the real cost of injury a workers’ compensation perspective robert m. sklar, bs, crcp january 27,...

Post on 19-Dec-2015

213 views

TRANSCRIPT

The Real Cost of InjuryA Workers’ Compensation Perspective

Robert M. Sklar, BS, CRCPJanuary 27, 2010

Insight. In Touch.

It’s after Lunch, I came for a Nap!

• Workplace Injury Claim

• How does the claim evolve – good vs. bad

• What does Safety have to do with it & why should I care?

• What are the financial drivers

• What impact can I have on claims

• What can I learn from claims data

• What priorities should I have based on my claims data

But Wait!

• I am just the Safety Person. Does

this really matter?

• What can I Do?

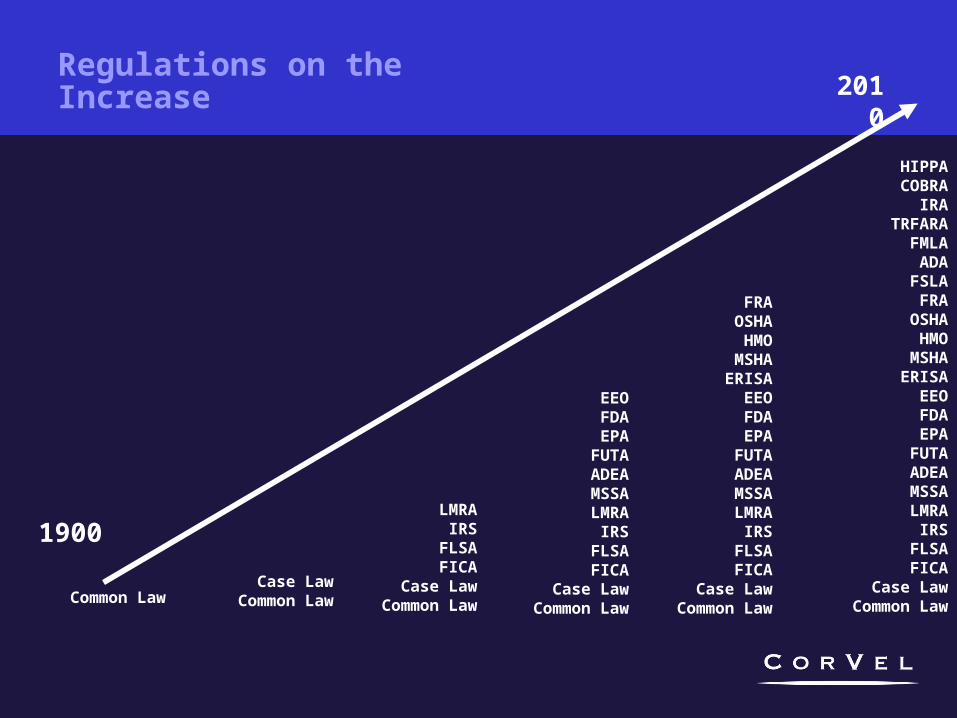

Regulations on the Increase

HIPPACOBRA

IRATRFARA

FMLAADA

FSLAFRA

OSHAHMO

MSHAERISA

EEOFDAEPA

FUTAADEAMSSALMRA

IRSFLSAFICA

Case LawCommon Law

FRAOSHAHMO

MSHAERISA

EEOFDAEPA

FUTAADEAMSSALMRA

IRSFLSAFICA

Case LawCommon Law

EEOFDAEPA

FUTAADEAMSSALMRA

IRSFLSAFICA

Case LawCommon

Law

LMRAIRS

FLSAFICA

Case LawCommon

Law

Case LawCommon LawCommon Law

1900

2010

Safety

• Identifying hazardous working conditions – develops strategies to eliminate or mitigate the identified hazard.

• Provides accident injury and illness profiles and data

• Identify accident trends, sources, and factors that

contribute to occupational injuries and illnesses

• Safety training programs:– Workplace violence Driving

– Ergonomics Lifting & Moving

– LOTO HazCom/HazWopper

What does Safety have to do with Claims?

Everything!

Claims are the result of failure. Management of Claims is managing

failure! Failure to act in a Safe Manner Failure to maintain Proper

Housekeeping Failure to use proper PPE Failure to Drive or Work Safely. Failure to adhere to Safety Policies

Workers’ Compensation - Defined

• A law in each U.S. state that requires employers to

assume obligation for employee injuries and some

occupational illnesses, as defined, that “arise out of

and in the course of employment.”

• Such obligation applies regardless of fault. The

obligation can be satisfied by an insurance policy or

by an approved self-insurance plan.

Workers’ Compensation

• Medical Treatment

• Payment of lost wages

• Payment for medical expenses

• Return to Work Program

• Vocational / Occupational Rehab

• Legal Expenses

• Psych Expenses

• Permanent Disabilities

• Claim Settlement

• Lifetime claims

Let’s talk about Claims

• Where does a claim start?

• Employer Knowledge– Personally Reported

– Verbal or Written

– Evidence of Medical Treatment• “Oh yeah, he did say he got hurt, but never told me it

was work related….” “So I never reported it.”

– Sometimes your first notice is a Petition or legal

action.

Definitions– DOL = Date of Loss (Date of Injury)– LT = Lost Time - When more than x days off

work– TTD = Temporary Total Disability

• The temporary wages paid during time off (66 2/3)• PLUS any medical bills (statutory coverage)

– TPD – Temporary Partial Disability• Can work limited duty but not full time• Partial Benefits are paid to supplement wages

– MMI = Maximum Medical Improvement• The doctor deems your as well as your going to get• No further improvement is ever expected

Definitions

– RTW = Return to work

• The employer can accommodate the employee’s

restrictions and provide some form of job to the

employee (can be temporary or permanent)

– AWW = 13/26/52 Week Average Weekly Wage

• The employee’s gross salary for 52 weeks prior to

the injury is added and then divided by 52 to derive

the average weekly wage.

Definitions

• IW – Injured Worker, Claimant,

Applicant– EE – Employee

– ER – Employer

• DC – Defense Counsel

• AA – Applicants Counsel

How does a claim start?• You've done it a thousand times.• It comes naturally to you. • You know what you're doing.• I don’t need to worry about that.• I can take care of myself.• Etc.• Etc.• Etc.

NOTHING CAN GO WRONG, RIGHT?

Think Again.

Injuries can be Acute or Cumulative

Acute Injury / Traumatic Injury?

1. A traumatic injury is a wound or other condition of the body caused by external force, including stress or strain.

2. The injury must occur at a specific time and place, and it must affect a specific part(s) or function(s) of the body

3. Must be caused by a specific event or incident, or a series of events or incidents, within a single day or work shift

+ =

Cumulative Injury or Occupational Disease?

1. An Occupational Disease is a condition produced by the work environment over a period longer than one work day or shift.

2. The length of exposure, not the cause of the injury or the medical condition which results, determines whether an injury is traumatic or occupational.

Examples: The condition may result from infection, repeated stress or strain, or repeated exposure to toxins, poisons, fumes or other continuing conditions of the work environment, carpal tunnel from daily use of computer keyboard, etc.

How does a claim start?

• Employer Knowledge.– Once the employer has knowledge than a claims

MUST be filed with your insurance carrier / TPA.• Even if you think it is False / Fraudulent

• Employer may be aware of accident

– Local Manager or Supervisor

– Some States – Treating Physician can initiate a claim

by filing a treatment form.• Late reports can result in penalties against the

employer/carrier. Think OSHA Penalties as well.

Benefits of early claim notice

• Provides baseline / time line for claim

investigation

• Documents incident facts while they are fresh– Witnesses

– Symptoms

– Recovery potential

– Identification of Red Flags

– Direct Care

Investigation of Claim

• Employer and Insurance Carrier investigate claim– Contact Employee, Supervisor, Witnesses, review medical

reports, policies, etc.

• Adjuster from Insurance Carrier/TPA may call and

take recorded statements (Not all States)

• Determine if RED Flags exist?

• Make a decision to Accept, Delay, Deny or take

other action.– Often anything other than accept Litigation.

Claim Process – Red Flags

– Horseplay

– Unauthorized activities

– Assaults

– Timing

– Delayed reporting

– Conflicting evidence

– Outside activities

– Nature of injury

– Treatment

Suspect Fraud?

• Refer to SIU

• Refer to State Insurance Commission

Usually want to deny the claim and let

the Applicant prove their claim in court.

Prepare for Litigation – you need to

defend your denial

Directing Care

• Established relationship with Occupational Medicine

Clinics

• Some states you can tell the worker where to treat

• Medical Management– PPO

– MCO

– MPN

• Workers will try to treat with friendly doctors– Keep out of work

– Delay medical reports

Directing Care

• Options against malingerers– Independent Medical Exam (IME)

– Nurse Case Management

– Compensability review

• Current condition denial

• Partial denial

• Do not authorize further treatment

– Legal review

The Workers Comp Claims Process

• Three point contact by adjuster:– Contacts employer– Contacts “Gate Keeper” Doctor– Contacts employee

• Administration of claim– Medical payments, drug payments, rehab etc

• Case Management, Litigation, Claim Determination

Compensability Decision

• Injury vs. Occupational Disease– AOE/COE

• Pre-existing, Major Contributing Cause

• Presumptions

• Operational / Employment issues – WC is not a

dumping ground for bad employees

• HR Issues

• LP Issues

• Failed Drug Screen???

Make sure to

SHARE information

Make sure to

SHARE information

Accept Claim

• You pay for everything

• Benefits are issued based on State Specific

criteria– Loss Time Payments are generally 66 2/3% for

Average pre-injury wages

– Light duty needs to pay at the pre-injury rate

– Provide treatment, move case toward closure

Deny the Claim

• Litigation

• Go Away

• Some claims can be denied even after initial

treatment– May still have some payments on the claim

• Litigation adds 30-40% to the value of the claim

• Improper Denials – Recent RICO Case

Retaliation Claims

• Workers will get hurt

• Workers will get terminated

• Workers will hire attorneys

• Workers will allege that their termination was a

result of filing a Work Comp Claim.

THE BURDON OF PROOF WILL NOW BE ON THE

COMPANY TO PROVE OTHERWISE

Return to Work / TAW / Modified Duty

• Goal of early and safe Return-to-Work– Return the worker to suitable employment with little or

no loss of earnings

– Employer’s Responsibilities• Contact worker ASAP after accident

• Maintain the communication

• Attempt to provide suitable work

• Provide all information to Adjuster

– Benefits can be terminated if you Offer and employee refuses

work

Return to Work

• Suitable employment• Productive• Available• Medically approved / appropriate

– Within worker’s physical ability– Within worker’s skill set– Will not slow recovery

• Not demeaning• Restores pre-injury earnings close as possible• Temporary or Permanent (ADA)

Safety Violations

• Some states allow for the reduction of claim

benefits or even denial if the Injured Worker

violated safety policies:– Must have known about them (training)

– Employer makes reasonable efforts to enforce

– Employee or Employer intentionally violated rule

– Injury is proximate cause to violation

• This is where your compliance / Safety Awareness

Programs can be vital.– Can you show proof of training?

Safety Violations

• CA +/- up to 50%

• GA up to 100% reduction (denial)

• FL up to 25% reduction

• OH Penalties against Employer up to 50% +

$ 50K

• NC +/- 10%

• MO 25-50% reduction

What does the claim data tell us?

• What is driving the costs of claims?

• Frequency?

• Medical Costs?

• Severity?

• Location?

• Morale?

• Seasonal?

Why is Looking at the Most Expensive Claims Important?

• Traditional approaches to workplace loss prevention and safety

focused on decreasing the number (frequency) of accidents to

reduce the costs of WC. (OSHA Likes This)

• Data from Insurers and Company Management indicates that more

effective prevention and cost control might come from identifying

and preventing those factors (costs) that turn an average claim into

one of the most costly.

Why is Looking at the Most Expensive Claims Important?National Data

Least Costly85%

Most Costly15%

All WC Claims Least Costly15%

Most Costly85%

Claims Costs

Insurer data indicates that 15% of WC Claims make up 85% of the total Comp. Costs

Most Costly Claim Trends

• Most of the 15% had noted

Surgery Issues:

– Multiple Surgeries

– Failed Surgeries

– Predominance of Back

Surgery

• Many noted Psychological

Elements:

– Stress

– Anxiety

– Suicide

– Chronic Pain Syndrome

– Insomnia

– Psych

– ED

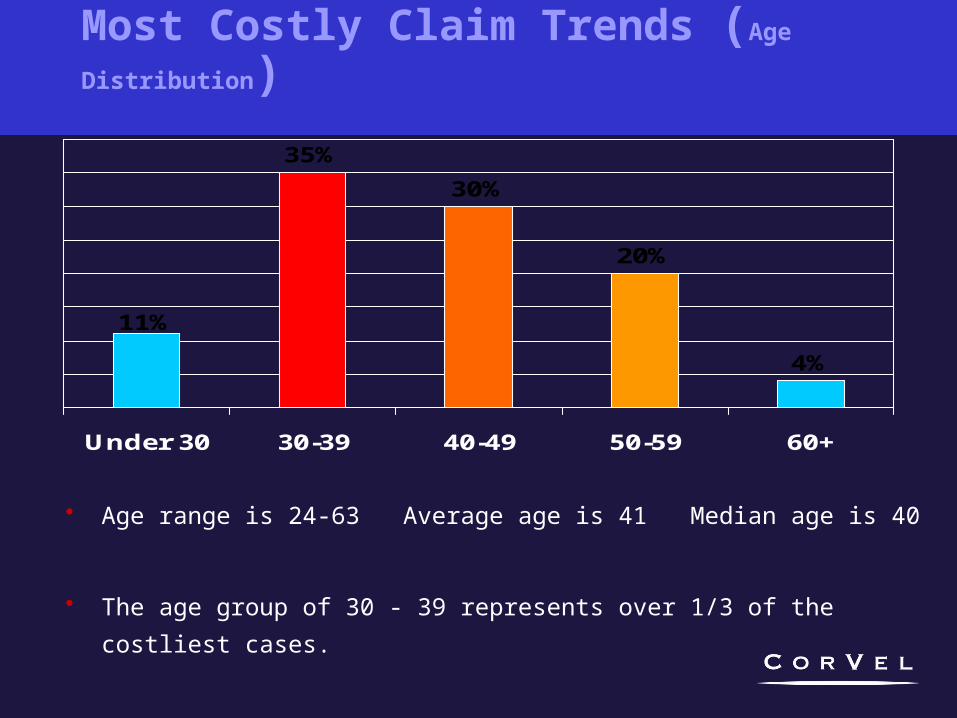

Most Costly Claim Trends (Age Distribution)

30%

20%

4%

11%

35%

Under 30 30-39 40-49 50-59 60+

• Age range is 24-63 Average age is 41 Median age is 40

• The age group of 30 - 39 represents over 1/3 of the costliest cases.

Gender Comparison Frequency (Fx) and Cost ($)

66%

78%

22%

34%37%

63%

All Claims Fx

All Claims $

Most CostlyFx & $

Female

Male

Fx = Frequency Analysis $ = Cost Analysis

Typical Claim Financials

Paid Reserve Total IncMedical 155,000 276,000 431,000 Indemnity 81,256 124,777 206,033 Expenses 26,210 21,080 47,290 Recovery - Other 8 8

Total 262,474 421,857 684,331

Where does the $$ Go?Cost Data

Benefit Payments

18%

Settlements41%

Other2%

Employer Legal1%

Medical 38%

Most Costly The Role of Surgery

2 Sx26%(14)

1 Sx51%(27)

5 Sx4%(2)

4 Sx8%(4)

3 Sx11%(6)

Most Costly and Surgery

Extremities12%

Back62%

Internal6%

Carpal Tunnel

6%

Head4%

Amputation10%

Most Costly: Psychological Elements

• 46% claims had some “psych” issues alleged.

• Post Traumatic Stress

• Anxiety

• Insomnia

• Depression

• Low Self-Esteem

• Suicidal Thoughts

• Hopelessness

Most Costly and Dispute Activity

• 60% of the claimants had some kind of dispute between

themselves and the insurer/employer.

• The NOC (Notice of Controversy) serves as notice that either

benefits or other elements of the claim are in disputed pending

WCB resolution.. There are many things that can be disputed:

– Causation - Service - Mileage

– Treatment - Doctor’s Services

– Supplies

– Diagnosis - Etc.

Why Accidents Happen

0%10%20%30%40%50%60%70%80%

UnsafeActs

UnsafeConditions

• Unsafe Behaviors/Acts = 80% of accidents

• Unsafe Conditions = 20%

• Inspections (Self & OSHA) – Usually are overly focused

on conditions– Include safe and unsafe

behaviors in your checklist

• Watch People Work!

Underlying Causes of Most Workplace Injuries• #1 - Management

Behavior - nearly every

unsafe action and condition

can be traced back to a

lack of adequate safety

management / Supervision

(enforcement)

• #2 - Employee Behavior -

is often a reflection of

safety training and

enforcement

• Dupont Chemicals, • Congress 1994, Jeff Wilson,

manager, says when an injury occurs, instead of the typical reaction:– “What could that

person have been thinking?”

the better response is:– “Where did we (the

company) fail?”

Other Prevention Techniques“Before the Accident”

• Hiring Practices

- Drug screening

- Prior employers

- MVR’s

- Competency tests

- Criminal records

- Prior Claims

• Authority to STOP if danger

is imminent

- Employees need this to

work safely

• Health

- Helps keep employees alert and focused

- Eat well balanced meals

- Avoid alcohol, drugs & tobacco

• Exercise

- Body reacts better

- Reduces stress

- Less likely to be injured

Loss Control: Claims Mitigation

Communication with Employees• This is where most employers fall short

– Do you have the ability to track and prove training?• Serious and willful violations +/- $$

• Put yourself in the injured employee’s position:– Injured on the job– Alone, in pain, disabled, at hospital/home– No flowers, no get well cards, no calls of concern from employer– Resentment builds– TV attorneys care more than you!

• Employees less likely to seek a lawyer with a concerned employer

Are you paying the IW to watch this?

Or This?

Loss Control: Claims Mitigation• Communicate with Medical Provider

– Learn if they were told about the accident/injury

– Compare notes!• Return to Work/Light Duty Program

– Message to injured employee that you care– Screens out fraud cases– Message to other employees – Reduces Indemnity pay (for time off)

• Reduces overall claim payment– Insurance carrier can stop payments if

employee refuses to return to work

Old School

• “as in many workplaces, safety issues — like environmental issues — were seen as a nuisance, a drain on profits and a drag on production. Safety was delegated to safety inspectors, who were routinely ignored.”

• The larger problem is in the executive suite. The CEO is not going to fall off the staging or have a forklift mash him into the wall. He’s got a safety guy to take care of all that stuff, and mostly what he wants to hear from the safety guy is nothing. Don’t bother me, buddy, I’m working on cost containment, quality control, financing, CEO stuff, stuff that makes us money. Safety? Not my job.

http://thechronicleherald.ca/NovaScotian/1113824.html

10-K: DOLLAR GENERAL CORP, 3/24/09

“Our increased sales levels favorably impacted SG&A, as a

percentage of sales, in addition to a reduction in workers'

compensation expense, resulting from safety initiatives

implemented over the last several years,...”

“Our third priority is leveraging process improvements…”

“Examples of cost reduction initiatives in 2008 include…

reduction of workers compensation expense through a

focus on safety,…”

10-K: QUALITY DISTRIBUTION INC. 3/13/09

• “We have made safety the main focus of

our organization. We implemented several

comprehensive process improvement

programs to further identify and implement

opportunities for sustainable safety

improvement. Tangible results of this focus

have already manifested themselves in a

substantial decrease in preventable events

and claim frequency.”

Safety and What it means to Sr. Mgmt.

• Becoming ever more important

• Increase in Sr. Management Awareness

• They are now starting to realize that Safety

translates to decrease in expenses which

means they can add to the bottom line.

• What’s the ROI?

Let’s make it evident! Safety Pays

• Pay for your Safety Programs with Saved Dollars– Back Claims:

• $ 33,000 average expense

– Store with 12% Profit Margin• $ 275,000 In Sales just for the claim

• + Overtime

• + Lost Productivity

• + Hiring and Training Costs

• $ 577,500 savings by preventing 1 back claim!

Cost of Claim Matrix

Cost of Claim 2% 4% 5% 8% 10% 12% 15%

2,500

125,000

62,500

50,000

31,250

25,000

20,833

16,667

5,000

250,000

125,000

100,000

62,500

50,000

41,667

33,333

10,000

500,000

250,000

200,000

125,000

100,000

83,333

66,667

25,000

1,250,000

625,000

500,000

312,500

250,000

208,333

166,667

50,000

2,500,000

1,250,000

1,000,000

625,000

500,000

416,667

333,333

75,000

3,750,000

1,875,000

1,500,000

937,500

750,000

625,000

500,000

100,000

5,000,000

2,500,000

2,000,000

1,250,000

1,000,000

833,333

666,667

250,000

12,500,000

6,250,000

5,000,000

3,125,000

2,500,000

2,083,333

1,666,667

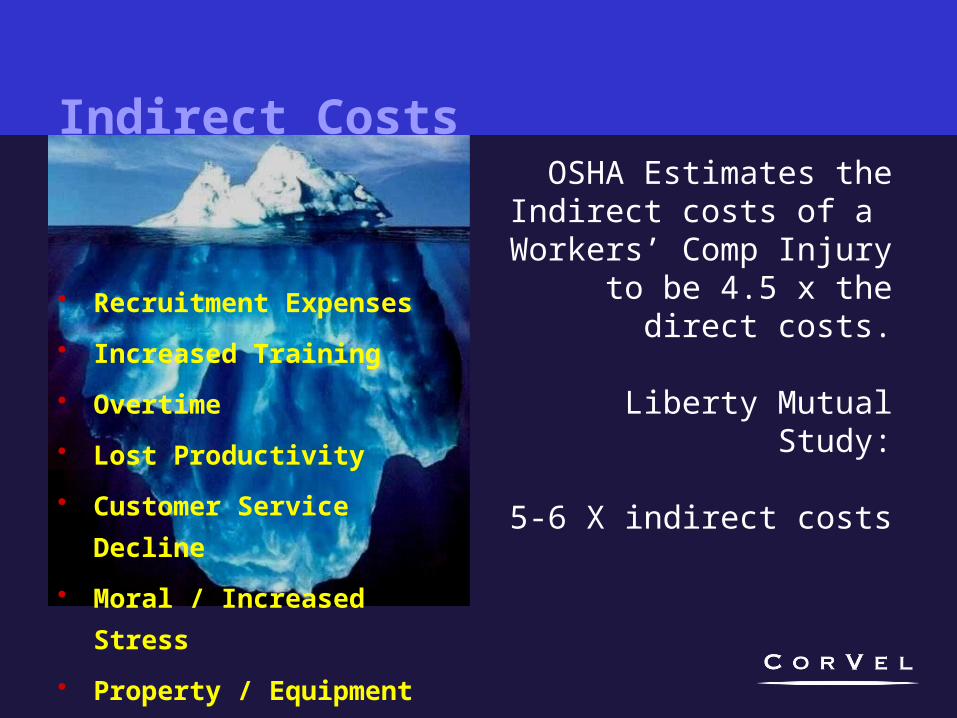

Indirect Costs

• Recruitment Expenses

• Increased Training

• Overtime

• Lost Productivity

• Customer Service Decline

• Moral / Increased Stress

• Property / Equipment Dmg.

OSHA Estimates the Indirect costs of a

Workers’ Comp Injury to be 4.5 x the direct

costs.

Liberty Mutual Study:

5-6 X indirect costs

Indirect Cost Calculation

If Direct Cost Is

Use ThisMultiplier

$0 - $2,999 4.5

$3,000 - $4,999 1.6

$5,000 - $9,999 1.2

$10,000 or more 1.1

2,500 * 4.5 = 11,250 + 2,500 = 13,750 /

8% = $ 171,875

75,000 * 1.1 = 82,500 + 75,000 =

157,500 / 8% = $ 2M

http://www.mwecc.com/Files/SIB/Stop%20Looking%20The%20Wrong%20Way%20December_03.pdf

Cost of Claim Matrix + IndirectCost of Claim 2% 4% 5% 8% 10% 12% 15%

2,500

125,000

687,500

62,500

50,000

31,250

25,000

20,833

16,667

5,000

250,000

125,000

100,000

62,500

50,000

41,667

33,333

10,000

500,000

250,000

200,000

125,000

100,000

83,333

66,667

25,000

1,250,000

625,000

500,0

00 1,050,

000

312,500

250,000

208,333

166,667

50,000

2,500,000

1,250,000

1,000,000

625,000

500,000

416,667

333,333

75,000

3,750,000

1,875,000

1,500,000

937,500

750,000

625,000

500,000

100,000

5,000,000

2,500,000

2,000,000

1,250,000

1,000,000

2,100,000

833,333

666,667

250,000

12,500,000

6,250,000

5,000,000

3,125,000

2,500,000

2,083,333

1,666,667