the impact of product market competition on firms’ …grullon/wp/competition.pdf · the impact of...

TRANSCRIPT

The Impact of Product Market Competition on Firmsrsquo Payout Policy

by

Gustavo Grullon Rice University

and

Roni Michaely

Cornell University and IDC

May 2014

We thank Amir Barnea Yaniv Grinstein Gerard Hoberg Gordon Phillips and seminar participants at the American Finance Association Meetings the Caesarea Center Annual Conference Cornell University Georgia State University Rice University Texas AampM International Texas State University and the University of Maryland for helpful comments We are grateful to Gordon Philips for providing us with the industry concentration ratios We also thank Daniela Covarrubias and Christopher Vincent for their research assistance An earlier version of this paper was circulated under the title ldquoDividend Policy and Product Market Competitionrdquo Please address correspondence to Gustavo Grullon grullonriceedu or Roni Michaely rm34cornelledu

The Impact of Product Market Competition on Firmsrsquo Payout Policy

Abstract This paper investigates the interaction between product market competition and managersrsquo decision to distribute cash to shareholders Using a large sample of manufacturing firms we find that firms in more competitive industries pay more dividends than firms in less competitive markets Further consistent with agency theory we find that the effect of product market competition on corporate payouts became significantly stronger after an exogenous event that intensifies the agency conflict between managers and shareholders (the business combination laws adopted by several states in the US during the 1980s and 1990s) Overall our findings are consistent with the notion that the disciplinary forces of competition induce managers to pay out excess cash and with the idea that dividends are the ldquooutcomerdquo of external factors

1

1 Introduction

It has been argued in the economic literature that intense product market competition

provides corporate managers with incentives to behave efficiently (eg Allen and Gale (2000))

One of the main rationales for this theoretical argument is that the disciplinary forces of

competition rapidly remove incompetent managers from the market This is an old idea that was

recognized by Adam Smith in The Wealth of Nations who wrote that ldquomonopolyhellipis a great

enemy to good managementrdquo Other examples include Hicks (1935) who acknowledges that

ldquothe best of all monopoly profits is a quiet liferdquo and Caves (1980) who comments that

economists seem to have a ldquovague suspicion that competition is the enemy of slothrdquo Over the

past few decades several theoretical papers have tried to formalize this idea by examining the

potential channels through which competition can have an effect on managerial incentives (see

for example Holmstrom (1982) Hart (1983) Nalebuff and Stiglitz (1983) Scharfstein (1988)

Hermalin (1992) Schmidt (1997) Aghion Dewatripont and Rey (1999) Jagannathan and

Srinivasan (1999) and Raith (2003)) Allen and Gale (2000) for example conclude that

competition among firms may be a more effective corporate governance mechanism than either

the market for corporate control or institutional monitoring

From an empirical perspective several recent studies seem to support the idea that

competition incentivizes managers to be more efficient and more aligned with shareholders For

example Graham Kaplan and Sibley (1983) find that airlines experienced significant

productivity improvements after the deregulation of their industry in 1978 Nickell (1996)

documents that total factor productivity growth among a sample of UK firms is positively

correlated with proxies for competition intensity Berger and Hannan (1998) find a strong

negative relation between cost efficiency and measures of market power in the US banking

2

industry Griffith (2001) provides evidence that an increase in product market competition leads

to increases in productivity especially among those firms in which managers are less aligned

with shareholders More recently several studies find evidence suggesting that product market

competition has the disciplinary effects that mitigate the need for either internal or external

corporate controls (Giroud and Mueller (2010) and Chhaochharia Grinstein Grullon and

Michaely (2011))

Financial economists also suggest that dividends could be used as a mean to reduce

agency conflict between management and shareholders (eg Jensen (1986) Easterbrook (1984)

La Porta Lopez-de-Silanes Shleifer and Vishny (2000)) Higher dividends reduce managersrsquo

ability to enjoy the quiet life (Bertrand and Mullainathan (2003)) or build unjustified empires

(Jensen (1986)) The idea that agency considerations are an important determinant of payout

policy has received empirical support (see for example Lie (2000) Grullon and Michaely

(2004) and DeAngelo DeAngelo and Stulz (2006))

In this paper we investigate the link between product market competition managerial

incentives and corporate payout policy There are several potential reasons why product market

competition and payout policy might be related Perhaps the most important one is the

interaction between competition and agency conflicts It is possible that product market

competition through its effect on agency conflicts may be an important determinant of the

decision to pay out excess cash to shareholders Similar to La Porta Lopez-de-Silanes Shleifer

and Vishny (2000) (henceforth LLSV) we argue that product market competition can potentially

have two opposing effects on payout policies One possibility is that firms pay dividends

because competition acts as an enforcement mechanism that exerts pressure on managers to

distribute cash to their shareholders by increasing the risk and the cost of overinvesting (eg

3

higher probability of liquidation greater transparency) The main idea here is that intense

competition can affect corporate payouts in ways similar to a strong legal systemmdashby creating

conditions that pressure managers to pay out rather than invest in non-profitable investments (the

ldquooutcomerdquo model) Alternatively payout policy can be a substitute for competition managers

use dividends as a substitute for the external disciplinary factors to establish good reputation in

the capital markets to be able to raise capital on better terms (the ldquosubstitutionrdquo model)

There are significant disagreements in the literature on how corporate governance affects

payout policy On the one hand consistent with the outcome model LLSV (2000) find that

firms in countries with strong minority shareholder rights tend to pay higher dividends More

recently Michaely and Roberts (2012) compare dividend policies of firms with weak corporate

governance (private firms) to dividend policies of firms with strong corporate governance (public

firms) and find that firms with stronger corporate governance pay higher dividends On the

other hand consistent with the implications of the substitution model several recent papers find

evidence supporting the notion that firms use dividend payments to reduce agency costs that are

caused by poor governance (Officer (2006) and John and Knyazeva (2006)) Further Grinstein

and Michaely (2005) find that firms with high institutional holding (an external governance

proxy) generally pay lower dividends In this paper we test these competing hypotheses by

examining the relation between product market competition and corporate payout policy

Using the Herfindahl-Hirschman Index (HHI) from the Census of Manufacturers as a

measure of market concentration we find that firms in more concentrated industries have

significantly lower dividend payout ratios and are less likely to pay and increase dividends than

firms in less concentrated industries These results hold even after controlling for other factors

that have been documented to affect corporate payout policy such as size profitability growth

4

opportunities firm age leverage and volatility Moreover we find that the effect of

concentration levels on corporate dividend payouts is not only statistically significant but also

economically significant

While the large sample regression analysis control for many of the factors found by prior

literature to affect dividend policy (as well as industry- and time-fixed-effects) given the nature

of the investigation it may not be enough To address this issue we use a natural experiment that

exogenously exacerbated the agency problems between managers and shareholders

Specifically following Bertrand and Mullainathan (2003) and Giroud and Mueller (2010) we

use the adoption of business combination (BC) laws to examine the how agency issues affect the

relation between corporate payouts and product market competition Because these laws

substantially reduced the chance of hostile takeover they increased the opportunity of

managerial misbehavior among the firms affected by the BC laws The reason for this is that the

market for corporate control is an external factor that serves as a substitute for the lack of

product market competition (Giroud and Mueller (2010)) Therefore if our main results are

mainly driven by the interaction of competition and agency issues then managers in less

competitive markets should become more entrenched after the adoption of the BC laws than do

managers in more competitive markets which should lead to a larger differential in payout ratios

between firms in concentrated markets and firms in competitive markets

Using the business combination (BC) laws passed between 1985 and 1991 on a state-by-

state basis we perform a differences-in-differences analysis to investigate whether these anti-

takeover laws increased the gap in payout ratios between competitive and non-competitive firms

Consistent with the predictions of agency theory we find that the negative relation between

industry concentration levels and dividend payout ratios becomes much stronger after the

5

passage of the BC laws These results are consistent with the conceptual framework in LLSV

(2000) that dividends are the outcome of external factors

We also investigate the possibility that firms in more concentrated markets pay lower

dividends because they need to hoard cash to fend off predatory behavior from competitors as in

Bolton and Scharfstein (1990) Although there is evidence that especially for financially

constrained firms strategic product market considerations are an important determinant of

payout policy (Hoberg Phillips and Prabhala (2014)) and cash holdings (Haushalter Klasa and

Maxwell (2007)) our analysis indicates that these interactions are not the main drivers of our

results As discussed above we find that the differential in payout ratios between firms in

competitive and non-competitive markets increases after the passage of the BC laws For this

result to be consistent with the predation hypothesis BC laws should make firms in non-

competitive markets more prone to predatory behavior From a theoretical perspective it is not

clear why this should be the case Moreover if our results were mainly driven by strategic

interactions then firms in concentrated markets would not only hoard more cash after the

adoption of BC laws but would also try to improve their operational efficiency to better cope

with the increased predatory threats However contrary to this prediction and consistent with

the idea that managers decided to enjoy the ldquoquiet liferdquo Giroud and Mueller (2010) find that

these firms became less efficient after the passage of the BC laws Finally we also find that the

negative relation between industry concentration levels and corporate disbursements is much

stronger among large firms This result is unlikely to be driven by strategic considerations

because predatory issues should be less of a concern for large firms as they possess more

resources and potentially more market power to fend off any predatory attack than do small

firms

6

In a recent paper Hoberg Phillips and Prabhala (2014) also examine the effect of

industry concentration on corporate payout policy Using a new measure of the HHI based on

text-based analysis these authors find that firms in more concentrated industries tend to pay

more dividends In this paper we reconcile our results with these recent findings by showing that

the HHI based on text-based analysis is not a good instrument for actual industry concentration

According to theory concentrated industries (eg oligopolistic markets) should be populated by

larger and more profitable firms Consistent with these predictions we corroborate the findings

in Ali Klasa and Yeung (2008) and show that the HHI from the Census of Manufacturers is

positively correlated with firm size and price-cost margins (Lerner index) In contrast the

measure constructed by Hoberg Phillips and Prabhala (2014) is negatively correlated with firm

size and unrelated to price-cost margins For example according to this measure the average

sales of firms in the least concentrated industries are 26 larger than the average sales of the firms

in the most concentrated industries This evidence suggests that the measure of concentration

we use in this paper is better proxy for competition than the one used in recent studies

Overall our settings enable us to analyze the interaction between two corporate

governance mechanisms an internal onemdashdividend policy and an external onemdashcompetition

The higher payouts in more competitive industries suggest that intense product market

competition appears to have induced management to disgorge cash through dividends These

findings lend further support to the idea that corporate payouts are the outcome of external

disciplinary forces similar to LLSV (2000) where the external force is the extent of investorsrsquo

protection or Michaely and Roberts (2012) where the external force is the disciplinary force of

public financial markets The findings also underscore the importance of agency conflicts in the

7

determination of corporate payout policy Finally they provide another example of how product

market competition can have a significant effect on corporate financial decisions

The paper is organized as follows Section 2 discusses the theoretical arguments linking

corporate payout policy to product market competition Section 3 describes the sample selection

procedure defines the variables and provides summary statistics Section 4 investigates the

empirical relation between industry concentration levels and corporate payout policy In Section

5 we investigate whether agency theory can explain the relation between product market

competition and corporate payout policy documented in this paper In Section 6 we reconcile

our results with the existing literature that indicates that firms in less concentrated markets have

lower payout ratios Section 7 concludes

2 The Link between Corporate Payout Policy and Product Market Competition

In this section we discuss several potential channels through which product market

competition can affect managersrsquo decision to distribute cash to their shareholders Building on

the work of LLSV we explain how corporate payouts could be the outcome of intense product

market competition or alternatively a substitute for competition Further we explain how

potential predatory behavior in less competitive markets can affect corporate payout policy

21 Outcome Model

The outcome model contends that managers need some inducements to dispense free cash

flows This inducement can be stricter investorsrsquo protection laws (LLSV (2000)) tighter

regulation and corporate control (Michaely and Roberts (2012)) or product market competition

Managers in highly competitive markets should distribute more cash to their shareholders

because they are more likely to be penalized by the disciplinary forces of competition if they

mishandle the resources of the firm The premise of competition as a disciplinary role is not

8

new and can be based on several theoretical arguments The first argument is related to the

threat-of-liquidation hypothesis (see for example Schmidt (1997) and Aghion Dewatripont and

Rey (1999)) which states that if a firm in a highly competitive industry begins investing in

negative NPV projects or overspending then it will become less competitive (eg raising prices

to subsidize the bad projects) and consequently more likely to be driven out of the market

Thus to avoid liquidation loss of bonuses that are related to stock price performance or the loss

of their jobs managers in more competitive markets are more likely to pay higher dividends and

avoid negative NPV projects The second argument is related to the yardstick competition

hypothesis (see for example Holmstrom (1982) Nalebuff and Stiglitz (1983) and Shleifer

(1985)) Under this hypothesis product market competition reduces asymmetric information and

monitoring costs by generating greater opportunities for outsiders to benchmark the performance

of a firm to the performance of its competitors Therefore according to this argument intense

competition could make dividends more appealing by reducing the likelihood of overinvestment

and management failure

The ldquooutcomerdquo model has two important implications On the one hand it predicts a

negative relation between industry concentration levels and corporate payouts On the other

hand it predicts that the negative relation between concentration levels and payouts should be

stronger among firms with severe agency problems of free cash flows The main rationale for

the latter prediction is that if competition affects corporate payout policy by increasing the risk

and the cost of overinvesting then its effect on payouts should be stronger among those firms

that are more likely to overinvest We test this implication in two ways First we examine the

effect of business combination laws on the relation between payout policy and product market

competition As discussed above these laws exogenously exacerbated the agency conflicts

9

between managers and shareholders by (at least partially) immunizing firms from the market for

corporate control Since the market for corporate control is viewed as a substitute for product

market competition one would expect managers in less competitive markets to face less pressure

from external factors than managers in more competitive markets after the adoption of these

laws Therefore the ldquooutcomerdquo model predicts that the passage of the business combination

laws should lead to a larger gap in dividends between firms in competitive and non-competitive

markets Second we examine whether the relation between concentration levels and corporate

payouts is stronger among large and low-growth firms which due to their nature are more likely

to have agency problems of free cash flows

22 Substitution Model

Firms in less competitive markets face higher agency costs associated with free cash

flows One potential reason for this is that these firms have the ability to generate extraordinary

rents which allows managers to have access to more free cash flows (eg Jensen (1986)

Shleifer and Vishny (1997) Giroud and Mueller (2010)) Another potential reason is that

managers in less competitive markets are more likely to overinvest because they are less

susceptible to the disciplinary forces of product market competition As discussed above since

value-destroying managers in less competitive markets have more slack to subsidize negative

NPV projects they are more likely to avoid liquidation than similar managers in more

competitive industries

Under the ldquosubstitutionrdquo model dividends are a substitute for other disciplinary measures

such as laws and regulations (LLSV (2000)) compliance and regulations of public markets

(Michaely and Roberts (2012)) or the disciplinary role of market competition Additionally

payout may be used more commonly in less competitive markets (ie markets with less

10

information) because of reputation and signaling Thus managers in less competitive markets

pay dividends and repurchase shares to mitigate the potential agency costs generated by the lack

of competitive pressure from the product market According to recent theoretical arguments

managers of under-valued firms may rationally pay dividends to either establish a reputation for

treating shareholders well so they can raise capital at favorable terms in the future (LLSV

(2000)) or to maximize the value of their holdings in the firm (Gomes (2000))

The empirical implication is that corporate payouts should be positively correlated with

industry concentration levels because dividends and share repurchases are being used as a

substitute for intense competition However this model does not provide clear predictions on

how the magnitude of potential agency problems should affect the positive relation between

concentration levels and corporate payouts If managers use corporate payouts to establish a

reputation as good managers to raise capital on better terms in the future (LLSV (2000)) then the

positive relation between concentration levels and payouts should be stronger among high-

growth firms that generate low cash flows because these are the firms that are most likely to

access the capital markets in the future (eg small firms) If on the other hand managers use

corporate payouts to mitigate the agency costs of free cash flows so they can maximize the value

of their holdings in the firm (Gomes (2000)) then we should expect a stronger positive

correlation between concentration levels and payouts among firms with severe agency costs of

free cash flows (eg large firms) The main reason for this is that the benefits of reducing

potential agency problems are larger among this type of firms

23 Predation Hypothesis

It is also possible that product market competition and payout policy may interact for

strategic consideration such as predation risk For example an implication of Bolton and

11

Scharfstein (1990) is that firms will tend to pay lower dividends and hoard more cash so that

they are better able to fend off potential predatory behavior1 Since this behavior is unlikely to

be effective in competitive markets not only because prices are equal to marginal costs but also

because there is no gain from having n-1 firms instead of n firms in the market predatory risk is

higher in less competitive markets Thus the major prediction of the predation hypothesis is that

payouts should be lower in more concentrated industries

Note that the predation hypothesis and the ldquooutcomerdquo model generate similar predictions

regarding the relation between product market competition and corporate payouts lower level of

dividends in less competitive markets However while the predation hypothesis does not have

any clear predictions regarding the effect of the BC laws on the relation between concentration

levels and corporate payout policy the ldquooutcomerdquo model predicts that the relation between these

two variables should become stronger after the passage of the BC laws Therefore our tests

examining the effects of the BC laws on the HHI-payout policy relation allow us to distinguish

between these two hypotheses Further the predation hypothesis predicts that the negative

relation between concentration levels and payouts should be stronger among small firms This

follows from the idea that predation is less likely to occur against large firms since these firms

possess more resources and market power to fend off any predatory attack Further because

large firms are less likely to be financially constrained than small firms (eg Hadlock and Pierce

(2010)) holding cash to avoid passing profitable investment opportunities is less of a concern for

large firms than it is for small firms (see for example Acharya Almeida and Campello (2007))

24 Agency Theory and the Form of Payout Dividends vs Repurchases

Over the last two decades share repurchases have become an important payout

mechanism in part as a substitution for dividends (Grullon and Michaely (2002)) At the same 1 Bolton and Scharfsteinrsquos (1990) original argument is about debt but it also holds for dividends (and repurchases)

12

time there is clear evidence that repurchases are less persistent than dividends (eg Leary and

Michaely (2011)) and that they are more likely to be used to distribute non-recurring cash flows

than to distribute permanent cash flows (Jagannathan Stephens and Weisbach (2000))

Because of these differences dividends are perceived as a stronger commitment device than

share repurchases As in the case of debt (Zwiebel (1996)) this suggests that dividends are a

more credible mechanism to reduce the amount of free cash flow in the firm than share

repurchases Therefore if agency considerations are an important determinant of our results

then one would expect product market competition to have a stronger effect on dividends than on

share repurchases

3 Sample Selection Variable Definitions and Descriptive Statistics

31 Sample Selection

Our initial sample consists of all firms operating in any of the industries covered by the

Census of Manufacturers (SIC code interval 2000-3990) This census reports the results from a

survey taken every five years in which all manufacturing firms in the US are asked to provide

information on their number of employees payroll and total output Unlike most surveys this is

a fully comprehensive sample since firms are required by federal law to respond to the survey

supplied by the US Census (Title 13 of the US Code) Thus selection bias is not a significant

issue Using this information the US Census calculates several summary statistics including

the Herfindahl-Hirschman index (HHI) that we use in this paper

Since the HHIs are only reported every five years we assume that the indexes stay

constant until the results from a new survey are available For example we use the HHIs

reported in 1987 for the observations in years 1987 1988 1989 1990 and 1991 This approach

is unlikely to bias our empirical results because the HHI does not experience large changes over

13

time For example the probability that an industry in the smallest HHI quintile moves to the

largest HHI quintile (or vice versa) over a period of 5 years is virtually zero

From our initial sample of manufacturing firms we then select those observations that

satisfy the following criteria (1) the firm appears on the CRSPCompustat merged files (2) the

firm operates in an industry covered by the Census of Manufacturers (SIC code interval 2000-

3990) and (3) the firmrsquos total assets are greater than $1 million This selection process generates

a final sample of 64647 firm-year observations over the period 1972 to 2010 This is a

relatively large sample considering that it only contains manufacturing firms

32 Variable Definitions

321 Proxy for Industry Concentration

Following Aggarwal and Samwick (1999) Allayanis and Ihrig (2001) Campello (2006)

MacKay and Phillips (2005) Akdoğu and MacKay (2008) and Haushalter Klasa and Maxwell

(2007) among others we use the Herfindahl-Hirschman Index (HHI) from the Census of

Manufacturers as a proxy for product market competition The US Census calculates this index

by summing up the squares of the individual market shares for the 50 largest firms in the

industry If the industry has less than 50 firms then the US Census uses the total number of

firms in the industry Since in most industrial groups the largest 50 firms capture most of the

market this index is a reasonable proxy for the overall level of industry concentration In this

paper we use four-digit SIC HHIs

322 Measures of Corporate Payouts

Using data from Compustat we construct the following six measures of corporate

payouts dividends and share repurchases scaled by total sales (item SALE) dividends and share

repurchases scaled by total assets (item AT) and dividends and share repurchases scaled by the

14

market value of equity (item CSHO times item PRCC_F) Dividends (DIV) are equal to the total

dollar amount of dividends declared on the common stock of a company during a year (item

DVC) Share repurchases (REPO) are equal to the expenditure on the purchase of common and

preferred stocks (item PRSTKC) We examine share repurchases because they have become an

important payout method for many firms (see for example Grullon and Michaely (2002))

Finally to mitigate the effect of outliers we exclude from our analyses all observations where

the payout ratios are greater than one

323 Control Variables

Following the literature on corporate payout policy we control for the following firm

characteristics in our empirical analyses

bull Maturity Our proxies for the level of firm maturity are the market value of equity

(MV) and the age of the firm (AGE) MV is defined as the total number of common

shares outstanding (Compustat item CSHO) times the closing stock price at the end of

the fiscal year (item PRCC_F) AGE is the time (in years) from the firmrsquos CRSP

listing date

bull Investment Opportunities We use the market-to-book ratio (MB) as a proxy for

investment opportunities MB is equal to the book value of assets (item AT) plus the

market value of equity (MV) minus the book value of equity (item CEQ) scaled by

the book value of assets

bull Risk Our proxy for risk is the volatility of stock returns (RETVOL) RETVOL is

the standard deviation of monthly stock returns over a one-year period

15

bull Profitability We use the return on assets (ROA) as a proxy for the level of

profitability of the firm ROA is the operating income before depreciation (item

OIBDP) scaled by the book value of assets

bull Leverage We define leverage (DEBTASSETS) as long-term debt (item DLTT) plus

short-term debt (item DD1) scaled by the book value of assets

To mitigate the effect of outliers MB and ROA have been winsorized at the 1 and the

99 of their empirical distribution Further since there is evidence that corporate payout policy

in the US has significantly changed over the last three decades (see for example Fama and

French (2001) and Grullon and Michaely (2002)) we also include year dummies in our

regressions to control for any time trends Finally we include industry fixed effects where

industry is defined by the firmrsquos two-digit SIC code

Given the well documented fact that large stable profitable old firms with low

investment opportunities are more likely to distribute cash to their shareholders than are other

types of firms we expect the coefficients of MV AGE and ROA to have a positive sign and the

coefficients of MB and RETVOL to have a negative sign However the coefficient of

DEBTASSETS could be positive or negative depending on whether firms treat leverage as a

substitute for payouts or as a complement to payouts

324 Descriptive Statistics

Table 1 reports summary statistics for the firms in our sample This table shows that the

average sample firm has a dividend yield (DIVMV) equal to 106 and a repurchase yield of

(REPOMV) equal to 105 These payout ratios are very similar to the ones reported in

Grullon and Michaely (2002) Further the average firm in our sample is almost 13 years old and

it has a market value of equity (MV) of $11 billion a market-to-book ratio (MB) equal to 20 a

16

debt-to-asset ratio (DEBTASSETS) equal to 167 and a return on assets (ROA) equal to

43 The characteristics of the average firm in our sample are very similar to the characteristics

of the average firm in Compustat (not reported in a table) Thus it seems that our sample is not

biased toward a particular type of firm Finally Table 1 also shows that there are large cross-

sectional differences in payout ratios and firm characteristics This large dispersion in both

dependent and independent variables should improve the power of our empirical tests to detect

any effect of concentration levels on corporate payouts

4 The Relation between Industry Concentration Levels and Corporate Payout Policy

In this section we investigate whether product market competition affects managersrsquo

decision to distribute cash to their shareholders We perform this analysis by regressing scaled

measures of dividends and repurchases on the Herfindahl-Hirschman Index (HHI) size (MV)

market-to-book ratio (MB) return on assets (ROA) debt-to-total assets ratio (DEBTASSETS)

age of the firm (AGE) stock return volatility (RETVOL) year dummies and industry dummies

Since our measures of corporate payouts are truncated at zero and one we estimate the

regression coefficients using a two-sided Tobit model Following Petersen (2009) we control

for possible cross-sectional dependence in the residuals by adjusting the standard errors for

within-firm correlation and control for any time series dependence by including time dummies

We do not include firm-fixed effects in our panel data regressions because the HHIs do not

change much over time However we include two-digit SIC code dummies to control for

industry-fixed effects

The first three columns of Panel A of Table 2 report estimates of regressions relating

scaled dividends to the HHI and other control variables Consistent with the predictions of the

ldquooutcomerdquo model and the predation risk hypothesis these columns show that dividend payout

17

ratios are negatively correlated with industry concentration levels Note that the coefficient of

the HHI is negative and statistically significant in all the specifications To control for potential

non-linearities in the relation between payout ratios and HHI we also consider specifications in

which instead of using the continuous variable HHI we use a dummy variable equal to one if the

HHI is above its median zero otherwise We report the results from this alternative specification

in the last three columns of Panel A of Table 2 Consistent with our results using the continuous

variable we find that firms in high HHI industries have lower dividend payout ratios than firms

in low HHI industries

As expected Table 2 shows that dividend payout ratios are positively correlated with size

(MV) maturity level (AGE) and profitability (ROA) and negatively correlated with growth

opportunities (MB) and volatility (RETVOL) Moreover there is evidence that dividends are

negatively related to leverage (DEBTASSET) which suggests that firms use debt as a substitute

for dividends In general these results are consistent with the stylized fact that large stable

profitable old firms with low investment opportunities pay more dividends

As discussed earlier dividends have been shown to be a stronger commitment device

than share repurchases (see for example Jagannathan Stephens and Weisbach (2000) and

Guay and Harford (2000)) Consequently if agency considerations are an important determinant

of the relation between competition and payouts then product market competition should have a

weaker effect on share repurchases To test this hypothesis we replicate the previous analyses

using share repurchases instead of dividends (Panel B of Table 2) We find that the relation

between repurchases and the HHI appears to be weaker than the relation between dividends and

the HHI Consistent with the implications of agency theory these results indicate that product

market competition has the strongest effect on the least flexible payout method

18

We augment the previous analysis by examining the effect of industry concentration on

the decision to increase distribute cash to shareholders We use this alternative approach to

examine whether our main results hold over the following discrete payout decisions (1) the

decision to pay dividends (Div gt 0) (2) the decision to increase dividends (change in Div gt 0)

and (3) the decision to repurchase shares (Rep gt 0) Given the nature of these dependent

variables we estimate the regression parameters using a Logit model Table 3 reports the results

from this analysis Consistent with the results in Table 2 we find that firms in less competitive

markets are less likely to pay dividends and less likely to increase dividends relative to firms in

more competitive markets Further there is some evidence that firms in less competitive

markets are less likely to repurchase shares (see columns 3 amp 6) albeit these results are much

weaker than the ones for dividends

The results in Tables 2 and 3 are also economically significant For example Table 2

results imply that an increase of one standard deviation in the HHI reduces the dividend yield

(DIVMV) by 27 from its mean value and the dividend-to-assets ratio (DIVASSETS) by

almost 41 from its mean value Overall the empirical results in this section indicate that firms

in more competitive market tend to have significantly higher dividend payout ratios than firms in

less competitive markets

5 Explaining the Negative Relation between Industry Concentration and Corporate Payout Policy

In the previous section we show that corporate payouts particularly dividend payments

are negatively related to industry concentration levels These results are consistent with both the

ldquooutcomerdquo model proposed by LLSV (2000) and the predation hypothesis In the next two sub-

sections we perform several tests to disentangle these two explanations

51 A quasi-natural experiment The Effect of Business Combination Laws

19

The negative correlation between corporate payouts and HHI supports one of the

implications of agency theorymdashthat payouts are the outcome of external factors However this

negative relation could be driven by some unobservable factor that could be unrelated to agency

problems Therefore to examine whether agency issues are driving our main results we need to

show that an exogenous shock to agency conflicts strengthens the negative relation between

payouts and industry concentration levels

Following the work of Bertrand and Mullainathan (2003) and Giroud and Mueller (2010)

we use the adoption of business combination (BC) laws in the US as a natural experiment to

examine how agency issues affect the relation between corporate payouts and product market

competition The business combination laws were enacted in more than 25 states between 1985

and 1991 These laws make hostile takeovers significantly more difficult by imposing a

moratorium of three to five years on certain types of transactions such as asset sales and mergers

Bertrand and Mullainathan (2003) and Giroud and Mueller (2010) provide empirical evidence

that the BC laws exacerbated the agency problems between managers and shareholders

Therefore we use these laws to examine whether our main results are mainly driven by agency

issues If the market for corporate control serves as a substitute for the lack of product market

competition (Giroud and Mueller (2010)) then the outcome model predicts that the negative

relation between the HHI and payouts should become stronger after the passage of the BC laws

If on the other hand dividends in concentrated industries are being limited as a consequence of

predatory concerns then we expect that the adoption of the BC laws to have no effect on

dividend policy Further since the BC laws only reduce the likelihood of a firm becoming a

takeover target these exogenous events allow us to control for any unobservable factor that

could drive the negative relation between payouts and concentration levels

20

To investigate the effect of the BC laws on the relation between concentration levels and

payouts we perform a differences-in-differences analysis using data around the adoption of these

laws (we use data from 1979 until 1997) We do this by including in our regressions a dummy

variable (DUMBC) equal to one if the firm is incorporated in a state that has passed a business

combination law zero otherwise and a term in which we interact the HHI with DUMBC By

design this latter term should capture the change in the gap in payout ratios between competitive

and non-competitive firms after the passage of the BC laws Thus if agency conflicts are driving

force behind the relation between HHI and corporate payouts then the coefficient on the

interaction term HHI x DUMBC should be negative

Table 4 reports the results from this analysis using scaled measures of dividends and

share repurchases Consistent with the predictions of the outcome we find evidence that the

negative relation between dividends and industry concentration levels becomes significantly

stronger after the passage of the BC laws Panel A of Table 4 shows that the interaction term

Log(HHI) x DUMBC is negative and statistically significant in most specifications

Interestingly when we use the dummy variable DUMHHI to measure concentration we find that

that the regression coefficient on DUMHHI x DUMBC is statistically significant in all

specifications but the coefficient on DUMHHI is not This indicates that the negative

correlation between dividends and concentration levels is only significant for firms incorporated

in states that have passed business combination laws On the other hand Panel B of Table 4

shows that the BC laws did not have any effect on the relation between concentration levels and

share repurchases This suggest that the shock to agency conflicts generated by the BC laws

only affected dividends ndash the payout method that is less flexible and consequently more likely

to reduce agency problems consistent with our findings in the previous section

21

Finally we examine whether the effect of the BC laws on the relation between

concentration levels and corporate payouts hold over discrete payout decisions whether to pay

dividends whether to increase dividends and whether to repurchase shares We report the

results from this analysis in Table 5 Corroborating the results in Table 4 we find that the

negative effect of the HHI on the likelihood of paying dividends or increasing dividends

becomes much stronger after the passage of the business combination laws Note that the

coefficients on Log (HHI) x DUMBC and DUMHHI x DUMBC are negative and statistically

significant all the specifications using dividend decisions as the choice variable (see columns 1

2 4 and 5) Further consistent with our previous results we do not find any effect of the BC

laws on the relation between the HHI and the decision to repurchase shares

Overall the results in this section support the idea that the negative relation between

concentration and corporate dividend payouts is driven by agency considerations In particular

they provide support to the theoretical argument in LLSV (2000) that corporate dividend policy

is the outcome of external factors Further since it is not clear why BC laws should only make

firms in less concentrated markets more vulnerable to predatory threats these results suggest that

strategic interactions in the product market are not a main determinant of the negative relation

between competition and payout ratios In fact if our results were mainly driven by predatory

issues then the firms in concentrated markets that were affected by the BC laws would have

tried to become more efficient to fend off potential predatory attacks by their competitors

However the evidence in Giroud and Mueller (2010) indicates managers of these firms decided

to adopt the ldquoquiet liferdquo which suggests that they were not extremely concerned about predation

52The Effect of Firm Size

22

In the previous sub-section we examine the effect of the BC laws on the relation between

market concentration and corporate payout policy to distinguish the ldquooutcomerdquo model from the

predation hypothesis The results from these seem to support the predictions of the ldquooutcomerdquo

model To further investigate whether agency or predatory issues are driving our main results in

this sub-section we examine the effect of firmrsquos position within the industry (proxied by their

relative market cap) on the relation between concentration and payout

The predation risk hypothesis suggests that the negative relation between the HHI and

payout ratios should be weaker among large firms and stronger among small firms The main

intuition behind this argument is that the largest firms in a particular industry should be less

concerned about inducing predatory behavior than the smallest firms because the former firms

have more resources and potentially more market power to fend off any predatory attack than the

latter firms

If corporate payouts are the ldquooutcomerdquo of intense product market competition however

then we should expect that the effect of competition on payouts should be stronger among those

firms that are more likely to have high agency cost of free cash flows2 Thus since large firms

tend to be mature firms that generate substantial and stable cash flows the ldquooutcomerdquo model

predicts that the negative relation between the HHI and payouts should be stronger among this

type of firms

To investigate whether the relation between the HHI and payout ratios is different

between large and small firms we include in our regressions a term that interacts the

concentration measure (HHI) with a dummy variable (LARGE) that is equal to one if a firmrsquos

market value is above its industry (four-digit SIC code) average market value at time t If the

2 Jensen (1986) argues that agency costs of free cash flows are likely to be more severe among ldquofirms that have stable business histories and substantial free cash flow (ie low growth prospect and high potential for generating cash flows)rdquo

23

predation risk hypothesis is correct then the coefficient of the interaction term (HHI x LARGE)

should be positive However if agency considerations are the main drivers behind the relation

between concentration levels and corporate payouts then the coefficient of the interaction term

should be negative

Table 6 reports the results from this analysis Consistent with the predictions of the

ldquooutcomerdquo model Panel A shows that the coefficient of the interaction term (HHI x LARGE) is

negative and statistically significant in all specifications using scaled measures of dividends as

dependent variables This result implies that the negative relation between the HHI and

dividend payout ratios is much stronger among large firms Interestingly Panel A shows that the

coefficients on Log (HHI) and DUMHHI are not statistically significant which suggests that the

relation between concentration levels and dividend payout ratios is mainly driven by large firms

In Panel B of Table 6 we find similar results using scaled measures of share repurchases as

dependent variables but the results are weaker than the ones using dividends Table 7 replicates

the analysis in Table 6 using discrete payout decisions as dependent variables Consistent with

our previous empirical results Table 7 shows that the effect of the HHI on the decision to pay

dividends increase dividends or repurchase shares is generally stronger among the largest firms

in a particular industry

One again the economic magnitude of the coefficients reported in Table 6 and 7 is large

For example among large firms an increase of one standard deviation in the HHI reduces the

dividend yield (DIVMV) by 47 from its mean value and the dividend-to-assets ratio

(DIVASSETS) by almost 74 from its mean value In general the empirical results in this

section indicate that the negative relation between HHI and corporate payouts is mainly driven

by firms that are likely to have high agency cost of free cash flows While these findings seem

24

to support the idea that corporate payouts are the ldquooutcomerdquo of external factors they are

inconsistent with the idea that firms in more concentrated markets tend to pay less cash to fend

off predatory behavior from competitors

6 Does the Choice of Concentration Measure Matter

In a recent paper Hoberg and Phillips (2014) developed an alternative measure of the

HHI (TNIC3 HHI) using industry classifications based on firm pairwise similarity scores from

text analysis of firm 10K product descriptions Hoberg Phillips and Prabhala (2014) use this

alternative measure of concentration in their empirical tests and find that firms in more

concentrated industries tend to pay more dividends Given that these results are at odds with our

main findings we investigate in this section the source of the discrepancy between the Census

HHI and the TNIC3 HHI

To illustrate this issue Table 8 examines the empirical relation between dividend payout

ratios and these two alternative measures of concentration over the period 1997-20103 While

columns 1 2 and 3 show that our main results are robust over this sample period columns 4 5

and 6 show that dividends are positively related to the TNIC3 HHI This inconsistency in the

relation between corporate payouts and concentration levels strongly suggests that the Census

HHI and the TNIC3 HHI are measuring different aspects of firmsrsquo product markets

One potential reason for this discrepancy is that Hoberg and Phillips (2014) construct

their measure of concentration using data from publicly-traded firms that appear on Compustat

As pointed out by several authors the concentration measures derived from Compustat data are

less meaningful than the ones reported by the Census of Manufacturers because the former

measures are constructed only using public firms while the latter measure uses both private and

public firms In a recent study Ali Klasa and Yeung (2009) show that this key difference 3 We restrict our analysis to this sample period because the TNIC3 HHI is only available after 1996

25

between these two measures seems to significantly bias the HHI derived from Compustat data

For example consistent with the idea that more concentrated industries should be populated by

larger and more profitable firms Ali et al (2009) find that the Census HHI is positively

correlated with both average firm size and price-cost margins Further they show that the total

number of firms in the industry is negatively related to the Census HHI However they do not

find these results when they use the HHI derived from Compustat data In fact they find that

industries classified as concentrated using the Compustat HHI tend to be populated by smaller

firms These findings suggest that the use of Compustat concentration measures as proxy for

industry concentration may lead to incorrect inferences

To investigate whether the TNIC3 HHI is good proxy for competition we replicate the

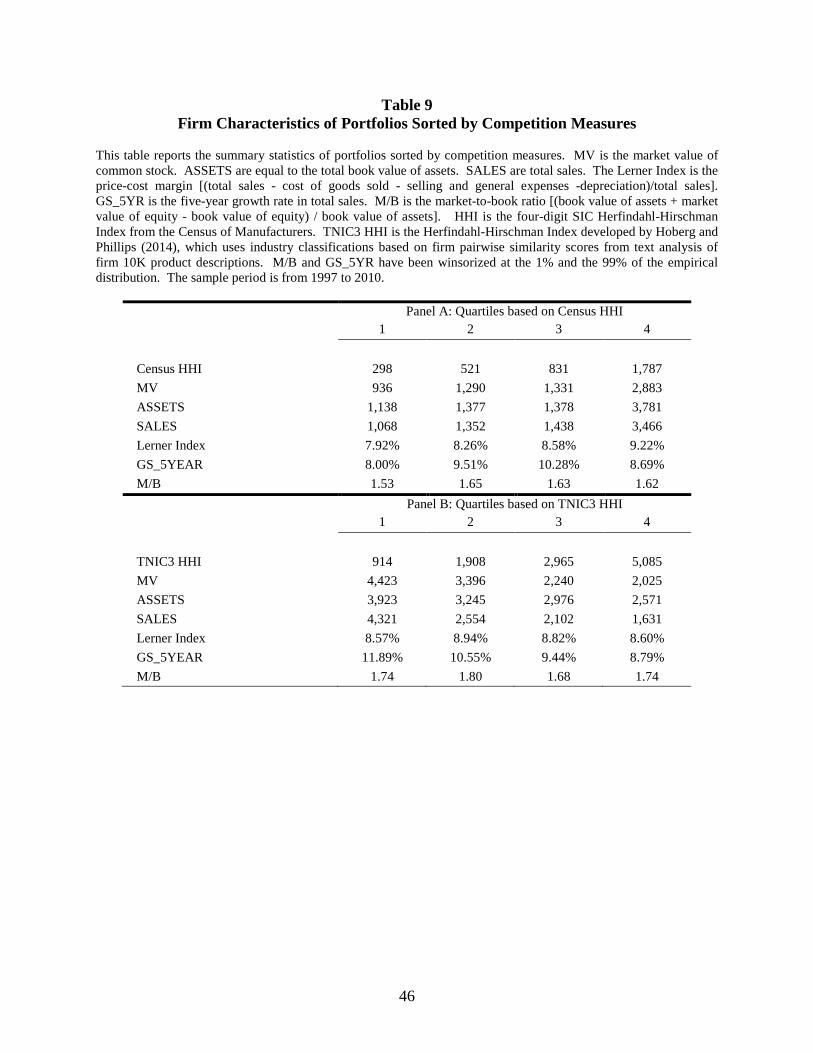

analysis in Ali et al (2009) for both the Census HHI and the TNIC3 HHI The results from this

analysis are reported in Table 9 Corroborating the findings in Ali et al (2009) Panel A shows

that the Census HHI is positively correlated with several proxies for firm size (market

capitalization total assets and total sales) and price-cost margins In contrast Panel B shows

that the TNIC3 HHI is negatively correlated with all the proxies for firm size and uncorrelated

with price-cost margins To better visualize these patterns Figures 1 and 2 depicts the

characteristics of portfolios sorted by competition measures In general these results indicate

that TNIC3 HHI suffers from the same biases as the Compustat HHI which raises important

concerns about the validity of this concentration measure

7 Conclusion

Our study extends the work of LLSV (2000) by arguing that product market competition

can be viewed as an additional external disciplinary factor Based on the idea that competition

can exert pressure on managers to distribute cash to their shareholders by increasing the risk and

26

the cost of overinvesting we argue that corporate payouts could either be the result of product

market competition or alternatively a disciplinary devise that substitutes for competition A

third alternative is that payout policy is related to competition through predation risk Firms in

less competitive markets pay out less and hoard more cash to reduce potential predatory attacks

from competitors

The results in this paper seem to support the idea that corporate payouts are the outcome

of the disciplinary forces of product market competition We find that corporate payouts are

positively correlated with the intensity of industry competition even after controlling for

potential confounding effects There is no support for the notion that corporations use payout

policy as an alternative governance mechanism to competition Moreover consistent with the

implications of agency theory we find that the effect of product market competition on payouts

becomes much stronger among firms affected by the business combinations laws adopted by

several states in the US during the 1980s and 1990s Since these laws exacerbated the agency

conflict between managers and shareholders by immunizing firms against the market for

corporate control our findings indicate that the link between concentration levels and corporate

payouts is mainly driven by agency considerations

The initial results-that firms in more competitive market have higher payout than

otherwise similar firms in less competitive markets-is also consistent with the predation-risk

alternative The use of the change in the BC laws sheds some light on this issue as well since

predation risk imply no change in payout policy as a consequence of these law changes Our

findings of great effect of competition on payout after the passage of the law is not consistent

with the notion that predation is the dominant factor affect the relation between competition and

payout Further analysis reveals that the difference in payout policy between firms in competitive

27

and less competitive market is primarily driven by large firms That is our main results are

driven by firms who are more likely to be subject to free cash flow issues rather than to predatory

issues

Overall our results complement the empirical results in LLSV While they find evidence

suggesting that a strong legal system exerts pressure on corporate managers to distribute excess

cash to their shareholders we find that intense product market competition appears to have

similar effects These findings are important because they further suggest that competition is

indeed a strong disciplinary devise At the same time the findings suggest that agency problems

play an important role in managersrsquo decision to distribute cash to shareholders and that at times

external disciplinary devises such as competition induce managers to behave more optimally

28

References

Acharya V H Almeida and M Campello 2007 ldquoIs Cash Negative Debt A Hedging Perspective on Corporate Financial Policiesrdquo Journal of Financial Intermediation 16 515-554

Aggarwal R and A Samwick 1999 ldquoExecutive Compensation Strategic Competition and

Relative Performance Evaluation Theory and Evidencerdquo Journal of Finance 54 1999-2043

Aghion P M Dewatripont and P Rey 1999 ldquoCompetition Financial Discipline and

Growthrdquo Review of Economic Studies 66 825-852 Akdoğu E and P MacKay 2008 ldquoInvestment and Competitionrdquo Journal of Financial and

Quantitative Analysis 43 299-330 Ali A S Klasa and E Yeung 2009 ldquoThe Limitations of Industry Concentration Measures

Constructed with Compustat Data Implications for Finance Researchrdquo Review of Financial Studies 22 3839-3871

Allayannis G and J Ihrig 2001 ldquoExposure and Markupsrdquo Review of Financial Studies 14

805-835 Allen F and D Gale 2000 ldquoCorporate Governance and Competitionrdquo published in Corporate

Governance Theoretical and Empirical Perspectives edited by X Vives Cambridge University Press 23-94

Allen F A Bernardo and I Welch 2000 ldquoA Theory of Dividends Based on Tax Clientelesrdquo

Journal of Finance 55 2499-2536 Ang J R Cole and J Lin 2000 ldquoAgency Costs and Ownership Structurerdquo Journal of Finance

55 81-106 Arabmazar A and P Schmidt 1981 ldquoFurther Evidence on the Robustness of the Tobit

Estimator to Heteroskedasticityrdquo Journal of Econometrics 17 253-258 Arabmazar A and P Schmidt 1982 ldquoAn Investigation of the Robustness of the Tobit

Estimator to Non-Normalityrdquo Econometrica 50 1055-1063 Bebchuk L A Cohen and A Ferrell 2009 ldquoWhat Matters in Corporate Governancerdquo Review

of Financial Studies 22 783-827 Berger A and T Hannan 1998 ldquoThe Efficiency Cost of Market Power in the Banking

Industry A Test of the ldquoQuiet Liferdquo and Related Hypothesesrdquo The Review of Economics and Statistics 80 454-465

29

Bertrand M and S Mullainathan 2003 ldquoEnjoying the Quiet Life Corporate Governance and Managerial Preferencesrdquo Journal of Political Economy 111(5) 1043-1075

Bolton P and D Scharfstein 1990 ldquoA Theory of Predation Based on Agency Problems in

Financial Contractingrdquo American Economic Review 80 93-106 Boudoukh J R Michaely M Richardson and M Roberts 2007 ldquoOn the Importance of

Measuring Payout Yield Implications for Empirical Asset Pricingrdquo Journal of Finance 62 877-915

Campello M 2006 ldquoDebt Financing Does it Boost or Hurt Firm Performance in Product

Marketsrdquo Journal of Financial Economics 83 135-172 Caves R 1980 ldquoIndustrial Organization Corporate Strategy and Structurerdquo Journal of

Economic Literature 18 64-92 Chhaochharia V Y Grinstein G Grullon and R Michaely 2012 ldquoProduct Market

Competition and Internal Governance Evidence from the Sarbanes Oxley Actrdquo Working Paper Cornell University

DeAngelo H L DeAngelo and R Stulz 2006 ldquoDividend Policy and the EarnedContributed

Capital Mix A Test of the Lifecycle Theoryrdquo Journal of Financial Economics 81(2) 227-254

DeFond M and C Park 1999 ldquoThe Effect of Competition on CEO Turnoverrdquo Journal of

Accounting and Economics 27 35-56 Fama E and K French 2001 ldquoDisappearing Dividends Changing Firm Characteristics or

Lower Propensity to Payrdquo Journal of Financial Economics 60 3-43 Fee C and C Hadlock 2000 ldquoManagement Turnover and Product Market Competition

Empirical Evidence from the US Newspaper Industryrdquo Journal of Business 73 205-243

Giroud X and H M Mueller 2010 ldquoDoes Corporate Governance Matter in Competitive

Industriesrdquo Journal of Financial Economics 95 312-331 Giroud X and H M Mueller 2011 ldquoCorporate Governance Product Market Competition and

Equity Pricesrdquo Journal of Finance 66 563-600 Gomes A 2000 ldquoGoing Public without Governance Managerial Reputation Effectsrdquo Journal

of Finance 55 615-646 Gompers P J Ishii and A Metrick 2003 Corporate Governance and Equity Prices

Quarterly Journal of Economics 118 107-155

30

Graham D D Kaplan and D Sibley 1983 ldquoEfficiency and Competition in the Airline Industryrdquo Bell Journal of Economics 14 118-138

Griffith R 2001 ldquoProduct Market Competition Efficiency and Agency Cost An Empirical

Analysisrdquo Working Paper Institute for Fiscal Studies Grinstein Y and R Michaely 2005 ldquoInstitutional Holdings and Payout Policyrdquo Journal of

Finance 60 1389-1426 Grinstein Y and A Palvia 2006 ldquoExecutive Loans Corporate Governance and Firm

Performance - Evidence from Banksrdquo Working Paper Cornell University Grullon G and R Michaely 2002 ldquoDividends Share Repurchases and the Substitution

Hypothesisrdquo Journal of Finance 57 1649-1684 Grullon G and R Michaely 2004 ldquoThe Information Content of Share Repurchase Programsrdquo

Journal of Finance 59 651-680 Guay W and J Harford 2000 ldquoThe Cash-Flow Permanence and Information Content of

Dividend Increases versus Repurchasesrdquo Journal of Financial Economics 57 385-415 Hart O 1983 ldquoThe Market as an Incentive Mechanismrdquo Bell Journal of Economics 14 336-

382 Haushalter D S Klasa and W Maxwell 2007 ldquoThe Influence of Product Market Dynamics on

the Firms Cash Holdings and Hedging Behaviorrdquo Journal of Financial Economics 84 797-825

Hermalin B 1992 ldquoThe Effects of Competition on Executive Behaviorrdquo RAND Journal of

Economics 23 350-365 Hicks J 1935 ldquoAnnual Survey of Economic Theory The Theory of Monopolyrdquo Econometrica

3 1-20 Hoberg G and G Phillips 2014 ldquoText-Based Network Industries and Endogenous Product

Differentiationrdquo Working Paper University of Maryland Hoberg G G Phillips and N Prabhala 2014 ldquoProduct Market Threats Payouts and Financial

Flexibilityrdquo Journal of Finance 69 293-324 Holmstrom B 1982 ldquoMoral Hazard in Teamsrdquo Bell Journal of Economics 13 324-340 Jagannathan R and S B Srinivasan 1999 ldquoDoes product market competition reduce agency

costsrdquo North American Journal of Economics and Finance 10 387ndash399

31

Jagannathan M C Stephens and M Weisbach 2000 ldquoFinancial Flexibility and the Choice between Dividends and Stock Repurchasesrdquo Journal of Financial Economics 57 355-384

Jensen M 1986 ldquoAgency Costs of Free Cash Flow Corporate Finance and Takeoversrdquo

American Economic Review 76 323-329 John K and A Knyazeva 2006 ldquoPayout Policy Agency Conflicts and Corporate

Governancerdquo Working Paper NYU Kruse T and C Rennie 2006 ldquoProduct Market Competition Excess Free Cash Flows and

CEO Discipline Evidence from the US Retail Industryrdquo Working Paper University of Arkansas

La Porta R F Lopez-de-Silanes A Shleifer and R Vishny 2000 ldquoAgency Problems and

Dividend Policies around the Worldrdquo Journal of Finance 55 1ndash33 Lie E 2000 ldquoExcess Funds and Agency Problems An Empirical Study of Incremental Cash

Disbursementsrdquo Review of Financial Studies 13 219-248 Linderberg E and S Ross 1981 ldquoTobinrsquos q Ratio and Industrial Organizationrdquo Journal of

Business 54 1-32 MacKay P and G Phillips 2005 ldquoHow Does Industry Affect Firm Financial Structurerdquo The

Review of Financial Studies 18 1433-1466 Massa M Z Rehman and T Vermaelen 2007 ldquoMimicking Repurchasesrdquo Journal of Financial

Economics 84 624-666 Michaely R and M Roberts 2012 ldquoCorporate Dividend Policies Lessons from Private

Firmsrdquo Review of Financial Studies 25 711-746 Nalebuff B and J Stiglitz 1983 ldquoPrizes and Incentives Towards a General Theory of

Compensation and Competitionrdquo Bell Journal of Economics 14 21-43 Nickell S 1996 ldquoCompetition and Corporate Performancerdquo Journal of Political Economy 104

724-746 Officer M 2006 ldquoDividend Policy Dividend Initiations and Governancerdquo Working Paper

University of Southern California Petersen M 2009 ldquoEstimating Standard Errors in Finance Panel Data Sets Comparing

Approachesrdquo Review of Financial Studies 22 435-480 Powell J 1984 ldquoLeast Absolute Deviations Estimation of the Censored Regression Modelrdquo

Journal of Econometrics 25 303ndash325

32

Raith M 2003 ldquoCompetition Risk and Managerial Incentivesrdquo American Economic Review 93

1425-1436 Salinger M 1984 ldquoTobinrsquos q Unionization and the Concentration-Profits Relationshiprdquo Rand

Journal of Economics 15 159-170 Scharfstein D 1988 ldquoProduct-Market Competition and Managerial Slackrdquo RAND Journal of

Economics 19 147-155 Schmidt K 1997 ldquoManagerial Incentives and Product Market Competitionrdquo Review of

Economic Studies 64 191-213 Skinner D 2008 ldquoThe Evolving Relation between Earnings Dividends and Stock

Repurchasesrdquo Journal of Financial Economics 87 582-609 Shleifer A 1985 ldquoA Theory of Yardstick Competitionrdquo RAND Journal of Economics 16 319-

327 Shleifer A and R Vishny 1997 ldquoA Survey of Corporate Governancerdquo Journal of Finance 52

737-783 Zwiebel J 1996 ldquoDynamic Capital Structure under Managerial Entrenchmentrdquo American

Economic Review 86 1197-1215

33

Figure 1 Average Total Sales of Portfolios Sorted by Competition Measures

This figure depicts the average total sales of portfolios sorted by competition measures Census HHI is the four-digit SIC Herfindahl-Hirschman Index from the Census of Manufacturers TNIC3 HHI is the Herfindahl-Hirschman Index developed by Hoberg and Phillips (2014) which uses industry classifications based on firm pairwise similarity scores from text analysis of firm 10K product descriptions The sample period is from 1997 to 2010

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1 2 3 4

Mill

ions

of $

Quartiles based on Census HHI

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1 2 3 4

Mill

ions

of $

Quartiles based on TNIC3 HHI

34

Figure 2 Average Lerner Index of Portfolios Sorted by Competition Measures

This figure depicts the average Lerner index sorted by competition measures The Lerner Index is the price-cost margin [(total sales - cost of goods sold - selling and general expenses -depreciation)total sales] Census HHI is the four-digit SIC Herfindahl-Hirschman Index from the Census of Manufacturers TNIC3 HHI is the Herfindahl-Hirschman Index developed by Hoberg and Phillips (2014) which uses industry classifications based on firm pairwise similarity scores from text analysis of firm 10K product descriptions The sample period is from 1997 to 2010

700

750

800

850

900

950

1 2 3 4Quartiles based on Census HHI

700

750

800

850

900

950

1 2 3 4Quartiles based on TNIC3 HHI

35

Table 1 Summary Statistics

This table reports the summary statistics for the sample firms To be included in the sample the observation must satisfy the following criteria the firmrsquos financial data is available on Compustat the firm operates in an industry covered by the Census of Manufacturers (SIC code interval 2000-3990) total assets are greater than $1 million DIV is the total dollar amount of dividends declared on the common stock REPO is the expenditure on the purchase of common and preferred stocks SALES are total sales MV is the market value of common stock ASSETS are equal to the total book value of assets AGE is the time (in years) from the firmrsquos CRSP listing date MB is the market-to-book ratio [(book value of assets + market value of equity - book value of equity) book value of assets] DEBTASSETS is equal to long-term debt plus short-term debt scaled by total assets HHI is the four-digit SIC Herfindahl-Hirschman Index from the Census of Manufacturers ROA is the operating income before depreciation scaled by total assets CAPEX is the level of capital expenditures All the payout measures MB and ROA have been winsorized at the 1 and the 99 of their empirical distribution MV and ASSETS have been deflated by the Consumer Price Index (1982-1984=100) The sample period is from 1972 to 2010

Mean Std Dev 5th Median 95th N Payout Measures DIV ASSETS 080 150 0 0 380 64644 DIV SALES 074 152 0 0 357 63647 DIV MV 106 192 0 0 538 63616 REPO ASSETS 102 305 0 0 649 60056 REPO SALES 116 378 0 0 696 59270 REPO MV 105 304 0 0 637 59026 Proportion of Firms with DIV gt 0 359 Proportion of Firms with REPOgt 0 297 Firm Characteristics MV 1138 5980 3 64 4305 63794 ASSETS 1154 5958 3 62 4253 64866 AGE 134 144 0 9 45 64866 MB 20 14 07 14 56 61718 DEBTASSETS 0167 0170 0 0129 0494 63500 HHI 857 680 270 647 2300 64780 ROA 0043 0246 -0500 0111 0281 64634 RETVOL 0155 0106 0055 0131 0330 58731 CAPEXASSETS 0056 0056 0005 0041 0158 64097

36

Table 2 The Relation between Product Market Competition and Corporate Payouts

This table reports estimates of regressions relating scaled measures of dividends and share repurchases to the Herfindahl-Hirschman Index and other control variables DIV is the total dollar amount of dividends declared on the common stock REPO is the expenditure on the purchase of common and preferred stocks SALES are total sales MV is the market value of common stock ASSETS are equal to the total book value of assets HHI is the four-digit SIC Herfindahl-Hirschman Index from the Census of Manufacturers scaled by 100 DUMHHI is a dummy variable equal to one if the HHI is above its median zero otherwise MB is the market-to-book ratio [(book value of assets + market value of equity - book value of equity) book value of assets] ROA is the operating income before depreciation scaled by total assets DEBTASSETS is equal to long-term debt plus short-term debt scaled by total assets AGE is the time (in years) from the firmrsquos CRSP listing date All the payout measures MB and ROA have been winsorized at the 1 and the 99 of their empirical distribution Since the dependent variables are truncated at zero and one we estimate the regression coefficients using a two-sided Tobit model Standard errors adjusted for within-firm correlation are reported in parentheses below coefficient estimates Superscripts a b and c denote significantly different from zero at the 1 5 and 10 level respectively The sample period is from 1972 to 2010 Panel A Dividends Dependent Variable DIV

SALES DIV MV

DIV ASSETS

DIV SALES

DIV MV

DIV ASSETS

Intercept -00233a -00226a -00209a -00251a -00243a -00227a (00029) (00033) (00027) (00028) (00032) (00026) Log (HHI) -00016a -00015a -00017a (00005) (00006) (00005) DUMHHI -00020a -00017b -00019a (00007) (00080) (00007) log (MV) 00039a 00043a 00031a 00039a 00043a 00031a (00002) (00002) (00002) (00002) (00002) (00002) log (MB) -00057a -00243a -00055a -00058a -00244a -00055a (00008) (00010) (00008) (00008) (00010) (00008) ROA 00680a 00773a 00837a 00683a 00776a 00840a (00037) (00044) (00040) (00037) (00044) (00040) DEBTASSETS -00183a -00166a -00241a -00183a -00165a -00241a (00023) (00026) (00021) (00023) (00026) (00022) log (1+ AGE) 00056a 00072a 00063a 00057a 00072a 00064a (00004) (00005) (00004) (00004) (00005) (00004) RETVOL -01299a -01607a -01330a -01296a -01606a -01328a (00075) (00085) (00073) (00075) (00085) (00073) Year-Fixed Effects Yes Yes Yes Yes Yes Yes Two-Digit SIC Industry-Fixed Effects Yes Yes Yes Yes Yes Yes N 54715 55343 55343 54715 55343 55343

37

Panel B Share Repurchases Dependent Variable REPO

SALES REPO

MV REPO

ASSETS REPO SALES

REPO MV

REPO ASSETS

Intercept -00573a -00437a -00472a -00574a -00440a -00472a (00056) (00045) (00046) (00053) (00044) (00044) Log (HHI) -00004 -00005 -00002 (00010) (00009) (00009) DUMHHI -00027c -00022c -00020c (00015) (00012) (00012) log (MV) 00055a 00033a 00035a 00056a 00033a 00035a (00005) (00004) (00004) (00005) (00004) (00004) log (MB) -00017 -00161a 00009 -00018 -00161a 00008 (00018) (00013) (00014) (00018) (00013) (00014) ROA 00432a 00500a 00636a 00431a 00499a 00636a (00052) (00037) (00043) (00052) (00037) (00043) DEBTASSETS -00407a -00202a -00346a -00408a -00202a -00347a (00049) (00039) (00038) (00049) (00039) (00038) log (1+ AGE) 00051a 00052a 00056a 00051a 00051a 00056a (00008) (00007) (00007) (00008) (00007) (00007) RETVOL -00982a -00821a -00843a -00975a -00816a -00839a (00100) (00078) (00078) (00100) (00078) (00078) Year-Fixed Effects Yes Yes Yes Yes Yes Yes Two-Digit SIC Industry-Fixed Effects Yes Yes Yes Yes Yes Yes N 51101 51608 51608 51101 51608 51608

38

Table 3 Logit Regressions Product Market Competition and Payout Decisions

This table reports estimates of Logit regressions relating payout decisions to the Herfindahl-Hirschman Index and other control variables DIV gt 0 is a dummy variable equal to one if the total dollar amount of dividends declared on the common stock is positive zero otherwise Change in DIV gt 0 is a dummy variable equal to one if the firm increases its dividends from year t-1 to t zero otherwise REPO gt 0 is a dummy variable equal to one if the expenditure on the purchase of common and preferred stocks is positive zero otherwise MV is the market value of common stock HHI is the four-digit SIC Herfindahl-Hirschman Index from the Census of Manufacturers scaled by 100 DUMHHI is a dummy variable equal to one if the HHI is above its median zero otherwise MB is the market-to-book ratio [(book value of assets + market value of equity - book value of equity) book value of assets] ROA is the operating income before depreciation scaled by total assets DEBTASSETS is equal to long-term debt plus short-term debt scaled by total assets AGE is the time (in years) from the firmrsquos CRSP listing date RETVOL is the standard deviation of monthly stock returns MB and ROA have been winsorized at the 1 and the 99 of the empirical distribution Standard errors adjusted for within-firm correlation are reported in parentheses below coefficient estimates Superscripts a b and c denote significantly different from zero at the 1 5 and 10 level respectively The sample period is from 1972 to 2010 Dependent Variable

DIV gt 0 Change in DIV gt 0 REPO gt 0 DIV gt 0

Change in DIV gt 0 REPO gt 0

Intercept -37083a -39547a -12362a -35544a -37831a -11803a (02596) (02025) (01465) (02568) (02009) (01441) Log (HHI) -01312a -01468a -00441 (00501) (00414) (00291) DUMHHI -02028a -02305a -00729c (00695) (00582) (00407) log (MV) 04984a 03818a 01344a 04986a 03819a 01343a (00243) (00178) (00127) (00242) (00177) (00127) log (MB) -13758a -08140a -03352a -13809a -08211a -03356a (00790) (00663) (00417) (00788) (00662) (00417) ROA 65581a 80272a 17317a 65870a 80652a 17355a (03023) (02879) (01248) (03029) (02884) (01249) DEBTASSETS -13200a -06518a -09733a -13229a -06540a -09730a (01949) (01673) (01248) (01954) (01679) (01248) log (1+ AGE) 06786a 04850a 01830a 06816a 04875a 01836a (00420) (00325) (00226) (00420) (00325) (00226) RETVOL -12192a -10083a -2942a -12153a -10028a -2934a (05268) (04747) (02408) (05246) (04719) (02409) Year-Fixed Effects Yes Yes Yes Yes Yes Yes Two-Digit SIC Industry-Fixed Effects Yes Yes Yes Yes Yes Yes N 55343 54552 51608 55343 54552 51608

39

Table 4 The Effect of Business Combination Laws on the Relation between Product Market

Competition and Corporate Payouts

This table examines the effect of business combination laws on the relation between the Herfindahl-Hirschman Index and scaled measures of dividends and share repurchases DIV is the total dollar amount of dividends declared on the common stock REPO is the expenditure on the purchase of common and preferred stocks SALES are total sales MV is the market value of common stock ASSETS are equal to the total book value of assets HHI is the four-digit SIC Herfindahl-Hirschman Index from the Census of Manufacturers scaled by 100 DUMHHI is a dummy variable equal to one if the HHI is above its median value zero otherwise DUMBC is a dummy variable equal to one if the firm is incorporated in a state that has passed a business combination law zero otherwise MB is the market-to-book ratio [(book value of assets + market value of equity - book value of equity) book value of assets] ROA is the operating income before depreciation scaled by total assets DEBTASSETS is equal to long-term debt plus short-term debt scaled by total assets AGE is the time (in years) from the firmrsquos CRSP listing date All the payout measures MB and ROA have been winsorized at the 1 and the 99 of their empirical distribution Since the dependent variables are truncated at zero and one we estimate the regression coefficients using a two-sided Tobit model Standard errors adjusted for within-firm correlation are reported in parentheses below coefficient estimates Superscripts a b and c denote significantly different from zero at the 1 5 and 10 level respectively The sample period is from 1979 to 1997 Panel A Dividends Dependent Variable DIV

SALES DIV MV

DIV ASSETS

DIV SALES

DIV MV

DIV ASSETS

Intercept 00054 00250a 00150a 00014 00208a 00106a (00033) (00043) (00038) (00029) (00038) (00034) Log (HHI) -00021b -00024b -00024b (00009) (00011) (00010) Log (HHI) x DUMBC -00028a -00009 -00024b (00010) (00012) (00010) DUMBC 00064b 00026 00049b (00023) (00028) (00024) DUMHHI -00009 -00018 -00011 (00010) (00013) (00011) DUMHHI x DUMBC -00052a -00029b -00045a (00012) (00014) (00012) DUMBC 00035a 00022 00024