the health of the u.s. defense industry “in the eye of a ... · • rockwell defense to boeing...

TRANSCRIPT

Defense-IndustrialInitiatives Group

February 19, 2004 1

The Health of the U.S. Defense Industry“In the Eye of a Perfect Storm”

Pierre A. ChaoSenior Fellow and Director Defense-Industrial Initiatives

National Defense Industrial Association2004 Munitions Executive Summit

Tampa, FL

February 19, 2004

Defense-IndustrialInitiatives Group

February 19, 2004 2

�

Defense-IndustrialInitiatives Group

February 19, 2004 3

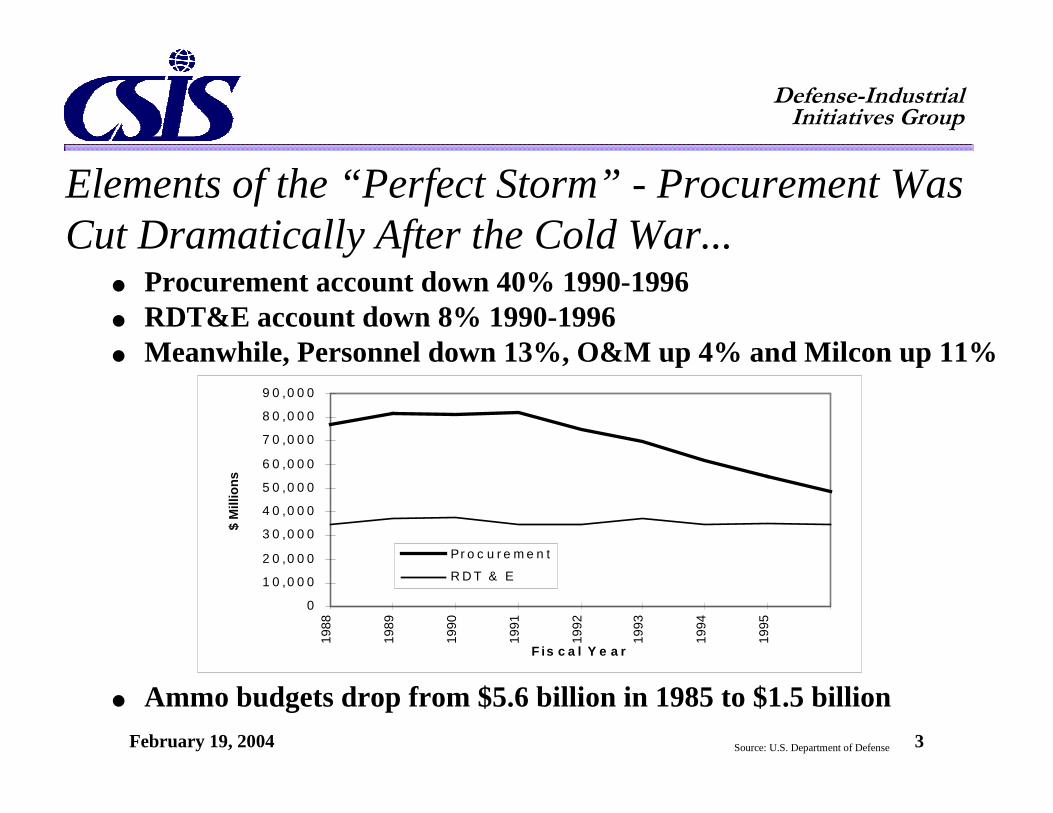

Elements of the “Perfect Storm” - Procurement WasCut Dramatically After the Cold War...

� Procurement account down 40% 1990-1996� RDT&E account down 8% 1990-1996� Meanwhile, Personnel down 13%, O&M up 4% and Milcon up 11%

0

1 0 ,0 0 0

2 0 ,0 0 0

3 0 ,0 0 0

4 0 ,0 0 0

5 0 ,0 0 0

6 0 ,0 0 0

7 0 ,0 0 0

8 0 ,0 0 0

9 0 ,0 0 0

1988

1989

1990

1991

1992

1993

1994

1995

F is c a l Y e a r

$ M

illio

ns

Pr o c u r e m e n t

R D T & E

Source: U.S. Department of Defense

� Ammo budgets drop from $5.6 billion in 1985 to $1.5 billion

Defense-IndustrialInitiatives Group

February 19, 2004 4

Elements of the “Perfect Storm” –Changes in Business Philosophy

� 1980s/1990s saw� Attacks on the multi-industrial firm/conglomerate

� 1980s hostile takeovers/leverage buyouts – break up the conglomerate

� Be number one/number two or get out

� Stick to your knitting

� More sophisticated and active investors� Diversification undertaken at investor portfolio level rather than

corporate

Defense-IndustrialInitiatives Group

February 19, 2004 5

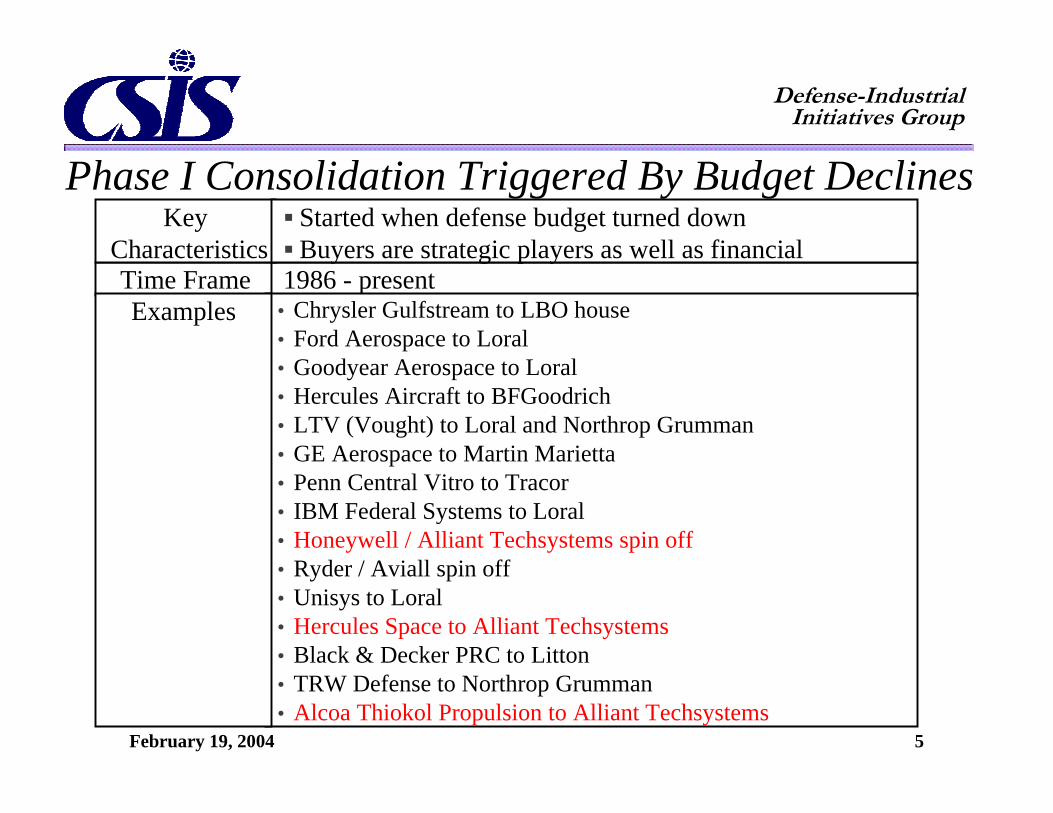

Phase I Consolidation Triggered By Budget Declines

Time Frame 1986 - present• Chrysler Gulfstream to LBO house• Ford Aerospace to Loral• Goodyear Aerospace to Loral• Hercules Aircraft to BFGoodrich• LTV (Vought) to Loral and Northrop Grumman• GE Aerospace to Martin Marietta• Penn Central Vitro to Tracor• IBM Federal Systems to Loral• Honeywell / Alliant Techsystems spin off• Ryder / Aviall spin off• Unisys to Loral• Hercules Space to Alliant Techsystems• Black & Decker PRC to Litton• TRW Defense to Northrop Grumman• Alcoa Thiokol Propulsion to Alliant Techsystems

KeyCharacteristics

� Started when defense budget turned down� Buyers are strategic players as well as financial

Examples

Defense-IndustrialInitiatives Group

February 19, 2004 6

Elements of the “Perfect Storm” –There Was a New Environment After the Cold War

� Weapon systems more complex and expensive to developExample: F-22 fighter development costs 2.5 times F-16

� Fewer programs are launchedExample: Fighters introduced in 1940s: 17 in 1980s: 2

in 1950s: 9 in 1990s: 2 in 1960s: 9 in 2000s: 1

in 1970s: 6

� Programs take longer to go from development to production, more"stretch outs"

� Higher technical, political and service-specific risk

� RESULT: Need to reduce industry capacity and create larger companieswith "deep pockets“ and a breadth of capabilities/programs

Defense-IndustrialInitiatives Group

February 19, 2004 7

Elements of the “Perfect Storm” –Pentagon Established Consolidation Rules

� Secretary of Defense Perry hosts "Last Supper" and announcesthat the Pentagon cannot afford to keep everyone in business

� Industry told it must consolidate, but Pentagon says it will notdecide who or how (directly...still has influence throughprogram decisions)

� Pentagon establishes a merger review process (focuses onconcentration within industry segments, access to technologiesand ability of companies to survive)

� Pentagon agrees to reimburse merger-related restructuringcosts in exchange for cost savings and lower prices

Defense-IndustrialInitiatives Group

February 19, 2004 8

Phase II Consolidation FollowedSector Consolidation/

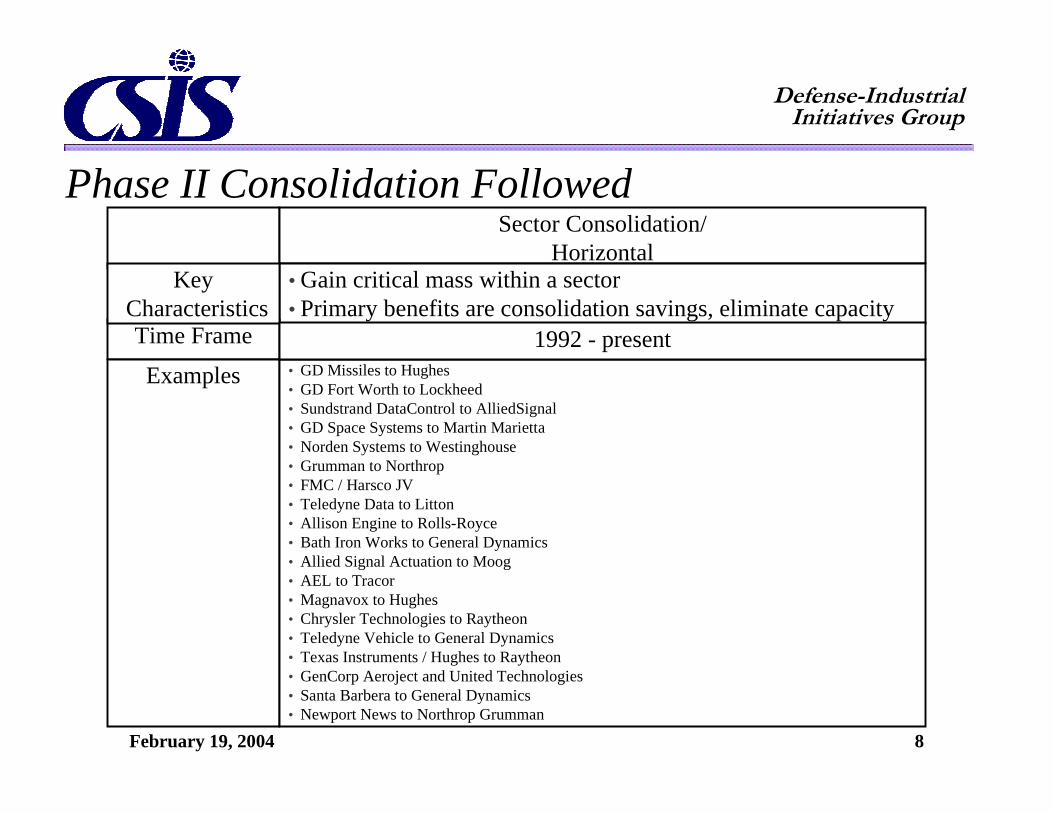

Horizontal• Gain critical mass within a sector• Primary benefits are consolidation savings, eliminate capacity

Time Frame

Examples • GD Missiles to Hughes• GD Fort Worth to Lockheed• Sundstrand DataControl to AlliedSignal• GD Space Systems to Martin Marietta• Norden Systems to Westinghouse• Grumman to Northrop• FMC / Harsco JV• Teledyne Data to Litton• Allison Engine to Rolls-Royce• Bath Iron Works to General Dynamics• Allied Signal Actuation to Moog• AEL to Tracor• Magnavox to Hughes• Chrysler Technologies to Raytheon• Teledyne Vehicle to General Dynamics• Texas Instruments / Hughes to Raytheon• GenCorp Aeroject and United Technologies• Santa Barbera to General Dynamics• Newport News to Northrop Grumman

KeyCharacteristics

1992 - present

Defense-IndustrialInitiatives Group

February 19, 2004 9

Elements of the “Perfect Storm” –Key Issues Related to Vertical Integration

� Mass becomes even more critical to the industry as budgets continue dropping

� Technologies shifting - electronics becoming the value-added component� Example - first generation/unguided missiles the key was speed and

propulsion, key players were chemical/motor players; now the key is thesensor and guidance, key players are electronics houses

� Who should be prime? - metal bender or electronics house

� Players vertically integrate to understand the technology or satisfy markettrend

� Electronics related budgets have suffered the least

� Sources of technical innovation

Defense-IndustrialInitiatives Group

February 19, 2004 10

Phase III Consolidation Followed"Broadening"/

Vertical Consolidation• Broaden business base and increase industry critical mass• Add complementary businesses• Reduce overhead, R&D, cross sell products

Time Frame

Examples • E-Systems to Raytheon• Lockheed with Martin• Loral to Lockheed Martin• Rockwell Defense to Boeing• Westinghouse Defense to Northrop Grumman• McDonnell Douglas to Boeing• Logicon to Northrop Grumman• Northrop Grumman to Lockheed Martin (failed)• GEC Marconi to British Aerospace• Federal Data to Northrop Grumman• Motorola Fuze by Alliant Techsystems

KeyCharacteristics

1995 - present

Defense-IndustrialInitiatives Group

February 19, 2004 11

�

�

Defense-IndustrialInitiatives Group

February 19, 2004 12

A Decade of Consolidation...

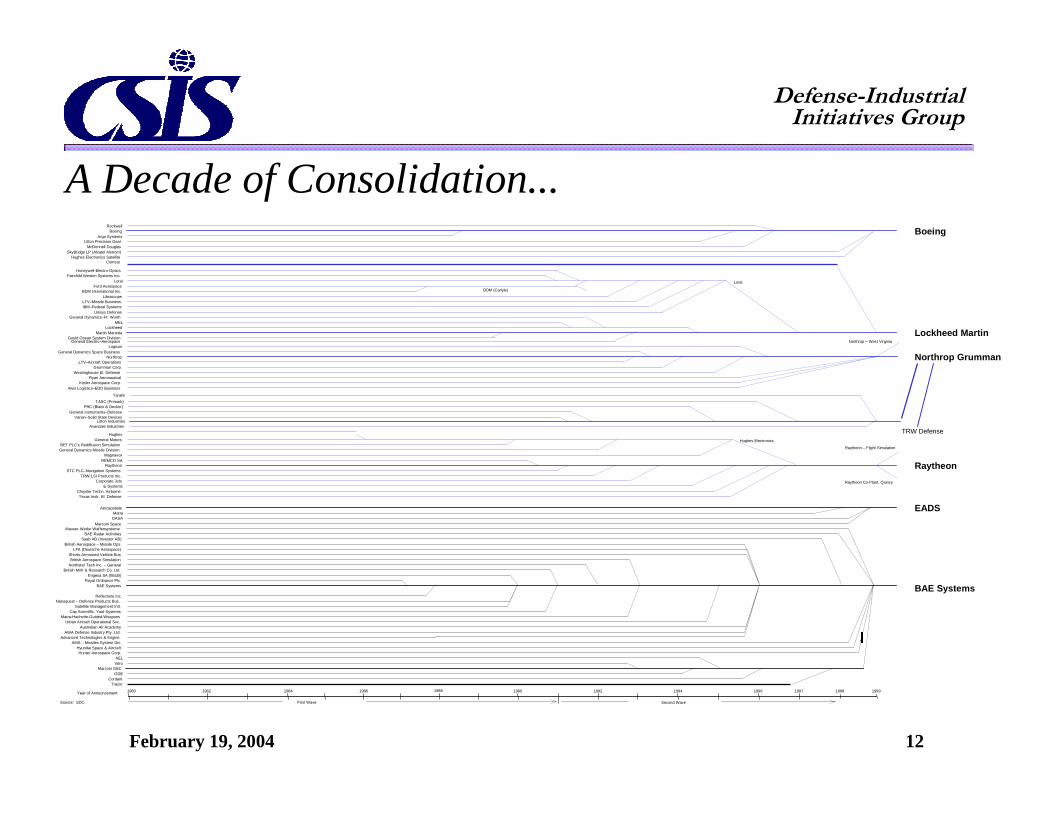

Source: SDC.

Year of Announcement 199019881980 1982 1984 1986 1992 1994 1996 1997 1998 1999

First Wave Second Wave

BAE Systems

EADSMatra

LFK (Deutsche Aerospace)

Royal Ordnance Plc.

Matra-Hachette-Guided-Weapons

Australian Air Academy

AELVitro

GDECordant

Tracor

BAE Systems

Engesa SA (Brazil)

Northstar Tech Inc. – General

Saab AB (Investor AB)

Urban Aircraft Operational Svc.

British Mnfr & Research Co. Ltd.

Cap Scientific, Yard Systems

British Aerospace Simulation

Reflectone Inc.Nanoquest – Defense Products Bus.

Satellite Management Intl.

Mauser-Werke WaffensystemeBAE-Radar Activities

British Aerospace – Missile Ops

Shorts-Armoured Vehicle Bus

AWA Defense Industry Pty. Ltd.Advanced Technologies & Engine

AMS – Missiles System Div.Hyundai Space & AircraftHunter Aerospace Corp.

Marconi GEC

Aerospatiale

DASAMarconi Space

Hughes Electronics

Loral

BDM (Carlyle)

Northrop Grumman

Lockheed Martin

Raytheon

Fairchild Weston Systems Inc.Loral

Honeywell-Electro-Optics

Ford AerospaceBDM International Inc.

Librascope

IBM–Federal SystemsUnisys Defense

General Dynamics–Ft. WorthMEL

Lockheed

General Electric–Aerospace

General Dynamics Space Business

LTV–Aircraft OperationsGrumman Corp.

Ryan AeronauticalKistler Aerospace Corp.

Alvis Logistics–EDD Business

HughesGeneral Motors

BET PLC's Rediffusion Simulation

MagnavoxREMCO SA

STC PLC–Navigation SystemsTRW-LSI Products Inc.

Corporate JetsE-Systems

Chrysler Techn. AirborneTexas Instr. El. Defense

Martin Marietta

Northrop

Raytheon

Northrop – West Virginia

Raytheon – Flight Simulation

Raytheon Co-Plant, Quincy

LTV–Missile Business

General Dynamics Missile Division

BoeingRockwell

Argo SystemsLitton Precision Gear

SkyBridge LP (Alcatel Alstrom)Hughes Electronics Satellite

Boeing

McDonnell Douglas

TASC (Primark)PRC (Black & Decker)

General Instruments–DefenseVarian–Solid State Devices

Taratin

Litton IndustriesAvandale Industries

Gould Ocean System Division

Logicon

Westinghouse El. Defense

Comsat

TRW Defense

Defense-IndustrialInitiatives Group

February 19, 2004 13

Has Resulted in A Three-Tiered U.S. Defense Industry..

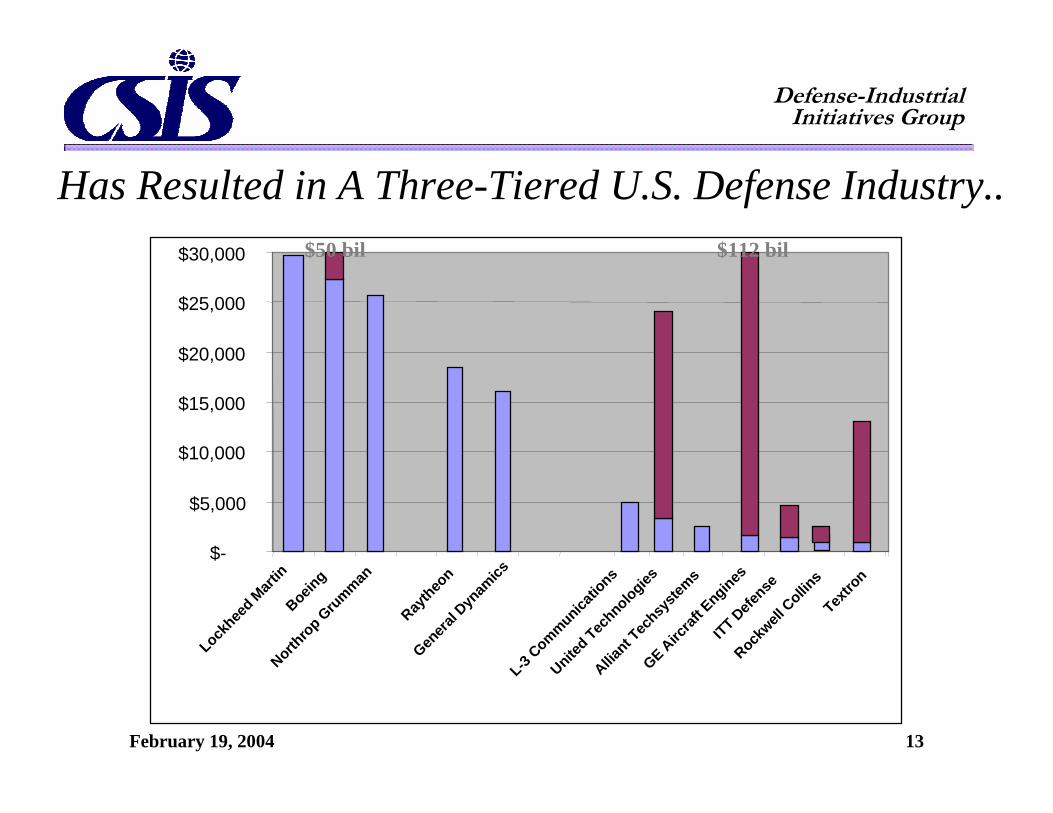

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Lock

heed M

artin

Boein

g

Ray

theon

North

rop Grumman

G

enera

l Dyn

amics

Unite

d Technologies

L-3

Communicatio

ns

GE Airc

raft E

ngines

IT

T Defense

Allia

nt Tec

hsyste

ms

Tex

tron

$50 bil $112 bil

Rock

well Collin

s

Defense-IndustrialInitiatives Group

February 19, 2004 14

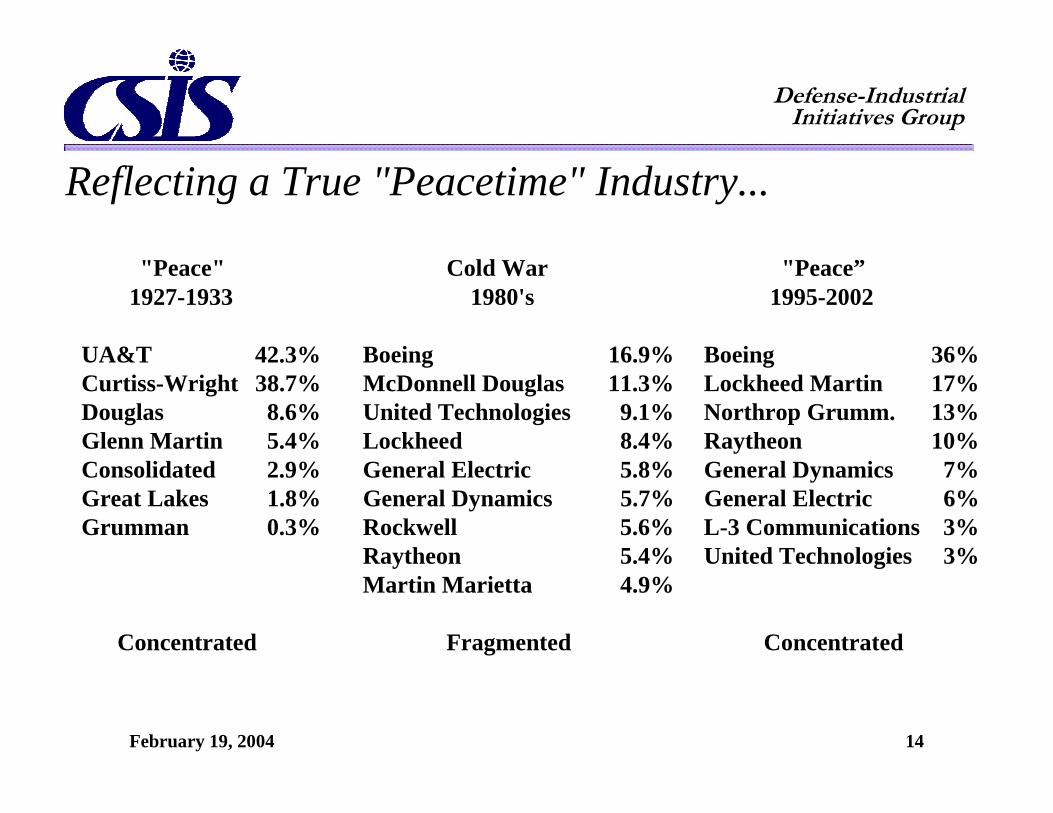

Reflecting a True "Peacetime" Industry...

"Peace" Cold War "Peace” 1927-1933 1980's 1995-2002

UA&T 42.3% Boeing 16.9% Boeing 36%Curtiss-Wright 38.7% McDonnell Douglas 11.3% Lockheed Martin 17%Douglas 8.6% United Technologies 9.1% Northrop Grumm. 13%Glenn Martin 5.4% Lockheed 8.4% Raytheon 10%Consolidated 2.9% General Electric 5.8% General Dynamics 7%Great Lakes 1.8% General Dynamics 5.7% General Electric 6%Grumman 0.3% Rockwell 5.6% L-3 Communications 3%

Raytheon 5.4% United Technologies 3%Martin Marietta 4.9%

Concentrated Fragmented Concentrated

Defense-IndustrialInitiatives Group

February 19, 2004 15

Top 20 Defense Contractors 1980 2002General Dynamics Lockheed MartinMcDonnell Douglas BoeingUnited Technology Northrop GrummanBoeing RaytheonGeneral Electric General DynamicsLockheed United TechnologiesHughes SAICRaytheon TRWTenneco HealthnetGrumman L-3 CommunicationsNorthrop General ElectricMotor Oil Hellas United DefenseChrysler DyncorpRockwell HumanaWestinghouse HoneywellSperry BAE SystemsFMC BechtelMartin Marietta ITTHoneywell TextronLitton Triwest

Source: Department of Defense

Pure DefenseAero/DefenseMultiPure Commercial

Defense-Industrial Ghetto?

Defense-IndustrialInitiatives Group

February 19, 2004 16

(Preliminary Analysis)

Defense Margins Have Improved, BUT…Industry Average Operating Margin (weighted by revenue)

0%

2%

4%

6%

8%

10%

12%20

02

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

1986

1985

1984

1983

1982

1981

1980

CSIS DefenseIndex

Sources: FactSet, S&P Compustat, EnergyInformation Administration, CSIS Analysis

Notes: 1) CSIS Defense Index comprises 36 publicly-traded companies with majority revenues derivedfrom US defense business.(2) S&P Sub-sector constituents accurate back to 1994; composition held constant for years 1980 to1993.

Defense-IndustrialInitiatives Group

February 19, 2004 17

� What are the alternative investments when you consider thedefense sector?

Source: CSFB survey

Entire Market

Transportation

Technology

Commercial Aero

Capital goods/Industrial

Defense Industry Does Not Operate in a Vacuum

Defense-IndustrialInitiatives Group

February 19, 2004 18

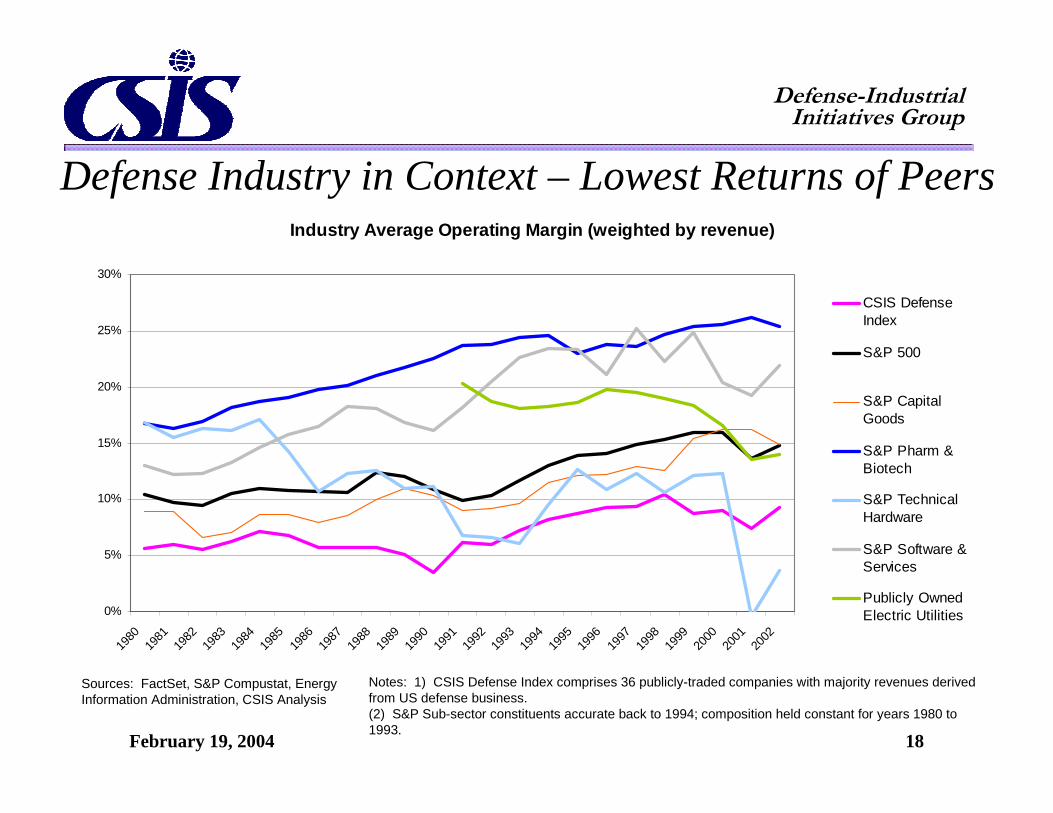

Industry Average Operating Margin (weighted by revenue)

0%

5%

10%

15%

20%

25%

30%20

02

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

1986

1985

1984

1983

1982

1981

1980

CSIS DefenseIndex

S&P 500

S&P CapitalGoods

S&P Pharm &Biotech

S&P TechnicalHardware

S&P Software &Services

Publicly OwnedElectric Utilities

Defense Industry in Context – Lowest Returns of Peers

Sources: FactSet, S&P Compustat, EnergyInformation Administration, CSIS Analysis

Notes: 1) CSIS Defense Index comprises 36 publicly-traded companies with majority revenues derivedfrom US defense business.(2) S&P Sub-sector constituents accurate back to 1994; composition held constant for years 1980 to1993.

Defense-IndustrialInitiatives Group

February 19, 2004 19

Investors Prized the Industry for its Stability� What is more important to you: top-line growth or consistency of

earnings?

Growth

ConsistencySource: MSDW survey

2002

1999

“Predictability of source andlevel of earnings, as opposed tosmoothness”

Growth

Consistency

Defense-IndustrialInitiatives Group

February 19, 2004 20

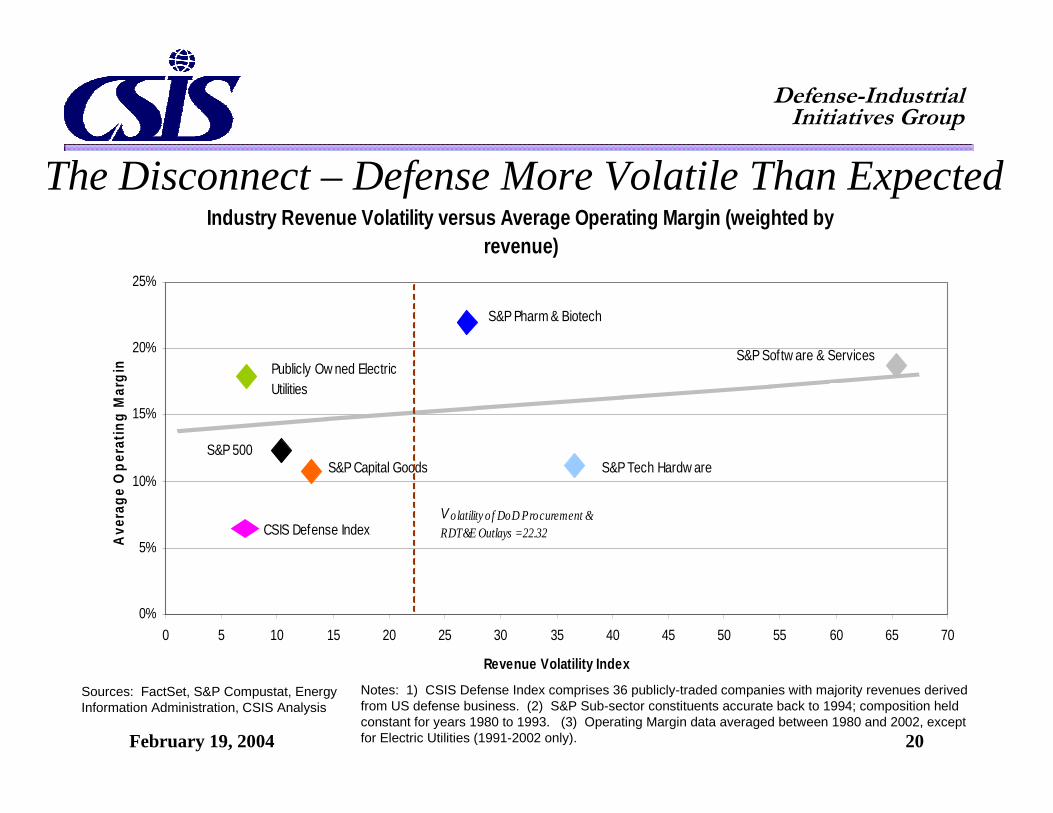

The Disconnect – Defense More Volatile Than ExpectedIndustry Revenue Volatility versus Average Operating Margin (weighted by

revenue)

R2 = 0.0888

0%

5%

10%

15%

20%

25%

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70

Revenue Volatility Index

Ave

rage

Ope

ratin

g M

argi

n

V olatility of DoD Procurement & RDT&E Outlays = 22.32CSIS Defense Index

S&P 500S&P Capital Goods

S&P Pharm & Biotech

S&P Softw are & Services

S&P Tech Hardw are

Publicly Ow ned Electric Utilities

Notes: 1) CSIS Defense Index comprises 36 publicly-traded companies with majority revenues derivedfrom US defense business. (2) S&P Sub-sector constituents accurate back to 1994; composition heldconstant for years 1980 to 1993. (3) Operating Margin data averaged between 1980 and 2002, exceptfor Electric Utilities (1991-2002 only).

Sources: FactSet, S&P Compustat, EnergyInformation Administration, CSIS Analysis

Defense-IndustrialInitiatives Group

February 19, 2004 21

Key Questions on Future Industry Structure...

LSI

Pure Outsourcing Vertical “Light”

Global Player

Systems / Component

Vertical Integrator

How does DoD manage?

Defense-IndustrialInitiatives Group

February 19, 2004 22

Key Questions on Future Industry Structure...

� Defense vs. National Security

� Is Homeland Security real?

� Who will respond?

� Civil-Military Integration

� Transformation

� What does it mean?

� Who will be the true leaders? Traditional players or new comers

Defense-IndustrialInitiatives Group

February 19, 2004 23

�

�

Defense-IndustrialInitiatives Group

February 19, 2004 24

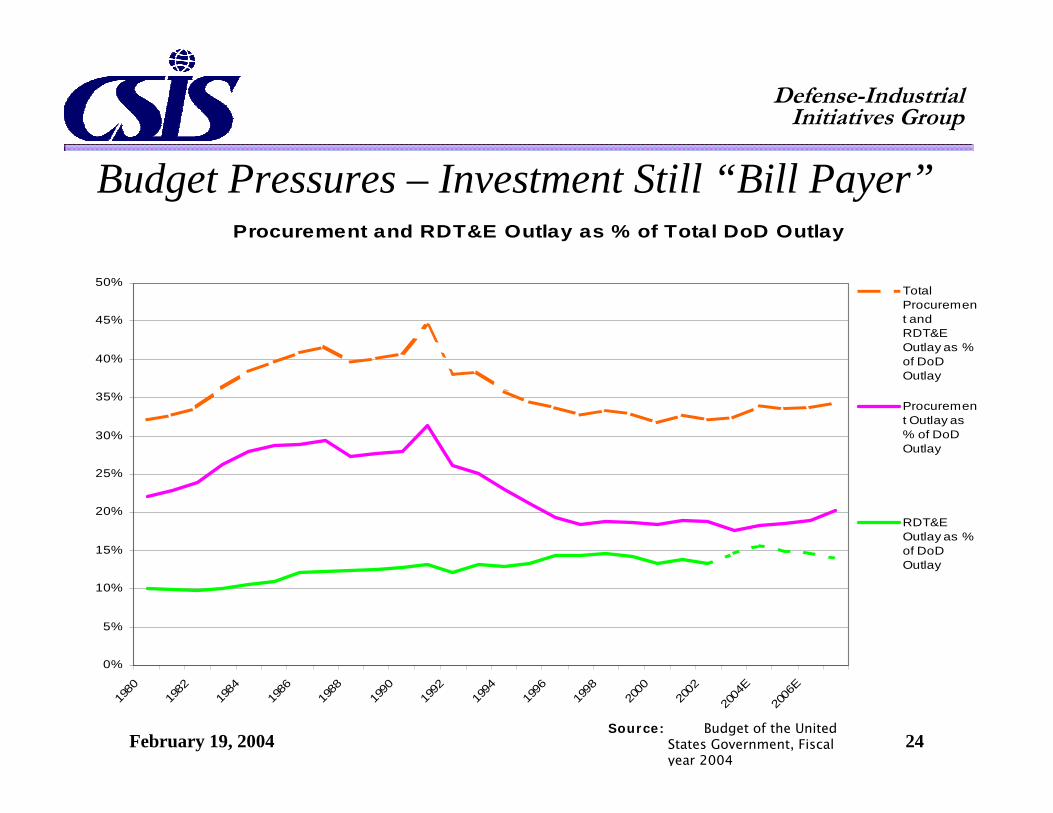

Procurement and RDT&E Outlay as % of Total DoD Outlay

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

E

2006

E

TotalProcurement andRDT&EOutlay as %of DoDOutlay

Procurement Outlay as% of DoDOutlay

RDT&EOutlay as %of DoDOutlay

Source: Budget of the UnitedStates Government, Fiscalyear 2004

Budget Pressures – Investment Still “Bill Payer”

Defense-IndustrialInitiatives Group

February 19, 2004 25

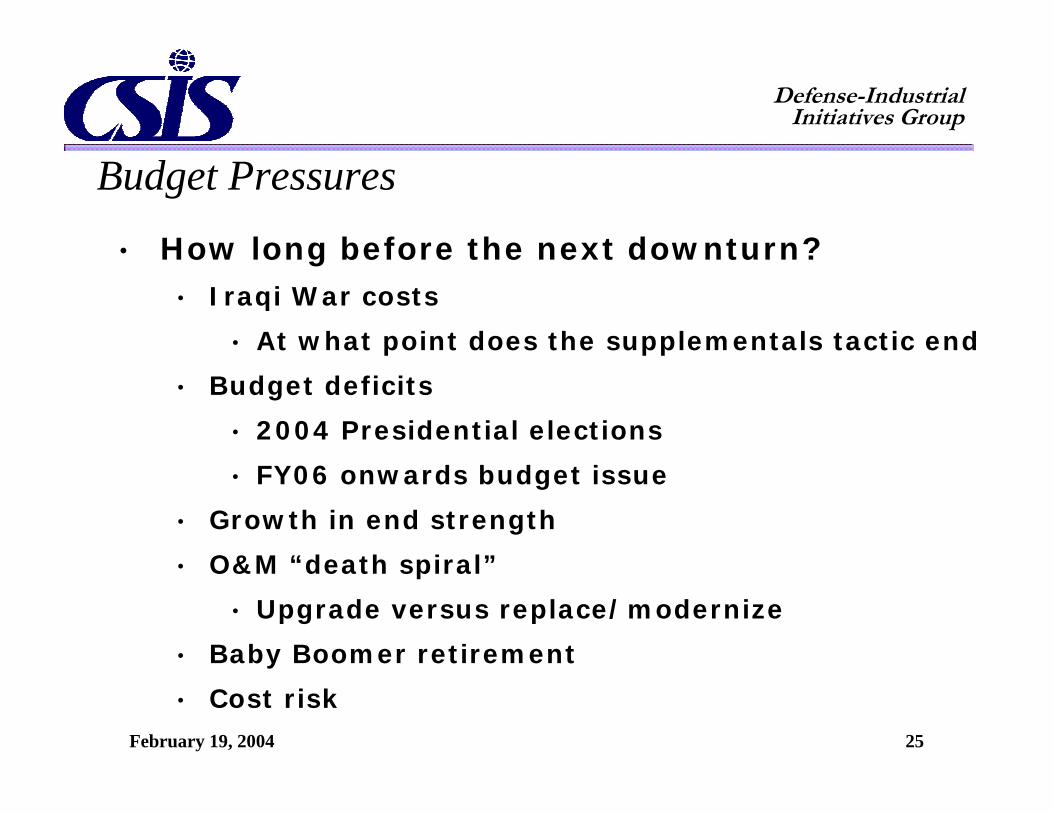

• How long before the next downturn?• Iraqi War costs

• At what point does the supplementals tactic end

• Budget deficits

• 2004 Presidential elections

• FY06 onwards budget issue

• Growth in end strength

• O&M “death spiral”

• Upgrade versus replace/modernize

• Baby Boomer retirement

• Cost risk

Budget Pressures

Defense-IndustrialInitiatives Group

February 19, 2004 26

Defense = Alliant Techsystems, General Dynamics, Grumman, Litton, Lockheed Martin, Martin Marietta, Northop, Northrop Grumman, Newport News

Defense Electronics = E-Systems, L-3 Communications, Logicon, Loral, Raytheon, Tracor Source: Factset, CSFB Analysis, CSIS Analysis

0

100

200

300

400

500

600

700

800

900

12/3

1/90

10/2

5/91

5/19

/92

12/0

9/92

7 /02

/93

1/24

/94

8/17

/ 94

3/10

/ 95

10/0

2/95

4/24

/96

11/1

3/96

6/09

/97

1 2/3

0/9 7

7/24

/98

2/17

/99

9/09

/99

3/31

/00

1 0/2

3/00

5/17

/01

12/1

3/01

7/10

/ 02

1/31

/03

8/25

/03

DefenseDefense Electronics

S&P500

Stock Market Already Factoring in a Decline

Defense-IndustrialInitiatives Group

February 19, 2004 27

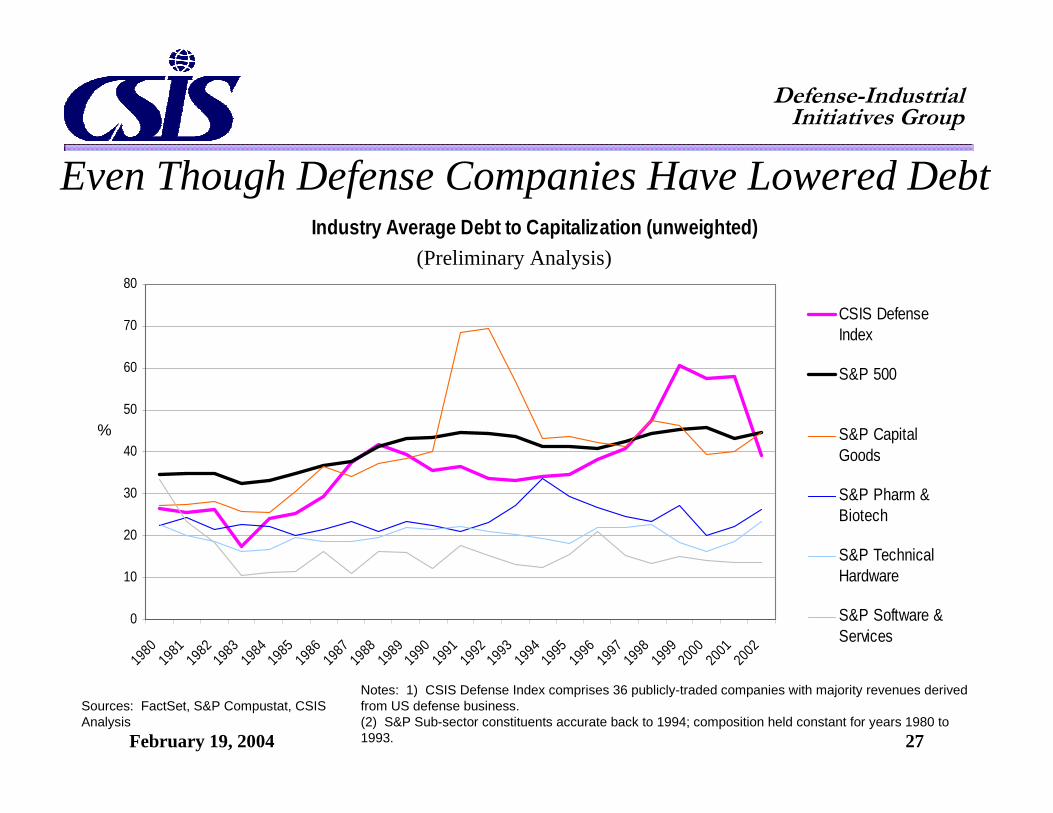

(Preliminary Analysis)

Even Though Defense Companies Have Lowered DebtIndustry Average Debt to Capitalization (unweighted)

0

10

20

30

40

50

60

70

80

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

1987

1986

1985

1984

1983

1982

1981

1980

CSIS DefenseIndex

S&P 500

S&P CapitalGoods

S&P Pharm &Biotech

S&P TechnicalHardware

S&P Software &Services

Sources: FactSet, S&P Compustat, CSISAnalysis

Notes: 1) CSIS Defense Index comprises 36 publicly-traded companies with majority revenues derivedfrom US defense business.(2) S&P Sub-sector constituents accurate back to 1994; composition held constant for years 1980 to1993.

%

Defense-IndustrialInitiatives Group

February 19, 2004 28

(Preliminary Analysis)

Bond Markets Still Rate Industry Near “Junk”Average Debt Ratings (unweighted)

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

13.00

14.00

15.00

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

CSIS DefenseIndex

S&P 500

S&P CapitalGoods

S&P Pharm &Biotech

S&P TechnicalHardware

S&P Software &Services

AAA

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

Sources: FactSet, S&P Compustat, CSISAnalysis

Notes: 1) CSIS Defense Index comprises 36 publicly-traded companies with majority revenues derivedfrom US defense business.(2) S&P Sub-sector constituents accurate back to 1994; composition held constant for years 1980 to1993.

Defense-IndustrialInitiatives Group

February 19, 2004 29

�

Defense-IndustrialInitiatives Group

February 19, 2004 30

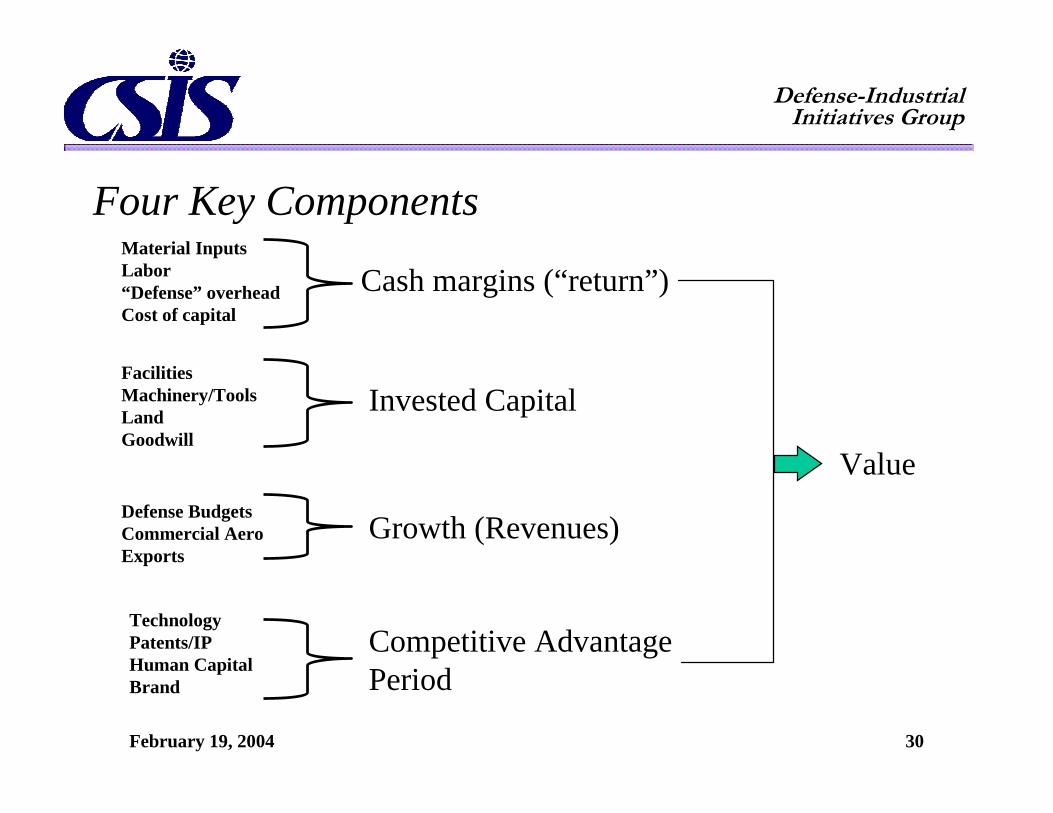

Four Key Components

Cash margins (“return”)

Invested Capital

Growth (Revenues)

Competitive AdvantagePeriod

TechnologyPatents/IPHuman CapitalBrand

ValueDefense BudgetsCommercial AeroExports

FacilitiesMachinery/ToolsLandGoodwill

Material InputsLabor“Defense” overheadCost of capital

Defense-IndustrialInitiatives Group

February 19, 2004 31

� Strategically– Exit non-core, underperforming businesses– Move to higher valued-added, more profitable areas - “System

of systems” (which requires electronics/software expertise)

� Internally– Re-engineering efforts– Cost-reduction plans

� Government policy– Defense Science Board look at industry margin rates and

ability to retain cost savings– Proposed changes to R&D margins, cost saving retentions

Addressing Return/Margins

Defense-IndustrialInitiatives Group

February 19, 2004 32

Addressing Return/Margins - Six SigmaThree of Fortune’s Top Ten Most Admired Corporations Uses Six Sigma

(three of the top four manufacturers)1. Wal Mart 6. Johnson & Johnson2. Southwest 7. Microsoft3. Berkshire Hathaway 8. FedEx4. Dell Computer 9. Starbucks5. General Electric 10. Proctor & Gamble

Eight of Fortune’s Top Ten Most Admired Aerospace/Defense Co’s Uses Six Sigma1. United Technologies 6. General Dynamics2. Lockheed Martin 7. Textron3. Northrop Grumman 8. Rockwell Collins4. Boeing 9. Goodrich5. Honeywell 10. Raytheon

Defense-IndustrialInitiatives Group

February 19, 2004 33

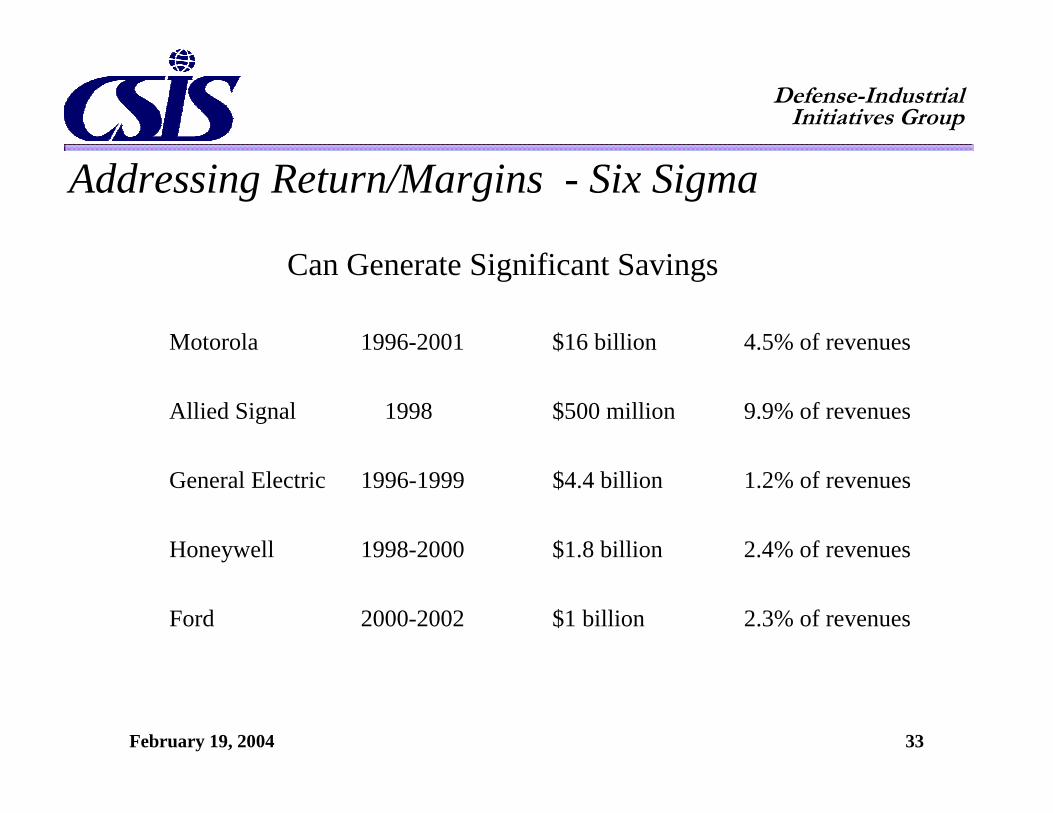

Addressing Return/Margins - Six Sigma

Can Generate Significant Savings

Motorola 1996-2001 $16 billion 4.5% of revenues

Allied Signal 1998 $500 million 9.9% of revenues

General Electric 1996-1999 $4.4 billion 1.2% of revenues

Honeywell 1998-2000 $1.8 billion 2.4% of revenues

Ford 2000-2002 $1 billion 2.3% of revenues

Defense-IndustrialInitiatives Group

February 19, 2004 34

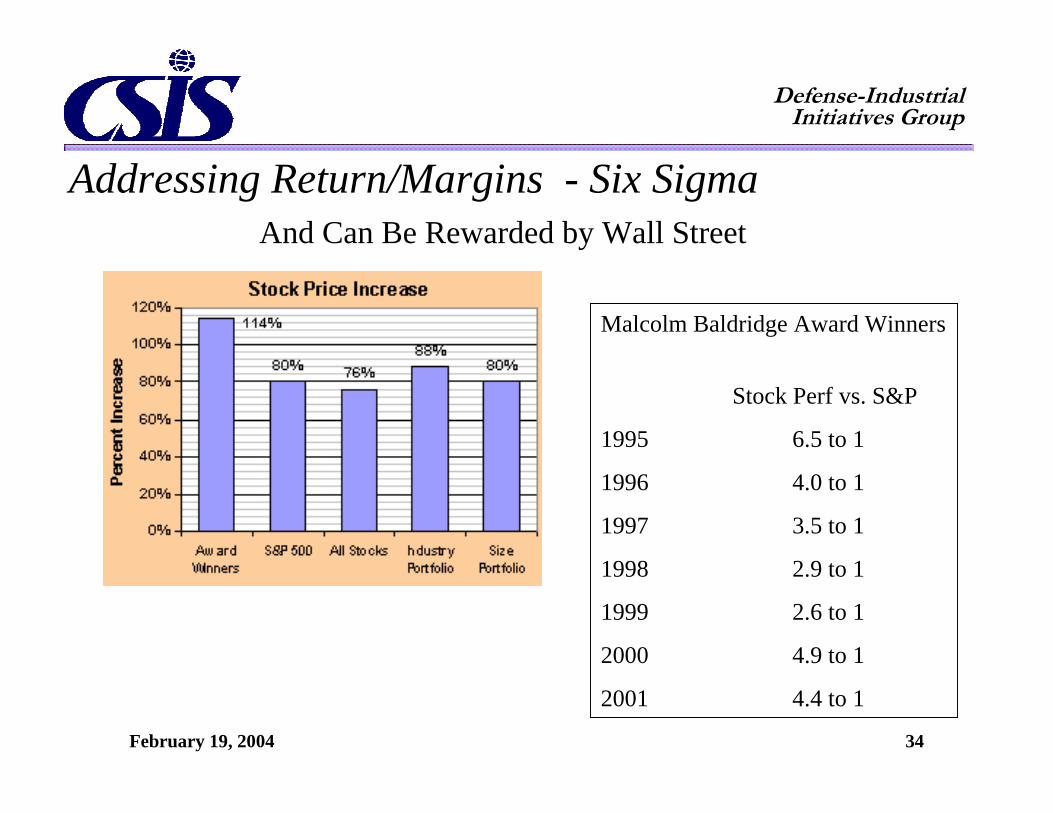

Addressing Return/Margins - Six SigmaAnd Can Be Rewarded by Wall Street

Malcolm Baldridge Award Winners

Stock Perf vs. S&P

1995 6.5 to 1

1996 4.0 to 1

1997 3.5 to 1

1998 2.9 to 1

1999 2.6 to 1

2000 4.9 to 1

2001 4.4 to 1

Defense-IndustrialInitiatives Group

February 19, 2004 35

� Strategically– Continued consolidation of the second and third tiers of the

industry– Longer-term pressure for international consolidation

� Internally– Continue to eliminate excess facilities– Lean manufacturing efforts / recapitalization

� Government policy– Defense Science Board look at progress payments, paid cost

rules– Pentagon changes to paid cost rules, progress payments

Addressing the Invested Capital Problems

Defense-IndustrialInitiatives Group

February 19, 2004 36

� Defense electronics/information systems faster growing part ofthe defense budget– As electronics-related budgets increase– As electronics/info systems become a greater portion of the

weapon system

� “Vertical integration”

� Government policy– Mergers and acquisitions/competition rules

Addressing the Growth Problems

Defense-IndustrialInitiatives Group

February 19, 2004 37

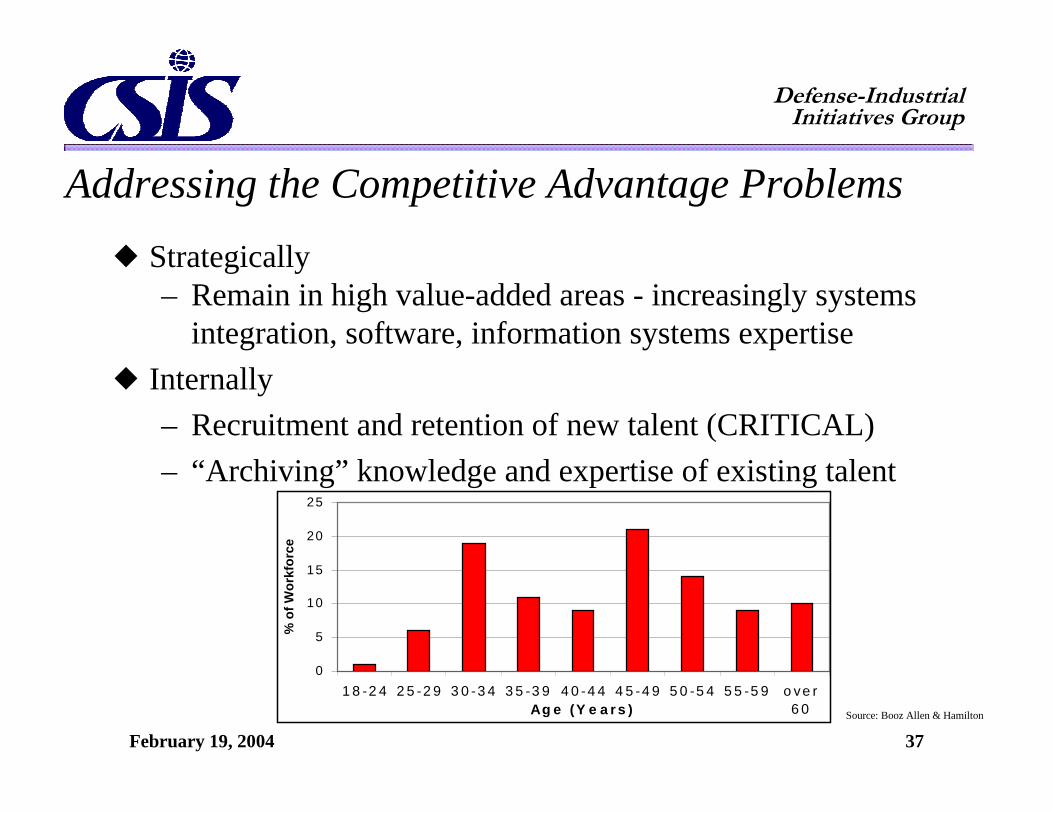

� Strategically– Remain in high value-added areas - increasingly systems

integration, software, information systems expertise� Internally

– Recruitment and retention of new talent (CRITICAL)– “Archiving” knowledge and expertise of existing talent

Addressing the Competitive Advantage Problems

0

5

10

15

20

25

1 8 -2 4 2 5 -2 9 3 0 -3 4 3 5 -3 9 4 0 -4 4 4 5 -4 9 5 0 -5 4 5 5 -5 9 o ve r6 0Ag e (Y e a r s )

% o

f Wor

kfor

ce

Source: Booz Allen & Hamilton