tower resources research report 19.11.2007

TRANSCRIPT

Tower Resources plc

Year

End 31 Dec

Revenue

(US$000s)

PBT

(US$000s)

FRS3

EPS

(US$)

FRS3

DPS

(US$)

PE

(x)

Yield

(%)

2006a 0.00 (940) (0.01) 0.00 n/a 0

2007e 0.00 (3,500) (0.08) 0.00 n/a 0

2008e 0.00 (5,750) (0.11) 0.00 n/a 0

2009a 0.00 (11,650) (0.22) 0.00 n/a 0

Company Review

Investment Summary: An African Star in the making

Tower Resources is an AIM listed company, with exciting exploration assets in Uganda and

Namibia. In Uganda, the Company holds Block EA5, a wholly-owned onshore block of 6040 sq

kms at the northern end of the Albertine Graben. In Namibia, Tower Resources acquired three

offshore blocks that cover an area of approximately 23,000 sq kms. Tower Resources is likely to

drill a number of wells in Uganda next year and a first well in 2009. Tower Resources is fully

funded and does not need to raise additional funds in the foreseeable future

Uganda

The Company holds a wholly-owned onshore block of 6040 sq kms at the northern end of the

Albertine Graben. The block’s prospective basin is the Rhino Camp, where gravity

interpretation has shown large structural features of 35 sq kms. The Company is currently

shooting 285 kilometres of 2D Seismic with the expectation of drilling two wells next year.

Namibia

In Namibia, Tower Resources acquired three offshore blocks that cover an area of 23,000 sq

kms. Tower Resources has interpreted 10,000 kms of 2D Seismic and has undertaken a

comprehensive geochemical study as well as a surface oil seep survey. The Company has

identified 18 leads, with the resource potential between 40m – 5bn bbls of oil or 10 TCF of

natural gas. Tower holds a 15 % carried interest in the three blocks.

Financials

We expect the Company to report a net loss of US$3.5m in 2007 compared with a net loss of

US$1m the previous year. The losses are likely to increase considerably if the Company

discovers and develops a large hydrocarbon field in either Uganda or Namibia.

Valuation

We can assign a minimum value of £22.5 - 25m for Tower Resources by the implied minimum

expenditure of the farm-outs of its Ugandan and Namibian assets. Our financial model for the

Company’s discounted cash flows on our risked hypothetical resource base gives a value of

£290m compared to the current market value of £14.8m.

November 2007

Price (p) 2.75

Market Cap £m 14.8

Chart

SHARE DETAILS

CODE TRP

LISTING AIM

SECTOR Oils

SHARES IN ISSUE 536.7

PRICE

52 weeks

High 3.88

Low 1.75

BALANCE SHEET

Debt/Equity 2008e (%) 37

NAV (£m) 25-290

(Net borrowings)/Cash

(US$m) (27)

BUSINESS

Tower Resources is an AIM listed

company, with exciting oil and gas

exploration assets in Uganda and

Namibia. In Uganda it is currently

preparing to shoot 285 kilometres of

seismic with the expectation of drilling

two wells next year. In Namibia, 700

km of 2D Seismic was re-interpreted

and it is planning to shoot 3D Seismic

next year.

GEOGRAPHY (Revenues US$m)

UK UGANDA NAMIBIA OTHERS

0 0 0 0

ANALYST

Brian McBeth +44 (0)20 7920 3390

SALES

Paul Backhouse +44 (0)20 7920 3391

2 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

Investment Summary: A new African Star

Tower Resources to start

drilling in 2008

Tower Resources is an AIM listed company, with

exciting exploration assets in Uganda and Namibia.

In Uganda, the Company holds Block EA5, a

wholly-owned onshore block of 6040 sq kms at the

northern end of the Albertine Graben. In Namibia,

Tower Resources acquired three offshore blocks that

cover an area of approximately 23,000 sq kms.

Tower Resources is likely to drill a number of wells

in Uganda in 2008 and in Namibia in 2009. Tower

Resources is fully funded and does not need to raise

additional funds in the foreseeable future.

Valuation: significant

exploration upside

The main driver in the oil industry is the oil price,

which is currently above US$90/bbl for WTI crude.

Oil prices have remained at relatively high levels for

the last 24 months, mainly because of strong demand

driven by economic growth, the decline in OPEC

production and political instability in the Middle

East. During this period, Nigerian production has

fallen by 500,000 bopd because of the activities of

insurgents in the country. In addition, Iran and

Venezuela have been unable to meet their OPEC

quotas, Indonesia is in long term decline, and Iraq

continues to be plagued by terrorist attacks. This

has resulted in OPEC crude oil output declining

from around 31.6 m bopd during the fourth quarter

last year to current levels of around 30.7m bopd.

OPEC has agreed to increase production by at least

0.5m bopd but this is insufficient to reverse the

inexorable upward increase in crude oil prices. There

is however a view that if world economic growth

starts to slow down as a result of a general increase

in interest rates that oil prices could weaken in 2008.

We can assign a minimum value of £22.5 - 25m for

Tower Resources by the implied minimum

expenditure of the farm-outs of its Ugandan and

Namibian assets. We have also modelled five

prospective oil and gas prospects detailed below, and

have risked the results for success in the following

manner: an assumed success rate of 25 % for 100m

bbls, 20 % for 150m bbls, 15 % for 200m bbls and 10

% for 250m bbls; and 10 % for the Namibian

prospects. We have also calculated the NPVs using

various discount factors as well as a constant crude

oil price of US$70/bbl and declining crude oil prices

to US$22/bbl in 2017. Although current crude

prices are above US$90/bbl and the futures crude oil

curve to 2015 stands at US$80/bbl we have used

US$70/bbl to maintain our conservative position.

Our matrix gives a conservative risked resource

NPV of £290m.

Sensitivities: four main

challenges

The Company faces three main challenges:

• To find hydrocarbon resources in both Uganda

and Namibia.

• The thermal maturity of the source rocks could

be the main exploration risk.

• To secure a drilling rig in the required time

frame.

• Managing social and environmental issues in

emerging oil provinces.

Financials

At the end of June 2007, Tower Resources had cash

balances of £2.13m, after spending £0.48m in

capital expenditure and a reported loss for the six

months to 30 June 2007 of £0.25m. For the current

year we expect the Company to report a net of loss

of US$3.5m.

We have estimated the Company's Profit & Loss,

Balance Sheet and Cash Flows up to 2009. In our

financial projections, we have used a declining crude

oil price from US$70/bbl in 2007 to US$63.18 in

2009. The hypothetical financial projection shows

that if Tower Resources found a 100m bbls field in

Uganda and assuming it receives world crude oil

prices that it could report negative operating cash

flows of US$12m in 2009. Its balance sheet will

clearly deteriorate as its capital expenditure

increases significantly after 2009 with an estimated

closing net debt of US$48m in 2009.

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 3

The road to the Albertine & Dolphin

Grabens

HISTORY In August 2005, Tower Resources was admitted to the AIM market. A few months later in January

2006, it acquired Neptune Petroleum, which hold licences in northern Uganda and offshore northern

Namibia. Tower Resources paid for the acquisition by issuing 200 m shares to the Neptune equity

holders Peter Blakey, Peter Taylor and Mark Savage through his Bayview Investments LLC. Through

Neptune, Tower Resources acquired exploration acreage in two of the hottest plays in Africa at the

moment. In Uganda, Tower Resources holds a 100 % stake in Exploration Area (EA) 5 in the

prospective Albertine Graben. Block EA5 is the largest licence so far awarded by the Uganda

Government covering an area of 6040 sq kms. In Namibia, Tower Resources holds a 15 % stake in three

offshore exploration blocks that cover an area of approximately 23,000 sq kms after Arcacia farmed in to

its acreage.

UGANDA - Background The recent large discoveries made by Tullow Oil, Hardman (now part of Tullow) and Heritage Oil &

Gas have made Uganda one of the hottest areas for hydrocarbon exploration. There is no petroleum

production in Uganda presently, but the recent large discoveries make it clear that the country has the

potential of becoming a big crude oil producer in the near future.

The main prospective area for finding hydrocarbon reserves in Uganda is the Albertine Graben, which

is the northern extension of the western arm of the East African Rift Valley, stretching some 500 kms

from Sudan in the north to Lake Edward in the south. The Albertine Graben is commonly 45 kms wide

and extends in some parts into the Democratic Republic of Congo. To the north of Lake Albert in Sudan

there is large oil production in the Thar Jath, Heglig and Unity fields in the Muglad Basin, which are

producing around 260,000 bopd.

The Albertine Graben is regarded as a particularly prospective area for oil exploration in the East

African Rift Valley. The Albertine Graben can be compared to other large basins in Africa such as the

Muglad basin in Sudan and the Gulf of Suez basin in Egypt. The basins found in the Albertine Graben

are bounded by dip-slip and oblique-slip fault systems that are typically 100 km long dating to the

Miocene. It is thought that boundary faults in the Albertine Graben vary from 600 metres to around

5000 metres in depth in parts. The Graben is in turn sub-divided into smaller basins such as Lake

Albert, Semliki, Lake Edward, Lake George, and Rhino Camp. Good reservoirs with porosities

exceeding 30% are found in the Tertiary sandstones as shown by the 1938 Waki-B1 deep test well that

encountered shows in the Tertiary sands and shales. The presence of good source rocks is inferred from

surface oil seeps that have been known for many years. For example, a sandstone outcrop at Kibiro is

saturated with 14.7 gravity oil with a sulphur content of 0.31%. In addition, two boreholes drilled close

by found heavy asphalt oil of 15.9 gravity.

Exploration History

Exploration for oil and gas in Uganda started in 1913, when W. Brittlebank acquired a licence to

explore for crude oil. Further licences were awarded in 1920-21, but no exploration was undertaken. A

number of reconnaissance field surveys, acquisition of gravity data, the drilling of shallow stratigraphic

tests, and the drilling of two deeper exploratory tests were undertaken between 1920-40. The period

from 1947-90 was dominated by work done by the Uganda Geological Survey, which included a World

Bank funded Petroleum Exploration Promotion Project started in 1983. Since 1991, the Petroleum

Exploration and Production Department of the Ministry of Natural Resources has been active in

geological mapping, gravity and magnetic surveys.

The Albertine Graben, one

of the hottest plays in Africa

The Albertine Graben can

be compared to the Gulf of

Suez basin in Egypt

4 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

It is clear that the Albertine Graben is underexplored, with reports of oil seeps dating as far back as

1925 when 52 separate hydrocarbon occurrences were logged around Lake Albert, with nine of these oil

seeps still active today. In the past, several stratigraphic tests were drilled but these were shallow wells.

In 1938, Shell Oil drilled the deepest exploration well to date to a depth of 1,232 metres. For the next

half century very little activity took place until the mid 1990s when the government using aerial,

gravity and magnetic surveys divided the area into five exploration zones. So far, five sedimentary areas

have been identified with sediments in some areas of more than 5 kms thick. The Rhino Camp Basin is

located within Tower Resources' EA5 block with good hydrocarbon resource potential by analogy to

other basins in the Albertine Basin. The main exploration risk is considered to be the thermal maturity

of the source rocks.

The Uganda government so far has awarded five exploration blocks (detailed below), with Tower

Resources holding the largest one.

Table I: Uganda Exploration Acreage

Size km2 Company Basin Activities

Exploration Area 1 4,285 Tullow/ Heritage Pakwach Current seismic + 3 wells in 2008.

Exploration Area 2 4,675 Tullow (Hardman Petroleum)

Mother Lake Albert Waraga-1 12000 bopd & 3 wells in Kaiso-

Tonya

Exploration Area 3 4630 Heritage Oil & Gas/ Tullow

Semliki & Southern Lake Albert

Kingfisher-1 14,000 bopd

Exploration Area 4 2021 Dominion Oil & Alpha Oil (Uganda)

Lakes Edward-George

Exploration Area 5 6040 Tower Resources Rhino Camp Seismic to be shot later this year,

followed by two exploration wells in

2008

Source: VSA Capital

Exhibit I:Uganda: Explorations Blocks

Rhino Camp basin good

hydrocarbon resource

potential

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 5

Source: Tower Resources

Tower Resources' Fiscal Terms

Tower Resources' exploration licence is for six years and is divided into three exploration periods: (1) an

initial exploration period of two years; (2) a first extension period of two years; and (3) a second

extension period of two years. A mandatory relinquishment takes place at the end of each exploration

period. A production licence is awarded for 25 years with a possibility of a five year extension after

approval of a development plan and the fiscal regime includes a sliding scale royalty of 5% - 12.5 % and

a Production Sharing Agreement (PSA).

6 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

Recent Discoveries

In 2006, five wells were drilled in the Albert Basin, all of which were discoveries. In Block EA2, the

Waraga-1 well tested 12050 bopd and in November 2006 in Block EA3 a shallower zone was tested on

the Kingfisher prospect that yielded 4120 bopd of 30 API, with a low gas-oil ratio. Earlier this year,

Heritage drilled a deeper well on its Kingfisher discovery which tested 13,893 bopd across four potential

pay zones with a net pay of 37 metres. It is estimated that the Kingfisher prospect could hold more than

500m bbls of upside potential, and this estimate does not take into account the primary deep target

because the well did not reach it owing to problems with the drilling rig. The well did however intersect

three hydrocarbon zones, thereby derisking the deeper primary target that will be drilled in 2008. The

Kingfisher reservoirs are sandstones of Tertiary age and the prospect could extend over 70 sq kms.

Tullow also drilled the Nzizi-2 and Mputa-3 wells on its Kaiso-Tonya appraisal programme in Block

EA2, with both wells encountering hydrocarbons. The Mputa-3 well intersected three oil-bearing

zones, with a total net pay of 19.5 metres, the best result to date in the appraisal programme. Well data

indicates that all three zones in Mputa-3 could flow at a combined rate of more than 4,000 bopd of oil,

and the well was suspended as a future producer The Mputa-4 appraisal well, drilled 1 km east of the

Mputa-1 discovery, was to test an adjacent fault block, with the well reaching just over 1000 metres in

depth and encountering three oil-bearing zones with a total net pay of 15.4 metres. Downhole pressure

testing and sampling of Mputa-4 has shown moveable light, sweet crude with very good permeability,

as seen in the other Mputa wells.

The data compiled from the drilling programme has confirmed the extent of the reservoir sands.

Heritage estimates its risked reserve base in the country at 643m bbls in Block EA1 and 330m bbls in

block Block EA3, while Tullow estimates its risked reserve base in Uganda at 100-250m bbls.

Early Production

It is possible that commercial oil production in Uganda could start as early as 2009 with Heritage Oil

and Tullow Oil supplying light, sweet crude from their exciting discoveries to be used locally to

produce kerosene and other fuels, as well as supplying feedstock to a small power plant. This is part of

the government's Early Oil Production scheme that involves building a mini-refinery to produce diesel,

kerosene and heavy oil, and, in addition, building a heavy fuel oil-based power plant to generate cheap

electricity. According to President Yoweri Kaguta Musewi in a speech given in October 2006, Uganda

will be able to ‘produce oil-based electricity that is almost comparable to hydro-electricity at a cost of

about six American cents per unit. This is a far cry from the present 24 American cents per unit of

electricity using imported diesel without subsidies’. In 2006, Uganda imported the equivalent of just

over 10,000 bopd at a cost of US$443.3m. The increase in domestic crude oil production will have a

favourable impact on the country’s balance of payments. In addition, both companies are currently

trying to determine whether to start laying a US$2 bn, 1,300 km export pipeline to Mombassa, the

Kenyan port which serves land-locked Uganda.

Recent large discoveries:

Waraga-1 12,050 bopd &

Kingfisher-1 13,893 bopd

Risked reserve base 100 -

973m bbls

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 7

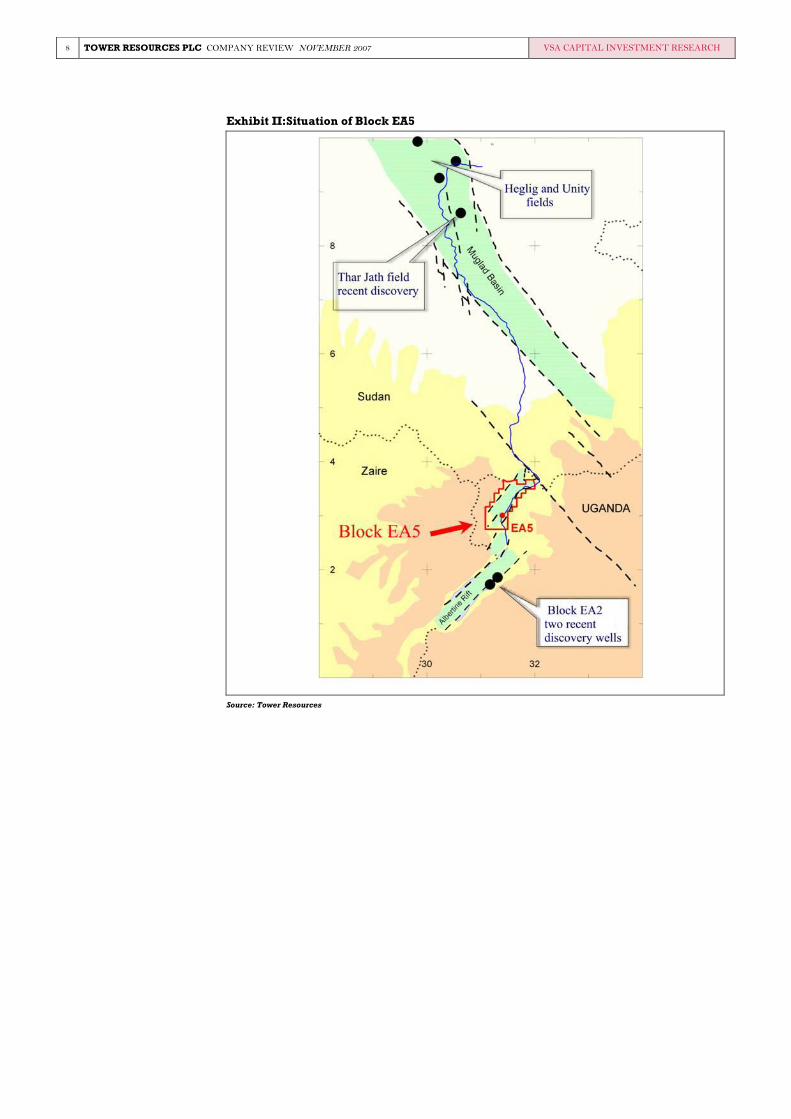

Block EA5

Tower Resources holds a 100 % interest in Block EA5, the largest block awarded so far in the country

covering an area of 6040 sq. kms at the northern end of the Albertine Graben. The Rhino Camp basin

located on the block is an unexplored basin with good potential by analogy to the recent discoveries

detailed above made by Heritage and Tullow.

It is anticipated that there is a high probability of finding large structures with good reservoirs in the

Rhino-Camp basin. According to Tower Resources, geochemical studies indicate that source rocks could

be mature below 2000 metres, while gravity modelling shows large structures. In addition, anecdotal

evidence suggests that extensive local oil seepages have occurred on the acreage and that some recent

water wells have been contaminated with crude oil. Moreover, the region has a number of hot springs

indicating locally high subsurface temperatures. Furthermore, gravity interpretation shows large

structural features of 35 sq kms. If the current porgramme of 285 kms of 2D seismic lines together with

the drilling of its two commitment wells next year confirms such an interpretation, then it is likely that

Tower Resources will find some very large structures when its exploration drilling campaign is

completed in 2008.

There are no major ecological problems and because the block is not over Lake Albert or Lake Edward

it will be easier to conduct seismic surveys and drill wells. This means that Tower Resources will be

able to catch up with the existing companies operating in the country. In addition, there is a moratorium

on the allocation of new licences even though 30 companies since 2005 have applied for them. This will

allow the current licensees to drive the initial stage of development.

Tower Resources has set up offices in Kampala, the country’s capital, as well as a regional operational

centre at Arua. Tower Resources is also embarking on a programme of community social investment

focused on higher education, health and infrastructure improvements.

Rhino Camp basin: good

potential by analogy

Local anecdotal evidence of

extensive local seepages

No ecological problems

8 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

Exhibit II:Situation of Block EA5

Source: Tower Resources

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 9

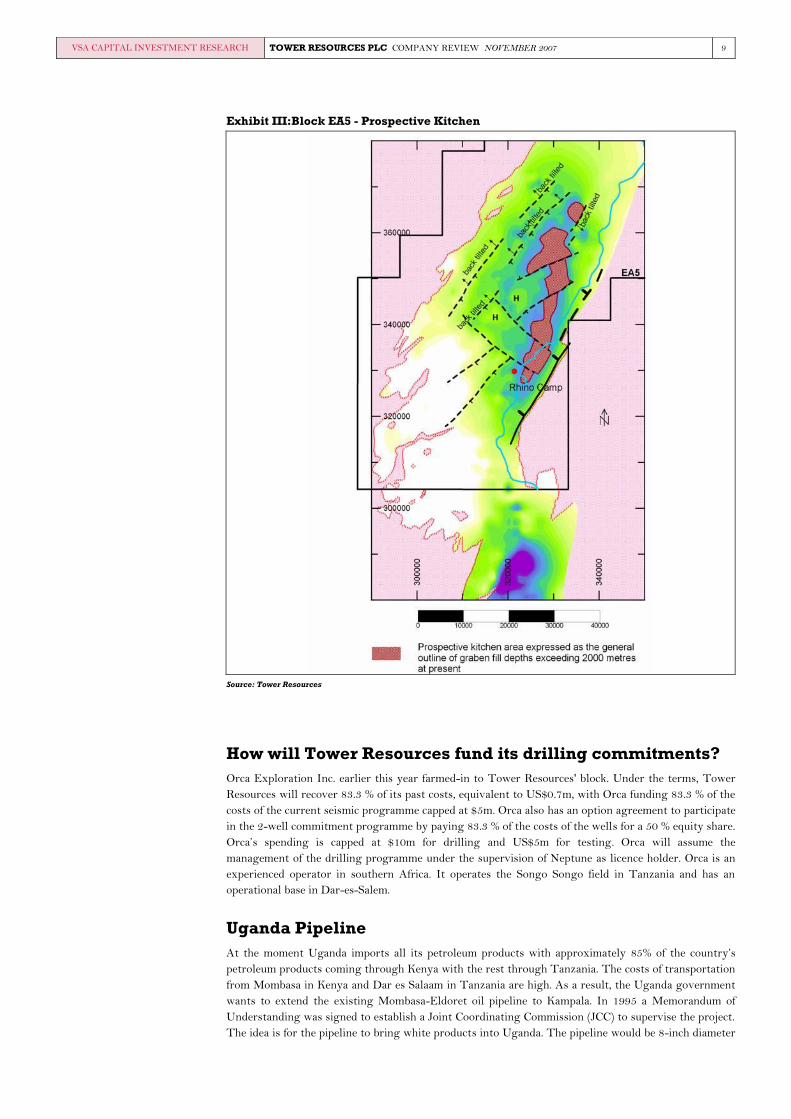

Exhibit III:Block EA5 - Prospective Kitchen

Source: Tower Resources

How will Tower Resources fund its drilling commitments?

Orca Exploration Inc. earlier this year farmed-in to Tower Resources' block. Under the terms, Tower

Resources will recover 83.3 % of its past costs, equivalent to US$0.7m, with Orca funding 83.3 % of the

costs of the current seismic programme capped at $5m. Orca also has an option agreement to participate

in the 2-well commitment programme by paying 83.3 % of the costs of the wells for a 50 % equity share.

Orca’s spending is capped at $10m for drilling and US$5m for testing. Orca will assume the

management of the drilling programme under the supervision of Neptune as licence holder. Orca is an

experienced operator in southern Africa. It operates the Songo Songo field in Tanzania and has an

operational base in Dar-es-Salem.

Uganda Pipeline

At the moment Uganda imports all its petroleum products with approximately 85% of the country’s

petroleum products coming through Kenya with the rest through Tanzania. The costs of transportation

from Mombasa in Kenya and Dar es Salaam in Tanzania are high. As a result, the Uganda government

wants to extend the existing Mombasa-Eldoret oil pipeline to Kampala. In 1995 a Memorandum of

Understanding was signed to establish a Joint Coordinating Commission (JCC) to supervise the project.

The idea is for the pipeline to bring white products into Uganda. The pipeline would be 8-inch diameter

10 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

and extend from Eldoret to Kampala, some 320 kms. The ownership of the pipeline would be a

combination of private and public funds, with Kenya and Uganda owning 24.5 % each and the rest held

in private hands. In 2004 the JCC invited companies to express an interest and 12 firms submitted

detailed proposals. The possibility of building a 1,450 km pipeline through Tanzania to Uganda is also

being examined.

It is likely that with the large crude oil discoveries made, and the possibility of building a small crude oil

refinery possibly close to Kampala, that an export pipeline will be built in parallel with the product

pipeline.

Reserve base in Uganda

We give below a hypothetical matrix of what to expect if one prospect is successful in Uganda. We have

risked the possibility of finding these resources from 25 % to 10 % and have also assumed that Tower

Resources’ equity stake in Uganda is 50 %. Our risks factors are clearly conservative compared with the

current success rates of almost 100 % achieved by Tullow and Heritage. We can see that on a severe

risked basis Tower Resources could hold resources of between 12.5 m - 15 m bbbls of crude oil.

Table I: Tower Resources - Matrix of estimated risked hypothetical resources (m bbls)

Prospects Hypothetical

Resource size (m bbls/ BCF)

Risk Success factor (%)

Risked Proven & Probable Gross Oil Equivalent

Resources (m boe)

Tower Resources Net Equity

Interest (%)

Tower Resources Risked Net

Resources (m boe)

Uganda

100 25 25 50 12.5

150 20 30 50 15

200 15 30 50 15

250 10 25 50 12.5

Source: VSA Capital

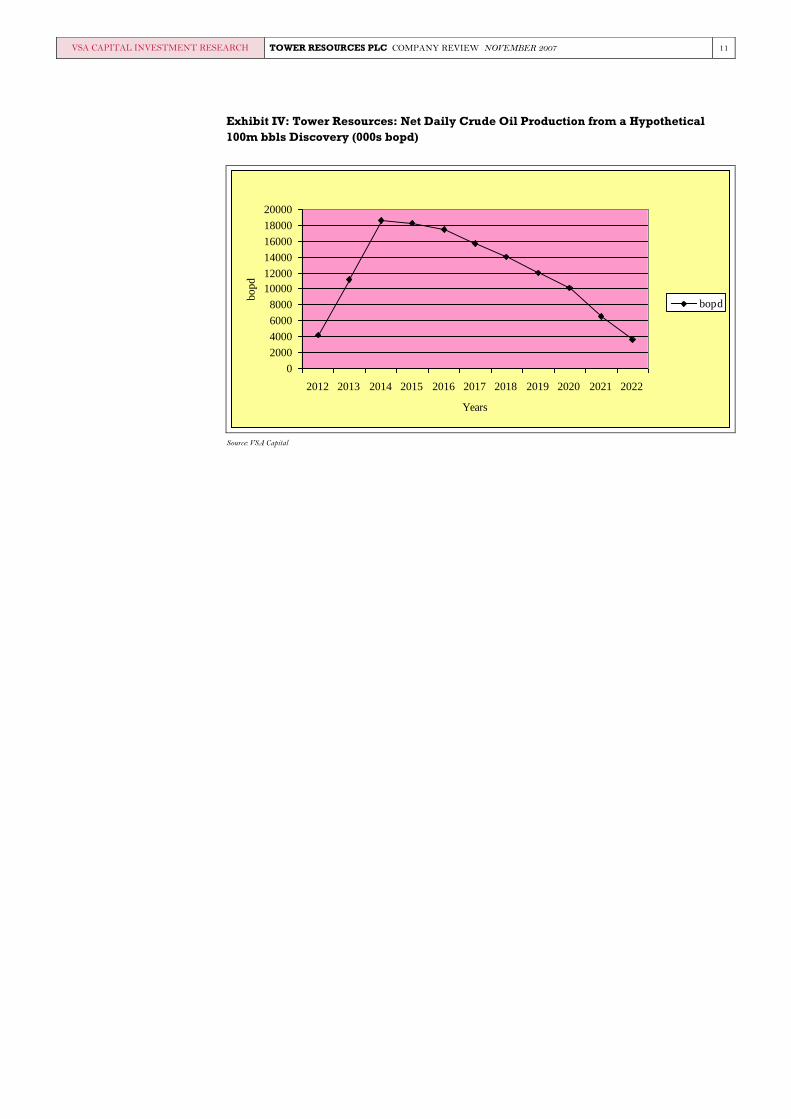

Hypothetical Uganda Net Crude Production

We give below a hypothetical net crude oil production curve for a 100m bbls discovery in Uganda. It

should be noted that this is only shown to give investors a flavour of what could come out of Uganda if

a small discovery of 100m bbls is found.

Our hypothetical crude oil production curve starts in 2012 and quickly reaches peak production of

around 18,750 bopd in 2014. Please note that there is a major constraint in getting the oil out of the

country that is being addressed by all operators in Uganda at the moment. The possibility of upgrading

the railway line to Kenya in order to export future oil production is currently under discussion.

Risked hypothetical

resource base of 12.5 - 15m

bbls of crude oil

Hypothetical production of

18.750 bopd in 2014

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 11

Exhibit IV: Tower Resources: Net Daily Crude Oil Production from a Hypothetical

100m bbls Discovery (000s bopd)

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Years

bopd

bopd

Source: VSA Capital

12 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

NAMIBIA Namibia is another southern African country that is underexplored with only seven onshore wells and

11 offshore wells drilled. Offshore exploration started in 1968 and so far the only significant discovery

has been the Kudu gasfield with 3 TCF of reserves discovered by Chevron in 1973. For political reasons

no further exploration and appraisal work took place until 1987-88 when a number of wells were drilled

by the forerunner of the National Petroleum Corporation of Namibia (NAMCOR), the country’s

national oil company. Further exploration did not start until after Independence on March 21, 1990.

The geological interpretation of the area indicates considerable oil and gas potential that is linked to the

opening of the Atlantic Ocean which was accompanied by heavy volcanism. The most common

interpretation of the basin's formation is that preceding the separation of the tectonic plate of Africa

from South America a thermal subsistence and shift in plate location took place. This volcanism lead to

the formation of continental flood basalts such as the Etendeka and Paraná flood basalt provinces in

Africa and South America respectively. A large number of 60 - 100 km wide seaward dipping seismic

reflection patterns, commonly known as ‘seaward dipping reflector sequences’ (SDRS) are found in

water depths of between 200 metres and 4500 metres at approximately 70 % of the continental margins

of the Atlantic. The discovery of the Kudu gas field at the edge of an SDRS put the passive volcanic

margins on the petroleum industry’s agenda.

Recent Discoveries

In May 2004 Tullow, through its take-over of Energy Africa, acquired Production Licence 005 that

contains the large Kudu gasfield with estimated 9 TCF of gas reserves in situ, with proven reserves of

1.5 TCF of gas reserves. In April this year, Tullow sold a 20% interest in the licence to the Itochu

Corporation of Japan, which will pay 40% of the cost of two appraisal wells in 2008 to earn a 20 %

equity stake. In May, the two-well appraisal programme started when the Pride South Seas semi-

submersible rig started drilling Kudu-8 to establish commercially productive flow rates from the

extensive Kudu East reservoir originally tested by the Kudu-5 well. In early September, the well

penetrated the primary objective section and was found to be gas bearing. The well reached its target

depth of 4500m in October. In addition to pursuing development of the field as a single gas-to-power

project supplying electricity to Namibia and South Africa, the partners expect to export the remaining

natural gas directly to South Africa

Underexplored region

Considerable oil & gas

potential

Kudu gasfield with GIIP

estimated at 9 TCF

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 13

Tower Resources' Namibian Interests

Tower Resources holds three offshore blocks (1910a, 1911, 2011a), which extend approximately to

23,000 sq kms at water depths between 200 metres to 3000 metres in the Dolphin Graben. In the 1990s,

Norsk Hydro drilled two wells, 1911/15-1 and 1911/10-1, on block 1911. Both wells were drilled to the

Lower Cretaceous Volcanics but no test was undertaken of the deeper Cretaceous and Jurassic. The data

from the wells confirmed extensive basins along the coast with good traps and source rocks.

Tower Resources acquired 10,000 kms of 2D Seismic from TGS-Nopec that covers most of the licence.

As a result of the seismic interpretation, Tower Resources has identified 18 leads with an upside

hydrocarbon potential of between 40m to 5.4bn bbls of crude oil or 10 TCF of gas. It has also

conducted a geochemical study of the region as well as a sea surface oil seep survey by satellite imaging.

The results were extremely encouraging with the Company reinterpreting and reprocessing a number

of seismic lines using the technique of Amplitude Variations Offset (AVO). This technique uses the

contrast in the physical properties of rocks, allowing information to be established on the different

lithology and fluids found in the various geological horizons. AVO works by using the property

associated with ‘energy partitioning’. When seismic waves hit a boundary, part of the energy is reflected

while the rest is transmitted. The AVO on Block 1911 indicated the presence of natural gas in two

adjacent, very large structural features in the northern part of the block, to the west of the Norsk Hydro

wells. It also confirmed the lack of hydrocarbon indications at the two dry holes. As a result, Tower

Resources shot just under 800 kms of 2D Seismic earlier this year to confirm this interpretation and

now intends to shoot 1000 kms 3D seismic at the end of 2008 to determine a suitable well location.

Tower Resources' Fiscal Regime

Tower Resources' fiscal regime is comparatively benign given the country's underexplored nature and

includes a 5 % royalty and a Petroleum Income Tax (PIT) of 35 % of taxable income. Both exploration

and operating expenditure can be written off immediately and in full and development expenditure is

depreciated over three years.

Farm-Out Agreement with Arcadia Petroleum

Earlier this year, Tower Resources farmed-out to Arcadia Petroleum Ltd., which will assume

operatorship with Tower Resources retaining a 15 % carry over the 2D and 3D Seismic shoot as well as

over the drilling of two exploration wells in 2008, which will probably cost between US$100m -

US$150m. This is a very favourable development for Tower Resources because Arcadia, which is a large

oil trader with turnover last year of US$17bn, is a subsidiary of the very large Farahead Holding Ltd.

that specialises in the construction of offshore floating production platforms, as well as transporting

LNG. It also has expertise in drilling wells, and in developing and marketing any hydrocarbon

resources discovered. The significance of Arcadia taking such a large interest in Tower Resources'

acreage is that the Farahead Group has the resources to develop any gasfields found in the country,

which would be developed as LNG trains and through Golar trade the LNG cargoes. It is estimated

that worldwide LNG trading will grow from 145 m tonnes in 2006 to 370 m tonnes in 2015 and

demand is expected to eclipse supplies by 20 m tonnes per annum between 2008 and 2015.

Resource base in Namibia

We give below a hypothetical matrix of what to expect if one prospect is successful in Namibia. We

have risked the possibility of finding these resources to 10 % and have also assumed that Tower

Resources’ carry in Namibia is 15 %. We can see that on a severe risked basis, Tower Resources could

hold reserves of between 7.5 m barrels of crude oil to 11.7m bbls of crude oil equivalent.

Table II: Tower Resources: Estimated Risked Hypothetical Resources in Namibia

Prospects Hypothetical Resource size

(m bbls/ BCF) Risk Success

factor (%)

Risked Proven & Probable Gross Oil Equivalent

Resources (m boe)

Tower Resources Net Equity

Interest (%)

Tower Resources Risked Net

Resources (m boe)

Namibia

Dolphin Graben

Amplitude Variations Offset

Farm-out to Arcadia

Petroleum Ltd.

Hypothetical risked

resources of 7.5m bbls of

crude oil or 11.7m boe gas

reserves

14 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

Oil 500 10 50 15 7.5

Gas 5000 10 78.13 15 11.72

Source: VSA Capital

Hypothetical Namibia Net Crude Production

We give below a hypothetical net crude oil production curve for a 500m bbls discovery in Namibia and

an alternative 5 TCF gas discovery in the country. It should be noted that this is only shown to give

investors a flavour of the potential of the prospective resource base detailed above. Our hypothetical

crude oil production curve starts in 2015 and reaches peak production of around 30,000 bopd in 2017.

Exhibit V: Hypothetical Net Namibian Crude Oil Production (500m bbls)

0.00

5000.00

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

bopd

Source: VSA Capital

A hypothetical natural gas production curve scenario also starts in 2015 and reaches peak production of

120 bcf per annum in 2017.

Exhibit VI: Hypothetical Net Natural Gas Annual Production for a 5 TCF Discovery

(BCF)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

bcf

Hypothetical peak

production of 30,000 bopd

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 15

Source: VSA Capital

Total net hypothetical crude oil and gas resources

Our hypothetical resource base with the various risk factors is given below for both Uganda and

Namibia. As we can see, our risked hypothetical resource base is between 12.5m - 27m boe.

Table III: Hypothetical Crude Oil & Natural Gas Resources

Prospects Hypothetical Resource size

(m bbls) Risk Success

factor (%)

Risked Proven & Probable Gross Oil Equivalent

Resources (m boe)

Tower Resources Net Equity

Interest (%)

Tower Resources Risked Net

Resources (m boe)

Uganda

100 25 25 50 12.5

150 20 30 50 15

200 15 30 50 15

250 10 25 50 12.5

Namibia

Oil 500 10 50 15 7.5

Gas 5000 10 78.13 15 11.72

Source: VSA Capital

FUTURE Tower Resources is working towards acquiring more assets of similar quality and size in southern

Africa.

Risked hypothetical

resources of between 12.5m

- 27m boe.

16 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

Directors & Senior Management

Peter Kingston, Executive Chairman, graduated from Oxford University with a degree in

Mathematics, and is a Petroleum Engineer with almost 40 years of experience in technical, executive

and advisory roles. He has been directly engaged, as a director, in the strategic development of oil

companies for over 20 years and has served as executive and non-executive director of UK-based oil and

gas companies, including LSE-listed, AIM-listed and private companies. He was Joint-Managing

Director of Enterprise Oil Plc from 1984 to 1992. He is currently Deputy Chairman and Senior

Independent Director of Soco International Plc. He became Chairman of Tower Resources on 1st

February 2006.

Peter Taylor, Non-Executive Director, trained as a chemical engineer, and is Joint Chairman of TM

Services Ltd, an international oil and gas consulting company. In 1991, he was a founding member and

director of TM Oil Production Ltd, which is now Dana Petroleum Plc, an oil and gas company listed on

the Official List and one of the UK’s leading independents. Mr Taylor was a director of Dana until 2001.

He was also a founding member and director of Consort Resources Ltd, which became a significant

North Sea gas production company, and of Planet Oil Limited, which was merged with Hardman

Resources Limited in 1998. Mr Taylor was a founding member and director of Star Petroleum PLC,

which was incorporated into Global Petroleum Ltd, which is dual ASX and AIM listed and which has

significant interests in Kenya and the Falkland Islands. Mr Taylor is a founding member and director of

Neptune.

Peter Blakey Non-Executive Director, trained as a chemical engineer, and is Joint Chairman of TM

Services Ltd, an international oil and gas consulting company. In 1991, he was a founding member and

director of TM Oil Production Ltd, which is now Dana Petroleum Plc, an oil and gas company listed on

the Official List and one of the UK’s leading independents. He was also a founding member and director

of Consort Resources Ltd, which became a significant North Sea gas production company, and of Planet

Oil Limited, which was merged with Hardman Resources Limited in 1998. Mr Blakey was a founder

member and director of Star Petroleum PLC, which was incorporated into Global Petroleum Ltd, which

is dual ASX and AIM listed and which has significant interests in Kenya and the Falkland Islands. Mr

Blakey is a founding member and director of Neptune.

Mark Savage, Non-Executive Director, holds a business degree from the University of Colorado and

was senior executive for a number of US banks before he joined an Australian based merchant bank. Mr

Savage has experience in debt and equity markets as well as in the corporate advisory area. He has held

directorships with a number of public companies. Mr Savage is also a director of Global Petroleum Ltd.

Jeremy Asher, Non-Executive Director, is a graduate of the London School of Economics and the

Harvard Business School. He is Chairman of Agile Energy Limited, a privately held energy investment

company; and a director of several non-energy-related companies. Following several years consulting

with Mercer Management Consulting, Jeremy ran the global oil products trading business at Glencore

AG, and then acquired, developed and sold the 275,000 b/d Beta oil refinery at Wilhelmshaven in

Germany. As CEO of PA Consulting Group, he oversaw PA’s globalisation and growth from 2,500 to

nearly 4,000 staff.

Jim Webb, Exploration Manager, graduated from London University with a degree in Geology, and

has more than 35 years of experience in the international oil and gas exploration and production

business. He is a former Director of Exploration for Kerr-McGee, and Hunt Oil Company, he currently

advises on exploration for Tower, Global Petroleum and several other junior oil companies. Jim also

advised Falklands Oil and Gas.

SENSITIVITIES: four main challenges The Company faces four main challenges:

• To find hydrocarbon resources in both Uganda and Namibia.

• The thermal maturity of the source rocks could be the main exploration risk.

• To secure a drilling rig in the required time frame and at a reasonable cost.

• Managing social and environmental issues in an emerging oil province.

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 17

The remote possibility of crude oil prices weakening is always a fundamental point of concern as it is the

main driver in the sector, but this is one area where we do not expect any weakness for some years to

come.

VALUATION The main driver in the oil industry is the oil price, which is currently above US$90/bbl for WTI crude.

Oil prices have remained at relatively high levels for the last 24 months, mainly because of strong

demand driven by economic growth, the decline in OPEC production and political instability in the

Middle East. During this period, Nigerian production has fallen by 500,000 bopd because of the

activities of insurgents in the country. In addition, Iran and Venezuela have been unable to meet their

OPEC quotas, Indonesia is in long term decline, and Iraq continues to be plagued by terrorist attacks.

This has resulted in OPEC crude oil output declining from around 31.6 m bopd during the fourth

quarter last year to current levels of around 30.7m bopd. OPEC has agreed to increase production by at

least 0.5m bopd but this is insufficient to reverse the inexorable upward increase in crude oil. There is,

however, a view that if world economic growth starts to slow down as a result of a general increase in

interest rates that oil prices could weaken in 2008.

We can assign a minimum value of US$45 - 50m to Tower Resources by the implied minimum

expenditure to be undertaken by the farm-outs of its Ugandan and Namibian assets. In arriving at this

figure we have used US$20m that Orca is committed to spend following its farm-in to Tower Resources'

Ugandan acreage, and US$25 - 30m for the value of Arcadia's farm-in for 85 % of the Namibian acreage.

We have modelled a number of hypothetical oil and gas prospects in both Uganda and Namibia, and

have risked the results for success in the following manner: an assumed a success rate of 25 % for 100m

bbls, 20 % for 150m bbls, 15 % for 200m bbls and 10 % for 250 m bbls; and 10 % for the Namibian

prospects. We have also calculated the NPVs using various discount factors as well as a constant crude

oil price of US$70/bbl and declining crude oil prices to US$22/bbl in 2017. Although current crude

prices are above US$90/bbl and the futures crude oil curve to 2015 stands at US$80/bbl we have used

US$70/bbl to maintain our conservative position. Our matrix gives a conservative risked resource NPV

of between US$-199m - US$1360m, an average of US$580.5m.

Table IV: Net Present Value of Hypothetical Resource Development (US$m)

Constant Oil Price US70$/bbl

Declining Oil Price US$70/bbl to

US$22/bbl

Discount Factor

10 15 20 25 10 15 20 25

Uganda

100 m bbls prospect

279.23 155.70 81.45 36.30 -1.81 -34.24 -49.76 -56.02

150 m bbls prospect

667.12 329.76 251.74 149.39 -47.71 -90.40 -108.24 -112.80

200 m bbls prospect

1095.63 668.92 405.84 240.92 -164.78 -198.52 -205.20 -198.59

250 m bbls prospect

1360.27 845.22 526.41 325.40 -107.71 -166.50 -187.26 -188.57

Namibia

500m bbls oil prospect

967.95 681.41 484.91 347.23 -273.96 -243.43 -210.89 -180.83

5 TCF prospect

999.06 629.47 394.59 242.03 160.10 63.65 17.51 -3.90

Source: VSA Capital

We can see from the table given below that if Tower Resources finds and develops one prospect of

100m bbls that on a severe risked basis and with both constant and declining crude oil and gas prices,

Minimum value of US$45m -

US$50m.

Conservative risked

resource NPV of around

US$580m

18 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

together with discount factors of between 10 % – 25 %, that Tower Resources has an NPV per share

range of between $-0.1 cents – 84 cents, compared with the current share price of 5.5 cents.

Table V: Hypothetical Returns per share (US$cents)

Constant Crude Oil Price US$70/bbl

Uganda Namibia

100m bbls 150m bbls 200m bbls 250m bbls 500m bbls 5 TCF

Net Return on Investment

0.299 0.372 0.834 0.677 0.289 0.534

Net Return on Investment (%)

0.091 0.130 0.157 0.152 0.110 0.104

Risked NPV Value (10 % disc.)

0.077 0.122 0.301 0.249 0.064 0.162

Risked NPV Value (15 % disc.)

0.043 0.060 0.184 0.155 0.027 0.094

Risked NPV Value (20 % disc.)

0.022 0.046 0.111 0.096 0.007 0.055

Risked NPV Value (25 % disc.)

0.010 0.027 0.066 0.060 -0.003 0.033

Declining Crude Oil Price US$70 - US$22 per barrel

Net Return on Investment

0.055 0.045 0.039 0.324 -0.042 0.143

Net Return on Investment (%)

0.033 0.027 0.011 0.225 -0.025 0.075

Risked NPV Value (10 % disc.)

0.000 -0.009 -0.045 -0.020 -0.050 0.029

Risked NPV Value (15 % disc.)

-0.009 -0.017 -0.054 -0.030 -0.045 0.012

Risked NPV Value (20 % disc.)

-0.014 -0.020 -0.056 -0.034 -0.039 0.003

Risked NPV Value (25 % disc.)

-0.015 -0.021 -0.054 -0.034 -0.033 -0.001

Source: VSA Capital

Comparative Valuation

We have also compared Tower Resources with other listed companies on the full LSE list and on AIM.

We can see from the table given below that Tower Resources is backed by a risked hypothetical

resource base of 77 bbls of crude oil resources per £100 market value, placing it ahead of Global Energy

Development with 42.9 bbls per £100 market value. The average value of reserves assigned by the

market for our universe given above is £6.8/bbl. If we assign such a figure to Tower Resources, then

the market value of the company assuming our hypothetical resource base would be £84.3m, compared

with a current market value of £14.8m.

There are two companies in our universe that resemble most closely Tower Resources, namely, Tullow

and Heritage. If we take the average value assigned by the stock market for the reserves of these

companies of £9.4/bbl, we can see that the market potential of Tower Resources is very large.

Table VI: Tower Resources: Comparison with other E&P Companies on the LSE & TSX

Share

Price

p/share

(29.10.0

Market

Capitalisation

(£millions)

Hydrocarbo

n Prod.

(boepd)

2P

Hydrocarbo

n Reserves

(million

bbls of oil

2P

Hydrocarbo

n Reserves

per £100

Market

Value of

reserves

assigned

by

market

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 19

7) equivalent) Capitalisati

on

£/bbl

LSE - Full Listing

Burren 1184 1669.5 38000.0 214.2 12.8 7.8

Cairn Energy 2463 3211.2 111700.0 568.0 17.7 5.7

Dana Petroleum Plc 1323 1152.2 20285.0 131.2 11.4 8.8

Dragon Oil 305.5 1559.1 28321.0 303.0 19.4 5.1

Emerald Energy 215 120.6 3674.0 14.5 12.0 8.3

JKX Oil & Gas 394.25 608.3 11146.0 56.0 9.2 10.9

Premier Oil 1181 968.0 33300.0 164.0 16.9 5.9

Tullow 647.5 4504.0 69700.0 492.0 10.9 9.2

LSE - AIM

Global Energy Development

115.5 40.8 1236.0 17.5 42.9 2.3

TSX

Heritage Oil Corp (£) 2752 669.0 169.0 69.5 10.4 9.6

Tower Resources 3 16.1 18750.0* 12.4** 77.0 1.3

* Hypothetical production

** Hypothetical risked resources

6.8

Source: VSA Capital

20 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

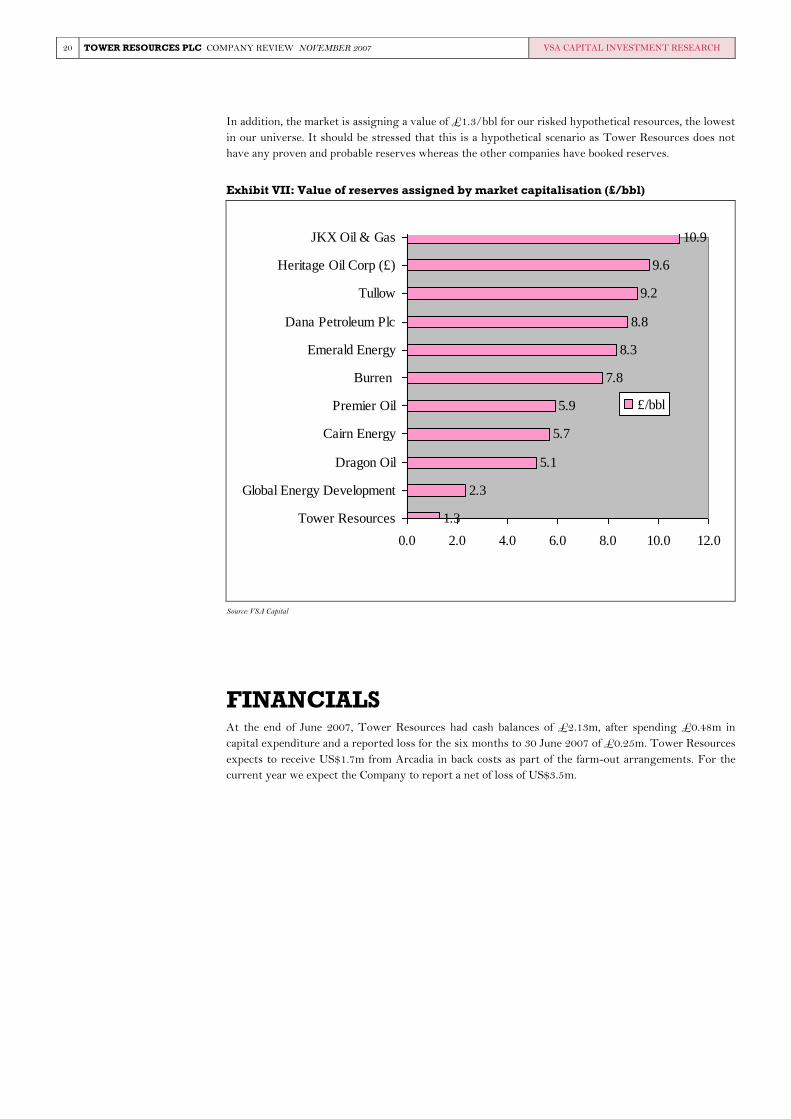

In addition, the market is assigning a value of £1.3/bbl for our risked hypothetical resources, the lowest

in our universe. It should be stressed that this is a hypothetical scenario as Tower Resources does not

have any proven and probable reserves whereas the other companies have booked reserves.

Exhibit VII: Value of reserves assigned by market capitalisation (£/bbl)

10.9

9.6

9.2

8.8

8.3

7.8

5.9

5.7

5.1

2.3

1.3

0.0 2.0 4.0 6.0 8.0 10.0 12.0

JKX Oil & Gas

Heritage Oil Corp (£)

Tullow

Dana Petroleum Plc

Emerald Energy

Burren

Premier Oil

Cairn Energy

Dragon Oil

Global Energy Development

Tower Resources

£/bbl

Source: VSA Capital

FINANCIALS At the end of June 2007, Tower Resources had cash balances of £2.13m, after spending £0.48m in

capital expenditure and a reported loss for the six months to 30 June 2007 of £0.25m. Tower Resources

expects to receive US$1.7m from Arcadia in back costs as part of the farm-out arrangements. For the

current year we expect the Company to report a net of loss of US$3.5m.

VSA CAPITAL INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 21

We have estimated the Company's Profit & Loss, Balance Sheet and Cash Flows up to 2009. In our

financial projections, we have used a declining crude oil price from US$70/bbl in 2007 to US$63.18 in

2009. We have also assumed a 100m bbls reserve field that comes on-stream in 2012. Again, this is for

illustrative purposes as the Company does not have a reserve base.

The hypothetical financial projection shows that if Tower Resources found a 100m bbls field in Uganda

it will probably report a negative operating cash flow of US$12m in 2009 as it starts developing its

discovery. Its balance sheet will clearly deteriorate as its capital expenditure increases significantly in

2010, with estimated closing net debt of US$48m in 2009.

Table VII: Profit & Loss, Balance Sheet & Cash Flow Projections, 2005-2009

PROFIT & LOSS US$m 2005a 2006a 2007e 2008e 2009e

Year End 31 December

Revenue 0 0 0 0 0

Cost of Sales 0 0 (2) (3) (6)

Gross Profit 0 0 (2) (3) (6)

EBITDA 0 (2) (5) (9) (5)

Operating Profit (before GW and except.)

0 (2) (5) (9) (5)

Goodwill Amortisation 0 0 0 0 0

Exceptionals 0 0 0 0 (1)

Other 0 1 2 (3) (6)

Operating Profit 0 (1) (4) (12) (12)

Net Interest 0 0 0 0 0

Profit Before Tax (norm)

0 (1) (4) (6) (11)

Profit Before Tax (FRS 3)

0 (1) (4) (6) (12)

Tax (0) 0 0 0 0

Profit After Tax (norm) (0) (1) (-4) (-6) (-12)

Profit After Tax (FRS3) 0 (1) (4) (6) (12)

Average Number of Shares Outstanding (m)

536.7 536.7 536.7 536.7 536.7

EPS - normalised (p) (0.0) (0.0) (-0.1) (-0.1) (-0.2)

EPS - FRS 3 (p) 0.0 (0.0) (0.1) (0.1) (0.2)

BALANCE SHEET

Fixed Assets 0 0 5 13 15

Intangible Assets 0 0 1 5 5

Tangible Assets 0 0 4 8 10

Investment in associates 0 0 0 0 0

Current Assets 1 1 8 39 124

Debtors 0 0 3 25 75

Cash 1 1 4 13 34

Current Liabilities 0 0 5 45 75

Creditors 0 0 5 45 75

Short term borrowings 0 0 0 0 0

Long Term Liabilities 0 0 35 75 100

Long term borrowings 0 0 35 75 100

Other long term liabilities

0 0 0 0 0

Net Assets 1 1 52 171 314

CASH FLOW

Operating Cash Flow (0) (1) (4) (6) (12)

Net Interest 0 0 0 0 0

2009 closing net debt of

US$48m

22 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA CAPITAL INVESTMENT RESEARCH

Tax 0 0 0 0 0

Capex 0 (1) (1) (5) (5)

Acquisitions/disposals 0 0 (1) (1) (5)

Financing 0 2 11 25 50

Dividends 0 0 0 0 0

Opening net debt/(cash) 0 0 1 7 20

HP finance leases initiated

0 0 0 0 0

Other (0) (1) (12) (27) (56)

Closing net debt/(cash)

0 1 7 20 48

Source: VSA Capital

DIVIDEND POLICY The Company is unlikely to pay a dividend while it builds its asset base.

MAJOR SHAREHOLDERS The major shareholders in the Company are given below:

Table VIII: Major Shareholders

Name %

Bayview Investments 18.6

Credit Suisse Clients Nominees 12.4

Peter Taylor 9.82

Peter Blakey 9.82

Forest Nominees 9.7

Teawood Nominees 6

Bruce Rowan 4.7

TOTAL 71.04

Source: VSA Capital

VSA RESOURCES INVESTMENT RESEARCH TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 23

S.W.O.T. Analysis

Strengths

Good and experienced management, with extensive knowledge of the oil industry.

Situated in one of the hottest areas for finding hydrocarbon resources in the world at the moment.

Its exploration and drilling commitments are fully funded having farmed-out its interest to strong industry players.

Weaknesses

Main competitors with substantial financial muscle.

Lack of readily available drilling rigs.

Potential time scale of development.

Opportunities

High oil prices expected to remain for some time leading to continued interest in the Oils sector.

Uganda's Albertine Graben and Namibia's Dolphin Graben are underexplored basins.

Further opportunities in Africa.

Threats

High oil prices lead to a decline in world economic growth and hence weakening demand for crude oil.

Exploration drilling in Uganda and Namibia is unsuccessful.

Exploration acreage close to Congolese war zones.

Political instability in central African regions.

24 TOWER RESOURCES PLC COMPANY REVIEW NOVEMBER 2007 VSA RESOURCES INVESTMENT RESEARCH

EBITDA Profit after Tax (FRS3) Net Closing Cash Balances

EBITDA

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

2005a 2006a 2007e 2008e 2009e

US$m

Profit after Tax (FRS3)

-14

-12

-10

-8

-6

-4

-2

0

2005a 2006a 2007e 2008e 2009e

US$m

Closing Net Debt

0

10

20

30

40

50

60

2005a 2006a 2007e 2008e 2009e

US$m

Growth metrics % Profitability metrics % Balance sheet metrics %

EPS CAGR 05-09e n/a ROCE 2008e (0.0) Gearing 2008e 37

EPS CAGR 07-09e n/a Avg ROCE 05-09e n/a Interest cover 2008e 0

EBITDA CAGR 05-09e n/a ROE 2008e 3 % Stock turn 2008e 0

EBITDA CAGR 07-09e n/a Gross margin 2008e n/a Debtor days 2008e 0

Sales CAGR 07-09e n/a Operating margin 2008e n/a Creditor days 2008e 0

Gross mgm/Op margin n/a

Principal shareholders % Forthcoming announcements/catalysts Management

team

Bayview Investments 18.6 Preliminaries 2007 5.5.2008 Chairman: Peter Kingston

Credit Suisse Clients Nominees 12.4 Annual Report 2007 6.5.2008 Non-Ex Director: Peter Taylor

Peter Taylor 9.82 AGM 2.6.2008 Non-Ex Director: Peter Blakey

Peter Blakey 9.82 Interims 20.9.2008 Non-Ex Director: Mark Savage

Forest Nominees 9.7 Non-Ex Director: Jeremy Asher

Teawood Nominees 6.0

Bruce Rowan 4.7

IMPORTANT NOTICE

This research report has been prepared by VSA Resources

Limited, for which it has been paid a fee, as corporate finance

advisors and arrangers to Tower Resources plc and is solely for

and directed at persons who have professional experience in

matters relating to investments and who are Investment

Professionals, as specified in Article 19(5) of the Financial

Services and Markets Act 2000 (Financial Promotion) Order

2001. This research report is exempt from the general

restriction on the communication of invitations or inducements

to enter into investment activity and has therefore not been

approved by an authorised person, as would otherwise be

required by Section 21 of the Financial Services and Markets

Act 2000 (the "Act"). Persons who do not fall within the above

category should return this research report to VSA Resources

Limited, 43 London Wall, London, EC2M 5TF, immediately.

This research report is not intended to be distributed or passed

on, directly or indirectly, to any other class of persons. It is

being supplied to you solely for your information and may not

be reproduced, forwarded to any other person or published, in

whole or in part, for any purpose, without out prior written

consent.

Neither the information nor any opinion expressed

constitutes an offer, or an invitation to make an offer, to buy or

sell any securities or any options, futures or other derivatives

related to such securities.

The information and opinions contained in this research

report have been compiled or arrived at by VSA Resources

Limited (the "Company") from sources believed to be reliable

and in good faith but no representation or warranty, express or

implied, is made as to their accuracy, completeness or

correctness. All opinions and estimates contained in the research

report constitute the Company's judgements as of the date of the

report and are subject to change without notice. The

information contained in the report is published for the

assistance of those persons defined above but it is not to be

relied upon as authoritative or taken in substitution for the

exercise of the judgement of any reader.

The Company accepts no liability whatsoever for any direct

or consequential loss arising from any use of the information

contained herein. The company does not make any

representation to any reader of the research report as to the

suitability of any investment made in connection with this report

and readers must satisfy themselves of the suitability in light of

their own understanding, appraisal of risk and reward,

objectives, experience and financial and operational resources.

The value of any companies or securities referred to in this

research report may rise as well as fall and sums recovered may

be less than those originally invested. Any references to past

performance of any companies or investments referred to in this

research report are not indicative of their future performance.

The Company and/or its directors and/or employees may

have long or short positions in the securities mentioned herein,

or in options, futures and other derivative instruments based on

these securities or commodities.

Not all of the products recommended or discussed in this

research report may be regulated by the Financial Services and

Markets Act 2000 and the rules made for the protection of

investors by that Act will not apply to them.

If you are in any doubt about the investment to which this

report relates, you should consult a person authorised and

regulated by the Financial Services Authority who specialises in

advising on securities of the kind described.

The Company does and seeks to do business with the

companies covered in its research reports. Thus, investors

should be aware that the Company may have a conflict of

interest that may affect the objectivity of this report.

The analyst who prepared this report has not and will not

receive any compensation for providing a specific

recommendation or view in this report.

Investors should consider this report as only a single factor

in making their investment decision.

The information in this report is not intended to be

published or made available to any person in the United States

of America (USA) or Canada or any jurisdiction where to do so

would result in contravention of any applicable laws or

regulations. Accordingly, if it is prohibited to make such

information available in your jurisdiction or to you (by reason of

your nationality, residence or otherwise) it is not directed at you.

VSA Capital Ltd. is Authorised and Regulated by the

Financial Services Authority