tnt express capital markets day analyst presentation nl australia & pacific rest of asia india...

TRANSCRIPT

11

Agenda

Opening 13:00 Antony Burgmans

Express investment opportunity

Marie-Christine LombardEMEA

Americas

Aspac

International and SME sales Jan Willem Breen

Aspac Michael Drake

Short break 14:30

Finance 14:50 Bernard Bot

Q&A 15:15

Closing 16:00 Marie-Christine Lombard

Drinks – reception

TNT ExpressCapital Markets Day

Marie-Christine Lombard3 May 2011

33

TNT Express organisation

Supervisory Board

Mr A BurgmansChairman Mr T Gunning Ms M Scheltema Mr R King Mr S Levy Ms M Harris

Executive BoardMs MC Lombard

CEOMr B Bot

CFO

Management BoardMr JW Breen

Director Marketing & Sales

Ms C GoossensDirector Global

Operations

Mr G MasonICS Managing

Director

Mr S ScheersHR Director

Mr D BurtonRegional Managing

Director Northern Europe

Mr C DrenthenRegional Managing

Director SE and MEA

Mr M DrakeRegional Managing

Director ASPAC

44

Agenda

Express investment opportunity

EMEA

Americas

Aspac

5

TNT: leader in Europe, attractive growth options

Unique position in attractive Express market

• Large and growing Express market• Unique position TNT

Leader in Europe and MEA with significant upside potential

• Number 1 B2B Express player in Europe

• Track record of high margins

Positioned to leverage high-growth in emerging markets

• Number 1 China to Europe with dedicated fleet

• Leading presence in domestic emerging markets

High growth and high returns

6

Large and growing market benefiting TNT networks

Source: TNTNote: € 22 billion includes intercontinental; Aspac excludes €8 billion Japan

Revenuegrowth

Real GDPgrowth

South America

4

Aspac

8

EMEA

22

2.0 – 2.5x

Large market with leading presence TNT€ billion, 2009, B2B

TNT

Other

GrowingGDP multiple revenue growth – 2005 to 2010

Enablingleverage of

network economics

7

Global footprint TNT

OtherAmericas

Aspac

EMEA

0.40.5

1.74.5

Africa & ME Rest of Europe

Belgium

France

GermanyItaly

UK

NL

Australia & Pacific

Rest of Asia

India

Greater China

South & Middle America

Brazil

USA and Canada

Revenue contribution and headcount by segment and by country

Headcount

EMEA 36,184

Aspac 31,924

Americas 11,081

Other 4,047

(€ billion)

88

Unique position TNTWide product offer Broad geographic presence

Flexible cost model

Europe

Intercontinental

Emerging platforms

TNTOutsourced

Parcels

Spee

d

Weight

Express

EconomyExpress

Freight

Time certain/Next day

Day uncertain/Standard

Same day

Day certain/Expedited

1kg ~30 kg 1,000 kg

Customer-first focus

99

Number 1 Significant upside potential

Leading in Europe and MEA with significant upside potential

Note: 2001 – 2003 Express division restated for one-offs, from 2007 revenue at reported rates

2

4

6

8

10

12

14

10090807060504030201

Operating margin (%)

DPD/La Poste

8%

UPS9%

DHL15%

TNT

18%

Other 50%

Intra-Europe B2B Express 100% = € 19 billion (2009)

Medium term

10

Strong growth as first mover in emerging markets

#1 China to Europe

• Own-controlled Express uplifts • Seamless connectivity • Key sectors

Share of revenues China-to-Europe Express

Leading domestic positions

• Double-digit growth• Upgrading of delivery infrastructure• TNT first-mover advantage

DHL 31%

TNT 33%Other46%

100% = € 1.2 billion (2009)

Largest domestic operator with ~20% market share

Largest privately owned domestic network

1111

TNT’s global footprint

Americas

Aspac

EMEA

Other

Africa & ME Rest of Europe

Belgium

France

GermanyItaly

UK

NL

Australia & Pacific

Rest of Asia

India

Greater China

South & Middle America

Brazil

USA and Canada

Revenue contribution by segment and by country

1212

Unique geographic European footprint

8%9%

DPD/La PosteUPS

15% DHL

TNT

18%

Other 50%

B2B Express intra-Europe market share100% = € 19 billion (2009)

Iberia

0.2

EE

0.3

Nordics

0.3

I

0.6

BNL

0.7

F

0.7

G

0.8

UK

0.9

Revenues by country2010, € billion

1313

Leading European road and air networks

European road network European air network

• 39 countries• 16 road hubs • 85 international depots• Connecting 523 depots• 70% of customers by value can

be reached overnight by truck

• 46 planes• 65 airports• 19 countries• 635 flights per week• Late pick-up and early

next-day drop-off

Unique combination networks: Air / Road

International / Regional / Domestic

1414

Good growth prospects Europe

Europe growth

Organic

New initiatives

2.0 – 2.5

2.12.0 2.1

201420132012

Europe GDP forecasts*

x=

* Source: Economist Intelligence Unit

Express factor growth

• Value added solutions (VAS)• Parcels B2C• Freight

15

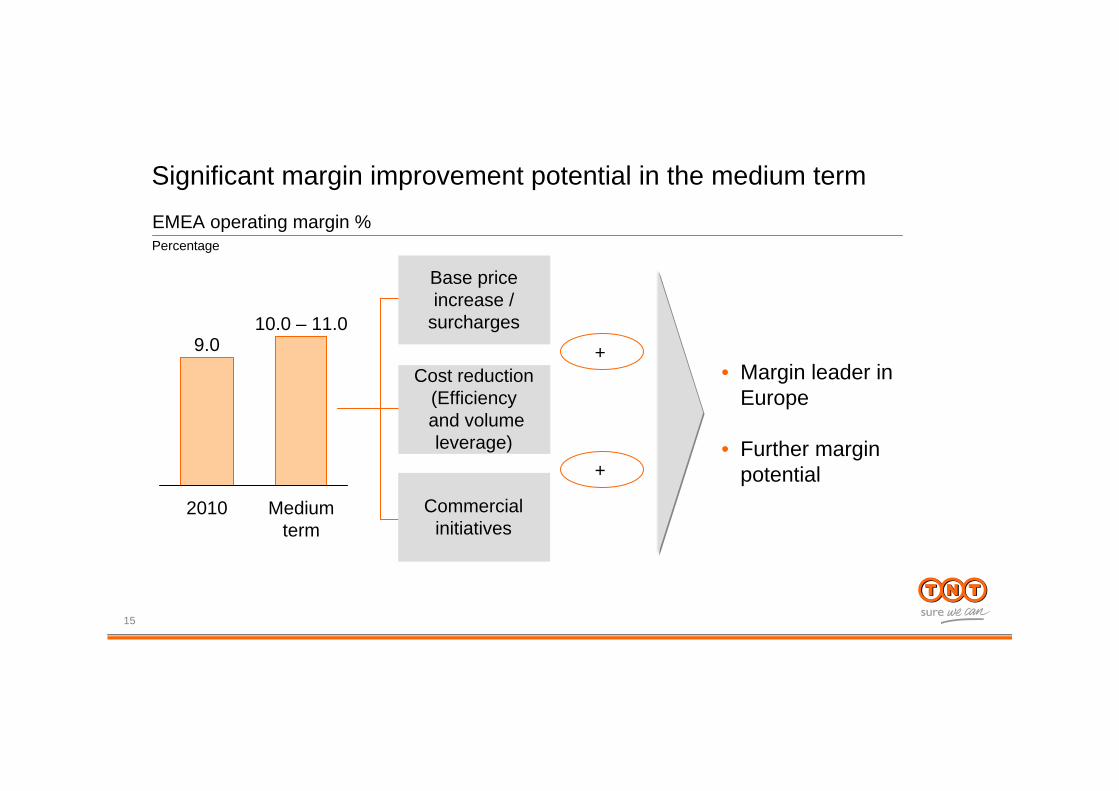

Base price increase /

surcharges

Significant margin improvement potential in the medium term

Medium term

10.0 – 11.0

2010

9.0 +

+

Cost reduction(Efficiencyand volume leverage)

Commercial initiatives

EMEA operating margin %Percentage

• Margin leader in Europe

• Further margin potential

1616

Base price increases and surcharge opportunitiesEMEA

Price Q1 2011 Objectives

International Express Positive

• Focus on increasing volumes• Application of surcharges

International Economy Above inflation

Further increase price given high demand/differentiated service

Domestic Some pressure Focus on most attractive accounts given solid growth

1717

Cost reductions to continue

Average cost per consignmentYoY growth %

Targets

-2

-10

32

2010200920082007

Local operations• LEAN depot and warehouse• PUD routing optimisation

Central operations• Capacity optimisation• HUB operations productivity

Indirect and other• Target indirect cost reduction

18

+

Commercial initiatives

Margins

+

Express Economy DomesticSolutions

Globalaccounts

Majoraccounts

SME

Solutions

Broadest product offering

Customer service

1919

TNT’s global footprint

Americas

Aspac

EMEA

Other

Australia & Pacific

Rest of Asia

India

Greater China

South & Middle America

Brazil

USA and Canada

Revenue contribution by segment and by country

Africa & ME Rest of Europe

Belgium

France

GermanyItaly

UK

NL

20

• Global customer demand• High growth market• Opportunity to leverage from domestic

position to intra-regional and intercontinental services

20

Brazil: strategic rationale

Other

79%

Integrators1%

TNT

20%

Domestic Brazil market share100% = ~€1.8 billion; domestic Express

• Combination of Mercúrio (acquired 2007) and Araçatuba (acquired 2009)

• 140 locations, ~8,000 employees, more than 3,000 vehicles

• Leading automation and track & trace technology

Current footprint

Mercúrio depots

Franchisees

Araçatuba depots

2121

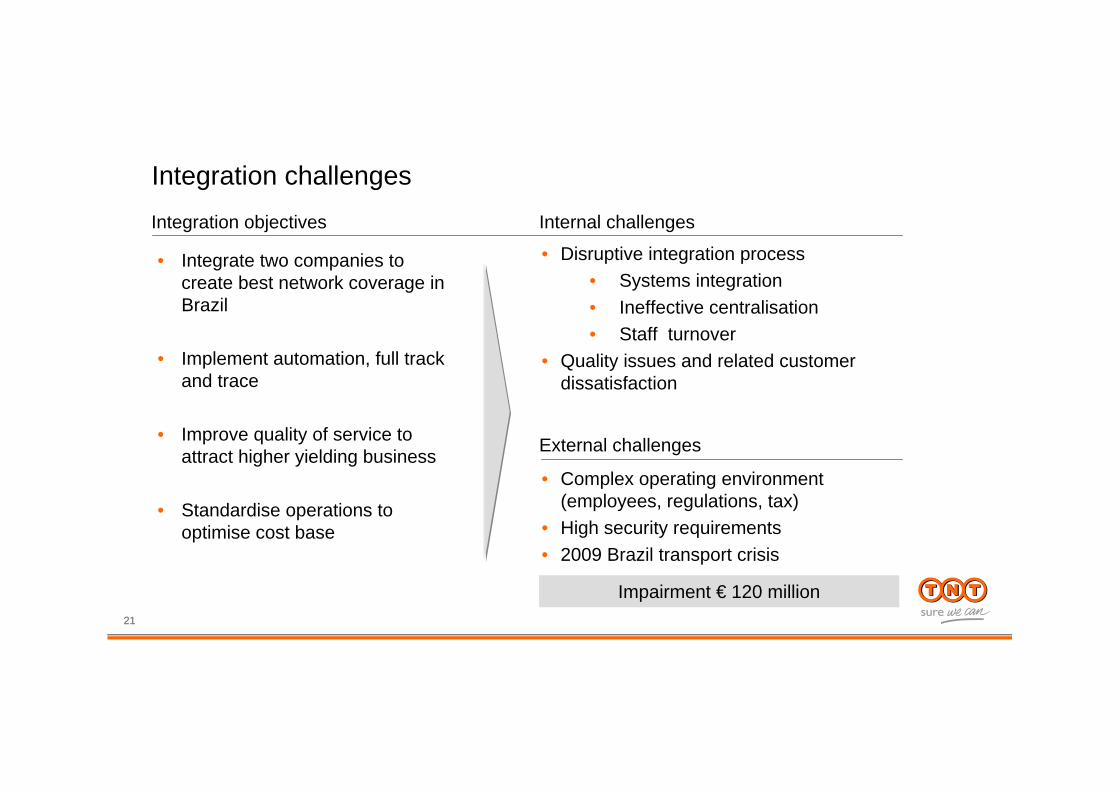

Integration challengesIntegration objectives

• Integrate two companies to create best network coverage in Brazil

• Implement automation, full track and trace

• Improve quality of service to attract higher yielding business

• Standardise operations to optimise cost base

Internal challenges

External challenges

• Disruptive integration process• Systems integration• Ineffective centralisation• Staff turnover

• Quality issues and related customer dissatisfaction

• Complex operating environment (employees, regulations, tax)

• High security requirements• 2009 Brazil transport crisis

Impairment € 120 million

2222

Turnaround Brazil – target breakeven 2H 2012

Organisation Deliverable

• New, experienced leadership team in place since March, with local know-how

• New organisation structure around regional and depot management implemented

• Controls and systems adjusted to local controls• Cut indirect costs

• Service quality improvement

• Control

Commercial

• Stabilisation of top 25 customers• Sales drive focused on TNT major / global

accounts and local key customers

• Additional compatible volumes to fuel existing network

Operations

• Service quality target of >90% on-time for all customers

• Focus on absorbing volume loss

• Price increase opportunity

• Fewer claims

Full turn-aroundplan beingdeveloped

• Continuous monitoring

2323

TNT’s global footprint

Americas

Aspac

EMEA

Other

Australia & Pacific

Rest of Asia

India

Greater China

South & Middle America

Brazil

USA and Canada

Revenue contribution by segment and by country

Africa & ME Rest of Europe

Belgium

France

GermanyItaly

UK

NL

2424

Solid positioning Asia-PacificRevenue contribution 2010

Rest of AsiaAustralia & Pacific

Greater China

India

Total revenue € 1.6 billion (2010)China• International connection Europe• Differentiating domestic footprint

Australia• Leverage solid domestic position• Grow International share

India• International focus Europe and Asia• Domestic footprint (road and air)

Rest of Asia• Growth based on existing regional

and international connectivity

TNT ExpressCapital Markets Day

Jan Willem Breen3 May 2011

26

Marketing & Sales organisation

Globalaccounts

Majoraccounts

SME

Customer segments Sales channels

• Corporate and Global account management teams

• National account management teams

• Territory sales teams• Self-service e-sales

Central organisation

Ensure balanced growth

Indicative # of customers

40%

30%

30%

Revenues

• Marketing• Sales processes

and collaterals• Pricing• Product

management• Reporting

27 +

Commercial initiatives to improve yield and margins

Margins

+

Express Economy DomesticSolutions

Controlled growth especially in Domestic

Limited volume growth but focus on higher margin industry specific value added solutions

Express parcel growth to improve both product and customer mix

Globalaccounts

Majoraccounts

SME

28

Innovation in value added solutions

Lifestyle & Other

Healthcare

High tech

Automotive &Industrial

After-market /service logistics

• Last mile delivery

• Critical parts/FSL

• Innight delivery

• Replenishment

• Temperature controlled end-to-end shipping

• Hospital deliveries

Sector split of top 500 accountsEuropean revenues

• High-end B2C

• Multi-modal and direct solutions inbound Europe

29

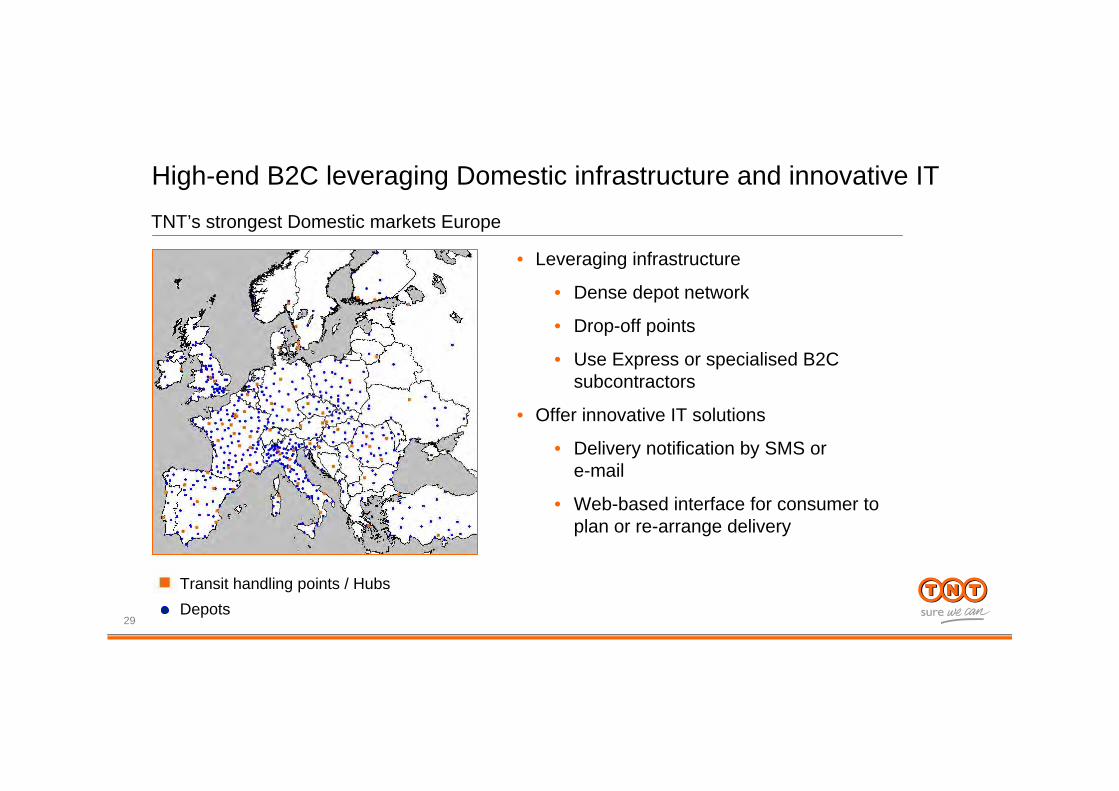

High-end B2C leveraging Domestic infrastructure and innovative IT

• Leveraging infrastructure

• Dense depot network

• Drop-off points

• Use Express or specialised B2C subcontractors

• Offer innovative IT solutions

• Delivery notification by SMS or e-mail

• Web-based interface for consumer to plan or re-arrange delivery

TNT’s strongest Domestic markets Europe

Transit handling points / HubsDepots

30

Leveraging our SME sales machine…

FieldSales

IndoorSales

888 940

25

Visits Calls

150

1.0

CallsVisits

6.2

44 weeks/year

ActivityMillion per year

European salesforceFTE

Actual activity levels# per week

x

x

Existing customers

1/3

Prospects

2/3

Target group

95% of TNT’s individual customers and > 40% of revenue

31

… to sell Express parcels to SMEs

• International express commission > 2x domestic

• Internal sales teamcompetition

• ‘Automatic’ Monthly Volume Discount

• Parcel acquisition tariff

• Campaign management system

• Automated activity scheduling

• Electronic salespresenter

• Express Import• 12:00 Express• Intercontinental

Sales incentives Sales systems

Pricing Direct marketing campaigns

Example – Express parcel booster programmeTarget annualised revenues

20,000 to 25,000 new traders

15 to 20 consignments per trader

More than € 100 average price per consignment

Significant annualised revenues (at very high margin)

x

x

=• Internal sales team competition

• Parcel acquisition tariff with introduction discount

Sales incentives

Pricing

32

TNT ExpressCapital Markets Day

Michael Drake3 May 2011

34

Number 1 Asia – Europe with dedicated fleet

34

SIN

PVGCKG

LGG

HKG

TNT proposition

• Reliable and consistent service – owned air assets

• End to end solution including customs clearance

• Complementary Europe air / road capabilities

• Global account management

• Migration of manufacturing to West (Chongqing)

3535

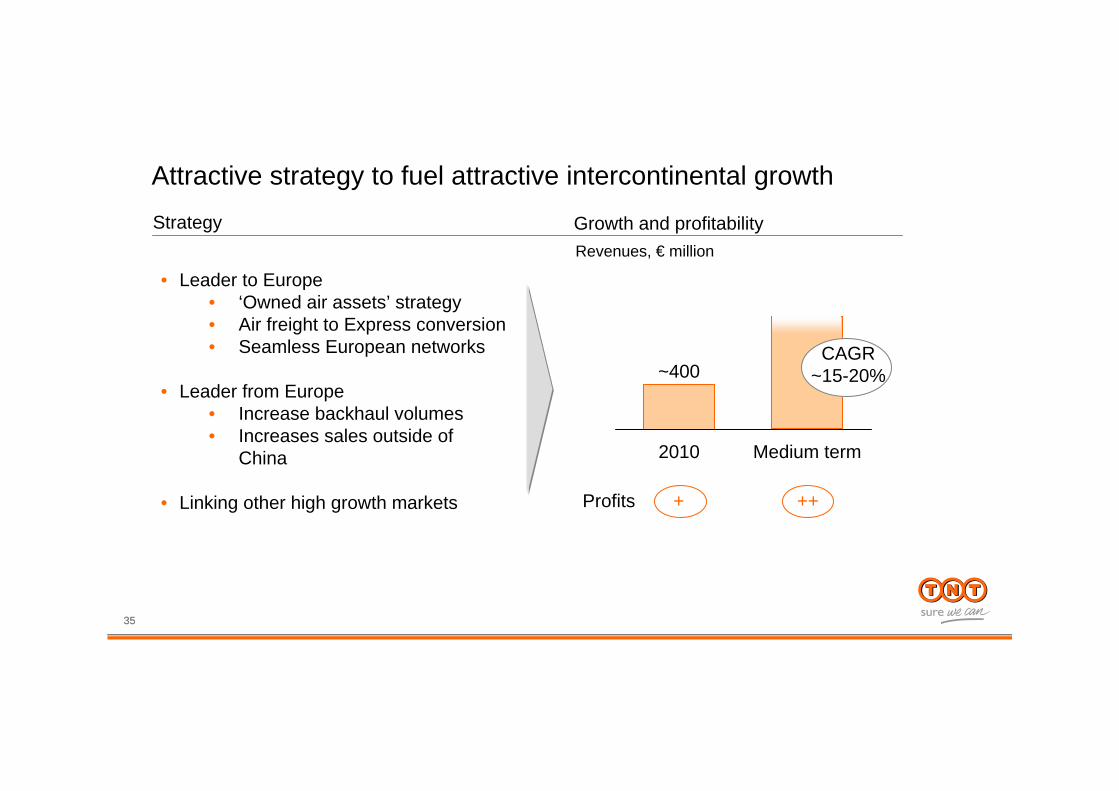

Attractive strategy to fuel attractive intercontinental growthStrategy Growth and profitability

Medium term2010

~400

• Leader to Europe• ‘Owned air assets’ strategy• Air freight to Express conversion• Seamless European networks

• Leader from Europe• Increase backhaul volumes• Increases sales outside of

China

• Linking other high growth markets

Revenues, € million

Profits + ++

CAGR ~15-20%

36

Optimise profit and cash flow

36

Emerging markets: domestic strategy

Acquire Transform Establish and grow high-end

services

Pro

fitab

ility

0

2008 - 2010

>2010

>2013

• Invest in linehaul, PUD and depot infrastructure

• Reduce share heavy day-uncertain freight

• Launch Day Definite Service

• Expand network• Introduce tracking

• Continue service innovation

• Optimise yield, capacity management and operations

Acquisition Hoau

2007

3737

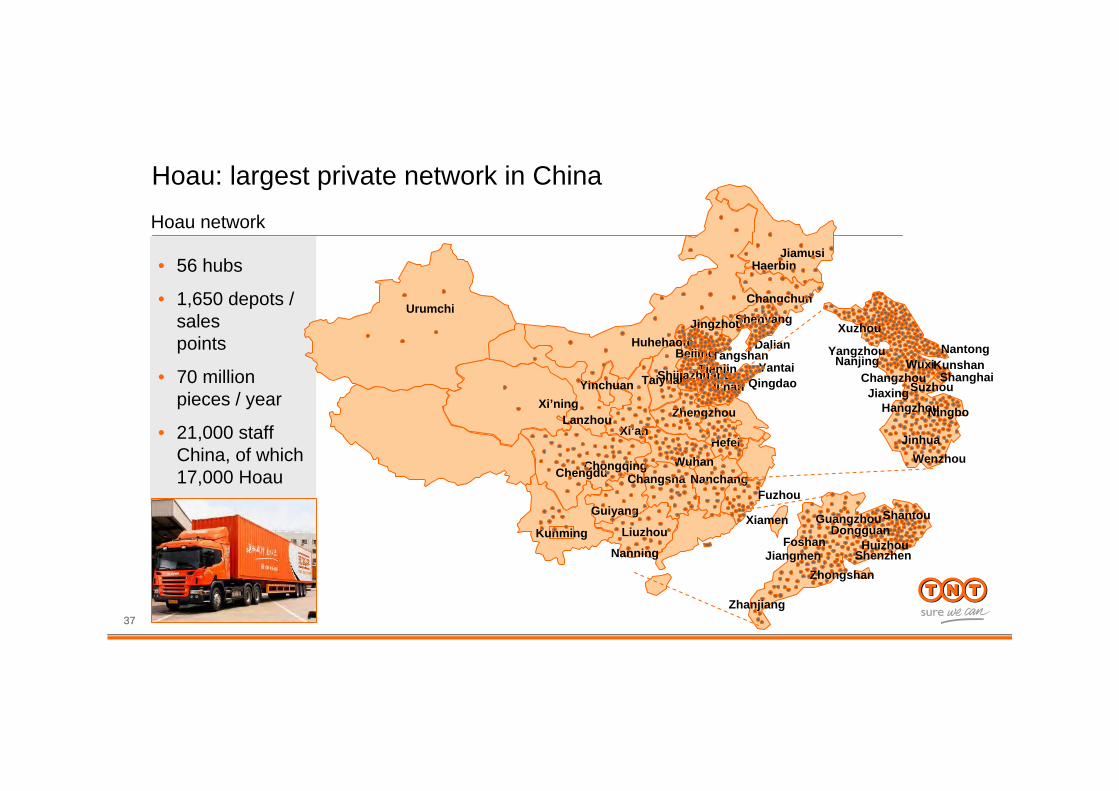

• 56 hubs

• 1,650 depots / sales points

• 70 million pieces / year

• 21,000 staff China, of which 17,000 Hoau

Nanning

Guiyang

Kunming

Hefei

LanzhouXi’ning

Xi’an

ChongqingChengdu

Yinchuan

Urumchi

NanchangWuhan

Changsha

BeijingTangshanHuhehaote

ShenyangJingzhou

Changchun

JiamusiHaerbin

Zhengzhou

Ji’nanShijiazhuangTaiyuan

Liuzhou

QingdaoYantai

Fuzhou

Xiamen

Dalian

TianjinShanghai

KunshanNantong

SuzhouChangzhou

Yangzhou

Xuzhou

HangzhouNingbo

WenzhouJinhua

Jiaxing

GuangzhouShantou

HuizhouDongguan

Foshan

ZhongshanJiangmen

Zhanjiang

WuxiNanjing

Shenzhen

Hoau: largest private network in ChinaHoau network

3838

• Dedicated service hot line• Arrival notice by SMS• Full track and trace

Superior customer proposition with Day Definite Product

Committed Time

Guaranteed Safety

Superior Service

Weight limitation

Customer feedback

High reputation

Convenience

Strong network

Good service

Punctuality

Price

Speed

Security

Purchase criteria

• On time departure & transit• On-time delivery (via GPS)• Transit tracing

• Cage & seal operation• Bar coding and GPS• Insurance

3939

Day-definite ‘sweet spot’

Price

Speed and Service Quality

FTL / LTL

Air Freight

Rail Day Definite

Freight

Road Day Definite

Freight

• Day-definite market in the making with Hoauand a few others defining offering

• Attractive alternative to rail / air freight with consistent service at competitive price

4040

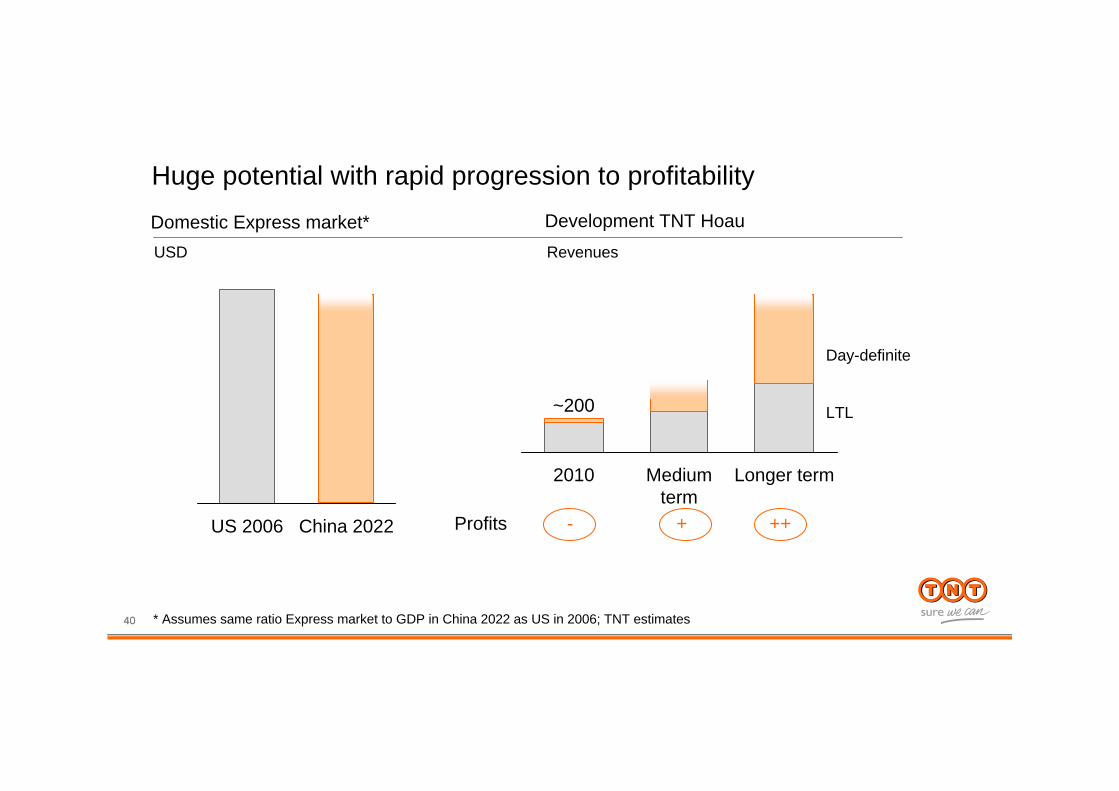

Huge potential with rapid progression to profitability

China 2022US 2006

Domestic Express market*USD

Longer termMedium term

2010

~200

Development TNT HoauRevenues

* Assumes same ratio Express market to GDP in China 2022 as US in 2006; TNT estimates

Profits - + ++

Day-definite

LTL

TNT ExpressDelivering our customers’ success

Bernard Bot3 May 2011

Agenda

Q1 recap

Finance priorities

Q1 2011

Q1 2011 Q1 2010 % change

Revenues 1,796 1,685 6.6%

EBITDA 96 110 -12.7%

Operating income (79) 59

EMEA • Resilient European performance: cost control offsetting negative impacts• Tariff measures and sales initiatives to improve product and customer mix

ASPAC• Lower China-Europe air volumes at start of the year, recovered since week 10• Negative impact one-offs• Restructuring costs regional head office

Americas

• Unexpected and recent volume losses and performance pressure in Brazil• Impairment € 120 million• New experienced leadership team in place• Deadline for realising turnaround no later than by 2H 2012

Other• Restructuring of indirect and non-core activities targeted savings of

€ 40 - 50 million• Expected related charges and write-offs of € 45 - 65 million

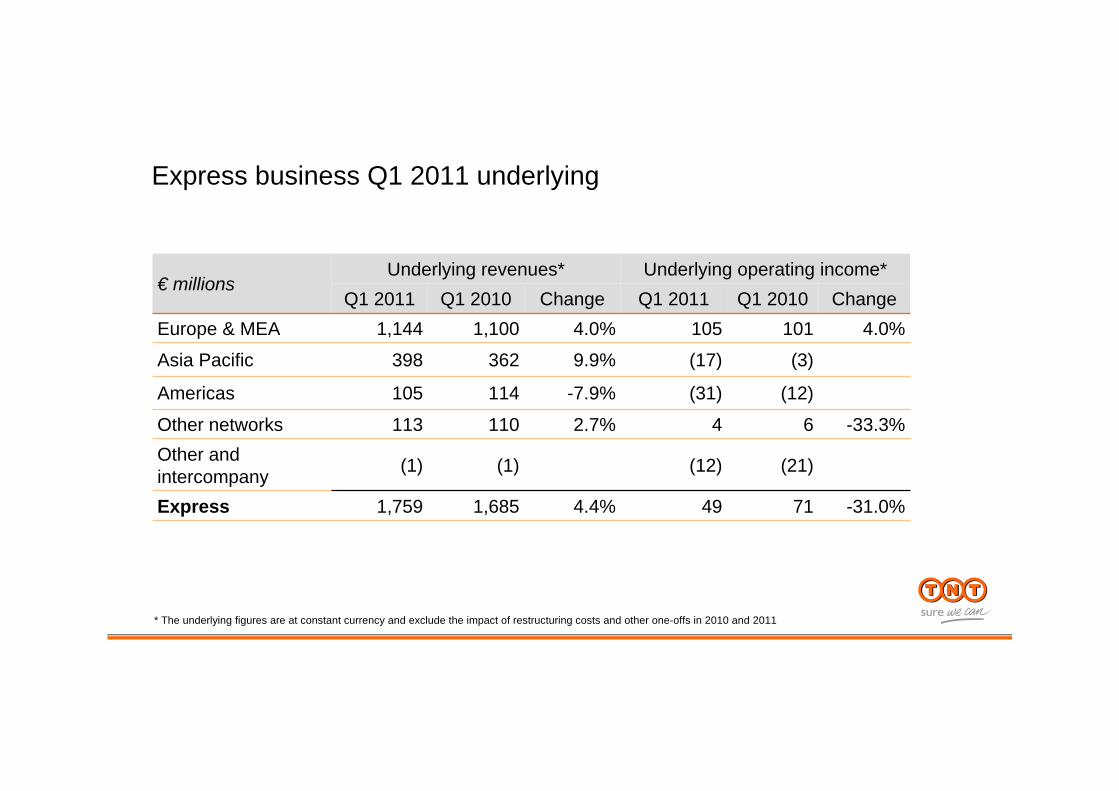

Express business Q1 2011 underlying

€ millionsUnderlying revenues* Underlying operating income*

Q1 2011 Q1 2010 Change Q1 2011 Q1 2010 ChangeEurope & MEA 1,144 1,100 4.0% 105 101 4.0%

Asia Pacific 398 362 9.9% (17) (3)

Americas 105 114 -7.9% (31) (12)

Other networks 113 110 2.7% 4 6 -33.3%Other and intercompany (1) (1) (12) (21)

Express 1,759 1,685 4.4% 49 71 -31.0%

* The underlying figures are at constant currency and exclude the impact of restructuring costs and other one-offs in 2010 and 2011

Impact restructuring initiatives

• Target € 40-50 million annualised savings

• Implementation 2H 2011• Full impact of savings in 2012• Total charges expected of

€ 45 – 65 million, around one-third non-cash

• Indirect and non-core activities

• All functions• Central, regional and

operating units • Third-party and staff

Indirect andnon-core

• Impairment € 120 million included in Q1 results

• Additional losses, restructuring charges and provisions expected in 2011

• Quick fixes and milestones• Deadline turnaround by no

later than 2H 2012Brazil

Agenda

Q1 recap

Finance priorities

Key finance priorities defined

• Maintain BBB+ / Baa1 credit rating• Sufficient financial headroom

Solid balance sheet and financing structure

• Stringent investment and working capital management

• Cash flow managementAsset efficiency

• Balanced mix of high return high growth activities• Tax optimisation

Revenue and margin growth + tax efficiency

2011 and medium term: continued growth, higher returns

In line with prior year

Negative, to be addressed through corrective measures

Partially recover on the back of improving intercontinental volumes

9% or slightly above

Modest growth2011 Medium term aims

• Double digit revenues growth

• Solid contribution

1,656RevenuesAspac10-11%9.0%Margin

399Operating incomeOrganic growth + initiatives4,453RevenuesEMEA

2010

(7.8%)Margin(39)Operating income502RevenuesAmericas

0.8%Margin14Operating income

(55)Operating incomeSavings

(6)RevenuesUnallocated4.2%Margin

19Operating income448RevenuesOther Networks

Excluding one-offs, in € million

EMEA: further increase returns

2007 -2010 margins

9.0

12.8

Medium term

20102007

10.0-11.0~-4%+1-2%

Operating margin, percentage; approximate impact

-2%

-2%

-5%

+5%

Product mix

Customer mix

Base price

Cost reduction

Price

Cost

2010 – Medium term margins aims

Ongoing efficiencies and volume leverage

Base price increases and

surcharges

Product and customer mix

initiatives

Aspac and Americas: strong growth, secure profitability

FinancialB

usiness

Value drivers Example Brazil Example China

Growth Double-digit Double-digit

Competitiveedge Market leader

• Seamless international network• Domestic footprint• Day-definite

Customer support Local + global Local + global

Leadership Turnaround team Experienced local team

Historicperformance Requires turnaround

International profitableContinuous improvement

Future Break even by H2 2012 Domestic profits by 2013

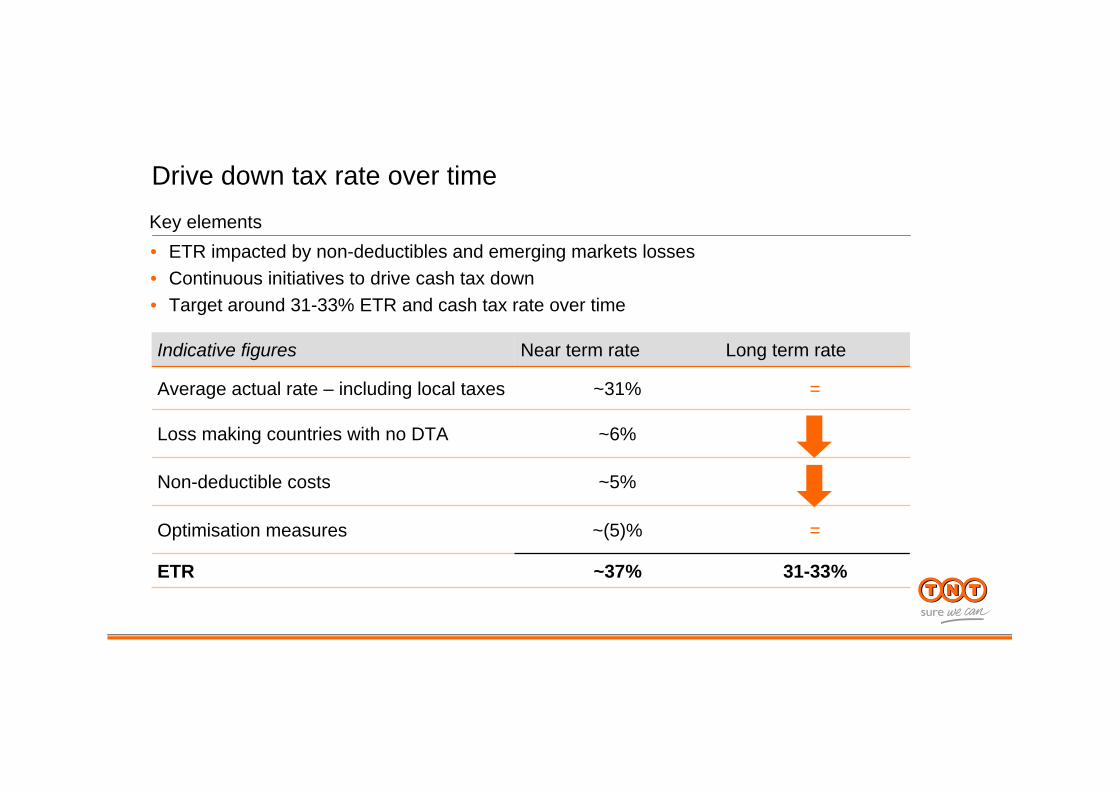

Indicative figures Near term rate Long term rate

Average actual rate – including local taxes ~31% =

Loss making countries with no DTA ~6%

Non-deductible costs ~5%

Optimisation measures ~(5)% =

ETR ~37% 31-33%

Drive down tax rate over timeKey elements• ETR impacted by non-deductibles and emerging markets losses• Continuous initiatives to drive cash tax down• Target around 31-33% ETR and cash tax rate over time

Focus on cash flow to continue

1514131211100908

Uses - Capex and acquisitionsSources356416771Cash from ops

(26)(44)(42)Net interest paid(76)(34)(152)Taxes paid

606425Δ profit pool / demerger(12)(28)84Δ taxes302374686Sources-31128172WC movements

333246514Sources ex. WC

143129243Net capex317712Acquisitions

174206255Uses

2008 2009 2010

Sources and uses of cash flow

Tight capex and working capital management

• Continue successful working capital initiatives, roll out globally• Remain restrictive on capex

<10%~10%Trade working capital

% of revenues Current Range medium-term

Capex* ~2.5% - 3.0%

~2.5% - 3.0% maintenance investments

1.0% - 2.0% points higher for extension investments in specific years

65% spent on EMEA, 25% Aspac

* Excluding operating leases

10090807060504

Capex / revenues

10090807060504

WC / revenues

Key elements

Solid capital structure

• Sufficient financial headroom maintained• Target net debt demerger accounts 31 December 2010 around zero• Availability of € 570 million currently undrawn committed facilities• Focus on free cash flow and cash concentration• S&P preliminary credit rating ‘BBB+ Stable’ after demerger• Moody’s provisional credit rating '(P) Baa1 Stable'

Indicative figures based on S&P methodology DebtTNT Express demerger target net debt ~0Lease adjustments 925Pension adjustments 50De-central cash adjustments 100Adjusted net debt ~1,075Expected net interest ~€25 - 35 million per year (finance leases, local loans and interest included in FX hedges)

Key elements

Dividend: manageable cash flow impact

• Target 40% of normalised net income• In line with UPS, Deutsche Post, K&N, Panalpina• Cover expectations global investors

• Payment in cash and/or in ordinary shares• Withholding tax benefit• Interim and first dividend

Key elements

TNT ExpressCapital Markets Day

Marie-Christine Lombard3 May 2011

5757

Three key reasons to invest

Unique position in attractive Express market

Leader in Europe and MEA with significant upside potential

Leverage positions in high-growth emerging markets

5858

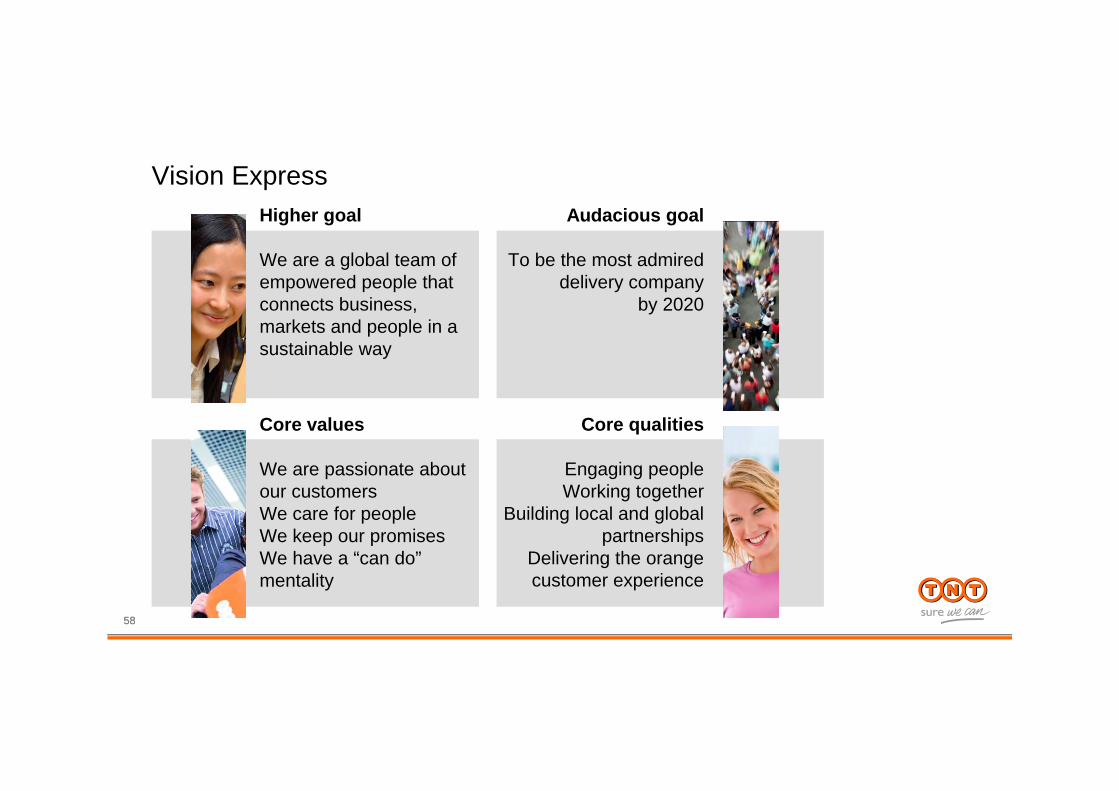

Vision ExpressAudacious goal

To be the most admired delivery company

by 2020

Higher goal

We are a global team of empowered people that connects business, markets and people in a sustainable way

Core values

We are passionate about our customersWe care for peopleWe keep our promisesWe have a “can do”mentality

Core qualities

Engaging peopleWorking together

Building local and global partnerships

Delivering the orange customer experience

59

Keeping our promises to customers

Eye for detail in operations

Engaging people

60

Focus on one business

Improve performance

Focus on shareholder value

TNT ExpressCapital Markets Day

Appendix ICurriculum VitaeExecutive BoardSupervisory Board

62

Marie-Christine Lombard

BIO

GR

AP

HY

Marie-Christine Lombard has been CEO and chairman of the Executive Board since 2 March 2011. Prior to that date, Ms Lombard was group managing director of Express and a member of the board of management of TNT N.V. since January 2004. She joined Jet Services in France in 1993. Upon TNT N.V.’s acquisition of Jet Services in 1999, Ms Lombard joined TNT as the managing director of the domestic Express business and from March 2001 until January 2004 she was managing director of TNT’s international Express business in France. Ms Lombard is an independent member of the Supervisory Board since January 2011 of Groupe BPCE, a French banking group. Ms Lombard is also president of the ‘‘Lyon Ville de l’Entrepreneuriat’’ Business Network Group. She served as a member of the supervisory board of Royal Wessanen N.V. until 22 April 2009 and as a member of the supervisory board of METRO AG until 31 December 2010.

63

Bernard BotBernard Bot has been CFO and member of the Executive Board since 2 March 2011. Prior to that date, Mr Bot was acting CFO of TNT N.V. from August 2010. Before joining TNT N.V. in 2005, he worked for 13 years at McKinsey & Company, where he was a partner serving clients in the post, logistics and transportation sectors. At TNT N.V., he was appointed Group Director Business Control directly reporting to the CFO. His responsibilities included internal control, mergers and acquisitions and business control. Bernard Bot is a member of the supervisory board of Avio-Diepen B.V.

BIO

GR

AP

HY

64

A. (Antony) BurgmansMr Burgmans held several positions with Unilever Plc/N.V. From 1999 until 2005 he was CEO and chairman of Unilever N.V. and from 2005 until 2007 he was chairman of Unilever N.V. and Unilever plc. His current responsibilities include: non-executive board member of BP plc, member of the supervisory boards of AkzoNobel, AEGON, SHV and Jumbo Supermarkten, chairman of the supervisory boards of WWF The Netherlands, theDutch National Opera (Amsterdam), and Intergamma B.V. and member Advisory Board CVC Capital Partners Nederland.

BIO

GR

AP

HY

65

L.W. (Tex) GunningMr Gunning held several positions with Unilever Plc/N.V., lastly as Business Group President Asia Foods. He was chief executive officer and chair of the management board of Vedior and is a member of AkzoNobel’s Executive Committee and responsible for its Decorative Paints business.

BIO

GR

AP

HY

66

M.E. (Mary) HarrisMs Harris was appointed as a member of the supervisory board of TNT N.V. on 20 April 2007. From 1994 to 2006, Ms Harris held a number of positions at McKinsey & Company in London, China, South-east Asia and Amsterdam. Previously, Ms Harris held positions at media venture capital firm Maxwell Entertainment Group, Pepsi Cola Beverages and Goldman Sachs & Co. Ms Harris is a non-executive director at J. Sainsbury plc, a member of the supervisory board of Unibail-Rodamco SE and a member of the advisory board of Irdeto B.V.

BIO

GR

AP

HY

67

R. (Roger) KingMr King was appointed as a member of the supervisory board of TNT N.V. on 20 April 2006. Mr King is non-executive director of Orient Overseas International Limited (Hong Kong) and Sincere Watch (Hong Kong) Limited. He is Honorary Consul for the Republic of Latvia in Hong Kong SAR, and serves on various business and community committees. Mr King is adjunct professor of finance and director of the Center for Asian Family Business and Entrepreneurship Studies at Hong Kong University of Science and Technology and director of the Center for Business Case Studies School of Business & Management. He is former president and chief executive officer of Sa Sa International Holdings Limited, former chairman and chief executive officer of ODS System-Pro Holdings Limited (Hong Kong), part of the CY Tung Group of Companies, and was managing director and chief operating officer of Orient Overseas International Limited and non-executive director of Arrow Electronics, Inc. (USA).

BIO

GR

AP

HY

68

S. (Shemaya) LevyMr Levy was appointed as a member of the supervisory board of TNT N.V. in 2005 and as the vicechairman of the supervisory board of TNT N.V. as of 1 January 2009. Mr Levy is a member of the supervisory boards of Safran, Segula Technologies Group and AEGON N.V. Formerly, Mr Levy was chief executive officer of Renault Industrial Vehicles Division and executive vice-president and chief financial officer of Renault Group as well as member of the supervisory boards of Nissan and Renault Spain.

BIO

GR

AP

HY

69

M. (Margot) ScheltemaMs Scheltema spent most of her career abroad with Royal Dutch Shell, in various management positions, always in finance. Since 2009 she manages a portfolio of executive and supervisory positions. She is also a research fellow at the Erasmus University of Rotterdam. Her current responsibilities include: vice-chairman supervisory board Triodos Bank, chairman audit committee, supervisory board ASR Verzekeringen, external member audit committee ABP, supervisory board Schiphol Group, supervisory board Energy Research Centre, Petten, supervisory board of Stichting Rijksmuseum, member of the committee on External Reporting of the AFM, member of the board of World Press Photo and chairman of the curatorium of the post-doctoral controllers education at the Vrije Universiteit, Amsterdam.

BIO

GR

AP

HY

TNT ExpressCapital Markets Day

Appendix II

Summary other indicators

Medium-term indication

ETR Target 31% - 33%

Capex*• 2.5 - 3.5% of revenues maintenance • 1.0 - 2.0% points higher for extension in specific years

Working capital Target <10% of revenues

Credit rating BBB+ / Baa1

Net interest payments ~€ 25-35 million per year (relating to financial leases, local debts and foreign currency hedges)

Dividend policy Target 40% of normalised net income

* Excluding operating leases

72

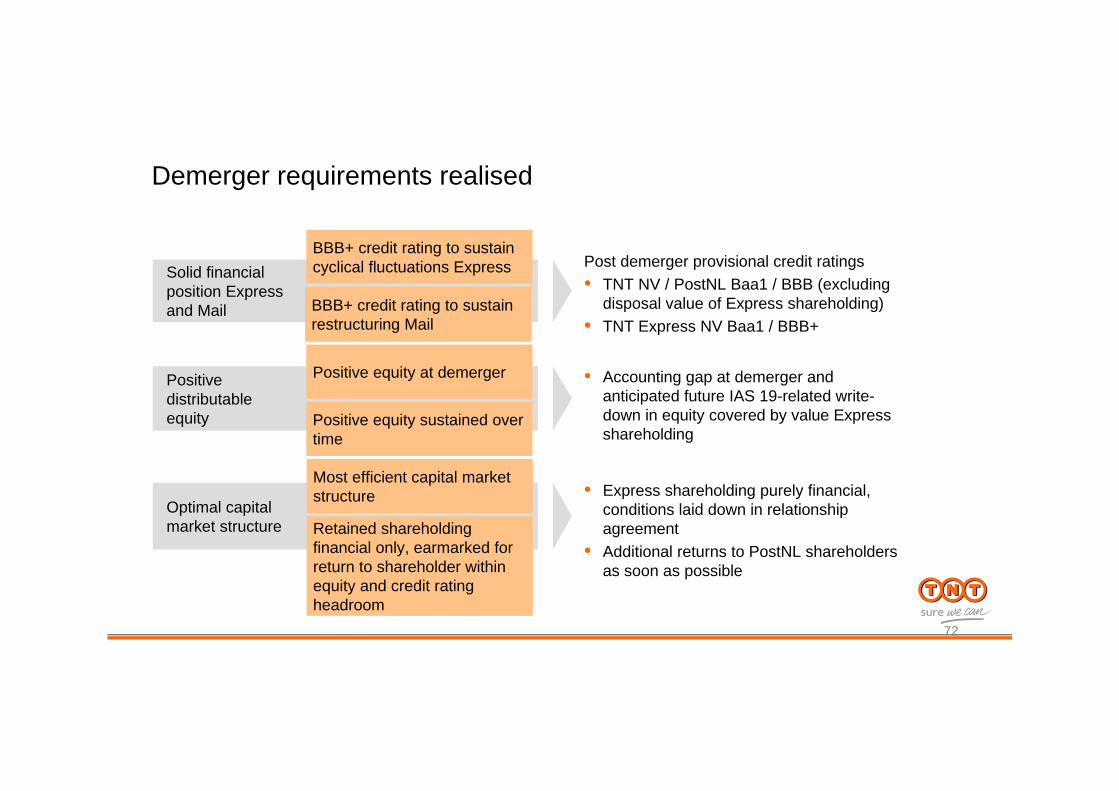

Demerger requirements realised

Optimal capital market structure

• Express shareholding purely financial, conditions laid down in relationship agreement

• Additional returns to PostNL shareholders as soon as possible

Positivedistributableequity

• Accounting gap at demerger and anticipated future IAS 19-related write-down in equity covered by value Express shareholding

Solid financial position Express and Mail

Most efficient capital market structure

Retained shareholding financial only, earmarked for return to shareholder within equity and credit rating headroom

Positive equity at demerger

Positive equity sustained over time

BBB+ credit rating to sustain cyclical fluctuations Express

BBB+ credit rating to sustain restructuring Mail

Post demerger provisional credit ratings• TNT NV / PostNL Baa1 / BBB (excluding

disposal value of Express shareholding)• TNT Express NV Baa1 / BBB+

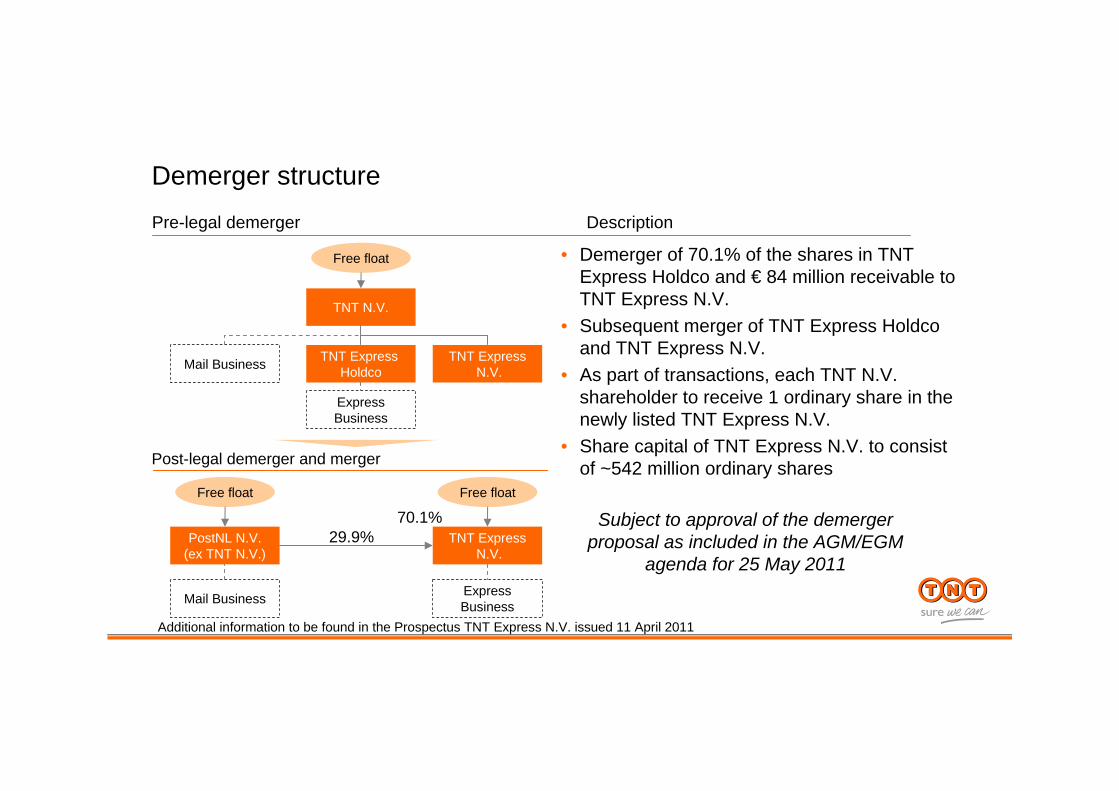

Demerger structurePre-legal demerger Description

• Demerger of 70.1% of the shares in TNT Express Holdco and € 84 million receivable to TNT Express N.V.

• Subsequent merger of TNT Express Holdco and TNT Express N.V.

• As part of transactions, each TNT N.V. shareholder to receive 1 ordinary share in the newly listed TNT Express N.V.

• Share capital of TNT Express N.V. to consist of ~542 million ordinary shares

Subject to approval of the demerger proposal as included in the AGM/EGM

agenda for 25 May 2011

TNT N.V.

TNT Express Holdco

ExpressBusiness

PostNL N.V.(ex TNT N.V.)

Mail Business TNT ExpressN.V.

Mail Business ExpressBusiness

TNT ExpressN.V.

Free float Free float

Free float

29.9%70.1%

Post-legal demerger and merger

Additional information to be found in the Prospectus TNT Express N.V. issued 11 April 2011

Relationship agreement and related party transactions

• Six months lock up from date of demerger• Maximum offering of 15% of the shares of TNT Express to one party

or group of related parties• In case of public offer, obliged to tender if supported by TNT Express

or if 50% of the ordinary shares tendered*• PostNL to abstain from voting on specified decisions entailing

significant change in identity, demerger or merger

Other

Relationshipagreement

• Separate execution agreements with the Dutch pension funds• Subsidiary cross-guarantees regarding accrued pension benefits

up to date of demerger in case of default / bankruptcy• Transitional agreement for period 1-36 months for use of TNT

brand by Mail• Limited set of other agreements related to separation

* If Mail’s stake is between 29.9% and 25% if 66.67% of the other shares are tenderedAdditional information to be found in the Prospectus TNT Express N.V. issued 11 April 2011

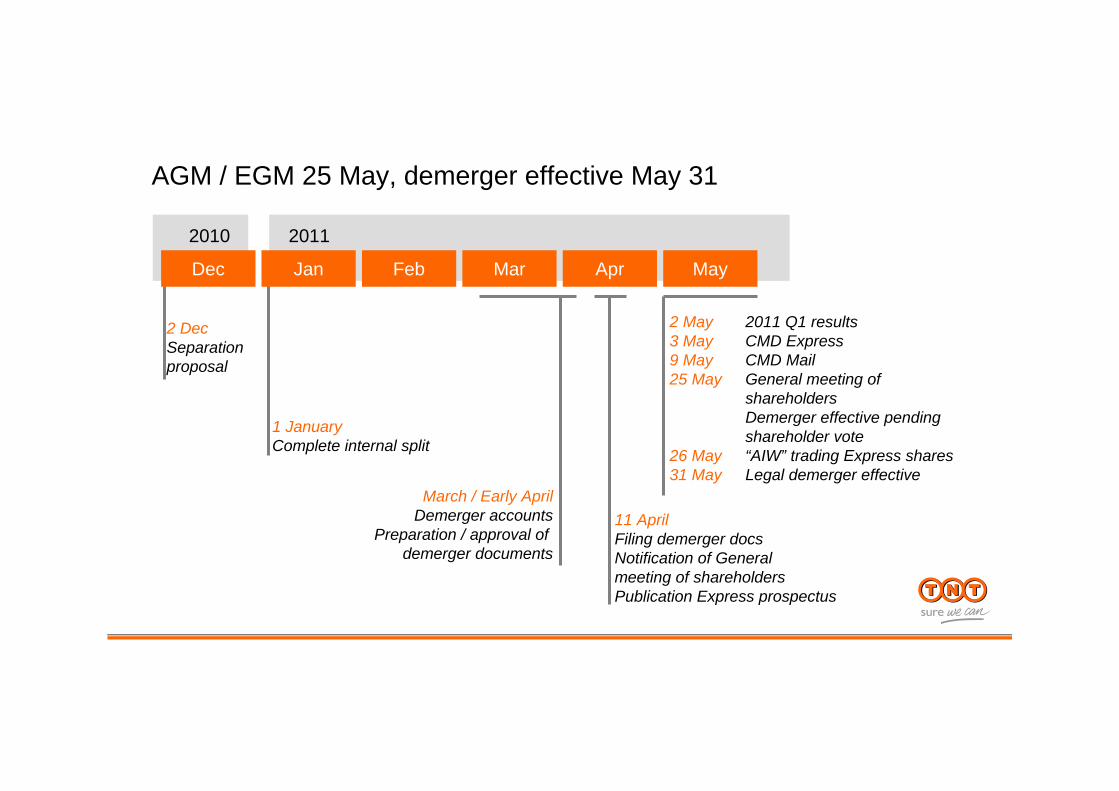

AGM / EGM 25 May, demerger effective May 31

11 AprilFiling demerger docsNotification of General meeting of shareholdersPublication Express prospectus

2 DecSeparation proposal

1 JanuaryComplete internal split

March / Early AprilDemerger accounts

Preparation / approval of demerger documents

Dec Jan Feb Mar Apr May

2011

2 May 2011 Q1 results3 May CMD Express9 May CMD Mail25 May General meeting of

shareholdersDemerger effective pending shareholder vote

26 May “AIW” trading Express shares31 May Legal demerger effective

2010

Trading of TNT Express N.V. shares

• First trading Express shares and ‘ex-spin off’ TNT N.V./PostNL N.V. shares expected on 26 May 2011

• Express to trade under symbol ‘TNTE’, Mail under ‘PNL’

• Settlement of trades on First Trading date and first date of irrevocable trading on 31 May 2011

Timetable Description

May 31First day of irrevocable trading

Approval demerger proposal May 25

Expected first trading TNT Express NV on ‘as-if-and-when issued’ basis

May 26

PostNL N.V. ‘ex-spin off’ May 26

Record date May 30

Execution demerger structure effective May 31

Allotment, delivery and settlement May 31