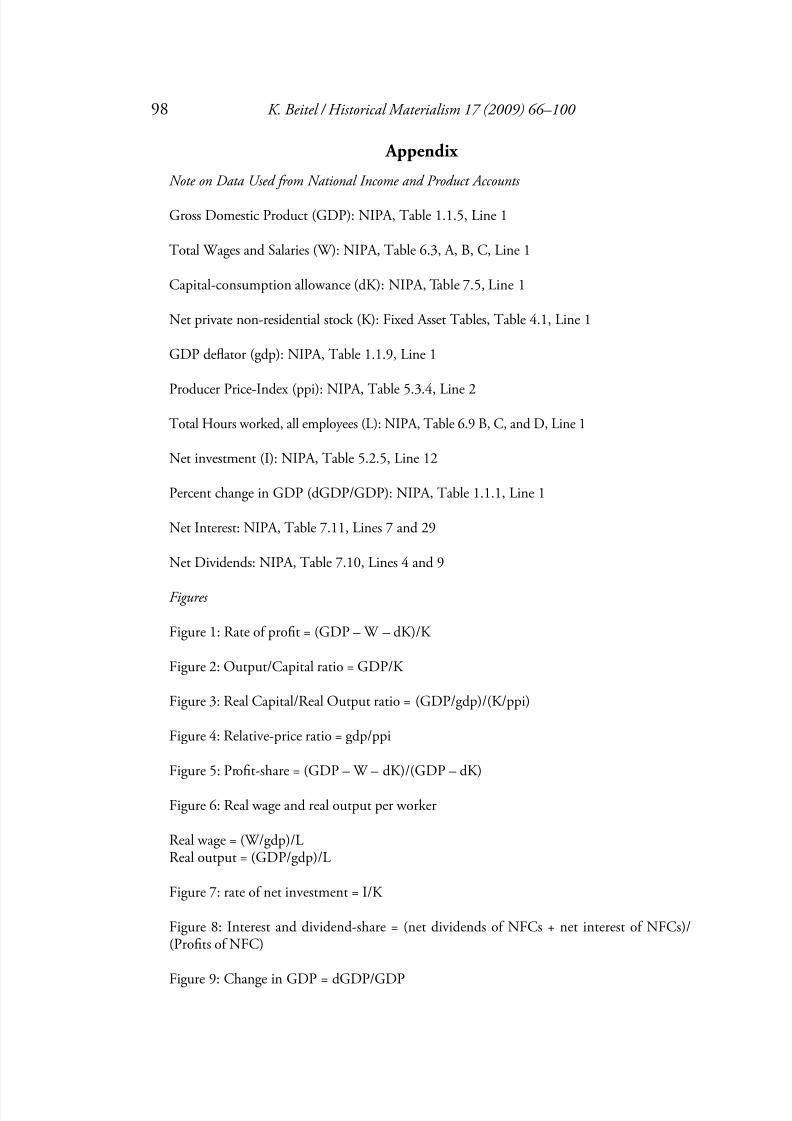

the rate of profit and the problem of stagnant

TRANSCRIPT

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 1/36

Historical Materialism 17 (2009) 66–100 brill.nl/hima

Te Rate of Prot and the Problem of StagnantInvestment: A Structural Analysis of Barriers to

Accumulation and the Spectre of Protracted Crisis *

Karl Beitel American Federation of eachers

Abstract Tis paper situates the subprime crisis in the context of the performance of the Americaneconomy over the last twenty-ve years. Te restructuring of the US economy is brieyreviewed, followed by an examination of some of the contradictions of the neoliberal model.Particular emphasis is placed on understanding the reasons behind stagnant investment, andhow the US nance-led accumulation-régime has become dependent upon, and threatenedby, credit-creation delinked from the nancing of xed-capital formation. I argue that while

the defeat of the remnants of the New-Deal/Civil-Rights liberal-democratic coalition hasprovided the political context for the bold re-assertion of the prerogatives of capitalist owners,the neoliberal model has not provided a path out of problems of stagnation and growing debt-dependency that presently plague the US (and global) economy. Further, I argue that evidencesuggests that the post-1982 restoration of protability that underpinned the relativeimprovement of US economic performance has peaked, and that compelling historical andtheoretical reasons exist to expect that the prot-rate will decline in the coming decade. Tis

will introduce additional stresses on the current debt-structure of the US economy, triggeringa period of prolonged crisis and economic dislocation. Te conclusion is that the US economyfaces the spectre of a protracted crisis associated with the reassertion of the falling rate ofprot.

Keywordsnancial crisis, subprime crisis, Marxist theory of the prot rate, long waves, nancialisation

* Te author would like to thank anonymous reviewers for their helpful comments on anearlier version of this paper. Te views expressed here are those of the author, and do not reectthe positions of the American Federation of eachers.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 2/36

K. Beitel / Historical Materialism 17 (2009) 66–100 67

Introduction

Tis essay situates the recent nancial crisis in a review of the performanceof the American economy over the last twenty-ve years. Factors governingmovements in the rate of prot are reviewed, followed by an examination ofsome of the contradictions of the US neoliberal model that developed overthe 1982–2006 period. Particular emphasis is placed on understanding howthe nance-led accumulation-régime is both dependent upon, andpotentially threatened by, the enormous growth of debt that has characterisedthe developmental trajectory of US capitalism over the last three decades.

Te assessment offered is mixed. It is impossible to deny that the yearssince 1982 have seen signicant improvement in US economic performancealong a range of key indicators. Productivity-growth has been restored tolevels approaching those of the Golden Age of the post-WWII period.echnological innovation and new product-applications have re-established

US leadership – or at very least parity – with other major capitalist economiesin cutting-edge industrial sectors such as computing and information-technology. Te vast network of US multinationals continues to provide thestructural underpinnings of the dollar’s role as the world’s pre-eminentinternational reserve-currency, and Wall Street still reigns supreme in the

world of international nance. Domestically, US capital today presides overa largely quiescent and demobilised working class. Union-density is at itslowest rate in over seventy years, and few restrictions exist upon capital’sability to hire and re workers at will. America’s exible labour-markets arethe envy of many European business-leaders, and are regularly touted,however incorrectly, as the reason for higher rates of US productivity-growthover the last decade. Nor has the massive US trade-decit as yet induced acrisis in the dollar, due to the sheer size of the American economy and therole of the US household as global consumer of last resort. Most signicantly,the US prot-rate underwent a steady and signicant improvement thatbegan in 1982 and continued unabated through 1997. Tis indicates thatUS capital was able to partially overcome the supply-side barriers toprotability that undermined the coherence of the Keynesian-Fordistrégime.

At the same time, the improvement in protability has not translated intoa corollary increase in the level of private investment-demand. In the absenceof the restoration of a higher rate of accumulation, insuring an adequate rateof growth of effective demand has become dependent on borrowing by thegovernmental and household sectors to nance current consumption. As aresult, debt-obligations have risen at a rate that far exceeds the growth of real

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 3/36

68 K. Beitel / Historical Materialism 17 (2009) 66–100

income or the rate of accumulation. Tis was the source of the structuralvulnerability that erupted in the subprime crisis. Te short-to-medium term

fate of the US and global economy is bound to the ability of the monetaryauthorities to engineer a partial unwinding of over-leveraged investment-positions and ‘controlled’ destruction of nancial claims. Over the longerterm, I argue that rate of prot is the critical variable regulating system-performance. Reduced to its essentials, the argument is that the ability tomanage the crisis depends upon maintaining a stable or rising rate of returnon tangible capital-investments. Te problem is that the favourable prot-rate conjuncture of the last two decades is unlikely to persist. Te conclusionis that there are reasonable grounds to suppose that the US economy is on the

precipice of a protracted crisis taking the form of nancial-asset deation (inreal terms) and, over the longer term, a reassertion of a falling rate of protand spiralling ination. Falling protability will, in turn, require a prolongedperiod of debt and equity-deation to correct the structural imbalances thathave built up over the course of the prior prot-rate upswing, with anuncertain long-term outcome.

Te paper is organised as follows. In the rst section, I review historicaldata on movements in the rate of prot since 1947 to place the post-1982recovery in some historical perspective. I discuss and subject to critique the

work of Robert Brenner in order to situate and distinguish the analysis thatfollows. Te prot-rate is decomposed and its various determining factorsare analysed to isolate various causal effects that explain periods of falling andrising protability in the post-WWII period. I then turn to a discussion ofsome of the internal contradictions of this debt-fuelled régime. Te paperconcludes with some comments on the future of neoliberalism and why Ibelieve a renewed period of crisis is inevitable given US capitalism’s currenttrajectory.

Explaining the prot recovery

Figure 1 shows the rate of prot in the US economy over the period 1947–2007. Following standard practice, the rate is calculated by subtracting total

wages and salary-compensation from net national income and then dividingthe difference by the net capital-stock valued at replacement-cost. Between1947 and 1959 the prot-rate shows evidence of a slight downward trend.Protability then boomed between 1960 and 1966, driven in part by US entryinto the Vietnam War in what would prove to be the nal hurrah of theKeynesian-Fordist era. In 1967, the rate of prot entered a period of decline

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 4/36

K. Beitel / Historical Materialism 17 (2009) 66–100 69

that, by the early 1980s, had plunged the US and global economy intotheir deepest economic recession since the Great Depression. Contrary toexpectations, however, the contraction of 1980–2 marked a turning point inthe fortunes of US capital. Te prot-rate rose sharply between 1982 and1986, and would continue to improve through 1995. Te prot-rate fellbetween 1996 and 2000, largely due to a rise in the wage-share of nationalincome brought about by low rates of unemployment during the dot.comboom. Tis decline has been reversed in the years since, although there isevidence of a renewed reassertion of a downward trend. I will return to this

point at some length below.Much recent debate over the causes of the protability-crisis and the

subsequent performance of the US economy in the post-1979 period has beenframed by the publication of Robert Brenner’s 1998 book-length essay ‘TeEconomics of Global urbulence’ in theNew Left Review .1 Brenner’s workspurred a welcome renewal of interest in the macro-dynamics of accumulationand crisis amongst radical political economists, despite the signicant theoreticaland empirical problems with his account. Given the extensive response his work

1. Brenner 1998.

Source: National Income and Product Accounts, able 1.1.5, able 6.3; Net Fixed Assets, able 4.1

Figure 1. US rate of prot, 1997–2007

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 5/36

70 K. Beitel / Historical Materialism 17 (2009) 66–100

has received, I will here summarise Brenner’s account to draw out the contrast with the approach developed below that, despite some supercial points of

overlap, is founded on different methodical and theoretical presuppositions.Reduced to its essentials, Brenner’s argument is that the decline in the

rate of prot that began in 1967 was the result of the entry of newer, lower-cost producers that placed a downward pressure on prices and hence theprots of established rms – particularly those in the core-industries of theUS Fordist economy. As Europe and Japan recovered from WWII and beganto rebuild their productive base, US producers in particular found themselvescompeting against lower-cost and, in many cases, more technologicallyeffi cient competitors. Because these new entrants into the global

manufacturing markets set output-prices at levels that would allow them torealise the prevailing average rate of prot, this lowered the prot-marginsof older, less effi cient rms. However, rather than shutting down thesecostlier, less technologically effi cient plants, US rms and older producers inEurope kept existing plants in operation. Brenner suggests several reasonsfor this refusal to exit from existing branches of production in which rmshad large capital-investments – the development of sector-specictechnological expertise, the formation of extensive networks of business-relations and customer-contacts that could not be transferred to new

branches of production, the accumulation of ‘goodwill’ and reputation, andthe fact that rms had already recovered the value of older stocks throughdepreciation. Tis last factor is highly signicant in Brenner’s account. Itmeant that, even as prices fell, producers that had already depreciated thevalue of xed stocks could continue to realise at least the average rate ofprot on their circulating variable and constant capital. For all these reasons,older capitals refused to readily withdraw from existing branches ofproduction. Te result was a condition of ‘too much entry and not enoughexit’ resulting in overcompetition and overcapacity that placed a sustained

downward pressure on prices and prots.Te protability-crisis is thus explained as the result of excessivecompetition and a failure of the market to effectively co-ordinate andorchestrate suffi cient exit from overinvested sectors leading to a fall in therate of prot. Lower rates of prot in turn discouraged new investment. Tislowered the rate of productivity-growth and placed additional pressures onrms’ prot-margins. Te eventual result was a generalised crisis characterisedby plummeting investment, rising unemployment, and pervasive overcapacityand overproduction throughout the productive circuit.

In subsequent writings, Brenner has sought (unsuccessfully in my view)to reconcile his 1998 account of the fall in the (global) rate of prot with the

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 6/36

K. Beitel / Historical Materialism 17 (2009) 66–100 71

apparent paradox of the post-1982 recovery in the prot-rate that co-exists with a declining trend in the rate of net investment. Without making any

overt declaration to this effect, Brenner essentially shifts from a supply-sideapproach to a demand-based explanation rooted in an insuffi cient level ofeffective demand. In various contributions, Brenner locates the origins ofpersistent stagnation in scal monetary policies that have failed to providesuffi cient economic stimulus, wage-repression leading to a chronic problemof insuffi cient growth of demand, and still ongoing problems of overcapacityin global manufacturing that acts as a barrier to investment – although thislatter relationship is never fully explained, but apparently is due to thepersistence of insuffi cient exit that continues to result in overinvestment. 2

Brenner’s work has undergone extensive critique.3

As such, I will not hererehearse the full litany of aws pointed out by his critics but will connemyself to issues most relevant to distinguishing his account from the analysisthat follows. For one, Brenner asserts that lower-cost entrants set prices atlevels that will earn them the prevailing average rate of prot. Tis is a curiousassertion, given that the entire motive driving cost-reducing technologicalinnovation is to allow those deploying the new production-methods toachieve a higher rate of prot by undercutting their less effi cient rivals. omotivate his argument, Brenner must impose the assumption that innovating

rms set prices at levels that realise the prevailing average prot-rate. At nopoint does Brenner demonstrate that this assumption corresponds to theactual pricing behaviour of rms. More problematic still, as Zacharias hasshown, technological change along lines indicated by Benner can just aseasily cause the prot-rate to rise. It all depends on the level at whichinnovating rms set prices.4

Further, if Brenner was correct in his assumptions regarding the pricingpractices of rms, it is easy to show that, for a given rate of cost-reducingtechnological change, the rate of prot would converge over time to a

constant level, and that the faster the rate of cost-reducing technical change,the lower would be the prot-rate towards which the system eventuallyconverges. Brenner’s analytical frame thus encounters problems in explaininghow periods of accelerated technical change – such as what occurred afterthe Volcker shock of the early 1980s – can correspond to a rising prot-rate.

2. Brenner 2000, 2001, 2004.3. Of particular note, see Shaikh 1999; Duménil and Levy 2002b; Fine, Lapavitas, and

Milonakis 1999; Freeman 1999; and Zacharias 2002.

4. Zacharias 2002. If rms lower prices, these will reduce the cost of inputs; hence the effecton the overall aggregate rate of prot is unclear.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 7/36

72 K. Beitel / Historical Materialism 17 (2009) 66–100

Tis explains the highly ad hoc and non-systemic character of Brenner’ssubsequent accounts of the post-1982 period.

Second, there are signicant problems with the timing in Brenner’s linkingof intensied international competition to downward pressure on pricesand prots. As Brenner notes, increased international pressure to expandmarkets, by placing pressure on output prices, should lead to either a fall inprices or, at the very least, should cause the rate of annual ination to decline(deation). Tis follows directly from Brenner’s assertion that the entry oflower-cost producers will undercut the pricing power of established rmsand impose a downward pressure on prots via falling prices. Te problemis that the decline in the prot-rate after 1967 is correlated with a higher,

not lower, ination-rate. Te only way the phenomenon of higher inationcan be reconciled with Brenner’s formulation is by reference to externalnon-endogenous ‘shocks’ such as the OPEC oil-price embargo andexcessively lax scal and monetary policy that increased nominal demandfaster than the growth of real output. While oil-prices where certainly afactor in higher ination, empirical research suggests that less than 15 percent of the rise in prices observed in the 1970s can be directly attributed tothe OPEC embargo. Nor does the timing of the downturn in the prot-rate(1965–7) correspond to the point at which international competition in

manufacturing began to ramp up, as most of the major inroads into USmarkets by foreign rms occurred after 1970. aken in tandem, problemsconcerning timing and the inability to explain the inationary form assumedby the crisis raise serious questions about the validity of an approach thatexplains falling prot-rates as an outcome of a competition-induced fall inprices. Interestingly, none of Brenner’s critics have made much of this point,

which seems critical to me: namely, that the crisis did not manifest itself inthe form a deationary spiral, but, rather, took the form of price-wageination. 5

Tird, Brenner’s ‘horizontalist’ account, that explains falling protabilityas the outcome of excessive competition, cannot offer a compellingexplanation of why the rate of decline was ubiquitous across all economicsectors, not just in manufacturing or sectors directly exposed for intensiedinternational competition. Brenner himself acknowledges the problem,particularly in the case of non-manufacturing rms and services. Given thatthese rms did not experience intensied international price- and prot-

5. Tis is not a peripheral issue. Any account of the crisis must be able to account for both

the underlying origins of the fall in the rate of prot, and the phenomenal form through whichthis decline is manifest. Why falling prots corresponded with a rise in the ination rate is acentral fact that any account of the 1967– 82 crisis must explain.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 8/36

K. Beitel / Historical Materialism 17 (2009) 66–100 73

competition, and given the presumed fall in prices of manufactured goodsrelative to services, this would imply that the prot-rate in these sectors

would be rising. o get around this problem, and reconcile his manufacturing-centred account with the generalised nature of the fall in the prot-rate,Brenner ends up surreptitiously re-introducing the very wage-squeezeargument that he had previously gone to great lengths to debunk – forexample, by claiming that wages rose faster than prices in many non-manufacturing sectors, thus placing a wage-induced squeeze on prots. 6 Problems are compounded by empirical work by Duménil and Lévy thathas shown that, once certain extremely capital-intensive sectors are excludedfrom the calculation (mining, utilities, and heavy transportation), the

decline of the rate of prot in the manufacturing and non-manufacturingsectors is roughly equivalent.7 Tis undermines Brenner’s claim thatovercapacity and excess-competition (due to insuffi cient exit) is at the rootof the fall in the prot-rate. 8

Finally, Brenner’s reliance on overcompetition and lack of capital-exitcannot readily explain persistent stagnation in the rate of net investment.Once older capitals were retired following the wave of industrial shakeoutsthat occurred in the years 1982–5, pressures on prices and prots due toexcess-competition and overproduction should have worked their way

through the industrial system. Hence, the problem of overcapacity andstagnation should be a transitory phenomenon in Brenner’s framework. Yet, as I show below, and as Brenner himself notes, declining rates of netinvestment have persisted despite the post-1982 recovery in the prot-rate.Given his inability to reconcile persistent investment-stagnation with hisaccount of the crisis of the 1965–82 period, Brenner’s subsequent writingstreat the lack of adequate investment-outlets as a problem of insuffi cientlevels of effective demand. As such, his post-1998 contributions veertowards a left-Keynesian position that ascribes sub-par investment and

growth to the mismatch between the growth of wages relative to the increase

6. Shaikh 1999.7. Duménil and Lévy 2002b.8. Much of Brenner’s problem seems to derive from his inability to see that one cannot

explain movements in the prot-rate through the pricing behaviour of individual rms. Price-formation is governed, over the long term, by underlying factors such as the output/capital ratioand the prot-share that regulate the aggregate rate of prot. Pricing practices of rms will reectmovements of these underlying determinants of the prot-rate, and hence cannot be used todevelop a coherent account of the determinants of longer-term changes in the rate of prot. In

part, Brenner’s problem on this count derives from the undercurrent of methodologicalindividualism that pervades his account, as that leads him to seek to derive the prot-rate as theaggregated outcome of a multitude of uncoordinated individual decisions.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 9/36

74 K. Beitel / Historical Materialism 17 (2009) 66–100

in worker-output. Recourse to lack of effective demand due to inadequategrowth of wages involves an explicit repudiation of his prior theoretical

framework according to which changes in the rate of prot govern the rateof net investment. Te sum result is a highly eclectic and increasinglyincoherent account that must continually introduce a host of contingentand transitory factors to explain the problem of stagnant investment. Tisis not surprising, given that Brenner’s prior framework, already deeplyawed to begin with, cannot offer any compelling explanation or accountof why investment has failed to respond to the improvement in the rate ofprot. In the end, we are left with a highly ad hoc and empiricist treatmentof the post-1982 period that lacks any rigorous or unifying theoretical

basis. Providing a more theoretical coherent account of the apparentcontradiction between the post-1982 recovery of the prot-rate concurrent with a long-term decline in the rate of net investment is one of the chiefobjectives of this paper.

In the following section, I decompose the rate of prot calculated fromthe National Income and Product Accounts (NIPA) into some of itscomponent factors in order to isolate various forces at work that explainobserved movements in the price-rate of prot. Te method utilised hassignicant overlap with prior work by Wolff, Duménil and Lévy, and

Moseley.9

While the results of this section are generally congruent with theseprior analyses, there are some differences in the relative emphasis placed onvarious forces operating on protability, particularly movements in theoutput-to-capital ratio and the timing of changes in the prot-share.

Where I part company with these prior analyses is in my treatment of thefactors governing longer-term changes in the rate of investment. Drawing onone strand in the work of the ‘monopoly-capital school’, I argue that thematuration of the US – and global – industrial system has imposed barriers toaccumulation that appear to have largely offset any stimulus due to the

improvement in the prot-rate. Barriers to investment have been exacerbatedby a phenomenon of ‘disaccumulation’ occurring within the productivecircuit, due to an improvement in the output-to-capital ratio that has allowedrms to meet output-targets with a lower rate of net investment. I furtherargue that barriers to a renewal of a higher rate of accumulation and growthhave been compounded by the increased appropriation of surplus-value

9. Wolff 1992 and 2002; Duménil and Lévy 2002a, 2002b and 2004; Moseley 1997 and1999.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 10/36

K. Beitel / Historical Materialism 17 (2009) 66–100 75

(prots) by the owners of nancial assets that has siphoned off funds that would otherwise be available for productive investment.

Te sum result has been a situation where in higher prot-rates co-exist with a persistent underaccumulation of capital within the productive circuit.Tis has required that other means be found to guarantee the expansion ofthe market, primarily through a phenomenal expansion of household- andpublic-sector debt. While this has provided a provisional means ofovercoming problems of stagnant investment, the ight into the futureevidenced in expansion of credit has insurmountable limits. I conclude witha discussion of the conditions that have facilitated the Federal Reserve’sability to underwrite speculative credit, and the conditions under which this

form of systemic management will no longer serve to overcome problems ofstagnant investment.

Analysis of the prot-rate

Te prot-rate can be decomposed into the product of the ratio of prots tothe total national product and the ratio of total output to the net capital-stockas follows:

Prot-rate = [(prots)/(GDP)]*[(GDP)/(Capital-stock)]

Te rate of prot rises when either the output-to-capital ratio or the prot-share of national income rises, holding the other factor constant. Figure 2graphs movements in the output/capital ratio and the prot-rate over theyears 1947–2006. Changes in the rate of prot are highly correlated withchanges in output per unit of net capital-investment, measured at currentreplacement-cost. Both the output/capital ratio and the rate of prot riseduring the boom of 1960 –6, and then begin a long and precipitous fall. Teturning point occurs in 1982, following the worst recession in the US sincethe Great Depression. Te output-to-capital ratio rises sharply from 1982 –5, and continues to improve, albeit at a slower annual rate, until 1995. Teoutput/capital ratio then attens out, before entering what appears to be aperiod of renewed decline beginning in 2003.

We can decompose the nominal output/capital ratio into a ‘real’ and price-component. Figure 3 shows the real output-to-capital ratio derived by deatingboth output and the current cost of the net capital-stock by price-indexes forGDP and capital-goods (the PPI), respectively. What is particularly striking isnot only that the ratio of real output per unit of real capital-investment shows

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 11/36

76 K. Beitel / Historical Materialism 17 (2009) 66–100

evidence of a steady long-term secular decline, but the sheer magnitude of thedecline, falling from a peak of 1.64 in 1965 to 0.81 in 2006. Tis implies that,in real terms, the capital-stock is only half as productive today as it was fortyyears ago.10

Figure 4 plots the ratio of the price index for GDP (the GDP deator) tothe price-index for producer-goods (the PPI deator). Te ratio rises rapidlybetween 1982 and 1985, followed by another increase between 1993 and2003. When this ratio is rising, the values (measured in socially-necessarylabour-time), hence the prices of capital-goods are falling relative to the values,hence the prices of the goods and services that compose nal output. Giventhat capital-stocks are composed of manufactured goods, and nal output is

10. One must treat these numbers with some caution. While NIPA chain-weighted price-deation attempts to provide a means for rigorously accounting for technical change, it is notclear we can compare ‘real’ output to capital-measures over an extended period of time due tofundamental qualitative change in the composition of both the means of production and output.Let me here note that the decline in the real output-to-capital ratio has coincided with a markedshift in the composition of the capital-stock. Te ratio of the stock of capital accumulated innancial and real-estate trading activities has risen relative to the capital invested in manufacturing,transportation, and utilities. As I will argue below, this pattern is congruent with the decline

observed in Figure 3, as capital invested in FIRE is non-productive in both Marxian (value) andreal terms – protestations to the contrary, bond-traders and real-estate agents do not themselvesproduce any ‘real’ output, but are primarily engaged in the speculative reshuffl ing of ownership-

Figure 2. Rate of prot and output/capital ratio

Source: National Income and Product Accounts, able 1.1.5, able 6.3; Net Fixed Assets, able 4.1

0

0.2

0.4

0.6

0.8

1

1.2

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Output/CapitalRate of Prot

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 12/36

K. Beitel / Historical Materialism 17 (2009) 66–100 77

Figure 3. Real output/capital ratio, 1947–2007

Source: National Income and Product Accounts, able 1.1.5, able 1.1.9, able 5.3.4;Net Fixed Assets, able 4.1

Figure 4. Ratio of (GDP deator) / (PPI deator), 1947–2007

Source: National Income and Product Accounts, able 1.1.5, able 6.3; Net Fixed Assets, able 4.1

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

0

0.2

0.4

0.6

0.8

1

1.2

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 13/36

78 K. Beitel / Historical Materialism 17 (2009) 66–100

composed of a mix of goods and services, a rise in this ratio indicatesthat productivity-gains in manufacturing exceed those of services, and,

secondarily, that productivity-gains by manufacturing rms in Department Ilikely exceed those in Department II.

What Figures 3 and 4 show is that the rise in the nominal output-to-capital ratio is entirely due to the cheapening of the prices of capital-goodsrelative to the price composite of goods and services that enter directly intoGDP. Given that movements in the output/capital ratio tends to dominatemovements in the rate of prot, it follows that the most signicant factorunderlying the improvement in protability since 1982 is the decline in theprices of capital-goods relative to the prices of all capital- and consumer-

goods that compose the gross domestic product.Te other principal factor that enters into the determination of the prot-rate is the prot-share, or the share of the total value-product appropriated inthe form of prots (retained prots, interest, and dividends). Followingstandard practice, I calculate the prot-share by subtracting the total annual

wage- and salary-compensation paid to employees from the estimate of the

Figure 5. Prot-share, 1947–2007

Source: National Income and Product Accounts, able 1.1.5, able 7.5, able 6.3

0.38

0.4

0.42

0.44

0.46

0.48

0.5

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 14/36

K. Beitel / Historical Materialism 17 (2009) 66–100 79

GDP reported in the National Income and Product Accounts.11 Figure 5shows the prot-share over the years 1947–2006.

Between 1947 and 1971, we observe a pattern of (uneven) decline that isparticularly pronounced between 1947–52 and then again during the boomof 1965–71. Te prot-share then undergoes a secular rise continuing through1995. Te high-tech/dot.com boom of 1996 –2000 drove down unemploymentand temporarily eroded capitalists’ income-share. Tis decline was reversed in2001, with the prot-share recovering to levels approaching the peak reachedat the beginning of the 1990s high-tech boom.

Variations in the prot-share will reect relative changes in real wages andreal output per hour of labour-time expended. If real wages rise faster than

output per hour, the prot-share falls. Conversely, if output per unit oflabour-input exceeds the increase in real wages, the prot-share rises.Figure 6 shows real wages and real output per worker over the 1947–2006

period with each series normalised to one for the year 1948 to facilitatecomparison. In periods during which the prot-share falls real-wage growthexceeds the growth of productivity (for example, in 1966–71 and 1995–2000the slope of the incline in the former exceeds that of the latter), and vice-versa

when the prot-share is rising.Te rise in the prot-share since 1971 is indicative of several longer-term

trends that have fundamentally recomposed the relative balance of class-powerin favour of capitalist owners. For one, structural unemployment began to risein 1969 and continued to rise for over a decade thereafter due to thecombination of slower accumulation and increased mechanisation. Tis

weakened the position of organised labour and broke the link establishedunder Fordism between increases in labour-productivity and the growth ofreal wages for workers in the manufacturing core. Second, the rise in theprot-share after 1971 reects an ongoing recomposition of labour-marketsand employment-relations that was occurring along a variety of dimensions.

Key aspects of this structural recomposition include the following: decliningrates of unionisation; the growing absorption of labour into lower-wage

11. Tis ratio functions as a crude but useful proxy for what Marx termed the rate ofexploitation, or the total share of new value created by (abstract) labour in excess of the valueadvanced in the form of wages. Te rate of surplus-value is calculated by dividing unpaid by paidlabour-time. Realised prots that can be calculated from the NIPA are the difference betweentotal national income and the total outlay of wage- and salary-expenditure. Te latter includes

what Marx termed unproductive labour – for example, work that may perform a necessaryfunction in the reproduction of the capital-ratio yet that does not constitute a direct source of

new value and surplus-value. Tis would include, for instance, workers employed in advertising,sales, and nance.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 15/36

80 K. Beitel / Historical Materialism 17 (2009) 66–100

service- and retail-sectors; the individualisation of the wage-contract in amanner that favours employers (with the exception of some groups of highlyskilled workers who have been able to command higher wages); the prevalenceof disguised unemployment in the form of a reduction in labour-forceparticipation (particularly amongst African-American males); unreported

joblessness and involuntary part-time employment; reductions in the realvalue of the federal minimum-wage; worries over impending job-loss due tothe effects of corporate restructuring and layoffs; the rise of contract-andcontingent employment; the inux of cheap immigrant-labour that has driven

down wages in many service-sectors; the greater threat of capital-mobility thatserves as a weapon through which to discipline labour; the growing exposureof US manufacturing workers to lower-cost foreign competitors (via Wal-Mart); and the growth of household-debt that has served as a mechanism forinculcating acceptance of free-market values within the working class. Allthese processes were underway to varying degrees at the time when Volckertook over as Chair of the Federal Reserve. Te often-noted effects of the‘Volcker shock’ that gure prominently in many accounts of neoliberalismmust be interpreted within this context. 12

Volcker’s decisions to jack unemployment to record post-WWII levels

amounted to a brutal hit upon an already weakened US working class. Similarconsiderations apply to Reagan’s summary ring of the striking federal PA CO

Figure 6. Labour-productivity and real wage, 1948–2007, all workers

Source: National Income and Product Accounts, able 1.1.5, able 6.9, able 5.3.4and 5.2.5, able 6.3

0

0.5

1

1.5

2

2.5

3

3.5

1 9 4 8

1 9 5 0

1 9 5 2

1 9 5 4

1 9 5 6

1 9 5 8

1 9 6 0

1 9 6 2

1 9 6 4

1 9 6 6

1 9 6 8

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

real wagereal output per hour

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 16/36

K. Beitel / Historical Materialism 17 (2009) 66–100 81

workers in 1981 and his stacking of the National Labor Relation board withanti-labour appointments. What was decisive about the Volcker-Reagan era is

that it marked the watershed moment in the ideological consolidation of apolitical-economic régime predicated upon an ethos of market-fundamentalismand the construction of a new class-alliance between certain highly-skilledsectors of the white-collar salariat and corporate management. It was not,however, the decisive turning point in boosting the prot-share, which hadbeen ongoing during the previous ten years.

o sum up, movements in the output-to-capital ratio dominated thebehaviour of the rate of prot between 1965–96.13 While the fall in the prot-share was a signicant factor contributing to the initial downturn in 1965, the

rise in the prot-share after 1971 proved insuffi cient to reverse the decline inthe rate of prot brought about – and sustained – by the decline in the output/capital ratio. Te onset and duration of the crisis of the Keynesian-Fordistrégime cannot be primarily attributed to the rising power of organised labouror a major shift in the relative balance of class-power. On the contrary, theduration and extent of the crisis is largely explained by the fall in the output/capital ratio.

Tis trend reversed itself following the sharp contraction of the 1980–2period. Falling prot-rates and Volcker’s decision to jack interest-rates to

record-levels plunged the US and global economy into its deepest recessionsince the Great Depression. Te crisis had a salutary effect on the rate of prot.Te sharp contraction in domestic demand and the sky-rocketing price of thedollar undermined the competitive position of large portions of US capital.Plant-closures destroyed massive sums of capital-value amongst rms nolonger able to conrm to new international cost-standards imposed by moreeffi cient foreign producers. Tis purged the US manufacturing base of itsolder, less technologically-advanced xed capital. Te defeat imposed on USlabour was decisive in clearing the path for the accelerated restructuring of

rms’ xed capital and the introduction of labour-process transformationsassociated with lean production. As new methods and labour-processinnovations were disseminated, productivity-growth in manufacturing rose.Firms that survived the shakeout of the 1979–85 period began to recapitalisetheir xed stock through ‘rationalising’ forms of investment that sought toeconomise on both capital and labour.

Te sharp upturn in labour-productivity in the capital-goods sector reducedthe prices of capital-stocks relative to the prices of nal output. Te combination ofthe rise in the prot-share and the decline in the relative price of capital-goods

13. Tis analysis is congruent with historical studies by Duménil and Lévy that have argued

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 17/36

82 K. Beitel / Historical Materialism 17 (2009) 66–100

in tandem laid the basis for the post-1982 recovery in the prot-rate. Tecrisis and post-1982 recovery affi rms one of Marx’s central contentions, namely

that crisis is both the expression of the maturation of capitalism’s internalcontradictions and the means through which barriers to protability areforcibly resolved.

Some contradictions of the neoliberal régime

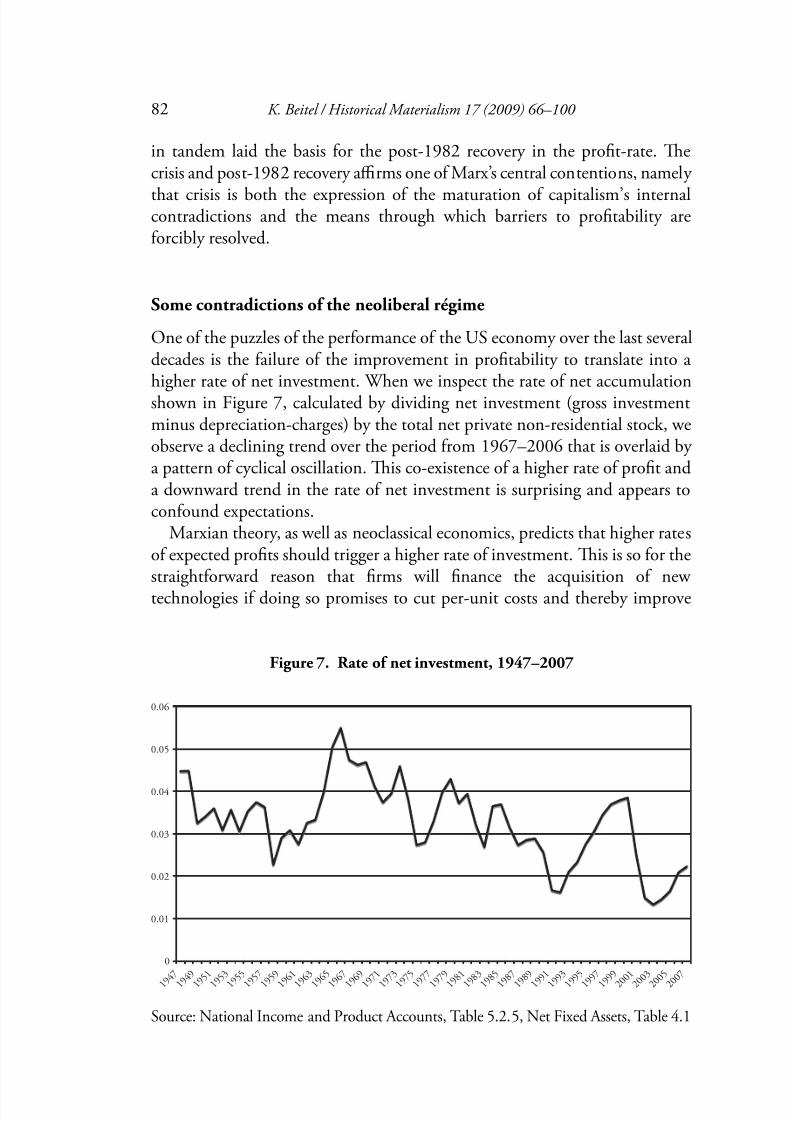

One of the puzzles of the performance of the US economy over the last severaldecades is the failure of the improvement in protability to translate into ahigher rate of net investment. When we inspect the rate of net accumulationshown in Figure 7, calculated by dividing net investment (gross investmentminus depreciation-charges) by the total net private non-residential stock, weobserve a declining trend over the period from 1967–2006 that is overlaid bya pattern of cyclical oscillation. Tis co-existence of a higher rate of prot anda downward trend in the rate of net investment is surprising and appears toconfound expectations.

Marxian theory, as well as neoclassical economics, predicts that higher ratesof expected prots should trigger a higher rate of investment. Tis is so for thestraightforward reason that rms will nance the acquisition of newtechnologies if doing so promises to cut per-unit costs and thereby improve

Figure 7. Rate of net investment, 1947–2007

Source: National Income and Product Accounts able 5 2 5 Net Fixed Assets able 4 1

0

0.01

0.02

0.03

0.04

0.05

0.06

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

1 9 7 7

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 18/36

K. Beitel / Historical Materialism 17 (2009) 66–100 83

their competitive position. echniques that achieve major reduction in per-unit costs should, therefore, stimulate an upsurge in new investment as rms

rush to capture technological rents and above-average prots accruing to thosecapitals that succeed in being the rst to bring these new methods intooperation. It follows that a steady stream of cost-reducing innovations shouldbe correlated with a sustained upturn in the rate of accumulation.

Tree factors explain the breakdown of the expected prot-investmentrelation. In the most general sense, the delinking of the rate of investmentfrom the prot-rate reects the fact that, in a mature industrial economy suchas the US (this is also true for most of Europe and Japan), a diminishing shareof investment is tied to the development of entirely new industrial sectors,

including services. Once such a stage of maturity is reached, the prior stimulusto accumulation provided by the impetus to develop and build up the basicbranches of industry is progressively exhausted. A point is eventually reached

wherein investment in a growing number of sectors occurs primarily to replace worn-out or technologically obsolete stocks funded out of capital-consumptionallowances. Te result is a tendency for the system to drift towards a lower rateof investment absent the appearance of major capital-absorbing technologicalinnovations that drive recapitalisation of existing branches of industry andspur the emergence of entirely new industrial sectors. For all the hype

surrounding the ‘New Economy’, the evidence suggests that the digitalrevolution has failed to provide a stimulus to accumulation on a scalecomparable to that provided by the railroad and the auto.14

Tis stagnationist tendency that overlays the entire neoliberal period hasbeen exacerbated by the fact that the rise in the output/capital ratio has allowedcapitalists to be able to meet output-targets with a smaller proportionateamount of net investment. Te basic logic can be illustrated with a simpleexample. Suppose that rms expect market-demand in a given line of industryto grow at a rate of 3 per cent per annum. If capital is becoming more effi cient

in money-terms – for example, if a higher level of output can be achieved fromeach additional unit of new investment – this means that rms will increaseplanned investment at a slower rate, say at a rate of 2 per cent per annum, thanthe expected rate of growth of market-demand (both measured in monetaryterms). In other words, the rise in the nominal output/capital ratio means thatcapitalists as a whole can meet any expected rate of growth of market-demand

with a proportionately smaller outlay on new plants and equipment.

14. Te claim that industrial maturity will act as a drag on the rate of net accumulation has a

long pedigree in neo-Marxist theory dating back to the seminal work of Michal Kalecki 1954and as developed in the subsequent writings of authors such as Steindl 1952 and Baran andSweezy 1966.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 19/36

84 K. Beitel / Historical Materialism 17 (2009) 66–100

In sectors characterised by advanced maturity, where demand can be met with existing capacity, new investment may well occur at levels below

replacement-value. In this case, investment-expenditures do not even manageto absorb capital-consumption allowances. Tis highlights the paradox ofrising ‘capital-productivity’ in the current neoliberal context. Te rise inproductivity, rather than serving as a stimulus to invest, can just as easily placea downward pressure on accumulation as rms nd they can do more withless.15 Te result is that a growing portion of funds recovered throughamortisation are released back into active circulation, where they are usedeither for speculative purposes or disposed of through an increase in capitalists’personal consumption.16

Tis brings us to a third factor exerting a depressive effect on the rate ofaccumulation, namely the rising share of total prots paid out to nancialowners in the form of dividends and interest. As seen in Figure 8, interestand dividends rose as a share of total prots from an average of 47 per centthe years 1970–8 to 68 per cent for the period 1979 –2003. Te major jumpin rentier income-share occurred between 1978 and 1982, as rising interest-rates and structural shifts in the relative power welded by nancial marketsover productive enterprise effected a massive reallocation of prot fromproduction to nance. Over time, the structure of rentier -income has changed

from primarily loan-based interest-income to greater weighting of equity-based returns.17 Te interest-share, while showing signicant variation overthe course of the business-cycle, shifts to a higher overall level in the 1980s,followed by a decline in the years since 1991, albeit with a major spike duringthe 2001 recession. Conversely, net dividends have tended to rise as a shareof booked prots over the entire period between 1979 and 2002, and appearto have remained at high levels in all years since, except for 2005.18

15. o avoid potential confusion, note that this investment-depressing effect has been due

entirely to the shift in relative prices that has reduced the value (hence the relative price) of theelements composing the xed stock of productive capital relative to the aggregated value of thegross output of nal goods and services. Tis point needs to be borne in mind when discussingthe question of the rate of accumulation, which refers to a monetary, as opposed to a use-valuephenomenon. Capitalists accumulate things as vehicles for the accumulation of value; if value(hence relative price) is falling, a greater mass of use-values purchased can be associated with asmaller sum of value. Hence, use-values may be augmented at a higher rate while the rate ofaugmentation of capital value is falling.

16. Tis argument is one of the core propositions of the monopoly-capitalist theory found inthe work of Steindl 1952, pp. 107–55; Baran and Sweezy 1966, pp. 52–78; Sweezy and Magdoff1987; Foster 1989; and Haveli and Lucarelli 2002.

17. Note also that the relative share ofrentier -income, particularly in the form of interest-payments, shows a pronounced cyclical effect. Tis is because debt payments on long-term debtobligations are xed in nominal terms, and thus rise/fall as a share of total prots in response to

li l d li /i i h f

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 20/36

K. Beitel / Historical Materialism 17 (2009) 66–100 85

Tis reallocation of prots from production to nance marks the reassertionof the power and prerogatives of capitalist owners – in particular, that sectorof the capitalist class that controls the origination and allocation of credit andnance. Beginning in the late 1970s, and then exploding with the ascensionof Volcker-Reagan, a market for corporate control developed in the form ofleveraged buy-out operations and private-equity acquisitions. Entire enterprises

were transformed into objects of speculation. Buyout-specialists and private-equity rms found ways to load up on debt, buy out existing shareholders, and

take the company private. A ruthless round of cost-cutting would follow. Terestructured rms could then be re-sold on the public-equity market at ahandsome prot or, alternatively, held as a privately-owned proprietaryenterprise.

Private-equity rms and buyout-specialists have used this process to leveragehigher returns on their paid-in equity-investments. At the same time, thisprocess has had an impact on decisions regarding capital-allocation and rms’

prots at several points. Tis indicates that nancial payments are ‘cannibalising’ the productivesector through a process of productive disinvestment. Tis would conrm the overall accountpresented in this article. However, some caution must be exercised in evaluating the exact levelsshown in the National Income and Product Accounts, given certain accounting complexitiesh f i h h f NFC ll d d Wh i i f

Figure 8. Net dividend and interest as share of NFC booked prots, 1960–2007

Source: National Income and Product Acounts, able 7.10, able 7.11, able 6.16

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

160.00%

1 9 6 0

1 9 6 2

1 9 6 4

1 9 6 6

1 9 6 8

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 21/36

86 K. Beitel / Historical Materialism 17 (2009) 66–100

‘propensity to invest’. Internal cash-ows have increasingly been siphoned offthrough debt-repayments, as opposed to being utilised to nance tangible

investments in new plants and equipment. Surpluses remaining after debt-servicing are then returned to private owners or distributed through dividend-payments to equity-holders. Lacking protable investment-outlets in theproductive sectors, these funds are funnelled back into the capital-markets

where they are deployed for largely speculative purposes.Te post-1980 development of a ‘market for corporate control’ and increased

shareholder-activism similarly transformed the environment within whichtop-tier management presently operate. CEOs have been transformed intorentier -capitalists by having their compensation tied to stock-options and

dividend-payments. Te rapacious scrutiny by the capital-markets forundervalued corporate assets has compelled them to manage their rms anddistribute prots with a constant eye towards warding off the spectre ofshareholder-revolt and leveraged buyouts. Under such circumstances,management is far more inclined to dispose of nancial surpluses throughincreases in quarterly dividend-payouts – stock-buybacks that articiallyinate stock-prices – or by nancing mergers and acquisitions that createpaper capital-gains without any actual augmentation of the value of theunderlying tangible capital from which equity-valuations are (in principle)

derived.19

Meeting rentiers ’ rapacious demands for higher dividend-paymentsand capital-gains requires that rms try to squeeze more output from theirexisting stock. o the extent that rms can meet production- and output-targets with a lower per-unit rate of net investment, nancial surpluses thatmight otherwise have been dedicated to expanding plants and equipment aresiphoned off in the form of dividend-payments. Tis exacerbates problems ofstagnant investment.20

19. Financialisation has effected a growing ‘rentierisation’ of top management by tying CEOcompensation to the performance of a company’s share-price through stock-options. Tis resultsin the creation of incentive-structures that directly tie CEO compensation to short-term stock-price and added incentives if rms exceed certain performance benchmarks. Stock-options andother forms of equity-linked compensation-packages have created powerful incentives for CEOsto manage enterprises in view of maximising short-term stock-performance, and have been usedto resolve the principal-agent problem inherent in the system of joint-stock ownership byeffectively fusing the incentives of wealthy shareholders (owners) and top management.

20. For various accounts, see Lazonick and O’Sullivan 2000; Duménil and Lévy 2002; Crotty2003; and Kalecki 1954, pp. 145–161. Orhangazi 2008 presents econometric evidence regarding

the effect of nancialisation on the capital-expenditures by non-nancial corporations thatconrms claims regarding the depressive effect of higher payments torentiers on the long-termallocation of prots to xed investment.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 22/36

K. Beitel / Historical Materialism 17 (2009) 66–100 87

Tis combination of factors explains the neoliberal paradox of robust andrising prots co-existing with subpar investment. Te result is that sustaining

the ability to convert the surplus-product into realised monetary prots hasbecome increasingly dependent on the growing indebtedness of the USgovernment and, particularly over the last decade, on the growth in the debt-encumbrance of the working class. It can be shown within a Marxian-Kaleckianmodel of the capital-circuit that the greater the difference between the rate ofprot (rising since 1982) and the rate of accumulation (falling over the sameperiod), the greater the rate of growth of household- and government-debtthat is required in order for rms to convert their imposed mark-ups intorealised prots.21 It can further be shown that the total amount of rms’

retained prots is equal to the amount of debt-nanced household- andgovernment-expenditure, adjusted for leakages due to the trade-decit.Because these retained prots are not offset by an equivalent amount of debt-nanced capital-investment, rms are not required to allocate these prots toretire short-term bank-credits used to nance their initial investment. Teresult is that the growth of government- and household- debt-nancedconsumption necessary to sustain demand and realise prots creates a massivepool of ‘unattached’ prots that are distributed either to capitalist householdsvia higher dividend-payments or placed directly into the capital-markets.

Retained prots are in this manner recycled back into the nancial markets where they are transformed via purchases of yield-bearing nancial assets(securities) into claims on future wages and prots. Te circuit of securitisedcredit is, in this sense, ‘self-nanced’.22

Te recycling of this massive pool of distributed prots back through thesecondary capital-markets introduces a long-term inationary bias into asset-prices. Higher asset-prices in turn lie at the core of how the ‘crisis’ of insuffi cientreal investment has been deferred over recent decades. Particularly during thelast decade, growth has become dependent on the so-called ‘wealth-effect’.

Tis refers to a dynamic whereby rising asset-prices lead households to feelmore secure about their economic prospects. Buttressed by higher portfolio-values and rising home-prices, households decide to reduce their rate of saving

21. See Rochon 1999; Seccareccia 1996.22. Te relation between debt-nanced expenditure and realised prots originates in the

work of Michal Kalecki, who demonstrated how capitalist’s actually-realised collective prots were exactly equivalent to their own outlays on consumption and investment. Either capitalists’consumption out of prots, or debt-nanced investment generates revenue on the income sideof the aggregated balance-sheet of the private sector for which there is no offsetting factor-cost.

Similarly, when working-class households go into debt to nance consumption, this generates aow of sales-revenue for which there is no offsetting cost and hence enters into the total globalprots (surplus-value) realised by the capitalist class. See Kalecki 1954, pp. 45–69.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 23/36

88 K. Beitel / Historical Materialism 17 (2009) 66–100

and increase their issue IOUs to boost consumption-spending. Trough theprocess described above, this debt-funded expenditure leads to the formation

of prots distributed to capitalist households that are subsequently recycledback into the nancial markets. Tis dynamic of debt-nanced consumptionis what essentially drove prot-formation during the dot.com boom and thehousing bubble.23

Monetary interventions of the Federal Reserve over recent decades,particularly during the Greenspan years, have been driven by the need tomanage the contradictions internal to a system in which growth and prot-creation has become inextricably tied to credit-fuelled asset-bubbles andborrowing secured against appreciating property- and equity-collateral.

Interest-rate reductions allow indebted yet functional solvent entities to re-nance their existing liabilities. Tis reduces the share of current incomeabsorbed by payments of principal and interest, raising the manageable debt-to-income ratio of already over-leveraged nancial rms and households.Lower interest-rates, in turn, induce an inationary dynamic into asset-prices,both through increasing viable debt-loads and by increasing the rate at whichfuture income-streams are ‘capitalised’ into the current prices paid for nancialassets on the secondary market. Te subsequent emergence of nancial excessand asset-overvaluation could be partially slowed and deated by raising

interest-rates. Because prots were generally robust, higher interest-rates didnot impose excessive strains on private non-nancial corporations. Once therequisite – albeit partial – purging of the prior period’s excess was complete,the Federal Reserve would again lower interest-rates. Tis created the basis forthe next credit-fuelled rise in asset-prices leading to higher levels of consumptionand output.

Te ability of the Federal Reserve to use aggressive interest-rate reductionsto avert a potentially destabilising meltdown of asset-prices without having to

worry about triggering excessive ination reects the favourable prot-ination

trade-off that has prevailed over the last two decades. Although this point isoften overlooked in discussions of neoliberalism, it is essential to understandingboth the capacity – and the limits – of the Federal Reserve’s ability to managethese contradictions.

23. By some estimates, over the course of the boom of 1996–2000, each dollar-increase inshare-values gave rise to a corresponding increase in consumption-expenditure of between 5 and15 cent. Similarly, the boost to housing prices provided by the sequence of interest-rate reductionsimplemented by the Federal Reserve between 2001–5 was critical in supporting higher levels ofconsumer-demand and averting a deep and prolonged recession following the collapse of the

dot.com boom. For insightful analyses of the contradictions of this nance-led régime ofaccumulation, see O’Hara 2001 and 2002.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 24/36

K. Beitel / Historical Materialism 17 (2009) 66–100 89

In an economic system dominated by large oligopolistic corporations, there will typically be an inverse correlation between changes in the rate of prot

and ination. Oligopolistic rms set prices at levels such that, for a ‘normal’level of capacity-utilisation, total revenues will cover total per-unit costs plusadministrative overheads plus debt-servicing costs, with a net prot-margin‘left over’ that may be used for internally funded investment or distributedthrough dividend-payment.24 When prot-rates are stable or rising, rms canmeet their retained earning targets at (more or less) constant prices. Conversely,

when prot-rates are falling, rms may seek to increase their mark-ups andmay be forced to increase borrowing, often on an involuntary basis, to acquiresuffi cient funds to cover ongoing investment-projects. Hence, periods of

strong (and rising) protability will typically be associated with lower rates ofination and a decline in rms’ debt-to-equity ratio. Conversely, whenprotability is falling, both price- and debt-to-equity ratios tend to rise.25

Te favourable prot-ination trade-off since the mid-1980s allowed theFederal Reserve ample latitude in setting the price of credit and pumpingmassive amounts of liquidity into the system as needed without having to

worry about igniting a price-wage inationary dynamic. Monetary policy waselevated to an increasingly prominent role in the management of the historicallyanomalous combination of a higher rate of prot and stagnant investment,

overlaid by a massive expansion of the debt-loads of households andgovernment. Interest-rate adjustments were the means through which theFederal Reserve sought to permanently defer the point of ultimate settlement.

24. See Lipietz 1985, pp. 107–33; Lee 1998; and Godfrey and Lavoie 2007. Arguing thatlarge corporations administer prices does not imply that rms can set prices at any desired level.Te actual mark-up on per-unit costs will vary with the level of concentration, the homogeneityof the product, the degree of inter-rm competition, and the rate at which technological leadersare achieving reductions in per-unit costs. Where some left analysts err is in assuming that the

restoration of international competition has caused rms to lose any effective control over thedetermination of prices. In my view, this claim is vastly overstated. Te majority of oligopolisticsectors are not characterised by falling prices or frequent pricing wars. Sectors with some variantof ‘mark-up’ or ‘full-cost’ pricing include almost all major capital-goods producers: aerospace; allprivate military contractors; private hospitals; the pharmaceutical industry; medical equipment;medical services; the hospitality industry; ‘big box’ retail; the fast-food industry; most mediaproducts; commercial construction; apparel and textiles; and nancial and producer-services.Exceptions are manufacturing sectors exposed to foreign competition. However, if GM nolonger determines prices, then oyota (or some global corporation) does. In doing so, oyotaimposes a mark-up on costs, or some variant of full-cost pricing.

25. Empirical support is seen in the correlation between prot-rates and ination over the

entire post-WWII period, and the inverse movement of prot-rates, rms’ debt-to-equity ratio,and the share of interest-payments as a percentage of net prots.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 25/36

90 K. Beitel / Historical Materialism 17 (2009) 66–100

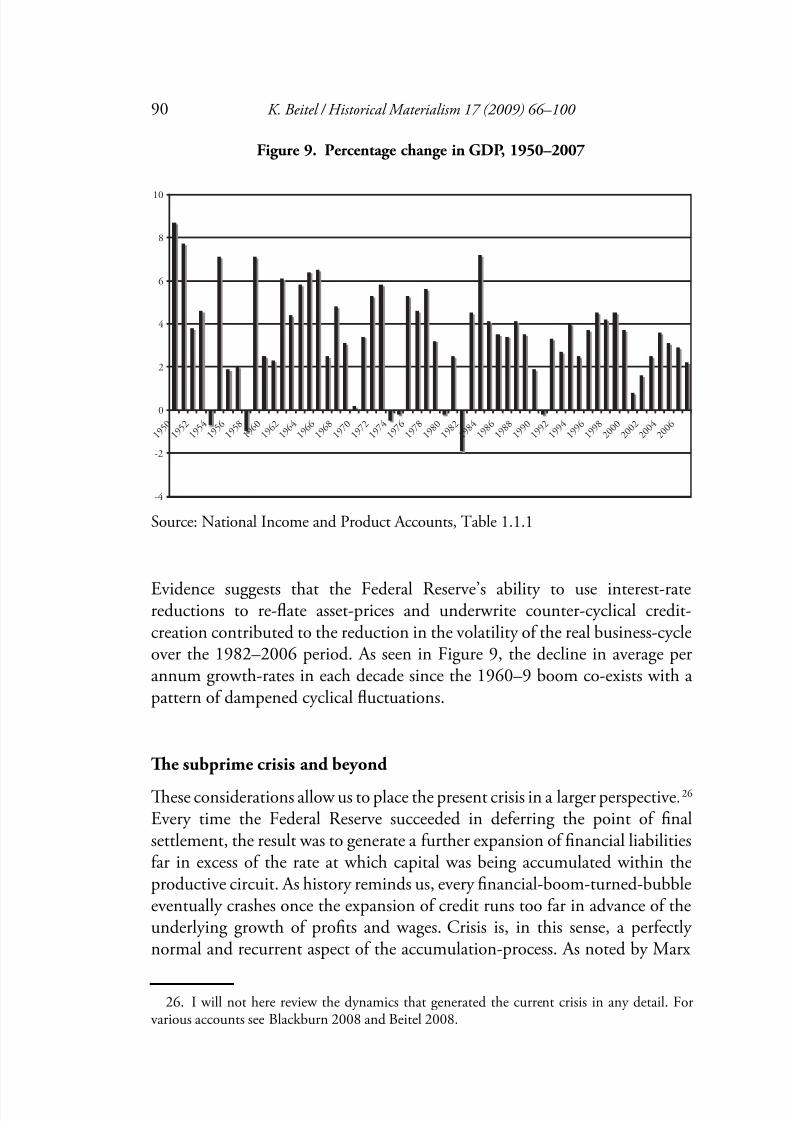

Evidence suggests that the Federal Reserve’s ability to use interest-ratereductions to re-ate asset-prices and underwrite counter-cyclical credit-creation contributed to the reduction in the volatility of the real business-cycleover the 1982–2006 period. As seen in Figure 9, the decline in average perannum growth-rates in each decade since the 1960–9 boom co-exists with apattern of dampened cyclical uctuations.

Te subprime crisis and beyond

Tese considerations allow us to place the present crisis in a larger perspective.26 Every time the Federal Reserve succeeded in deferring the point of nalsettlement, the result was to generate a further expansion of nancial liabilitiesfar in excess of the rate at which capital was being accumulated within theproductive circuit. As history reminds us, every nancial-boom-turned-bubbleeventually crashes once the expansion of credit runs too far in advance of theunderlying growth of prots and wages. Crisis is, in this sense, a perfectlynormal and recurrent aspect of the accumulation-process. As noted by Marx

26. I will not here review the dynamics that generated the current crisis in any detail. Forario s acco nts see Blackb rn 2008 and Beitel 2008

Figure 9. Percentage change in GDP, 1950–2007

Source: National Income and Product Accounts, able 1.1.1

-4

-2

0

2

4

6

8

10

1 9 5 0

1 9 5 2

1 9 5 4

1 9 5 6

1 9 5 8

1 9 6 0

1 9 6 2

1 9 6 4

1 9 6 6

1 9 6 8

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 26/36

K. Beitel / Historical Materialism 17 (2009) 66–100 91

throughout his voluminous writings on economics, crises are required toperiodically destroy overvalued ‘ctitious capital’ whose prices no longer

conform to the underlying rates of return on productive investments.Crisis simultaneously purges technologically obsolete capital from the

productive circuits. Te salutatory effect – for capital as a whole – is to rid thesystem of excess (for example, non-redeemable) debt-overhang and toannihilate sub-par capitals that no longer conform to prevailing technologicalstandards. Tis process of debt-deation and destruction of technologically-obsolete capital is the necessary precursor to the restoration of a higher rate ofprot. Tis is, in turn, a necessary – albeit not suffi cient – condition for therestoration of a higher rate of accumulation.

Te anomaly of the subprime crisis is that both the origins of the initialdistress and the initial phase of asset-destruction were almost entirely conned within the household- and nancial sector. By contrast, the non-nancialcorporate sector entered the crisis with a relatively low debt-to-equity ratio ascompared to prior decades and high returns on xed capital (Figure 1). As aresult, the immediate problem confronting managers of the US system is nothow to engineer a massive destruction of technologically-obsolete productivecapital, as was the case in 1979, but how to sustain the monetisation of protsin the wake of the collapse of the housing bubble. Te solution, in one sense,

is quite obvious. o the extent that the immediate impacts of the crisis werelocated primarily in the sphere of the realisation of value, the remedy is toreate the real economy, hence prots, through a massive increase ingovernment-decit expenditure to offset prot-destruction tied to the credit-contraction transpiring in the household-sector.

We should not conclude, however, that a robust dose of Keynesian scalstimulus – tax-cuts and increased decit-spending by the federal government –can provide a longer-term solution to the problem of the secular decline in therate of net investment and reset the economy back on a self-sustaining growth-

path. Decit-spending can, at best, provide a temporary means for deferring arealisation-crisis by allowing rms to continue to convert their imposed mark-ups into realised money-prots. However, decit-expenditure is far less effectiveas a longer-term counter-measure for offsetting a renewed decline in the rate ofprot. Here is where the Keynesian stimulus-measures reveal their limits. Tequestion, therefore, is whether we are at a turning-point in the prot-rate cycle.Or whether, on the contrary, neoliberalism and the digital revolution haveannulled the falling rate of prot as a ‘law of motion’ governing the evolutionarytrajectory of capital.

I believe the evidence suggests that the system is at a turning point in thelonger-period oscillation in the prot-rate. For one, the output/capital ratiobegan falling in 2003 Te attening of the relative price ratio (Figure 4)

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 27/36

92 K. Beitel / Historical Materialism 17 (2009) 66–100

suggests that the ability of manufacturing rms (capital-goods producers inparticular) to realise higher productivity-gains from ‘post-Fordist’ practices is

exhausted.27 If so, this suspends the primary factor counter-acting the fall inthe rate of prot brought about by the decline in the (real) output/capitalratio. Faced with falling prots, capitalists will respond (as always) byincreasing their substitution of xed capital for living labour. Tis will reducethe labour-to-capital ratio. If the fall is not offset by a suffi cient increasein real output per worker-hour, this will lower the real output-to-capitalratio. In order to avoid a decline in the monetary measure of the output/capital ratio, the value, hence the prices, of capital-goods must fall at asuffi cient rate relative to the value, hence the prices, of aggregate output.

While productivity-growth in manufacturing remains higher than in services,the attening of the relative-price ratio suggests that this differential rate isdeclining. If the trend continues, this will impose a sharp downward pressureon the prot-rate.

Second, after rising at an impressive clip between 1996 and 2003,productivity-growth appears to be slowing. Full explication of factorsimpacting productivity-growth is beyond the scope of this paper. For nowlet me simply note that the overall pattern observed in Figure 6 showsevidence of a long-term cyclical pattern that cannot be explained as an effect

of cyclical oscillations in the business-cycle. Te rate of growth increases ata (more or less) constant rate between 1947–70, 1982–6, and 1996–2004.By contrast, productivity rises, but at a slower rate during the slowdown of1971–80, the years 1987–92, and in the years since 2004.

Any secular decline in the rate of productivity-growth will impose limitson the ability to offset the fall in the output-to-capital ratio by recourse torelative surplus-value – i.e. by reducing the portion of the working dayrequired to reproduce the value equivalent of workers’ money-wages. Tis

will compel rms to attempt to increase the rate of exploitation through the

extraction of surplus-value in its absolute form – for example, by reducing wages, increasing labour-intensity, and extracting longer working hours without a corresponding increase in pay. Te problem is that even in theUS, minimum-wage laws and last-ditch social safety-nets provide someminimal oor below which living standards cannot fall. Furthermore,maintaining the loyalties of salaried cadre charged with oversight of the day-to-day operations of the corporate apparatus requires the redistribution of a

27. Post-Fordist methods include just-in-time inventory-management, dissemination of

Japanese-style managerial techniques to wring slack out of the assembly-line, acceleration of theproduct-cycle through the rational organisation of knowledge creation, and more effi cientsystems of large-scale transport to reduce turnover-time.

8/13/2019 The Rate of Profit and the Problem of Stagnant

http://slidepdf.com/reader/full/the-rate-of-profit-and-the-problem-of-stagnant 28/36

K. Beitel / Historical Materialism 17 (2009) 66–100 93

signicant share of the social surplus to this administrative-managerial stratum.Social limits thus exist on the ability to impose a suffi cient intensication of

the rate of surplus-value in absolute form to offset the decline in the output/capital ratio. In combination with the productivity-slowdown, the result

will be the imposition of barriers to achieving a suffi cient increase in the rateof surplus-value to offset the decline in the output/capital ratio. If recenttrends are in fact indicative of a structural shift in productivity-growth, thisindicates that US capitalism may be poised at the edge of the precipice ofthe next great secular downturn in the prot-rate.

o these factors must be added the looming spectre of ‘peak oil’. Whilemuch dispute remains over the exact state of the global oil-supply, what is

certain is that, at some point in the next ve to fteen years, we will probably witness the end of abundant access to cheap, readily available fossil-fuels.Tis will lead to increases in the costs of energy and raw materials. Risinginput-costs will place additional pressure on prots, triggering ination asrms impose higher mark-ups in an attempt to protect their (nominal)prots. Te result will be the return of cost-push ination. Over the longerterm (twenty-ve years and out), the outcome is far less certain. However, itis not a far-fetched scenario to surmise that the exhaustion of cheap fossil-fuels will require either a signicant reduction in aggregate consumption,

marking the end of an economic régime predicated on unlimited growthand accumulation; or some technological ‘x’ that at present is nowhere onthe historical horizon. 28

Falling prot-rates and resurgent cost-push ination will put the FederalReserve (and the other major Central Banks) between a rock and a hard place.In the short term, the ongoing unwinding of over-leveraged positions in whathave proved to be badly placed bets on non-redeemable mortgage-debt willcontinue to have an impact on liquidity-conditions in the inter-bank capital-market and cause major lenders to ration credit. 29 For some, this has raised

28. Work in Marxist ecology has been slow to recognise the realities of impending exhaustionof cheap sources of fossil-fuel. Te argument regarding ‘peak oil’ is well established and waspowerfully conrmed in the case of the post-1972 decline in production in the contiguous US,as predicted by Hubbert in the late 1950s. Te question is not whether world oil-production willeventually hit a peak, but how soon, and how the capitalist system will adjust. For accounts ofthe peak-oil phenomenon, see Hubbert 1957; Goodstein 2004; Deffeyes 2001; and Campbelland Laherrere 1998.

29. Te subprime crisis unleashed a powerful set of self-reinforcing dynamics that has plungedthe US into a potentially protracted recession. Falling housing prices lead to negative net equity