the furniture industry in - squarespace2008.pdf · the furniture industry in germany 10/09 ......

TRANSCRIPT

© Copyright CSIL

CSIL Milano scrl15 corso Monforte 20122 Milano Italy

tel. +39 02 796630 fax +39 02 [email protected] – www.csilmilano.com

THE FURNITURE INDUSTRY IN GERMANY SCENARIO

Multiclient Research COUNTRY REPORTS

September 08 – R2413.DE HOME FURNITURE

UPHOLSTERY

MATTRESSES

OFFICE

KITCHEN

APPLIANCES

LIGHTING

All CSIL publications are available for online purchase and immediate download from: http://www.csilmilano.com http://www.worldfurnitureonline.com Reports are also available in printed form. For further information, please contact: [email protected]

© Copyright CSIL

CSIL Milano scrl15 corso Monforte 20122 Milano Italy

tel. +39 02 796630 fax +39 02 [email protected] – www.csilmilano.com

SCENARIO

The furniture industry in Germany COUNTRY REPORTS

Report prepared by C. Pisa Coordinated by A. Tracogna HOME FURNITURE

UPHOLSTERY

MATTRESSES

OFFICE

KITCHEN

APPLIANCES

LIGHTING

All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise. Any such action is an infringement of the Italian Law (L.18 August 2000 n.248) and may give rise to a legal action for damages and may be prosecuted as a criminal offence. All information in this report is verified to the best of the author's and the publisher's ability. However, CSIL does not accept responsibility for any errors and/ or omissions resulting from any source and for any loss arising from reliance on it.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

I

CONTENTS 1. GERMANY. FURNITURE INDUSTRY SUMMARY 1 2. FORESTRY RESOURCES, SEMI-FINISHED GOODS AND TECHNOLOGY 3 3. THE FURNITURE SECTOR: BASIC DATA 5

3.1. Furniture production 7 3.2. Furniture consumption 10 3.3. Furniture distribution channels 12

4. MAJOR FURNITURE MANUFACTURERS 14 5. INTERNATIONAL TRADE 72

5.1. Furniture exports 73 5.2. Furniture imports 76

6. IMPORT AND EXPORT TABLES 82

LIST OF FIGURES AND TABLES Table 1.1 Germany. Economic indicators 1 Table 1.2 Germany. Exchange rates 1 Table 1.3 Germany. Real growth of furniture consumption: forecast 2 Table 1.4 Germany. Main furniture trading partners 2 Table 2.1 Germany. Production, exports, imports and consumption of the main semi-finished goods, 2000-2006. Thousands of cubic

metres 3 Table 3.1 Germany. The furniture sector: basic data, 2002-2007 5 Figure 3.1 Germany. The openness of the furniture market, 2002-2007. Exports/production and imports/consumption ratios 6 Figure 3.2 Germany. Furniture production, 2002-2007. Million Eur and annual percentage changes at current prices 7 Table 3.2 Germany. Furniture production prices, 2002-2007. Annual percentage changes 8 Figure 3.3 Germany. Furniture production by segment, 2002 and 2007. Percentage breakdown of value data 8 Table 3.3 Germany. Furniture production by segment, 2002-2007. Million Eur 8 Figure 3.4 Germany. Furniture consumption, 2002-2007. Million Eur and annual percentage changes at current prices 10 Figure 3.5 Germany. Furniture consumption by segment, 2002 and 2007. Percentage breakdown of value data 11 Table 3.4 Germany. Furniture consumption by segment, 2002-2007. Million Eur 11 Figure 3.6 Germany. Home furniture sales by distribution channel, 2006. Percentage breakdown of value data 13 Table 4.1 Germany. Major furniture manufacturers 14 Figure 5.1 Germany. Furniture exports, imports and trade balance, 2002-2007. Million Eur 72 Figure 5.2 Germany. Furniture exports, 2002-2007. Million Eur and annual percentage changes 73 Figure 5.3 Germany. Furniture exports by segment, 2002 and 2007. Percentage breakdown in value 74 Figure 5.4 Germany. Furniture exports by segment. Annual percentage changes at current prices 2007 on 2006 and average growth

rates, 2002-2007 75 Figure 5.5 Germany. Furniture imports, 2002-2007. Million current Euro and annual percentage changes 76 Figure 5.6 Germany. Furniture imports by segment, 2002 and 2007. Percentage breakdown in value 77 Figure 5.7 Germany. Furniture imports by segment. Annual percentage changes at current prices 2007 on 2006 and average growth

rates, 2002-2007 78 Table 6.1 Germany. Furniture exports by product, 2002-2007 83 Table 6.2 Germany. Furniture imports by product, 2002-2007 83 Table 6.3 Germany. Exports of furniture including parts by country and by geographical area, 2002-2007 84

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

II

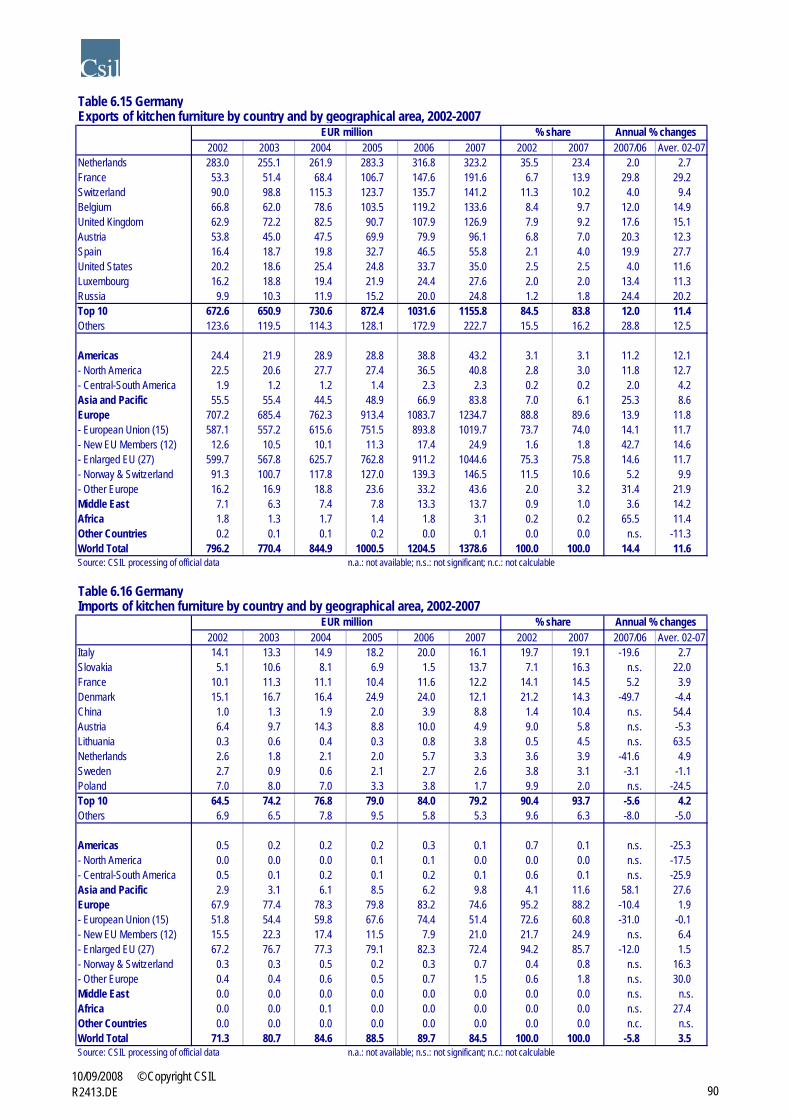

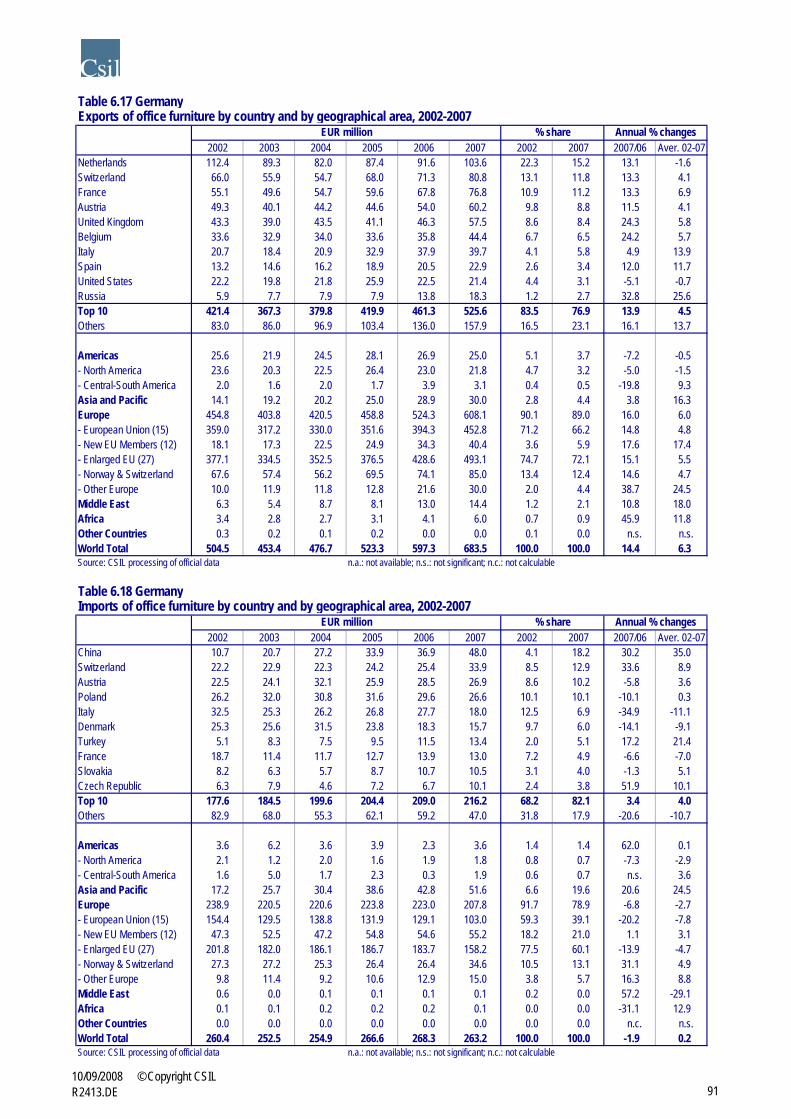

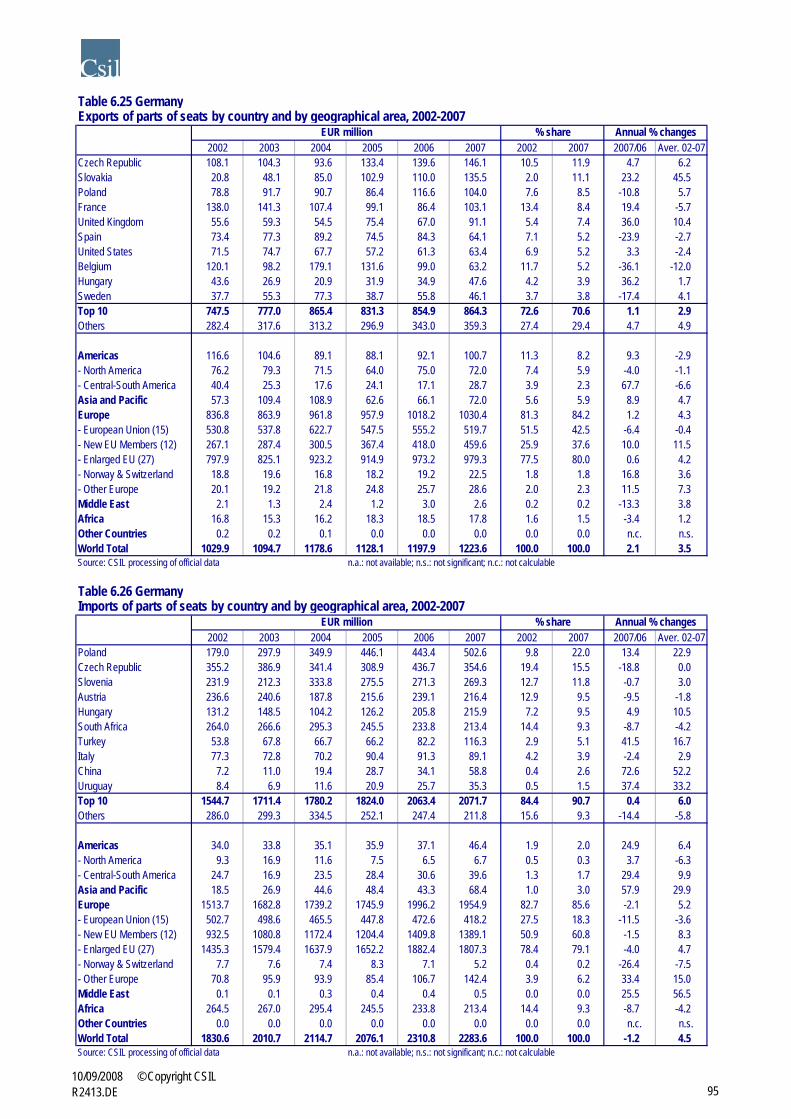

Table 6.4 Germany. Imports of furniture including parts by country and by geographical area, 2002-2007 84 Table 6.5 Germany. Exports of furniture excluding parts by country and by geographical area, 2002-2007 85 Table 6.6 Germany. Imports of furniture excluding parts by country and by geographical area, 2002-2007 85 Table 6.7 Germany. Exports of furniture parts by country and by geographical area, 2002-2007 86 Table 6.8 Germany. Imports of furniture parts by country and by geographical area, 2002-2007 86 Table 6.9 Germany. Exports of upholstered furniture by country and by geographical area, 2002-2007 87 Table 6.10 Germany. Imports of upholstered furniture by country and by geographical area, 2002-2007 87 Table 6.11 Germany. Exports of non-upholstered seats by country and by geographical area, 2002-2007 88 Table 6.12 Germany. Imports of non-upholstered seats by country and by geographical area, 2002-2007 88 Table 6.13 Germany. Exports of bedroom furniture by country and by geographical area, 2002-2007 89 Table 6.14 Germany. Imports of bedroom furniture by country and by geographical area, 2002-2007 89 Table 6.15 Germany. Exports of kitchen furniture by country and by geographical area, 2002-2007 90 Table 6.16 Germany. Imports of kitchen furniture by country and by geographical area, 2002-2007 90 Table 6.17 Germany. Exports of office furniture by country and by geographical area, 2002-2007 91 Table 6.18 Germany. Imports of office furniture by country and by geographical area, 2002-2007 91 Table 6.19 Germany. Exports of furniture for dining and living rooms by country and by geographical area, 2002-2007 92 Table 6.20 Germany. Imports of furniture for dining and living rooms by country and by geographical area, 2002-2007 92 Table 6.21 Germany. Exports of other furniture by country and by geographical area, 2002-2007 93 Table 6.22 Germany. Imports of other furniture by country and by geographical area, 2002-2007 93 Table 6.23 Germany. Exports of furniture parts excluding parts of seats by country and by geographical area, 2002-2007 94 Table 6.24 Germany. Imports of furniture parts excluding parts of seats by country and by geographical area, 2002-2007 94 Table 6.25 Germany. Exports of parts of seats by country and by geographical area, 2002-2007 95 Table 6.26 Germany. Imports of parts of seats by country and by geographical area, 2002-2007 95

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

1

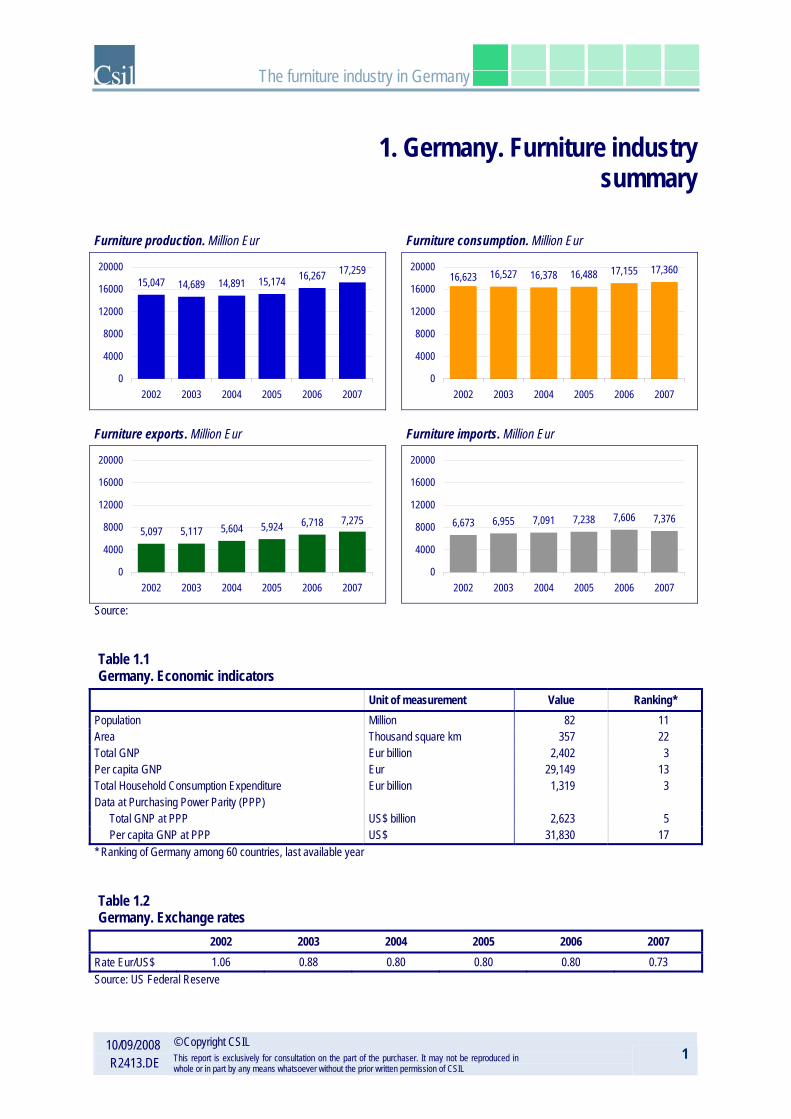

1. Germany. Furniture industry summary

Furniture production. Million Eur

Furniture consumption. Million Eur

15,047 14,689 14,891 15,174 16,267 17,259

0

4000

8000

12000

16000

20000

2002 2003 2004 2005 2006 2007

16,623 16,527 16,378 16,488 17,155 17,360

0

4000

8000

12000

16000

20000

2002 2003 2004 2005 2006 2007

Furniture exports. Million Eur

Furniture imports. Million Eur

7,2756,7185,9245,6045,1175,097

0

4000

8000

12000

16000

20000

2002 2003 2004 2005 2006 2007

7,3767,6067,2387,0916,9556,673

0

4000

8000

12000

16000

20000

2002 2003 2004 2005 2006 2007

Source:

Table 1.1 Germany. Economic indicators

Unit of measurement Value Ranking* Population Million 82 11 Area Thousand square km 357 22 Total GNP Eur billion 2,402 3 Per capita GNP Eur 29,149 13 Total Household Consumption Expenditure Eur billion 1,319 3 Data at Purchasing Power Parity (PPP)

Total GNP at PPP US$ billion 2,623 5 Per capita GNP at PPP US$ 31,830 17

* Ranking of Germany among 60 countries, last available year

Table 1.2 Germany. Exchange rates

2002 2003 2004 2005 2006 2007 Rate Eur/US$ 1.06 0.88 0.80 0.80 0.80 0.73 Source: US Federal Reserve

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

2

Table 1.3 Germany. Real growth of furniture consumption: forecast

2008 2009 1% 1%

Exports/production ratio

Imports/consumption ratio

33.9 34.8 39.0 41.3 42.237.6

0

20

40

60

80

100

2002 2003 2004 2005 2006 2007

Exports / production

40.1 42.1 43.9 44.3 42.543.3

0

20

40

60

80

100

2002 2003 2004 2005 2006 2007

Imports / consumption

Table 1.4 Germany. Main furniture trading partners

Destination of furniture exports Origin of furniture imports Netherlands 12.9% Poland 21.3% France 11.5% China 11.0% Austria 9.9% Italy 9.5% Switzerland 9.9% Czech Republic 6.7% United Kingdom 8.2% Austria 6.1% Belgium 6.4% Denmark 4.7% Spain 4.0% Hungary 4.4% United States 3.7% Slovenia 4.1% Italy 3.5% Switzerland 3.7% Czech Republic 3.3% South Africa 2.9%

Breakdown of furniture exports by area

Breakdown of furniture imports by area

0%

20%

40%

60%

80%

100%

Americas Europe Asia andPacific

MiddleEast

Africa WorldTotal

2003 2005 2007

0%

20%

40%

60%

80%

100%

Americas Europe Asia andPacific

MiddleEast

Africa WorldTotal

2003 2005 2007

Sources: CSIL, Eurostat, United Nations, World Bank and National Statistical Offices

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

3

2. Forestry resources, semi-finished goods and technology

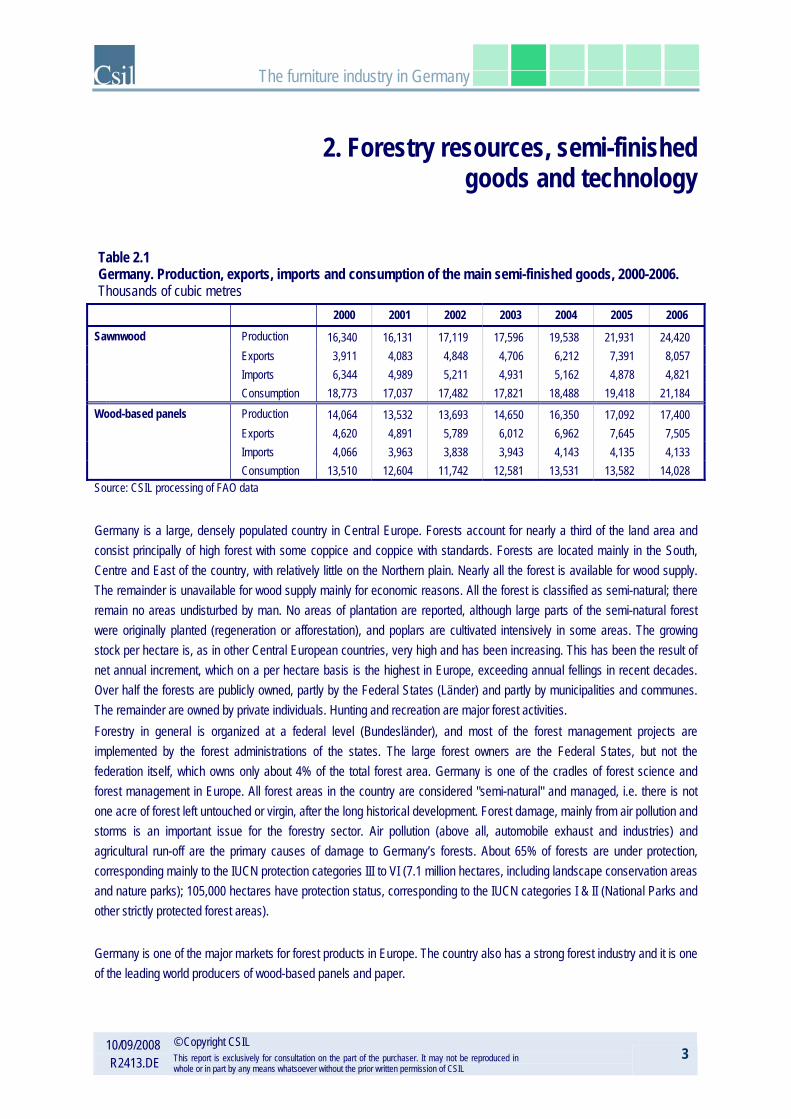

Table 2.1 Germany. Production, exports, imports and consumption of the main semi-finished goods, 2000-2006. Thousands of cubic metres

2000 2001 2002 2003 2004 2005 2006

Sawnwood Production 16,340 16,131 17,119 17,596 19,538 21,931 24,420 Exports 3,911 4,083 4,848 4,706 6,212 7,391 8,057 Imports 6,344 4,989 5,211 4,931 5,162 4,878 4,821 Consumption 18,773 17,037 17,482 17,821 18,488 19,418 21,184 Wood-based panels Production 14,064 13,532 13,693 14,650 16,350 17,092 17,400 Exports 4,620 4,891 5,789 6,012 6,962 7,645 7,505 Imports 4,066 3,963 3,838 3,943 4,143 4,135 4,133 Consumption 13,510 12,604 11,742 12,581 13,531 13,582 14,028 Source: CSIL processing of FAO data

Germany is a large, densely populated country in Central Europe. Forests account for nearly a third of the land area and consist principally of high forest with some coppice and coppice with standards. Forests are located mainly in the South, Centre and East of the country, with relatively little on the Northern plain. Nearly all the forest is available for wood supply. The remainder is unavailable for wood supply mainly for economic reasons. All the forest is classified as semi-natural; there remain no areas undisturbed by man. No areas of plantation are reported, although large parts of the semi-natural forest were originally planted (regeneration or afforestation), and poplars are cultivated intensively in some areas. The growing stock per hectare is, as in other Central European countries, very high and has been increasing. This has been the result of net annual increment, which on a per hectare basis is the highest in Europe, exceeding annual fellings in recent decades. Over half the forests are publicly owned, partly by the Federal States (Länder) and partly by municipalities and communes. The remainder are owned by private individuals. Hunting and recreation are major forest activities. Forestry in general is organized at a federal level (Bundesländer), and most of the forest management projects are implemented by the forest administrations of the states. The large forest owners are the Federal States, but not the federation itself, which owns only about 4% of the total forest area. Germany is one of the cradles of forest science and forest management in Europe. All forest areas in the country are considered "semi-natural" and managed, i.e. there is not one acre of forest left untouched or virgin, after the long historical development. Forest damage, mainly from air pollution and storms is an important issue for the forestry sector. Air pollution (above all, automobile exhaust and industries) and agricultural run-off are the primary causes of damage to Germany’s forests. About 65% of forests are under protection, corresponding mainly to the IUCN protection categories III to VI (7.1 million hectares, including landscape conservation areas and nature parks); 105,000 hectares have protection status, corresponding to the IUCN categories I & II (National Parks and other strictly protected forest areas). Germany is one of the major markets for forest products in Europe. The country also has a strong forest industry and it is one of the leading world producers of wood-based panels and paper.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

4

In 2006 sawnwood production was rather stable (-0.8%) compared to 2005, while wood-based panels production, composed mainly (62%) by particle board panels and fibreboard panels (34%), recorded growth by 7% compared to 2005. Germany is also an important exporter of semi-finished products: in 2006 it exported 33% of its sawnwood production and 43% of wood-based panels production. Germany has the highest share of wood-based panels exports (29%) among European (EU17) countries and the second highest share of sawnwood exports (19%) after Sweden. Exports of sawnwood registered a strong increase by 9% compared to 2005, while wood-based panels decreased slightly by 1.8%. Germany has the largest engineered wood product industry in Europe, which is based partly on sawnwood imports. Two thirds of the paper production is based on imported wood pulp. Paper recycling is well organised in Germany and it is one the largest exporters and consumers of recycled paper.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

5

3. The furniture sector: basic data

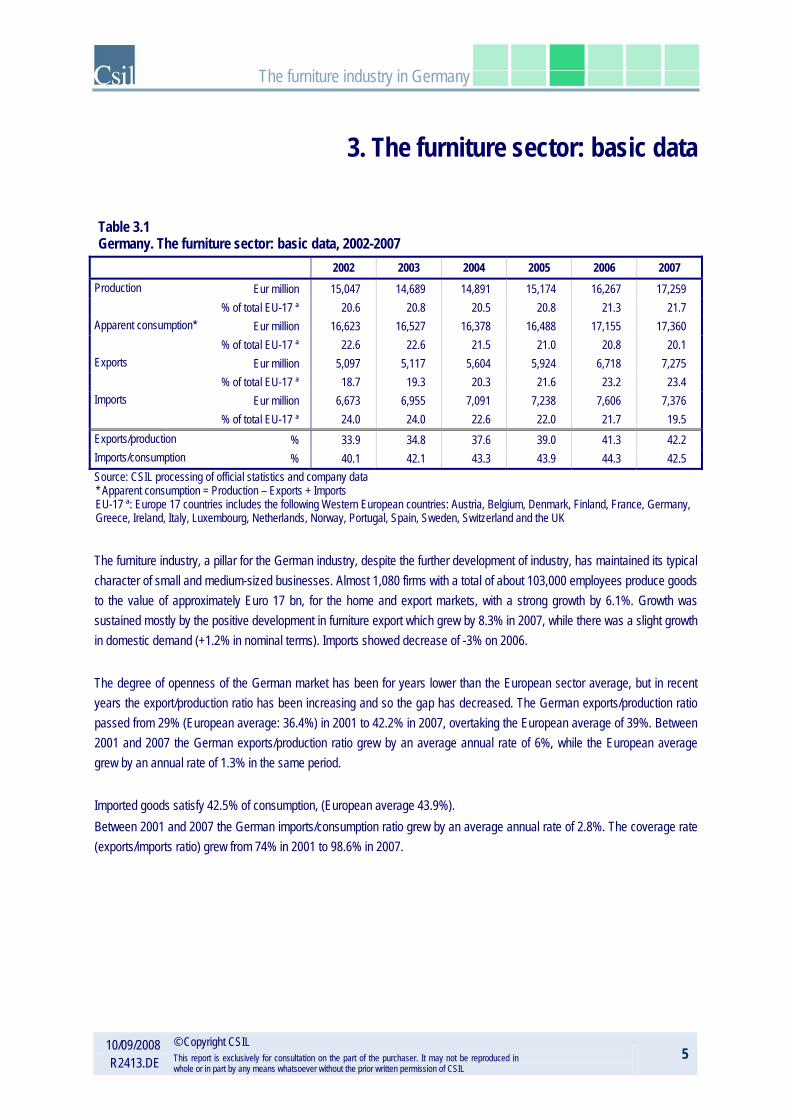

Table 3.1 Germany. The furniture sector: basic data, 2002-2007

2002 2003 2004 2005 2006 2007 Production Eur million 15,047 14,689 14,891 15,174 16,267 17,259 % of total EU-17 ª 20.6 20.8 20.5 20.8 21.3 21.7 Apparent consumption* Eur million 16,623 16,527 16,378 16,488 17,155 17,360 % of total EU-17 ª 22.6 22.6 21.5 21.0 20.8 20.1 Exports Eur million 5,097 5,117 5,604 5,924 6,718 7,275 % of total EU-17 ª 18.7 19.3 20.3 21.6 23.2 23.4 Imports Eur million 6,673 6,955 7,091 7,238 7,606 7,376 % of total EU-17 ª 24.0 24.0 22.6 22.0 21.7 19.5 Exports/production % 33.9 34.8 37.6 39.0 41.3 42.2 Imports/consumption % 40.1 42.1 43.3 43.9 44.3 42.5 Source: CSIL processing of official statistics and company data * Apparent consumption = Production – Exports + Imports EU-17 ª: Europe 17 countries includes the following Western European countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the UK

The furniture industry, a pillar for the German industry, despite the further development of industry, has maintained its typical character of small and medium-sized businesses. Almost 1,080 firms with a total of about 103,000 employees produce goods to the value of approximately Euro 17 bn, for the home and export markets, with a strong growth by 6.1%. Growth was sustained mostly by the positive development in furniture export which grew by 8.3% in 2007, while there was a slight growth in domestic demand (+1.2% in nominal terms). Imports showed decrease of -3% on 2006. The degree of openness of the German market has been for years lower than the European sector average, but in recent years the export/production ratio has been increasing and so the gap has decreased. The German exports/production ratio passed from 29% (European average: 36.4%) in 2001 to 42.2% in 2007, overtaking the European average of 39%. Between 2001 and 2007 the German exports/production ratio grew by an average annual rate of 6%, while the European average grew by an annual rate of 1.3% in the same period. Imported goods satisfy 42.5% of consumption, (European average 43.9%). Between 2001 and 2007 the German imports/consumption ratio grew by an average annual rate of 2.8%. The coverage rate (exports/imports ratio) grew from 74% in 2001 to 98.6% in 2007.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

6

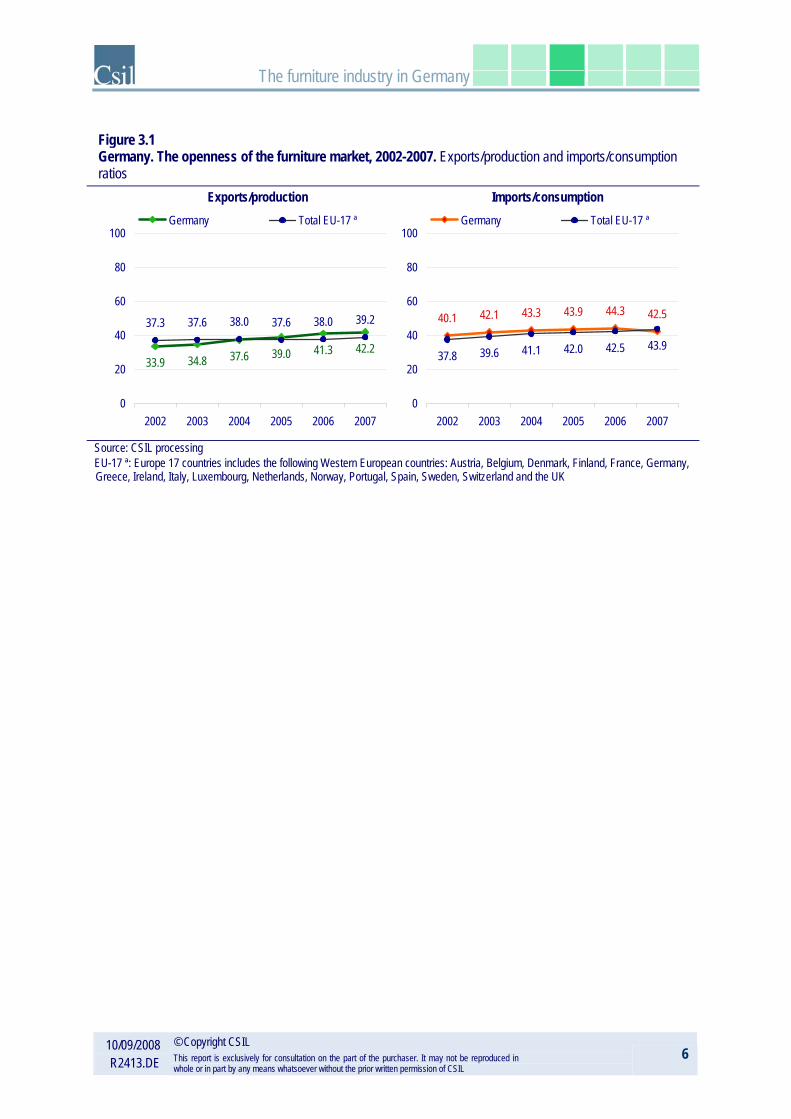

Figure 3.1 Germany. The openness of the furniture market, 2002-2007. Exports/production and imports/consumption ratios

Exports/production Imports/consumption

37.3 37.6 38.0 37.6

39.037.634.833.942.241.3

39.238.0

0

20

40

60

80

100

2002 2003 2004 2005 2006 2007

Germany Total EU-17 ª

40.1 42.1 43.3 43.9

37.8 41.1 42.0

44.3 42.5

39.6 42.5 43.9

0

20

40

60

80

100

2002 2003 2004 2005 2006 2007

Germany Total EU-17 ª

Source: CSIL processing EU-17 ª: Europe 17 countries includes the following Western European countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the UK

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

7

3.1. Furniture production

Figure 3.2 Germany. Furniture production, 2002-2007. Million Eur and annual percentage changes at current prices

17,25916,26715,17414,89114,68915,047

0250050007500

1000012500150001750020000

2002 2003 2004 2005 2006 2007

million EUR

1.4

7.2

-12.8

6.1

-2.41.9

-15

-10

-5

0

5

10

2002 2003 2004 2005 2006 2007

% changes

Source: CSIL processing

Germany is Europe’s second producer of furniture after Italy: with a volume of production of Euro 17,259 million in 2007, provides 22% of total European supply. From the industrial point of view Germany is the main reference point for the economies of the euro area, and also the country that suffered most from the negative effects of the serious crisis post-2001. In 2002 and 2003 growth in GDP was zero in real terms and over the course of 2005 it increased by roughly 1% confirming the performance of 2004. Germany showed a return to growth in 2006 at a healthy rate (GDP: +2.9%), a level close to that of 2000 and also in 2007 German economy continued its positive trend (GDP: +2.5%), in spite of the initial fears linked to the global economy and to the effects of the VAT increase on private consumption. Growth was sustained by exports dynamics, which recorded decisive growth over the last year, but also by investments and public consumption. This general trend had an influence on the performance of the furniture segment, in fact, over the 2001-2004 period the average annual change in production was –4.8%. It was in these years that an extensive process of downsizing occurred, with numerous firms restructuring and closing factories with strong repercussions on employment levels. Starting in 2004, the strong increase by 7.2% in 2006 was followed by a 6% growth in 2007 (+3.8% in real terms), driven by exports which recorded increase by 8.3% in 2007.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

8

Table 3.2 Germany. Furniture production prices, 2002-2007. Annual percentage changes

2002 2003 2004 2005 2006 2007

Furniture prices 1.9 0.4 0.9 1.9 1.6 2.2 Source: CSIL processing

Production by segment

Figure 3.3 Germany. Furniture production by segment, 2002 and 2007. Percentage breakdown of value data

1715

10

2

11

161714

22

10

6

2

11

17

8

21

0

5

10

15

20

25

Office furniture Upholsteredfurniture

Kitchenfurniture

Bedroomfurniture

Dining andliving room

furniture

Non-upholstered

seats

Other furniture Furniture partsand seating

parts

2002 2007

Source: CSIL processing

Table 3.3 Germany. Furniture production by segment, 2002-2007. Million Eur

2002 2003 2004 2005 2006 2007 Total furniture 15,047 14,689 14,891 15,174 16,267 17,259 Of which: Office furniture 2,541 2,204 2,162 2,315 2,570 2,909 Upholstered furniture 2,223 2,178 2,266 2,377 2,441 2,483 Kitchen furniture 3,164 3,048 3,185 3,307 3,690 3,882 Bedroom furniture 1,538 1,516 1,519 1,513 1,661 1,732 Dining and living room furniture 1,213 1,069 1,081 1,061 1,129 1,096 Non-upholstered seats 267 290 285 299 307 346 Other furniture 1,657 1,973 1,912 1,753 1,708 1,833 Total furniture excluding parts 12,603 12,279 12,409 12,625 13,506 14,281 Furniture parts and seating parts 2,444 2,411 2,483 2,549 2,760 2,979 Source: CSIL processing

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

9

The most important segment of the German furniture industry is the kitchen furniture segment which represents 22% of total furniture. Germany is the leading producer of kitchen furniture in Europe (27% on total European supply) and also the top market in terms of consumption. In 2007 kitchen production increased by 5.2%, reaching a total value of Euro 3,882 million. The increase in production recorded by segment firms last year was destined especially for international markets. In 2007 total exports of kitchen furniture recorded growth of 14% reaching a value of Euro 1379 million. The German kitchen furniture industry employs almost 17,000 persons in about 100 firms. Germany produces kitchens for the low (57%) and the middle (21%) segments, with a 22% share of the upper and the upper-middle segments. Germany is the second producer of upholstered furniture in Europe after Italy, with a 21% share on total European supply. After registering important decreases over the last years, upholstery production in Germany recovered in 2004 and registered another growth of 3% in real terms in 2005. In 2006 production growth remained positive and increased by 1.2% in real terms, while it became negative in 2007, decreasing by 0.3% in real terms. Along with the drop in production, export activity dropped by 8.4% in nominal terms in 2007. After a negative trend over the 2001-2004 period (the average annual change in office furniture production was -7%), in 2005 office furniture production began to grow and in 2007 it recorded the highest growth in the last decade (+9.6% in real terms), enabling production to reach a value of Euro 2,909 million. Germany is also Europe’s leading producer of office furniture, providing a quota of 30.3% of total European supply, about one percentage point higher than the previous year. Germany is also the second producer of bedroom furniture and dining and living room furniture among the European countries (EU-17), with respectively 19% and 17% share on total European supply. After a negative trend in the 2001-2005 period, in 2007 bedroom furniture production continued to grow by 4.3% in nominal terms. Living room furniture production, instead decreased by 3% at current prices. Manufacturers of living room, dining room and bedroom furniture employ approximately 45,000 persons in 480 businesses.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

10

3.2. Furniture consumption

Figure 3.4 Germany. Furniture consumption, 2002-2007. Million Eur and annual percentage changes at current prices

17,36017,15516,48816,37816,52716,623

0250050007500

1000012500150001750020000

2002 2003 2004 2005 2006 2007

million EUR

0.74.0

-12.7

-0.9-0.6 1.2

-15

-10

-5

0

5

10

15

2002 2003 2004 2005 2006 2007

% changes

Source: CSIL processing Apparent consumption = production + imports – exports. Furniture consumption is at production prices

Germany is Europe’s largest furniture consumer: with a volume of consumption of Euro 17,360 million in 2007, it provides 20% of total European demand. After a decreasing trend between 1999-2005 (-2.4% annually) and a 4% increase in 2006, furniture consumption in Germany decreased slightly in real terms (-1%) in 2007, following the stagnation of private consumption. Despite the recovery of the German economy, which was driven by exports and by the domestic demand, in the component of gross fixed investments (+5% in 2007), families maintained a high level of saving and private consumption was rather stable (–0.1%). While the anticipation of the VAT increase led to a temporary growth in private consumption in 2006, the negative effects of this could be felt in 2007. Of greater importance, however, was the strong acceleration of inflation, which had a particular impact on consumer confidence because it is concentrated in high frequency purchases like fuel and food. In Germany there are over 39 million households. They spend annually about Euro 275 in furniture (European average: Euro 354).

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

11

The German annual per capita household furniture consumption in 2007 was Euro 131, a little lower than the average for Europe 17 (Euro 152). Between 2001 and 2007 the furniture household expenditure decreased by an average annual rate of 2.5%.

Consumption by segment

Figure 3.5 Germany. Furniture consumption by segment, 2002 and 2007. Percentage breakdown of value data

18

22

19

1213

4

13

19

23

19

11 10

5

12

0

5

10

15

20

25

Office furniture Upholsteredfurniture

Kitchen furniture Bedroom furniture Dining and livingroom furniture

Non-upholsteredseats

Other furniture

2002 2007

Source: CSIL processing

Table 3.4 Germany. Furniture consumption by segment, 2002-2007. Million Eur

2002 2003 2004 2005 2006 2007 Total furniture excluding parts 13,084 12,924 12,768 12,782 13,092 13,278 Of which: Office furniture 2,297 2,003 1,940 2,058 2,241 2,489 Upholstered furniture 2,853 2,840 2,922 3,072 3,111 3,093 Kitchen furniture 2,439 2,358 2,425 2,395 2,575 2,588 Bedroom furniture 1,548 1,498 1,463 1,434 1,522 1,502 Dining and living room furniture 1,744 1,563 1,543 1,517 1,510 1,365 Non-upholstered seats 538 621 614 631 620 671 Other furniture 1,664 2,041 1,862 1,674 1,513 1,570 Source: CSIL processing

The most important segment of the German furniture market is the upholstered furniture segment which represents 23% of total furniture, excluding parts. Germany is the second consumer of upholstered furniture in Europe (22% on total European market) after the United Kingdom. After the downturn in 2006, upholstery consumption continued to slow down, decreasing by 2.5% in real terms in 2007.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

12

The other most important segments are the kitchen furniture and office furniture ones, with shares of 19% each on total furniture consumption. Germany is the top market of kitchen furniture in Europe, with 19% share on total European market. In 2007 stagnation of private consumption was reflected in kitchen furniture consumption which was rather stable, growing slightly by only +0.5% in nominal terms. Germany is also Europe’s leading consumer of office furniture: with a volume of consumption of Euro 2,489 million in 2007 covers 27% of total European office market. After a negative trend over the 2000-2004 period, growth in domestic demand (+3.2% at constant prices) began in 2005 and continued to follow the particularly positive trend also in 2007 (+7.6% at constant prices). The post-2000 policies of limiting industrial investments took a U-turn in 2004 and investments continued throughout 2006 at significant rates, sustained the office furniture sector in 2007, too. Office furniture consumption was sustained by domestic production, while imports decreased by 2%. Germany is also the third consumer of bedroom furniture and the second of dining and living room furniture among the European countries (EU-17), with respectively 16% and 18% share on total European supply. After a negative trend in the 1999-2005 period, in 2006 bedroom furniture grew by 6% in nominal terms, but in 2007 bedroom consumption recorded a downturn of 1.3% at current prices. Also living room furniture continued to decrease by 9.6% in nominal terms.

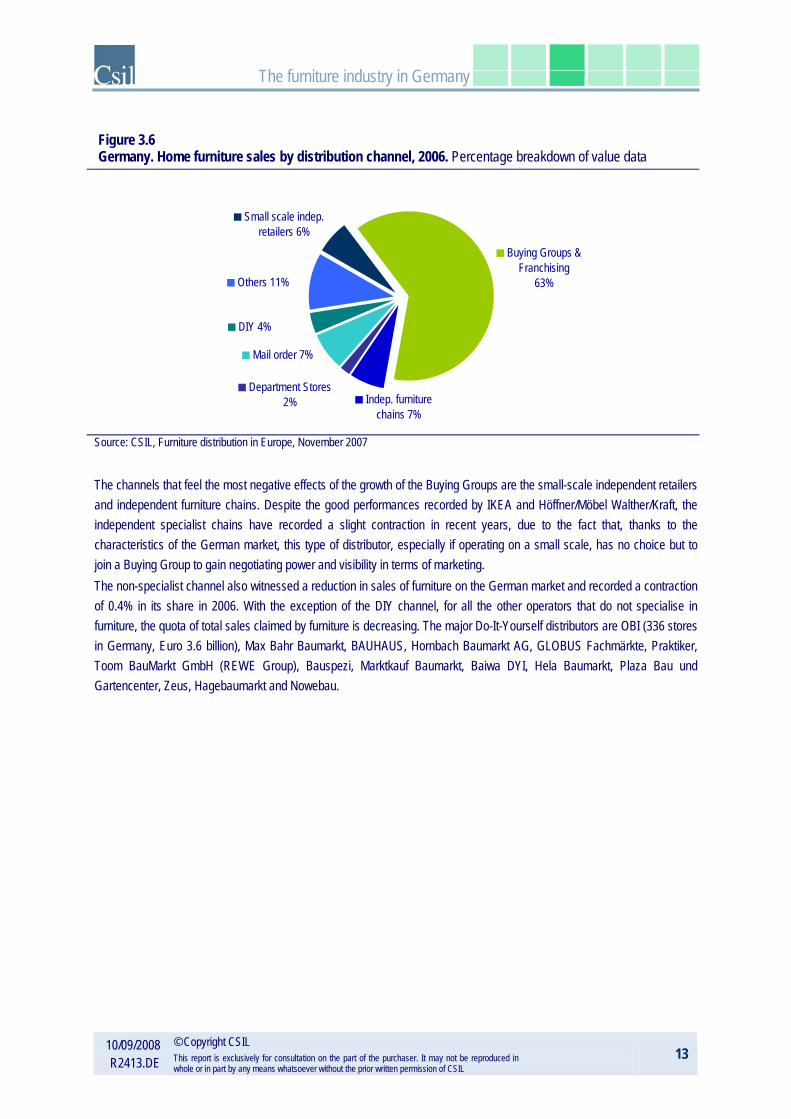

3.3. Furniture distribution channels In Germany 70% of the sales of home furniture are made through the large specialist retailers. In 2006 growth was recorded in this channel, which includes Buying Groups, both franchised and independent chains, although the latter are declining in importance. Growth was mainly due to the gradual expansion of the Buying Groups through the acquisition of important new members. The process of concentration within the German distribution system continued in 2006 with chains of stores and Buying Groups combining forces to share and optimize some phases of their activities. The main reason why small and medium-sized operators want to join Buying Groups is to be able to benefit from the services offered and to carry out more aggressive commercial policies (for both purchases and sales) which would be difficult to implement on a small scale. The excellent performances recorded by the major Buying Groups, including EMV, Union, Atlas and MVH, is proof of the success of the Buying Group formula. In 2006 the furniture chains belonging to an association, such as Lutz, Schaffrath Gruppe, Ostermann and Dodenhof that are all part of the most important German buying group Begros, also continued to record good results.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

13

Figure 3.6 Germany. Home furniture sales by distribution channel, 2006. Percentage breakdown of value data

DIY 4%

Others 11%

Indep. furniture chains 7%

Buying Groups & Franchising

63%

Small scale indep. retailers 6%

Mail order 7%

Department Stores 2%

Source: CSIL, Furniture distribution in Europe, November 2007

The channels that feel the most negative effects of the growth of the Buying Groups are the small-scale independent retailers and independent furniture chains. Despite the good performances recorded by IKEA and Höffner/Möbel Walther/Kraft, the independent specialist chains have recorded a slight contraction in recent years, due to the fact that, thanks to the characteristics of the German market, this type of distributor, especially if operating on a small scale, has no choice but to join a Buying Group to gain negotiating power and visibility in terms of marketing. The non-specialist channel also witnessed a reduction in sales of furniture on the German market and recorded a contraction of 0.4% in its share in 2006. With the exception of the DIY channel, for all the other operators that do not specialise in furniture, the quota of total sales claimed by furniture is decreasing. The major Do-It-Yourself distributors are OBI (336 stores in Germany, Euro 3.6 billion), Max Bahr Baumarkt, BAUHAUS, Hornbach Baumarkt AG, GLOBUS Fachmärkte, Praktiker, Toom BauMarkt GmbH (REWE Group), Bauspezi, Marktkauf Baumarkt, Baiwa DYI, Hela Baumarkt, Plaza Bau und Gartencenter, Zeus, Hagebaumarkt and Nowebau.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

14

4. Major furniture manufacturers

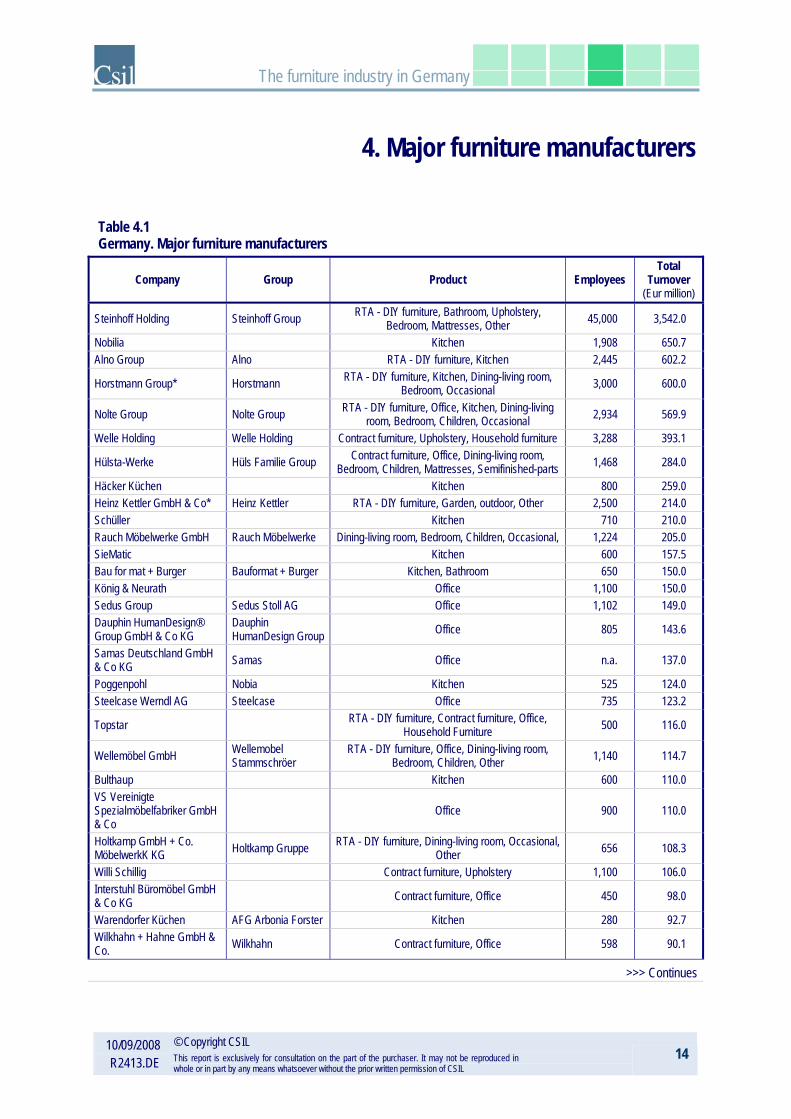

Table 4.1 Germany. Major furniture manufacturers

Company Group Product Employees Total

Turnover (Eur million)

Steinhoff Holding Steinhoff Group RTA - DIY furniture, Bathroom, Upholstery, Bedroom, Mattresses, Other 45,000 3,542.0

Nobilia Kitchen 1,908 650.7 Alno Group Alno RTA - DIY furniture, Kitchen 2,445 602.2

Horstmann Group* Horstmann RTA - DIY furniture, Kitchen, Dining-living room, Bedroom, Occasional 3,000 600.0

Nolte Group Nolte Group RTA - DIY furniture, Office, Kitchen, Dining-living room, Bedroom, Children, Occasional 2,934 569.9

Welle Holding Welle Holding Contract furniture, Upholstery, Household furniture 3,288 393.1

Hülsta-Werke Hüls Familie Group Contract furniture, Office, Dining-living room, Bedroom, Children, Mattresses, Semifinished-parts 1,468 284.0

Häcker Küchen Kitchen 800 259.0 Heinz Kettler GmbH & Co* Heinz Kettler RTA - DIY furniture, Garden, outdoor, Other 2,500 214.0 Schüller Kitchen 710 210.0 Rauch Möbelwerke GmbH Rauch Möbelwerke Dining-living room, Bedroom, Children, Occasional, 1,224 205.0 SieMatic Kitchen 600 157.5 Bau for mat + Burger Bauformat + Burger Kitchen, Bathroom 650 150.0 König & Neurath Office 1,100 150.0 Sedus Group Sedus Stoll AG Office 1,102 149.0 Dauphin HumanDesign® Group GmbH & Co KG

Dauphin HumanDesign Group Office 805 143.6

Samas Deutschland GmbH & Co KG Samas Office n.a. 137.0

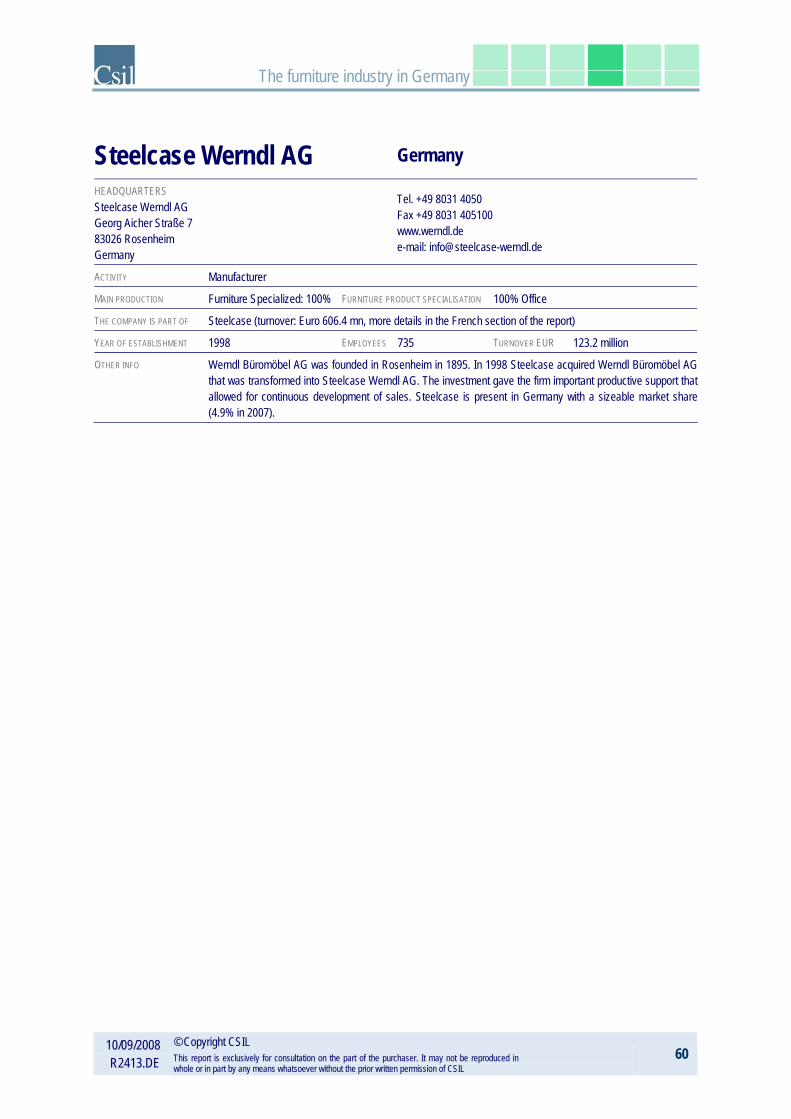

Poggenpohl Nobia Kitchen 525 124.0 Steelcase Werndl AG Steelcase Office 735 123.2

Topstar RTA - DIY furniture, Contract furniture, Office, Household Furniture 500 116.0

Wellemöbel GmbH Wellemobel Stammschröer

RTA - DIY furniture, Office, Dining-living room, Bedroom, Children, Other 1,140 114.7

Bulthaup Kitchen 600 110.0 VS Vereinigte Spezialmöbelfabriker GmbH & Co

Office 900 110.0

Holtkamp GmbH + Co. MöbelwerkK KG Holtkamp Gruppe RTA - DIY furniture, Dining-living room, Occasional,

Other 656 108.3

Willi Schillig Contract furniture, Upholstery 1,100 106.0 Interstuhl Büromöbel GmbH & Co KG Contract furniture, Office 450 98.0

Warendorfer Küchen AFG Arbonia Forster Kitchen 280 92.7 Wilkhahn + Hahne GmbH & Co. Wilkhahn Contract furniture, Office 598 90.1

>>> Continues

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

15

Company Group Product Employees Total

Turnover (Eur million)

Elastoform Polstermöbel GmbH & Co Upholstery 700 90.0

Wöstmann Gruppe Upholstery, Dining-living room, Bedroom, Tables-chairs, 500 78.2

HABA Habermaaß GmbH* HABA Corporate Family Children, Other n.a. 75.0

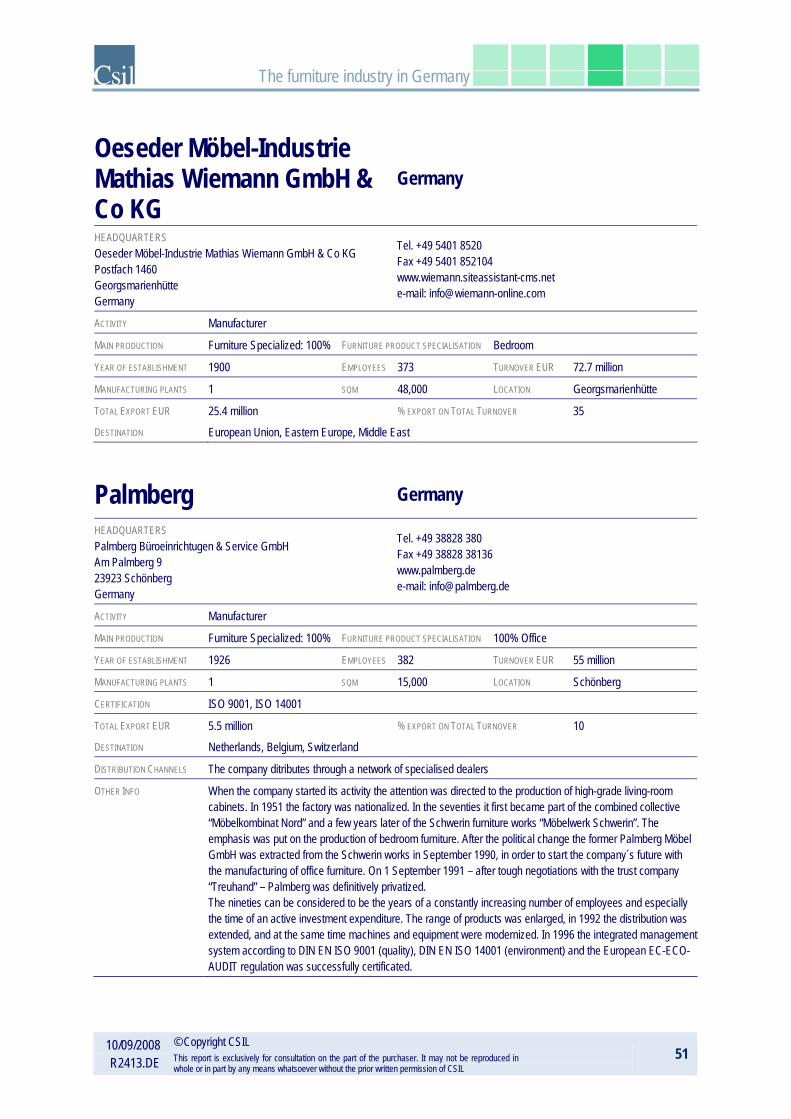

Burgbad AG Burgbad Bathroom, Other 598 73.7 Oeseder Möbel-Industrie Mathias Wiemann GmbH & Co KG

Bedroom 373 72.7

Keuco GmbH & Co KG Bathroom, Sanitary fittings 427 72.0 Koinor Polstermöbel GmbH & Co KG Upholstery, Tables-chairs, Textiles 480 72.0

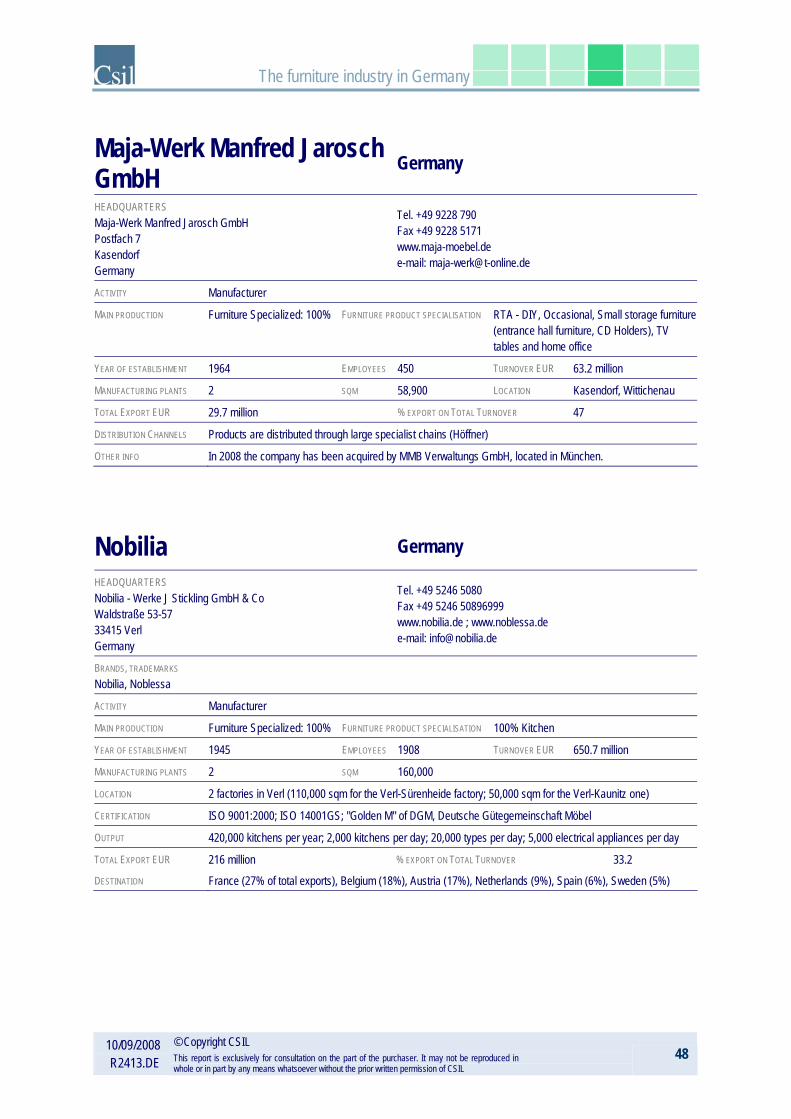

Ballerina Küchen Kitchen 240 70.0 Haworth GmbH Haworth Office n.a. 67.6 Maja-Werk Manfred Jarosch GmbH RTA - DIY furniture, Occasional, Household

Furniture, Other 450 63.2

Brunner GmbH Contract furniture, Office 350 60.0

Walter Knoll AG & Co KG Contract furniture, Office, Upholstery, Household Furniture 210 60.0

Assmann Büromöbel GmbH & Co Contract furniture, Office 256 55.0

Palmberg Büroeinrichtugen & Service GmbH Office 382 55.0

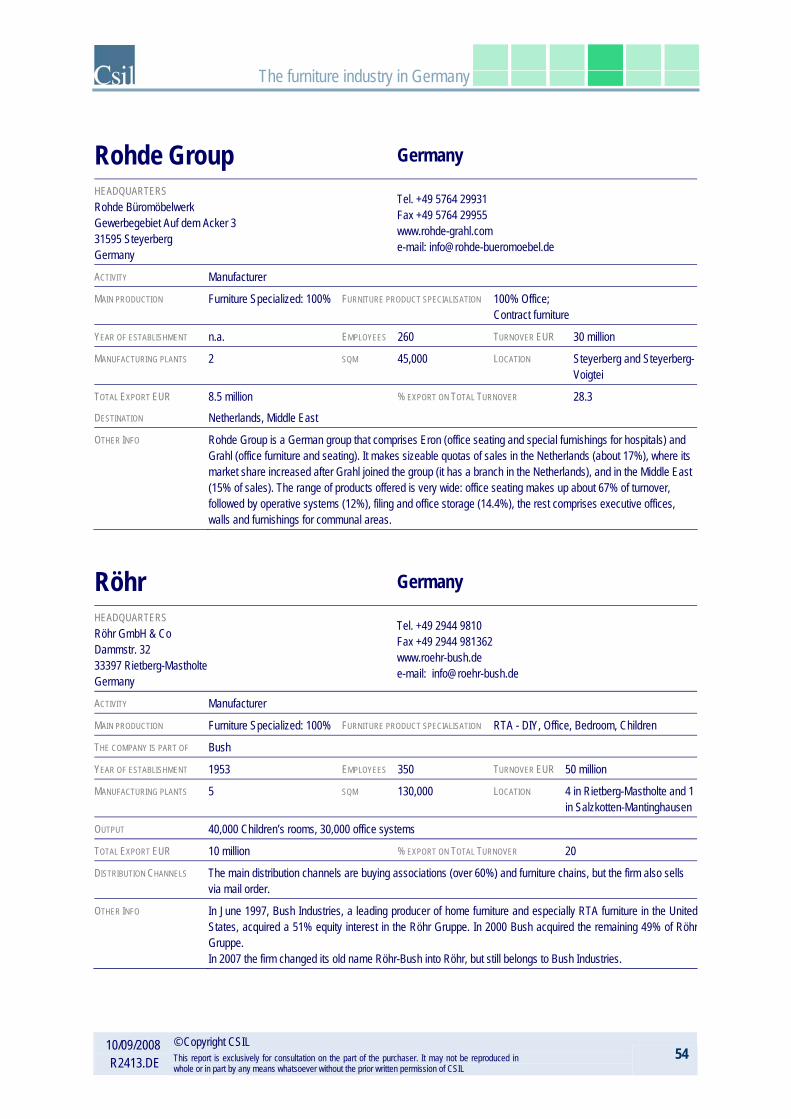

Röhr GmbH & Co Bush RTA - DIY furniture, Office, Bedroom, Children 350 50.0

Interlübke Contract furniture, Office, Dining-living room, Bedroom 328 45.7

Dedon GmbH Garden, outdoor, 400 40.0 Paschen & Companie GmbH & Co KG RTA - DIY furniture, Contract furniture, Dining-living

room, 200 40.0

Wössner GmbH Möbelwerk Dining-living room, Tables-chairs, 300 37.5 WINI Büromöbel Georg Schmidt GmbH & Co KG Contract furniture, Office 190 36.1

Rohde Büromöbelwerk Contract furniture, Office 260 30.0 Karl Vierhaus GmbH & Co KG Vierhaus Group Tables-chairs, Occasional, Household Furniture, 200 25.0

Gwinner GmbH & Co KG Office, Dining-living room, 184 24.5 SIEGER GmbH + Co Tables-chairs, Garden, outdoor, 295 23.3

Draenert Studio GmbH Contract furniture, Upholstery, Tables-chairs, Occasional, Household Furniture, 60 12.5

EMCO Bad GmbH & Co KG* Erwin Müller Gruppe Lingen Bathroom, Other n.a. n.a.

* Not furniture specialised

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

16

Alno Group Germany

HEADQUARTERS Alno AG Heiligenbergerstrasse 47 88630 Pfullendorf Germany

Tel. +49 7552 213189 Fax +49 7552 213400 www.alno.de e-mail: [email protected]

CONTROLLED COMPANIES, SUBSIDIARIES, OTHER RELATED COMPANIES Gustav Wellmann GmbH & Co. KG, Impuls Küchen GmbH, Pino Küchen GmbH

BRANDS, TRADEMARKS Alno, Impuls Küchen, Pino Küchen, Spectra Küchen, Wellmann, Geba, AME

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION 100% Kitchen; RTA - DIY

STOCK EXCHANGE Stock Exchanges in Frankfurt and Stuttgart STOCK SYMBOL ANO

THE COMPANY IS PART OF Alno

YEAR OF ESTABLISHMENT 1927 EMPLOYEES 2,445 TURNOVER EUR 602.2 million

TOTAL EXPORT EUR 186.7 million % EXPORT ON TOTAL TURNOVER 31

History

Alno Group, based in Pfullendorf, Germany, is a manufacturing company.

The company was established in 1927 in Wangen bei Göppingen, Baden-Württemberg, Germany by Albert Nothdurft who opened up a small carpentry workshop.

The positive development of this workshop led to the relocation of its production facilities to Pfullendorf in 1957, and in 1958 the carpentry workshop developed into ALNO Möbelwerke GmbH + Co. KG (ALNO Furniture Production Ltd).

The company was listed on the Stock Exchanges in Frankfurt and Stuttgart in 1995 (trading symbol: ANO).

Financial Highlights

In 2007 Alno Group recorded a total turnover of Euro 602.2 million, compared to 615.5 million in 2006. Despite a decline of about 9% in the domestic market, Alno recorded only a slight drop of 2.2% in sales compared to the previous year. This was principally thanks to growth in exports, which ALNO managed to increase by 7.5 % on the year before.

Manufacturing process

The company employed 2,445 people in 2007 (-8% on 2006).

In addition to the factories in the company’s traditional home town of Pfullendorf, where fitted kitchens are manufactured under the Alno brand name, Alno AG has at its disposal various other subsidiary German production companies that manufacture kitchens for specialized market segments: Pino Küchen GmbH in Coswig-Klieken, Impuls Küchen GmbH in Brilon and Gustav Wellmann GmbH + Co. KG in Enger. Elsewhere in Europe, ALNO has eight wholly-owned marketing subsidiary companies.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

17

In 1990 Impuls Küchen GmbH was established in Brilon and in 1992 a joint venture was set up with the Polish company Forte S.A. that enabled the company to penetrate the Polish and Eastern European markets (Forte was sold in 2003).

In 1994 Alno established another furniture manufacturing company in Klieken, called Pino Küchen GmbH.

In 1998 Alno decided to flank its Brilon factory with a new plant to produce bathroom furniture in order to diversify its product range. Puris Bad GmbH was sold to Steinhoff in 2003.

In August 2003 Alno AG merged with the Casawell Service Group, a network of companies active across the world in the fields of fitted kitchens and DIY-kitchens and in kitchen technology. Currently Casawell consists of Wellmann, the main company and brand of Casawell in the middle market range. Gustav Wellmann Ltd. was founded in 1953 as a craftsman’s business.

In mid-2005 Alno sold its company Wellpac Möbelwerke GmbH (RTA kitchen), the biggest loss maker of 2004, and disposed of its unprofitable electrical appliance warehouse in Ennigloh. Also in 2005 Alno Middle East (AME) started business and was the Alno Group's first-ever international production site.

During 2006 Alno handed over the remaining business, not including the kitchen sector with a core business increase of 1.5%.

Products

Kitchen furniture sales were Euro 602.2 million (-2.2% on 2006) and account for 100% on total turnover.

Strategic growth initiatives

In 2007 ALNO Group approved further restructuring measures, which have been completed in 2008, by cutting also jobs. The company invested around Euro 32.5 million in one-off and restructuring costs.

In 2008 ALNO AG gains a strong partner in Al Khayyat Investments L.L.C (a holding based in Dubai), who acquires 50% of shareholding in its whole subsidiary ALNO Middle East (AME). The aim is to use the strong ALNO brand and Al Khayyat’s network and experience to sustainably strengthen the long-term growth of AME across the Middle East.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

18

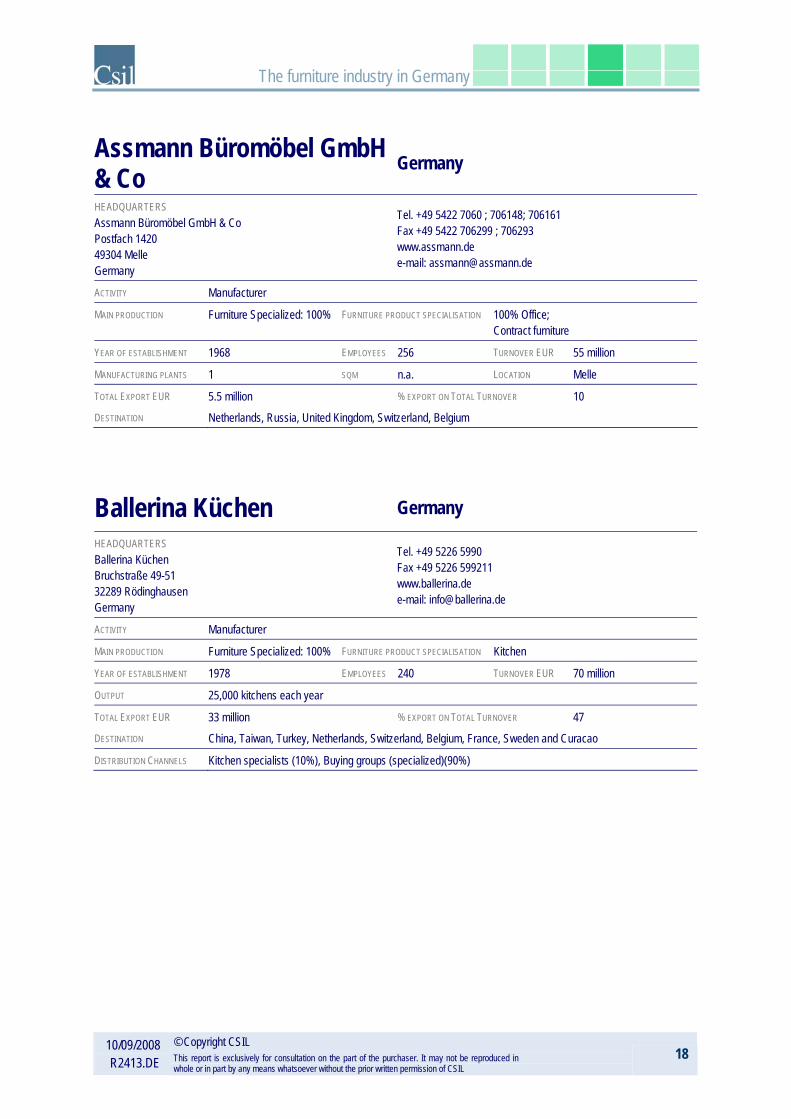

Assmann Büromöbel GmbH & Co Germany

HEADQUARTERS Assmann Büromöbel GmbH & Co Postfach 1420 49304 Melle Germany

Tel. +49 5422 7060 ; 706148; 706161 Fax +49 5422 706299 ; 706293 www.assmann.de e-mail: [email protected]

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION 100% Office; Contract furniture

YEAR OF ESTABLISHMENT 1968 EMPLOYEES 256 TURNOVER EUR 55 million

MANUFACTURING PLANTS 1 SQM n.a. LOCATION Melle

TOTAL EXPORT EUR 5.5 million % EXPORT ON TOTAL TURNOVER 10 DESTINATION Netherlands, Russia, United Kingdom, Switzerland, Belgium

Ballerina Küchen Germany

HEADQUARTERS Ballerina Küchen Bruchstraße 49-51 32289 Rödinghausen Germany

Tel. +49 5226 5990 Fax +49 5226 599211 www.ballerina.de e-mail: [email protected]

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION Kitchen

YEAR OF ESTABLISHMENT 1978 EMPLOYEES 240 TURNOVER EUR 70 million

OUTPUT 25,000 kitchens each year

TOTAL EXPORT EUR 33 million % EXPORT ON TOTAL TURNOVER 47 DESTINATION China, Taiwan, Turkey, Netherlands, Switzerland, Belgium, France, Sweden and Curacao

DISTRIBUTION CHANNELS Kitchen specialists (10%), Buying groups (specialized)(90%)

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

19

Bau for mat + Burger Germany

HEADQUARTERS Bau for mat Küchen GmbH & Co KG Kattwinkel 1 32584 Löhne Germany

Tel. +49 5732 1020 Fax +49 5732 102208 www.bauformat.de e-mail: [email protected]

BRANDS, TRADEMARKS Bau for mat, Burger, Badea

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION Kitchen, Bathroom

THE COMPANY IS PART OF Bauformat + Burger

YEAR OF ESTABLISHMENT 1985 EMPLOYEES 650 TURNOVER EUR 150 million

MANUFACTURING PLANTS 2 SQM 51,000 LOCATION In Löhne (Westphalia) and Burg (Magdeburg)

TOTAL EXPORT EUR 47 million % EXPORT ON TOTAL TURNOVER 31.5 DESTINATION Western Europe, Eastern Europe, the USA and Asia

DISTRIBUTION CHANNELS Bau-for-mat Küchen GmbH & Co. KG and Burger Küchenmöbel GmbH products are exclusively distributed by specialist kitchen retailers and chain stores with an exclusive kitchen department.

History

Bau for mat, based in Löhne, Germany, is a manufacturing company. The company was established in 1985. Bau-for-mat Küchen GmbH & Co. KG and the Burger Küchenmöbel GmbH have worked together for many years. Both companies started with the production of kitchen buffets. In the sixties the companies started producing fitted kitchens.

Financial Highlights

In 2007 Bau for mat recorded a total turnover of Euro 150 million, of which around 60% came from Bau-for-mat and 40% from Burger. Exports account for about over 30% of Bau-for-mat + Burger’s turnover. The main export markets are Western Europe, Eastern Europe, the USA and Asia. The major outlet markets in Western Europe are the Netherlands, Belgium, Luxembourg, Switzerland and Austria.

Manufacturing process

Today Bau-for-mat Küchen GmbH & Co. KG and Burger Küchenmöbel GmbH manufacture fitted kitchens at their two production plants in Löhne, Westphalia and Burg, Magdeburg. Together, the two production sites boast a production area of 51,000 square metres (33,000 square metres for Bau-for-mat and 18,000 square metres for Burger). In addition to its kitchen furniture production Burger offers a small supply of bathroom furniture. The company Group employed 650 workers in 2006.

Products

Kitchen furniture sales were about Euro 135 million, accounting for about 90% on total turnover.

Distribution channels

Bau-for-mat Küchen GmbH & Co. KG and Burger Küchenmöbel GmbH products are exclusively distributed by specialist kitchen retailers and chain stores with an exclusive kitchen department.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

20

Brunner GmbH Germany

HEADQUARTERS Brunner GmbH Im Salmenkopf 10 77866 Rheinau Germany

Tel. +49 7844 4020 Fax +49 7844 40280 www.brunner-stuehle.de e-mail: [email protected]

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT

SPECIALISATION 20% office; 80% other household; Contract furniture, Office (contract chairs and tables for theatres, auditoriums, hotels, restaurants and offices)

YEAR OF ESTABLISHMENT 1977 EMPLOYEES 350 TURNOVER EUR 60 million

OUTPUT The firm produces 1,500 seating articles and 400 tables each day.

TOTAL EXPORT EUR 24 million % EXPORT ON TOTAL TURNOVER 40

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

21

Bulthaup Germany

HEADQUARTERS Bulthaup GmbH & Co KG Aich / Werkstraße 6 84155 Bodenkirchen Germany

Tel. +49 8741 800 Fax +49 8741 80309 www.bulthaup.com e-mail: [email protected]

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION Kitchen

YEAR OF ESTABLISHMENT 1949 EMPLOYEES 600 TURNOVER EUR 110 million

OUTPUT 12,000 kitchen sets

TOTAL EXPORT EUR 82 million % EXPORT ON TOTAL TURNOVER 74.5 DESTINATION Its main export markets in Europe are the Netherlands (10% of total sales), France (7%), Spain (8%), Italy (6%),

UK (6%). Outside the EU Bulthaup gets good results in the North American Area (USA and Canada, 8%) and in the Asia Pacific area (9%)

DISTRIBUTION CHANNELS Kitchen specialists (100%)

History

Bulthaup, based in Bodenkirchen, Germany, is a manufacturing company.

The company was established in 1949 by Martin Bulthaup in Bodenkirchen, Lower Bavaria.

In 1978 Gerd Bulthaup, Martin’s son, took over as head of the company with the aim of becoming the market leader in design-oriented kitchens. In order to achieve this aim he needed to start cooperating with designers of which the most important was Otl Aicher.

Today the company manufactures contemporary design kitchen furniture for the upper-end of the market. The company has its head office in Germany and subsidiaries not only in Germany but also in the United Kingdom, France, Italy, Spain, the Netherlands, Switzerland, Japan, Hong Kong and the USA.

Financial Highlights

In 2007 Bulthaup recorded a total turnover of Euro 110 million (+17% on 2006). Exports account for about 75% of total turnover. Its main export markets in Europe are the Netherlands (10% of total sales), France (7%), Spain (8%), Italy (6%), UK (6%). Outside the EU Bulthaup gets good results in the North American Area (USA and Canada, 8%) and in the Asia Pacific area (9%).

Manufacturing process

The company employed around 600 employees in 2007 (+ 3% on 2006).

Products

Kitchen furniture sales were Euro 110 million and accounts 100% on total turnover. In the same year it produced around 12,000 kitchen sets.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

22

Marketing In recent years the firm has been more and more oriented towards reinforcing the Bulthaup brand on the world markets. Its strategy was not only designed to remind people of its product lines, but at the same time to give greater value to the articles.

The communication strategy is moving towards showing that the products are not only aesthetically attractive, but also boast ergonomic features and are of excellent quality.

Distribution channels

Bulthaup distributes mostly throughout a network of exclusive kitchen specialists in some 50 countries worldwide. The company sells also to furniture retailers.

The company has showrooms in major cities including Munich, Milan, London, New York and Tokyo.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

23

Burgbad AG Germany

HEADQUARTERS Burgbad AG Bad Fredeburg, Kirchplatz 10 57392 Schmallenberg Germany

Tel. +49 2974 96170 Fax +49 2974 9617278 www.burgbad.de e-mail: [email protected]

BRANDS, TRADEMARKS Burg, Kama, Schock, Burg Paris

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 93,8% FURNITURE PRODUCT SPECIALISATION Bathroom OTHER PRODUCTION Mirror cabinets, cast mineral products for bathrooms and adjacent areas

STOCK EXCHANGE Frankfurt Stock Exchange STOCK SYMBOL n.a.

THE COMPANY IS PART OF Burgbad

YEAR OF ESTABLISHMENT n.a. EMPLOYEES 598 TURNOVER EUR 73.7 million

MANUFACTURING PLANTS 4 LOCATION in Bad Fredeburg and Greding, in Lauterbach-Allmenrod, and in Nogent-le-Roi

TOTAL EXPORT EUR 32.2 million % EXPORT ON TOTAL TURNOVER 43.7 DESTINATION France, Austria, Eastern Europe

History

Burgbad AG, based in Schmallenberg, Germany, is a manufacturing company.

The company was listed on the Frankfurt Stock Exchange in 2000.

As the superordinate management holding company, Burgbad AG manages the 3 operating subsidiaries Burgkama GmbH, Société d'Equipement Postformé (S.E.P.) in France and Miral GmbH. Burgbad has radically simplified the structure of the Group in recent years.

Financial Highlights

In 2007 sales amounted to Euro 73.7 million, falling 1.7% short of the previous year’s figure of Euro 75 million. Furniture sales were Euro 69.1 million (-1.7% on 2006). While the dynamic growth seen in 2006 continued in the first quarter of 2007 (due to various factors, such as purchases being brought forward on account of the VAT increase and the backlog of construction orders resulting from the abolition of the owner-occupied housing subsidy), the German business became increasingly weak as the year progressed. Furniture sales on the domestic market were Euro 38.8 million (-9.3% on 2006).

Overall, the company’s international sales, instead, grew by 10% to Euro 32.2 million (in 2006: Euro 29.3 million), representing 43.7% of total sales. Burgbad’s expansion into other countries has enabled it to reduce its dependence on the German market. In France, which is the most important international market, by expanding the product portfolio on offer at Burg Paris, the company succeeded in countering the stagnant market and increasing its sales by 10%. The Group reported growth also in Austria and met high levels of demand in Eastern Europe, in particular UKraine and in Russia.

The company aims to increase its international share of sales to at least 50% in the medium term.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

24

Manufacturing process

The company employed 598 employees in 2007 (+ 2% on 2006).

The Group has four production plants: with locations in Bad Fredeburg and Greding, Burgkama GmbH is responsible for the Burg, Kama and Schock brands. The cast mineral products are supplied by Miral GmbH in Lauterbach-Allmenrod. The French market is supplied by the subsidiary S.E.P. in Nogent-le-Roi in France.

Products

Burgbad manufactures and sells high quality bathroom furniture, room concepts, mirror cabinets, cast mineral products for bathrooms and adjacent areas.

The business activities of the Group are divided into 3 primary segments: bathroom furniture, cast mineral products and consolidation and other segment (Holding company and transactions within the Group).

At Euro 69.1 million, sales in the bathroom furniture matched the level of sales reported in 2006 (Euro 70.4 million), thanks to the strength of the international business. In the cast mineral segment, Burgbad achieved slight sales growth from Euro 11.3 million to Euro 11.5 million.

Marketing Burgbad pursues a multi-brand strategy with Burg, Kama, Schock and Burg Paris. Each brand is specifically tailored to the needs of the respective target group. Today the subsidiary Burgkama produces and sells furniture concepts for Burg, Kama and Schock brands at two locations. The company has a separate brand for the French market - Burg Paris - for which the subsidiary Société d'Equipement Postformé is responsible. The subsidiary Miral GmbH produces cast mineral products, such as washstands, bathtubs and shower basins, both for the Burgbad Group and for external customers.

Strategic growth initiatives

Burgbad intends to strengthen its position in the European market and to expand into high-margin markets in the future. During 2007 Burgbad established the structures required to access the US market, where sales activities are due to take up in 2008. It is also planned to step up the company’s sales and marketing activities in Southern Europe (Italy).

The company has an investment policy which focuses on modernising and enhancing the efficiency of its machines and production processes in order to reduce costs. In 2007 the Group invested in a new edge processing facility at its Greding location. Total investments in property, plant and equipement rose by 45% from Euro 2.6 million to Euro 3.8 million in 2007.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

25

DAUPHIN Germany

HEADQUARTERS Dauphin HumanDesign® Group GmbH & Co KG Espanstrasse 36 91238 Offenhausen Germany

Tel. +49 9158 17550 Fax +49 9158 17787 www.dauphin-group.com e-mail: [email protected]

CONTROLLED COMPANIES, SUBSIDIARIES, OTHER RELATED COMPANIES Trend!Office, Züco Bürositzmöbel AG, Dauphin Components, Artifex GmbH, Dauphin Entwicklungs- und Beteiligungs GmbH BRANDS, TRADEMARKS Dauphin, Zuco, Trend!Office, Bosse

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION 100% Office

THE COMPANY IS PART OF Dauphin HumanDesign Group

YEAR OF ESTABLISHMENT 1969 EMPLOYEES 805 TURNOVER EUR 143.6 million

CERTIFICATION ISO 9001, ISO 14001

TOTAL EXPORT EUR 71.8 million % EXPORT ON TOTAL TURNOVER 50 DESTINATION Austria, Switzerland, France, United Kingdom, Belgium, Netherlands

History

Dauphin HumanDesign® Group GmbH & Co KG, based in Offenhausen, Germany, is a manufacturing company.

The company was established in 1969.

The family-owned company in 1992 became a 100% subsidiary of the Dauphin Office Interiors GmbH & Co. KG holding company. Dauphin has developed enormously thanks to a series of acquisitions and the setting up of new companies: in the nineties it acquired two seating producers, Zueco (CH) and Trend!Office (DE), while Bosse Design of Höxter (DE) was incorporated in order to introduce the firm to the market of wall-to-wall units and partition walls; Dauphin Components (mechanisms for seating) and Artifex GmbH (coverings and fillings) were created in Germany in 1993 with two production plants that supply all the firms in the group. In 2002 an operation of consolidation resulted in the creation of Dauphin Human Design Group which, in 2004, was flanked by another new firm specialising in the planning and design of working space and in consultancy: Sectio Aurea Consult GmbH & Co KG based in Munich.

Financial Highlights

In 2007 DAUPHIN recorded a total turnover of Euro 143.6 million (+8.8% on 2006). Furniture sales on the domestic market were Euro 71.8 million. Main exporting countries are: Austria, Switzerland, France, United Kingdom, Belgium, Netherlands.

Manufacturing process

The company employed 805 employees in 2007 (+ 6% on 2006).

At an international level the firm has 14 subsidiaries in the United States, South Africa, the United Kingdom, Spain, Singapore, France, Denmark, Benelux, Italy and Switzerland; six production plants and numerous licensed partners and agencies in more than 50 countries.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

26

Products

The Dauphin HumanDesign Group creates ergonomic working environments for people living in the 21st century.

Office furniture sales were Euro 143.6 million (+ 8.8% on 2006) and accounts for 100% on total turnover.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

27

Dedon GmbH Germany

HEADQUARTERS Dedon GmbH Stadtkoppel 26 21337 Lüneburg Germany

Tel. +49 4131 224470 Fax +49 4131 2244730 www.dedon.de e-mail: [email protected]

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized FURNITURE PRODUCT SPECIALISATION Garden, outdoor OTHER PRODUCTION Fabrics

YEAR OF ESTABLISHMENT 1990 EMPLOYEES 400 TURNOVER EUR 40 million

MANUFACTURING PLANTS n.a. LOCATION Island of Cebu (Philippines)

EXPORT DESTINATION More than 65 markets

DISTRIBUTION CHANNELS The contract segment accounts for an estimated 40% (5 star hotels, spas, restaurants, lounges and on the sundecks of international cruise liners etc.). Dedon operates company owned showrooms in Barcelona, Vienna, Paris and plans to open further showrooms. Besides, products are distributed in independent upper rangefurniture stores and outdoor specialists. In France Dedon products are imported by Sifas, in the UK products are imported by Leisure Plan, in Italy products are imported by Roda.

History

Dedon GmbH, based in Lüneburg, Germany, is a manufacturing company. The company was established in 1990 by Bobby Dekeyser.

Financial Highlights

Dedon GmbH has an annual total turnover of about Euro 40 million.

Manufacturing process

The company employed about 3,000 people in 2006 (80-90 employees in admnistration and sales, 310 in Cebu and about 3,000 all over the world). Its product range focuses on the mix of aluminium parts and synthetic fibre (the synthetic material called Hularo was developed by the company in the end of the 80’s, rattan like but weatherproof, resistant to UV light). The synthetic fibre is produced at the company’s North German headquarters in Lüneburg. The company’s furniture production plant is based on the Island of Cebu (Philippines). Each article is a one-of-a-kind piece of hand-woven hand crafted furniture.

Products

Dedon is specialised in upper end outdoor furniture and focuses increasingly also the indoor market. This is due to the development of the lifestyles and that outdoor design is being increasingly adapted for indoor use and indoor furniture increasingly made of material adapted for outdoor use. Products manufactured include dining, low seating, modular, bench chair, signature pieces, accessories and fabrics.

In 2007 production of accessories has been increasing and is planned to further increase in 2008. According to Dedon the accessory offer is getting increasingly important for the marketing of the production.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

28

Draenert Studio GmbH Germany

HEADQUARTERS Draenert Studio GmbH Steigwiesen 3 88090 Immenstaad am Bodensee Germany

Tel. +49 7545 2080 Fax +49 7545 20810 www.draenert.de e-mail: [email protected]

CONTROLLED COMPANIES, SUBSIDIARIES, OTHER RELATED COMPANIES Draenert Swiss AG

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized:100% FURNITURE PRODUCT SPECIALISATION Contract, Tables-chairs, Upholstery, Occasional

YEAR OF ESTABLISHMENT 1968 EMPLOYEES 60 TURNOVER EUR 12.5 million

TOTAL EXPORT EUR 4.1 million % EXPORT ON TOTAL TURNOVER 33 DESTINATION 30 countries

OTHER INFO The company is specialised in the production of dining and coffee tables with patented extension-mechanisms, as well as chairs matching in form and style. The brand is representative since four decades for art and designer furniture, traditional craftsmanship, quality and first-class workmanship. Due to the big sales of chairs, the exclusive upholstery factory DRAENERT SWISS AG was founded inSwitzerland. The future strategy lies in the development, as well as production of full programmes in the seatingfurniture area. In addition, the company is known as stone specialist with a huge stone collection. The cooperation with well-known designers like Werner Aisslinger and Prof. Wulf Schneider gave DRAENERT several awards up to the red dot "Best of the best". In the autumn 2007, it was opened a cooperation withPoggenpohl: the trend of joining kitchen and living/dining area is taken account of by the so-called Dining Desk.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

29

Elastoform Germany

HEADQUARTERS Elastoform Polstermöbel GmbH & Co Postfach 14 12 40 47228 Duisburg/Rheinhausen Germany

Tel. +49 2065 6990 Fax +49 2065 699109 www.elastoform.de e-mail: [email protected]

BRANDS, TRADEMARKS Formart, Teleform, Ergoform, Wohnform, Multiform, Cosyform, Pure

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION 100% Upholstery

YEAR OF ESTABLISHMENT 1919 EMPLOYEES 700 TURNOVER EUR 90 million

MANUFACTURING PLANTS n.a. SQM 75,000 LOCATION n.a.

TOTAL EXPORT EUR 17.7 million % EXPORT ON TOTAL TURNOVER 19.6 DESTINATION Main export markets are the Netherlands and France

DISTRIBUTION CHANNELS Elastoform sells its products throughout Buying Groups and through independent specialists and upholstery specialist retailers. The company operates a permanent exhibition of its complete product range on a 4,200 square metre showroom.

History

Elastoform Polstermöbel GmbH & Co, based in Duisburg/Rheinhausen, Germany, is a manufacturing company.

The company was established in 1919 by Gerhard Brinkel.

Financial Highlights

In 2007 Elastoform recorded a total turnover of Euro 90 million of which 19.6% came from exports. Main export markets are the Netherlands and France.

Manufacturing process

Today the company counts around 700 employees, producing several hundred pieces of furniture daily in a 75,000 square metres production plant.

Products

The company offers 125 different models, each available in a wide range of fabrics and leathers. Leather coverings represent 80% of total company sales. Motion upholstery represents about 40% of total production.

The company offers eight different lines:

- Wohnform includes upholstered furniture. Familiar, classical shapes are the hallmark of this line of armchairs, two- and three-seater sofas, and corner combinations.

- Multiform integrated chaises-lounges, beds and bedding boxes, sofas and variable corner and side units.

- Teleform TV recliners have a range of sophisticated technical features.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

30

- Formart is a programme of sophisticated upholstered furniture in modern styles.

- Formart relax is the offer of recliners.

- Cosy sofas.

- Cosyform seats have integrated foot parts.

- Pure is the luxurious line.

Distribution channels

Elastoform sells its products throughout Buying Groups and through independent specialists and upholstery specialist retailers. The company operates a permanent exhibition of its complete product range on a 4,200 square metre showroom.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

31

EMCO Bad GmbH & Co KG Germany

HEADQUARTERS EMCO Bad GmbH & Co KG Breslauer Straße 34-38 49803 Lingen (Ems) Germany

Tel. +49 591 9140194 Fax +49 591 9140812 www.emco-bad.de

ACTIVITY Manufacturer

MAIN PRODUCTION FURNITURE PRODUCT SPECIALISATION Bathroom OTHER PRODUCTION Bathroom accessories, mirrors, lamps

THE COMPANY IS PART OF Erwin Müller Gruppe Lingen

YEAR OF ESTABLISHMENT 1952 EMPLOYEES n.a. TURNOVER EUR n.a.

CERTIFICATION ISO En 9001

OTHER INFO Emco bad has been operating for 50 years as a manufacturer of design-orientated bathroom furnishings. The product range includes bathroom accessories such as paper, glass and towel holders, mirrors, lamps andluminaires as well as high-quality bathroom furniture. Emco Bad belongs to the Lingen-based group of companies Erwin Müller. The Erwin Müller Group is a holding that unites five strong brands under one roof: NOVUS (staplers, perforators,desktop accessoires and tools for both the DIY and the professional trade) and the three Emco subsidiaries, Emco Bau (products for residential and commercial entrance areas), Emco Klima (products for air conditioning, heating and ventilation technology) and Emco Bad, as well as the Dahle company (guillotines, trimmers, heavy duty cutters, scissors and cutting accessoires...) in Coburg. With five distribution companies abroad, three foreign subsidiaries in China, the Czech Republic and France, with majority holdings domestically, over 900employees, 590 of these (including 30 trainees) in Lingen and annual turnover in excess of Euro 100 million, the Erwin Müller Group is one of the world's leading companies on the market.

Gwinner GmbH & Co KG Germany

HEADQUARTERS Gwinner GmbH & Co KG Postfach 1149 72281 Pfalzgrafenweiler Germany

Tel. +49 7445 1830 Fax +49 7445 183199 www.gwinner.de e-mail: [email protected]

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized:100% FURNITURE PRODUCT

SPECIALISATION Wood veneer furniture Office, Dining-living room (specialised in wall units and modular construction systems for the home sector and in furnishings for management and executive offices)

YEAR OF ESTABLISHMENT 1930 EMPLOYEES 184 TURNOVER EUR 24.5 million

MANUFACTURING PLANTS 3 SQM 20,000 LOCATION n.a.

CERTIFICATION ISO 9001

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

32

HABA Habermaaß GmbH Germany

HEADQUARTERS HABA Habermaaß GmbH Postfach 1107 96476 Bad Rodach Germany

Tel. +49 9564 929100 Fax +49 9564 3513 www.haba.de e-mail: [email protected]

CONTROLLED COMPANIES, SUBSIDIARIES, OTHER RELATED COMPANIES JAKO-O, Wehrfritz GmbH

ACTIVITY Manufacturer and Retailer

MAIN PRODUCTION Not Furniture Specialized FURNITURE PRODUCT SPECIALISATION Children furniture OTHER PRODUCTION Toys, games, jewelry, porcelain dishes and textiles

THE COMPANY IS PART OF HABA Corporate Family (Turnover: Euro 230 mn, 1,500 employees)

YEAR OF ESTABLISHMENT 1938 EMPLOYEES n.a. TURNOVER EUR 75 million

CERTIFICATION ISO 9001, ISO 14001

OUTPUT Small parts production of wooden articles focusing on toys, approx. 40,000 active basic parts. Furniture production with about 30,000 active basic parts, 50,000 cupboards, 75,000 chairs, 15,000 tables. Outdoor play equipment with 1,500 units.

DISTRIBUTION CHANNELS Three distribution channels: specialized trade, institutions, catalog mail order. Under the HABA brand names the complete range of products are distributed to some 6,000 specialized dealers and social institutions all over the world. Besides the branches in France and the USA, HABA has its own agencies in 20 other countries, including Switzerland, Japan, Italy, Korea, Russia and Slovenia.

OTHER INFO Members of the HABA Corporate Family are: - HABA, a wood manufacturing company of high-quality baby and children's toys, as well as children's games

and furniture. The company is expanding the product portfolio beyond wood products, thus, offering also jewelry, porcelain dishes and textiles.

- JAKO-O, the mail order firm, set up in 1978, offering toys, clothing and other Haba products. - Wehrfritz, a single-source supplier for furnishing social care facilities.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

33

Häcker Küchen Germany

HEADQUARTERS Häcker Küchen GmbH & Co KG Werkstrasse 3 32289 Rödinghausen Germany

Tel. +49 5746 9400 Fax +49 5746 940301 www.haecker-kuechen.de e-mail: [email protected]

BRANDS, TRADEMARKS Systemat, Classic

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION Kitchen

YEAR OF ESTABLISHMENT 1938 EMPLOYEES 800 TURNOVER EUR 259 million

MANUFACTURING PLANTS n.a. SQM 191,000 LOCATION n.a.

CERTIFICATION ISO 9001

TOTAL EXPORT EUR 121.7 million % EXPORT ON TOTAL TURNOVER 47 DESTINATION Switzerland, UK, Netherlands

DISTRIBUTION CHANNELS Häcker-Küchen furniture is exclusively distributed through specialist kitchen retailers and furniture retailers with a kitchen department. The company works with a total of 2,500 trading partners in 37 countries in the kitchen tradeand with furniture stores that have specialist departments.

History

Häcker Küchen, based in Rödinghausen, Germany, is a manufacturing company.

The company was established in 1938 by Friedrich Häcker as a joinery and in 1972 the company transformed from a workshop to an industrial manufacturer.

Financial Highlights

In 2007 Häcker Küchen recorded a total turnover of Euro 259 million (+5.3% on 2006).

Furniture sales on the domestic market were Euro 137.3 million (-3.8% on 2006). The export share rose from 33% in 2003 to 47% in 2007. The most dynamic markets for Häcker-Küchen are the Netherlands, the UK, Belgium, France, Switzerland and Austria.

Manufacturing process

The company covers an area of 191,000 sqm of which 106,000 sqm of production area and 16,000 sqm of administration area.

The company employed 800 people in 2007, working in three factories.

Products

The company, specialized in the production of kitchen furniture, offers two line of kitchen: Classic and Systemat. Systemat is the high quality and ergonomic kitchen with a sophisticated design.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

34

Häcker-Küchen operates in the middle price range.

Distribution channels Häcker-Küchen furniture is exclusively distributed through specialist kitchen retailers and furniture retailers with a kitchen department. The company works with a total of 2,500 trading partners in 37 countries in the kitchen trade and with furniture stores that have specialist departments.

The furniture industry in Germany

10/09/2008 R2413.DE

© Copyright CSIL This report is exclusively for consultation on the part of the purchaser. It may not be reproduced in whole or in part by any means whatsoever without the prior written permission of CSIL

35

Haworth GmbH Germany

HEADQUARTERS Haworth GmbH Von-Achenbach-Straße 21-23 59229 Ahlen Germany

Tel. +49 2382 7810 ; 781117 Fax +49 2382 781182 www.haworth.de

BRANDS, TRADEMARKS Art.collection, Comforto, Dyes, Röder and Nestler

ACTIVITY Manufacturer

MAIN PRODUCTION Furniture Specialized: 100% FURNITURE PRODUCT SPECIALISATION 100% Office

THE COMPANY IS PART OF Haworth (Haworth Europe’s turnover: Euro 298 mn; employees: 2,031)

YEAR OF ESTABLISHMENT n.a. EMPLOYEES n.a. TURNOVER EUR 67.5 million