taxing wealth: policy challenges and recent debates; · pdf file ·...

TRANSCRIPT

WEALTH-RELATED TAXES:

WHAT FUTURE?

Michael Keen

Sixth IMF-Japan High-Level Tax Conference For Asian Countries in Tokyo

April 7, 2015

Outline

• Context

• What types of taxes?

• Capital income and/or capital taxes?

• Differentiating across assets?

• Tax competition and EOI

Context

Revival of Interest—?

• Marked increase in income inequality—especially at very top—and in wealth-income ratios

– Cannot “leave equity objectives to spending side”

• Recognition redistribution may not be bad for growth

• Need for revenue

Recurrent Wealth Taxes: Demise or Recovery?

• Demise

– Removal in Canada, Sweden, Australia, Pakistan… (but France, Norway, Switzerland…)

– Reflecting

• Tax competition

• “Healthy, wealthy and well-advised” manage to escape

• But some revival? Spain, Iceland

– Still (increasingly?) implicit in ‘standard of life’ checks

• Historically, a major tax base—What happened?

In the Region

• Wealth tax: – India, to be removed 2015-6 – Pakistan (removed 2001, revived 2013 only) – Thailand, subnational land tax

• Estate tax: – Philippines; – (Sri Lanka eliminated 2008)

• Inheritance/gift tax: – Bangladesh (inheritance but no gift tax) – Philippines – Thailand, proposed – Vietnam

Growth in Wealth (current exchange rates)

Source: James Davies, Rodrigo Lluberas, and Anthony Shorrocks, Credit Suisse Global Wealth Databook 2014

0

10

20

30

40

50

60

70

80

90

100

IDN

MYS

IND

PH

L

THA

KO

R

PN

G

FJI

CH

N

SLB

LKA

TON

VU

T

KH

M

LAO

MD

V

MN

G

VN

M

NP

L

BG

D

PA

K

Wealth Gini

Disposable income Gini

= 70.7

= 37.7

8

Source: Disposable income Gini is taken from OECD; Luxembourg Income Study Database; Socio-Economic Database for Latin America and the Caribbean (SEDLAC); World Bank; Eurostat. Wealth Gini data comes from Credit Suisse Global Wealth Databook (2012).

Countries included: BGD=Bangladesh; BTN=Bhutan; KHM=Cambodia; CHN=China; FJI=Fiji; IND=India; IDN=Indonesia; KIR=Kiribati; KOR=Korea, Republic of; LAO=Laos; MYS=Malaysia; MDV=Maldives; MHL=Marshall Islands; MNG=Mongolia; MMR=Myanmar; NPL=Nepal; PNG=Papua New Guinea; PHL=Philippines; WSM=Samoa; SLB=Soloman Islands; LKA=Sri Lanka; THA=Thailand; TON=Tonga; VUT=Vanuatu; VNM=Vietnam; PAK=Pakistan.

Inequality in the Region

Wealth Inequality Not Especially High…

65.0

70.0

75.0

80.0

West

ern

Hem

isp

here

Mid

dle

East

an

d

Cen

tral A

sian

Asi

a a

nd

Paci

fic

Afr

ican

Eu

rop

ean

…But Increasing?

IDN

MYS IND

PHL

THA

KOR

PNG

FJI

CHN

SLB

LKA TON VUT

KHM

LAO MDV

MNG

VNM

NPL BGD

PAK

60

65

70

75

80

85

90

60 65 70 75 80 85 90

20

14

2010

10

Billionaires!

0

50

100

150

200

250

300

350

400

450

0

10

20

30

40

50

60

70

China Russia Germany India United

Kingdom

Japan United

States

(RHS)

2000 2005 2010

What Types of Taxes?

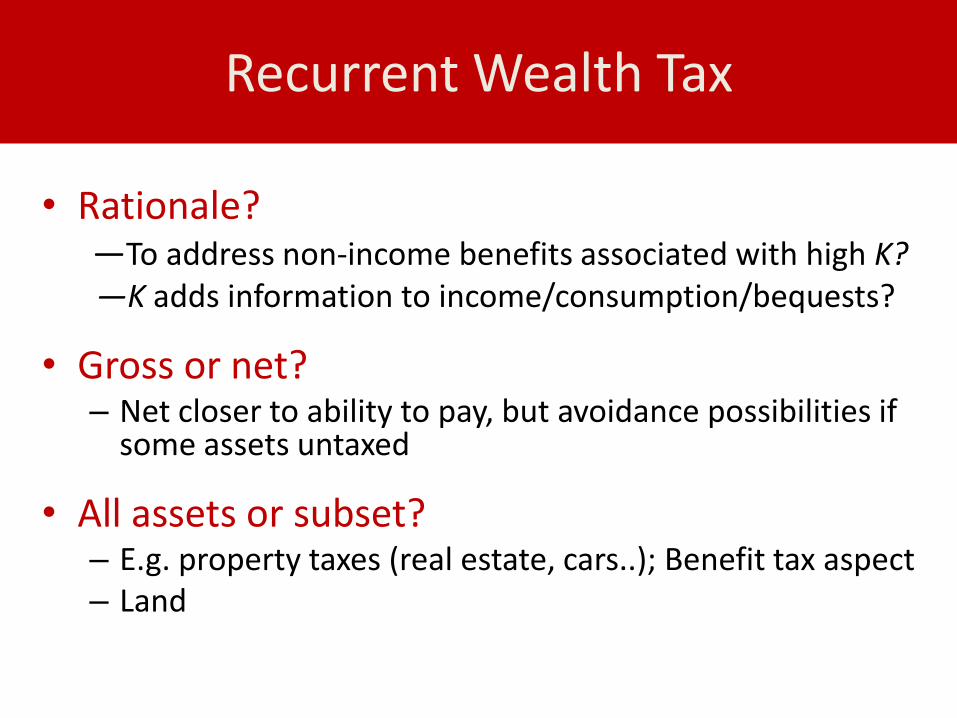

Recurrent Wealth Tax

• Rationale? —To address non-income benefits associated with high K? —K adds information to income/consumption/bequests?

• Gross or net? – Net closer to ability to pay, but avoidance possibilities if

some assets untaxed

• All assets or subset? – E.g. property taxes (real estate, cars..); Benefit tax aspect – Land

Others

Non-recurrent (capital levy)

• Alternative to default; but few successful examples

Non-market transfers

• Estate/accessions, and gift tax as corollary

—motive matters: unintended bequests (up to 100%) vs. warm glow (subsidy?

Market transfers

• Stamp duties, FTT

—Convenient! Stability?

Huge Variation Even in OECD

0

1

2

3

4

5M

EX

ES

TC

ZE

SV

KS

VN

AU

TH

UN

DE

UTU

RN

OR

CH

LF

INP

RT

PO

LS

WE

GR

CN

LDD

NK

NZ

LIT

AIR

LE

SP

CH

EIS

LA

US

BE

LJP

NIS

RK

OR

US

ALU

XC

AN

FR

AG

BR

Rev

enue

Taxes on f inancial and capital transactionsEstate, inheritance and gif t taxesRecurrent taxes on net wealthRecurrent taxes on immovable property

Source: OECD Revenue Statistics

…incl. for Estate, Inheritance and Gift Taxes…

0

5

10

15

20

25

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8E

ST

AU

T

SW

E

TUR

PO

L

ITA

CZE

GR

C

CH

E

DE

U

PR

T

ES

P

DN

K

IRL

LUX

GB

R

NLD

FRA

BE

L

Eff

ectiv

e ta

x ra

te (p

erce

nt)

Tax

reve

nue

(per

cent

of G

DP

)

Estate, inheritance and gif t taxes (lef t scale)Ef fective tax rate (right scale)

Source: Calculations described in October 20i3 Fiscal Monitor

Capital income and/or capital taxes?

Are They Equivalent?

Taxing wealth at rate TK has same effect as taxing capital income at TR if

(1-TK)(1+R)= 1+(1-TR)R

which requires TR = TK(1+R)/R

—e.g. With R = 5%, TK = 1% equivalent to TR = 21%

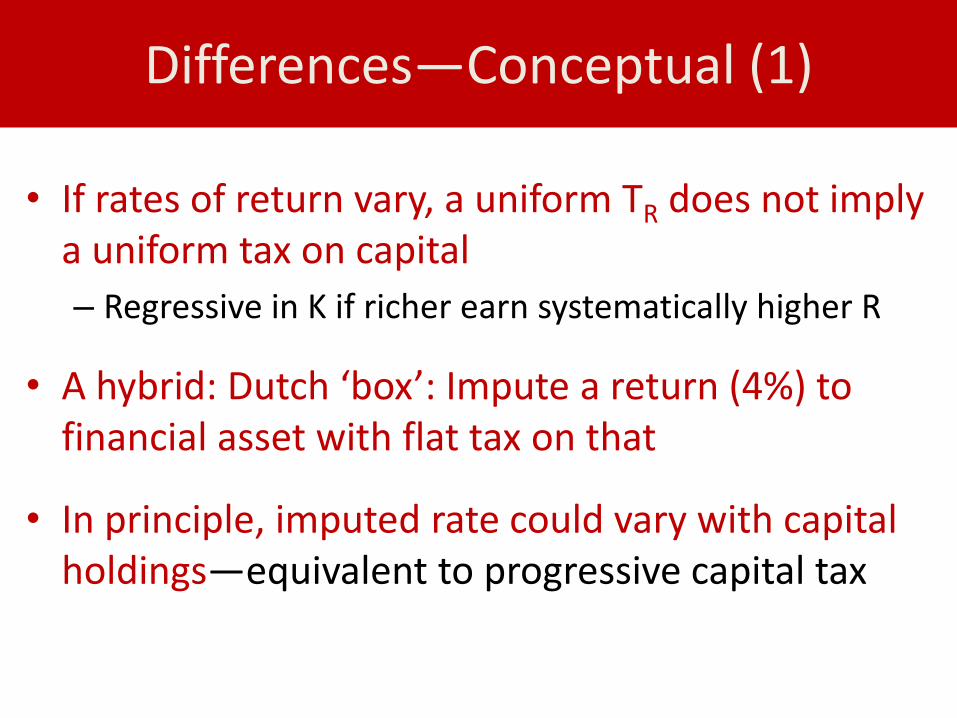

Differences—Conceptual (1)

• If rates of return vary, a uniform TR does not imply a uniform tax on capital

– Regressive in K if richer earn systematically higher R

• A hybrid: Dutch ‘box’: Impute a return (4%) to financial asset with flat tax on that

• In principle, imputed rate could vary with capital holdings—equivalent to progressive capital tax

Differences—Conceptual (2)

• Treatment of losses

– Liability with loss zero/negative tax under tR ; remains positive under tK

A timing issue, but differing volatility and automatic stabilization properties may matter

• Distinguishing capital and labor incomes and values is an issue for both

– Except not present under comprehensive income tax

Differences—Practical (1)

• Withholding/3rd party reporting well developed for at least some forms of capital income

– May, inter alia, reduce resistance (cf. estate tax)?

• Unrealized capital gains problematic for TR…

– Though there are schemes to address this

…less so for TK if asset can be valued (though then could also tax the gain)

Differences—Practical (2)

• Non-cash asset returns—e.g. owner-occupation

– less of an issue for TK if asset can be valued, though in that case could also impute a return

• Has TR proved more robust against exemptions/special treatment than TK?

• Merits in greater familiarity with TR?

Differentiating Across Assets?

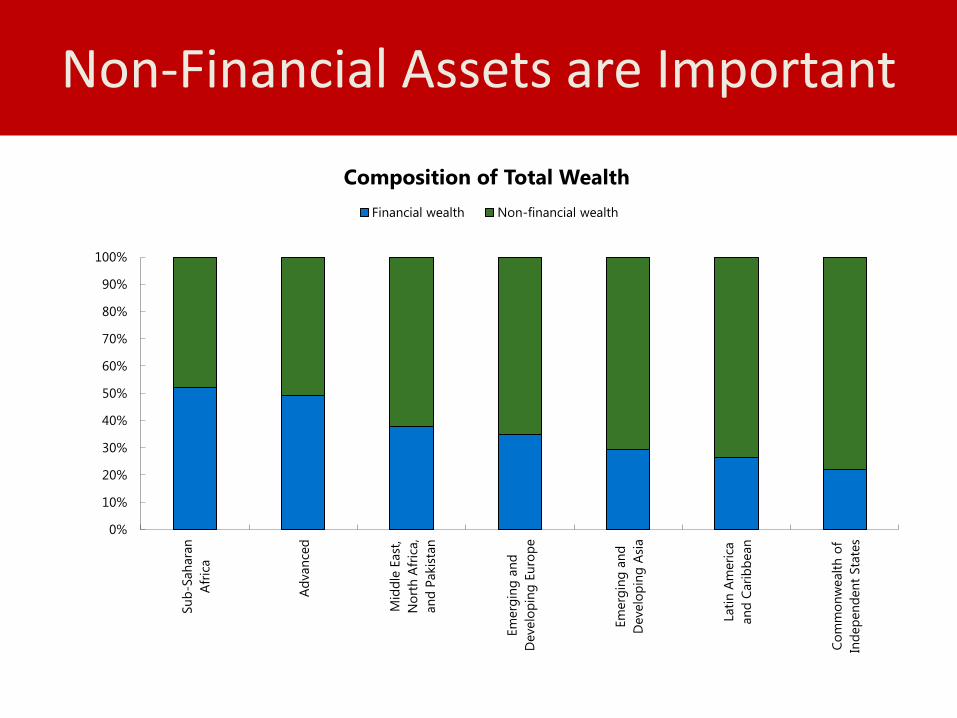

Non-Financial Assets are Important

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Su

b-S

ah

ara

n

Afr

ica

Ad

van

ced

Mid

dle

East

,

No

rth

Afr

ica,

an

d P

akis

tan

Em

erg

ing

an

d

Develo

pin

g E

uro

pe

Em

erg

ing

an

d

Develo

pin

g A

sia

Lati

n A

meri

ca

an

d C

ari

bb

ean

Co

mm

on

wealt

h o

f

Ind

ep

en

den

t Sta

tes

Composition of Total Wealth

Financial wealth Non-financial wealth

• Scope to do more:

• Top of hierarchy of relatively growth-friendly taxes

Recurrent Taxes on Immovable Property

Source: Fiscal Monitor October 2013

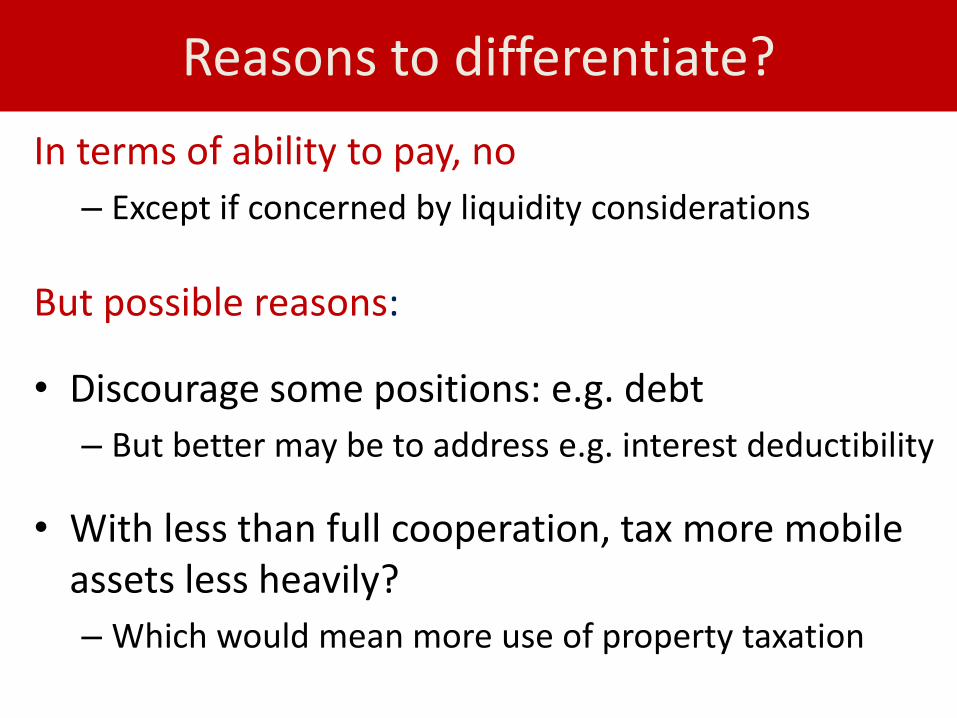

Reasons to differentiate?

In terms of ability to pay, no

– Except if concerned by liquidity considerations

But possible reasons:

• Discourage some positions: e.g. debt

– But better may be to address e.g. interest deductibility

• With less than full cooperation, tax more mobile assets less heavily?

– Which would mean more use of property taxation

With Some Challenges

• Building capacity—cadastre, valuation—can be expensive and time consuming

• Keeping (relative) valuations up to date

• Retain as marginal source local government finance—benefit principle at margin?

• What role for taxes on non-residential real estate?

Tax competition and EOI

International Tax Competition

Much blamed for decay of taxes on capital/capital inc.

• Downward spiral in ‘source’ taxation

• Concealment: $4.5 trillion in havens (Zucman, 2013)

Exchange of information (EOI) can help enforce of residence-based taxes—and world is changing…

– EU Savings Directive, FATCA, AEOI as new global standard

…in an important and positive way

Limits?

• Gains from cooperation—but maybe bigger gains from remaining outside

– Money may flow to non-participating jurisdictions

– Value of being a haven increases as others close

• Personal mobility

– Inversions a warning

– Three times as many US citizens renounced citizenship in 2014 as in 2012