political changes since 2017

• Emissions – political initiatives which should reduce smog in urban areas

• CO2-targets – uncertain transformation path to ecofriendly powertrain concepts

• Migration streams – lead to a global growing number of refugees and emigrants

• Long-term consequences– are currently not foreseeable, but they could result in changes of economic growth

• Changed consumer behavior –especially for younger customers and as a result of a progressing digitalization

• Business model transformation –Future business models are currently developed and tested

PwC

7. June 2017

Europe sales updates

6

Updates on the Automotive Industry • PwC Automotive

PwC Autofacts ®

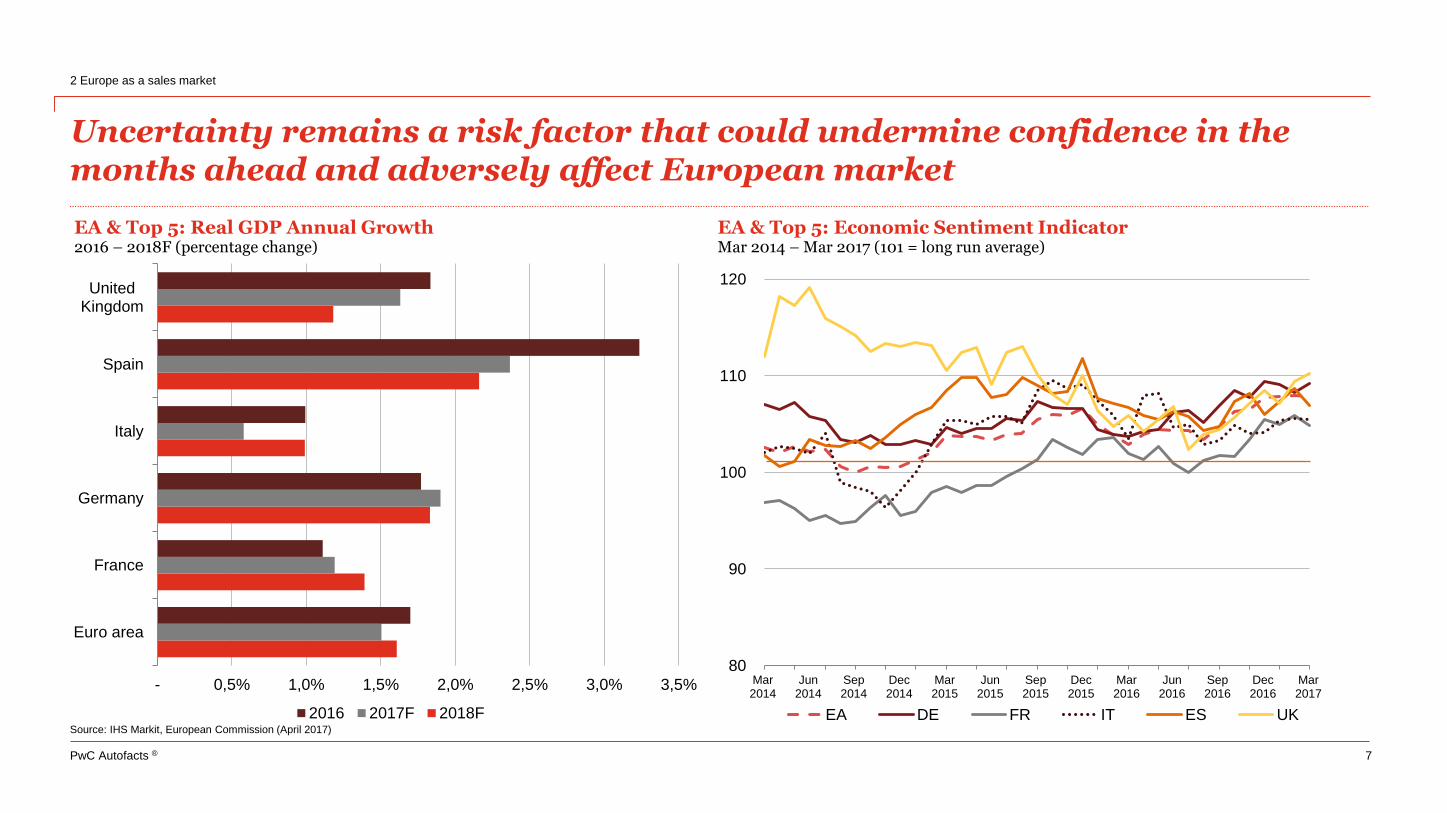

Uncertainty remains a risk factor that could undermine confidence in the months ahead and adversely affect European market

2 Europe as a sales market

7

- 0,5% 1,0% 1,5% 2,0% 2,5% 3,0% 3,5%

Euro area

France

Germany

Italy

Spain

UnitedKingdom

EA & Top 5: Real GDP Annual Growth2016 – 2018F (percentage change)

2016 2017F 2018F

80

90

100

110

120

Mar2014

Jun2014

Sep2014

Dec2014

Mar2015

Jun2015

Sep2015

Dec2015

Mar2016

Jun2016

Sep2016

Dec2016

Mar2017

EA & Top 5: Economic Sentiment IndicatorMar 2014 – Mar 2017 (101 = long run average)

EA DE FR IT ES UKSource: IHS Markit, European Commission (April 2017)

PwC Autofacts ®

Europe’s new passenger car market maintains positive momentum in Q1 and still holds significant structural upside potential

2 Europe as a sales market

8

0

1

2

3

4

5

Germany France UnitedKingdom

Italy Spain Poland CzechRepublic

EU+EFTA: New Car Registration Variance1990 – 2017F (millions)

Source: ACEA, Autofacts Analysis

2016

28-year high

(1990-2017)

28-year low

(1990-2017)

2017F

10

11

12

13

14

15

16

17

Mar2008

Mar2009

Mar2010

Mar2011

Mar2012

Mar2013

Mar2014

Mar2015

Mar2016

Mar2017

EU+EFTA: Rolling 12 Months Car RegistrationsMar 2008 – Mar 2017 (millions)

Rolling 12-Month Car Registrations Annual Registrations

PwC Autofacts ®

Autofacts expects light vehicle registrations to grow by +3.8% to 17.8m in 2017 – with a perspective to higher sales driven by legislation impacts

2 Europe as a sales market

9

Source: ACEA, Autofacts Analysis

(10%)

(6%)

(2%)

2%

6%

10%

-

5

10

15

20

25

2008 2010 2012 2014 2016 2018F 2020F 2022F

EU+EFTA: New Light Vehicle Registrations 2008 – 2023F (millions)

Car Registrations LCV Registratons YOY Change (R-Axis)

PwC

7. June 2017

Europe as a production location

10

Updates on the Automotive Industry • PwC Automotive

PwC Autofacts ®

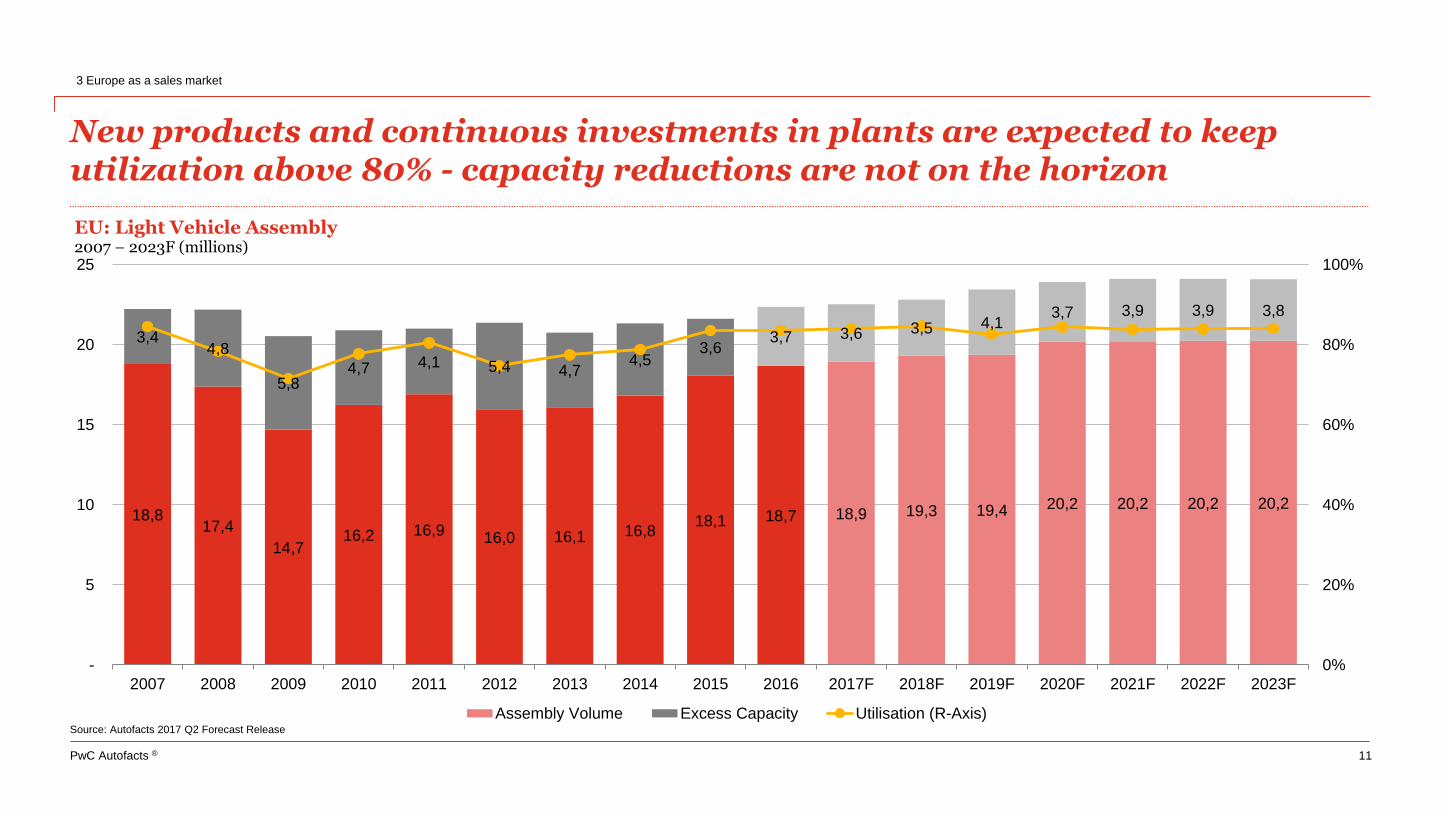

New products and continuous investments in plants are expected to keep utilization above 80% - capacity reductions are not on the horizon

3 Europe as a sales market

11

18,817,4

14,716,2 16,9 16,0 16,1 16,8

18,1 18,7 18,9 19,3 19,4 20,2 20,2 20,2 20,2

3,44,8

5,84,7 4,1 5,4 4,7

4,53,6

3,7 3,6 3,5 4,13,7 3,9 3,9 3,8

0%

20%

40%

60%

80%

100%

-

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F

EU: Light Vehicle Assembly2007 – 2023F (millions)

Assembly Volume Excess Capacity Utilisation (R-Axis)Source: Autofacts 2017 Q2 Forecast Release

PwC Autofacts ®

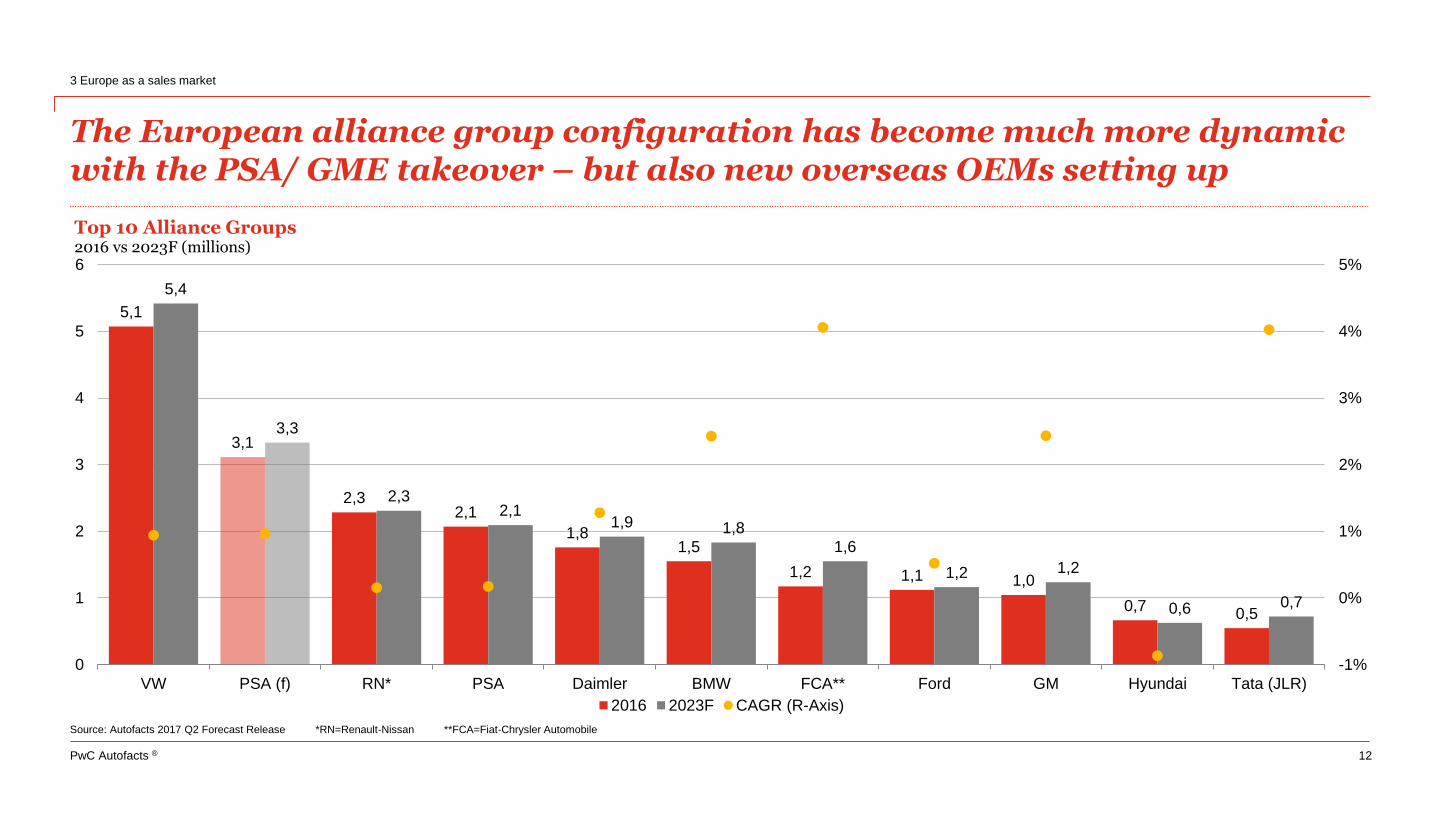

The European alliance group configuration has become much more dynamic with the PSA/ GME takeover – but also new overseas OEMs setting up

3 Europe as a sales market

12

5,1

3,1

2,32,1

1,81,5

1,2 1,1 1,0

0,70,5

5,4

3,3

2,32,1

1,9 1,8

1,6

1,2 1,2

0,6 0,7

-1%

0%

1%

2%

3%

4%

5%

0

1

2

3

4

5

6

VW PSA (f) RN* PSA Daimler BMW FCA** Ford GM Hyundai Tata (JLR)

Top 10 Alliance Groups2016 vs 2023F (millions)

2016 2023F CAGR (R-Axis)

Source: Autofacts 2017 Q2 Forecast Release *RN=Renault-Nissan **FCA=Fiat-Chrysler Automobile

PwC Autofacts ®

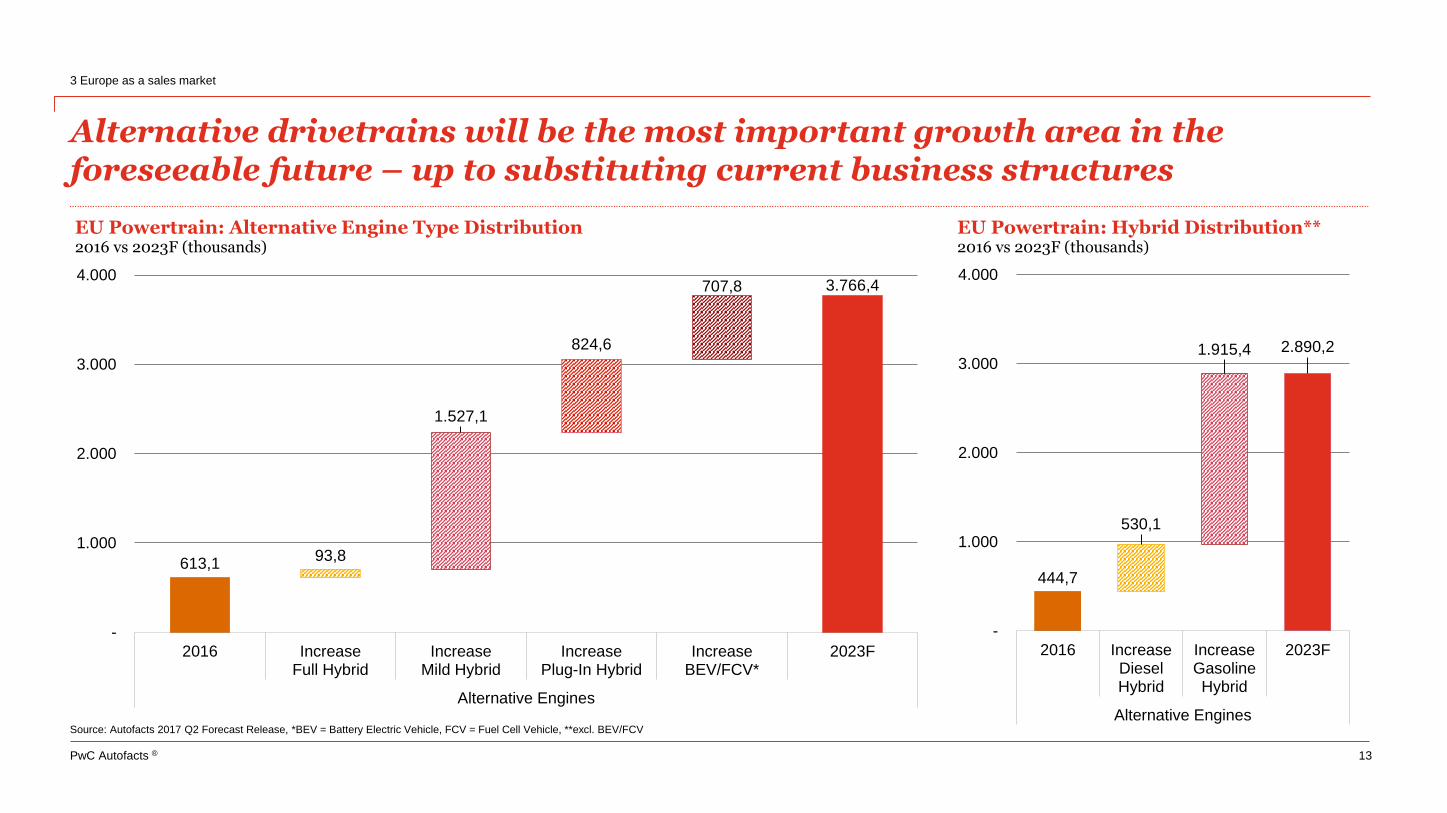

Alternative drivetrains will be the most important growth area in the foreseeable future – up to substituting current business structures

3 Europe as a sales market

13

613,193,8

1.527,1

824,6

707,8 3.766,4

-

1.000

2.000

3.000

4.000

2016 IncreaseFull Hybrid

IncreaseMild Hybrid

IncreasePlug-In Hybrid

IncreaseBEV/FCV*

2023F

Alternative Engines

EU Powertrain: Alternative Engine Type Distribution2016 vs 2023F (thousands)

444,7

530,1

1.915,4 2.890,2

-

1.000

2.000

3.000

4.000

2016 IncreaseDieselHybrid

IncreaseGasolineHybrid

2023F

Alternative Engines

EU Powertrain: Hybrid Distribution**2016 vs 2023F (thousands)

Source: Autofacts 2017 Q2 Forecast Release, *BEV = Battery Electric Vehicle, FCV = Fuel Cell Vehicle, **excl. BEV/FCV

PwC

7. June 2017

Brexit – Whiter Britannia?

14

Updates on the Automotive Industry • PwC Automotive

PwC Autofacts ®

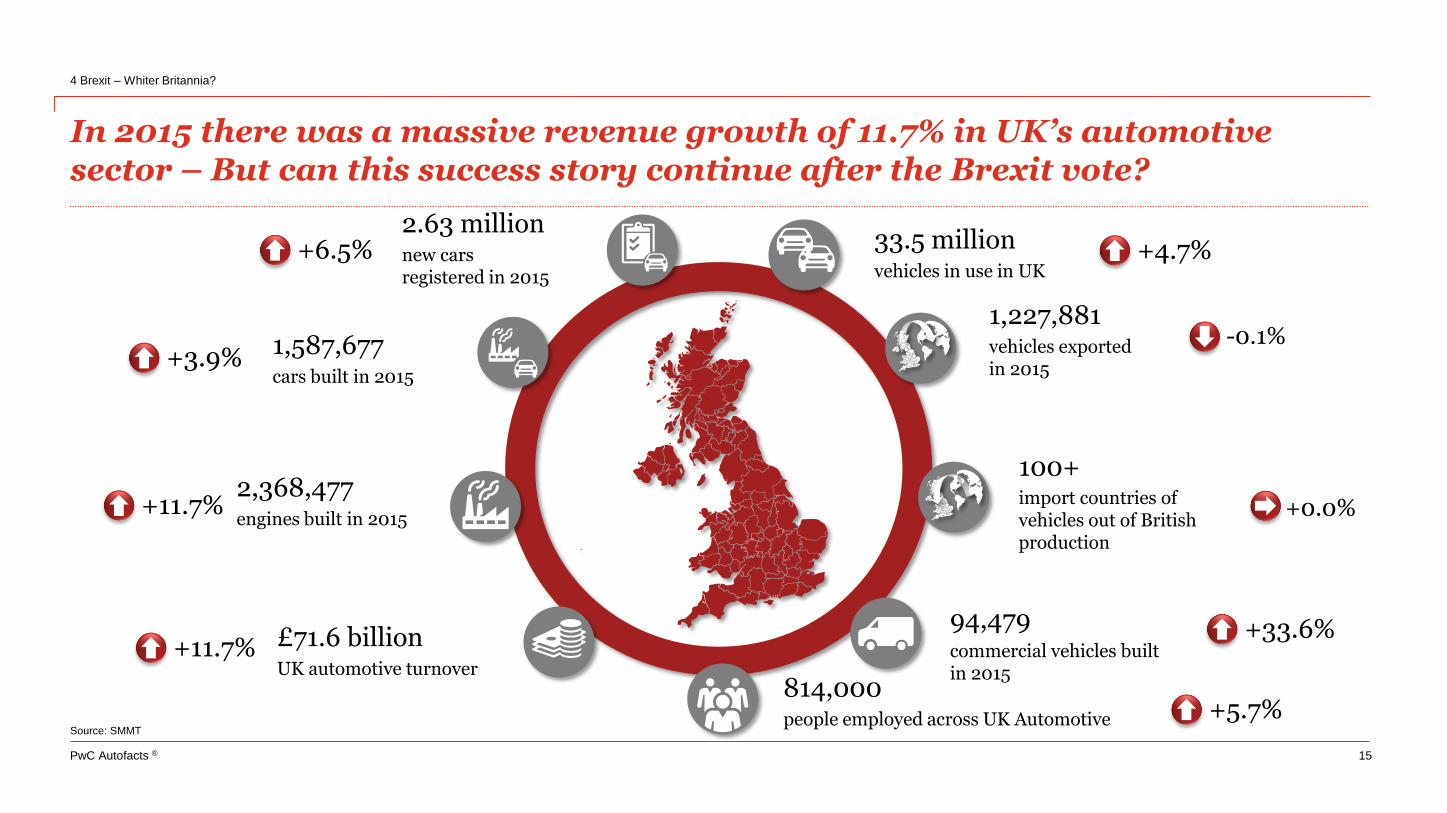

In 2015 there was a massive revenue growth of 11.7% in UK’s automotive sector – But can this success story continue after the Brexit vote?

4 Brexit – Whiter Britannia?

15

Source: SMMT

94,479commercial vehicles built in 2015

2.63 millionnew cars registered in 2015

1,227,881vehicles exportedin 2015

100+import countries of vehicles out of British production

1,587,677cars built in 2015

£71.6 billionUK automotive turnover

814,000people employed across UK Automotive

33.5 millionvehicles in use in UK

2,368,477engines built in 2015

-0.1%

+4.7%

+0.0%

+33.6%

+5.7%

+11.7%

+11.7%

+3.9%

+6.5%

PwC Autofacts ®

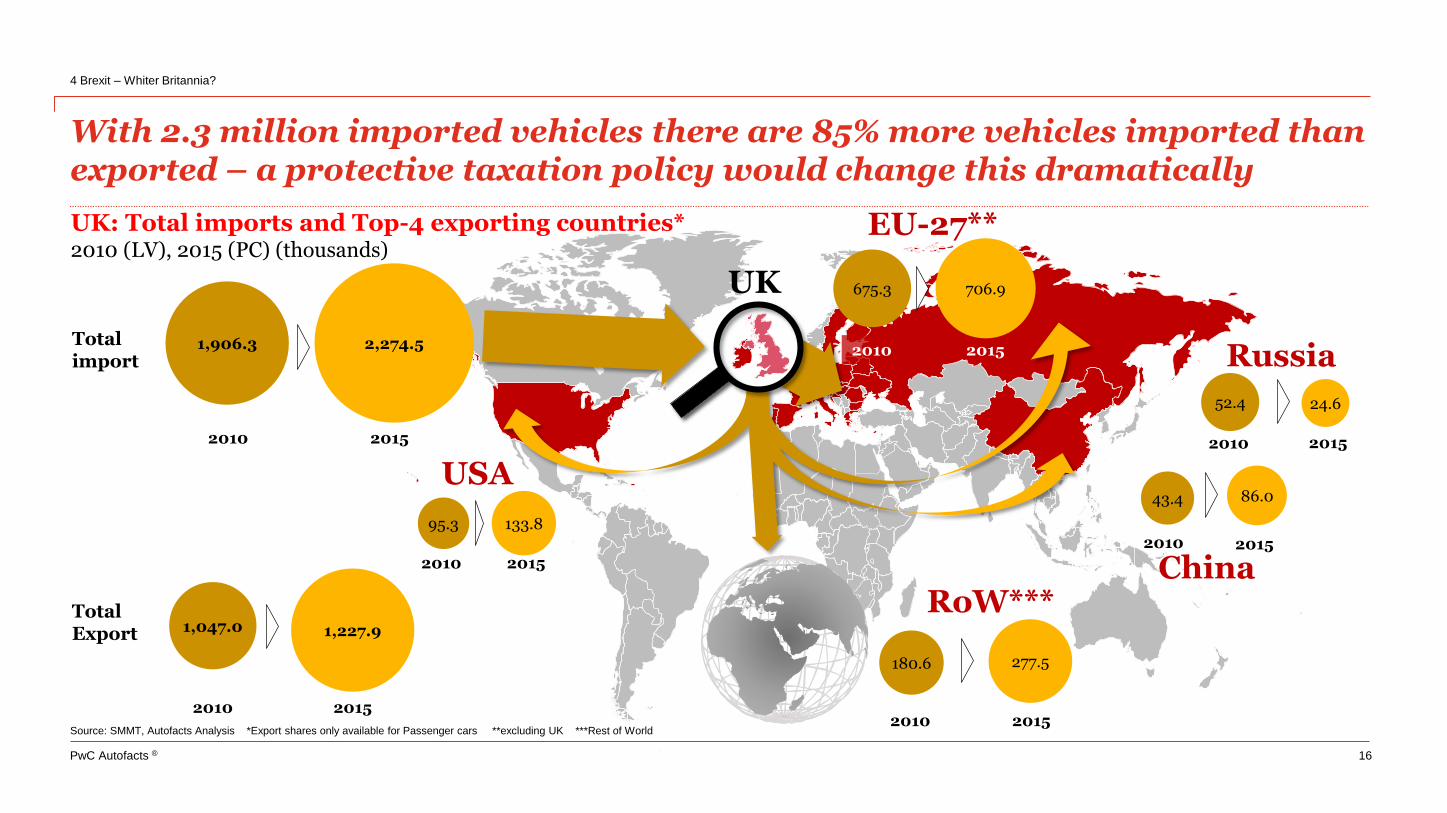

With 2.3 million imported vehicles there are 85% more vehicles imported than exported – a protective taxation policy would change this dramatically

4 Brexit – Whiter Britannia?

16

Source: SMMT, Autofacts Analysis *Export shares only available for Passenger cars **excluding UK ***Rest of World

USA

UK: Total imports and Top-4 exporting countries* 2010 (LV), 2015 (PC) (thousands)

UK

Russia

RoW***

95.3 133.8

2010 2015

TotalExport

Totalimport

2010 2015

1,227.91,047.0

2010 2015

2,274.51,906.3

2010 2015

24.652.4

277.5180.6

2010 2015

2010

China2015

86.043.4

EU-27**

706.9

20152010

675.3

PwC Autofacts ®

2,0

1,6

1,7

1,1

0,5

1,0

1,5

2,0

2,5

2015 2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F

UK: Light vehicle assembly scenarios2015 – 2023 (millions)

In the worst examined case, vehicle production in the United Kingdom would decrease to 1.1 million units by 2023: no FTA and high exchange rate!

4 Brexit – Whiter Britannia?

17

Source: Autofacts 2017 Q2 Forecast Release *Free Trade Agreement

„Turkey Scenario“

„South Korea Scenario“

„Brasil Scenario“

•No FTA* with EU & high exchange rate•Relocation of production capacity to other EU plants

•No investments in R&D•Factory closures

•FTA* with EU & subsidies & low exchange rate •New plants•New R&D investment•New hires

•FTA* with EU & high exchange rate•Most likely under today‘s conditions •Currently planned SOPs take place

PwC Autofacts ®

If decisions were taken today, it would be theoretically possible to shift 2/3 of United Kingdom’s light vehicle assembly volume to the EU by 2020

4 Brexit – Whiter Britannia?

18

Source: Autofacts 2017 Q2 Forecast Release

0,0

0,5

1,0

1,5

2,0

2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F

Effort of assembly shifting to the continent 2016 – 2023 (millions)

No equivalence Equal OEM Equal platform Equal vehicle

UK assembly share

2017 – 2023

49.3%

9.0%

16.9%

24.8%

Transfer to EU from UK

Immediatelyfeasible

Requires plantRefitting (1 years)

BrownfieldSetup (2 years)

GreenfieldSetup (3 years)

Thank you for your attention!

Autofacts®

PwC Autofacts ®

Autofacts contact

20

Christoph StürmerGlobal Lead AnalystPwC Germany (Europe)T: +49 69 9585 6269E: [email protected]

PwC Autofacts ®

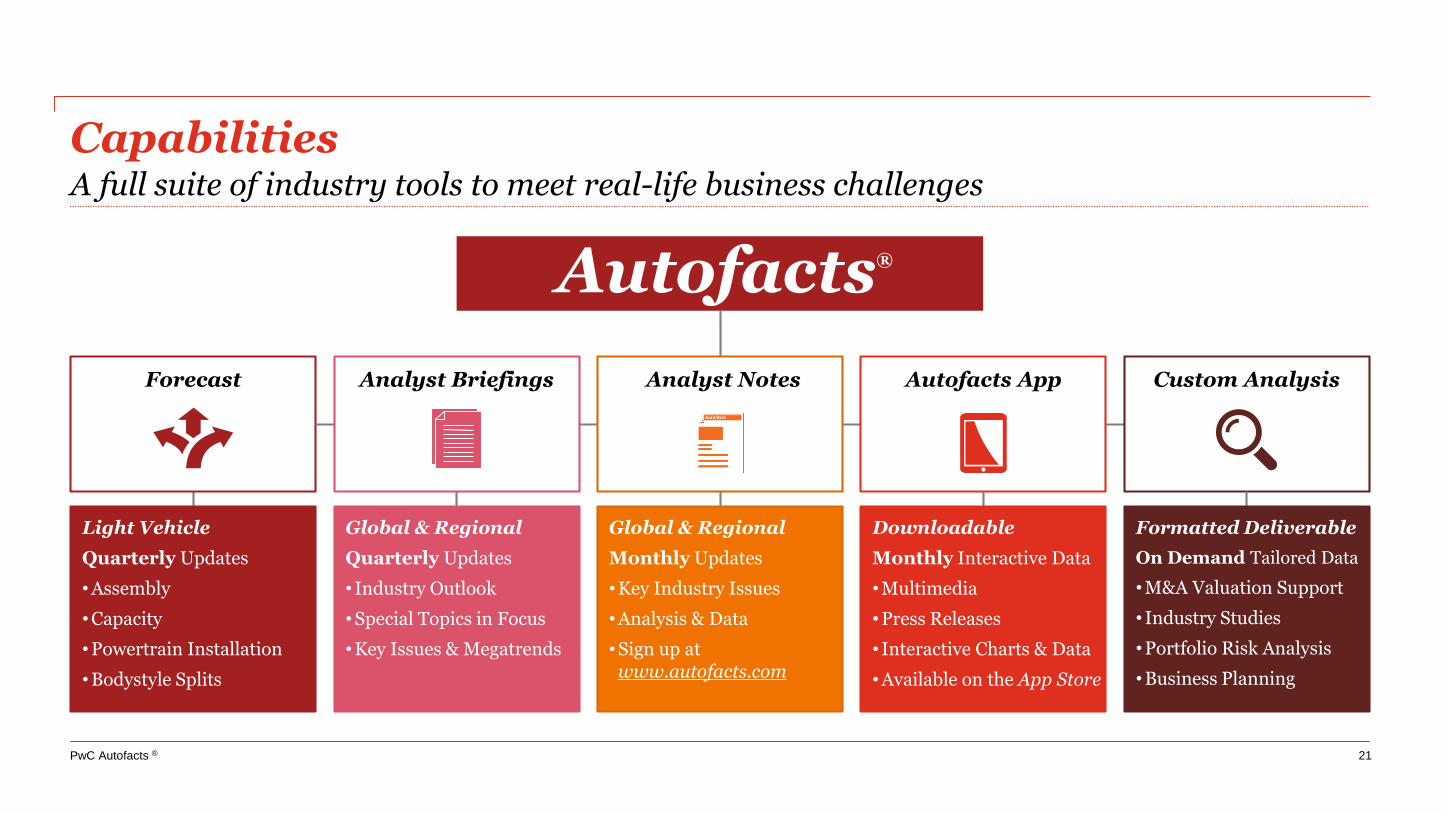

CapabilitiesA full suite of industry tools to meet real-life business challenges

Forecast

Light Vehicle

Quarterly Updates

• Assembly

• Capacity

• Powertrain Installation

• Bodystyle Splits

Analyst Briefings

Global & Regional

Quarterly Updates

• Industry Outlook

• Special Topics in Focus

• Key Issues & Megatrends

Autofacts®

Analyst Notes

Global & Regional

Monthly Updates

• Key Industry Issues

• Analysis & Data

• Sign up at www.autofacts.com

Autofacts App

Downloadable

Monthly Interactive Data

• Multimedia

• Press Releases

• Interactive Charts & Data

• Available on the App Store

Custom Analysis

Formatted Deliverable

On Demand Tailored Data

• M&A Valuation Support

• Industry Studies

• Portfolio Risk Analysis

• Business Planning

21

PwC Autofacts ®

The information contained in this report represents the culmination of proprietary research conducted by Autofacts, an analytical group within PwC. All material contained in this report was developed independently of any

PwC client relationship and does not represent the firm’s view as an auditor to any legal business entity. While every effort has been made to ensure the quality of information provided, no representation or warranty of any

kind (whether expressed or implied) is given by PwC as to the accuracy, completeness or fitness for any purpose of this document. As such, this document does not constitute the giving of investment advice, nor a part of

any advice on investment decisions. Accordingly, regardless of the form of action, whether in contract, tort or otherwise, and to the extent permitted by applicable law, PwC accepts no liability of any kind and disclaims all

responsibility for the consequences of any person acting or refraining from acting in reliance on this document.

©2017 PwC. All rights reserved. “PwC” refers to PricewaterhouseCoopers LLP (a Delaware limited liability partnership) or, as the context requires, other member firms of PricewaterhouseCoopers International Ltd., each of

which is a separate and independent legal entity. “Autofacts” is a globally registered trademark of PwC.

Autofacts®

Autofacts® – Dedicated to the Automotive Industry

22