to assess the affect of perceived usefulness, ease of …

TRANSCRIPT

International Journal of Research in Marketing Management 2017

28 Volume 1 Number 1

TO ASSESS THE AFFECT OF PERCEIVED USEFULNESS, EASE OF USE, SECURITY & PRIVACY ON CUSTOMER

ATTITUDE AND CUSTOMER ADAPTATION: A STUDY OF E-BANKING IN INDIA

Dr. Nischay K. Upamannyu, Assistant Professor, Prestige Institute of Management, Gwalior, [email protected]

Prof. Chanda Gulati, Assistant Professor, Prestige Institute of Management, Gwalior, [email protected]

Ms. Kirti Sharma, Student of MBA, Prestige Institute of Management, Gwalior,

Ms. Ragani Jain, Student of MBA, Prestige Institute of Management, Gwalior, [email protected]

ABSTRACT

E-banking has become a focal point for all baking service provider in the current scenario having understood the need of customers. Gradually, Customers have started adopting e-banking service and for this, the perceived attitude of customer has significant matter for adopting e-banking services. The objective of the current study is to understand the effect of perceived usefulness, perceived ease of use, perceived privacy and perceived security on customer attitude and customer adoption. The adequate research methodology has been adopted to conduct the current study. The standardized questionnaires have been used to collect the data. To establish the relationship the structural equation modeling has been applied and results of the current study indicated the significant relationship between Perceived Ease of use and Attitude, Perceived Privacy and customer attitude, Perceived usefulness and consumer adaption, Perceived privacy and consumer adaption, and perceived ease of use and consumer adaption.

Key Word: Perceived usefulness, Perceived ease of use, perceived privacy perceived security, customer adaption, customer attitude and e-banking

INTRODUCTION

A bank is a financial institution that provides banking and other financial services to their customers. The Indian banking system consists of 26 public sector banks, 20 private sector banks, 43 foreign banks, 56 regional rural banks, 1,589 urban cooperative banks and 93,550 rural cooperative banks, in addition to cooperative credit institutions. Public-sector banks control nearly 80 percent of the market, thereby leaving comparatively much smaller shares for its private peers. The emergence of e-commerce has revolutionized the way we live, shop, entertain and interact. Electronic banking is generally an extension of traditional banking, using the internet as an Electric delivery channel for banking products and services. The evolution of e-banking started from the use of Automatic teller Machines and telephone banking (ATM), direct bill payment, electronic fund transfer (EFT) and the revolutionary online banking. The banking today is redefined and Re-

International Journal of Research in Marketing Management 2017

29 Volume 1 Number 1

engineered with the use of IT and it is sure that the future of banking will offer more sophisticated services to customers with the continuous product and process innovations. Thus there is a paradigm shift from seller’s market to buyer’s market. As time factor, is very much important for all the people in this modernized world, hence we are waiting in a queue spending the precious time which will lead us to go backward. Hence the customers don’t want to waste their precious time for waiting in a queue. The e-banking system addresses several emerging trends: customer’s demand for anytime, anywhere service, product time-to-market imperatives and increasingly complex back-office integration challenges. The challenges that oppose electronic banking are concerns of security and privacy of information. The use of e-banking has brought many concerns from different perspectives: government, business, banks, individuals and technology.

CONCEPTUAL FRAMEWORK

Perceived Usefulness: Perceived Usefulness is the degree to which a person believes that using a particular system would enhance his or her job performance (Davis, 1989). The individual perceives the information and communication technologies (ICT) to improve his performances; he uses them more frequently in his daily activities at work. However, one may think, as does this research, that the external factors can lead to relatives the significance of this hypothesis. In a developing country, too, the conventional wisdom that perceived usefulness is the main predictor of adoption has also been challenged.

Ease of Use: Ease of use is the degree to which a person believes that using a particular system would be free from efforts (Davis, 1989). The easier it is for a user to interact with a system, the more likely he or she will find it useful. In learning environments, web based technologies are designed to facilitate the learning process, and therefore their perceived ease of use is a definite necessity, especially where the learners have only recently been introduced to computer and Internet technology, as is typically the case for first year University students in a developing country.

Privacy & Security: Customers have doubts about the trust ability of the e-bank's privacy policies. Privacy is an important dimension that may affect users' intention to adopt e-based transaction systems. Assurance about security relates to the extent to which the web site guarantees the safety of customers` financial and personal information, an area which has witnessed a proliferation of research interest.

Customer Attitude: Attitude is generally considered to be a two-part concept that, when measured, involves attitude direction and attitude intensity. Consumer attitudes are a composite of a consumer’s (1) beliefs about, (2) feelings about, (3) and behavioral intentions toward some object--within the context of marketing, usually a brand or retail store. In the electronic banking context, consumers attitude is assorted in terms of perceptions regarding product information, form of payment, delivery terms, service offered, risk involved, privacy, security, personalization, visual appeal, navigation, entertainment and enjoyment.

International Journal of Research in Marketing Management 2017

30 Volume 1 Number 1

Customer Adaptation: Customer adaptation is determined by intention to perform the behavior. However, factors affecting the adaptation of a new information technology are likely to vary with the technology, target users, and context. Customer adaptation describes beliefs about having necessary resources and opportunities for an individual’s intention to perform. These are facilitating conditions, which refer to the availability of resources, i.e. the technological resources and infrastructure needed to engage in the adaptation. The adaptation of electronic banking depends on the service firm’s resource management by lowering delivery costs and by releasing service personnel to provide better and more varied service

E-Banking: E-banking is the use of a computer to retrieve and process banking data (statements, transactions details, etc.) and to initiate transactions (payments, transfers, requests for services, etc.) directly with a bank or other financial services provider remotely via telecommunications network. Electronic banking system addresses several emerging trends: customer demand for anytime, anywhere service, product-to-market imperatives and increasingly complex back-office integration challenges. This system allows consumers to access their banking accounts, review most recent transactions, request a current statement, view current product information, and re-order checks.

REVIEW OF LITERATURE

Islam, Nushrat (2005) found that perceived ease of use is having a significant positive relationship with customer adaptation and concluded that perceived usefulness and customer attitude were found to be unrelated in respect of customer adaptation. Ayo, CK (2010) found that there is a positive relationship between customers' perceived usefulness, customers' perceived ease of use, and their continued intention to use E-banking services and suggested that more attention ought to be paid on trust-building actions in the industry and incorporating trust-building measures into online customer relationships. Gautam, Lilesh & Khare, Sanjeev Kumar (2013) explored the relationship between Security and privacy, Trust, Innovativeness, Familiarity and Awareness has significantly positively related to acceptance of Internet banking among customers and found that the banks have to increase the level of trust between banks' website and customers and for this, banks ought to organize seminar and conference to educate the customers for using online banking as well as security and privacy of their accounts in order to increase the efficacy of e-banking among customers.

Fonchamnyo, Dobdinga Cletus (2012) concluded his study as customer attitude influences the intention to adopt e-banking, perceived usefulness, perceived trust, perceived security, Perceived Accessibility on customers’ attitude, Perceived Accessibility & Perceived Reliability on Perceived Usefulness and also found that Perceived Reliability and Quality of Internet Access do not have positive influence on Customers’ attitude. He found that demographic characteristic such as age was found to have a negative effect on customers’ attitude towards e-banking adoption. Goudarzi, Shidrokh (2013) found that there is an important positive relationship between trust and Internet banking adoption and also explored that the trust has a strong influence on Internet banking adoption. Juan, Carlos Roca,

International Journal of Research in Marketing Management 2017

31 Volume 1 Number 1

Juan, José García and Juan, José de la Vega (2009) suggested that perceived trust, usefulness and ease of use are important issues in online trading systems and also put emphasis on the online financial dealers and stockbrokers improve the security of the online system since e-investors form perceptions about its perceived security and when these perceptions are confirmed, and their trust should be enhanced.

Er. Goyal, Vishal Mohan & Mrs. Goyal, Gania (2009) found that Security is the main reason therefore, people are not interested to open their internet bank accounts where as the second reason was found is that people are not ready to try new experience and they become resist because customers have a fear of hacking of accounts and thus do not adopt internet banking. Shrivastava, Gitanjali & Bapna, Ira (2011) found that convenience, trust, privacy, ease of use and security are the important determinants of online banking, whereas, Privacy of data and security measures of the e-Banking technology are the main problem in the minds of users and also emphasized that the main problem lies that people have a fear of hacking of accounts and thus do not go on for internet banking.

Shah, Ankit (2011) found that the overall satisfaction of online consumers is mainly affected by Banking Needs, followed by Core Services, Problem Resolution, Cost Saved, Convenience and Risk and Privacy Concerns. He has also found customer satisfaction to be the important factor for trying something new for any customer. Rani, Malika (2012) concluded that people are not using all the E-banking services frequently because they less knowledge about computer and internet, Hence, they feel hesitation in using E-banking services and also found that people have around 60 % people have positive perception & are satisfied with E-Banking in context of services of e-banking, using e-banking services frequently, safety and security except one parameter (E-Banking is easy to use). Abadi, Hossein & Nematizadeh, Fateme (2012) concluded there is a positively significant relationship between customers’ attitude towards perceived ease of use, perceived usefulness, perceived credibility, perceived enjoyment and intention to use electronic banking system and found that customer attitude and behavioral intention and customer attitude have a positive and significant effect on intention to use e-banking and concluded that lack of trust in terms of the security measure of e-banking technology and the ability of e-Banking systems to protect privacy, if these are improved so the ease of use and usage would be increased.

Jalal, Akram, Marzooq, Jassim & A. Nabi, Hassan (2011) found that people consider Internet banking as an alternative for going to the bank and useful to conduct their banking activities more quickly. He also found that Perceived usefulness and Perceived Ease of Use are positively related with Internet Banking, positive effect of perceived usefulness on customer acceptance of e-banking. Jahangir, Nadim and Begum, Noorjahan (2008) in this study found that there exists a positive and significant relationship perceived usefulness, perceived ease of use. Security & Privacy and customer adaptation mediated by customer attitude and direct also. He also found that the management needs to pay attention on customer attitude, of which perceived usefulness, ease of use, security and privacy are very important antecedents.

Ahmad, Raies, RifatAra, Mir & Dr. Dar, Altaf A (2013) found that the customer attitude, perceived usefulness and perceived ease of use affect the user acceptance

International Journal of Research in Marketing Management 2017

32 Volume 1 Number 1

critically and emphasized on the positive feeling and attitude of user is essential for the e-banking usage level, whereas, the positive feeling such as enjoyment and excitement is related to efficiency, effectiveness and convenience which falls on the variables Perceived Usefulness and Perceived Ease of Use. Aderonke, Adesina & Ayo (2010) viewed that computer self-efficacy has a positive relationship with perceived ease of use and perceived usefulness, perceived credibility is significantly associated with perceived ease of use, perceived usefulness and customer attitude, Perceived credibility has a significant positive effect on perceived ease of use, perceived usefulness and customer attitude. Ease of use positively affects customer attitude and customer attitude has a positive significant on behavioral intention to use e-Banking system.

Eriksson, Kent (2000) found that the perceived use is positively affected by perceived usefulness, But perceived ease of use has not a positive effect on perceived use. Perceived ease of use has a positive effect on the perceived usefulness and Trust has a positive effect on both perceived ease of use and perceived usefulness. He also found that perceived ease of use has an effect on perceived use, but only via as the mediating variable, perceived usefulness. Intana, & Chuvej (2014) found that the original TAM construct of Perceived Usefulness as the strongest predictor of Intention to Use. However, it is found that Perceived Ease of Use is not a directly significant predictor of Intention to Use and also found that Perceived Ease of Use has an indirect effect on Intention to Use via Perceived Usefulness. Wu, Chun & Li, Cheng-Lung (2010) found that trust and perceived ease of use were the most influential factors explaining perceived usefulness of online banking services and Perceived ease of use was almost statistically significant, which found that PEOU has an impact on PU. Mir, Raies, Rifat & Altaf (2013) found that as customer attitude, perceived usefulness and perceived ease of use are critical factors that affect the user acceptance and also found that the positive feeling and attitude of user is essential for the e-banking usage level.

Dickinson & Rogers (2013) found that there is a significant relationship between Security & Privacy and information availability with Perceived Value and Perceived Value of Internet Banking. Srivastava (2007) found that the perception of the consumers can be changed by awareness program, friendly usage, less charges, proper security, and the best response to the services offered and suggested that banks need to concern about awareness among the customers.

Kumar (2004) found that there is strong association between Perceived Ease of Use, Perceived Enjoyment and Attitude towards Internet Banking and also found that the Perceived Enjoyment is the major factor determining the attitudes of customers towards Internet Banking. Al-Smadi (2012) found that perceived usefulness and perceived ease of use has a positive and significant impact on customers' attitude toward electronic banking services and also found that there is a positive and significant impact of perceived risk on the customers' attitudes to use electronic banking services. Wang, Changlin & Fang, Runsheng (2012) concluded that the perceived security is an important factor affecting the perceived usefulness and the perceived value, but it doesn’t have remarkable effects on users’ intention to use. But the perceived security and the perceived usefulness greatly affects users perceived value.

International Journal of Research in Marketing Management 2017

33 Volume 1 Number 1

Fred D. Davis (2008) found that Perceived Usefulness is significantly related to the Perceived Usage and significantly effect on User Acceptance and affect ease of use also but less intensely than on perceived usefulness. Singh (2013) explored that Security & Privacy is the most important factor that influences the adoption of internet banking rather than other factors. Waithaka and Nzeveka (2015) found that security and privacy of internet banking significantly explains the effects of customer’s perception on usage of internet banking in commercial banks and found that there is a general concern that internet banking security and privacy is not fully guaranteed. Khalaf, Ahmad & Ali (2011) found that customer satisfaction has a positive significant influence on customer loyalty of adopting e-banking service. Loong, Binshan & Boon-In (2010), found that perceived usefulness, trust and government support all are positively associated with the intention to use online banking. On the other hand, Technology acceptance model, perceived ease of use was found to be not significant.

OBJECTIVES OF THE STUDY

To investigate the cause and effect relationship among Perceived Usefulness, Ease of Use, Security & Privacy on Customer Attitude in the context of E-banking services.

To evaluate the cause and effect relationship among Perceived Usefulness, Ease of Use, Security & Privacy on Customer Adaptation in the context of E-banking services.

To check the relationship between customer attitude and customer adoption.

HYPOTHESIS OF THE STUDY

H01: There is no relationship between Perceived Usefulness and Customer Attitude in the context of e-banking.

H02: There is no relationship between Ease of Use and Customer Attitude in the context of e-banking.

H03: There is no relationship between Security and Customer Attitude in the context of e-banking.

H04: There is no relationship between Privacy and Customer Attitude in the context of e-banking.

H05: There is no relationship between Perceived Usefulness and Customer Adaptation in the context of e-banking.

H06: There is no relationship between Ease of Use and Customer Adaptation in the context of e-banking.

H07: There is no relationship between Security and Customer Adaptation in the context of e-banking.

International Journal of Research in Marketing Management 2017

34 Volume 1 Number 1

H08: There is no relationship between Privacy and Customer Adaptation in the context of e-banking.

H09: There is no relationship between Customer Attitude and Customer Adaptation in the context of e-banking.

RESEARCH METHODOLOGY

The study was causal in nature being survey method was used for data collection. Sample design consists of the size of population, sample element, sample size and sampling techniques. The population of the current study was all the user of E-Banking services who were enjoying banking services from various banks in India. The sample size of the current study was two hundred three. It consists of combination of Gender and Age. Age was used as demographics and it consists of three different categories of respective respondents in the current study e. i., there were 153 respondents in age group of 19-39, 25 respondents who were between 34-46 and 27 respondents in age group 47-59. Gender was illustrated as between male and female towards the adaptation of e-banking. In the study there were total 112 males and 91 females. Sampling techniques referred as the way to collect the data in the research. Hence, Non probabilities judgemental sampling techniques was used to get respond from the respondents. Individual respondent was treated as sampling element in the current study.

Measures: For the purpose of data collection a standardized questionnaires were utilized with bit modification having understood the requirement of the current study e.,i. Perceived Usefulness, Ease of Use, Security, Privacy, Customer Attitude and Customer Adaptation on Likert type of scale and possessed a sensitivity between 1-5 where the extreme value 1 and 5 representative strongly disagree and strongly agree Five items scale of Perceived Usefulness and Ease of Use was adopted and used in the current study Cited from: Mwesigwa ROGERS (2008), Four items scale of Security & Six items scale of Privacy was assessed for current study form Juan Carlos Roca, Juan José García, Juan José de la Vega, (2009), Seven items scale of Customer Attitude was originally developed by Davis, 1989 and used by Pikkarainen et al. (2004) Jahangir and Begum (2008), Amin (2007), Shih and Fang (2004), Eriksson et al. (2005) and customer attitude was Cited from: Alain Yee-Loong Chong, Keng-Boon Ooi, Binshan Lin, Boon-In Tan, (2010) in the current study, Five item scale of Customer Adaptation was originally developed by Davis (1989) and used by Pikkarainen et al. (2004), Jaruwachirathanakul and Fink (2005), Tan and Teo (2000), Shih and Fang (2004), Jahangir and Begum, 2008) and Customer attitude was Cited from: Alain Yee-Loong Chong, Keng-Boon Ooi, Binshan Lin, Boon-In Tan, (2010).

RESULTS & DISCUSSION

Reliability Test

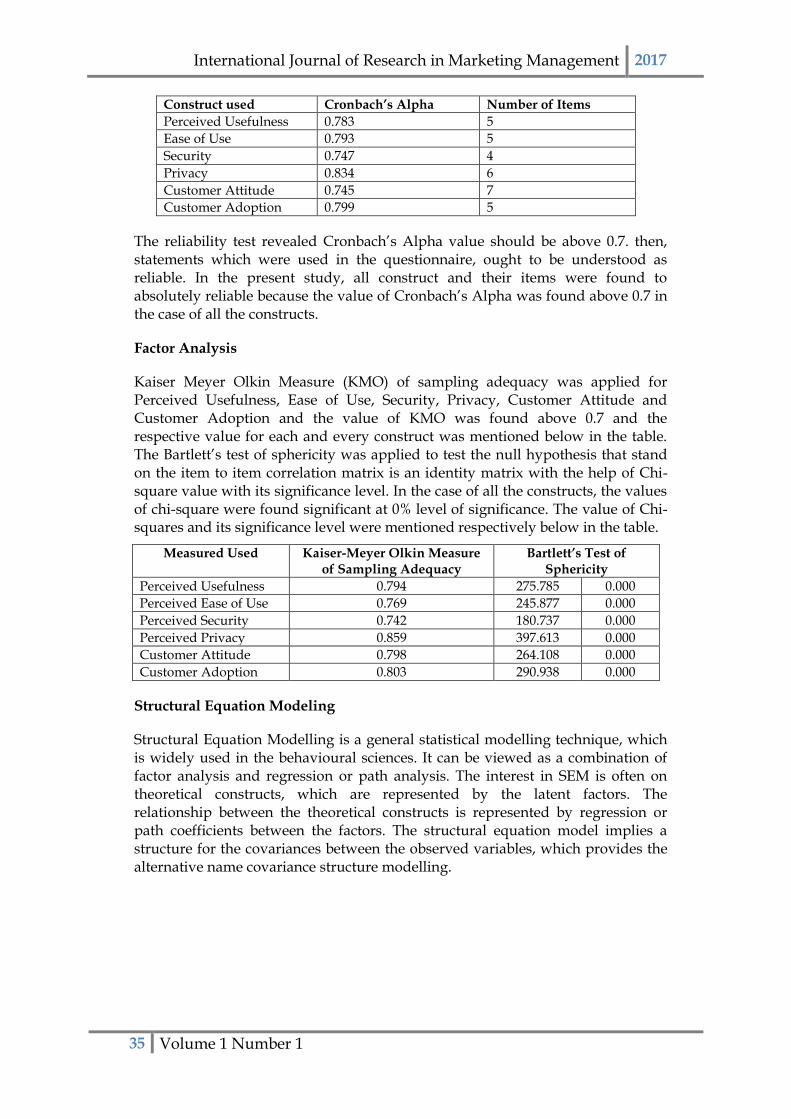

The reliability was computed by using IBM SPSS 18 version software. Cronbach’s alpha reliability test was applied to check the reliability coefficient was computed for the all statements in the questionnaire for the variables perceived usefulness, ease of use, security, privacy, customer attitude and customer adaptation.

International Journal of Research in Marketing Management 2017

35 Volume 1 Number 1

Construct used Cronbach’s Alpha Number of Items

Perceived Usefulness 0.783 5

Ease of Use 0.793 5

Security 0.747 4

Privacy 0.834 6

Customer Attitude 0.745 7

Customer Adoption 0.799 5

The reliability test revealed Cronbach’s Alpha value should be above 0.7. then, statements which were used in the questionnaire, ought to be understood as reliable. In the present study, all construct and their items were found to absolutely reliable because the value of Cronbach’s Alpha was found above 0.7 in the case of all the constructs.

Factor Analysis

Kaiser Meyer Olkin Measure (KMO) of sampling adequacy was applied for Perceived Usefulness, Ease of Use, Security, Privacy, Customer Attitude and Customer Adoption and the value of KMO was found above 0.7 and the respective value for each and every construct was mentioned below in the table. The Bartlett’s test of sphericity was applied to test the null hypothesis that stand on the item to item correlation matrix is an identity matrix with the help of Chi-square value with its significance level. In the case of all the constructs, the values of chi-square were found significant at 0% level of significance. The value of Chi-squares and its significance level were mentioned respectively below in the table.

Measured Used Kaiser-Meyer Olkin Measure of Sampling Adequacy

Bartlett’s Test of Sphericity

Perceived Usefulness 0.794 275.785 0.000

Perceived Ease of Use 0.769 245.877 0.000

Perceived Security 0.742 180.737 0.000

Perceived Privacy 0.859 397.613 0.000

Customer Attitude 0.798 264.108 0.000

Customer Adoption 0.803 290.938 0.000

Structural Equation Modeling

Structural Equation Modelling is a general statistical modelling technique, which is widely used in the behavioural sciences. It can be viewed as a combination of factor analysis and regression or path analysis. The interest in SEM is often on theoretical constructs, which are represented by the latent factors. The relationship between the theoretical constructs is represented by regression or path coefficients between the factors. The structural equation model implies a structure for the covariances between the observed variables, which provides the alternative name covariance structure modelling.

International Journal of Research in Marketing Management 2017

36 Volume 1 Number 1

Proposed Model for testing

Absolute Fit Indices

Absolute fit indices determine how well a tested model fits the sample data (Mc Donald and Ho, (2002) and demonstrates which proposed model has the most superior fit. These measures provide the most fundamental indication of how well the proposed theory fits the data. The Chi-square value is the traditional measure for evaluating overall model fit and , ‘Assesses the magnitude of discrepancy between the sample and fitted covariance matrices’ (Hu and Benter, 1999:2). A good model fit would provide an insignificant result at a 0.05 threshold (Barrett, 2007).

As it was mentioned above that the first and foremost indicator of testing fitness of model is chi-square and in the current study the value of chi square was found 144.263 significant at 0.065 level of significance. As it was also stated that in case

International Journal of Research in Marketing Management 2017

37 Volume 1 Number 1

of SEM Model the chi-square value should be significant at more than 0.05 value of significant then only the SEM model is considered as fits.

There are few more indices which are tested through their threshold value Such as RAMSEA. The RAMSEA is the second fit statistic and was developed by steiger and Lind (1980, Cited in steiger, 1990). The RAMSEA tell us how well the model, with unknown but optimally chosen parameter estimates would fit the population covariance matrix (Byrne, 1998). RAMSEA In the range of 0.05 to 0.10 was considered an indication of fair fit and value 0.10 indicated poor fit (Mac Callum et al. 1996). RAMSEA between 0.08 - 0.10 provides a mediocre fit and below 0.08 shows a good fit (Mac Callum et al, 1996). However, a cut off value close to 0.06 (Hu and Bentler , 1996) or stringent upper limit of 0.07 (Steiger, 2007) seems to be the general consensus amongst authorities in this area.

The value of RAMSEA was found in the current study was 0.032, indicating the current model is absolute fit because the value of RAMSEA is in range of threshold value 0.06.

Table: 6 Absolute Model Fit Statistics of Final Model

Absolute Fit Measures

χ2 DF χ2/DF RMR RMSEA GFI AGFI P

Criteria 1< 2 < 0.05 < 0.05 ≥0.90 ≥0.90

Obtained 144.263 120 144.263 0.45 0.032 0.929 0.899 0.065

Incremental Fit Measures

NFI RFI IFI TLI CFI

Criteria ≥0.90 ≥0.90 ≥0.90 ≥0.90 ≥0.90

Obtained 0.872 0.837 0.976 0.968 0.975

Goodness of Fit Indices

The result of model fit indicates that most of the goodness of fit indices were found to be good with their relative recommended thresholds. The fit indices of SEM are showing (GFI) of 0.929. The adjusted goodness of the fit Index (AGFI) shows a value of 0.899 implying an acceptable model fit. The (PGFI) value was found to be 0.652 and this value should be below from 0.5 wherein it was found to be a little weak. The model result indicates the other goodness of fit indicate a good parsimony fit. The model result indicates that the other goodness of fit indices was also found to be good with respect to their relative recommended thresholds; CFI= 0.975; NFI = 0.872; TLI = 0.968. The results implied that it has a good model fit.

Badness of Fit Indices

The RMSEA value was found in 0.032 which is less than the threshold value 0.05 therefore it can be considered to be good. According to Diamantopoulos and Siguaw (2000) RMSEA is generally regarded as one of the most informative fit indices. The RMR measures residual variances which reveal the average amount of variance and covariance’s which are not accounted for by the model. Usually value less than.05 is regarded as an indication of good model. In the current model, RMR was found to be.0.45 indicating a good fit.

International Journal of Research in Marketing Management 2017

38 Volume 1 Number 1

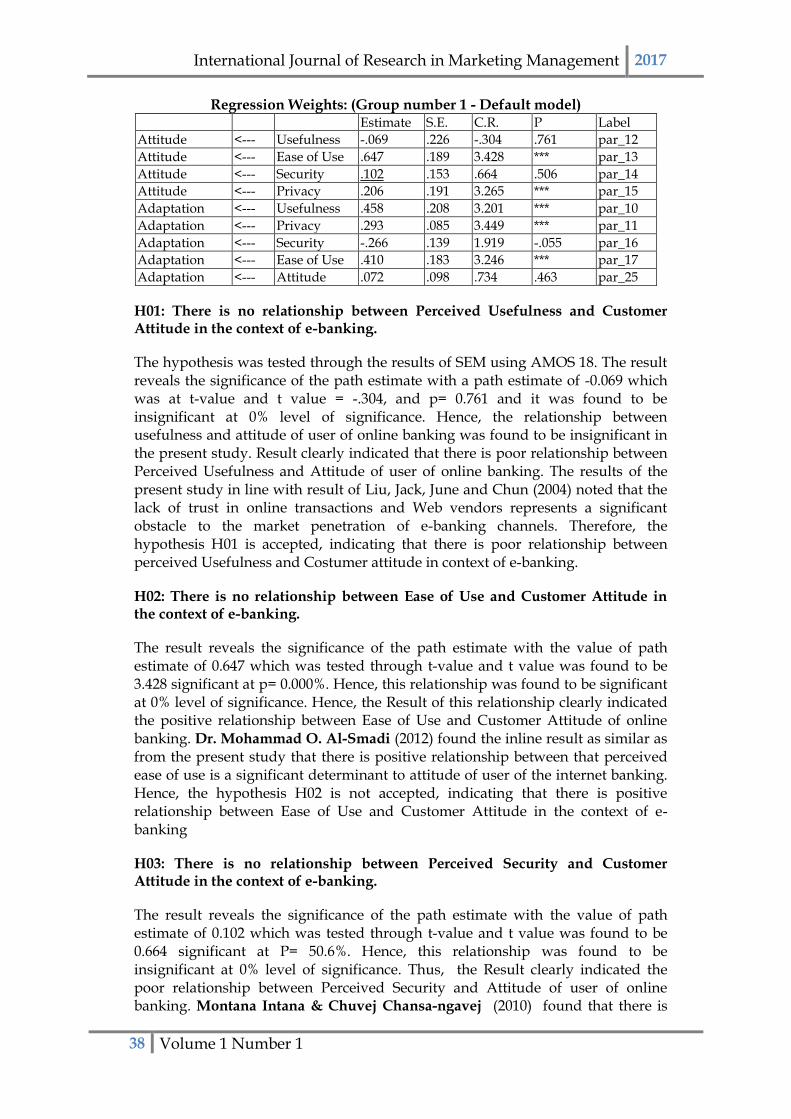

Regression Weights: (Group number 1 - Default model) Estimate S.E. C.R. P Label

Attitude <--- Usefulness -.069 .226 -.304 .761 par_12

Attitude <--- Ease of Use .647 .189 3.428 *** par_13

Attitude <--- Security .102 .153 .664 .506 par_14

Attitude <--- Privacy .206 .191 3.265 *** par_15

Adaptation <--- Usefulness .458 .208 3.201 *** par_10

Adaptation <--- Privacy .293 .085 3.449 *** par_11

Adaptation <--- Security -.266 .139 1.919 -.055 par_16

Adaptation <--- Ease of Use .410 .183 3.246 *** par_17

Adaptation <--- Attitude .072 .098 .734 .463 par_25

H01: There is no relationship between Perceived Usefulness and Customer Attitude in the context of e-banking.

The hypothesis was tested through the results of SEM using AMOS 18. The result reveals the significance of the path estimate with a path estimate of -0.069 which was at t-value and t value = -.304, and p= 0.761 and it was found to be insignificant at 0% level of significance. Hence, the relationship between usefulness and attitude of user of online banking was found to be insignificant in the present study. Result clearly indicated that there is poor relationship between Perceived Usefulness and Attitude of user of online banking. The results of the present study in line with result of Liu, Jack, June and Chun (2004) noted that the lack of trust in online transactions and Web vendors represents a significant obstacle to the market penetration of e-banking channels. Therefore, the hypothesis H01 is accepted, indicating that there is poor relationship between perceived Usefulness and Costumer attitude in context of e-banking.

H02: There is no relationship between Ease of Use and Customer Attitude in the context of e-banking.

The result reveals the significance of the path estimate with the value of path estimate of 0.647 which was tested through t-value and t value was found to be 3.428 significant at p= 0.000%. Hence, this relationship was found to be significant at 0% level of significance. Hence, the Result of this relationship clearly indicated the positive relationship between Ease of Use and Customer Attitude of online banking. Dr. Mohammad O. Al-Smadi (2012) found the inline result as similar as from the present study that there is positive relationship between that perceived ease of use is a significant determinant to attitude of user of the internet banking. Hence, the hypothesis H02 is not accepted, indicating that there is positive relationship between Ease of Use and Customer Attitude in the context of e-banking

H03: There is no relationship between Perceived Security and Customer Attitude in the context of e-banking.

The result reveals the significance of the path estimate with the value of path estimate of 0.102 which was tested through t-value and t value was found to be 0.664 significant at P= 50.6%. Hence, this relationship was found to be insignificant at 0% level of significance. Thus, the Result clearly indicated the poor relationship between Perceived Security and Attitude of user of online banking. Montana Intana & Chuvej Chansa-ngavej (2010) found that there is

International Journal of Research in Marketing Management 2017

39 Volume 1 Number 1

insignificant relationship between Perceived Security and Customer Attitude in the context of e-banking. Thus, the result of this study provided support or found in line the result of present study. Hence, the hypothesis H03 is accepted, indicating that there is poor relationship between Perceived Security and Customer Attitude in the context of e-banking.

H04: There is no relationship between Perceived Privacy and Customer Attitude in the context of e-banking.

The result of this relationship reveals the significance of the path estimate with the value of path estimate of .206 which was tested through t-value and t value was found to be 3.265 significant at p= 0.000% level of significance. Hence, this relationship was found to be significant at 0% level of significance. Thus, the result clearly indicated the positive relationship between Perceived Privacy and Customer Attitude of users with respect of online banking. Eng. Dickinson

Turinawe & Rogers Mwesigwa (2012) found inline result as from present study that there is a positive relationship between Perceived Privacy and Attitude in internet banking. Hence, the hypothesis H04 is not accepted, indicating that there is positive relationship between Perceived Privacy and Customer Attitude in the context of e-banking.

H05: There is no relationship between Perceived Usefulness and Customer Adaption in the context of e-banking.

The result of this relationship reveals the significance of the path estimate with the value of path estimate of .458 which was tested through t-value and t value was found to be 3.201 significant at, p = 0.00% level of significance. Hence, this relationship was found to be significant at 0% level of significance. Thus, the result clearly indicated the positive relationship between Perceived Usefulness and Customer Adaption with respect of online banking. Alain Yee-Loong Chong,

Keng-Boon Ooi, Binshan Lin, Boon-In Tan (2010) found that perceived usefulness is a significant determinant to predict the intention to use the internet banking. Hence, hypothesis H05 is not accepted, indicating that there is positive relationship between Perceived Usefulness and Costumer Adaptation in context of e-banking.

H06: There is no relationship between Ease of Use and Customer Adaption in the context of e-banking.

The result of this relationship reveals the significance of the path estimate with the path estimate of .410 which was tested through t-value and t value was found to be 3.246, significant at p= 0.000% level of significance. Hence, the result clearly indicated the positive relationship between Ease of Use and Customer Adaption in the context of E-banking. Thus, The Result clearly indicated the positive relationship between Ease of Use and Adaption for online banking. Nushrat Islam (2008) found there is positive and significant relationship between perceived ease of use and customer adaptation of electronic banking. Therefore, the hypothesis H06 is not accepted, indicating that there is positive relationship between Perceived Ease of Use and Costumer Adaptation in context of e-banking

H07: There is no relationship between Perceived Security and Customer Adaption in the context of e-banking.

International Journal of Research in Marketing Management 2017

40 Volume 1 Number 1

The result of this relationship reveals the significance of the path estimate with the path estimate of -0.266 which was tested through t-value and t value was found to be -1.919, significant at p= 5.5% level of significance. Hence, the result clearly indicated the negative insignificant relationship between Perceived Security and Customer Adaption in context of E-Banking. Thus, it was found to be insignificant at 0% level of significance. Result clearly indicated that there is poor relationship between Perceived Security and Customer Adaption in the context of e-banking. Lilesh Gautam & Sanjeev Kumar Khare (2013) found that there is no positive and significant relationship between Perceived Security and Customer Adaption in the context of e-banking.

H08: There is no relationship between Perceived Ease of Use and Customer Adaption in the context of e-banking.

The result of this relationship reveals the significance of the path estimate with the path estimate of .410 which was tested through t-value and t value was found to be 3.449, significant at p= 0.000% level of significance. Hence, the relationship between Perceived Ease of Use and Customer Adaption clearly indicated the positive relationship between Perceived Usefulness and Adaption of users of online banking. Lilesh Gautam & Sanjeev Kumar Khare (2013) found that there is positive and significant relationship between Perceived Ease of use and Customer Adaption in the context of e-banking. Thus, the result of this study provides support to this relationship. Hence, the hypothesis H08 is not accepted, indicating that there is positive relationship between Perceived Ease of Use and Customer Adaption in the context of e-banking.

H09: There is no relationship between Customer Attitude and Customer Adaption in the context of e-banking.

The results reveal the significance of the path estimate with the path estimate of .072 which was tested through t-value and t value was found to be 0.734, significant at p=46.3% level of significance. Hence, Result clearly indicated the poor relationship between Customer Attitude and Customer Adaption of users of online banking. Nushrat Islam (2005) found that there is insignificant relationship between Customer Attitude and Customer Adaption in his research study. Thus, the result of this study support significant to the result of the current study, Hence, the hypothesis H09 is not accepted, indicating that there is poor relationship between Customer Attitude and Customer Adaption in the context of e-banking.

IMPLICATIONS

The current study is very useful to identify the effect of perceived usefulness, ease of use, security & privacy on customer attitude and customer adaptation which will help the policy maker in banks to develop the adequate and effective online banking services. Customer attitude and consumer adaption are crucial determinant which have been discussed in detail in the current study so it would help to understand customer attitude and consumer adaption through perceived usefulness, ease of use, security & privacy.

International Journal of Research in Marketing Management 2017

41 Volume 1 Number 1

Researcher can use the used standardized questionnaire of perceived usefulness, ease of use, Security & Privacy and Customers’ Attitude and Adaptation in future to identify new gaps. Although the results of the study are helpful in understanding the perceived usefulness, ease of use, security and privacy and its relationship with the customers’ attitude and customers’ adaptation, yet it is not without certain limitations that need to be addressed with future research. The study was done by taking only sample size of 203 respondents therefore it is suggested to take large sample size in order to obtain more accurate results.

CONCLUSION

The study is resulted in number of findings. All the variables were find to be consistent reported reliability near about or higher than 0.7 in all the cases. The study was intended to study about the use of e-banking. The study can be concluded in such a manner that the strong relationship was found between the Ease of Use and Attitude, Privacy and Attitude, Perceived Usefulness and Customer Adaptation, Ease of Use and Customer Adaptation, Privacy and Customer Adaptation and Security and Customer Adaptation.

REFERENCES

Adesina Aderonke, A., and Ayo Charles (2010). An Empirical Investigation of the Level of Users’ Acceptance of E-Banking in Nigeria, Journal of Internet Banking and Commerce, 15(1): 102-145.

Akram Jalal, Jassim Marzooq and Hassan A. Nabi (2011), Evaluating the Impacts of Online Banking Factors on Motivating the Process of E-banking, Journal of Management and Sustainability, Vol.1, Issue-1, pp.32-42.

Ala`Eddin Mohd Khalaf Ahmad & Dr. Hasan Ali Al-Zu’bi (2011), E-banking Functionality and Outcomes of Customer Satisfaction, International Journal of Marketing Studies. Vol. 3, No. 1; pp. 50-65

Alain Yee-Loong Chong, Keng-Boon Ooi and Binshan Lin, BoonIn Tan (2010). Online banking adoption: an empirical analysis. International Journal of Bank Marketing. 28(4): 267-287

Ayo, C.K (2010), the State of e-Banking Implementation in Nigeria: A Post-Consolidation Review, Journal of Emerging Trends in Economics and Management Sciences. 1 (1): 37-45

Changlin Wang, Runsheng Fang (2012), Perceived Usefulness, Perceived Security and Adoption of Mobile Government: An Empirical Research, Journal of Advances in information

Sciences and Service Sciences (AISS). 4(6): 234-244.

Coughlan Joseph and Mullen Michael (2008), Structural Equation Modelling: Guidelines for Determining Model Fit, Electronic Journal of Business Research Methods Volume 6 Issue 1; pp. 53 – 60

Diamantopoulos, A., & Judy A. Siguaw (2000) “Introducing LISREL: A Guide for the Uninitiated”: SAGE Publications, Ltd, ISBN 144622659X, 9781446226599. doi: http://dx.doi.org/10.4135/978184920935

International Journal of Research in Marketing Management 2017

42 Volume 1 Number 1

Dickinson Turinawe & Rogers Mwesigwa (2013), Relationship between Security and Privacy, Quality of Internet Connection and Internet Banking Acceptance in Uganda: Testing for Perceived Value as a Mediator using Multiple Regression, International Journal of Business and Behavioral Sciences, vol., No 6 pp 1-20.

Dobdinga Cletus Fonchamnyo (2013), Customers’ Perception of E-banking Adoption in Cameroon: An Empirical Assessment of an Extended TAM, International Journal of Economics and Finance. vol. 5, no. 1, 2013, pp. 166-176.

Fred D. Davis (1989), Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology, in Computer and Information Systems Graduate School of Business Administration University of Michigan Ann Arbor, 13(3): 319-340

Gitanjali Shrivastava, Dr. Ira Bapna (2011), Perception of Youth towards Internet Banking - Remodeling Banking Industry Globally, Altius Shodh Journal of Management & Commerce. Vol.1 Issue 8, ISSN 2231 5780 pp 62-72

Hossein Rezaei Dolat Abadi & Fateme Nematizadeh (2012), An Empirical Investigation of the Level of User's Acceptance of E-Banking among Some Customers of Banks in Iran, International Journal of Academic Research in Business and Social Sciences. Vol. 2, No. 6 ISSN: 2222-6990 pp 418-430

Hsueh-Ying Wu,Chun-Chun Lin,Cheng-Lung Li (2010), A Study of Bank Customers’ Perceived Usefulness of Adopting Online Banking, Global Journal of Business Research. Vol. 4, No. 3, pp. 101-108, 2010

Juan Carlos Roca, Juan José García, Juan José de la Vega (2009), Information Management & Computer Security Emerald Article: The importance of perceived trust, security and privacy in online trading systems, Vol. 17 Iss: 2, pp.96 – 113

Kent Eriksson (2000), Customer Acceptance of Internet Banking in Estonia, International Journal of Bank Marketing 23(2), DOI: 10.1108/02652320510584412

Lilseh Gautam & Sanjeev Kumar Khare (2013), Factors Affecting the Acceptance of E-Banking among Customers of Gwalior Region, shodh sanchayan, An Internationally Indexed Refereed Research Journal & A complete Periodical dedicated to Humanities & Social Science Research, VOL-4,Issue 2, pp 1-6, ISSN:2249-9180.

MacCallum, Robert C and Browne, Michael W (1996), Power Analysis and Determination of Sample Size for Covariance Structure Modelling Psychological Method, Vol. I, No. 2, 13(1 149) pp 130-149

Malika Rani (2012), A Study on the Customer Perception towards e-banking in Ferozepur District, International Journal of Multidisciplinary Research. Vol.2 Issue 1, January 2012, ISSN 2231 5780 pp 108-118

Mohammad O. Al-Smadi (2012), Factors Affecting Adoption of Electronic Banking: An Analysis of the Perspectives of Banks' Customers, International Journal of Business and Social Science. Vol. 3 No. 17; September 2012 pp 294-309

Montana Intana, Shinawatra & Suvarnabhumi (2010), An extended technology acceptance model for internet banking adoption, Asian Journal of Management Rresearch. Volume 5 Issue 1, 2014 pp 124-137

International Journal of Research in Marketing Management 2017

43 Volume 1 Number 1

Maduku, D.K. (2013), Predicting retail banking customers’ attitude towards Internet banking services in South Africa, Southern African Business Review. Volume 17 Number 3 2013 pp 76-100

Nadim Jahangir and Noorjahan Begum (2008), The role of perceived usefulness, perceived ease of use, security and privacy, and customer attitude to engender customer adaptation in the context of electronic banking, African Journal of Business Management. Vol.2 (1), pp. 032-040, February, 2008

Raies Ahmad Mir RifatAra & Dr. Altaf A Dar (2013), Customer Attitude and Factors Influencing Users Acceptance of E-Banking in J&K, International Journal of Business and Management Invention. ISSN (Online): 2319 – 8028, ISSN (Print): 2319 – 801X www.ijbmi.org Volume 2 Issue 7ǁ July. 2013ǁ PP.68-78

Raies Ahmad, Mir RifatAra & Dr. Altaf A Dar (2013), Customer Attitude and Factors Influencing Users Acceptance of E-Banking in J&K, International Journal of Business and Management Invention. Volume 2 Issue 7ǁ July. 2013ǁ PP.68-78

Rajesh Kumar Srivastava (2007), Customer’s Perception on usage of Internet Banking, Innovative Marketing Volume 3, Issue 4, 2007 pp 67-73

Roderick, P. McDonald and Moon-Ho Ringo, Ho (2002), Principles and Practice in Reporting Structural Equation Analyses, Psychological Methods 7(1), 64–82.

S. Arunkumar (2004), A study on attitude and intention towards Internet banking with reference to Malaysian consumers in klang valley region, The International Journal of Applied Management and Technology 6(1). Pp 115-146

Shah Ankit (2011),Factors Influencing Online Banking Customer Satisfaction and Their Importance in Improving Overall Retention Levels: An Indian Banking Perspective, Information and Knowledge Management.1(1):45-54

Shidrokh Goudarzi, Mohammad Nazir Ahmad, Seyed Ahmad Soleymani, Nastaran Mohammadhosseini (2013), Impact of Trust on Internet Banking Adoption: A Literature Review, Australian Journal of Basic and Applied Sciences.Vol. 7 Issue 7, p334

Steiger, James H. (1990), Structural Model Evaluation and Modification: An Interval Estimation Approach, Multivariate Behavioural Research 25(2), 173-180.

Stephen Titus Waithaka & Kilembwa Muthengi Joseph Nzeveka (2015), The Effect of Customers Perception on Security and Privacy of Internet Banking On Its Usage in Commercial Banks in Kenya, International Journal of Recent Research in Mathematics Computer Science and Information Technology Vol. 2, Issue 1, pp: (219-229),

Tejinderpal Singh (2013), Security and Privacy issues in e-banking: an empirical study of Customers’ Perception, Indian Institute of Banking and Finance (iibf) Mumbai. Downloaded at www.iibf.org.in/documents/reseach-report/Tejinder_Final%20.pdf , dated on 16/12/2016,at 10:39 am.

Vishal Mohan Goyal & Mrs. Gania Goyal (2009), w.r.f to private and foreign banks in India, International Journal of Computing & Business Research. ISSN: 2229-6166.