the sixth imf -japan high level tax conference for asian ... · the sixth imf -japan high level tax...

TRANSCRIPT

The Sixth IMF-Japan High Level Tax Conference For Asian Countries Tokyo, 7-9 April 2015

Page 2 Ministry of Finance

Republic of Indonesia

Self Assessment System Types of Tax:

Income Tax Individual : progressive rate 5%-30% Corporation : flat rate 25% (starting from 2010) Small and Medium Enterprise : 1% from total gross profit (terms & condition applied)

Value Added Tax : flat rate 10% Property Tax : flat rate 5% (effective rate 0.1%) Stamp Duty : 2 rates

Tax Treaty: 65 countries Organization:

Head Office (1) Regional Office (31) Operational Office (331)

Large Taxpayers Office - LTO – (4) Medium Taxpayers Office - MTO – (28), including special region tax offices Small Taxpayers Office - STO – (299)

Human Resources ± 32,000 staff

Page 3 Ministry of Finance

Republic of Indonesia

Type of Office No. of Offices Taxpayers Administered

Regional Office 31 -

Large Taxpayers Office 4 ± 300

Medium Taxpayers Office 19 ± 1.000

Special Region Tax Office 9 ± 1.000

Small Taxpayers Office 299 ± 50.000

TOTAL 331

Tax Services, Dissemination, And Consultation Office (KP2KP) 207

Data Processing Centre 4

Call Centre 1

3

Page 4 Ministry of Finance

Republic of Indonesia

1

3

DGT RTO Aceh 7 KPP

14 KP2KP

DGT RTO Sumatera Utara I

9 KPP

DGT RTO Sumatera Utara II

8 KPP 11 KP2KP

DGT RTO Kalimantan Barat

6 KPP 7 KP2KP

DGT RTO Kalimantan

Selatan & Tengah 9 KPP

18 KP2KP

DGT RTO Kalimantan Timur

8 KPP 6 KP2KP

DGT RTO Sulawesi Selatan, Barat & Tenggara

8 KPP 6 KP2KP

KPDDP Makassar

DGT RTO Riau & Kep. Riau

13 KPP 10 KP2KP

DGT RTO Sulawesi Utara, Tengah, Gorontalo &

Maluku Utara 11 KPP

16 KP2KP DGT RTO

Papua & Maluku 7 KPP

15 KP2KP

19 18 17 16 2 1

20

21 4

5 KPDDP Jambi

DGT RTO Sumatera Barat &

Jambi 8 KPP

19 KP2KP

DGT RTO Sumatera Selatan

& Kep. Babel 13 KPP

13 KP2KP 6

7

DGT RTO Bengkulu & Lampung

9 KPP 11 KP2KP

DGT RTO Banten 9 KPP

1 KP2KP 8

DGT RTO Jakarta Pusat

16 KPP

DGT RTO Jakarta Selatan

13 KPP

DGT RTO Jakarta Barat

11 KPP PPDDP KPDE

DGT RTO Jakarta Timur

9 KPP

DGT RTO Jakarta Utara

8 KPP 1 KP2KP

DGT RTO Jakarta Khusus

9 KPP

DGT RTO Wajib Pajak

Besar 4 KPP

KLIP

9 DGT RTO

Jawa Barat I 16 KPP

2 KP2KP

DGT RTO Jawa Barat II

17 KPP 2 KP2KP

10 DGT RTO

Jawa Tengah I 17 KPP

5 KP2KP

DGT RTO Jawa Tengah II

12 KPP 6 KP2KP

11 DGT RTO

DIY 5 KPP

DGT RTO Jawa Timur I

13 KPP

DGT RTO Jawa Timur II

15 KPP 7 KP2KP

DGT RTO Jawa Timur III

15 KPP 7 KP2KP

DGT RTO Bali 8 KPP

4 KP2KP

DGT RTO Nusa Tenggara

11 KPP 11 KP2KP

12 14 15

13

1

2

3

4 5

6

7 8

9 10 11

12 13 14 15

16

17

18

19

20

21

331 Tax Offices (TOs) for 511 Municipalities/Cities

(132 TOs with area > 1 Municipalities/Cities)

31 Tax Regional Offices (TROs) for 34 Provinces

(9 TROs with area > 1 Province)

3

Page 5 Ministry of Finance

Republic of Indonesia

1,610 1,787 2,303

2,730 3,338

3,957

4,949

5,604

6,423

7,419

8,229

9,084

176 205 239 299 358 425 571 545 628 743 835 921 13.0% 13.5% 12.2% 12.7% 12.3%

12.4% 13.3% 11.1% 11.2% 11.8% 11.9% 12.1%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

GDP Indonesia

Tax Revenues by DJP

Tax Ratio

Description Year

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 GDP Indonesia* 1.610 1.787 2.303 2.730 3.338 3.957 4.949 5.604 6.423 7.419 8.229 9.084 Tax Revenues by DGT* 176 205 239 299 358 425 571 545 628 743 835 921 Tax Ratio** 13,0% 13,5% 12,2% 12,7% 12,3% 12,4% 13,3% 11,1% 11,2% 11,8% 11,9% 12,1% Realisation of Revenue Target 98% 97% 100% 99% 96% 98% 107% 94% 95% 97% 94% 93%

*) in Trillion Rupiah **)including revenues from Customs and Excises. For year 2011, 2012, and 2013, Tax ratios are 10%, 10,1% and 10,13%

For the last 11 years, tax ratios were being relatively stagnant with tendency of

decreasing. Revenue target was only achieved 2 times (year 2004 and year

2008)

Target Tax Ratio year

2019

16%

Tax Revenue

2014 981 T

Page 6 Ministry of Finance

Republic of Indonesia

Description Year

2006 2007 2008 2009 2010 2011 2012 2013

Number of Registered Taxpayers 4.478.032 6.645.060 10.212.067 15.911.576 19.112.590 22.319.073 24.812.569 28.002.205

Number of Tax Officers 30.196 31.034 31.151 31.825 31.590 31.733 31.316 32.270 Registered Taxpayers to Tax Officers ratio 148 214 328 500 605 703 792 868

4,478,032

6,645,060

10,212,067

15,911,576

19,112,590

22,319,073

24,812,569

28,002,205

148

214 328

500 605

703 792 868

Number of Registered Taxpayers from year 2006 to 2012 have increased nearly 6 times, meanwhile number of Tax Officers are relatively

stagnant.

30,196 31,034 31,151 31,825 31,590 31,733 31,316 32,270

2006 2007 2008 2009 2010 2011 2012 2013

Country Number of Tax Officer

Number of Country

Population

Tax Officer to Country Population

Ratio

Germany 110K 80 mio 1:727

Australia 25K 25 mio 1:1.000

Japan 66K 120 mio 1:1.818

Indonesia 31K 240 mio 1:7.700

6

Page 7 Ministry of Finance

Republic of Indonesia

Current DG Tax segmentation and tax office coverage does not cater to the diverse needs of taxpayers. There are no differentiation within SME segment;

Criteria for assigning taxpayers to LTO, MTO and STO is not updated regularly;

STOs have very burdensome coverage ratios, which are imbalanced across geographies: Each STO serves ~250,000 potential

taxpayers Severe geographic imbalance Revenue potency not fully captured STO as the primary channel for serving

individuals and SMEs Format of STO is exactly the same as MTO

and LTO (i.e., 8 sections with ~70-80 staffs) • One-size-fits all regulation for audit

procedures Access to data is limited; DGT must to follow

long procedure to obtain data from other parties (eg. Banks)

• Insufficient number of auditors and Account Representatives (AR) – Auditors account for 14% of

DG Tax workforce – ~4,500 auditors – ~6,800 ARs conduct both

supervision and services function

• Challenges in Promotions and Transfers – Gender imbalance – Wide Geographic areas

• Improving on the job training system to increase skill and knowledge of staff across the nation

• Setting up employee's performance evaluation system (KPIs)

Challenges related to Human Resources

Page 8 Ministry of Finance

Republic of Indonesia

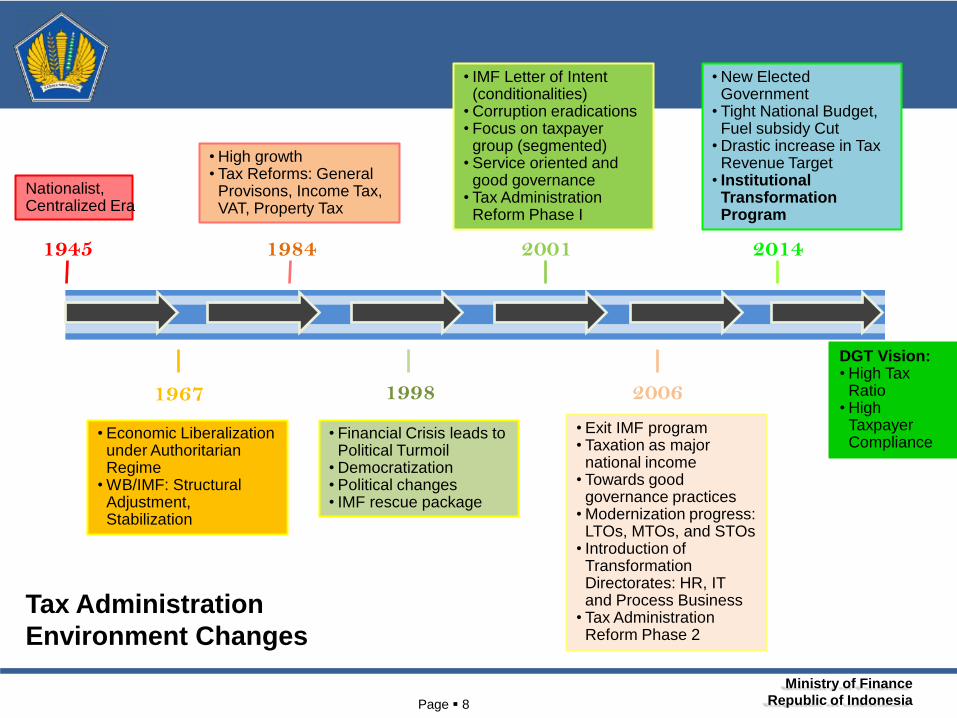

1945 1984 2001 2014

1967 1998 2006

Nationalist, Centralized Era

•High growth • Tax Reforms: General

Provisons, Income Tax, VAT, Property Tax

• Economic Liberalization under Authoritarian Regime •WB/IMF: Structural

Adjustment, Stabilization

• Financial Crisis leads to Political Turmoil •Democratization • Political changes • IMF rescue package

• Exit IMF program • Taxation as major

national income • Towards good

governance practices •Modernization progress:

LTOs, MTOs, and STOs • Introduction of

Transformation Directorates: HR, IT and Process Business • Tax Administration

Reform Phase 2

• IMF Letter of Intent (conditionalities) •Corruption eradications • Focus on taxpayer

group (segmented) • Service oriented and

good governance • Tax Administration

Reform Phase I

•New Elected Government • Tight National Budget,

Fuel subsidy Cut •Drastic increase in Tax

Revenue Target • Institutional

Transformation Program

DGT Vision: •High Tax

Ratio •High

Taxpayer Compliance

Tax Administration Environment Changes

Page 9 Ministry of Finance

Republic of Indonesia

Change in Paradigm

Taxpayers Orientation

Equal Treatment

Simplification

Efficiency

ICT-based

Good Governance

“Excellent Services and Intensive Monitoring with Good Governance”

High Voluntary of Tax Compliance High Trustworthy on Tax Administration High Integrity and Productivity of Tax Apparatus

9

Page 10 Ministry of Finance

Republic of Indonesia

Vision

To be a trusted tax administration institution that treats

all taxpayers fairly and delivers excellent service

through technology

Emphasizes ‘tax fairness’

Opportunity to leapfrog to ‘advanced services’ through technology

Mission

Improve the welfare of all Indonesians by:

▪ Collecting revenues and enforcing the law

equally to all taxpayers

▪ Making it easy for taxpayers to comply

▪ Staying at the forefront of relevant technology

▪ Attracting and developing best-in-class talent

Inspirational and meaningful

How services will be delivered

Employees as key stakeholder

What it means to treat taxpayers fairly

What it means to deliver excellent service

Page 11 Ministry of Finance

Republic of Indonesia

Initial emphasis on TAX FAIRNESS Shift towards SERVICE EXCELLENCE

Establish DG Tax credibility and capture the deterrent effect Increase audit coverage; reduce time to audit Improve integrity of law enforcement Launch integrated communications

Data-driven taxpayer outreach and risk-based compliance Establish seamless access to 3rd party data for

detection of the informal economy and for the compliance risk model (crm)

Link compliance risk model to critical business processes

Lay the foundation for advanced services by improving data management & investing in IT Clean taxpayer registry Process tax returns faster via improved DPC Drive e-filing aggressively Link NPWP to e-KTP Revamp SIDJP

Offer relevant, advanced services to taxpayers Push for e-filing (and other e-services) at scale Shift aggressively to web and call centers

Secure the flexibility to attract and develop best-in-class talent; restructure the organization

Quick wins (2013-2014) Long term (2020-2025) Medium term (2015-2019)

Page 12 Ministry of Finance

Republic of Indonesia

Institutional Transformation

Program

Collect revenues and

enforce the law fairly

Make it easy for taxpayers to

comply

Stay at the forefront of

relevant technology

Attract and develop top

Talent

The Transformation will carry out 4 Missions …

Page 13 Ministry of Finance

Republic of Indonesia

Transformation themes

Collect revenues and enforce the law fairly

Attract and develop top talent

Mission

Make it easy for taxpayers to comply

Shift the tax mix to include all taxpayers I

V Strengthen external partnerships

II Enforce risk-based compliance

III Improve the integrity of law enforcement

Strengthen human capital IX

X Empower the organization

IV Capture the deterrent effect with integrated communications

Stay at the fore-front of relevant technology

VIII Revamp and integrate IT systems

Implement ‘lean operations’ and electronification

Shift to a multi-channel service model

VI

VII

Page 14 Ministry of Finance

Republic of Indonesia

1 Improve segmentation and coverage model of small taxpayers

Transformation themes Key initiatives

Make it easy for taxpayers to comply

Collect revenues and enforce the law fairly

Attract and develop top talent

Launch an integrated communications strategy 7 Capture the ‘indirect effect’ via integrated communications

Ensure quality and consistency of law enforcement 6 Improve the integrity of law enforcement

Migrate taxpayers to e-filing 11

Enhance tax offices 9

Selectively increase DPC coverage and improve data capturing capabilities 10

8 Systematically engage 3rd parties for data, enforcement and taxpayer outreach

Implement ‘lean’ operations and end-to-end electronification

Shift to a multi-channel service model Expand functionality of website 13

Drastically increase call center capacity 12

Secure flexibilities needed for the transformation 16

Restructure the organization 15

Strengthen external partnerships

Pursue the informal economy through an end-to-end approach 2

Revamp the VAT administration system 3

Enforce risk-based compliance 5 Improve audit and collections effectiveness1

4 Develop a predictive, risk-based compliance model linked to business processes

Revamp and integrate IT systems Stay at the forefront of relevant technology

IT initiatives are implemented in coordination with MOF; details are provided in the ICT Blueprint

Empower the organization

Strengthen human capital Re-align functional staff and selectively increase capacity 14

Cross-cutting HR initiatives on talent and performance management are implemented in coordination with MOF

Shift the tax mix to include all taxpayers

IV

III

VI

V

VII

X

I

II

VIII

IX

CONTEXT AND OVERVIEW

Page 15 Ministry of Finance

Republic of Indonesia

Transformation themes

QUICK WINS (2013-2014) Gain the license to reform

Long term (2020-2025) Institutionalize breakthroughs

Revamp and integrate IT systems

VIII IT initiatives are implemented in coordination with MOF; details are provided in the ICT Blueprint

Key initiatives

Medium term (2015-2019) Achieve operational excellence at scale

Secure and strengthen human capital

IX

Cross-cutting HR initiatives on talent and performance management are implemented in coordination with MOF

14 Re-align functional staff and selectively increase capacity

▪ Business processes adjusted to re-align account representative (AR) role in the short term

▪ Increased automation results in reduced need for manpower in labor intensive roles

▪ 75% of ARs transition to become auditors; remaining 25% form part of new “consultation section” within KPPs

▪ KPP enhanced to ensure separation of roles

Empower the organization X

Enforce risk-based compliance II

Shift the taxpayer mix to include all taxpayers

I 2 Pursue the informal economy through an end-to-end approach

▪ 100% of taxpayers with NPWP (linked to e-KTP) by 2017 ▪ Informal economy captured sector-by-sector, through an end-to-end

approach (until crm is implemented in 2018)

▪ Informal economy detected through comprehensive 3rd party data

▪ Study on informality completed

3 Revamp VAT administration system ▪ Mandatory roll out of e-invoice by 2016 ▪ Real-time validation for VAT e-invoice ▪ Testing of e-invoice client application

1 Improve segmentation and coverage model of small taxpayers

▪ Services offered at 3rd party branch networks (e.g., post office) by 2016 ▪ Full roll-out of mobile tax units by 2017 ▪ KP2KP revamped into “KPP-B”; selective increase in rural areas

▪ Significant shift to web and call center; KPP can be rationalized in urban areas

▪ Segmentation of small taxpayers refined

Maximize the ‘deterrent effect’ via integrated communications

IV

7 Launch an integrated communications strategy

▪ Taxpayers are aware of their obligation to pay tax, understand the consequences of non-compliance, and believe that DG Tax is making it easy for them to comply

▪ Taxpayers consider DG Tax a trusted institution, striking the balance between law enforcement and taxpayer service

▪ Tax education becomes part of structured and integrated curriculum by 2019

▪ Credible reputation established internally & among government agencies

▪ Support and commitment from top national leadership

Strengthen partnerships with external parties

v

8 Systematically engage 3rd parties for data, enforcement and taxpayer outreach

▪ Full access to all 3rd party data; seamless inter-linkage of IT system and data exchange

▪ Priority 3rd parties systems linked to DG Tax (e.g., e-KTP, BI) for the risk-based compliance model

▪ Top-down mandate secured (e.g., President) & minister-level engagement

▪ Law enforcement partnerships strengthened

Implement ‘lean’ operations and end-to-end electronification

VI

Shift to a multi-channel service model

VII

Improve integrity of law enforcement III

4 Develop a predictive, risk-based compliance model linked to business processes

▪ Automated and centralized risk engine completed (by 2018) ▪ Tailored business processes implemented nationally, including audit (e.g.,

“lean” approach for STO), collections, service and education

▪ Intelligence-led risk identification; predictive power of risk engine enhanced with comprehensive 3rd party data

▪ Risk engine prototype piloted ▪ Taxpayer registry data cleaned for

inconsistencies and duplicates

5 Improve audit and collections effectiveness (until CRM is implemented)

▪ Differentiated audit and collections approach launched (e.g. SWAT team with highly experienced and specialized skills

▪ Simplified audit steps ▪ Improved case allocation ▪ Improved tools and worksheet template ▪ Transition to CRM

6 Ensure quality and consistency of law enforcement

▪ Workload analysis of law enforcement employees completed

▪ Comprehensive knowledge management system across audit, objection, appeal & investigation function

▪ Peer review and quality assurance process integrated with HR management system e.g., KPIs, reward & punishment

▪ Full roll-out of integrated case workflow management (potency revenue, audit, objection, appeal & investigation)

13 Expand functionality of website

12 Drastically increase call centers capacity

▪ Continued shift away from tax offices towards alternate channels

▪ Single taxpayer account, payments and select services (e.g., tax refund status) available online; service offerings integrated with call center

▪ 2-3x increase in manpower; IVR system piloted

▪ Website redesigned

11 Migrate taxpayers to e-filing

9 Enhance tax offices

10 Selectively increase DPC coverage and improve data capturing capabilities

▪ Universal adoption of e-filing ▪ Paper based tax returns remain only in

most remote areas; submission can be done directly to DPC for processing

▪ Paper-based tax returns for single-income individuals (1770SS) can be received through any tax offices and sent directly to DPC by 2015; DPC coverage selectively expanded until 2019

▪ Universal e-filing capability platform available for all type of tax return in DG Tax by 2018

▪ Nationwide archive digitalization by 2018 ▪ All paper-based tax return sent directly to DPC by 2019

▪ Standardized document management system in tax offices

▪ Consistent taxpayer service interaction in tax offices

▪ e-filing available for single-income individuals

16 Secure flexibilities needed for the transformation

15 Re-structure the organization ▪ Approval from MenPan, President and Parliament for DG Tax to reduce span of control, set compensation, manage performance, and set own budget

▪ DG Tax is a “privately run government revenue agency” which is structured around customer segments

▪ Functional organization structure with dedicated offices for large taxpayers by 2019; audit becomes increasingly specialized

▪ Employee value proposition is competitive with public and private sector

Page 16 Ministry of Finance

Republic of Indonesia

Transformation themes From… To…

Empowered organization

▪ Bureaucratic processes; wide span of control ▪ Limited flexibilities

▪ Revamped organization structure ▪ DG Tax as a “privately run government agency” 10

Taxpayer mix 1 ▪ Corporate-focused, export-reliant ▪ One-to-one extensification; <50% compliance

▪ 100% of Indonesian taxpayers with an NPWP ▪ Data-driven outreach with 100% compliance

▪ Time consumed by low-risk taxpayers ▪ One-size-fits all approach Risk-based

compliance 2 ▪ Data-driven compliance risk model (CRM)

enables business processes to be tailored to risk level (e.g., SWAT team vs “lean” approach)

Lean operations and electronification 6

▪ Extremely low e-filing rate ▪ Paper-based and labor intensive processes ▪ Limited digitization capacity, low accuracy

▪ e-filing available for all Indonesians ▪ Streamlined returns processing in <15 days ▪ Selective expansion of data processing centers

Multi-channel service 7

▪ Tax-office centric service model (high touch, high cost)

▪ Extremely low call center capacity

▪ Call center capacity expanded 10x ▪ Full suite of e-services offered on pajak.go.id

(e.g., e-payment, single sign on)

Integrity law enforcement

▪ Perception of lack of transparency, consistency, and integrity

▪ Rigorous internal controls (e.g., peer reviews), knowledge-based tools and proper incentives 3

Integrated communications

▪ Audits and investigations not publicized ▪ Communications driven by single directorate

▪ Deterrent effect captured ▪ Integrated governance and processes 4

External partnerships

▪ Bottom-up, one-by-one engagement ▪ Low cooperation

▪ Top down engagement for data, enforcement and taxpayer outreach

▪ Intensive cooperation (e.g., stakeholder labs) 5

Revamped IT ▪ Data is not clean, no ‘single source of truth’ ▪ Fragmented systems and manual processes

▪ Systems centralized and rationalized ▪ Relevant technologies adopted 8

Human capital ▪ Insufficient manpower to cover new taxpayers ▪ Lack of functional staff ▪ No performance differentiation

▪ Selective increase in capacity (e.g., auditors) ▪ End-to-end talent and performance management 9

Page 17 Ministry of Finance

Republic of Indonesia

Initial focus on TAX FAIRNESS Shift towards SERVICE EXCELLENCE

Short term (2013-2014) Gain the license to reform

Medium term (2015-2019) Establish operational and service excellence at scale

Long term (2020-2025) Institutionalize breakthroughs

▪ Highly skilled ‘SWAT team’ of auditors, lawyers and bailiffs serve large, high-risk taxpayers

▪ Up to 700,000 new e-filers ▪ Tax returns processing time

reduced by 50% ▪ Call center expanded 2-3x ▪ Approval secured to reduce

span of control, offer competitive compensation and make major investments in IT infrastructure

▪ 100% of Indonesians registered, with their NPWP fully linked to e-KTP

▪ 25 million e-filers for all types of taxes; incl. access to single taxpayer account

▪ Paper tax returns sent directly to data processing centers for digitization

▪ Every citizen with access to a physical point of contact in their district

▪ Access to priority 3rd party data aids in extensification and intensification; informality is addressed sector-by-sector

▪ Compliance risk model enables segmented approach for service, education and law enforcement

▪ DG Tax operates as a “privately run government agency”

▪ Full suite of services available electronically (e.g., e-payment); removal of paper in processing

▪ Seamless access to 3rd party data enables easier detection of the informal economy; and allows for a fully automated risk-based compliance model

▪ Process automation at scale (e.g., automation of case allocation, risk rating of refunds)

▪ Organization structure shifts to become taxpayer-centric

Page 18 Ministry of Finance

Republic of Indonesia

▪ Up to 700,000 new e-filers

▪ 100% of Indonesians registered, with their NPWP fully linked to e-KTP

▪ 25 million e-filers for all types of taxes; incl. access to single taxpayer account

▪ Paper tax returns sent directly to data processing centers for digitization

▪ Compliance risk model enables segmented approach for service, education and law enforcement

CONTEXT AND OVERVIEW

Page 19 Ministry of Finance

Republic of Indonesia

End of Presentation Thank You