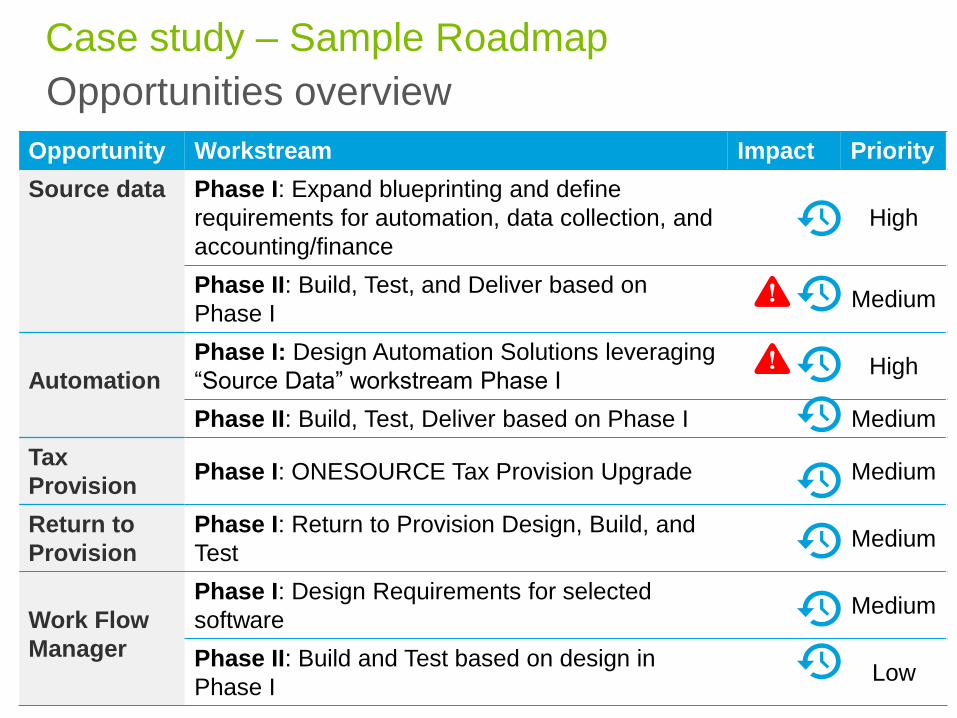

transform today for the challenges of tomorrow plenary

TRANSCRIPT

Transform today for

the challenges of

tomorrow

Plenary

Maison de L’automobile15 December 2015

Andre Claes – Partner, Deloitte BelgiumMark Kennedy – Partner, Deloitte UKPatrick Joucken – Partner, Deloitte Belgium

1

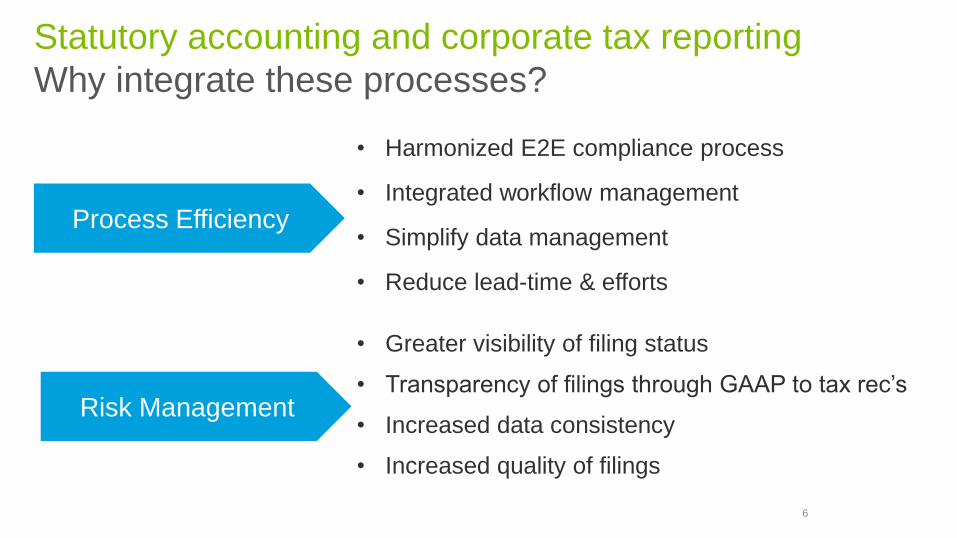

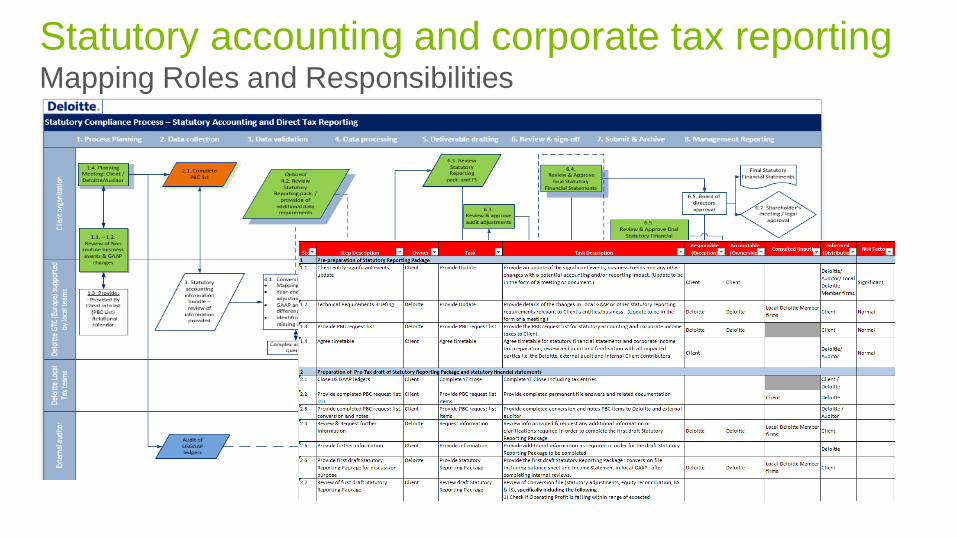

Introduction

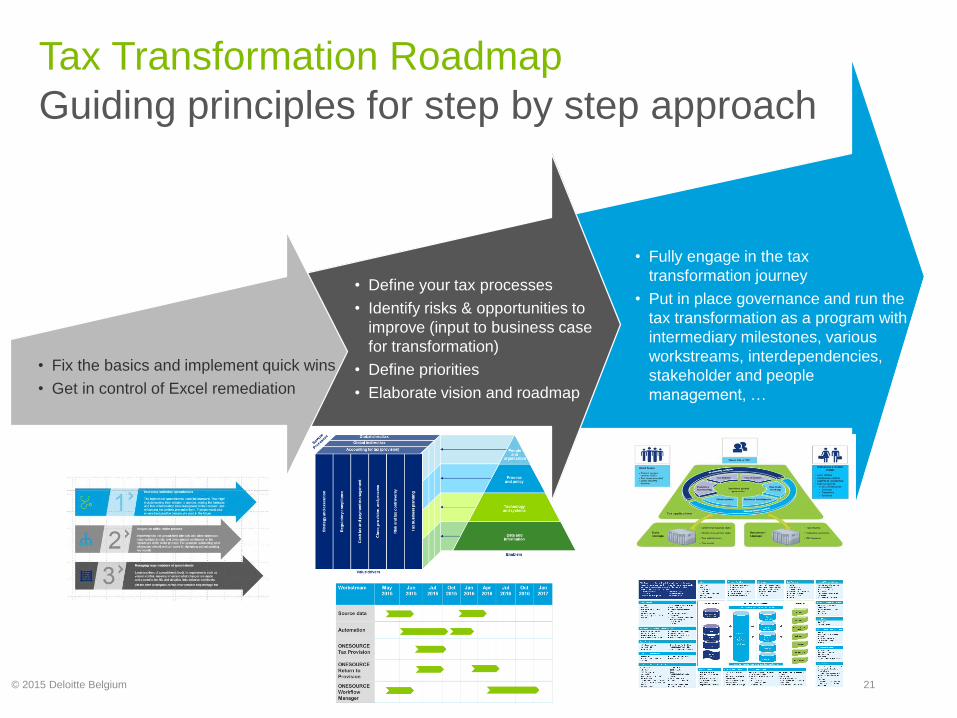

Transformation – why?

Transformation – what and how?

Conclusion

Contents

"Everything that can be

invented has been invented”

Charles Holland Duell c1899

US Commissioner of Patents

Transformation?Introduction

"Everything that can be

invented has been invented”

Charles Holland Duell c1899

US Commissioner of Patents

Thomas Watson 1943

President of IBM

Transformation?Introduction

Bill Gates

Chairman and CEO of Microsoft

Transformation?Introduction

"Everything that can be

invented has been invented”

Charles Holland Duell c1899

US Commissioner of Patents

Thomas Watson 1943

President of IBM

“When we set the upper limit of PC-DOS at 640 KB,

we thought nobody would ever need that much memory”

6

Transform today for

the challenges of

tomorrow

Transformation –

why?

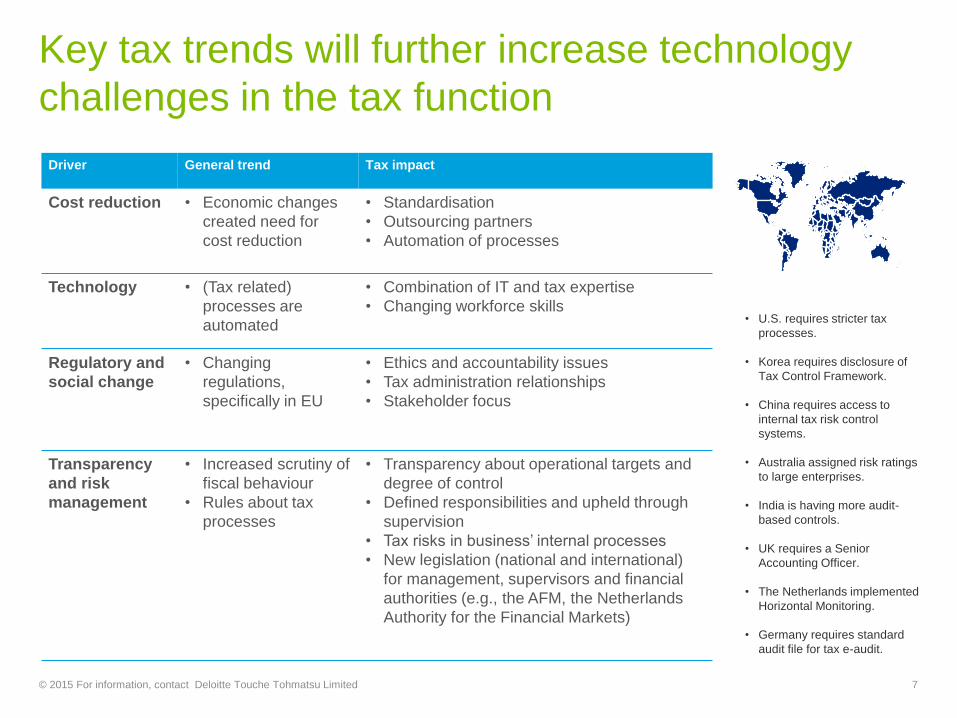

Transformation why? External trends are impacting Tax …

As business GLOBALIZES … so do tax

obligations together with a pressure for

centralized global delivery

TECHNOLOGY proliferation … fuels

expectations for wholesale process

change, and becomes a catalyst for re-

engineering tax

Transformation of REVENUE

AUTHORITIES … the way they go about

their work

Increased REGULATION makes business

more complex but also more transparent

... raising risk and enabling mainstream

media coverage

TALENT … new skills are needed and

there is a new environment within which

to attract and retain people

New STAKEHOLDERS … have emerged

and we are confronted by a new era of

socially responsible tax

8

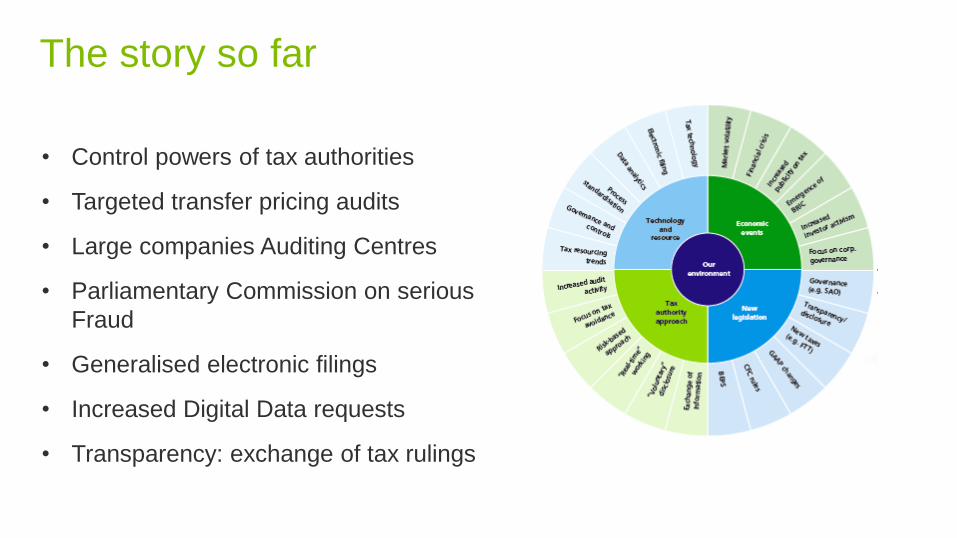

New practices

and regulations

• Control powers of tax authorities

• Targeted transfer pricing audits

• Large companies Auditing Centres

• Parliamentary Commission on serious

Fraud

• Generalised electronic filings

• Increased Digital Data requests

• Transparency: exchange of tax rulings

The story so far

9

OECD’s Base Erosion & Profit Shifting study

The European Response

State Aid

Tax Rulings: automated exchange

Action Plan on Corporate Taxation

Unilateral measures

International response

10

• More taxes and more reporting in more jurisdictions

• Evaluate the impact of change on tax operations

• Modelling the impact of new measures

• How? New management processes & tools

• When?

What does it mean?

11

The Global Tax Reset & BEPS

12

Global Tax Reset: the changing world of tax

The Global Tax Reset is bringing in a new era of

international tax, with an emphasis on transparency,

consistency and sharing of information between tax

authorities. This paper discusses the forces driving

significant change to the international tax landscape,

as well as key areas of business impact and

resulting challenges.

About BEPS and FAQs

The OECD’s Base Erosion and Profit Shifting actions

are well underway with proposals and consultations

on all actions. Change is coming. These pages will

help businesses navigate what is happening, key

deadlines and issues they might want to consider.

Articles, briefings and discussion papers

The OECD’s Base Erosion and Profit Shifting actions

are well underway with proposals and consultations

on all actions. Change is coming. These pages will

help businesses navigate what is happening, key

deadlines and issues they might want to consider.

News & updates

Visit Deloitte tax@hands for tax news and updates on

BEPS and other issues driving the global tax reset

Dbriefs webcasts

Dbriefs Webcasts feature our professionals discussing

critical issues that affect your business.

Country-by-country reporting (CbCR)

This perspective paper aggregates frequently asked

questions by business leaders about Country-by-

country reporting (CbCR), a requirement detailed in

Action 13 of the OECD's BEPS guidelines, and is

intended to help companies understand what CbCR

is, what information is needed, who CbCR applies to,

and how businesses can prepare.

BEPS Actions

There are 15 BEPS Actions that are currently being

considered and worked on by the OECD. For each of

the Actions, there are factors to consider such as the

timing, impact and potential impact on policy. The

OECD/G20 has set a number of deadlines to

conclude on the BEPS Actions.

G20/OECD Timeline

An overview of the information and documentation

that has been released by the OECD during the

course of the BEPS Action Plan, together with

relevant Deloitte or third party content and

commentary. As well as containing details of all of

the releases to date, the timeline shows what is

expected over the coming months, in accordance

with the schedule published by the OECD.

13

Transform today for

the challenges of

tomorrow

Transformation –

what and how?

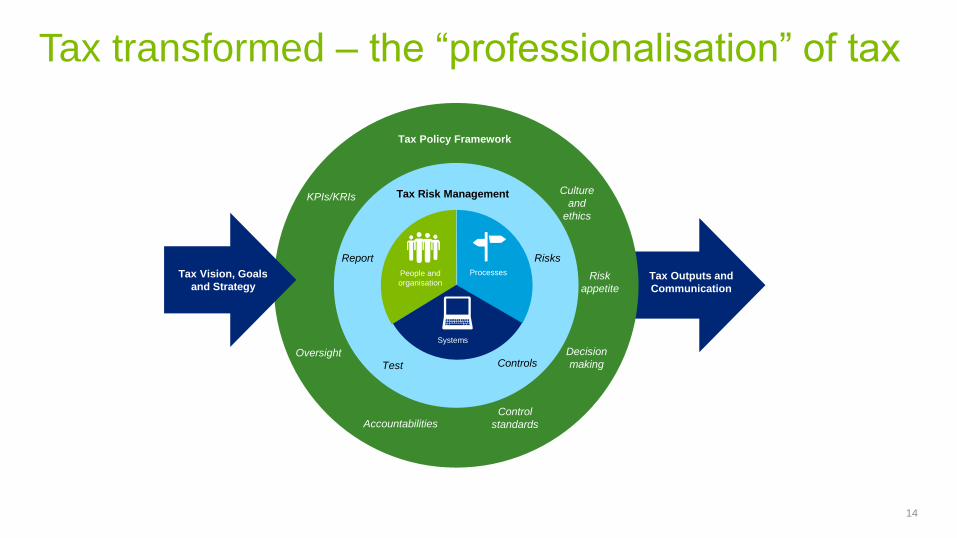

Tax transformed – the “professionalisation” of tax

14

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

15

Tax policy,

risk and operations

Increasing formalisation of tax policy

16

Accountabilities for taxes getting clearerGroups are increasingly defining their tax policy

Source: Deloitte Global Market Research, 2014

47%

29%

23%No

Yes, for some areas

Yes, for all four areas

Answering key questions

17

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

“How is success

measured?”

“How are key

decisions made?”

“Who owns each

tax?”

“What governance

is there over tax?”

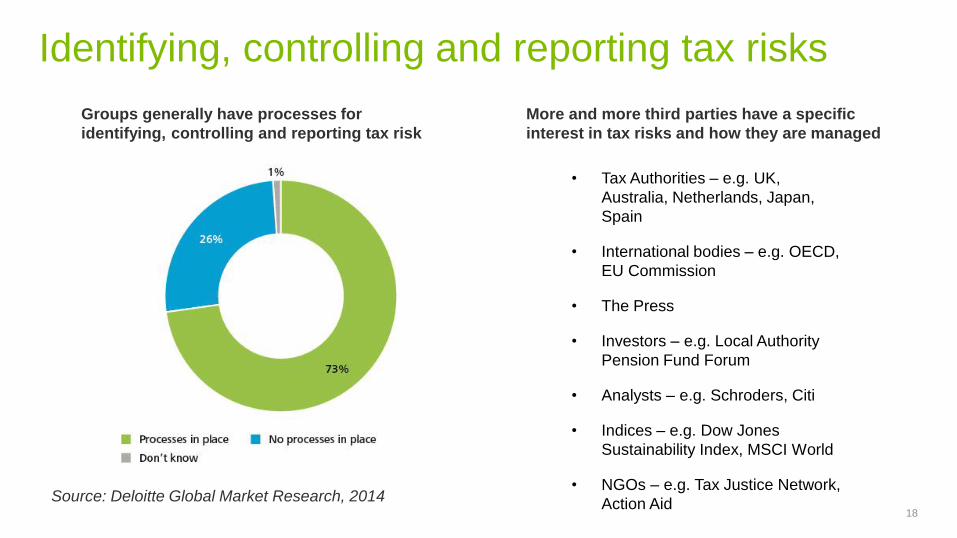

Identifying, controlling and reporting tax risks

18

Groups generally have processes for

identifying, controlling and reporting tax risk

More and more third parties have a specific

interest in tax risks and how they are managed

• Tax Authorities – e.g. UK,

Australia, Netherlands, Japan,

Spain

• International bodies – e.g. OECD,

EU Commission

• The Press

• Investors – e.g. Local Authority

Pension Fund Forum

• Analysts – e.g. Schroders, Citi

• Indices – e.g. Dow Jones

Sustainability Index, MSCI World

• NGOs – e.g. Tax Justice Network,

Action AidSource: Deloitte Global Market Research, 2014

Developing a risk-based approach

19

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

“How do we report to

the Tax Committee?”

“What are our key

tax risks?”

“Who are our ‘lines

of defence’?”

“When is Internal

Audit testing tax?”

20

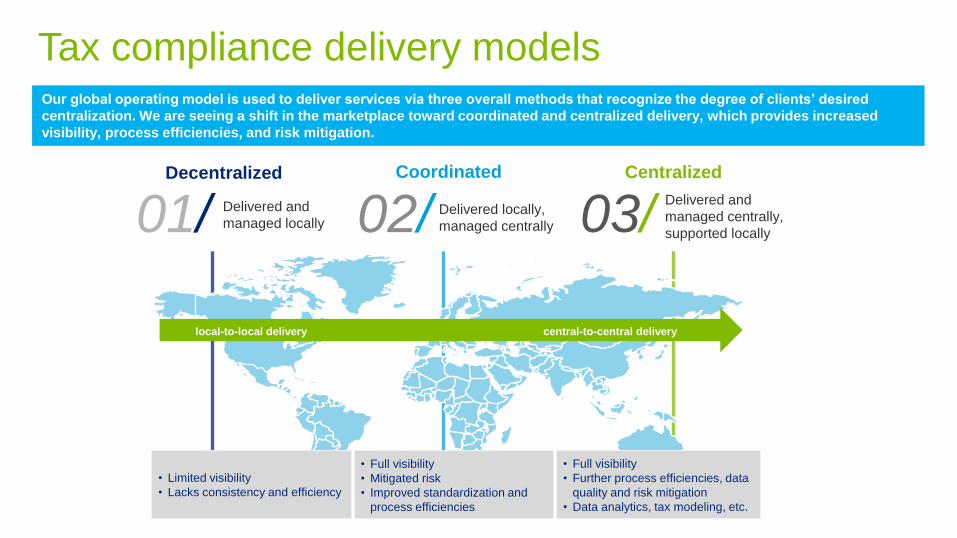

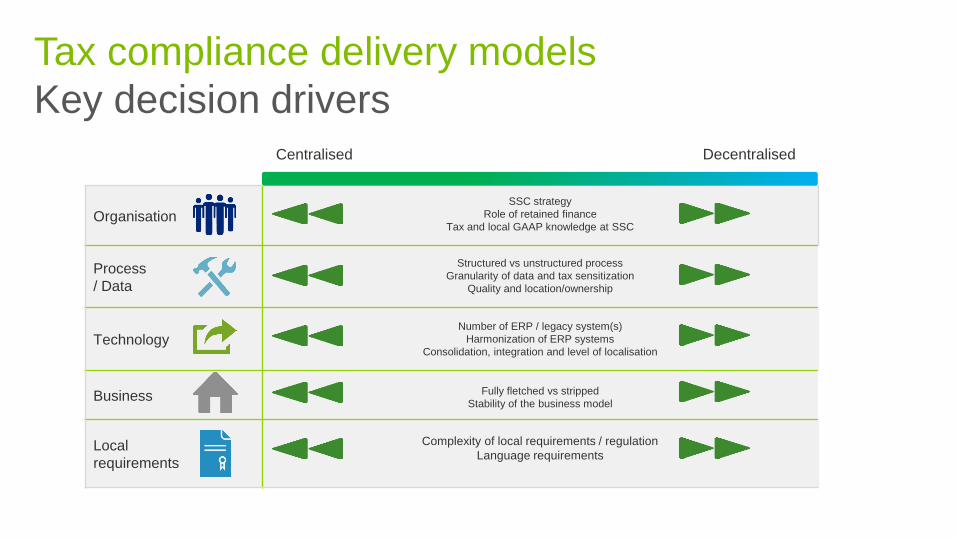

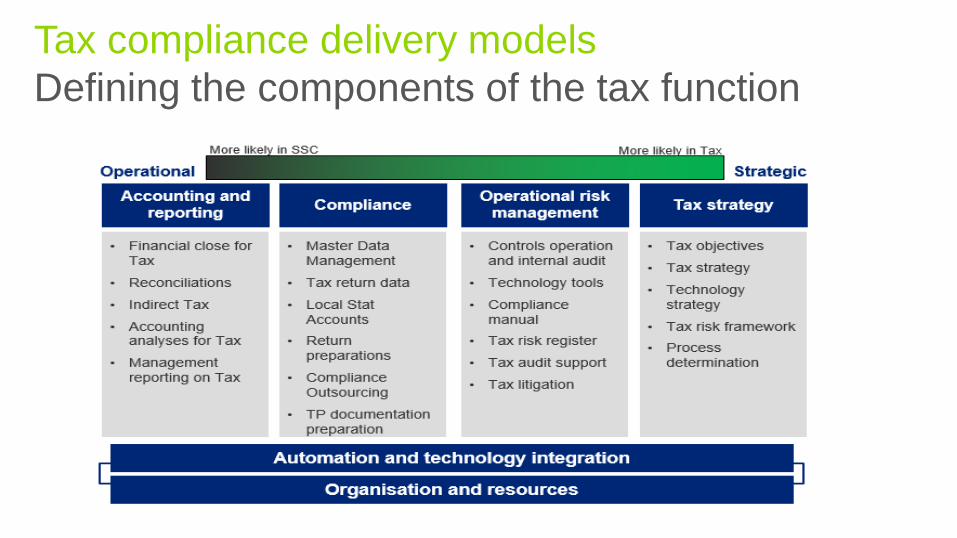

Compliance

operating models

Global tax operating models

21

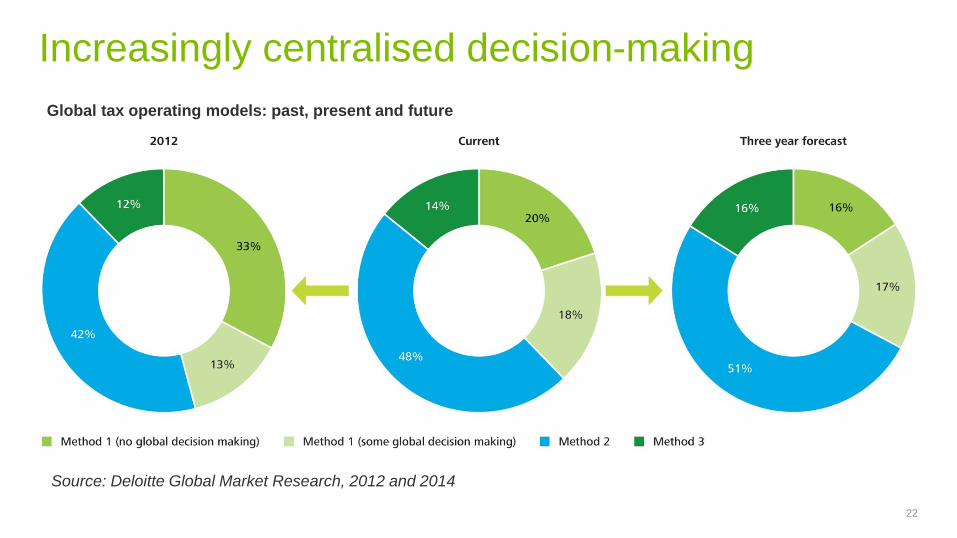

Increasingly centralised decision-making

22

Global tax operating models: past, present and future

Source: Deloitte Global Market Research, 2012 and 2014

Pressure for continuous improvement

23

Satisfaction (% happy) with current model by driver and method

Source: Deloitte Global Market Research, 2014

Evolving the operating model

24

“Do we have the

right scale, roles,

locations?”

“Can we streamline

adjacent

processes?”

“What is the right

in/out/co-source

model?”

People and

organisation

Processes

Systems

Tax Risk Management

Risks

ControlsTest

Report

Tax Policy Framework

Risk

appetite

Decision

making

Control

standards

Oversight

KPIs/KRIsCulture

and

ethics

Accountabilities

Tax Vision, Goals

and StrategyTax Outputs and

Communication

“Can we leverage

our Shared Service

Centres?”

25

Tax technology

Tax Department is a large consumer of data

26© 2015 Deloitte Belgium

Complexity of Tax Technology Landscape

27

© 2015 Deloitte Belgium

Tax transformation framework

28

Str

ate

gy a

nd

ex

ec

uti

on

Reg

ula

tory

co

mp

lia

nc

e

Cas

h t

ax

an

d p

aym

en

t m

an

ag

em

en

t

Clo

se

, p

rovis

ion

, a

nd

pro

ce

ss

Ta

x b

us

ine

ss

pla

nn

ing

Ris

k a

nd

ta

x c

on

tro

ve

rsy

Global direct tax

Global indirect tax

Accounting for tax (provision) People and

organization

Technologyand systems

Processand policy

Data and information

Enablers

Value drivers

29

Conclusion

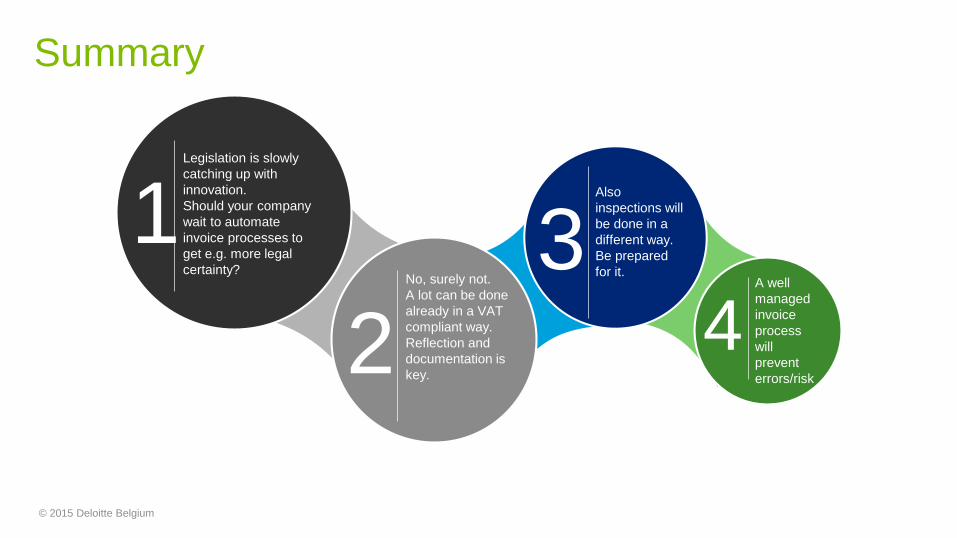

Main points?Conclusion

1. Policy, Risk and Operations

2. Compliance Operating models

3. Technology

Interconnections – Change management – Communication

30

Agenda of the dayConclusion

31

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member

firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most

complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte

Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained

by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 32

Transform today

for the challenges

of tomorrow

Operational

Transfer Pricing

1

Maison de L’automobile15 December 2015

Maria Panina – Senior Director, Deloitte BelgiumThierry chaumantin – Senior Manager, Deloitte Belgium

1. Definition

2. Issues & Challenges

3. Solution Framework

4. Implementation & Monitoring – SAP example

5. Summary

Contents

1. Definition

3

Definition

People, Processes and

Technology employed to

ensure that chosen

business model and

transfer pricing policies are

ultimately reflected in its

books and statutory returns

Transfer pricing policy

Operational TP Monitoring Implementation

Documen-tation

2. Issues &

Challenges

5

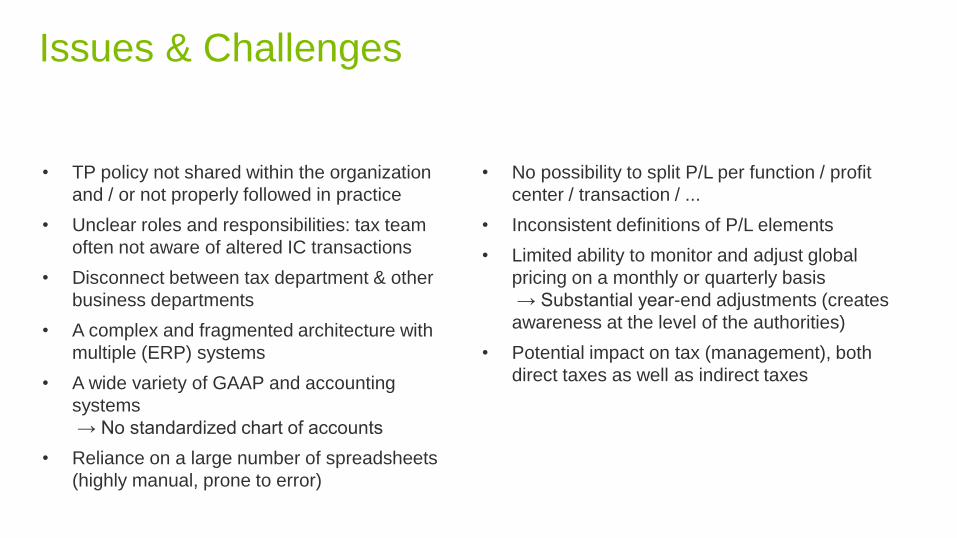

• TP policy not shared within the organization

and / or not properly followed in practice

• Unclear roles and responsibilities: tax team

often not aware of altered IC transactions

• Disconnect between tax department & other

business departments

• A complex and fragmented architecture with

multiple (ERP) systems

• A wide variety of GAAP and accounting

systems

→ No standardized chart of accounts

• Reliance on a large number of spreadsheets

(highly manual, prone to error)

• No possibility to split P/L per function / profit

center / transaction / ...

• Inconsistent definitions of P/L elements

• Limited ability to monitor and adjust global

pricing on a monthly or quarterly basis

→ Substantial year-end adjustments (creates

awareness at the level of the authorities)

• Potential impact on tax (management), both

direct taxes as well as indirect taxes

Issues & Challenges

3. Solution

Framework

7

Technology

Process

People

Data collection is

complete and

accurate

Policies are

properly translated

into practice

Calculations and

adjustments are

automated and accurate

Audit status is visible

on a global basis

Reporting and

requirements are identified

and fulfilled locally

Policy or calculation

changes effected on a

timely basis

How do you get there – some key considerations?

• Who are the people involved in process – are they the optimum people; do they understand their part

in the process?

• Do those involved have clearly defined roles and responsibilities?

• How are training and legislative updates handled?

• Are key responsibilities understood and allocated to the right people?

• How frequently would the business like the calculation/true-up process to be run in an ideal situation

(as part of each month end close / quarterly / bi-annually / annually)?

• Where should the different elements of the end-to-end process be run (usually Finance/Tax/Business

split)?

• What controls should be in place to counter key risks? How are the controls going to be monitored?

• What technology is used currently to support the people and processes?

• How suitable is that for the complexity and / or risks of transfer pricing within the business?

• Have all technology options been considered given the significant advances in recent years?

• What level of automation is optimum for the business?

Priorities

Solution Framework – Key considerations

People: Clear definition of Roles & Responsibilities

• TP policy design

• TP documentation

• TP policy defence

• Financial reporting to Tax

• MIS reporting to Business

• Legal entity reporting

• Implementation

• Data gathering

• Monitoring

• Identifying changes of facts

TP Policy Implementation

processMonitoring Documentation

Tax

Finance

Business

Operations

Legal

Treasury

IT

Board

Budgets:Segmentation by products,

flows and legal entities

Available financial data may be insufficiently segmentedTP policies

Calculation of

Adjustments

Adjustments need to be

allocated across multiple cost

centers or SKUs

Price lists: 1000s SKUs

and discounts

Statutory results

Adjustments need to reflected in statutory financials so results correspond to the TP policy

Update of budgets

Automation

Processes (and data) - Implementation

Considerations

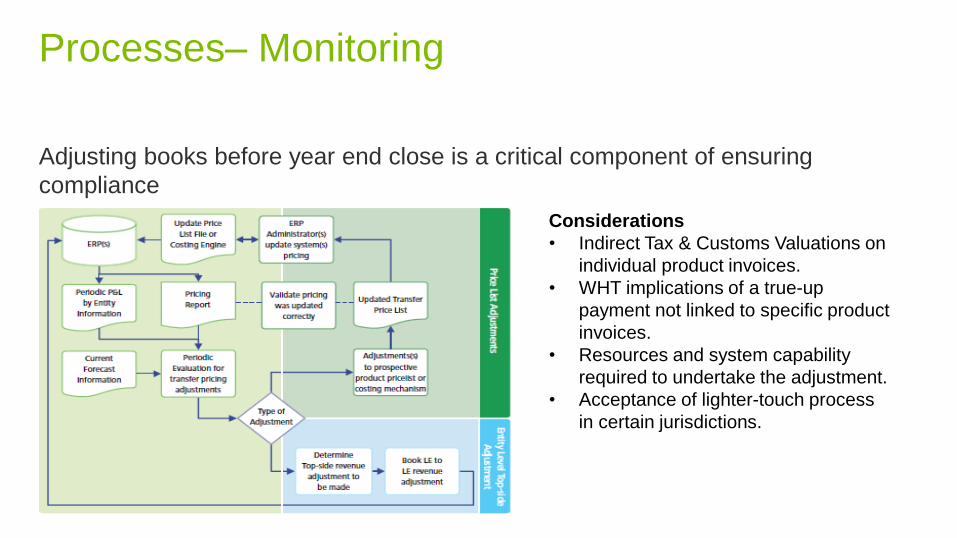

• Indirect Tax & Customs Valuations on

individual product invoices.

• WHT implications of a true-up

payment not linked to specific product

invoices.

• Resources and system capability

required to undertake the adjustment.

• Acceptance of lighter-touch process

in certain jurisdictions.

Processes– Monitoring

Adjusting books before year end close is a critical component of ensuring

compliance

4. Implementation

& Monitoring

on SAP

12

A combination of SAP modules can be used to effectively implement and monitor

the TP policy

BPC: Budgeting Module - Determine transfer price by product

family based on budget P&L and target Profit Level Indicators

(PLIs)

SD: Pricing Module – Configure transfer price by product

family using appropriate TP mechanism (e.g. cost plus, re-sale

minus) and generate intercompany billing invoices

FICO (COPA): Controlling Module – Analyse PLI variances and

determine transfer price corrections (TP true up adjustments or

transfer price update)

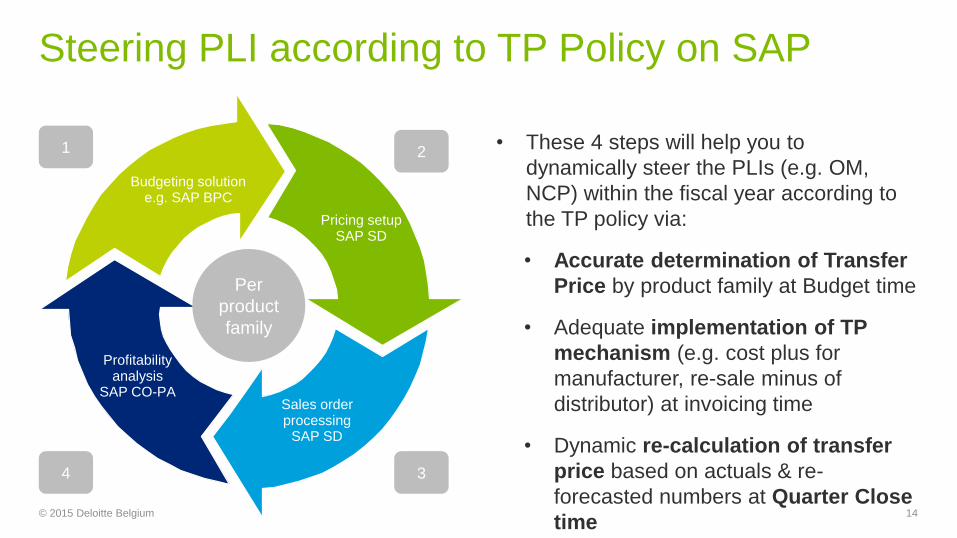

TP policy: implementation & monitoring on SAP

Steering PLI according to TP Policy on SAP

• These 4 steps will help you to

dynamically steer the PLIs (e.g. OM,

NCP) within the fiscal year according to

the TP policy via:

• Accurate determination of Transfer

Price by product family at Budget time

• Adequate implementation of TP

mechanism (e.g. cost plus for

manufacturer, re-sale minus of

distributor) at invoicing time

• Dynamic re-calculation of transfer

price based on actuals & re-

forecasted numbers at Quarter Close

time© 2015 Deloitte Belgium 14

Pricing setupSAP SD

Budgeting solutione.g. SAP BPC

Profitabilityanalysis

SAP CO-PASales orderprocessing

SAP SD

Per

product

family

1 2

34

1.Budgeting & Transfer Price Determination

• Budget input

During the budget exercise, OPEX, sales

and cost of sales quantities and prices

will be loaded in the system by the

business teams

• PLI computation

Based on the data entered, the

budgeting tool will compute the PLIs by

legal entity/function

• Transfer Price margin calculation

PLI can be iteratively refined by adjusting

the percentages in the budget tool (cost

plus, re-sale minus) to reach the target

PLI (OM,NCP) by legal entity/function© 2015 Deloitte Belgium 15

Pricing setupSAP SD

Budgeting solutione.g. SAP BPC

Profitabilityanalysis

SAP CO-PASales orderprocessing

SAP SD

Per

product

family

1

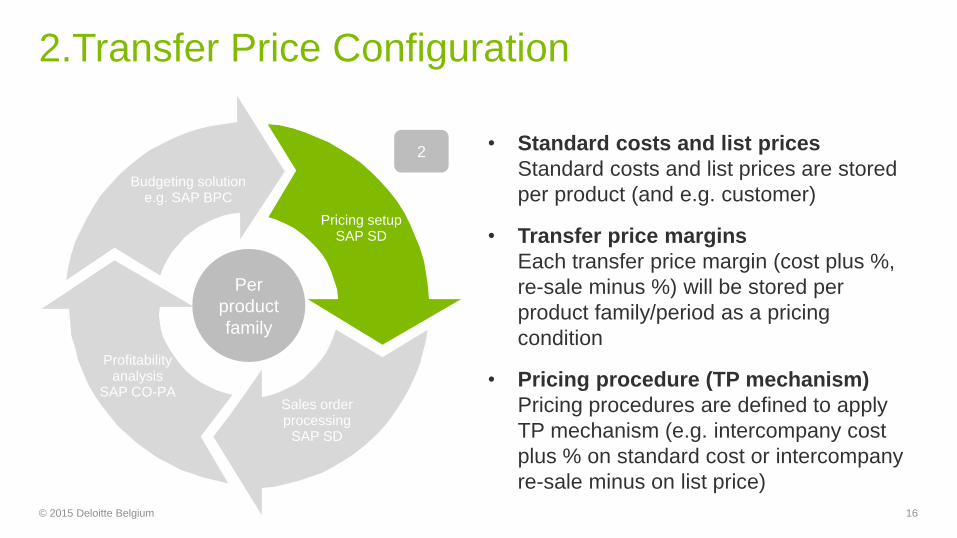

2.Transfer Price Configuration

• Standard costs and list prices

Standard costs and list prices are stored

per product (and e.g. customer)

• Transfer price margins

Each transfer price margin (cost plus %,

re-sale minus %) will be stored per

product family/period as a pricing

condition

• Pricing procedure (TP mechanism)

Pricing procedures are defined to apply

TP mechanism (e.g. intercompany cost

plus % on standard cost or intercompany

re-sale minus on list price)

© 2015 Deloitte Belgium 16

Pricing setupSAP SD

Budgeting solutione.g. SAP BPC

Profitabilityanalysis

SAP CO-PASales orderprocessing

SAP SD

Per

product

family

2

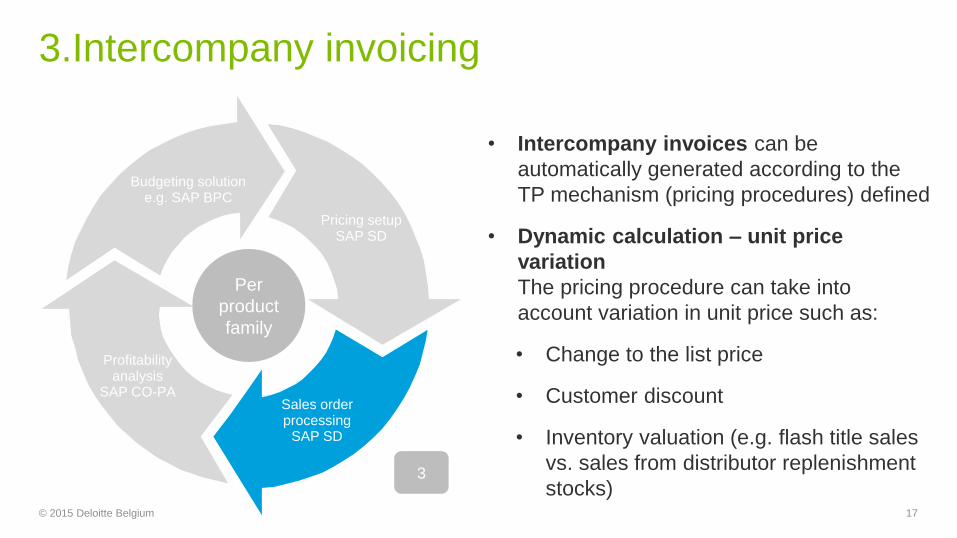

3.Intercompany invoicing

• Intercompany invoices can be

automatically generated according to the

TP mechanism (pricing procedures) defined

• Dynamic calculation – unit price

variation

The pricing procedure can take into

account variation in unit price such as:

• Change to the list price

• Customer discount

• Inventory valuation (e.g. flash title sales

vs. sales from distributor replenishment

stocks) © 2015 Deloitte Belgium 17

Pricing setupSAP SD

Budgeting solutione.g. SAP BPC

Profitabilityanalysis

SAP CO-PASales orderprocessing

SAP SD

Per

product

family

3

4. Transfer Price Controlling (*)

• Analyze Actual PLI (OM, NCP) by segmented

P&L (legal entity/function)

Compare actual vs. budget, break-down GM by

product family, identify variance origin (volume,

unit price)

• Determine Transfer Price adjustment

Combine actual YTD plus remainder of the year

forecasts. Determine transfer price adjustment

by product family (% of cost plus or re-sale

minus) to reach target PLI for the fiscal year

• Implement Transfer Price adjustment

Either via transfer price update in SD (adjust %

of cost plus or re-sale minus) or via posting of

TP true-up adjustments (generate credit

note/debit note)© 2015 Deloitte Belgium 18

(*) Combined usage of COPA & BPC to get full picture

actual & budget/forecast numbers

Pricing setupSAP SD

Budgeting solutione.g. SAP BPC

Profitabilityanalysis

SAP CO-PASales orderprocessing

SAP SD

Per

product

family

4

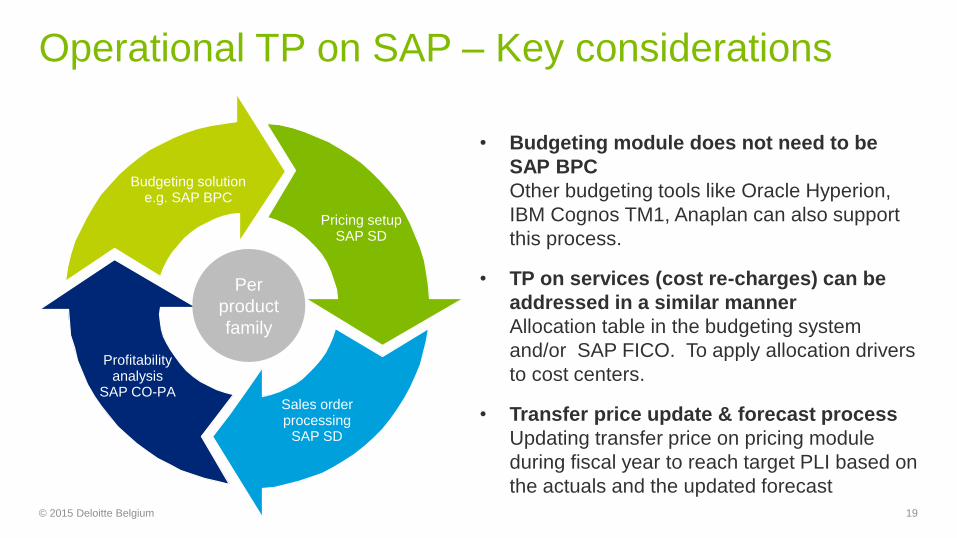

Operational TP on SAP – Key considerations

• Budgeting module does not need to be

SAP BPC

Other budgeting tools like Oracle Hyperion,

IBM Cognos TM1, Anaplan can also support

this process.

• TP on services (cost re-charges) can be

addressed in a similar manner

Allocation table in the budgeting system

and/or SAP FICO. To apply allocation drivers

to cost centers.

• Transfer price update & forecast process

Updating transfer price on pricing module

during fiscal year to reach target PLI based on

the actuals and the updated forecast

© 2015 Deloitte Belgium 19

Pricing setupSAP SD

Budgeting solutione.g. SAP BPC

Profitabilityanalysis

SAP CO-PASales orderprocessing

SAP SD

Per

product

family

6. Summary

20

Solution Framework- The Building Blocks

Master File

Legal structure, business

area, intangibles, financial

activities, financial & tax info

Local Files

Local mgmt. info, org chart,

intra-group payments,

financial data for arms

length calcs., APAs

Operational Transfer Pricing

Tax FinanceSupply

ChainLegal

Other

Board, IA

People

Organisation

Stakeholders

Process

Technology

Systems

and data

1.

3.

2. ITTreasury

Risk, controls and governance

Strategic objective

setting

Workflow

Reporting

• Country by country

reporting

• Tax return information

• Internal stakeholders

Analytics and

monitoring

• Validation of policy

operation

• Value-added analytics

and insight

Policy determination

Policy documentation

Audit defence

• Audit defence

approach

• Process / workflow

• Feedback and update

Economic analysis and initial

documentation

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.

This communication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member firms, and their related entities (collectively, the “Deloitte Network“). None of the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 22

Transform today for

the challenges of

tomorrow

The new Union

Customs Code

Maison de L’automobile15 December 2015

Dries Bertrand – Senior Manager - Deloitte BelgiumAlexander Baert – Attorney-at-law - Laga

1

Introduction

Introduction of Union Customs Code / Transformation – why?

How does this impact your GTM systems & tools / Transformation – what?

Transform today for the challenges of tomorrow – how?

Conclusion

Contents

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 2

3

Introduction of

Union Customs

Code

Transformation –

why?

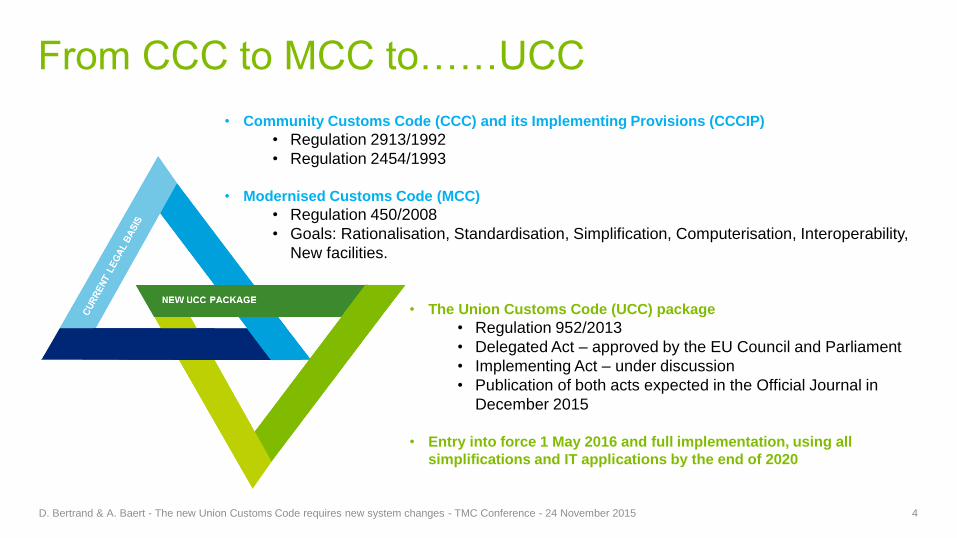

From CCC to MCC to……UCC

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 4

• Community Customs Code (CCC) and its Implementing Provisions (CCCIP)

• Regulation 2913/1992

• Regulation 2454/1993

• Modernised Customs Code (MCC)

• Regulation 450/2008

• Goals: Rationalisation, Standardisation, Simplification, Computerisation, Interoperability,

New facilities.

• The Union Customs Code (UCC) package

• Regulation 952/2013

• Delegated Act – approved by the EU Council and Parliament

• Implementing Act – under discussion

• Publication of both acts expected in the Official Journal in

December 2015

• Entry into force 1 May 2016 and full implementation, using all

simplifications and IT applications by the end of 2020

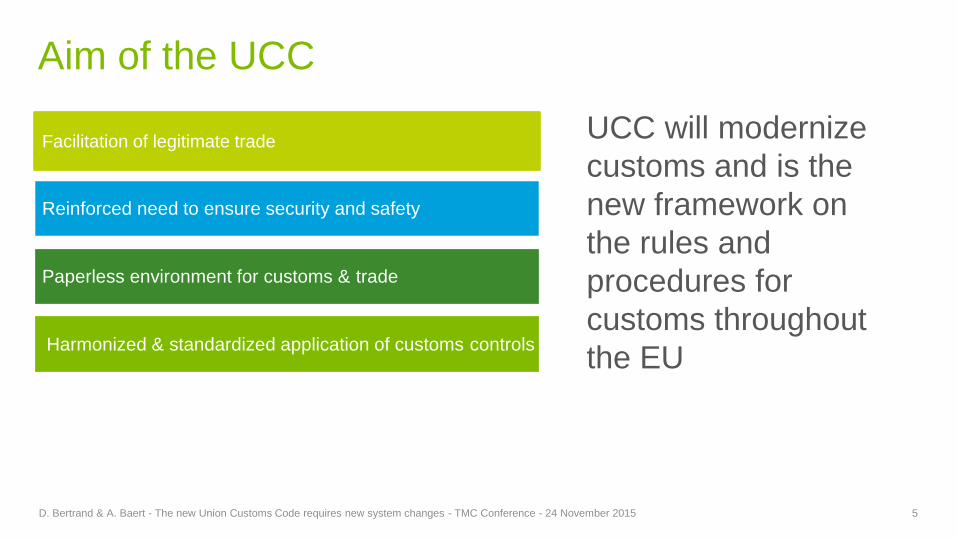

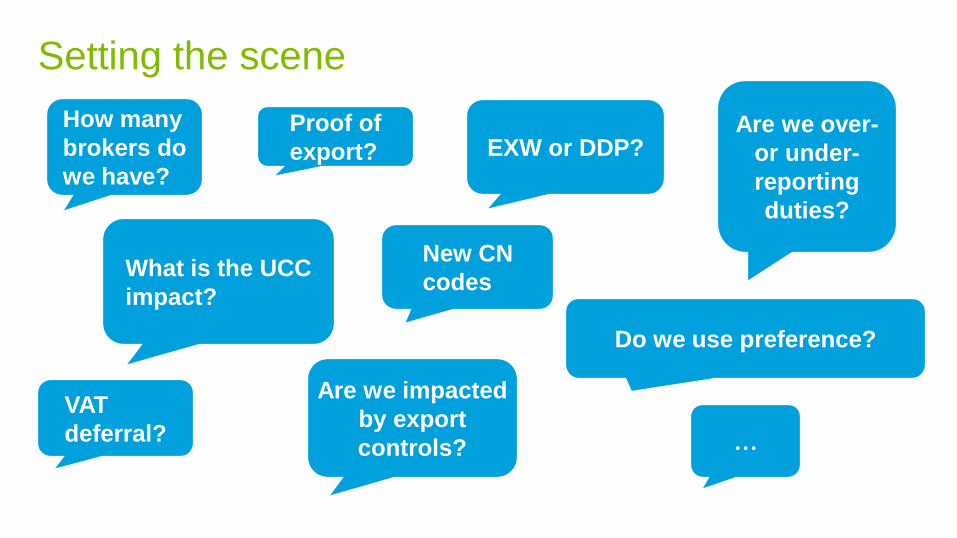

Aim of the UCC

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 5

Facilitation of legitimate trade

Reinforced need to ensure security and safety

Paperless environment for customs & trade

Harmonized & standardized application of customs controls

UCC will modernize

customs and is the

new framework on

the rules and

procedures for

customs throughout

the EU

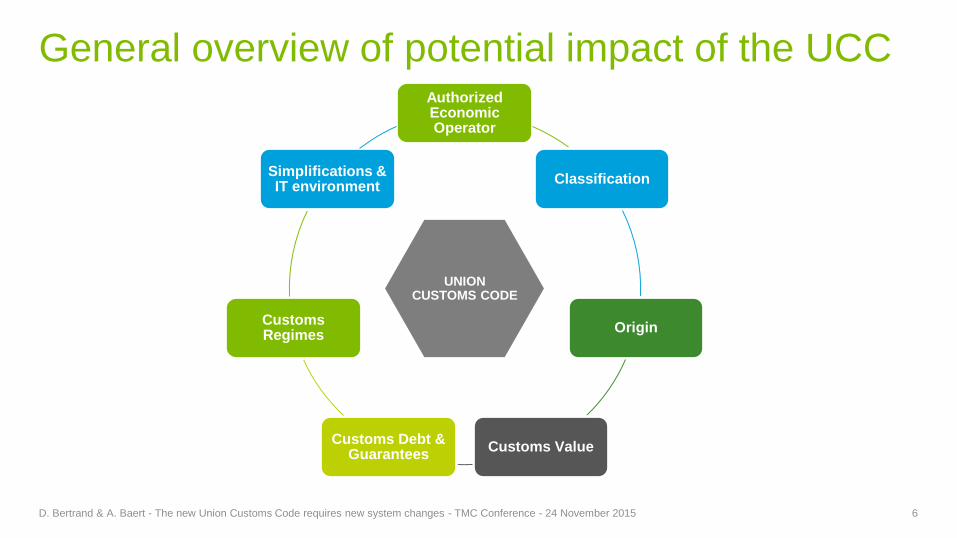

General overview of potential impact of the UCCAuthorized Economic Operator

Classification

Origin

Customs ValueCustoms Debt &

Guarantees

Customs Regimes

Simplifications & IT environment

UNION CUSTOMS CODE

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 6

© 2015 Deloitte. Private and confidential.

UCC Projects Timeline

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 7

UCC Projects related to electronic systemsTarget date of

deployment

S1

2017

S2

2017

S1

2018

S2

2018

S1

2019

S2

2019

S1

2020

S2

2020

1. UCC Registered Exporter System (REX) 01.01.2017

2. UCC Binding Tariff Information System (BTI) Update - Phase 1 01.03.2017

2. UCC Binding Tariff Information System (BTI) Update - Phase 2 01.10.2018

3. UCC Customs Decisions 02.10.2017

4. Direct trader access to European Information Systems

(Uniform user management & digital signature)02.10.2017

5. UCC Proof of Union Status (PoUS) 02.10.2017

6. UCC AEO updates 01.03.2018

7. UCC New Computerised Transit System (NCTS) update 01.10.2018

8. UCC Surveillance 3 02.10.2018

9. UCC Automated Export System (AES) 01.03.2019

10. UCC Information Sheets (INF) for Special Procedures 01.10.2019

11. UCC Special Procedures 01.10.2019

12. UCC Notification of arrival, presentation notification and

temporary storage02.03.2020

13. UCC Centralised Clearance for Import (CCI) 02.10.2020

14. UCC Guarantee Management 02.10.2020

15. UCC Safety and Security and Risk Management TBD

16. UCC Classification (CLASS) TBD

Staged

approach of

implementing IT

projects /

solutions

8

How does this

impact your GTM

systems & tools

Transformation –

what?

Example of potential impact of the UCC

EUROPEAN UNION/SWITZERLAND

India

3. Origin (BOI)

2. Classification (BTI)

I

ME

X

4. Customs Value

5. Customs Clearance

6. Customs

Debt

7. Special Procedures

USA

8. Simplifications and IT

systems

1. Authorized Economic Operator

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 9

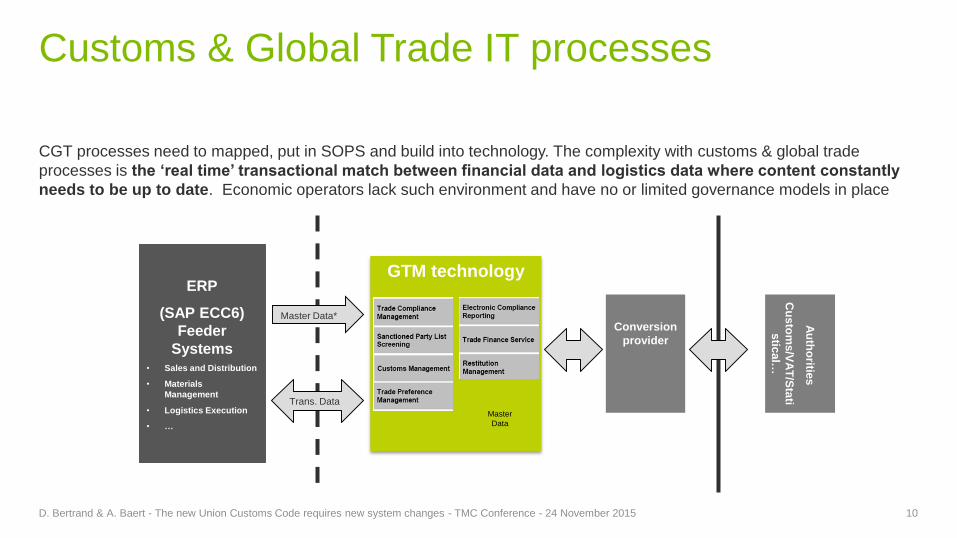

Customs & Global Trade IT processes

CGT processes need to mapped, put in SOPS and build into technology. The complexity with customs & global trade

processes is the ‘real time’ transactional match between financial data and logistics data where content constantly

needs to be up to date. Economic operators lack such environment and have no or limited governance models in place

10

Conversion

provider

ERP

(SAP ECC6)

Feeder

Systems• Sales and Distribution

• Materials

Management

• Logistics Execution

• …

Au

tho

rities

Cu

sto

ms

/VA

T/S

tati

stic

al…

GTM technology

Master

Data

Master Data*

Trans. Data

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015

Global trade master data – UCC impact

11D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015

Master Data Management

Business Partner

Customers

ProductBill Of

Material

Product data

Banks

Duty RatesBOM

Exchange Rates

Customs codes (HTS/CN Code)

Licenses

Import/Export Licenses

Vendors

Rates

Economical Origin

Preferential Status

License Rules

Letter of Credit

Classification

Origin

SPL List

Export Control Codes

(ECCN/ECN/ ITAR)

ERP

ERP/Global Trade

Global Trade

Product values

Global trade functionalities – UCC impact

12D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015

Excise warehousing

FTZ/ Bonded

warehousing

Customs

Processing

Brokerage / e-filing

declaration model

Product

Classification

Product

Classification

Export License

Screening

Import License

Screening

Embargo

Screening

Black List

Screening

Certificate

Management

Preference

Determination

Supplier Declaration

Handling

Letter of Credit

Intrastat reporting

Country of Origin

OGA management

Regulatory

management

Customs

management

Special

regimesPreference

management

Other trade

compliance

Duty Drawback

The Four Keystones of CGT management

13D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015

Processes & Procedures• Service provider management• Customs filing• Applying for licenses• License reporting• Agreements reporting• Mergers and acquisitions advisory• End-use research and assurance management• Anti-boycott research and assurance

management• Training

People & Organization• Leadership and commitment• Policies definition and management• Culture of awareness• Global regulatory knowledge• Regional regulatory knowledge• Technical regulatory knowledge• Systems and tools proficiency• Cross functional collaboration

Technology• Restricted party screening• Embargo screening• End-use screening• Anti-boycott screening• Classification management• License management• Free Trade Agreements management• Import/Export filing• Trade document generation• Broker integration• Records retention• Metrics and reporting• Workflow and rules

Data Management • Master data management• Data quality management• Global trade content• Restricted parties/entities• Embargo lists• Classification data• Systems role definitions• Data tagging• Data access policy management• Metrics and reportingTechnology

Processes

&

Procedures

People &

Organization

Data

Management

14

Transform today for

the challenges of

tomorrow

Transformation –

how?

Summary – Points of attention

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 15

01

02

03

04

05 Internal and external processes and relationships are in

scope

Processes will need to be reconsidered from a financial

point of view

Compliance procedures will need to be reassessed

Master data will need to be reassessed

Only 6 months to go to have a number of key processes,

authorizations, systems and control changes in place

What do you need to do?

• 1 May 2016 will be here soon

• A thorough assessment of the

impact of the UCC is necessary

• A project plan & strict timeline

must be drafted in order to

implement the changes of the

UCC in a strict and concise way

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 16

Way forward

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 17

Unlocking the

potentials of the UCC

while being/growing

compliant

UCC

OPPORTUNITY

SPOTTING /

RISK

MITIGATION

AWARENESS

&TRAINING

ADAPTING PROCESSES &

PROCEDURES

Thank you

Q & A

D. Bertrand & A. Baert - The new Union Customs Code requires new system changes - TMC Conference - 24 November 2015 18

Fernand Rutten, Partner, Customs & Global Trade, Global lead, +32 2 600 66 06 or [email protected]

Dries Bertrand, Customs & Global Trade, Senior Manager, +32 2 600 66 76, [email protected]

Alexander Baert, Attorney-at-law, Laga, +32 2 800 71 51 or [email protected]

Transform today

for the challenges

of tomorrow

Centralized VAT

compliance

Christophe De Waele - Deloitte

Sabine Boone – Deloitte

1

• The Current Landscape

• The Push to Centralisation

• Components of Compliance

• Focus on Technology : The SMART example

• Executing on strategy

Contents

In Deloitte’s 2014 indirect tax client

survey, our clients identified indirect tax

compliance as their number 1 priority

area.

Only 30% of respondents to our global

compliance survey were happy that their

centralised compliance processes were

efficient.

The current landscape

4

Pressures on indirect tax teams

VAT is a big number

Imposed risk managementregimes such as SAO

Public scrutiny and boardroom attention

Behaviour-based penalty regimes

Desire to “do more” withthe same resources

New resourcing and deliverymodels, such as SSC/GBS

Increasingscope of‘indirect’

taxes

More to manage alongside greater scrutiny over performance and compliance

The tax

team

Operating model evolutionThe evolution of compliance strategy from discrete functional-

and country-based models to integrated, global and cross functional services

Limited automation Medium automation

Sharing of tools and processes

Global

Maximum automation

One function Multi-function

Little sharing Full integrationCo-location

Transactional and advisory

Local Regional

Two to three functions

Transactional

SSC geographical scope

Degree of automation

Functional scope

Degree of functional integration

Degree ofvalue add

Outsourcing model Decentralized Coordinated, consolidated Centralized, Integrated

Prepared by separate local country teams

With ad-hoc use of advisors on country by country basis

Tax and statutory accounts processes aligned

Co-ordinated global outsource working with SSC

Shared service team prepares tax returns and statutory accounts

Local support for quality assurance and specialist input

Tax and statutory accounts

Operating model

7

The push to

centralization

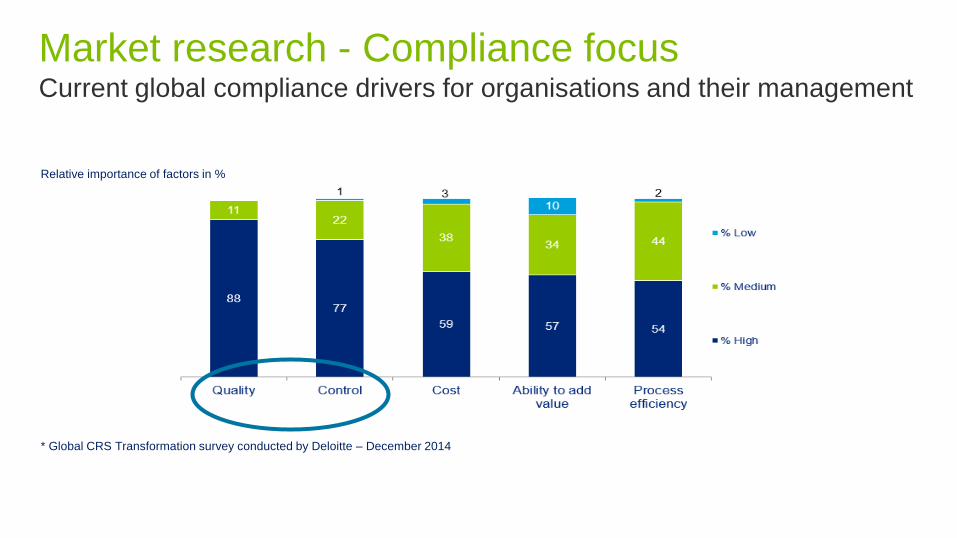

Market research - Compliance focus

Relative importance of factors in %

Current global compliance drivers for organisations and their management

* Global CRS Transformation survey conducted by Deloitte – December 2014

Market research - Compliance focus

(% Happy)

Satisfaction with the current model for managing global compliance

Delivered and

managed locally

Delivered locally,

managed centrally

Delivered and

managed

centrally

Method 1

Decentralised

Method 2

Co-ordinated

Method 3

Centralised

Market research - Compliance focus

21% 14%7% 5%

Indirect taxreturns and payments

Global taxprovision

Statutoryaccounts

Corporate incometax returns and payments

Specific issues…

Does not perform as well for…

• Lack of control; monitoring; management

• Complications of local knowledge

• No central strategy

• Lack of control; monitoring; management

• Lack of communication from external partners

• Lack of skills/ expertise

• Lack of control; monitoring; management

• Less focus on these areas

• Problems with data collection/ integration

• Lack of control; monitoring; management

• Lack of communication from external partners

• No central strategy

• Lack of skills/ expertise

Satisfaction with the current model for managing global compliance

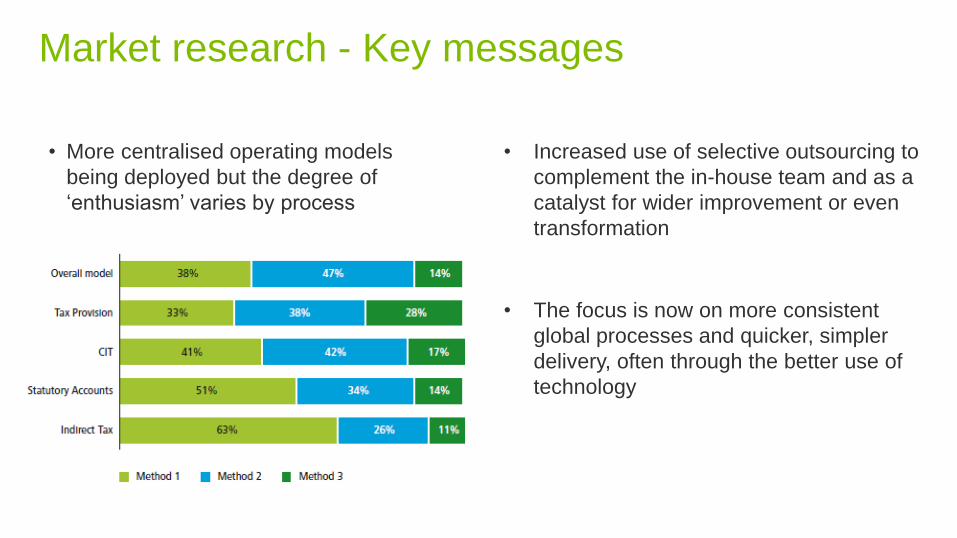

Market research - Key messages

• More centralised operating models

being deployed but the degree of

‘enthusiasm’ varies by process

• Increased use of selective outsourcing to

complement the in-house team and as a

catalyst for wider improvement or even

transformation

• The focus is now on more consistent

global processes and quicker, simpler

delivery, often through the better use of

technology

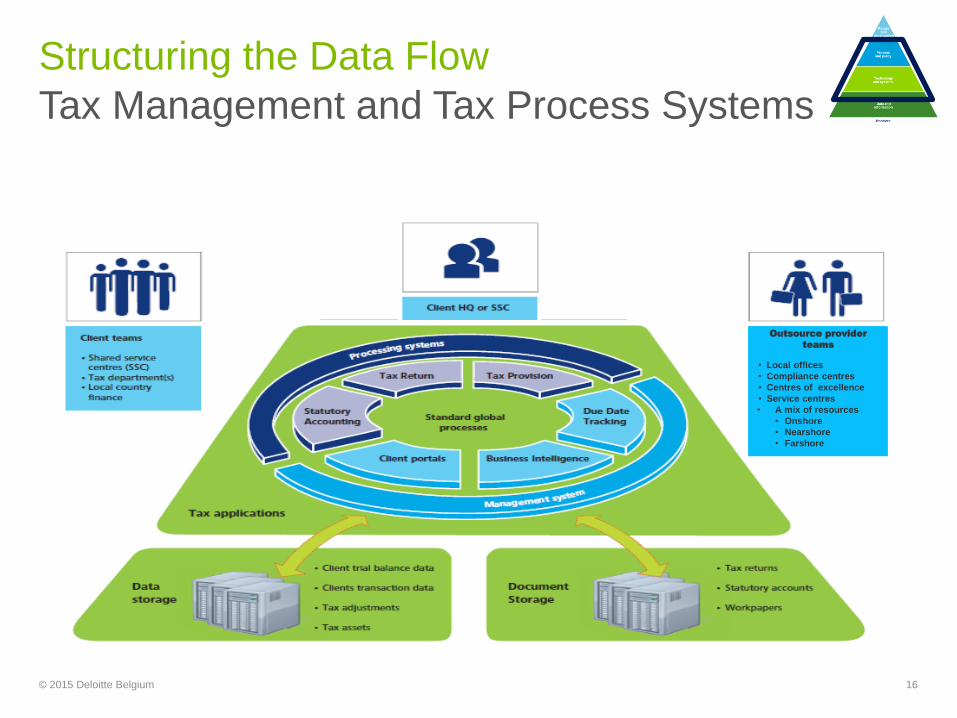

Components of

tax compliance

12

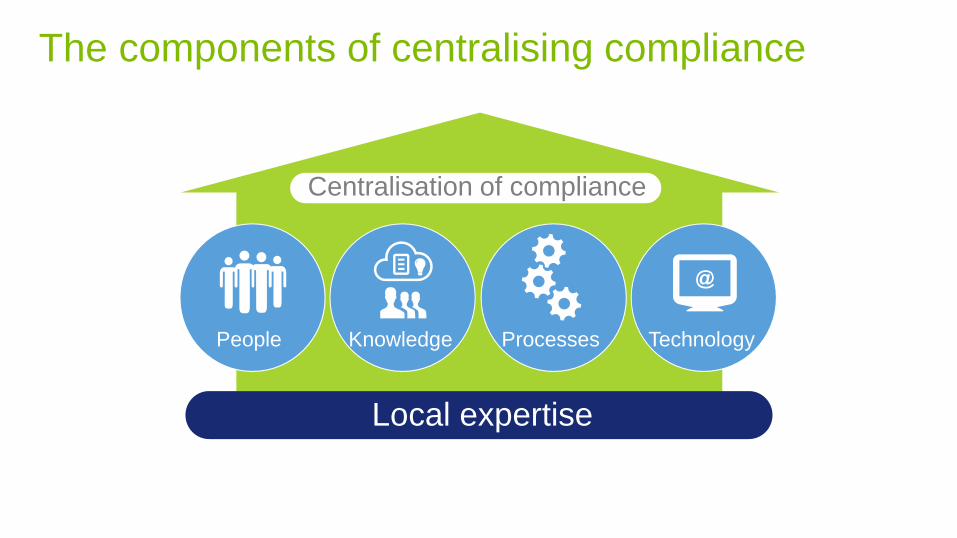

The components of centralising compliance

People Knowledge Processes Technology

Local expertise

Centralisation of compliance

The right mix of people

An multi-disciplinary team comprising:

• Tax technical specialists

• Data management resources

• IT and Excel skillsets

• Accounting knowledge

• Project & Process managers and owners

• 3rd party providers where appropriate

Nationalities Skill sets

The right mix of talents to consolidate and

test data, submit returns, adapt systems

and handle relationships with wider

business and local tax authorities

PeoplePeople

Knowledge is a key to success

Periodical Newsletters

Strong Tax technical knowledgePractical “problem solving”

experience

Innovative EMEA Tax tools

EMEA Tax matrix and overviews

Updated tax Information per country

Expertise

Co

mb

inatio

n o

fS

up

po

rted

by

Perio

dic

al

ou

tpu

t

Continuous professional training

Regular updates of knowledge databases

Knowledge

Knowledge

Reliable processesProcesses

Processes• Important to recognise what

‘compliance’ encompasses

• Preparing the return is a single step in the

cycle

• Centralising compliance will surface pain

points that need to be addressed

• We’re becoming more adept at segmenting

and aligning steps across processes

• Styles of process improvement look different

across businesses but key steps are often

common

Technology trends

• VAT compliance technology market still evolving:

− The number of international solution providers is increasing: with an eye on

making the most of an under exploited market.

− Differing views on how much integration with the source financial systems is

needed

− Still a lot of excel automation being offered in the market

− No solution does it all… yet

• Underpinning technology solutions are supporting more flexible approaches to

delivery. Clients deciding how much Indirect Tax compliance they want to share

with a service provider will replace the ‘binary’ in house vs. outsource decision.

• The systems for managing the tax process, KPI data and document

management are becoming ‘standard’ in many Tax functions, but adoption and

approach vary from group to group.

ProcessesTechnology

© 2014 Deloitte LLP. All rights reserved.

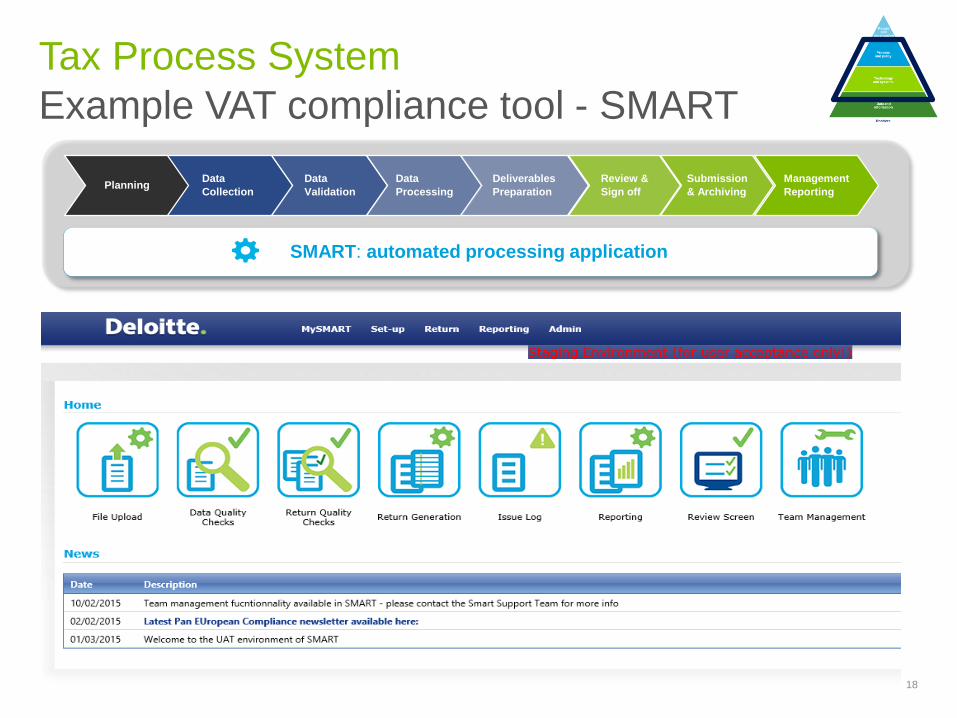

The SMART example

18

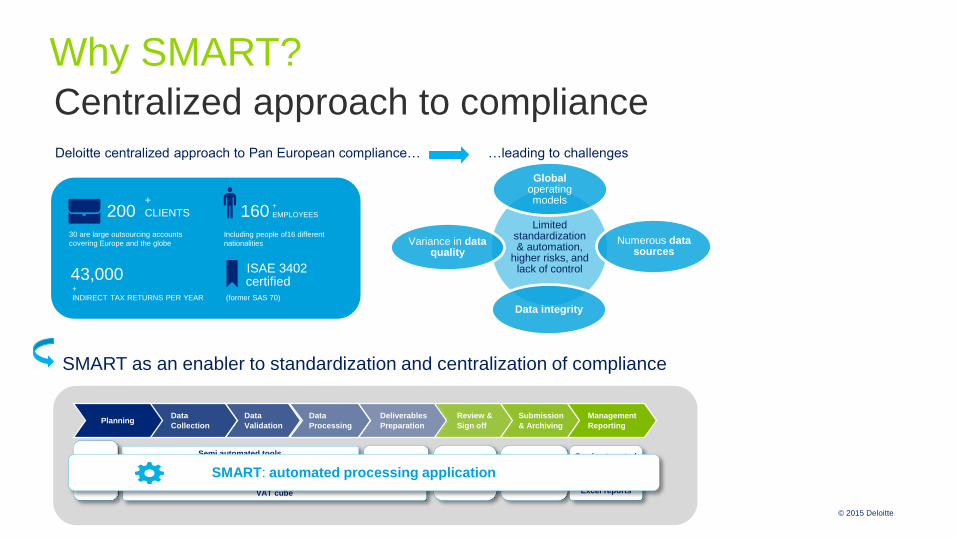

© 2015 Deloitte

Why SMART?

Data

Collection

Data

Validation

Data

Processing

Deliverables

Preparation

Review &

Sign off

Submission

& Archiving

Management

ReportingPlanning

Centralized approach to compliance

SMART as an enabler to standardization and centralization of compliance

20030 are large outsourcing accounts

covering Europe and the globe

+

CLIENTS 160+

EMPLOYEES

Including people of16 different

nationalities

43,000+

INDIRECT TAX RETURNS PER YEAR

ISAE 3402certified

(former SAS 70)

Deloitte centralized approach to Pan European compliance…

Limited standardization & automation,

higher risks, and lack of control

Global operating models

Numerous data sources

Data integrity

Variance in data quality

…leading to challenges

Return

generatorManual entry

in e-filing

software

Semi automated tools Semi automated

toolsExcel review

sheets

VAT cube

Manual checks and adjustments

Excel reports

Excel

tracker SMART: automated processing application

© 2015 Deloitte

Reporting requirements

SMART is an application developed by Deloitte that bridges the gap between

companies’ ERP systems and their global indirect tax reporting obligations.

Company data sources

ERP

Legacy Systems

DWH

ITX returns

Listings Reports

End-to-end Indirect Tax Compliance Solution

SMART key features

• Flexible set-up

• Data cleansing and consolidation

• 35+ Quality checks

• Ready-to-file ITX returns

• Full audit trail

• Standard management reporting

Flat files

What is SMART?

© 2014 Deloitte LLP. All rights reserved.21

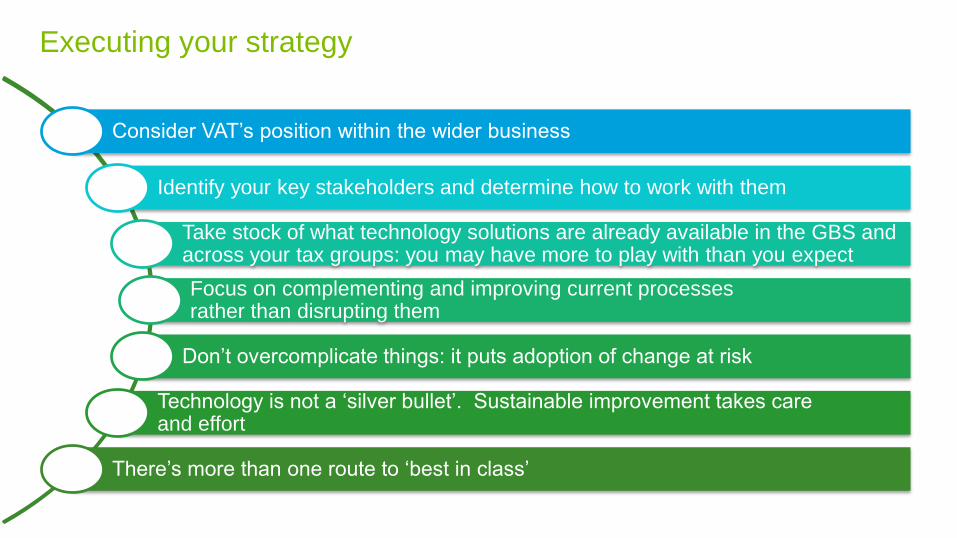

Executing the strategy

Consider VAT’s position within the wider business

Identify your key stakeholders and determine how to work with them

Take stock of what technology solutions are already available in the GBS and across your tax groups: you may have more to play with than you expect

Focus on complementing and improving current processesrather than disrupting them

Don’t overcomplicate things: it puts adoption of change at risk

Technology is not a ‘silver bullet’. Sustainable improvement takes careand effort

There’s more than one route to ‘best in class’

Executing your strategy

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.

This communication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member firms, and their related entities (collectively, the “Deloitte Network“). None of the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 23

Transform today for

the challenges of

tomorrow

The hidden

challenges of country-

by-country reporting

Maison de L’automobile15 December 2015

Lucas Yüksel – Director, Deloitte BelgiumMourad Chatar – Senior Manager, Deloitte Belgium

1

1. Introduction

2. Global tax reset

3. What are the new requirements?

4. How to get prepared ?

5. Conclusion

Contents

3

1. Introduction

1. Introduction

4

Tax & Legal Risk

Management

Volatile economic

environment

Increased complexity of

legislation

More vigilant tax

authorities

Globalized business models

Technology challenges

Customers / Suppliers

Media / NGO’s /

Lobbyists

OECD / BEPS

EU / Anti-abuse

National tax

authorities

Share holders /

Boardroom

CFO / Tax Dir / Staff

New stakeholders in the tax landscape The perception of tax avoidance has

become a reputational risk

5

2. Global tax reset

Feb 2013 July 2013

G20 leaders meet

“Addressing Base

Erosion and Profit

Shifting” published

• Digital economy

• Hybrid mismatches

• Harmful tax practices – phase 1

• Treaty abuse

• Intangibles

• Transfer pricing documentation

• Multilateral instrument – phase 1

• CFC rules

• Permanent establishments

• Interest deductions – phase 1

• Harmful tax practices – phase 2

• Risk and capital, other high-risk

transactions

• Disclosure of aggressive tax planning

• Dispute resolution

• Data collection and analysis measuring

BEPS

• Interest deductions – phase 2

• Harmful tax practices – phase 3

• Multilateral instrument – phase 2

September 2014 September 2015 December 2015

Late 2013Early 2014

Discussion drafts, public

comments, public consultations

on 2014 deliverables

Action Plan delivered to G20 Finance Ministers

November 2012

6

2. Global tax resetBEPS Actions Related to Transfer Pricing

Unilateral measures

7

2. Global tax reset

Example of Unilateral Measures

Anti-hybrid rules introduced and proposals are discussed in the digital area

Announced reform of the corporate tax system to align on international tax law

Legislation on the double Irish Tax structure applicable since 1/1/15 with a 6-

year transitional arrangement.

Law dealing with cross-border transactions incl. advertising industry &

digital economy enacted

Introduction of the tax on diverted profits. Applicable as from 1/4/158

2. Global tax reset

9© 2015 Deloitte Belgium

BEFORE AFTER

CbC Reporting

The CbC revolution2. Global tax reset

10

Filing of the 1st

CbC

Action 13: timing 1st CbC reporting

2016 2017 2018

Preparation of

the 1st CbC

Transmission of the 1st CbC

to concerned tax authorities

Next steps

• Adoption of new documentation requirements in domestic legislations;

• Creation of a centralized exchange platform for tax authorities;

• Formal signing ceremony of MCAA (January 2016).

• 2020 ?

2. Global tax reset

Article 6 of the proposed Model Legislation

Country tax administrations should use the report to:

- Assessing high level Transfer Pricing Risks where “effective risk assessment becomes an

essential prerequisite for a focused and resource-efficient tax audit”

- Assess other Base Erosion and Profit Shifting risks in country

Transfer Pricing adjustments imposed by country tax administration shall not be based on CBC

reports: “Country by Country report on its own does not constitute conclusive evidence that

transfer pricings are or are not appropriate”

11

2. Global tax resetAction 13: Country-by-Country reporting implementation package

12

Already implemented /

Implementation in progress

Expected to implement

Hard to predict

Current view on CbC implementation

Further to the release of final report on Action 13, the three-tier documentation package is designed to be implemented via

changes in domestic law by the end of 2016.

2. Global tax reset

13

3. What are the

new requirements?

3. What are the new requirements?BEPS-driven structure of transfer pricing documentation

14© 2015 Deloitte Belgium

Implementation framework

Timeline

Threshold

• Country-by-Country reporting to be filed from for fiscal years beginning

on or after 1 January 2016. First report due in 2017.

• Filing no later than 12 months after the last day of the Reporting Fiscal

Year of the MNE Group.

• Country-by-Country reporting would be required for MNEs with

revenues above 750 million Euro.

Filing &

information

exchange

• Jurisdictions should require CbC reporting from ultimate parent entities

of MNE groups resident in their country.

• Automatic information exchange with the relevant qualifying

jurisdictions in which the MNE group operates.

• Emphasis on the need to protect confidentiality of the tax information.15

3. What are the new requirements?

Notification

obligation

• Any Constituent shall notify the tax authority of its tax residence

country whether it is the Ultimate Parent Entity or Surrogate Parent

Entity who files the CBC Report

• If the Constituent is not the Ultimate Parent or Surrogate UP, it shall

report the identification and address of the UP or SUP.

Reporting

Entity

• Ultimate parent of MNE groups or

• Another Constituent of the MNE when the ultimate parent is located

in a country not having a Qualified Competent Authority Agreement

or is in Systemic Failure

• MNE may chose another Constituent Entity to file the CBC

16

Implementation framework

3. What are the new requirements?

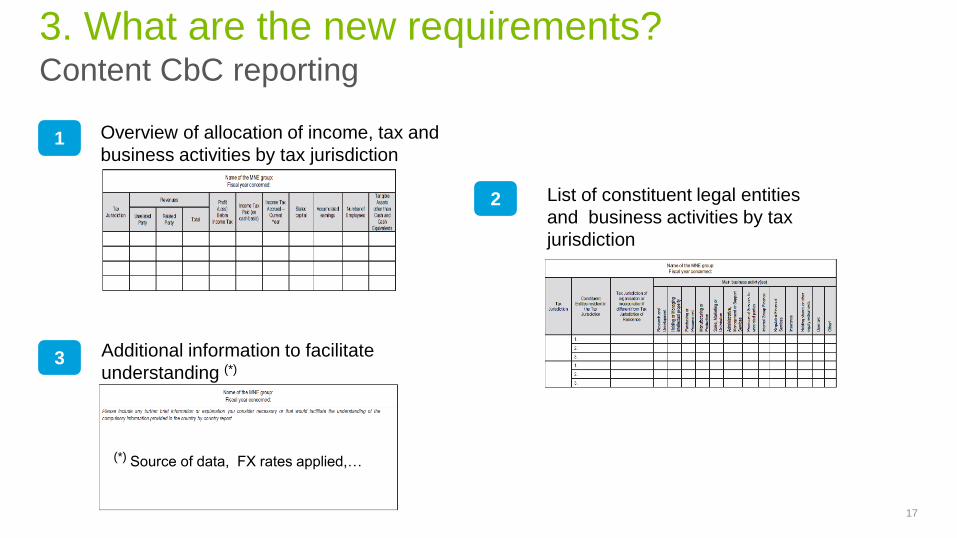

Content CbC reporting

17

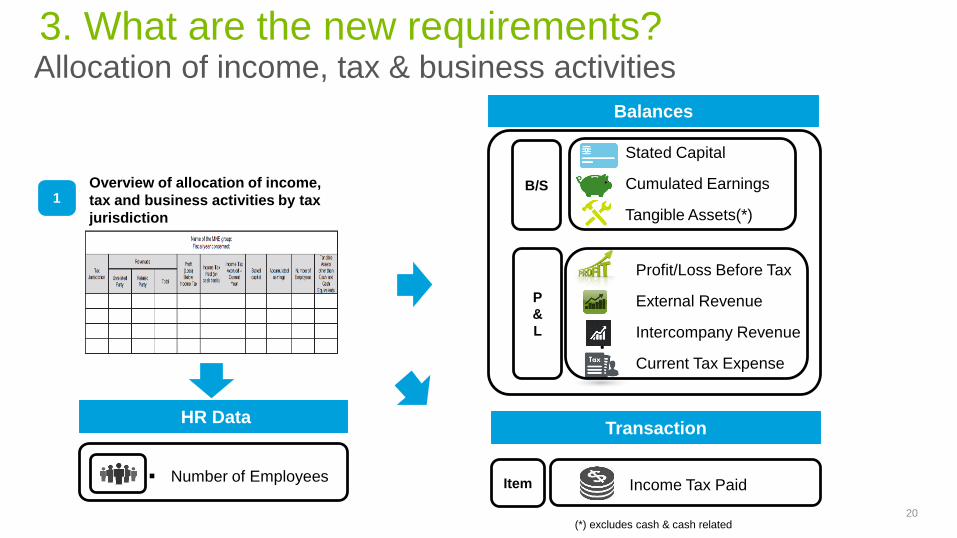

Overview of allocation of income, tax and

business activities by tax jurisdiction

List of constituent legal entities

and business activities by tax

jurisdiction

Additional information to facilitate

understanding (*)

1

2

3

(*) Source of data, FX rates applied,…

3. What are the new requirements?

1. Overview of allocation of income, tax and business activities by tax jurisdiction

18

3. What are the new requirements?

2. List of constituent legal entities and business activities by tax jurisdiction

19

3. What are the new requirements?

Allocation of income, tax & business activities

(*) excludes cash & cash related

Overview of allocation of income,

tax and business activities by tax

jurisdiction

1

Balances

Stated Capital

Cumulated Earnings

Tangible Assets(*)

B/S

P

&

L

Profit/Loss Before Tax

External Revenue

Intercompany Revenue

Current Tax Expense

Item Income Tax Paid#

HR Data

Number of Employees

Transaction

20

3. What are the new requirements?

21

4. How to get prepared ?

Different operating possibilities

22© 2015 Deloitte Belgium

Insource

• Potential lack of

expert knowledge

• Potentially more

expensive

• Risk of other

priorities

Outsource

• Access to expert

knowledge and

network

• Free up in-house

resources

• Customised

solutions

• Consistent and

proven approach

Co-source

• Access to expert

knowledge and

network

• Integrated approach

4. How to get prepared?

COLLECT FINANCIAL DATA CENTRALLY IN MGMT. GAAP FORMAT

+ less time consuming data collection process

- need to reconcile CbC data with local filings

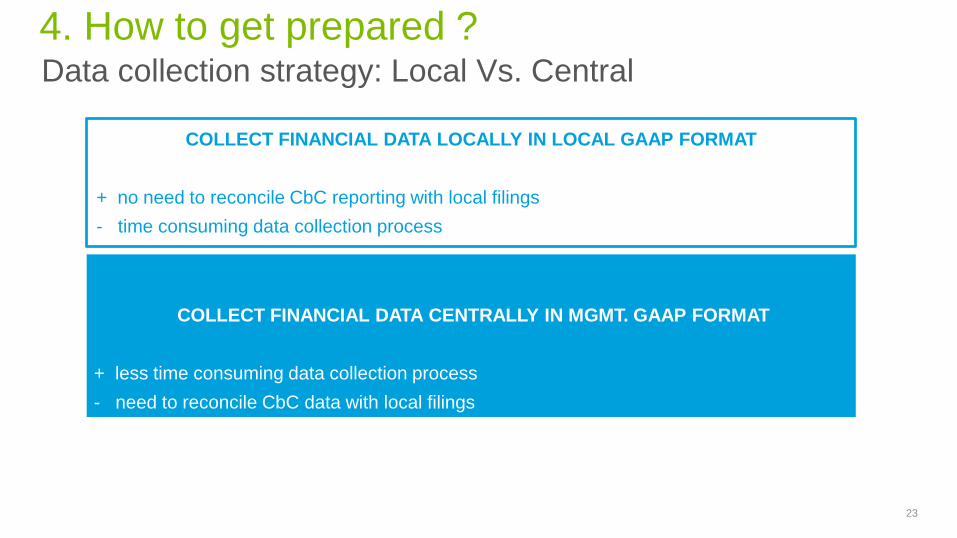

Data collection strategy: Local Vs. Central

COLLECT FINANCIAL DATA LOCALLY IN LOCAL GAAP FORMAT

+ no need to reconcile CbC reporting with local filings

- time consuming data collection process

23

4. How to get prepared ?

Identifying & extracting the right financial data source

Which System to use?

Accounting System

(ERP) SAP ECC

Oracle EBS

PeopleSoft

JD Edwards

Other…

Consolidation System

(EPM)

BPC

HFM

Cognos Controller

Other…

DataWarehouse

(BI)

BW

OBIEE

Cognos TM1

..

Number of System Instances

Granularity of Chart of Account

“Legal Entity” Dimension

Point of attentions

24

4. How to get prepared ?

Leveraging on an end-to-end statutory compliance process

• Calendar of

internal and legal

due dates

• Provide data

• Business information update • Clarify/confirm ad hoc matters• Review and

approve• Submit

Financial

Statements

and CIT return• Review of Financial Statements

and equity

• Review LTP, CITR

• Review and agree

calendar

• Governance and

process

• Upload TB’s

• Update mapping

• Upload integrated PBC data

• Check completion of PBC

• Conduct integrity checks

• Identify, prepare and document

Mgmt to Local GAAP and tax

adjustments

• Preparation of local GAAP TB,

Financial Statements and equity

reconciliation

• Prepare LTP, CITR

• Store on

Deloitte Tax

Insight

• Data analytics

Client

Deloitte

Local

Team

Deloitte

Central

Supporting

Technology

Deloitte Conversion Tool (DCT)

E-filing software

Data Collection Data ValidationData

Processing

Deliverable

Drafting

Review & Sign

off

Submit &

Archive

Mgmt.

Reporting

Process

Planning

CBC reporting Tool

Integrate CBC additional data

points in PBCs:

- Tax Cash

- Income by party

(IC/external)

Review

CBC & TP

ratios

Consolidate

CBC report

26

4. How to get prepared ?

26

CDX

CDX+

Te

ch

no

log

ical M

atu

rity

Functional Capabilities

Important note regarding attest clients: Neither CbC Digital Exchange (CDX) nor CDX+ (TMC tool) have been

approved for use by Restricted Entity Clients. Consult a QRM before discussing with a Restricted Entity.

Technology : Deloitte CbC reporting solutions

• Multiple ERP or

no ERP

• No dual GAAP

capabilities in

system or not

maintained /

used currently

• No uniform

Statutory

Accounts

Process /

System (Excel

based

adjustments)

4. How to get prepared ?

© 2015 Deloitte Belgium

Ratio 1 – Accumulated earnings vs Assets

As one can observe, CbC reporting eases the identification of tax / profit

discrepancies among Group (per country) from a high-level perspective.

CbC first experiencesTaxpayer: case 2

28

© 2015 Deloitte Belgium

As one can observe, CbC reporting eases the identification of

substance / profit discrepancies among Group (per country)

from a high-level perspective.

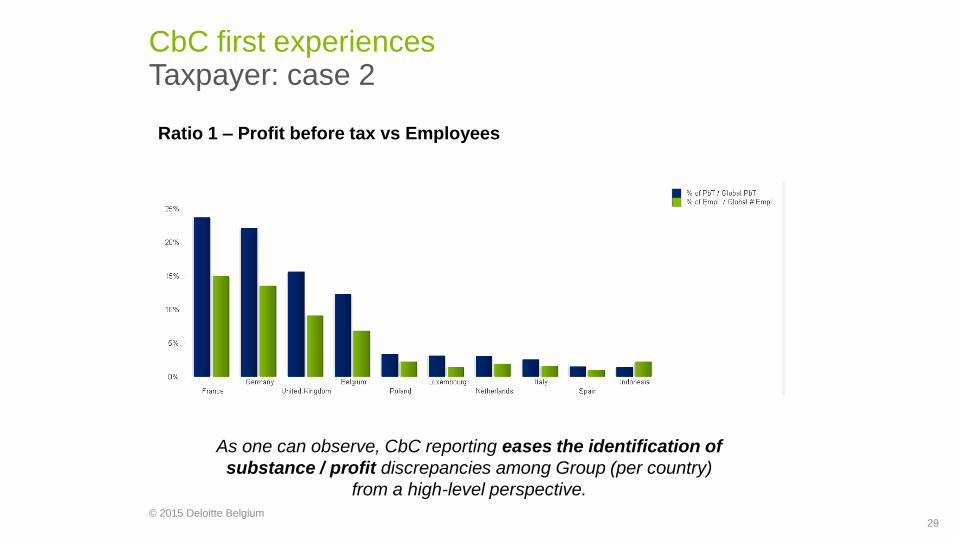

Ratio 1 – Profit before tax vs Employees

CbC first experiencesTaxpayer: case 2

29

29

Technology: Deloitte CDX / CDX+ - Live Demo

CDX: Data Collection - TP Ratios

4. How to get prepared ?

30

Technology: Deloitte CDX / CDX+ - Live Demo

CDX+: Audit Trail to Financial Systems - IFRS to Stat Rec - TP Ratios

4. How to get prepared ?

31

5. Conclusion

Key considerations to address in a CBC discussion

Risk Management

What/Where are the Group “material” legal entities?

25

5. Conclusion

Tax Audit Readiness

Can the main statutory differences be explained?

Opportunity

What else can be done with “CbC-like” data?

5. Conclusion

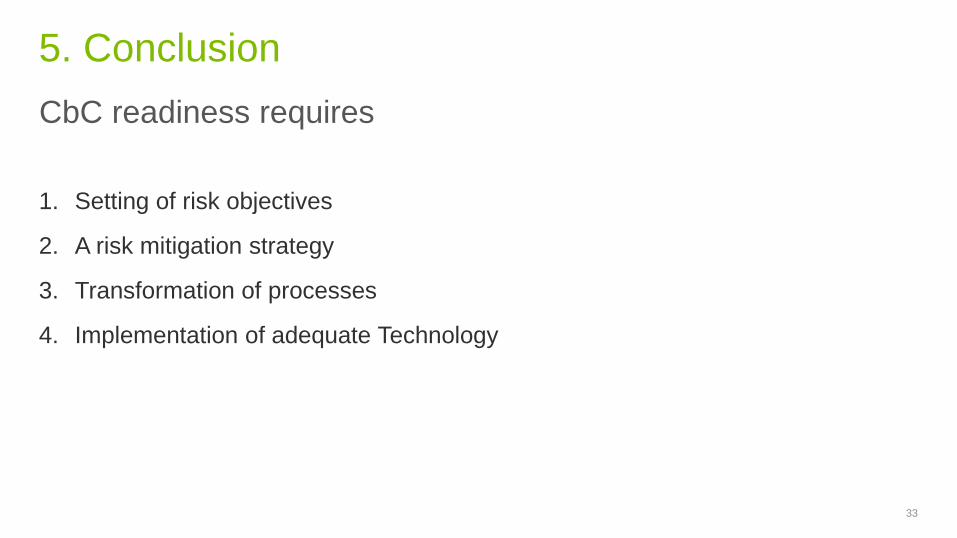

1. Setting of risk objectives

2. A risk mitigation strategy

3. Transformation of processes

4. Implementation of adequate Technology

33

CbC readiness requires

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member

firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most

complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte

Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained

by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 34

Transform today for the

challenges of tomorrow

Electronic tax audits:

Trends, risks and

approaches

1

Maison de L’automobile

15 December 2015

Rainer Eismayr – Director, Deloitte Germany

Pieter Van Dyck – Manager, Deloitte Belgium

Market trends & SAF-T in general

eAudits across Europe

Our approach & typical challenges

eAudit in Germany: deep dive & case study

eAudit in France: deep dive & case study

eAudit & your organisation

Contents

Market trends &

SAF-T

3

E-Data requirements

Common IT & ERP Landscape

ERP

Apportionment

Manual data

Depreciation

ERP

ERP

L1 L2

Financial systems

Main ERP

Legacy

Other

Extra

ct

Tra

nsfo

rmL

oa

d

Tax data warehouse

Transactions

data store

General ledger

data

Adjustments

data

Results data

Documentation

management

Tax compliance and assurance system

Tax desktop

Tax process management

Tax forms

Provision reports

Ad hoc reports

Reporting

and fillings

Reporting

and fillings

Analysis,

calculation,

adjustments

Income

Tax software

Tax provision

software

Sales/use tax

software

Analysis,

calculation,

adjustments

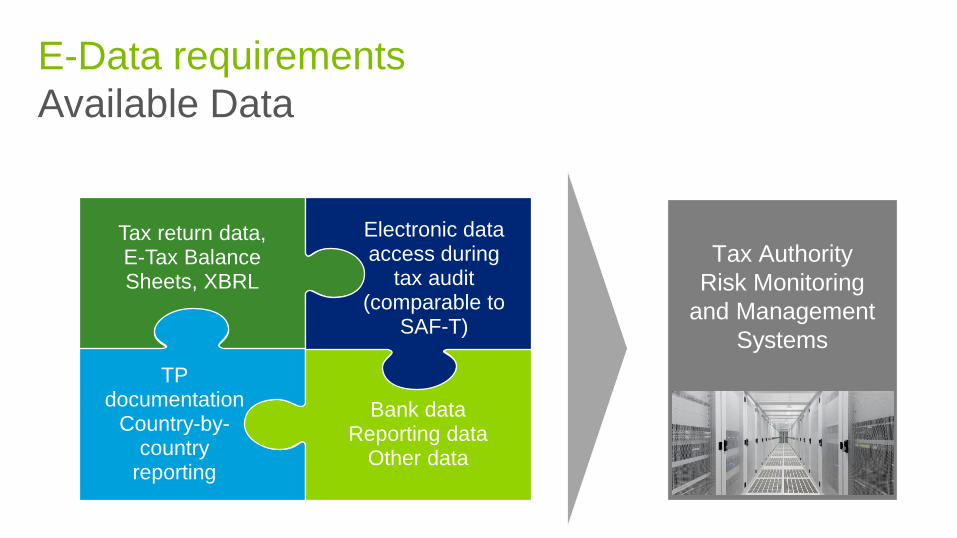

E-Data requirements

Available Data

TP documentation

Country-by-country

reporting

Electronic data access during

tax audit (comparable to

SAF-T)

Bank dataReporting data

Other data

Tax Authority

Risk Monitoring

and Management

Systems

Tax return data, E-Tax Balance Sheets, XBRL

E-Data requirements - Annual data mining

I. Master Data Tax Code

Accounts

Payable

Accounts

Receivable

Transfer

Pricing

II. Tax

Determination

III. Tax Reporting

Sales and Use Tax

Excise Tax

Customs

IFRS

Cross border reporting

Hidden data Known output

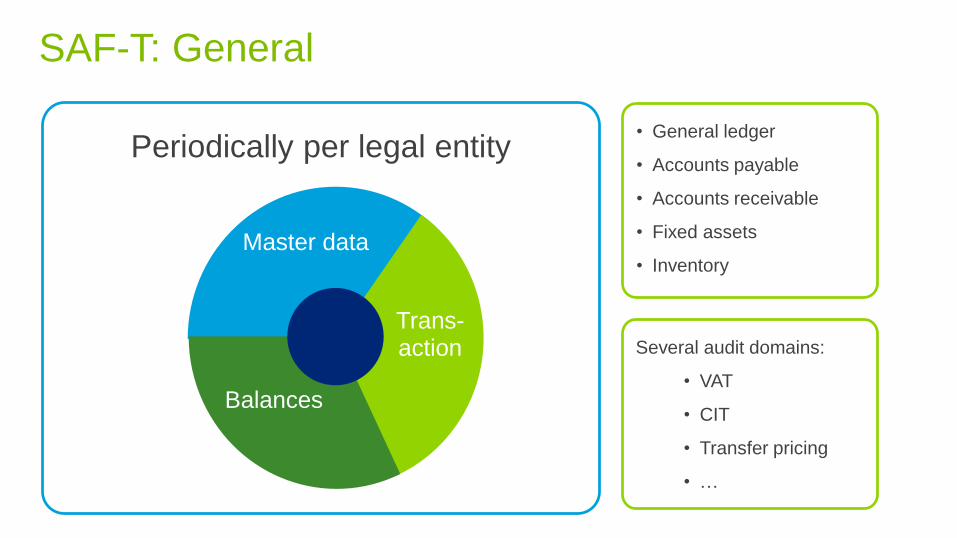

SAF-T

Periodically per legal entity• General ledger

• Accounts payable

• Accounts receivable

• Fixed assets

• Inventory

SAF-T: General

Several audit domains:

• VAT

• CIT

• Transfer pricing

• …

Master data

Trans-action

Balances

eAudit across

Europe

8

9

eAudit across Europe

Priority 1 countries

Portugal

France

Luxembourg

Germany

Hungary (2016)

Poland (mid 2016)

Priority 1

eAudit across Europe

Priority 2 & 3 countries

• Austria

• Belgium

• Finland

• Ireland

• Spain

• UK

• Czech Rep

• Denmark

• Netherlands

• Norway

• Slovenia

• Sweden

• Switzerland

• Bulgaria

• Cyprus

• Greece

• Italy

• Latvia

• Lithuania

• Malta

• Romania

Priority 2

Medium

Priority 3

Low

eAudit across Europe

Different levels of complexity & likelihood

Luxembourg

France Germany

• Any tax audit

• Local GAAP

• Exemptions for FSI

• SAF-T Lite

• At discretion of tax auditor

• All tax relevant data

• Scope of requested data can vary

Lik

elih

oo

d

High

Low

ComplexityLess data More data

Our approach &

typical

challenges

12

Technology Organisatio

n

Step 5

Analyze

> Review

significant

Business

event for the

period

> Review

Accounting

systems

landscape

> Review tax

audit history

Extract

Extract the tax

relevant data

from the ERP

system.

Tax relevant

data depends

on the

jurisdiction

Complement

Add relevant

working

documents:

> GAAP to

Stat

conversion file

> VAT

computation

Reconcile

Reconcile tax

eAudit file

with working

documents

Format

Format Tax

eAudit File

according to

local

requirements

Explain

Prepare

explanatory

notes

regarding the

various data

sets (eAudit

File, working

documents,..)

Archive

Store tax

eAudit Files,

Supporting

Documents &

Explanatory

notes on a

CD/DVD/Hard

drive

Step 6 Step 7Step 4Step 3Step 2Step 1

Our approach

Typical challenges

14

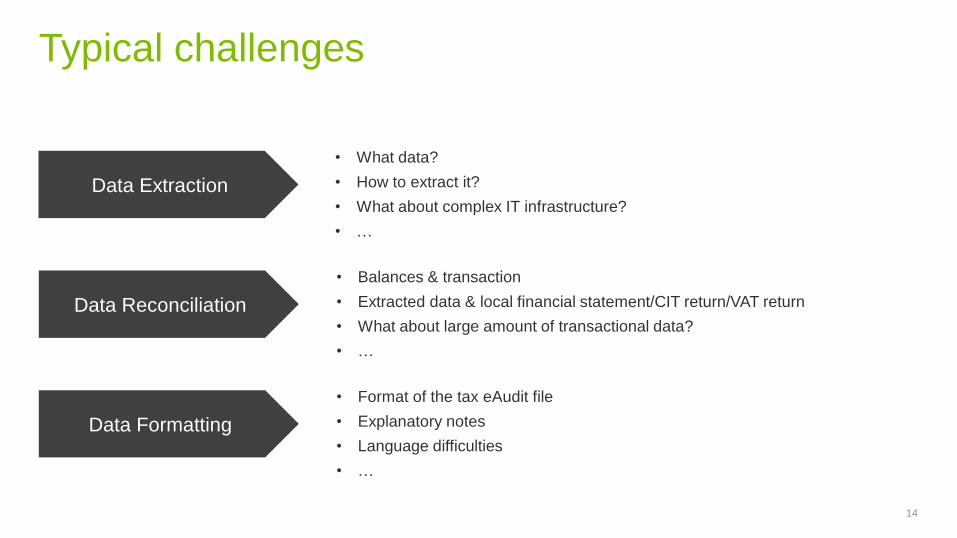

Data Extraction

• Balances & transaction

• Extracted data & local financial statement/CIT return/VAT return

• What about large amount of transactional data?

• …

Data Reconciliation

• Format of the tax eAudit file

• Explanatory notes

• Language difficulties

• …

Data Formatting

• What data?

• How to extract it?

• What about complex IT infrastructure?

• …

eAudit in

Germany

15

eAudit in Germany

Introduction

The rules governing the powers of the tax authorities are set out in detail in the German

Principles of electronic archiving of accounting and tax information, Data Access and the

Auditability of Digital Records (“GoBD”).

These rules define 3 levels of data access

• Direct (Z1)

• Indirect (Z2)

• eAudit file (Z3)

The eAudit file needs to contain all tax relevant data. German tax legislation does not provide

formal specifications regarding form & content of the tax eAudit data file.

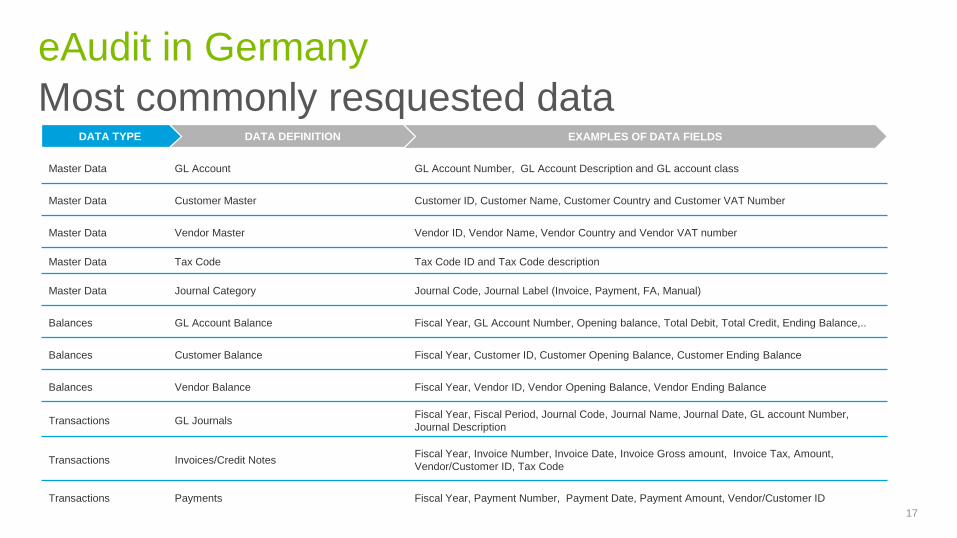

Most commonly resquested data

eAudit in Germany

17

Master Data GL Account GL Account Number, GL Account Description and GL account class

Master Data Customer Master Customer ID, Customer Name, Customer Country and Customer VAT Number

Master Data Vendor Master Vendor ID, Vendor Name, Vendor Country and Vendor VAT number

Master Data Tax Code Tax Code ID and Tax Code description

Master Data Journal Category Journal Code, Journal Label (Invoice, Payment, FA, Manual)

Balances GL Account Balance Fiscal Year, GL Account Number, Opening balance, Total Debit, Total Credit, Ending Balance,..

Balances Customer Balance Fiscal Year, Customer ID, Customer Opening Balance, Customer Ending Balance

Balances Vendor Balance Fiscal Year, Vendor ID, Vendor Opening Balance, Vendor Ending Balance

Transactions GL JournalsFiscal Year, Fiscal Period, Journal Code, Journal Name, Journal Date, GL account Number,

Journal Description

Transactions Invoices/Credit NotesFiscal Year, Invoice Number, Invoice Date, Invoice Gross amount, Invoice Tax, Amount,

Vendor/Customer ID, Tax Code

Transactions Payments Fiscal Year, Payment Number, Payment Date, Payment Amount, Vendor/Customer ID

DATA TYPE DATA DEFINITION EXAMPLES OF DATA FIELDS

Risks & Penalties for non complianceeAudit in Germany

Penalties up to 250.000 EUR in case:

• Electronic bookkeeping maintained abroad without prior authorization

• Data access not provided to tax auditor within a reasonable timeframe

Bookkeeping not kept in accordance with German tax Law can lead to:

• Ex-officio assessment (Estimation of German tax base)

• Electronic bookkeeping (Server) to be relocated (back) to Germany

• GL bookkeeping process of German Tax Payer to be relocated (back) to Germany

18

Tools & Auditing method used by tax authorities eAudit in Germany – Periodic data mining

• Electronic tax data testing

• Software publicly available for sale

19

AIS Tax Audit and

IDEA

Macros

• Set of different macros at disposal

• Reproduce typical tax audits tests for income, wage and

value added tax

eAudit in Germany – Periodic data mining

Tools used by the German tax authorities

Example: Tax officer looking for non-deductible expenses for tax purposes

• AIS Tax Audit: query to detect non-deductible expenses like donations, penalties or

presents which are not accounted correctly

• Following steps are carried out by the tax officer:

1. Mapping of the relevant fields

2. Determination of filters (e.g.: GL accounts, keywords)

3. Preparation of a file including the relevant accounting lines

4. Preparation of a documentation regarding the findings

eAudit in Germany – Periodic data mining

Example / best practicesA. Mapping of the relevant fields Mapping

ERP

tables as

uploaded

into the

software

by the tax

auditor

Required

data fields

to

perform

the test

macro

eAudit in Germany – Periodic data mining

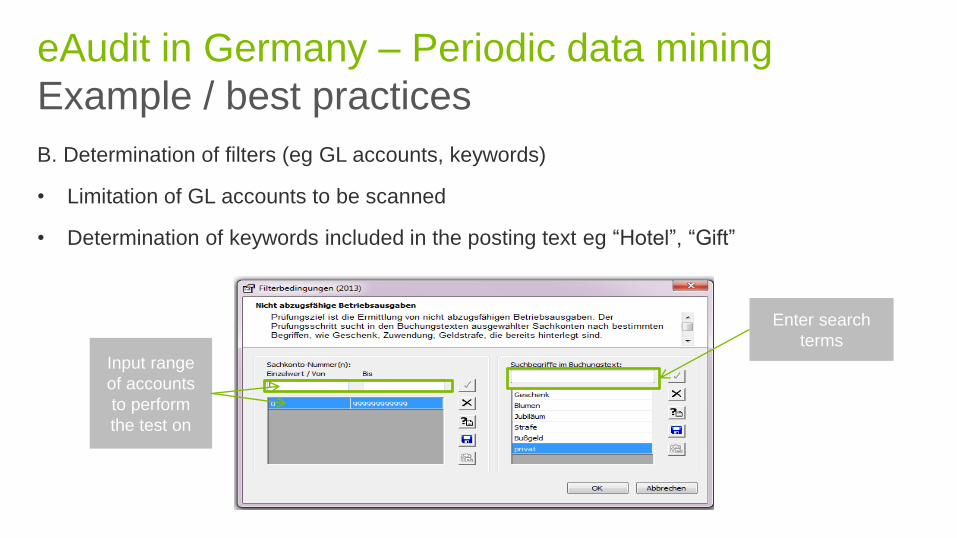

Example / best practices

B. Determination of filters (eg GL accounts, keywords)

• Limitation of GL accounts to be scanned

• Determination of keywords included in the posting text eg “Hotel”, “Gift”

Input range

of accounts

to perform

the test on

Enter search

terms

eAudit in Germany – Periodic data mining

Example / best practices

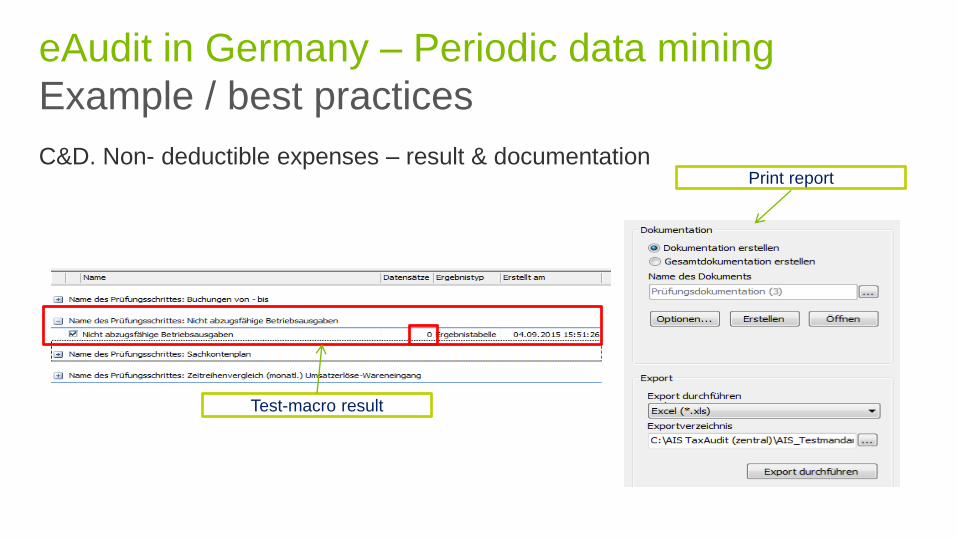

C&D. Non- deductible expenses – result & documentation

Test-macro result

Print report

eAudit in Germany – Periodic data mining

Example / best practices

C&D. Non- deductible expenses –

result & documentation

• Direct display findings with regard to

the non-deductible expenses

> all expenses are booked correctly /

incorrectly

• Tax auditor can prepare a

documentation regarding

his / her findings during the audit

• All validation routines in the software

can be performed

by the tax auditor in one batch, i.e.

very low effort with a

high statistical likelihood to find errors

leading to additional

tax assessments at the end of the tax

audit

eAudit in Germany

Case study

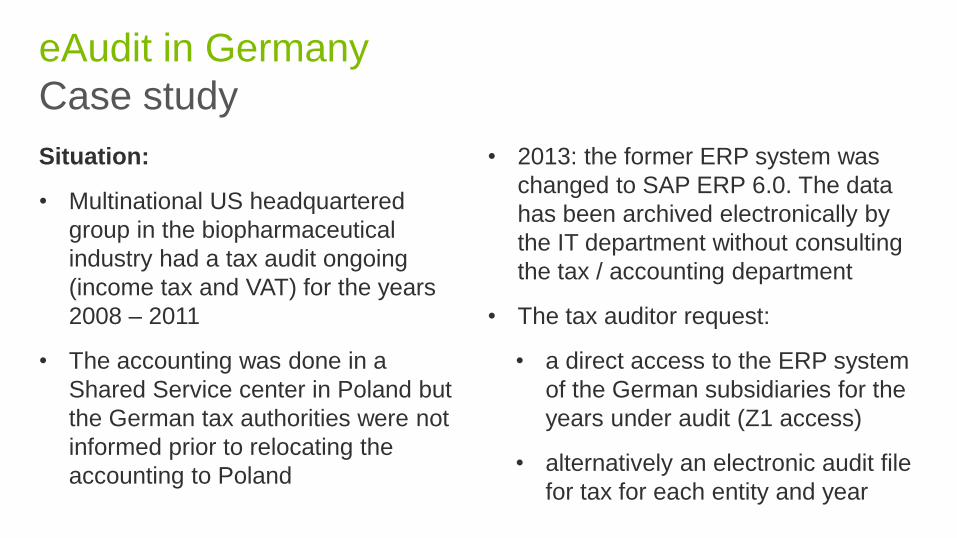

Situation:

• Multinational US headquartered

group in the biopharmaceutical

industry had a tax audit ongoing

(income tax and VAT) for the years

2008 – 2011

• The accounting was done in a

Shared Service center in Poland but

the German tax authorities were not

informed prior to relocating the

accounting to Poland

• 2013: the former ERP system was

changed to SAP ERP 6.0. The data

has been archived electronically by

the IT department without consulting

the tax / accounting department

• The tax auditor request:

• a direct access to the ERP system

of the German subsidiaries for the

years under audit (Z1 access)

• alternatively an electronic audit file

for tax for each entity and year

eAudit in Germany

Case study

Issue:

An analysis revealed that the former system could not be restored. A review of the

electronic data files showed that the data was not in line with the German financial

statements as the US-GAAP to German GAAP bridge was missing in the data

files.

Tax auditor threatened to estimate the taxable profits which would have led to

additional income taxes of approx. € 5mio.

eAudit in Germany

Case study

Outcome:

Client had to

• Go through a full restructuring exercise of the electronic raw data to prepare the

data in accordance with the financial statements in order to avoid an estimation

of the tax base and a relocation of the accounting back to Germany

• Draft new eAudit files for all years under audit

Recommendation:

Prepare the electronic audit files each year together with the filing of the tax return

in order to avoid issues with the tax authorities in a later tax audit.

© 2014 Deloitte LLP. All rights reserved.

eAudit in France

28

eAudit in France

Introduction

eAudit Legislation into force since

01/01/2014 for all years open for audit

The eAudit legislation is applicable on:

• Legal entities

• Branches

• Non established VAT registered

entities

A transactional French GAAP tax eAudit

file (FEC - Fichier d’Ecritures

Comptables) must be submitted to the

French tax administration (FTA) at the

beginning of the tax audit.

The eAudit file has a fix format and

contains 18 mandatory fields

eAudit in France18 mandatory fields

Field name Information

1. JournalCode The journal entry code

2. JournalLib The journal entry label

3. EcritureNum The accounting entry number

4. EcritureDate The accounting date

5. CompteNum The account number

6. CompteLib The account label, under the French Accounting Plan

7. CompAuxNum The sub-ledger account number

8. CompAuxLib The sub-ledger account label

9. PieceRef Supporting document reference

10. PieceDate Supporting document date

11. EcritureLib Accounting entry label

12. Debit Debit amount

13. Credit Credit amount

14. EcritureLet “Apply-to/clearing” entry

15. DateLet Clearing date

16. ValidDate Posting date

17. Montantdevise Currency amount

18. Idevise Transaction currency name

eAudit in France

Risks & penalties for non-compliance

Limited administrative penalty, eAudit file remains due

Application of the ‘ex officio’ procedure

• Reversal of the burden of the proof from the start of the audit

• Additional 100% penalty computed on additional amounts of taxes to be paid at

the end of the audit.

eAudit in France

Case study

Situation:

A multinational operating in the IT

industry has an tax audit ongoing (VAT

& CIT) and generates the eAudit file for

3 years.

The client engages Deloitte for a

technical validation of the file.

After testing the file is provided to the

auditor.

The auditor challenges several entries

as it seems that eg some sales invoices

are booked as cost minus instead of

revenue.

eAudit in France

Case study

Issue:

Analyses disclose that the mapping

done between management GAAP and

French GAAP is incorrect. Several

turnover accounts in management

GAAP are mapped to French costs

accounts etc

Outcome:

Client had to

• Revise mapping & update their ERP

system

• Draft 3 new eAudit files

• Draft 3 corrected financial statements

Additional, the processes were heavily

challenged and an additional IT audit

was launched.

© 2014 Deloitte LLP. All rights reserved.

eAudit & your

organisation

34

eAudit & your organisation

Conclusion

• Large volumes

• Extraction programs

• Assembly & storage

• ERP localizations

• Local adjustments

• Reconciliations

• Extraction – storage

• Data sources

• Data collection

• Data limitations

• Audit trail

• Legacy systems

• Policy review

• Process manuals

• Training

• Roles and

responsibilities

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of excellence.

This communication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member firms, and their related entities (collectively, the “Deloitte Network“). None of the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 36

Transform today

for the challenges

of tomorrow

Invoice

Management

1

Maison de L’automobile15 December 2015

Hilde Vandeperre – Director, Deloitte BelgiumSara Claeys – Manager, Deloitte Belgium

1. Introduction

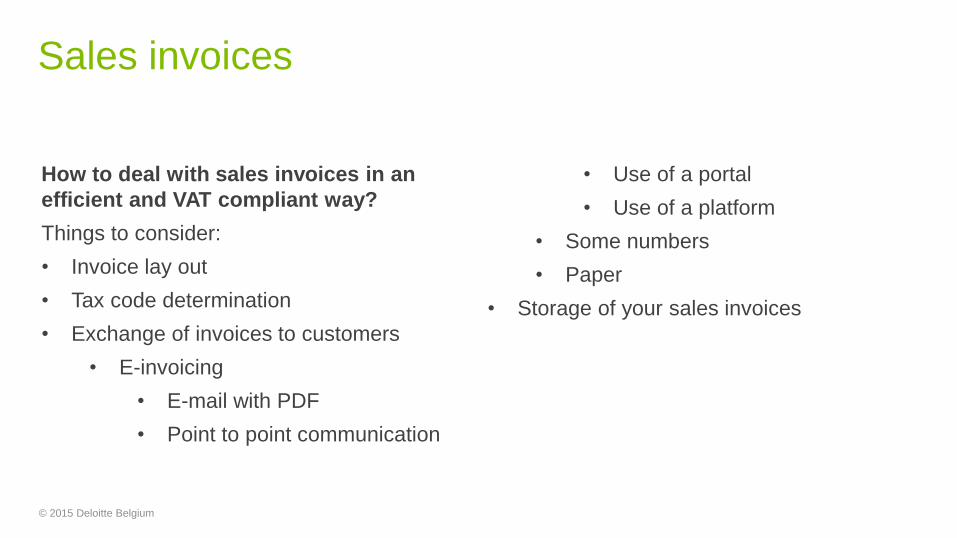

2. Sales invoices

3. Purchase invoices

4. Other relevant documents

5. Conclusions

Contents

© 2015 Deloitte Belgium 2

Introduction

© 2015 Deloitte Belgium

Although largely

harmonized, we need to

check which Member

State’s rules apply.

LEGISLATION

AUTOMATION

Automate as much as you

can but in a smart way.

HIGH VOLUMES

How to deal with high volumes

of invoices in an efficient but