the end of the beginning - cbre

TRANSCRIPT

The End of the BeginningN O R T H A M E R I C A F L E X I B L E O F F I C E M A R K E T I N 2 0 2 0

The flexible office industry is withstanding its greatest challenge and adapting to meet new office requirements.

Flexible office space is no longer seen as a niche sector but as a strategic solution for a broad range of companies. As this shift begins to unfold, certain structural changes in the way flexibility is being delivered to the market are underway. Strong players and alliances between flexible office operators and building

owners are emerging, new markets are being explored and new business models are being developed to engage office users. The upheaval that has defined 2020 will lead to the evolution of the flexible office industry to a more mature state in the years to come.

2 North America Flexible Office Market in 2020

Figure 1: Total Flexible Office Inventory (U.S. & Canada)

100

60

20

80

40

0

90

50

10

70

30

Downtown SuburbanInventory (MSF)

H1 2010 H1 2014H1 2012 H1 2016 H1 2019H1 2011 H1 2015 H1 2018H1 2013 H1 2017 H1 2020

Source: CBRE Research, Q2 2020.Note: CBRE tracks flexible office space in 49 markets (U.S. & Canada).

3© 2020 CBRE, Inc.

Executive Summary

Positive Demand OutlookLike the overall office market, demand for flexible office space has been challenged in the near term. The long-term outlook is positive when tenants return to the workplace.

Moderating GrowthAnnual supply growth of flexible office space slowed to just 7% for the year ending in Q2 2020. Rightsizing efforts are ongoing. However, in the first half of 2020, only 1% of flex space was closed from an operational standpoint.

Acceleration of Partnerships Landlords and flex providers are working together in a more transparent way this year to support their viability during the COVID-induced market downturn. These relationships are increasingly moving toward partnership agreements and away from traditional lease structures.

4 North America Flexible Office Market in 2020

Mainstream AdoptionOccupier sentiment toward agile real estate solutions is strong, as evidenced by a recent CBRE occupier survey in which 86% of respondents see flexible office space as a key component of their future real estate strategies.

Evolving ModelsFlexible office providers are evolving their business models to meet current and future demand. Interest is growing in subscription-based models that support a more distributed network of people and suite offerings to promote privacy over community.

Competition from LandlordsBuilding owners are increasingly offering their own flexible office options in the form of owner-operated space or pre-built suites, sometimes using flexible office providers to operate the space on their behalf.

5© 2020 CBRE, Inc.

Contents

08 Initial impacts of the COVID-induced recession24 Expected demand increase from enterprise tenants29 Evolution of flexible office space models38 Landlords playing a more prominent role 46 Conclusion51 Individual market profiles

6 North America Flexible Office Market in 2020

7© 2020 CBRE, Inc.

Initial impacts of the COVID-induced recession As flexible office space grew over the past decade, the biggest cause for concern was what would happen during a recession.

We now have this experience. During the recession, and with the pandemic exacerbating the operational challenges in many locations, evidence has emerged of flexible office providers’ resiliency. The following six key emerging trends are positive indicators for the future of the flexible office market environment.

8 North America Flexible Office Market in 2020

9© 2020 CBRE, Inc.

1/ Strong Activity PipelineIn the short-term, flexible office membership has been negatively impacted as individuals revert to work-from-home options. But activity pipelines, especially from enterprise tenants, give reason for optimism.

Demand for flexible office space has fallen off this year as more people work remotely and are reluctant to return to office settings due to health concerns. However, the pipeline for future leasing activity is encouraging, especially from enterprise tenants—traditional corporate office users as opposed to just startup companies and entrepreneurs.

Inquiries, occupancy and membership all fell significantly for flexible office providers in the months following the first round of pandemic lockdowns. Initially, it was government restrictions that hampered access to the physical space. Since those restrictions have eased, the reluctance of individuals to return until the pandemic is under control has prolonged the challenges.

As with the overall real estate recovery efforts, not all markets and submarkets perform equally. Suburban locations have fared better than urban ones. For example, monthly key swipes in suburban office buildings are averaging 33% vs. 12% in Manhattan office buildings, although both are increasing.

Inquiry levels for flexible office space have recently ticked up. There is anecdotal evidence of workers who don’t yet have access to company offices using flex locations for distraction-free workspace away from their homes. Additionally, enterprise tenants are exploring new ways to fulfill their space requirements in an uncertain environment. As a result, flexible office leasing is expected to increase next year once COVID transmission moderates.

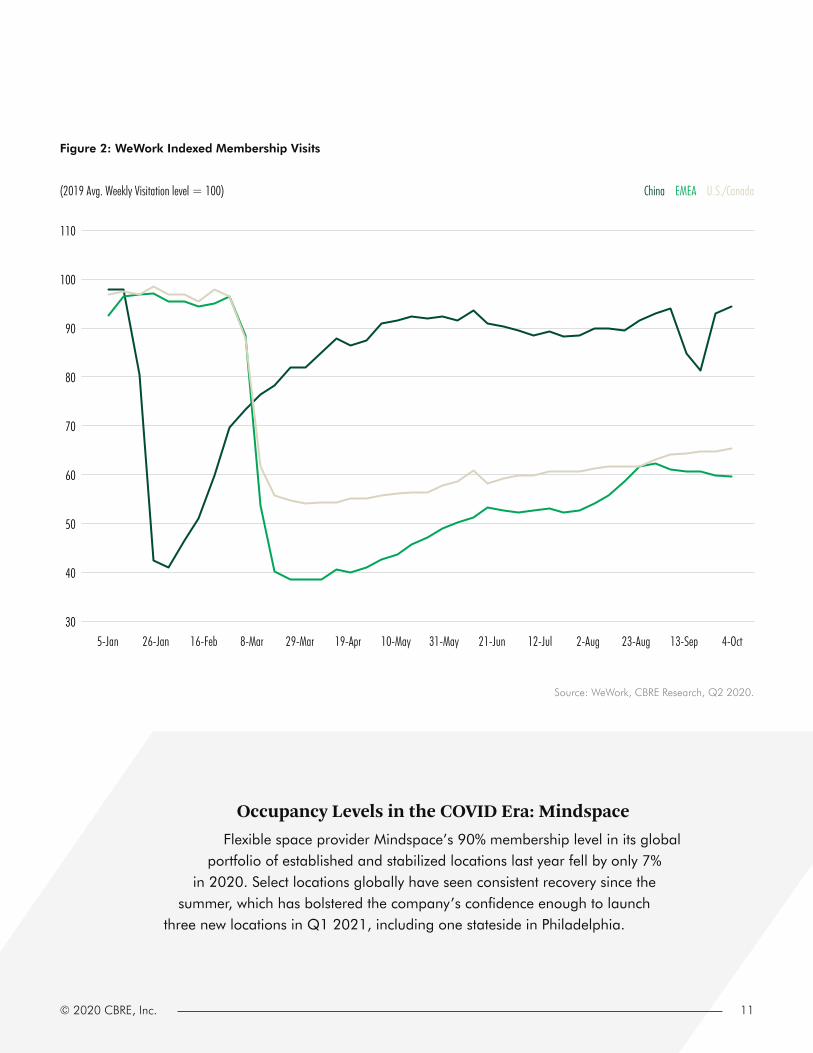

China provides an example of what the future may hold for the U.S. flex office market. Major flex provider WeWork had consistently falling membership visits in China until the pandemic was controlled there. Since then, WeWork’s Chinese member visits have increased. Flex office membership visits in North America and EMEA remain substantially lower than they were before the pandemic, but both have improved over the past few months and will continue to improve as the pandemic is controlled.

10 North America Flexible Office Market in 2020

Figure 2: WeWork Indexed Membership Visits

110

60

80

40

30

90

100

50

70

China EMEA U.S./Canada(2019 Avg. Weekly Visitation level = 100)

5-Jan 29-Mar16-Feb 10-May 12-Jul 13-Sep26-Jan 19-Apr 21-Jun 23-Aug8-Mar 31-May 2-Aug 4-Oct

Source: WeWork, CBRE Research, Q2 2020.

Occupancy Levels in the COVID Era: MindspaceFlexible space provider Mindspace’s 90% membership level in its global

portfolio of established and stabilized locations last year fell by only 7% in 2020. Select locations globally have seen consistent recovery since the

summer, which has bolstered the company’s confidence enough to launch three new locations in Q1 2021, including one stateside in Philadelphia.

11© 2020 CBRE, Inc.

12 North America Flexible Office Market in 2020

2/ Pent-up Demand BuildingEnterprise tenants are executing short-term lease renewals and space reductions as future headcount requirements remain uncertain. When demand picks up, flexible office space is expected to be a key component of new requirements.

In a recessionary environment, tenant behavior becomes more cautious, especially one like today where the dependence on office is being challenged. Overall office metrics to date are highlighting the uncertainty in the market. Leasing activity fell by 45% year-over-year and the share of renewals increased significantly in Q2 2020. The overall term of space renewals was 8.2% less than a year ago. Additionally, many tenants placed their excess space on the sublease market. All this signals that occupiers are lowering their traditional lease liabilities as they wait to see what the future holds.

Once tenant demand returns, flexible space will be a viable option that was not available during the recovery period of the Global Financial Crisis. The structural shift toward a more fluid workforce, which is less dependent on any one physical location, is making more agile real estate options top of mind

for occupiers today. The availability of options today along with a structural shift in tenant behavior likely will be a tailwind for flexible office space in the future.

Figure 3: Change in Key Office Metrics from Q2 2019 to Q2 2020

Decline in renewal term length since mid-2019

Increase in sublease space since March 2020

Decline in leasing since mid 2019-45.0%

-8.2%41.0%

Source: CBRE Research, Q2 2020.

13© 2020 CBRE, Inc.

3/ Greater TransparencyBuilding owners and flexible office providers are working together in a more transparent way to support their viability during the COVID-induced market downturn.

Flexible office space operators increased their leasing activity during the recent expansion cycle as rents marched higher. As such, many operators executed leases at rents near the cycle high and are now often burdened with above-market rents. Additionally, flexible office providers are struggling with lower revenues and the complexity and expense of making their environments safe to reenter amid the pandemic. Combined, this is creating a financial burden for some providers.

Some landlords offered rent abatements and deferrals in the early days of the pandemic to help their flex office tenants avoid permanent closure. But rent relief measures have since moderated as landlords focus on keeping existing tenancy amid rising vacancies and less demand. Although the flexible space market is under pressure today, many still believe in its staying power. Landlords and flex providers are now working together in a more transparent way to identify creative structures that ensure their mutual viability.

14 North America Flexible Office Market in 2020

Figure 4: Rent Cycle & Flex Office Expansion

140 8

105 -6

115 -2

95 -10

90 -12

120 0

125 2

130 4

135 6

100 -8

110 -4

Class A Rent Index (L) Y-o-Y Class A Rent Growth (R) Period of Flexible Office ExpansionClass A Rent Index (2009 = 100) Class A Rent Growth (%)

2009 20132011 2015 20182010 2014 2017 20202012 2016 2019

Source: CBRE Research, CBRE EA, Q3 2020.

15© 2020 CBRE, Inc.

4/ Partnership Agreements AcceleratingEvolved thinking is leading to variation on partnership agreements between landlords and providers that are more sustainable today and in the future.

16 North America Flexible Office Market in 2020

creating an environment where creative agreements are on the table.

Flex provider Industrious, which has not signed a lease since 2017, estimates that 75% of its portfolio will consist of landlord partnership agreements by the end of 2020. The company recently announced a deal with EQ Office for 52,000 sq. ft. in Chicago’s Willis Tower. Similarly, all of flex provider Premier Workspaces’ newly committed space in 2019 was a mix of landlord partnership arrangements. These agreements allow flex providers to engage with the marketplace in a more sustainable way and allow landlords to share in the revenue as demand begins to stabilize and grow.

Landlords are beginning to move away from traditional lease structures and toward partnership agreements with their flex office providers in which they share in profits, losses and capital expenditures. These agreements range from a simple revenue-sharing model that resembles a retail lease to a pure management fee for the provider to operate the space on behalf of the landlord. This is an acceleration of a trend that was already occurring in the market. Flex providers are finding that the traditional lease model is unsustainable, especially in the current environment, while landlords are realizing flex options will be in even more demand by tenants in the future. This convergence of enlightenment is

Figure 5: Industrious Annual Space Commitments by Type

1.6

0.8

1.2

0.4

0.0

1.4

0.6

1.0

0.2

Traditional Lease Management Agreement(MSF)

2013 20172015 20192014 20182016

Source: Industrious, H1 2020.

17© 2020 CBRE, Inc.

5/ Rightsizing Efforts UnderwayAlthough some flex providers are undertaking strategic expansions, many are in the process of rightsizing their portfolios.

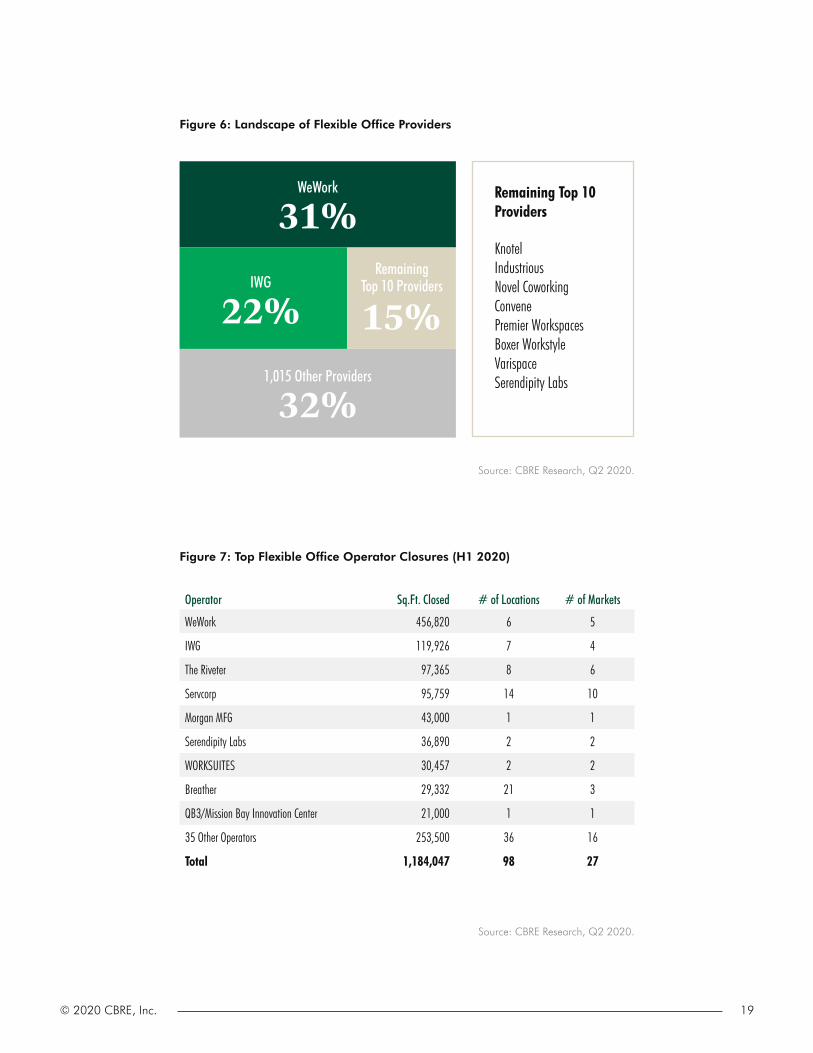

Current market conditions are making some operations unsustainable, but the industry has remained relatively resilient. The nation’s total flex office inventory was reduced by only about 1% in H1 2020, primarily by the largest flex operators in select underperforming locations. WeWork and IWG, which account for more than 50% of total U.S. flex office inventory, are both reducing their global footprints. WeWork plans to reduce its 840 global locations by about 4-5% this year. Additionally, almost 100 entities associated with IWG’s Regus and Spaces brands have filed for Chapter 11 bankruptcy this year. As a result, the company has indicated that up to 4% of its global portfolio could close.

Many of these large providers have leases structured under special purpose entities that allow them

to close individual locations without risking the remaining portfolio. Other smaller providers have been harder hit during the pandemic, such as Riveter’s cessation of business operations in May and Servcorp’s closure of half its locations in July.

In the longer-term, it is likely that more closures will occur as government assistance wanes, membership demand regulates and flexibility gets delivered in more competitive ways. Although all operators have reason for duress under the current environment, the 32% of the market made up of small local or regional players is especially important to monitor as members of this type of space may revert in the mid-term to work-from-home arrangements. Given the pandemic-led recession, the limited supply closure activity is painting quite a resilient picture.

18 North America Flexible Office Market in 2020

Figure 7: Top Flexible Office Operator Closures (H1 2020)

Operator Sq.Ft. Closed # of Locations # of Markets

WeWork 456,820 6 5

IWG 119,926 7 4

The Riveter 97,365 8 6

Servcorp 95,759 14 10

Morgan MFG 43,000 1 1

Serendipity Labs 36,890 2 2

WORKSUITES 30,457 2 2

Breather 29,332 21 3

QB3/Mission Bay Innovation Center 21,000 1 1

35 Other Operators 253,500 36 16

Total 1,184,047 98 27

Source: CBRE Research, Q2 2020.

Figure 6: Landscape of Flexible Office Providers

Source: CBRE Research, Q2 2020.

WeWork

31%

1,015 Other Providers

32%

IWG

22%Remaining

Top 10 Providers

15%

Remaining Top 10 Providers

KnotelIndustriousNovel CoworkingConvenePremier Workspaces Boxer WorkstyleVarispaceSerendipity Labs

19© 2020 CBRE, Inc.

20 North America Flexible Office Market in 2020

6/ Supply Growth SlowsExpansion by flexible office providers has slowed as they focus on sustaining operations in existing locations and increasing their strategic partnership agreements.

U.S. office market fundamentals have deteriorated from the impacts of the COVID-19 pandemic and subsequent recession. As of mid-2020, new office leasing activity was down 35% year-over-year, driven by occupier uncertainty about the future use of office space. New leasing by flexible space providers also has dropped as providers are more cautious about expanding portfolios in an uncertain environment.

Flexible office supply growth slowed to 7% year-over-year in Q2 from a peak of 41% in the same period a year ago. This slowdown began after WeWork’s

unsuccessful IPO in Q3 2019 and accelerated once COVID-related government restrictions were imposed in late March. Muted supply growth is a positive indicator that, at least for now, the industry is remaining resilient during this period.

Only 3% of the 8.5 million sq. ft. of gross flexible office supply added over the past year was delivered in Q2 2020. Assuming there are no additional large-scale closures, the annualized growth rate of flex office supply as of Q2 would be 1.1% as flex providers focus on profitability rather than expansion.

21© 2020 CBRE, Inc.

Figure 8: Flexible Office Supply Growth (U.S. & Canada)

H1 2011

19.3%

24.1%26.0% 25.3%

26.7%

32.1%

41.2%

7.3%

28.2% 28.4%

H1 2015 H1 2018H1 2013 H1 2017 H1 2020H1 2012 H1 2016 H1 2019H1 2014

Note: Represents annualized growth. Source: CBRE Research, Q2 2020.

45%

25%

35%

15%

5%

40%

20%

30%

10%

0%

22 North America Flexible Office Market in 2020

Figure 9: Historical Gross Flex Office Space Additions

Q2 2018

3.2 MSF

5.8 MSF 5.8 MSF

4.9 MSF

6.4 MSF

6.8 MSF

Q2 2019 Q1 2020Q4 2018 Q4 2019Q3 2018 Q3 2019 Q2 2020Q1 2019

Source: CBRE Research, 2020.

2.1 MSF

1.3 MSF

0.2 MSF

23© 2020 CBRE, Inc.

Expected demand increase from enterprise tenants CBRE’s September 2020 Occupier Sentiment Survey reveals that occupiers anticipate more use of flexible office space as they integrate agile strategies into their portfolio planning.

The need for agility by traditional enterprise tenants stems from continued economic uncertainty and new workforce behaviors. COVID-19 has accelerated many trends, the most transformational of which may be employee work patterns. Choice, mobility and autonomy are words that describe workstyles in the future. As the role of the office evolves, so too will its design, location and utilization. Flexible office space is poised to play a significant role in this evolution as it allows enterprise occupiers to better balance supply and demand in the future. The reasons for engaging with flex space are also evolving from ones that were focused on simply exploring the concept to ones that are more sophisticated, indicating that a more programmatic approach to using flex in real estate planning is underway.

24 North America Flexible Office Market in 2020

25© 2020 CBRE, Inc.

“Companies are planning to experiment much more broadly with using workplace-as-a-service in 2021. The question is: How will they feel about the outcome of that experiment? If companies feel they get an adequate workplace outcome, flex will continue to grow at a healthy clip. But if they feel the outcome was not just adequate, but better than traditional modes of occupancy, it will transform commercial real estate faster than anyone expects.”

O N W O R K P L A C E A S A S E R V I C E

JAMIE HODARICEO, INDUSTRIOUS

26 North America Flexible Office Market in 2020

Figure 10: What role will flexible office play in your long-term real estate strategy?

Source: 2020 Global Occupier Sentiment Survey, CBRE Research, September 2020.

Significant role Significant role

Some kind of role Some kind of role73%23%

86%36%

JUNE SEPTEMBER

Figure 11: Main reasons for use of a flexible office space

Source: 2020 Global Occupier Sentiment Survey, CBRE Research, September 2020.

Provide a network of locations for more mobile workforce access

Test of alternate workspace or occupancy models

Short-term space solution for temporary dispersed workforce

Access new services or amenities

Enter a new market(s)

Swing space while leased space is under construction

Reduce capital expenditure

Access more modern workplace design

Other

45.5%

43.9%

42.4%

40.9%

37.9%

25.8%

9.1%

7.6%

6.1%

27© 2020 CBRE, Inc.

28 North America Flexible Office Market in 2020

Evolution of flexible office models Many flexible office providers are evolving their models and diversifying their products to meet new demands on an individual, local, regional, national and even global scale. CBRE has identified the following three key strategies to attract new occupiers.

“With real estate and workplace choices now in the hands of individual employees, commercial real estate planning becomes

increasingly difficult. Flexible office solutions allow for a faster and more

efficient matching process between varying employees needs and space.”

CHRISTELLE BRONAMERICAS AGILE PRACTICE LEADER

CBRE

29© 2020 CBRE, Inc.

1/ On-Demand & Subscription-based Membership StructuresMany regional and national flex office providers are offering on-demand “pay-by-use” memberships or subscription-based services.

Examples include WeWork’s All-Access plan, Oasis by Industrious and IWG’s mobility program that offer their members access to the full network of locations in an efficient cost-effective way. These are highly configurable models that allow providers to

flex their supply of real estate with real-time demand and manage it using technology-driven apps and dashboards. This emerging model gives providers more flexibility as workers return to the office.

30 North America Flexible Office Market in 2020

31© 2020 CBRE, Inc.

Long-Term Distributed Workforce: The trend toward a more distributed workforce is placing less dependence on centralized hubs and more reliance on a larger network of spaces to get work done. While urban-core locations still play an important role, they will be only part of a larger ecosystem of locations. Flexible office space will be one component of this ecosystem and will offer a ready-made network of locations from which employees can work and seamlessly access through mobile technology. While not all categories of employees may benefit from this, those that have more mobile profiles could achieve productivity gains from accessing this type of space structure depending on location.

Other concerns that these emerging membership services can help address include:

Near-Term Dedensification: As companies gradually reopen their workplaces, social distancing guidelines are restricting office capacities. Although remote working has been a viable solution for many, there are increased reports that social isolation, home distractions and imbalance between personal and professional life are affecting employee engagement. Offering a network of locations to supplement reduced office capacity can help companies prioritize employee health & well-being.

Distributed Workforce in the Real World: DropboxDropbox recently announced its plan to become a “virtual first” company,

an approach that provides the increased flexibility of working in distributed teams while maintaining meaningful access to in-person engagement.

Dropbox employees will be able to work from anywhere, including a network of leased Dropbox offices, flex office suites, private offices and

meeting & training rooms on demand. The physical spaces, called Dropbox Studios, will be hubs to spark creativity, build community and maintain

company culture. However, these workplaces will not be used for daily individual work.

By balancing the flexibility and freedom of remote work while also retaining in-person engagement, Dropbox hopes it will gain the best of both worlds

and see clear long-term benefits.

32 North America Flexible Office Market in 2020

preferred suburban locations in the past, in recent years it has expanded heavily in downtown areas, mostly through its Spaces brand. Likewise, WeWork primarily located in downtown locations expanding to suburban locations beginning in 2017. Knotel has recently announced plans for space in select suburban locations in New York and San Francisco.

The good news for occupiers is that there are options from providers of all types in all kinds of locations. Even among the 10 largest operators, while there is a clear preference to be in Class A space, many also have suburban locations. IWG, the second largest flexible office operator, is almost equally weighted between downtown and suburban locations. While IWG (best known for its Regus brand) has

Figure 12: Largest Flexible Office Operators Composition

Convene

WeWork

KnotelNovel Coworking

Boxer Workstyle Executive Suites

Premier WorkspacesVarispace

IWGSerendipity Labs

Industrious

Class A Class B/C

Subu

rban

Down

town

Source: CBRE Research, Q2 2020.

33© 2020 CBRE, Inc.

2/ Integrated Enterprise Solutions Some flexible office providers are bundling all the elements of real estate planning and execution in one place to make the process more efficient and effective.

This reduces capital outlay for occupiers and allows them to capitalize on efficiencies of scale from flex providers. This solution is typically best for larger teams that have a mid-term requirement for a single-market location, privacy and potentially some level of customization to reflect branding. These requirements can be met through tailored workspace services such as Geometry (Knotel), Canvas (Industrious), Spaces

(IWG), Teams (Hana) and Headquarters (WeWork). Occupiers may be interested in this strategy as they look to open individual offices in a more efficient way. The number of leases of less than 75,000 sq. ft. have been declining and are at historically low levels, signaling a desire for this size space requirement to be satisfied in other ways once demand returns.

34 North America Flexible Office Market in 2020

Integrating Flexible Solutions in Overall Strategy:

The Lily Pad ApproachA fast-growing San Francisco Bay Area tech company was finding it

difficult to develop a long-term real estate strategy and stick to it. It ultimately adopted what CBRE terms the “lily pad approach,” which

incorporates flexible office space to support hyper-growth until sufficient scale is reached to justify a long-term lease. In line with the tech industry

philosophy of “build fast, fail fast,” the lily pad approach allowed this occupier to enter new markets quickly and tap into new talent pools.

By using this type of standardized and programmatic approach to integrating flexible solutions into its portfolio, this company has

maintained an agile and stable growth strategy.

35© 2020 CBRE, Inc.

3/ Private Suite OfferingsMany flexible office providers are offering more private suite solutions vs. pure coworking space to enterprise tenants that desire privacy and security over community.

As with integrated enterprise solutions, this reduces capital outlay and allows occupiers to capitalize on efficiencies of scale and to access shared conference, lobby and social spaces. Although customization is limited, terms are more flexible and the ability to flex space requirements is more easily attained as this type of space is usually easy to reconfigure.

36 North America Flexible Office Market in 2020

37© 2020 CBRE, Inc.

Landlords playing a more prominent roleOffice occupiers are increasingly considering flexible space solutions as part of their long-term real estate strategies.

Landlords are responding with their own flex offerings, ranging from on-demand coworking options to turnkey solutions. These offerings are becoming part of an integrated suite of solutions that progressive landlords are building into their portfolios to engage and attract tenants. This is challenging the precedent of the last decade where flexible space options were delivered by third-party providers often under scrutiny by the landlords that engaged with them.

38 North America Flexible Office Market in 2020

39© 2020 CBRE, Inc.

Figure 13: What are the most desired building attributes by tenants in the future?

Source: 2020 Global Occupier Sentiment Survey, CBRE Research, September 2020.

Flexible office space options

Sustainable building design

Indoor air quality

Onsite café food and beverage

Shared meeting space

Touchless technologies

Connected technologies/Building apps

Public transportation access

Fitness facilities

Outdoor amenities

Concierge services

82.0%

74.0%

68.0%

62.0%

52.0%

51.0%

48.0%

33.0%

27.0%

22.0%

18.0%

40 North America Flexible Office Market in 2020

Although speculative office suites are often offered for shorter traditional lease terms, they satisfy the speed to market and capital expense savings that many occupiers desire. Manhattan, the birthplace of coworking and the most prominent flexible space market, offers a good example of what the future may hold for this product type. Spec suite growth in Manhattan has hovered around 90% to 100%

annually over the past few years and nearly 90 building owners now offer a combined total of more than 300 spec suite spaces. Amid the COVID-19 pandemic, only 48% of this square footage is currently occupied. As companies begin to develop business plans for 2021, spec suites could offer many of them a ready-made alternative to renewing in place with traditional space.

Figure 14: Manhattan Spec Suite Footprint

3.0

1.0

2.0

0.0

2.5

0.5

1.5

Total Spec Suite Footprint New Spec Suite Listing(MSF)

2014 201820162015 20192017 2020*

*Represents 2020 through Q2.Source: CBRE Research, Q2 2020.

2.57

1.33

0.68

0.310.230.120.06

41© 2020 CBRE, Inc.

THAIS GALLIMANAGING DIRECTOR, INNOVATION

TISHMAN SPEYER (STUDIO)

“Tishman Speyer is driven by the goal to offer best-in-class spaces, services and experiences to our customers, independently of what their needs are. For that reason, we believe that the future of the workspace will be more flexible and with greater focus on the workspace experience, something that cannot be replicated at home, which has driven us to be the first landlord to launch its own global flex platform.”

42 North America Flexible Office Market in 2020

A Traditional Owner’s Commitment to Flex

Tishman Speyer was one of the first traditional office owners to offer coworking and private office space when it launched its Studio brand in

2018. Studio now operates 500,000 sq. ft. of flexible office space in 10 Tishman Speyer buildings across seven markets.

Even amid the COVID pandemic, Tishman Speyer plans to open an additional 700,000 sq. ft. of flexible space over the next two years in the

U.S., Brazil and Western Europe. The company estimates that as much as 20% of its overall portfolio could be flexible in nature over the next

10 years. This would entail not only retail coworking space and private offices, but also more flexible terms for traditional occupiers.

43© 2020 CBRE, Inc.

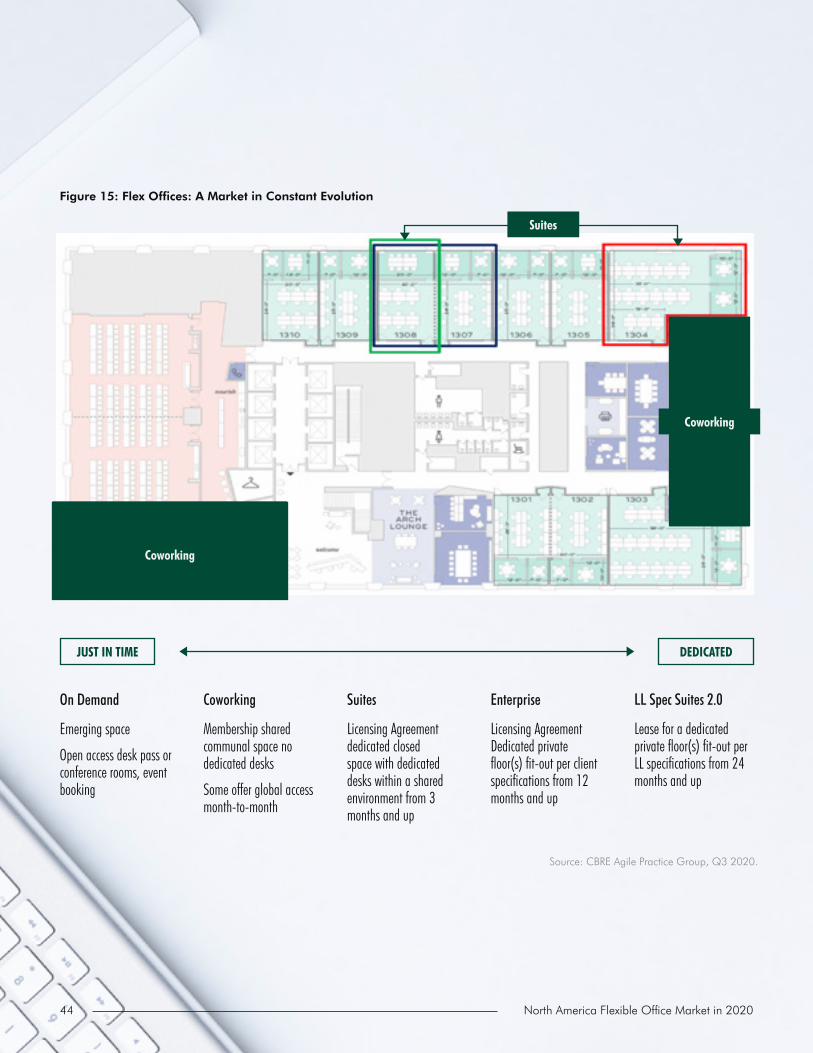

Figure 15: Flex Offices: A Market in Constant Evolution

Source: CBRE Agile Practice Group, Q3 2020.

Coworking

Coworking

Suites

JUST IN TIME DEDICATED

On Demand

Emerging space

Open access desk pass or conference rooms, event booking

Coworking

Membership shared communal space no dedicated desks

Some offer global access month-to-month

Suites

Licensing Agreement dedicated closed space with dedicated desks within a shared environment from 3 months and up

Enterprise

Licensing Agreement Dedicated private floor(s) fit-out per client specifications from 12 months and up

LL Spec Suites 2.0

Lease for a dedicated private floor(s) fit-out per LL specifications from 24 months and up

44 North America Flexible Office Market in 2020

45© 2020 CBRE, Inc.

ConclusionThe flexible office industry is facing the dual challenge of a recession and a pandemic that is hindering use of its product.

Even in the face of these obstacles, industry leaders remain optimistic about the viability of flex solutions for enterprise office occupiers. Flexible space ultimately will become an integral part of office buildings and a sought-after solution for the enterprise tenants that occupy them. Following are the biggest trends that will drive change in the flexible office landscape next year:

46 North America Flexible Office Market in 2020

47© 2020 CBRE, Inc.

1. “Consumerization,” fueled by a rise in digital real estate: 2021 will mark a new era in which employee or “consumer” wants or preferences influence office requirements. One of the ways consumers will impact real estate decisions is by using consumer-oriented digital real estate tools like concierge apps that connect employees to amenities and communities.

2. Occupiers adopting Core + Flex models: Post- pandemic, companies will place increased value on flexibility in their real estate portfolios. As a result, companies will seek to bring employees back to the office while avoiding large capital commitments. They also will look for ways to create more flexibility within their long-term commitments, including mixing conventional and flex leases within the same building.

3. The rise of management agreements and revenue-sharing structures: The global pandemic’s pervasive and unpredictable impact highlights the value of flexible space as an asset class. As a result, flex providers and landlords will increasingly coalesce around capital-light deal structures with landlords, including management agreements, that offer higher returns for owners with limited capital commitment from operators.

4. Hybrid models driven by cost savings: Global occupiers will increasingly realize that incorporating flexible space in their real estate portfolios can result in significant cost savings. Their focus will shift to finding the right balance of agile and long-term commitments to cut costs while maximizing productivity. This will give rise to a new, dominant hybrid workforce model that includes concepts such as hub-and-spoke, on-demand coworking and project offices.

5. An emphasis on health, safety and community: Flex operators have adopted a range of best practices to mitigate COVID and promote well-being in their facilities. They will continue to focus on both virtual and in-person community events that foster collaboration and set them apart from other office providers.

6. The expansion of flex space into more asset types: Coworking and shared-office concepts will become more prevalent in diverse asset types, such as industrial, labs, studios and retail. Emerging players like Saltbox, Peerspace, Ghost Kitchens and others are early manifestations of this trend.

The flexible office industry’s many challenges this year are giving way to opportunities in 2021. The way in which occupiers use flexible space continues to evolve and will be the impetus for demand over the long-term. The industry is now at the “end of the beginning” and its future looks bright.

48 North America Flexible Office Market in 2020

Figure 16: The Office of the Future

Source: CBRE Research, Q3 2020.

ROOF TERRACE/EVENT SPACE BAR/RESTAURANT

ACTIVATED COMMUNITY AREAS/EVENT SPACES

SHARED FOOD HALL/CONFERENCE AUDITORIUM

CONCIERGE/BIKE STORAGE/GYM & LEISURE FACILITIES

FITTED/SPEC SUITES

CONVENTIONAL FLOORS WITH LONG TERM LEASES

SPACE AS A SERVICE

49© 2020 CBRE, Inc.

50 North America Flexible Office Market in 2020

Individual market profilesATLANTA

LAS VEGAS

PHILADELPHIA

CALGARY

MIAMI

RALEIGH-DURHAM

DETROIT

NORTHERN VIRGINIA

SAN FRANCISCO

TAMPA

WALNUT CREEK/I-680 CORRIDOR

BALTIMORE

MADISON, WI

PITTSBURGH

DALLAS/FT. WORTH

NASHVILLE

SAN ANTONIO

ST. LOUIS

CHICAGO

MINNEAPOLIS/ST. PAUL

SACRAMENTO

SEATTLE

INDIANAPOLIS

ORANGE COUNTY

AUSTIN

LOS ANGELES

PHOENIX

CHARLOTTE

MILWAUKEE

RICHMOND, VA

HOUSTON

OAKLAND

SAN FRANCISCO PENINSULA

TORONTO

WASHINGTON, D.C.

BOSTON

MANHATTAN

PORTLAND

DENVER

NEW JERSEY

SAN DIEGO

SUBURBAN MARYLAND

VANCOUVER

COLUMBUS

MONTREAL

SALT LAKE CITY

SILICON VALLEY

KANSAS CITY

ORLANDO

51© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

3,000,000 100

2,500,000 80

90

2,000,00060

70

1,500,000

40

50

1,000,000

20

30

500,00010

0 0

(%)

2.5

2.0

1.5

1.0

0.5

0.0

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassSpaces 29,000 Q4 2019 Buckhead A

Total Top Five 29,000

Total Sq. Ft. New Transactions Y-o-Y 29,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 652,543 0.0% 25.2% 14 Midtown

Regus 610,313 -11.6% 23.6% 32 North Fulton

Spaces 328,187 9.7% 12.7% 8 Cumberland/Galleria

Industrious 198,635 0.0% 7.7% 7 Midtown

Peachtree Offices 165,265 0.0% 6.4% 6 Buckhead

Total Top Five 1,954,943 75.4% 67 Top 5 as a % of Total 75.4%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsMidtown 27.7% 0.0%

Low HighSingle Office/Suite Rates $390 $670

Atlanta Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 2,591,083 -2.4%

Downtown Flex Sq. Ft. 1,447,363 -0.1%

Suburban Flex Sq. Ft. 1,143,720 -5.2%

Overall Market Penetration (%) 1.9% -0.1%

Downtown Penetration (%) 2.8% 0.0%

Suburban Penetration (%) 1.3% -0.1%

# of Operators 23 -1

# of Locations 94 -5

Avg. Size of Location Sq. Ft. 27,565

Atlanta

52 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassCommon Desk 12,000 Q4 2019 East B

Novel Coworking 10,000 Q1 2020 North B

Common Desk 8,000 Q2 2020 North B

Common Desk 4,000 Q4 2019 North B

Total Top Five 34,000

Total Sq. Ft. New Transactions Y-o-Y 34,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 433,659 0.0% 35.3% 7 CBD

Regus 267,077 0.0% 21.7% 16 Central

Capital Factory 58,647 0.0% 4.8% 1 CBD

Spaces 53,129 0.0% 4.3% 1 CBD

Industrious 52,714 0.0% 4.3% 3 CBD

Total Top Five 865,226 70.4% 28 Top 5 as a % of Total 70.4%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsCBD 48.9% 0.0%

Low HighSingle Office/Suite Rates $370 $510

Austin Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 1,229,774 -5.4%

Downtown Flex Sq. Ft. 601,832 -4.9%

Suburban Flex Sq. Ft. 627,942 -6.0%

Overall Market Penetration (%) 2.2% -0.3%

Downtown Penetration (%) 5.2% -0.3%

Suburban Penetration (%) 1.4% -0.2%

# of Operators 41 -6

# of Locations 72 -4

Avg. Size of Location (SF) 17,080

3.0

2.5

2.0

1.5

1.0

0.5

0.00

1,400,000

1,200,000

1,000,000

800,000

600,000

200,000

400,000

Austin

53© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

450,000

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

0

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0.0

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

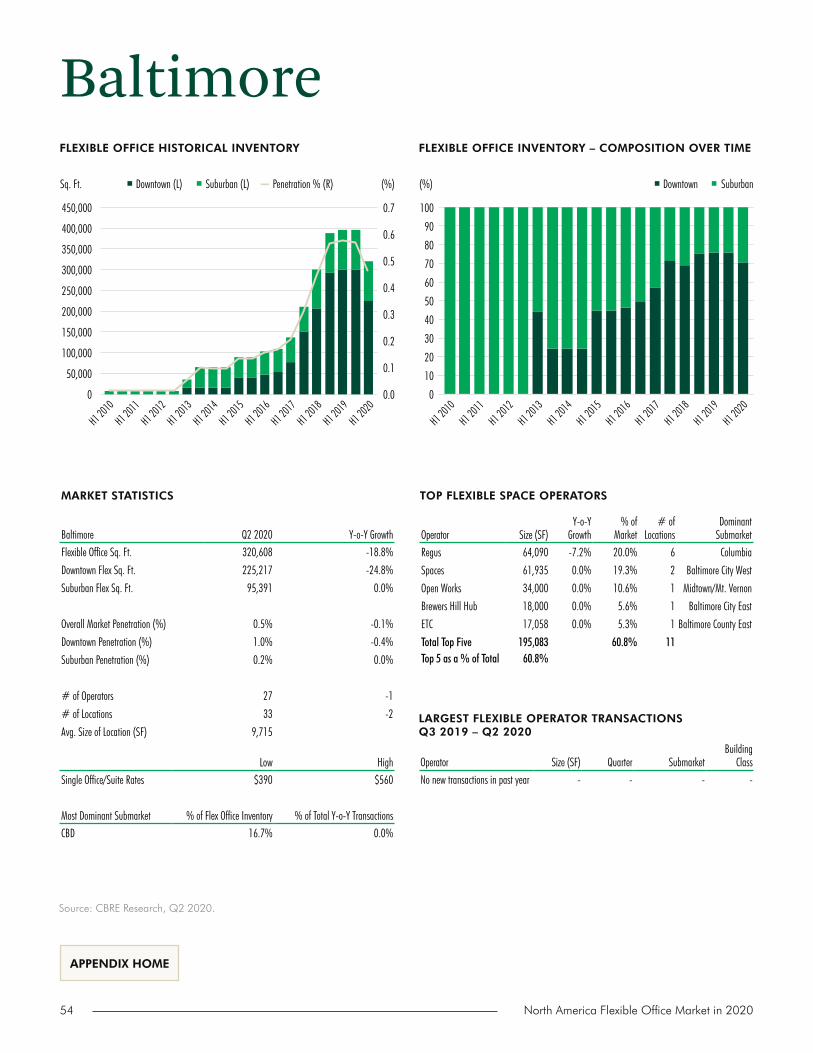

SubmarketRegus 64,090 -7.2% 20.0% 6 Columbia

Spaces 61,935 0.0% 19.3% 2 Baltimore City West

Open Works 34,000 0.0% 10.6% 1 Midtown/Mt. Vernon

Brewers Hill Hub 18,000 0.0% 5.6% 1 Baltimore City East

ETC 17,058 0.0% 5.3% 1 Baltimore County East

Total Top Five 195,083 60.8% 11 Top 5 as a % of Total 60.8%

Operator Size (SF) Quarter SubmarketBuilding

ClassNo new transactions in past year - - - -

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsCBD 16.7% 0.0%

Low HighSingle Office/Suite Rates $390 $560

Baltimore Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 320,608 -18.8%

Downtown Flex Sq. Ft. 225,217 -24.8%

Suburban Flex Sq. Ft. 95,391 0.0%

Overall Market Penetration (%) 0.5% -0.1%

Downtown Penetration (%) 1.0% -0.4%

Suburban Penetration (%) 0.2% 0.0%

# of Operators 27 -1

# of Locations 33 -2

Avg. Size of Location (SF) 9,715

Baltimore

54 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 1,649,094 9.2% 41.4% 23 CBD

CIC 348,243 0.0% 8.7% 4 East Cambridge

Regus 328,437 -9.7% 8.2% 15 CBD

Robert and Renee Belfer Office for Dana-Farber Innovations

252,255 0.0% 6.3% 1 Fenway/Kenmore Square

The Engine 224,000 0.0% 5.6% 2 East Cambridge

Total Top Five 2,802,029 70.3% 45 Top 5 as a % of Total 70.3%

Operator Size (SF) Quarter SubmarketBuilding

ClassLabCentral 101,000 Q3 2019 East Cambridge A

WeWork 100,000 Q3 2019 Back Bay B

Knotel 27,000 Q4 2019 North Station/Waterfront B

WeWork 25,000 Q4 2019 Seaport B

Knotel 14,000 Q4 2019 Back Bay B

Total Top Five 266,000

Total Sq. Ft. New Transactions Y-o-Y 286,000

Top 5 as a % of Total 93.0%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsCBD 32.1% 2.1%

Low HighSingle Office/Suite Rates $580 $795

Boston Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 3,984,326 2.7%

Downtown Flex Sq. Ft. 3,854,426 2.8%

Suburban Flex Sq. Ft. 129,900 0.0%

Overall Market Penetration (%) 1.8% 0.1%

Downtown Penetration (%) 4.0% 0.2%

Suburban Penetration (%) 0.1% 0.0%

# of Operators 46 -3

# of Locations 97 0

Avg. Size of Location (SF) 41,076

100

95

85

90

80

75

2.0

1.6

1.2

0.8

0.4

0.0

4,500,000

4,000,000

3,500,000

3,000,000

2,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

Boston

55© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassiQ Office Suites 25,000 Q4 2019 Central Core Other*

OxWorx 7,000 Q1 2020 Central Core A

Culinary Coworking 4,000 Q3 2019 Southcentral Other*

Total Top Five 36,000

Total Sq. Ft. New Transactions Y-o-Y 36,000

Top 5 as a % of Total 100.0%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsCentral Core 34.9% 89.1%

Low HighSingle Office/Suite Rates (US$) $370 $560

Calgary Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 977,091 -1.4%

Downtown Flex Sq. Ft. 553,694 4.2%

Suburban Flex Sq. Ft. 423,397 -7.8%

Overall Market Penetration (%) 1.4% 0.0%

Downtown Penetration (%) 1.3% 0.0%

Suburban Penetration (%) 1.6% -0.1%

# of Operators 30 0

# of Locations 52 -1

Avg. Size of Location (SF) 18,790

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketRegus 203,993 -7.2% 20.9% 12 Central Core

WeWork 175,000 0.0% 17.9% 2 East End

TradeSpace 75,000 0.0% 7.7% 1 Southcentral

WC Business Centres 72,000 0.0% 7.4% 2 Central Core

Stratus 61,000 -13.8% 6.2% 5 Beltline

Total Top Five 586,993 60.1% 22 Top 5 as a % of Total 60.1%

1.6

1.4

1.2

0.8

1.0

0.4

0.6

0.0

0.2

1,200,000

1,000,000

800,000

600,000

400,000

200,000

0

Calgary

*Not located in a traditional office space.

56 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

2.5

2.0

1.5

1.0

0.5

0.0

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassRegus 28,000 Q3 2019 SouthPark A

Venture X 23,000 Q1 2020 Midtown/Southend A

Serendipity Labs 23,000 Q3 2019 Midtown/Southend A

YourOffice 11,000 Q4 2019 SouthPark B

Total Top Five 85,000

Total Sq. Ft. New Transactions Y-o-Y 85,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 289,865 0.0% 33.1% 3 CBD

Regus 207,048 15.9% 23.6% 10 CBD

Hygge 75,500 0.0% 8.6% 5 North

Spaces 58,928 0.0% 6.7% 2 CBD

Venture X 47,080 93.1% 5.4% 2 I-485/South

Total Top Five 678,421 77.4% 22 Top 5 as a % of Total 77.4%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsCBD 45.5% 0.0%

Low HighSingle Office/Suite Rates $460 $590

Charlotte Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 876,744 7.6%

Downtown Flex Sq. Ft. 398,615 0.0%

Suburban Flex Sq. Ft. 478,129 14.9%

Overall Market Penetration (%) 2.0% 0.1%

Downtown Penetration (%) 2.2% -0.2%

Suburban Penetration (%) 1.8% 0.2%

# of Operators 17 0

# of Locations 36 +3

Avg. Size of Location (SF) 23,696

1,000,000

800,000

900,000

600,000

700,000

400,000

500,000

200,000

300,000

0

100,000

Charlotte

57© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Chicago

Operator Size (SF) Quarter SubmarketBuilding

ClassWeWork 110,000 Q3 2019 West Loop A

Co-Optim 100,000 Q3 2019 Northwest Suburbs B

WeWork 93,000 Q3 2019 Fulton Market/ Far West Loop A

WeWork 63,000 Q1 2020 River North A

FBRK 45,000 Q3 2019 West Loop B

Total Top Five 411,000

Total Sq. Ft. New Transactions Y-o-Y 683,000

Top 5 as a % of Total 60.2%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

Submarket

WeWork 1,177,836 15.3% 26.0% 15 Fulton Market/ Far West Loop

Regus 901,248 1.2% 19.9% 49 East-West Tollway

Convene 354,506 -17.4% 7.8% 5 West Loop

Industrious 286,126 0.0% 6.3% 8 Central Loop

Novel Coworking 271,177 0.0% 6.0% 5 West Loop

Total Top Five 2,990,893 66.1% 82 Top 5 as a % of Total 66.1%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsWest Loop 22.5% 27.0%

Low HighSingle Office/Suite Rates $490 $730

Chicago Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 4,526,869 6.4%

Downtown Flex Sq. Ft. 3,669,844 1.5%

Suburban Flex Sq. Ft. 857,025 34.4%

Overall Market Penetration (%) 1.9% 0.0%

Downtown Penetration (%) 2.7% -0.1%

Suburban Penetration (%) 0.8% 0.2%

# of Operators 45 0

# of Locations 159 +6

Avg. Size of Location (SF) 28,471

2.0

1.6

1.2

0.8

0.4

0.0

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

58 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

2.5

2.0

1.5

1.0

0.5

0.0

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassHaven Collective 6,000 Q3 2019 Downtown C

Total Top Five 6,000

Total Sq. Ft. New Transactions Y-o-Y 6,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketRegus 97,264 0.0% 12.0% 5 Easton

Rev1 Ventures 64,000 0.0% 7.9% 1 Upper Arlington

Columbus Idea Foundry 60,584 0.0% 7.5% 1 Downtown

The Point at Otterbein University 60,000 0.0% 7.4% 1 Westerville

Versa 47,000 0.0% 5.8% 2 Grandview

Total Top Five 328,848 40.5% 10 Top 5 as a % of Total 40.5%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsDowntown 44.0% 100.0%

Low HighSingle Office/Suite Rates $400 $650

Columbus Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 811,361 -1.7%

Downtown Flex Sq. Ft. 357,362 -3.8%

Suburban Flex Sq. Ft. 453,999 0.0%

Overall Market Penetration (%) 2.1% -0.1%

Downtown Penetration (%) 2.8% -0.1%

Suburban Penetration (%) 1.8% -0.1%

# of Operators 38 0

# of Locations 52 -1

Avg. Size of Location (SF) 15,603

900,000

800,000

700,000

500,000

600,000

300,000

400,000

100,000

200,000

0

Columbus

59© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

2.5

2.0

1.5

1.0

0.5

0.0

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassVarispace 380,000 Q4 2019 Mid-Cities A

WeWork 72,000 Q3 2019 Preston Center A

Spaces 53,000 Q1 2020 Far North Dallas A

WeWork 53,000 Q3 2019 Far North Dallas A

WorkLodge 31,000 Q4 2019 Stemmons Freeway Flex

Total Top Five 589,000

Total Sq. Ft. New Transactions Y-o-Y 771,000

Top 5 as a % of Total 76.4%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketRegus 816,571 -2.2% 17.1% 46 Far North Dallas

Varispace 685,000 124.6% 14.3% 2 Mid-Cities

WeWork 667,969 22.9% 14.0% 12 Far North Dallas

Boxer Workstyle Executive Suites 355,938 0.0% 7.4% 10 Dallas CBD

WORKSUITES 345,913 17.9% 7.2% 17 Central Expressway

Total Top Five 2,871,391 60.1% 87 Top 5 as a % of Total 60.1%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsFar North Dallas 24.9% 13.8%

Low HighSingle Office/Suite Rates $370 $570

Dallas/Ft. Worth Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 4,778,962 17.3%

Downtown Flex Sq. Ft. 942,673 -1.1%

Suburban Flex Sq. Ft. 3,836,289 22.9%

Overall Market Penetration (%) 2.1% 0.3%

Downtown Penetration (%) 3.5% -0.1%

Suburban Penetration (%) 1.9% 0.3%

# of Operators 50 +2

# of Locations 178 +10

Avg. Size of Location (SF) 26,848

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

Dallas/Ft. Worth

60 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassShift Workspaces 32,000 Q3 2019 Southwest A

Industrious 25,000 Q4 2019 Cherry Creek A

Thrive Workplace 22,000 Q4 2019 Southeast B

Enterprise 20,000 Q1 2020 Southeast A

Park 8,000 Q1 2020 Colorado Blvd/Midtown B

Total Top Five 107,000

Total Sq. Ft. New Transactions Y-o-Y 120,000

Top 5 as a % of Total 89.2%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 810,338 -9.6% 26.5% 12 Downtown

Regus 379,982 0.0% 12.4% 22 Southeast

Novel Coworking 343,519 0.0% 11.2% 3 Downtown

Industry 230,000 0.0% 7.5% 2 River North

Office Evolution 143,387 0.0% 4.7% 11 West Hampden/Alameda

Total Top Five 1,907,226 62.3% 50 Top 5 as a % of Total 62.3%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsDowntown 41.9% 0.0%

Low HighSingle Office/Suite Rates $390 $555

Denver Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 3,062,671 0.5%

Downtown Flex Sq. Ft. 1,283,134 0.0%

Suburban Flex Sq. Ft. 1,779,537 0.9%

Overall Market Penetration (%) 2.6% 0.0%

Downtown Penetration (%) 4.4% -0.1%

Suburban Penetration (%) 2.0% 0.0%

# of Operators 52 -1

# of Locations 121 +5

Avg. Size of Location (SF) 25,311

0 0.0

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

3.0

2.5

2.0

1.5

1.0

0.5

Denver

61© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassWeWork 91,000 Q3 2019 Detroit Downtown A

Spaces 49,000 Q4 2019 Detroit Downtown A

Venture X 22,000 Q3 2019 Detroit Downtown A

Total Top Five 162,000

Total Sq. Ft. New Transactions Y-o-Y 162,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 178,300 104.2% 27.7% 3 Detroit Downtown

Regus 147,192 0.0% 22.9% 8 Troy

Americenter 82,637 0.0% 12.9% 5 Farmington Hills/West Bloomfield

Spaces 49,056 0.0% 7.6% 1 Detroit Downtown

Venture X 21,767 0.0% 3.4% 1 Detroit Downtown

Total Top Five 478,952 74.5% 18 Top 5 as a % of Total 74.5%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsDetroit Downtown 58.4% 100.0%

Low HighSingle Office/Suite Rates $330 $440

Detroit Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 642,942 33.6%

Downtown Flex Sq. Ft. 375,567 75.7%

Suburban Flex Sq. Ft. 267,375 0.0%

Overall Market Penetration (%) 0.8% 0.2%

Downtown Penetration (%) 2.2% 1.0%

Suburban Penetration (%) 0.4% 0.0%

# of Operators 22 +2

# of Locations 35 +3

Avg. Size of Location (SF) 18,370

0.9

0.7

0.8

0.5

0.6

0.3

0.4

0.1

0.2

0.0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

Detroit

62 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassThe Cannon 120,000 Q3 2019 Energy Corridor Unknown

Spaces 63,000 Q4 2019 CBD Unknown

WeWork 56,000 Q3 2019 CBD Unknown

Spaces 52,000 Q4 2019 West Loop/Galleria A

Fuse Workspace 29,000 Q1 2020 Katy Freeway Unknown

Total Top Five 321,000

Total Sq. Ft. New Transactions Y-o-Y 417,000

Top 5 as a % of Total 77.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketRegus 717,107 -4.7% 24.9% 41 West Loop/Galleria

Boxer Workstyle Executive Suites 683,902 0.1% 23.8% 23 Clear Lake

WeWork 253,288 28.4% 8.8% 4 CBD

Spaces 201,407 134.6% 7.0% 4 CBD

The Cannon 130,000 1200.0% 4.5% 2 Energy Corridor

Total Top Five 1,985,704 69.0% 74 Top 5 as a % of Total 69.0%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsCBD 17.2% 32.7%

Low HighSingle Office/Suite Rates $430 $570

Houston Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 2,878,418 14.6%

Downtown Flex Sq. Ft. 496,029 33.7%

Suburban Flex Sq. Ft. 2,382,389 11.3%

Overall Market Penetration (%) 1.4% 0.2%

Downtown Penetration (%) 1.2% 0.3%

Suburban Penetration (%) 1.4% 0.2%

# of Operators 36 +5

# of Locations 115 +8

Avg. Size of Location (SF) 25,030

1.6

1.2

1.4

0.8

1.0

0.4

0.6

0.2

0.0

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

Houston

63© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

2.5

2.0

1.5

1.0

0.5

0.0

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassWyrk Space 12,000 Q3 2019 Speedway B

Cowork 1010 5,000 Q3 2019 College Park B

Total Top Five 17,000

Total Sq. Ft. New Transactions Y-o-Y 17,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketYeager Office Suites 179,081 0.0% 25.4% 7 Greenwood

Regus 134,744 0.0% 19.1% 7 Keystone Crossing

Cowork Indy 125,000 0.0% 17.7% 1 Downtown

Launch Fishers 51,747 0.0% 7.3% 1 Fishers/Geist

Refinery46 31,992 0.0% 4.5% 1 Midtown

Total Top Five 522,564 74.0% 17 Top 5 as a % of Total 74.0%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsDowntown 31.9% 0.0%

Low HighSingle Office/Suite Rates $420 $580

Indianapolis Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 706,115 -1.1%

Downtown Flex Sq. Ft. 234,162 -8.8%

Suburban Flex Sq. Ft. 471,953 3.3%

Overall Market Penetration (%) 1.9% -0.1%

Downtown Penetration (%) 2.0% -0.2%

Suburban Penetration (%) 1.8% 0.0%

# of Operators 24 0

# of Locations 38 -1

Avg. Size of Location (SF) 18,582

800,000

700,000

600,000

500,000

300,000

400,000

100,000

200,000

0

Indianapolis

64 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassWeWork 100,000 Q3 2019 Downtown A

Plexpod 39,000 Q2 2020 Downtown A

Industrious 37,000 Q3 2019 Plaza A

Serendipity Labs 26,000 Q4 2019 South Johnson County A

King's Cove Executive Suites 14,000 Q4 2019 North Johnson County B

Total Top Five 216,000

Total Sq. Ft. New Transactions Y-o-Y 223,000

Top 5 as a % of Total 96.9%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketPlexpod 253,926 18.1% 27.3% 5 Midtown

Regus 155,357 0.0% 16.7% 11 South Johnson County

WeWork 144,686 223.8% 15.5% 2 Downtown

iWerx 64,000 0.0% 6.9% 2 Kansas City North

Edison Spaces 43,692 0.0% 4.7% 2 South Johnson County

Total Top Five 661,661 71.0% 22 Top 5 as a % of Total 71.0%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsDowntown 34.8% 65.4%

Low HighSingle Office/Suite Rates $360 $600

Kansas City Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 931,831 30.0%

Downtown Flex Sq. Ft. 323,955 74.0%

Suburban Flex Sq. Ft. 607,876 14.6%

Overall Market Penetration (%) 1.8% 0.4%

Downtown Penetration (%) 2.6% 1.1%

Suburban Penetration (%) 1.5% 0.2%

# of Operators 19 +3

# of Locations 36 +5

Avg. Size of Location (SF) 25,884

2.0

1.6

1.2

0.8

0.4

0.0

1,000,000

800,000

600,000

400,000

200,000

0

Kansas City

65© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassNo new transactions in past year - - - -

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketRegus 246,878 0.0% 53.8% 15 West

WeWork 152,152 0.0% 33.2% 2 Airport

Premier Workspaces 36,533 0.0% 8.0% 2 Southwest

Co-Operate on Main 8,785 0.0% 1.9% 1 Downtown

Bottega Exchange 6,235 0.0% 1.4% 1 Southwest

Total Top Five 450,583 98.2% 21 Top 5 as a % of Total 98.2%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsWest 27.3% 0.0%

Low HighSingle Office/Suite Rates $420 $540

Las Vegas Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 458,734 0.0%

Downtown Flex Sq. Ft. 31,336 0.0%

Suburban Flex Sq. Ft. 427,398 0.0%

Overall Market Penetration (%) 1.3% 0.0%

Downtown Penetration (%) 1.5% 0.0%

Suburban Penetration (%) 1.2% 0.0%

# of Operators 9 0

# of Locations 25 0

Avg. Size of Location (SF) 18,349

1.4

1.2

1.0

0.6

0.8

0.2

0.4

0.0

500,000

400,000

300,000

200,000

100,000

0

Las Vegas

66 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Dowtown (L) Suburban (L) Penetration % (R) Dowtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassWeWork 135,000 Q3 2019 Hollywood/Wilshire Corridor A

Second Home Hollywood 90,000 Q3 2019 Hollywood/Wilshire Corridor A

WeWork 68,000 Q3 2019 West Los Angeles A

WeWork 60,000 Q3 2019 Tri-Cities/Glendale A

Industrious 40,000 Q4 2019 Tri-Cities/Glendale A

Total Top Five 392,000

Total Sq. Ft. New Transactions Y-o-Y 796,000

Top 5 as a % of Total 49.2%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 2,251,126 19.9% 35.0% 34 West Los Angeles

Regus 914,235 0.0% 14.2% 49 West Los Angeles

Spaces 545,825 7.7% 8.5% 12 West Los Angeles

Premier Workspaces 510,991 2.8% 7.9% 34 West Los Angeles

Barrister Executive Suites 375,500 0.0% 5.8% 24 West Los Angeles

Total Top Five 4,597,677 71.4% 153 Top 5 as a % of Total 71.4%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsWest Los Angeles 40.7% 47.9%

Low HighSingle Office/Suite Rates $450 $610

Los Angeles Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 6,437,204 10.6%

Downtown Flex Sq. Ft. 959,551 -5.1%

Suburban Flex Sq. Ft. 5,477,653 14.0%

Overall Market Penetration (%) 2.8% 0.2%

Downtown Penetration (%) 2.9% -0.2%

Suburban Penetration (%) 2.8% 0.3%

# of Operators 72 -7

# of Locations 294 +10

Avg. Size of Location (SF) 21,895

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

7,000,000

5,000,000

6,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

Los Angeles

67© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassMadison Commercial Real Estate 5,000 Q1 2020 Madison West B

AMPED Association Management 1,000 Q3 2019 Madison West B

Total Top Five 6,000

Total Sq. Ft. New Transactions Y-o-Y 6,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketNovel Coworking 95,000 0.0% 45.0% 1 Madison Central

Spaces 34,328 0.0% 16.3% 1 Madison Central

Serendipity Labs 23,172 0.0% 11.0% 1 Madison Central

Industrious 20,000 0.0% 9.5% 1 Madison Central

Regus 18,648 0.0% 8.8% 2 Madison West

Total Top Five 191,148 90.5% 6 Top 5 as a % of Total 90.5%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsMadison Central 86.8% 0.0%

Low HighSingle Office/Suite Rates $380 $510

Madison, WI Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 211,115 3.0%

Downtown Flex Sq. Ft. 183,278 0.0%

Suburban Flex Sq. Ft. 27,837 27.9%

Overall Market Penetration (%) 1.3% 0.0%

Downtown Penetration (%) 4.2% 0.0%

Suburban Penetration (%) 0.2% 0.1%

# of Operators 11 +2

# of Locations 12 +2

Avg. Size of Location (SF) 17,593

1.4

1.2

1.0

0.6

0.8

0.2

0.4

0.0

250,000

200,000

150,000

100,000

50,000

0

Madison, WI

68 North America Flexible Office Market in 2020

FLEXIBLE OFFICE HISTORICAL INVENTORY

LARGEST FLEXIBLE OPERATOR TRANSACTIONS

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2015

H1 2012

H1 2018

H1 2014

H1 2011

H1 2017

H1 2013

H1 2010

H1 2020

H1 2016

Sq. Ft. Dowtown (L) Suburban (L) Penetration % (R) (%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassWeWork 362,000 Q3 2019 Midtown Other*

WeWork 108,000 Q3 2019 Midtown South Other*

Industrious 103,000 Q1 2020 Midtown Other*

HANA 86,000 Q1 2020 Downtown Other*

Knotel 84,000 Q3 2019 Downtown Other*

Total Top Five 743,000

Total Sq. Ft. New Transactions Y-o-Y 1,459,000

Top 5 as a % of Total 50.9%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 8,067,172 7.8% 47.7% 97 Midtown

Knotel 2,310,112 13.1% 13.7% 98 Midtown South

Regus 1,062,661 0.0% 6.3% 35 Midtown

Convene 809,939 9.5% 4.8% 14 Downtown

Spaces 608,028 0.0% 3.6% 8 Midtown

Total Top Five 12,857,912 76.0% 252 Top 5 as a % of Total 76.0%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsMidtown 48.4% 53.2%

Low HighSingle Office/Suite Rates $610 $900

Manhattan Q2 2020 Y-o-Y GrowthFlexible Office Sq. Ft. 16,910,367 8.4%

Downtown Flex Sq. Ft. 16,910,367 8.4%

Suburban Flex Sq. Ft. N/A N/A

Overall Market Penetration (%) 4.1% 0.3%

Downtown Penetration (%) 4.1% 0.3%

Suburban Penetration (%) N/A N/A

# of Operators 79 +1

# of Locations 454 +29

Avg. Size of Location (SF) 37,248

18,000,000

16,000,000

14,000,000

10,000,000

12,000,000

6,000,000

8,000,000

2,000,000

4,000,000

0

4.5

3.5

4.0

2.5

3.0

1.5

2.0

0.5

1.0

0.0

Manhattan

*Manhattan does not differentiate office product by class.

69© 2020 CBRE, Inc.

FLEXIBLE OFFICE HISTORICAL INVENTORY FLEXIBLE OFFICE INVENTORY – COMPOSITION OVER TIME

LARGEST FLEXIBLE OPERATOR TRANSACTIONS Q3 2019 – Q2 2020

TOP FLEXIBLE SPACE OPERATORS MARKET STATISTICS

H1 2019

H1 2019

H1 2015

H1 2015

H1 2012

H1 2012

H1 2018

H1 2018

H1 2014

H1 2014

H1 2011

H1 2011

H1 2017

H1 2017

H1 2013

H1 2013

H1 2010

H1 2010

H1 2020

H1 2020

H1 2016

H1 2016

Sq. Ft. (%)Downtown (L) Suburban (L) Penetration % (R) Downtown Suburban

100

80

90

60

70

40

50

20

30

10

0

(%)

APPENDIX HOME

Source: CBRE Research, Q2 2020.

Operator Size (SF) Quarter SubmarketBuilding

ClassNeueHouse Coworking 33,000 Q1 2020 Biscayne Blvd Corridor B

Industrious 30,000 Q4 2019 Aventura Other*

Industrious 25,000 Q3 2019 Coral Gables Other*

CoSuite 14,000 Q4 2019 Brickell B

Total Top Five 102,000

Total Sq. Ft. New Transactions Y-o-Y 102,000

Top 5 as a % of Total 100.0%

Operator Size (SF)Y-o-Y

Growth% of

Market# of

LocationsDominant

SubmarketWeWork 589,013 0.0% 30.1% 8 Brickell

Regus 343,304 0.0% 17.5% 21 Airport/Doral

Spaces 191,385 0.0% 9.8% 6 Miami Beach

Quest Workspaces 123,508 0.0% 6.3% 5 Brickell

CustomSpace Co. 85,344 0.0% 4.4% 1 Airport/Doral

Total Top Five 1,332,554 68.1% 41 Top 5 as a % of Total 68.1%

Most Dominant Submarket % of Flex Office Inventory % of Total Y-o-Y TransactionsBrickell 24.8% 13.9%