the power of productivity - london school of economics · the key to unlocking the power of...

TRANSCRIPT

1

ThePowerofProductivity

AnAssessmentofUKFirmsandFactorsContributingtoProductivityEnhancement

DrAlexanderGrous

LondonSchoolofEconomicsandPoliticalScience

December,2016

2

Overview...........................................................................................................................31. UKProductivity:MacroEnvironmentandRegionalVariations.................................51.1 WhatisProductivity?............................................................................................51.2 MeasuringProductivityintheUK..........................................................................62. RegionalProductivityintheUK.................................................................................82.1 NUTS-1(Regionalareas/countygroups)LevelProductivityVariation..................82.2 NUTS-2(Singlecounties):RegionalVariation........................................................92.3 NUTS-3(Cities)RegionalProductivity:GettingGranular.....................................112.4 ManufacturingVersusServicesProductivity.......................................................152.5 ComparingRegionsofDifferentSize...................................................................162.6 GrowthinProductivityacrosstheUK:RegionalVariationbyMajorCities.........172.7 UKBusinessDistribution.....................................................................................202.8 Productivity:HowDoestheUKCompare?..........................................................212.9 UKRegionalProductivityVariations:GovernmentInterventionInitiatives........243. FirmSpecificFactors:DefiningGranularProductivityEnhancingOpportunities....274. ManagementPractices:The‘Lever’forFirm-LevelProductivityEnhancement.....274.1 DefiningManagementPractices.........................................................................274.2 EstablishingBestPractices..................................................................................284.3 AddressingManagementPracticestoOptimiseFirm-LevelProductivity...........294.4 WhyDoesManagementMatter?........................................................................324.5 ComplacencyisnotanOption.............................................................................334.6 ManagingforGrowth.........................................................................................345. InformationandCommunicationsTechnology.......................................................355.1 ICTAdoptionFactors...........................................................................................355.3 ChangingSocioeconomicDrivers........................................................................375.4 EnhancingProductivitywithICT..........................................................................385.5 APortfolioofOptions..........................................................................................405.6 MakingtheRightCall...........................................................................................415.6.1 MobileBroadband:Casestudy-PoliceandEmergencyServices...................425.7 ICTandConnectivity:WiderUseandBenefits....................................................436. FlexibleWorkforcePractices...................................................................................446.1 AnEvolvingWorkplace........................................................................................446.2 BenefitsofFlexibleWorkforcePractices.............................................................466.3 AdoptingFlexibleWorkforcePracticeTechnologicalEnablersforProductivity.47Conclusion.......................................................................................................................49

3

OverviewTheUKdisplaysdifferingproductivityacrossregionsandlagsallbutoneG7country.ThispaperreviewsavailableUKproductivitydatatopresentabackdropofproductivityintheUKandagainstG7countriesbeforedepictingoptionstoaddressfirm-levelproductivity.Thedatadepictsvariedproductivityresultswithsomecities,countiesandregionsperformingaboveorbelowtheUKaverage.FollowingthepresentationofavailableregionalUKproductivityresults,subsequentsectionsinthepaperaddresstheopportunitytoimproveresultsatthefirm-level:unlockingthepowerofproductivityrequiresamoregranularassessmentatthelevelofthefirm.Althoughlocalfactorsmayinfluencesomeaspectsofafirm’soperation,ultimately,afirm’smanagementpracticesarethekeyleverdictatingitsperformance,irrespectiveofitslocation.1Figure1depictstheresearchapproachutilisedinthispaper,withmanagementpracticesintegraltoproductivityenhancement,complementedbyinformationandcommunicationstechnology(ICT)andmobiletechnology,andflexibleworkforcepractices.2Beforetheseareexplored,resultsfromacrosstheUKarepresentedtohighlighttheobservedvariabilityinproductivityandthepotentialtoimprovethis.

FosteringUKProductivityEnhancement

UKproductivitydata(ONS)

LSE&McKinseyandCo,Stamford+,ManagementPracticesresearch:20,000

interviews

AdditionalLSEresearch:Productivityenhancing ICTand

Mobility

LSEandadditionalresearch:ChangingWorkforcePatterns

Figure1:Researchschema

Followingthisreview,therolethatmanagementpracticescanplayinfirm-levelproductivityimprovement is presented,drawingonover adecadeof leading researchby the LSEwithMcKinsey&Company,StanfordUniversity,andmorerecentlyotherparticipants, toassessmanagementpracticesusing aunique toolset developedandapplied in 20,000 interviewswith firmmanagers in 35 countries alongwith the analysis of firmaccounts. Results haveconsistently shown a statistically significant correlation between good practices and firmperformance: well-run companies are in general more productive, profitable, and havehigher sales growth than thosewith inferior practices.3Utilising the conclusions reachedfromtheextendedmanagementpracticesstudies,threecomplementarythreadshavebeenincluded as facilitators to increasing a firm’s performance:management practices,whichrepresents thekeyenablingmode; InformationandCommunicationsTechnology (ICT) and

1Bloom,N.,VanReenen,J.(2004).ManagementPractices,Work–LifeBalance,andProductivity:AReviewofSomeRecentEvidence.OxfordReviewofEconomicPolicy.Volume.22(4);pp:457-482.

2Bloom,Netal.(2011).ManagementPracticesAcrossFirmsandCountries.HarvardBusinessReview.Working-Paper12-052.December09.

3VanReenen,Jetal.(2006)ManagementPractices,Work—LifeBalance,andProductivity:AReviewofSomeRecentEvidence.OxfordReviewofEconomicPolicy(Winter)22(4):pp:457-482.

4

flexibleworkforcepractices,thatwhencombinedwithmanagementpracticescanmaximisepotential productivity enhancement. This paper discusses how these elements can beapplied more effectively by UK firms to optimise their productivity with the extendedresearchconfirmingthatitisn’twhatfirmsdothatmakesthemproductive;it’showtheydoit:4AnapproachforUKcompaniestoassesstheirmanagementpractices,andhowICTcanenableproductivitytobe‘unlocked’,isprovided.Following a review of management practices, this paper addresses flexible workforcepractices and the role that technical factors can play in unlocking productivity. The keyconclusionsummarizedisthatwhensupportedbybestmanagementpracticesandenablingICT, flexible work practices in the firm can result in greater employee well-being andmotivation.Thishasbeenfoundtoresult in lowerabsenteeismanddepartures,whichcanreduce firm-costs: the estimated replacement cost of an employee in the UK is £30k,resultinginanannualcosttotheeconomyofanestimated£4.1billion.5

This report provides a startingpoint for identifyinghow thepowerof productivity canbeunlockedinthefirm.Ifundertakensuccessfully,‘thesumoftheparts’canpotentiallyresultina lift inproductivitybyasmuchas20%6and intheprocess, result inbetterperformingfirms, content employees and regions with improved productivity. Although someoperational improvements can be made faster, more structural results incorporatingtechnological,organisationalandworkforcepracticeschangescantakelonger.The key to unlocking the power of productivitymost often already existswithin the firm:findingitrequirestakingthefirststepsinthisjourney.Thetoolstoenablebetterpractices,appropriate technology adoption and flexible workforce engagement are all readilyavailable.‘Time’maynotbehowever.

4Ibid.5http://www.hrreview.co.uk/hr-news/recruitment/it-costs-over-30k-to-replace-a-staff-member/506776Sadun,R.,etal(2005).InformationTechnologyandProductivity:Itain’twhatyoudoit’sthewaythatyoudoI.T.EDSInnovationResearchProgrammeDiscussionPaper.

5

LabourProductivity(outputperhour)

Output[GrossValueAdded(GVA)]LabourInput[Totalhoursworkedintheeconomy;workers,orjobs]=

=

1. UKProductivity:MacroEnvironmentandRegionalVariations

1.1 WhatisProductivity?

Productivity indicateshowwellresourcesarebeingutilised.7It iscommonlydefinedastheratio of a volumemeasure of output (goods and services) to a volumemeasure of input(labour and capital) used.8Production measures what is produced whilst productivity isconcernedwithhow it isproduced.9Thenotionofproductivity isakeydriverofeconomicgrowthandcompetitiveness10providingessentialperformancemeasurement; internationalcomparisons; the determination of capacity utilisation and living standards, and theforecastingofeconomicgrowth.11Acountry’sability to improve its standardof livingovertimedependslargelyonitsabilitytoraiseitsoutputperworker.12Labour productivity is one of themost widely usedmodes of productivitymeasurement.With labour costs comprising around two-thirds of the overall cost of production of UKeconomicoutput,thismeasureisanimportantindicatorofeconomicperformance.13Labourproductivitymeasuresoutput,asexpressedintermsofGrossDomesticProduct(GDP)GrossValue Added (GVA) (also known as ‘whole economy output’)14divided by labour inputs,utilisinghoursworkedoremploymentlevel.15GVAiscalculatedusingtheincomeapproach,andrepresentsthetotalvalueofgoodsandservicesproduced,minusthecostofproducingthose goods and services: it is a key component of GDP, reflecting the output of theeconomy.16Attheoverarchinglevel,labourproductivitycanbeexpressedinequationform:

Figure2:Labourproductivityequation17

NumerousproductivityindicatorsarecompiledintheUKbytheOfficeforNationalStatistics(ONS)acrossthethreemajorsectorsofProduction,ManufacturingandServices.Theseincludeoutputperworker,outputperjobandhourworked,andGVAperjobfilled

7Koch,M.J.,andandMcGrath,R.G.(1996)ImprovingLaborProductivity:HumanResourceManagementPoliciesdoMatter.StrategicManagementJournal.Vol.17,No.5(May);pp.335-354.

8OECD(2001).Measuringproductivity:OECDManual.Measurementofaggregateandindustrylevelgrowthhttps://www.oecd.org/std/productivity-stats/2352458.pdf

9Coelli,T.J,etal(2005)AnIntroductiontoEfficiencyandProductivityAnalysis.Springer.10Ibid.11McCann,P.(2016).TheUKRegional–NationalEconomicProblem:Geography,globalizationandgovernance.Routledge.

12HouseofCommons(2016).ProductivityintheUK.BriefingPaperNo06492,May.13ONS.StatisticalBulletin:LabourproductivityQ22015.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/bulletins/labourproductivity/2015-10-01

14https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/bulletins/labourproductivity/jantomar2016

15Ibid.16DepartmentforBusinessInnovationandSkills(BIS)(2012).CommentaryonRegionalEconomicPerformanceIndicators.September.https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/16338/12-p162-commentary-on-regional-economic-performance-indicators.pdf

17ONSStatisticalBulletin.RegionalGrossValueAdded(IncomeApproach):December2015.http://www.ons.gov.uk/economy/grossvalueaddedgva/bulletins/regionalgrossvalueaddedincomeapproach/december2015

6

GrossValueAdded(GVA)

OutputSectorsAreasNUTS:TheEconomy,Regions,City

Production

Manufacturing

Services

Outputperworker

Outputperjob

Outputperhour

Unitlabourcosts

Unitwagecosts

NominalGVAperfilledjob

NominalGVAperhourworked

NUTS-0 Country Level

NUTS-1 Group ofcounties/regions

NUTS-2 Singlecounty/region

NUTS-3 City

decreasing

pop

ulationsize

Costs

Productivity

andperhourworked.Unitlabourcostsarealsocollatedasamarkerofinflationarypressuresintheeconomy.18Figure3depictstheselabourproductivityindicators.

Figure3:MajorproductivitycategoriesforregionalUKcomparison

GVAperhourworkedorGVAperjobfilledarethemostrelevantindicatorswhenassessingregionaleconomicperformance.Ofthesemeasures,GVAperhourworkedisrecommendedasittakesintoconsiderationregionallabourmarketstructuresanddifferentworkingpatterns,suchasthemixofpart-timeandfull-timeworkers,homeworkersandjobshares.19ThisreportutilisesthesetwomeasuresandotherstooutlineproductivityintheUK.

1.2 MeasuringProductivityintheUK

Productivity indicators in the UK are compiled by the ONS using the Nomenclature ofTerritorial Units for Statistics (NUTS) and adopted throughout the EU since 2015.20Thisdivides a country into NUTS segments, with population criteria defining the size of each.Foursegmentsareutilisedcommencingatthemacroeconomiclevel,denotedbyNUTS-0,toNUTS-3, reflecting an individual city,withproductivitydata compiled for eachof thesebytheONSasdepictedinFigure4.

Figure4:NUTSsegmentationforproductivitydata(Source:ONS)21

ThirteenNUTS-1,2241NUTS-2and169NUTS-323areasexistfortheUK.The13NUTS-1areasaredepictedinTable1.

18ONSStatisticalBulletin.LabourProductivity:JantoMar2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/bulletins/labourproductivity/jantomar2016

19ONS.2016.AReviewofRegionalandSub-RegionalProductivityStatistics.https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/areviewofregionalandsubregionalproductivitystatistics/2016-04-06#note-on-gva-per-head

20https://www.destatis.de/Europa/EN/Methods/Classifications/OverviewClassification_NUTS.html21Ibid

7

Perhourworked

AverageUKGVA:

Perjobfilled

Otherindicators

BaseProductivity Base

Productivity

EnhancedProductivity

Table1:NUTS-1areasintheUK(Source:ONS)24

Table2providesanexampleofaNUTS-1areacascadedintoNUTS-2andNUTS-3areasasappliedbytheONStodefineregionalproductivityintheUK.

NUTS-CodesRegion NUTSlevel CodeUnitedKingdom NUTS-0 UKYorkshireandtheHumber NUTS-1 UKEWestYorkshire NUTS-2 UKE4Leeds NUTS-3 UKE42

Table2:ExampleofNUTSclassificationintheUK(Source:ONS)25

ThisresearchexaminesNUTS-1-3categoriesfromtheONStopresentregionalproductivityintheUK,asdepictedinthemethodologyinfigure3andsummarisedbelowinFigure5.

Figure5:Regionalproductivityandenhancementmodes

22ONSDataset:LabourProductivity:Tables1-10andR1.https://www.ons.gov.uk/file?uri=/employmentandlabourmarket/peopleinwork/labourproductivity/datasets/labourproductivitytables110andr1/current/lprod01q12016unlinked.xls

23SubregionalProductivity:LabourProductivity(GVAperhourworkedandGVAperfilledjob)indicesbyUKNUTS2andNUTS3subregions.https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/datasets/subregionalproductivitylabourproductivitygvaperhourworkedandgvaperfilledjobindicesbyuknuts2andnuts3subregions

24ONSDataset:LabourProductivity.Opcit.25Ibid.

NorthEastNorthWest

YorkshireandtheHumberEastMidlandsWestMidlandsEastofEngland

LondonSouthEastSouthWestEnglandWales

ScotlandNorthernIreland

Others

BestManagementpractices

ICTuse

Workpattern

+

+

+

Enhancingmodes

Regionalproductivity

8

RegionalproductivitydataformthebasisfortheconsolidationofLSEresearchandotherresearchonproductivityoptimisation.2. RegionalProductivityintheUK

2.1 NUTS-1(Regionalareas/countygroups)LevelProductivityVariationTheUKdisplaysregionalvariationsinproductivity.26AttheNUTS-1level(groupofcounties),thisvariationisevidentwhenreviewingGVAperjobfilledandperhour,aspresentedinGraph1forthemostrecentlyavailabledatain2014.

Graph1:LabourproductivitybyNUTS1regionorcountry,2014

Source:ONS27GVAhoursperfilledjobandperhourworkedin2014werehigherthantheUKaverageinLondon(30%higher)andtheSouthEast(9%higher)andlowerthantheUKaverageinotherareas.28InWalesandNorthernIrelandproductivitywas17%and19%belowtheUKaveragerespectively,whilstinScotland,productivitywas2%belowtheUKaverage.Theremainingregionshadproductivitylevelsbetween9to13%belowtheUKaverage.29Theresultsarerelativelyconstantovertime,withGraph2depictingproductivityoveraseven-yearperiodfrom2007-2014forthemostproductiveregions.

26Ibid.27ONS.AReviewofRegionalandSub-RegionalProductivityStatistics.April2016.https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/areviewofregionalandsubregionalproductivitystatistics/2016-04-06#local-enterprise-partnerships-and-city-regions

28Ibid.29Ibid.

9

Graph2:UKNUTS1regionsandcountrieswithhighestGVAperhourworked,1997to2014Source:ONS30

ThehigherproductivitygrowthofLondonwasdrivenbya38%increaseinproductivityhours,withitsshareofUKGVAincreasingfrom18.9%to22.5%from1997to2014.31

2.2 NUTS-2(Singlecounties):RegionalVariation

AllfiveNUTS-2regionsintheGreaterLondonareawereamongthe10mostproductiveintheUKintermsofGVAperhourworked,withproductivitylevelsabovetheUKaverage.InnerLondonEastshowedthehighestproductivitylevel,withaGVAperhourworkedaround38%higherthantheUKaverage.ThiswasfollowedbyInnerLondonWestwithamarginallysmallerproductivitylevel.OnlytwootherregionsachievedGVAperhourworkedabovetheUKaveragebetween1997-2014:EastofEnglandandtheSouthEast.ThevariationbetweenareascanbereviewedattheNUTS-2level.Graph3reflectstheGVAperhourworkedforthetop10areasinNUTS-2.

Graph3:GVAperhourworked-highestrankingUKNUTS2sub-regions,2014Source:ONS32

30ONS.AReviewofRegionalandSub-RegionalProductivityStatistics.April2016.https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/areviewofregionalandsubregionalproductivitystatistics/2016-04-06#local-enterprise-partnerships-and-city-regions

31Ibid.

10

Incontrast,Graph4depictsthe10NUTS-2areaswiththelowestproductivitywiththisrangingfrom12%to20%lowerthanthenationalaverage.

Graph4:GVAperhourworked-lowestrankingUKNUTS2sub-regions,2014Source:ONS33

Althoughthelowerrankedareasarepredominantlylocatedinruralareas,urbanareasarerepresentedincludingSouthYorkshireandWestMidlands.SelectedcitiesacrosstheNUTSsubregionsreinforcethedisparateproductivitypicturefortheUK,asdepictedinGraph5.

Graph5:GVAperhourworked–SelectedCities2014

Source:ONS3432ONS.AReviewofRegionalandSub-RegionalProductivityStatistics.April2016.https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/areviewofregionalandsubregionalproductivitystatistics/2016-04-06#local-enterprise-partnerships-and-city-regions

33ONS.AReviewofRegionalandSub-RegionalProductivityStatistics.April2016.https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/areviewofregionalandsubregionalproductivitystatistics/2016-04-06#local-enterprise-partnerships-and-city-regions

11

LondonexhibitsthehighestlabourproductivityintheUK,at30%abovethenationalaveragein2014,followedbyAberdeenwith17%higherthanthenationalaverageandBristolataroundthenationalaverage.Othermajorcitiesdisplaylabourproductivity7-14%lowerthanthenationalaverage.2.3 NUTS-3(Cities)RegionalProductivity:GettingGranularProductivitymeasuresatthemostgranularlevelarerepresentedbyNUTS-3measures,withnominalGVAperhourworkedutilisedbytheONSforEngland,ScotlandandWales.ForEngland,4regionsareassessed:GreaterLondon,SouthofEngland,Midlands,NorthofEngland.Graph6depictstheproductivityforLondon,withallsubregionsdisplayingproductivitylevelsabovetheUKaverage.ThemostproductivesubregionwasTowerHamlets(whichincorporatestheCanaryWharffinancialdistrict),followedbyCamdenandtheCityofLondon,withproductivitylevelsof85%and43%abovetheUKaveragerespectively,withthesetwosubregionsthemostproductiveintheUK.Fromthetotal168NUTS-3subregions,48hadaGVAperhourworkedabovetheUKaverage,withjustunder50%ofthisnumberlocatedinLondon.

Graph6:NUTS-3GVAperhourworkedLondon

Source:ONS35

34ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalprodutivity/march2016

35ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalproductivity/march2016

12

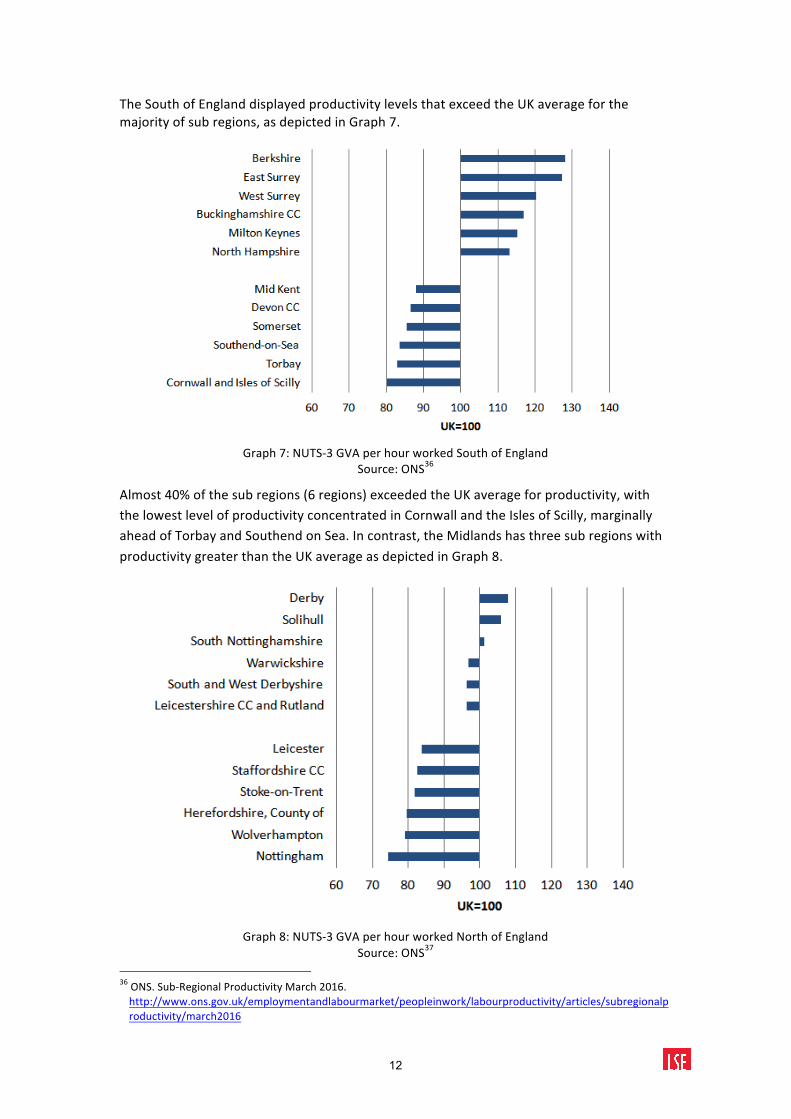

TheSouthofEnglanddisplayedproductivitylevelsthatexceedtheUKaverageforthemajorityofsubregions,asdepictedinGraph7.

Graph7:NUTS-3GVAperhourworkedSouthofEngland

Source:ONS36

Almost40%ofthesubregions(6regions)exceededtheUKaverageforproductivity,withthelowestlevelofproductivityconcentratedinCornwallandtheIslesofScilly,marginallyaheadofTorbayandSouthendonSea.Incontrast,theMidlandshasthreesubregionswithproductivitygreaterthantheUKaverageasdepictedinGraph8.

Graph8:NUTS-3GVAperhourworkedNorthofEngland

Source:ONS3736ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalproductivity/march2016

13

OnlythreesubregionsdisplayproductivityabovetheUKaverage:Derby,SolihullandSouthNottinghamshire,at8%,6%and2%respectively.Thedistributionofsubregionsregisteringproductivityofbetween25%lowerthantheUKaveragewassimilartothedistributionfortheSouthofEngland.AmarginallyhigherproportiondepictedalowerproductivitythantheSouthofEngland.ThistrendwasalsomirroredintheproductivityofScotland,withonlythreesubregionsdisplayingproductivityabovetheUKaverageforAberdeenCityandAberdeenshire,EdinburghandSouthAyrshireof17%,5%and3%respectively.Graph9depictsthisdistribution.

Graph9:NUTS-3GVAperhourworkedNorthofScotland

Source:ONS38

IncontrasttoallotherNUTS-3regions,WalesdepictsproductivitylowerthantheUKaverageforallsubregions,rangingfrom8%lowerfortheCentralValleyto33%lowerforPowys,asdisplayedinGraph10.

37ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalproductivity/march2016

38ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalproductivity/march2016

14

Graph10:NUTS-3GVAperhourworkedNorthofWales.

Source:ONS39

ThefinalNUTS-3regiontobecomparedisNorthernIreland,withthisareadisplayingasimilartrendtoWales:allsub-regionsdisplayedproductivitylevelslowerthantheUKaverage,asdepictedinGraph11.

Graph11:NUTS-3GVAperjobfilledIreland.

Source:ONS40

ThemostproductiveregioninNorthernIrelandwasBelfast,whichdisplayedproductivitylevelsof8%lowerthantheUKaverage,increasingto20%lowerfortheNorthofNorthernIreland.AcomparisonoftheNUTS-3regionsindicatestherelativedifferencesinproductivitybetweenregionalareasforsubregionsaboveandbelowtheUKproductivityaverage,asdisplayedinGraph12.

39ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalproductivity/march2016

40ONS.Sub-RegionalProductivityMarch2016.http://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/subregionalproductivity/march2016

15

Graph12:NUTS-3GVAperhourworkedcomparison:aboveandbelowUKaverageSource:ResearchTeamconsolidationofdatafromONS41

2.4 ManufacturingVersusServicesProductivity

Atanaggregatelevel,UKproductivityvariesbetweenManufacturingandServices.NUTS-3providesblendeddatafrombothareasforGVA,hoursworkedandemployment(‘jobs’).Inthecaseofmanufacturingproductivity,Graph13depictstheinitialdeclineinproductivitybetween2008and2009.ThissituationhadreversedbyQ22011,whenallsub-industriesdisplayedpositiveresultsandproductivitywas6.6%higherthaninQ12008.A‘see-saw’hasbeenobservedsincemid-2011however,withrisesandfallsobserved,withthelatestdatain2016indicatingariseinmanufacturingjobsandGVA.

Graph13:Manufacturingproductivitymeasures

Source:ONS42

ThesamecriteriaareutilisedtodefineproductivityforServices,depictedinGraph14.41https://www.ons.gov.uk/methodology/geography/ukgeographies/eurostat#relationship-of-nuts-areas-to-uk-administrative-geographies

42https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/bulletins/labourproductivity/aprtojune2016#manufacturing-labour-productivity-measures

16

Graph14:Servicesproductivitymeasures

Source:ONS43

ProductivityhasimprovedinServicesacrossallthreeindicators,althoughtheseinitiallytrendeddownwardsbetween2008-2009,beforepickingupinQ3.In2015,growthoccurredintheseandeightofthe11serviceindustriestheGovernmentutilisesfor‘Servicesproductivity’,withanoverallupturnoccurring.

2.5 ComparingRegionsofDifferentSize

GVAperheadprovidesacomparisonofresultsbasedonpopulation.ItdividesGVAinmillions(£)bythepopulationofaregiontogiveGVAperheadinpounds.ThisprovidesamodeforcomparingregionsofdifferentsizesbutisnotameasureofregionalproductivityasthismethodutilisestheentirepopulationtoderiveGVAperhead,includingsegmentsofthepopulationwhoarenoteconomicallyactive.GVAperheadprovidesanadditionalmeansofcomparingregionsofdifferentsize.Map1depictstheUKNUTS-1GVAperregionassegmentedbytheONS.RegionsindarkercolourindicatehigherGVAperhead,withLondonindicatingthehighestshareofGVAperhead,atover22%,followedbytheSouthEastatalmost15%,andthelowestsharefromNorthernIrelandatjustover2%.44

Map1:RegionalGVAperheadbyNUTS12013(Source:ONS45)

43https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/bulletins/labourproductivity/aprtojune2016#manufacturing-labour-productivity-measures

44RegionalGrossValueAdded(IncomeApproach):December2015

17

ThemapindicatesthataconcentrationofhigherGVAperheadexistsintheSouth,withthisdecreasinginsomeNorthernareas.KeyregionalGVAperheadindicatorsare:

• London’sGVAperheadwas£42,666in2014:thehighestintheUK.• Wales’GVAperheadwas£17.573:thelowestintheUK.• GreaterLondondisplayedthehighestGVAperheadgrowthrates,at7.4%.• OnlyoneUKregiondisplayedadecreaseinGVAperheadin2014:CornwallandIsles

ofScillywith0.1%fall.

Graph15summarisestheproportionofGVAperheadbyregionoftheUKtotal.

Graph15:NUTS1percentageshareofUKGVA,2013

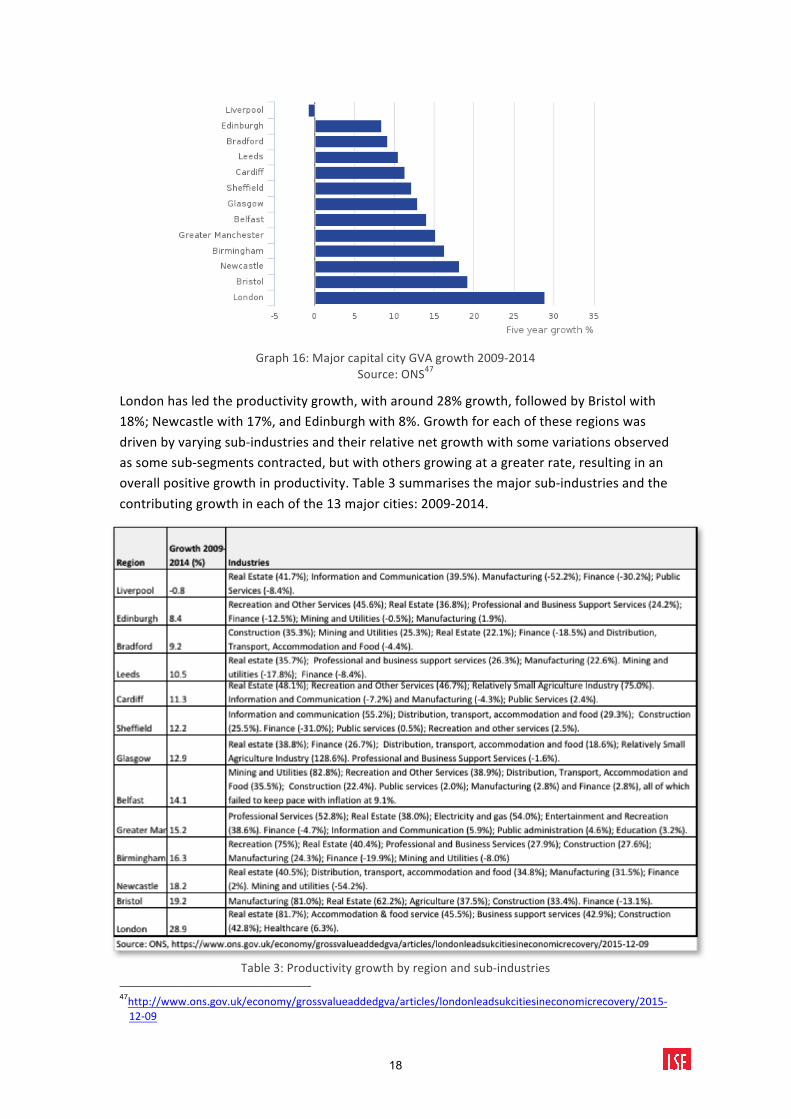

Source:ONS462.6 GrowthinProductivityacrosstheUK:RegionalVariationbyMajorCitiesProductivitychangehasshownamixedpictureacrosstheUK.Between2009-2014totalGVAgrewforallmajorcapitalcitiesexceptforLiverpool.Graph16depictsthetotalGVAfor13majorcapitalcitiesacrossUKregions.

45ONS(2014):RegionalGrossValueAdded.http://www.ons.gov.uk/economy/grossvalueaddedgva/bulletins/regionalgrossvalueaddedincomeapproach/2014-12-10

46Ibid

18

Graph16:MajorcapitalcityGVAgrowth2009-2014

Source:ONS47

Londonhasledtheproductivitygrowth,witharound28%growth,followedbyBristolwith18%;Newcastlewith17%,andEdinburghwith8%.Growthforeachoftheseregionswasdrivenbyvaryingsub-industriesandtheirrelativenetgrowthwithsomevariationsobservedassomesub-segmentscontracted,butwithothersgrowingatagreaterrate,resultinginanoverallpositivegrowthinproductivity.Table3summarisesthemajorsub-industriesandthecontributinggrowthineachofthe13majorcities:2009-2014.

5

Table3:Productivitygrowthbyregionandsub-industries47http://www.ons.gov.uk/economy/grossvalueaddedgva/articles/londonleadsukcitiesineconomicrecovery/2015-12-09

19

Themajorcapitalcities’GVAreflectsbothlocalfactorsaswellasnationalinfluences.48Thisthemewillbeexploredinthesubsequentsectionofthispaper.Keyvariationsbetweentheregionsinclude:

• LondonhasthehighesttotalGVAcontributionfromFinanceofanyregion.• LondonalsohasthehighestcontributionfromProfessionalandBusinessSupport

Services,andInformationandCommunication,marginallyaheadoftheSouthEast,butthelowestcontributionfromManufacturing;Construction;Agriculture,MiningandUtilities,andPublicServices,ofanyotherregion.

• TheNorthEastdisplayedthehighestcontributionfromPublicServices.

Theproductivity‘snapshot’providedbyboththeregional(NUTS-1)dataandforthecapitalcitiesdepictsthevariationintotalGVA.ConsiderabledebateandresearchhasoccurredontheUK’sproductivity.ThispaperreviewscontributingfactorstoproductivityimprovementfromleadingresearchfromtheLSEandothersources,todefineoptionsforbestpracticeswithsomefurtherdiscussionoffurtherpotentialcontributingfactorstoregionalvariationsinproductivity.

Graph17:CompositionofindustriesunderpinningtotalGVAinNUTS-1regions,2014

Source:ONS49

48Body,M,etal.,(2005).Regionalproductivitydifferentials:explainingthegap."DiscussionPapers515.

20

2.7 UKBusinessDistributionz

Smalltomediumenterprises(SMEs)accountfor99.3%ofallprivatesectorbusinesses;employ15.6millionpeople(60%ofallprivatesectoremployment),andgenerate£1.8trillioninrevenues(47%ofallprivatesectorrevenues).50Incontrast,MediumUKbusinesscomprise0.6%ofthetotalnumberofbusiness,andLargefirms0.1%,buttheyaccountfor12and40%oftotalemploymentrespectively,and14and53%oftotalturnover.51Graph18depictsUKbusinessesperheadofpopulationshowingtheunevendistributionacrossterritories.Londoncontainsthehighestdensityat1,464businessesper10,000residents,versus679businessesintheNorthEast,thelowestdensity.

Graph18:Numberofbusinessesper10,000residentadults,2016Source:HouseofCommonsBriefingPaperNo06152,26October2016.

Graph19depictsthedistributionofpercapitabusinessesagainsttheabsolutenumber.2

Graph19.NumberofbusinessesandbusinessdensityrateintheprivatesectorbyEnglishregionandUKcountry(beginningof2015)

Source:DepartmentofBusinessInnovationandSkills.StatisticalRelease.BusinessPopulationEstimates2015.5249ONS,(2015).StatisticalBulletin.GrossValueAddedIncomeApproach,December.50https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/467443/bpe_2015_statistical_release.pdf

51Ibid.52Ibid.

21

ThedistributionoffirmsisskewedtoLondonandtheSouthEast;followedbyagroupcomprisingtheNorth,SouthandEastofEngland;afurthergroupcomprisingWestMidlands,YorkshireandtheHumberandEastMidlands,andtheNorthEast.Severalobservationscanbemadefromtheregionalproductivityresults:(i)lowerproductivitywasobservedinmanyoftheregionswithlowerbusinessdensity(GVAperhourworked)andviceversa;(ii)manyoftheseregionsdisplaylowerproximityto‘economicmass’.Thereisapotentialtoenhanceproductivitythroughreducedjourneytimes:

1. Estimatesindicatethata10%reductioninaveragejourneytimesthroughouttheUKcouldraiseproductivityby1.12%.53

2. Thisrangesfromamaximumof2.22fortheEastofEngland;1.73%forWestMidlands;1.66%forEastMidlands;1.57%forWales;1.55%forScotland;1.45%forYorkshireandHumberside.

IncontrastLondonwouldbenefitbyanestimatedmaximum1.08%reflectingitsalreadyhighdensity.Thebenefitisgreatestwhereaccesstocitiesincreasesthemost.54Thisraisessocioeconomicconsiderationsforlongterminfrastructureandtransportinvestment.

2.8 Productivity:HowDoestheUKCompare?

Theglobalbankingcrisisof2008precipitatedwhathasbecomeknownasthe‘GreatRecession’acrossdevelopedcountries.TheUK’stwodecadesofconsistenteconomicgrowthleadinguptothiseventwereextinguishedalmost‘instantly’,withoutputperhourstaying0.4%belowthepre-recessionlevelof2007.55LabourproductivityintheUKwas15-16%lowerthanwhereitwouldhavebeenhadtherecessionnotoccurred,equatingtoaproductivitygapofaround6%fortherestoftheG7countries:Canada,France,Germany,GreatBritain,Italy,Japan,andtheUnitedStates.56Bothoutputperhourandoutputperworkerhavenotshownsignificantimprovementsince2007,incontrasttotheUS,wheretheyhavegrownandarearound7%higherthanin2007.57Onlyonethirdofthevariationinlabourproductivityissuggestedasbeingattributabletothereallocationoffactorsofproductiontomoreproductivesectors,executedthroughthemovementoflabourandtheentryandexitoffirms.58

UKfirmsshowahighersensitivitytotheavailabilityoffinancethanfirmsinmanyotherEuropeancountries:59Anincreasedcostoffinancecanleadtothesubstitutionoflabourforcapital,drivingreducedlabourproductivitygrowth.Althoughthisisacontributingfactortolowerproductivity,itisnottheprimaryreasonforthis.Firmbehaviourhasbeenidentifiedastheprimaryfactorincontributingtolowerproductivityaftertherecession.60Post-

53Rice,P.,andVenables,T.,(2004)opcit.54Ibid.55Bryson,A.,andForth,J.,(2015).TheUK’sProductivityPuzzle.OccasionalPaper45.CentreforEconomicPerformance.LondonSchoolofEconomicsandPoliticalScience.

56Ibid.57OfficeforNationalStatistics(ONS).(2015).InternationalComparisonsofProductivity:FinalEstimates,2013.ONSStatisticalBulletin.February.

58Bryson,A.,andForth,J(2015).Opcit.59Bond,S.,etal.(2003).FinancialFactorsandInvestmentinBelgium,France,GermanyandtheUnitedKingdom:AComparisonUsingCompanyPanelData.ReviewofEconomicandStatistics.Vol.85;pp.153-165.

60Riley,R.,etal.(2014).TheFinancialCrisis,BankLendingandUKProductivity:SectoralandFirm-levelEvidence.NationalInstituteEconomicReview.No.228:R17-R34.

22

recession‘cleansing’(theentryandexitoffirms)hasalsonotbeenfoundtobeaprimarycontributingfactortolowerproductivity:61EvidencefromJapanindicatesthatwithin-firmfactorsweretheprimarycauseforweakproductivitygrowthversusanabsenceofthecleansingeffectsofrecession.Graph20providesacomparisonofproductivitymeasuredbyGDPperhoursworkedacrossG7countries.

Graph20ComparisonofGDPperhourworkedbetweentheUKandotherG7countriesSource:ONS62

TheUKillustrateslowerproductivitythanallcountriesexceptforJapan.ItlagsGermanyby36%,andtheUSandFrancebyaround30%.Itisalso10%lowerthanItalyand4%lowerthanCanada.Graph21providesfurtherdataonthevaryinghoursworkedbetweencountries.

61Griffin,N.,andOdaki,K.(2009).ReallocationandproductivitygrowthinJapan:Revisitingthelostdecadeofthe1990s.JournalofProductivityAnalysis.V3;pp:125-136.

62ONS.InternationalComparisonsofProductivity-FinalEstimates:2014.http://www.ons.gov.uk/economy/economicoutputandproductivity/productivitymeasures/bulletins/internationalcomparisonsofproductivityfinalestimates/2014

23

Graph21:ComparisonofaverageweeklyhoursworkedperG7countrySource:ONS63

In2014,USworkersworkedthemosthoursperweek,followedbyJapan,Canada,andtheUK.Anoveralldownwardstrendcanbeobservedacrosscountriesforhoursworked,withtheUKdisplayingamarginalrise.ComparedwiththeG7theUK:64

• hasthesecondlowestGDPperhourworked;• rankssecondlowestforproductivitygrowthsince2007;• lagsinproductivitycomparedwiththeeconomiesoftheUS,Germany,Franceand

Italyinallsub-sectorsandparticularlyinmanufacturing;• lagstheproductivityofFrance,ItalyandtheUSinfinancialservices;• lagsininoutputperhourbehindFrance,GermanyandtheUSforprivatenon-

financialservices.

An assessmentof firm-specific factors canprovide insight into elements that can improveproductivity,with threeareas that could contribute to this: (1)managementpractices; (2)useoftechnology;(3)flexibleworkforcepractices.65Inaddition,researchhasindicatedthatsome other contributing factors could also exist such as firm-location, but ultimately, afirm’smanagementpracticesarethekeylevertoimprovingproductivity.66Thesefactorswillbe reviewed in this paper to identify areas that have the potential to improve a firm’sproductivity.Researchhas indicated thatwell-run firmsperformbetter irrespectivewheretheyarelocated.67

63Ibid.64Ibid.65Bloom,N.,andVanReenen,N.(2007).MeasuringandExplainingManagementpracticesacrossfirmsandnations.QuarterlyJournalofEconomics.Vol:122(4);pp:1351-1408.

66Rice,P.,andVenables,A.J.,(2004).SpatialDeterminantsofProductivity:AnalysisfortheRegionsofGreatBritain.CEPDiscussionPaperNo642.CentreforEconomicPerformance.LondonSchoolofEconomicsandPoliticalScience.

67Bloometal,(2007).Opcit.

24

2.9 UKRegionalProductivityVariations:GovernmentInterventionInitiatives

TheUK’sdisparateproductivityperformancebetweenregionshasbeenreviewedinUKParliament68andbeenthesubjectofGovernmentplanstoaddress.69Tostimulateproductivityandattempttocreateamorebalancedscenario,15productivity-enhancinginitiativeshavebeendefinedforthelongtermaswellasthenearterm(‘dynamic’):70

Longterminvestment:

(1) Cuttingcorporationtaxto18%by2020(2) Investmentandsavingsincentivestostimulatebusinessinvestment(3) UpgradeUKskills,whichhavebeenidentifiedasanareaofweaknessand

impedimenttoproductivity(seebelow)(4) Improvingaccesstouniversitiestoenhanceskillsandprovidinggreateropportunity

forinstitutionstodefinefeesandothervariables(5) Addressingthetransportsystemwithadditionalinvestmentininfrastructureand

theappointmentofadditionalindividualstooverseeareas(6) Createinvestmentopportunitiesforlowcarbon-energyandreviewbusinessand

consumerenergybills(7) Continueexpansionofdigitalinfrastructurewithimprovedspeedstotheconsumer

andforbusinessesincludingfixedandmobile(8) Deliver£6.9billiononsciencecapitalandestablishcommercialisationcentresand

fosteruniversitycollaborativefacilities

DynamicEconomy:

(9) Improvingplanningfreedomtostimulategreaterhousinginvestment(10) Reducingwelfarecostandintroducehigherpay(11) Increaseemploymentandreducedisabilityemploymentgap(12) Continuetoreformfinancialservicesthroughregulatoryandindustryengagement(13) Openvariousmarketsupfurtherthroughreducedadministration(14) Focusonstimulatingexportsfurther(15) RebalancingNorth-Southeconomicimbalancethrough£13billioninvestmentin

‘NorthernPowerhouse’

ManyoftheseinitiativesseektoaddressseveralfactorsbelievedtocontributetoregionalproductivityvariationscapturedwithinNUTS-3data.71ThevariationsinproductivityacrossUKregionsdepictedintheearlierportionofthisreportcouldbedrivenbythethreeeffectsdepictedinFigure6.

68HMTreasury.Fixingthefoundations:Creatingamoreprosperousnation.July2015.69HouseofCommonsBusiness,InnovationandSkillsCommittee:TheGovernment’sProductivityPlan.SecondReportofSession2015–16.

70HMTreasury.Fixingthefoundations:Creatingamoreprosperousnation.July2015.71Rice,P.,andVenables,J.(2004).Opcit.

25

Benefitsofbeingclosertoeconomicmass:

• Knowledgespillover• Thicklabourmarkets• Closeproximitytosuppliersandcustomers

àDoublingeconomicmassanareahasaccesstoraisesproductivityby3.5%

àBelowaverageaccesstocitiesequalspoorerperformance

• 10%riseindegrees=1%riseinproductivity

• 10%increasewithoutdegree=0.7%lowerproductivity

Figure6:EffectcontributingtoregionalproductivityvariationsSource:Rice,P.,andVenables,(2004)72

Thethreeeffectsdepictedaspotentiallycontributingtoregionalproductivityvariationinclude:

(1)Alreadyproductiveareasinfluenceearningsthroughthecreationandattractionofhigherpayingjobs,oftenrequiringgreaterskillsandcomplexity-thiscreatesfurtherdemand;(2)Proximitytolargercities,orareaswithaconcentrationoffacilities(‘economicmass’)canraiseincomeandproductivity,withthedensityofactivityhavingbeenshowntohaveapositiveeffectonproductivity;(3)Themixofeducationinthepopulation,withahigherproportionoftheworkingpopulationhavingdegreesincreasingproductivity.73Researchindicatesthatbenefitsalsoexistinfirmsbeingcloserto‘clustered’cities,orlocationsofconcentratedindustriesintermsofknowledgetransferbetweenindividualsandorganisationstofosterproductivityandinnovation.74Estimatesarethata10%reductioninaveragejourneytimesintheUKcouldraiseproductivityby1.2%to2.4%dependingonthedensityoftheareas.75BelowaverageaccesstocitieshasbeenestimatedtobeacontributingfactortothepoorerperformanceofregionsofScotland,Wales,theSouthWestandNorthEast.76Atrendtowardsmoreflexibleworkingpracticescouldassistinovercomingsomechallengesofdistance,withsomeGovernmentdigitalinitiativesalsoaimedatupgradingdigitalskills.77

72Ibid.73Ibid.74Muro,M.,andKatz,B.,(2010).TheNew‘ClusterMoment’:HowRegionalInnovationClustersCanFostertheNextEconomy,inEntrepreneurshipandGlobalCompetitivenessinRegionalEconomies;Chapter5;pp:93-141.Emerald.

75Rice,P.,andVenables,J.(2004).Opcit.76Rice,P.,andVenables,J.(2004).Productivity:understandingregionaldifferences.CEPDiscussionPaper162.CentreforEconomicPerformance.LondonSchoolofEconomicsandPoliticalScience.

77http://www.gov.scot/Resource/0044/00448804.pdf

• Highproductivityareasbenefitfromalargershareofjobsinhighpayingoccupations

1. Productivitydrivesspatialvarianceinearnings(Occupational):66%ofUKspatialvariationinearningisattributabletovariationsinproductivity

2. Proximitytoeconomicmassraisesincome:Averageearningsincreasewhenaccessto‘economicmass’iswithincloserproximity

• Travelwithin40minutesdrivingtimemaximisesproductivityopportunity.

• Noeffectbeyond80minutesdrivingtime

3. Educationalqualificationsdrivehigherproductivity:Regionalproductivityvariationisaffectedbythedegreeofeducationattained.

• Increasingthe%ofwork-forceeducatedto1stdegreelevelandreducing%withsub-degreesraisesproductivity

26

TheoptionsavailabletodiminishsomeoftheproductivityvariationshighlightedarestructuralandpotentiallyareaffectedbyGovernmentpoliciesoutlinedinthissectionbothforlongertermgrowthandinadynamiccapacity.Managersdictatelocationandundertakerecruitmenttoattaintherequiredmixofskillsandqualificationsfortheorganisation,whilstindividualsmakechoicesonwheretowork,commuting,andtheeducationtheyattain.Suchdecisionsareoftencomplexandensconcedwithinbroadersocial,financial,andotherconsiderations.Firmsandindividualsmaydirectlyfactormassproximityintotheirdecisionsorinothercases,thisisasecondaryfactor.

27

3. FirmSpecificFactors:DefiningGranularProductivityEnhancingOpportunities

Firm-specificfactorshavebeenshowntoenhanceproductivity.78Threeareashavebeenreviewedinthelastsectionsofthisreport,andtheopportunitiestoenhanceproductivitypresented,basedonappliedresearchthathasoccurred.Insomecases,theresultsobtainedhavebeenstatisticallysignificant:adoptionofattributes,suchasgoodmanagementpractices,haveshownastatisticallysignificantcorrelationwithfirmperformance.79Inotherwords,betterperformingfirmsarebetterrun.ThethreeareasoutlinedinFigure7willbereviewedinthesubsequentsectionsofthisreporttodefineopportunitiesthatcanenhancefirmlevelproductivity:managementpractices;changingworkforcepractices;ICTandmobility.

FosteringUKProductivityEnhancement

LSE&McKinseyandCo,Stamford+,ManagementPracticesresearch:20,000

interviews

AdditionalLSEresearch:Productivityenhancing ICTand

Mobility

LSEandadditionalresearch:ChangingWorkforcePatterns

Figure7:Reviewingfirm-levelareastoenhanceproductivity

Whilsta‘onesizefitsall’modelforproductivityenhancementdoesnotexist,firmscanadoptarangeofpracticesandstrategiesthatmaximisethepotentialforsuccessintheirspecificenvironmentandcompetitivescenario.

4. ManagementPractices:The‘Lever’forFirm-LevelProductivityEnhancement

4.1 DefiningManagementPractices

“Humanfactorsaremorelikelytocausefailurethanhardwareandsoftwaredeficiencies.”

Howland,2000

Theterm‘managementpractices’lacksaconcretedefinition.Theconceptcanbestbereviewedasanamalgamationofitstwoprincipalparts:

“Management”:80theprocessofleadinganddirectingallorpartofanorganisationthroughthedeploymentandmanipulationofresources.

“Practice”:81theactualapplicationofaplanormethod,asopposedtothetheoriesrelatingtoit.

Thenotionofmanagementpracticesisbroad,butcan,atafundamentallevel,bedefinedaswhatanorganisation’smanagersdo:howtheyplan,deliver,andutilisethefirm’sassets,bothhumanandcapital.Managersare‘influencers’intheuseofthefirm’sassetswithresearchhighlightingthat,“topexecutivesvaryconsiderablyintheirmanagementstyles….raisingquestionsastowhymanagersmaybehavesodifferentlyinapparentlysimilar

78Ibid.79Bloom,N.,andVanReenen,N.(2010).WhyDoManagementPracticesDifferacrossFirmsandCountries?JournalofEconomicPerspectives.Vol:24(1);pp:Pages203–224.

80en.wikipedia.org/wiki/Management81http://www.askoxford.com/concise_oed/practice?view=uk

28

economicenvironments.”82Firmsachievingbetterperformancehavebeenfoundtobebettergovernedingeneral,withmanagersalsooftenreceivinghighercompensationasanincentivetomaximiseperformance.83Thefirm’sCEO/Managerplaysacrucialroleindrivingthefirm’sperformance,strategy,andsetting‘acceptablepractices’.84Notwomanagersarealike,withCEOs/Managersinterpretingthesameenvironmentdifferently,andtheseinterpretationsleadingtothedevelopmentofspecificpoliciesandactions.Thesedifferencesultimatelyaffectorganisationalperformance.85Managementpracticesaremorethantheattributesoftopmanagershowever;overtimetheyformpartoftheorganisationalstructureandbehaviourofthefirmandadoptedintheorganisation.86

Managerialpracticescanbestrategicandincludebusinessplans;visionstatements;memos;technologyplans;memosandpresentations(ibid),ortheycanbeoperational.87Theycanincludeabroadrangeofactivitiesincluding:HRpractices;Productionpractices;Financialpractices;otherfunctionalpractices(Marketing;Operational;others).Appropriateandwell-executedpracticesareparticularlyrelevantforUKmanagersconsideringslowergrowthintheUK-followingtherecentrecessionandtheUK’slaggingG7positioninproductivity,asoutlinedintheprevioussectionsofthisreport.

Theabilityofmanagerstoembraceandadapttonewtechnology;engageininnovation,andaddressprocessesandelements,canimprovetheircompetitivepositionandproductivity.88Themaininhibitorsfortheexploitationofnewtechnologiesmostoftenappeartobealackofknowledge,poormanagementskillsandqualificationsforbothentrepreneursandemployees.89Adoptingbestpracticesinthefirmisarguablythemostinfluentialandrelevantmeansofimprovingitsproductivityandpositioningitforlong-termsuccess.90UKRegionsreflectaheterogeneousmixoffirmsoperatingwithineach,representingthesectorsdefinedearlierinthisreport.WithUKproductivity18%belowtheaverageoftheotherG7countries,representingthelargestproductivitygapsince1991whentheONSdataseriesbegan91,theadoptionofbestpracticesmanagementcouldhelptoaddressthisshortfall.

4.2 EstablishingBestPractices

“Alargenumberoffirmsareextremelybadlymanagedwithineffectivemonitoring,targetsandincentives.Wepresentcompellingevidencethatbettermanagerialpracticesaresignificantlyassociatedwithhigherproductivity.”

Bloometal,2005.

82Bertrand,M.,andSchoar,A.(2003).ManagingwithStyle:TheEffectofManagersonFirmPolicies.QuarterlyJournalofEconomics.Vol:118(4);pp:1169-1208.

83Ibid.84Lefebvre,L.A.,Lefebvre,L.,Mason,R.,(1997).TheInfluencePrisminSMEs:ThepowerofCEOsPerceptionsonTechnologyPolicyandItsOrganisationalImpacts,ManagementScience.Volume.43(6)

85Ibid.86Bloom,N.,etal,(2005).Opcit.87Suitaris,V.(2001).StrategicInfluencesofTechnologicalInnovationinGreece.BritishJournalofManagement.Volume12;pp:131-147.

88Chesbrough,H.(2006).OpenBusinessModels:HowtoThriveInTheNewInnovationLandscape.HBS.89Buhalis,D.,Deimezi,Q.,(2003).ITPenetrationandE-commerce:DevelopmentsinGreece,ElectronicMarkets.Volume13(4);pp309-324.

90Bloom,N.,andVanReenen,J.(2010).WhyDoManagementPracticesDifferacrossFirmsandCountries?TheJournalofEconomicPerspectives:Vol:24(1);pp:203-224.

91HouseofCommonsLibrary,(2016).ProductivityintheUK.BriefingPaper.Number06492,October.

29

Agapexistedinthedefinitionandexplorationoffirm-levelmanagementpracticesthataddressedthequery:doesmanagementmatter?Leadingresearch,commencedin200292,continuestoassessthis,withresultsconfirmingastatisticallysignificantcorrelationbetweengoodmanagementpracticesandfirmperformancewith20,000interviewsundertakenwithfirmsin35countriesinfoursectors.93ThisutilisedatoolkittoassessmanagementpracticesacrosskeyareasthataffectfirmperformancedevelopedbyMcKinseyandCoforuseexclusivelyintheLSEstudy.AdditionalstudieswerealsoundertakenonasmallersampleoffirmsviasitevisitsandinterviewsofmanagersinProduction,HR,Technologyandshop-floorworkers,toprovidedeeperinvestigations.

Theresultsalsoindicatedastatisticallysignificantrelationshipbetweenmanagementpracticesandfirmperformance.94Thisdualapproachandextensiveworkremaintheonlyempiricalinvestigationatthisscaleandbreadthtoassesskeyfactorscontributingtofirmproductivity.95Thesebestpracticesareingeneralagnosticoffirmlocationandcanbeappliedacrossgeographiesandsectors.

4.3 AddressingManagementPracticestoOptimiseFirm-LevelProductivity

Afirm’smanagementpracticesdrivethecraftingandexecutionofstrategiesthatcanmaximiseproductivity.96‘Badpractices’correctedcantransformabusinessandescalateitsproductivity.97TheapplicabilityoftheLSE-McKinseyresearchanditsutilisationinover20,000instancesin35countriesisrepletewithexamplesofmanagerswhohavereviewedtheirbusinessandimprovedperformancebyaddressingfour‘straightforward’practicesinoperations,performance,targetsandtalent:

• OperationManagement:Howeffectivelyhavemodernmanagementtechniquesbeenintroducedinthecompany:whywerethesemodernprocessesintroduced,forhowlonghavethesepracticesbeeninplace,howareotherdepartmentsofthecompany,outsideofthecompany,involvedinimplementingtheseprocesses?

• Performancemonitoring:Howwelldoestheperformancemonitoringsysteminformmanagersandtheiremployees'oftheirday-to-dayoperations:howdoprocessesandattitudesarescreened,howmeaningfularemetricsinrelationtohowfrequentlytheyaremeasuredandreviewed,towhatdegreethedetectionofdifferentlevelsofprocess-basedperformanceleadstoadequateandconsequentialprocess?

• Targetsetting:Howtightlyaretargetslinkedtothecompany'swiderobjectives:aretargetscoveringasufficientlybroadsetofmetrics,howstronglyareshortandlongtermtargetsconnected,howwellaretheycascadeddownandclarifiedtoworkers?

92ThisstudyisbeingundertakenbytheLSE’sCentreforEconomicPerformance,aleadinginterdisciplinaryEuropeaneconomicsresearchcenter,incollaborationwithMcKinseyandCoandremainstheleadingresearchonmanagementpracticesatfirm-levelglobally,commencingin2002andcontributedtosincethattimebothinexpansionto35countriesandinassessingfirmsfromfoursectors.

93Bloom,N.,etal.(2005).OpCit.94Grous,A.(2011).Grous,A.(2011).LSEmimeo.95Themethodology,sampleset,questionnairesandotherelementsareavailableat:http://worldmanagementsurvey.org

96Bender,S.,etal.(2016).ManagementPractices,WorkforceSelectionandProductivity.CEPDiscussionPaperNo1416.CentreforEconomicPerformance.LondonSchoolofEconomicsandPoliticalScience.

97https://hbr.org/2012/10/the-radical-beauty-of-three-si

30

• Talentmanagement:Howarepeoplemanaged:towhatdegreeispeoplemanagementemphasizedwithinthecompany,howcarefularehiringpolicies,howcloselyarepayandpromotionslinkedtotheabilityandeffortofemployees,howareunder-performersdealtwith,andhowarebest-performersretained?

Atotalof18sub-areashavebeendefinedacrossthesepracticesandprovidetheopportunitytoreviewandaddressafirm’soperation.Theinitialandpredominantmanagementpracticesapproachthatcommencedoveradecadeagohasbeendevelopedtoassessamanufacturing/productiondrivenenvironment.Thishasalsobeenadaptedtocoverretail,hospitalsandschools.Thefundamentalfourpracticesunderpinningthesearethesamehowever,withvariationsoccurringinthe18sub-areastoadaptthemforrelevance.Table4definesthemanufacturing/productionfocusedapproachtoassessmanagementpracticesthatformsthecoreapproach.

Manufacturing/ProductionFirm

OperationsManagement

Moderntechniques Whatmodernorleanpracticeshavebeenadopted?

Bestpractices:Allmajoraspectsofmodern/leanmanufacturinghavebeenintroduced(Just-in-time,automation,flexiblemanpower,supportsystems,attitudesandbehaviour)inaformalway

Rationaleforadoption Whatfactorsledtotheiradoption?

Bestpractices:Modern(lean)manufacturingtechniqueswereintroducedtoenableustomeetourbusinessobjectives(includingcosts)

PerformanceMonitoring

Processdocumentation Howareproblemsexposedandcorrected?

Bestpractices:Exposingproblemsinastructuredwayisintegraltoindividuals'responsibilitiesandresolutionoccursasapartofnormalbusinessprocessesratherthanbyextraordinaryeffort/teams

Performancetracking Whatkindofindicatorsareusedforperformancetracking?

Bestpractices:Performanceiscontinuouslytrackedandcommunicated,bothformallyandinformally,toallstaffusingarangeofvisualmanagementtools.

Performancereview Howdoyoureviewtheseperformanceindicators?

Bestpractices:Performanceiscontinuallyreviewed,basedonindicatorstracked.Allaspectsarefollowedupensurecontinuousimprovement.Resultsarecommunicatedtoallstaff

Performancedialogue Howdoyoureviewtheseperformanceindicators?

Bestpractices:Regularreview/performanceconversationsfocusonproblemsolvingandaddressingrootcauses.Purpose,agendaandfollow-upstepsarecleartoall.Meetingsareanopportunityforconstructivefeedbackandcoaching.

Consequencemanagement Whatwouldhappenifafollowupplanagreedduringoneofyourmeetingswerenotenacted?

Bestpractices:Afailuretoachieveagreedtargetsdrivesretraininginidentifiedareasofweaknessormovingindividualstowheretheirskillsareappropriate

TargetSettingTypeoftarget Whattargetsaresetforthecompany?

Bestpractices:Goalsareabalanceoffinancialandnon-financialtargets.

31

Seniormanagersbelievethenon-financialtargetsareoftenmoreinspiringandchallengingthanfinancialsalone(e.g.60%marketshareby2003)

Interconnectionofgoals Whatisthemotivationbehindyourgoalsandhowaretheycascadeddowntotheindividualworkers?

Bestpractices:Corporategoalsfocusonshareholdervalue.Theyincreaseinspecificityastheycascadethroughbusinessunitsultimatelydefiningindividualperformanceexpectations.

TimeHorizon Whatkindoftimescaleareyoulookingatwithyourtargets?Areyourgoalssetindependentlyofeachother?

Bestpractices:Longtermgoalsaretranslatedintospecificshorttermtargetssothatshorttermtargetsbecomea"staircase"toreachlongtermgoals

Goalsarestretching Howtoughareyourtargets?Doyoufeelpushedbythem?

Bestpractices:Goalsaregenuinelydemandingforalldivisions.Theyaregroundedinsolid,solideconomicrationale

Clarityofgoalsandmeasurement

Ifyourstaffwereaskedaboutindividualtargets,whatwouldtheysay?

Bestpractices:Longtermgoalsaretranslatedintospecificshorttermtargetssothatshorttermtargetsbecomea"staircase"toreachlongtermgoals

TalentManagementInstillingatalentmindset Howdoseniormanagersshowthatattractinganddevelopingtalentisa

toppriorityinyourcompany?

Bestpractices:Seniormanagersareevaluatedandheldaccountableonthestrengthofthetalentpooltheyactivelybuild

Buildingahighperformanceculture

Howdoesyourappraisal/rewardsystemwork?

Bestpractices:Westrivetooutperformthecompetitorsbyprovidingambitiousstretchtargetswithclearperformancerelatedaccountabilityandrewards

Makingroomfortalent Ifyouhadaworkerwhocouldorwouldnotdohis/herjobwhatwouldthecompanydo?

Bestpractices:Longtermgoalsaretranslatedintospecificshorttermtargetssothatshorttermtargetsbecomea"staircase"toreachlongtermgoals

Developingtalent Howwouldyouidentifyanddevelopyourstarperformers?

Bestpractices:Longtermgoalsaretranslatedintospecificshorttermtargetssothatshorttermtargetsbecomea"staircase"toreachlongtermgoals

Creatingadistinctiveemployeevalueproposition

Whatmakesitdistinctivetoworkatyourcompanyasopposedtoyourcompetitors?

Bestpractices:Weprovideauniquevaluepropositiontoencouragetalentedpeoplejoinourcompanyaboveourcompetitors

Retainingtalent Ifyouhadastarperformerwhowantedtoleavewhatwouldthecompanydo?

Bestpractices:Wedowhateverittakestoretainourtalent.Source:LSE-McKinseyManagementMattersSurvey.Alsoavailableonline98

Table4:Managementpracticescheck-listformanufacturing/productionbusinesses

Thisapproachisvalidacrossorganisationaltypesincludingcorporates,largefirms,smalltomediumenterprisesandhasbeentestedacross20,000interviewsinmultiplecountries.

98http://worldmanagementsurvey.org/benchmark-your-organization/benchmark-your-manufacturing-firm/

32

4.4 WhyDoesManagementMatter?

Identifying,correctingandutilisingbettermanagementpracticeshavebeenshowntobeeffectiveinimprovingfirmperformance.99Extensiveresearchandthereal-worldapplicationofprinciplestoimprovemanagementpracticessince2002hasconfirmedthepotentialresultsavailabletofirmsthatcanmanagebetter:100

• Defectsreducedby50%;• Inventoryreducedby20%;• Outputraisedby10%;• Firmsthatimprovepracticesby1pointinthereviewoftheiroperationscorrelate

withsignificantpotentialperformanceimprovements:

o 23%higherproductivityo 14%highermarketcapitalisationo 1.4%higherannualsalesgrowthrate

Theimprovedresultsfromenhancedmanagementpracticescarrynumerousorganisationalbenefits:

• Staffretention:Rewardingandretaininggoodemployeeshasapositiveimpactonthefirm,withtheaveragefinancialimpactofthelossofanemployeeestimatedtobe£30k,comprisedofalossofoutput(£25k)andthelogisticalcostofabsorbinganewworker(£5k).101LabourturnoverwasestimatedtocosttheUKeconomy£4.1bnin2013.102

• Inventorymanagement:Reducingthefirm’sinventory,accountsoutstanding,andcashconversioncycleimprovesthefirm’svalueandprofitability.103Addressingpracticessurroundingthisareacangeneraterapidresultsforthefirm.

• Fasterandmoreaccurateproduction:Applyingsimpleleanandmodernstreamliningprinciplesandconsolidatingteamstoimprovelocalworkflowscanproducerapidgainswithinthreeweekstotwomonths.Morecomplicatedissuesthatrequirelongerdatacollectionandanalysiscantakesixtoeighteenmonths.104Thebenefitscanbedramatic,withFordintheUSincreasingproductivityby30%offrontaxlesforitstrucksandSUV’sthatresultedinanadditional$2billioninprofit.105

• Linkingstrategywithdelivery.Acontinuousreviewandimprovementprocesstosetappropriatetargetsand‘extend’thefirm’smanagersandemployeestodelivercansustainprofitabilityandproductivity.106Resultshavefoundthatproductivityis

99https://hbr.org/2012/10/the-radical-beauty-of-three-si100Ibid.101OxfordEconomics-Unum.(2014).TheCostofBrainDrain.102Ibid.103Garcia-Turel,P.,J.,andMartinez-Solano,P.(2007).EffectsofworkingcapitalmanagementonSMEprofitability.InternationalJournalofManagerialFinance.Vol:3(2);pp.164–177.

104TajS.,andBerro,L.(2006).Applicationofconstrainedmanagementandleanmanufacturingindevelopingbestpracticesforproductivityimprovementinanauto-assemblyplant.InternationalJournalofProductivityandPerformanceManagement.Vol.55(3/4);pp.332–345.

105 Robinson, R. (1999). Welcome to OR territory OR/MS Today. August; pp. 40-3. 106McAdam,R.,andBailie,B.(2002).Businessperformancemeasuresandalignmentimpactonstrategy.InternationalJournalofOperations&ProductionManagement.Vol:22(9);pp.972–996.

33

optimisedwhentargetsareexplicitlyincludedinstrategic/businessplansandutilisedsubsequentlywithinthefirmandlinkedbacktothis.107

A‘planofaction’ofenhancingproductivitybyfirmsintheUKcouldinclude:

1. Reviewthemanagementpracticesdefinedinthispaper.2. Usethemasaguidetoassesswherethefirmispositionedandconsideroptionsto

addresswherepracticesappeartobedivergenttothis.3. Undertakeself-analysisbasedonthesemanagementpracticeswithbenchmarksand

optionstoself-assessafirm’smanagementpractices.The‘WorldManagementSurvey’isthefirstcross-country,cross-industrydatasetbuilttomeasurethequalityofmanagementpracticesinestablishments.Itassessessub-themesforeachpracticeandprovidesascoreforthefirmincludingfeedback,toassistinidentifyingareasthatcouldrequirefocus.108

4. Useasecondaryself-analysistoolsuchastheReadyBusinessIndicator,developedbyVodafoneUK,tobenchmark‘businessreadiness’inlinewithdigitaltransformationandidentifyareasforpotentialfocus.109

5. Addressareasrequiredwithbothfirmresourcesandotherswheremanagementrequiresadditionalexpertise.

Theaboveprovidesanexpedient,testedapproachtoquicklyaddressingandquantifyingthequalityoffirmpractices.Ifutilisedasaguide,benefitscanaccrueashasbeenshownonnumerousoccasionsinternationally.

4.5 ComplacencyisnotanOptionAdoptingbestpracticesmanagementshouldnotbeleftto‘crisis’scenariosorwheneconomicorotherpressureoccurs.Organisationsneedtoperiodicallyre-structureandre-aligntorespondtomarketchanges:researchindicatesthatorganisationsthatbelievethattheircurrentconfigurationwillpermitthemtosurvivethroughanyfuturescenariosareorganisationsthatareunlikelytoseethefuture.110Managersshouldneverbecomesocomfortableinaccommodatingtheircurrentexternalenvironmentthattheycan’taltertorespondtoenvironmentalchanges.111Attemptingtochangetoolatecanresultinthefirm’sdemise.112

LeadingresearchacrosstheEUhasshownthatcurrentinvestmentinafirm’sinnovationsandITwillhaveadirectbearingonfuturecompetiveness:firmsthatare‘thrivers’arethosethatinvestinbestpracticesandITthroughoutthebusinesscycle.113Inparticular,firmsthatareconstantlyassessingtheirperformance,theirenvironmentandforecastingfutureissues

107Ibid.108http://worldmanagementsurvey.org/benchmark-your-organization/109http://readybusiness.vodafone.co.uk110 Ulen, T. (2010) Responding to change: internal and external factors in organizational success. Journal of Institutional Economics. Vol: 6(1): pp: 133–137 111Ibid.112Posner,R.(2004),Catastrophe:RiskandResponse,NewYork:OxfordUniversityPress.113http://www.businesswire.com/news/home/20090901005446/en/Important-Research-Innovators-Beating-Recession-Pulling-Competitors

34

arethosewiththehighestpotentialtosurvive.114‘Thrivers’aretwiceaslikelytosucceedinobtainingafastROIandreinvestcostsavingsintoITinnovationandefficiency.Recessionsandotherexternalshockspresentanopportunity,withthesecompaniespreparedinthefaceofdownturnstorespondandsurvive.Resultsindicatethatwhile52%ofthesetypesof‘thriver’businessesmayhavebeenimpactedbytherecession,only28%haveobservedadecreaseinsales.115Thesetypesofbusinessesaremuchmorelikelytosurvivenegativeshocksandadverseconditionsthanthosethatare‘Hiders’,thathavenotadjustedanykeyelementsaheadofthis,or‘Survivors’-firmsthatmaymakeitthroughsuchconditionsbutcannotadjusttothemlongtermanddonoteventuallysurvive.UKbusinessesfacecontinuedchallengesfromarangeofissues:EU-drivenpoliticalandlegalchanges;economicconditionsincludinganysofteningofdemand;cyber-securityanddata-centricchallenges;alteringworkforcepractices;governmentlegislationonpensionandotherworkforcerequirements;workingcashflowandaccesstofunds;andothers.Firmswhosemanagersareengagedintheirbusinessandcontinuouslyseektomaximiseperformanceandproductivitystandthehighestchanceofmakingitthroughnegativecycleswiththefactorsrequiredtosurviveandprosper.Familyownedfirmshaveshownnegativeresultsinadjustingtochangescomparedtootherfirmtypesandwithgreaterresistancetochangeandnegativeproductivity:instillingbestmanagementpracticesandtechnologyadoptioninthesefirmtypescanhaveparticularlypositivepotentialbenefits,butappliesasaprincipalacrossallfirmtypes.116

4.6 ManagingforGrowth

Best-practicefacilitatesmanagementattentionbeingtargetedtokeydevelopmentactivitiesacrossallbusinessownershiptypes.Researchindicatedthattheimprovementofmanagementpracticeswasachievedbymanagersinseveralways117:

• Firmmanagersworkingatcapacityundertookatwo-foldstrategy:(1)delegatedtasksinitiallyandfocusedonfirmexpansionviaexportingornationally;and(2)afterafurtherperiod,employedadditionalresourceswhoundertookdedicatedexportdutiesornewchannelandrelatedopportunities,supportedbytheadditionalbusinessgrowth;

• SoughtexportassistancefromGovernmentagenciesaboutexporting;• Partneredwithadditionalorganisationsfromtheoutsettodistributegoodswithout

furtherresourcerecruitment,withsomeadditionaldutiesbeingundertakenbyfirmmanagersand/orfurtherdelegation.

114Ibid.115Ibid.116Ward,J.,L.(1997).GrowingtheFamilyBusiness:SpecialChallengesandBestPractices.FamilyBusinessReview.Vol:10(4);pp:323–337.

117LSEResearchacross50firmsforManagementMatters:2009-2012.

35

5. InformationandCommunicationsTechnology

“Businesssuccessincreasinglydependsontheorganization’sabilitytofusethepowerofITintothefabricofbusinessprocessesandbusinessnetworks.ThecontinuouslygrowingimportanceofITrequiresorganisationstointegrateITdecisionswithintheircommonplanninganddecision-makingprocessesatallorganizationslevels.”

VanderZeeandDeJong,(1999).1185.1 ICTAdoptionFactors

“EvidencehasshownthateffectivedeploymentofICT,orthefailuretodoso,aredeterminantsofproductivitygrowthfarmoreimportantthanICTexpenditure.InordertogetthemostoutoftheirICT,companieswillhavetomakesophisticateduseofICTandmanagetheprocessofchangerequiredtoembedtechnologyinthecompanyorganisation.”

VanZoest,(2003).119

InformationandCommunicationsTechnology(‘ICT’)hasthepotentialtobeamajortransformativetoolforproductivityinthefirm.120TherelationshipbetweenICTinvestmentandfirmperformancecanbecomplexandmultifaceted,andmoderatedamongstotherfactorsbycompanystrategyandmanagerialpractices.121NineoutoftenSMEsinOECDcountriesareequippedwithcomputersandeightoutoftenhaveInternetpenetration.122

AccesstoanduseofICTcanpermitSMEstobecomeorremainprofitable,exploittheirintellectualpropertyandempowertheiremployeestoutilisetechnology‘onthemove’orwithgreaterfunctionalitythaninthepast.123SMEswithhighproductivitygrowtharemorelikelytoadoptagreaternumbersofadvancedICTsandforthesetobeusedtofosterinnovationandproductivity.124AllthreefirmtypesutiliseICTtovaryingdegrees,withanumberoffactorsincreasingasfirmsizeincreases:sophisticationoftechnologyutilisedincludingsecurity,infrastructure,functionality;integrationwithEnterprisesystems;analyticsandreporting,andotherattributes.125Asiteratedthroughoutthispaper,thekeyleveragetomaximizingthepowerofICTtofosterproductivityismanagementpractices:whilstICTandmanagementpracticesarecomplementary,thelatteristheleverforincreasesinproductivity.Firmswithbetterpracticesaremoreproductive,profitable,andhavehighersalesgrowththanthosewith

118VanderZee,J.T.M.andDeJong,B.(1999).Alignmentisnotenough:integratingbusinessandinformationtechnologywiththebalancedbusinessscorecard.JournalofManagementInformationSystems.Volume16(2);pp:137–156.

119VanZoest,A.,(2000).UKBusinessesandICTs:WhereistheProductivityGrowth?120Brynjolfsson,E.,andHitt,L.M.(2003).ComputingProductivity:Firm-LevelEvidence.MITSloanWorkingPaper4210-01,SloanSchoolofManagement,eBusiness@MITWorkingPaper139;June.

121Rondeau,P.J.,etal.(2006).Howinvolvement,ISmanagementeffectiveness,andend-usercomputingimpactISperformanceinmanufacturingfirms.Information&Management.Vol:43(1;pp93-107.

122OECD(2004),ICT,E-BusinessandSMEs123Stroeken,J.(2001).TheadoptionofITbySMEs:TheDutchcase.JournalofEnterprisingCulture.Volume:9(1);pp:129-152.

124Higón,D.,A.,(2012).TheimpactofICToninnovationactivities:EvidenceforUKSMEs.InternationalSmallBusinessJournal.Vol.30(6);pp.684-699.

125Hollenstein,H.(2004).DeterminantsoftheadoptionofInformationandCommunicationTechnologies(ICT):Anempiricalanalysisbasedonfirm-leveldatafortheSwissbusinesssector. StructuralChangeandEconomicDynamics.Vol:15(3);pp:315–342.

36

‘worse’practices.126Figure8depictsresultsindicatingthatICTadoptedwithbettermanagementpracticesachieves20%productivityimprovementcomparedtoonlya2%upliftwhentechnologyisadoptedwithpoorpractices.127

Figure8:ManagementpracticesandICTadoptioncomplementarity

FirmswhichadoptorganisationalchangesandintroduceICTdisplayahigherfrequencyofproductivityimprovementandhigherratesofinnovation.128TheadoptionofICTbyfirmshasbeenlinkedtoseveralbenefits,enhancedwhenthisoccurswithgoodpractices:129

• Productivityenhancement;130• Greaterinnovation;131• Processimprovement;132• Flexibleorganisationalstructures.133

Complementaryinvestmentsinskills,organisationalchangeandinnovationarealsoviewedasinstrumentalinfacilitatingthesuccessfuluseofICT,andaffectingfirmperformance.134Withoutthesesupportingelements,theeconomicimpactofICTmaybelimited.135

126VanReenen,Jetal.(2006)ManagementPractices,Work—LifeBalance,andProductivity:AReviewofSome

RecentEvidence.OxfordReviewofEconomicPolicy(Winter)22(4):pp:457-482.127Dorgan,S.J.,andDowdy,J.J.(2004).WhenITLiftsProductivity.McKinseyQuarterly;4.128Brynjolfsson,E.,andHitt,L.(2000).BeyondComputation:InformationTechnology,Organization

TransformationandBusinessPerformance.JournalofEconomicPerspectives;Vol:14;pp:23-48.129Mundlak,Y.(1961).EmpiricalProductionFunctionFreeofManagementBias.JournalofFarmEconomics.

Volume43(1);pp:44-56.130Morikawa,M.(2004).InformationtechnologyandtheperformanceofJapaneseSMEs.SmallBusiness

Economics.Vol:23(3);pp:171–177.131Koellinger.,P.(2008).Therelationshipbetweentechnology,innovation,andfirmperformance-Empirical

evidencefrome-businessinEurope.ResearchPolicy.Vol:37;pp:1317–1329.132Ibid.133Gera,S.,andGu,W.,(2004).Theeffectoforganisationalinnovationandinformationtechnologyonfirmperformance.InternationalProductivityMonitor;No.9.

134James,J.A.Bhalla.(1994).FlexibleSpecialization,NewTechnologiesandFutureIndustrializationinDevelopingCountries.Futures.July/August.

135OECD,(2004).TheEconomicImpactofICT:Measurement,EvidenceandImplications,Paris.

37

Ultimately,thekeyfactorbelievedtoaffecttechnologyadoptionandproductivityis‘managerialquality’deliveredbyboththeCEO/Managerandmiddlemanagers,withpracticesformingpartoftheorganisationalstructureand‘behaviour’ofthefirmthatevolvesovertimewithsuccessiveleaders.136Competition,organisationalpracticesandotherstrategiesinfluencethevalueofICTinvestmentsandinternalworkorganisation,137withineffectivemonitoring,alackofanyorappropriatetargetsettingandincentives,resultinginlowerproductivityandinefficientuseofICT,irrespectiveoflocation.138

5.3 ChangingSocioeconomicDrivers

Organisationsandindividualshaveaplethoraofcommunicationsoptionsavailabletothemforwork,socialtasks,andablurringofthelinebetweenthetwo.Organisationscantodayadoptanarrowernumberoftechnologyoptionsandstillenhanceproductivity,withthisparticularlyapplicabletoSMEsandsoletraders.Asfirmsincreaseincomplexity,sizeandgeographicaldisbursement,additionalcomponentsareoftenobservedsuchasEnterpriseapplicationsfordata,security,email,andotherareas,facilitatedbymobilebroadbandinparticular.139Individualsarenowworkingandlivinginanerawherefixedtelephonelinesarebecominglessrelevant;mobileinteractive,entertainmentandworktasksarebecomingingrainedas‘normal’,andpersonaldevicessuchassmartphones,tabletsandlaptopshavebecomeubiquitous.140ThenewgenerationofMillennialandGenerationZemployeesintheworkplacearecitizensofthemostdiverseandsophisticatedmedia,computerandmobileenvironmentever141andfarsurpasstheexperienceofBabyBoomers(GenerationX).142ThisishavingasignificantimpactonhowbusinessesadoptanduseICT.Fourfifthsoforganisationsalsobelievethatdigitaltransformationwillbecriticaltotheirorganisationwithintwoyears,andover90%ofemployeesbelieveitisthecorrectapproach.143Managersinlargerfirmsarebecomingmoreawarethatemergingtechnologieslikesocialmediaandmobilecommercerequireadifferentcultureandskillsthanutilisedinthepast:144

136Syverson,C.(2004a).MarketStructureandProductivity:Aconcreteexample.JournalofPoliticalEconomy.

112(6);pp:1181-1222.137Brynjolfsson,E.,Hitt,L.M.(1995).Informationtechnologyasafactorofproduction:Theroleofdifferences

amongfirms.EconomicInnovationofNewTechnology.Volume3(3);pp:183-199.138Black,S.andLynch,L.(2001).HowtoCompete:TheImpactofWorkplacePracticesandInformation

TechnologyonProductivity.ReviewofEconomicsandStatisticsVolume83(3);pp.434-445.139Ciprinan,A,etal(2011).TheProceedingsoftheInternationalConference:Marketing-FromInformationtoDecision;pp:21-35.

140Akman,I.,andRehan,M(2016).Examinationoffactorsinfluencingemployees’adoptionofmobilecommerceandservicesinTurkey,EconomicResearch-EkonomskaIstraživanja;Vol29(1);pp:770-781.

141Gupta,O.,Gulati,G.(2014).Psycho-analysisofMobileapplicationsusageamongGenerationZTeens.InternationalJournalonGlobalBusinessManagementandResearch.August;pp80-95.

142http://socialmarketing.org/archives/generations-xy-z-and-the-others/143MITSloaneManagementReview(2013).ResearchReport:EmbarkingDigitalTechnology.ANewStrategicImperative.

144Ibid.

38

5.4 EnhancingProductivitywithICT

BothfirmsandindividualscanadoptICTtoenhancetheirproductivity.TherangeofICTavailabletofirmsissignificantandinvolvesbothexternalandinternalcomponentsanddrivers.Figure9depictstheconsolidatedenvironmentinwhichapplicationsandtechnologyareimplemented.

Figure9:Impingingcommunicationfactorsdrivebothfrontandbackendselections

Firmscanselectfromfixedandmobiletechnologycomponentstomeettheirbusinessrequirements.BeforereviewingtheICTavailable,itisrelevanttooutlinetheenablingnetworksacrossmobilebroadband;fixedsuperfastbroadbandandinternetaccess.Themost‘disruptive’ofthesecontinuestobemobilebroadband–drivenbythecontinuingrolloutof4Gservices.145ThegrowthoffixedandmobilebroadbandintheUKcontinues,althoughruralareasarestillatsomedisadvantagetodenserurbanareasforhigherspeed4G:aroundhalfofUKpremisesarecovered,butthisincreasesto88%for3Gand93%for2G,asdepictedintable5.CoverageiscontinuingtogrowacrosstheUK.

Table5:OutdoormobilecoveragefromallUKoperators

Source:OFCOM,ConnectedNations2015,p8.146

Theageofthesmartphonehasarrived,withOFCOMdata147indicatingthat:

• Smartphoneshaveovertakenlaptopsasaninternetuser’sprincipaldevice• Twohoursperdayarespentonsmartphones,twiceaslongaslaptopsandPCs• 4Gsubscriberssurgedfrom67%to39.5millionover2015

145Basole,R.,C.(2008).Enterprisemobility:Researchinganewparadigm.InformationKnowledgeSystems

Management.Vol:(7)1,2;pp.1-7.146https://www.ofcom.org.uk/__data/assets/pdf_file/0028/69634/connected_nations2015.pdf147Ofcom,(2015).CommunicationsMarketReport.

39

• Increaseacrossdata-drivenactivities:onlineshopping;TV;messaging;face-to-faceandvoicecalls;videoandpicturesharingandothers.

TheavailabilityofsuperfastbroadbandtopremisesisafurtherenablerofbusinessesadoptingproductivityenhancingICT,andbasictelephoneservice.Thishasalsobeenincreasing,with83%oftheUKhavingaccessto63Mbit/s,upfrom75%in2013,asindicatedintable6.

Table6:Coverageofsuperfastbroadbandcoverage

Source:OFCOM,ConnectedNations2015,p16.148

Around27%ofUKbusinesseshavetakenupsuperfastbroadbandintheUK(8million).149Anadditional22%havenottakenthisup,yieldingatotalpotentialfigureofaroundhalfofallUKbusinesses.150Thespeedofsuperfastbroadbandrollouttosomeruralandurbanareasisatopicofdebate,withtheGovernmenttargeting95percentpenetrationoftheUKbyDecember2017andtheprovisionofbasicaccessof2MbpsforallfromDecember2015.151TheUKCultureSecretaryhasstatedthatreachingthefinalfivepercentinruralareaswouldbe‘challenging’,buthasconcurrentlyindicatedthat,"thebenefitsofsuperfastbroadbandareclearfromincreasingproductivityandeconomicgrowthtotransformingfamilyentertainmentathome…Wehopetofindwaysinwhichthosebenefitscanbebroughttoevenmorepeople."152Ofcom,theUK’scommunicationsregulator,haspublishedconclusionsfromastrategicreviewofdigitalcommunicationsintheUK,includingademandthatBTprovideassistancetorivalsbypermittingthemaccesstoitsinfrastructuretolayfibreamongstothers.153Increasedbroadbandpenetration,coupledwithhighspeedsandbusinessadoption,areintegraltotheadoptionofmanyservicesbyindividualsandfirmsalikeandcanimproveproductivity.154Firmsutiliseabroadrangeoftechnologyservicesthatreflectfirmtype,size,

148https://www.ofcom.org.uk/__data/assets/pdf_file/0028/69634/connected_nations2015.pdf149Ibid.150Ibid.151https://www.gov.uk/guidance/broadband-delivery-uk152http://www.telegraph.co.uk/news/2016/05/05/ministers-halt-automatic-broadband-roll-out-for-rural-families-b/

153https://www.ofcom.org.uk/__data/assets/pdf_file/0016/50416/dcr-statement.pdf154Colombo,G.,M.,andCroce,A.(2013)ICTservicesandsmallbusinesses’productivitygains:AnanalysisoftheadoptionofbroadbandInternettechnology.InformationEconomicsandPolicy.Vol:25(3);pp:171–189.

40

location,andotherfactors.Graph22depictstheprincipalservicesthatUKbusinessesutiliseICTforindescendingorderofuse,withemailthemostprevalent.Someoftheseareenabledbybroadbandwhilstothersreflectabroadarrayofbusinessservices.

Graph22:UseofapplicationsbyUKSMEs

Source:BroadbandStakeholderGroup(2015);Ofcom,2014.155

5.5 APortfolioofOptions

TheUKissecondtotheUSintermsofICTassetsasapercentageofgrossfixedcapitalformation,at20%versus25%respectively.156Firm-levelresearchandcasestudyworkwithinthemanagementpracticesstreamacrossasampleofaround50firmstodatehasindicatedseveralareasofconcernrelatedtoICTadoptionbymanagersinCorporatesandSMEs.Graph23depictsthetopfiveforeachofthesetwofirmtypes.Thepriorityforcorporatemanagerswasthesecurityofdataaccessedexternallybyemployees,whilstforSMEManagers,connectivitytotheirintranetfromamobiledevicewasthemostpressingICT-relatedpriority.

155Ofcom.(2014)SMEexperienceofcommunicationsservices–aresearchreport.October16,and:BroadbandStakeholderGroup,(2015).ThebroadbandrequirementsofsmallbusinessesintheUK.August.AblendedrateforapplicationusebybothsmallandlargerSMEswasutiliseddrawingondataforbothtodefinethischart.

156Miller,B.,andAtjinson,R.(2014).RaisingEuropeanProductivityGrowthThroughICT.

41

Graph23:TopfiveareasidentifiedbyCorporate&SMEmanagersandemployeesforICTadoptionSource:LSEresearch

Additionalresearchhasindicatedthataround50%ofBritishbusinessmanagersandpublicsectormanagersdonotfeelthattheirbusinesswillbeabletoaddresskeychallengesoverthenextfiveyears.157Theuseofdigitaltechnologyishoweverseenaskeyenablingmodetoassistwithchange,withYouGovdatafromasurveyof1,110Britishmanagersindicatedthatthetopfiveusesofdigitalwereperceivedasbeing:

• Deliveringhigherqualitycustomerservice(74%)• Providinghigherqualityproductsandservices(72%)• Providingvalueformoney(65%)• Costcontrol(65%)• Profitabledelivery,andgeneratingareturnforinvestors(53%)

Thekeychallengehoweverisexecution:firmsoftendon’tadoptreadilyavailableandcost-effectiveICTordigitalmeasures.Researchindicatestwoprimaryreasonsthatthisoccurs:(1)75%offirmmanagers,particularlyinSMEs,arenotawareofthetechnologyanddigitaloptionsthatcanfacilitateproductivityenhancement;(2)amongstmanagerswhoareawareofsomeoptions,overtwo-thirdswerenotawarewheretheycouldseekassistancefrom,withthemajoritybelievingthatthisrequired‘expensiveconsultants’,or‘hiringanITmanager’,withneitheroptioncost-effectiveforthemajorityofsmallerfirms.158

5.6 MakingtheRightCall

ICTadoptionbyfirmsreflectstheirdecisionmaker’smanagementpractices.Considerableresearchhasidentifiedseveralwaysinwhichproductivityisbeingenhancedacrosstheprivateandpublicsector,includingemergencyservicesandlawenforcement.Thefollowing157YouGovSurvey,commissionedbyVodafoneUK,of1,130managers,undertakenonline16-23September2015.http://mediacentre.vodafone.co.uk/pressrelease/millions-of-british-businesses-dont-feel-ready-to-deal-with-the-future-of-digital-technology/

158LSEResearchforManagementMatters.50firmsub-samplefromprimarysample.

SME

Corporate

42

reflectanumberofpotentialareasofICTadoptionthatPublicSector,Corporates,LargeFirmsandSMEscanundertaketoenhanceproductivity.

5.6.1 MobileBroadband:Casestudy-PoliceandEmergencyServices159

ThesocioeconomicimpactoftheadoptionofmobilebroadbandbyemergencyservicesincludingPoliceandAmbulancecanbesignificant.Thiscallsforastep-changefromtoday’suseofnarrowerdata,withthepotentialtobothbecomemoreefficientwithasmallernumberofpoliceofficersonthebeatfollowingbudgetaryreductionsinsomeareasandforambulanceservices,intheabilitytoreducefatalitiesduealackofreal-time,accuratedataonpatienthistoryavailable.160ThetransformativeeffectofmissioncriticalmobilebroadbandhasthepowertoeffectchangebothatthefrontandbackendofPoliceandEmergencyServices.EstimatesarethattheadoptionofmobilebroadbandbyPoliceintheUKwithend-to-endchangescouldresultina10%productivityupliftreflectedbyanimprovedabilitytoundertakeinterventioninscenarioswhereotherwisethisisnotoccurring.161Thiswouldequatetoa£1billionbenefittotheeconomyannually.ExamplesofICTboostingproductivityintheUKarealreadyoccurring:• WiltshirePolice’smobileandremoteworkingsolutionthatisestimatedtohaveresulted