the future of financial reportinggy by government not … · reportinggy by government...

TRANSCRIPT

Webinar SeriesWebinar Series

The Future of Financial Reporting by Government g y

Not-For-Profit Organizations

Moderated by:Moderated by:Tim Beauchamp, Director

Public Sector Accounting BoardPublic Sector Accounting BoardPresented by:Andrew Newman, Partner

KPMGJim Keates, Principal

Public Sector Accounting Board

ObjectiveObjective

• To enhance awareness as to why theTo enhance awareness as to why the Public Sector Accounting (PSA) Handbook and to generate comments on the Publicand to generate comments on the Public Sector Accounting Board’s (PSAB’s) Exposure DraftExposure Draft

• Comments are due July 15, 2010

This webinarThis webinar

• History of the projectHistory of the project• What is being proposed for government

not for profit organizations (GNFPOs) andnot-for-profit organizations (GNFPOs) and whyDiff b t th PSA H db k• Differences between the PSA Handbook and the CICA Handbook

• The long-term objectives for financial reporting by GNFPOs

The NFPO CommunityThe NFPO Community

• Many not-for-profit organizations (NFPOs)Many not for profit organizations (NFPOs) operate independently of governments but with common objectiveswith common objectives

• Some NFPOs may receive funding from governments but without influence overgovernments but without influence over their financial and operating policiesF th NFPO fi i l d ti• For other NFPOs financial and operating policies are directed by a government

What is a Government Organization?What is a Government Organization?

• A government organization is an• A government organization is an organization controlled by the

tgovernment• Indicators of control are provided in p

Section PS 1300• Control is the power to govern the• Control is the power to govern the

financial and operating policies of th i tianother organization

What is a GNFPO?What is a GNFPO?A government organization that has all of the following g g g

characteristics• Has counterparts outside the public sector• Is an entity normally without transferable ownership

interests• Is organized and operated exclusively for social• Is organized and operated exclusively for social,

educational, professional, religious, health, charitable or any other not-for-profit purpose

• Its members, contributors and other resource providers do not receive any financial return from the organization

Accounting Standards Board (AcSB) strategic plan

• In the past PSAB directed NFPOsIn the past, PSAB directed NFPOs controlled by government to use the CICA HandbookHandbook

• The current CICA Handbook will be replaced by:replaced by:– IFRSs

P i t E t i t d d– Private Enterprise standards

Gathering the views of constituentsGathering the views of constituents

• A joint Invitation to Comment (PSAB inA joint Invitation to Comment (PSAB in conjunction with the AcSB) was issued in December 2008December 2008

• More than 20 presentations and roundtables were held to enhanceroundtables were held to enhance awarenessI f 150 i d• In excess of 150 responses were received to the Invitation to Comment

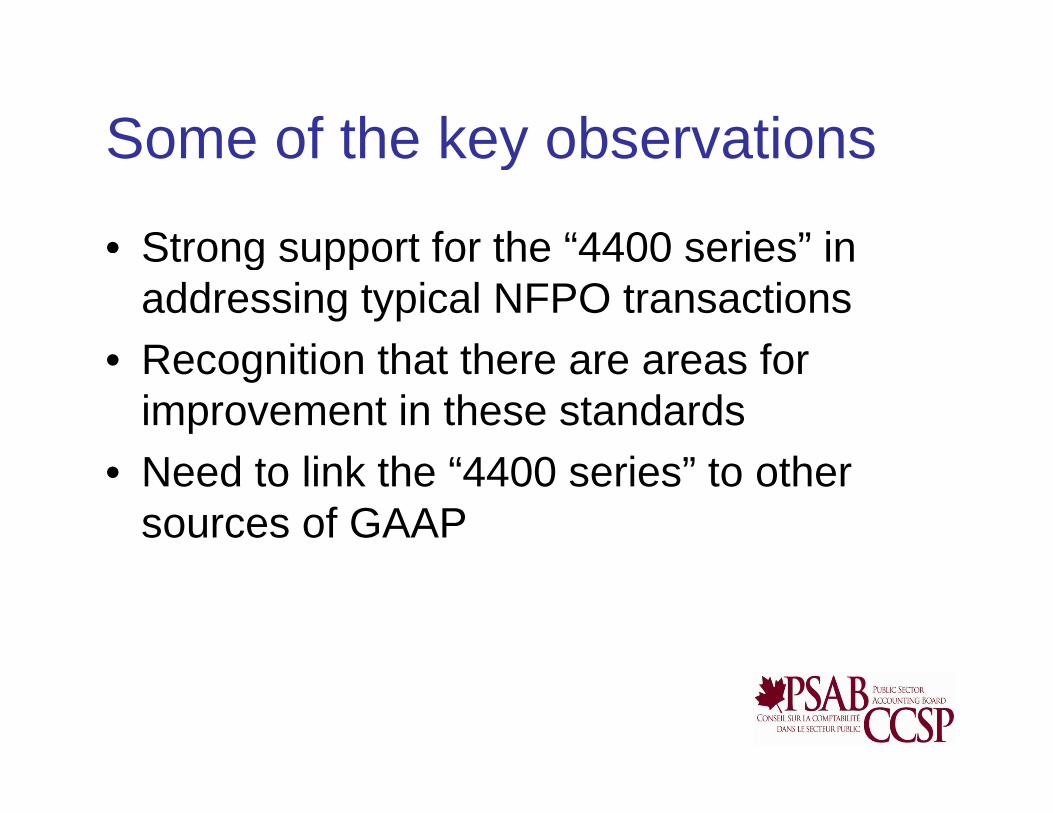

Some of the key observationsSome of the key observations

• Strong support for the “4400 series” inStrong support for the 4400 series in addressing typical NFPO transactions

• Recognition that there are areas for• Recognition that there are areas for improvement in these standardsN d t li k th “4400 i ” t th• Need to link the “4400 series” to other sources of GAAP

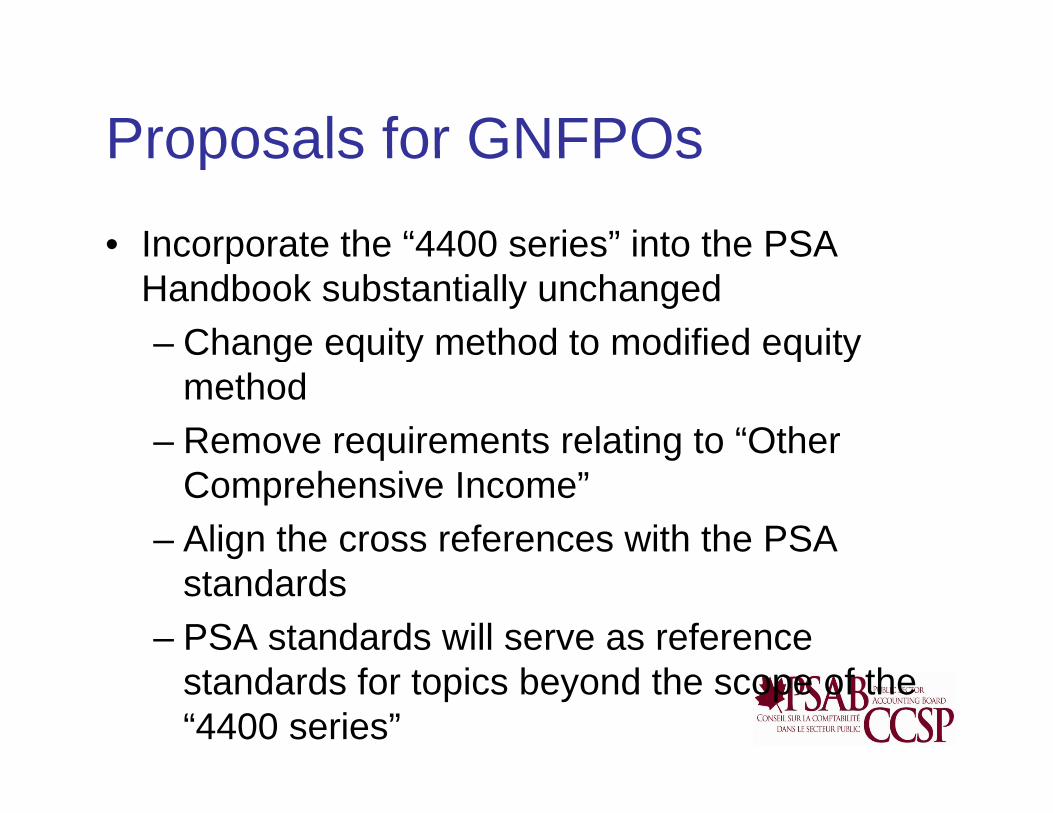

Proposals for GNFPOsProposals for GNFPOs

• Incorporate the “4400 series” into the PSAIncorporate the 4400 series into the PSA Handbook substantially unchanged– Change equity method to modified equity g q y q y

method– Remove requirements relating to “Other q g

Comprehensive Income”– Align the cross references with the PSA

standards– PSA standards will serve as reference

standards for topics beyond the scope of the “4400 series”

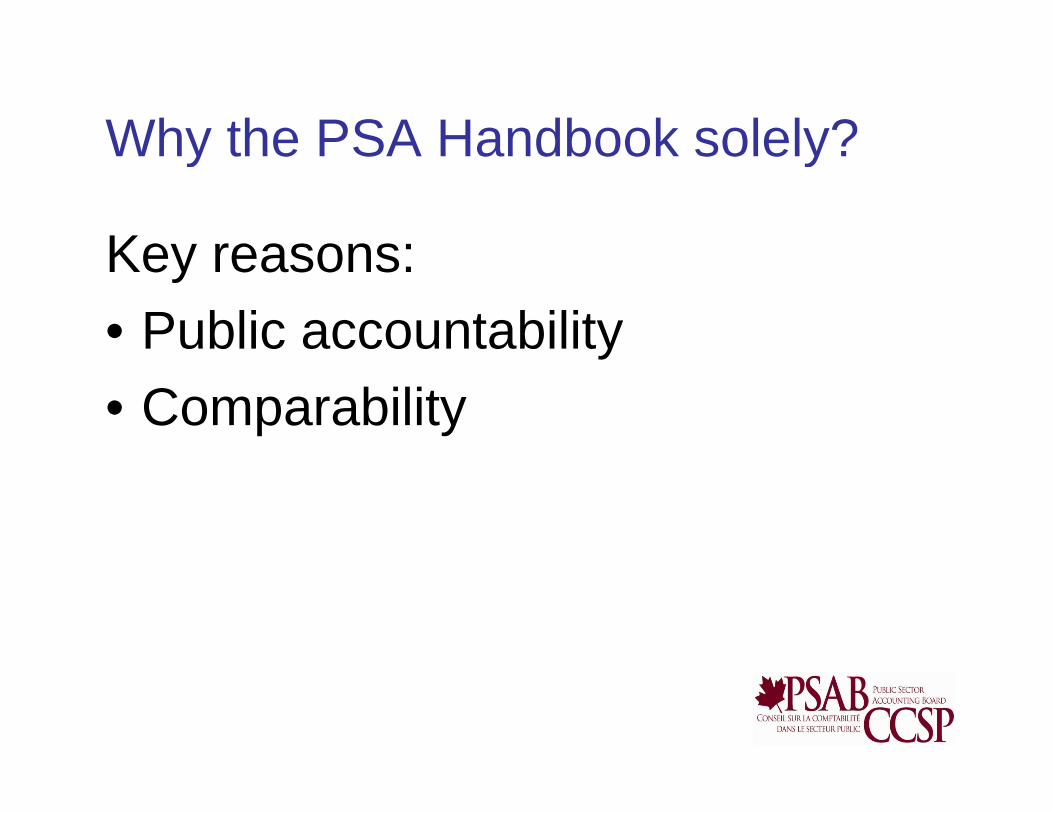

Why the PSA Handbook solely?Why the PSA Handbook solely?

Key reasons:Key reasons:• Public accountabilityy• Comparability

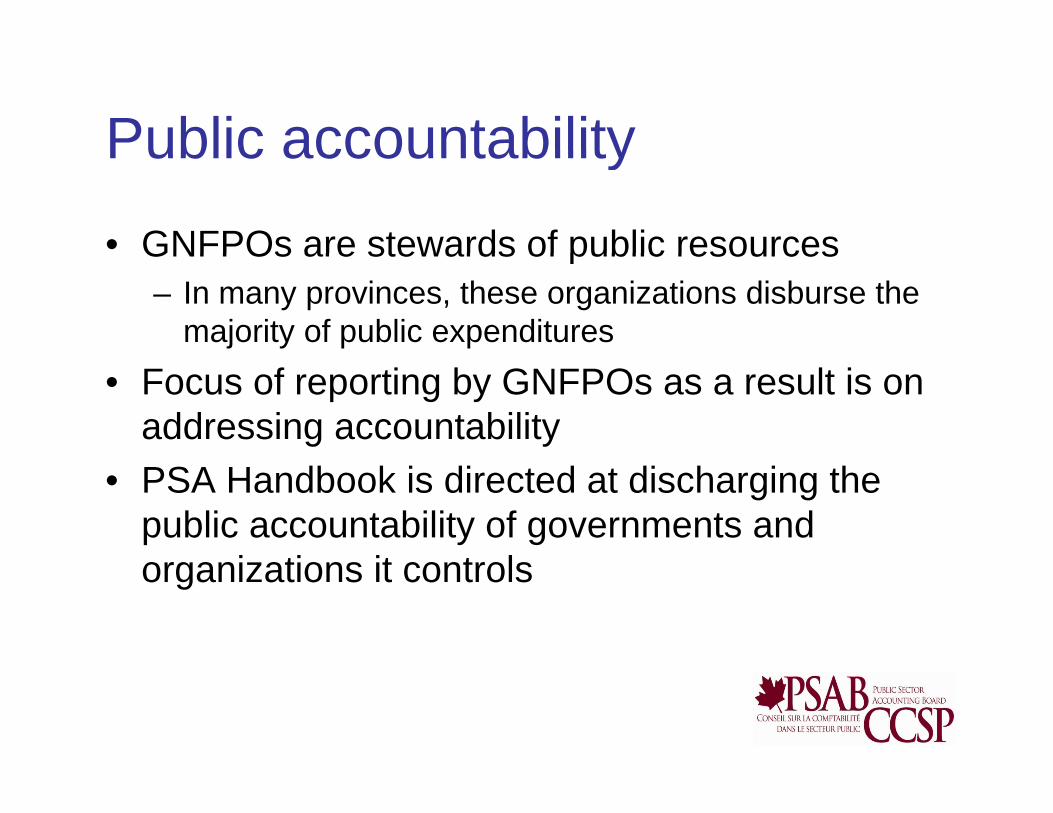

Public accountabilityPublic accountability

• GNFPOs are stewards of public resourcesGNFPOs are stewards of public resources– In many provinces, these organizations disburse the

majority of public expenditures• Focus of reporting by GNFPOs as a result is on

addressing accountability• PSA Handbook is directed at discharging the

public accountability of governments and i ti it t lorganizations it controls

ComparabilityComparability

• In the private sector, NFPOs will be followingIn the private sector, NFPOs will be following IFRSs or their own standards including private enterprise standards where NFPO standards are silent

• Providing options will reduce comparability • Directing all GNFPOs to the PSA Handbook will

enhance comparability with both other i i d h GNFPOgovernment organizations and other GNFPOs

• Enhanced comparability supports resource ll ti d t bilit d i iallocation and accountability decisions

Continue to follow the 4400 SeriesContinue to follow the 4400 Series

• GNFPOs will continue to use the reportingGNFPOs will continue to use the reporting model in the “4400 series”

• GNFPOs will continue to account for• GNFPOs will continue to account for transactions within the scope of the “4400 series” based on that guidance Thisseries based on that guidance. This includes:

R iti f i t ibl– Recognition of intangibles– Controlled and related entities

C i l i i– Capital asset reporting exemption– Recognition of collections

PSA Handbook / CICA Handbook Differences

• A PSA Handbook / CICA Handbook comparison is available at www psabcomparison is available at www.psab-ccsp.ca which highlights some differences between the standardsdifferences between the standards.

PSA Handbook / CICA Handbook Differences

• Financial instruments

• Hedge accounting

PSA Handbook / CICA Handbook Differences

• Long term foreign currency denominated monetary itemsmonetary items

• Pension and employee future benefits

Transition to the PSA HandbookTransition to the PSA Handbook

• Effective for fiscal periods beginning on orEffective for fiscal periods beginning on or after January 1, 2012

• General requirement to adopt PSA• General requirement to adopt PSA Handbook on a retroactive basis although an Exposure Draft proposes certainan Exposure Draft proposes certain exemptions or exceptions on first-time adoption of the PSA Handbook byadoption of the PSA Handbook by government organizations (www.psab-ccsp ca/projects)ccsp.ca/projects)

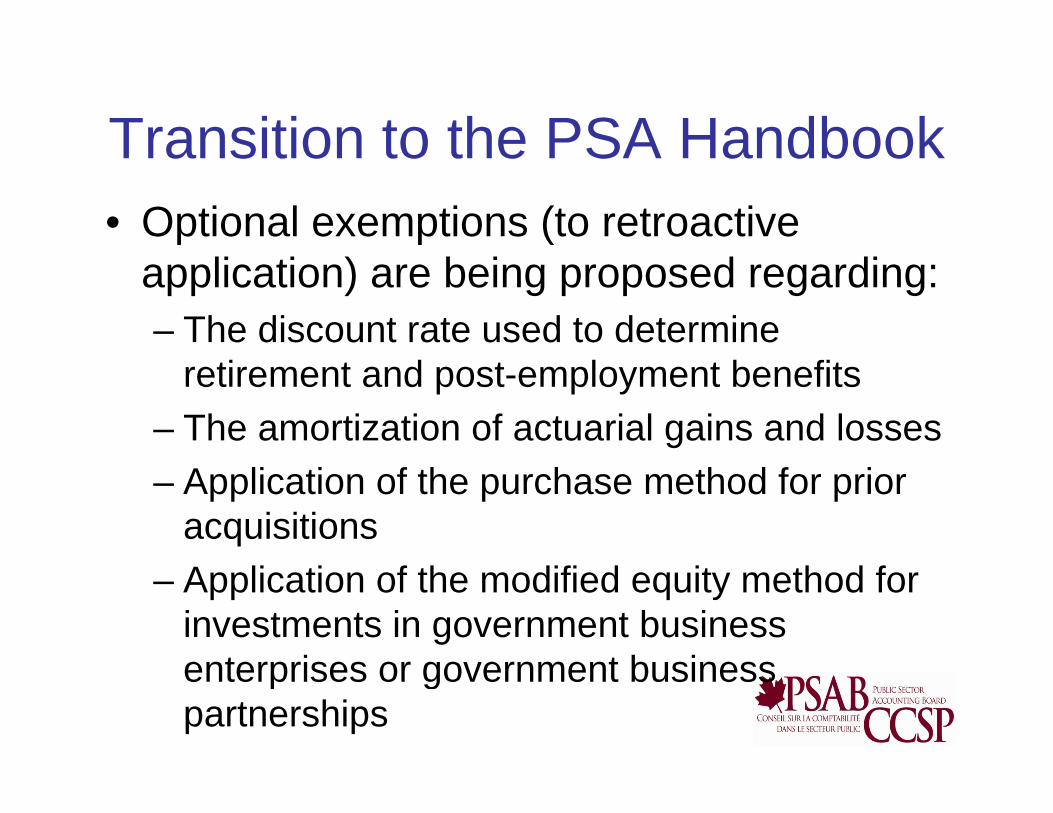

Transition to the PSA HandbookTransition to the PSA Handbook• Optional exemptions (to retroactive

application) are being proposed regarding:– The discount rate used to determine

retirement and post-employment benefits– The amortization of actuarial gains and losses– Application of the purchase method for prior

acquisitions– Application of the modified equity method for

investments in government business enterprises or government businessenterprises or government business partnerships

Transition to the PSA HandbookTransition to the PSA Handbook

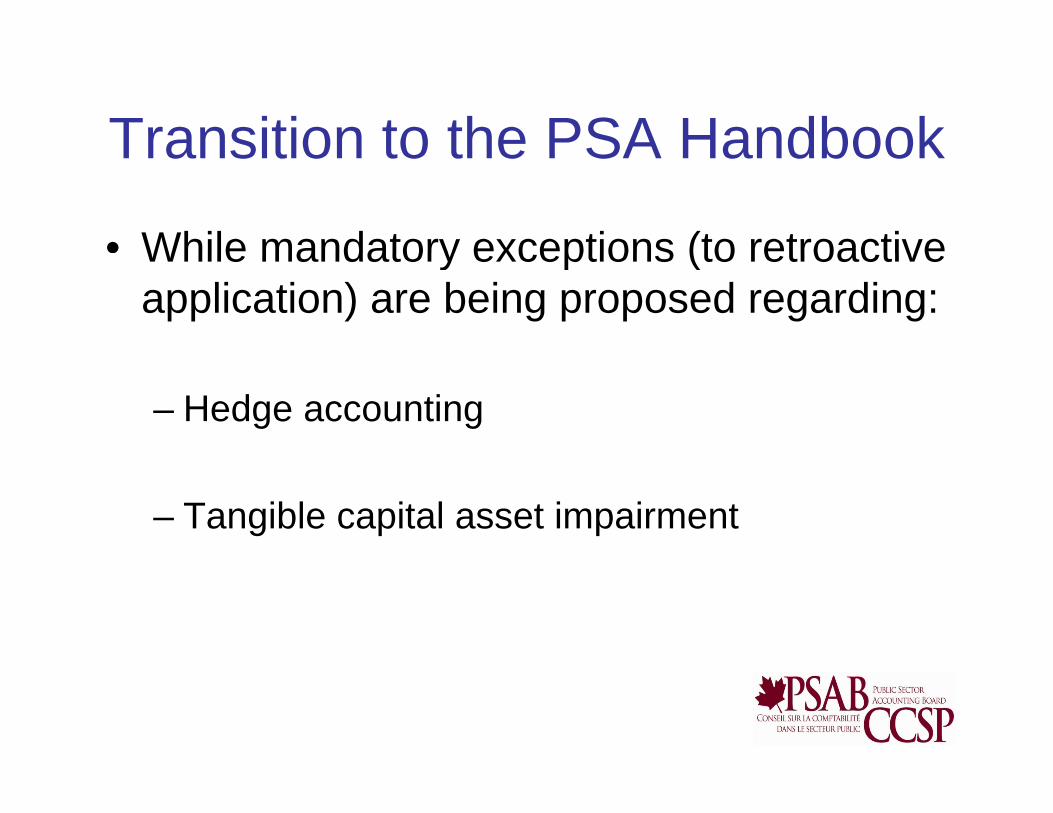

• While mandatory exceptions (to retroactiveWhile mandatory exceptions (to retroactive application) are being proposed regarding:

– Hedge accounting

– Tangible capital asset impairment

Long-term objectivesLong term objectives

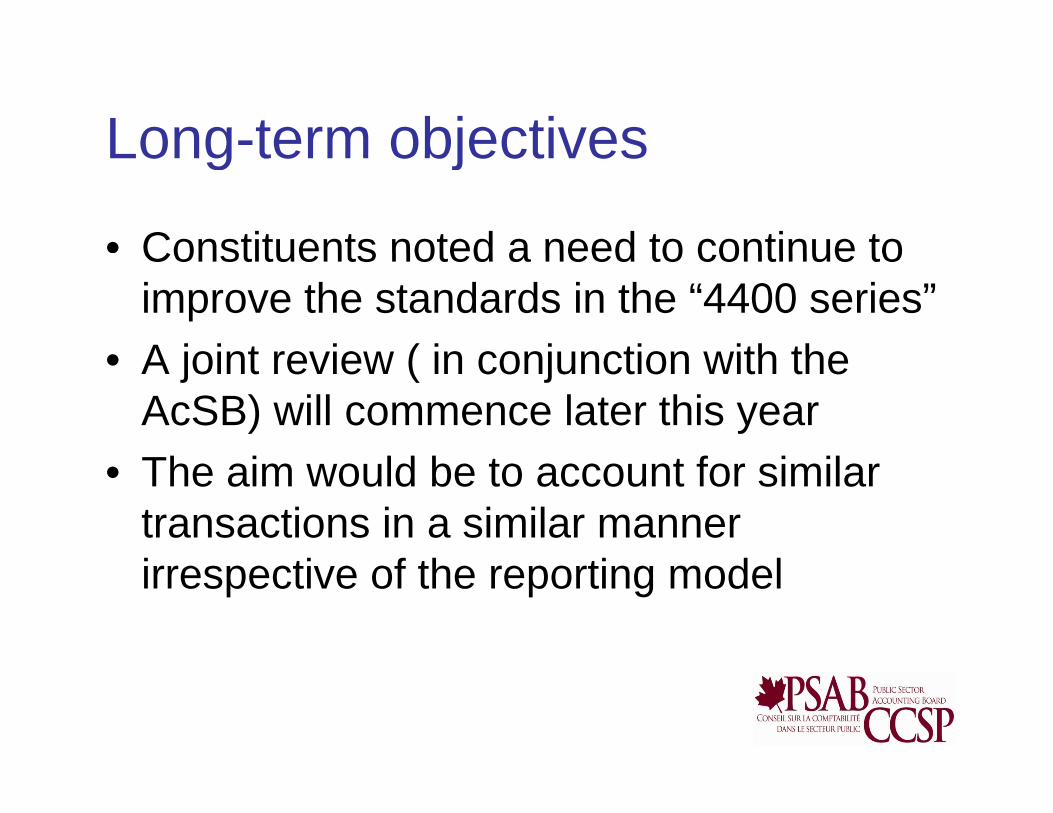

• Constituents noted a need to continue toConstituents noted a need to continue to improve the standards in the “4400 series”

• A joint review ( in conjunction with the• A joint review ( in conjunction with the AcSB) will commence later this yearTh i ld b t t f i il• The aim would be to account for similar transactions in a similar manner i ti f th ti d lirrespective of the reporting model

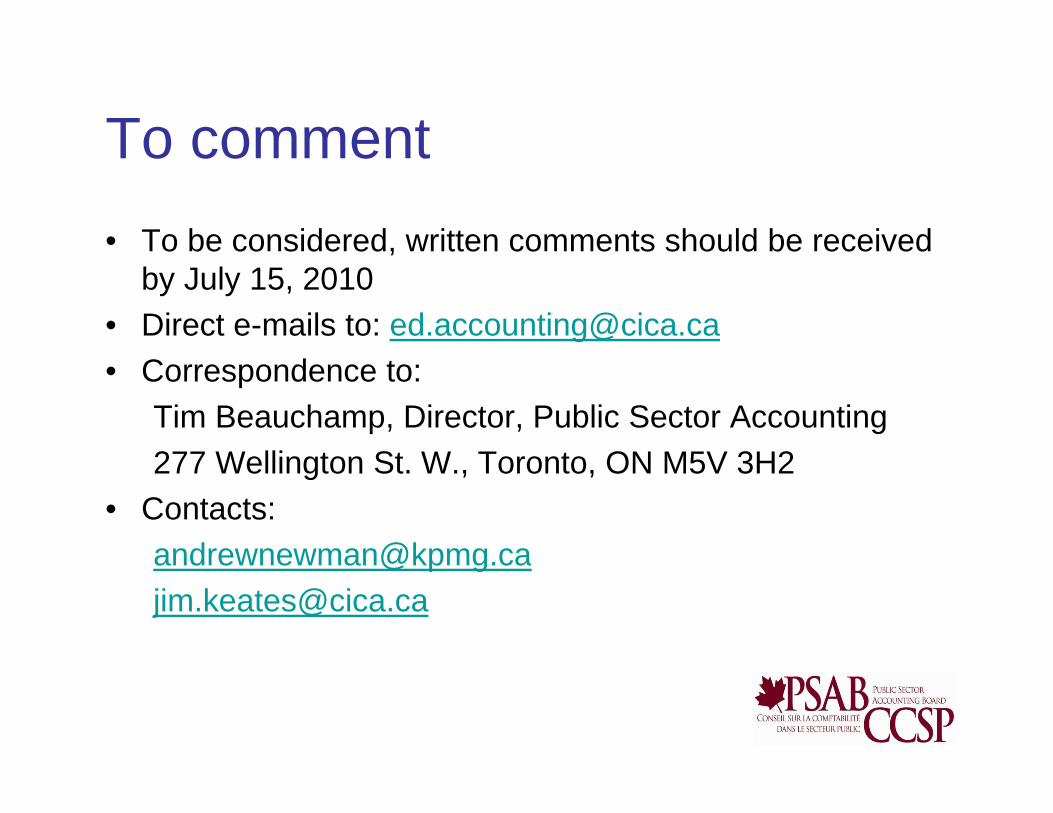

To commentTo comment• To be considered, written comments should be received ,

by July 15, 2010• Direct e-mails to: [email protected]• Correspondence to:

Tim Beauchamp, Director, Public Sector Accounting277 Wellington St W Toronto ON M5V 3H2277 Wellington St. W., Toronto, ON M5V 3H2

• Contacts:andrewnewman@kpmg [email protected]@cica.ca

Q estions and Ans ersQuestions and Answers