the strategic implications of scale in choice-based

TRANSCRIPT

This article was downloaded by: [74.104.133.83] On: 11 December 2019, At: 07:29Publisher: Institute for Operations Research and the Management Sciences (INFORMS)INFORMS is located in Maryland, USA

Marketing Science

Publication details, including instructions for authors and subscription information:http://pubsonline.informs.org

The Strategic Implications of Scale in Choice-BasedConjoint AnalysisJohn R. Hauser, Felix Eggers, Matthew Selove

To cite this article:John R. Hauser, Felix Eggers, Matthew Selove (2019) The Strategic Implications of Scale in Choice-Based Conjoint Analysis.Marketing Science 38(6):1059-1081. https://doi.org/10.1287/mksc.2019.1178

Full terms and conditions of use: https://pubsonline.informs.org/Publications/Librarians-Portal/PubsOnLine-Terms-and-Conditions

This article may be used only for the purposes of research, teaching, and/or private study. Commercial useor systematic downloading (by robots or other automatic processes) is prohibited without explicit Publisherapproval, unless otherwise noted. For more information, contact [email protected].

The Publisher does not warrant or guarantee the article’s accuracy, completeness, merchantability, fitnessfor a particular purpose, or non-infringement. Descriptions of, or references to, products or publications, orinclusion of an advertisement in this article, neither constitutes nor implies a guarantee, endorsement, orsupport of claims made of that product, publication, or service.

Copyright © 2019, The Author(s)

Please scroll down for article—it is on subsequent pages

With 12,500 members from nearly 90 countries, INFORMS is the largest international association of operations research (O.R.)and analytics professionals and students. INFORMS provides unique networking and learning opportunities for individualprofessionals, and organizations of all types and sizes, to better understand and use O.R. and analytics tools and methods totransform strategic visions and achieve better outcomes.For more information on INFORMS, its publications, membership, or meetings visit http://www.informs.org

MARKETING SCIENCEVol. 38, No. 6, November–December 2019, pp. 1059–1081

http://pubsonline.informs.org/journal/mksc ISSN 0732-2399 (print), ISSN 1526-548X (online)

The Strategic Implications of Scale in Choice-BasedConjoint AnalysisJohn R. Hauser,a Felix Eggers,b Matthew Selovec

a Sloan School of Management, Massachusetts Institute of Technology, Cambridge, Massachusetts 02142; b Faculty of Economics andBusiness, University of Groningen, 9747 AE Groningen, Netherlands; cThe George L. Argyros School of Business and Economics,Chapman University, Orange, California 92866Contact: [email protected], http://orcid.org/0000-0001-8510-8640 (JRH); [email protected], https://orcid.org/0000-0001-9753-1227 (FE);[email protected], http://orcid.org/0000-0001-6706-0049 (MS)

Received: October 3, 2017Revised: June 19, 2018; November 9, 2018;March 8, 2019; April 26, 2019Accepted: May 5, 2019Published Online in Articles in Advance:November 14, 2019

https://doi.org/10.1287/mksc.2019.1178

Copyright: © 2019 The Author(s)

Abstract. Choice-based conjoint (CBC) studies have begun to rely on simulators to forecastequilibrium prices for pricing, strategic product positioning, and patent/copyright val-uations. Whereas CBC research has long focused on the accuracy of estimated relativepartworths of attribute levels, predicted equilibrium prices and strategic positioningare surprisingly and dramatically dependent on scale: the magnitude of the partworths(including the price coefficient) relative to the magnitude of the error term. Althoughthe impact of scale on the ability to estimate heterogeneous partworths is well known,neither the literature nor current practice address the sensitivity of pricing and posi-tioning to scale. This sensitivity is important because (estimated) scale depends on seeminglyinnocuous market-research decisions such as whether attributes are described by text or byrealistic images. We demonstrate the strategic implications of scale using a stylized model inwhich heterogeneity is modeled explicitly. If a firm shirks on the quality of a CBC study andacts on incorrectly observed scale, a follower, but not an innovator, can make costlystrategic errors. Externally valid estimates of scale are extremely important. We dem-onstrate empirically that image realism and incentive alignment affect scale sufficientlyto change strategic decisions and affect patent/copyright valuations by hundreds ofmillions of dollars.

History: Yuxin Chen served as the senior editor and Carl Mela served as associate editor for this article.Open Access Statement: This work is licensed under a Creative Commons Attribution 4.0 International

License. You are free to copy, distribute, transmit and adapt this work, but youmust attribute this workas “Marketing Science. Copyright © 2019 The Author(s). https://doi.org/10.1287/mksc.2019.1178, usedunder a Creative Commons Attribution License: https://creativecommons.org/licenses/by/4.0/.”

Supplemental Material: Data files and the online appendices are available at https://doi.org/10.1287/mksc.2019.1178.

Keywords: conjoint analysis • market research • choice models • scale

1. Scale Affects Strategic DecisionsWith an estimated 18,000 applications per year, conjointanalysis is one of the most-used quantitative marketresearch methods (Orme 2014, Sawtooth Software2015). Over 80% of these conjoint applications arechoice based (Sawtooth Software 2016). Firms rou-tinely use choice-based conjoint (CBC) analysis toidentify preferred product attributes in the hopes ofmaximizing profit—for example, General Motors alonespends tens of millions of dollars each year (Urbanand Hauser 2004). CBC analysis is increasingly usedin litigation, and courts have awarded billion-dollarjudgments for patent or copyright infringement basedon CBC studies (Mintz 2012, Cameron et al. 2013,McFadden 2014).

Research in CBC analysis has long focused onthe ability to estimate accurate relative trade-offsamong product attribute levels. Improved question

selection, improved estimation, and techniques suchas incentive alignment all enhance accuracy of iden-tified relative trade-offs and lead to better managerialdecisions. However, with the advancement of CBCsimulators and faster computers, researchers havebegun to use CBC studies to estimate price equilibriaand the resulting equilibrium profits (e.g., Allenbyet al. 2014). This use of CBC analysis raises a newconcern because, as shown in this paper, the calculatedprice equilibria depend critically on “scale,” wherescale is the magnitude of the partworths (includingthe price partworths) relative to the magnitude of theerror.1 Whereas the literature has long focused onthe impact of scale heterogeneity in CBC estimation,our focus is on a common scale factor in CBC studies.For example, we demonstrate that scale can be quitedifferent if we use realistic images rather than text-only stimuli or if we use incentive alignment rather

1059

than no incentive alignment. (The goal of realism isto represent better choices made by consumers in themarketplace.)

Our research combines formal modeling to un-derstand the phenomena and empirical CBC studiesthat vary on the realism of the stimuli and on incentivealignment. The empirical studies include a delayed vali-dation task that mimics consumers’ marketplace de-cisions as a proxy to estimate “true” scale. Together, thetheory and practice provide complementary insights:

Theory• Scale affects strategic decisions, such as how to

position and set price, even when we account forunobserved attributes and preference heterogeneity(a stylized version of commonhierarchical Bayes [HB],latent structure, or machine-learning estimation).

• Equilibria prices are extremely sensitive to truescale; that is, the scale that best describes marketplacedecisions.

• For high relative values of true scale, the profit-maximizing strategy is to differentiate. For low relativevalues of true scale, the profit-maximizing strategy isnot to differentiate.

• If a follower shirks onmarket research and gets abiased estimate of scale, the follower could make thewrong strategic decisions (price and positioning) andforego substantial profits.

• The innovator’s strategic decisions do not dependon estimated scale.

Practice• When the stylized assumptions are relaxed in

empirical studies, the identified phenomena and stra-tegic recommendations remain valid.

• Seemingly innocuous aspects of a CBC study canhave huge effects on predicted equilibrium prices. Wetest incentive alignment and image realism.

• Aspects of a CBC study can affect strategic po-sitioning, that is, which attribute level maximizesequilibrium profits.

• If estimated scale is adjusted based on a mar-ketplace validation task, then both pricing and po-sitioning decisions are affected. A firm may positiondifferently and choose a different price dependingon whether the firm acts on unadjusted scale orvalidation-adjusted scale.

• Data-based hypotheses for further research areas follows: (1) Image realism is very important.(2) Image realism may be more important than incen-tive alignment. (3) Validation-adjusted scale impliespredicted price equilibria that differ dramaticallyfrom price equilibria based on scale estimated fromthe CBC profile choices.

The practical implications are important. Althougha few CBC studies (academic literature and practice)

use highly realistic images and incentive alignment,most do not. Although a very few CBC studies adjustestimates with validation tasks, the vast majority donot. Because our theory and data suggest that such“craft” matters substantially, we also recommendpractical decision processes by which firms can de-cide whether to invest in these elements of CBC craft.We expect that CBC craft can impact managerial

decisions—this is intuitive. But neither the magni-tude and direction of the strategic errors nor the largeeffect of seemingly minor differences in CBC craftare obvious without the insights from the stylizedmodel. (At minimum, many aspects of craft are un-derappreciated in the academic literature and the vastmajority of CBC applications.)

2. Typical Practice in CBC Studies andRecent Changes in Practice

2.1. Typical Current PracticeIn CBC analysis, products (or services) are summa-rized by a set of levels of the attributes. For example, asmartwatchmight have awatch face (attribute) that iseither round or rectangular (levels), be silver or goldcolored, and have a black or brown leather band. Byvarying the smartwatch attribute levels systemati-cally within an experimental design, CBC analysisestimates preferences for attribute levels (and price),called “partworths,” which describe the differentialvalue of the attribute levels. For example, one part-worth might represent the differential value of a rect-angular watch face relative to a round watch face.Applied practice focuses on estimating accurately

the relative partworths. For example, if rectangularand round watch faces are equally costly but thepartworth of a rectangular watch face is greater thanthe partworth of a round watch face for most con-sumers, then a typical recommendation would beto launch a product with a rectangular watch face.The relative partworths can also be used to calculatewillingness to pay (WTP) by comparing differencesin partworths to the estimated price coefficient. Forexample, if a consumer’s differential value between arectangular and a round watch face is higher thanthe consumer’s valuation of a $100 reduction in thepurchase price,firms typically infer that the consumeris willing to pay more than $100 for a rectangularrather than a round watch face. (There are subtletiesin this calculation because of the Bayesian nature ofmost estimates, but this is the basic concept.)These calculations depend only on the (posterior

distribution of) relative partworths. Because attribute-level partworths and the price coefficient are definedrelative to one another, if we multiply all partworths andthe price coefficient by a constant, the comparative valueandWTPcalculations remainunchanged.However, the

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1060 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

literature has established that estimated partworthsalso depend on scale heterogeneity. In particular, ifscale varies among consumers, then the accuracy withwhich the relative partworths can be estimated dependson accounting for heterogeneity in scale during esti-mation (e.g., Beck et al. 1993, Swait and Louviere 1993,Fiebig et al. 2010, Salisbury and Feinberg 2010,Pancreas et al. 2016). Scale heterogeneity affects part-worth estimation and/or aggregation of respondents’WTP, but, once researchers account for heterogene-ity, WTP does not depend on a common (across re-spondents) increase or decrease in scale (e.g., Ofek andSrinivasan 2002, equation 15). The phenomenon weinvestigate is different from scale heterogeneity; wefocus on the strategic implications of a common scalefactor in a stylized model assuming accurate relativepartworths and assuming the estimation accounts forscale heterogeneity. (The assumptions of accurate rela-tive partworths is relaxed in the empirical analyses.)

The literature recognizes that estimated partworthsmay need to be adjusted to better represent market-place choices. One approach is to adjust scale andrelative partworths to match market shares and use theadjusted scale and partworths in simulations (e.g.,Gilbride et al. 2008). The adjustments are motivatedby predictive ability rather than strategic implica-tions. A second approach adjusts scale directly or in aprocedure known as randomized first choice (RFC),in which an additive error is included in the simu-lations (Huber et al. 1999). RFC automatically de-termines the random perturbations to yield “ap-proximately the same scale factor as the [logit]model”(Sawtooth Software 2019). Scale adjustments are easyto implement, but usage is rare—users almost alwaysstick with the scale observed in the CBC estimation(Orme 2017). Many users report that marketplacedata, as a benchmark to adjust scale and relativepartworths, are often not available, for example, forinnovations, or not relevant to the simulated markets.Our stylized model and empirical illustrations suggestthat validation adjustments are critical and should beused more often. We also provide an alternative ad-justment that does not require marketplace data.

2.2. Current Practice is Changing: The Implicationsof Price Equilibria

WTP provides valuable diagnostic information forpricing and attribute-level decisions and has beenused to motivate and interpret valuations in patent/copyright cases (e.g., Mintz 2012, Cameron et al. 2013,McFadden 2014), but WTP does not account forcompetitive response. WTP does not indicate howmarketplace prices will respond to new products orchanges in a product’s attributes (Orme 2014, pp. 90–91;Orme and Chrzan 2017, p. 194). Because of the in-fluence of game theory in marketing science, CBC

simulators are beginning to consider competitive re-sponse. For example, if an innovator introduces asilver-colored watch face and a follower respondswith a gold-colored watch face (and all other attri-butes are held constant), then CBC simulations can beused to calculate the Nash price equilibrium. Allenbyet al. (2014) propose that these methods be used tovalue patents and copyrights. Courts recognizedthe issue as early as 2005 for class-action cases (e.g.,Whyte 2005; albeit not CBC) and since at least 2012 inpatent cases (Koh 2012). Although not proposed pre-viously, simulators can use equilibrium prices to calcu-latethefollower’smost-profitable strategic-positioningresponse (silver versus gold) to the innovator’s newproduct (silver or gold).We show that scale (and validation-based scale

adjustment) plays a central role when predicting priceequilibria and predicting optimal competitive reac-tions. We illustrate the magnitude of the managerialimplications. (Sawtooth Software estimates that 80%of managerial CBC applications consider competi-tion in market simulations, although the explicitcalculation of equilibrium prices is relatively new(Orme 2017).)

3. Empirical Illustration to Motivate thePhenomena We Seek to Study

Before we derive the stylized model and before we de-scribe fully the empirical tests, it is useful to illustrate thephenomena we seek to study.

3.1. Scale Affects the Price Equilibria ThatAre Calculated

As an illustration, we plot the predicted equilibriumprice of an innovator as a function of the true scale(γtrue). Figure 1 illustrates how the predicted priceequilibrium might change if estimated scale dependson the craft of a CBC study. We use the distribution ofrelative partworths obtained in our empirical study

Figure 1. Predicted Equilibrium Price Depends on Scale

Notes. Data are from our empirical study of smartwatches. Error barsare posterior standard deviations.

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1061

about smartwatches (HB CBC details in Section 8.5)and calculate the (counterfactual) price equilibria foreach level of scale (methods described in Section 8.8).The equilibria are based on a market with two firmswhose products differ on the watch color (silverversus gold). We chose the range of the scales to betypical of those reported in the literature and in ourempirical studies. (Over the range in Figure 1, equi-librium prices are monotonically deceasing in scale,but there is no guarantee that they do not increaseslightly as γtrue →∞. Indeed, they do so in the illustra-tive example in Online Appendix 1.) We obtain similarresults for watch face (round versus rectangular) andwatch band (combinations of three levels).

The intuition of Figure 1, shown formally in thestylized model, is that simulated choice probabilitiesare more sensitive to price changes (or changes inattribute levels) when scale increases even though therelative partworths remain unchanged. Greater sen-sitivity implies more price competition, which drivesdown equilibrium prices.

This wide difference in (predicted) equilibrium priceshasmanagerial and litigation implications. For example,suppose that a firm’s CBC study reports scale � 0.4 butthe marketplace acts according to scale � 1.0; then thefirm would likely earn substantially less profit than itexpects. The effect is real. In Section 8.7, data suggestthat differences in craft yield estimates of (relative)scale that vary from 0.35 to 1.00.

Using estimates of over 11.9 million Apple Watchsales in 2016 (Reisinger 2017), the calculated priceequilibrium swing of $158 implies a swing of morethan $1.8 billion in revenue. If the predicted multiyearprofit were only a small fraction of the revenue swing,it would still be substantial. Profits are based on prices,quantities, and costs, which we address later. In litiga-tion, units sold and costs are often held constant in the“but-for” world; CBC craft would swing damagesestimates by $1.8 billion.

3.2. Scale Affects Strategic Positioning DecisionsWe use the same smartwatch empirical data, but re-port predicted profits for (counterfactual) values ofscale. In this illustration, profits are price times share.We consider a two-stage game. In the first stage, firmschoose their positioning (silver versus gold). In thesecond stage, firms launch their products, the mar-ketplace reacts, and the firms obtain equilibriumprofits based on equilibrium prices. Table 1 presentsthe equilibrium profits for all possible positioningdecisions by an innovator and a follower. (The in-novator’s profit is the top number in each subcell ofTable 1; the follower’s profit is the bottom number.)If scale is higher, in equilibrium, the innovator andfollower choose to differentiate their products (theinnovator chooses silver, the follower chooses gold),

whereas if scale is lower, the innovator and followerchoose to offer the same product (both choose silver).At least for the follower, the recommended attributelevel depends on the “true” scale, holding relativepartworths constant.Typical CBC studies make recommendations based

on the partworths and scale as estimated based on theCBC design (choice sets). But consumers may choosedifferently in the marketplace. In Section 8, we use avalidation task that mimics the marketplace to adjustscale. We illustrate that strategic recommendationschange depending on whether scale is adjusted basedon the validation task. Unadjusted scale recommendsdifferentiation; validation-adjusted scale recommendsno differentiation for the data in this paper. This is a newreason to consider including realistic validation tasksthat go beyond holdout validation in a CBC study.

4. General Formulation andBasic NotationWe begin with notation for a fully heterogeneous modelbecause the empirical studies in Section 8 use a fullyheterogeneous model. (Different consumers can havedifferent relative partworths and scale.) Appendix Asummarizes notation for both the heterogeneousmodel and a more stylized formal model. Althoughempirical studies, including ours, can have many at-tributes and many levels for each attribute, we focusin the stylized model on a single attribute with twolevels. This focus in the stylized model is sufficient toillustrate the impact of scale and is consistent withIrmen and Thisse (1998, p. 78), who conclude that“differentiation in a single dimension is sufficient torelax price competition and to permit firms to enjoy theadvantages of a central location in all other characteris-tics.”Our stylized model also applies to simultaneousdifferentiation of a composite of multiple dimensions,say, a silver smartwatch with a rectangular face anda black leather band versus a gold smartwatch with a

Table 1. Relative Profits as a Function of StrategicPositioning

Follower’s position

Innovator’s position Silver GoldHigher scale (0.8)Silver 72.7 110.8

72.7 81.2

Gold 81.2 62.8110.8 62.8

Lower scale (0.4)Silver 112.6 132.9

112.6 106.6Gold 106.6 100.2

132.9 100.2

Notes. RelativeHBCBCpartworths are heterogeneous, but the same inhigher- and lower-scale markets. Innovator’s profit is the top numberin a subcell; follower’s profit the bottom number. Bold indicates anequilibrium.

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1062 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

round watch face and a metal band. Both stylisticallyand empirically, we hold all attributes other than ourfocal attributes constant across products. In the stylizedmodel, there are no unobserved attributes.

4.1. Formal DefinitionsTo match typical applications of CBC, we focus ondiscrete (horizontal) levels of an attribute that we labelr and s. A product can have either ror s, but not both. Ifmnemonics help, think of r as round, regular, routine,ruby, or rust colored, and s as square, small, special,sapphire, or scarlet. Although the empirical model canhandle many firms, it is sufficient for the stylized modelto focus on twofirms, each ofwhich sells one product.Weallow an “outside option” to capture other firms andproducts that are exogenous to the strategic decisionsof the two-firm duopoly. In Section 9.4, we show thatthe insights apply when there are more than two prod-ucts, more than one attribute, and more than two levels.

Let uij be consumer i’s utility for firm j’s product, letuio be i’s utility for the outside option, and let pj beproduct j’s price. Let βri and βsi be i’s partworths forattribute levels r and s, respectively, and let δrj and δsjbe indicator functions for whether firm j’s producthas r or s, respectively. Let ηi indicate i’s preferencefor price, let εij be an extreme value error term withvariance π2/6γ2

i . If the error terms are independentand identically distributed, we have the standardlogit model for the probability, Pij, that consumer ipurchases firm j’s product (relative to firm k’s productand the outside option):

uij � βriδrj + βsiδsj − ηipj + εij,

Pij � eγi(βriδrj+βsiδsj−ηipj)

eγi(βriδrj+βsiδsj−ηipj) + eγi(βriδr,k≠ j+βsiδs,k≠ j−ηipk≠ j) + eγiuio.

(1)

Utility (uij) is unique to at most a positive lineartransformation (Train 2009, p. 27); hence, the mag-nitude of the error term (εij), the inverse of the errorstandard deviation (γi), and the price and partworthcoefficients (ηi, βri, βsi) are defined to at most a mul-tiplicative constant. For a single CBC study, we cannotsimultaneously estimate βri, βsi, ηi, and γi, nor can weindependently interpret the magnitude of any of theseconstructs. Within a CBC study, the magnitudes ofthese constructs can be interpreted (and estimated) onlyrelative to one another. (We can, and do, show howestimates can vary between different domains such asbetween higher-cost and lower-cost CBC studies.)

4.2. Relationships Among Different NormalizationsBecause βri, βsi, ηi, and γi are relative constructs, wemust impose one constraint for identification for bothinterpretation and estimation. The constraint variesin the literature. McFadden (2014) constrains the price

coefficient, ηi, to unity. In the McFadden (2014) nor-malization, scale is defined as ηiγi. Because ηi ≡ 1,scale becomes ηiγi � γi. The McFadden (2014) nor-malization has the intuitive advantage that the attribute-level relative partworth differences are measured incurrency units and can be interpreted as WTPs. Fromour perspective, the McFadden (2014) normalizationenables the stylized model to manipulate scale in-dependently from the relative partworths.Sonnier et al. (2007) normalize theCBCmodel using

µi � 1/γi. When ηi � 1, we define scale as ηi/µi �1/µi ≡ γi. The Sonnier et al. (2007) normalization hasno effect for maximum-likelihood estimation, butwe must adjust the prior distributions for µi whencomputing Bayesian posterior distributions. For thestylized model, we use the McFadden (2014) normal-ization because it is more intuitive when greater scaleimplies that the “signal-to-noise” ratio is larger.The Allenby et al. (2014) normalization, used com-

monly in practice, sets γi � µi � 1. In this normali-zation, WTPs require division by ηi and scale isproportional to the magnitude of the partworths. For-mally, in the Allenby et al. (2014) normalization, scalebecomes ηiγi ≡ ηi/µi � ηi. Although the Allenby et al.(2014) normalizationmakes it more difficult to untanglerelative partworths and scale, the basic theoretical andpractical insights do not change. For the stylizedmodel, all three normalizations are strategically equiv-alent (Keeney and Raiffa 1976). Empirically, HB, butnot maximum likelihood, estimation is slightly dif-ferent with the Allenby et al. (2014) normalizationversus the McFadden (2014) and the Sonnier et al.(2007) normalizations. Section 9.1 summarizes the em-pirical implications of the three normalizations.In our stylized model, we focus on the effect of a

common scale factor that may be affected by CBCcraft. To isolate the effect of scale in the stylizedmodel, we assume relative partworths are not af-fected by craft. (The impacts on relative partworthsare well studied, not new to this paper, and are addedback to the empirical model.)When CBC craft affects both scale and relative part-

worths (Section 9.3), researchers may prefer a dif-ferent empirical definition of scale. For example, withthe Allenby et al. (2014) normalization, researchershave defined scale as the sum of the estimated im-portances. (The importance of an attribute is defined asthe difference between the largest and smallest part-worth of an attribute.) This alternative definition doesnot affect the stylized model, because, in the styl-ized model, relative partworths do not depend on craft.Empirically, when scale is isolated such that relativepartworths are mostly unaffected by craft, the compar-isons among experimental conditions do not depend onthe normalization-dependent definition of scale.

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1063

4.3. Profit EquationsIf V is the market volume (including volume due tothe outside option), cj is the marginal cost for productj, Cj is firm j’s fixed cost, and f (βri, βsi, γi) is the prob-ability distribution over the relative partworths andscale (posterior if Bayesian), then the profit, πj, forfirm j is given by

πj � V (pj − cj)∫

Pij f (βri, βsi, γi)dβridβsidγi − Cj. (2)

(Empirically, if all estimates are Bayesian, we use theposterior distribution in the standard way.)

For the purposes of this paper, we assume that cjdoes not depend on the quantity sold nor the choice ofr or s. These assumptions can be relaxed and do notreverse the basic intuition in this paper. (The effect ofthe relative cost of r or s is well studied; see, e.g.,Moorthy 1988.)

4.4. Interpretation and Implications of theError Term

The error term in CBC analysis has many interpre-tations and implications. It has been interpreted asinherent stochasticity in consumer choice behavior and/or sources that are unobservable to the researcher, suchas unobserved heterogeneity, unobserved attributes,functional misspecifications, or consumer stochasticitythat is introduced by the CBC experiment (e.g., becauseof fatigue; see, e.g., Thurstone 1927, Manski 1977). Weare most interested in what happens to the (observed)scale when the craft of the CBC study changes, say,by the addition of incentive alignment or images thatbetter approximate the marketplace (more realisticimages). To address this issue, we assume that thefirm acts strategically on a CBC study anticipating theprice equilibria implied by the CBC study. However,after the firm selects its positioning strategy (saya silver versus gold smartwatch) and launches itsproduct, the prices are set by market forces; that is, themarketplace reaches the equilibrium prices becausefirms adjust price after launch until they reach a Nashprice equilibrium.

If the firm acts on a CBC study it believes to becorrect, the firm will anticipate a price equilibriumbased on the scale it believes to be true andwill chooseits position optimally based on its beliefs. But theactual realized equilibrium prices may differ if thefirm’s beliefs about scale are not sufficiently accurate.The mechanism by which marketplace prices adjustafter positioning decisions is based on market re-action. The mechanism is different from the more com-mon simplifying assumption in modern game theorythat “firms compete non-cooperatively in productspecifications with instantaneous adjustment to theNash equilibrium prices” (Economides 1986, p. 67).

The difference is necessary because, unlike typicalmodels, the firm may act based on market research itonly believes to be accurate. Ourmechanism is similarto that expressed by Hotelling (1929, pp. 48–49):

But understandings between competitors are notori-ously fragile. Let one of these business men, say B, findhimself suddenly in need of cash. Immediately at handhe will have a resource: Let him lower his price a little,increasing his sales. His profits will be larger untilA decides to stop sacrificing business and lowers hisprice to the point of maximum profit. B will now belikely to go further in an attempt to recoup, and so thesystem will descend to the equilibrium position. Hereneither competitor will have any incentive to lower hisprice further, since the increased business obtainablewould fail to compensate him.

Because actual sales and equilibrium prices dependon how consumers react to the products’ chosenpositions after the products are introduced to themarket, we need the concept of a true scale (γtrue) thatrepresents how the marketplace reacts. We pur-posefully do not define true scale as a philosophicalconstruct—it is defined as the scale that best repre-sents how consumers actually react in the market-place. Practically, we expect the true scale to be finitebecause of inherent stochasticity (e.g., Bass 1974),but our stylized theory allows true scale to approachinfinity. Our model admits many explanations of in-herent uncertainty. The stylized model needs to assumeonly that, even with the best possible craft, the firm’sprediction of consumer behavior includes a (possiblyzero) error term. True scale is a latent construct; thefirm can at best estimate its value.

4.5. Relationship to Prior ResearchOur perspective draws on, but is quite different fromthe pioneering work by Anderson et al. (1999), dePalma et al. (1985, 1987), and Rhee et al. (1992), whoalso explore the strategic implications of a normali-zation constant in a logit model. They represent themarketplace, not individual consumers, by a logitmodel and interpret the normalization constant(µ � 1/γ) as heterogeneity in consumer utility as inthe paper by de Palma et al. (1985, p. 779), who state,“theworld is pervasively heterogeneous, andwehavemade it clear how, in a particular model, this restoressmoothness [that leads to differentiation].” In theiranalyses, the firms act strategically on their un-certainty about this heterogeneity. As heterogeneityincreases firms on a Hotelling line seek minimumdifferentiation.Our stylized model makes different assumptions

and has different foci:• We explicitly constructed the stylized model to

model heterogeneity and, hence, rule out unobserved

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1064 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

heterogeneity as an explanation for scale and crafteffects.

• We explicitly constructed the stylized model sothat there are no unobserved attributes and, hence,rule out unobserved attributes as an explanation forscale and craft effects. (Online Appendix 13 reviewsminimum versus maximum differentiation theoriesthat rely on unobserved attributes.)

• We focus on how craft (and external validation)in CBC studies affects scale and, through scale, dif-ferentiation.We do not focus on differentiation per se.

• We allow firms to act on different types of in-formation (CBC studies) about consumers; our theoryseeks to provide practical suggestions forwidely usedmarket research methods.

• We illustrate the effects of craft on scale andprovide examples of the effect sizes, using data fromprofessional-quality CBC studies.

• Empirically, we model heterogeneity explicitlyand attempt to rule out unobserved attributes.

5. Stylized Formal Model withTwo-Segment Heterogeneity

In the stylized model, we focus on two mutuallyexclusive and collectively exhaustive consumer seg-ments with different relative partworths. This level ofheterogeneity is sufficient to enable two firms to targetdifferent segments and sufficient to illustrate the stra-tegic effects of scale. The strategic effects survive themore general empirical applications in Section 8, whichuse standard estimation procedures (HB CBC, testedwith three related normalizations).

We label the segments R and S, with segment sizesR and S, respectively. Partworths vary between seg-ments, but are homogeneous within segment (βri � βrRand βsi � βsR for all i in segment R; βri � βrS and βsi �βsS for all i in segment S). Scale varies among consumersin the empirical applications, but in the stylized modelwe focus on a common scale adjustment that mightvary among CBC studies of different quality. For thispurpose, it is sufficient to assume scale is constant acrossconsumers such that γi � γ for all i.

We investigate trade-offs that firms make between(1) a differentiated strategy in which each firm targetsdifferent attribute levels and (2) an undifferentiatedstrategy in which both firms target the same attributelevels. To do so, we need one attribute level to bemoreattractive than the other. Given the other symmetriesin the model, it is sufficient to model the relativeinfluence of an attribute level by the percent of con-sumerswhoprefer that attribute level,Ror S.We needpartworths to vary between segments. It is suffi-cient that their relative values reverse (r_s in onesegment and s_r in the other segment). Although thepartworths differ between segments, it would be re-dundant to also vary the magnitude of partworth

differences; thus, we set βrR � βsS � βh and βsR � βrS �βℓ. We set βh ≥ βℓ and R≥ Swithout loss of generality.Setting R≥S assures that the firm prefers r≽ s, ceterisparibus. (We can also set βℓ = 0 without loss of gen-erality, but interpretations are more intuitive if weretain βℓ in the notation.)The costs, cj and Cj, affect strategic decisions in the

obvious ways and need not be addressed in thispaper. For example, a firm might require a minimumprice such that pj ≥ cj or choose not to enter if Cj is toolarge. Such effects are well studied and affect firmdecisions above and beyond the strategic effect ofscale. For focus, we normalize V to a unit marketvolume, set Cj � 0, and roll marginal costs into priceby setting cj � 0.We label the potential strategic positions for firms 1

and 2, respectively, as either rr, rs, sr, or ss. For example,rsmeans that firm 1 positions at r and firm 2 positionsat s. Because prices,market shares, and profits dependon these strategic positioning decisions, we subscriptprices, shares, and profits accordingly. For example,p1rr is firm 1’s price in a market in which firm 1’sposition is r and firm 2’s position is r.

6. The Effect of Scale on Equilibrium Pricesand Strategic Positioning Decisions

6.1. Basic Game to Demonstrate the Impact of TrueScale (Inherent Stochasticity)

The price-positioning game is consistent with keyreferences in the strategic positioning literature (seeOnline Appendix 13) and realistic for most markets.Temporarily, we assume the firms believe they knowγtrue, which may be either finite or approach infinity.(Infinite γtrue is equivalent to a first-choice rule in CBCsimulators.) Based on this knowledge, the firms firstchoose their product positions (r or s) sequentially,and then the marketplace sets prices. (If the firmsare correct in their beliefs, they correctly anticipateequilibriumprices.)Thepositioningdecisions,oncemade,are not easily reversible, perhaps because of produc-tion capabilities or ephemeral advertising investments.Without loss of generality, firm 1 is the innovator, andfirm 2 is the follower. The innovator enters assumingthat the follower will choose its positions optimally.(We abstracted away from entry decisions by settingcj � Cj � 0.) After the firms have entered, Nash equilib-rium prices, if they exist, are realized. This two-stagegamewill be embedded in another game in Section 7 inwhich firms know that the CBC study may be im-perfect and choose whether to invest in higher-costcraft to better estimate scale prior to making strategicpositioning decisions. We address the relationship tosimultaneous entry in Online Appendix 14. We useasterisks to indicate Nash equilibrium prices, shares,and profits.

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1065

The equilibria we obtain, and strategies that arebest for the innovator and follower, have the flavorof models in the asymmetric competition literature(minimum versus maximum differentiation), butwith two important differences: (1) Our results are notdriven by unobserved heterogeneity or strategicallyrelevant unobserved attributes. (2) Our results arefocused on providing a structure to understand andevaluate the impact of improvements in CBC craft. Wedevelop the formal structure as a practical tool to eval-uate whether improvements, such as more realistic im-ages or incentive alignment, affect strategic decisions.

6.2. Price Equilibria in Heterogeneous Logit Models(as in CBC Analysis)

We are not the first to investigate price equilibria inlogit models. Choi et al. (1990) demonstrate that priceequilibria exist if partworths are homogeneous and con-sumers are not overly price sensitive. Their condition(Choi et al. 1990, p. 179) suggests that price equilibriaare more likely to exist if there is greater uncertaintyin consumer preferences—a result consistentwith ourmodel which, in addition, accounts for heterogeneity.Choi andDeSarbo (1994) use similar concepts to solvea positioning problem with exhaustive enumeration.Luo et al. (2007) extend the analysis to include het-erogeneous partworths and equilibria at the retaillevel. They use numeric methods to find Stackelbergequilibria if and when the equilibria exist.

We cannot simply assume that price equilibria existand are unique. For example, Aksoy-Pierson et al.(2013) (hereafter, APAF) warn that price equilibriain heterogeneous logit models may not exist. APAFgeneralize the analyses of Caplin and Nalebuff (1991)to establish sufficient conditions for price equilibriato exist, to be unique, and to be given by thefirst-orderconditions. The APAF conditions apply to typical HBCBC studies (Aksoy-Pierson et al. 2013, section 6);thus, we check existence and uniqueness in both ourstylized model and in our empirical analyses.

6.3. Equilibria in the Price SubgameUsing Equation (1), we obtain implicit first-orderand second-order conditions for optimal prices andprofits. We use these conditions to derive implicitequations for the equilibrium prices and profits.Differentiating further, we obtain implicit second-order and cross-partial conditions (see Appendix B).We establish that interior equilibria exist and areunique given (mild) sufficient conditions. Equilibriaexist and are unique for most posterior draws in theempirical analysis when prices are constrained to bewithin the range of measurement. When they exist,the empirical equilibria are unique. The equilibriaexist and are unique in an illustrative example of thestylized model (Section 7.6).

6.4. True Scale Affects the Relative Profits of theFirms’ Positioning Strategies

We temporarily assume the firm believes it knows thetrue scale, which can be either finite (inherent un-certainty in consumer choices) or approach infinity(no inherent uncertainty). In Section 7, we use theresults of this section to explore what happens whenthe firm does not know the true scale and bases itsdecisions on CBC market research. All proofs areformalized in Appendix B.To understand the effect of true scale on firms’

positioning strategies (choice of attribute levels inequilibrium), we examine how profit-maximizingattribute levels change as true scale increases fromsmall to large. Because the functions are continuous,we need only show the extremes. Appendix B es-tablishes that, for sufficiently low true scale, pricemoderation through differentiation does not offsetthe advantage of targeting the larger segment andboth innovator and follower choose the most profit-able attribute level, r. The proof is driven by the factthat the logit curve becomes flatter as γtrue → 0. Inthis regime, the effect of attribute changes or pricechanges has less effect on choice probabilities.When price is endogenous, common intuition is not

correct. All shares, including the outside option, donot tend toward equality as γtrue → 0. The endogenousincrease in equilibrium prices offsets this effect. In-stead, while the innovator and follower shares movecloser to one another, the equilibrium prices increaseand reduce shares relative to the outside option.As γtrue gets large, both the innovator and the fol-

lower prefer differentiation. Formally, we use twomild sufficient, but not necessary, conditions: (1) therelative partworth of r is larger than the relativepartworth of the outside option and (2) the relativepartworth of the outside option is at least as large asthe relative partworth of s. We also prove that, amongthe undifferentiated strategies, both the innovator andfollower prefer to target the larger segment and, underthe sufficient conditions and large γtrue, the innovatorprefers the larger segment. These intermediate re-sults produce an equilibrium in product positions.(See Appendix B for proofs.)

6.5. Equilibrium in Product Positions

Proposition 1. For low true scale (γtrue → 0), the innovator(firm 1) targets the larger segment (r), and the followerchooses not to differentiate. The follower targets the largersegment (r).

Proposition 2. If βh is sufficiently larger than uo and ifuo ≥ βℓ, then there exists a sufficiently large γtrue such thatthe innovator targets the larger segment (r), and the followerchooses to differentiate by targeting the smaller segment (s).

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1066 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

Because the profit functions are continuous (seealso APAF), Propositions 1 and 2 and the mean valuetheorem imply that there exists a γcutoff such that thefollower is indifferent between rr and rs. We calculateγcutoff as {γ : π*

2rs(γ) � π*2rr(γ)}. Numerically, for awide

variety of parameter values, the profit functions aresmooth, the cutoff value is unique, and π*

2rs − π*2rr is

monotonically increasing in γtrue. We have not founda counterexample.

7. Implications for Investing in the Qualityof CBC Studies

7.1. Aspects of Craft in CBC StudiesWe reviewed the conjoint analysis papers in Mar-keting Science from the last 16 years (2003–2018).Forty-six papers addressed new estimation methods,newadaptivequestioningmethods,methods tomotivaterespondents, more efficient designs, noncompensatorymethods, and other improvements. Mostly, papers fo-cused on the improved estimation of relative partworthsor implied managerial interpretations. Six of the papersaddress the implications of scale (or a related conceptfor non-CBC papers) explicitly, and of those six, threefocus on more accurate estimation, one on weightingconsumers, one on brand credibility, and one on peerinfluence. None discuss the strategic (price or position-ing) implications of scale (see Online Appendix 15).

There is substantially less focus in the conjoint-analysis literature on data-quality issues such asselecting stimuli to best represent marketplace choices(realistic stimuli). Most papers do not report whetherstimuli are text only, pictorial, or animated, but of thosethat do, the vast majority are text only. Although in-terest in incentive alignment is growing, no papersdiscuss the impact of either realistic stimuli or incentivealignment on the scale observed for the estimation data.Furthermore, in practice, defaults in software leadmostapplications to use text-only stimuli without incentivealignment.

Improving craft in CBC can be expensive. Somefirms, such as Procter & Gamble, Chrysler, andGeneral Motors, are sophisticated and spend sub-stantially on CBC. Some CBC studies invest tens ofthousands of dollars to create realistic animated de-scriptions of products and attributes complete withtraining videos. And some include additional preteststo assure that the stimuli are seen as realistic-to-marketplace by consumers. Incentive alignment canalso be expensive: one CBC study gave 1 in 20 re-spondents $300 toward a smartphone and anothergave every respondent $30 toward amusic-streamingsubscription (Koh 2012, McFadden 2014). Firms rou-tinely use high-quality internet panels, often pay-ing as much as $5–$10 for each respondent and up to$50–$60 for hard-to-reach respondents. Our reviewof the literature suggests that firms believe that each

of these investments increases the accuracy withwhich relative partworths are estimated. On the otherhand,manyfirms reduceCBC costs by using text-onlyattribute descriptions, no incentive alignment, lesssophisticated methods, convenience samples, andsmall sample sizes. We show, in the stylized modeland by example empirically, that the managerialimplications of these craft decisions (and defaults)are not trivial.

7.2. Modeling Decisions with Respect to CBC CraftIn Section 6.4, we temporarily assumed the firm be-lieved the true scale to be accurate. True scale was thescale that described how consumers would react to r,s, and price in the marketplace. We are interested inwhat happens if the firms (or testifying experts) shirkon their investments in the craft of CBC studies. Wedefine two additional constructs: γmarket research is thescale estimated by the CBC study, and may or maynot equal the true scale, and γasymptotic is the scale thatthe firm would obtain with the highest possible levelof CBC craft. If craft were costless, the firm wouldalways seek the best craft in the hopes that γasymptotic

would approximate (unobserved) γtrue. But craft isnot costless.We embed the game from Section 6 into a larger

game. We assume that if the firm invests more in CBCcraft, its estimate of scale becomes better, that is,|γmarket research − γtrue | becomes smaller. (Strategic er-rors can be made if γtrue is underestimated or over-estimated.) To focus on scale in the stylized model, weassume all (reasonable) CBC studies estimate the rel-ative partworths correctly so that the firm knows thatr_s in R, s_r in S, and R> S. In Section 9.3, we in-vestigate a double whammy whereby craft affectsboth estimated scale and estimated relative part-worths. Our results are complementary to researchto improve relative partworth estimates; hence, weneed not address the accuracy of relative partworthsin the stylized model.It is sufficient to illustrate the phenomenon in the

stylized model if we consider lower-cost and higher-cost CBC studies such that γhigher � γtrue for the higher-cost study and γlower ≠ γtrue for the lower-cost study.(In Sections 8 and 9, we demonstrate empirically thatcostly craft affects γmarket research and that it is likelythat costly craft reduces |γmarket research − γtrue |.) For thestylized model, we formally state the game order eventhoughwe can prove the results for other orders andwecan relax many assumptions empirically.) The gameorder is as follows:

1. The innovator decides whether to invest in thelower-cost or the higher-cost CBC study. (To focuson scale, we assumed that both CBC studies revealcorrectly that r_s in R, s_r in S, and R>S.)

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1067

2. The innovator completes its CBC study andobserves γmarket research.i.

3. Based on its observed γmarket research.i, the inno-vator announces and commits to either r or s.

4. The follower decides whether to invest in the lower-cost or the higher-cost CBC study. (By assumption, bothCBC studies reveal that r_s in R, s_r in S, and R> S.)

5. The follower completes its CBC study and ob-serves γmarket research.f . (The innovator has already acted;the follower observes the innovator’s position, r or s.)

6. Based on its observed γmarket research.f , the followerannounces and commits to either r or s. (Becausethe innovator has acted, the follower need not as-sume anything about the innovator’s belief aboutγmarket research.i.)

7. Both firms launch their products. The market-place determines sales and price based on γtrue—thescale that best describes consumer response. Thefirms realize their profits.

It will be obvious in Section 7.3 that the followercould have made its craft decision before learning ofthe innovator’s positioning—such a game orderingwould give the same results. Commitment to r or s im-plicitly assumes that positioning decisions are “sticky,”expensive, or based on know-how, patents, or copy-rights. Once made, the firm cannot change its position-ing even when the market price, market shares, andprofits are not as forecast. Propositions 1 and 2 give ussufficient insight to understand the innovator’s and thefollower’s craft decisions. Online Appendix 14 ad-dresses a game in which the innovator and followermove simultaneously. The simultaneous game doesnot determine which firm positions at r in a differ-entiated market, but all other implications remain.

7.3 Innovator’s Strategic Positioning Decision DoesNot Depend on Observed Scale

The innovator chooses to target the larger segment (r)in both Propositions 1 and 2, and thus the innovatormakes the same decision whether γmarket research � γtrue

or γmarket research ≠γtrue. Because the innovator’s stra-tegic positioning decision is independent of the ob-served scale, investing in a higher-cost CBC study hasno effect on the innovator’s positioning strategy. (Westate and prove the result formally in Appendix B.)The insight is consistent with recommendations inproduct development (e.g., Urban and Hauser 1993,Ulrich and Eppinger 2004). These texts advise inno-vators to use market research to identify the best at-tributes, but also advise that the accuracy need only besufficient for a go/no-go decision.

7.4. Follower’s Strategic Positioning DecisionDepends on Observed Scale

If a naıve follower underinvests in CBC craft andobserves γlower ≠γtrue, and if either γlower <γcutoff <γtrue

or γlower >γcutoff >γtrue, then the follower makes astrategic error by choosing the wrong strategic po-sition (the wrong attribute level). We state and provethe result formally in Appendix B. For example, ifγcutoff <γtrue, then Proposition 2 implies that the mostprofitable attribute level for the follower is s. How-ever, if the follower acts on γmarket research � γlower, and ifγlower <γcutoff , then, by Proposition 1, the follower willchoose the less profitable attribute level, r. In somecases, the naıve follower may underinvest in CBCstudies, but get lucky, say, if γtrue <γcutoff and γlower <γcutoff . The first inequality implies r is the follower’smost profitable attribute level, and the second in-equality implies the follower chooses r. The importantinsight is that if the naıve follower underinvests inthe craft of a CBC study, then it is relying on luck tomake the right decision.Although some authors interpret higher scale as a

surrogate for higher response accuracy (Toubia et al.2004, Evgeniou et al. 2005), we interpret scale as moreaccurate if |γmarket research − γtrue | is lower. A CBC studythat uses less costly craft can have higher estimatedscale, but those estimates can be less accurate forrepresenting the marketplace. For example, a CBCstudy with two convenient attributes, text-only stim-uli, and no incentive alignment might estimate thatscale is high because respondents answer choice tasksmore consistently. But the CBC study with such craftmight overestimate true scale because two text-basedattributes without incentive alignment may not ap-proximate marketplace choices that are more de-liberate and externally valid.

7.5. Sophisticated Bayesian Follower’s Decision onInvestments in CBC Studies

As firms become more sophisticated, they might useBayesian decision theory to decide whether to investin a higher-cost or lower-cost craft. For example, if thefollower can investK dollars to learn γtrue, the firm cancompare expected profits, from acting optimally onγtrue, to expected profits based on the prior distri-bution of γtrue. If the higher-cost study updates theprior, the calculations take this into account. Theexpected-value-of-sample-information calculationsare straightforward and provide no incremental insightabout craft decisions. For completeness, we provideexample calculations in Online Appendix 2.

7.6. Illustrative ExampleIn Online Appendix 1, we provide an illustrativenumerical example with βh � 2, βℓ � 1, uo � 1, andR � 0.55. (R programs are available from the authors.)The effect of γtrue on equilibrium prices is similar tothat observed for the empirical data in Figure 1. Forthe vast majority of the range of scale, especially inthe range we observe in empirical data, equilibrium

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1068 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

prices (and profits) decrease with scale. Prices in-crease slightly as γtrue →∞. The latter is a result ofmultiple offsetting forces when the market ap-proaches extreme behavior—very small increases inprice relative to competition have large impacts onmarket shares. As predicted, differentiated positionsare most profitable when γtrue is large, and undif-ferentiated positions are most profitable when γtrue issmall. In the illustrative example, we calculate γcutoff �{γ : π*

2rs(γ) � π*2rr(γ)} to be approximately 1.0. For the

illustrative example, opportunity losses for choosingan incorrect strategic position are quite large.

7.7. Sensitivity of the Stylized Model toAlternative Normalizations

All three normalizations imply the same stylized re-sults. For the Allenby et al. (2014) normalization (γ �µ � 1), holding the ratios of βh/η and βℓ/η constant,firms differentiate if η→∞ and choose not to differ-entiate if η→ 0. For the Sonnier et al. (2007) normali-zation (η � 1, γ ≡ 1/µ), firms differentiate as µ→ 0and choose not to differentiate as µ gets large.

8. Empirical Test: SmartwatchesIt is reasonable to ask whether the phenomena westudy stylistically are sufficiently strong that they areobservable in empirical applications. Our empiricalapplications relax the formalized assumptions of onestrategic attribute, two levels, two products, hetero-geneity limited to two segments, homogeneous scale,and homogeneous within-segment partworths. Wedemonstrate that scale can be manipulated by differ-ences in CBC craft and that recommended strategic priceand positioning decisions depend on whether scale isadjusted with validation tasks. Empirically, scale drivesstrategic decisions even when relative partworths donot vary, when firms do not react to unobserved attri-butes, and when we allow full heterogeneity.

To test the implications of the stylized theory, weundertake CBC studies in a realistic product categoryusing multiple attributes, some with more than twolevels. We vary two representative aspects of craft whilemaintaining other aspects at professional-level quality.We test the implications of an example validation task.

8.1. Smartwatch CBC StudiesWe focused on four attributes of smartwatches: casecolor (silver or gold), watch face (round or rectan-gular), watch band (black leather, brown leather, ormatching metal color), and price ($299, $349, $399, or$449). We held all other attributes constant, includingbrand and operating system. (In Section 9.4, we discusstwo studies with more attributes and a multitudeof levels.) We designed our stimuli so that any un-observed attributes were unlikely to vary amongexperimental conditions. By assumption in counterfactual

simulations, unobserved attributes were not usedstrategically for positioning decisions.We used 16 choice sets for estimation (and two as

internal holdouts) with three profiles per choice set.We included the outside option via a dual-responseprocedure (Meissner et al. 2016, Wlomert and Eggers2016).We followed standard survey design principlesincluding extensive pretesting (66 respondents) toassure that (1) the questions, attributes, and tasks wereeasy to understand; (2) that the manipulation of craftbetween respondents was not subject to demand ar-tifacts; and (3) that respondents did not report basingdecisions on any attributes that were not varied.

8.2. Image Realism and Incentive AlignmentWe varied image realism and incentive alignment in a2 × 2 between-subjects design. These aspects of CBCcraft are chosen as illustrative—we expect many as-pects of craft to have strategic implications, includingthe representativeness of the respondents, the com-pleteness and clarity of the product attributes, thetype of questions (simple versus dual response), thenumber of choice tasks, the number of profiles per choicetask, the quality of respondent training, and the qualityof partworth estimation. We chose incentive alignmentbecause of the growing academic interest in incentivealignmentandbecauseof its proven impact onpredictiveability, for example, in Ding (2007) and Ding et al.(2005, 2011). We chose image realism because theproduct-development literature suggests visual de-pictions and animations provide nearly the sameresults as physical prototypes and that rich visual rep-resentations are more realistic than text and morelikely to evoke marketplace-like responses fromrespondents (e.g., Vriens et al. 1998, Dahan andSrinivasan 2000, Dahan and Hauser 2002). Further-more, Dzyabura et al. (2019) suggest that conjointanalysis with physical prototypes provides differentconjoint-analysis estimates than less realistic stimuli. Ourreview of the Marketing Science literature (Section 7.1)suggests that realistic images and incentive alignmentare rare in the academic literature and in practice.

8.2.1. Image Realism. After the screening questions,respondents entered the CBC section. Following atraining task (not used in estimation), each respondentchose repeatedly among three smartwatch profilesand indicated whether he or she would purchase thesmartwatch. Respondents in the realistic-image exper-imental cells saw high-realism images that attemptedto represent marketplace stimuli closely (Figure 2). Tomake the images more realistic, the respondent couldtoggle among a detailed view, a top view, and an appview (not shown in Figure 2). Respondents in the less-realistic-image cells saw only text-based stimuli (withsimple images) and coud not toggle among views

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1069

(see Figure 3). Text-only stimuli are common in prac-tice and are the defaults in most professional CBCsoftware packages. On the other hand, realistic imagesare common in marketplace choices among smart-watches (see https://www.apple.com/watch/compare/).

8.2.2. Incentive Alignment. In the incentive-alignedexperimental cells, respondents saw an animatedvideo to induce incentive alignment (https://www.youtube.com/watch?v=DBLPfRJo2Ho). Specifically,respondents were told that 1 in 500 respondentswould receive a smartwatch and/or cash with a com-bined value of $500, based on their answers to thesurvey. Image realism in the video was matched toimage realism in the experimental cell (see Figure 4).Respondents who were not in incentive-aligned ex-perimental cells received the same cash offer, but thecash was not tied to their answers.

8.3. Validation TaskThe ideal external validation is whether the CBCmodel predicts the choices consumers would makeif the hypothetical profiles were to become realproducts in the marketplace. But most hypotheticalprofiles will never be market tested. Instead, wemimic marketplace choices by creating a “market”that approximates the marketplace as closely as

feasible while controlling for unmodeled market-ing actions. In this validation task, respondents choseamong 12 smartwatches and an outside option.Twelve smartwatches represent all possible designcombinations. Price was chosen randomly (withoutreplacement) according tominimal overlap regardingthe design attributes. The resulting prices are almostorthogonal to the design attributes. The task wasdelayed three weeks to cleanse memory. We believe,and an empirical posttest confirms, that this valida-tion task is perceived by respondents to be closer tomarketplace choices thanwithin-study holdout tasks.(See Online Appendix 12 for an empirical posttest.Marketplace market shares were not available forthe hypothetical smartwatch profiles in our experi-ment.) If scale adjustment based on this validation taskaffects strategic decisions, then we have demonstratedthe phenomenon empirically. Future research can ex-plore other validation tasks such as those proposed byGilbride et al. (2008) and Wlomert and Eggers (2016).

8.4. SampleOur sample was drawn from a professional panel.2

We screened the sample so that respondents ex-pressed interest in the category but did not own asmartwatch,were based in theUnited States, were aged20–69, and agreed to informed consent as required by

Figure 2. Realistic Images: Choice-Based Dual Response Task

Note. The images were animated allowing respondents to toggle views.

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1070 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

our institutional review boards. Respondents in bothstudies received standard panel incentives for par-ticipating in the study.

Overall, 1,693 respondents completed thefirstwaveof studies, and, of these, 1,147 completed the delayedvalidation task (68%). We considered respondentswho completed both the study and validation task. Weremoved respondents who always chose the outsideoption. There were no significant differences betweenthe experimental cells and the exclusion of respon-dents (p = 0.86). The final sample size was 1,044 withsample sizes varying from 248 to 275 among exper-imental conditions. To illustrate the effect of CBCcraft, we focus on comparisons among the realistic-image, incentive-aligned experimental cell (n = 270)and the text-only, not-incentive-aligned experimentalcell (n = 275). In Section 9.2, we compare the effect ofrealistic images to the effect of incentive alignmentusing the full 2 × 2 design.

8.5. Estimation of Heterogeneous Partworths andScale: Standard HB CBC Model

We adopt a standard HB CBC estimation methodconsistent with the stylized model. The basic utilitymodel generalizes the utility model in the stylizedmodel (recall that uij is consumer i’s utility for productprofile j and pj is the price). For notational simplicity,we state the utility for binary attributes recognizingthe standard generalization to multilevel attributes(as in our empirical CBC studies). If profile j has at-tribute k, then ajk � 1; otherwise ajk � −1. The utilitymodel is

uij � γi

(∑Kk�1

βkiajk − pj

)+ εij. (3)

The probability of choosing each profile (or the out-side option) is given by the standard logit modelanalogous to that used for the stylized model. This

Figure 3. Lower-Quality Study: Choice-Based Dual Response Task (No Ability to Toggle)

Figure 4. Incentive Alignment Screenshot

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1071

McFadden (2014) normalization is similar to thenormalization used by Sonnier et al. (2007) withthe exception that the latter estimate µi ≡ 1/γi. TheAllenby et al. (2014) normalization estimates an ex-plicit price coefficient ηi by setting γi � µi � 1; hence,scale is quantified by ηi. Empirically, strategic im-plications from the three normalizations are notsignificantly different (see Online Appendices 6, 7,and 8).

Like Allenby et al. (2014, p. 436), we use a hierar-chical estimation that assumes the observed data aregiven by the choice model (as a function of theβki

′s, γi′s, and ajk′s). The βki’s and ln(γi)’s are distrib-

uted multivariate normal. We use a random-effectsspecification for scale allowing the means of thedistribution to vary according to the experimentalcondition (see Section 8.6). The second-stage prior isthe standard Normal-inverted-Wishart conditionallyconjugate prior. Allenby et al. (2014) use the standardrelatively diffuse prior for the βki’s, but modify the priorfor ln(γi) to be more diffuse (ln(ηi) in their model).Details are provided in Online Appendix 5 and byAllenby et al. (2014), who provide graphical moti-vation for the prior.

To avoid misspecification errors, we tested for in-teraction effects. We did not detect significant im-provements, and hence our final model is based onmain effects. All settings not specified by Allenby et al.(2014) followed standard procedures as in SawtoothSoftware (2015). For example, we used 10,000 burn-initerations for convergence and a subsequent 10,000iterations to draw partworths and scale, from whichwe kept every 10th draw. All subsequent summaries,profits, and other reported quantities are based onthe posterior distributions.

8.6. Identification of Relative Scale as a Function ofCraft and Validation

We identify how scale changes as a function of craftby using an experimental design. The ratio of scaleamong experimental conditions is well defined andidentified for all three normalizations. With twoexperimental cells times two types of choice tasks(estimation and validation), we identify three scaleadjustments, all relative to the text-only, not-incentive-aligned, no-validation-adjustment factor, which wenormalize to 1.0. Accordingly, we estimate scale-adjustment factors for the realistic-image, incentive-aligned condition, λQh ; the validation task, λV ; andtheir interaction, λQhV . Following Fiebig et al. (2010),we use an exponential transformation to assure thatall scale factors are positive.

Let Qhi � 1 if respondent iwas exposed to the realistic-

image, incentive-aligned condition (0, otherwise), and

let Vi � 1 for respondent i’s validation task (0 for theestimation tasks). Then we obtain

uij � γQVγi

(∑Kk�1

βkiajk − pj

)+ εij, (4)

where ln(γQV) � λQhQhi + λVVi + λQhVQh

i Vi.

This specification was estimated as a random-effects model within a HB framework that assumes anormal distribution for ln(γi) with means accordingto ln(γQV). The priors are otherwise consistent. Thefull specification can be found in Online Appendix 6.Following Bayesian principles, this specification

uses all of the data simultaneously and rigorously.Wecompared this specification to an ad hoc method inwhich we estimate parameters for each experimen-tal cell using the CBC choice tasks and then use asingle-parameter logit model to estimate a scale-adjustment factor between choice tasks and the vali-dation task. The ad hoc specification has the advan-tage of separating relative partworth estimation fromscale-adjustment because the relative partworths areestimated independently for each experimental cell.When we compared the results, the specification inEquation (4) was highly correlated with the ad hocmethod (ρ = 0.995).

8.7. CBC Market-Research Quality and ValidationAffect Scale as Observed by the Firm

The posterior means and standard deviations of thescale-adjustment posterior distributions of γQV aregiven in Table 2. First, we notice that in the major-ity of posterior draws (99%) for the estimation choiceprofiles only, relative scale is higher for text-onlyquestions without incentive alignment than it is formore realistic images with incentive alignment. Ifscale is used as a surrogate for response accuracy asin Evgeniou et al. 2005, Toubia et al. 2004, and others,the firm might conclude that investments in realisticimages and incentive alignment reduced responseaccuracy among the CBC profiles. But the goal is nota higher scale based on CBC profiles; the goal is tominimize |γmarket research − γtrue |.Scale might be artificially inflated among text-only

choice tasks because it is easier for respondents toanswer such questions consistently, but at the sametime text-only choice tasks might be less predictiveof choices in a marketplace than incentive-alignedquestions based on stimuli that match the market-place. To the extent that scale based on realistic im-ages and incentive alignment and adjusted for thevalidation task is our best estimate of γtrue, then|γmarket research − γtrue | is best, by assumption, for the

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint Analysis1072 Marketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s)

realistic-image, incentive-aligned, validation-adjustedestimates. All relative comparisons make intuitivesense. The next-best estimate is for realistic-image,incentive-aligned, estimation-only scale, then text-only, not-incentive-aligned, validation-adjusted scale.The worst estimate is text-only, not-incentive-aligned,estimation-only scale.

Table 2 isolates a scale effect. A common measure,hit rates, isolate a relative-partworth effect. As ex-pected, hit rates are substantially improved for therealistic-image, incentive-aligned condition—hit ratesincrease from 24% to 39% (chance is 7.7%) for thevalidation task and from 64% to 77% (chance is 25%)for the estimation task.

Uncertainty explained (U2; Hauser 1978) is basedon the joint accuracy of scale and relative partworths.In our data, U2 increases for the realistic-image,incentive-aligned condition—from 0.16 to 0.33 forthe validation task and from 0.34 to 0.53 for the es-timation task. Based on the posterior distribution, alldifferences (hit rates and U2) are significant (seeOnline Appendix 11). There was no draw in whichthe text-only, not-incentive-aligned condition per-formed better. Taken together, these results implythat γmarket research is closer to γtrue for the realistic-image, incentive-aligned condition.

The effects appear to be robust. For example, whenwe use a mixture of normal distributions to estimateupper-level heterogeneity or random splits of thesample or the choice tasks used for the estimation, weobtain the same basic results. Scale adjustment fac-tors are also not affectedwhen using less data, neithervia splits of the sample nor choice tasks; only posteriorstandard deviations increase for subsets of the sample(see Online Appendix 8). The results are robust to al-ternative model normalizations (see Section 9.1).

Table 2 is important for practice because the vast ma-jority of CBC studies rely on unadjusted CBC-choice-task-only estimates of scale. Text-only, not-incentive-alignedmeasures based on estimation data alonemightgive the firm false confidence because the analysisoverestimates scale, but increases |γmarket research − γtrue |.We next show that errors due to over- or underesti-mating scale have substantial strategic implications.

8.8. The Empirical Data Produce Strategic EffectsAnalogous to Those in the Stylized Model

Table 1 previewed relative profits as a function ofstrategic positioning. We created Table 1 by holdingconstant the (heterogeneous) relative partworths fromthe smartwatch study, but counterfactually varying thelevel of scale adjustment. (Unadjusted γi continues tovary among respondents.) For each combination ofstrategic positioning attributes (silver versus goldcolor), we use the root-finding method described inAllenby et al. (2014) to find the price equilibria. Inorder to avoid extrapolation beyond the price rangeused in the CBC experiment, we cap prices at the upperlimit of the data ($449). Because more respondentspreferred silver to gold (65.7%) than vice versa, theanalogy to the stylizedmodel is r = silver, even though“r” is mnemonically cumbersome for silver.Using the same heterogeneous relative partworths,

we calculate γcutoff as the scale adjustment for whichthe follower’s undifferentiated profits (π*

2rr) equal itsdifferentiated profits (π*

2rs). Numerically, γcutoff @ 0.6.As an illustration only, we choose a true scale abovethe cutoff (γtrue � 0.8) and a true scale below the cutoff(γtrue � 0.4). If we assume that the true scale is 0.8 andthe market is 11.9 million units (Reisinger 2017), thenmisestimating the true scale to be below the cutoff andnot differentiating from the innovator would result inover a $100 million opportunity loss for the follower.We obtained similar results when we used CBC sim-ulators forwatch face (rectangular versus round),watchband (black versus brown or other combinations), oralternative model normalizations. In all counterfactualtests using empirical HB CBC partworths, the marketalways shifted from differentiated to undifferentiatedas (true) scale decreased through a critical value.With γcutoff @ 0.6, we interpret the implications of

Table 2. For the text-only, no-incentive CBC study,estimation-based scale implies differentiation, whereasvalidation-based scale reverses the strategic recom-mendation to no differentiation. For the realistic-image,incentive-aligned CBC study, estimation-based scaleimplies differentiation, whereas validation-based scaleimplies that scale is close to the cutoff where differen-tiation and no differentiation are equally profitable.Validation adjustment has strategic implications.

Table 2. Posterior Means of Relative Scale Adjustment

Text only, no incentive alignment Realistic images, incentive alignment

Scale is based on estimation choice tasks 1.00a 0.86(n.a.) (0.06)

Scale is adjusted to validation task 0.35 0.61(0.04) (0.06)

Notes. Standard deviations are in parentheses. The full posterior distribution is available from the authors. n.a., not applicable.aNormalized to 1.00 for identification.

Hauser, Eggers, and Selove: Scale in Choice-Based Conjoint AnalysisMarketing Science, 2019, vol. 38, no. 6, pp. 1059–1081, © 2019 The Author(s) 1073

9. Robustness Tests9.1. Alternative Normalizations of Scale Do Not

Change the ResultsWe compare empirical estimates obtained from theMcFadden (2014) normalization in the stylizedmodel(ηi � 1 and γi log-normally distributed), the Sonnieret al. (2007) normalization (ηi � 1 and µi � 1/γi log-normally distributed), and the Allenby et al. (2014)normalization (γi � 1 and ηi log-normally distrib-uted). The posterior means of the scale adjustmentsvary slightly, but well within posterior confidenceintervals. The implications of the stylized model arenot dependent on the empirical normalization. Ratio-based WTP posterior means and medians are almostidentical between the McFadden (2014) normaliza-tion, and the Sonnier et al. (2007) normalization. Asanticipated by Sonnier et al. (2007, pp. 315–317), ratio-basedWTPposteriormeans varymore for theAllenbyet al. (2014) normalization, although median WTPestimates reduce this variation. Detailed estimatesare provided in Online Appendix 10.

9.2. Realistic Images and Incentive Alignment, EachActing Alone, Affect Relative Scale

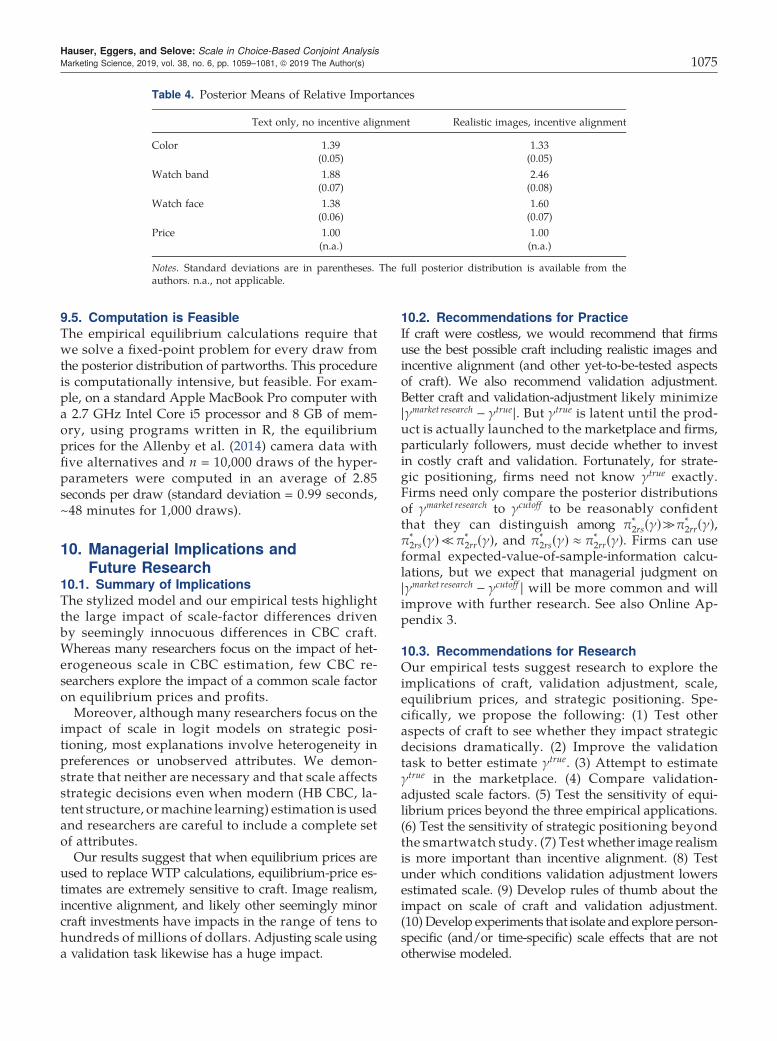

Table 3 extends the analyses in Table 2 to provide theposterior means of the scale adjustments separatelyfor realistic images, incentive alignment, and theirinteraction. The results suggest that using realisticimages impacts scale at least as much as incentivealignment—more for validation-based adjustments.The relative improvement due to realistic images isabout three times that of incentive alignment forvalidation-based adjustments: 0.53 − 0.35 � 0.18 ver-sus 0.41 − 0.35 � 0.06. Interactions increase both ef-fects. If the hypothesis that image realism is more im-portant than incentive alignment holds up, the resultsare important. Whereas incentive alignment is gain-ing traction in academia and in practice, much lessattention has been devoted to image realism.

9.3. Results Survive a Double Whammy If CBC CraftAlso Affects Relative Partworths